The Market for Foreign Exchange (FX or FOREX) Chapter 5.

49

The Market for Foreign Exchange (FX or FOREX) Chapter 5

-

Upload

cody-mclaughlin -

Category

Documents

-

view

221 -

download

1

Transcript of The Market for Foreign Exchange (FX or FOREX) Chapter 5.

The Market for Foreign Exchange (FX or FOREX)

Chapter 5

Lecture Objectives

Introduce the institutional framework within which exchange rates are determined

Lay the foundation for much of the discussion throughout the course

Lecture Outline

• Structure of the FX Market • The Spot Market• The Forward Market

Structure of the FX Market

The FX market – Involves market participants buying and selling of

different currencies all over the world.

– A worldwide network of traders, connected by telephone lines and computer screens – there is no central headquarters. Trading also occurs around the clock.

– Includes trading currencies spot and forward, bank deposits of foreign currencies, foreign trade financing, trading in currency options, futures and swaps.

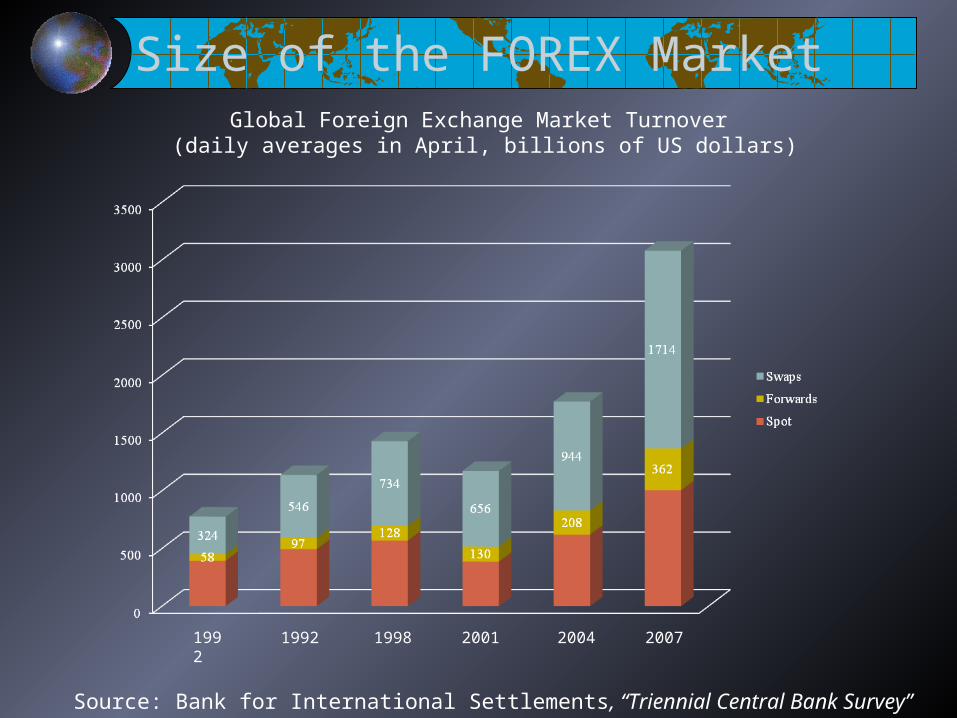

Size of the FOREX MarketGlobal Foreign Exchange Market Turnover

(daily averages in April, billions of US dollars)

Source: Bank for International Settlements, “Triennial Central Bank Survey” April 2007.

20011992 1992 1998 2004 2007

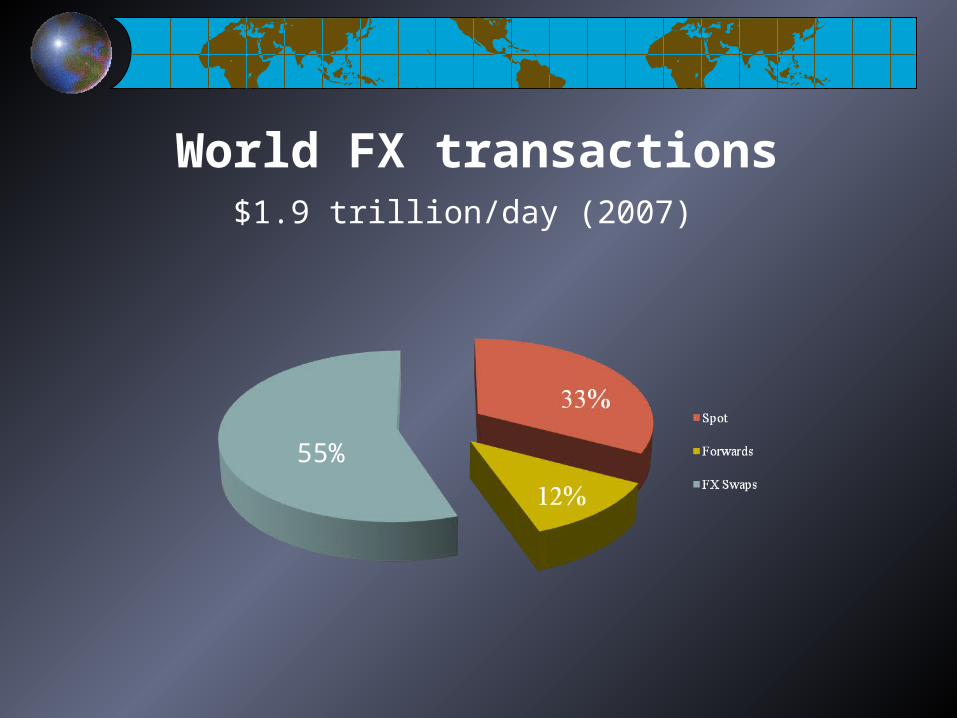

World FX transactions$1.9 trillion/day (2007)

