The Future of Tax in Australia s Federation - KPMG US LLP · 2 The Future of Tax in Australia’s...

36

February 2017 kpmg.com.au The Future of Tax in Australia’s Federation

Transcript of The Future of Tax in Australia s Federation - KPMG US LLP · 2 The Future of Tax in Australia’s...

2 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Executive summary This paper is about the future of our Federation viewed through a tax lens.

It is an enormous subject, hugely complex and incredibly important. This paper does not present a solution, however is designed to prompt thinking about potential paths.

Our approach has been to look at the grand themes in which we face: whether there is a new global order, intergenerational inequity, productivity, whether the 21st century will see rising inequality.

Then we turn to 15 principles on federalism that we might adopt if had a blank sheet of paper. They include the need to minimise Vertical Fiscal Imbalance (VFI), the benefits of Horizontal Fiscal Equity (HFE), principles of autonomy and accountability, transparency, preferred taxation of immobile factors rather than mobile ones, and taxation of more efficient taxes as against less efficient ones.

We then turn to the historical and institutional factors – the Constitution, Commonwealth Grants Commission and Council of Australian Governments – which provide both constraints on what can be done and the current political infrastructure.

We look at each of the major tax bases: their volatility, their likely future and their efficiency. We also look at potential new tax bases which include rectification of the cash economy, viewed as a tax base, environmental taxes, congestion charging and asset, wealth and inheritance taxes.

Some options are temporally closed-off in the current environment. These include changes to the GST rate and base, probably the reduction in the company tax rate and the land tax – stamp duty trade off.

We deal with options for “what is to be done?” and what is needed to change to get there. These involve cultural shifts and altered political infrastructure. Ultimately, there is a need for political champions at the federal and state levels.

Finally, we deal with how we prepare the community for change. This involves a new transparency which would include Combined Australian Government Accounts, Intergenerational Accounts, Efficiency indices for taxes and simplicity indices for tax administration. These ideas have been previously enunciated in our Submission on Tax Reform in 2015.

Ultimately, this is about prompting thought on the future direction we might take in Australia.

Overall most of us, but not all, have experienced Australia as a remarkably prosperous country. We need to think deeply about how this prosperity might extend both to future generations and to all.

David Linke National Managing Partner, Tax

Grant Wardell-Johnson Leader, Australian Tax Centre

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

3The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

ContentsGrand themes 05

Our Federation 10

Current tax bases and their future 18

Potential future tax bases 26

Options, pathways and political infrastructure 31

Contact us

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

4 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. © 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

5The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

A new global order?

In thinking about a future Australia, one must consider the future global environment. With the inauguration of the new American President, two views are forming. The first is that very little will change in the global economic order. On this view, the system of checks and balances that the US Constitutional forefathers put in place will ensure that change occurs at the edges and that outside the level of rhetorical political discourse the show will simply go on in much the same manner.

The second view is that the world is experiencing dramatic change. Indeed we are seeing the beginnings of a new world order. The benefits of trade are being seriously questioned by the United States – the world’s biggest economy in nominal GDP terms. More than that there is a significant risk that the US will withdraw from its role as a major stabilising force in the global political order. For at least the last 70 years, and filling the void left by a declining British Empire, the US has played a major role as the world’s leader in the geopolitical realm, through, for example, the Bretton Woods agreement in 1944 where it delivered currency stability for 30 years, the Marshall Plan which involved providing approximately $US120 billion (in current terms) in rebuilding Europe after WWII, playing a key role in institutions such as the IMF and the World Bank.

The costs of this global leadership role are often immediate and visible. The benefits can be secondary and less tangible, though nonetheless very real. The significant “soft power” that the US has exercised in the last 70 years – to use the expression of

Joseph Nye to cover the ability to co-opt and attract, rather than the ability to coerce – is very much a function of this global leadership role.

The fear is that the US withdrawing from this position of global leadership will create a vacuum. A significant question is who and how it will be filled. India and Brazil do not yet have the economic power. Europe’s power is fragmenting as a result of Brexit and the possibility of Frexit. China has the capacity to fill the global leadership role, but to do so means that it will need to operate through a very broad concept of its national interest. To date China has tended to operate through a narrower domain of self-interest.

On this basis the world is likely to become more volatile, both politically and economically. Related to this is the prospect of higher US trade barriers and the potential for a Border Tax or a Destination Tax that acts as a de facto trade barrier for those importing goods into the United States.

How does this relate to the future of our tax system in Australia? The answer is that the new global order, if there is one, increases the dimension and role of uncertainty. Stable tax bases become more valuable. In an era of uncertain global growth, our ability to rely on strong company profits that depend on increased demand for our major exports and improved terms of trade may be diminished. On the other hand, the desire for foreign residents to find a safe “store of value” in an increasingly volatile world may produce even greater demand for Australian property with higher prices and both beneficial and detrimental flow-on effects.

Grand themesThe new globalorder, if there is one, increases thedimension and role of uncertainty.Stable tax bases become morevaluable. In an era of uncertain global growth, our ability to rely on strong company profits that depend on increased demand for our major exports and improved terms of trade may be diminished.

