The Geography of International Portfolio Flows ...

51

The Geography of International Portfolio Flows, International CAPM, and the Role of Monetary Policy Frameworks ∗ Roberto A. De Santis European Central Bank Using bilateral data on international equity and bond flows, we find that (i) the prediction of the International Capital Asset Pricing Model is partially met and that global equity markets might be more integrated than global bond markets, and (ii) asset allocators engage in trend-chasing activities, par- ticularly in bond markets. Moreover, over the turbulent 1998– 2001 period characterized by an equity bubble and the subse- quent burst, we find evidence that investors preferred portfolio assets of countries where the central bank gave relative impor- tance to money. As for EMU, once controlling for diversifica- tion benefits and the elimination of the exchange rate risk, we show that cross-border portfolio flows among euro-area coun- tries have increased due to the catalyst effect of EMU. Coun- tries’ shares in the world market portfolio, home bias, initial degree of misallocation across countries, past returns, diversi- fication benefits, and EMU can explain 35–40 percent of the total variation in equity and bond asset flows. JEL Codes: C13, C21, F37, G11. 1. Introduction The International Capital Asset Pricing Model (IntCAPM) suggests that international investors should hold assets of each country in ∗ The views expressed in this paper are those of the author and do not nec- essarily reflect those of the European Central Bank or the Eurosystem. Author Contact: European Central Bank, Kaiserstrasse 29, 60311 Frankfurt am Main, Germany. E-mail: roberto.de [email protected]; Tel: +49-69 1344 6611. 147

Transcript of The Geography of International Portfolio Flows ...

The Geography of International PortfolioFlows, International CAPM, and the Role of

Monetary Policy Frameworks∗

Roberto A. De SantisEuropean Central Bank

Using bilateral data on international equity and bond flows,we find that (i) the prediction of the International CapitalAsset Pricing Model is partially met and that global equitymarkets might be more integrated than global bond markets,and (ii) asset allocators engage in trend-chasing activities, par-ticularly in bond markets. Moreover, over the turbulent 1998–2001 period characterized by an equity bubble and the subse-quent burst, we find evidence that investors preferred portfolioassets of countries where the central bank gave relative impor-tance to money. As for EMU, once controlling for diversifica-tion benefits and the elimination of the exchange rate risk, weshow that cross-border portfolio flows among euro-area coun-tries have increased due to the catalyst effect of EMU. Coun-tries’ shares in the world market portfolio, home bias, initialdegree of misallocation across countries, past returns, diversi-fication benefits, and EMU can explain 35–40 percent of thetotal variation in equity and bond asset flows.

JEL Codes: C13, C21, F37, G11.

1. Introduction

The International Capital Asset Pricing Model (IntCAPM) suggeststhat international investors should hold assets of each country in

∗The views expressed in this paper are those of the author and do not nec-essarily reflect those of the European Central Bank or the Eurosystem. AuthorContact: European Central Bank, Kaiserstrasse 29, 60311 Frankfurt am Main,Germany. E-mail: roberto.de [email protected]; Tel: +49-69 1344 6611.

147

148 International Journal of Central Banking June 2010

proportion to the country’s share in the world market portfolio.1

This implies that all countries, in a world without transaction andinformation costs, would hold the same portfolio and would diver-sify their investment in other countries in proportion to the size oftheir financial markets. In this respect, global indices such as thepopular Morgan Stanley Capital International (MCSI) All CountryWorld Index (ACWI), Datastream Global index, and Standard andPoor’s (S&P’s) Global index are widely used by investors as theirperformance benchmarks for the global asset portion of their equityportfolio. The first aim of this paper is to examine whether countriesallocate money according to the simple prediction of the IntCAPM.We also assess the empirical relevance of the IntCAPM for the bondmarket. In order to carry out this test, we employ the Lehman Broth-ers Multiverse index released in 2001 as the benchmark for the globalbond market.

It is useful to point out that recent studies have looked at the con-temporaneous link between the actual weight of country j in fundi’s equity portfolio and the optimal weight suggested by the Int-CAPM for emerging markets (Gelos and Wei 2005). We instead aimat investigating whether portfolio flows (divided by the size of theinvestors) and, therefore, the global reallocation of portfolio capitalacross twenty-three developed countries and seven emerging-marketeconomies are functions of the optimal weights at the beginning ofthe period as suggested by the IntCAPM.

In order to carry out such a study, we construct a database onbilateral cross-border equity and bond flows for thirty countries cov-ering in 2001 80 percent of world GDP, 84 percent of world inter-national investment in equity portfolios, and 71 percent of worldinternational investment in bonds and notes portfolios. Therefore,the thirty countries of the sample and the cross-section of 870 bilat-eral observations encompass all important international investmentdecisions (excluding official investments by monetary authorities).

Specifically, we construct measures of bilateral net asset flows ofequities and bonds mainly on the basis of the International Monetary

1The International Capital Asset Pricing Model and the Intertemporal AssetPricing Model are often referred to using the same label: I-CAPM. We useIntCAPM to avoid confusion.

Vol. 6 No. 2 The Geography of International Portfolio Flows 149

Fund (IMF) Coordinated Portfolio Investment Survey (CPIS) data-base, which reports bilateral holdings at end-1997 and end-2001. Wedefine net asset flows of equities and bonds as the purchases minusthe sales of country k’s equities and bonds by citizens of country c.The considered period was characterized by the sharp rise in cross-border capital flows globally, the increased percentage of householdsavings invested in capital markets, the boom and bust of the equitybubble, and the establishment of European Economic and MonetaryUnion (EMU) in January 1999. Looking at cumulated portfolio netasset flows over the four-year period 1998–2001 has the advantageof abstracting from short-run variations in international portfolioflows, which could be due to unexpected economic news and cyclicaldevelopments, as well as phenomena which are difficult to pin down.

The second aim of the paper is to assess whether, during thisturbulent period for asset markets, central banks’ monetary pol-icy frameworks across countries influenced the geography and sizeof international capital flows.2 As a consequence of the asset-priceshocks, international investors might have preferred to reallocatetheir portfolio assets toward countries that gave importance to spe-cific characteristics of monetary policy frameworks. Therefore, weemploy the results of a survey commissioned and coordinated by theBank of England in 1998 aiming at measuring several key charac-teristics of the monetary frameworks consistently across ninety-fourcentral banks (Mahadeva and Sterne 2000). Moreover, given the newmonetary policy framework, which came to light in Europe in Janu-ary 1999, we also look and control for the potential impact of EMUon global portfolio flows as found by Lane (2006) for fixed-incomeinvestments and by De Santis and Gerard (2009) for both equityand fixed-income investments.

International portfolio flows have skyrocketed in the last fifteenyears, and a large number of studies have tried to explain their

2A large body of the literature pointed to the importance of institutionalcharacteristics of the monetary policy framework—such as central banks’ inde-pendence, accountability, and transparency—to control inflationary expectationsand safeguard financial stability (i.e., Rogoff 1985; Alesina and Summers 1993).Several measures of central banking independence were also constructed andused to study the impact on inflation (Grilli, Masciandaro, and Tabellini 1991;Cukierman 1992; Jacome and Vazquez 2005).

150 International Journal of Central Banking June 2010

determinants. However, data limitations have meant that these con-tributions focused on country aggregates of net equity and debt flows(De Santis and Luhrmann 2009), on country aggregates of inflowsof equity capital—foreign direct investment plus portfolio equitysecurities—(Alfaro, Kalemli-Ozcan, and Volosovych 2007), or haveonly considered a single source country, most often the United Statesbeing the recipient or the source of the investment (Bohn and Tesar1996; Brennan and Cao 1997; Coval and Moskowitz 1999; Froot,O’Connell, and Seasholes 2001; Huberman 2001; Ahearne, Griever,and Warnock 2004). Portes and Rey (2005) is the only study thatlooks at bilateral cross-border equity flows between fourteen coun-tries pointing to the role played by information costs. De Santis andGerard (2009) is the only study looking at the determinants of bilat-eral changes in portfolio country weights in both equity securitiesand fixed income for a panel of thirty countries pointing to the roleplayed by the non-linear fully hedged diversification benefits, the ini-tial degree of misallocation, and the establishment of EMU. Anotherbranch of the literature has studied the determinants of bilateralbank and portfolio holdings using empirical methods borrowed fromthe traditional gravity models of international goods trade (Faruqee,Li, and Yan 2004; Lane 2006; Aviat and Coeurdacier 2007; Lane andMilesi-Ferretti 2008; Papaioannou 2009).