55%

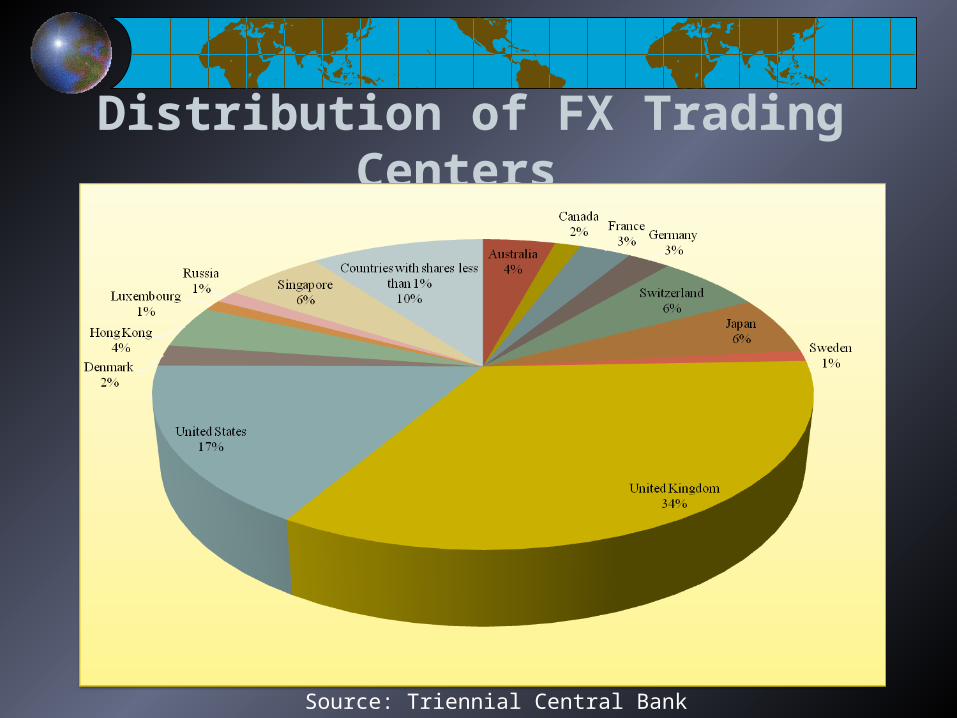

Distribution of FX Trading Centers

Source: Triennial Central Bank Survey 2007

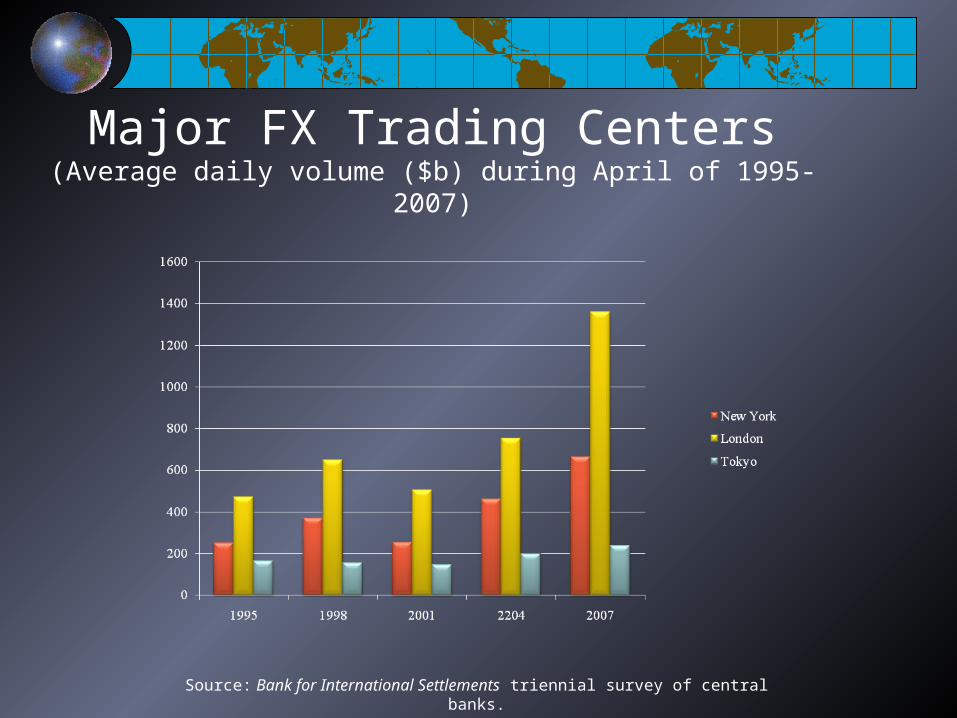

Major FX Trading Centers(Average daily volume ($b) during April of 1995-2007)

Source: Bank for International Settlements triennial survey of central banks.

Top 5 Most Traded Currencies

Rank Currency Code Symbol

1 United States USD $

2 Eurozone EUR €3 Japanese Yen Yen ¥

4 British Pound Sterling GBP £

5 Swiss Franc CHF -

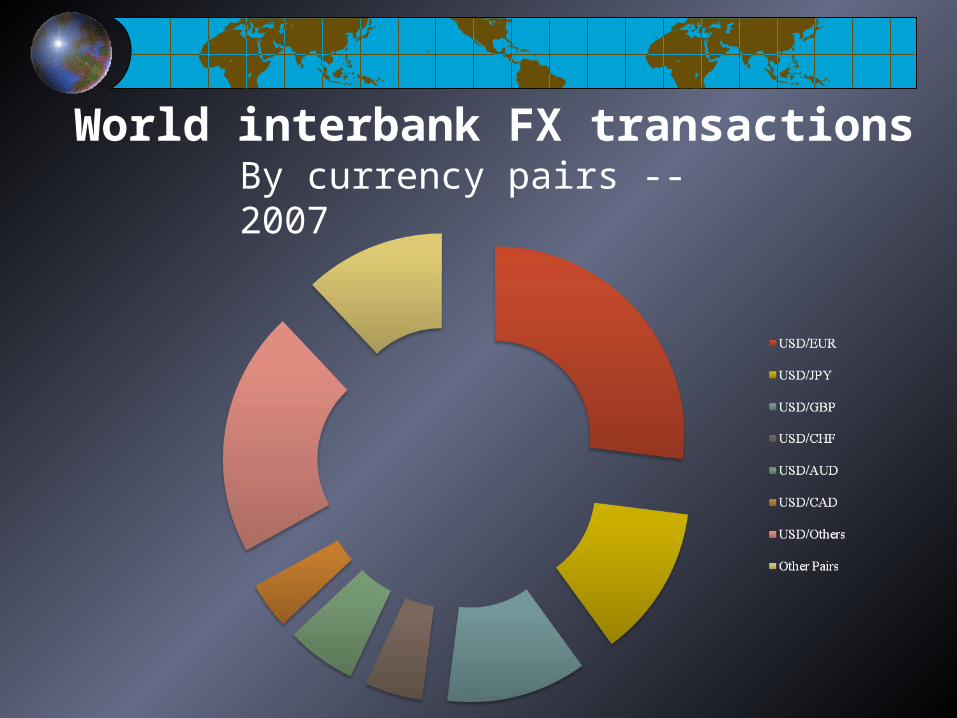

World interbank FX transactionsBy currency pairs -- 2007

The FX market in the U.S. is the most active market in the U.S.

($664 billion turnover per day, in April 2007)

2001 200419981995 2007

The FX market in the U.S. is the most active market in the U.S.

$664 billion turnover per day, in April 2007

Comparisons with U.S. asset markets:10 times the turnover of U.S. gov’t bonds

50 times the turnover of NYSE stocks

Comparisons with real activity in U.S.:10 times U.S. daily GDP

30 times U.S. daily exports + imports

Primary functions of FX Market

Currency conversions associated with international payments process

Provision of credit to clients(also part of international payments process)

Managing exchange rate risk

Structure of the FX Market

The FX market is a two-tiered market:Interbank Market (Wholesale)

About 700 banks worldwide stand ready to make a market in foreign exchange.

Nonbank dealers account for about 40% of the market in 2007.There are FX brokers who match buy and sell orders but do not

carry inventory.

Client Market (Retail): central banks and companies; account about 17% in 2007.

Market participants include international banks, their customers, nonbank dealers, FX brokers, and central banks.

Direct vs. brokered interbank tradesDirect dealing banks face another bank’s bid-ask spread, at which

they can transact immediately

Brokered tradesGet best price of all posted buys/sells

If you post an order, may not get executed

Electronic brokerage has become the primary method of trading interbank spot FX; drawback is that it covers only major currencies.

Much (56%) of FX trading is in the interbank (wholesale) market56% of all dealers’ trades are with other dealers

31% are with other financial institutions (brokers, mutual funds, ...)

13% are with nonfinancial customers

66% of all trades are with foreign counterparties

However, the retail orders are the important ones that determine exchange ratesInterbank traders are intermediaries

(market makers)

temporarily take positions intradaily, but

work hard to zero out their positions regularly and by the end of the day

The Spot Market

Spot Rate Quotations

The Bid-Ask Spread

Spot FX trading

Cross Rates

Spot Rate Quotations

“Spot” - settlement happens on the second working day after the deal is done. The exceptions are US dollar trades against the Canadian Dollar and Mexican Peso, which are settled next day.