6 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

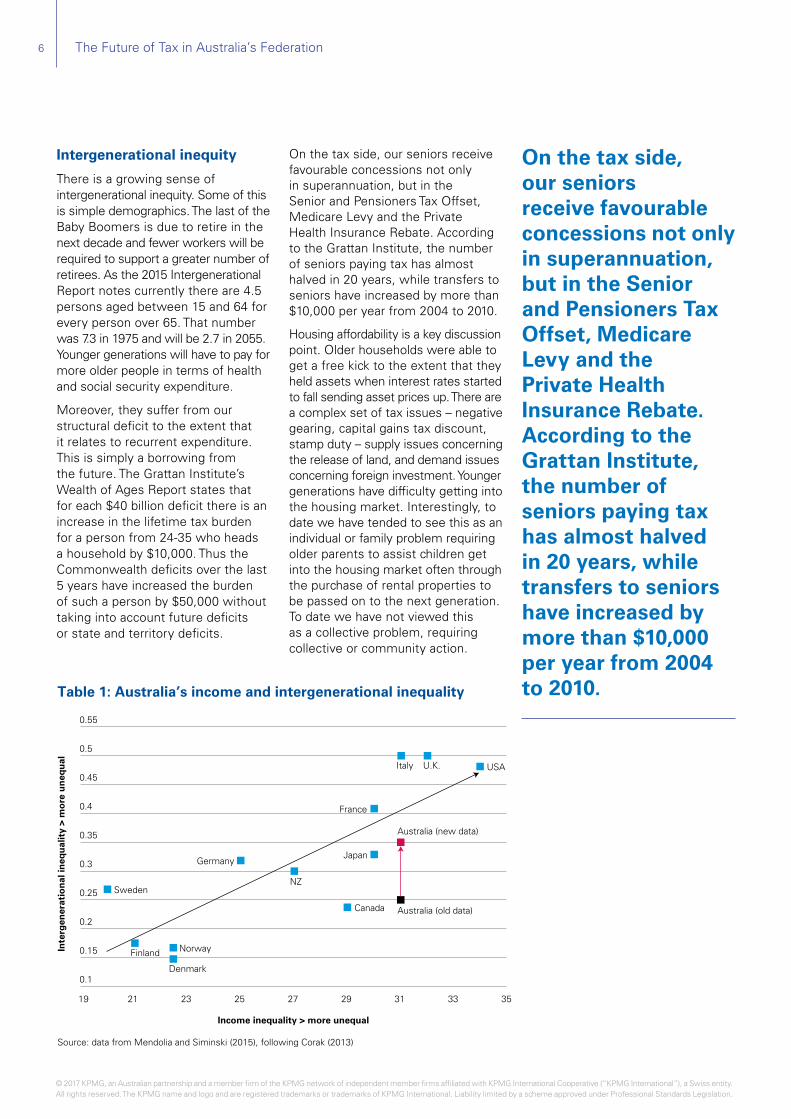

Intergenerational inequity

There is a growing sense of intergenerational inequity. Some of this is simple demographics. The last of the Baby Boomers is due to retire in the next decade and fewer workers will be required to support a greater number of retirees. As the 2015 Intergenerational Report notes currently there are 4.5 persons aged between 15 and 64 for every person over 65. That number was 7.3 in 1975 and will be 2.7 in 2055. Younger generations will have to pay for more older people in terms of health and social security expenditure.

Moreover, they suffer from our structural deficit to the extent that it relates to recurrent expenditure. This is simply a borrowing from the future. The Grattan Institute’s Wealth of Ages Report states that for each $40 billion deficit there is an increase in the lifetime tax burden for a person from 24-35 who heads a household by $10,000. Thus the Commonwealth deficits over the last 5 years have increased the burden of such a person by $50,000 without taking into account future deficits or state and territory deficits.

On the tax side, our seniors receive favourable concessions not only in superannuation, but in the Senior and Pensioners Tax Offset, Medicare Levy and the Private Health Insurance Rebate. According to the Grattan Institute, the number of seniors paying tax has almost halved in 20 years, while transfers to seniors have increased by more than $10,000 per year from 2004 to 2010.

Housing affordability is a key discussion point. Older households were able to get a free kick to the extent that they held assets when interest rates started to fall sending asset prices up. There are a complex set of tax issues – negative gearing, capital gains tax discount, stamp duty – supply issues concerning the release of land, and demand issues concerning foreign investment. Younger generations have difficulty getting into the housing market. Interestingly, to date we have tended to see this as an individual or family problem requiring older parents to assist children get into the housing market often through the purchase of rental properties to be passed on to the next generation. To date we have not viewed this as a collective problem, requiring collective or community action.

0.55

0.5

0.45

0.4

0.35

0.3

0.25

0.2

0.15

0.1

19 21 23 25 27 29 31 33 35

Table 1: Australia’s income and intergenerational inequality

Inte

rgen

erat

ion

al in

equ

alit

y >

mo

re u

neq

ual

Income inequality > more unequal

Source: data from Mendolia and Siminski (2015), following Corak (2013)

Germany

Sweden

Finland Norway

Denmark

U.K.Italy

France

USA

Australia (new data)

Australia (old data)

Japan

NZ

Canada

On the tax side, our seniors receive favourable concessions not only in superannuation, but in the Senior and Pensioners Tax Offset, Medicare Levy and the Private Health Insurance Rebate. According to the Grattan Institute, the number of seniors paying tax has almost halved in 20 years, while transfers to seniors have increased by more than $10,000 per year from 2004 to 2010.

7The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Productivity

The benefits and costs of changing technology is a critical theme surrounding our future economy and tax system. This was explored recently in Tax 2025. It would seem our changing world will give rise to a less traditional employment relationship and a greater sharing or gig economy, possibly greater wealth generated in cities, certainly a more global world and potentially significant dislocation in key industries such as transport and distribution. This realm is exciting, daunting and very difficult to predict.

There is a domain within our Federation, however, that is ripe for productivity improvement. This is the demand on business to deal with multiple rules in different jurisdictions. Ten years ago the BCA undertook a survey of Australia’s Business Tax Landscape. It said that with multiple tax types applicable in multiple jurisdictions, a business operating in every Australian state and territory could potentially be

subject to 182 taxing points (BCA, Tax Nation, 2007 p. 8). Little has changed since that time.

Significant productivity improvement could be achieved by bringing uniformity to the tax system, particularly in relation to the tax base. Indeed we advocate that Australia move to one tax administrator and the Offices of State Revenue be conflated into the ATO. This would give rise to substantial benefits for business and individuals in dealing with one administrator, for simplifying returns, reducing the need for multiple computer systems and properly dealing with compliance risk. This does not require complete harmonisation of state tax systems, although that may well be desirable.

A 21st Century of rising inequality

In 2013 a French economist, Thomas Piketty, published a work called Capital in the Twenty First Century which studied wealth inequality over

0

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

0.05

0.1

0.15

0.2

0.25

0.3

Table 2: Trends in income inequality in Australia, Gini coefficient, 1981 to 2011

Source: Johnson and Wilkins (2006), ABS (2013a)

Johnson and Wilkins ABS

There is a domain within our Federation that is ripe for productivity improvement. Thisis the demand on business to dealwith multiple rules in different jurisdictions.

8 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

the past 250 years in many developed economies. The conclusion drawn from this empirical study is that if the rate of return of capital is persistently greater than the rate of economic growth, then there will be a tendency towards rising inequality. From this he concluded that developed countries should move to progressive taxation of wealth and estate duties.

The OECD has argued for the past 30-40 years that personal capital taxation should be lighter taxes on wages and salaries on the basis that it will lead to greater investment and thus greater jobs. Very recently, Pascal Saint-Amans has indicated a reversal of this thinking. Part of this thinking relates to the reduced opportunities for avoidance due to Automatic Exchange of Information Agreements, but some of this relates to Piketty’s influence.

A number of observations should be made about rising inequality. It would seem that this has been greater for the United States and the United Kingdom, than for Australia.

Be that as it may, the question arises as to whether it will become part of a future political discourse.

The second is that for developing countries, increased inequality can be viewed as a transitory phase as a limited number of individuals take control of businesses with massive growth. This phase may reverse over time, through the rise of the middle class and disruption to those gaining greater economic power, thus political discussion surrounding inequality is less likely to take hold in developing countries.

Summary of grand themes

Thus we can expect a world of greater uncertainty and volatility, possibly with new global leadership, most likely without for some period of time. Intergenerational inequity will become a greater concern which will manifest in many dimensions including taxation, expenditure on health and social security. It is too early to tell whether there will be a greater political discourse on rising inequality in Australia, but it is certainly a backdrop which may give rise to calls for higher personal capital taxation and, possibly, death duties in the longer term.

... we can expect a world of greater uncertainty and volatility, possibly with new global leadership, most likely without for some period of time.

9The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. © 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

10 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

15 Principles for a blank sheet of paper

Whatever one thinks about our current system, it would seem clear that one would not embrace it from scratch. It is worth asking what principles one would adopt in a federal system of government if one had the luxury of a blank sheet of paper. Professor Neil Warren wrote a report on intergovernmental arrangements in 2006 using a series of benchmarks from which he compared Australia to other Federations – including the United States, Canada, Germany, Austria and Switzerland. His conclusion was that “Australia performs comparatively poorly in international comparisons on intergovernmental fiscal arrangements.”

