INDEX Direct Taxation Indirect Taxation International Taxation Corporate & Other Laws

The Future of Lease Taxation & Planning

Strategies and Reporting

October 24, 2006

2ELA – 45th Annual Convention – Facing Your Future

IntroductionsMr. David FowlerTax PartnerPricewaterhouseCoopers LLPPh: 614.225.8736E-mail: [email protected]

Mr. William J Bosco, Jr.PresidentLeasing 101Ph:914.522.3233E-mail: [email protected]

Ms. Laurie HumannAsst. Tax DirectorUSBancorpPh: 612.303.4811E-mail: [email protected]

Mr. Jeff NelsonManaging DirectorPricewaterhouseCoopers LLP.Ph: 612.596.4444E-mail: [email protected]

The Future of Lease TaxationTax Incentives & Benefits “TIBs” available to the leasing industry

Dave Fowler

PricewaterhouseCoopers LLP

October 24, 2006

4ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Identifying TIBs available to the leasing industry

Background – Lessees and Lessors have a choice between- Lease- Loan

5ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Identifying TIBs available to the leasing industry

Why lease?- Lessee vs. Lessor tax position- Reduction of lessee costs (Lessor utilizes TIBs)- Improved lessee cash flows (finance full cost of

equipment)- Financial reporting- Lessor tax shelter for other income

6ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Identifying TIBs available to the leasing industry

Impact of - NOLs- AMT- Desired financial reporting- Pricing

7ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Identifying TIBs available to the leasing industry

Lessor/Lessee Treatments- Depreciation- Rental- Principal amortization and Interest

8ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Identifying TIBs available to the leasing industry

Depreciation- Accelerated Depreciation - MACRS- Bonus Depreciation – 30 & 50%- Like Kind Exchange – Deferred recognition of Gain

9ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Identifying TIBs available to the leasing industry

Credits- Clean Fuel Vehicle Deductions (pr law)- Alternative Fuel vehicles (new iteration)

• Hybrid vehicles• Advanced lean-burn technology vehicles• Fuel cell vehicles• Alternative fuel vehicles

10ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Identifying TIBs available to the leasing industry

New IRC Sec. 199 - Special deduction for Qualified Production Income- QPI includes any gross receipts derived from:

• Lease, rental, license, sale, exchange or other disposition of:Tangible personal propertyComputer software and other

• that have been manufactured, produced, grown or extracted by thetaxpayer in whole or significant part within the U.S.

- less cost and deductions allocable to such gross receipts

11ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Current developments and legislative updates

Potential Gulf Opportunity Zone Proposals- Similar to 9/11 proposals- Secretary Snow before the Senate Finance

Committee on October 6:• Affected Zone specific?• Raise cap on Sec. 179 expensing to $200,000 for 2

years• Provide 50% bonus depreciation• Provide tax relief for building new structures

12ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits (“TIB”)Current developments and legislative updates

Gulf Opportunity Zone Proposal- Special NOL C/Os & C/Bs for affected businesses- Specific industries in affected states or counties?- Impacts proposed governmental spending cuts?- Most likely the next major legislation to be

considered- Potential timing of passage & effective dates?

• House scheduled to consider in early Nov.• Senate to follow closely thereafter

The Future of Lease Taxation____________________________________________

William Bosco

Leasing 101

October 24, 2006

jtn2

Slide 13

jtn2 JTN draft editsJeff Nelson, 10/9/2005

14ELA – 45th Annual Convention – Facing Your Future

AgendaTargeting customers for tax lease- NOL & AMT discussion- Reading a tax footnote

GAAP treatment of tax benefits- Operating lease example- Direct finance lease example

Understanding MISF vs. ROA for tax lease pricing

15ELA – 45th Annual Convention – Facing Your Future

Why Do Customers Lease? To Manage Taxes!

Problem

Net operating loss (NOL)

Alternative minimum tax(AMT)

Leasing solution

Manages unfavorable tax positions, while at the same time reduces after-tax cost of borrowing

Leasing companies target customers by their tax position.

16ELA – 45th Annual Convention – Facing Your Future

Net Operating Loss - “NOL”A tax position where a company has negative taxable income.- Can be carried back to generate a refund. - Unused NOL is carried forward but can expire.

Customers with an NOL lease to lower their after-tax cost of financing equipment. - Customer can’t take advantage of tax benefits currently. - The lessor will take the tax benefits currently and charge a lower tax

effected rent rate. Lease vs. buy analysis determines if the trade off of tax benefits for a lower financing rate is beneficial.

17ELA – 45th Annual Convention – Facing Your Future

Alternative Minimum Tax - “AMT”AMT causes companies with significant tax preferences to pay a minimum tax. - AMT tax is calculated by adding back preference items to regular taxable income

and applying a 20% AMT rate to the AMT income. - The higher of AMT tax or regular tax is paid.- AMT credits (excess of AMT over regular tax) carried forward with no expiration.

AMT customers can lower after tax financing cost by leasing as MACRS is a preference item, thus leasing equipment rather than buying equipment helps reduce AMT. - The lessor will take the full MACRS benefit at the higher regular tax rate (35%)

currently and charge a lower tax effected rent rate.-

Lease vs. buy analysis determines if the trade off of tax benefits for a lower financing rate is beneficial.

18ELA – 45th Annual Convention – Facing Your Future

Lease vs. Buy AnalysisAnalysis done by the lessee to determine if a tax lease financing is more cost-effective than borrowing to buy the equipment

The dilemma is that the tax lease rent rate looks better than the loan rate but the lessee is giving up potentially valuable tax benefits

19ELA – 45th Annual Convention – Facing Your Future

Lease vs. Buy AnalysisThe calculation is a discounted cash flow analysis:- Calculates the PV of the after tax cash flows of the lease- Rent to be paid less the tax benefit of deducting the rent- Tax deductions are adjusted for impact of NOL & AMT - Calculates the PV of the after tax cash flows of a loan- Loan payments to be paid less the tax benefit of deducting the interest

on the loan & the depreciation on the asset net of the after tax gain on sale of the asset

- Tax deductions are adjusted for impact of NOL & AMT- Must assume the asset is either sold under the loan or bought under the

lease assumptions to be comparableThe lowest PV of the 2 choices = the lowest after tax cost & therefore it is the best choice

20ELA – 45th Annual Convention – Facing Your Future

How Do We Know the Lessee’s Tax Position?Read the tax footnote in their annual report before we contact the customer- Tax position is a factor in determining the structures we

present to the customer- The text of the footnotes will disclose any negative tax

positions- The current tax provision in the P&L is not a good indicator

We should ask!- Often the leasing decision maker/customer contact doesn’t

know - the customer’s tax department knows best!- Tax considerations are often not focused on in mid/smaller

ticket deals

21ELA – 45th Annual Convention – Facing Your Future

Note 15 — Income Taxes

The effective tax rate varied from the statutory federal corporate income tax rate as follows:

Year Ended December 31,

2003

Three Months Ended December

31, 2002

Year Ended September 30,

2002

June 2 through September 30,

2001

January 1 through June,

2001(successor) (successor) (successor) (successor) (predecessor)

Federal income tax rate 35.0% 35.0% 35.0% 35.0% 35.0%Increase (decrease) due to:

State and local income taxes, net of federal income tax benefit. 3.7 2.6 (0.3) 2.2 2.2

Foreign income taxes 1.0 1.6 (0.4) 2.2 2.2Goodwill impairment — — (36.1) — —Interest expense — TCH — — (4.2) — —Goodwill amortization — — — 6.2 7.8Other (0.7) (0.2) 0.1 0.2 2.6Effective tax rate 39.0% 39.0% -5.9% 45.8% 49.8%

