THE INSTITUTE OF CHARTERED ACCOUNTANTS OF...

12

EIRC 1st October 2017 1 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA EIRC NEWSLETTER VOL 43 ISSUE : 8 1st OCTOBER 2017 ` 10/- EASTERN INDIA REGIONAL COUNCIL (Set up by an Act of Parliament)

Transcript of THE INSTITUTE OF CHARTERED ACCOUNTANTS OF...

EIRC 1st October 2017 1

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

EIRC NEWSLETTERVOL 43 ISSUE : 8 1st OCTOBER 2017 ` 10/-

EASTERN INDIA REGIONAL COUNCIL(Set up by an Act of Parliament)

2 EIRC 1st October 2017

EIRC 1st October 2017 3

Information Kiosks installed in the Institute for quick resolution for members and students issues at ICAI.

I am happy to introduce a dedicated Mobile no 90519-30000 for sharing information about EIRC & ICAI activities. I urge upon the members to kindly store this number on their mobile as Chairman-EIRC so that we can send broad cast messages to you. You may also send sms/ whats app to this number so that the incumbent could be aware of problems which are not being resolved otherwise.

Networking opportunities are equally important in this era. It is vital to interact with fellow comrade to survive in this century. Newer opportunities can be explored by understanding the experiences of experts and intellectuals. This opportunity would be provided to you at the 42nd Regional Conference 2017 which is to be held on 22nd & 23rd Dec’17 at Science City, Kolkata. The preparations for the same are at its brim. The theme for the conference is “Transcending Transformation”.

TRANSCEND AND TRANSFORM is about how to gear up oneself to face the upcoming challenges, in spite of all odds, move forward, prove your mettle and thereby adapting to deal with a new situation. We urge upon all our members to kindly block their diary for attending the same and make it a grand success.

EIRC is taking a lead role in interacting with state government We have approached to the state government and offered our services for training of youths at their youth centres so that adequate semi skilled manpower could be created to handle the work related to GST compliance. This would not only provide employment opportunities to the youth but also help the small traders in making compliances. We are also in the process of making representations to the state government in regards to revamping of audit of cooperatives in the state. I would urge dear members to kindly share your ideas and inputs on matters which could help in brand building of ICAI and also for creating opportunities for our professional brethren. I truly believe in the words of Mahatma Gandhi that “The future depends on what we do in the present“ Taking cue from it we at EIRC are striving hard to give the best to the profession.

As I sign off I wish you all a very Happy Diwali. As you celebrate Valour & Courage, Triumph of Good over Evil. I wish you Success & Happiness in everything you do.

With Warm Regards

CA Manish GoyalChairman, EIRC of ICAI

Dear professional colleagues,

Wishing you all Subho Bijaya. With festivities around and also with the pressing timelines for completing professional assignments I am sure you all must be having a tough time balancing with family and social commitments and that with the profession. However, over the years we

have been able to do a balancing act and we all have emerged as true managers of life. However, we all must remember an old adage “So many people spend their health gaining wealth, and then have to spend their wealth to regain their health”. So, please keep yourself healthy through mind and body.

The busy time of the year where returns were to be filed by the end of September has seen some respite. The extension of the dates for filing has brought some relief to the professionals and provided the breathing space to enjoy the festive season. However, I also remind all my beloved colleagues not to wait for the last date to fulfil their professional obligations rather complete them in a phased manner. My earnest wish in this regard that none of my professionals should face any problems due to the last minute rush, with all possibility of hassles in the portal.

I take this opportunity to wish you and your family a very Happy Dussehra and Subho Bijaya. The memories of festival must be very fresh and to add to this another great festival awaits all of us. May the great festival of lights illuminate all our lives and rejuvenates us with new rays of hope and good luck. On this note, I would like to wish all my fellow members a very Happy Diwali.May the divine light of Diwali spread into your life and bring peace, prosperity, happiness, success and good health.

In the current times, our profession is gearing up for new avenues and amongst them ‘Digital financials, data analytics and cyber security are paving the road for new generation Chartered Accountants. In the light of this, I would like to present before you the “Technology Summit - 2017”, which is scheduled on 14th October 2017 at Park Hotel, Kolkata. The deliberation by world renowned speakers at the event will surely give us deep insights at what the profession is going to be like in near future.

There have been developments as far as technology is considered at EIRC. We have come up with latest updates in the EIRC Mobile App & the revamped Website, so that the members have a one-step solution to all their queries. There are

