The Evolving Digital & Mobile Lending Landscape - … · The Evolving Digital & Mobile Lending...

25

The Evolving Digital & Mobile Lending Landscape May 9, 2017 RCGILTNER Services, Inc. Trevor Knott SVP, BSG Financial Group Robert C. Giltner Chairman, RCGILTNER Services, Inc. In association with

Transcript of The Evolving Digital & Mobile Lending Landscape - … · The Evolving Digital & Mobile Lending...

The Evolving Digital & Mobile Lending

Landscape

May 9, 2017

RCGILTNER Services, Inc.

Trevor Knott SVP, BSG Financial Group

Robert C. Giltner Chairman, RCGILTNER Services, Inc.

In association with

Copyright CourtesyCloud Management Solutions LLC, 2017 • All Rights Reserved • Confidential and Proprietary • v 916.3

2

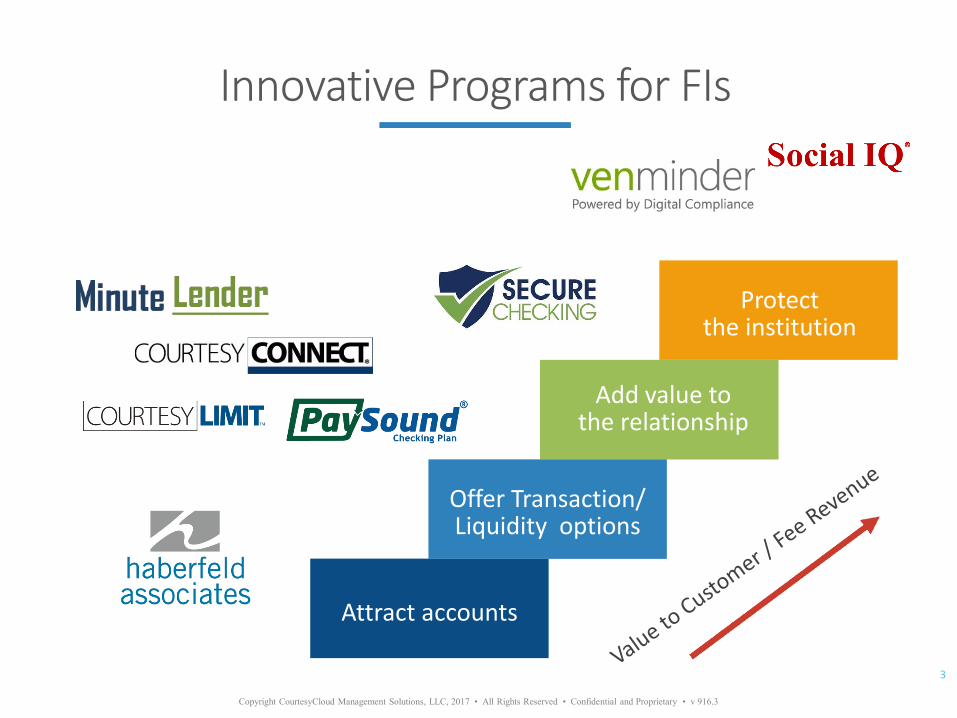

Helps financial institutions build a successful fee-revenue strategy–STEP-BY-STEP–by meeting account holders’ retail banking needs and protecting the institution.

• Offering OD programs for over 20 years

• Worked with RCG since 1997

• Emphasizes Compliance

• Provides Implementation & Training

• Is a Consultative Partner

The BSG Financial Group of Companies

Add value to the relationship

3

Copyright CourtesyCloud Management Solutions, LLC, 2017 • All Rights Reserved • Confidential and Proprietary • v 916.3