From Neil Warren’s benchmarks we have extrapolated 17 principles which one might adopt with a blank sheet of paper.

1. Principle of subsidiarity

This principle is derived from theories of organisation within the Roman Catholic Church which held that decisions should be made at the most local level consistent with their resolution. The Oxford English Dictionary defines subsidiarity as, “the principle that a central authority should have a subsidiary function, performing only those tasks which cannot be performed at a more local level.”

Thus governments should be responsible for services whose benefits are confined primarily to that geographic area. Defence should be entirely within the purview of the Federal Government as the benefits accrue across the entire country. Clearly foreign affairs, international trade, immigration, fiscal and currency

Our Federation It is worth askingwhat principles you would adopt in a federal system of government if you had the luxury of a blank sheet of paper.

Table 3: Tiers of Government

Country National State Regional Local

Australia 1 6 States, 2 Territories 673

Canada 1 10 Provinces, 2 Territories 3160

France (metropolitan) 1 22 Regions 96 Departments 36,679

Germany 1 16 Länder 439 Districts 12,320

Italy 1 20 Regions 110 Provinces 8,101

Japan 1 47 Prefectures 3,100

Russia 1 89 Regions 12,215

South Africa 1 9 Regions 284

Switzerland 1 26 Cantons 2,867

United States 1 50 States 87,849

United Kingdom 1 3 Devolved Governments 367

Source: A. Twomey and G. Withers, (2007)

11The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

policy and interstate trade must fall within the realm of a Federal Government under this principle.

Interestingly virtually all Federations would place income support for social security at the federal level based on this principle. Here, the benefits of the redistribution of income as a social protection mechanism are seen to accrue across the entire country.

For other services, such as education, health, police and justice, the principle of subsidiarity would suggest a state involvement. This would be true of intrastate roads, with local roads being dealt with by local government and interstate roads being allocated to the Federal Government.

Environment, parks and recreation, industry and agriculture are areas where it might be thought that benefits or costs whilst more local on one level, can have clear “spillover effects” to the wider group.

2. Principle of Horizontal Fiscal Equity (HFE)

Under this principle there should be a policy to correct economic disabilities experienced by different states and territories. These disabilities arise because states have different tax-raising capacities (thus one state might have lower per capita taxable income than another) or there are different cost disabilities for the provision of services (one state may have a different age profile than another). In our system, HFE has largely become a question of how we divvy up the GST revenue amongst the states and territories.

A number of points should be made about the Australian system of HFE. Firstly, unlike many countries we try to achieve full equalisation. Many other Federations either try to achieve equity on revenue-raising capacity only and do not deal with the expense side or they aim for minimum standards.

Secondly, it is remarkable how the Australian community accepts HFE as a fundamental principle of our Federation. While it has been criticised by some states (usually at a time when it does not suit them), HFE has not been questioned by the largest states who are not the direct beneficiaries of the system. This must be seen as a positive thing about Australian culture and values.

Thirdly, where HFE has been criticised, it has been based on the allocation mechanism itself. Criticisms in this arena deal with time frames, flexibility and what is measurable and what is not.

Fourthly, there is a question of whether HFE is economically inefficient or not. This is not an easy question to answer. On the one hand it might be said that HFE discourages interstate migration decisions: that a resident obtains a share of the state fiscal pie which results in a lesser incentive to move to another state, even though that would improve

12 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

national output. Against this, however, it might be said that the absence of HFE, might occur for unproductive fiscal reasons. There would be an effect whereby larger and more wealthy states would be able to offer greater incentives (through lower taxes) to residents of other states, which would in turn lead to the greater capacity to offer even greater incentives to the detriment of the other states.

3. Principle of minimisation of Vertical Fiscal Imbalance (VFI)

Underlying this principle is the notion that the assignment of taxes between federal and state governments should follow expenditure responsibilities. Ideally, there would be no VFI. Each body would be responsible for raising its own revenue. This would assist in accountability, transparency, sound management and greater flexibility for communities to act in accordance with their own choices.

Australia is very far from this ideal. The Commonwealth passes on almost a quarter of its own revenue to the states. About 40 percent of the revenue of the states is from the Commonwealth. This is very high by international standards.

VFI raises many questions. Firstly, do you have to reduce it to zero to promote the positive behaviours of accountability and sound management so as to eliminate ‘passing the buck’. Some would argue that the complete elimination of VFI is required for a change in behaviour, whilst others would argue that a partial reduction in VFI would be of assistance.

Secondly, how do you achieve a reduction in VFI? The main possibilities include handing over a tax from the Federal Government to the states, sharing a tax base or reallocating expenditure responsibilities. They have not always been successful.

Payroll Tax, was handed to the states from the Federal Government in 1971. Within 2 years the states double the rate, but within the next 20 years they halved the rate through the provision of concessions.

There have been several attempts to provide the states with a shared power to raise income tax, after the Federal Government took it away from the states “temporarily” during the Second World War. They have failed politically.

4. Principle of autonomy and accountability

Under our blank sheet of paper, states would be autonomous in the sense that they would not be reliant on the Federal Government. In Australia, autonomy is denied not simply by virtue of VFI, but also because many of the grants provided by the Federal Government are “tied” or Special Purpose Grants. Often these grants require the State Government to

0

10

20

30

40

50

60

70

Australia

39.7

17.2

58.7

44.1

66.4

29.3

66.3

40.4 54.2

31.7

Canada Germany Switzerland USA

Table 4: Vertical Fiscal Imbalance: Selected Federations, 1990

Per

cen

tag

e o

f T

ota

l Pu

blic

Ou

tlay

s o

r R

even

ue

Source: A. Twomey and G. Withers, (2007)

State and Local Share of Total Public Spending State and Local Own-Share of Total Public Revenue

13The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

match the federal funding. Hence there is a limitation not only how the grant money can be spent, but on the requirement for matched funds, it takes funding out of a discretionary pool, thereby denying the states additional autonomy.

Accountability is a corollary of the principle of autonomy. An ideal Federation would have clear lines of expenditure responsibility based on autonomy. This would lead to greater accountability.

5. Principle of independence of transfer allocations

As no federal system reaches the ideal of zero VFI, there needs to be a mechanism for determining the level of transfer from the Federal Government to the states. Clearly this needs to be independent of political processes.

In Australia this function is largely performed by the Commonwealth Grants Commission which operates independently of the political process. That said, there can be a politically driven overlay of the decisions of the CGC. In 2015, the Federal Government provided Western Australia with an additional $500 million on the basis that the allocation of the GST proceeds to that state had been unfair. This is unusual. However, it is very normal for the Federal Government to co-fund state projects and provide money or withdraw it based on political considerations.

6. Principle of revenue and expenditure expansion

If one were to allocate revenue rights and expenditure responsibilities, one would try to match growing revenue bases with those expenditures that were growing and allocate diminishing revenue bases to those expenditures that are contracting. This clearly is not an easy task in an environment where a large

portion of expenditure, including health and infrastructure is expanding far more rapidly than any of the major revenue bases.

