The Handbook of Trading: Strategies for Navigating and ......Delaware Derivative Action 171 Edward...

497

Transcript of The Handbook of Trading: Strategies for Navigating and ......Delaware Derivative Action 171 Edward...

The

HANDBOOKof

TRADING

Other McGraw-Hill Books Edited by Greg N. Gregoriou

The Credit Derivatives Handbook: Global Perspectives, Innovations, and MarketDrivers (2008, with Paul U. Ali)

The Handbook of Credit Portfolio Management (2008, with Christian Hoppe)

The Risk Modeling Evaluation Handbook (2010, with Christian Hoppe andCarsten S. Wehn)

The VaR Implementation Handbook (2009)

The VaR Modeling Handbook: Practical Applications in Alternative Investing,Banking, Insurance, and Portfolio Management (2009)

The

HANDBOOKof

TRADING

New York Chicago San FranciscoLisbon London Madrid Mexico City

Milan New Delhi San Juan SeoulSingapore Sydney Toronto

STRATEGIES FOR NAVIGATING

AND PROFITING FROM CURRENCY,

BOND, AND STOCK MARKETS

Greg N. GregoriouEditor

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Except as permitted under the United States Copyright Act of 1976, no part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of the publisher.

ISBN: 978-0-07-174354-9

MHID: 0-07-174354-5

The material in this eBook also appears in the print version of this title: ISBN: 978-0-07-174353-2, MHID: 0-07-174353-7.

All trademarks are trademarks of their respective owners. Rather than put a trademark symbol after every occurrence of a trademarked name, we use names in an editorial fashion only, and to the benefi t of the trademark owner, with no intention of infringement of the trademark. Where such designations appear in this book, they have been printed with initial caps.

McGraw-Hill eBooks are available at special quantity discounts to use as premiums and sales promotions, or for use in corporate training programs. To contact a representative please e-mail us at [email protected].

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that neither the author nor the publisher is engaged in rendering legal, accounting, futures/securities trading, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought. —From a Declaration of Principles jointly adopted by a Committee of the American Bar Association and a Committee of Publishers

TERMS OF USE

This is a copyrighted work and The McGraw-Hill Companies, Inc. (“McGrawHill”) and its licensors reserve all rights in and to the work. Use of this work is subject to these terms. Except as permitted under the Copyright Act of 1976 and the right to store and retrieve one copy of the work, you may not decompile, disassemble, reverse engineer, reproduce, modify, create derivative works based upon, transmit, distribute, disseminate, sell, publish or sublicense the work or any part of it without McGraw-Hill’s prior consent. You may use the work for your own noncommercial and personal use; any other use of the work is strictly prohibited. Your right to use the work may be terminated if you fail to comply with these terms.

THE WORK IS PROVIDED “AS IS.” McGRAW-HILL AND ITS LICENSORS MAKE NO GUARANTEES OR WARRANTIES AS TO THE ACCURACY, ADEQUACY OR COMPLETE-NESS OF OR RESULTS TO BE OBTAINED FROM USING THE WORK, INCLUDING ANY INFORMATION THAT CAN BE ACCESSED THROUGH THE WORK VIA HYPERLINK OR OTHERWISE, AND EXPRESSLY DISCLAIM ANY WARRANTY, EXPRESS OR IMPLIED, INCLUD-ING BUT NOT LIMITED TO IMPLIED WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE. McGraw-Hill and its licensors do not warrant or guarantee that the functions contained in the work will meet your requirements or that its operation will be uninterrupted or error free. Neither McGraw-Hill nor its licensors shall be liable to you or anyone else for any inaccuracy, error or omission, regardless of cause, in the work or for any damages resulting therefrom. McGraw-Hill has no responsibility for the content of any information accessed through the work. Under no circumstances shall McGraw-Hill and/or its licensors be liable for any indirect, incidental, special, punitive, consequential or similar damages that result from the use of or inability to use the work, even if any of them has been advised of the possibility of such damages. This limitation of liability shall apply to any claim or cause whatsoever whether such claim or cause arises in contract, tort or otherwise.

CONTENTS

EDITOR xvii

CONTRIBUTORS xix

ACKNOWLEDGMENTS xxxiii

PA RT I EXECUTION AND MOMENTUM TR ADING 1

C H A P T E R 1 Performance Leakage and ValueDiscounts on the TorontoStock Exchange 3

Lawrence Kryzanowski and Skander LazrakAbstract 3Introduction 4Sample and Data 5Measures of Performance Leakage and Value Discounts 5Empirical Estimates for the TSX 7Conclusion 18Acknowledgments 18References 19Notes 20

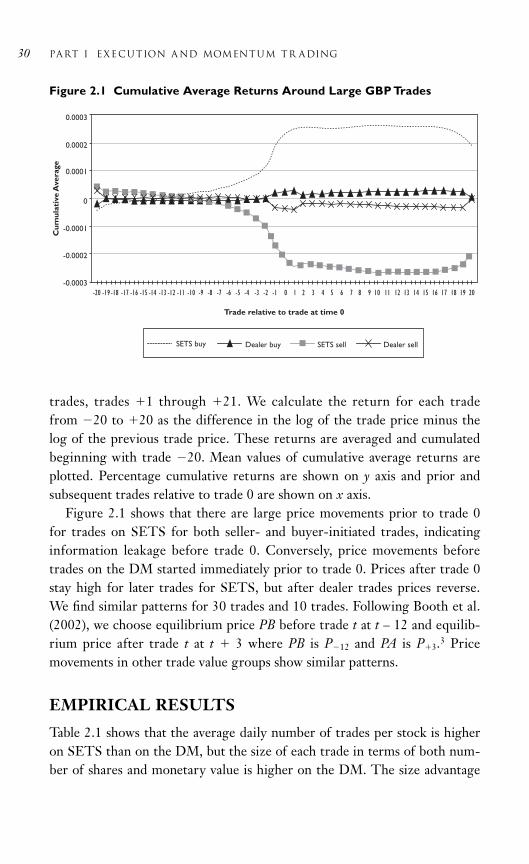

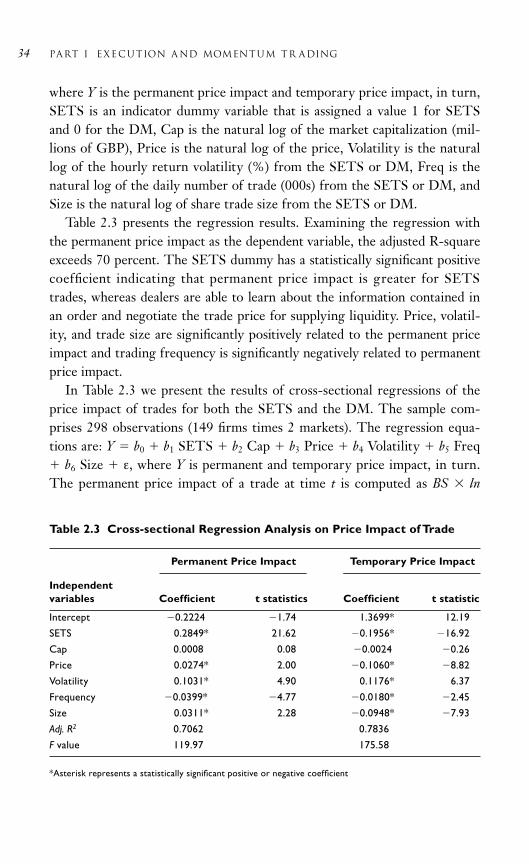

C H A P T E R 2 Informed Trading in ParallelAuction and Dealer Markets: The Case of the London Stock Exchange 23

Pankaj K. Jain, Christine Jiang, Thomas H. McInish, and Nareerat Taechapiroontong

Abstract 23Introduction 23Trading Systems and Venues 24Institutional Background, Data, and Methodology 27

v

Empirical Results 30Conclusion 35Acknowledgments 36References 36Notes 38

C H A P T E R 3 Momentum Trading for thePrivate Investor 39

Alexander Molchanov and Philip A. StorkAbstract 39Introduction 39Data 40Momentum Trading Results 41Robustness Tests 45Trading with a Volume Filter 47Private Investor Trading 49Conclusion 50Acknowledgments 51References 51Notes 52

C H A P T E R 4 Trading in Turbulent Markets: Does Momentum Work? 53

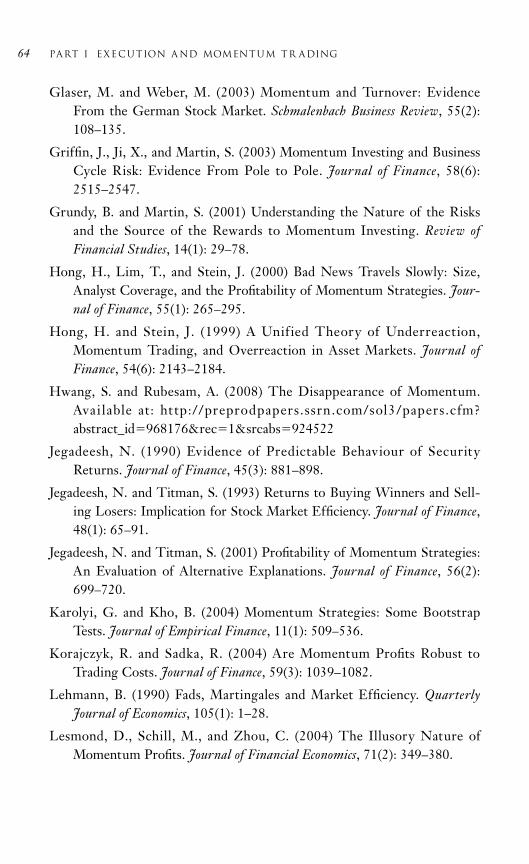

Tim A. Herberger and Daniel M. KohlertAbstract 53Introduction 53Literature Review 54Data and Methodology 55Results 57Conclusion 62References 63Notes 65

C H A P T E R 5 The Financial Futures Momentum 67

Juan Ayora and Hipòlit TorróAbstract 67Introduction 67Literature Review 68

vi contents

Data 69Methodology and Results 69Conclusion 77Acknowledgments 79References 79Notes 80

C H A P T E R 6 Order Placement Strategies inDifferent Market Structures: A Primer 83

Giovanni PetrellaAbstract 83Introduction 83Costs and Benefits of Limit Order Trading 84Trading in a Continuous Order-Driven Market 86Trading in a Call Auction 89Conclusion 91References 92

PA RT II TECHNICAL TR ADING 95

C H A P T E R 7 Profitability of Technical Trading Rules in an EmergingMarket 97

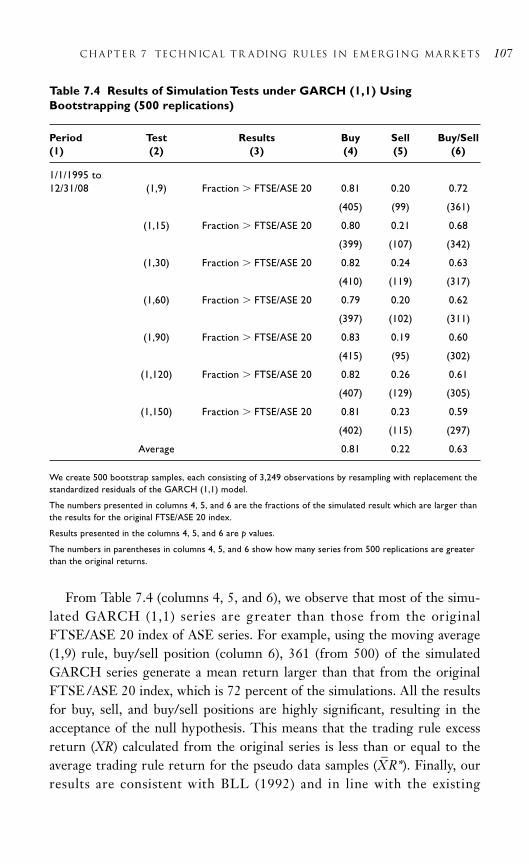

Dimitris Kenourgios and Spyros PapathanasiouAbstract 97Introduction 98Methodology 100Data and Empirical Results 103Conclusion 108References 109Notes 111