Our main contribution to the literature is that we find clear evi-dence that portfolio asset flows are influenced positively by the rela-tive size of the recipient countries’ financial markets. The predictionsof the IntCAPM are only partially met, as the estimated coefficienton the benchmarks is less than unity: 0.4 for the equity portfolioand 0.2 for the bond portfolio. Moreover, we find that asset alloca-tors engage in trend-chasing activities, particularly in bond markets.These results do not change when controlling for home bias and theinitial degree of underweight, which enters non-linearly, thereforepotentially proxying for initial direct and indirect costs.

We also find that, during the turbulent 1998–2001 period, inter-national investors in both equity and fixed-income markets had atendency to purchase assets issued by countries whose monetaryauthorities gave importance to money.

We estimate on a 95 percent confidence interval the potential cat-alyst effect of the euro within the euro area to amount to USD 22–47billion in equity securities and USD 32–76 billion in bonds and notes,

Vol. 6 No. 2 The Geography of International Portfolio Flows 151

which implies that EMU might have enhanced risk sharing amongeuro-area member states. The catalyst effect of the euro is esti-mated after controlling for the elimination of the exchange rate riskamong euro-area member states and the effect of being a memberof the European Union (EU). EMU boosted the cross-border invest-ment activity among euro-area member states due to the removal ofintra-area currency-matching rules, the sharing of common tradingplatforms, and the cross-border merger of the Amsterdam, Brussels,Lisbon, and Paris exchanges (Euronext).

The proportion of the total variation explained by our empiricalmodels amounts to 35–40 percent for both equity and bond flows.This is a valuable result given that we look at the geography ofinternational portfolio flows during a very difficult period for assetmanagement.

The remainder of the paper is organized as follows. Section 2discusses the key ideas. Section 3 describes the databases used forthe analysis. Section 4 outlines the empirical approach and teststhe IntCAPM. Section 5 assesses the role of monetary policy frame-works and estimates the potential impact of EMU on portfolio flows.Section 6 reports how robust the model specifications are when con-trolling for other variables, which could potentially affect portfolioflows. Section 7 concludes.

2. A Simple Theory

2.1 The IntCAPM

Consider a representative investor from a generic country c and letγc denote the investor’s degree of risk aversion. Also, indicate withμc the (N × 1)-vector of expected returns in excess of the risk-freerate on the N risky assets, and with Σc the expected (N × N)-covariance matrix for the risky assets, where the subscript c indi-cates that returns are measured in the currency of country c. If theinvestor faces no constraints on foreign holdings and financial mar-kets are perfectly integrated, mean-variance optimization implies thefollowing portfolio allocation:

w∗c,t =

1γc

Σ−1c,t μc,t,

152 International Journal of Central Banking June 2010

where w∗c,t is the (N × 1)-vector of optimal weights for the N risky

assets.The optimal weights are not observable. However, in a fully

integrated world where purchasing power parity (PPP) holds, Sol-nik (1974) and Sercu (1980) show that the international version ofthe simple CAPM of Sharpe (1964) and Lintner (1965) holds: themarket equilibrium is achieved when all investors hold the worldmarket portfolio, where each country portfolio is weighted by itsmarket capitalization. Therefore, an observable estimate of the opti-mal weight invested in each country k is equal to that country k’smarket capitalization weight in the world index portfolio, wBench

k,97 :

w∗c,t = wBench

k,t .

There exist several standard benchmarks for the equity portfolio,such as the popular MCSI ACWI, Datastream Global index, andS&P’s Global index, as they provide consistent data, have suffi-ciently long price history, and are widely used by global investors.We use the Datastream Global index and compare the results withS&P’s Global index, as both include the country coverage used inthis study.

To our knowledge, a similar benchmark for the bond portfoliofor such a number of countries was never used due to difficulty incompiling countries’ bond market capitalization at market value. InJanuary 2001, Lehman Brothers launched a new index (i.e., Multi-verse index), which provides a broad-based measure of the interna-tional fixed-income bond market, with index history dating back toJanuary 1999. Multiverse index provides information on the overallstatus of the global debt asset class and offers a means to comparethe entire global debt asset class across countries.

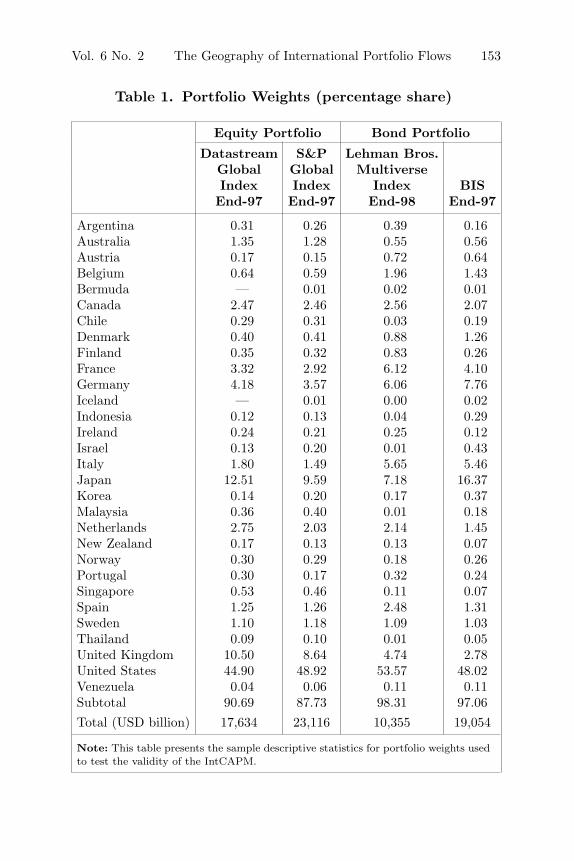

Table 1 provides the estimated market shares across countries inboth equity and bond markets, which will then be used to test theIntCAPM. The first and second columns report the equity portfolioweights computed using the market value of the Thomson Data-stream and S&P’s Global indices, respectively. The last two columnsreport, respectively, the bond portfolio weights computed using themarket value of the Lehman Brothers Multiverse index and the out-standing amount as reported by the Bank for International Settle-ments (BIS). The equity portfolio weights of Datastream and S&P

Vol. 6 No. 2 The Geography of International Portfolio Flows 153

Table 1. Portfolio Weights (percentage share)

Equity Portfolio Bond Portfolio

Datastream S&P Lehman Bros.Global Global MultiverseIndex Index Index BISEnd-97 End-97 End-98 End-97

Argentina 0.31 0.26 0.39 0.16Australia 1.35 1.28 0.55 0.56Austria 0.17 0.15 0.72 0.64Belgium 0.64 0.59 1.96 1.43Bermuda — 0.01 0.02 0.01Canada 2.47 2.46 2.56 2.07Chile 0.29 0.31 0.03 0.19Denmark 0.40 0.41 0.88 1.26Finland 0.35 0.32 0.83 0.26France 3.32 2.92 6.12 4.10Germany 4.18 3.57 6.06 7.76Iceland — 0.01 0.00 0.02Indonesia 0.12 0.13 0.04 0.29Ireland 0.24 0.21 0.25 0.12Israel 0.13 0.20 0.01 0.43Italy 1.80 1.49 5.65 5.46Japan 12.51 9.59 7.18 16.37Korea 0.14 0.20 0.17 0.37Malaysia 0.36 0.40 0.01 0.18Netherlands 2.75 2.03 2.14 1.45New Zealand 0.17 0.13 0.13 0.07Norway 0.30 0.29 0.18 0.26Portugal 0.30 0.17 0.32 0.24Singapore 0.53 0.46 0.11 0.07Spain 1.25 1.26 2.48 1.31Sweden 1.10 1.18 1.09 1.03Thailand 0.09 0.10 0.01 0.05United Kingdom 10.50 8.64 4.74 2.78United States 44.90 48.92 53.57 48.02Venezuela 0.04 0.06 0.11 0.11Subtotal 90.69 87.73 98.31 97.06Total (USD billion) 17,634 23,116 10,355 19,054

Note: This table presents the sample descriptive statistics for portfolio weights usedto test the validity of the IntCAPM.