Innovative Programs for FIs

Attract accounts

Offer Transaction/ Liquidity options

Protect the institution

4

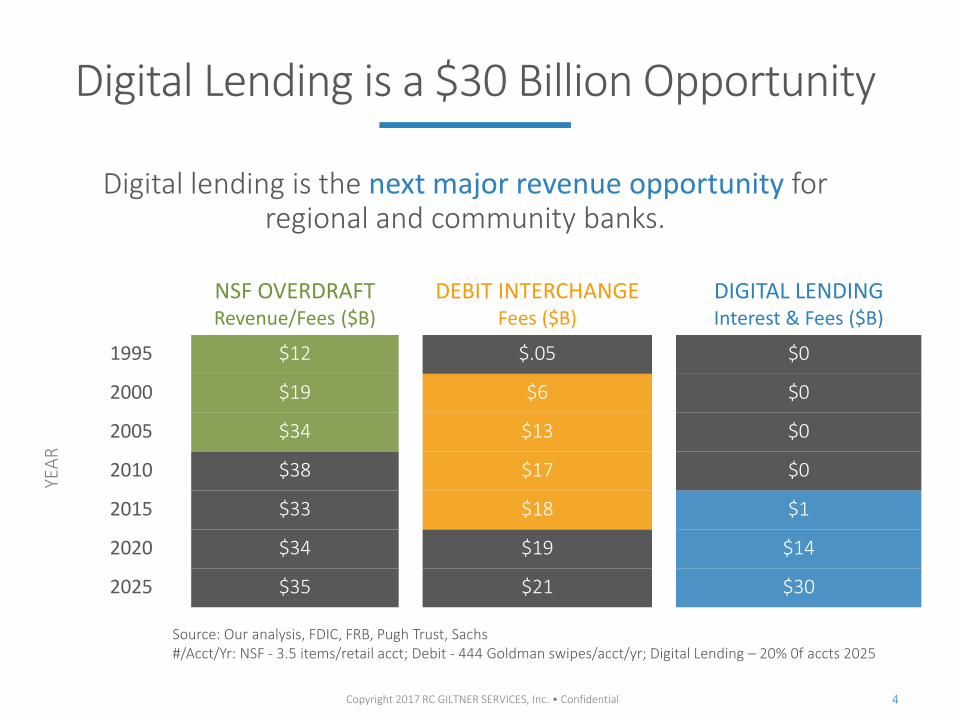

Digital lending is the next major revenue opportunity for regional and community banks.

NSF OVERDRAFT Revenue/Fees ($B)

DEBIT INTERCHANGE Fees ($B)

DIGITAL LENDING Interest & Fees ($B)

1995 $12 $.05 $0

2000 $19 $6 $0

2005 $34 $13 $0

2010 $38 $17 $0

2015 $33 $18 $1

2020 $34 $19 $14

2025 $35 $21 $30

Source: Our analysis, FDIC, FRB, Pugh Trust, Sachs #/Acct/Yr: NSF - 3.5 items/retail acct; Debit - 444 Goldman swipes/acct/yr; Digital Lending – 20% 0f accts 2025

YEA

R

Digital Lending is a $30 Billion Opportunity

Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

5

FIs WIN COMPETITIVELY WITH:

Documented compliance

Lower cost of funds

Established customer relationships

Digital Lending is a $30 Billion Opportunity

FIs just need the technology.

Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

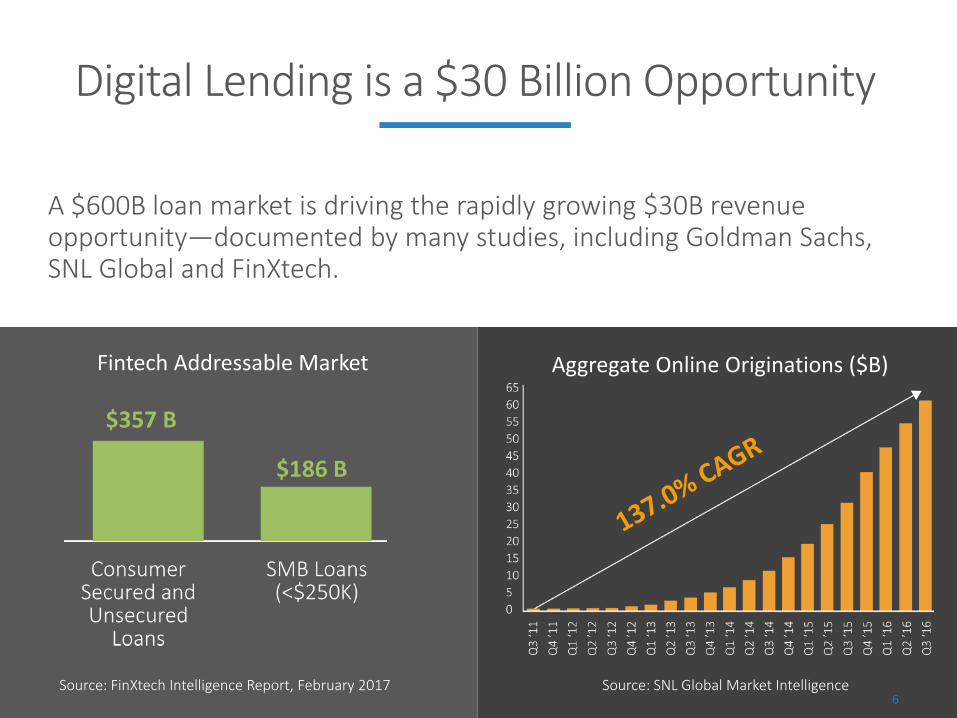

A $600B loan market is driving the rapidly growing $30B revenue opportunity―documented by many studies, including Goldman Sachs, SNL Global and FinXtech.