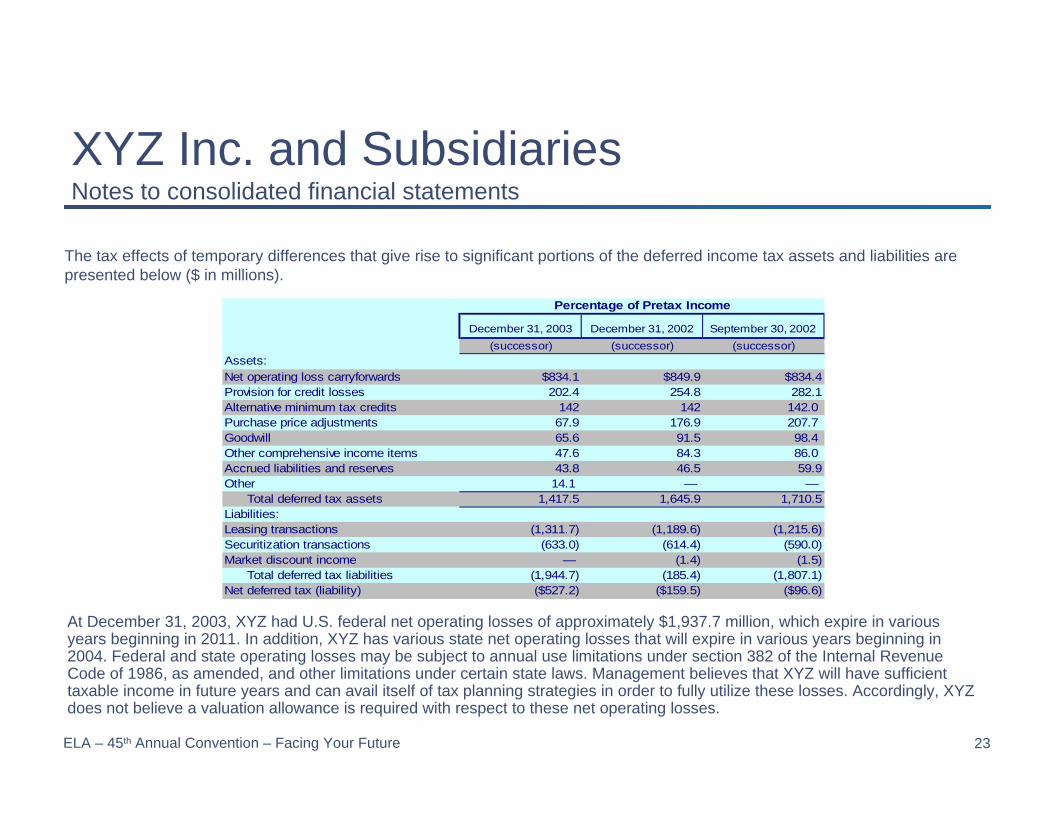

Percentage of Pretax Income

XYZ Inc. and SubsidiariesNotes to consolidated financial statements

22ELA – 45th Annual Convention – Facing Your Future

Note 15 — Income Taxes

The provision for income taxes is comprised of the following ($ in millions):

Year Ended December 31,

2003

Three Months Ended December

31, 2002

Year Ended September 30, 2002

June 2 through September 30,

2001

January 1 through June,

2001(successor) (successor) (successor) (successor) (predecessor)

Current Federal income tax provision $ - $ - $ - $ - $ -Deferred Federal income tax provision 265.1 71.9 276.9 113.6 63.7Total Federal income taxes 265.1 71.9 276.9 113.6 63.7State and local income taxes 53.5 9.4 30.4 11.7 5.7Interest expense — special transaction — — (4.2) — —Foreign income taxes 46.4 10.7 66.7 32.1 15.4

Total provision for income taxes $365.0 $92.0 $374.0 $157.4 $84.8

XYZ Inc. and SubsidiariesNotes to consolidated financial statements

23ELA – 45th Annual Convention – Facing Your Future

The tax effects of temporary differences that give rise to significant portions of the deferred income tax assets and liabilities are presented below ($ in millions).

December 31, 2003 December 31, 2002 September 30, 2002(successor) (successor) (successor)

Assets:Net operating loss carryforwards $834.1 $849.9 $834.4Provision for credit losses 202.4 254.8 282.1Alternative minimum tax credits 142 142 142.0Purchase price adjustments 67.9 176.9 207.7Goodwill 65.6 91.5 98.4Other comprehensive income items 47.6 84.3 86.0Accrued liabilities and reserves 43.8 46.5 59.9Other 14.1 — —

Total deferred tax assets 1,417.5 1,645.9 1,710.5Liabilities:Leasing transactions (1,311.7) (1,189.6) (1,215.6)Securitization transactions (633.0) (614.4) (590.0)Market discount income — (1.4) (1.5)

Total deferred tax liabilities (1,944.7) (185.4) (1,807.1)Net deferred tax (liability) ($527.2) ($159.5) ($96.6)

Percentage of Pretax Income

At December 31, 2003, XYZ had U.S. federal net operating losses of approximately $1,937.7 million, which expire in various years beginning in 2011. In addition, XYZ has various state net operating losses that will expire in various years beginning in 2004. Federal and state operating losses may be subject to annual use limitations under section 382 of the Internal Revenue Code of 1986, as amended, and other limitations under certain state laws. Management believes that XYZ will have sufficient taxable income in future years and can avail itself of tax planning strategies in order to fully utilize these losses. Accordingly, XYZ does not believe a valuation allowance is required with respect to these net operating losses.

XYZ Inc. and SubsidiariesNotes to consolidated financial statements

24ELA – 45th Annual Convention – Facing Your Future

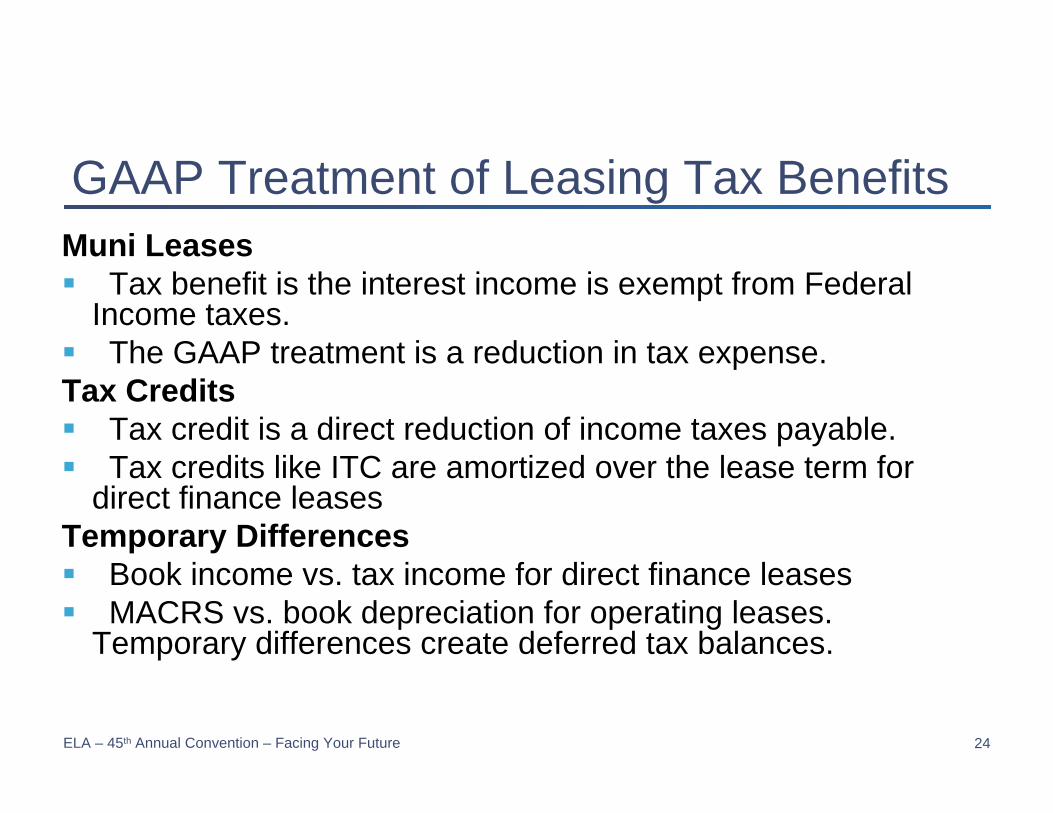

GAAP Treatment of Leasing Tax BenefitsMuni Leases

Tax benefit is the interest income is exempt from Federal Income taxes. The GAAP treatment is a reduction in tax expense.

Tax CreditsTax credit is a direct reduction of income taxes payable.Tax credits like ITC are amortized over the lease term for

direct finance leasesTemporary Differences

Book income vs. tax income for direct finance leases MACRS vs. book depreciation for operating leases.

Temporary differences create deferred tax balances.