When looking at foreign exchange quotations, it is necessary to decide immediately which is the “home” currency and which the “foreign” currency.

For the purposes of this class, the dollar will always be the “home” currency.

Spot Rate Quotations

There are two ways of quoting spot rates:No of units of home currency per 1 unit of foreign currencyNo of units of foreign currency per 1 unit of home currency

These are called, respectively, “Direct” and “Indirect” quotations. If the home currency is the dollar they are sometimes called “American” and “European” quotations, respectively.

Direct quotation: the U.S. dollar equivalente.g. “a Japanese Yen is worth about a penny”

Indirect Quotation: the price of a U.S. dollar in the foreign currencye.g. “you get 100 yen to the dollar”

Spot Rate Quotations

For example:

US$1 = S$1.789 is equivalent to

S$1 = US$0.559

Note: No different from any other price.

10 US dollar/One umbrella

1/10 umbrella/$

We will use the notation, for example, S$/US$ as the numbers of Singapore dollars per 1 dollar - that is an indirect quotation from an American perspective.

The Wall Street Journal gives both quotes.

Spot Rate Quotations

Country

USD equiv Friday

USD equiv Thursday

Currency per USD Friday

Currency per USD Thursday

Argentina (Peso) 0.3309 0.3292 3.0221 3.0377

Australia (Dollar) 0.5906 0.5934 1.6932 1.6852

Brazil (Real) 0.2939 0.2879 3.4025 3.4734

Britain (Pound) 1.5627 1.566 0.6399 0.6386

1 Month Forward 1.5596 1.5629 0.6412 0.6398

3 Months Forward 1.5535 1.5568 0.6437 0.6423

6 Months Forward 1.5445 1.5477 0.6475 0.6461

The direct quote for British pound is:

£1 = $1.5627

Spot Rate Quotations

The indirect quote for British pound is:

£.6399 = $1

1.49751.51060.66780.6626 Months Forward

1.48881.5020.67170.66583 Months Forward

1.48351.49680.67410.66811 Month Forward

1.48131.49430.67510.6692Canada (Dollar)

0.64610.64751.54771.54456 Months Forward

0.64230.64371.55681.55353 Months Forward

0.63980.64121.56291.55961 Month Forward

0.63860.63991.5661.5627Britain (Pound)

3.47343.40250.28790.2939Brazil (Real)

1.68521.69320.59340.5906Australia (Dollar)

3.03773.02210.32920.3309Argentina (Peso)

Currency per USD Thursday

Currency per USD Friday

USD equiv Thursday

USD equiv FridayCountry

Spot Rate Quotations

Note that the direct quote is the reciprocal of the indirect quote:

.6399

15627.1

1.49751.51060.66780.6626 Months Forward

1.48881.5020.67170.66583 Months Forward

1.48351.49680.67410.66811 Month Forward

1.48131.49430.67510.6692Canada (Dollar)

0.64610.64751.54771.54456 Months Forward

0.64230.64371.55681.55353 Months Forward

0.63980.64121.56291.55961 Month Forward

0.63860.63991.5661.5627Britain (Pound)

3.47343.40250.28790.2939Brazil (Real)

1.68521.69320.59340.5906Australia (Dollar)

3.03773.02210.32920.3309Argentina (Peso)

Currency per USD Thursday

Currency per USD Friday

USD equiv Thursday

USD equiv FridayCountry

The Bid-Ask Spread

In general, banks do not charge commissions on foreign currency transactions. They profit from bid-ask spread.

The bid-ask spread is the difference between the bid and ask prices.

The bid price is the price a dealer is willing to pay you for a foreign currency.

The ask price is the amount the dealer wants you to pay for the foreign currency.

The Bid-Ask Spread

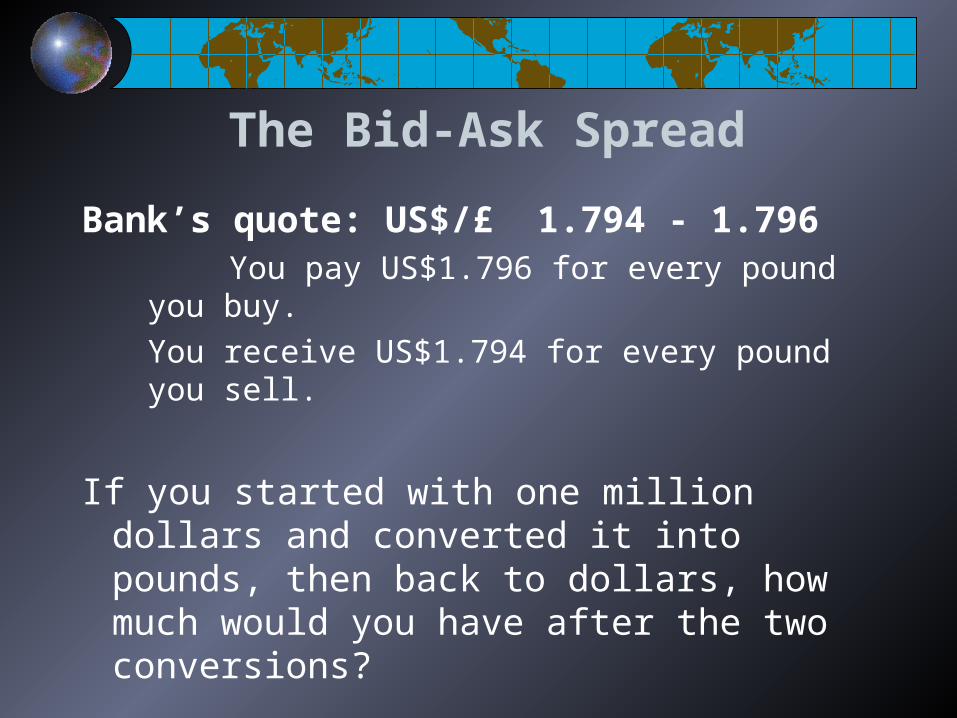

Bank’s quote: US$/£ 1.794 - 1.796 1.794 is the “Bid” price. A bank will buy

pounds for $1.794/pound; same as bank selling $1.794 for £1.

1.796 is the “Offer” price. A bank will sellpounds for $1.796; same as bank buying

$1.796 for £1 pound.

Bank’s profit = ASK-BID = “Bid-Ask Spread”.

The Bid-Ask Spread

Bank’s quote: US$/£ 1.794 - 1.796 You pay US$1.796 for every pound you buy.

You receive US$1.794 for every pound you sell.

If you started with one million dollars and converted it into pounds, then back to dollars, how much would you have after the two conversions?