6 Source: FinXtech Intelligence Report, February 2017

Aggregate Online Originations ($B)

Source: SNL Global Market Intelligence

Fintech Addressable Market

Digital Lending is a $30 Billion Opportunity

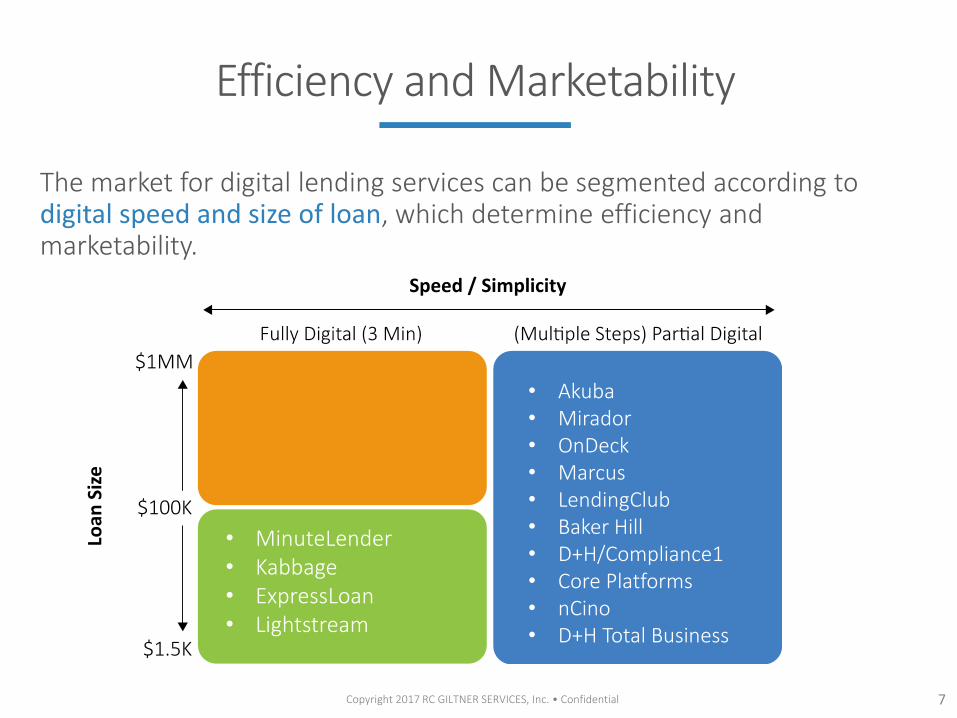

The market for digital lending services can be segmented according to digital speed and size of loan, which determine efficiency and marketability.

7

Efficiency and Marketability

Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

• MinuteLender • Kabbage • ExpressLoan • Lightstream

• Akuba • Mirador • OnDeck • Marcus • LendingClub • Baker Hill • D+H/Compliance1 • Core Platforms • nCino • D+H Total Business