4 EIRC 1st October 2017

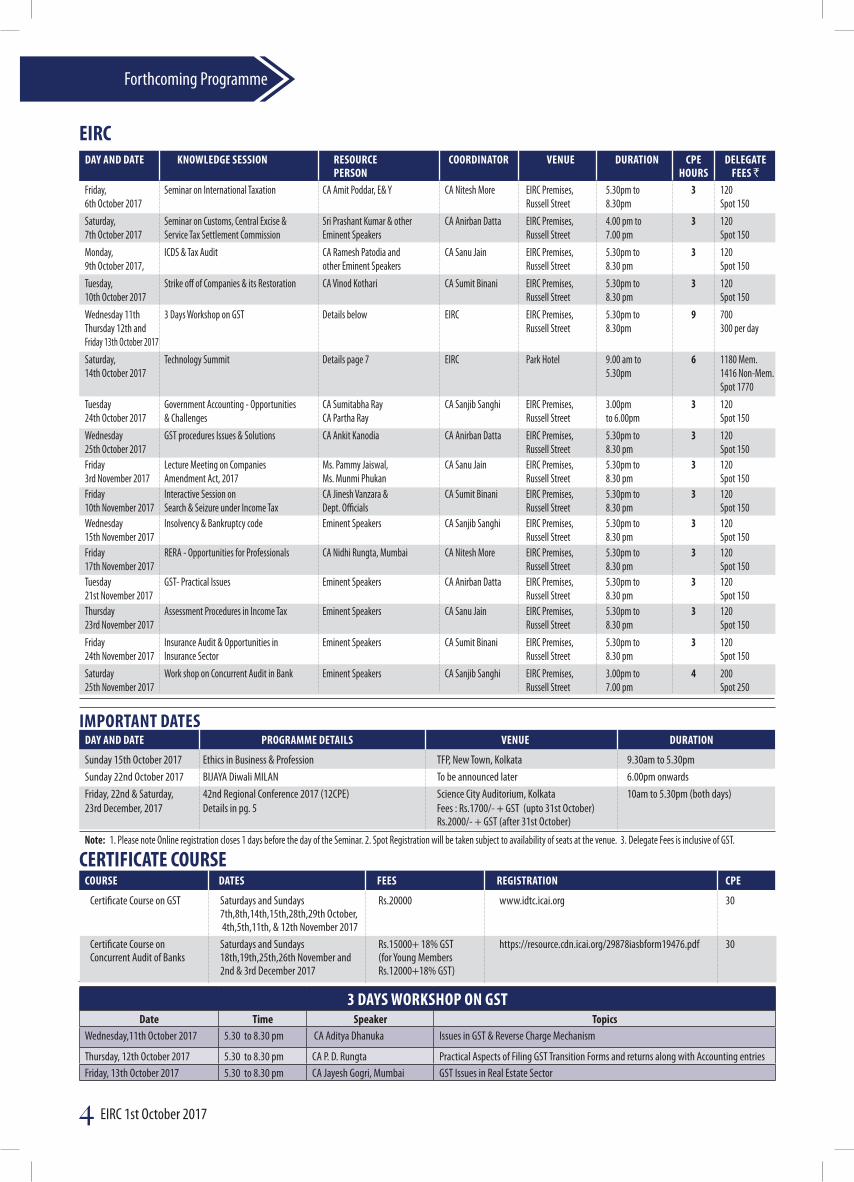

Forthcoming Programme

DAY AND DATE KNOWLEDGE SESSION RESOURCE COORDINATOR VENUE DURATION CPE DELEGATE PERSON HOURS FEES `

EIRC

DAY AND DATE PROGRAMME DETAILS VENUE DURATIONIMPORTANT DATES

Sunday 15th October 2017 Ethics in Business & Profession TFP, New Town, Kolkata 9.30am to 5.30pmSunday 22nd October 2017 BIJAYA Diwali MILAN To be announced later 6.00pm onwardsFriday, 22nd & Saturday, 42nd Regional Conference 2017 (12CPE) Science City Auditorium, Kolkata 10am to 5.30pm (both days)23rd December, 2017 Details in pg. 5 Fees : Rs.1700/- + GST (upto 31st October) Rs.2000/- + GST (after 31st October)

Note: 1. Please note Online registration closes 1 days before the day of the Seminar. 2. Spot Registration will be taken subject to availability of seats at the venue. 3. Delegate Fees is inclusive of GST.

CERTIFICATE COURSECOURSE DATES FEES REGISTRATION CPE

Certificate Course on GST Saturdays and Sundays Rs.20000 www.idtc.icai.org 30 7th,8th,14th,15th,28th,29th October, 4th,5th,11th, & 12th November 2017 Certificate Course on Saturdays and Sundays Rs.15000+ 18% GST https://resource.cdn.icai.org/29878iasbform19476.pdf 30Concurrent Audit of Banks 18th,19th,25th,26th November and (for Young Members 2nd & 3rd December 2017 Rs.12000+18% GST)

Friday, Seminar on International Taxation CA Amit Poddar, E& Y CA Nitesh More EIRC Premises, 5.30pm to 3 1206th October 2017 Russell Street 8.30pm Spot 150Saturday, Seminar on Customs, Central Excise & Sri Prashant Kumar & other CA Anirban Datta EIRC Premises, 4.00 pm to 3 1207th October 2017 Service Tax Settlement Commission Eminent Speakers Russell Street 7.00 pm Spot 150Monday, ICDS & Tax Audit CA Ramesh Patodia and CA Sanu Jain EIRC Premises, 5.30pm to 3 1209th October 2017, other Eminent Speakers Russell Street 8.30 pm Spot 150Tuesday, Strike off of Companies & its Restoration CA Vinod Kothari CA Sumit Binani EIRC Premises, 5.30pm to 3 12010th October 2017 Russell Street 8.30 pm Spot 150Wednesday 11th 3 Days Workshop on GST Details below EIRC EIRC Premises, 5.30pm to 9 700Thursday 12th and Russell Street 8.30pm 300 per dayFriday 13th October 2017 Saturday, Technology Summit Details page 7 EIRC Park Hotel 9.00 am to 6 1180 Mem.14th October 2017 5.30pm 1416 Non-Mem. Spot 1770Tuesday Government Accounting - Opportunities CA Sumitabha Ray CA Sanjib Sanghi EIRC Premises, 3.00pm 3 12024th October 2017 & Challenges CA Partha Ray Russell Street to 6.00pm Spot 150Wednesday GST procedures Issues & Solutions CA Ankit Kanodia CA Anirban Datta EIRC Premises, 5.30pm to 3 12025th October 2017 Russell Street 8.30 pm Spot 150Friday Lecture Meeting on Companies Ms. Pammy Jaiswal, CA Sanu Jain EIRC Premises, 5.30pm to 3 1203rd November 2017 Amendment Act, 2017 Ms. Munmi Phukan Russell Street 8.30 pm Spot 150Friday Interactive Session on CA Jinesh Vanzara & CA Sumit Binani EIRC Premises, 5.30pm to 3 12010th November 2017 Search & Seizure under Income Tax Dept. Officials Russell Street 8.30 pm Spot 150Wednesday Insolvency & Bankruptcy code Eminent Speakers CA Sanjib Sanghi EIRC Premises, 5.30pm to 3 12015th November 2017 Russell Street 8.30 pm Spot 150Friday RERA - Opportunities for Professionals CA Nidhi Rungta, Mumbai CA Nitesh More EIRC Premises, 5.30pm to 3 12017th November 2017 Russell Street 8.30 pm Spot 150Tuesday GST- Practical Issues Eminent Speakers CA Anirban Datta EIRC Premises, 5.30pm to 3 12021st November 2017 Russell Street 8.30 pm Spot 150Thursday Assessment Procedures in Income Tax Eminent Speakers CA Sanu Jain EIRC Premises, 5.30pm to 3 12023rd November 2017 Russell Street 8.30 pm Spot 150Friday Insurance Audit & Opportunities in Eminent Speakers CA Sumit Binani EIRC Premises, 5.30pm to 3 12024th November 2017 Insurance Sector Russell Street 8.30 pm Spot 150Saturday Work shop on Concurrent Audit in Bank Eminent Speakers CA Sanjib Sanghi EIRC Premises, 3.00pm to 4 20025th November 2017 Russell Street 7.00 pm Spot 250

3 DAYS WORKSHOP ON GSTDate Time Speaker Topics

Wednesday,11th October 2017 5.30 to 8.30 pm CA Aditya Dhanuka Issues in GST & Reverse Charge Mechanism