C H A P T E R 8 Testing Technical Trading Rules as Portfolio Selection Strategies 113

Vlad Pavlov and Stan HurnIntroduction 113

contents vii

Data 115Portfolio Formation 116Bootstrap Experiment 122Conclusion 124Acknowledgments 126References 126Notes 127

C H A P T E R 9 Do Technical Trading Rules Increase the Probability of Winning? Empirical Evidence from the Foreign Exchange Market 129

Alexandre RepkineAbstract 129Introduction 130Empirical Methodology 131Empirical Results 135Conclusion 139References 140

C H A P T E R 10 Technical Analysis in Turbulent Financial Markets:Does Nonlinearity Assist? 141

Mohamed El Hedi Arouri, Fredj Jawadi, and Duc Khuong NguyenAbstract 141Introduction 142Nonlinear Modeling for Technical Analysis 143Data and Empirical Results 147Conclusion 150References 150Notes 153

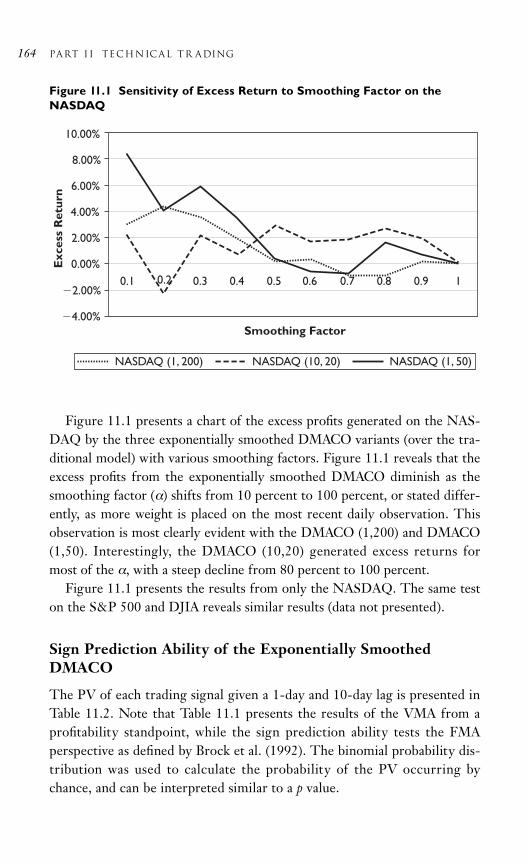

C H A P T E R 11 Profiting from the Dual-MovingAverage Crossover withExponential Smoothing 155

Camillo LentoAbstract 155

viii contents

Introduction 156Background on the Moving Averages 157Methodology 159Data 161Trading with the Exponentially

Smoothed DMACO 162Conclusion 167References 168Notes 170

C H A P T E R 12 Shareholder Demands and theDelaware Derivative Action 171

Edward PekarekAbstract 171Introduction 171Policy Purposes for Derivative Actions 173Demand Requirements 174Standing to Sue Derivatively 178Futility Excuses the Demand Requirement 179Futility, Director Independence, and Business

Judgment 180Conclusion 181Acknowledgments 182References 183

PA RT III EXCHANGE-TR ADED FUND STR ATEGIES 187

C H A P T E R 13 Leveraged Exchange-Traded Funds and Their TradingStrategies 189

Narat CharupatAbstract 189Introduction 189Trading Strategies 190Conclusion 197References 197Notes 197

contents ix

C H A P T E R 14 On the Impact of Exchange-Traded Funds over Noise Trading: Evidence from European Stock Exchanges 199

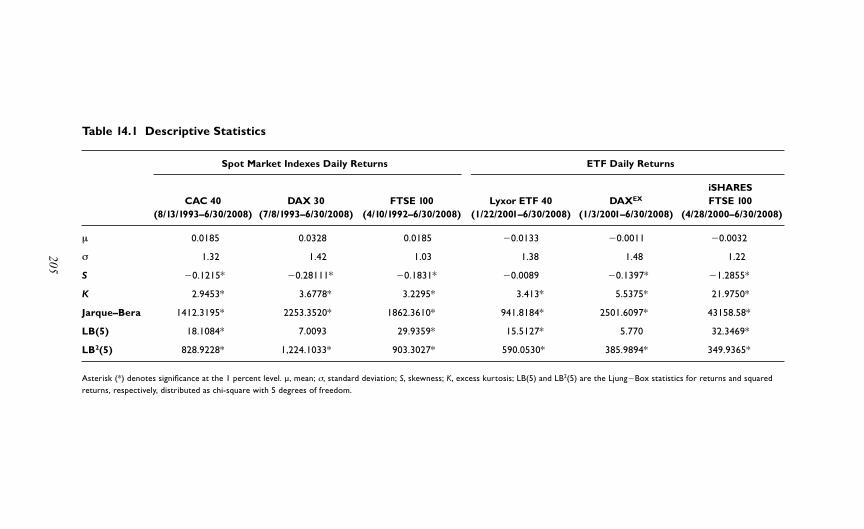

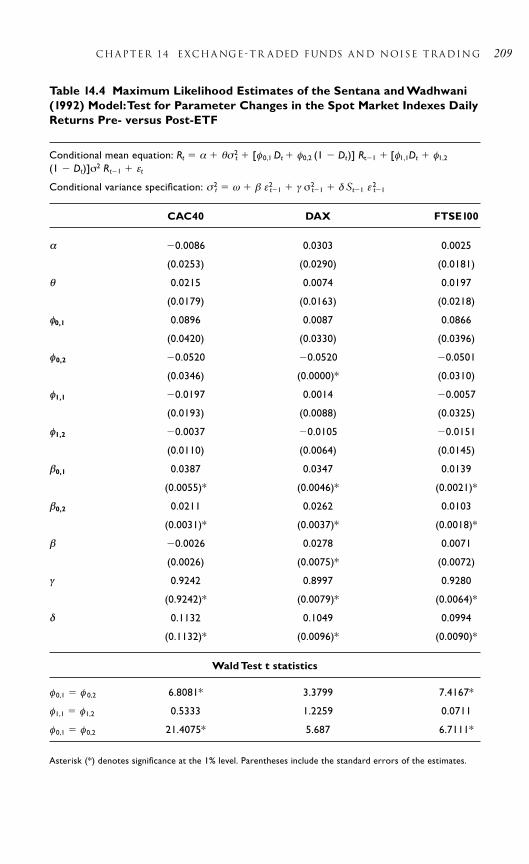

Vasileios Kallinterakis and Sarvinjit KaurAbstract 199Introduction 199Data 201Methodology 201Descriptive Statistics 204Results; Conclusion 204References 211Notes 211

C H A P T E R 15 Penetrating Fixed-IncomeExchange-Traded Funds 213

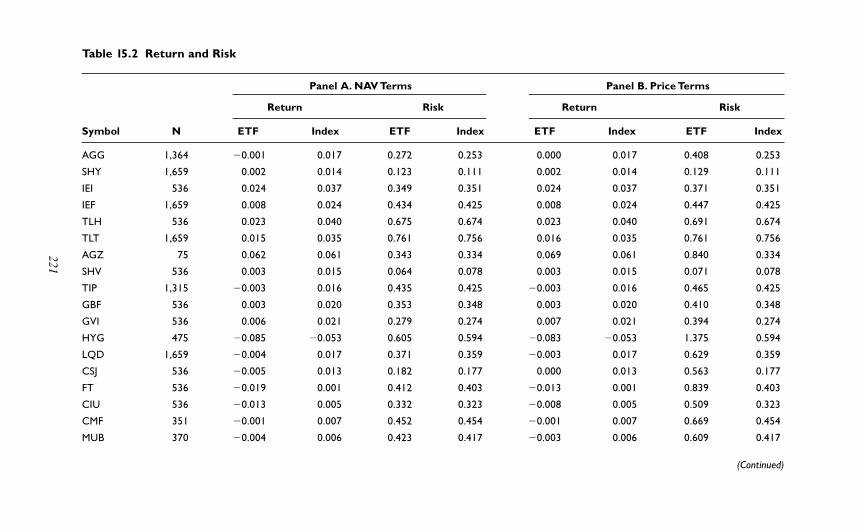

Gerasimos G. RompotisAbstract 213Introduction 213Methodology 215Data and Statistics 217Empirical Results 220Conclusion 229References 231

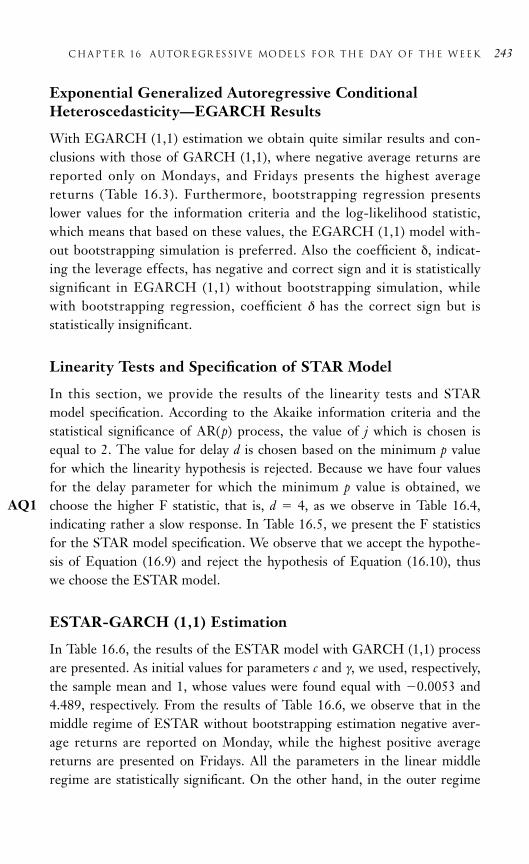

C H A P T E R 16 Smooth Transition AutoregressiveModels for the Day-of-the-WeekEffect: An Application to the S&P 500 Index 233

