THE IMPACT OF FINANCIAL REFORMS ON MONEY DEMAND · PDF filestock market as banks raised their...

82

THE IMPACT OF FINANCIAL REFORMS ON MONEY DEMAND AND ECONOMIC GROWTH IN NIGERIA BY ANUMNU CLARA CHIALUKA PG/MSC/12/61860 AN M.SC PROPOSAL SUBMITTED TO THE DEPARTMENT OF ECONOMICS, FACULTY OF THE SOCIAL SCIENCES, UNIVERSITY OF NIGERIA NSUKKA, ENUGU STATE. SUPERVISOR PROF. (MRS.) S.I. MADUEME NOVEMBER, 2014

Transcript of THE IMPACT OF FINANCIAL REFORMS ON MONEY DEMAND · PDF filestock market as banks raised their...

i

THE IMPACT OF FINANCIAL REFORMS ON MONEY DEMAND AND

ECONOMIC GROWTH IN NIGERIA

BY

ANUMNU CLARA CHIALUKA

PG/MSC/12/61860

AN M.SC PROPOSAL SUBMITTED TO THE DEPARTMENT OF ECONOMICS,

FACULTY OF THE SOCIAL SCIENCES, UNIVERSITY OF NIGERIA NSUKKA, ENUGU

STATE.

SUPERVISOR PROF. (MRS.) S.I. MADUEME

NOVEMBER, 2014

i

TITLE PAGE

THE IMPACT OF FINANCIAL REFORMS ON MONEY DEMAND AND ECONOMIC

GROWTH IN NIGERIA

i

ii

CERTIFICATION

This is to certify that Anumnu Clara Chialuka, an M.Sc student of the University of Nigeria, Nsukka

with registration number PG/MSC/12/61860 has successfully completed the research required for the

Award of Master of Science degree in Economics, University of Nigeria Nsukka, Enugu State.

PROF. (MRS) S.I. MADUEME PROF. C. C. AGU

Supervisor Head of Department

iii

APPROVAL PAGE

This research work titled: ―The Impact of Financial Reforms on Money Demand and Economic

Growth in Nigeria‖ has followed due process and has been approved to have met the minimum

requirements for the award of the Master of Science Degree in the Department of Economics,

University of Nigeria, Nsukka.

PROF. (MRS) S.I. MADUEME PROF. C. C. AGU

Supervisor Head of Department

PROF. I. A. MADU

Dean, Faculty of Social sciences External Examiner

iv

DEDICATION

This research work is dedicated to Almighty God my creator who is the fount of all wisdom and

knowledge

v

ACKNOWLEDGMENTS

I must in the first instance express my endless and sincere gratitude and thanks to God Almighty for

giving me strength, will, power and wisdom during the process of conducting this research work, may

His name alone be praised forever, Amen.

A well deserved appreciation goes to my project supervisor Prof. S.I. Madueme whose kindness,

attention and co-operation during the research are immeasurable.

My profound gratitude goes to my brother Justin for his encouragement and the challenges he gave

me acted as propelling force towards the rounding up of this work. Also to friends who in one way or

the order contributed to the success of this work.

Lastly but very important my love to my family for their great support, financially and morally.

I thank you all and pray for God‘s continued guidance and protection.

vi

Table of Content Title Page ............................................................................................................. Error! Bookmark not defined.

Certification Page ................................................................................................ Error! Bookmark not defined.

Approval Page...................................................................................................... Error! Bookmark not defined.

Dedication ............................................................................................................ Error! Bookmark not defined.

Acknowledgement ............................................................................................... Error! Bookmark not defined.

Table of Content .................................................................................................................................................. vi

CHAPTER ONE ................................................................................................................................................... 1

INTRODUCTION ................................................................................................................................................ 1

1.1 Background of the Study ................................................................................................................................ 1

1.2 Statement of Problems .................................................................................................................................... 4

1.3 Research Questions ......................................................................................................................................... 6

1.4 Objectives of the Study ................................................................................................................................... 6

1.5 Research Hypotheses ...................................................................................................................................... 6

1.6 Scope of the Study ....................................................................................................................................... 6

1.7 Significance of the Study ................................................................................................................................ 7

LITERATURE REVIEW ..................................................................................................................................... 8

2.1 Conceptual Framework ................................................................................................................................... 8

2.2 Theoretical Literature ................................................................................................................................... 10

2.2.1Theory on Financial Reforms ................................................................................................................. 10

2.2.2 Theory on Money Demand .................................................................................................................... 12

2.2.2.1 Keynesian Liquidity Preference Theory ............................................................................................. 12

2.2.3 Post-Keynes Theory ............................................................................................................................... 14

2.2.4 Classical Theories .................................................................................................................................. 14

2.3 Empirical Literature on Financial Reforms and Demand for Money ........................................................... 17

2.3.1Review of Foreign Studies ...................................................................................................................... 17

2.3.2 Review of Domestic Studies .................................................................................................................. 21

2.4 Limitations of Previous Studies .................................................................................................................... 27

CHAPTER THREE ........................................................................................................................................ 31

RESEARCH METHODOLOGY ....................................................................................................................... 31

3.1 Theoretical Framework ................................................................................................................................. 31

3.2 Model Specification ...................................................................................................................................... 32

3.2.1 Financial reform and Money Demand ................................................................................................ 32

vii

3.2.2Financial Reform and Economic Growth ............................................................................................... 34

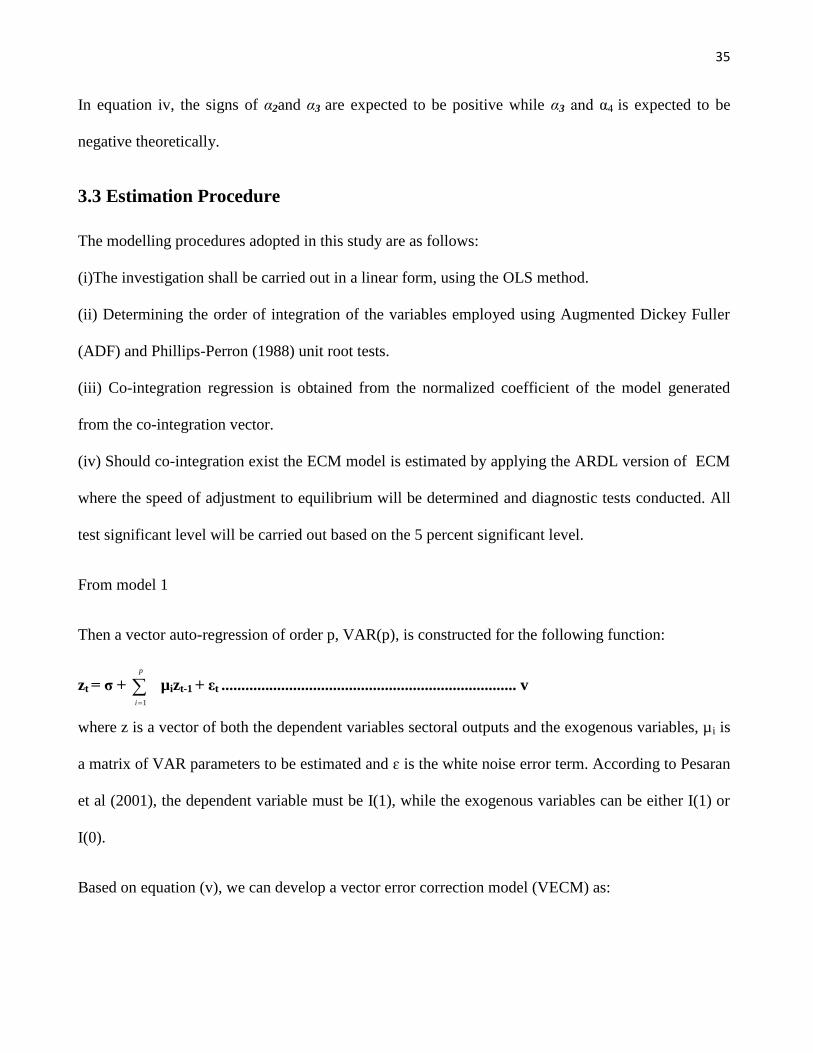

3.3 Estimation Procedure .................................................................................................................................... 35

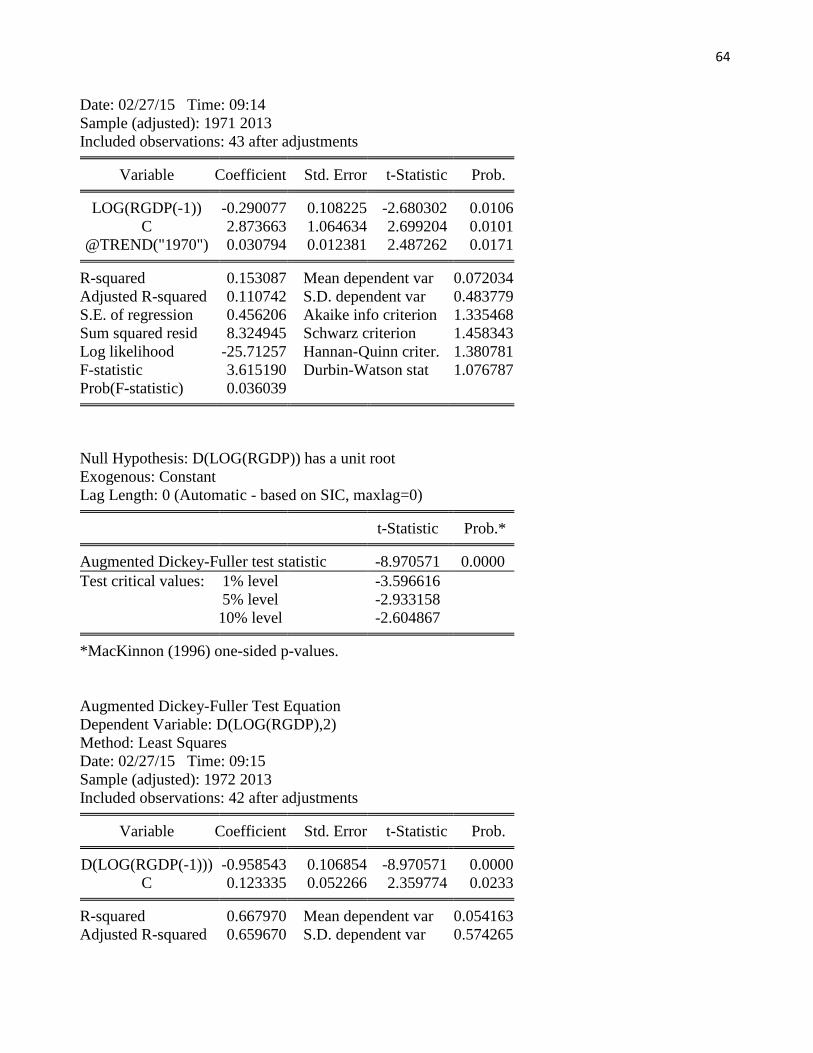

3.3.1 Unit Root Test ............................................................................................................................................ 37

3.4 Justification of the Model ............................................................................................................................. 38

3.5 Preliminary tests on variables of the study ................................................................................................... 38

3.5.1 Testing for normality ............................................................................................................................. 39