Thursday, 12th October 2017 5.30 to 8.30 pm CA P. D. Rungta Practical Aspects of Filing GST Transition Forms and returns along with Accounting entriesFriday, 13th October 2017 5.30 to 8.30 pm CA Jayesh Gogri, Mumbai GST Issues in Real Estate Sector

EIRC 1st October 2017 5

Announcements

42ND REGIONAL CONFERENCE OF EIRCTheme: Transcending Transformation

Day & Dates: 22nd & 23rd (Friday & Saturday) December 2017Venue: Science City Auditorium, Kolkata l CPE Hrs. : 12 (TWELVE) l Organized by: EIRC, The Institute of Chartered Accountants of India

ADVERTISEMENT & SPONSORSHIP DETAILS

A. Advertisement in Souvenir Full Page Colour (Back) Rs.75,000/- Full Page Colour (Inside Back) Rs.50,000/- Full Page Colour (Inside Front) Rs.55,000/- Full Page (Colour) Rs.35,000/- Half Page (Colour) Rs.25,000/-

B. Banner (Size 6’x3’) Rs.30,000/-C. Conference Kit, Pad & Pen (2500 Nos) Rs.3,00,000/-D. Insertions in Kit Rs.30,000/-E. Exhibition Stall (1 Day) Rs.40,000/-F. Exhibition Stall (2 Days) Rs.60,000/-

Day 1 : Friday, 22nd December 2017 Inaugural Session (10.00 AM to 10.45 AM)Chief Guest Shri Suresh Prabhakar Prabhu, Hon’ble Union Minister of Commerce & Industry, Govt. of IndiaGuest of Honour Eminent GuestPresidential Address CA Nilesh S Vikamsey, President, ICAIAddress by CA Naveen ND Gupta, Vice President, ICAI

First Knowledge Session (10.45 AM to 12.00 Noon) Direct Taxes - Eradicating Black Economy Key note Address & Chairman Session Shri Sushil Chandra*, Chairman, CBDTCritical Issues - Income Tax CA Adv. Firoze B. Andhyarujina, MumbaiSecond Knowledge Session (12.00 Noon to 2.00 PM)IND AS Compliances in Transitional EconomiesKey note Address by CA Subodh Kumar Agrawal, Past President, ICAIInd AS Implementation Issues & Opportunities CA Dolphy D Souza, MumbaiLunch (2.00 PM to 3.00 PM)Third Knowledge Session (3.00 PM to 5.30 PM)Panel Discussion – Insolvency & Bankruptcy CodeInsolvency code a Catalyst to Industrial Eminent PanelistsRevival & Resolution

Fourth Knowledge Session (10:00 AM to 12:00 Noon)

Keynote Address & Dr. Asim Dasgupta,Session Chairman Former Finance Minister, Government of West Bengal

Important Issues in GST CA S. Venkataramani, Bengaluru

Fifth Knowledge Session ( 12.00 Noon to 1.30 PM) : Special Session

Topic : Reform, Perform & Transform : The Mantra to resurgent economies Key Note Speaker Eminent Speaker Lunch : 1.30 PM TO 2.15 PM

Sixth Knowledge Session (2.15 PM TO 4.00 PM)Beyond the Cloud : The future of AuditingSpecial Address by CA Yogesh Gupta*, IPS, ED (ER)Digital Forensics & IT Security Mr. Sachin Dedhia, Mumbai Cyber Crime Investigator & Cert. Ethical Hacker, USA

Seventh Knowledge Session (4.00 PM TO 5.30 PM)

Panel Discussion on GST : Eminent Panelists180 Days of GST Implementation in India

Day 2 : Saturday, 23rd December 2017

1. Platinum Sponsor – Rs. 11,00,000/-

A. Company Logo / Branding Ø Backdrop Ø Brochure Ø Souvenir & printed material of Regional Council Ø Standee B. Full page advertisement in the Souvenir C. Post Event Covering in printing media / Newspaper D. One Stall – Two Days (6’ x 4’) to show case your products E. 20 delegates with all facilities F. ½ Hour Slot / Session in the Technical Session G. Recognition in Valedictory Session H. Two Banners inside the venue (Science City) I. Logo in Entry / Welcome Gate J. Insertion in Kit K. Banner Display in Dining Area L. Standdee - On approach to the main venue M. Promotional Videos

2. Diamond Sponsor – Rs. 8,00,000/-

A. Company Logo / Branding Ø Backdrop Ø Brochure Ø Souvenir & printed material of Regional Council Ø Standee B. Full page advertisement in the Souvenir C. Post Event Covering in printing media / Newspaper D. One Stall – Two Days to show case your products E. 10 delegates with all facilities F. Recognition in Valedictory Session G. One Banner inside the venue (Science City) H. Logo in Entry / Welcome Gate I. Insertion in Kit J. Promotional Videos

3. Gold Sponsor – Rs. 6,00,000/- A. Company Logo / Branding Ø Backdrop Ø Brochure Ø Printed material of Regional Council B. Full page advertisement in the Souvenir C. Post Event Covering in printing media / Newspaper D. One Stall - 2 days to show case products E. 5 delegates with all facilities E. Recognition in Valedictory Session F. Logo in Entry / Welcome Gate H. Promitional Videos4. Silver Sponsor – Rs. 4,00,000/- A. Company Logo / Branding Ø Backdrop - Innder Side Wings Ø Brochure Ø Printed material of Regional Council B. Full page advertisement in the Souvenir C. 5 delegates with all facilities D. Recognition in Valedictory Session E. Logo in Entry / Welcome Gate5. Bronze Sponsor – Rs. 2,00,000/- A. Company Logo / Branding Ø Backdrop - Outer side wings Ø Brochure Ø Printed material of Regional Council B. Full page advertisement in the Souvenir C. Recognition in Valedictory Session D. Logo in Entry / Welcome Gate6. Associate Sponsor (A) – Rs.1,00,000/- A. Company Logo / Branding Ø Standee Ø Brochure Ø Printed material of Regional Council B. Half page advertisement in the Souvenir C. Recognition in Valedictory Session

For details please contact: CA Vikash Mawandia, Sr. Executive Officer, EIRC l Ph : 30211136 l Email : [email protected]

Mr. Amit Paul, Assistant Secretary, EIRC l Ph : 30211133 l Email : [email protected] l Website : www.eirc-icai.org

* Confirmation Awaited

CPE : 12 Hrs.Fees :

Online Registration from www.eirc-icai.org

Offline Registration by Cash/Cheque or Draft in favour of

“EIRC- Regional Conference”

Rs. 2000/- + GST (after 31st October)Rs.1700/- + GST (before 31st October)

6 EIRC 1st October 2017

Dear Students,

Though may sound harping on the same string,

I take it a pleasure to write to you every month.