25ELA – 45th Annual Convention – Facing Your Future

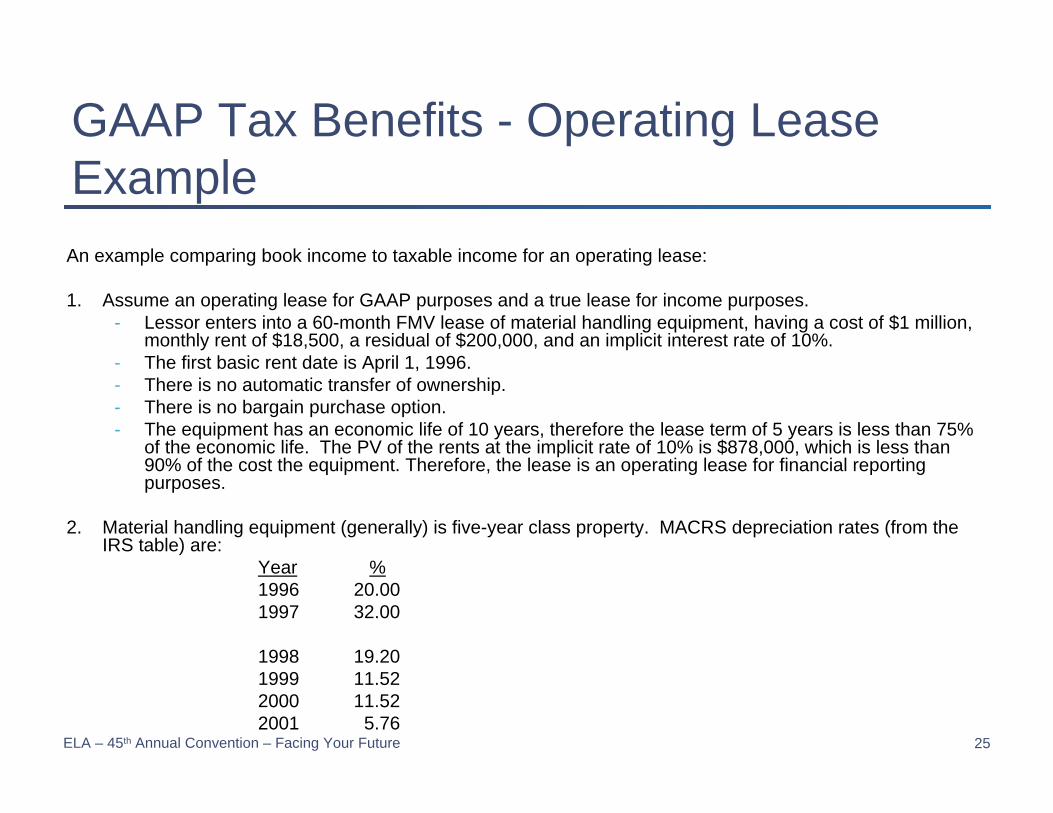

GAAP Tax Benefits - Operating Lease ExampleAn example comparing book income to taxable income for an operating lease:

1. Assume an operating lease for GAAP purposes and a true lease for income purposes.- Lessor enters into a 60-month FMV lease of material handling equipment, having a cost of $1 million,

monthly rent of $18,500, a residual of $200,000, and an implicit interest rate of 10%. - The first basic rent date is April 1, 1996.- There is no automatic transfer of ownership.- There is no bargain purchase option.- The equipment has an economic life of 10 years, therefore the lease term of 5 years is less than 75%

of the economic life. The PV of the rents at the implicit rate of 10% is $878,000, which is less than 90% of the cost the equipment. Therefore, the lease is an operating lease for financial reporting purposes.

2. Material handling equipment (generally) is five-year class property. MACRS depreciation rates (from the IRS table) are:

Year %1996 20.00 1997 32.00

1998 19.201999 11.522000 11.522001 5.76

26ELA – 45th Annual Convention – Facing Your Future

From the standpoint of the lessor, the lease will have the following earnings pattern:

Year ended December 31Tax Books 1996 1997 1998 1999 2000 2001 TotalRental Income $166,500 $222,000 $222,000 $222,000 $222,000 $55,500 $1,110,000

Sale Proceeds 200,000 200,000

Depreciation Expense 200,000 320,000 192,000 115,200 115,200 57,600 1,000,000

Tax Income (Loss) (33,500) (98,000) 30,000 106,800 106,800 197,900 310,000

Tax Rate 40% (CombinedFederal & State Rate) 40% 40% 40% 40% 40% 40% 40%

Tax Liability (Savings) ($13,400) ($39,200) $12,000 $42,720 $42,720 $79,160 $124,000

GAAP Books

Rental Income $166,500 $222,000 $222,000 $222,000 $222,000 $55,500 $1,110,000

Sale Proceeds 200,000 200,000

Depreciation Expense 120,000 160,000 160,000 160,000 160,000 240,000 1,000,000

Income before Tax 46,500 62,000 62,000 62,000 62,000 15,500 310,000

Tax Expense @ 40% 18,600 24,800 24,800 24,800 24,800 6,200 124,000

Net Income $27,900 $37,200 $37,200 $37,200 $37,200 $9,300 $186,000

Current Tax Liability 13,400 39,200 (12,000) (42,720) (42,720) (79,160) (124,000)

Deferred Tax Balance (32,000) (96,000) (108,000) (90,880) (72,960) 0 0

GAAP Tax Benefits - Operating Lease Example

27ELA – 45th Annual Convention – Facing Your Future

Operating Lease Tax Provision Calculation

1996 1997 1998 1999 2000 2001

Equipment Tax Basis 800,000 480,000 288,000 172,800 57,600 -

Equipment Book Basis 880,000 720,000 560,000 400,000 240,000 -

Taxable Temporary Difference (80,000) (240,000) (272,000) (227,200) (182,400) -

Applicable tax rate 40% 40% 40% 40% 40% 40%

Deferred tax liability (32,000) (96,000) (108,800) (90,880) (72,960) -

Current tax receivable/(payable) 13,400 39,200 (12,000) (42,720) (42,720) (79,160)

Change in the Deferred Tax Liability (32,000) (64,000) (12,800) 17,921 17,920 72,960 (Deferred Tax Expense)Total Income Tax Provision (18,600) (24,800) (24,800) (24,800) (24,800) (6,200)

The deferred tax provision is calculated by identifying the temporary differences and carryforwards.

GAAP Tax Benefits - Operating Lease Example

28ELA – 45th Annual Convention – Facing Your Future

A simple GAAP balance sheet presentation of the lease:

Year ended December 31GAAP Books 1996 1997 1998 1999 2000 2001

Cash $179,900 $441,100 $651,100 $830,380 $1,009,660 $1,186,000

Equipment under lease 1,000,000 1,000,000 1,000,000 1,000,000 1,000,000 0

Accumulated depreciation (120,000) (280,000) (440,000) (600,000) (760,000) 0

Equipment under lease, net 880,000 720,000 560,000 400,000 240,000 0

Total Assets $1,059,900 $1,161,100 $1,211,100 $1,230,380 $1,249,660 $1,186,000

Deferred Taxes 32,000 96,000 108,800 90,880 72,960 0

Stockholder’s Equity 1,027,900 1,065,100 1,102,300 1,139,500 1,176,700 1,186,000

Total Liabilities & Equity $1,059,900 $1,161,100 $1,211,100 $1,230,380 $1,249,660 $1,186,000

GAAP Tax Benefits - Operating Lease Example

29ELA – 45th Annual Convention – Facing Your Future

GAAP Tax Benefits - Direct Finance Lease ExampleAn example comparing book income to taxable income for direct finance lease:

1. Assume an direct finance lease for GAAP purposes and a true lease for income purposes.- Lessor enters into a 60 month FMV lease of material handling equipment, having a cost of $1 million,

monthly rent of $20,087, a residual of $100,000, and an implicit interest rate of 10.25%. The first basic rent date is April 1, 1996.

- There is no automatic transfer of ownership.- There is no bargain purchase option.- The equipment has an economic life of 10 years, therefore the lease term of 5 years is less than 75%

of the economic life. The PV of the rents at the implicit rate of 10% is $939,970, which is more than 90% of the cost of the equipment. Therefore, the lease is a direct finance lease for financial reporting purposes.

