The First Steps in Implementing a Simplified Earned Value ... · The First Steps in Implementing a...

22

The First Steps in Implementing a Simplified Earned Value Management System Dorothy Tiffany, CPA, PMP NASA/GSFC 2007 Joint ISPA/SCEA National Conference & Workshop June 12-15, 2007 Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

Transcript of The First Steps in Implementing a Simplified Earned Value ... · The First Steps in Implementing a...

The First Steps in Implementing a Simplified Earned Value

Management System

Dorothy Tiffany, CPA, PMPNASA/GSFC

2007 Joint ISPA/SCEA National Conference & Workshop

June 12-15, 2007

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

2

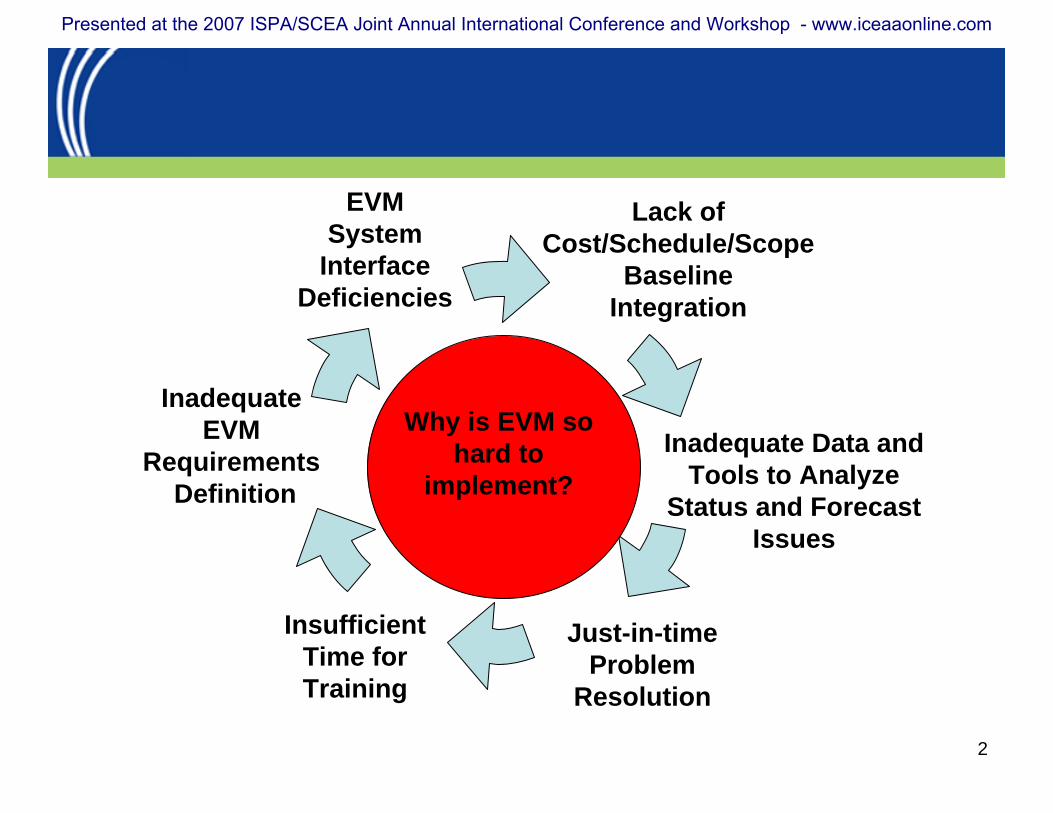

Why is EVM so hard to

implement?

Inadequate EVM

RequirementsDefinition

EVMSystem

Interface Deficiencies

Lack of Cost/Schedule/Scope

BaselineIntegration

Just-in-time Problem

Resolution

Insufficient Time forTraining

Inadequate Data and Tools to Analyze

Status and Forecast Issues

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

3

Insufficient Time forTraining

Lack of Cost/

Schedule/Scope Baseline

Integration

EVMSystem

Interface Deficiencies

Inadequate EVM

RequirementsDefinition

Just-in-timeProblem

Resolution

Why is EVM so hard to

implement?

Inadequate Data and Tools to Analyze Status

and Forecast Issues

No time for analysis

System Limitations

Processes developed from most complex project imaginable

Unrealistic cost and schedule

targets

Frequent replanningwith insufficient

understanding of impacts to data

integrity

Over reliance on COTS tools and

under appreciation of basic EVM

concepts

Cut back in staffing

Reliance on COTS to solve

the problem

Cut back in training funds

Lack of management emphasis on EVM analysis

Mission Impossible???

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

4

Does EVM really have to be

this hard to implement?

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

5

“Earned Value Project Management is not a difficult concept to understand or to employ. It is certainly not as complicated a process as some have made it to be over the years.”