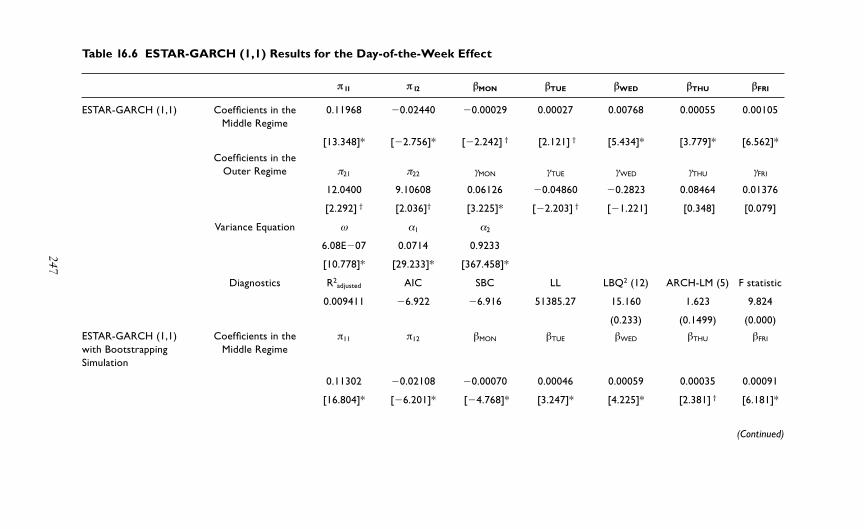

Eleftherios GiovanisAbstract 233Introduction 233Literature Review 234Methodology 235Data 238Empirical Results 239Conclusion 249References 250

x contents

PA RT IV FOREIGN EXCHANGE MARKETS,ALGORITHMIC TR ADING, AND RISK 253

C H A P T E R 17 Disparity of USD Interbank Interest Rates in Hong Kong and Singapore: Is There AnyArbitrage Opportunity? 255

Michael C. S. Wong and Wilson F. ChanAbstract 255Introduction 255HIBOR and SIBOR 256Data And Findings 257Explanations for the HIBOR-SIBOR Disparity 259Conclusion 260References 261

C H A P T E R 18 Forex Trading OpportunitiesThrough Prices Under ClimateChange 263

Jack Penm and R. D. TerrellAbstract 263Introduction 263Methodology 267Data and Empirical Application 271Conclusion 274References 274

C H A P T E R 19 The Impact of Algorithmic Trading Models on the Stock Market 275

Ohannes G. PaskelianAbstract 275Introduction 276The Impact of Algorithmic Trading on the Market 277Algorithmic Strategies 279Algorithmic Trading Advantages 281Algorithmic Trading Beyond Stock Markets 282

contents xi

Conclusion 282References 283

C H A P T E R 20 Trading in Risk Dimensions 287

Lester IngberAbstract 287Introduction 287Data 288Exponential Marginal Distribution Models 288Copula Transformation 289Portfolio Distribution 293Risk Management 294Sampling Multivariate Normal Distribution 295Conclusion 297References 298

C H A P T E R 21 Development of a Risk-Monitoring Tool Dedicated to Commodity Trading 301

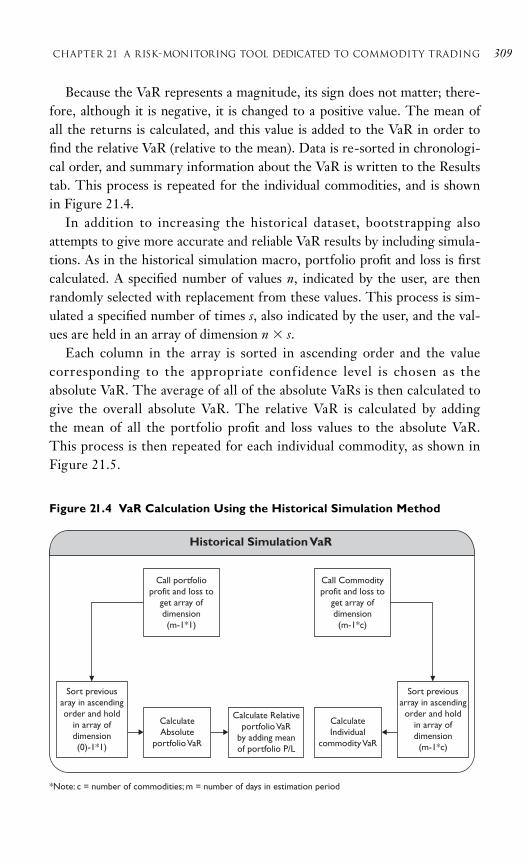

Emmanuel Fragnière, Helen O’Gorman, and Laura WhitneyAbstract 301Introduction 301Literature Review 303Methodology 305Conclusion 313Resources 314

PA RT V TR ADING VOLUME AND BEHAVIOR 317

C H A P T E R 22 Securities Trading, AsymmetricInformation, and MarketTransparency 319

Mark D. Flood, Kees G. Koedijk, Mathijs A. van Dijk, and Irma W. van Leeuwen

Abstract 319Introduction 320

xii contents

Experimental Design and Terminology 323Data 326Results 328Conclusion 337Acknowledgments 338References 339Notes 341

C H A P T E R 23 Arbitrage Risk and the High-Volume Return Premium 343

G. Geoffrey Booth and Umit G. GurunAbstract 343Introduction 343Data and Method 344Tests 346Conclusion 348References 349

C H A P T E R 24 The Impact of Hard versus SoftInformation on Trading Volume:Evidence from ManagementEarnings Forecasts 351

Paul Brockman and James CiconAbstract 351Introduction 352Data and Methodology 353Empirical Results 356Conclusion 361References 362

C H A P T E R 25 Modeling Bubbles and Anti-Bubbles in Bear Markets: A Medium-Term Trading Analysis 365

Dean FantazziniAbstract 365Introduction 365

contents xiii

Log-Periodic Models: A Review 367Empirical Analysis with World Stock Market Indexes 372Out-of-Sample Empirical Analysis 381Conclusion 387References 387

C H A P T E R 26 Strategic Financial Intermediaries with Brokerage Activities 389

Laurent Germain, Fabrice Rousseau, and Anne VanhemsAbstract 389Introduction 390The Benchmark Model: No Noise Is Observed 392The General Model: When Some Noise Is Observed 394Conclusion 398References 398Appendix 399

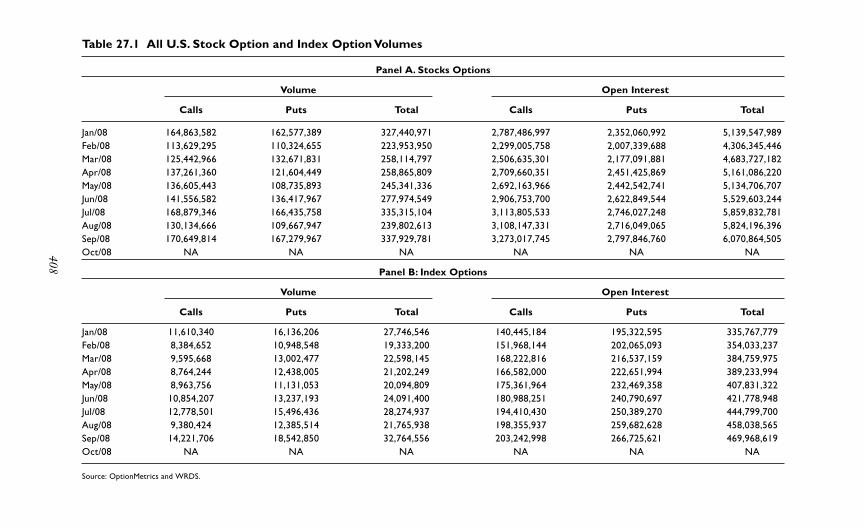

C H A P T E R 27 Financial Markets, InvestmentAnalysis, and Trading in Primary and Secondary Markets 403

André F. GygaxAbstract 403Introduction 404Investment Analysis and Types of Trading 404Composition of Trading Volume and Trading 406Trading in Primary Versus Secondary Markets 407Conclusion 412References 412

C H A P T E R 28 Trading and Overconfidence 417

Ryan Garvey and Fei WuAbstract 417Introduction 417Data 418

xiv contents

Empirical Results 420Conclusion 425References 426Notes 427

C H A P T E R 29 Correlated Asset Trading and Disclosure of Private Information 429

Ariadna DumitrescuAbstract 429Introduction 429The Model 433Disclosure of Information and Market Liquidity 436Conclusion 440Acknowledgments 440References 440

INDEX 443

contents xv

This page intentionally left blank

xvii

EDITOR

Greg N. Gregoriou has published 38 books, 60 refereed publications inpeer-reviewed journals, and 20 book chapters since his arrival at SUNY(Plattsburgh) in August 2003. Professor Gregoriou’s books have been pub-lished by John Wiley & Sons, McGraw-Hill, Elsevier-Butterworth/Heinemann, Taylor and Francis/CRC Press, and Palgrave-Macmillan. Hisarticles have appeared in the Journal of Portfolio Management, Journal of Futures Markets, European Journal of Operational Research, Annals ofOperations Research, Computers and Operations Research, and elsewhere. Pro-fessor Gregoriou is hedge fund editor and an editorial board member forthe Journal of Derivatives and Hedge Funds, as well as an editorial boardmember for the Journal of Wealth Management, the Journal of Risk Manage-ment in Financial Institutions, and the Brazilian Business Review. He is also amember of the curriculum committee at Chartered Alternative InvestmentAnalyst (CAIA) Association based in Amherst, Massachusetts. A native ofMontreal, Professor Gregoriou obtained his joint Ph.D. in finance at theUniversity of Quebec at Montreal, which merges with the resources ofMontreal’s three other major universities (McGill University, ConcordiaUniversity, and HEC-Montreal). Professor Gregoriou’s interests focus onhedge funds and CTAs.

This page intentionally left blank

xix

CONTRIBUTORS

Mohamed El Hedi Arouri is an associate professor of finance at the University of Orleans, France and a researcher at EDHEC Business Schoolin France. He holds a master’s degree in economics and a Ph.D. in financefrom the University of Paris X Nanterre. His research focuses on the costof capital, stock market integration, and international portfolio choice. Hehas published articles in refereed journals such as the International Journalof Business and Finance Research, Frontiers of Finance and Economics, theAnnals of Economics and Statistics, Finance, and Economics Bulletin.

Juan Ayora is an investment manager. He obtained a degree in actuarialand financial Studies (2006) and the MSc in banking and quantitativefinance (2008), both with honors from the University of Valencia, Spain.His areas of interest focus on portfolio management and trading rules.

G. Geoffrey Booth holds the Frederick S. Addy Distinguished Chair inFinance, serves as the Department of Finance Chairperson, and is the Acting Associate Dean for Academic Affairs and Research at MichiganState University. He received his Ph.D. from the University of Michigan in 1971. Professor Booth’s research focuses on the behavior of financialmarkets. He serves on several editorial boards and is the editor of the Journal of International Financial Markets, Institutions & Money.

Paul Brockman is the Joseph R. Perella and Amy M. Perella Chair ofFinance at Lehigh University. He holds a bachelor’s degree in internationalstudies from Ohio State University (summa cum laude), an MBA fromNova Southeastern University (accounting minor), and a Ph.D. in finance (economics minor) from Louisiana State University. He received his Certi-fied Public Accountant (CPA) designation (Florida, 1990) and worked forseveral years as an accountant, cash manager, and futures and optionstrader. His academic publications have appeared in the Journal of Finance,the Journal of Financial Economics, the Journal of Financial and QuantitativeAnalysis, the Journal of Banking and Finance, the Journal of CorporateFinance, the Journal of Empirical Finance, the Journal of Financial Research,Financial Review, Review of Quantitative Finance and Accounting, and Finan-cial Markets, Institutions and Instruments, among others. Professor Brock-man has served as a member of the editorial board for the Journal of

Multinational Financial Management and the Hong Kong Securities Insti-tute’s Securities Journal.

Wilson F. Chan is an assistant general manager of Shanghai CommercialBank, a former assistant general manager and head of Treasury & Marketsof Industrial and Commercial Bank of China (Asia), and a former directorof Citi Private Bank. He has 20 years’ experience in currency and interestrate trading, and holds the degrees MA, MSocSci, and MBA. Mr. Chan hadserved as the secretary of ACI–Hong Kong Financial Markets Associationfor more than 10 years. In 2005, the association was merged into TreasuryMarkets Association, where he leads its education subcommittee.