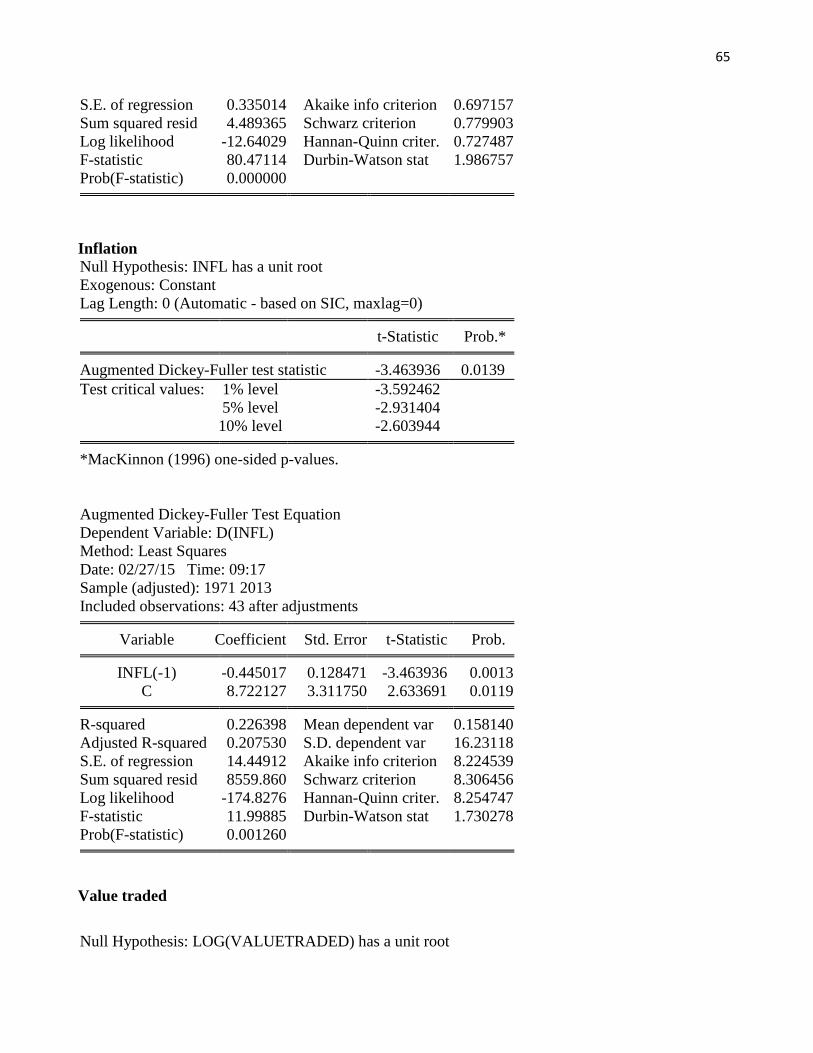

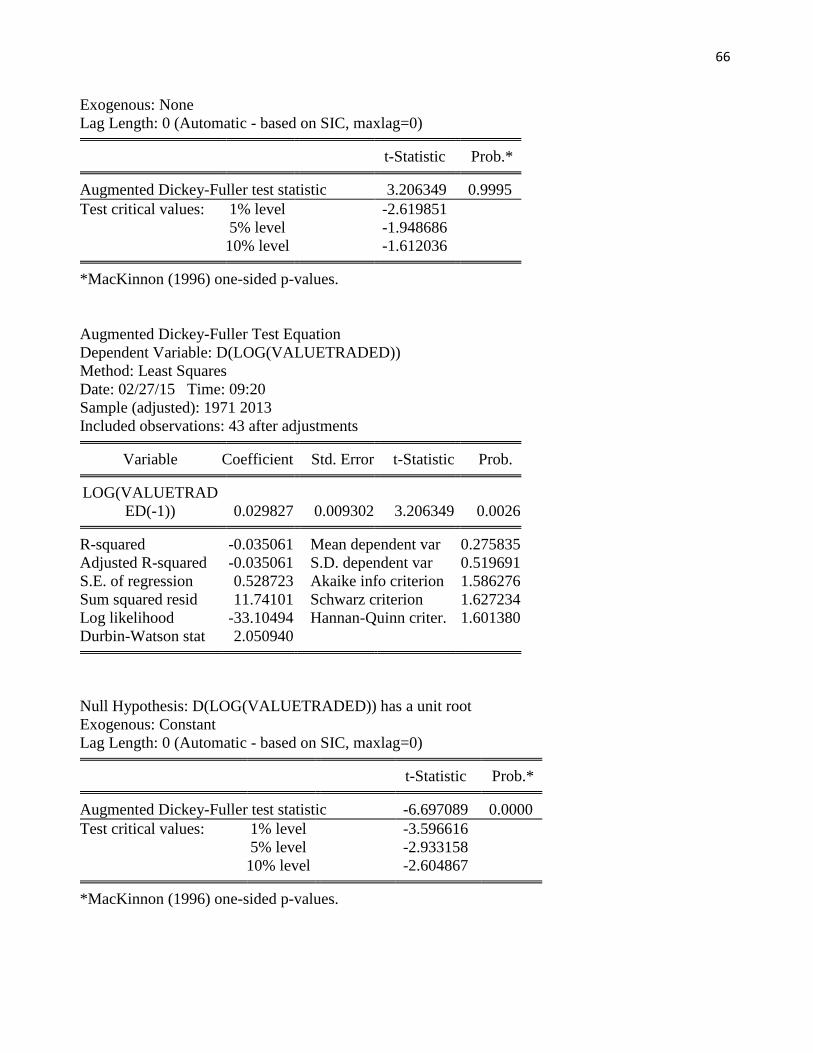

3.5.2 Testing for stationarity ........................................................................................................................... 39

3.5.3 Testing for serial correlation. ................................................................................................................. 40

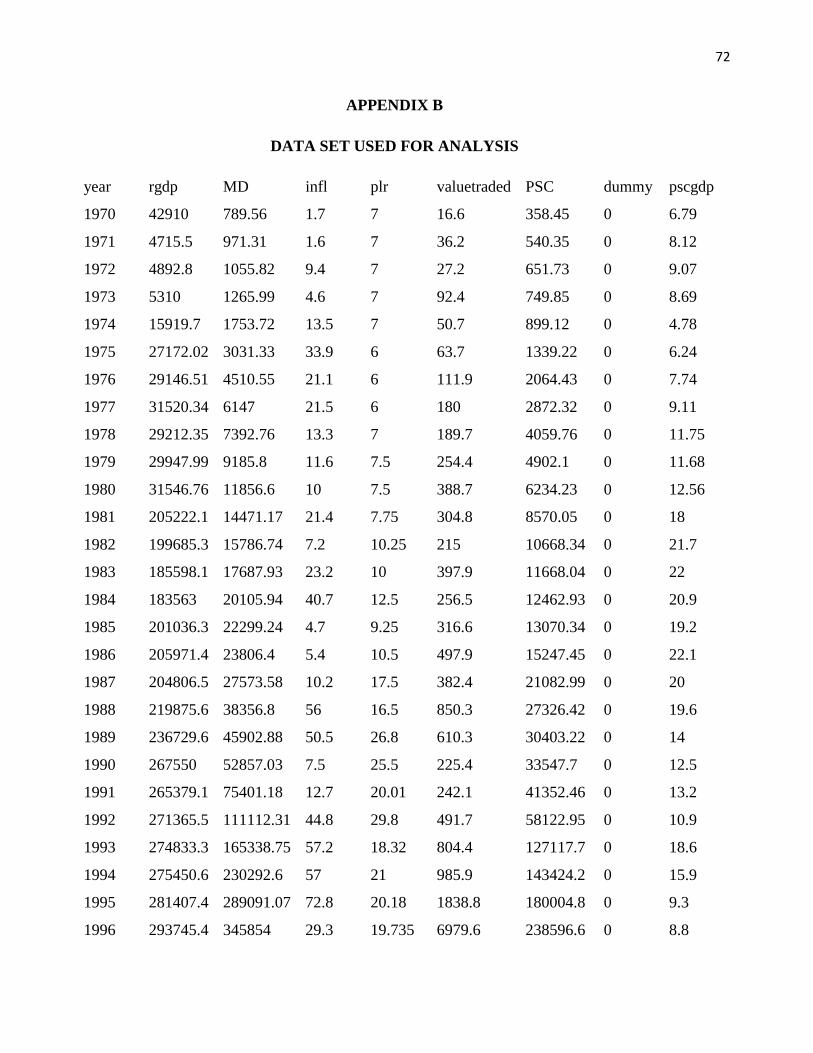

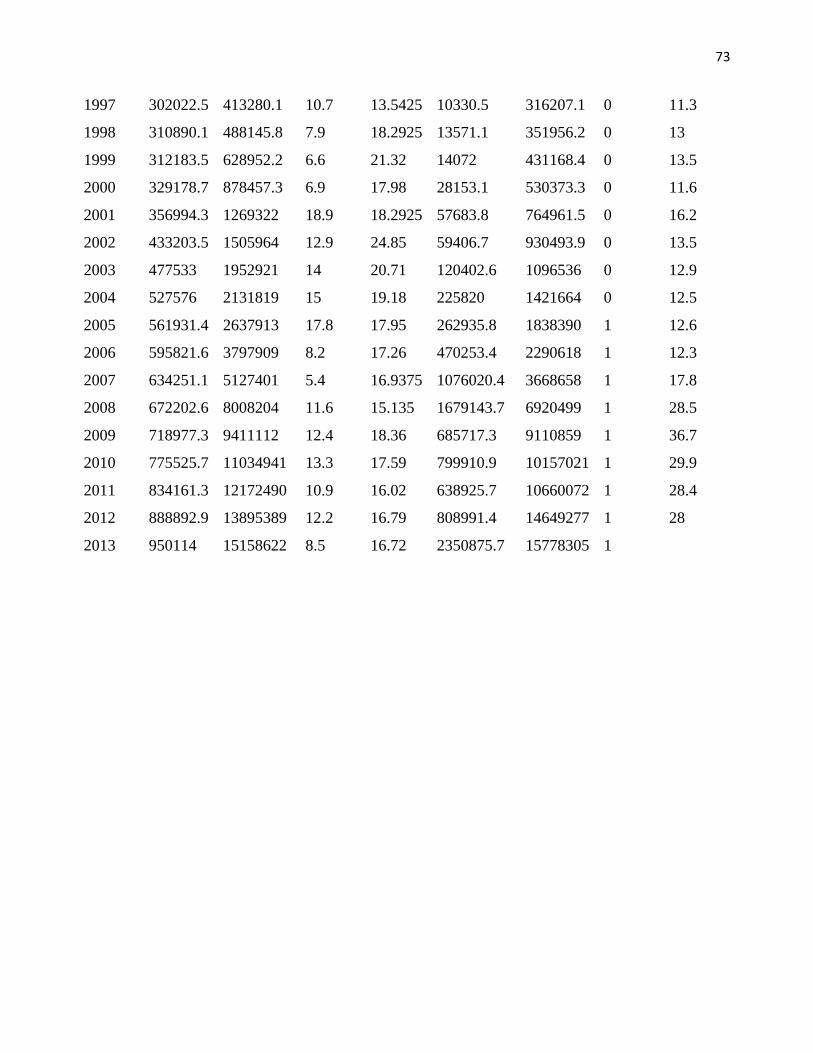

3.6 Data and Sources .......................................................................................................................................... 41

3.7 Econometric Software ................................................................................................................................... 41

4.1 Introduction ......................................................................................................................................... 42