7. Principle of predictability of transfer allocations

This is relatively simple. Good government requires a level of predictability in one’s revenue in order to be able to plan for long term projects. Unpredictability in the Australian system emanates from three main sources. The first is that the allocation of GST revenues by the CGC varies from year to year. The second is that many tied grants, while running for multiple years, are only renewed late (or not at all) for the rollover year. The third is that agreements made by the Federal Government with the states may be reversed by a subsequent Government. A major example of that in recent times is the decision of the Coalition Government to abandon the agreement of a funding formula to the states for hospital and related funding.

8. Principle of flexibility for transfer allocations where circumstances change

There is a tension between this principle and one that provides for predictability. In circumstances where a state receives an economic shock, say through the collapse of commodity prices as experienced by Western Australia in recent times, the system needs to be able to cater for those changed economic circumstances.

9. Principle of minimised manipulation for transfer allocations by state behaviour

Any formula which equity allocates transfer funds between states should not be open to manipulation such that additional funds are received or denied under the formula if certain policy or expenditure choices are made

Under our blank sheet of paper, states would be autonomous in the sense that they would not be reliant on the FederalGovernment. In Australia, autonomy is denied not simplyby virtue of VFI, but also because many of the grants provided by the Federal Governmentare “tied” or Special Purpose Grants.

14 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

or not. This is very complex, but if a state determines to reduce taxes in a specific area, it may not feel the full cost of that reduction if it receives additional funds as an indirect consequence of that action. In some cases this is the unintended consequence of our current system.

10. Principle of transparency

There should be a high degree of transparency surrounding the transfer system. This transparency should extend not only to what information is provided to the public, but also how and when it is provided. Our system suffers from a lack of real transparency on the nature and amounts of transfers to each of the states, partly based on a reasonable fear of how the information might

be misinterpreted by the press and general public. Thus the public discourse surrounding a funding statistic that shows state A receives more per capita than state B on a particular item of expenditure may be perceived to undermine sound community acceptance of HFE. While difficulties with interpreting data need to be acknowledged. They should be dealt with head-on and not through less transparency.

Transparency is most important in circumstances where functions overlap. This is the case in health, some areas of education and the environment. Deeper public understanding of those areas of overlap, while not without risk of the presentation of misinformation, may give rise to greater clarity and efficiency.

11. Principle of simplicity and community understanding

There is a tension between simple formulas for determining transfers which could be readily understood by the community and more complex ones which may produce a more equitable result by virtue of their sophistication. Both objectives are important. The manner of presenting information, its timeliness and the fact that it is in one location are important factors in driving efficiency in a Federation.

12. Principle of sound budgetary and public administration management

The principle of sound budgetary management is that state deficits should not be funded by the

Table 5: Marginal excess burden rankings by tax instrument

Tax instrument Marginal excess burden ($)

1. Stamp duty on conveyances 0.41

2. Company income tax 0.35

3. Insurance taxes 0.29

4. Payroll tax – current base 0.25

5. GST – current-base 0.23

6. Payroll tax – broad base 0.23

7. Labour income tax 0.20

8. GST – broad-base 0.19

9. Personal income tax 0.16

10. Municipal rates and land tax 0.00

Source: B. Rynne, KPMG (2016)

15The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Federal Government and that over the medium term, budgets should be balanced. State public debt should only be used to finance capital (and not recurrent expenditure) mostly with a clear return on investment. The principle of sound public administration management would involve independent efficiency audits, anti-corruption watchdogs and sensible key performance indicators which are not open to abuse. In an ideal world, states would conduct peer reviews with a view to ensuring that the best practice in one state would flow through to other states. Managing this politically is not without difficulties, but could give rise to very tangible benefits.

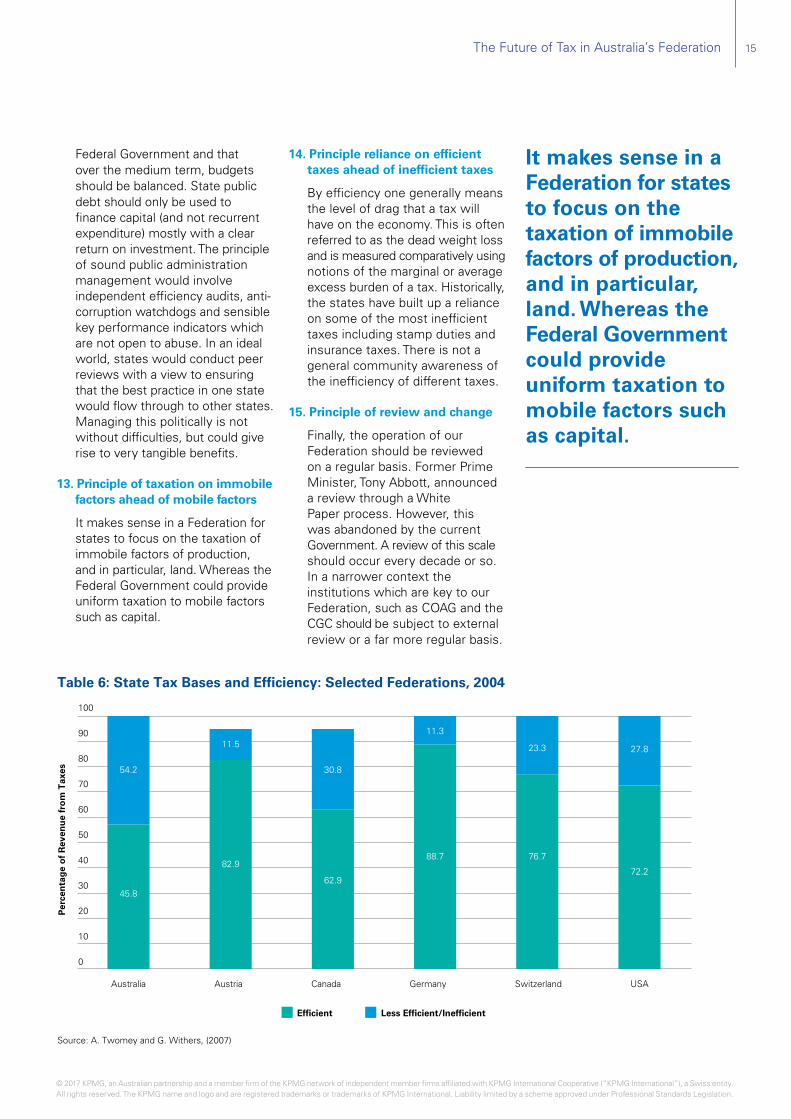

13. Principle of taxation on immobile factors ahead of mobile factors

It makes sense in a Federation for states to focus on the taxation of immobile factors of production, and in particular, land. Whereas the Federal Government could provide uniform taxation to mobile factors such as capital.

14. Principle reliance on efficient taxes ahead of inefficient taxes

By efficiency one generally means the level of drag that a tax will have on the economy. This is often referred to as the dead weight loss and is measured comparatively using notions of the marginal or average excess burden of a tax. Historically, the states have built up a reliance on some of the most inefficient taxes including stamp duties and insurance taxes. There is not a general community awareness of the inefficiency of different taxes.

15. Principle of review and change

Finally, the operation of our Federation should be reviewed on a regular basis. Former Prime Minister, Tony Abbott, announced a review through a White Paper process. However, this was abandoned by the current Government. A review of this scale should occur every decade or so. In a narrower context the institutions which are key to our Federation, such as COAG and the CGC should be subject to external review or a far more regular basis.