This gives me a kind of pleasure cannot be

expressed by mere words.

I wonder how it moves ! When I am writing

to you, listening and enjoying the pre-puja

celebrations and mirth and rejoicing. When it

will be reaching you, everything will be over

with the idol getting immersed into the eternal flow of the holy Ganges. In between,

there are invoking the Mother Goddess, worshipping and celebrating this festivity.

Many a way, people from all religions remain involved in this occasion. The greatest

message it conveys is that there is only one religion – the religion of humanity. I

pray from my innermost that being a part of a noble profession like Chartered

Accountancy, you may learn and imbibe this tenet of living in your entire attitude

to profession and life.

New TEAM EICASA has assumed office on 16th September 2017. I expect from

them a lot of energy and vitality to be invested. I wish to tell them that previous

shortcomings must be sent to non-recycle bin while the innovations must come

in procession. It is really rejoicing to share that during transition period of TEAM EICASA , no communication gap has been noticed, which surely establishes that our students association has been really doing wonderfully.

When sounds and fury end, silence starts working. Just the same way, when attitude works, ego escapes. Very often, this innocent-looking 3-lettered word rules and emerges imperialistic keeping the objective interest way aside. TEAM EICASA is beyond this. They have cultivated this ATTITUDE of getting un-egoistic realising the basic truth that living finds its purpose only when ego gets cremated.

I ,being the supreme authority of this great and energetic TEAM , feel proud and glad to see them work under my leadership. Great numbers of programmes for all levels of CA Course are being conceived by us. Feel free to write your grievance and gratitude directly to me at [email protected], stay connected to the whatsapp groups being created and enriched by TEAM EICASA with discussion and details of various events.

Finally requesting you all to that observation is better than anything while participation can be replaced by nothing.

Wrapping up with heartiest wishes of Durgapuja.

CA Sonu JainChairperson EICASA and Vice Chairperson EIRC of ICAI

EICASA

Mega Career Counselling on 31st August 2017

Help in building a tax-compliant nation, Support Operation Clean Money

Lighting the Inauguration Lamp L –R: CA (Dr) Debashis Mitra, Dy. Convener, Career Counselling Group, ICAI, CA Dhiraj Kumar Khandelwal, Convener, Career Counselling Group, ICAI, Prof. (Dr.) Ashok Banerjee, CA Manish Goyal, Chairman, EIRC, CA Ranjeet Kumar Agarwal, Council Member, ICAI, CA Sushil Kumar Goyal, Council Member, ICAI, CA Sanjib Sanghi, Treasurer, EIRC

The students of various Schools participating in the programme

In the light of demonetisation, Income Tax Department (ITD) initiated Operation Clean Money (OCM) or Swachh Dhan Abhiyan on 31st January 2017 with the objective, to create a tax compliant society through a fair, transparent and non-intrusive tax administration. In this regard, Operation Clean Money Portal (https://www.cleanmoney.gov.in/) was launched by the Union Minister of Finance, Shri Arun Jaitley, wherein, section on citizen engagement was included. (Refer ‘Clean Money Participants’ section).

We, at ICAI, are thereby pledging our support for the mission. In this regard, we urge you to actively participate in Operation Clean Money by extending your support and filling up your credentials [membership no. and DOB] under the ‘Most Important ’section of ICAI Website by clicking at “Operation Clean Money – Take a Pledge!”

For more information, visit www.cleanmoney.gov.in or for any queries, suggestions, feedback, reach out at [email protected]

9th ANNUAL CONFERENCE OF VIPCADate: Saturday, 18th November 2017 l Time: 9.30am to 5.30pm

Venue: Royal Bengal Room, City Centre-I, Kolkata l 6 CPE @ RS 1000/-(online Registration from www.vipca.in)

Various topics on Goods & Service Tax Direct Tax Implications on Benami Transaction, Shell CompaniesAnd other Anti Tax Avoidance Measures

1) CA. S. Venkataramni, Bengaluru 1) Advocate Kapil Goel, New Delhi

2) CA. Atul Kumar Gupta, New Delhi 2) CA. Manish Dafria, Indore

For any further details Please contact: VIP Road, CA Study Circle - EIRC

CA S N Jajodia - 9830071300, CA Rajesh Singhania - 9830094600, CA Kamal Bajoria - 9830281151, Rajesh Jalan 9831228811

EIRC 1st October 2017 7

Announcements

TECHNOLOGY SUMMITOrganised By :

DIGITAL ACCOUNTING & ASSURANCE BOARD (DAAB), ICAIHosted By:

Eastern India Regional CouncilThe Institute of Chartered Accountants of India

Theme: Empowering CAs to meet Challenges of Digital InformationDay & Date: Saturday, 14th october 2017

Time: 10.00am to 5.30pm l Venue: Park Hotel, Kolkata

CPE : 6 Hrs.Members: Rs. 1000/- +GSTSpot : Rs.1500/- + GSTNon Members : Rs.1200/-+GST

* Confirmation awaited

Fees :

Registration (9.00am to 10.00am)

Inaugural Session (10.00am to 10.30am)Chief Guest - Shri Debashis Sen, IAS – Addl. Chief Secretary

Ministry of Information Technology & Electronics, Govt. of West BengalTechnical Session – I : 10.30 am to 11.45 am

How to empower Audit through Data Analytics?CA Abdul Rafeq, Bangalore

Technical Session – II : 11.45 am to 1.00 pmHow to use Artificial Intelligence & Analytics in Audit?