Narat Charupat is an associate professor of finance at the DeGrooteSchool of Business, McMaster University. He has conducted research in theareas of financial innovation, security designs, annuity and insurance prod-ucts, commodity investment, and behavioral finance. His research has beenpublished in various journals such as the Journal of Economic Theory, theJournal of Banking and Finance, the Journal of Risk and Insurance, and theJournal of Financial and Quantitative Analysis (forthcoming). He has taughtcourses in financial derivatives, international finance, and personal finance.Prior to joining McMaster University, he worked for an investment bankand a risk management software company.

James Cicon holds a law degree ( JD) and an MBA from the University ofMissouri. Prior to returning to school for his joint JD/MBA he was an elec-trical and computer engineer (Brigham Young University) and worked manyyears modeling, simulating, and designing new products for companies,such as Hewlett Packard and Fluke. Mr. Cicon has written hundreds ofthousands of lines of code and debugged codebases with millions of lines.Some of the new products he developed include drivers and hardware forinkjet printers, ATM and Frame Relay wide area network analyzers, andindustrial/automotive monitoring and protection systems. He has writtenneural network software enabling Pepsico to place Taco Bell restaurant sitesand he has designed adaptive controllers which learn how to best controlbrain slice chambers used in biomedical research. Mr. Cicon served fouryears in the U.S. Military Intelligence Corp and worked live missions in theiron curtain in Germany gathering and processing information from East-ern bloc countries. At the time of this writing, Mr. Cicon is a Ph.D. candi-date in the finance department of the University of Missouri. He haspresented twice at FMA and has several working papers based on latentsemantic analysis and textual analysis of corporate documents.

xx contributors

Ariadna Dumitrescu holds a Ph.D. in economics from IDEA (UniversitatAutònoma de Barcelona), and a bachelor’s degree in mathematics from theUniversity of Bucharest. She is an assistant professor of finance at ESADEBusiness School, France. Her research interests include asset pricing andstrategic behavior in financial markets, with applications to market microstruc-ture and valuation of corporate debt. Her research results have been publishedin leading field journals such as the Journal of Corporate Finance, the Journal ofBanking and Finance, and European Financial Management.

Dean Fantazzini is an associate professor in econometrics and finance atthe Moscow School of Economics–Moscow State University (MSU), atrainer at the Academy of Business–Ernst & Young in Moscow and, sinceSeptember 2009, a visiting professor in econometrics and finance at theHigher School of Economics, Moscow. He graduated with honors from theDepartment of Economics at the University of Bologna (Italy) in 2000. Heobtained the master in f inancial and insurance investments from theDepartment of Statistics–University of Bologna (Italy) in 2000 and a Ph.Din economics in 2006 from the Department of Economics and QuantitativeMethods, University of Pavia (Italy). Before joining the Moscow School ofEconomics, he was a research fellow at the Chair for Economics andEconometrics, University of Konstanz (Germany) and at the Department ofStatistics and Applied Economics, University of Pavia (Italy). A specialist intime-series analysis, financial econometrics, multivariate dependence infinance and economics, Professor Fantazzini has to his credit more than 20publications, including three monographs. In 2009 he was awarded forfruitful scientific research and teaching activities by the former USSR Pres-ident and Nobel Peace Prize winner Mikhail S. Gorbachev and by the MSURector Professor Viktor A. Sadovnichy.

Mark D. Flood completed his undergraduate work at Indiana Universityin Bloomington, where he majored in finance (B.S., 1982) and German andeconomics (B.A., 1983). In 1990, he received his Ph.D. in finance from theGraduate School of Business at the University of North Carolina at ChapelHill. He was a visiting scholar and economist in the research department ofthe Federal Reserve Bank of St. Louis from 1989 to 1993. From 1993 to2003, he served as an assistant professor of finance at Concordia Universityin Montreal, a visiting assistant professor of finance at the University ofNorth Carolina at Charlotte, and a senior financial economist in the Divi-sion of Risk Management at the Office of Thrift Supervision. He is a seniorfinancial economist at the Federal Housing Finance Agency in Washington,DC; a partner with RiskTec Currency Management, which markets

contributors xxi

currency funds; and the co-founder of ProBanker Simulations, which sellseducational simulations of a banking market. His research interests includefinancial markets and institutions, data integration technologies, securitiesmarket microstructure, and bank market structure and regulatory policy.His research has appeared in a number of scholarly journals, including theReview of Financial Studies, Quantitative Finance, the Journal of InternationalMoney and Finance, and the St. Louis Fed’s Review.

Emmanuel Fragnière is a Certified Internal Auditor and a professor ofservice management at the Haute École de Gestion in Geneva, Switzerland.He is also a lecturer at the Management School of the University of Bath,UK. He specializes in energy, environmental, and financial risk. He haspublished several papers in academic journals such as the Annals of Opera-tions Research, Environmental Modeling and Assessment, Interfaces, the Inter-national Journal of Enterprise Information Systems, and Management Science.

Ryan Garvey is an associate professor in finance and chair of the Depart-ment of Finance at Duquesne University, Pittsburgh, PA. Professor Garvey’sresearch has been published in the Journal of Financial Markets, FinancialAnalysts Journal, Journal of Portfolio Management, Journal of EmpiricalFinance, and many other journals. He has devised intraday trading modelsimplemented by a U.S. broker-dealer.

Laurent Germain is a professor of finance and the head of the FinanceGroup at Toulouse Business School, France. His research interests includemarket microstructure, behavioral finance, and corporate finance. He grad-uated from Toulouse Business School, Toulouse School of Economics, NewYork University, and the University Paris Dauphine. After a post-doctoratefrom London Business School in 1996 financed by the European Commis-sion, he attained a position of assistant professor of finance at London Busi-ness School. He left LBS in 2000 to join Toulouse Business School. He isone of the directors of the European Financial Management Associationand has published articles in leading journals such as the Review of FinancialStudies, the Journal of Financial and Quantitative Analysis, and the Journal ofFinancial Intermediation.

Eleftherios Giovanis studied economics at the University of Thessaly(Volos-Greece) and graduated in July 2003. He went on to graduate with anMSc in applied economics and finance at the University of Macedonia(Thessaloniki-Greece) in 2009. Mr. Giovanis complete a second MSc inquality assurance at the Hellenic Open University in Patra, Greece, at the

xxii contributors

School of Technology & Science. His dissertation is on reliability andmaintenance analysis. He also works as a statistician for a well-knownGreek firm.

Umit G. Gurun joined the University of Texas at Dallas as an assistantprofessor of accounting in August 2004, after receiving his Ph.D. in financefrom Michigan State University. Professor Gurun also holds an MBA fromKoc University of Turkey, and a bachelor’s degree in industrial engineeringfrom Bilkent University of Turkey. His research interests are in the areas ofasset pricing, market microstructure, and investments.

André F. Gygax (lic.oec.HSG St.Gallen; MS, MBA Colorado; Ph.D. Mel-bourne) is a faculty member at the University of Melbourne in Australia.He has published research articles in the areas of corporate finance, entre-preneurial finance, and asset pricing. Professor Gygax has worked for theUniversity of Colorado and the University of Technology in Sydney. Hehas also worked in the corporate sector for Swiss Bank Corporation, BusagVentures, Mercis, the World Trade Center, and Micrel.

Tim A. Herberger is a Ph.D. candidate as well as a research and teachingassistant in finance at the department of management, business administra-tion, and economics at Bamberg University (Germany). He studied businessadministration at the University of Erlangen-Nuernberg (Germany), and atthe University of St. Gallen (Switzerland). He received his MSc in 2007.His major fields of research are behavioral and empirical finance as well asinvestments in human capital.

A. Stan Hurn graduated with a D.Phil. in economics from Oxford in1992. He worked as a lecturer in the Department of Political Economy atthe University of Glasgow from 1988 to 1995 and was appointed OfficialFellow in Economics at Brasenose College, Oxford in 1996. In 1998 hejoined the Queensland University of Technology as a professor in theSchool of Economics and Finance. His main research interests are in thefield of time-series econometrics. He is foundation board member ofthe National Centre for Econometric Research.

Lester Ingber received his diploma from Brooklyn Technical High Schoolin 1958; a bachlor’s degree in physics from Caltech in 1962; and a Ph.D. intheoretical nuclear physics from the University of California, San Diego in1966. He has published approximately 100 papers and books in theoreticalnuclear physics, neuroscience, finance, general optimization, combat analysis,

contributors xxiii

karate, and education. He has held positions in academia, government, andindustry. Through Lester Ingber Research (LIR), he develops and consultson projects documented in his Webste (http://www.ingber.com/ archive).

Pankaj K. Jain is the Suzanne Downs Palmer Associate Professor ofFinance at the Fogelman College of Business at the University of Memphis.Previously he worked in the financial services industry. He has publishedhis award-winning research on financial market design in leading journalssuch as the Journal of Finance, the Journal of Banking and Finance, FinancialManagement, the Journal of Investment Management, the Journal of FinancialResearch, and Contemporary Accounting Research. He has been invited topresent his work at the New York Stock Exchange, National StockExchange of India, National Bureau of Economic Research in Cambridge,and the Capital Market Institute at Toronto.

Fredj Jawadi is currently an assistant professor at Amiens School ofManagement and a researcher at EconomiX at the University of ParisOuest Nanterre La Defense (France). He holds a master’s degree ineconometrics and a Ph.D. in financial econometrics from the Universityof Paris X Nanterre (France). His research topics cover modeling assetprice dynamics, nonlinear econometrics, international finance, and finan-cial integration in developed and emerging countries. He has published ininternational refereed journals such as the Journal of Risk and Insurance,Applied Financial Economics, Finance, and Economics Bulletin, as well asauthoring several book chapters.

Christine Jiang is a professor of finance at the Fogelman College of Busi-ness and Economics at the University of Memphis, Tennessee. ProfessorJiang’s research includes issues in market microstructure, investments, andinternational finance. She has made numerous presentations at national andinternational conferences. She has published articles on market microstruc-ture, exchange rates, mutual fund performance, and asset pricing in theJournal of Finance, the Journal of Banking and Finance, Financial AnalystsJournal, Decision Science, the Journal of Financial Research, Financial Review,and other refereed journals. Her work has been featured in articles in theFinancial Times and Dow Jones News Service. Winner of the SuzanneDowns Palmer Professorship in Research in 2003 and 2006 at the Univer-sity of Memphis, Professor Jiang earned her Ph.D. in finance from DrexelUniversity in Philadelphia, PA. She also holds a master’s degree from theSloan School of Management of the Massachusetts Institute of Technology,and a bachelor’s of science from Fudan University in Shanghai, China.

xxiv contributors

Vasileios Kallinterakis (BSc., double MSc, Ph.D.) works as a teachingfellow in finance at Durham Business School, UK. His research interestsrelate to behavioral finance with particular emphasis on issues of herdingand feedback trading and his research has been presented in several confer-ences and published in peer-reviewed journals. Professor Kallinterakis hasserved as referee and member of the editorial board for several academicjournals and is currently providing consultancy services for a major globalbrokerage house.