8

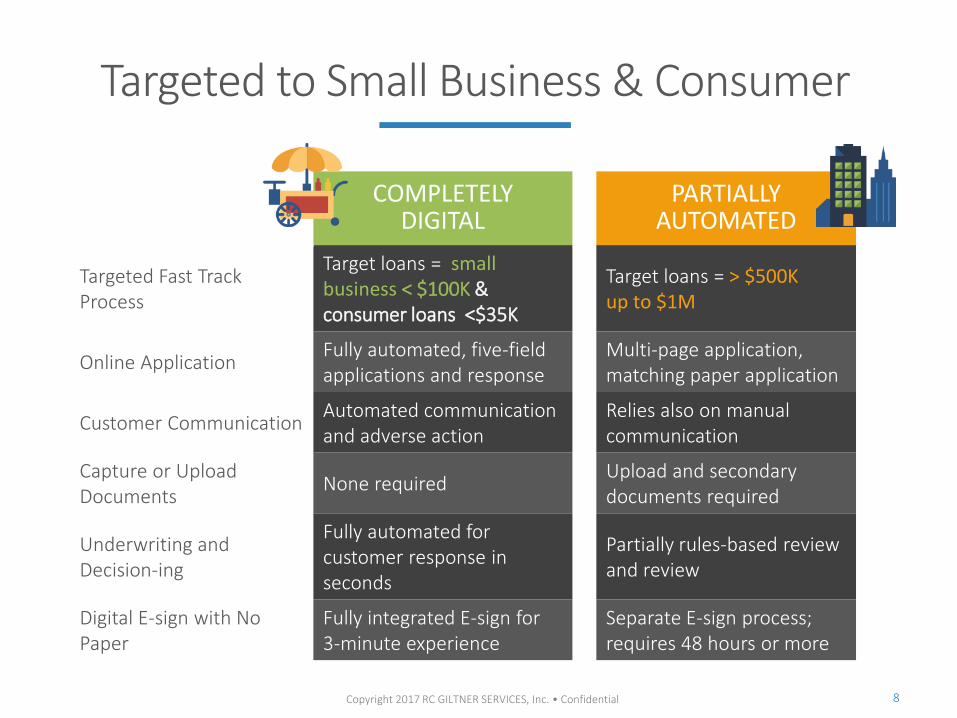

COMPLETELY DIGITAL

PARTIALLY AUTOMATED

Targeted Fast Track Process

Target loans = small business < $100K & consumer loans <$35K

Target loans = > $500K up to $1M

Online Application Fully automated, five-field applications and response

Multi-page application, matching paper application

Customer Communication Automated communication and adverse action

Relies also on manual communication

Capture or Upload Documents

None required Upload and secondary documents required

Underwriting and Decision-ing

Fully automated for customer response in seconds

Partially rules-based review and review

Digital E-sign with No Paper

Fully integrated E-sign for 3-minute experience

Separate E-sign process; requires 48 hours or more

Targeted to Small Business & Consumer

Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

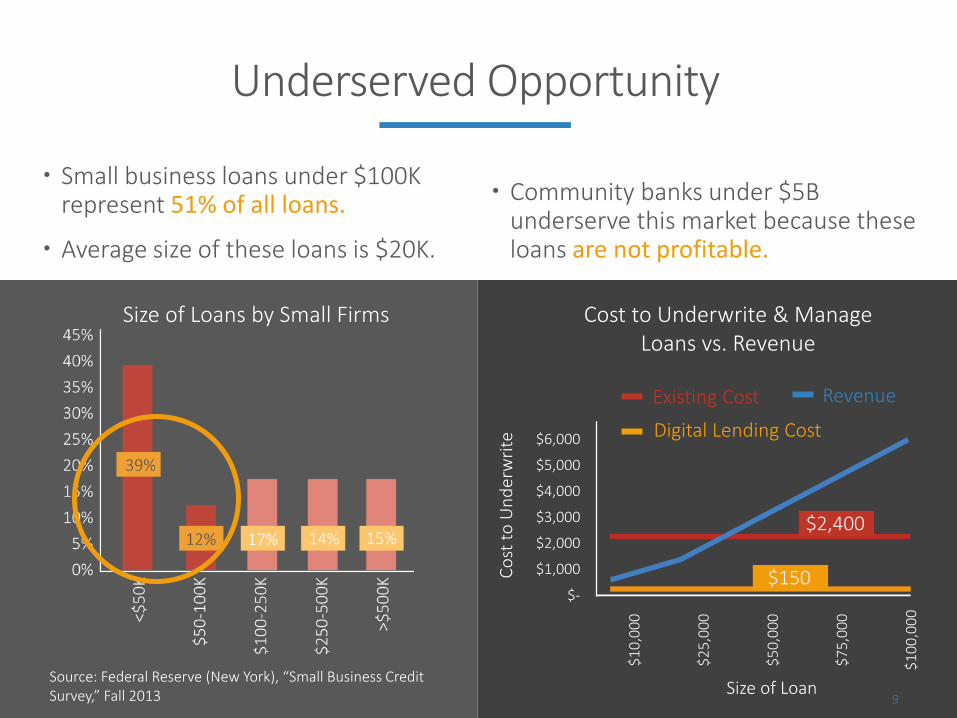

Small business loans under $100K represent 51% of all loans.

Average size of these loans is $20K.

9

Underserved Opportunity

Source: Federal Reserve (New York), “Small Business Credit Survey,” Fall 2013

Community banks under $5B underserve this market because these loans are not profitable.