CA Babu Jayendran, Bangalore

Technical Session – III : 1.45 pm to 3.00 pmHow to protect confidential information at CA’s office using cyber

security best practices?CA E Narasimhan*, Bangalore

Technical Session – IV : 3.00 pm to 4.00 pmAvenues for CAs in Auditing or Implementing SAP / ERP Software

Eminent Speaker

Panel Discussion : 4.00 pm to 5.30 pm How to use automation for pro-active compliance of GST

Moderator : Eminent PersonalityPanelists : CA Venugopal, Bangalore* and Others

Programme ChairmanCA MP Vijay Kumar, Chairman, DAAB, ICAI

Programme DirectorCA (Dr.) Debashis Mitra, Member, DAAB, ICAI

Programme CoordinatorCA Manish Goyal, Chairman, EIRC

8 EIRC 1st October 2017

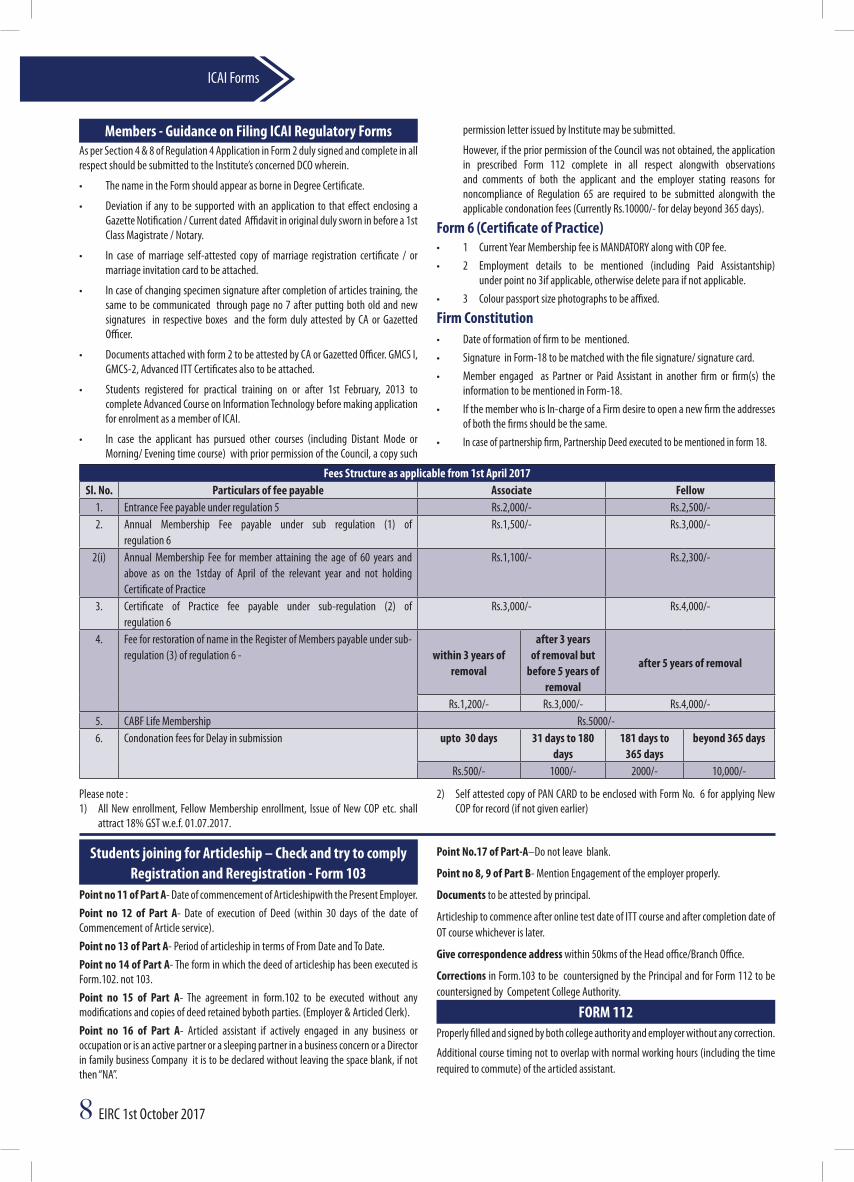

ICAI Forms

permission letter issued by Institute may be submitted.

However, if the prior permission of the Council was not obtained, the application in prescribed Form 112 complete in all respect alongwith observations and comments of both the applicant and the employer stating reasons for noncompliance of Regulation 65 are required to be submitted alongwith the applicable condonation fees (Currently Rs.10000/- for delay beyond 365 days).

Form 6 (Certificate of Practice)• 1 CurrentYearMembershipfeeisMANDATORYalongwithCOPfee.• 2 Employment details to be mentioned (including Paid Assistantship)

under point no 3if applicable, otherwise delete para if not applicable. • 3 Colourpassportsizephotographstobeaffixed.

Firm Constitution• Dateofformationoffirmtobementioned.• SignatureinForm-18tobematchedwiththefilesignature/signaturecard.• Member engaged as Partner or Paid Assistant in another firm or firm(s) the

information to be mentioned in Form-18.• IfthememberwhoisIn-chargeofaFirmdesiretoopenanewfirmtheaddresses

of both the firms should be the same.• In case of partnership firm, Partnership Deed executed to be mentioned in form 18.

Fees Structure as applicable from 1st April 2017Sl. No. Particulars of fee payable Associate Fellow

1. Entrance Fee payable under regulation 5 Rs.2,000/- Rs.2,500/-2. Annual Membership Fee payable under sub regulation (1) of

regulation 6 Rs.1,500/- Rs.3,000/-

2(i) Annual Membership Fee for member attaining the age of 60 years and above as on the 1stday of April of the relevant year and not holding Certificate of Practice

Rs.1,100/- Rs.2,300/-

3. Certificate of Practice fee payable under sub-regulation (2) of regulation 6

Rs.3,000/- Rs.4,000/-

4. Fee for restoration of name in the Register of Members payable under sub-regulation (3) of regulation 6 - within 3 years of

removal

after 3 years of removal but

before 5 years of removal

after 5 years of removal

Rs.1,200/- Rs.3,000/- Rs.4,000/-5. CABF Life Membership Rs.5000/-6. Condonation fees for Delay in submission upto 30 days 31 days to 180

days181 days to

365 daysbeyond 365 days

Rs.500/- 1000/- 2000/- 10,000/-

Please note :1) All New enrollment, Fellow Membership enrollment, Issue of New COP etc. shall

attract 18% GST w.e.f. 01.07.2017.

2) Self attested copy of PAN CARD to be enclosed with Form No. 6 for applying New COP for record (if not given earlier)

Point No.17 of Part-A–Do not leave blank.

Point no 8, 9 of Part B- Mention Engagement of the employer properly.

Documents to be attested by principal.

Articleship to commence after online test date of ITT course and after completion date of OT course whichever is later.

Give correspondence address within 50kms of the Head office/Branch Office.

Corrections in Form.103 to be countersigned by the Principal and for Form 112 to be countersigned by Competent College Authority.

FORM 112Properly filled and signed by both college authority and employer without any correction.

Additional course timing not to overlap with normal working hours (including the time required to commute) of the articled assistant.

Members - Guidance on Filing ICAI Regulatory FormsAs per Section 4 & 8 of Regulation 4 Application in Form 2 duly signed and complete in all respect should be submitted to the Institute’s concerned DCO wherein.