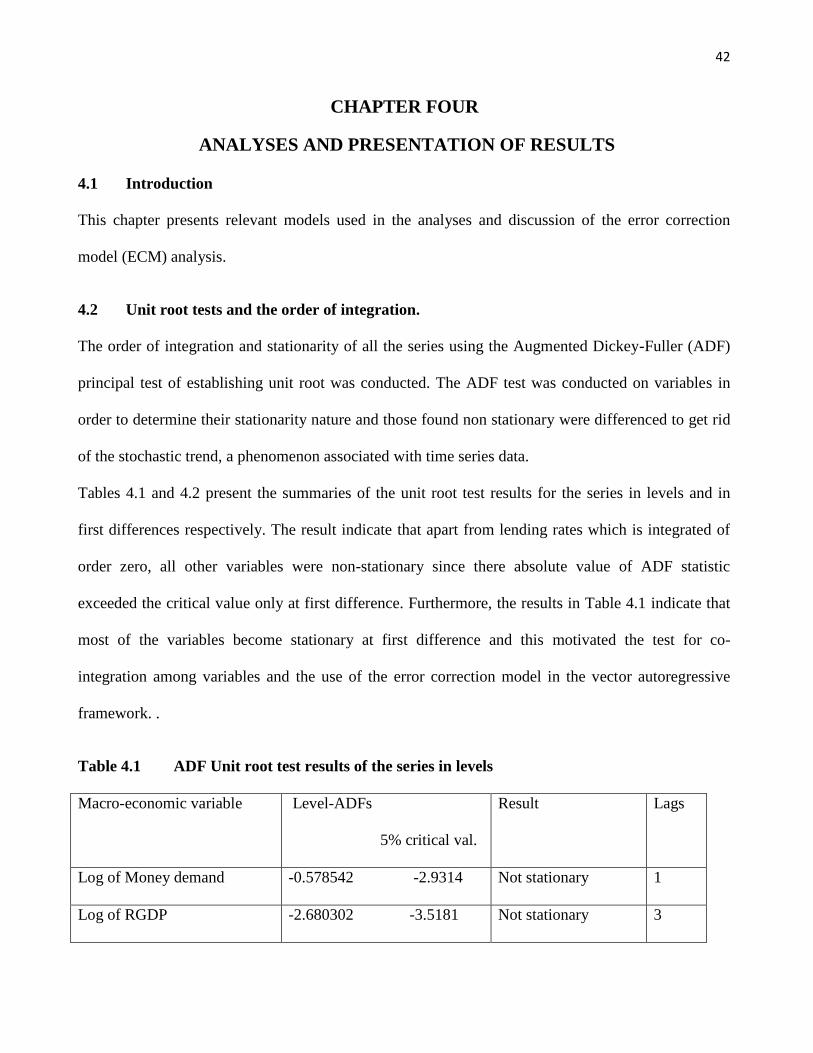

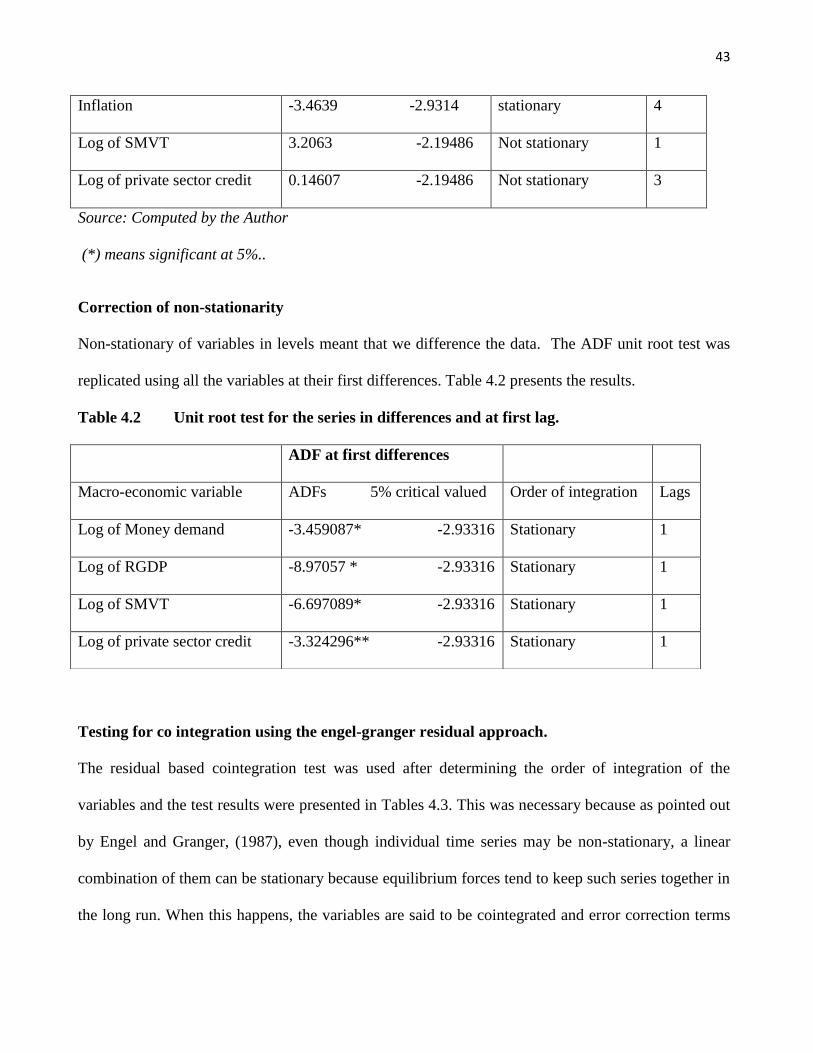

4.2 Unit root tests and the order of integration. .................................................................................... 42

4.3 Correction of non-stationarity ........................................................................................................ 43

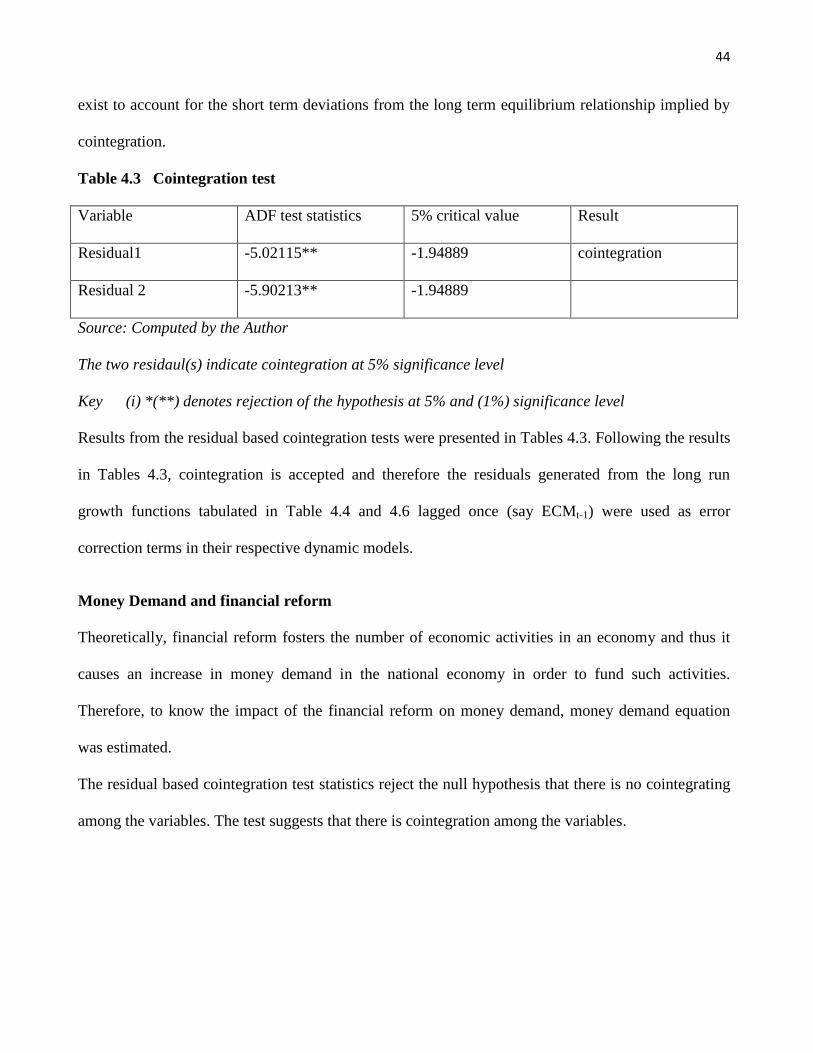

4.4 Testing for co integration using the engel-granger residual approach. ......................................... 43

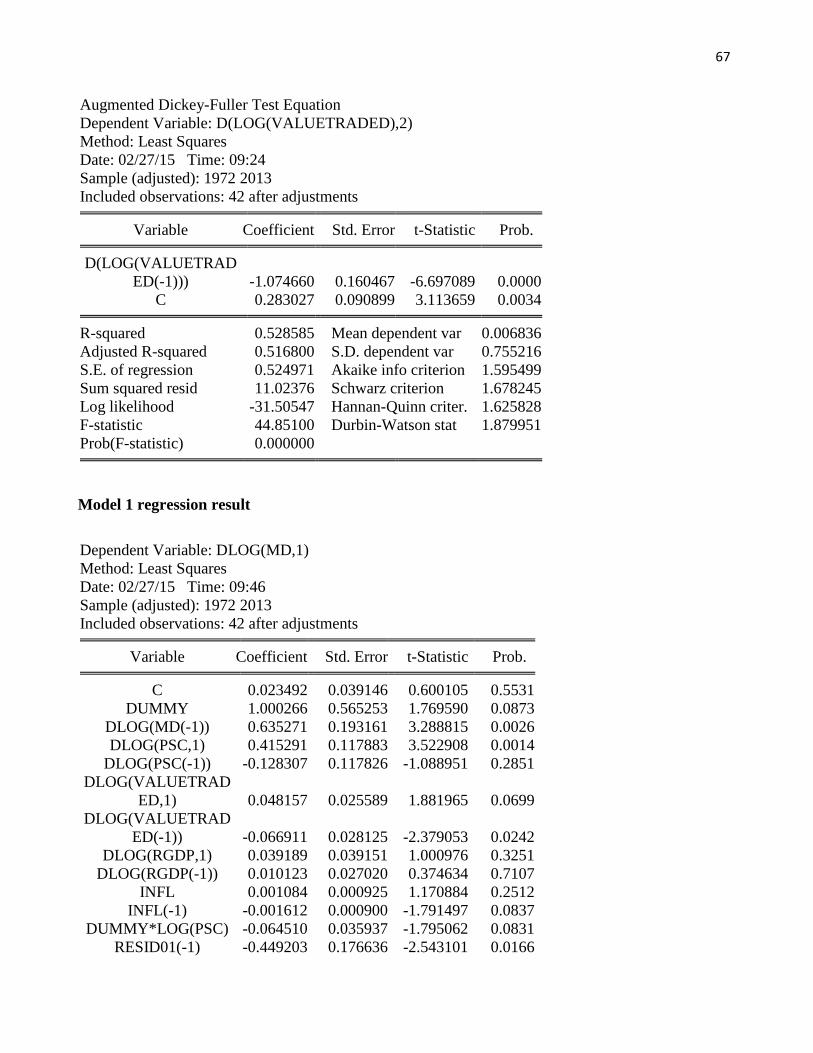

4.5 Money Demand and financial reform ........................................................................................... 44