Existing Cost Revenue

Cost to Underwrite & Manage Loans vs. Revenue

Digital Lending Cost

Size of Loans by Small Firms

$150

$2,400

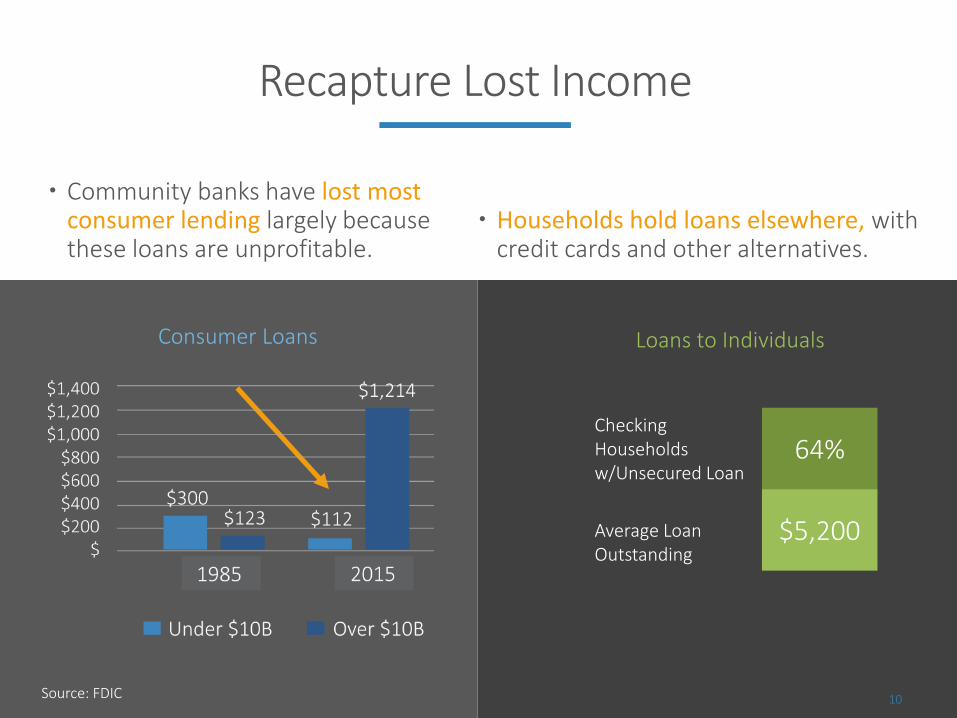

Community banks have lost most consumer lending largely because these loans are unprofitable.

10

Recapture Lost Income

Checking Households w/Unsecured Loan

64%

Average Loan Outstanding

$5,200

Source: FDIC

Consumer Loans

Households hold loans elsewhere, with credit cards and other alternatives.

Loans to Individuals

Community banks have the highest customer satisfaction with lending

11

Customers Want Speed & Simplicity

Source: 2015 Small Business Credit Survey, FRB, March, 2016.

Borrower Satisfaction by Institution Type

Borrower Satisfaction for Speed/Simplicity

However, they significantly lag online lenders for “simple application” and “speed of services.”