154 International Journal of Central Banking June 2010

are very similar. Some small differences can be identified for the bondportfolio weights mainly due to the fact that the Lehman BrothersMultiverse index is evaluated at market value, while the BIS bondoutstanding is at face value.

The computations reported in table 1 indicate that accordingto the IntCAPM, almost 50 percent of world portfolio should beinvested in U.S. securities. As for the euro area (e.g., Luxembourgand Greece), approximately 14 percent of world portfolio should beinvested in euro-area equity securities and 25 percent in euro-areabonds.

We will report the empirical results using Datastream weights forequity portfolio and Lehman Brothers weights for bond portfolio.3

It is useful to point out that all the results remain invariant whenusing, respectively, S&P weights and BIS weights.

2.2 The Role of Central Banks

There is no doubt that capital flows are affected by the institutionsof a country (Alfaro, Kalemli-Ozcan, and Volosovych 2007; Coeur-dacier, De Santis, and Aviat 2009; De Santis and Luhrmann 2009).However, there is no empirical study looking at the role of centralbanking institutional setting. Surely, monetary policy influences thedecisions of international investors, but less obvious is understand-ing why specific central bank monetary policy characteristics shouldaffect international investment decisions. Moreover, at the turn ofthe century, as a consequence of the asset-price shocks, internationalinvestors might have preferred to reallocate their portfolio assetstoward countries that gave importance to specific characteristics ofmonetary policy frameworks.

Therefore, we employ the results of a comprehensive survey com-missioned by the Bank of England in 1998, because it aimed atmeasuring consistently the diversity in monetary frameworks acrossninety-four central banks with a coverage of characteristics thatstretched beyond previous studies (Mahadeva and Sterne 2000).Specifically, we look at the following characteristics: (i) short- and

3The employed portfolio weights for Bermuda and Iceland amount to 0.01percent as indicated by S&P’s Global index.

Vol. 6 No. 2 The Geography of International Portfolio Flows 155

medium-term policy focus—inflation, money, exchange rate, and dis-cretionary policy; (ii) institutional characteristics—independence,accountability, and transparency of policy explanations; and (iii)structural characteristics—importance given to financial stability inthe setting of monetary policy instruments.

Central bank independency is defined by a range of character-istics covering legal objectives, goal, instruments, finance of thegovernment deficit, and term of office of the governor.

The measure of accountability was constructed by assessing howfar the central bank has a legal or informal responsibility to explainand defend its policies to government and parliament and to involveparliament in monetary policy decisions. Therefore, the measurerelates to accountability to a specific target as well as to govern-mental and parliamentary monitoring of the central bank.

The measure of policy explanations is defined by the effortmade by the central bank in explaining policy decisions, assess-ment of the economy, and forecasts and forward-looking analy-sis. It can be interpreted as one aspect of transparency in thatdeeper explanations of policy, which allow us to understand itsgoal and the means by which policymakers react to changes in eco-nomic conditions, is one important manifestation of higher degree oftransparency.

As for the measures of monetary policy objectives, they aredefined and classified by the exchange rate, money growth, andinflation dimensions, rather than just one dimension, and give thedegree to which a country’s policy focused on a particular objective.Therefore, the survey is constructed to avoid a 100 percent commit-ment to a single objective, as in most cases definitions that focus onthe explicit variable targeted may not fully capture policy prefer-ences. The general measure of discretion is a non-linear combinationof the scores for exchange rate focus, money focus, and inflationfocus.

Finally, the importance of financial stability in the monetaryframework is defined by various financial stability issues, such asthe volatility of asset prices, domestic and overseas financial sectorinsolvency, and credit rationing.

The eight indices range between 0 and 100, where a high scoreimplies more independence, more accountability of central bank togovernment, more policy explanations to those outside the central

156 International Journal of Central Banking June 2010

bank, and a higher degree of importance given to policy objectivesand financial stability issues (see table 2).4

Some of these indices are also strongly correlated (see table 3).The focus on the exchange rate is strongly correlated with the focuson inflation and money, with the transparency index, and with theimportance given to financial stability; in turn, the focus on moneyis strongly correlated with the importance of financial stability.

Interestingly, independence and accountability are negativelycorrelated (−20 percent), which implies that explaining and defend-ing monetary policies to government and parliament and the involve-ment of parliament in monetary policy decisions might be partly seenby central banks as an infringement on their independence.

2.3 The Role of EMU

The establishment of EMU in January 1999 was a fundamentalinstitutional change in the world economy that has affected thedirection and the magnitude of global portfolio flows. Lane (2006)and De Santis and Gerard (2009) uncover evidence of euro-areainvestors having assigned a higher weight to portfolio investmentin euro-area countries, which implies that EMU has facilitatedportfolio market access, enhancing risk sharing and regional finan-cial integration. EMU boosted the cross-border investment activityamong euro-area member states due to the removal of intra-areacurrency-matching rules, the sharing of common trading platforms(such as the MTS model composed of several national Europeanmarkets for trading fixed-income securities),5 and the cross-bordermerger of the Amsterdam, Brussels, Lisbon, and Paris exchanges(Euronext).

In most countries, portfolio funds are often subject to someform of restriction on the level of their non-domestic investment.

4For a comprehensive analysis on the construction of all the indices measuringthe monetary policy frameworks across countries, refer to chapter 4 of Mahadevaand Sterne (2000). Bermuda and Venezuela are not included in the survey. There-fore, we use the U.S. characteristics for Bermuda, as the Bermuda dollar is atpar with the U.S. dollar, and we use the Uruguay characteristics for Venezuelagiven the similarities of the monetary policy frameworks of these two countries(see Jacome and Vazquez 2005).

5Detailed information can be found at http://www.mtsgroup.org/.

Vol. 6 No. 2 The Geography of International Portfolio Flows 157

Tab

le2.

Sam

ple

Des

crip

tive

Sta

tist

ics

for

the

Char

acte

rist

ics

ofth

eM

onet

ary

Pol

icy

Fra

mew

ork

Str

uct

ura

lPol

icy

Focu

sIn

stit

uti

onal

Fac

tors

Fac

tor

Exch

ange

Fin

anci

alIn

flat

ion

Mon

eyR

ate

Dis

cret

ion

Indep

enden

ceA

ccou

nta

bility

Tra

nsp

aren

cySta

bility

Arg

enti

na0

010

00

7910

053

58A

ustr

alia

940

06

7383

788

Aus

tria

00

8813

6867

2717

Bel

gium

00

946

7733

688

Ber

mud

a19

250

8492

8395

33C

anad

a88

06

1691

100

7933

Chi

le88

031

2893

1783

17D

enm

ark

00

946

8875

700

Fin

land

560

6366

9192

748

Fran

ce40

4658

8490

8353

50G

erm

any

1988

1329

9617

7033

Icel

and

190

7534

5992

658

Indo

nesi

a50

636

6656

8383

83Ir

elan

d19

075

3487

8378

8Is

rael

880

1319

6610

068

33It

aly

4444

5094

8858

8133

Japa

n50

00

5093

089

50K

orea

6375

659

7383

8858

(con

tinu

ed)

158 International Journal of Central Banking June 2010

Tab

le2.

(Con

tinued

)

Str

uct

ura

lPol

icy

Focu

sIn

stit

uti

onal

Fac

tors

Fac

tor

Exch

ange

Fin

anci

alIn

flat

ion

Mon

eyR

ate

Dis

cret

ion

Indep

enden

ceA

ccou

nta

bility

Tra

nsp

aren

cySta

bility

Mal

aysi

a44

038

7585

8371

67N

ethe

rlan

ds0

088

1391

8379

8N

ewZea

land

940

06

8910

092

8N

orw

ay0

069

3157

5089

17Por

tuga

l6

075

2885

8378

33Si

ngap

ore

190

5653

9025

4917

Spai

n56

063

6680

8359

33Sw

eden

100

013

697

8395

42T

haila

nd31

66

7582

5067

83U

nite

dK

ingd

om10

00

00

7710

094

16U

nite

dSt

ates

1925

084

9283

9533

Ven

ezue

la25

088

2570

834

17

Note

s:T

his

table

pre

sent

sth

esa

mple

des

crip

tive

stat

isti

csfo

rth

ech

arac

teri

stic

sof

the

mon

etar

ypol

icy

fram

ewor

k(s

eeM

ahad

eva

and

Ste

rne

2000

,pp.14

1–62

).T

he

eigh

tin

dic

esra

nge

bet

wee

n0

and

100,

wher

ea

hig

hsc

ore

implies

mor

ein

dep

enden

ce,m

ore

acco

unt

ability

togo

vern

men

ts,m

ore

pol

icy

expla

nat

ions

toth

ose

outs

ide

the

cent

ralban

k,an

da

hig

her

deg

ree

ofim

por

tance

give

nto

pol

icy

obje

ctiv

esan

dfinan

cial

stab

ility

issu

es.