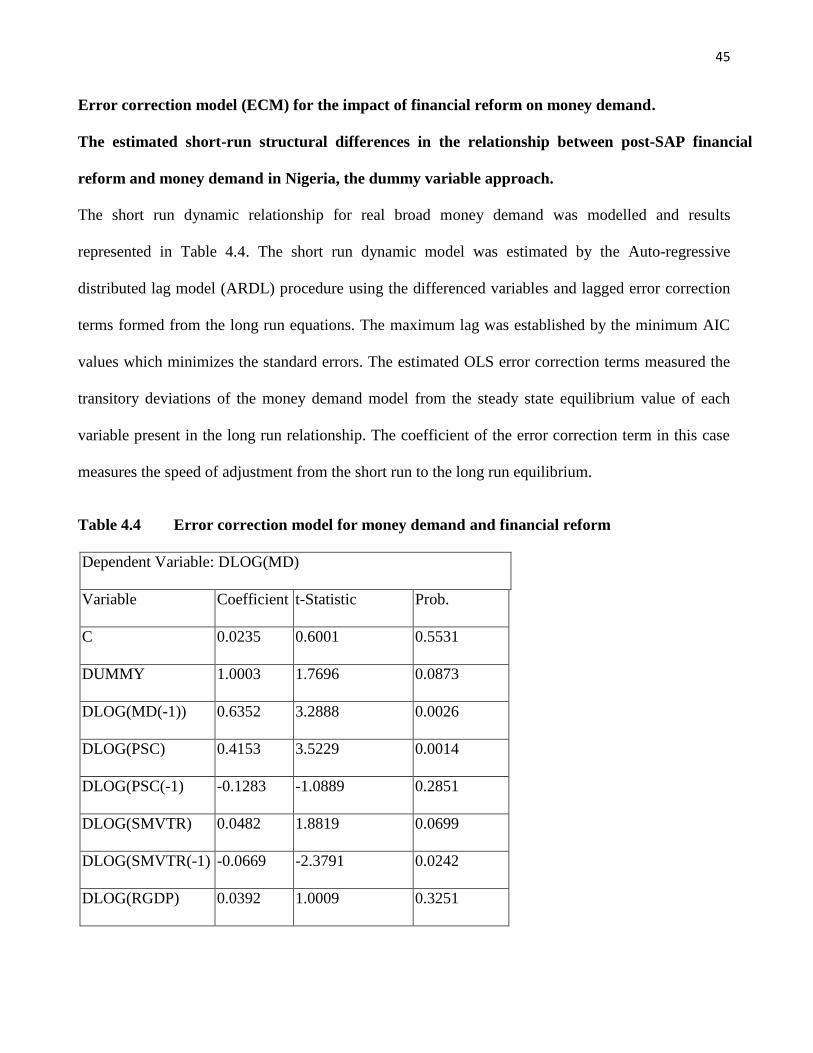

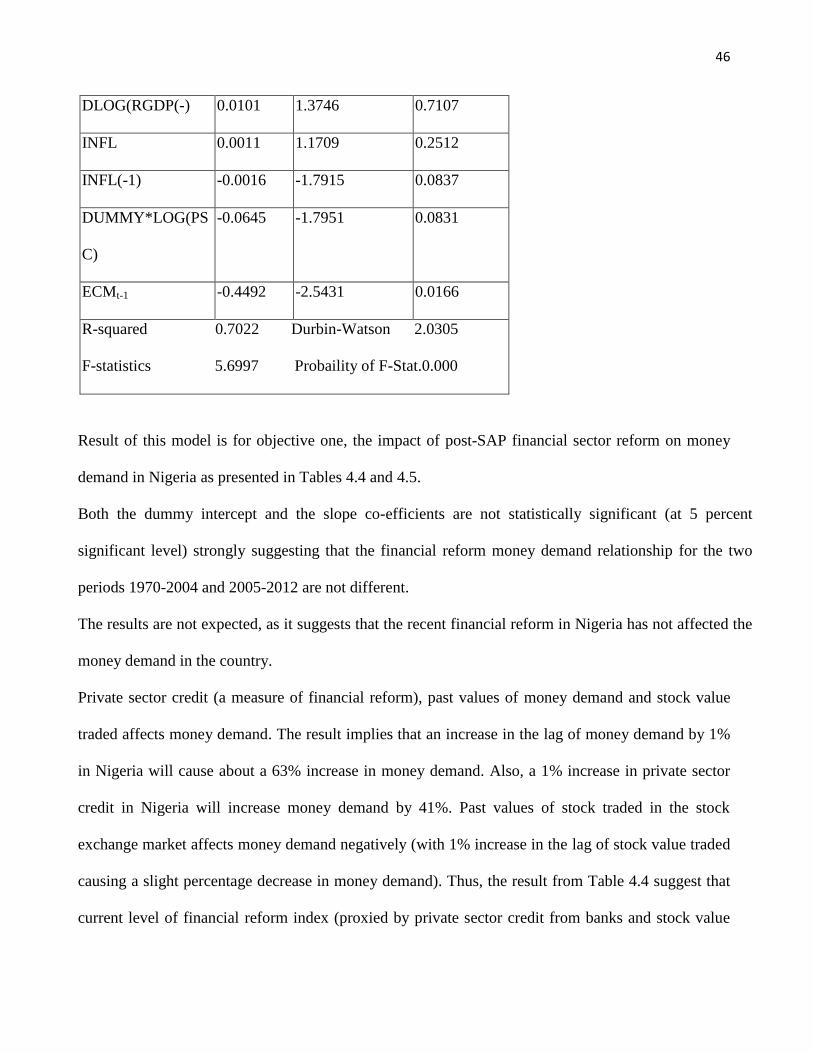

4.6 Error correction model (ECM) for the impact of financial reform on money demand. ............... 45

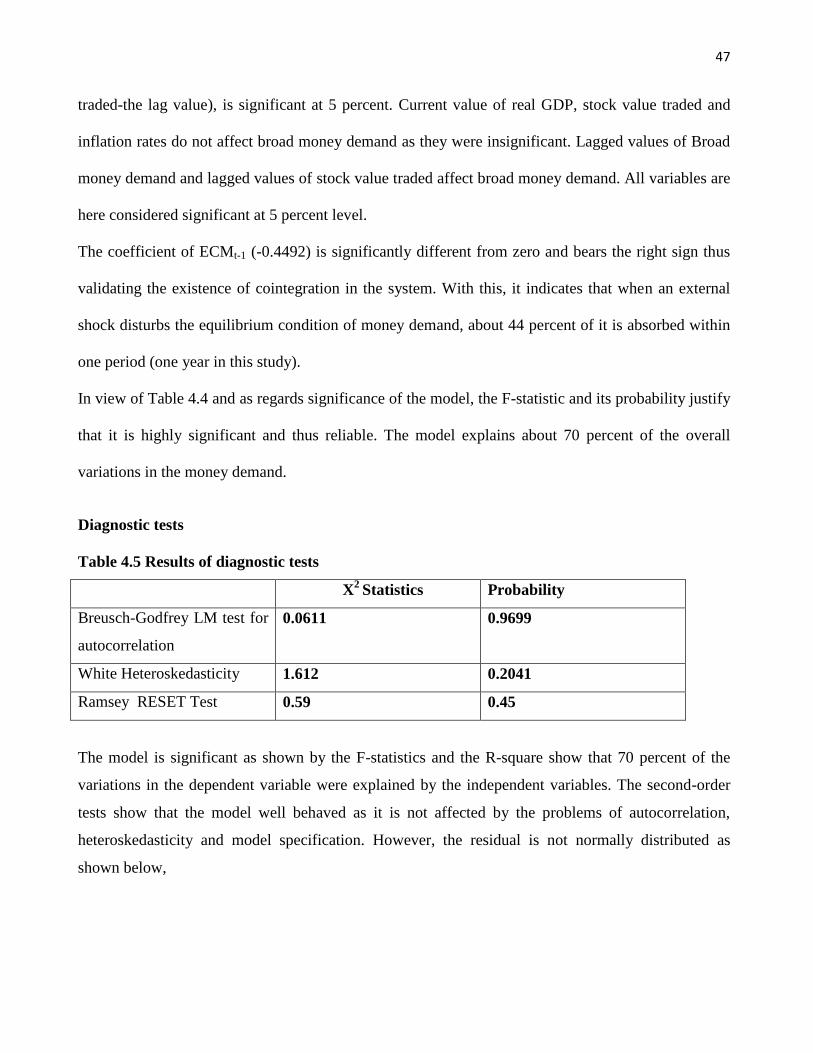

4.7 Diagnostic tests ............................................................................................................................ 47

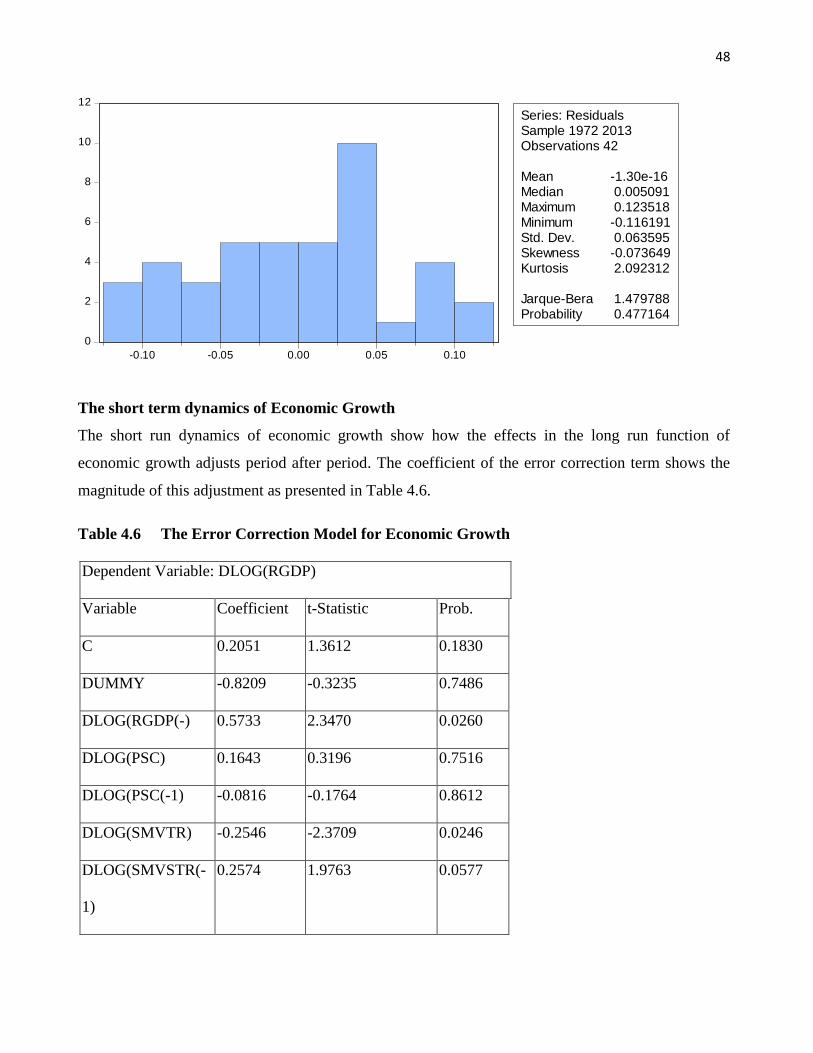

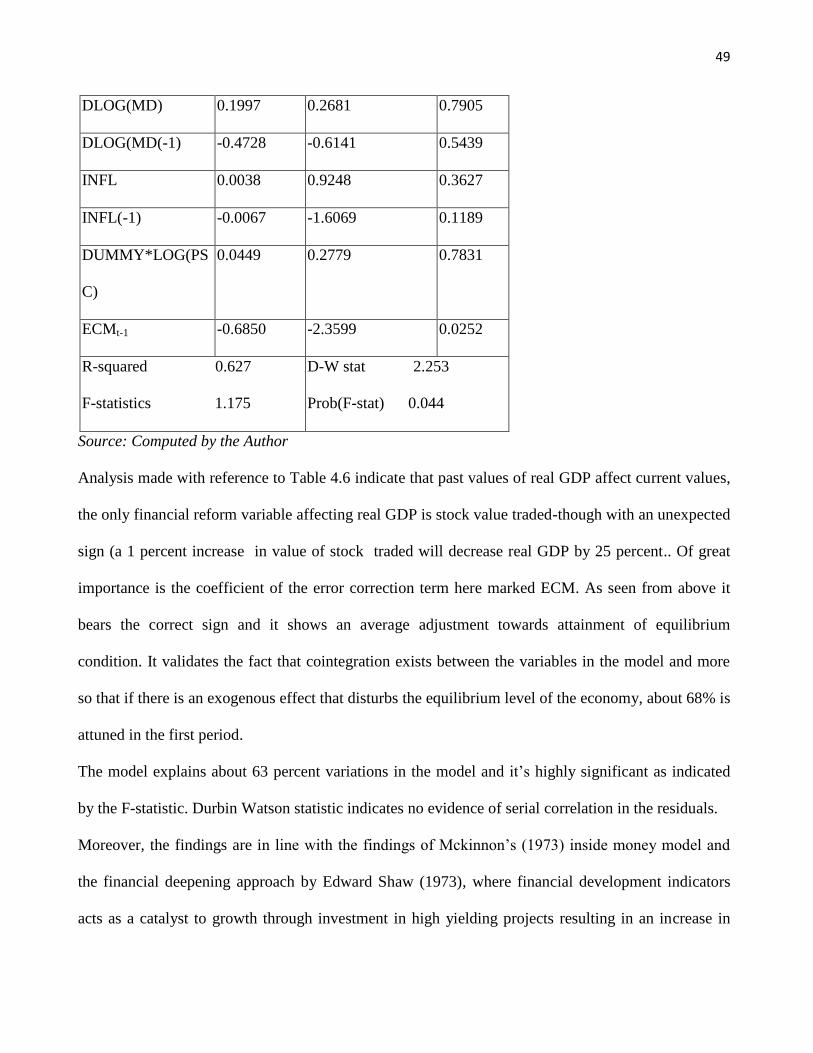

4.8 The short term dynamics of economic growth ................................................................................. 48

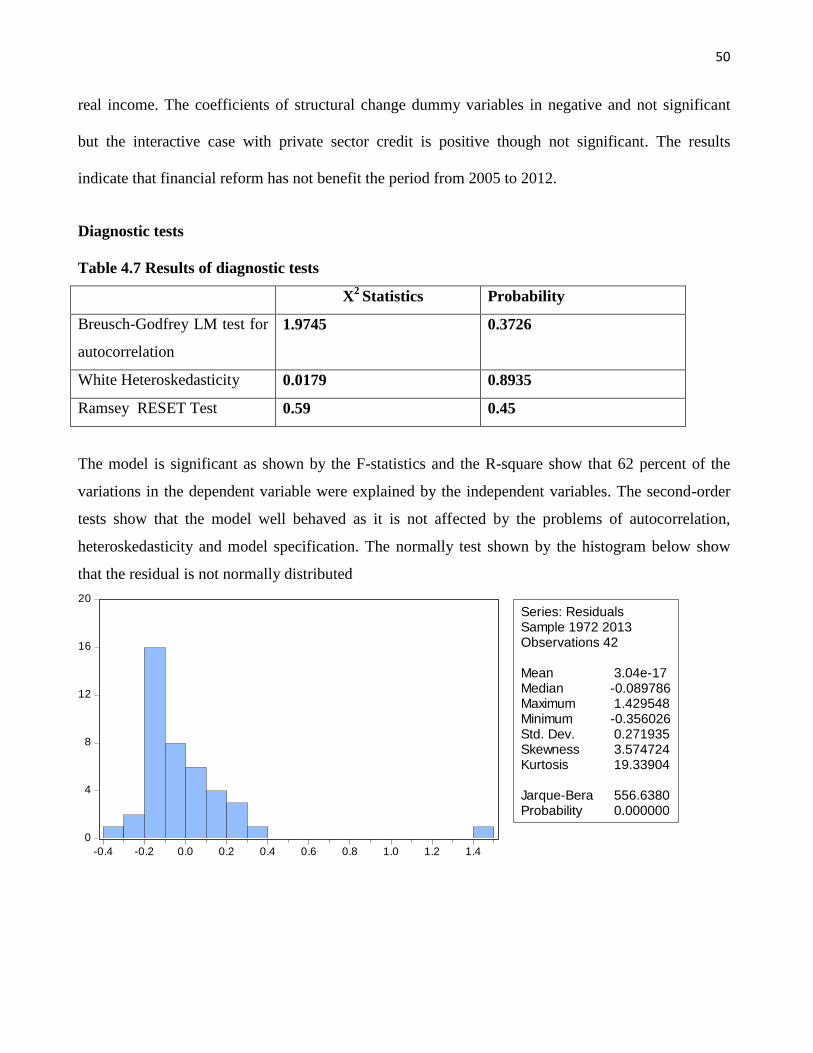

4.9 Diagnostic tests ............................................................................................................................. 50

CHAPTER FIVE ................................................................................................................................................ 51

SUMMARY OF THE FINDINGS, CONCLUSIONS AND RECOMENDATIONS ........................................ 51

5.1 Summary of the findings ......................................................................................................................... 51

5.2 Recommendations ................................................................................................................................... 51

5.3 Conclusions ................................................................................................................................................... 53

5.4 Areas for further study ............................................................................................................................ 55

REFERENCES ................................................................................................................................................... 56

APPENDICES…………………………………………………………………………………..……………..62

viii

ABSTRACT

The study investigated the impact of financial sector reform on money demand and the rate of economic growth in Nigeria. The residual based autoregressive distributed lag-error correction model (ARDL-ECM) was used to analyse the study with a time series data sourced from the central bank of Nigeria statistical bulletins and World Bank Development Indicators records covering a period of 1970-2013. A dummy variable was created to represent the financial reform periods-especially the recent reform periods that commenced fully in 2005. The result established that money demand and economic growth have responded positively to policies of financial sector reform introduced in Nigeria recently as both the bank reform indicator-private sector credit and stock exchange indicator stock value traded-though with a negative impact. In agreement, the study also investigated the impact of money demand on economic growth via financial development. The results also indicate that financial development has positively affected money demand in Nigeria-when examined from private sector credit from banks and negatively related to economic growth from the stock market side. Thus, from the findings of the study, financial reform was found to have positively impacted on money demand and economic growth.