The Bid-Ask Spread

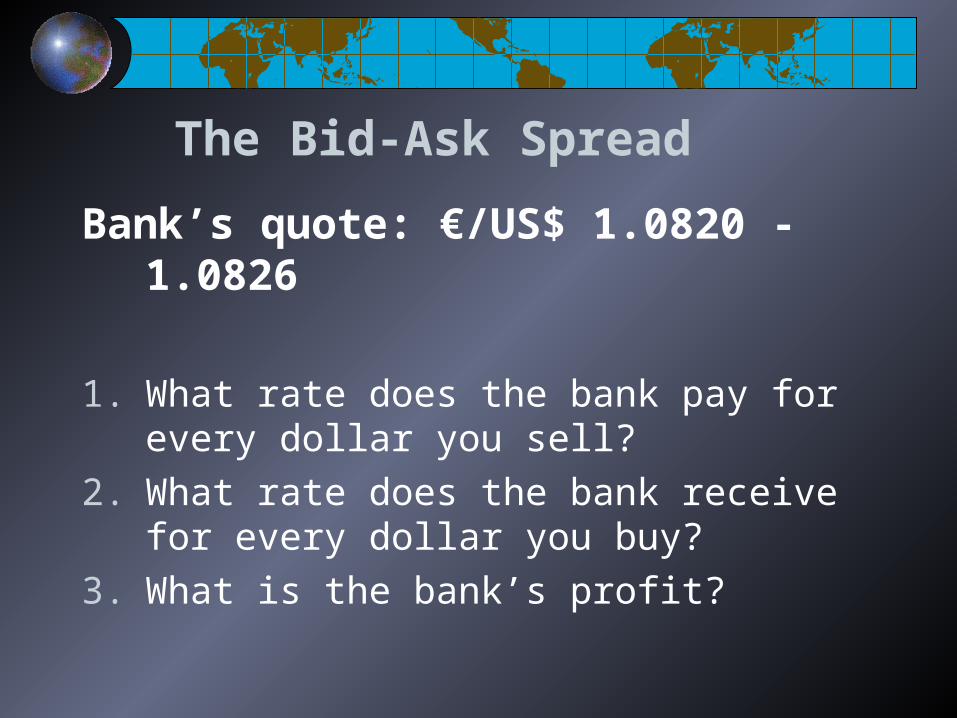

Bank’s quote: €/US$ 1.0820 - 1.0826

1. What rate does the bank pay for every dollar you sell?

2. What rate does the bank receive for every dollar you buy?

3. What is the bank’s profit?

Cross Rates

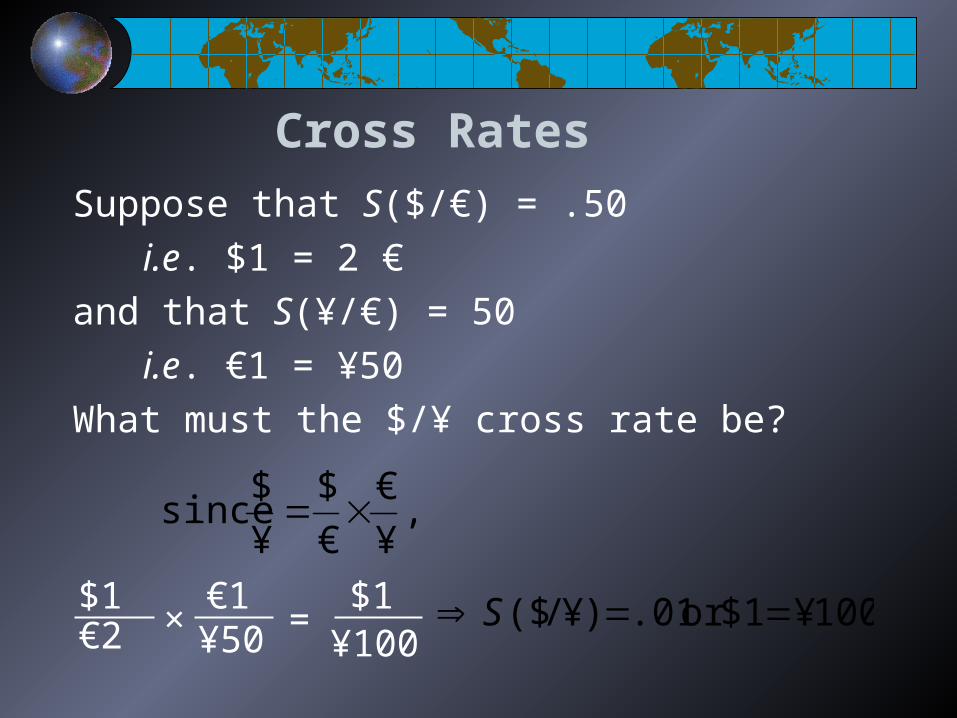

Suppose that S($/€) = .50

i.e. $1 = 2 €

and that S(¥/€) = 50

i.e. €1 = ¥50

What must the $/¥ cross rate be?

,¥

€

€

$

¥

$ since

$1 €1€2 ¥50×

$1¥100

= 100¥ $1or .01 )¥/($ S

Cross Rates

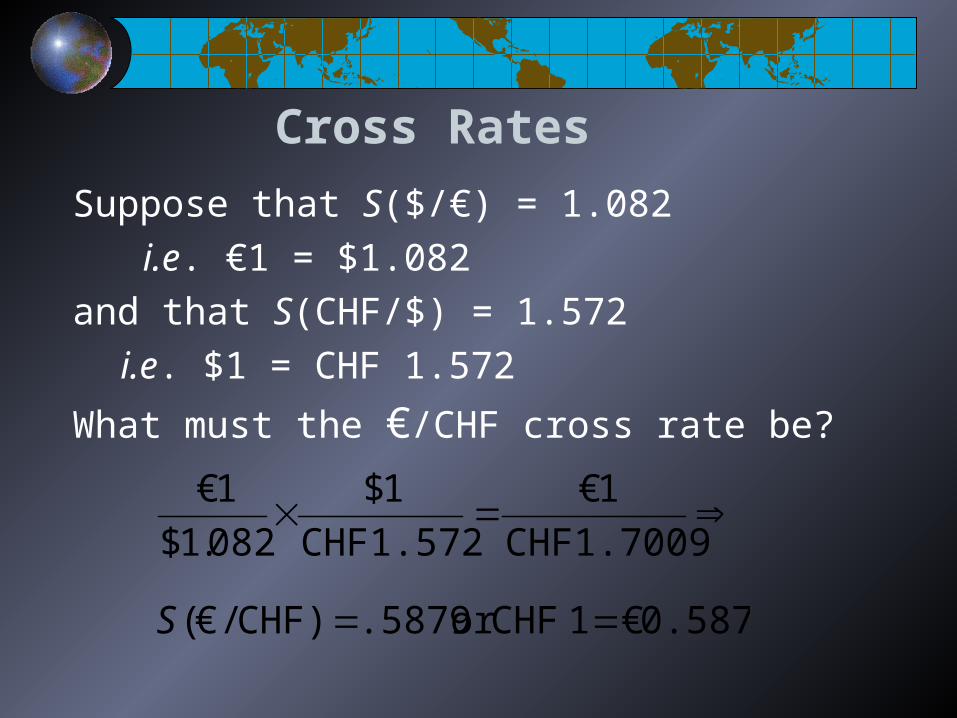

Suppose that S($/€) = 1.082

i.e. €1 = $1.082

and that S(CHF/$) = 1.572

i.e. $1 = CHF 1.572

What must the €/CHF cross rate be?

CHF1.7009

1€

CHF1.572

1$

082.1$

1€

0.5879€ 1 CHFor .5879 CHF)/€( S

Cross Rates

Suppose that S($/€) = 1.20 and that S($/¥) = 0.009. What must the S(¥/€) cross rate be?

Suppose that S(AUD/$) = 2.What must the S(AUD/€) cross rate be?