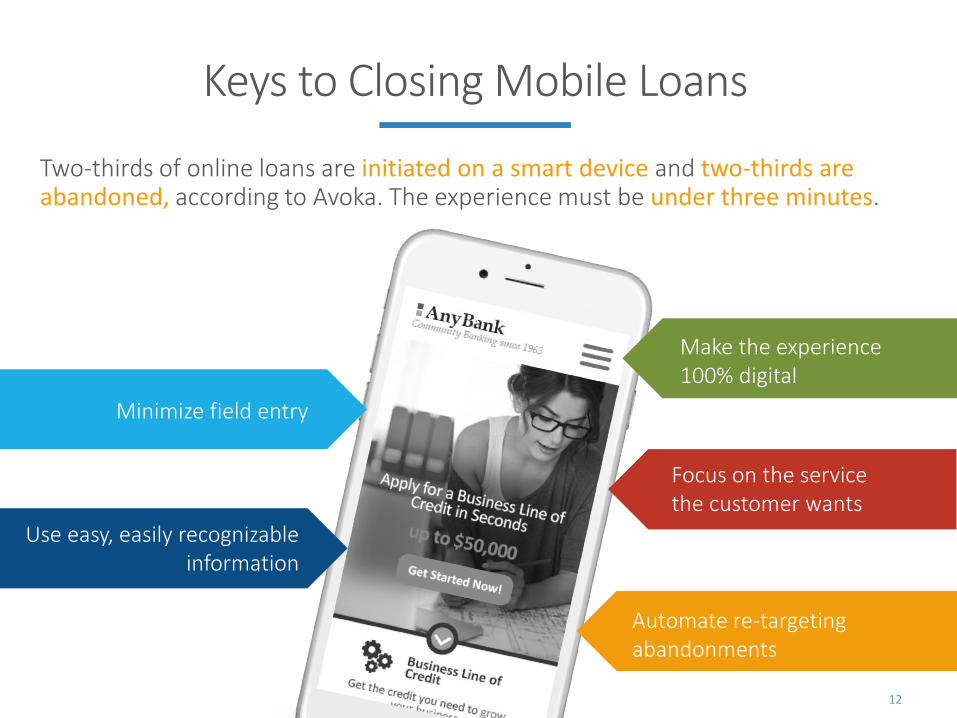

Two-thirds of online loans are initiated on a smart device and two-thirds are abandoned, according to Avoka. The experience must be under three minutes.

12

Keys to Closing Mobile Loans

Automate re-targeting abandonments

Minimize field entry

Use easy, easily recognizable information

Make the experience 100% digital

Focus on the service the customer wants

“ A sea change in banking economics is gathering strength–as digital grows the fight to hold on to customer relationships will be banks’ high stakes struggle.

The Fight for the Customer, McKinsey, 2015

13

They’re Coming for Your Customers

SMALL BUSINESS

REAL ESTATE

CONSUMER

SOLAR EDUCATION MEDICAL RECEIVABLES

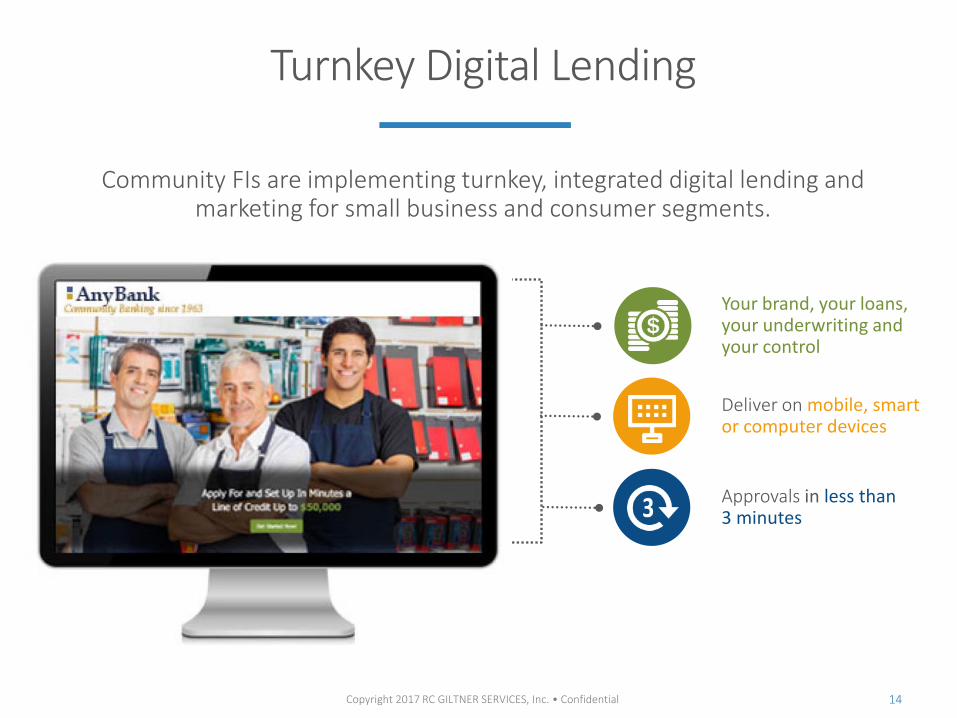

Community FIs are implementing turnkey, integrated digital lending and marketing for small business and consumer segments.

