THE INFLUENCE OF E-TAX SERVICES, INCOME AND …

12

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021 Available Online: https://dinastipub.org/DIJEFA Page 109 DOI: https://doi.org/10.38035/dijefa.v2i1 Received: 30 Maret 2021, Revised: 8 April 2021, Publish: 15 April 2021 THE INFLUENCE OF E-TAX SERVICES, INCOME AND COMMUNICATION STYLE ON TAX COMPLIANCE Nany Saryono Putri 1 , Apollo Daito 2 1) Department of Accounting, Universitas Mercubuana, Jakarta, Indonesia, [email protected] 2) Department of Accounting, Universitas Mercubuana, Jakarta, Indonesia Corresponding Author: Nany Saryono Putri 1 Abstract: This study aims to determine what factors affect taxpayer compliance. The variables to be studied are e-tax services, income level, and communication style. The sample of this research is 88 individual taxpayers (WPOP) in the city of Tangerang. Data collection was carried out by distributing questionnaires to the WPOP. The data that has been obtained is tested using the second order method with the help of the SmartPLS program. The overall results of this study indicate that e-tax services have a significant effect on taxpayer compliance, with the level of income and communication styles not having a significant effect on taxpayer compliance. This study has limitations, namely the sample used is less than 100 samples. Keywords: e-tax services, income, communication syle, tax compliance, individual taxpayers. INTRODUCTION In recent years, tax compliance has become one of the targets for contribution of tax revenue in Indonesia (DGT, 2018). This is because taxes are mandatory contributions to the State that are owed by individual or entities that are compelling, without receiving direct compensation and used for the State's needs for the welfare of the people (Taxation Law, 2011: 7). It is said to be compulsory and compelling because taxes are the main source of state revenue. This can be seen from the posture of the 2018 State Budget, state revenue is budgeted at IDR 1,894.7 trillion, where state revenue is dominated by taxes. Tax revenue in 2018 is targeted at Rp. 1,424 trillion, while tax revenue realization only reaches Rp. 1,315.51 trillion, so that by the end of 2018 the tax revenue target has not been achieved. Table 1.Target and realization of tax revenue Year 2016 2017 2018* Target 1.355,20 1.283,57 1.424,00 Realization 1.105,73 1.151,03 1.315,51 Achievement 81,59% 89,67% 92,24% source : annual report

Transcript of THE INFLUENCE OF E-TAX SERVICES, INCOME AND …

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 109

DOI: https://doi.org/10.38035/dijefa.v2i1

Received: 30 Maret 2021, Revised: 8 April 2021, Publish: 15 April 2021

THE INFLUENCE OF E-TAX SERVICES, INCOME AND COMMUNICATION STYLE ON TAX COMPLIANCE

Nany Saryono Putri1, Apollo Daito 2

1) Department of Accounting, Universitas Mercubuana, Jakarta, Indonesia, [email protected] 2)

Department of Accounting, Universitas Mercubuana, Jakarta, Indonesia

Corresponding Author: Nany Saryono Putri 1

Abstract: This study aims to determine what factors affect taxpayer compliance. The variables

to be studied are e-tax services, income level, and communication style. The sample of this

research is 88 individual taxpayers (WPOP) in the city of Tangerang. Data collection was

carried out by distributing questionnaires to the WPOP. The data that has been obtained is

tested using the second order method with the help of the SmartPLS program. The overall results

of this study indicate that e-tax services have a significant effect on taxpayer compliance, with

the level of income and communication styles not having a significant effect on taxpayer

compliance. This study has limitations, namely the sample used is less than 100 samples.

Keywords: e-tax services, income, communication syle, tax compliance, individual taxpayers.

INTRODUCTION

In recent years, tax compliance has become one of the targets for contribution of tax

revenue in Indonesia (DGT, 2018). This is because taxes are mandatory contributions to the

State that are owed by individual or entities that are compelling, without receiving direct

compensation and used for the State's needs for the welfare of the people (Taxation Law,

2011: 7).

It is said to be compulsory and compelling because taxes are the main source of state

revenue. This can be seen from the posture of the 2018 State Budget, state revenue is

budgeted at IDR 1,894.7 trillion, where state revenue is dominated by taxes. Tax revenue in

2018 is targeted at Rp. 1,424 trillion, while tax revenue realization only reaches Rp. 1,315.51

trillion, so that by the end of 2018 the tax revenue target has not been achieved.