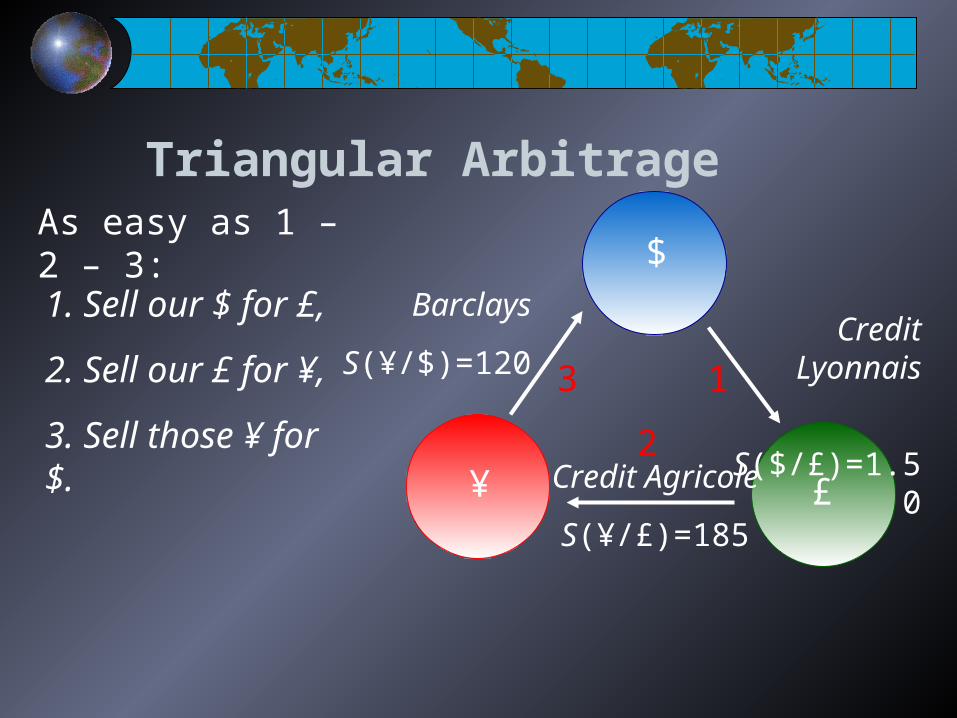

Triangular Arbitrage

$

£¥

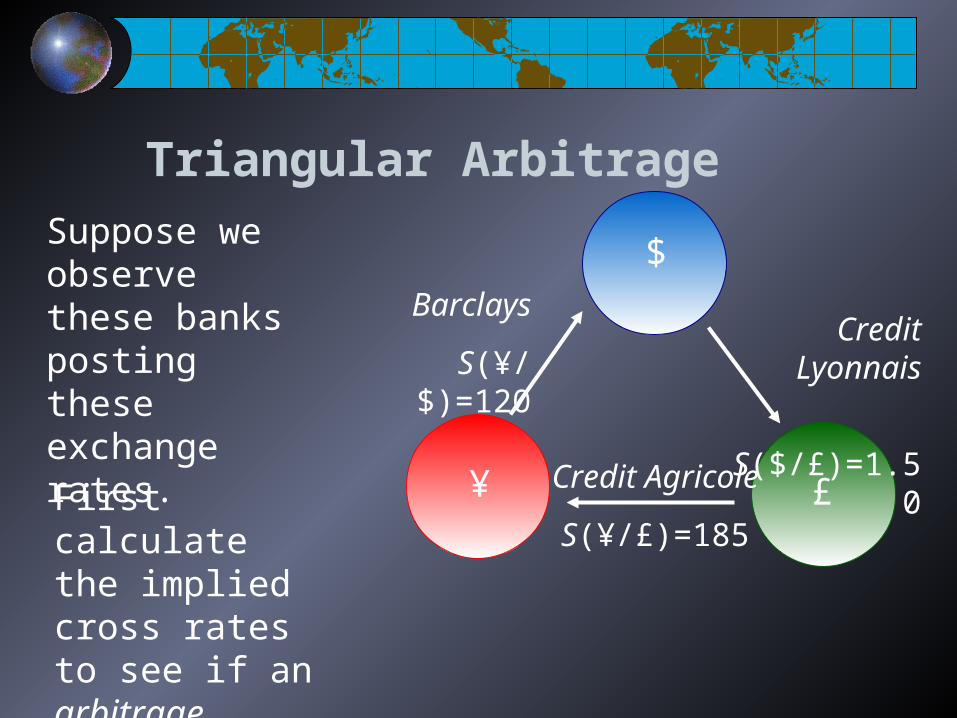

Credit Lyonnais

S($/£)=1.50

Credit Agricole

S(¥/£)=185

Barclays

S(¥/$)=120

Suppose we observe these banks posting these exchange rates.

First calculate the implied cross rates to see if an arbitrage exists.

Triangular Arbitrage

$

Credit Lyonnais

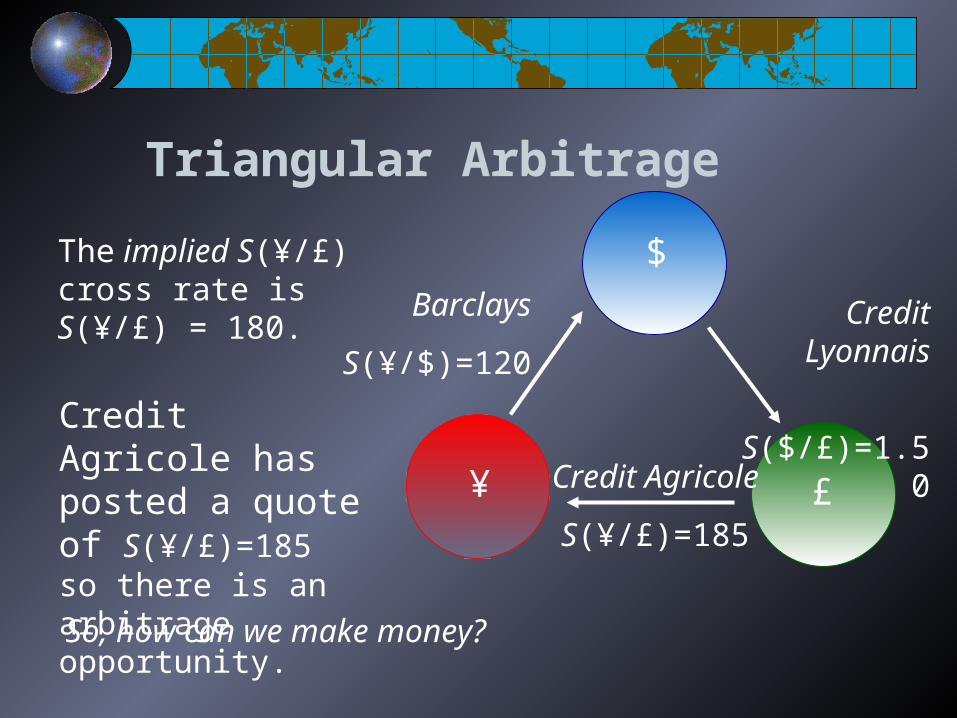

S($/£)=1.50

Credit Agricole

S(¥/£)=185

Barclays

S(¥/$)=120

The implied S(¥/£) cross rate is S(¥/£) = 180.

Credit Agricole has posted a quote of S(¥/£)=185 so there is an arbitrage opportunity.

So, how can we make money?