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

The rising importance of the financial sector in the economic development of countries especially

developing countries, as well as the rapid rate of innovation in the sector has generated growing

research interest in financial policy changes. The Nigerian financial system is one of the largest and

most diversified in Sub-Saharan Africa (Afangideh, 2010). The system became liberalized when the

structural adjustment programme was introduced in 1986. In recent years, the system had undergone

significant changes in terms of the policy environment, number of institutions, ownership structure,

depth and breadth of markets, as well as in the regulatory framework.

The financial reforms which began in 2004 with the consolidation programme were necessitated by

the need to strengthen the banks and financial sector in general. The policy thrust at inception, was to

grow the banks and position them to play pivotal roles in driving development across the sectors of

the economy. As a result, banks were consolidated through mergers and acquisitions, raising the

capital base from N2 billion to a minimum of N25 billion, which reduced the number of banks from

89 to 25 in 2005, and later to 24. However, this led to the expanded use of branches by existing and

new banks. The expansion of branch banking in Nigeria has occurred with the development of new

technologies to deliver financial services, such as Automated Teller Machines (ATMs) and other

stored value cards. These cost effective innovations and products that have become available, have

the purpose of reducing the pressure on over-the-counter services to bank customers.

It is important to note that the recapitalisation and merging of some banks affected dealings in the

stock market as banks raised their required minimum capital through the capital market by issuing

new securities. Beyond the need to recapitalize the banks, the regulatory reforms also focused on the

2

following: risk-focused and rule-based regulatory framework, zero tolerance in regulatory framework

in data/information rendition/reporting and infractions; strict enforcement of corporate governance

principles in banking; expeditious process for rendition of returns by banks and other financial

institutions through Electronic Flight Assistance (e-FASS); as well as the introduction of a flexible

interest rate based framework that made the monetary policy rate the operating target. The new

framework has enabled the banking sector to be proactive in countering inflationary pressures and has

helped to check wide fluctuations in the interbank rates and also engendered orderly development of

the money market segment and payments system reforms, among others. Moreover, in 2010, the

Asset Management Corporation of Nigeria (AMCON) was established following the promulgation of

its enabling Act by the National Assembly. It is a special purpose vehicle aimed at addressing the

problem of non-performing loans in the Nigerian banking industry, among others. And in 2011, the

financial sector introduced a new policy ―Cash less Policy‖ as part of ongoing reforms to address

currency management challenges in Nigeria, as well as enhance the national payments system.

However, one crucial question that needs to be addressed is whether these financial reforms have led

to an improvement in the allocation of resources or not, since proper allocation of resources leads to

high real output. Economic theory tells us that financial reforms foster economic growth; empirical

works so far have not found evidence for the existence of such a link. While some countries have

benefited from tools of financial reforms others have not enjoyed higher economic growth. Some

have even experienced serious crises and recessions in those years, following (Fratzscher and

Bussiere, 2004). The impact of financial reforms on macroeconomic performance is very important

for relatively developing countries like Nigeria, empirical evidence from World Bank (2012) and

CBN (2012) reveals that from 1986 to 2012, macroeconomic outcomes in Nigeria such as growth

rate, real interest rate and inflation were among the most affected. The rate of growth in Nigeria was

3

3% in 1986 during financial liberalization but declined to -1% in 1987 and thereafter soared to 10%

in 1988. It further declined to 7% in 1989 and rose again to 8% in 1990. From 1990 to 1994, there

was a continuous decline reaching as low as 1.3% in 1994. There was a little improvement between

1995 and 1996 when the economy grew from 2% to 4%, but it began to decline again from 3% in

1997 to 1% in 1999, the very year Nigeria embraced a new democratic leadership. Owing to some

policy initiatives, the economy improved to 5% in 2000 but declined again to 3% and 2% in 2001 and

2002 respectively. However, when the CBN implemented the recapitalization policy the GDP growth

was short-lived as the economy nosedived again to 5% in 2005 but increased minimally to 6%

between 2006 and 2008.The economy experienced another growth between 2009 and 2010 at 7% and

8% respectively but declined again to 7% in 2011. These fluctuations in growth rates of the economy

have been attributed to many factors ranging from economic mismanagement to erratic financial

policy reversals.

Moreover, the stability of money demand function was at the centre of monetarist claims that

financial reforms should be the backbone of a non-inflationary policy stance (Ighodaro & Ihaza

2008). Starting with Poole (1988) and Lucas (1988), there is a growing consensus that long run

money demand is stable. This view is supported by the findings of a cointegrating relation among real

M1, interest rates and output (Hoffman and Rasche, 1991 and Stock & Watson 1993). Generally, the

stability of the demand for money function has profound implications for the conduct of monetary

policy particularly in this era of economic/financial reforms in Nigeria. Meanwhile, Gbadebo, (2010),

is of the view that the search for a stable demand for money has been a very contentious issue

between the Keynesians and Monetarists of the 1960s and 1970s, as no model on the demand for

money set forth by any of these two schools as well as their contemporaries has withstood the test of

time. He further stated that the instability of the demand for money in the 1970s and in the 1980s has

4

been attributed primarily to changes in the performance of financial markets in the area of new

financial products arising out of financial policy changes.

Meanwhile, the use of monetary policy as a tool for macro-economic stabilization depends largely on

the behaviour of the demand for money or real cash balances in the hands of economic agents. This

brings in the demand for money function which expresses a mathematical relationship between the

quantity of money demanded and its various determinants; interest rate, income, price level, credit

availability, frequency of payments etc. The stability of these relationships is vital in determining the

appropriateness and effectiveness of the tools or instruments of monetary policy. In recent times the

instability of the previously stable demand for money function has thrown up new studies at its

various determinants and several other fronts have been explored by economists and econometricians

alike, (Busari, 2005). One of these fronts is financial policy reforms which has blurred the distinction

between M1 and other assets. Earlier on Miller, (1986) posited that it has blurred the various

definitions of money – M1, M2, M3 etc. In Nigeria, it has begun to hit home with the recent

recapitalization of the banking sector, with the banks now bringing in new financial products that

have combinations of savings features, higher interest earnings, easy withdrawals and transfers, with

increasingly close substitutes for money being introduced by the day, good news for customers but a

hellish nightmare for monetary authorities, (Busari 2005).

1.2 Statement of Problems

Nigerian economy had gone through several financial reforms in the last ten years, including

facilitating the new entry of many domestic banks, N25billion recapitalization of commercial banks,

the gradual deregulation of lending deposit interest rate; facilitating the use of updating payment

technologies like ATM and electronic transfer of deposits. Also included in this reform are, the

5

expansion of a variety of internet banking service like e-banking and mobile banking technology,

enhancement of telecommunication infrastructure, and many others. While these fast financial

developments could promote economic growth, such developments may also hamper the

effectiveness of monetary policy, (Sanya, 2013). For instance, financial development and the

proliferation of these new financial products and deposit substitutes could cause instability in the

underlying money demand relationship with important consequences for the conduct and efficacy of

monetary policy. These developments may have altered the relationship between money, income,

prices and other key economic variables, and may have caused the money demand function to

become structurally unstable (Gbadebo and Okunrinboye, 2009).Kumar et al (2012) has already

submitted that previous reform exercises, especially that of SAP, caused the country a serious

turbulence. They supported their argument with the submission of Anorou (2002) who tested for the

stability of the demand for M2 around the SAP period using quarterly data between 1986 (Q2) and

2000(Q1); the principal result was an unreasonably high estimate of 5.70 for the elasticity of demand.

In addition, Sanya (2013) stated that the recent upgrade the Nigerian financial institutions to global

standards may have implications on the money demand function. Thus, shocks in the global financial

scene and large capital inflows altered the money demand function, making the relationship between

monetary aggregates and output as well as prices less stable as experienced during the last global

financial crisis.

It has also been discovered by researchers (Gurley & Shaw, 1995; Darrat, 2010) that the emergence

of new interest bearing money substitute resulting from financial reforms may unexpectedly increase

the interest rate sensitivity of money holdings. Such elasticity shift in the money demand relations

could weaken the presumed stable relations between monetary aggregates and ultimate policy

objectives of price stability. If this arises, it casts serious doubt on time efficacy of monetary policy.

6

Thus, this study examines the impacts of the changing structure of Nigerian financial system on

money demand and the economic growth performance. More specifically, the study investigates

whether financial markets and stock market development are mutually reinforcing or not in

promoting economic growth and money demand in Nigeria.

1.3 Research Questions

(i) Do post-SAP financial sector reforms have significant effect on money demand in Nigeria?

(ii) Has post-SAP financial sector reforms impacted on the economic growth in Nigeria?

1.4 Objectives of the Study

The broad objective of this study is to examine the effect of financial reform on money demand and

economic growth in Nigeria. The specific objectives of this study include:

(i) To examine the effect of post-SAP financial sector reforms on money demand.

(ii) To investigate the effect of post-SAP financial sector reforms on economic growth.

1.5 Research Hypotheses

H01: Post-SAP financial reform indicators have no effect on money demand in Nigeria.

HA1: Post-SAP financial reform indicators have an effect on money demand in Nigeria.

H02: Post-SAP financial reform indicators have no effect on economic growth in Nigeria.

HA2: Post-SAP financial reform indicators have an effect on economic growth in Nigeria.

1.6 Scope of the Study

The study is a country specific study focusing on the financial sector of the Nigerian economy using

time series data covering the period 1970 to 2013. It has two models with the first model addressing

7

the impact of financial reform indicators on money demand and the second model addressing the

impact of financial reform indicators on GDP. Real GDP, consumer price index (CPI), stock market

value traded, private sector credit (PSC) will be used as proximate variables for performance of the

banking sector and will be expressed in the models as exogenous variables, while the natural log of

broad money demand (represented by M2) will be used as proximate variable to capture money

demand and will be expressed in the models as endogenous variable. FRD which represent financial

sector reform dummy will take the value 0 for period before 2004 and 1 for period after 2004.

1.7 Significance of the Study

It is important to know if money demand function has been unstable as a result of the recent financial

sector reforms. Knowing this is vital in order to establish the relationship between interest rates and

aggregate expenditure as this is important for choosing instruments for conducting monetary policy.

If the demand for money is significantly affected, then the case for conducting macro-economic

stabilization by regulating the growth of the money supply and interest rate changes may be seriously

threatened. Thus, from the findings of this study, knowledge of the extent to which the financial

sector reform policy has impacted on money demand and economic growth in Nigeria will be of great

interest to both the policy makers, monetary authorities and other researchers.

8

CHAPTER TWO

LITERATURE REVIEW

2.1 Conceptual Framework

Financial Reform

Financial sector reform refers to the process to liberalise the financial sector of a country with an aim

to create favourable environment to increase the money demand in the economy. This is assumed to

take place in two ways;

(i) By increasing the financial resources to lead the supply-induced demand for money.

(ii) By creating the enabling environment for investments in the economy.

For Nnanna and Dogo (1998) the concept of financial reform is usually employed to explain a state of an

atomized financial system (i.e.) a financial system which is largely free from financial repression.

According to Fisher (2001), financial reform refers to the greater financial resource mobilization in the

formal financial sector and the ease in liquidity constraints of banks and enlargement of funds available

to finance projects.

There are many different ways in which the financial sector can be said to be reformed. For example;(a)

the efficiency and competitiveness of the sector may improve (b) the range of financial services that are

available may increase (c) the diversity of institutions which operate in the financial sector may increase,

(d) the amount of money that is intermediated through the financial sector may increase,(e) the extent to

which capital is allocated by private sector financial institutions to private sector enterprises responding

to market signals may increase,(f) the regulation and stability of the financial sector may improve and (e)

particularly important from the welfare perspective more of the population may gain access to financial

services, (Department for International Development, 2004).