Table 1.Target and realization of tax revenue

Year 2016 2017 2018*

Target 1.355,20 1.283,57 1.424,00

Realization 1.105,73 1.151,03 1.315,51

Achievement 81,59% 89,67% 92,24%

source : annual report

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 110

The realization of the PPh Article 25/29 net income from individual taxpayers was

IDR 9.41 trillion while the tax revenue target was IDR 22,209.41 trillion. Meanwhile The

growth in tax revenue in 2018 reached 20.50%, while the growth in tax revenue in 2017

reached 48.03%. So that the data obtained information that the growth of tax revenue has

decreased.

Based on information from the DGT Performance Report 2018, information was

obtained that the compliance ratio for submitting Annual Tax Returns is still low because

individual awareness is still low in carrying out their tax obligations and not optimal

utilization of internal data (approweb and portal application DGT).

Based on information from the tax annual report, The number of registered taxpayers is

dominated by individual taxpayers. However, the tax revenue is not optimal.

The delivery target via e-filling in 2017 was 14 million, but the realization was only 8

million. This is not proportional to the number of registered taxpayers of 39 million

taxpayers. Meanwhile, on the other hand, to support taxpayer compliance, DGT is currently

developing information and communication technology (ICT). The ICT services referred to

by the DGT include e-filling, e-billing, e-registration, e-invoicing, the website

www.pajak.go.id, and others.

The amount of tax that must be paid to the state will be directly proportional to the

income level of the taxpayer. This income level fluctuation can be a consideration for

taxpayers in meeting their obligations such as paying taxes, living expenses, and other

considerations. A tax collection system that is a self-assessment system. With this collection

system it is possible to have a tax gap, so that it needs supervision for taxpayers.

The limited number of DGT employees is known that the number of DGT employees

only reaches around 40 thousand. DGT has an important role in increasing awareness of

taxpayers to comply.

So that the DGT makes use of social media, printed media, letters addressed directly to

taxpayers to educate and confirm the WP OP. Through social media and print media, DGT

publishes content that educates taxpayers to find out tax information. DGT can also issue a

letter of request for data and / or information explanation (SP2DK) addressed to taxpayers to

request an explanation of the data and / or information regarding the suspicion of not

fulfilling tax obligations (SE-39 / PJ / 2015).

However, SP2DK is presented in a very formal writing, so that it has not touched the

emotional side of the taxpayer. On the other hand, the SP2DK, which is a medium of

communication between the tax authorities and the WP, is not effective.

Based on information from the Director General of Taxes of the Ministry of the

Republic of Indonesia through Robert Pakpahan, there are two tax area offices that exceed

the tax revenue target of above 100% for 2017. The two regional offices are Kanwil DJP

Banten and East Java III. Tangerang City is an area within the area of Banten Regional Tax

Office which exceeds the tax revenue target. In addition, the economic growth of Tangerang

city tends to be fast. So this research is needed to determine whether these factors affect the

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 111

compliance of individual taxpayers. If these factors are considered capable of increasing

WPOP compliance, it is possible to implement them in other cities so that WPOP compliance

can increase so that tax revenues will also increase.

LITERATUREREVIEW

The Theory of Reasoned Action (TRA)

According to Ajzen and Fishbein, the theory of reasoned action, namely the

individual's desire, will determine the behavior to carry out or not carry out a particular

behavior. According to this theory, the determinants of willingness to behave are subjective

norms. Subjective norms are the beliefs of each person when they agree or disagree about

behavior based on normative beliefs (Mahyarni, 2013).

The Theory of Planned Behavior (TPB)

According to Ajzen, planned behavior theory develops an approach of reasoned action

by adding perceived control behavior. Perceptions of individual control behavior when

showing ease or difficulty in behaving. The perception of perceived control behavior is

control over beliefs, which includes the perception of each individual regarding the

ownership of expertise that requires resources or the possibility of success in carrying out

activities (Mahyarni, 2013).