¥ £

Cross Exchange Rate Equilibrium

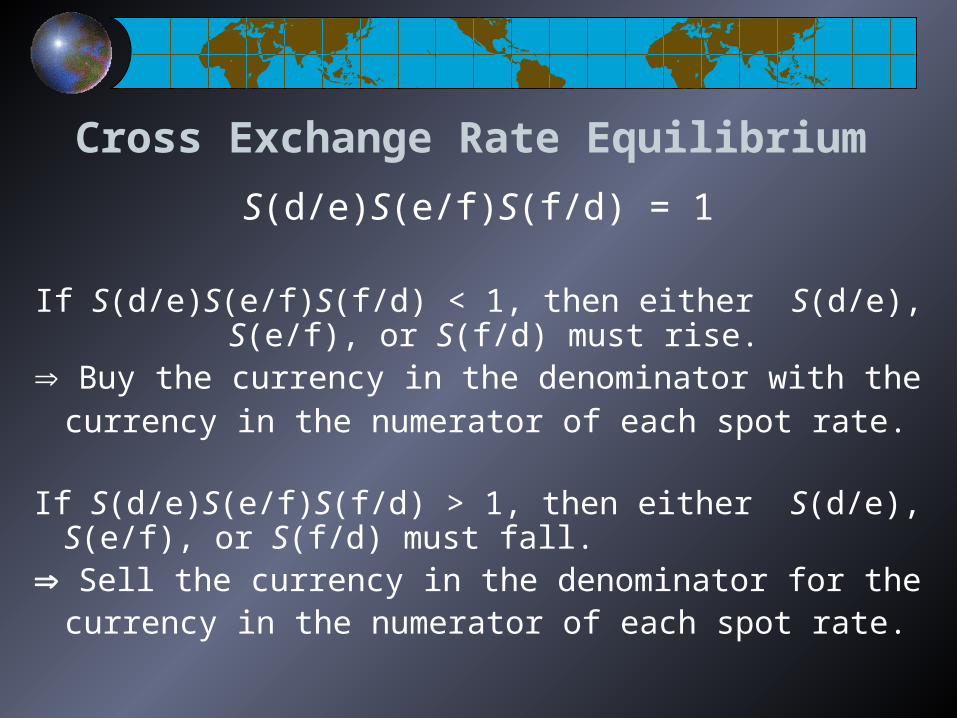

S(d/e)S(e/f)S(f/d) = 1

If S(d/e)S(e/f)S(f/d) < 1, then either S(d/e), S(e/f), or S(f/d) must rise.

Buy the currency in the denominator with the

currency in the numerator of each spot rate.If S(d/e)S(e/f)S(f/d) > 1, then either S(d/e), S(e/f), or S(f/d)

must fall. Sell the currency in the denominator for the

currency in the numerator of each spot rate.

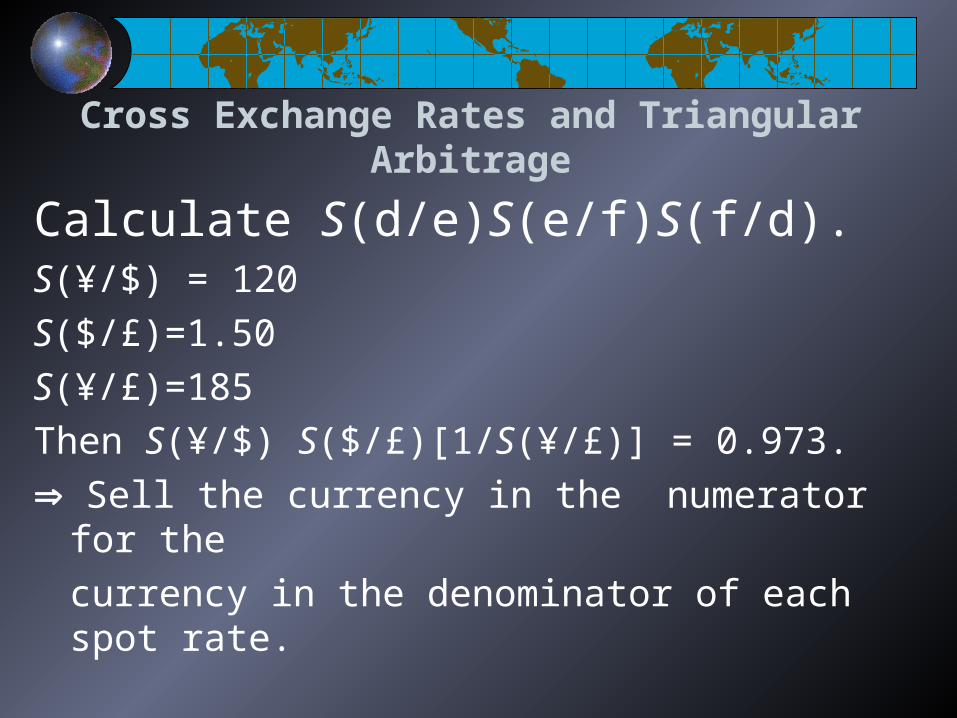

Cross Exchange Rates and Triangular Arbitrage

Calculate S(d/e)S(e/f)S(f/d).S(¥/$) = 120

S($/£)=1.50

S(¥/£)=185

Then S(¥/$) S($/£)[1/S(¥/£)] = 0.973.

Sell the currency in the numerator for the

currency in the denominator of each spot rate.

Triangular Arbitrage

$

Credit Lyonnais

S($/£)=1.50

Credit Agricole

S(¥/£)=185

Barclays

S(¥/$)=120

As easy as 1 – 2 – 3:

1. Sell our $ for £,

2. Sell our £ for ¥,

3. Sell those ¥ for $.¥ £

1

2

3

$

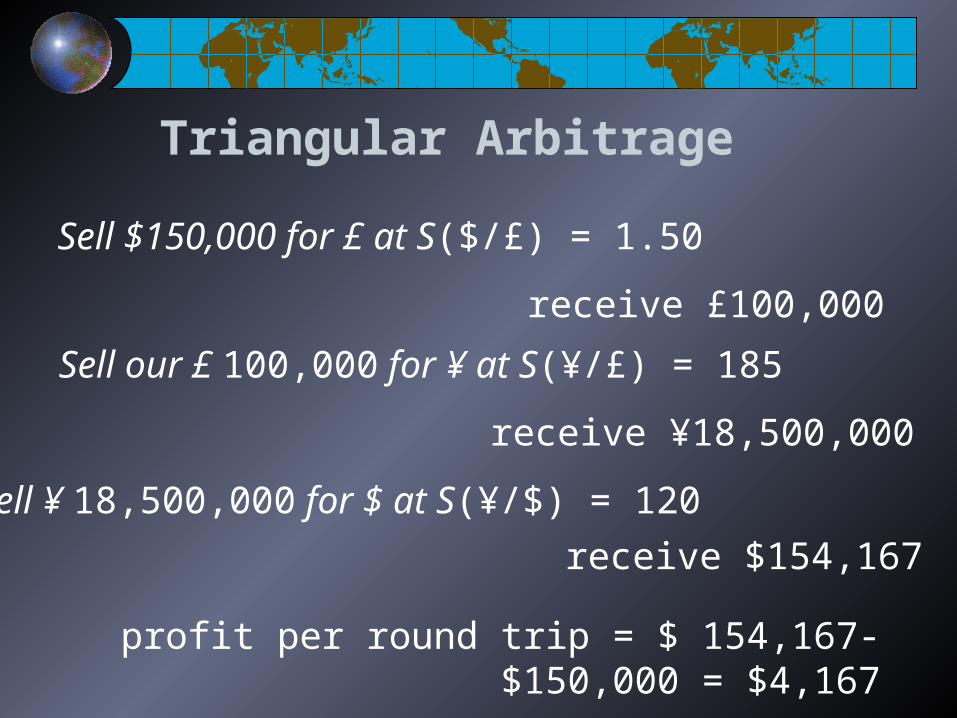

Triangular Arbitrage

Sell $150,000 for £ at S($/£) = 1.50

receive £100,000

Sell our £ 100,000 for ¥ at S(¥/£) = 185

receive ¥18,500,000

Sell ¥ 18,500,000 for $ at S(¥/$) = 120

receive $154,167

profit per round trip = $ 154,167- $150,000 = $4,167

The Forward Market

Forward Rate Quotations

Long and Short Forward Positions

Forward Premium

The Forward Market

A forward contract is an agreement to buy or sell an asset in the future at prices agreed upon today.