0

10

20

30

40

50

60

100

70

80

90

Australia CanadaAustria Germany Switzerland USA

Table 6: State Tax Bases and Efficiency: Selected Federations, 2004

Per

cen

tag

e o

f R

even

ue

fro

m T

axes

Source: A. Twomey and G. Withers, (2007)

Efficient Less Efficient/Inefficient

54.2

45.8

11.5

82.9

30.8

62.9

11.3

88.7

23.3

76.7

27.8

72.2

It makes sense in a Federation for states to focus on the taxation of immobile factors of production, and in particular, land. Whereas the Federal Government could provide uniform taxation to mobile factors such as capital.

16 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Historical and institutional perspectives

But we do not have a blank sheet of paper. Our constraints are largely historical, institutional and to some extent cultural.

Constitution

Our Constitution allocates powers based on three buckets.

The first bucket contains the exclusive powers of the Commonwealth. The main one lies in Section 90 which provides that the Commonwealth will have exclusive powers over customs and excise. How the term ‘excise’ has been interpreted by the High Court has been critical for the shape of our Federation.

The second bucket involves concurrent powers. Section 51 is the main provision. In particular the Federal Government has the power “to make laws for the peace, order and good government of the Commonwealth with respect to…(ii) Taxation but so as not to discriminate between states or parts of states”.

While the Constitution does not give direct power, even concurrently to the Federal Government on roads, education and the environment for example, there are two other critical powers that provide it with indirect power. Again, the High Court has been particularly important in how each of these have been interpreted. The first is Section 96 which enables the Commonwealth to grant financial assistance to the states on terms and conditions that it specifies. The second is the external affairs power in Section 51 (xxix) which famously was used to justify federal intervention in the area of the environment in what has become known as the Tasmanian Dams case in 1983.

The final bucket is a residual one. Unlike Canada, for instance, the Constitution is silent on these residual powers that remain with the states.

These concurrent and residual buckets are constrained by two other rules. The first is contained in Section 92 and provides that states are not permitted to impose a tax which conflicts with the guarantee that “trade, commerce and intercourse among the states … shall be absolutely free”. The second, contained in Section 114, is that states cannot impose a tax on the property of the Commonwealth.

Alfred Deakin, who was a leader of the reform movement that gave rise to the Federation and later, second, fifth and seventh Prime Minister of Australia famously said that the Constitution left the states legally free, but “financially bound to the chariot wheels of the Commonwealth”. The High Court certainly assisted in this binding.

The High Court of Australia

Possibly the history of the twentieth century was a history of centralisation of powers in central governments the world over due to two world wars, the increasing importance of foreign affairs and the demand for a social safety net and expanded government services after the Second World War. In this respect, Australia was no exception and the High Court played a significant role in interpreting the Constitution to allow for such centralisation.

On the taxation front, there are two main elements to this story, the first involving income tax and the second excise.

Income tax was levied by the states until World War I. The Commonwealth commenced to levy income tax in 1915. Both the states and the Commonwealth levied separate income taxes until 1942, although in a largely harmonised form from the Income Tax Assessment Act 1936.

In response to the need for additional funds as a result of the Second World War, Prime Minister Curtin and Treasurer Chifley raised Commonwealth taxation to a level equivalent to that of the

Commonwealth and states combined. They provided an amount to the states which reflected their previous share as financial assistance on the proviso that the states did not levy their own income tax. While this was said to be a temporary feature, it has remained in place to the current day. The High Court in two cases known as the First and Second Uniform Tax Cases in 1942 and 1957 upheld the Commonwealth’s ability to exercise its power under Section 86 in this manner.

The second case concerned the meaning of excise. Excise, at least as an economist would use the expression is a tax on the production or sale of goods and usually takes the form of an amount per unit of goods or as a percentage of value. It is an indirect tax because it is simply passed on to the consumer who thus pays for it indirectly.

In the 1970s the states developed new taxes generally called Business Franchise Fees on tobacco, alcohol and fuel. The manner in which they were collected was thought to fall outside the concept of an excise until the High Court struck them down in 1997. The Federal Government responded by levying a similar tax and returning the funds to the states in the form of Revenue Replacement Payments, thereby increasing the level of Vertical Fiscal Imbalance.

Thus, following these High Court decisions and others, there are significant Constitutional constraints on the manner in which the states can raise revenue. Moreover, the Commonwealth has considerable power in its ability to control state expenditure through financial assistance based on specific terms.

Loan Council

The Loan Council was established in 1927 and was enflamed in the Constitution through a referendum in 1928 introducing Section 105A. This was the political architecture to deal with states increasing borrowings during the 1920s. It constrained such

17The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

states, and the Federal Government except for defense, by requiring the Loan Council to agree to new borrowings. It comprises the Commonwealth Treasurer as Chair and each of the state and territory counterparts. During the 1930s it played a significant role as the NSW Premier, Jack Lang tried to subvert its limits. The 1950s saw the era of ‘Gentlemen’s Agreements’ on borrowing limits of the states, replaced in the mid-1980s by Global Borrowing Limits. In the mid-1990s the Loan Council has been conflated with a general Financial Agreement between the Commonwealth and the states and meets once a year. There are no longer effective limitations on state borrowings through the Loan Council and it acts more as a body concerned with transparency and accountability on State Government indebtedness.

Commonwealth Grants Commission

The Commonwealth Grants Commission was established in 1933 to assess claims made by the states under Section 86 of Constitution which dealt with financial assistance. When the Commonwealth took over state income taxation in 1942, the role of the CGC began to expand given the heightened Vertical Fiscal Imbalance. The CGC is an independent statutory body which provides advice to the Federal Treasurer although its reports are immediately released to the state treasuries. It comprises a part-time Chair who is currently Professor Greg Smith and two or three part-time members who are supported by a secretariat. Thankfully, it is not a political body although its decisions have significant political consequences.

Council of Australian Governments (COAG)

COAG was formed in May 1992 by Prime Minister Keating and replaced the Premiers Conferences. It is chaired by the Prime Minister,

includes the State Premiers and the Chief Territory Ministers and the President of the Australian Local Government Association.

It meets on an as needs basis, although that is usually once a year with out of session meetings by correspondence. COAG currently has eight councils: (i) Federal Financial Relations (ii) Disability Reform; (iii) Transport and Infrastructure; (iv) Energy; (v) Industry and Skills, (vi) Law Crime and Community Safety, (vii) Education and (viii) Health. The members of these councils are the respective federal, state and territory ministers.

The Prime Minister sets the agenda. Thus COAG primarily focuses on the issues of the day and the current interest of the Prime Minister. A Communique is released after the conference which generally lasts 2 days.

Arguably COAG would benefit from an independent secretariat setting the agenda with a view to long term reform and improvement in the Federation. It would need the resources to produce substantive reports on the workings of the Federation. As a secretariat, it needs to be trusted and politically independent. It should be able to initiate any reform agenda of its choosing. The balance of power in COAG should move from one of federal domination to a more cooperative agenda.

... COAG would benefit from an independent secretariat setting the agenda with a view to long term reform and improvement in the Federation. It would need the resources to produce substantive reports on the workings of the Federation.