Technology Acceptance Model (TAM) theory

This theory was developed by Davis (1986). According to Davis, et al (1986),

individuals use information technology begins with perceptions of its benefits and ease of

use. Perception of benefits is defined as the benefits an individual believes in using the

information technology. Meanwhile what is meant by perceived ease is that in using the

information technology, it does not experience difficulties or does not require more effort in

its use.

Attribution Theory

This attribution theory is a theory which states that when individuals observe a person's

behavior, they try to determine whether the behavior is caused internally or externally.

Behavior that is caused due to internal factors is behavior that is believed by the individual

himself, such as awareness, will, and others. Meanwhile, behavior is caused by external

factors, namely behavior that is influenced from outside, such as government policies to pay

taxes so that the individual is willing or unwilling to do so (Robbins, 1996).

Taxes

Based on Article 1 of Law of the Republic of Indonesia Number 28 of 2007, what is

meant by tax is Compulsory contributions to the state that are owed by private persons or

entities that are compelling based on law, without receiving direct compensation and used for

the state's needs for the greatest prosperity of the people. "Taxpayer is an individual or entity,

including taxpayers, tax cutters and tax collectors, who have tax rights and obligations in

accordance with the provisions of taxation laws and regulations.

E-Tax Services

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 112

What is meant by e-tax services is an electronic service channel provided by the DGT

in the framework of developing Information and Communication Technology (TIK) to

exercise rights and obligations in terms of taxation (DGT, 2016: 87).

Income

In Article 4 of Law Number 36 Year 2008, what is meant by income is "any additional

economic capacity received or obtained by a taxpayer, both from Indonesia and outside

Indonesia, which can be used for consumption or to increase the wealth of the taxpayer

concerned, with name and in any form. ”So that what is meant by income level is the size of

the additional economic capacity received by taxpayers from inside and outside Indonesia

which can be used to meet the necessities of life and increase wealth. Where if the higher the

income, the tax paid will be quite large. And conversely, if the income tends to be low, the

taxes that must be paid will also be low.

Communication style

In the Big Indonesian Dictionary (KBBI), what is meant by style is, "the ability to do, a

push or pull that will grind, or an interaction which when working alone causes changes in

circumstances". Meanwhile, the definition of communication in KBBI is "sending and

receiving messages or news between two or more people so that the message in question can

be understood". Communication is also defined by Carl I. Hovland as a process carried out

by the informer so that the recipient of the information can change their behavior.

Tax Compliance

Compliance is the motivation of an individual, group, or organization to do something

in accordance with the applicable rules. Where obedience behavior is an interaction between

individual, group and organizational behavior (Robbins, 2001 in Triyono 2012). Based on

Law 28 of 2007, taxpayers is an individual or entity that has tax rights and / or obligations in

accordance with applicable regulations. In the taxpayer rights and obligations manual, the

Director General of Taxes explains that the taxpayer's obligations are; (1) registering

themselves, (2) payment, withholding / collection, and reporting taxes, (3) fulfilling tax

audits. So that what is meant by taxpayer compliance is the motivation of individuals who

have tax rights and / or obligations to carry it out in accordance with applicable regulations.

RESEARCH FRAMEWORK

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 113

RESEARCH METHODS

In data processing using the structural equation modeling / SEM method because this

study looks at the simultaneous relationship between latent variables and other manifest

variables, as well as the relationship between one latent variable and other latent variables

based on previous research journals and other references (Latan, 2013 ). Thus, the SEM

method can analyze the multivariate analysis which can analyze the relationship between more

complex variables.

In this study, there is a flowchart & measurement model which is a summary of the research to

be carried out.

Pict 2. Flowchart

FINDINGS AND DISCUSSION

Respondents Profile Description

a. Respondents by Education Level

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 114

Pict 3. Respondent’s Education Level

a. Respondents by Type of Work

Pict 4. Respondents’s Occupation

Convergent Validity

Based on the results of the validity test, there is no loading factor whose value is below 0.5, so

there is nothing to drop .