If you have ever had to order an out-of-stock textbook, then you have entered into a forward contract.

Forward Rate Quotations

The forward market for FOREX involves agreements to buy and sell foreign currencies in the future at prices agreed upon today.

Bank quotes for 1, 3, 6, 9, and 12 month maturities are readily available for forward contracts.

Forward Rate Quotations

Consider the example from above:

for British pound, the spot rate is

$1.5627 = £1.00

While the 180-day forward rate is

$1.5445 = £1.00

What’s up with that?

Spot Rate Quotations

Clearly the market participants expect that the pound will be worth less in dollars in six months.

1.49751.51060.66780.6626 Months Forward

1.48881.5020.67170.66583 Months Forward

1.48351.49680.67410.66811 Month Forward

1.48131.49430.67510.6692Canada (Dollar)

0.64610.64751.54771.54456 Months Forward

0.64230.64371.55681.55353 Months Forward

0.63980.64121.56291.55961 Month Forward

0.63860.63991.5661.5627Britain (Pound)

3.47343.40250.28790.2939Brazil (Real)

1.68521.69320.59340.5906Australia (Dollar)

3.03773.02210.32920.3309Argentina (Peso)

Currency per USD Thursday

Currency per USD Friday

USD equiv Thursday

USD equiv FridayCountry

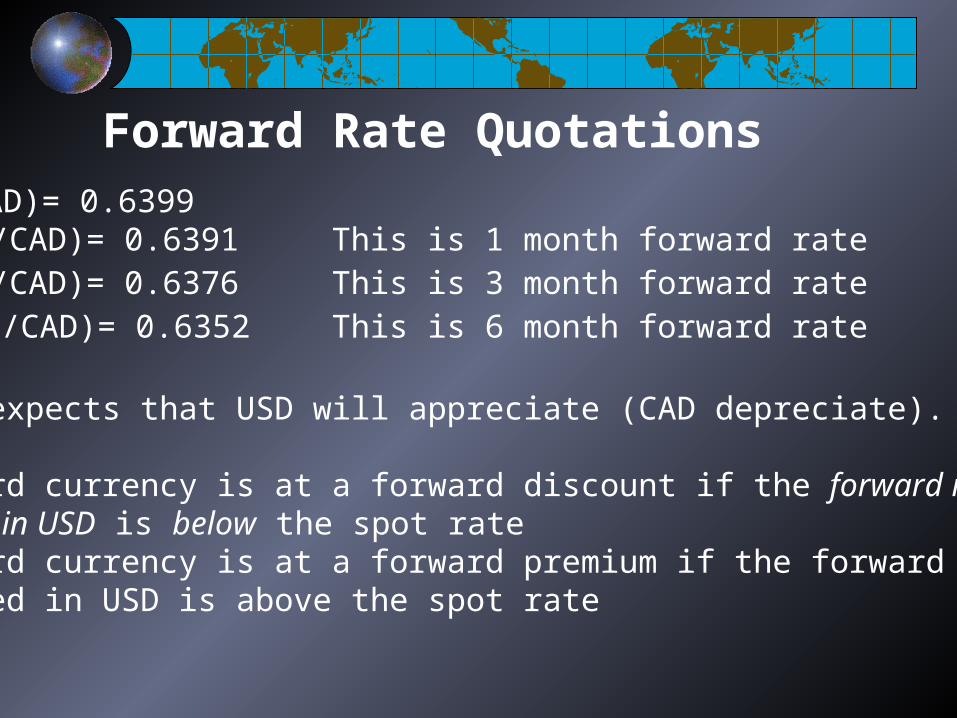

Forward Rate QuotationsS(USD/CAD)= 0.6399 F30 (USD/CAD)= 0.6391 This is 1 month forward rateF90 (USD/CAD)= 0.6376 This is 3 month forward rateF180 (USD/CAD)= 0.6352 This is 6 month forward rate

Market expects that USD will appreciate (CAD depreciate).

A forward currency is at a forward discount if the forward rate expressed in USD is below the spot rateA forward currency is at a forward premium if the forward rate expressed in USD is above the spot rate

Long and Short Forward Positions

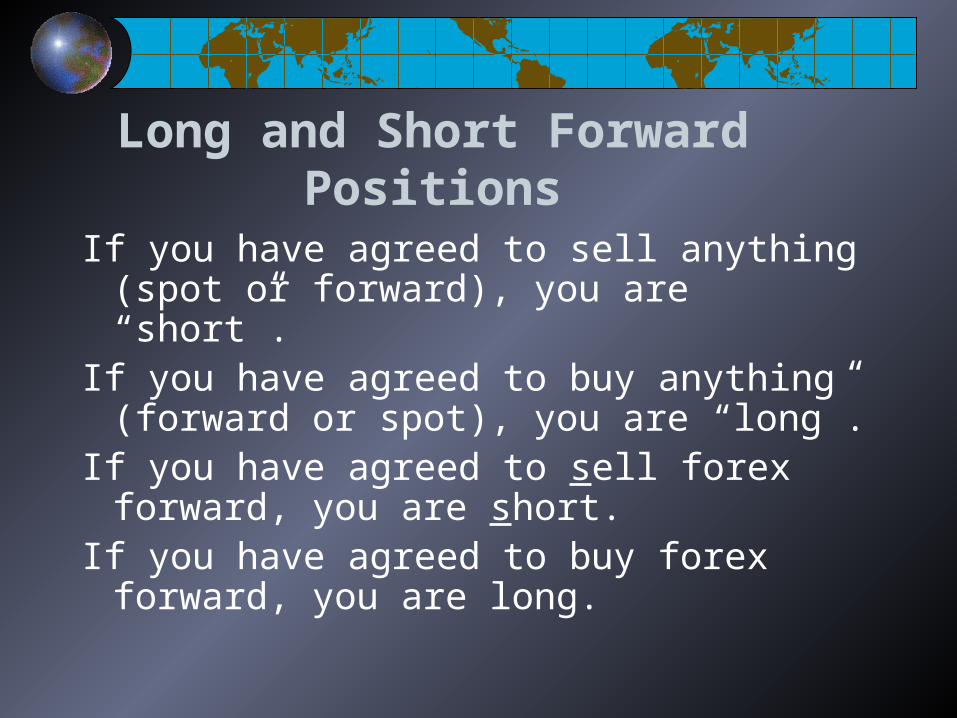

If you have agreed to sell anything (spot or forward), you are “short”.

If you have agreed to buy anything (forward or spot), you are “long”.

If you have agreed to sell forex forward, you are short.

If you have agreed to buy forex forward, you are long.