• ThenameintheFormshouldappearasborneinDegreeCertificate.

• Deviation if any tobe supportedwithanapplication to thateffectenclosingaGazette Notification / Current dated Affidavit in original duly sworn in before a 1st Class Magistrate / Notary.

• In case of marriage self-attested copy of marriage registration certificate / ormarriage invitation card to be attached.

• Incaseofchangingspecimensignatureaftercompletionofarticlestraining,thesame to be communicated through page no 7 after putting both old and new signatures in respective boxes and the form duly attested by CA or Gazetted Officer.

• Documentsattachedwithform2tobeattestedbyCAorGazettedOfficer.GMCSI,GMCS-2, Advanced ITT Certificates also to be attached.

• Students registered for practical training on or after 1st February, 2013 tocomplete Advanced Course on Information Technology before making application for enrolment as a member of ICAI.

• In case the applicant has pursued other courses (including Distant Mode orMorning/ Evening time course) with prior permission of the Council, a copy such

Students joining for Articleship – Check and try to complyRegistration and Reregistration - Form 103

Point no 11 of Part A- Date of commencement of Articleshipwith the Present Employer.Point no 12 of Part A- Date of execution of Deed (within 30 days of the date of Commencement of Article service).Point no 13 of Part A- Period of articleship in terms of From Date and To Date.Point no 14 of Part A- The form in which the deed of articleship has been executed is Form.102. not 103.Point no 15 of Part A- The agreement in form.102 to be executed without any modifications and copies of deed retained byboth parties. (Employer & Articled Clerk).Point no 16 of Part A- Articled assistant if actively engaged in any business or occupation or is an active partner or a sleeping partner in a business concern or a Director in family business Company it is to be declared without leaving the space blank, if not then “NA”.

EIRC 1st October 2017 9

IMPORTANT CASE LAWS (DIRECT TAXES)

Case Laws on Direct Taxes

Compiled by : CA Raj SinghaniaEmail : [email protected].

Important Case laws (Direct Taxes)1. Adiveppa vs. Bhimappa (Supreme Court) HUF Law: It is a settled principle of Hindu law that there lies a legal

presumption that every Hindu family is joint in food, worship and estate and in the absence of any proof of division, such legal presumption continues to operate in the family. The burden lies upon the member who after admitting the existence of jointness in the family properties asserts his claim that some properties out of entire lot of ancestral properties are his self-acquired property

(i) It is a settled principle of Hindu law that there lies a legal presumption that every Hindu family is joint in food, worship and estate and in the absence of any proof of division, such legal presumption continues to operate in the family. The burden, therefore, lies upon the member who after admitting the existence of jointness in the family properties asserts his claim that some properties out of entire lot of ancestral properties are his self-acquired property. (See-Mulla – Hindu Law, 22nd Edition Article 23 “Presumption as to co-parcenary and self acquired property”- pages 346 and 347).

(ii) In our considered opinion, the legal presumption of the suit properties comprising in Schedule ‘B’ and ‘C’ to be also the part and parcel of the ancestral one (Schedule ‘D’) could easily be drawn for want of any evidence of such properties being self-acquired properties of the plaintiffs. It was also for the reason that the plaintiffs themselves had based their case by admitting the existence of joint family nucleolus in respect of schedule ‘D’ properties and had sought partition by demanding 4/9th share.

(iii) In our considered opinion, it was, therefore, obligatory upon the plaintiffs to have proved that despite existence of jointness in the family, properties described in Schedule ‘B’ and ‘C’ was not part of ancestral properties but were their self-acquired properties. As held above, the plaintiffs failed to prove this material fact for want of any evidence.

2. CIT vs. Sinhgad Technical Education Society (Supreme Court) S. 153A/ 153C: The seized incriminating material have to pertain to the

AY in question and have co-relation, document-wise, with the AY. This requirement u/s 153C is essential and becomes a jurisdictional fact. It is an essential condition precedent that any money, bullion or jewellery or other valuable articles or thing or books of accounts or documents seized or requisitioned should belong to a person other than the person referred to in S. 153A. Kamleshbhai Dharamshibhai Patel 31 TM.com 50 (Guj) approved. SSP Aviation 20 TM.com 214 (Del) distinguished

In these appeals, qua the aforesaid four Assessment Years, the assessment is quashed by the ITAT (which order is upheld by the High Court) on the sole ground that notice under Section 153C of the Act was legally unsustainable. The events recorded above further disclose that the issue pertaining to validity of notice under Section 153C of the Act was raised for the first time before the Tribunal and the Tribunal permitted the assessee to raise this additional ground and while dealing 12 with the same on merits, accepted the contention of the assessee.

(ii) First objection of the learned Solicitor General was that it was improper on the part of the ITAT to allow this ground to be raised, when the assessee had not objected to the jurisdiction under Section 153C of the Act before the AO. Therefore, in the first instance, it needs to be determined as to whether ITAT was right in permitting the assessee to raise this ground for the first time before it, as an additional ground.

(iii) The ITAT permitted this additional ground by giving a reason that it was a jurisdictional issue taken up on the basis of facts already on the record and, therefore, could be raised. In this behalf, it was noted by the ITAT that as per the provisions of Section 153C of the Act, incriminating material which was seized had to pertain to the Assessment Years in question and it is an undisputed fact that the documents which were seized did not establish any co-relation, document-wise, with these four Assessment Years. Since this requirement under Section 153C of