Table 3. Convergent Validity

No. Variable Dimension Question

Item

Loading

Factor Result

1

E-tax services

X1.1

X1.1.1 0,96 Valid

2 X1.1.2 0,92 Valid

3 X1.1.3 0,97 Valid

4 X1.1.4 0,94 Valid

5

X1.2

X1.2.1 0,90 Valid

6 X1.2.2 0,91 Valid

7 X1.2.3 0,95 Valid

8 X1.2.4 0,95 Valid

9

X1.3

X1.3.1 0,90 Valid

10 X1.3.2 0,95 Valid

11 X1.3.3 0,92 Valid

12

Income level

X2.1

X2.1.1 0,90 Valid

13 X2.1.2 0,93 Valid

14 X2.1.3 0,81 Valid

15 X2.2

X2.2.1 0,92 Valid

16 X2.2.2 0,90 Valid

17 X2.3

X2.3.1 0,92 Valid

18 X2.3.2 0,92 Valid

19 X2.4

X2.4.1 0,92 Valid

20 X2.4.2 0,93 Valid

21

Communication

style X3

X3.1 0,87 Valid

22 X3.2 0,88 Valid

23 X3.3 0,92 Valid

24 X3.4 0,79 Valid

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 115

Source: Output SmartPLS (2021)

Average Variance Extracted (AVE)

Based on the test results, it is known that the AVE value of all research variables is> 0.5. The

AVE value indicates that the convergent validity of this study is adequate.

Table 4. AVE values

Source: Output SmartPLS (2021)

Reability Test

Croncbach alpha value> 0.6 and composite reliability> 0.7. This means that the instruments used

in this study have been consistent and will produce the same data when used for several tests on

the same object

Table 4. Reability Test

25 X3.5 0,86 Valid

26 X3.6 0,89 Valid

27 X3.7 0,87 Valid

28 X3.8 0,85 Valid

29 X3.9 0,78 Valid

30

Tax compliance

Y1.1 Y.1.1 0,97 Valid

31 Y.1.2 0,97 Valid

32 Y2 Y.2.1 1,00 Valid

33 Y3 Y.3.1 1,00 Valid

34 Y4 Y.4.1 1,00 Valid

35 Y5.1

Y.5.1.1 0,98 Valid

36 Y.5.1.2 0,98 Valid

Variable & Dimension AVE

values

E-tax services 0,815

Interest in using 0,901

Perceived usefulness 0,861

Perceived ease of use 0,854

Income level 0,689

The principle of carrying power 0,780

Equality principal 0,831

Certainty principal 0,842

Additional of income 0,861

Communication style 0,736

Nudges 0,736

Tax compliance 0,945

On time 0,945

Tax payable 1,000

Audit all taxes 1,000

Tax administration 1,000

Correct SPT filling 0,953

Variable & Dimension Cronbach's

Alpha

Composite

Reliability

E-tax services 0,977 0,980

Interest in using 0,963 0,973

Perceived usefulness 0,946 0,961

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 116

Source: Output SmartPLS (2021)

R Square

The R Square (R2) value of this study is 0.703 (strong) and the Adjusted R-Square (Adj-R2)

value is 0.689.

Table 5. R Square

Variable

R

Square

R Square

Adjust

Tax Compliance 0,703 0,689

Source: Output SmartPLS (2021)