Sarvinjit Kaur (ACCA, MSc) is a regulatory reporting manager withHSBC UK. She possesses extensive industry experience in auditing andfinancial analysis having previously worked in her native Malaysia forHSBC and Ernst & Young in various posts for several years. She is alsoactive in finance research, currently investigating the association betweenexchange-traded funds and investors’ behavior.

Dimitris Kenourgios is a lecturer in the Department of Economics atUniversity of Athens. He studied economics at the University of Athens andbanking and finance at the University of Birmingham, UK (MSc). He alsoholds a Ph.D. in finance from the University of Athens, Department of Eco-nomics. He specializes in emerging financial markets and risk management.His works have been published in Small Business Economics, the Journal of Policy Modeling, Applied Financial Economics, and the Journal of EconomicIntegration, among others.

Kees G. Koedijk is Dean of the Faculty of Economics and BusinessAdministration and Professor of Finance at Tilburg University, TheNetherlands. He is also affiliated with Maastricht University and the Cen-tre for Economic Policy Research. He has published widely on marketmicrostructure, risk management, international f inance, and sociallyresponsible investing. His work has appeared in leading internationaljournals such as the Review of Financial Studies, the Journal of Business,and the Journal of International Money and Finance. Professor Koedijk is aformer member of the economic advisory council for the Dutch House ofParliament.

Daniel M. Kohlert completed his Ph.D. (summa cum laude) in financialeconomics at Bamberg University (Germany) in 2008. He is an assistantprofessor of finance at the department of management, business administra-tion and economics at Bamberg University. He holds an MBA in financeand marketing from Western Illinois University and a MSc in finance from

contributors xxv

the University of Bamberg. His major fields of research are behavioral andempirical finance as well as neuro-finance.

Lawrence Kryzanowski is the senior research chair in finance at Concor-dia University in Montreal, Canada. He is the (co-)author of more than 110refereed journal articles and the recipient of 15 research awards, including abest paper award at the 2008 FMA (U.S.) meeting. He is the foundingchairperson of the Northern Finance Association and is active in variouseditorial capacities for various refereed journals. His more recent activitiesas an expert witness include utility rate of return applications and courtproceedings for price distortion due to alleged misrepresentation. He wasthe first representative of retail investors on the Regulation Advisory Com-mittee (RAC) of Market Regulation Services (now IIROC), which reviewsall amendments to the common set of equities trading rules established toregulate various trading practices in order to ensure fairness and maintaininvestor confidence in Canadian markets.

Skander Lazrak is an associate professor in finance at Brock University inSt. Catherines, Canada. The authors solely or jointly have published exten-sively on market performance.

Camillo Lento is a Ph.D. candidate at the Universit y of SouthernQueensland (Australia) and lecturer at Lakehead University (Canada). He isa chartered accountant (Canada) and holds an MSc (finance) and BComm(honours) from Lakehead University (Canada). Before embarking on hisPh.D., he worked in a variety of positions in accounting, auditing, and assetvaluation. He has authored numerous studies on technical analysis and trad-ing models. He is refining his research activities in combined signalapproach to technical analysis that jointly employs various individual trad-ing rules into a combined signal. His research on technical analysis appearsin both academic journals and practitioner magazines.

Thomas H. McInish is an author or coauthor of more than 100 scholarlyarticles in leading journals such as the Journal of Finance, the Journal ofFinancial and Quantitative Analysis, the Journal of Portfolio Management, theReview of Economics and Statistics, and the Sloan Management Review. Cited asone of the “Most Prolific Authors in 72 Finance Journals,” Professor McInishwas ranked 20 (tie) out of 17,573 individuals publishing in these journalsfrom 1953 to 2002. Another study ranked him as 58 out of 4,990 academicsin number of articles published during 1990 to 2002. Professor McInish’s co-authored, path-breaking article on intraday stock market patterns originally

xxvi contributors

published in the Journal of Finance was selected for inclusion in (1)Microstructure: The Organization of Trading and Short Term Price Behavior,which is part of the series edited by Richard Roll of UCLA entitled TheInternational Library of Critical Writings in Financial Economics (this series is acollection of the most important research in financial economics and serves asa primary research reference for faculty and graduate students); and (2) Con-tinuous-Time Methods and Market Microstructure, which is part of the Interna-tional Library of Financial Econometrics edited by Andrew W. Lo of MIT.Professor McInish’s book, Corporate Spin-Offs, was selected by Choice, a pub-lication of the Association of College and Research Libraries, for inclusion onits list of “Outstanding Academic Books 1984.” Blackwell Publishers pub-lished his book Capital Markets: A Global Perspective in 2000 in English andChinese. Professor McInish earned his Ph.D. from the University of Pitts-burgh. He is a Chartered Financial Analyst (CFA), a highly respected pro-fessional designation. Professor McInish holds the Wunderlich Chair ofExcellence in Finance at the University of Memphis, Tennessee.

Alexander Molchanov is a senior lecturer in finance at Massey University,New Zealand. He joined Massey in July 2006 after completing his mastersand doctoral degrees at the University of Miami, Florida. His research top-ics include, but are not limited to, market design and microstructure, inter-national finance, market efficiency, and econometrics. His research has beenpresented at major international conferences in the United States, Europe,and Australasia.

Duc Khuong Nguyen is a professor of finance and head of the Depart-ment of Economics, Finance and Law at ISC Paris School of Management(France). He holds an MSc and a Ph.D. in finance from the University ofGrenoble II (France). His principal research areas concern emerging mar-kets finance, market efficiency, volatility modeling, and risk managementin international capital markets. His most recent articles are published inrefereed journals such as the Review of Accounting and Finance, the Ameri-can Journal of Finance and Accounting, Economics Bulletin, the EuropeanJournal of Economics, Finance and Administrative Sciences, and Bank andMarkets.

Helen O’Gorman received her bachelor’s degree in mathematical studiesfrom the National University of Ireland Maynooth in 2008. She then pro-ceeded to complete an MSc in operational research at the University ofEdinburgh, Scotland. Her MSc dissertation project was titled “The Devel-opment of a Risk Monitoring Tool Dedicated to Commodity Trading in the

contributors xxvii

Precious Metals Sector” and contains material similar to that discussed inher respective chapter in this book.

Spyros Papathanasiou is head of investment department in SolidusSecurities S.A. He studied economics at the University of Athens (BSc,1995) and banking at the Hellenic Open University (MSc, 2003). He alsoholds a Ph.D. in finance from the Hellenic Open University (2009). Hismain research interests are international stock markets, derivatives, andentrepreneurship.

Ohaness G. Paskelian is an assistant professor of finance in the College ofBusiness at the University of Houston–Downtown. He received his Ph.D. in finance from the University of New Orleans (Louisiana). He holds a mas-ter’s in finance and economics from the University of New Orleans, and abachelor’s in computer engineering from the American University of Beirut,Lebanon. Professor Paskelian teaches financial management, cases in finan-cial management, and financial markets and institutions. His main researchinterests lie in the studies of asset pricing, agency issues and firm valuation,and corporate governance mechanisms in the emerging markets. He is a frequent presenter at national and international conferences on finance.

Vlad Pavlov received his MEc from the New Economic School in Moscow in1996. He completed his Ph.D. in 2004 from the Australian National Univer-sity. He joined the Queensland University of Technology as a lecturer infinance in 2000. In 2008 he spent a year working as a senior analyst for aglobal macro hedge fund. His research concentrates on financial econometricsand time-series analysis.

Edward Pekarek is a clinical law fellow for the nonprofit Investor RightsClinic of Pace University Law School, John Jay Legal Services, Inc., and aformer law clerk in the United States District Court for the Southern Dis-trict of New York. Mr. Pekarek holds an LLM degree in corporate bankingand finance law from Fordham University School of Law, a JD from Cleve-land Marshall College of Law, and a bachelor’s degree from the College ofWooster, Ohio. As a law student, Professor Pekarek co-authored and editedthe merit brief for the Respondents in the United States Supreme Courtmatter of Cuyahoga Falls v. Buckeye Community Hope Foundation, and anamicus brief in Eric Eldred, et al. v. John Ashcroft, Attorney General. He isthe former editor-in-chief of a specialty law journal and a nationally rankedlaw school newspaper, and is the author of numerous published articlesregarding securities, banking, and corporate governance issues, which have

xxviii contributors

been cited by such notables as former Securities and Exchange CommissionDirector of Enforcement Linda Chatman Thomsen, as well as the RANDInstitute for Civil Justice in a report commissioned by the SEC regardingbroker-dealer and investment adviser regulation.

Jack Penm is an Academic Level D at Australian National University(ANU). He has an excellent research record in the two disciplines in whichhe earned his two Ph.D.s, one in electrical engineering from the Universityof Pittsburgh, PA, and the other in finance from ANU. He is an author/co-author of more than 80 papers published in various internationallyrespected journals.

Giovanni Petrella is an associate professor of banking at the CatholicUniversity in Milan, Italy. In 2009 he was a visiting lecturer in the Depart-ment of Finance, Insurance & Real Estate at the University of Florida. Atthe Catholic University he teaches an undergraduate class on derivativesand a graduate class on market microstructure; at the University of Florida,he taught a securities trading course in the Master of Science in Finance(MSF) program. He has published papers in the areas of market micro-structure, derivatives, and portfolio management in the following journals:the Journal of Banking and Finance, the Journal of Futures Markets, theEuropean Financial Management Journal, the Journal of Trading, and theJournal of Financial Regulation and Compliance.

Alexandre Repkine graduated with BSc in mathematics from MoscowState University in 1993. He studied at the New Economic School in Rus-sia in the Master of Economics program, where he obtained the MSc ineconomics degree in 1995. He received his Ph.D. in economics from theCatholic University of Leuven, Belgium, in 2000 and has taught economicsat numerous Korean universities since 2001. He is an assistant professor inthe Department of Economics at Korea University.

Gerasimos G. Rompotis is a senior auditor at KPMG Greece and aresearcher with the faculty of economics at the National and KapodistrianUniversity of Athens. His main areas of research cover financial manage-ment and the performance of exchange-traded funds. His work has beenpublished in a number of industry journals. In addition, the work of theauthor has been presented at several international conferences.

Fabrice Rousseau is lecturer at the National University of IrelandMaynooth. His research interests include market microstructure, corporate

contributors xxix

finance with a focus on the design of initial public offerings, behavioralfinance, and financial integration. He graduated from the University ofToulouse and holds a Ph.D. in finance from the Universitat Autonoma deBarcelona. Upon completing his Ph.D., he joined the Department of Eco-nomics, Finance and Accounting at NUI Maynooth. From July 2006 toJune 2007, he was a visiting scholar at the Department of Economics atArizona State University. Some of his research has been published in TheManchester School.

Philip A. Stork is a visiting professor of finance at Massey University,New Zealand. He was a professor of finance at Erasmus University Rotter-dam where he also obtained his Ph.D, and a visiting professor at Duisen-berg School of Finance in Amsterdam and at the Business School ofAix-en-Provence. He has worked in various roles for banks, brokers, andmarket makers in Europe, Australia, and the United States. His academicwork has been published in major international journals, including theEuropean Economic Review, Economics Letters, the Journal of Applied Econo-metrics, the Journal of Fixed Income, and the Journal of International Moneyand Finance.

Nareerat Taechapiroontong received her Ph.D. from the University ofMemphis, Tennesee in market microstructure. She is a full-time lecturer atMahidol University, Thailand. She has previously worked as a trading offi-cer at Securities One Public Co., Ltd. She has published her work on infor-mation asymmetry and trading in the Financial Review. Her work has alsobeen presented at the 2003 FEA conference at Indiana University, the 2002FMA Annual Meeting in San Antonio, and the 21st Australasian Financeand Banking Conference 2008 in Australia.