Termination and Completion - Form 109 and 108No Signature mismatch of student and member (Articled Clerk and Employer).Work details in page 4 of form109 to tally with the period served and the leave taken in page 1 of form 109.Break in articleship due to termination to be given in form 108 with the exact period of articleship in terms of period served, leave, work details in the last term served. If termination takes place after 1 yearLetter from the student requesting for transfer/termination with valid reasons with documents.Letter from Principal giving consent for transfer/termination with documents.If termination takes place within 1 yearForm 109 duly filled and signed by both Principal and Student.Industrial Training - Form 104Both groups passed and the final registration fees paid for joining Industrial Training Form 104 to be executed in non-judicial stamp paper or affix special adhesive stamp of Rs 15.The current employment status in form 104 to be given.The article clerk to intimate the Employer three months in advance before taking Industrial Training.Articled assistants may visit www.icai.org for “List of Industries (Organisations) approved by ICAI for undergoing Industrial Training. Supplementary Registration – Form 107Form 107 to be executed in non-judicial stamp paper or affixed with special adhesive stamp of Rs. 15.Form 107 to be submitted within 60 days from the commencement date to avoid payment of condonation fees.Form 107 is applicable only in case of excess leave (after 3 years) where the student served the same firm same principal from the very next day after termination.To qualify for Final ExaminationStudents who have been registered for Final can appear for the examination during the last 6 months of their articled training provided they have completedat least 2 years 6months of articleship training as on 31st October for May Examination and at least 2 years 6 months as on 30th April for November Examination.The articleship status to be active on the first day of the month of examination. Balance period includes excess leaves if any, to be completed within six months i.e. on or before 30th April for May Examination and 31st October for November Examination.Calculation of excess leavea) Total period served during 3 years = 1095 daysb) Leave taken during the above period = 210 daysc) Period actually served = 885 days ( a - b)d) Leave Entitled/Earned -(1/6th of 885 days) = 147 days (1/6 of c)e) Excess Leave = 63 days (b - d)The student has to serve the excess leave period by submitting form 107 or 103 as required. It may be mentioned here that students are adviced not to take any leave during the excess leave period as those leave days need to be served again by submitting form 103.Note: Form 107 needs to be submitted when articleship is being done under the same Principal and there is no gap between the termination date of the previous articleship and the commencement date of the new articleship.Note: Sunday/ public holidays NOT to be considered as leave.For the purpose of preparing for CA Exam, the article clerk shall be granted leave by the Principal for 3 months or to the extent due, whichever is less, provided an application for leave has been made at least 15 days in advance before availing the leave.The days (including intervening holidays) on which the article clerk appears for any CA exam shall not be treated as leave but would be treated as period served under articleship.

10 EIRC 1st October 2017

Case Laws on Direct Taxes

the Act is essential for assessment under that provision, it becomes a jurisdictional fact. We find this reasoning to be logical and valid, having regard to the provisions of Section 153C of the Act. Para 9 of the order of the ITAT reveals that the ITAT had scanned through the Satisfaction Note and the material which was disclosed therein was culled out and it showed that the same belongs to Assessment Year 2004-05 or 13 thereafter. After taking note of the material in para 9 of the order, the position that emerges therefrom is discussed in para 10. It was specifically recorded that the counsel for the Department could not point out to the contrary. It is for this reason the High Court has also given its imprimatur to the aforesaid approach of the Tribunal. That apart, learned senior counsel appearing for the respondent, argued that notice in respect of Assessment Years 2000-01 and 2001-02 was even time barred.

(iv) We, thus, find that the ITAT rightly permitted this additional ground to be raised and correctly dealt with the same ground on merits as well. Order of the High Court affirming this view of the Tribunal is, therefore, without any blemish. Before us, it was argued by the respondent that notice in respect of the Assessment Years 2000-01 and 2001-02 was time barred. However, in view of our aforementioned findings, it is not necessary to enter into this controversy.

(v) Insofar as the judgment of the Gujarat High Court in Kamleshbhai Dharamshibhai Patel v. Commissioner of Income Tax-III, (2013) 31 taxmann.com 50 (Gujarat) relied upon by the learned Solicitor General is concerned, we find that the High Court in that case has categorically held that it is an essential condition precedent that any money, bullion or jewellery or other valuable articles or thing or books of accounts or documents seized or requisitioned should belong to a person other than the person referred to in Section 153A of the Act. This proposition of law laid down by the High Court is correct, which is stated by the Bombay High Court in the impugned judgment as well. The judgment of the Gujarat High Court in the said case went in favour of the Revenue when it was found on facts that the documents seized, in fact, pertain to third party, i.e. the assessee, and, therefore, the said condition precedent for taking action under Section 153C of the Act had been satisfied.

3. PCIT vs. Delhi Airport Metro Express Pvt. Ltd (Delhi High Court) S. 263 Revision: For the purposes of exercising jurisdiction u/s 263, the

conclusion of the CIT that the order of the AO is erroneous and prejudicial to the interests of the Revenue has to be preceded by some minimal inquiry. If the PCIT is of the view that the AO did not undertake any inquiry, it becomes incumbent on the PCIT to conduct such inquiry. The second option available u/s 263 (1) of sending the entire matter back to the AO for a fresh assessment can be exercised by the PCIT only after he undertakes an inquiry himself and not otherwise

(i) One of the factors that weighed with the PCIT in exercising jurisdiction under Section 263 of the Act was Circular No. 9 of 2014 dated 23rd April 2014 issued by the Central Board of Direct Taxes which stated that “under the BOT arrangement an assessee would only be allowed amortization in respect of expenditure incurred in creation of the infrastructure facility over the period of BOT arrangement and no depreciation would be allowed on such infrastructure under provisions of the Act”. The case of the Assessee was that such a Circular could not dictate to the AO how he should frame his assessment and, to the extent the Circular was prejudicial to the Assessee, its application would be beyond the scope and ambit of the powers conferred on the Board under Section 119 of the Act.

(ii) It is seen, in the order dated 30th March 2016, the PCIT has proceeded by setting out the contents of the SCN and the contents of the reply given by the Assessee. It appears that no inquiry, as such, was undertaken by the PCIT to come to the conclusion that the original assessment order was erroneous and prejudicial to the interests of the Revenue.

(iii) For the purposes of exercising jurisdiction under Section 263 of the Act, the conclusion that the order of the AO is erroneous and prejudicial to the interests of the Revenue has to be preceded by some minimal inquiry. In fact, if the PCIT is of the view that the AO did not undertake any inquiry, it becomes incumbent on the PCIT to conduct such inquiry. All that PCIT has done in the impugned order is to refer to the Circular of the CBDT and conclude that “in the case of the Assessee

company, the AO was duty bound to calculate and allow depreciation on the BOT in conformity of the CBDT Circular 9/2014 but the AO failed to do so. Therefore, the order of the AO is erroneous insofar as prejudicial to the interest of revenue”.

(iv) In the considered view of the Court, this can hardly constitute the reasons required to be given by the PCIT to justify the exercise of jurisdiction under Section 263 of the Act. In the context of the present case if, as urged by the Revenue, the Assessee has wrongly claimed depreciation on assets like land and building, it was incumbent upon the PCIT to undertake an inquiry as regards which of the assets were purchased and installed by the Assessee out of its own funds during the AY in question and, which were those assets that were handed over to it by the DMRC. That basic exercise of determining to what extent the depreciation was claimed in excess has not been undertaken by the PCIT.

(v) Mr. Asheesh Jain then volunteered that the PCIT had exercised the second option available to him under Section 263 (1) of the Act by sending the entire matter back to the AO for a fresh assessment. That option, in the considered view of the Court, can be exercised only after the undertakes an inquiry himself in the manner indicated hereinbefore. That is missing in the present case.