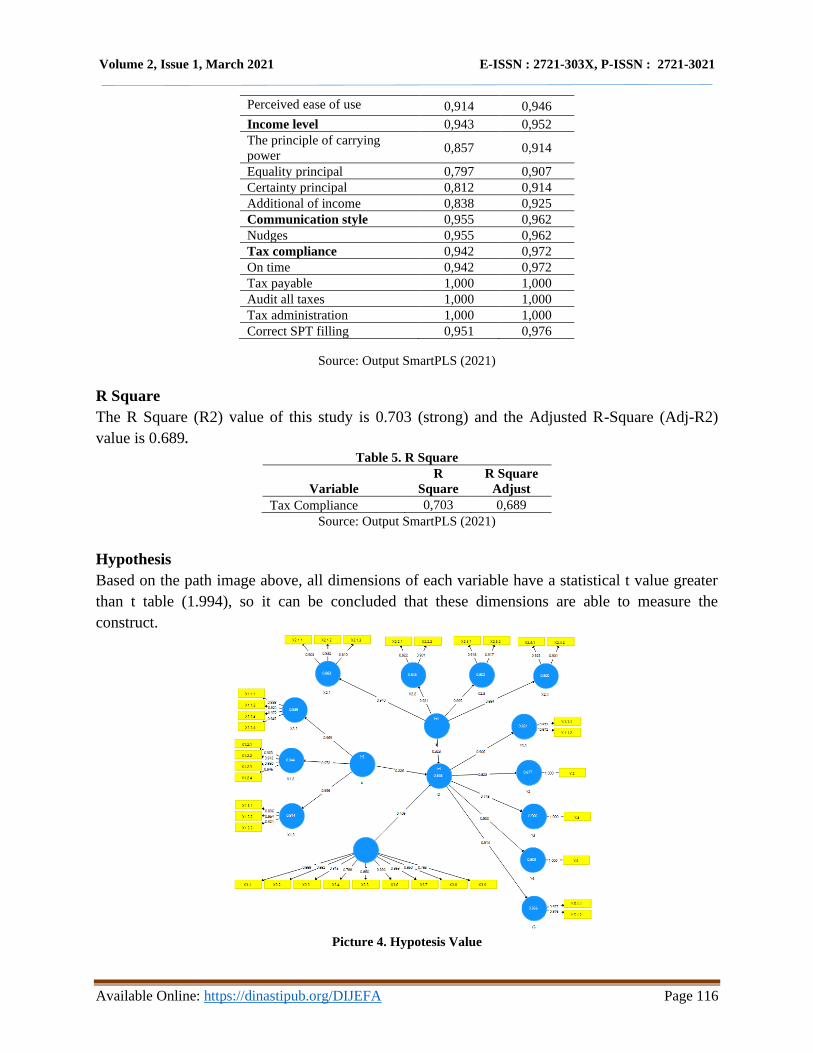

Hypothesis

Based on the path image above, all dimensions of each variable have a statistical t value greater

than t table (1.994), so it can be concluded that these dimensions are able to measure the

construct.

Picture 4. Hypotesis Value

Perceived ease of use 0,914 0,946

Income level 0,943 0,952

The principle of carrying

power 0,857 0,914

Equality principal 0,797 0,907

Certainty principal 0,812 0,914

Additional of income 0,838 0,925

Communication style 0,955 0,962

Nudges 0,955 0,962

Tax compliance 0,942 0,972

On time 0,942 0,972

Tax payable 1,000 1,000

Audit all taxes 1,000 1,000

Tax administration 1,000 1,000

Correct SPT filling 0,951 0,976

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 117

H1: E-Tax Services affects tax compliance

The statistical T value of the E-Tax Services variable is 2.457 or greater than the t table 1.995

(2.457> 1.995) with a significance level of 5% and P values of 0.014 (0.014 <0.05). This shows

the significant effect of E-Tax Services on mandatory compliance with individuals.

H2: Income affects Tax compliance

The T value of the variable statistic. The influence of the income level is 1.102 or less than the t

table 1.995 (1.102 <1.992) with a significance level of 5% and P values of 0.271 (0.271> 0.05).

This shows the insignificant effect of the level of income on mandatory compliance with

individuals.

H3:Communication Style affects Tax compliance

The T value of the variable statistical effect of communication style is 0.865 or less than the t

table 1.995 (0.865 <1.992) with a significance level of 5% and P values of 0.387 (0.387> 0.05).

This shows the insignificant effect of the level of income on mandatory compliance with

individuals.

CONCLUSION AND RECOMMENDATION

Based on the results of the discussion described in the previous chapters, it can be denied that as

follows.

1. Tax services have a positive and significant effect on taxpayers.

2. Income has a positive and not significant effect on taxpayer.

3. Communication style has a positive and not significant effect on taxpayers.

BIBLIOGRAPHY

Amran. 2018. Pengaruh Sanksi Perpajakan, Tingkat Pendapatan dan Kesadaran Wajib Pajak

Terhadap Kepatuhan Wajib Pajak Orang Pribadi (Studi Pada Kantor Pelayanan Pajak

Pratama Makasar Utara). Jurnal Ilmiah Akuntansi, vol. 1 September 2018, hal 1-15.

Antara. 2018. Ditjen Pajak : Realisasi Penerimaan Dua Kanwil Lampaui Target.,

https://mediaindonesia.com. Diakses pada 12 Agustus 2019.