Vol. 6 No. 2 The Geography of International Portfolio Flows 159

Tab

le3.

Cor

rela

tion

Mat

rix

ofth

eSta

teof

Dev

elop

men

t,Q

ual

ity

ofth

eIn

stitution

s,an

dM

onet

ary

Fra

mew

orks

Var

iable

s

Dev

elopm

ent

Qual

ity

ofth

eIn

stit

uti

ons

Monet

ary

Policy

Fra

mew

ork

s

GP

BC

RD

CL

LP

ICP

CIN

FM

ON

FX

DIS

IND

AC

CT

RA

FS

GP

1.00

BC

0.29

1.00

RD

0.66

0.32

1.00

CL

−0.

65−

0.09

−0.

451.

00LP

0.87

0.31

0.67

−0.

651.

00IC

0.78

0.08

0.42

−0.

540.

791.

00P

C0.

710.

020.

53−

0.58

0.85

0.77

1.00

INF

−0.

17−

0.08

0.18

−0.

01−

0.01

−0.

180.

151.

00M

ON

−0.

100.

030.

100.

17−

0.17

−0.

27−

0.35

−0.

051.

00FX

0.08

−0.

44−

0.24

−0.

070.

010.

300.

01−

0.68

−0.

321.

00D

IS−

0.15

0.32

−0.

090.

30−

0.20

−0.

22−

0.37

−0.

120.

44−

0.21

1.00

IND

0.21

0.39

0.29

−0.

240.

370.

400.

370.

120.

06−

0.21

0.16

1.00

AC

C−

0.10

−0.

37−

0.02

−0.

19−

0.04

−0.

230.

080.

26−

0.19

0.03

−0.

12−

0.20

1.00

TR

A0.

280.

370.

34−

0.31

0.31

0.12

0.27

0.37

0.12

−0.

600.

080.

280.

021.

00FS

−0.

580.

23−

0.26

0.56

−0.

61−

0.70

−0.

720.

090.

42−

0.38

0.49

−0.

02−

0.05

0.07

1.00

Note

s:T

heva

riab

lesof

this

tabl

ear

ela

bel

edas

follo

ws:

GP

=C

ount

ries

’GD

Pper

capi

tam

inus

the

GD

Pper

capi

taof

Nor

way

;BC

=B

ank

cred

itto

the

priv

ate

sect

or/G

DP

min

usw

orld

shar

e;R

D=

R&

Dex

pen

ditu

re/G

DP

min

usw

orld

shar

e;C

L=

Civ

illib

erti

esin

dex;

LP

=La

Por

tain

dex;

IC=

ICR

Gin

dex;

PC

=Per

ceiv

edco

rrup

tion

inde

x;IN

F=

Infla

tion

focu

sin

dex;

MO

N=

Mon

eyfo

cus

inde

x;FX

=E

xcha

nge

rate

focu

sin

dex;

DIS

=D

iscr

etio

nfo

cus

inde

x;IN

D=

Inde

pen

denc

ein

dex;

AC

C=

Acc

ount

abili

tyin

dex;

TR

A=

Tra

nspa

renc

yin

dex;

FS

=R

ole

offin

anci

alst

abili

tyin

dex.

160 International Journal of Central Banking June 2010

Currency-matching rules for portfolio funds, for example, are set toensure that foreign currency risk is reduced. Since the introductionof the euro in January 1999, the intra-euro-area currency-matchingrule has shifted from national currencies to the euro. The resultinggreater flexibility allowed individual euro-area country portfolios tosecure better diversification of investment risk by purchasing morenon-domestic euro-area assets.6

To control for the effect of EMU on global capital flows as wellas to measure its average impact, we include two sets of binary vari-ables. First we include a dummy which takes the value of 1 if thecountry receiving the investment belongs to the EMU. The coeffi-cient of this dummy measures the average portfolio asset flow intoindividual EMU countries for all investors. However, the effect of thesingle currency may be more pronounced on the investment decisionsof investor-residents in the euro area. To control for this differentialeffect, we include a dummy variable which takes the value of 1 whenboth investing and receiving countries belong to the EMU. The coef-ficient of this dummy measures the average portfolio asset flow intoindividual euro-area countries for all euro-area investors that comesin addition to the average flow observed for all investors. Accord-ingly, it quantifies the average financial integration effect of EMUfor the individual euro-area member state.7

6For example, Europe’s life insurance companies could not hold more than 20percent of their assets in foreign currencies unless they were matched by liabili-ties denominated in the same currency. As the vast majority of those liabilitieswere denominated in national currency, so were most of the assets. Quantitativerestrictions are also typical for pension funds. For a description of the restric-tions in the EU before EMU, see International Monetary Fund (1997, table 63,p. 213).

7A further complication comes from the role of the London market as a majorintermediary of foreign investments from and to the rest of the world. Due tothe large size and higher sophistication of the London markets, many investorschoose to make their foreign investments via the United Kingdom. For exam-ple, a Japanese investor may choose to select a British investment managerto invest in euro-area equities and bonds. The IMF data on portfolio holdingsreport an accurate country breakdown of bilateral investment, which tries to iden-tify the residence of the issuer. Nevertheless, since the city of London is a keyEuropean player, we control for that by including two additional dummies. Thefirst dummy takes a value of 1 if the receiving country is the United Kingdom.A second dummy takes the value of 1 if the investing country belongs to theEMU and the receiving country is the United Kingdom.

Vol. 6 No. 2 The Geography of International Portfolio Flows 161

3. Data: The Geography of International Portfolio Flows

The IMF Coordinated Portfolio Investment Survey (CPIS) databasereports the portfolio positions of international investors, excludingthe official holdings of monetary authorities disaggregated by regionsand instruments. More specifically, the CPIS data set provides ageographical breakdown of international portfolio holdings disag-gregated by three instruments—equity securities, long-term debtsecurities, and short-term debt securities—and includes virtually allmajor international investment, excluding foreign direct investment.An additional advantage of this data set is the consistency of thecompilation criteria:

• Participants undertake a benchmark portfolio asset survey atthe same time.

• Participants follow definitions and classifications that aremutually consistent by following the methodology set out inthe fifth edition of the IMF Balance of Payments Manual.

• All participants provide a breakdown of their stock of port-folio investment assets by the country of residency of thenon-resident issuer.

There are also several issues related to the CPIS database: (i)data on the rather poor countries is missing; (ii) coverage is incom-plete due to lack of important portfolio holders, such as Middle Eastcountries and China; (iii) several transactions are reported as con-fidential for offshore financial centers and emerging markets; (iv)liabilities are bigger than assets, pointing toward underreporting;and (v) collection methods differ from country to country, which isan issue particularly for identifying the nationality and/or institu-tional type of the investor. However, we focus the analysis on themost important countries, which have a long experience in com-piling balance of payments data and international investment posi-tions, while at the same time encompassing all important interna-tional investment decisions. The exclusion of Middle East countries,China, and monetary authorities is desired, as they have been pur-chasing securities to control developments in the exchange rate orstrategic assets. Both objectives are not related to the mean-varianceoptimization.