18 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Current tax bases and their future

The years 2015 and 2016 saw considerable discussion on tax reform. While the ostensible aspirations of the Tax White Paper were substantial, what was ultimately achieved was relatively small but important reform to the superannuation system. In some sense it is a relief to learn that the Australian political process can achieve reform at all. Here the policies of the major political parties were a hair’s breadth apart and the final result was still uncertain.

Reform to the company tax system through a rate reduction, while taken up by the Government, now seems unlikely to gain the sanction of Parliament.

This section looks at each of the major tax bases and asks the following questions:

1. What is the long term future of the tax base?

2. How volatile, stable or reliable is the tax base?

3. How efficient is it? That is, what is its excess burden?

4. What are the politics of changing the base?

Current tax bases and their future

$0$-25

$-20

$-15

$-10

$-5

$0

$5

$10

$15

$50

$100

$150

$200

$250

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

Table 7: State and Territory cash balance

$ b

illio

n

$ b

illio

n

Source: ABC 2014b

Notes: (a) Receipts are equal to cash receipts from operating activities and sales of non-financial assets. (b) Payments are equal to cash payments for operating activities, purchases of non-financial assets and net acquisition of assets under finance leases.

Receipts (a) (LHS) Payments (b) (LHS) Surplus(+)/Deficit(–) (RHS)

What is the long term future of the tax base?

How volatile, stable or reliable is the tax base?

How efficient is it? That is, what is its excess burden?

What are the politics of changing the base?

19The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Company tax

Australia is heavily reliant on company tax compared to other OECD countries. It is a volatile tax and has a relatively high excess burden. That is, it is comparatively inefficient. There is a debate on the incidence of company tax, but it would seem that in the long run it largely, falls on real wages. Discussion of the company tax, must be viewed in the light of our refundable imputation system. Refundable imputation erodes the company tax base to the extent that increased investment in domestic equities by superannuation funds and not-for-profit organisations results in a refund of tax paid at the corporate level.

The burden of our company tax lies largely on non-resident investors. In this sense it acts as a disincentive to foreign investment. That disincentive becomes starker in circumstances where company tax rates are in decline in an international setting. With the reduction of tax rates in the UK and the potential reduction of tax rates in the US to say 15 percent or 20 percent, Australia may suffer the dual problem of a shrinking corporate income tax take from a declining economic base arising from decreased foreign investment and a decreased corporate tax base arising from increased domestic investment which gives rise to refundable franking credits.

With the reduction of tax rates in the UK and the potential reduction of tax rates in the US to say 15 percent or 20 percent, Australia may suffer the dual problem of a shrinking corporate income tax take from a declining economic base arising from decreased foreign investment and a decreased corporate tax base arising from increased domestic investment which gives rise to refundable franking credits.

20 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

The company tax base is volatile and will be heavily dependent on our terms of trade, which in turn will be dependent on global and particularly Asian growth. This future is very uncertain.

The prospect of a Destination Tax or Border Adjustment Tax in the US, will not act to preserve the company tax base in Australia. Rather such taxes are likely to diminish global trade and make our exporters, at least to the US market, less competitive. In the longer term, they may result in a substantially different level of trade flows.

The OECD-G20 BEPS project will not change company tax revenues significantly. Indeed reported, but unconfirmed estimates of the tax gap for corporate tax is only in the vicinity of $2 billion to $3 billion.

Ultimately one should not rely on the company tax revenue base increasing or even holding its own in the long

run. This feeds into the discussion on the likely shape of our Federal Budget in the future. That said, if one were to take an optimistic view of global growth and trade, the resulting improved terms of trade and demand for our resources could render this tax a saviour.

Personal income tax

For the past 70 years the personal income tax take has received the benefit of relatively high wage inflation and bracket creep in our progressive tax system. However, in recent years we have experienced relatively low wage inflation. This may well be the new norm, meaning that bracket creep will not be the rescuer of the future. Low wage inflation is a complex phenomenon. To the extent that it is attributable to transitory factors such as unwinding the mining boom, then the position may change. However, it may well be attributable

to low growth in labour productivity, low price inflation and possibly greater exposure of our economy to the global economy.

There may be other pressures on the personal income tax system. The rise of the sharing economy locally, and the gig economy with services being provided from overseas (such as Fiverr) and a higher level of entrepreneurial start-ups may see the personal income tax base shrink. On a more minor level we are also seeing increased claims for work related expenses, although this may be arrested. There may be compensating factors in other areas.

The major potential for change in the personal tax system would focus on increasing participation rates through adjustment to the interaction between the transfer system and the tax system. Currently many women experience very high effective marginal

21The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Total Taxation by Level of Government (2014 – 15) – Australian Bureau of Statistics

$b

Commonwealth 358

NSW VIC QLD SA WA TAS NT ACT

State 26 19 13 4 9 1 1 1 74

Local 4 4 3 1 2 0 0 14

State & Local 30 23 16 5 11 1 1 1 446

Taxation by type and level of Government 2014 – 15: Australian Bureau of Statistics

$b

Commonwealth States Local All

Taxes on income 259 259

Employer Payroll taxes 22 22

Taxes on property including stamp duty on land & financial transactions

29 16 45

Taxes on provision of goods & services including GST, excise, gambling & insurance

93 11 104

Taxes on use of goods and performance of activities including motor vehicles & franschise fees

5 11 16

Total 357 73 16 446

22 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

tax rates when moving from 3 or 4 days a week to 4 or 5 days a week due to the loss of family and child benefits. There are similar problems for older workers. Rectifying these issues would have a short term cost, but a long term benefit.

The personal tax system to the extent that it deals with labour income is relatively stable and efficient, but with some long term challenges and potential. It is unlikely, however, to be the reliable growing tax base that it has been in the past.

Personal capital taxation

This is a complex area where there is a high divergence of effective tax rates such that there is significant differences on the taxation of interest income, positively geared property and negatively geared property, capital gains and franked and unfranked dividends. One can see changes, as we have advocated in the past, which may reduce the differential through a consistent 25 percent discount on both income and expense related to personal capital taxation.

Indeed the pressure for such changes may arise not because of the benefits of consistency, but because of the perception that changes to negative gearing and the capital gains tax discount may improve housing affordability and thus link up to the grand theme of intergenerational inequity.

It is unlikely that we will see either a drive for lower or higher personal capital taxation rates in the short term. In the longer term, it is a question of the extent to which Thomas Piketty’s ideas take hold with senior policy officials.

Consumption taxation

The major feature of our consumption tax is its narrow base. Only 47 percent of goods and services are subject to the GST, compared to 96 percent for New Zealand and 55 percent for the OECD average. Efforts to broaden the base are politically

very difficult. Indeed once a base is set for a GST or VAT, it is very difficult to change except at the edges. This has only occurred in Argentina which was in a very difficult economic circumstance at the time.

The revenue take from the GST, introduced in 2000, received a substantial boost in the early and middle part of that decade due to declining savings rates, increased domestic borrowing leading to higher consumption. Those economic circumstances, were temporary and reversed with the onset of the GFC. Instead GST is on a long term trajectory of decline as we see relatively higher consumption in areas such as health and education which are not subject to GST.

The politics of changing the GST in Australia has proved to be very difficult. One would have thought that a simple base and rate expansion will be problematic for a long period of time. Indeed introducing a cash flow tax, along the lines proposed by Ken Henry, which would replace the GST may be more politically tenable simply because it is not a GST. The inherent regressiveness of the GST is also being called into question as more empirical analysis is being undertaken.