Apollo, M Triandani. 2020. Effect The Understanding Of Taxation, Tax Sanctions And Taxpayer

Awareness Of Taxpayer Compliance (Research On Taxpayers Of Individual

Entrepreneurs In Tangerang Region). Dinasti International Journal of Digital Business

Management 2 (1), 87-93

Apollo, V Mailia. 2020. Pengaruh Profitabilitas, Ukuran Perusahaan Dan Capital Intensity

Terhadap Tax Avoidance. Jurnal Manajemen Pendidikan Dan Ilmu Sosial 1 (1), 69-77

Arief Budi Wardana. 2018. Nudges Pada SP2DK sebagai Bagian dari Upaya Peningkatan Tax

Compliance di Indonesia. Jurnal Pajak Indonesia vol 2 no 1, (2018), hal 23-38.

Arifin, Syamsul Bahri. 2019. Penerapan E-filling, E- Billing, dan Pemeriksaan Pajak Terhadap

Kepatuhan Wajib Pajak Orang Pribadi di KPP Pratama Medan Polonia. Jurnal Akuntansi

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 118

& Bisnis vol 4 No. 2, (2019), hal 9-21.

Asgarkhani, Mehdi. 2005. The Effectiveness of e- Service in Local Government : A Case Study.

Electronik Journal of e-Government Vol 3 issue 1 New Zealand.

Azleen Illias MBA, Mohd Zulkeflee Abd Razak MBA, Mohd Rushdan Yasoa MBA. 2009.

Taxpayer’s Attitude In Using E-Filling System : Is There Any Significant Difference

Among DemographicFactors. Journal of Internet Banking and Commerce, Vol. 14 No. 1.

Badan Pusat Statistik. 2019. Penduduk Berumur 15 Tahun Ke Atas di Kota Tangerang menurut

Golongan Umur dan Jenis Kegiatan Selama Seminggu yang Lalu, 2018.

https://tangerangkota.bps.go.id.Diakses pada 2

Agustus 2019.

Badan Pusat Statistik. 2019Perkiraan Penduduk Beberapa Negara, 2000-2014.Diunduh 22 Juni

2019, https://www.bps.go.id.

Badan Pusat Statistik. 2019. Proyeksi Penduduk Indonesia 2010 - 2035. Diunduh 22 Juni 2019,

https://www.bps.go.id.

Badan Pusat Statistik. 2019. Tabel Dinamis Kependudukan. Diunduh 22 Juni 2019,

https://www.bps.go.id.

Bungin, Burhan.2013. Metodologi Penelitian Sosial & Ekonomi. Kencana. Jakarta.

Christopher Larkin, et.al. 2019. Testing Local Descriptive Norms and Salience of

Enforcement Action : A Filed Experiment to Increase Tax Collection. Journal of Behavioral

Public Administration Vol. 2 No. 1.

Daniel M & Danuta Kasprzyk. 2008. Health Behavior and Health Education : Theory,

Research, and Practice : Thoery of Reasoned Action, Theory of Planned Behavior, and

The Integrated Behavioral Model. University of Washington Seattle.

Direktorat Jenderal Pajak, Kementrian Keuangan Republik Indonesia.2011. Susunan Dalam

Satu Naskah Undang-Undang Perpajakan. Jakarta. Penerbit Direktorat Penyuluhan

Pelayanan dan Humas.

Direktorat Jenderal Pajak, Kementrian Keuangan Republik Indonesia. 2018. Laporan Tahun

2017.

Diunduh tanggal 18 Mei 2019, https://www.pajak.go.id.

Ditjenpajak. 2019. Asas Pemungutan Pajak. https://www.pajak.go.id. Diakses pada1Agustus

2019.

DJPOnline. 2019. Layanan DJP Online. https://djponline.pajak.go.id/default. Diakses pada 21

September 2019.

DJP. 2019. Ditjen Pajak : Penagihan. https://pajak.go.id/id/penagihan. Diakses pada 22

September 2019.

Ghozali, Imam. (2013). Aplikasi Analisis Multivariat dengan Program IBM PLS 21. Edisi 7.

Semarang. Penerbit Universitas Diponegoro.