R. D. Terrell is a financial econometrician, and an officer in the generaldivision of the Order of Australia. He served as Vice-Chancellor of Aus-tralian National University from 1994 to 2000. He has also held visitingappointments at the London School of Economics, the Wharton School,University of Pennsylvania, and the Econometrics Program, PrincetonUniversity. He has published a number of books and research monographsand approximately 80 research papers in leading journals.

Hipòlit Torró is professor of finance in the department of financial eco-nomics at the University of Valencia (Spain). He obtained a degree in eco-nomics and business with honors and a Ph.D. in financial economics at the

xxx contributors

University of Valencia and a MSc in financial mathematics at the universitiesof Heriot-Watt and Edinburgh in Scotland. He has published articles infinancial journals such as the Journal of Futures Markets, the Journal of Busi-ness Finance and Accounting, the Journal of Risk Finance, Quantitative Finance,Investigaciones Economicas. His areas of research are portfolio management(hedging and trading rules) and financial modeling of stock, interest rates,bonds, and commodities (weather and electricity).

Mathijs A. van Dijk is an associate professor of finance at the RotterdamSchool of Management (Erasmus University). He was a visiting scholar atthe Fisher College of Business (Ohio State University) and the FuquaSchool of Business (Duke University, North Carolina). His research focuseson international finance. He has published in various journals in financialeconomics, including the Financial Analyst Journal, the Journal of Bankingand Finance, the Journal of International Money and Finance, and the Reviewof Finance. He has presented his work at numerous international confer-ences as well as seminars at, among others, Dartmouth, Harvard, andINSEAD. In 2008 he received a large grant from the Dutch National Sci-ence Foundation for a five-year research program on liquidity crises ininternational financial markets.

Irma W. van Leeuwen is senior learning officer at ICCO Netherlands.She was previously affiliated with the Research and Development Depart-ment of Oxfam Novib and with the Department of Finance at MaastrichtUniversity. Her past research has concentrated on market microstructure,in particular on price discovery and liquidity in multiple dealer financialmarkets. Her experimental study on interdealer trading appeared in thebook Stock Market Liquidity by François-Serge Lhabitant and Greg N. Gregoriou. Her current research interests include development economics.Her study on microinsurance has been published by the Institute of SocialStudies in The Hague.

Anne Vanhems is professor of statistics in Toulouse Business School,France. She obtained her Ph.D. in applied mathematics in 2001 at the Uni-versity of Toulouse, France and also graduated from ENSAE, Paris. Sheobtained the Fullbright grant to visit the Bendheim Center for Finance atPrinceton University in 2002. She was a visiting professor in the economicdepartment at University College London. She is working on structuralnonparametric econometrics, as well as on estimation of hedge funds per-formances and market microstructure.

contributors xxxi

Laura Whitney received a bachelor’s degree in mathematical economicsfrom Wake Forest University, NC, and worked for three years as an opera-tions research associate for a government contractor in the Washington, DCarea. She recently completed her MSc in operational research at the Univer-sity of Edinburgh, UK, where she took classes in modeling and simulation,optimization, risk analysis, and finance. Her dissertation project focused onthe development of a risk-monitoring tool dedicated to commodity trading,similar to the one developed for her respective chapter in this book.

Michael C. S. Wong is an associate professor at City University of HongKong. He architected risk systems for more than five banks, including thefirst Basel-standard IRB system in Hong Kong, as well as advised morethan 20 banks on risk management and provided training to more than3,000 risk managers and regulators in the China region. He is a foundingmember of CTRISKS, an Asia-based credit rating agency and a foundingmember of FRM Committee of GARP. Professor Wong is listed in RiskWho’s Who and was awarded Teaching Excellence Award by City Univer-sity of Hong Kong. Before his academic and consulting career, he workedin investment banking, specializing in currency, metals, and derivativestrading.

Fei Wu is a professor in finance at University of Electronic Science andTechnology of China, Chengdu, China. He taught at Massey University,New Zealand from 2004 to 2009. His research focuses on behavioralfinance and market microstructure. Dr. Wu’s research has been publishedin Financial Management, Journal of Financial Markets, Journal of Bankingand Finance, Journal of Portfolio Management, and many other journals.

xxxii contributors

ACKNOWLEDGMENTS

I would like to thank Ms. Morgan Ertel at McGraw-Hill (New York City)for assistance, suggestions, and development of the manuscript. I also thankthe production manager Richard Rothschild at Print Matters, Inc. (NewYork City) for assistance in the manuscript. Finally, I thank a handful ofanonymous referees for their valuable assistance in reviewing, selecting, andmaking comments to each chapter in this book. Neither the editor nor thepublisher can guarantee the accuracy of each chapter and each contributoris responsible for his or her own chapter.

xxxiii

This page intentionally left blank

P A R T I

EXECUTION ANDMOMENTUM

TR ADING

This page intentionally left blank

3

1C H A P T E R

PerformanceLeakage and ValueDiscounts on theToronto StockExchange

Lawrence Kryzanowski and Skander Lazrak

ABSTRACT

Various measures of liquidity are estimated for common and preferredshares (individual firms and exchange-traded funds), units (trusts and limited partnerships), notes (index linked and principal protected), andwarrants listed on the Toronto Stock Exchange. We document significantdifferences in potential and actual trade execution costs intra- and inter-security type and across time that impact on the net benefits of tradingfor different levels of trading patience, the valuation discounts of non-granular portfolios under various more or less patient exit strategies, andthe likely performance drag from investments in different security typesor the average security in that security type. We also provide an illustra-tion of how trade execution costs are affected adversely by worries of aglobal recession.

INTRODUCTION

Since the performance of all investment decisions are directly affected bythe quality of effecting such decisions in the marketplace and varies withinand across security types, all investors must carefully balance the marginalbenefits and costs of each transaction. Such costs include commissions, fees,execution, and opportunity costs. Execution quality reflects various tradingdemands for immediate liquidity (speed) based on different investmentstyles and on the availability and cost of such liquidity at each point in time.The latter includes the expected and actual impact of investor trade onmarket prices and on the cost and likelihood of concluding the remainder ofa trade. Since execution quality is most often unobservable, it is imputedfrom the data either as the difference between the actual trade executionprice and the price that would have existed in the absence of the trade or asthe difference (referred to as performance leakage) between the quoted oractual trade price and its counterpart in the absence of trade costs (referredto as the “fair” price). The time to complete a trade for a fixed concessionfrom the “fair” price is another dimension of execution quality, which cannot be measured using most available databases (such as the one usedherein) that do not provide information on order submissions and their sub-sequent fill history. Execution quality also affects the pricing of securitiesthrough its impact on value discounts.

Trade activity measures of liquidity include (un)signed number and dol-lar value of shares traded and the number of trades. Metrics for measuringexpected or actual trade execution costs include quoted, effective and real-ized spreads, and quoted depths. Hasbrouck (2009) provides a good reviewof various measures of trade and market impact costs using daily data.

Earlier research focuses on the measurement of execution cost (e.g.,Collins and Fabozzi, 1991), on the impact of execution costs on the speedand method by which institutional investors should implement buy and selldecisions (e.g., Bodurtha and Quinn, 1990; Wagner and Edwards, 1993;Wilcox, 1993), and on trading costs in different international markets (e.g.,Kothare and Laux, 1995). More recent studies examine the effects ofchanges in exchange rules on execution costs across trading platforms (e.g.,Venkataraman, 2001; SEC, 2001; Bessembinder, 2003; Boehmer, 2005) andon institutional differences (Eleswarapu and Venkataraman, 2006).

To our knowledge, few published studies examine the trade execution costperformance of security types other than stocks, bonds, and highly liquid

4 Part i EXECUTION A ND MOMENTUM TR ADING

derivatives. This study is the first to examine trade execution costs for all thesecurity types on the Toronto Stock Exchange (TSX). We expect to find sig-nificant differences in execution costs for a dichotomization of trades bysecurity type.

The remainder of this chapter is organized as follows. The second section ofthis chapter discusses the sample and data. This chapter’s third section presentsthe measures of market quality. The fourth section presents the empirical estimates of market quality; and the fifth section concludes the chapter.

SAMPLE AND DATA

Our initial sample contains all 2,300 listed securities on the TSX for thefirst two calendar months of 2008; namely, 1,300 common shares, 15 shareslisted in USD, 256 preferred shares, 396 units including income trustsunits, 149 debentures,1 119 warrants, and 65 NT_NO notes includingasset-linked, principal protected notes sponsored by the Royal Bank.2 As iscommon practice in the literature and reporting in the financial press (e.g.,Globe and Mail ) and following the definition of the SEC regarding pennyshares available at http://www.sec.gov/answers/penny.htm, the commonshare sample is split in two based on those trading at or above $5 per share(Common $5) and those trading at less that $5 per share (Common $5)based on the time-series mean price of each common share.

Trading data are extracted from the TSX’s Trades and Quotes (TAQ)database. As in Chordia, Roll, and Subrahmanyam (2001), the data arecleaned by removing: (i) quotes/trades outside regular trading hours of 9:30to 16:00 EST; (ii) trades with negative numbers of shares or trading prices;(iii) trades with delayed delivery, special settlement and/or delivery, or sub-ject to special restrictions and conditions; (iv) bids exceeding offers or eitherwith nil prices or volumes; and (v) quoted percentage spreads exceeding 30 percent.3 These filters delete 2.74 percent and 5.41 percent of the initial202,710,358 quotes and 27,276,955 trades, respectively.

MEASURES OF PERFORMANCE LEAKAGE AND VALUE DISCOUNTS

Our first measure is the quoted spread, QSi,t, for security i at time t or QSi,t (Aski,t Bidi,t) / [0.5(Aski,t Bidi,t)], where the denominator is themidspread. Our second measure is superior to the first for a patient investor

chapter 1 Performance Leakage and Value Discounts 5

given that limit orders can improve on the posted quotes of registered trad-ers on the TSX. Thus, the effective spread, ESi,tk, is given by ESi,t 2

[(Pricei,t MidSpread Prei,t)/MidSpread Prei,t] Ii,t where Ii,t is a trade indi-cator variable equal to 1 for buyer initiated (purchase) trades and 1 forseller initiated (sale) trades. Since benchmark quotes need to be observedwhen the trade decision is made and these times are not observable andquotes may move after submitting even small orders, a five-second lag isused to determine the pretrade benchmark midspread as recommended byBessembinder (2003).

Since the identity of the trade initiator is unobservable empirically, theLee and Ready (1991) algorithm is used to sign the transactions. The tradeis assumed to be buyer- (seller-) initiated when the traded price is higher(lower) than the prevailing midquote or if the last nonzero price change(tick) is positive (negative) for trade prices at the prevailing midquote (tickrule). Contemporaneous quotes (i.e., quotes for a zero-second lag) are usedto compute benchmark midquotes for trade signing purposes (Ellis,Michaely, and O’Hara, 2000; Bessembinder, 2003).