Ultimately the GST, as valuable as it is for the states to whom it is allocated, is a tax base in decline. It will not match the increased demands for health expenditure demanded of states.

The so-called ‘Sin taxes’ – tobacco, alcohol and gambling

It is clear that the taxation of tobacco is largely working. That is, it is leading to decreased demand for tobacco products and therefore tobacco excise will shrink as a revenue base. A packet of 25 cigarettes currently costs between $25 and $30 dollars. This is expected to rise to $40 by 2020. It must reach the point where the equity concerns arising from the inherent regressiveness of the tax, outweigh the clear health benefits of high taxation.

Personal capital taxation is a complex area where there is a high divergence of effective tax rates such that there is significant differences on the taxation of interest income, positively geared property and negatively gearedproperty, capital gains and frankedand unfranked dividends.

23The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

The thing about alcohol taxation is that it is internally messy and incoherent with multiple classifications producing odd results. It is ripe for reform, but this will not lead to an expansion of the tax base.

Gambling taxation is in a similar position. It is fraught with complexity and inconsistency, but is likely to be a declining source of revenue in the future.

Excise on fuels

Fuel excise (including related customs duty) raises around $20 billion per annum. It is now indexed to inflation, although it was not for much of its history and is nearly 40 cents per litre. The full amount of this is borne by consumers, but not by businesses who receive a rebate less a road user charge which is currently around 26 cents per litre.

The fuel price in Australia is relatively low compared to Europe, but not the United States. It fluctuates and varies

from city to country and substantially within the city. But let us say you are staring at the pump in Australia and it says $AU1.35 per litre. If you were to stare at an equivalent pump in Hong Kong or Norway it will say $AU2.55. In New Zealand, $AU2.09, in the UK $2.00 and in the United States $AU0.89.

This raises the question of the potential to raise the price of fuel excise. Indeed to double the price of excise would bring the price to approximately $AU1.75 per litre and very loosely raise $20 billion.

This raises significant equity issues concerning the regressiveness of the fuel excise and political issues concerning the rural city divide. A straight-forward attempt to increase fuel excise would be fraught with difficulty. That said, it could be linked to a package of other measures which may make it politically palatable.

Payroll taxes

Payroll tax was introduced in Australia in 1941 by the Federal Government to pay for child endowment. In 1971 it was handed to the state with a comprehensive base and a rate of 2.5 percent. Within 3 years the states uniformly doubled the rate to 5 percent. However, the next 20 years saw the states grant concessions and exemptions (including thresholds) such that it is now less than half of its comprehensive base.

Payroll tax with a wide base is a highly efficient tax. It is less so where the tax base is not comprehensive and more so where it is not harmonised. This is our present circumstance, although it is still a critical tax making up between one quarter and one third of State Government revenues.

There is a rhetoric associated with payroll tax which describes it as a tax on jobs. Most economists would assert that the effects of payroll tax

The politics of changing the GST in Australia has proved to be very difficult. Ultimately the GST, as valuable as it is for the states to whom it is allocated, is a tax base in decline.

24 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

A possible Property Services Tax

KPMG outlined a possible route for a Land tax – stamp duty trade-off in its Submission on Tax Reform in 2015. Key features of that proposal involved the following:

Our proposal involves the following regime:

– Abolish stamp duty on the transfer of residential and commercial property.

– Conflate rates, land tax, insurance taxes and emergency service levies into a new Property Services Tax which would be levied on progressive rates based on unit values and a minimum threshold and be administered by the ATO, and not state-based Offices of State Revenue.

– Two thirds of the property services tax would be spent locally, based on the desired form of local government attributable to the relevant state or territory.

– One third of the property services tax would go into a Property Services Equalisation Fund which would be organised by an independent state body equivalent to the Commonwealth Grants Commission.

– This body would distribute funds to local governments to help equalise the capacity of local government to provide local infrastructure and services. The remainder of the funds would be used for projects involving multiple local entities.

– The Property Services Equalisation Fund would produce highly transparent reports. It would show comparative income and expenditure of local government including top-up grants. This, of itself, would drive greater efficiency.

– Current federal government funding of local government which includes per capita and local road funding of about $2.3 billion would be redirected to the Property Services Equalisation Fund.

– The property services tax would involve a deferral scheme ’owned‘ by the Property Services Equalisation Fund but managed by a financial institution or consortia of financial institutions determined by tender. The deferral scheme would provide:

(a) That any individual owner over the age of 60 could defer 80 percent of the property services tax until sale of the property or death with a government bond rate interest charge. There would be pro rata rules for joint ownership.

(b) A selected group of others (disability pensioners etc.) would be able to enter the deferral scheme.

(c) Properties not owned individually (that is, those held in discretionary trusts) would not be entitled to the scheme.

25The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

are passed on either though higher prices and thus akin to a tax on consumption or lower wages and thus akin to a tax on income.

The US has used payroll tax extensively. It has grown as a percentage of total revenue while corporate tax has declined. US payroll tax is divided into a social security component and a medicare component. Together they comprise about a 15 percent tax on total wages, the legal incidence of which is borne, about half each by the employers and employees.

This is a potential source of increased revenue for the states. However, no state could do this on its own. It would require a federal-state package.

Land taxes

Land has the major advantage of being immobile. Its underutilisation in the Australian environment lies in the fact that there are exemptions for one’s principal place of residence, primary production, not for profit organisations and other selected exemptions such as low cost accommodation.

Thus it has a relatively narrow base and a relatively high rate where it does apply. One solution, previously proposed by KPMG, is to broaden the base with a comprehensive progressive property services charge which would conflate rates, insurance taxes, stamp duty into one charge.

There are clearly political and transitional difficulties with this option: the exemptions will be hard to unseat and there are difficulties converting a stamp duty payable on exchange of property into an annual tax. Such difficulties are not insurmountable.

Stamp duties

Stamp duties are one of the most inefficient taxes from an economist’s perspective. They lead to a lack of flexibility in the housing market so that the size of housing stock is greater than it should be: on the one hand it is a disincentive to sell

to down-size and on the other it is cheaper to renovate or extend than to sell and purchase a larger home. It also reduces labour mobility.

There are three main difficulties with abolishing stamp duty in some form of trade off. The first is that states are experiencing very high receipts in a current buoyant market. It is thus hard to replace now. Secondly, one can pin a non-resident purchaser surcharge on to stamp duty as many states have now done and thus benefit from the foreign investment into the Australian property market. This investment is likely to continue and may well even increase in a more volatile international environment. Thirdly, people tend to like to pay tax when they have access to cash (i.e. borrowing from a bank). In that sense stamp may be psychologically less imposing than annual taxation.

Annual taxation needs to deal with the difficult issue of home owners who are retired and do not have access to the same income as younger home owners. One could design a system so that a land tax or property services tax was paid for out of the equity in their home. This may need to be capped.

Miscellaneous taxes and levies

There are a series of miscellaneous taxes, such as insurance taxes, which are regressive and highly inefficient. There needs to be a long term plan for their removal.