(vi) Therefore, the Court is of the view that the ITAT was not in error in setting aside the impugned order of the PCIT under Section 263 of the Act.

4. H. T. Media Limited vs. Pr CIT (Delhi High Court) S. 14A/ Rule 8D: Entire law explained on what constitutes proper

recording of satisfaction by the AO, scope of disallowance of interest expenses under Rule 8D(2)(i), admin expenses under Rule 8D(2)(iii), need for nexus between borrowed funds and tax-free investments and power of the ITAT to remand to the AO

The High Court had to consider the following questions of law:

(1) “Whether the ITAT erred in remitting the matter concerning the deletion of disallowance of interest under clause (ii) of Rule 8 D (2) of the Income Tax Rules, 1962 to the Assessing Officer for a fresh determination in light of the decision of this Court in CIT v. Taikisha Engineering India Ltd. (2015) 370 ITR 338 (Del)?”

(2) “Whether the Assessing Officer recorded a proper satisfaction in terms of Section 14A (2) and Rule 8 (D) of the Income Tax Rules, 1962 and, in calculating the disallowance at 0.5% of average value of investments as per clause (iii) of Rule 8 D (2) of the Income Tax Rules, 1962?”

HELD by the High Court: 27. In cases involving Section 14 A of the Act, the constant tug-of-war

lies in the Revenue wanting to increase the expenditure incurred to earn exempt income for the purpose of disallowance, while the Assessee seeks to establish the opposite. In CIT v. Walfort Share and Stock Brokers P. Ltd. [2010] 326 ITR 1 (SC), the Supreme Court noted that legislative intent behind Section 14A was not to allow deduction in respect of any expenditure incurred by an Assessee in relation to exempt income, i.e. income which does not form part of the total income under the said Act, against the taxable income. The Supreme Court observed as under:

“In other words, section 14A clarifies that expenses incurred can be allowed only to the extent they are relatable to the earning of taxable income. In many cases the nature of expenses incurred by the assessee may be relatable partly to the exempt income and partly to the taxable income. In the absence of section 14A, the expenditure incurred in respect of exempt income was being claimed against taxable income. The mandate of section 14A is clear. It desires to curb the practice to claim deduction of expenses incurred in relation to exempt income against taxable income and at the same time avail of the tax incentive by way of an exemption of exempt income without making any apportionment of expenses incurred in relation to exempt income . . . Expenses allowed can only be in respect of earning of taxable income. This is the purport of section 14A. In section 14A, the first phrase is ‘for the purposes of computing the total income under this Chapter’ which makes it clear that various heads of income as prescribed in the Chapter IV would fall within section 14A. The next phrase is, ‘in relation to income which does not form part of total income under the Act’. It means that if an income does not form part of total income, then the related expenditure is outside the ambit of the applicability of section 14A.”

EIRC 1st October 2017 11

EIRC Events

Banking Colloquium on 16th September 2017

Seminar on Interactive Session on E - Filing of GST Returns & Other Compliances on

1st September 2017

Investor Awareness Programme on Commodity Derivatives on

5th September 2017

Companies Act 2013 and CSR on 9th September 2017

L- R: CS Reema Jain, CA Sonu Jain, Vice Chairperson, EIRC, CA Manish Goyal, Chairman, EIRC

Releasing the Official Souvenir. Seen CA Manish Goyal, Chairman, EIRC (extreme left) and CA Abhijit Bandyopadhyay, Past Council Member, ICAI (extreme right)

CA Manish Goyal, Chairman, EIRC addressing the gathering

Seminar on Issues in Tax Audit & Impact of IND AS on MAT on 6th September 2017

L - R: CA Sanjay Bhattacharya, CA Nitesh More, Member, EIRC, CA Vivek Agarwal

L - R: CA Manish Goyal, Chairman, EIRC, CA Gagan Kedia

Workshop on GST from 7th to 9th September 2017

CS T B Chatterjee CA Vivek Jalan CA Shivani Shah CA Vikash Parakh CA Rip Das CA Gagan Kedia

Faculty Identification Programme on 10th September 2017

Recent Changes in Companies Act on

11th September 2017

Seminar on ICDS on 12th September 2017

L – R: CA Jatin Christopher, CA Manish Goyal, Chairman, EIRC, CA Jayesh Gogri CA (Dr.) Debashis Mitra, Council Member, ICAI

CA Sanjib Sanghi, Treasurer, EIRC, CA Ayush Goel

Seminar on ROC Filing and Secretarial & Corporate Law Compliances on

18th September 2017

CS Munmi Phukan, CS Pammy Jaiswal

L - R: Mr. Arunava Chattopadhyay, Exe. Dev. MCX India Ltd., Mr. Laltu Pore, AGM, SEBI, CA Anirban Datta, Past Chairman, EIRC, CA Nitesh Kumar More, Member, EIRC, Mr. Vibhor Tandon, Asst. VP, MCX India Ltd.

If undelivered please return to : Eastern India Regional Council, The Institute of Chartered Accountants of India, 7, Anandilal Poddar Sarani (Russell Street), Kolkata - 700 071 12

Registered RN 27144/75 Registration No. KOL RMS / 227 / 2016-18

BOOK POSTCA Manish Goyal, EditorCA Sonu Jain, Jt. EditorCA Sumit Binani, Member

CA Sanjib Sanghi, MemberCA Debashis Mitra, MemberCA Sushil Kr. Goyal, Member

Owner: The Institute of Chartered Accountants of India, Eastern India Regional Council Printer: Shri Alok Ray, Joint Secretary, The Institute of Chartered Accountants of India, Publisher: Shri Alok Ray, Joint Secretary, The Institute of Chartered Accountants of India Published from : The Institute of Chartered Accountants of India, Eastern India Regional Council, 7, Anandilal Poddar Sarani, P.S.: Shakespeare Sarani, Kolkata - 700 071 Printed from: CDC Printers Pvt. Ltd., Tangra Industrial Estate - II, (Bengal Pottery), 45, Radhanath Chowdhury Road, P.S. :Tangra Kolkata - 700 015 Editor: CA Manish Goyal, Chairman, Eastern India Regional Council, The Institute of Chartered Accountants of India.

The Institute does not accept any responsibility for the view expressed in the contributions of advertisements published in the newsletter. Phone: 91-33-30211140/41, Fax: 033-22272317, Website: www.eirc-icai.org, Email : [email protected]