162 International Journal of Central Banking June 2010

The CPIS database for the year 1997 covers twenty-nine of thelargest economies in the world, nine of which belong to the euroarea—Austria, Belgium, Finland, France, Ireland, Italy, Nether-lands, Portugal, and Spain; the three old EU member states butnot members of the euro area—Denmark, Sweden, and the UnitedKingdom; another ten developed countries—Australia, Bermuda,Canada, Iceland, Israel, Japan, New Zealand, Norway, Singapore,and the United States; four Asian emerging markets—Indonesia,Korea, Malaysia, and Thailand; and three Latin American emergingmarkets—Argentina, Chile, and Venezuela. Germany did not reportdata in 1997, but did so in 2001. Since Germany is a key euro-areamember and its international portfolio holdings are substantial, weused an annual database on international investment positions fromthe Bundesbank to derive the geographical allocation of equities andbonds and notes positions abroad held by German residents at end-1997. Specifically, we use the Bundesbank 1997 and 2001 recordsand adjust all the 1997 positions consistently (including exchangerate movements) to make them comparable to the 2001 holdingsrecorded in the CPIS. In all, we employ a matrix formed by thirtycountries (that is 870 observations). However, we excluded from thedatabase the investing countries that allocated explicitly to specificreceiving countries less than 75 percent of their international port-folio either in 1997 or in 2001, or those countries that held less than100 million in U.S. dollars in their international portfolio in 1997or in 2001. In other words, we opted for excluding from the cross-section analysis economies that reported undetermined investmentpositions vis-a-vis the countries in the sample.8

The change in foreign holdings from end-1997 to end-2001 couldbe due to capital gains, exchange rate changes, portfolio trans-actions, and other adjustments (i.e., reclassification). Under thehypothesis that cross-border other adjustments are relatively neg-ligible, the actual portfolio flows from the investing country c tothe receiving country k over the period 1998–2001, Tck,t, can becomputed using the IMF data model widely employed in the field of

8We excluded the investment of Argentina, Indonesia, Israel, Thailand, andVenezuela from the equity holdings database and the investment of Iceland, Israel,and New Zealand from the long-term debt instrument holdings database. How-ever, in doing so, we simply lose, respectively, 0.05 percent and 0.20 percent ofallocated global equity and bond holdings.

Vol. 6 No. 2 The Geography of International Portfolio Flows 163

balance of payments, international investment positions, and exter-nal debt statistics:9

Tck,t =(

Invc,k,01

ek,01pk,01− Invc,k,97

ek,97pk,97

)ek,tpk,t

=[

Invc,k,01

(1 + xk,t) (1 + rk,t)− Invc,k,97

]ek,tpk,t

ek,97pk,97,

where Invc,k is the amount invested by country c in country k financialassets and held in country c currency; ek and pk are, respectively, theexchange rate (i.e., country c currency per unit of country k currency)and the asset price in country k financial assets at the end of 1997and at the end of 2001; xk,t and rk,t are, respectively, the change inthe exchange rate and the total asset return over the four-year period;and ek,t and pk,t are, respectively, the average exchange rate and theaverage asset price over the same period. This approach implies thattransactions are assumed to occur uniformly over the period 1998–2001. However, it facilitates the computation of the bilateral cross-border portfolio flows, as they do not depend on the choice of the priceindices’ base year.

As for the exchange rate adjustments, one should note that mostof the global portfolio allocation is in U.S. dollars and euros. Accord-ing to a subtotal of thirteen countries used in this study, 75 percentof equity portfolio and 80 percent of long-term debt portfolio are heldin these two currencies. International investors also held less than10 percent of their portfolios in British pounds and Japanese yen.Therefore, it would be a mistake to use local currencies in estimat-ing cross-border portfolio flows. Moreover, London is a key Europeanfinancial center generally issuing European assets in euros. Since theJapanese yen depreciated by only 1 percent against the U.S. dollarover the 1998–2001 period, and given the lack of a disaggregated cur-rency and geographical breakdown of portfolio holdings, a potentialalternative is to assume that all assets issued by European countriesare issued in euros, while all assets issued by non-European coun-tries are issued in U.S. dollars. This assumption finds its support inthe European Central Bank’s studies on the international role of theeuro, which point out that (i) the use of the euro in international

9See Committeri (2000) for a comprehensive analysis.

164 International Journal of Central Banking June 2010

markets has a strong regional dimension, as it is focused on countriesand financial centers geographically close to the euro area, and (ii)the city of London plays a pivotal role regarding the use of the eurooutside the euro area (European Central Bank 2003).

Table 4 reports the estimated cross-border portfolio flows aggre-gated for the thirty countries in the sample and the aggregate cumu-lated figures reported by the International Financial Statistics (IFS)of the IMF over the same period. The estimated flows and the IFSfigures are not directly comparable, as important countries such asoffshore centers and several Asian and Latin American countries arenot included in the CPIS database. Moreover, the cross-border flowsof debt instruments reported by the IFS include official flows frommonetary authorities and are the sum of bond and money marketinstrument flows. For example, the estimated foreign capital flows inU.S. long-term debt securities amount to USD 173 billion, while theU.S. debt liabilities reported by the IFS, which include the flows offoreign monetary authorities and offshore centers, amount to USD869 billion. However, it is useful to point out that the reserve assetsof Japan, China, and Southeast Asian countries increased by approx-imately USD 450 billion over the 1998–2001 period, and it is gener-ally agreed that the Asian monetary authorities purchased mostlyU.S. Treasury securities. It is also generally believed that monetaryauthorities might have a different profit-maximizing behavior thanprivate investors. Hence, the exclusion of their investment decisions,which is implicit when using the CPIS database, is cardinal to testthe IntCAPM.

Although differences for individual transactions clearly exist,the cross-section is acceptable. In fact, the correlation coefficientsbetween the estimated and the IFS figures amount to 95 percentand 88 percent on the asset side of equity and bond securities, andto 90 percent and 78 percent on their respective liability side.

The aggregate results for four country groupings show that port-folio flows of euro-area member states were substantially largercompared with other regions, particularly in the bond market (seetable 5). A deeper inspection of the data reveals, first, that allregions of the world purchased euro-area assets over the period 1998–2001 (see figure 1). Second, intra-euro-area allocation was extremelyhigh. The portfolio transactions among euro-area member statesamounted to USD 315 billion in equity securities and USD 754

Vol. 6 No. 2 The Geography of International Portfolio Flows 165

Tab

le4.

Est

imat

edan

dIF

SPor

tfol

ioFlo

ws

by

Cou

ntr

y,19

98–2

001

(USD

Million

s)

Est

imat

edU

sing

CP

IS(T

hir

tyC

ountr

ies)

IFS

(All

Countr

ies)

Equity

Bonds

Equity

Deb

tIn

stru

men

ts

Ass

etLia

bility

Ass

etLia

bility

Ass

etLia

bility

Ass

etLia

bility

Countr

ies

(1a)

(2a)

(3a)

(4a)

(1b)

(2b)

(3b)

(4b)

Arg

enti

na72

18−

1155

0−

156

−35

509

3057

−14

178

1894

9046

Aus

tral

ia26

894

−44

9742

10−

5550

2133

528

269

1391

934

153

Aus

tria

1694

6−

1668

2993

147

256

2591

220

3452

613

8933

0B

elgi

um32

027

1144

467

878

4369

4N

AN

AN

AN

AB

erm

uda

−28

958

5757

420

7724

9N

AN

AN

AN

AC

anad

a66

765

−11

080

−28

79−

2338

887

687

4631

810

347

7349

Chi

le17

39−

2394

1403

3372

6646

024

6043

58D

enm

ark

2310

5−

605

1212

6−

2865

2446

431

8423

611

2012

2Fin

land

1642

346

761

2649

3−

3564

1994

332

284

3017

682

33Fr

ance

9688

695

292

2045

0415

9606

9693

113

0205

3181

0128

6335

Ger

man

y16

8440

8782

316

6482

1963

1931

2046

1344

1131

7931

3735

99Ic

elan

d12

0212

461

1197

1340

6914

228

36In

done

sia

215

2845

6−

4435

NA

−57

320

−92

Irel

and

8789

444

127

1071

9926

771

1166

3724

8967

2273

3640

136

Isra

el11

1933

9729

9914

4814

3069

6635

86−

94It

aly

1031

3217

1214

2121

7951

1768

7172

1517

8246

2957

27Ja

pan

3070

310

8697

8991

8−

7570

7740

315

7815

3623

9413

3065

Sout

hK

orea

111

2226

0−

2066

−34

398

1201

3928

855

58−

5681

Mal

aysi

a−

401

−77

73−

9−

6245

NA

NA

028

3

(con

tinu

ed)

166 International Journal of Central Banking June 2010

Tab

le4.