Effective spreads are compensation for both the probability of adverseinformation and order execution. The former represents the loss incurredby market makers to better informed traders as prices move against themarket makers. The realized spread is not only a better measure of com-pensation for trade execution but a better indicator of market liquidity andtrading quality from the market-maker’s perspective. To estimate the real-ized spread and thus eliminate the loss to better informed traders, the trad-ing price is compared with a benchmark or a midquote that occurssometime after the trading takes place. This measures the market-maker’sprofit if she or he rebalances inventory after making the initial trade. As inHuang and Stoll (1996) and Bessembinder (2003), benchmark quotes forboth k 5 and 30 minutes after trades (i.e., MidSpreadPosti,t,k) are usedherein. Daily closing quotes are used for trades occurring within the last k 5 or 30 minutes of a trading session. The realized spread, RSi,t,k, isgiven by: RSi,t,k 2 [(Pricei,t MidSpreadPosti,t,k)/MidSpread Prei,t] Ii,t.Thus, the price impact of a trade, PIi,t,k, is given by the difference betweenthe effective spread and the realized spread, ESi,t RSi,t,k, or PIi,t,k 2 [(MidSpreadPosti,t,k MidSpreadPosti,t,k)/MidSpread Prei,t] Ii,t.

Since the effective/realized spreads or price impact can be negativedue to the measurement of the trade sign variable at a different time

6 Part i EXECUTION A ND MOMENTUM TR ADING

compared with the prevailing or subsequent quote, we also use an alter-native for these spread measures that relies on their absolute values. Forinstance, the alternative measure of the effective spread, AESi,t, is: AESi,t

2 |(Pricei,t MidSpread Prei,t)/MidSpread Prei,t|.The quoted dollar depth, which is the capacity of a market to absorb

trades with little or no price impact, also is measured to assess liquidityand market execution quality. As quotes represent prices at which marketmakers are willing to trade at a prespecified maximum trading size, weassume that this size is the highest possible volume before an order eatsup the available liquidity at the inside quotes and quotes need to be movedup or down depending on trade direction. We measure depth QDi,t, as theaverage quoted order flow size at both the inside bid and ask or QDi,t,

0.5 (Bidi,t BidSizei,t Aski,t AskSizei,t).

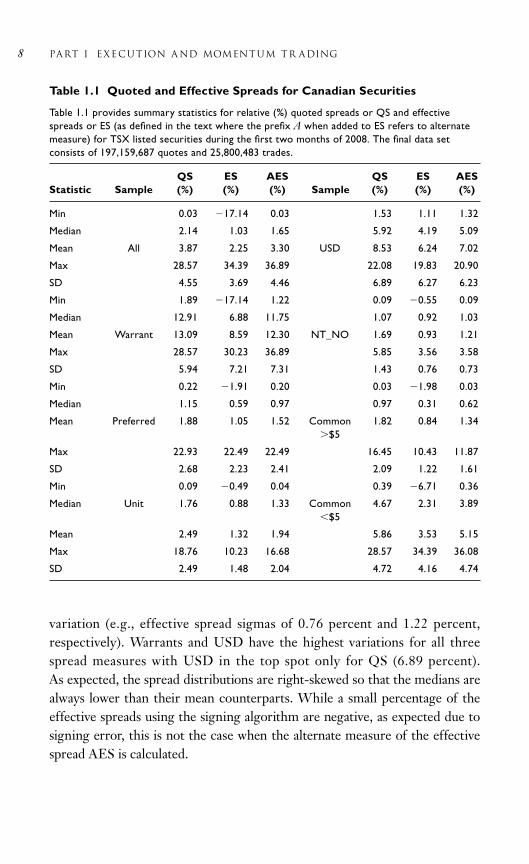

EMPIRICAL ESTIMATES FOR THE TSX

The relative quoted and effective spreads for all the securities listed onthe TSX and seven subsamples differentiated by security type (and pricein the case of common shares) are reported in Table 1.1. As expected, thelowest median spreads are for common shares with prices above $5 (Com-mon $5), followed by the asset-linked notes (NT_NO) for relativequoted spreads (QS) and preferred shares for the two measures of relativeand average effective spreads (ES and AES). The highest median spreadsare for Warrants. To illustrate, the median effective spreads are 0.31 per-cent and 6.88 percent for Common with prices above $5 and Warrants,respectively.

NT_NO and Common $5 are among the two lowest mean spreadswith Common $5 only occupying the lowest mean spread for the ESmeasure. Warrants have the highest mean spreads for each of the threemeasures. The relatively high trading costs associated with Warrants isprimarily due to the relatively low traded prices of Warrants (mean of$1.79 compared with $13.24 for all other securities). Securities denomi-nated in USD have the second highest mean and median spreads for all three measures. To illustrate, the median USD effective spread is 4.19 percent.

As expected, considerable variation exists in the spread measures withineach security type. The NT_NO followed by Common $5 have the lowest

chapter 1 Performance Leakage and Value Discounts 7

variation (e.g., effective spread sigmas of 0.76 percent and 1.22 percent,respectively). Warrants and USD have the highest variations for all threespread measures with USD in the top spot only for QS (6.89 percent). As expected, the spread distributions are right-skewed so that the medians arealways lower than their mean counterparts. While a small percentage of theeffective spreads using the signing algorithm are negative, as expected due tosigning error, this is not the case when the alternate measure of the effectivespread AES is calculated.

8 Part i EXECUTION A ND MOMENTUM TR ADING

Table 1.1 Quoted and Effective Spreads for Canadian Securities

Table 1.1 provides summary statistics for relative (%) quoted spreads or QS and effectivespreads or ES (as defined in the text where the prefix A when added to ES refers to alternatemeasure) for TSX listed securities during the first two months of 2008. The final data setconsists of 197,159,687 quotes and 25,800,483 trades.

QS ES AES QS ES AESStatistic Sample (%) (%) (%) Sample (%) (%) (%)

Min 0.03 17.14 0.03 1.53 1.11 1.32

Median 2.14 1.03 1.65 5.92 4.19 5.09

Mean All 3.87 2.25 3.30 USD 8.53 6.24 7.02

Max 28.57 34.39 36.89 22.08 19.83 20.90

SD 4.55 3.69 4.46 6.89 6.27 6.23

Min 1.89 17.14 1.22 0.09 0.55 0.09

Median 12.91 6.88 11.75 1.07 0.92 1.03

Mean Warrant 13.09 8.59 12.30 NT_NO 1.69 0.93 1.21

Max 28.57 30.23 36.89 5.85 3.56 3.58

SD 5.94 7.21 7.31 1.43 0.76 0.73

Min 0.22 1.91 0.20 0.03 1.98 0.03

Median 1.15 0.59 0.97 0.97 0.31 0.62

Mean Preferred 1.88 1.05 1.52 Common 1.82 0.84 1.34$5

Max 22.93 22.49 22.49 16.45 10.43 11.87

SD 2.68 2.23 2.41 2.09 1.22 1.61

Min 0.09 0.49 0.04 0.39 6.71 0.36

Median Unit 1.76 0.88 1.33 Common 4.67 2.31 3.89$5

Mean 2.49 1.32 1.94 5.86 3.53 5.15

Max 18.76 10.23 16.68 28.57 34.39 36.08

SD 2.49 1.48 2.04 4.72 4.16 4.74

A comparison of the mean, median, and sigma values for common sharestrading below and above $5 exemplifies the much higher trade costs associatedwith so-called “penny” stocks (e.g., median ES of 2.31 percent versus 0.31 percent and sigma of 4.16 percent versus 1.22 percent, respectively). Thismay have implications for small cap investing in national markets smaller thanin the United States.

The relative realized spreads for the various samples are reported inTable 1.2. With four exceptions (RS5 and RS30 for both USD and

chapter 1 Performance Leakage and Value Discounts 9

Table 1.2 Realized Spreads

Table 1.2 provides summary statistics for (%) realized spreads or RS (as defined in the textwhere the prefax A refers to alternate measure and the suffix 5 and 30 refer to quotes 5 and30 minutes, respectively, after trades) for TSX listed securities during the first two months of 2008.

RS5 ARS5 RS30 ARS30 RS5 ARS5 RS30 ARS30Statistic Sample (%) (%) (%) (%) Sample (%) (%) (%) (%)

Min 28.57 0.00 48.89 0.00 8.63 1.29 10.23 1.39

Median 1.20 1.84 1.16 2.11 1.23 6.06 2.79 4.92

Mean All 2.28 3.70 2.18 3.97 USD 0.60 8.18 1.64 6.05

Max 39.33 65.37 45.06 117.81 8.22 20.34 5.10 15.73

SD 3.65 5.49 3.88 6.04 5.24 6.69 4.31 4.16

Min 28.57 1.81 33.58 2.26 1.05 0.00 1.03 0.00

Median Warrant 6.03 12.28 5.52 13.00 NT_NO 0.83 1.25 0.96 1.21

Mean 7.13 14.91 6.97 16.01 0.75 1.74 0.86 1.66

Max 34.09 54.58 45.05 117.81 2.59 5.57 2.58 5.60

SD 8.42 10.66 9.41 14.69 0.82 1.45 0.75 1.34

Min 2.00 0.19 2.00 0.20 2.72 0.03 3.97 0.03

Median 0.72 1.03 0.71 1.05 0.43 0.90 0.41 1.37

Mean Preferred 1.19 1.56 1.17 1.61 Common 1.00 1.59 0.94 1.90$5

Max 21.43 21.43 21.43 21.43 10.58 10.98 10.58 11.44

SD 1.98 2.28 1.98 2.35 1.37 1.64 1.30 1.55

Min 0.03 0.04 0.60 0.05 19.05 0.37 48.89 0.36

Median 1.08 1.43 1.02 1.53 2.78 4.02 2.67 4.37

Mean Units 1.59 2.16 1.51 2.28 Common 3.62 5.55 3.41 5.86$5

Max 9.68 18.85 10.75 18.86 39.33 65.37 43.71 70.05

SD 1.66 2.34 1.61 2.29 4.07 5.87 4.48 5.84

NT_NO), the means are greater than their median counterparts, whichindicates right-skewed distributions. The median relative realized spreadsare lowest for Common $5 followed by Preferreds for all but theARS30 (Alteranative Realized Spread based on quotes 30 minutes aftertrades) measure where the lowest median is for Preferreds followed byNT_NO. To illustrate, the median RS5 and RS30 values are 0.43 per-cent and 0.41 percent, respectively, for Common $5. The highestmedian relative realized spreads are for Warrants. This is followed byCommon $5 for RS5 and by USD for the other three relative realizedspread measures.

The lowest mean RS5 and RS30 are for USD and NT_NO, respectively,followed by respectively NT_NO and Common $5. In contrast, the low-est mean ARS5 and ARS30 are for Preferreds followed by Common $5and NT_NO, respectively. Warrants always have the highest mean relativerealized spreads followed by Common $5 for RS5 and RS30 and by USDfor ARS5 and ARS30, respectively. Thus, the choice of how to calculate therelative realized spread has an impact on the rankings of this measureacross security types.

The lowest sigmas are found for NT_NO for all four relative realizedspread measures, followed by units for RS5 and Common $5 for theother three measures. Once again, Warrants have the highest relative real-ized spreads followed by USD for the two 5-minute measures and Com-mon $5 for the two 30-minute measures. To illustrate, the sigmas forRS5 and RS30 for Warrants are 8.42 percent and 9.41 percent, respectively.

The quoted depth-traded volumes (share numbers and dollars) and thenumber of trades for the various samples are reported in Table 1.3. All thedistributions are right-skewed. The lowest mean, median, and sigma ofquoted depth (QD), share volume (Shares vol) and number of trades are forWarrants, NT_NO, and NT_NO, respectively. With two exceptions, thehighest mean, median, and sigma of these three measures are for Common$5. The exceptions are NT_NO for the median QD and Common $5for the median Shares vol.

