The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010 The...

36

The Fermanian Business & Economic Institute – business & economics in action © FBEI The Economic Outlook: Will the Headwinds or Tailwinds Prevail? Lynn Reaser, Ph.D. Houston, March 25, 2010

-

Upload

jessica-barker -

Category

Documents

-

view

257 -

download

2

Transcript of The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010 The...

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

The Economic Outlook:Will the Headwinds or

Tailwinds Prevail?

Lynn Reaser, Ph.D.Houston, March 25, 2010

Key Topics

Global Outlook

U.S. Economy

Financial Markets

Texas/Houston

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Global Outlook

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Global Manufacturing Rebounds

Index, 50 plus = expansion

2005 2006 2007 2008 200930

35

40

45

50

55

60

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

2007 2008 2009 2010f-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

World Trade Dives, RecoversReal Volumes, annual percent change

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

China’s Motor Remains OnReal GDP, annual percent change

2006 2007 2008 2009 2010f0

2

4

6

8

10

12

14

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Nations’ Growth Rates to Diverge

Percent change in 2010 real GDP, forecast

Emer

ging

Mar

kets

U.S.

Euro

zone U.K

.

Japa

n0.0

2.0

4.0

6.0

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010f95

100

105

110

115

120

125

130Actual

Crosscurrents Keep Dollar Stable in 2010

Broad Trade-Weighted Index, Jan 97=100, December average

Forecast

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

U.S. Economy

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

2006 2007 2008 2009 2010f-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

U.S. Real GDP to Rebound4th quarter, percent change over prior

year

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Consumers Save More, but Trauma Contained

Saving rate, percent

0

2

4

6

8

10

12Actual Forecast

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

57-58 73-75 81-82 07-10f-6-4-202468

101214

Trough to 6 qtrs later

Peak-to-trough

Recovery Weaker than NormalReal GDP, percent change

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

12,400

12,600

12,800

13,000

13,200

13,400

13,600

13,800Actual Forecast

2007 2008 2009 2010f

Output to Recoup Losses in 2010GDP, billions of chained 2005 dollars

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Q1-09 Q2-09 Q3-09 Q4-09 Q1-10f Q2-10f Q3-10f Q4-10f-800

-600

-400

-200

0

200

400

Job Growth to Slowly ResumeChange in nonfarm employment, thousands

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

2006

2007

2008

2009

2010f

0

2

4

6

8

10

12Fore-cast

Actual

Jobless Rate to Edge Lower by Year-end 2010

Quarterly average, percent

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

2006 2007 2008 2009 2010f0.0

1.0

2.0

3.0

4.0

5.0

Consumer Prices Still Subdued4th quarter, percent change over prior year

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Financial Markets

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

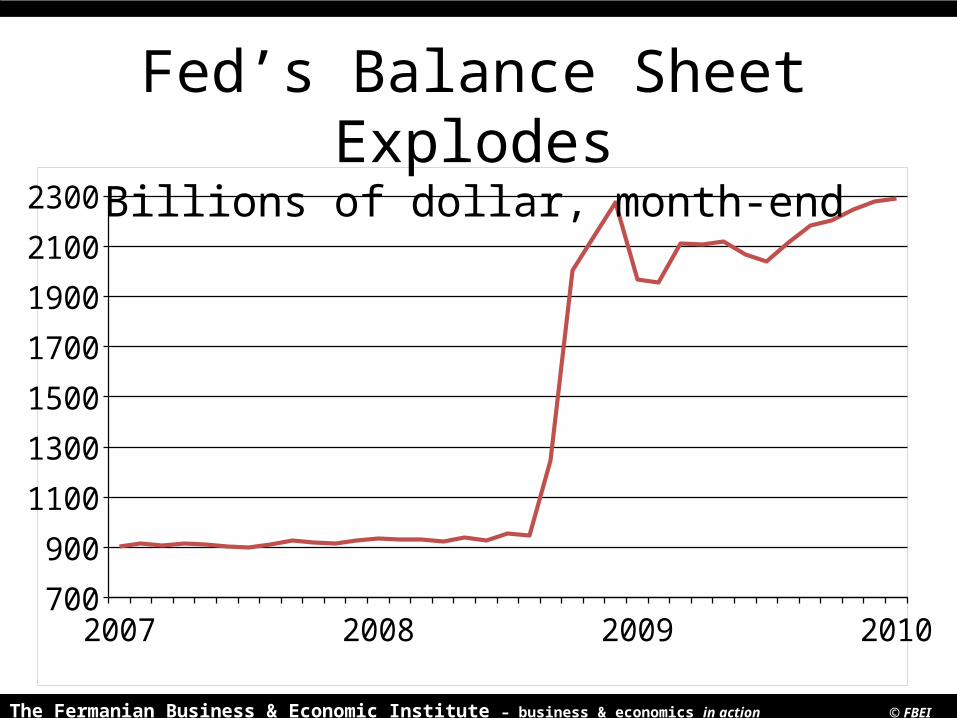

2007 2008 2009 2010700

900

1100

1300

1500

1700

1900

2100

2300

Fed’s Balance Sheet Explodes

Billions of dollar, month-end

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

2006

2007

2008

2009

2010f

0.0

1.0

2.0

3.0

4.0

5.0

6.0

10-year Treasury Note

Fed Funds Tar-get

Interest Rates to Slowly RiseQuarter-end, percent

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Profits to Bounce HigherAfter-tax profits, annual percent