Land has the major advantage of beingimmobile. Its underutilisation in the Australian environment lies in the fact that there are exemptions for one’s principal place of residence, primary production, not for profit organisations and other selected exemptions such as low cost accommodation.

26 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

What are the potential tax bases of the future? Below we suggest six.

1. Rectifying the cash economy

This is not a tax base but it touches on the income tax and consumption tax bases and the transfer system. On some estimates the size of the cash economy is more than $24 billion per year or about 1.5 percent of GDP.

A Black Economy Taskforce has been appointed to be chaired by Michael Andrew AO and will include the Reserve Bank of Australia, the Australian Federal Police, ASIC, APRA, AUSTRAC, and the Departments of Human Services and Immigration. It will provide an interim report in March 2017 and a final report in October 2017.

It will consider a wide range of options including requiring transactions of a certain size to be transacted through a bank account and even withdrawing the $100 note from circulation.

2. Environmental taxes

The obvious one here is putting a price on carbon, either directly through a tax, through an emissions trading scheme or a hybrid scheme. Given our abatement targets, it would seem that placing a price on carbon is almost inevitable. The question is simply one of timing.

It is possible to use the taxation system for other environmental goods. A different generation may seek to tax particulate matter, water usage, waste and even noise in a manner that we think should be subject to regulation.

Such taxation is most likely to occur at the federal level.

3. Sugar tax

The Grattan Institute has recently released a report advocating a tax on non-alcoholic drinks containing sugar. The tax would take the form of an excise of 40 cents per 100g of sugar and would raise approximately $500m.

As an excise such a tax could only be levied by the Federal Government. The health cost of obesity is estimated to be about $5.3 billion per year. Grattan estimates that approximately 10 percent of obesity is due to sugar sweetened beverages. Such a tax would clearly be regressive, however, it is argued that low income earners would receive the health benefits arising from reduced consumption of sugar sweetened beverages.

Potential future tax bases

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

27The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. © 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

28 The Future of Tax in Australia’s Federation

© 2017 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo and are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

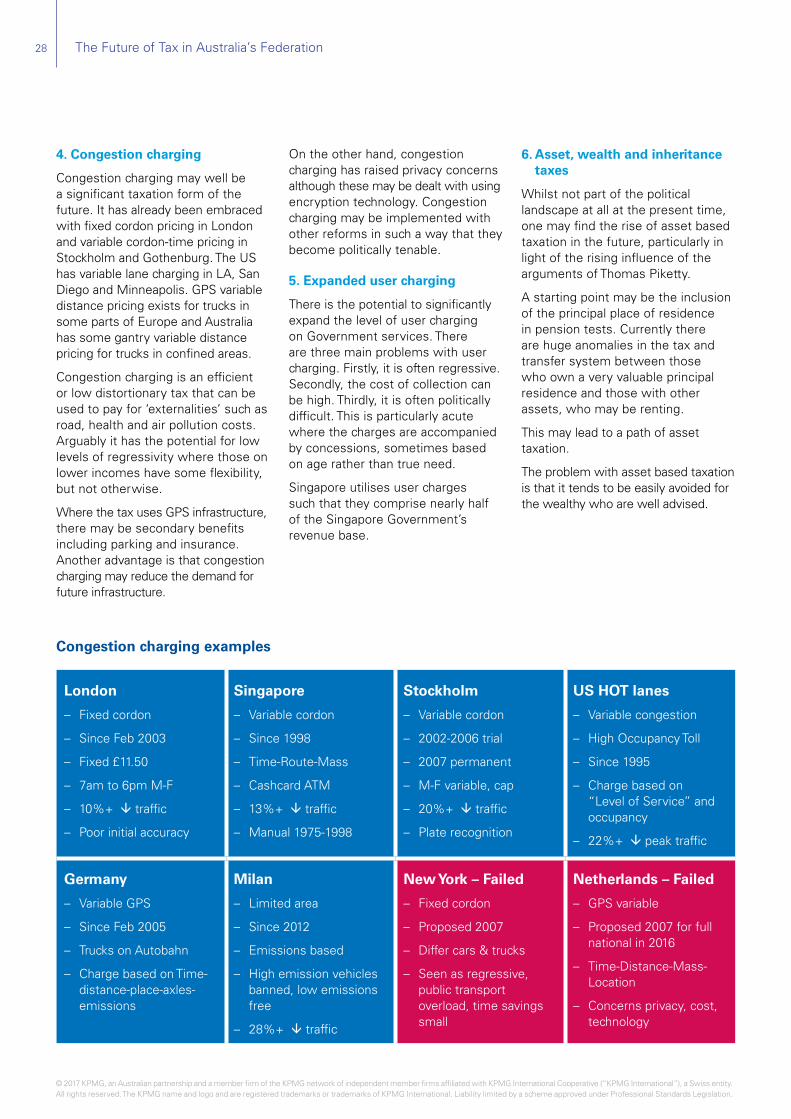

4. Congestion charging

Congestion charging may well be a significant taxation form of the future. It has already been embraced with fixed cordon pricing in London and variable cordon-time pricing in Stockholm and Gothenburg. The US has variable lane charging in LA, San Diego and Minneapolis. GPS variable distance pricing exists for trucks in some parts of Europe and Australia has some gantry variable distance pricing for trucks in confined areas.

Congestion charging is an efficient or low distortionary tax that can be used to pay for ‘externalities’ such as road, health and air pollution costs. Arguably it has the potential for low levels of regressivity where those on lower incomes have some flexibility, but not otherwise.

Where the tax uses GPS infrastructure, there may be secondary benefits including parking and insurance. Another advantage is that congestion charging may reduce the demand for future infrastructure.

On the other hand, congestion charging has raised privacy concerns although these may be dealt with using encryption technology. Congestion charging may be implemented with other reforms in such a way that they become politically tenable.

5. Expanded user charging

There is the potential to significantly expand the level of user charging on Government services. There are three main problems with user charging. Firstly, it is often regressive. Secondly, the cost of collection can be high. Thirdly, it is often politically difficult. This is particularly acute where the charges are accompanied by concessions, sometimes based on age rather than true need.

Singapore utilises user charges such that they comprise nearly half of the Singapore Government’s revenue base.

6. Asset, wealth and inheritance taxes

Whilst not part of the political landscape at all at the present time, one may find the rise of asset based taxation in the future, particularly in light of the rising influence of the arguments of Thomas Piketty.

A starting point may be the inclusion of the principal place of residence in pension tests. Currently there are huge anomalies in the tax and transfer system between those who own a very valuable principal residence and those with other assets, who may be renting.

This may lead to a path of asset taxation.

The problem with asset based taxation is that it tends to be easily avoided for the wealthy who are well advised.

London

– Fixed cordon

– Since Feb 2003

– Fixed £11.50

– 7am to 6pm M-F

– 10%+ â traffic

– Poor initial accuracy

Singapore

– Variable cordon

– Since 1998

– Time-Route-Mass

– Cashcard ATM

– 13%+ â traffic

– Manual 1975-1998

Stockholm

– Variable cordon

– 2002-2006 trial

– 2007 permanent

– M-F variable, cap

– 20%+ â traffic

– Plate recognition

US HOT lanes

– Variable congestion

– High Occupancy Toll

– Since 1995

– Charge based on “Level of Service” and occupancy

– 22%+ â peak traffic