Ghozali, Imam.(2011). Aplikasi Analisis Multivariate dengan Program PLS.Semarang.Badan

Penerbit Universitas Diponegoro.

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 119

James & Alley. 2010. Tax Compliance, Self Assessment and Tax Administration. University of

Exeter & University of Waikato, New Zealand.

John, Peggy, Simon, Marika. 2007. Persuasive Communications : Tax Compliance

Enforcement Strategies for Sole Proprietors. Contemporary Accounting Research vol 24

no 1. University of Notthingham.

Kementrian Keuangan Republik Indonesia. 2019. Ini Capaian APBN 2018,

https://www.kemenkeu.go.id.Diakses pada 3 Agustus 2019.Kementrian Keuangan

Direktorat Jenderal Pajak. 2017.Surat Edaran Nomor SE-06/PJ/2017. Jakarta.

Kementrian Keuangan Republik Indonesia. 2017. Perekonomian Indonesia dan APBN 2017,

https://www.kemenkeu.go.id/apbn2017. Diakses pada 6 Agustus 2019.

Kementrian Keuangan Direktorat Jenderal Pajak. 2019. Peraturan Direktur Jenderal Pajak

Nomor PER- 02/PJ/2019 Tentang Tata Cara Penyampaian, Penerimaan, dan Pengolahan

Surat Pemberitahuan. Jakarta

Kurnia Romi. 2017. Strategi Komunikasi Kantor Pelayanan Pajak Pratama Pekanbaru Tampan

Dalam Meningkatkan Kesadaran Wajib Pajak di Pekanbaru Melalui Sistem Layanan

Pajak Online E-Filling. JOM FISIP vol 4 no 2 Oktober 2017.

Kurniawan, Albert.2014. Metode Riset untuk Ekonomi & Bisnis. Alfabeta, Bandung.KBBI

Online. 2019.

Lembaga Ilmu Pengetahuan Indonesia. 2016. Jumlah Usia Produktif Besar, Indonesia

Berpeluang Tingkatkan Produktivitas, http://lipi.go.id. Diakses pada 16 Agustus 2019.

Luh Putu, Ni Ketut. 2018. Pengaruh Kesadaran Wajib Pajak, Sanksi Perpajakan, E-filling, dan

Tax Amnesty Terhadap Kepatuhan Pelaporan Wajib Pajak. E-Jurnal Akuntansi, vol 22.2.

Februari, hal 1626 – 1655.

Mahyarni, 2013. Theory of Reasoned Action dan Theory of Planned Behavior (Sebuah Kajian

Historis Tentang Perilaku). Jurnal El-Riyasah, vol 4 no 1.

Mardiasmo. 2011. Perpajakan Edisi Revisi Tahun. Yogyakarta: Andi.

Maria R.U.D Tambunan & Rozan Anwar, 2019. Transformasi Budaya Organisasi Otoritas

Perpajakan Indonesia Menghadapi Era Ekonomi Digital. Jurnal Aplikasi Manajemen dan

Bisnis, vol.5 No 2 Terakreditasi peringkat 2. Dirjen Penguatan Riset dan Pengembangan

Kemenristek.

Maulana Yusup, Aan Hardiyana, Iwan Sidharta. 2015. User Acceptance Model on E-Billing

Adoption : A Study of Tax Payment by Government Agencies. Asia Pasific Journal of

Multidisciplinary Research. Vol 3 No 4, hal 150– 157.

Michael Hallsworth. 2014. The Behavioralist as Tax Collector : Using Natural Field

Experiments to Enhance Tax Compliance. National Bureau of Economic Research,

Cambridge.

Nasional Kontan. 2018. BPS : Jumlah Angkatan Kerja Agustus naik 2,95 juta,

https://nasional.kontan.co.id.

Nurlaela Wati, Lela. 2018. Metodologi Penelitian Terapan Aplikasi PLS, Eviews, Smart PLS,

dan AMOS. Pustaka Amri. Bekasi.

Volume 2, Issue 1, March 2021 E-ISSN : 2721-303X, P-ISSN : 2721-3021

Available Online: https://dinastipub.org/DIJEFA Page 120

Ortax. 2018. Indikator Ketidakpatuhan Wajib Pajak Orang Pribadi di KPP Pratama.

http://www.ortax.org/ortax. Diakses pada 5 Agustus 2019.