change

2006 2007 2008 2009e 2010f-15

-10

-5

0

5

10

15

20

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Potential Potholes

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

House

hold

Busin

ess

Stat

e an

d Lo

cal G

over

nmen

t

Fede

ral

-5

5

15

25

Debt Shifts to the Public Sector

Q3 2009, Percent change from prior quarter, annualized

Federal Deficit Continues to Deepen

Deficit as percent of GDP, fiscal years

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Risks

•Terrorism

•Commercial Real Estate

•Oil Prices

•China

•Sovereign Risk

10-15%

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Texas Tracks U.S. Job Performance Percent change over prior year

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

U.S.

Texas

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

U.S.

Hous-ton

Houston and U.S. Job Trends ConvergePercent change over prior year

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Oil Prices Forecast to Stay at Higher LevelsDollars per barrel, quarterly average, WTI

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010f0

20

40

60

80

100

120

140Actual Forecast

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Most Houston Sectors Suffer Job Losses

January, percent change over prior year

Construction

Manufacturing

Mining

Total

Private Services

Government

-15 -13 -11 -9 -7 -5 -3 -1 1 3

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Houston Home Prices* to Rise Moderately

4th quarter, percent change over prior year

2006 2007 2008 2009 2010f0.0

1.0

2.0

3.0

4.0

5.0

6.0

*FHFA Index

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

PositivesOil drillingExportsHealth careHomebuilding

NegativesCommercial real

estateOil refining

marginsTight credit

Houston

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

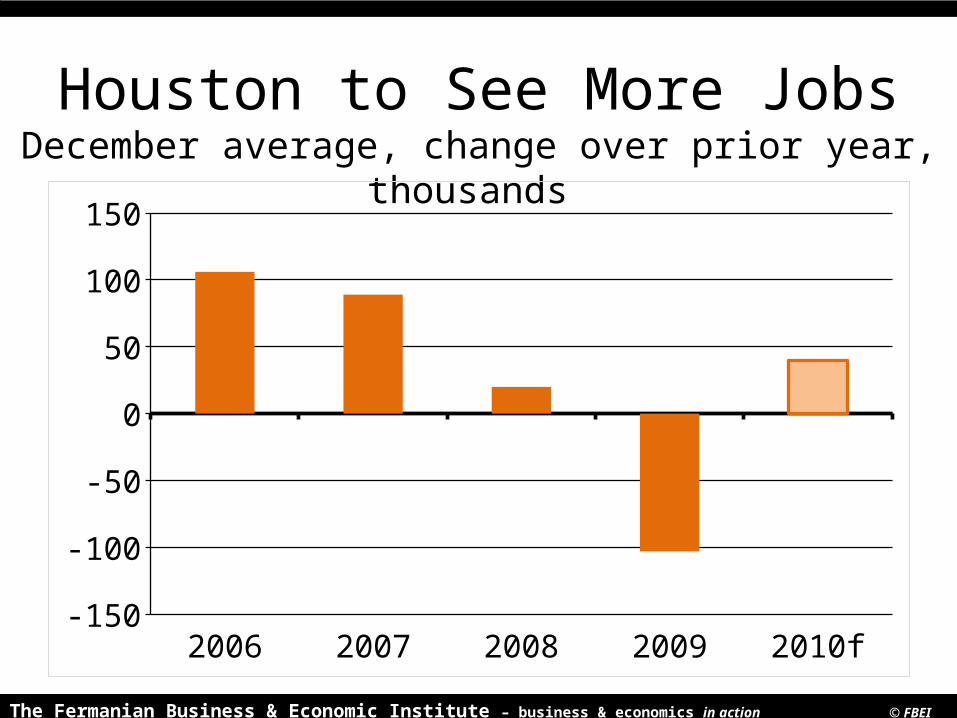

Houston to See More JobsDecember average, change over prior year,

thousands

2006 2007 2008 2009 2010f-150

-100

-50

0

50

100

150

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Recap

Global Economy Uneven

U.S. Recovers

Higher Interest Rates and Stock

Prices

Houston Outperforms Nation

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Real Change

Emerging Markets Take the Lead

Government Debt Escalates

Less Trust in Markets

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Change, but How Permanent?

Consumer Thrift

Green Economy

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010

Real Change

Complex Tax System

Risk Taking

Small Business

The Fermanian Business & Economic Institute – business & economics in action © FBEI 2010