2. Material handling equipment (generally) is five-year class property. MACRS depreciation rates (from the IRS table) are:

Year MACRS %1996 20.00%1997 32.00%1998 19.20%1999 11.52%2000 11.52%2001 5.76%

30ELA – 45th Annual Convention – Facing Your Future

From the standpoint of the lessor, the direct finance lease will have the following earnings pattern:Year ended December 31

Tax Books 1996 1997 1998 1999 2000 2001 TotalRental Income $180,786 $241,049 $241,049 $241,049 $241,049 $60,263 $1,205,245

Sale Proceeds 100,000 100,000

Depreciation Expense 200,000 320,000 192,000 115,200 115,200 57,600 1,000,000

Tax Income (Loss) (19,214) (78,951) 49,049 125,849 125,849 102,663 305,245

Tax Rate 40% (CombinedFederal & State Rate) 40% 40% 40% 40% 40% 40% 40%

Tax Liability (Savings) ($7,686) ($31,580) $19,620 $50,340 $50,340 $41,065 $122,098

GAAP Books

Rental Income $73,253 $84,247 $67,398 $48,738 $28,074 $3,534 $305,244

Sale Proceeds

Depreciation Expense 0 0 0 0 0 0 0

Income before Tax 73,253 84,247 67,398 48,738 28,074 3,534 305,244

Tax Expense @ 40% 29,301 33,699 26,959 19,495 11,230 1,414 122,098

Net Income $43,952 $50,548 $40,439 $29,243 $16,844 $2,120 $183,146

Current Tax Receivable (Liabili 7,686 31,580 (19,620) (50,340) (50,340) (41,065) (122,098)

Deferred Tax (liability) balance (36,987) (102,266) (109,065) (78,760) (39,650) 0 0

GAAP Tax Benefits - Direct Finance Lease Example

31ELA – 45th Annual Convention – Facing Your Future

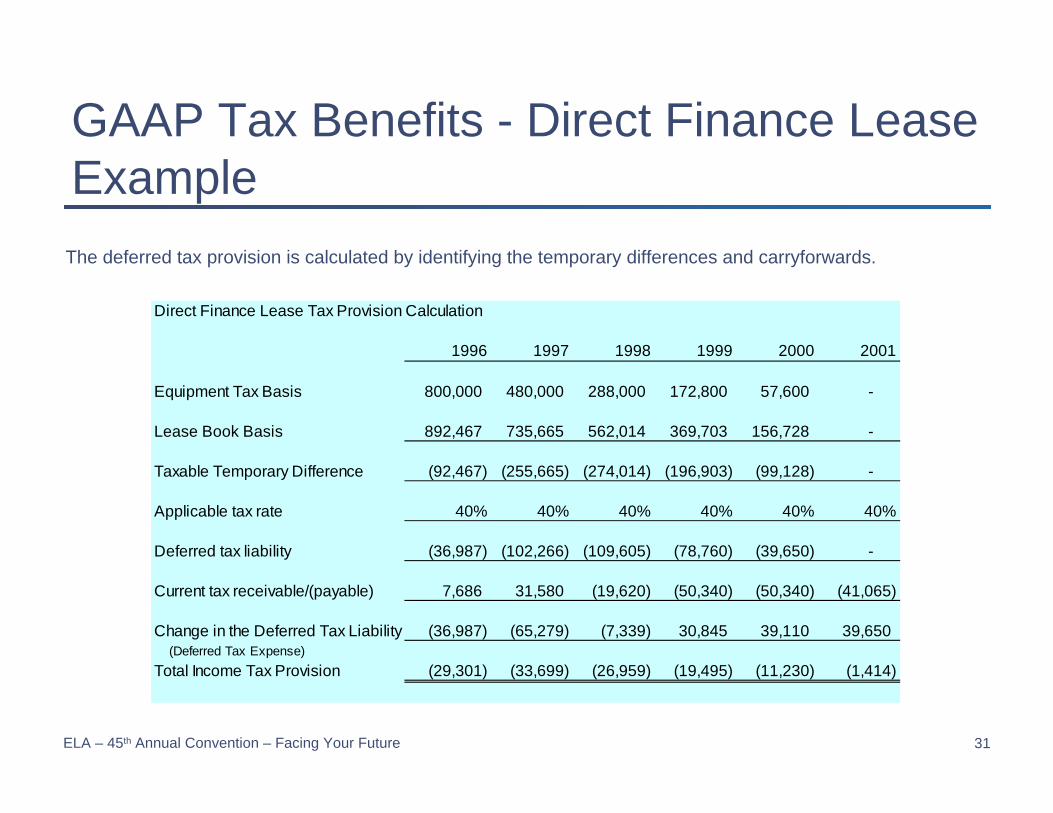

Direct Finance Lease Tax Provision Calculation

1996 1997 1998 1999 2000 2001

Equipment Tax Basis 800,000 480,000 288,000 172,800 57,600 -

Lease Book Basis 892,467 735,665 562,014 369,703 156,728 -

Taxable Temporary Difference (92,467) (255,665) (274,014) (196,903) (99,128) -

Applicable tax rate 40% 40% 40% 40% 40% 40%

Deferred tax liability (36,987) (102,266) (109,605) (78,760) (39,650) -

Current tax receivable/(payable) 7,686 31,580 (19,620) (50,340) (50,340) (41,065)

Change in the Deferred Tax Liability (36,987) (65,279) (7,339) 30,845 39,110 39,650 (Deferred Tax Expense)Total Income Tax Provision (29,301) (33,699) (26,959) (19,495) (11,230) (1,414)

The deferred tax provision is calculated by identifying the temporary differences and carryforwards.

GAAP Tax Benefits - Direct Finance Lease Example

32ELA – 45th Annual Convention – Facing Your Future

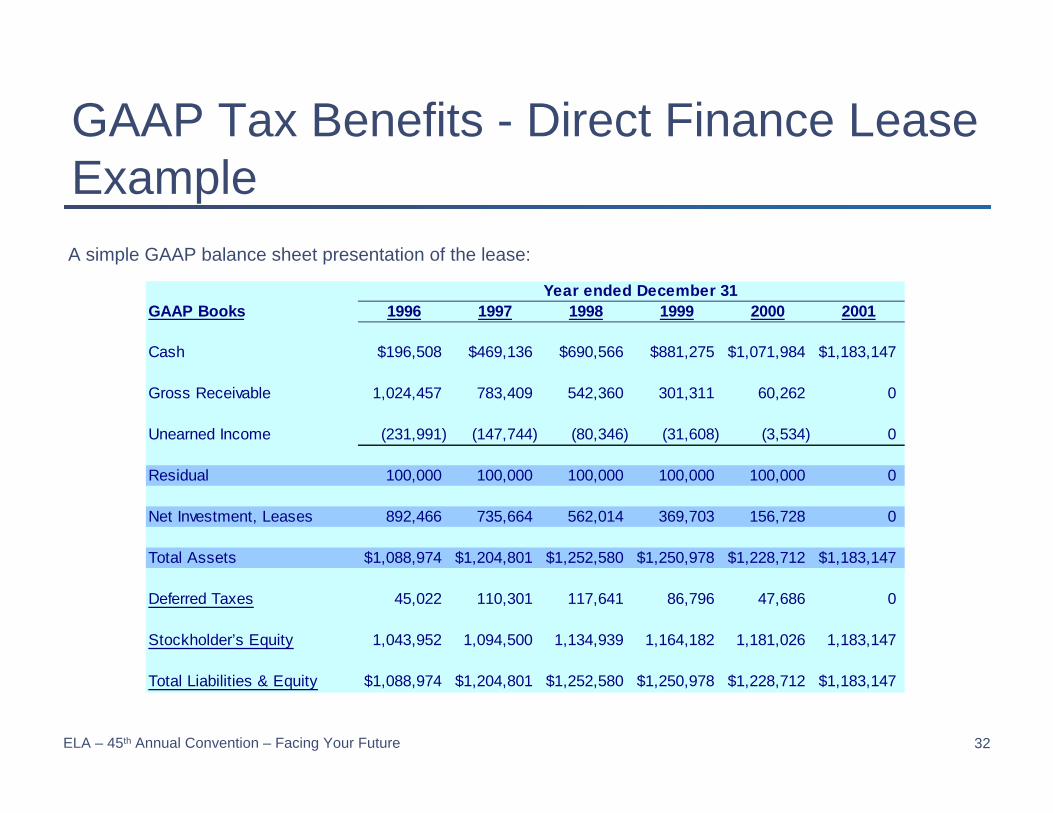

A simple GAAP balance sheet presentation of the lease:

Year ended December 31GAAP Books 1996 1997 1998 1999 2000 2001

Cash $196,508 $469,136 $690,566 $881,275 $1,071,984 $1,183,147

Gross Receivable 1,024,457 783,409 542,360 301,311 60,262 0

Unearned Income (231,991) (147,744) (80,346) (31,608) (3,534) 0

Residual 100,000 100,000 100,000 100,000 100,000 0

Net Investment, Leases 892,466 735,664 562,014 369,703 156,728 0

Total Assets $1,088,974 $1,204,801 $1,252,580 $1,250,978 $1,228,712 $1,183,147

Deferred Taxes 45,022 110,301 117,641 86,796 47,686 0

Stockholder’s Equity 1,043,952 1,094,500 1,134,939 1,164,182 1,181,026 1,183,147

Total Liabilities & Equity $1,088,974 $1,204,801 $1,252,580 $1,250,978 $1,228,712 $1,183,147

GAAP Tax Benefits - Direct Finance Lease Example

33ELA – 45th Annual Convention – Facing Your Future

Pricing for True LeasesMany lessors price to an MISF (Multiple Investor Sinking Fund) yield target.The MISF yield is the rate of return of after-tax cash flows on the amount of net cash invested, in periods where it is positive.It’s purpose is to amortize accounting earnings for leveraged leases where the net cash invested can be zero or even negative.It has incorrectly evolved into a measurement of profitability but does not correlate to GAAP returns.