9

Economic activities in the country can be greatly facilitated by modern banking services. Financial

reform involves the introduction and intensive use of new financial products. In this context, it is

aimed at modernizing the banking system in order to avail modern banking and financial services in

the Nigerian financial market.

Money Demand

In addition, defining the money demand function is a central concern for monetary policy authority

because the combination of money supply and money demand determines interest rates, and therefore

affects the goals of monetary policy. Thus, by definition, demand for money is the quantity of money

people are willing to hold at a given interest rate. In other words, the preference to hold their cash

balances instead of assets. This is referred to as the liquidity preference, (Aiyedogbon, Ibeh,

Ohwofasa, 2013). A stable money demand allows for better prediction of the effects of monetary

policy on interest rates, output, and inflation, and therefore reduces the possibility of an inflation bias

(Cziraky & Gillman, 2006). Stable money demand is a precondition for an effective monetary policy,

especially for countries pursuing a monetary targeting framework. This monetary policy focuses on

the relationship between the rates of interest in an economy, which is the price at which money can be

borrowed and the total supply of money. Monetary policy uses a variety of instruments to control one

or both of these, to influence outcomes like economic growth, inflation, exchange rates with other

currencies and unemployment. Where currency is under a monopoly of issuance, or where there is a

regulated system of issuing currency through banks which are tied to a Central Bank, the monetary

authority has the ability to alter the money supply and thus influence the interest rate to achieve

policy goals.

10

2.2 Theoretical Literature

2.2.1Theory on Financial Reforms

The intellectual framework for financial reforms in developing countries in the 1980s was provided by

the works of Mckinnon (1973) and Shaw (1973). The Mckinnon-Shaw (M-S) paradigm contained two

essential issues; (1) the financial sector is critical for economic growth and (2) extensive government

controls imposed on the financial sector prevents financial deepening and impedes the contribution of the

sector to development. The first issue was not all that new, but only reiterated and re-affirmed ideas

contained in the works of earlier writers such as Gurley and Shaw (1955), Patrick (1966) and Goldsmith

(1969). The second issue was innovative, with the M-S thesis systematically detailing the efficiency and

output costs associated with direct state intervention in the financial system labelled ―financial

repression‖. Goldsmith (1969), McKinnon (1973) and Shaw (1973) present their views by saying that the

poor performance of most developing economies is due to interest rate ceilings, high reserve

requirements, and quantitative restrictions in the credit allocation mechanism caused by financial

repression leading to low savings, credit rationings and low investments. In contrast, some of the works

have either ignored or opposed the financial development, for example; Arestis (2005) evaluated the

Financial Liberalisation in the lights of the relationship between financial development and growth and

clearly mentioned that no convincing empirical evidence was found to support the proposition of the

financial liberalisation hypothesis.

However, the general notion from their debate is that the functions of financial institutions in the savings-

investment process were spelt out as being an effective element for the mobilization and allocation of

capital by equilibrating the supply of loan-able funds with the demand for investment funds and the

transformation and distribution of risks and maturities.

11

Pagano (1993), Jappelli and Pagano (1994) suggest that financial intermediaries can contribute

positively to the growth of the economy only if the economic environment is favourable. King and

Levine (1993) argue that government intervention in the financial system has negative effect on the

equilibrium growth rate.

However, most of the literature on the impact of financial intermediation on economic growth points

to causation running from financial intermediaries. However, Patrick (1966) argues that causation is

bidirectional: financial intermediation is both supply-leading and demand-following, that is the

setting up of financial intermediaries enhances economic growth and it may, itself be enhanced by the

existence of stable economic growth. The ―supply-leading hypothesis‖ postulates a causal

relationship from financial development to economic growth, which means deliberate creation of

financial institutions and markets that increases the supply of financial services and thus leads to real

economic growth. Recent contributors in the new economic growth literature have considered the role

of financial structure and system; this presupposes that the level of money stock drives economic

growth Agu (2008). Numerous theoretical and empirical writings on this subject have shown that

financial development is important and causes economic growth. McKinnon (1973), King and Levine

(1993), all support the supply-leading phenomenon. On the other hand, the ―demand-following

hypothesis‖ postulates a causal relationship from economic growth to financial development. Here,

an increasing demand for financial services might induce an expansion in the financial sector as the

real economy grows (i.e. financial sector responds passively to economic growth), (Gold Smith 1969)

supports this hypothesis as well.

However, the arguments in favour of incorporating a role for financial innovation or technological

change in the demand for money has long been considered in the money demand literature (Arrau, De

Gregorio, Reinhart and Wickham 1995). The demand for money is considered a function of the

12

prevailing institutional and technological framework and thus sensitive to changes in these underlying

forces. The quantity of money demanded in any economy and indeed, the set of assets that have

monetary status is dependent upon the prevailing institutions, regulations, and technology,

(McCallum and Goodfriend, 1987).

2.2.2 Theory on Money Demand

The theoretical underpinnings of the demand for money have been well established in the economic

literature with widespread agreement that the demand for money is primarily determined by real cash

balances.

2.2.2.1 Keynesian Liquidity Preference Theory

Keynes (1936) built upon the Cambridge approach to provide a more rigorous analysis of money

demand, focusing on the motives of holding money. Keynes postulated three motives for holding

money: transactions, precautionary and speculative purposes. He also formally introduced the interest

rate as another explanatory variable in influencing the demand for real balances. The main

proposition of the Keynesian analysis is that when interest rates are low, economic agents will expect

a future increase in interest rates; thus, preferring to hold whatever amount of money is supplied.

Therefore, the aggregate demand for money becomes perfectly elastic with respect to the interest rate

(liquidity trap).

However, following the emergence of liquidity preference theory, several authors have questioned

Keynes‘s rationale for a speculative demand for money and have contributed to the theoretical

literature by distinguishing broadly between the transactions demand.

13

Laidler (1977) points out that Keynes did not regard the demand for money arising from the

transactions and precautionary motives as technically fixed in their relationships with the level of

income and therefore emphasizes that the most important innovation in Keynes‘ analysis is his

speculative demand for money. The primary result of the Keynesian speculative theory is that there is

a negative relationship between money demand and the rate of interest. That is, in a period of high

interest rate, people hold less cash and probably make more savings.

Friedman (1959) opposes the Keynesian view that money does not matter and presented the quantity

theory as a theory of money demand. He modelled money as an abstract purchasing power (meaning

that people hold it with the intention of using it for upcoming purchases of goods and services)

integrated in an asset and transactions theory of money demand set within the context of neoclassical

consumer and producer behaviour microeconomic theory. Friedman argued that the velocity of

money is highly predictable and that the demand for money function is highly stable and insensitive

to interest rates. This implies that the quantity of money demanded can be predicted accurately by the

money demand function.

Chuku (2009) argues that the economic environment that guided monetary policy before 1986 was

characterized by the dominance of the oil sector, the expanding role of the public sector in the

economy and over-dependence on the external sector. In order to maintain price stability and a

healthy balance of payments position, monetary management depended on the use of direct monetary

instruments such as credit ceilings, selective credit controls, administered interest and exchange rates,

as well as the prescription of cash reserve requirements and special deposits.

Al-Samara (2011) opines that the analysis of money demand function is regarded as a key factor in

conducting reliable strategy of monetary policy and selecting the suitable nominal anchor that

monetary policy makers use to tie down the price level. The marvellous strides in monetary analysis

14

showed why a nominal anchor, such as the inflation rate, an exchange rate, or the money supply, is

such a crucial element in achieving the price stability. Continuing further, Al-Samara (2011)

emphasizes that the choice of the intermediate target in the monetary policy strategy is one of the

principal purposes of the Central Banks.

2.2.3 Post-Keynes Theory

Following Keynes, a number of models were developed to confirm the relationship between the

demand for real money, income and interest rates. These models can be classified into three separate

frameworks, namely transactions, assets and consumer demand theories of money.

Under the transactions theory of money demand framework, the inventory-theoretic approach by

(Baumol 1952) and (Tobin 1956) and the precautionary demand for money of (Cuthbertson and

Barlow, 1991) models were introduced. These models were derived from the medium-of-exchange

function of money.

The asset function of money led to the asset or portfolio approach where major emphasis is placed on

risk and expected returns of assets (Tobin, 1956).

Alternatively, the consumer demand theory approach (Friedman, 1959 and Barnett, 1980) considers

the demand for money as a direct extension of the traditional theory of demand for any durable

goods.

2.2.4 Classical Theories

According to classical economists, money acts as a numéraire. In other words, it is a commodity

whose unit is used in order to express prices and values, but whose own value remains unaffected by

this role (Sriram, 1999). However, money is deemed neutral with no real economic consequences

since its role as a store of value, is limited under the classical assumption of perfect information and

15

negligible transaction costs (Sriram, 1999). The concept of money demand took formal shape through

the quantity theory developed in the classical equilibrium framework by two different but equivalent

expressions.

Fisher (1911) provided the famous equation of exchange (MsVt =PtT), where Ms is quantity of

money, Vt is the transactions velocity of circulation, Pt is prices and T the volume of transactions)

where money is held simply to facilitate transactions and has no intrinsic value.

However, the alternative paradigm, the Cambridge approach, was primarily associated with the neo-

classical economists. This approach stressed the demand for money as public demand for money

holdings, especially the demand for real balances, which was an important factor in determining the

equilibrium price level consistent with a given quantity of money (Sriram, 1999).

Growth Theories

The Harrod Domar Model

In theory, the Harrod-Domar model is a cross between the classical and the Keynesian theories of

growth. Harrod-Domar opined that economic growth is achieved when more investment leads to

more growth. The model creates demand but it also creates capacity (Baldwin 1972). Whereas the

Keynesians concentrated only upon the former, the classicists emphasized the latter. The variables

chosen by Harrod and Domar are the broad aggregates, e.g. investment, capital and output. The model

is an early attempt to show that growth is directly related to savings and indirectly related to the

capital/output ratio (Odularu, 2008). The theory is based on linear production function with output

given by capital stock ( ) times a constant. Investment according to the theory generates income and

also augments the productive capacity of the economy by increasing the capital stock. In as much as

there is net investment, real income and output continue to expand. And, for full employment

16

equilibrium level of income and output to be maintained, both real income and output should expand

at the same rate with the productive capacity of the capital stock (Atoyebi, Akinde, Adekunjo and

Femi, 2012)

The theory maintained that for the economy to achieve a full employment, in the long run, net

investment must increase continuously as well as growth in the real income at a rate sufficient enough

to maintain full capacity use of a growing stock of capital. This implies that a net addition to the

capital stock in the form of new investment will go a long way to increase the flow of national

income. From the theory, the national savings ratio is assumed to be a fixed proportions of national

output and that total investment is determined by the level of total savings (i.e ) which must

be equal to net investment I.

Solow's Neo-classical Theory

Following the seminal contributions of Solow (1956, 1957) and Swan (1956), the neoclassical model

became the dominant approach to the analysis of growth, at least within academia. Between 1956 and

1970 economists refined ‗old growth theory‘, better known as the Solow neoclassical model of

economic growth (Solow, 2000, 2002). Building on a neoclassical production function framework,

the Solow model highlights the impact on growth of saving, population growth and technological

progress in a closed economy setting without a government sector. Despite recent developments in

endogenous growth theory, the Solow model remains the essential starting point to any discussion of

economic growth. As Mankiw (1995, 2003) notes, whenever practical macroeconomists have to

answer questions about long-run growth they usually begin with a simple neoclassical growth model

(Abel and Bernanke, 2001); (Jones, 2001a); (Barro and Sala-i-Martin, 2003).

17

The Solow theory believes that a sustained increase in capital investment increases the growth rate

only temporarily: because the ratio of capital to labour goes up (i.e. there is more capital available for

each worker to use). However, the marginal product of additional units of capital is assumed to

decline and thus an economy eventually moves back to a long-term growth path, with real GDP

growing at the same rate as the growth of the workforce plus a factor to reflect improving

productivity. The Solow Growth Model is the most famous neoclassical growth model and it is the

most common starting point for any analysis of growth in a country. It treats technological growth as

well as the rate of savings in a country as exogenous (i.e., determined outside the system). It features

both labour and capital as the factors of production, and assumes constant returns to scale (CRS) in

both factors. This is an important assumption; it means that if capital and labour are doubled as

inputs, output will also double. The Solow model is a dynamic model that predicts convergence in the

long run to a steady state rate of growth for a country (Huggett, 2013).

2.3 Empirical Literature on Financial Reforms and Demand for Money

2.3.1Review of Foreign Studies

Bhatia and Khatkhate (1975) examined the relationship between economic growth and financial

intermediation for eleven African countries using correlation graphs. They measured financial

intermediation by taking the ratio of currency, demand deposits, and time and savings deposits to

GDP. The authors found no definite relationship between growth and financial intermediation for the

countries either individually, or for the whole group. Splitting the financial intermediation measure

into two—the ratio of money to GDP and the ratio of quasi-money to GDP, this still did not reveal

any definite relationship between growth and financial intermediation.