(Con

tinued

)

Est

imat

edU

sing

CP

IS(T

hir

tyC

ountr

ies)

IFS

(All

Countr

ies)

Equity

Bonds

Equity

Deb

tIn

stru

men

ts

Ass

etLia

bility

Ass

etLia

bility

Ass

etLia

bility

Ass

etLia

bility

Countr

ies

(1a)

(2a)

(3a)

(4a)

(1b)

(2b)

(3b)

(4b)

Net

herl

ands

8077

180

545

1123

5518

3460

1255

7064

234

1648

4119

5377

New

Zea

land

2071

−33

2319

44−

1362

3482

−33

211

8715

34N

orw

ay31

222

2658

2908

393

1534

820

3296

3657

420

665

Por

tuga

l30

4137

4411

857

2483

550

8856

4220

095

2221

9Si

ngap

ore

9342

1591

630

799

8844

3446

127

3912

749

801

Spai

n40

517

2949

065

833

7951

863

973

4697

213

2118

1007

06Sw

eden

4350

3−

1246

319

732

−75

6259

076

1143

931

101

1182

1T

haila

nd−

7930

3320

8−

6708

NA

2486

505

−33

29U

nite

dK

ingd

om−

1075

334

4075

5939

873

361

1209

2239

1493

1885

4715

2808

Uni

ted

Stat

es28

4130

2331

16−

6828

017

3220

4315

0646

9311

3948

686

8766

Ven

ezue

la1

−12

50−

930

−13

873

1761

−17

863

2Tot

al11

3501

511

3501

510

9404

810

9404

818

6125

818

1491

421

7533

726

7070

5

Cor

r.C

oeffi

cien

t(1

):0.

95(2

):0.

91(3

):0.

88(4

):0.

78

Note

s:T

he

firs

tfo

ur

colu

mns

ofth

eta

ble

repor

tth

ere

sult

sof

the

esti

mat

ednet

asse

ttr

ansa

ctio

ns

over

the

cum

ula

ted

per

iod

1998

–200

1ag

greg

ated

for

the

thir

tyco

unt

ries

ofth

esa

mple

.T

he

last

four

colu

mns

repor

tth

eco

unt

ries

’eq

uity

and

deb

tflow

sov

erth

esa

me

per

iod

repor

ted

byth

eIF

Sdat

abas

eof

the

IMF.T

he

esti

mat

edan

dth

eIF

Sfigu

res

are

not

dir

ectl

yco

mpar

able

,as

offsh

ore

cent

ers,

seve

ralA

sian

and

Lat

inA

mer

ican

count

ries

,an

dth

eoffi

cial

flow

sof

mon

etar

yau

thor

itie

sar

enot

incl

uded

inth

eC

PIS

dat

abas

e.M

oreo

ver,

the

deb

tin

stru

men

tflow

sre

por

ted

byth

eIF

Sar

eth

esu

mof

bon

ds

and

mon

eym

arke

tin

stru

men

tflow

s.

Vol. 6 No. 2 The Geography of International Portfolio Flows 167

Tab

le5.

Est

imat

edan

dIF

SPor

tfol

ioFlo

ws

by

Reg

ions,

1998

–200

1(U

SD

Billion

s)

Est

imat

edfr

om

CP

IS(T

hir

tyC

ountr

ies)

IFS

(All

Countr

ies)

Equity

Bonds

Equity

Deb

tIn

stru

men

ts

Ass

etLia

bility

Ass

etLia

bility

Ass

etLia

bility

Ass

etLia

bility

Countr

ies

(1a)

(2a)

(3a)

(4a)

(1b)

(2b)

(3b)

(4b)

Ten

EM

U64

6.1

397.

691

4.0

975.

894

3.0

672.

014

41.5

1411

.7T

hree

Non

-EM

UE

U55

.933

1.0

91.3

62.9

204.

540

6.1

243.

318

4.8

Ten

Non

-EU

424.

540

2.6

89.9

156.

469

3.5

714.

548

0.4

1069

.1D

evel

oped

Seve

nE

mer

ging

8.6

3.9

−1.

1−

100.

111

.522

.410

.25.

2M

arke

tsTot

al11

35.0

1135

.010

94.0

1094

.018

61.3

1814

.918

05.1

2337

.6

Cor

r.C

oeffi

cien

t(1

):0.

99(2

):0.

96(3

):0.

97(4

):0.

84

Note

s:T

he

figu

res

repor

tth

epor

tfol

ioflow

sof

equity

and

fixe

d-inco

me

aggr

egat

edfo

rfo

ur

count

rygr

oupin

gs.T

he

ten

EM

Uco

unt

ries

are

Aust

ria,

Bel

gium

,Fin

land,

Fra

nce

,G

erm

any,

Irel

and,

Ital

y,N

ether

lands,

Por

tuga

l,an

dSpai

n.

The

thre

enon

-EM

UEU

count

ries

are

Den

-m

ark,

Sw

eden

,an

dth

eU

nit

edK

ingd

om.T

he

ten

non

-EU

dev

elop

edco

unt

ries

incl

ude

Aust

ralia,

Ber

muda,

Can

ada,

Icel

and,Is

rael

,Ja

pan

,N

ewZea

land,

Nor

way

,th

eU

nit

edSta

tes,

and

Sin

gapor

e.T

he

seve

nem

ergi

ng

mar

kets

are

Arg

enti

na,

Chile,

Indon

esia

,K

orea

,M

alay

sia,

Thai

land,

and

Ven

ezuel

a.T

he

firs

tfo

ur

colu

mns

ofth

eta

ble

repor

tth

ere

sult

sof

the

esti

mat

ednet

asse

ttr

ansa

ctio

ns

over

the

cum

ula

ted

per

iod

1998

–200

1ag

greg

ated

for

the

thir

tyco

unt

ries

ofth

esa

mple

.T

he

last

four

colu

mns

repor

tth

eco

unt

ries

’eq

uity

and

deb

tflow

sov

erth

esa

me

per

iod

repor

ted

byth

eIF

Sdat

abas

eof

the

IMF.T

he

esti

mat

edan

dth

eIF

Sfigu

res

are

not

dir

ectl

yco

mpar

able

,as

offsh

ore

cent

ers,

seve

ralA

sian

and

Lat

inA

mer

ican

count

ries

,an

dth

eoffi

cial

flow

sof

mon

etar

yau

thor

itie

sar

enot

incl

uded

inth

eC

PIS

dat

abas

e.M

oreo

ver,

the

deb

tin

stru

men

tflow

sre

por

ted

byth

eIF

Sar

eth

esu

mof

bon

dan

dm

oney

mar

ket

inst

rum

ent

flow

s.

168 International Journal of Central Banking June 2010

Figure 1. Changes in Non-Domestic Euro-AreaAssets by Region

Notes: Panel A reports the estimated portfolio net flows of EMU assets transactedby residents of region i over the period 1998–2001 aggregated for four country group-ings. Panel B reports the estimated flows relative to foreign assets held in region iover the average period 1998–2001. The ten EMU countries are Austria, Belgium,Finland, France, Germany, Ireland, Italy, Netherlands, Portugal, and Spain. Thethree non-EMU EU countries are Denmark, Sweden, and the United Kingdom.The ten non-EU developed countries include Australia, Bermuda, Canada, Iceland,Israel, Japan, New Zealand, Norway, Singapore, and the United States. The sevenemerging markets are Argentina, Chile, Indonesia, Korea, Malaysia, Thailand, andVenezuela.

Vol. 6 No. 2 The Geography of International Portfolio Flows 169

billion in bonds and notes (see figure 1A), which represent, respec-tively, 31 percent and 51 percent of the non-domestic equity andbond assets held on average by euro-area member states over theperiod 1998–2001 (see figure 1B).

Several transactions are not reported in the CPIS database. Thisimplies either a rational portfolio allocation decision of not investingor the desire of not reporting confidential transactions. Specifically,the zeros reported by countries with more than 75 percent of theirinternational portfolio allocated account for 6.7 percent and 16.6 per-cent in equity and bond portfolios, respectively. It is important tostress that the zero flows can still occur if there were no transactionsor if transactions just offset each other during the 1997–2001 period.Also, negative transactions can occur if countries disinvested in 2001relative to 1997. Such zero and negative flows are not truncated; theyremain part of the database. However, given the zero reporting forsome holding positions, we estimate the same model, excluding andincluding such transactions. As shown in various regressions, resultsare barely affected, partly suggesting that most of the zero holdingsare based on actual portfolio investment decisions.