34ELA – 45th Annual Convention – Facing Your Future

Pricing for True Leases: ROAThe solution to the MISF dilemma is to target ROA (Return on Assets).The denominator is Net Asset (or Net GAAP Investment) usually discounted using the ROE return target rate to levelize uneven returns.The numerator is after-tax profits, also discounted at the ROE discount rate.Deferred taxes generate a free source of funds, which reduces interest cost to carry.

35ELA – 45th Annual Convention – Facing Your Future

MISF Profile

• MISF yield is the internal rate of return of the net cash flows versus the net cash invested.

100%

Inception Expiry

Residual

Net Cash Invested (Net Investment – Deferred Taxes)

Net Investment (GAAP)

• Net Cash Invested is reduced by:• Cash received from rents• Cash received from taxes (and then increased by cash paid for

taxes) (in effect the deferred tax balance is deducted from the investment)

36ELA – 45th Annual Convention – Facing Your Future

ROA Profile

• Under the ROA calculation the net risk asset is not reduced by the deferred tax balance as the risk is the unamortized balance of the your investment.

100%

Inception Expiry

Net Risk Asset (= Investment – rent + income)

Residual

Deferred Tax Balance

• The deferred tax balance is utilized under the ROA calculation as a reduction of the amount to be funded (reduction in cost of funds).

37ELA – 45th Annual Convention – Facing Your Future

Pricing for True Leases: ROA vs. MISF

Accounting for Leveraged Leases

Pricing all True Leases incl. Leveraged Leases

Best Suited for

No adjustmentVaries by lease classification

Income Pattern

Net Cash Invested

GAAP AssetDenominator (Asset)

After-tax cashBook IncomeNumerator (Income)

NoYesAligned with GAAP Books/Mgmt Acctg

MISFROA

38ELA – 45th Annual Convention – Facing Your Future

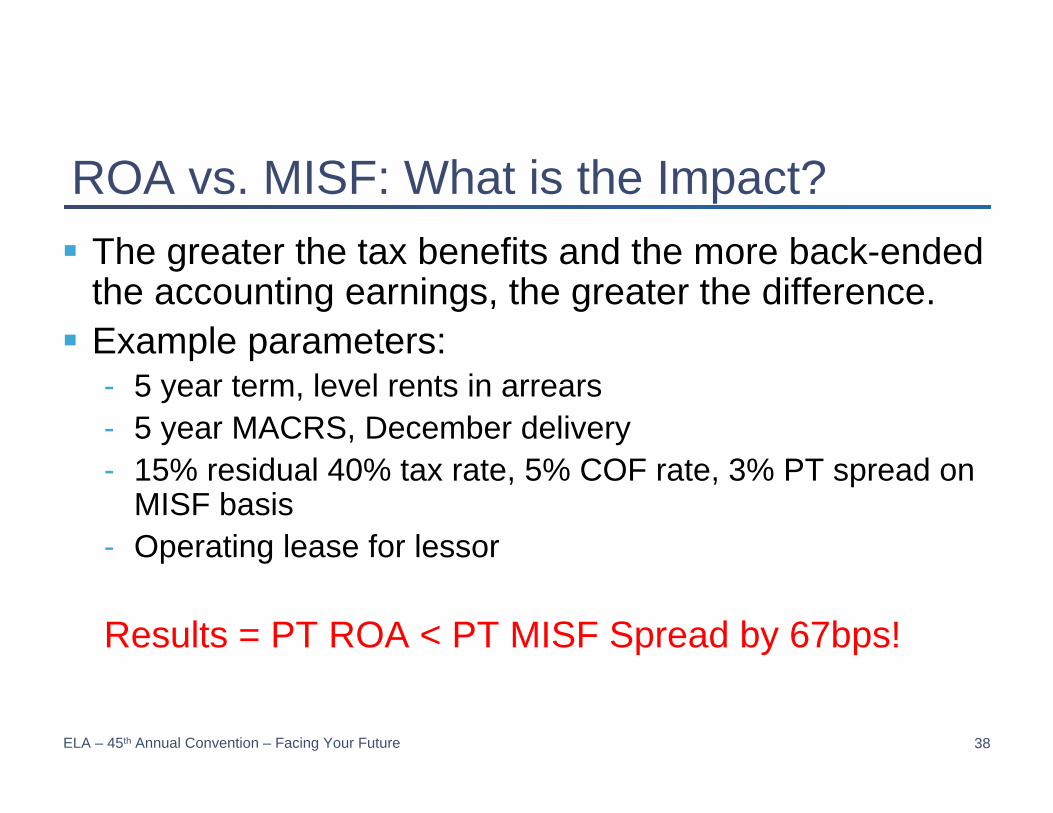

ROA vs. MISF: What is the Impact?The greater the tax benefits and the more back-ended the accounting earnings, the greater the difference.Example parameters:- 5 year term, level rents in arrears- 5 year MACRS, December delivery- 15% residual 40% tax rate, 5% COF rate, 3% PT spread on

MISF basis- Operating lease for lessor

Results = PT ROA < PT MISF Spread by 67bps!

The Future of Lease TaxationLike Kind Exchange Programs for Equipment Leasing

Jeff Nelson

PricewaterhouseCoopers LLP

October 24, 2006

40ELA – 45th Annual Convention – Facing Your Future

Today’s Agenda

• Background – What is Like Kind Exchange (LKE) and why should you consider an LKE Program for your business?

• IRS Safe Harbor Rules for Leasing LKE Programs

• Valuing LKE for your business? • Direct Benefits – cash flow, pricing, profitability and

competitiveness.• Indirect Benefits - proper state/fed reporting, vendor

programs.

• Questions

41ELA – 45th Annual Convention – Facing Your Future

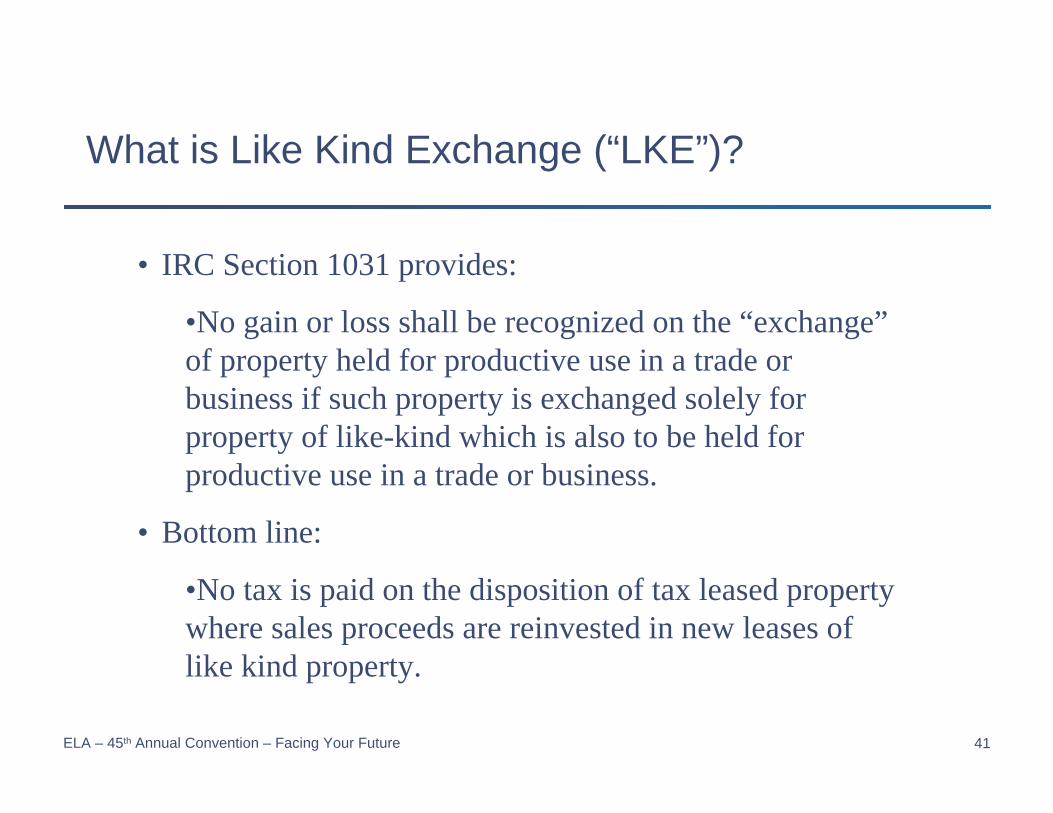

What is Like Kind Exchange (“LKE”)?