18

Ogun (1986) used cross-country analysis to estimate the correlation between financial deepening and

economic growth by using data for 20 countries in Africa from 1969 to 1983. The degree of financial

intermediation was measured using the ratios of monetary liabilities (M1, M2, and M3) to GDP. For

the full sample, all the monetary liabilities were negative and only the ratio of M3 to GDP was found

to be statistically significant. When the countries were split into high and low income countries, some

of the coefficients of the monetary liabilities are positive while some were negative. However, they

were all insignificant and offered no support to the growth enhancing capabilities of financial

intermediation.

Also, Oshikoya (1992) used time series econometrics to see how interest rate liberalization had

affected economic growth in Kenya using data from 1970 to 1989. The results showed a negative and

insignificant coefficient for the real interest rate. The sample was then split into two sub-periods:

1970–79 and 1980–89. The real interest rate had a negative and significant coefficient for the 1970–

79 period, but was positive and significant for the 1980–89 period; thus offering no robust result of

the effect of interest rate liberalization on growth. These results however were likely to have suffered

from eliminated variables bias as interest rate is not the only component of component financial

sector liberalisation.

Conversely, Arrau, et al, (1995) in a study of ten (10) developing countries argue that the failure to

model financial innovation in money demand functions has tended to yield unstable and miss-

specified functions. The central argument is that financial innovation or technical change, if not

modelled, has specification and stability implications for the money demand functions. They found

that financial innovation (however modelled), in their sample of countries, was quantitatively

important in determining money demand.

19

Alternatively, Sanjay (1998) in an error correction model of money demand in transition economies

finds that money demand function was well behaved. It was found that money demand was

homogenous with respect to price level, was inversely related to expected depreciation rate and was

positively related to interest rate and the level of economic activity. Exchange rate depreciation

passed through into price inflation, but not fully, resulting in a tendency for real exchange rate to

appreciate. The dynamics of the model suggests that adjustment to disturbance was faster in transition

countries than in industrialized countries.

Allen and Ndikumana (2000) used the ratio of Financial Liberalisation liquid liabilities, ratio of

banks‘ private sector credit, ratio of banks‘ total credit, and an index to include all three measures as

proxies for financial intermediation. The authors found that only the ratio of Financial Liberalisation

liquid liabilities is positive and significant, and even this variable was insignificant in the fixed effects

estimation and only when annual data were used. The other financial intermediation variables took on

different signs but were all insignificant.

Behamani-Oskooee and Bary (2000) examined the stability of the M2 money demand function in

Russia. They found evidence of cointegration among the series in the system though M2 money

demand was unstable. While the plot of the Cumulative Sum (CUSUM) provided evidence of

stability, the plot of the Cumulative Sum of Squares (CUSUMSQ) on the other hand revealed that M2

money demand function is not stable. Based on these conflicting results, the authors therefore

concluded that the Russian M2 money demand function is unstable.

Boyd, Levine and Smith (2001), examined five-year average data on bank credit extension to the

private sector, the volume of bank liabilities outstanding, stock market capitalization and trading

volume (all as ratios to GDP), and inflation for a cross-sectional sample over 1960-1995. They found

20

that, at low-to-moderate rates of inflation, increases in the rate of inflation leads to markedly lower

volumes of bank lending to the private sector, lower levels of bank liabilities outstanding, and

significantly reduced levels of stock market capitalization and trading volume. In addition, they also

found that the relationship between inflation and financial development is nonlinear. The adverse

effects of inflation on growth become ―flatter‖ as inflation increases up to a critical level: that is, a

given percentage-point increase in the rate of inflation has a much larger effect on financial

development at low than at high rates of inflation. However, they did not estimate the exact threshold

level. They experimented with critical values ranging from a 7.5 percent to 40 percent inflation rate

and then chose a 15 percent inflation rate as representative.

Wesso (2002) used a single equation error correction model (with fixed and variable coefficients) to

investigate the impact of financial liberalisation on broad money demand in the case of South Africa.

The study, which used quarterly data from 1970 to 1998, found that money demand seems to be

unstable because of the financial liberalisation and technological changes in the long-run.

Neil (2003) also carried out a study on money demand function in South Africa using annual data for

the period 1965 to 1997. His study which used both single and multivariate equation techniques

concluded that, notwithstanding the evidence of the stability of money demand function, M3 provided

little information about future price changes in the economy.

Bwire (2007) studied the impact of financial development on economic growth in Uganda. Using the

ratio of M2 to GDP as a proxy for financial development, the study found that financial development

has a positive impact on real GDP growth. He therefore concluded that the findings follows from the

wide range of financial assets that have been made available to the public through a wide network of

commercial bank branches since the liberalization of the financial sector in 1992.

21

Akhand and Sayera (2007) while investigating the sensitivity of money demand to interest rates also

for South Africa, used data for the period 1997-2006. They generated a standard demand function for

money with real output and a representative interest rate on treasury bills as key determinants.

Empirical results suggested that there existed a well-behaved and stable money demand function and

that the demand for money was sensitive to interest rate, per se on 182-day treasury bills. The long-

run income elasticity of the demand for narrow money was about 1.15 while the corresponding value

for broad money was about 1.7. The long-run interest elasticity of the demand for money was about

(-) 0.2.

Odhiambo (2009) using cointegration and error-correction models, found a strong support for the

positive impact of interest rate reforms on financial development in South Africa. However, contrary

to the results from some previous studies, the study found that financial development, which results

from interest rate reforms, did not Granger cause investment and economic growth. In addition, the

study found a unidirectional causal flow from investment to financial development and prima-facie

causal flow from investment to growth. The study, therefore, concludes that although interest rate

reforms impact positively on financial depth in South Africa, the causal relationship between

financial depth and economic growth tends to take a demand-following path.

2.3.2 Review of Domestic Studies

Teriba (1974) is one of the earliest studies of money demand in Nigeria and probably the foremost to

model demand deposit. Using a double log specification and static Ordinary Least Squares (OLS)

technique with annual data from 1958-1972, the study reported a high significant income-elasticity of

demand deposits in Nigeria while interest rates were not statistically significant.

22

Iyoha (1976) carried out estimation for money demand equation using data from 1950-1965 for

Nigeria. He found evidence in favour of stable demand for money in the Nigeria economy during the

period following World War II. He also found that current (real) income is a better predictor of the

demand for real balance than permanent (real) income in Nigeria. He also confirmed the evidence of

little or no influence of interest rate on money demand in Nigeria.

Nwaobi (2002) examined the stability of money demand function in Nigeria by using data from 1960

through 1995. Adopting the Johansen cointegration framework, the study found that money demand,

real GDP, inflation and interest rate are co integrated in Nigeria. He also found a stable money

demand function for Nigeria in the period under study.

Busari, (2004) examined the Nigerian money demand function by employing annual data for the

period 1970-2002. Using the cointegration and error correction approach, the study observed that

demand for money in Nigeria over this period was stable and that reform measures introduced in the

mid-1980s seems not to have significantly altered the demand function for money in Nigeria.

Adebiyi (2006) examined broad money demand, financial liberalization and currency substitution in

Nigeria using Error Correction Model (ECM). His results showed that long-run demand for real

balances in Nigeria depends upon real income on its own interest rate, interest rates on government

securities, inflation and expected exchange rates. He finally concludes that money demand function in

Nigeria was stable despite the economic reforms and financial crisis.

Akinlo (2006) using an autoregressive distributed lag (ARDL) technique combined with CUSUM and

CUSUMQ tests, examined the cointegrating property and stability of broad money demand(M2) in

Nigeria. The results show M2 to be cointegrated with income, interest rate and exchange rate. The

23

CUSUM test weakly reported a stable money demand for Nigeria. Omotor (2009) also applied the

ARDL technique and equally found a stable money demand for Nigeria.

Ighodaro and Ihaza (2008) examined the stability of broad money demand function in Nigeria using

data for 1970 to 2004. They applied the Johansen Cointegration and error correction approach with

the Cointegration test showing that long run equilibrium relationship exists between broad money

demand and its determinants. While the variance decomposition analysis shows that a high proportion

of broad money and its determinants are explained by their own innovation at the end of ten years, the

impulse response shows that one standard deviation shock on broad money induces more broad

money. Also innovations to income and interest rate induce more broad money demand. Their result

also shows that broad money demand Granger causes inflation rate and not the other way round.

Obamuyi (2009) in anattempt to establish the relationship between interest rates and economic

growth in Nigeria employed annual data from 1970–2006. Using the OLS estimation technique, he

found that real lending rates have significant effect on economic growth. In further analysis of the

results, he also found out that there exists a unique long-run relationship between economic growth

and its determinants, including interest rate. The results imply that the behaviour of interest rate is

important for economic growth in view of the relationships between interest rates and investment and

investment and growth. He concluded that, the formulation and implementation of financial policies

that enhance investment-friendly rate of interest is necessary for promoting economic growth in

Nigeria.

Gbadebo (2010) in his study attempts to analyse whether financial innovations that occurred in

Nigeria after the Structural Adjustment Programme of 1986 has affected the demand for money in

Nigeria using the Engle and Granger Two-Step Co integration technique. Though the study revealed

24

that demand for money conforms to the theory that income is positively related to the demand for

cash balances and interest rate has an inverse relationship with the demand for real cash balances, it

also discovered that the financial innovations introduced into the financial system have not

significantly affected the demand for money in Nigeria.

Yamden (2011) examined the demand for money in Nigeria from 1985 to 2007. The study used

annual time series spanning 26 years on both narrow and broad money, income, interest rate,

exchange rate and the stock market. The study employed the use of multiple regression analysis, the

unit-root test for stationarity and CUSSUM stability test and found out that money demand function

is stable in Nigeria for the sample period and that income is the most significant determinant of the

demand for money. It was also gathered that stock market variables can improve the performance of

money demand function in Nigeria. The study recommended policies aimed at improving stock

market activities and also monetary targeting as a tool for inflation control.

Bassey, Bessong and Effiong (2012) investigated the effect of monetary policy on demand for money

in Nigeria. Three hypotheses were formulated to guide and direct their study. The hypotheses

formulated were meant to evaluate the relationship between interest rate and demand for money,

inflation rate and demand for money and exchange rate and demand for money. Using the Ordinary

Least Square multiple regression statistical technique, their results revealed that there exists an

inverse relationship between interest rate, expected inflation rate, exchange rate and money

demanded, in Nigeria. They therefore recommended that the Nigerian government through the

Central Bank should formulate good money policies that will ensure a stable demand for money

function thereby enhancing economic growth in the country.

Aiyedogbon, et al, (2013) investigated the money demand function in Nigeria from 1986 to 2010.

The empirical analysis of the study involved application of tests for co-integration and vector error

25

correction model. A test of stability was also conducted. The variables of the study are real money

demand function (MD), gross capital formation (GCF), interest rate (INT), inflation rate (INF),

exchange rate (EXR), government expenditure (GEX) and openness of the economy (OPE). From

their findings, it was discovered that in the long run, interest rate, INF and OPE have negative impact

on MD while the impact of GCF, EXR and GEX on the other hand are positive on MD in Nigeria. In

the short run, lag values of MD, GCF, INT and EXR have negative relationship with current MD

while the impact of INF and OPE are positive. The test of stability showed that real money demand

function in Nigeria is stable as neither the CUSUM nor the CUSUMSQ plots cross the 5 percent

critical boundaries. The study therefore recommended that there should be a clear cut distinction

between short run and long run objectives as the monetary authority, for example, can use inflation to

reduce the level of money demand in the long run and increase it in the short run.

Iyoboyi and Pedro‘s (2013) paper was aimed at estimating a narrow money demand function of

Nigeria from 1970 to 2010. The autoregressive distributed lag bounds test approach to cointegration

was utilized for estimation. To determine the characteristics of the time series used in the study,

augmented Dickey–Fuller (ADF) and Philips–Perron (pp) unit root tests were adopted. The empirical

results found cointegration relations among narrow money demand, real income, short term interest

rate (STIR), real expected exchange rate (REER), expected inflation rate (EIR), and foreign real

interest rate (FRIR) in the period under investigation. Their study showed that real income and

interest rate are significant variables explaining the demand for narrow money in Nigeria, although

real income is a more significant factor in both the short and long term. Further evidences showed

that Nigeria was not immune from external shocks originating from capital flight due to changes in

REER and FRIR.

26

In the same vein, Sanya and Awe (2014) examined the impact of financial liberalization on the

stability of Nigerian Money Demand Function from 1970 to 2008. It surveyed a stream of theoretical

and empirical literatures on money demand in both developed and less-developed countries. The

study employed the multivariate co-integration methods by Johansen (1988) and Johansen and

Juselius (1990) to estimate the relationship between M1, M2, Gross Domestic Product, domestic

inflation exchange rate, foreign interest rate, Treasury bill rate and savings deposit rate. From their

findings, the long-run income elasticity is significant and positive while the short-run dynamics of the

demand for money function shows that the speed of adjustment to equilibrium are about 34 percent

for M2 and 56 percent for M1. This indicates that 34 percent and 56 percent of the errors in the short

run are corrected in the long run. Based on the fact that the shift variable that captured the impact of

financial liberalization is negative and significant, they concluded that financial liberalization has not

really altered the stability of Nigerian Money Demand Function and that a monetary aggregate can be

a viable policy for monetary authority in Nigeria.