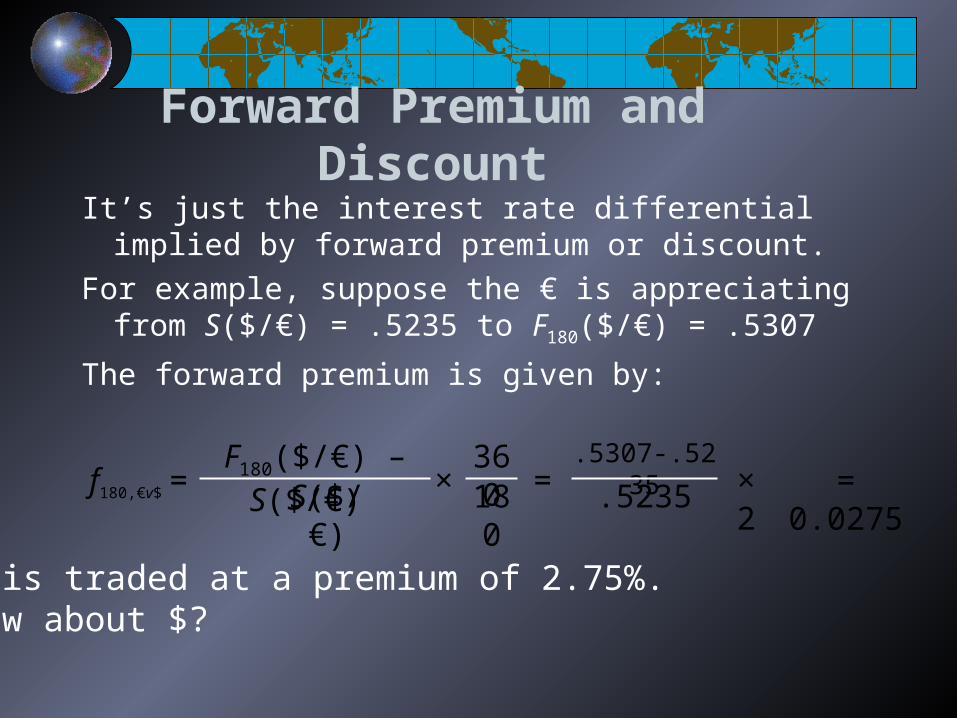

Forward Premium and Discount

It’s just the interest rate differential implied by forward premium or discount.

For example, suppose the € is appreciating from S($/€) = .5235 to F180($/€) = .5307

The forward premium is given by:

€ is traded at a premium of 2.75%.How about $?

f180,€v$

F180($/€) – S($/€) S($/€)= ×

360180

.5307-.5235

.5235 × 2= = 0.0275

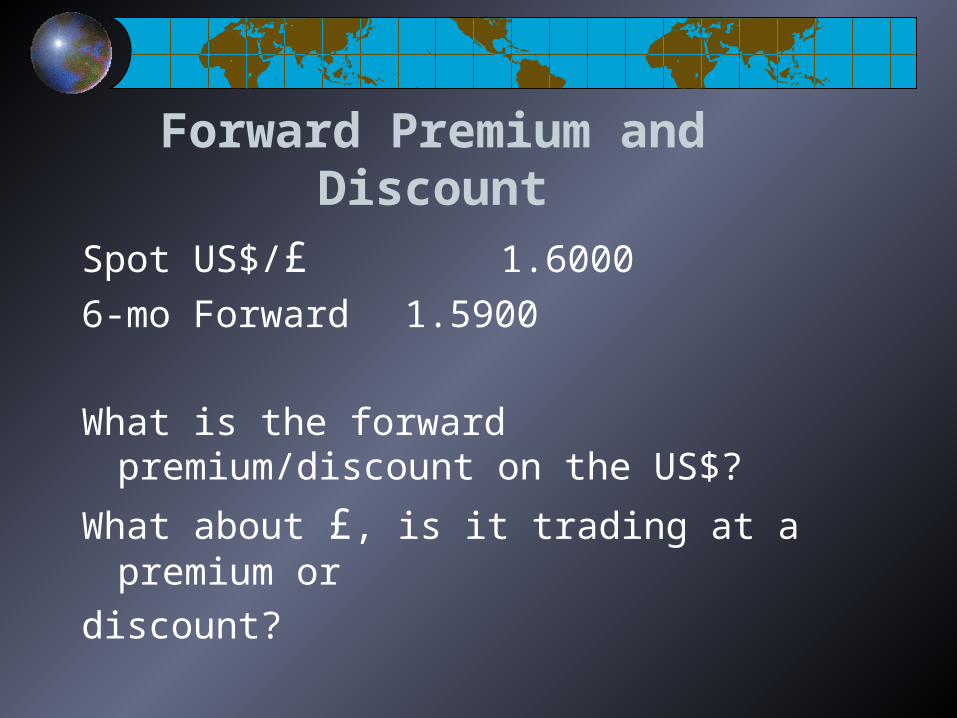

Forward Premium and Discount

Spot US$/£ 1.6000

6-mo Forward 1.5900

What is the forward premium/discount on the US$?

What about £, is it trading at a premium or

discount?

The following sections in chapter 5 are not

required for the exam:

Examples 5.2 and 5.3

Spot Foreign Exchange Microstructure

Swap transactions

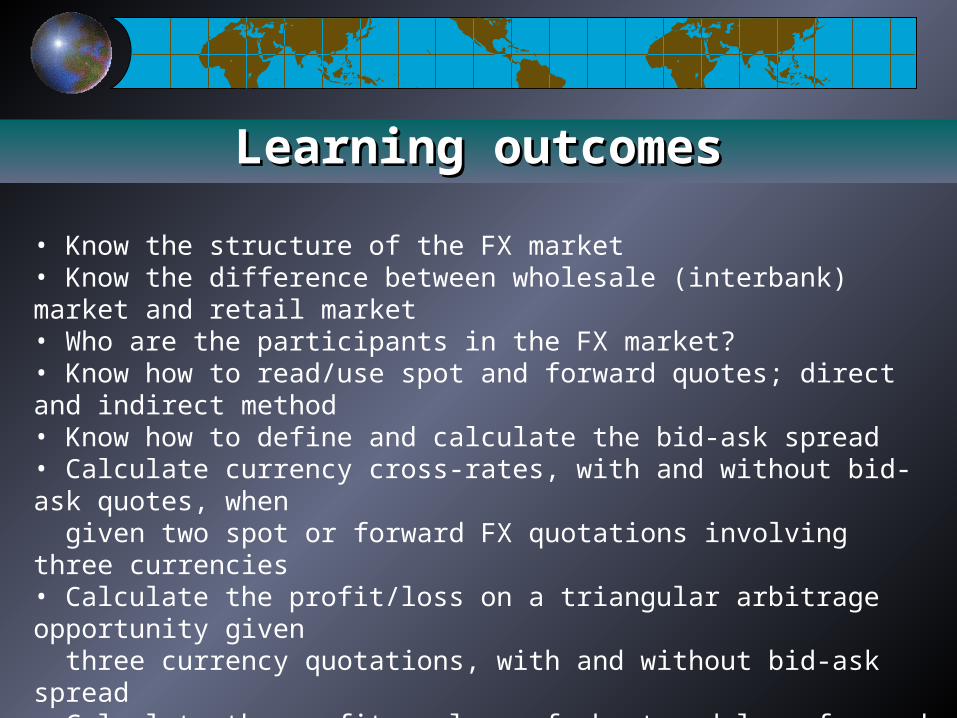

Learning outcomesLearning outcomes

• Know the structure of the FX market• Know the difference between wholesale (interbank) market and retail market• Who are the participants in the FX market?• Know how to read/use spot and forward quotes; direct and indirect method• Know how to define and calculate the bid-ask spread• Calculate currency cross-rates, with and without bid-ask quotes, when given two spot or forward FX quotations involving three currencies• Calculate the profit/loss on a triangular arbitrage opportunity given three currency quotations, with and without bid-ask spread• Calculate the profit or loss of short and long forward positions• Define and calculate the forward discount or premium