• IRC Section 1031 provides:

•No gain or loss shall be recognized on the “exchange”of property held for productive use in a trade or business if such property is exchanged solely for property of like-kind which is also to be held for productive use in a trade or business.

• Bottom line:

•No tax is paid on the disposition of tax leased property where sales proceeds are reinvested in new leases of like kind property.

42ELA – 45th Annual Convention – Facing Your Future

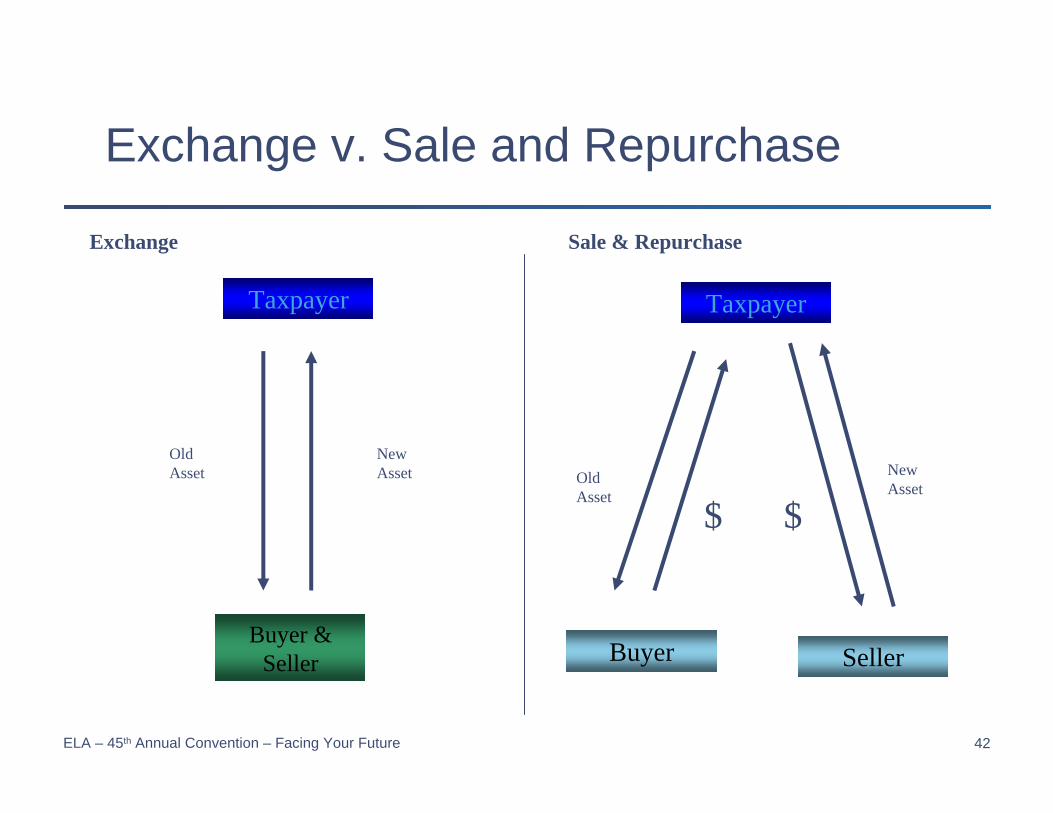

Exchange v. Sale and Repurchase

Taxpayer

$Old Asset

Exchange Sale & Repurchase

Buyer Seller

Taxpayer

Buyer & Seller

Old Asset

New Asset New

Asset

$

43ELA – 45th Annual Convention – Facing Your Future

Exchange v. Sale and RepurchaseQI Safe Harbor – A “Fictional” Exchange

Taxpayer

Qualified Intermediary (QI)

Buyer Seller

Old Asset New Asset

New Asset

$$Old Asset

Exchange of old and new assets

44ELA – 45th Annual Convention – Facing Your Future

Nature of LKE benefit

• Trade-off between current gain recognition and future depreciation deductions

• Single Asset LKE results in a “disappearing net deferral over the replacement assets tax depreciable life, however

• LKE “program” results in a “permanent” deferral to the extent taxpayers• continue their trade or business, and

• maintain the level of their $investment in Like Kind property

45ELA – 45th Annual Convention – Facing Your Future

Nature of LKE benefitsWhere does LKE make sense?

• Significant tax lease portfolio

• High rate of asset turnover - Recurring originations and dispositions

• High residual value relative to tax bases (however, “Bonus Op”)

• High unit volume

• Asset replacements occur as part of a continuous process

• Utilized “bonus” depreciation in 2001 thru 2004

46ELA – 45th Annual Convention – Facing Your Future

Equipment Leasing where LKE makes sense- vehicles (automobiles, trucks, trailers)- construction equipment- industrial machinery- aircraft- motor coaches / buses- railcars- tractors and trailers- barges & ships

Nature of LKE benefitsWhere does LKE make sense?

47ELA – 45th Annual Convention – Facing Your Future

Nature of LKE benefitsWhere does LKE make sense?

Assets subject to 50 & 30% “Bonus”Depreciation”

Commodity intensive industries• Oil and Gas Industry - pipelines, drilling, production

and refining equipment• Electrical Generation and Transmission - cable, poles

and insulators• Rail Transportation - ties, ballast and rail• Telecommunications – cable, switching and

microwave communications equipment

48ELA – 45th Annual Convention – Facing Your Future

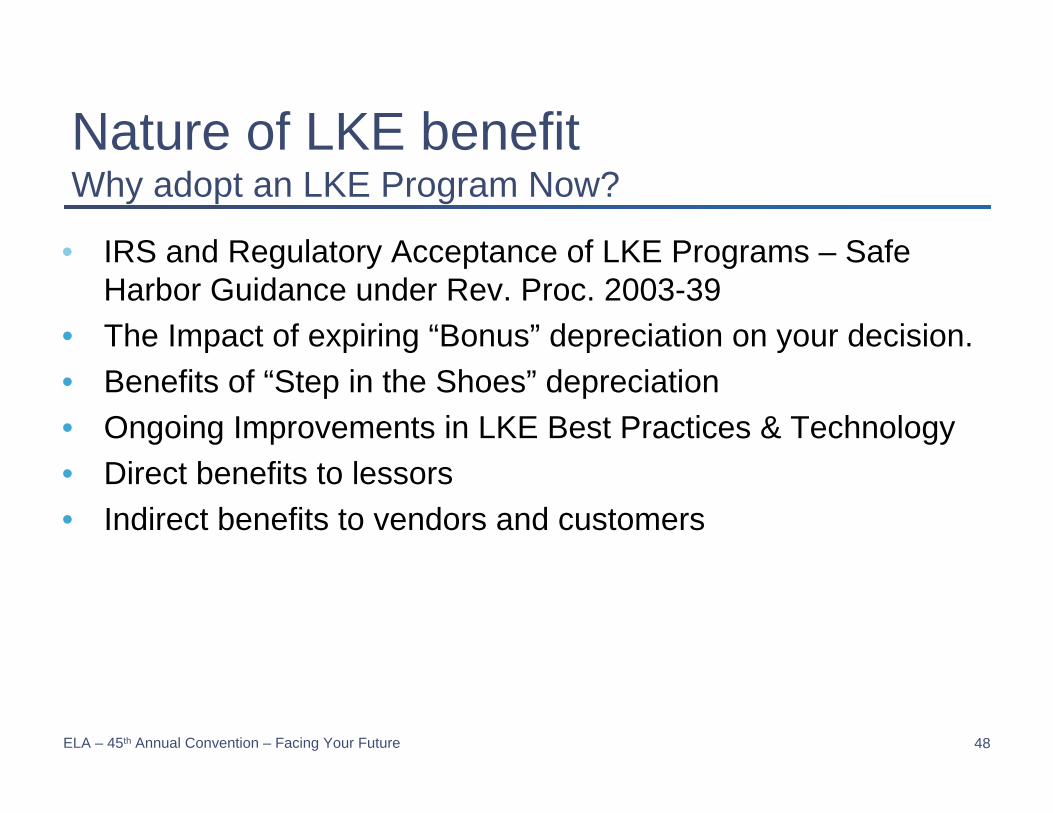

Nature of LKE benefitWhy adopt an LKE Program Now?