Onafowora and Owoye (undated) paper uses cointegration vector error correction analysis to test the

stability of the demand for real broad money (M2) in Nigeria over the quarterly period 1986:1 to

2001:4 in order to ascertain whether recent macroeconomic developments such as the implementation

of the structural adjustment programme (SAP) in 1986; the liberalization of the exchange rate,

domestic interest rate, and capital accounts; financial deepening and innovations; changes in

monetary policy regimes; and increased integration of the economy with the rest of the world may

have caused the real broad money demand function to become structurally unstable. Their empirical

results indicate that there exists a long-run relationship between the real broad money aggregate, real

income, inflation rate, domestic interest rate, foreign interest rate, and expected exchange rate.

Furthermore, both their CUSUM and CUSUMSQ tests confirm the stability of the short- and long run

27

parameters of the real money demand function. They therefore recommended that the stability of the

parameters of the money demand equation provides the justification for the monetary authority to

target the broad money supply in its bid to manage inflation and stimulate economic activity in

Nigeria.

2.4 Limitations of Previous Studies

Past empirical literature within and outside Nigeria shows that well-functioning structural changes in

the banks accelerate economic growth; but they have failed to simultaneously examine growth effect

of stock markets innovations (for e.g. see Bwire, 2007; Bhatia and Khatkhate, 1975; Allen and

Ndikumana (2000)). Omitting stock market development makes it difficult to assess whether the

positive relationship between bank development and growth holds when controlling for stock market

development, or banks and stock market each have an independent impact on economic growth. It

also impedes the ability to draw policy conclusions on whether overall financial sector reforms matter

for growth and to identify the separate impact of stock markets and banks on economic success

(Caporale & Gil-Alana, 2005).

While some studies made an effort in these regards, (for e.g. see Gbadebo, 2010; Onaforowa &

Owoye, 2007), they mostly concentrated on analysing its effects by focusing on the SAP era with no

emphasis on the current financial reforms that started in 2005.

Nwaeze et al, (2014) studied the extent to which financial intermediation impacts on the economic

growth of Nigeria between the period of 1992 – 2011. They adopted the ex-post facto research design

using secondary time series data for the twenty years period 1992 – 2011 and the Ordinary Least

Squares (OLS) regression technique to estimate the hypotheses formulated in line with the objectives

28

of the study. They adopted Real Gross Domestic Product, proxy for economic growth as the

dependent variable while the independent variables included total bank deposit and total bank credit.

Their empirical results show that both total bank deposit and total bank credit exert a positive and

significant impact on the economic growth of Nigeria for the period 1992 – 2011. They therefore

recommend amongst others that banks should increase the interest paid to customers on the different

bank accounts they operate to encourage more patronage from them and as well ensure that a major

part of their credit is channelled to the productive sectors of the economy such as agriculture, industry

and power.

Tonye and Adabai (2014) examined the relationship between financial intermediation and economic

growth in Nigeria using data spanning (1988-2013). Their hypotheses were formulated and tested

using vector error correction model and their test for stationarity proves that the variables are

integrated in the order which implies that unit roots do not exist among the variables. They also found

that there is a long-run equilibrium relationship between economic growth and financial

intermediation with their result confirming about 96% short-run adjustment speed from long-run

disequilibrium. From their result, the coefficient of determination indicates that about 89% of the

variations in economic growth are explained by changes in financial intermediation variables in

Nigeria. They therefore recommends that the monetary authorities should properly control and

regulate the activities of the intermediations in order to achieve a sound financial system in the

country, and finally, efforts should be made by monetary authorities to check mate banks from

possessing excess liquidity that would ensure the prevention of inflation in the economy.

Andrew and Osuji (2013) analyzed empirically the trends in financial reform and Output (GDP) in

Nigeria from the banking crises period beginning from 1981 to 2011. They study used the

29

endogenous components of financial intermediation such as Demand Deposits (DD), Time/Savings

deposits (T/Sav) and Credits (Loans and Overdraft) as explanatory variables to predict the outcome of

our dependent variable Output (GDP). Their regression estimation was carried out using IBM SPSS

statistics 20, which their findings suggests that though there exist a positive growth relationship

between financial intermediation and output in Nigeria, there also exist elements of negative short-

run growth relationship, especially for the periods that suffered financial shocks resulting from the

global financial crisis and perhaps, numerous bank failures.

Yakubu and Affoi (2013) analyzed the impact of the recapitalized commercial banks credit on

economic growth in Nigeria from 1992 to 2012. In order to examine the role of commercial bank

credit to the economy, they used commercial bank credit to the private sector of the economy to

estimate its impact on Nigeria‘s economic growth, which is proxy by gross domestic product. Using

the ordinary least square they found that the commercial bank credit has significant effect on the

economic growth in Nigerian.

Adekunle, Salami and Adedipe (2013) examined the impact of financial sector development and

economic growth in Nigeria. Their study seeks to know the impacts of the sector in the Nigerian

economy and whether the sector has been able to achieve its main objective of intermediation as a

result of the inability of the sector to assist the real sector despite the huge profits declared yearly and

also the short term lending of the banks instead of long term investment that can boost the economy.

They used the ordinary least square (OLS) method of the regression analysis; the financial

development was proxied by ratio of liquidity liabilities to GDP (M2/GDP), real interest rate (INTR),

ratio of credit to private sector to GDP (CP/GDP) while the economic growth was measured by the

30

real GDP (RGDP).Their study finds that only the real interest rate is negatively related as all their

explanatory variables were statistically insignificant. Though the overall statistic shows that their

independent variables were able to explain 74 percent variation in the dependent but contrary to a

priori expectation, it is statistically insignificant. They concluded that the link between the financial

sector and real sector still remains weak and could not propel the needed growth towards the vision

202020.

Shittu (2012) examined the impact of financial reform on economic growth in Nigeria. He used time

series data from 1970 to 2010 which he gathered from the CBN publications. For his analysis, he

used the unit root test and cointegration test and the error correction model which he estimated using

the Engle-Granger technique. His study established that financial intermediation has a significant

impact on economic growth in Nigeria.

However, one drawback of most of these studies is that although standard time series techniques were

used, they failed to consider structural changes in the cointegrating equations. Some of the studies

that examined the effect of structural change (focusing on the SAP reforms) used the chow test,

which have been proved to be not too effective in predicting structural breaks. Thus, this study

introduces the dummy variable in the interactive form. The interactive form of the dummy will enable

us to differentiate between the slope coefficients of the two periods. Therefore, given the economic

and political turbulence that occurred in Nigeria recently beginning from 2005, it would be prudent to

allow and explicitly estimate for the presence of structural change that could have influenced the

demand for money relationship.

31

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Theoretical Framework

The conventional formulation of the demand for money typically relates the demand for real money

balances (m = M/P), to the interest rate ―r‖ and some measure of economic activity such as real GNP

(y = Y/P), where M = money holdings, P = the price level and Y = gross national product.

Thus, m = f(r, y).

Several theories have been put forward to explain the equation above. These include the consumer

demand theory by Friedman (1956) and the asset function of money theory by Tobin (1958). Perhaps

the most appropriates are those of the transactions view, in which the demand for money evolves

from a lack of synchronization between receipts and payments and the existence of a transactions cost

in exchanging money for interest- bearing assets (usually taken to be short term). This transaction

view flows from the liquidity preference theory developed by Keynes (1936) which is the theoretical

basis on which the model developed in this present study is built on.

Keynes modelled money demand as the demand for the real quantity of money (real balances) or

M/P. In other words, if prices double, you must hold twice the amount of money to buy the same

amount of basket of goods, but your real balances stay the same. So people chose a certain amount of

real balances based on the interest rate, and income: M/P = f(i, Y).

The resulting inference from their theory is that the demand for money is positively related to income

and inversely related to interest rate.

32

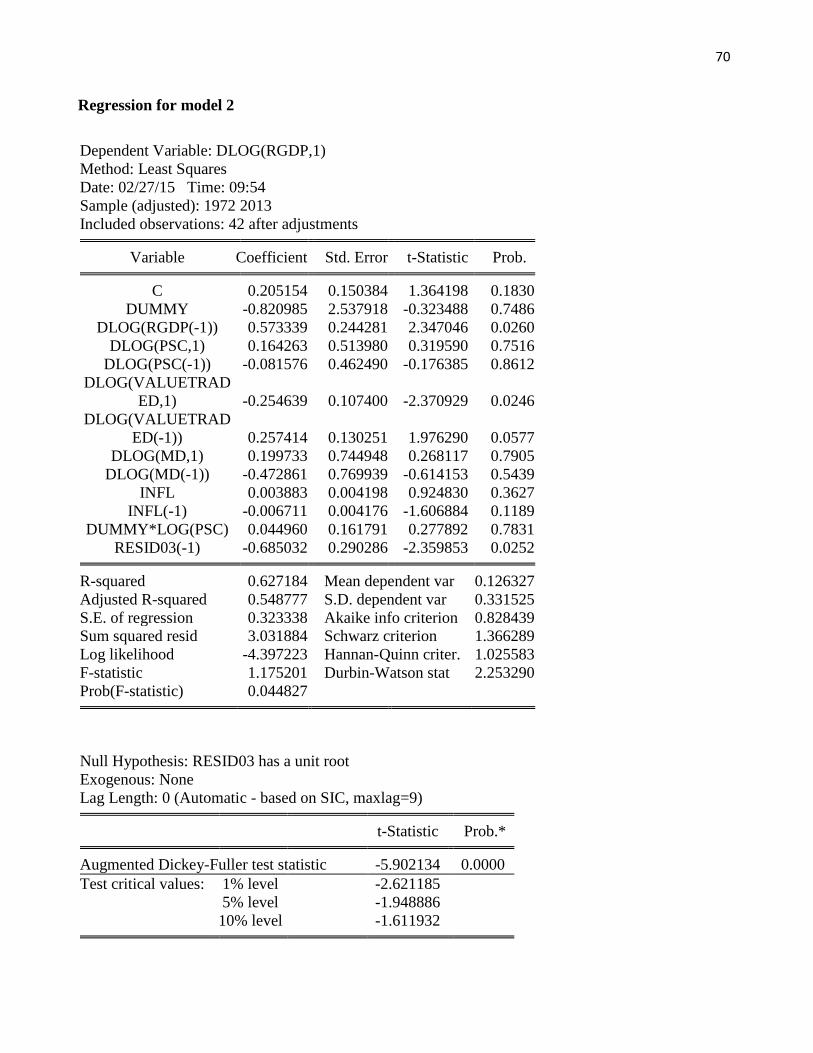

3.2 Model Specification

Model 1

3.2.1 Financial reform and Money Demand

Money demand and supply situation of a country shows the financial strength of an economy.

Increased money supply may induce the demand or increased money demand may induce the money

supply in an economy. The more the monetary expansion is, the more the expansion of the economy.

Therefore, it is assumed that financial reform brings monetary expansion. Financial reform is

supposed to be favourable for the expansion of money demand. Following Gbadebo, (2010) and

Dagher & Kovanen, (2011), studies, this study hereby models the effects of financial sector reforms

for (1970-2004) and for the period (2005-2012) on money demand represented by the equation

below.

Log (MD)t = α0 + α1FRDi + α2LogGDPt + α3LogPSCt+ α4INFt + α5LogSMVTRt + α5 FRD*PSC+

εt.............................................................................................................................................................i

where

LMD= log of broad money demand (represented by M2).

LGDP= Log of income proxy by real gross domestic product.

CPI = consumer price index.

FRD = Financial reform dummy, taking 0 for periods 1970 - 2004 reforms and 1 for periods 2005-

2013.

PSC = Private sector credit.

SMVTR = stock market value traded rate and

εt =error term.

33

0α = the constant or the intercept and 1= the differential intercept 5 = differential slope coefficient

for interactive case between the dummy and PSC-indicating by how much the slope coefficient of the

reform periods differ from the slope coefficient of the base period.

Economic theory predicts that the signs of α2 and α4 are likely to be positive while α3 and α5 are

expected to be negative as the lending rates and inflation affect the money demand negatively.

From the frameworks above, and adopting a linear specification with an assumption of linearity

among the variables given: where all coefficients and variables are as defined earlier, c is a constant

parameter and ɛ is the white noise error term.

The null hypothesis in the above equation is 1 = 0 and 5= 0 indicating that there are no structural

changes between the two periods, that is, the financial reform for the two periods are the same.

Model 2

Theoretical Framework

The theoretical framework to build the model of this study is anchored on Mc-Kinnon-Shaw hypothesis.

From their debate the functions of financial institutions in the intermediation process (through savings