Prita Saraswati, Endang Kiswara. 2013. Analisis Terhadap Penerapan Theory of Consumer

Acceptance Technology Pada E-SPT. Diponegoro Journal of Accounting. Vol 2 No 2, hal1.

Rakhmat, Jalaluddin. 2018. Psikologi Komunikasi. Bandung : PT Remaja Rosdakarya.

Ramdhani, Neila. 2011. Penyusuna Alat Pengukur Berbasis Theory of Planned Behavior.

Buletin Psikologi Universitas Gadjah Mada ISSN : 0854-7108, vol 19 no 2, 2011, 55-69.

Sekaran, Uma. 2006. Research Methods for Business. New York : John Willey and Sons.

Sri Widiyanesti, Mochamad Reno Reynaldi. 2016. Analisis Minat Penggunaan Layanan E-

filling oleh Wajib Pajak Melalui Pendekatan Technology Acceptance Model (TAM) di

KPP Pratama Purwakarta. Jurnal Manajemen Indonesia, vol. 16 April 2016.

Sugiyono. 2014. Metode Penelitian Pendidikan Pendekatan Kuantitatif, Kualitatif, dan R&D.

Alfabeta. Bandung

Suprayogo & Mhd. Hasyim. 2018. Pengaruh Penerapan Sistem E-filling Terhadap

Kepatuhan Wajib Pajak Orang Pribadi Dengan Pemahaman Internet Sebagai Variabel

Moderasi Pada Kantor Pelayanan Pajak Pratama Jakarta Jatinegara. Junral

Komunikasi Ilmiah Akuntansi dan Perpajakan. Vol.11 No 2.

Uly, Artha. 2019. Pajak Hanya Tumbuh 2,4%, Sri Mulyani Waspada,

https://economy.okezone.com.

Waluyo. 2016. The Effect of Addition of Taxpayers Number, Tax Audit, Tax Billing, and

Taxpayers Compliance Toward Tax Revenue. The Accounting Journal of BINANIAGA

vol. 01, No. 1, 2016 ISSN : 2527 – 4309.

Waluyo. 2017. Tax Amnesty and Tax Administration System : An Empirical Study in

Indonesia. European Research Studies Journal Vol xx, issue 4B, 2017

Weksi Budiaji. 2013.Skala Pengukuran dan Jumlah Respon Skala Likert. Jurnal Ilmu

Pertanian dan Perikanan ISSN 2302-6308. Vol 2 No 2, hal 127– 133.

Widya K. Sarunan. 2015. Pengaruh Modernisasi Sistem Administrasi Perpajakan Terhadap

Kepatuhan Wajib Pajak Orang Pribadi dan Wajib Pajak Badan Pada Kantor Pelayanan

Pajak Pratama Manado. Jurnal EMBA, vol 3 no 4 Desember 2015, hal 518-526.

Wirya, I Nyoman Sentanu & Ketut Budiartha. 2019. Effect of Taxation Modernization on Tax

Compliance. Internasional Research Journal of Management, IT & Social Sciences

ISSN : 2395- 7492.vol. 6 No. 4, hal 207-213

Wiyoso Hadi. 2017. Membangun Patriotisme Pajak.

https://www.pajak.go.id/id/artikel/membangun- patriotisme-pajak. Diakses pada 7

Agustus 2019.

Yenni Mangoting & Arja. 2013. Pengarug Postur Motivasi Terhadap Kepatuhan Wajib Pajak

Orang Pribadi. Jurnal Akuntansi dan Keuangan vol 15, no 2, November 2013, 106-116.

Zakky. Pengertian Komunikasi Menurut Para Ahli Secara Umum.

https://www.zonareferensi.com/pengertian- komunikasi/. Diakses pada 4 Agustus

2019.

![Volunteer Income Tax Assistance “VITA” Earned Income Tax ... · Volunteer Income Tax Assistance “VITA” Earned Income Tax Credit “EITC” Revised 1/28/19 [DOCUMENT TITLE]](https://static.fdocuments.net/doc/165x107/5fa5a5c85aa0bb13122ce462/volunteer-income-tax-assistance-aoevitaa-earned-income-tax-volunteer-income.jpg)