4. The Empirical Approach: Testing the IntCAPM

In a fully integrated world where purchasing power parity (PPP)holds, Solnik (1974) and Sercu (1980) show that the internationalversion of the simple CAPM of Sharpe (1964) and Lintner (1965)holds. Moreover, the equilibrium is achieved when all investorshold the world market portfolio, where each country’s portfolio isweighted by its market capitalization. In this model, the optimalshare invested in each country k is equal to that country k’s marketcapitalization weight in the world index portfolio, wBench

k,97 .The IntCAPM predicts a coefficient on wBench

k,97 equal to unity.However, due to home bias, marginal and fixed transaction costs,asymmetric information, heterogeneous belief about market perfor-mance, and trend-chasing behavior, the prediction of the IntCAPMmight not hold. Therefore, first we regress bilateral portfolio flowsin equity and bond securities upon their respective benchmarks,wBench

k,97 . Next, we control for the degree of home bias, the non-lineardegree of misallocation at the beginning of the period, and assetperformance in the previous period. Specifically, we estimate thefollowing model:

170 International Journal of Central Banking June 2010

tck,t = α0 + α1wBenchk,97 + α2HBc,97 + α3ΔHBc,01

+ α4DW 3ck,97 + α5rk,t−1 + εt,

where tck,t denotes country c’s international transactions invested incountry k divided by country c’s average international holdings overthe 1998–2001 period; HBc,97 and ΔHBc,01 are country c’s degreeof home bias at the beginning of the period and its first differenceover the sample period; DWck,97 denotes the degree of underweightof country k assets in investor c’s portfolio at the beginning of theperiod; rk,t−1 is the total returns on country k’s market portfolioin the previous period; and εt is a well-behaved term for all otherdeterminants of portfolio asset flows.

Home bias on the part of an investor, HBc,t, is broadly definedas the tendency to invest more in domestic assets even though therisk is shared more effectively if foreign assets are held. We expectthat the higher the degree of home bias, the larger the benefits offurther cross-border investments and the stronger the incentives forinternational diversification. Hence, net portfolio flows should bepositively related to the degree of home bias at the beginning of theperiod (α2 > 0) and negatively related to its increase over the period(α3 < 0). An index that is generally used to measure home bias is 1minus the Foreign Asset Acceptance Ratio (FAAR).10 FAAR meas-ures the extent to which the share of foreign assets in an investor’sportfolio diverges from the share of foreign assets that would be heldin a “borderless” global portfolio. By this metric, home bias is higherthe lower FAAR is from unity. Specifically, FAAR is computed as theactual share of foreign assets in total country holdings, wf

c,t, dividedby the optimal share of foreign assets in the total country portfolio,1 − wBench

c,t . This implies that

HBc,t = 1 −wf

c,t

1 − wBenchc,t

.

Since this measure is investor specific, it also plays the role of countryc’s fixed effect.

10See, for example, International Monetary Fund (2005) and De Santis andGerard (2009).

Vol. 6 No. 2 The Geography of International Portfolio Flows 171

The degree of underweight, DWck, is defined as the differencebetween the optimal and actual share of country k assets in investorc’s portfolio. It is generally agreed that the higher the costs in a par-ticular foreign market, the more severely underweighted that countrywill be in the investor’s portfolio (Ahearne, Griever, and Warnock2004). Therefore, we use the initial degree of bilateral misallocationpartly to instrument the role played by direct and indirect costs andasymmetric information on bilateral cross-border asset transactions.The larger the initial difference between optimal and actual share,the stronger the incentive to learn about the country and to reducethe associated asset allocation costs in order to trade back to opti-mal weights, reducing the position when the actual weight exceedsthe optimal weight and increasing the investment in an asset whenit is underweighted. Since our data focus exclusively on the foreignholdings of each country, the optimal weight to be invested in coun-try k by country c is equal to country k’s market capitalization inthe world market index, excluding the investing country c. Then

DWck,97 = wBenchck,97 − wck,97,

where wBenchck,97 = wBench

k,97

1−wBenchc,97

and wck,97 = Invc,k,97∑k Invc,k,97

.Since rebalancing a portfolio entails both direct and indirect fixed

transaction costs, it is unlikely to take place when bilateral actualportfolio weights differ only slightly from bilateral optimal portfolioweights. Therefore, we introduce some non-linearities by taking thecube of this measure. We expect that the degree of underweight atthe beginning of the period affects non-linearly and positively thegeography of portfolio flows (α4 > 0).11

11Ahearne, Griever, and Warnock (2004) and Portes and Rey (2005) pointedout that direct and indirect costs, such as information costs, to trade assets ina particular foreign market are key reasons why that country is more severelyunderweighted in the investor’s portfolio. While these factors undoubtedly influ-ence firms’ decisions about where to invest, a comprehensive evaluation of thismotivation is well beyond the scope of this paper, because we do not have meas-ures of bilateral cross-border fixed costs on equity and bond allocation, whichoften take the form of legal barriers and restrictive regulations. However, oncecontrolling for home bias, the initial non-linear degree of bilateral misalloca-tion could proxy at least partly the initial fixed costs on cross-border portfolioallocation.

172 International Journal of Central Banking June 2010

If portfolio decisions are based partly on past returns, theninvestors might tend to underweight countries whose stock marketshave performed poorly. Bohn and Tesar (1996) found that inter-national portfolio flows co-move with lagged measures of expectedreturns. This suggests that international investors engage in positive-feedback trading, also called “trend chasing.” To capture this type of“returns-chasing” behavior a la Bohn and Tesar, we use past returnsand expect α5 to be positive.

The results reported in table 6 indicate that wBenchk,97 is statisti-

cally significant, but its coefficient is less than unity: it is equal to0.4 for equities and 0.2 for bonds (see specification 1). A countrythat sees its market size increase by 1 percentage point relative tothe world market capitalization would attract international equity(bond) flows amounting to 0.4 percent (0.2 percent) of the equity(bond) assets held abroad by foreigners. The finding that the coeffi-cient on the bond benchmark is half that on the equity benchmarkmight imply that global equity markets are more integrated thanglobal bond markets.

The results do not change when we control for home bias (seespecification 2). On average, the decline in home bias in country cincreases international investment toward all destination countriesk in both models.

The results also do not change when we control for the non-lineardegree of underweight and past performance. Interestingly, the coef-ficient on DWck,97 is not statistically significant when taking thelinear measure (not reported). Conversely, it is strongly statisticallysignificant for the bond flow model when taking the non-linear meas-ure. One potential interpretation is the initial fixed-cost argumentdiscussed above. The willingness to close the initial gap betweenthe share of foreign assets that would be held in a “borderless”global portfolio and actual foreign investment weights is an impor-tant determinant of bond flows, as it raises the adjusted R2 by 7 per-centage points, from 14.6 percent in specification 2 to 21.9 percentin specification 3.

Finally, past performance in the destination country is statisti-cally significant for the equity and bond flow models (see specifi-cation 4a). While no prudent investor assumes future returns willmirror past returns, trend-chasing behaviors still characterize thegeography of international equity and bond flows in the long term.

Tab

le6.

Inte

rnat

ional

Por

tfol

ioA

sset

Flo

ws

and

IntC

AP

M

t ck

,t=

α0

+α

1w

Ben

chck

,97

+α

2H

Bc,9

7+

α3Δ

HB

c,0

1+

α4D

W3 ck

,97

+α

5r k

,t−

1+

ε t

Equity

Net

Ass

etFlo

ws

Bond

Net

Ass

etFlo

ws

Spec

if.1

Spec

if.2

Spec

if.3

Spec

if.4a

Spec

if.4b

Spec

if.1

Spec

if.2

Spec

if.3

Spec

if.4a

Spec

if.4b

Cst

0.00

5∗∗∗

−0.

036

−0.

036∗

−0.

039∗

∗−

0.03

8∗∗

0.01

2∗∗∗

−0.

011∗

∗−

0.01

1∗∗

−0.