The high depth for the index linked notes shows that dealers have mini-mal concerns about trading against informed traders as private informationis negligible about the entire index compared with individual securities. Thehigh median of penny stock trading volume measured in number of sharesis due to the larger round lot sizes of stocks trading below $1 and the needto trade more shares of a lower priced share to achieve a comparable dollar

10 Part i EXECUTION A ND MOMENTUM TR ADING

Table 1.3 Quoted Depth and Trading Activity

Table 1.3 provides summary statistics for quoted depth (QD ($)), share volume (Shares vol), and dollar traded volume ($ Vol) in thousands, and number oftrades (Nb_trades) for TSX-listed securities during the first two months of 2008.

Statistic Sample QD ($) Shares vol $ Vol Nb_trades Sample QD ($) Shares vol $ Vol Nb_trades

Min 0.023 0.100 0.390 1.000 3.115 0.465 2.890 1.500

Median 9.761 25.550 93.318 12.929 12.066 3.321 31.706 5.033

Mean All 23.442 195.475 3,356.594 297.921 USD 15.324 36.295 96.264 5.675

Max 1,415.986 11,170.279 259,932.309 18,540.071 36.073 363.262 597.645 15.929

SD 73.373 663.623 17,206.560 1,222.051 9.441 108.491 174.238 3.831

Min 0.062 0.667 0.495 1.000 8.727 0.830 7.924 1.000

Median Warrant 1.138 24.578 14.767 5.099 NT_NO 26.003 2.750 29.576 1.857

Mean 4.445 75.745 70.674 11.646 32.595 4.066 44.990 2.357

Max 31.628 2,127.875 784.184 142.750 162.306 20.800 241.305 9.000

SD 6.912 211.431 147.433 19.117 27.205 3.971 45.936 1.604

Min 0.045 0.100 0.425 1.000 1.393 0.180 1.239 1.000

Median 15.395 4.042 76.289 6.225 Common $5 14.472 49.815 523.919 61.664

Mean Preferred 18.977 6.924 135.580 9.343 50.722 358.856 9,990.020 809.795

Max 107.109 85.414 2,154.335 57.333 1,415.986 8,686.755 259,932.309 18,540.071

SD 12.090 9.514 204.020 8.798 118.336 893.362 30,241.782 2,111.872

Min 0.358 0.425 2.079 1.125 0.023 0.350 0.390 1.000

Median 11.070 14.754 123.071 15.190 3.595 59.620 51.275 14.110

Mean Unit 16.178 79.108 1,300.092 153.898 Common $5 6.384 216.275 327.037 79.110

Max 1,261.424 2,074.231 52,655.592 3,884.548 148.640 11,170.279 2,2652.803 1,965.429

SD 63.361 185.596 4,357.675 429.569 13.721 750.003 1,240.112 204.073

11

volume as for non-penny shares.4 Despite their high depths and low tradingcosts compared with other security types, the notes offered by the RoyalBank are not heavily traded as the exchange-traded funds are more popularinstruments. Units are the second most actively traded security type on theTSX. The income trust vehicle, which passes through its income untaxed,was a popular investment choice due to yields considerably higher thanthose on fixed income securities (Kryzanowski and Lu, 2009).

All of the nonparametric (distribution-free) Kruskal-Wallis tests of theequality of the medians as well as the ANOVA tests of equality of meansacross the seven security types for each of the 11 liquidity measures aresignificant at better than the 0.001 level. Based on tests of the means andmedians for all pairs of security types for each of the 11 liquidity measures,as summarized in Table 1.4 (further details available from the authors), wefind the following to be significant at better than the 0.05 level: (i) all pair-ings of Common $5 with Common $5 and with Preferreds; (ii) all butone of the pairings of Common $5 or Common $5 with Units (i.e.,median Nb_trades for Common $5) and with Warrants (i.e., mean QDfor Common $5); and (iii) all but one of the pairings of Warrants withPreferreds (i.e., mean and median Nb_trades), with Units (mean Share vol)and with NT_NO (mean $ Vol).

Although comparisons across markets (and especially for different timeperiods) are only indicative due to interexchange differences in designfeatures (e.g., tick and board lot sizes, order handling rules, and regula-tory rules and their enforcement), Warrants on the TSX have highermean relative quoted spreads (13.086 percent versus 7.308 percent) andlower quoted dollar depths (4,445 CAD versus 171,990 HKD) based onthe values reported for company warrants by Brockman and Chung(2007) for Hong Kong for the period of May 1996 to August 1997. Asexpected, the relative quoted and effective spreads for TSX Common$5 are inferior to the cross-sectional statistics for time-series meansreported by Roll (2005) for NYSE-listed securities. The mean, median,and sigma for the TSX (NYSE) are 1.82 percent (1.60 percent), 0.97 per-cent (1.15 percent), and 2.09 percent (1.36 percent) for relative quotedspreads, and are 1.82 percent (1.11 percent), 0.84 percent (0.77 percent)and 1.34 percent (1.32 percent) for the alternative relative effectivespreads. Not surprisingly, the mean relative quoted and effective spreadsof 1.82 percent and 1.34 percent are considerably higher than theirrespective counterparts of 0.54 percent and 0.50 percent for the TSX and

12 Part i EXECUTION A ND MOMENTUM TR ADING

13

Table 1.4 Tests of Pairwise Means and Medians for the Various Liquidity Measures

Table 1.4 reports the liquidity measures with p values 0.05 for tests of pairwise means and medians, which are reported in the lower and upper diagonals,respectively. Thus, they are not reported (such as between Common $5 and Common $5) if they are significant at the 0.05 level. They are underlined ifthe pairwise differences are significant at the 0.10 level.

Common CommonWarrant Preferred Unit USD NT_TO $5 $5

Warrant Nb_trades $ Vol, Nb_trades, ES

Preferred Nb_trades QD, Shares vol, QS, ES, AES, QDNb_trades, RS5 (A)RS5 & 30

Unit Shares vol QD, ES QD, RS5, RS30 QS, ES, AES, Nb_tradesARS5, (A)RS30

USD Shares & $ Vol, QD, $ Vol, QD, Shares & $ Vol, Shares & $ QS, $ Vol, AES, QD, RS5Nb_trades, Nb_trades, Nb_trades, Vol, RS5 (A)RS5 & 30ES, RS30 RS5 & 30 RS5, RS30

NT_NO $ Vol QS, Shares vol, QD, $ Vol, $ Vol, RS5&30 QS, (A)RS5 & 30(A)ES, (A)RS5, ES, ARS5,(A)RS30 ARS30

Common $5 QD QS, Shares & $ Vol, Shares & $ VolNb_trades, AES,ARS5, (A)RS30

Common $5 QS, ES, AES, QD, Shares & $ Vol, QS, QD, (A)ES,(A)RS5, RS30 Nb_trades, RS5 & 30 (A)RS5 & 30

considerably lower than their respective counterparts of 2.32 percent and 2.13 percent for the average exchange, which are reported by Jain(2003) based on closing daily values for the 25 highest market capitaliza-tion stocks for each of 51 major exchanges for the first four months of 2000.

Time-series plots of six of the liquidity measures for the various samplesare depicted in Figures 1.1 to 1.6. We examine the intertemporal variationin these series using the standard deviation (sigma) and coefficient of varia-tion (i.e., the sigma divided by the mean).

Based on untabulated results, the three security types with the highestspread sigmas are Warrants followed by USD and NT_NO for QS and aninterchange of Warrants and NT_NO for ES and RS30. The three securitytypes with the highest spread Coefficients of Variation (CVs) are NT_NOfollowed by USD and Preferreds for QS, and USD followed by NT_NO

14 Part i EXECUTION A ND MOMENTUM TR ADING

Warrant

Warrant

14

12

10

8

6

4

2

0

0102

0104

0108

0110

0114

0116

0118

0122

0124

0128

0130

0201

0205

0207

0211

0213

0215

0220

0222

0226

0228

Date—Daily first 2 months 2008

NT_NO

USD

Med

ian

Rel

ativ

e Q

uote

d S

prea

d (%

)

USD

Com<$5

AllCom>$5UnitPreferred

Figure 1.1 Time-Series of Median Relative Quoted Spreads (%)

chapter 1 Performance Leakage and Value Discounts 15

USD

35

30

25

20

15

10

5

0

Date—Daily first 2 months 2008

Med

ian

Quo

ted

Dep

th (

$000

)

NT_NO

USDCom<$5Warrant

Preferred

UnitCom>$5All

0102

0104

0108

0110

0114

0116

0118

0122

0124

0128

0130

0201

0205

0207

0211

0213

0215

0220

0222

0226

0228

Figure 1.2 Time-Series of Median Quoted Depths (in thousands of $)

8.00

7.00

6.00

5.00

4.00

3.00

2.00

1.00

0.00

Date—Daily first 2 months 2008

Med

ian

Rel

ativ

e E

ffec

tive

Spr

ead

(%)

NT_NOAllCom>$5Unit

Warrant

Warrant

Preferred

USD

USD

Com>$5

0102

0104

0108

0110

0114

0116

0118

0122

0124

0128

0130

0201

0205

0207

0211

0213

0215

0220

0222

0226

0228

Figure 1.3 Time-Series of Relative Effective Spreads (%)

16 Part i EXECUTION A ND MOMENTUM TR ADING

12

10

8

6

4

2

0

2

Date—Daily first 2 months 2008

Med

ian

Rel

ativ

e R

ealiz

ed S

prea

d (%

)

NT_NOAll; Com>$5;Unit; Preferred

Warrant

USD

USD

USD

Com>$5

0102

0104

0108

0110

0114

0116

0118

0122

0124

0128

0130

0201

0205

0207

0211

0213

0215

0220

0222

0226

0228

Figure 1.4 Time-Series of Relative 30-Minute Post-Realized Spreads (%)

180

160

140

120

100

80

60

40

20

0

Date—Daily first 2 months 2008

Med

ian

Vo

lum

e ($

000)

NT_NO

Com>$5Unit

Unit

WarrantUSD

Com<$5

0102

0104

0108

0110

0114

0116

0118

0122

0124

0128

0130

0201

0205

0207

0211

0213

0215

0220

0222

0226

0228

Preferred

All

Figure 1.5 Time-Series of Dollar Volume (in thousands of $)

and Warrants for ES and RS30. The security types with the largest QD ($)sigmas are NT_NO followed by USD and Preferreds, and with the largestQD ($), CVs are USD followed by Warrants and NT_NO. The securitytypes with the largest $ Vol sigmas are NT_NO followed by Units andUSD, and with the largest $ Vol CVs are NT_NO followed by USD andWarrants. The security types with the largest Nb_trade sigmas are Unitsfollowed by USD and Common $5, and with the largest Nb_trade CVsare USD followed by NT_NO and Preferreds.

Thus, Common $5 never appear and Common $5 only appears oncein the top three ranks for intertemporal variation for all six depicted liquidity measures. Units appear in the top three ranks for intertermporalvariation for only the two trade-activity measures of liquidity. WhileNT_NO has relatively low spreads and high quoted depths compared withthe other security types, it has relatively lower trade-activity measures ofliquidity and relatively higher intertemporal variation for all six liquiditymeasures.

chapter 1 Performance Leakage and Value Discounts 17

25

20

15

5

0

10

Date—Daily first 2 months 2008

Num

ber

of T

rade

s

NT_NO

Com>$5;Com<$5

Unit

Warrant

USD

0102

0104

0108

0110