• IRS and Regulatory Acceptance of LKE Programs – Safe Harbor Guidance under Rev. Proc. 2003-39

• The Impact of expiring “Bonus” depreciation on your decision.• Benefits of “Step in the Shoes” depreciation• Ongoing Improvements in LKE Best Practices & Technology • Direct benefits to lessors• Indirect benefits to vendors and customers

49ELA – 45th Annual Convention – Facing Your Future

Revenue Procedure 2003-39LKE Program Safe Harbors

Applicable only to “LKE Programs”Issued May 7, 2003Applicable to tax leases only

50ELA – 45th Annual Convention – Facing Your Future

Revenue Procedure 2003-39What is an “LKE Program”

Multiple exchanges of 100 or more properties with all the following characteristics.- Regular & routine purchase and sale of personal

property- Qualified Intermediary- Utilizes a “Master Exchange Agreement”- Process for collecting, holding & disbursing funds

ensuring QI control- Process that matches relinquished wt. replacement

property

51ELA – 45th Annual Convention – Facing Your Future

Revenue Procedure 2003-39Receipt of non-LKE property

- TP can process checks or instruments made payable to person other than TP (or disqualified person)

- Joint QI-TP account OK as long as in third party or QI name & QI must OK funds transfer

- Funds netting OK • Amounts owed by TP to buyer against buyer purchase• Amounts owed to TP by seller against TP purchase

52ELA – 45th Annual Convention – Facing Your Future

Revenue Procedure 2003-39Receipt of non-LKE property

- TP can loan purchase funds to Buyer (Conversion of lease to loan)• TP makes similar loans in ordinary course of its

business• Buyer has option to obtain other financing• Loans must be arm’s-length

- Security Deposits can be applied to Purchase Price

Continued

53ELA – 45th Annual Convention – Facing Your Future

The Bonus Depreciation “Bubble”Can Recapture be avoided?

- Bonus Depreciation expired as of 1-1-2005- Tax Lessors can expect a significant increase in taxes

and gains on dispositions of assets acquired under the “Bonus” rules

- What can lessors do to avoid paying tax on Bonus Depreciation recapture?

- Like Kind Exchange Programs under IRC Sec. 1031 and Rev Proc 2003-39.

54ELA – 45th Annual Convention – Facing Your Future

The Bonus Depreciation “Bubble”The future cost of depreciation recapture

Bonus DepreciationTax Bases, Gain and Increased TaxAssuming $1mil Asset Cost

Year Year Year Year Year Year1 2 3 4 5 6

Tax Basis under Reg. MACRS 800,000$ 480,000$ 288,000$ 172,800$ 57,600$ -$

Tax Basis under Bonus MACRS 400,000$ 240,000$ 144,000$ 86,400$ 28,800$ -$

Addt'l Gain due to Bonus Recapture 400,000$ 240,000$ 144,000$ 86,400$ 28,800$ -$

Increased Tax on Sale @ 40% 160,000$ 96,000$ 57,600$ 34,560$ 11,520$ -$

55ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessLKE Opportunities For Leasing Companies

- Direct or Captive Leasing Companies

- Vendor or Dealer Leasing Companies

- Funding Other Leasing Companies

56ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessLKE Opportunities For Leasing Companies

- Direct or Captive Leasing Companies• Source business directly • Can use the LKE benefit to reduce its funding costs,

increasing its profits• Can use the LKE benefit to reduce pricing on

replacement business

57ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessLKE Opportunities For Leasing Companies

- Vendor or Dealer Leasing Companies –• Source business through vendor or dealer

relationships• Can use the LKE benefits to reduce costs or

reduce pricing• Vendor or dealer may want a cut or may force LKE

process on the lessor to offer competitive pricing to vendor/dealer customers

58ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessLKE Opportunities For Leasing Companies

- Funding Other Leasing Companies –• Leasing companies with NOL or AMT problems can’t get the

full LKE benefit on tax lease business they do for their account

• Other leasing companies with big tax base target those leasing companies with sale-leasebacks and ongoing portfolio financings using LKE techniques to make the pricing attractive

• The lessor prices in the LKE on replacement leases so the NOL/AMT lessor gets a lower financing cost and possibly off-balance sheet financing

59ELA – 45th Annual Convention – Facing Your Future

Nature of LKE Program BenefitsSingle asset sale in year 1- Disappearing deferral

Year of SaleYear 1 Year 2 Year 3 Year 4 Total

Without LKEGain recognized on Relinquished Asset 10,000$ 10,000$ Depreciation on Replacement Asset (3,333)$ (4,445)$ (1,481)$ (741)$ (10,000)$

Net effect on taxable income 6,667$ (4,445)$ (1,481)$ (741)$ -$ With LKE

Gain recognized on Relinquished Asset -$ -$ Depreciation on Replacement Asset -$ -$ -$ -$ -$

Net effect on taxable income -$ -$ -$ -$ -$

Net Taxable Income Deferral 6667 -4445 -1481 -741 0

60ELA – 45th Annual Convention – Facing Your Future

Nature of LKE Program Benefits Recurring asset sales yr. 1 & after - “Permanent” deferral

Year of SaleYear 1 Year 2 Year 3 Year 4 Total

Without LKEGain recognized on Relinquished Assets 10,000$ 10,000$ 10,000$ 10,000$ 40,000$ Depreciation on Replacement Assets (3,333)$ (7,778)$ (9,259)$ (10,000)$ (30,370)$

Net effect on taxable income 6,667$ 2,222$ 741$ -$ 9,630$ With LKE

Gain recognized on Relinquished Assets -$ -$ Depreciation on Replacement Assets -$ -$ -$ -$ -$

Net effect on taxable income -$ -$ -$ -$ -$

Net Taxable Income Deferral 6,667$ 2,222$ 741$ -$ 9,630$ Cumulative Deferral 6,667$ 8,889$ 9,630$ 9,630$

61ELA – 45th Annual Convention – Facing Your Future

Nature of LKE benefitCumulative Tax Savings – Equipment LessorEquipment LessorLike Kind ExchangeEstimated Tax SavingsIn 000's Facts & Assumptions:

Tax Rate 38.0%Inflation Rate 3.0% Annual Sales Proceeds $200 millionFleet Growth 2.0% Annual Intial Tax Cost of Sales $300 millionAverage Lease Term 3.00 MACRS Life 3,5 & & years

2006Yr. Yr. Yr. Yr. Yr. Yr.1 2 3 5 7 10 Total

Taxable Income EffectWithout like kind exchange $73,324 -$47,075 -$171,674 -$213,776 -$235,688 -$272,838 -$1,803,105

With like kind exchange -$52,444 -$142,145 -$208,374 -$239,989 -$252,492 -$292,290 -$2,211,609

Tax Inc. Impact -$125,768 -$95,069 -$36,699 -$26,213 -$16,804 -$19,453 -$408,504

Annual Tax Savings $47,792 $36,126 $13,946 $9,961 $6,385 $7,392 $155,231Cumulative Tax Savings $47,792 $83,918 $97,864 $121,628 $134,095 $155,231