Earned Value ProjectManagement, Third Edition

Quentin W. Fleming and Joel M. Koppelman

EVM

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

6No time for

analysis

System Limitations

Processes developed from most complex project imaginable

Unrealistic cost and schedule

targets Frequent replanningwith insufficient

understanding of impacts to data

integrity

Over reliance on COTS tools and

under appreciation of basic EVM

concepts

Cut back in staffing

Reliance on COTS to solve

the problem

Cut back in training funds

Lack of management emphasis on EVM analysis

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

7

Implementing Simplified EVM

• Don’t try to solve all the complex problems at once

• Incrementally implement EVM as project planning progresses

• Do a good job in analyzing the data that you do have

• Engage the various stakeholders that will benefit with successful EVM implementation

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

8

EVM First Steps Roadmap

• Define the Project Scope• Assign Work Responsibility• Schedule the Work• Allocate the Resources• Establish the Earned Value Project Baseline• Assess and Award Earned Value• Accumulate Actual Cost• Analyze the Resulting Data Carefully

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

9

Define the Project Scope

Work Breakdown Structure:

Sample Project

1.0Component

A

2.0Component

B

3.0Component

C

7.0Component

G

6.0Component

F

5.0Component

E

4.0Component

D

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

10

Assign Work Responsibility

WBS 7.0

WBS 6.0

WBS 5.0

WBS 4.0

WBS 3.0

WBS 2.0

WBS 1.0

Mission Assurance & Safety BranchComponent G

Engineering DivisionComponent F

Flight Software BranchComponent E

SATERN CorporationComponent D

Launch Vehicle ManufacturerComponent C

Acme CompanyComponent B

Systems Engineering OfficeComponent A

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

11

Plan ScheduleID Task Name

1 Component A

2 Component B

3 Component C

4 Component D

5 Component E

6 Component F

7 Component G

May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct NovQuarter 3rd Quarter 4th Quarter 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

12

Allocate the Resources

WBSBudget at Completion

1.0 Component A 1002.0 Component B 2003.0 Component C 1504.0 Component D 7005.0 Component E 5006.0 Component F 3007.0 Component G 200Total 2150

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

13

Establish the Earned Value Performance Baseline

Cumulative Plan

Jul Aug Sep Oct Nov Dec Jan FebAt

Completion1.0 Component A 100 100 100 100 100 100 100 100 1002.0 Component B 20 50 60 90 100 120 2003.0 Component C 0 1504.0 Component D 50 200 300 400 550 600 700 7005.0 Component E 50 100 200 250 400 500 5006.0 Component F 75 80 100 115 125 130 145 150 3007.0 Component G 25 40 55 70 90 100 135 145 200Total 200 270 525 735 975 1220 1480 1715 2150

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

14

Traditional Plan versus ActualThrough November

How is the project doing?

Plan Actual1.0 Component A 100 1102.0 Component B 60 553.0 Component C 0 04.0 Component D 400 3755.0 Component E 200 1556.0 Component F 125 1357.0 Component G 90 95Total 975 925

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

15

Assess the ProgressID Task Name

1 Component A

2 Component B

3 Component C

4 Component D

5 Component E

6 Component F

7 Component G

Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Decr 3rd Quarter 4th Quarter 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

16

Assess Percent Complete

Note: Percent complete status is based on milestone completion,technical judgment, and/or physical inspection.

WBSBudget at

Completion

November Percent

Complete1.0 Component A 100 100%2.0 Component B 200 25%3.0 Component C 150 0%4.0 Component D 700 30%5.0 Component E 500 25%6.0 Component F 300 30%7.0 Component G 200 50%

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

17

Assess and Award Earned Value

Note: Earned Value = BAC x Percent Complete

WBSBudget at

CompletionPercent

CompleteEarned Value

1.0 Component A 100 100% 1002.0 Component B 200 25% 503.0 Component C 150 0% 04.0 Component D 700 30% 2105.0 Component E 500 25% 1256.0 Component F 300 30% 907.0 Component G 200 50% 100

November

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

18

Accumulate Actual Cost

Still think the project is doing okay?

WBSBudget at

CompletionPercent

CompleteEarned Value

Actual Cost

1.0 Component A 100 100% 100 1102.0 Component B 200 25% 50 553.0 Component C 150 0% 0 04.0 Component D 700 30% 210 3755.0 Component E 500 25% 125 1556.0 Component F 300 30% 90 1357.0 Component G 200 50% 100 95Total 2150 675 925

November

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

19

WBSPlanned

ValueEarned Value

Actual Cost

Budget at Completion

1.0 Component A 100 100 110 1002.0 Component B 60 50 55 2003.0 Component C 0 0 0 1504.0 Component D 400 210 375 7005.0 Component E 200 125 155 5006.0 Component F 125 90 135 3007.0 Component G 90 100 95 200Total 975 675 925 2150

November

Analyze the Resulting Data Carefully

The project has gotten far less work done than planned for a lot more money than the work should have cost.

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

20

Simple Formulas Forecast Problems Based on Past Performance

Note: EAC = BAC or EAC = BAC(EV / AC) (EV / PV)

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

21

Is the Data Worth the Effort?

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com

22

Thank you.

Dorothy TiffanyNASA

Presented at the 2007 ISPA/SCEA Joint Annual International Conference and Workshop - www.iceaaonline.com