023∗

∗∗−

0.01

7∗∗∗

(0.0

02)

(0.0

19)

(0.0

02)

(0.0

19)

(0.0

19)

(0.0

02)

(0.0

06)

(0.0

06)

(0.0

06)

(0.0

05)

wBen

chk

,97

0.42

7∗∗∗

0.42

5∗∗∗

0.44

9∗∗∗

0.44

1∗∗∗

0.44

7∗∗∗

0.19

0∗∗∗

0.19

3∗∗∗

0.23

3∗∗∗

0.23

2∗∗∗

0.23

4∗∗∗

(0.0

95)

(0.0

92)

(0.1

28)

(0.1

27)

(0.1

27)

(0.0

67)

(0.0

67)

(0.0

61)

(0.0

61)

(0.0

61)

HB

c,9

70.

038

0.03

80.

038

0.03

70.

015∗

∗0.

016∗

∗0.

017∗

∗0.

012∗

(0.0

24)

(0.0

24)

(0.0

24)

(0.0

23)

(0.0

08)

(0.0

08)

(0.0

08)

(0.0

08)

ΔH

Bc,0

1−

0.11

1∗∗∗

−0.

111∗

∗∗−

0.11

2∗∗∗

−0.

105∗

∗∗−

0.07

4∗∗∗

−0.

068∗

∗∗−

0.06

9∗∗∗

−0.

059∗

∗∗

(0.0

27)

(0.0

27)

(0.0

27)

(0.0

26)

(0.0

13)

(0.0

12)

(0.0

13)

(0.0

13)

DW

3 ck

,97

−0.

460

−0.

491

−0.

509

1.38

4∗∗∗

1.38

6∗∗∗

1.39

1∗∗∗

(1.1

49)

(1.1

47)

(1.1

46)

(0.2

85)

(0.2

82)

(0.2

84)

r k,t

−1

0.00

6∗∗∗

0.00

5∗∗∗

0.03

9∗∗∗

0.03

0∗∗∗

(0.0

02)

(0.0

02)

(0.0

07)

(0.0

06)

Adj

ust

edR

20.

283

0.31

50.

315

0.31

70.

319

0.10

40.

146

0.21

90.

235

0.23

7F

−S

tat

263.

5510

2.92

77.6

363

.06

68.9

274

.85

37.3

745

.65

40.1

549

.53

Note

s:T

his

table

repor

tsth

ere

sult

sof

the

cros

s-se

ctio

nal

regr

essi

onof

the

equity

and

bon

dnet

asse

tflow

s.T

he

expla

nat

ory

vari

able

sar

edes

crib

edin

appen

dix

1.T

he

sam

ple

size

for

spec

ifica

tion

s1–

4ais

n=

667

for

equity

flow

san

dn

=63

9fo

rbon

dflow

san

dex

cludes

all

zero

hol

din

gs.T

he

sam

ple

size

for

spec

ifica

tion

4bis

n=

725

for

equity

flow

san

dn

=78

3fo

rbon

dflow

san

din

cludes

allze

rohol

din

gs.O

LS,W

hit

ehet

eros

kedas

tici

ty-c

onsi

sten

tst

andar

der

rors

,an

dco

vari

ance

.Sta

ndar

der

rors

for

the

coeffi

cien

tsar

ere

por

ted

inpar

enth

eses

.**

*,**

,an

d*

den

ote

stat

isti

calsi

gnifi

cance

at1,

5,an

d10

per

cent

,re

spec

tive

ly.

174 International Journal of Central Banking June 2010

All in all, the proportion of the total variation explained by themodel is quite significant: 31.7 percent in equity flows and 23.5percent in bond flows.

The results are barely affected when treating the zero report-ing for some holding positions in the sample as actual portfolioinvestment decisions (see specification 4b).

5. Portfolio Flows, Monetary Policy Frameworks,and EMU

The second aim of the paper is to assess whether central banks’monetary policy frameworks across countries influenced the geog-raphy and size of international capital flows during the boom andbust of asset prices at the turn of the century. In this context wealso investigate the role of EMU on global portfolio reallocation.

5.1 The Impact of Monetary Policy Frameworks

We use the IntCAPM as our benchmark and add explanatory vari-ables describing key characteristics of monetary policy frameworksacross countries. Therefore, we estimate the following model:

tck,t = α0 + α1wBenchk,97 + α2HBc,97 + α3ΔHBc,01 + α4DW 3

ck,97

+ α5rk,t−1 + λ′Monk,t−1 + εt,

where the vector Monk,t−1 includes variables measuring the follow-ing characteristics of the monetary policy framework in country k:(i) the central bank’s objectives, such as the focus on inflation, onmoney, on the exchange rate, and on discretionary policy, (ii) thecentral bank’s institutional factors, such as independence, account-ability, and transparency, and (iii) the importance of financial stabil-ity in the setting of monetary policy instruments. Results reportedin table 7 are based on the sample that excludes the zero entrypositions. The results are the same when zero holding positions areincluded in the analysis (not reported; see also table 8).

Among the characteristics related to monetary policy, the focuson money played a significant and positive role in influencing thegeography of the portfolio flows. Given the link between asset pricesand credit growth (Borio and Lowe 2004; Detken and Smets 2004),

Vol. 6 No. 2 The Geography of International Portfolio Flows 175Tab

le7.

Inte

rnat

ional

Por

tfol

ioFlo

ws

and

Char

acte

rist

ics

ofM

onet

ary

Pol

icy

Fra

mew

orks

t ck,t

=α

0+

α1w

Ben

chk,9

7+

α2H

Bc,9

7+

α3Δ

HB

c,0

1+

α4D

W3 ck,9

7+

α5r k

,t−

1+

λ′ M

onk,t

−1

+ε t

Spec

if.

Expla

nat

ory

Equity

Flo

ws

Bon

dFlo

ws

Num

ber

Var

iable

Coeff

.s.

e.R

2C

oeff

.s.

e.R

2

Pol

icy

Focu

s

5In

flation

k,9

80.

004

(0.0

06)

0.31

7−

0.01

1∗∗

(0.0

04)

0.23

76

Mon

eyk,9

80.

021∗

∗∗(0

.007

)0.

322

0.06

2∗∗∗

(0.0

12)

0.28

67

Exc

hang

era

tek,9

8−

0.00

6(0

.006

)0.

309

0.00

5(0

.005

)0.

234

8D

iscr

etio

n k,9

80.

003

(0.0

07)

0.31

70.

010

(0.0

08)

0.23

6

Inst

itut

iona

lFa

ctor

s

9In

depe

nden

cek,9

80.

003

(0.0

14)

0.31

70.

046∗

∗∗(0

.016

)0.

240

10Acc

ount

abili

tyk,9

80.

006

(0.0

08)

0.31

7−

0.02

5∗∗∗

(0.0

09)

0.24

511

Tra

nspa

renc

y k,9

80.

006

(0.0

08)

0.31

7−

0.00

7(0

.006

)0.

234

Stru

ctur

alFa

ctor

sk

12Fin

anci

alSt

abili

tyk,9

80.

014

(0.0

09)

0.31

8−

0.00

6(0

.008

)0.

233

Pol

icy

Focu

sw

ith

Ger

man

yB

eing

the

Ben

chm

ark

for

Oth

erE

uro-

Are

aC

ount

ries

5aIn

flation

k,9

80.

003

(0.0

07)

0.31

7−

0.01

4∗∗∗

(0.0

04)

0.23

96a

Mon

eyk,9

80.

009∗

∗(0

.004

)0.

319

0.03

0∗∗∗

(0.0

04)

0.27

57a

Exc

hang

era

tek,9

8−

0.01

1∗∗∗

(0.0

04)

0.31

9−

0.01

8∗∗∗

(0.0

04)

0.24

08a

Dis

cret

ion k

,98

−0.

004

(0.0

14)

0.31

3−

0.01

6∗∗

(0.0

07)

0.23

6(c

ontinu

ed)

176 International Journal of Central Banking June 2010

Tab

le7.

(Con

tinued

)

Spec

if.

Expla

nat

ory

Equity

Flo

ws

Bon

dFlo

ws

Num

ber

Var

iable

Coeff

.s.

e.R

2C

oeff

.s.

e.R

2

Inst

itut

iona

lFa

ctor

sw

ith

Ger

man

yB

eing

the

Ben

chm