62ELA – 45th Annual Convention – Facing Your Future

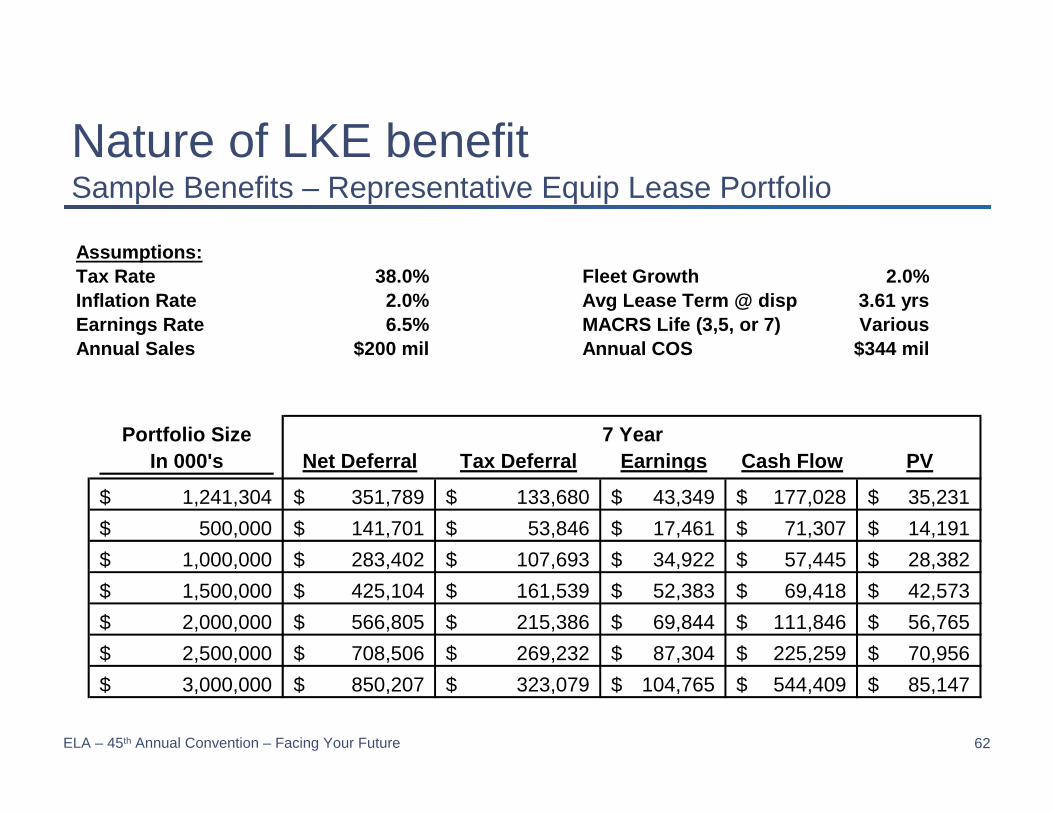

Nature of LKE benefitSample Benefits – Representative Equip Lease Portfolio

Portfolio SizeIn 000's Net Deferral Tax Deferral Earnings Cash Flow PV

1,241,304$ 351,789$ 133,680$ 43,349$ 177,028$ 35,231$ 500,000$ 141,701$ 53,846$ 17,461$ 71,307$ 14,191$

1,000,000$ 283,402$ 107,693$ 34,922$ 57,445$ 28,382$ 1,500,000$ 425,104$ 161,539$ 52,383$ 69,418$ 42,573$ 2,000,000$ 566,805$ 215,386$ 69,844$ 111,846$ 56,765$ 2,500,000$ 708,506$ 269,232$ 87,304$ 225,259$ 70,956$ 3,000,000$ 850,207$ 323,079$ 104,765$ 544,409$ 85,147$

7 Year

Assumptions:Tax Rate 38.0% Fleet Growth 2.0%Inflation Rate 2.0% Avg Lease Term @ disp 3.61 yrsEarnings Rate 6.5% MACRS Life (3,5, or 7) VariousAnnual Sales $200 mil Annual COS $344 mil

63ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessCase Study Analysis – Basis Point & Rental Rate Benefits

Most business managers want to know both the portfolio benefits of an LKE and the transactional benefits

Assumptions:- Equipment: Construction Equipment- 50% bonus MACRS- Same 5 year lease replaced with a new deal using regular MACRS

Calculation method- Target a yield of 6.50% and solve for rent.- Freeze rent, adjust depreciable basis – solve for new IRR

64ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessCase Study Analysis – IRR and Rental Rate Impact

Effect of LKE process benefits in the replacement lease

Increased Profits and Margins• Case Study - LKE produces an 84 bps after tax increase in IRR

Reduction of customer lease rates • Case Study - Lease rate reduced by 4.1% at the same IRR

65ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessCase Study Analysis – Facts

Example: Cash SavingsUtilizing a Like-Kind Exchange

Current Situation

Like-Kind Exchange Program

Sale of Old EquipmentProceeds 168,500 168,500 Tax Basis - -

Gain 168,500 168,500

Less Federal & State Taxes Due 67,400 - Cash available to acquire new equip 101,100 168,500

Assumptions: Combined tax rate 40%

66ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessCase Study Analysis – Basis Points Benefits

WITHOUT LKECASH FLOW

Pre-taxCash Flow Taxes Paid After-Tax Cash Flow IRR- =

Origination (235,000) - (235,000) 12/30/2006 42,500 (12,560) 55,060 12/30/2007 55,000 (19,800) 74,800 12/30/2008 55,000 8,080 46,920 12/30/2009 27,500 2,280 25,220 Termination 91,000 36,400 54,600

36,000 14,400 21,600 3.22%

67ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessCase Study Analysis – Basis Point Benefits

WITH LKE BENEFIT INCREASING IRRCASH FLOW

Pre-taxCash Flow Taxes Paid After-Tax Cash Flow IRR- =

Origination (235,000) - (167,600) 12/30/2006 42,500 8,400 34,100 12/30/2007 55,000 11,200 43,800 12/30/2008 55,000 18,400 36,600 12/30/2009 27,500 7,400 20,100 Termination 91,000 36,400 54,600

36,000 81,800 21,600 4.06%Without LKE 3.22%IRR BPS Advantage 0.83%

68ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessCase Study Analysis – Rental Rate Benefits

WITH LKE BENEFIT REDUCING RENTAL RATECASH FLOW

Pre-taxCash Flow Taxes Paid After-Tax Cash Flow IRR- =

Origination (235,000) - (167,600) 12/30/2006 40,736 7,620 33,116 12/30/2007 52,718 10,287 42,431 12/30/2008 52,718 17,487 35,231 12/30/2009 26,359 7,018 19,341 Termination 91,000 36,400 54,600

28,530 78,812 17,118 3.22%

69ELA – 45th Annual Convention – Facing Your Future

Valuing LKE for Your BusinessInternal Challenges to Implement LKE Program - Overview

The internal approval and implementation process is challenging• Economics may not work

• Low tax gains on sale• Small ticket assets• Low interest rates

• Business heads and tax staff are usually supportive• Need a project manager/champion to run the implementation• LKE software offers a solution for lack of detailed asset level systems

and record keeping for tax depreciation • Business people may have concerns about customer notifications • Treasury will have to change processes and add new ones• Treasury has to give allocate internal credit for the tax deferral

benefits

The Future of Lease TaxationCommunicating & allocating value to business units

Laurie HumannU.S. Bank

Jeff NelsonPricewaterhouseCoopers LLP

October 24, 2006

71ELA – 45th Annual Convention – Facing Your Future

Topics for DiscussionID the tax incentive or benefit (“TIB”)Quantify the value for the business unitPresent the value to leadershipImplement your planAllocating impacts to business lines

72ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and BenefitsID and quantify the value of the TIB for the business unit

Understand the value of the TIB- Permanent vs. deferral - Income vs. other- Jurisdictional & geographic differences

• Federal• State & Local• International

73ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and BenefitsFor example: Like Kind Exchange

Interest free loan from the IRS- Tax ownership creates a deferred tax liability

• LKE creates an additional deferred tax liability - Free cash flow/ROE/IRR

Strategic advantages- Pricing- Lower funding costs

74ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and BenefitsPresentation of Benefits to Leadership

Quantify the value- Benefits

• Enhanced cash flow• Strategic advantages

- Costs • Implementation and software costs• Ongoing costs such as Qualified Intermediary and processing• Headcount

Tailor message according to time constraints and audience- Pricing advantages- Payback period- Adoption hurdles

75ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and Benefits Implementing Your Plan - Adopting a LKE program

Recommendations for a smooth implementation- Need a point person from business line and tax- Optimal time for any data clean-up- Reconciliation efforts- Operational burdens

Benefits- Improved compliance efforts

76ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and BenefitsMaking it happen in the business

Example: USBEF Like Kind Exchange ProgramSuccess factors and process- Who? Who do you need to get buy-in?- What? What do they need to know?- When? Priorities and resources?- Where? Who benefits? - How? Logistics, scheduling and follow-up?

77ELA – 45th Annual Convention – Facing Your Future

Tax Incentives and BenefitsAllocating Impacts to Biz Lines

Attributing the value of LKE to business line- Improved cash flows- Lower funding costs

• Interest free loan from the IRS

Enhanced understanding of dataIncreased interaction with tax and financeIncreasing market competitiveness- Pricing impacts- Advantages for vendors & customers

78ELA – 45th Annual Convention – Facing Your Future

Questions and Panel Discussion

![Arnold and Commissioner of Taxation (Taxation) … and Commissioner of Taxation (Taxation) [2017] AATA 1318 PAGE 2 OF 26 CATCHWORDS TAXATION AND REVENUE – appeal …](https://static.fdocuments.net/doc/165x107/5af2c9387f8b9ac2469120bc/arnold-and-commissioner-of-taxation-taxation-and-commissioner-of-taxation.jpg)