14 Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

Turnkey Digital Lending

Approvals in less than 3 minutes

Deliver on mobile, smart or computer devices

Your brand, your loans, your underwriting and your control

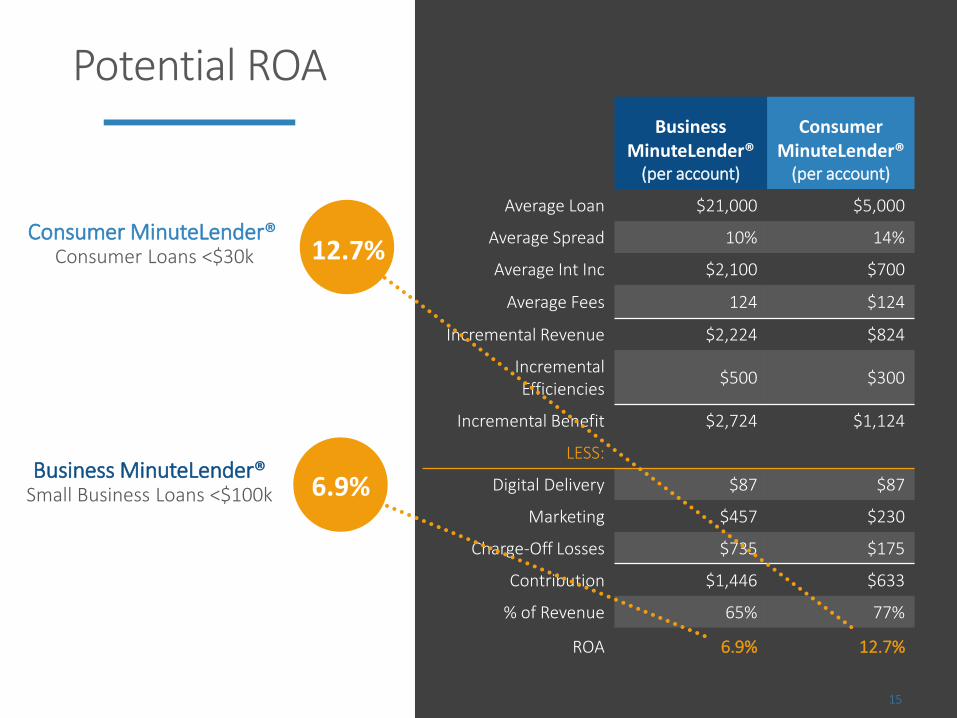

Business MinuteLender® Small Business Loans <$100k

15

Potential ROA Business

MinuteLender® (per account)

Consumer MinuteLender®

(per account)

Average Loan $21,000 $5,000

Average Spread 10% 14%

Average Int Inc $2,100 $700

Average Fees 124 $124

Incremental Revenue $2,224 $824

Incremental Efficiencies

$500 $300

Incremental Benefit $2,724 $1,124

LESS:

Digital Delivery $87 $87

Marketing $457 $230

Charge-Off Losses $735 $175

Contribution $1,446 $633

% of Revenue 65% 77%

ROA 6.9% 12.7%

Consumer MinuteLender® Consumer Loans <$30k 12.7%

6.9%

Business MinuteLender®

(per account)

Consumer MinuteLender®

(per account)

Average Loan $21,000 $5,000

Average Spread 10% 14%

Average Int Inc $2,100 $700

Average Fees 124 $124

Incremental Revenue $2,224 $824

Incremental Efficiencies

$500 $300

Incremental Benefit $2,724 $1,124

Less:

Digital Delivery $87 $87

Marketing $457 $230

Charge-Off Losses $735 $175

Contribution $1,446 $633

% of Revenue 65% 77%

ROA 6.9% 12.7%

16

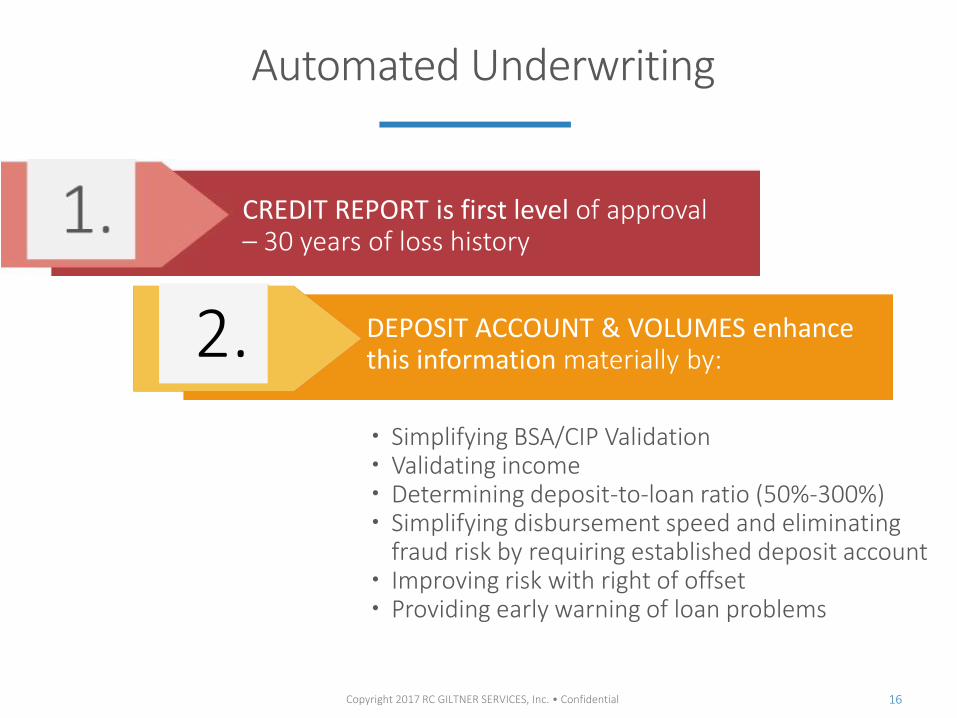

Automated Underwriting

Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

Simplifying BSA/CIP Validation Validating income Determining deposit-to-loan ratio (50%-300%) Simplifying disbursement speed and eliminating

fraud risk by requiring established deposit account Improving risk with right of offset Providing early warning of loan problems

CREDIT REPORT is first level of approval – 30 years of loss history

DEPOSIT ACCOUNT & VOLUMES enhance this information materially by:

17

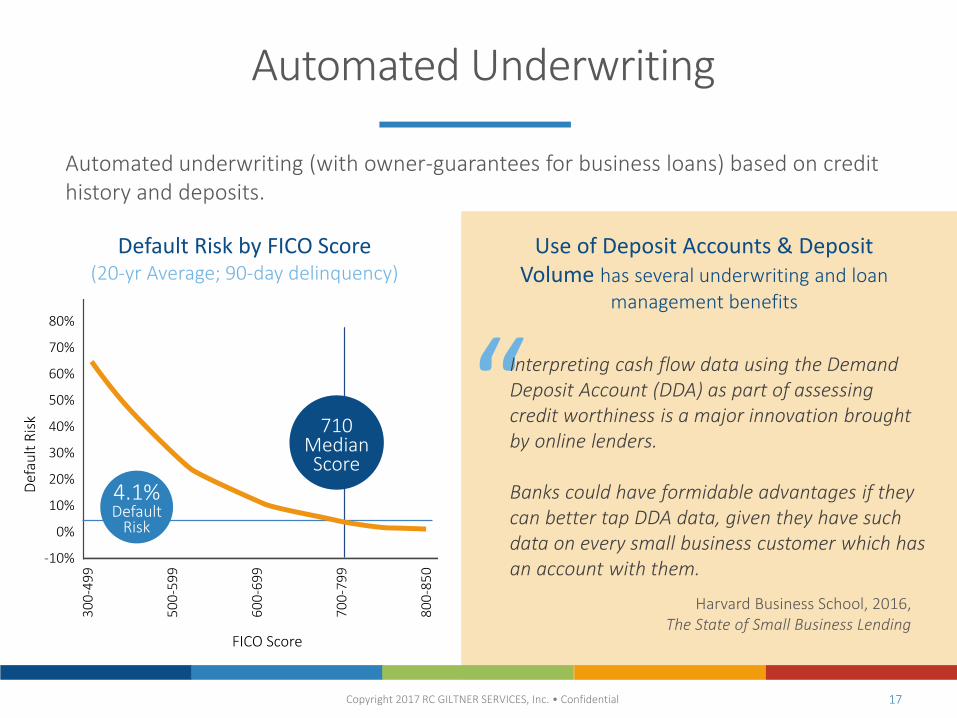

Harvard Business School, 2016, The State of Small Business Lending

Automated Underwriting

Use of Deposit Accounts & Deposit Volume has several underwriting and loan

management benefits

“

Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

Interpreting cash flow data using the Demand Deposit Account (DDA) as part of assessing credit worthiness is a major innovation brought by online lenders. Banks could have formidable advantages if they can better tap DDA data, given they have such data on every small business customer which has an account with them.

Automated underwriting (with owner-guarantees for business loans) based on credit history and deposits.

Default Risk by FICO Score (20-yr Average; 90-day delinquency)

710 Median Score

4.1% Default

Risk

18

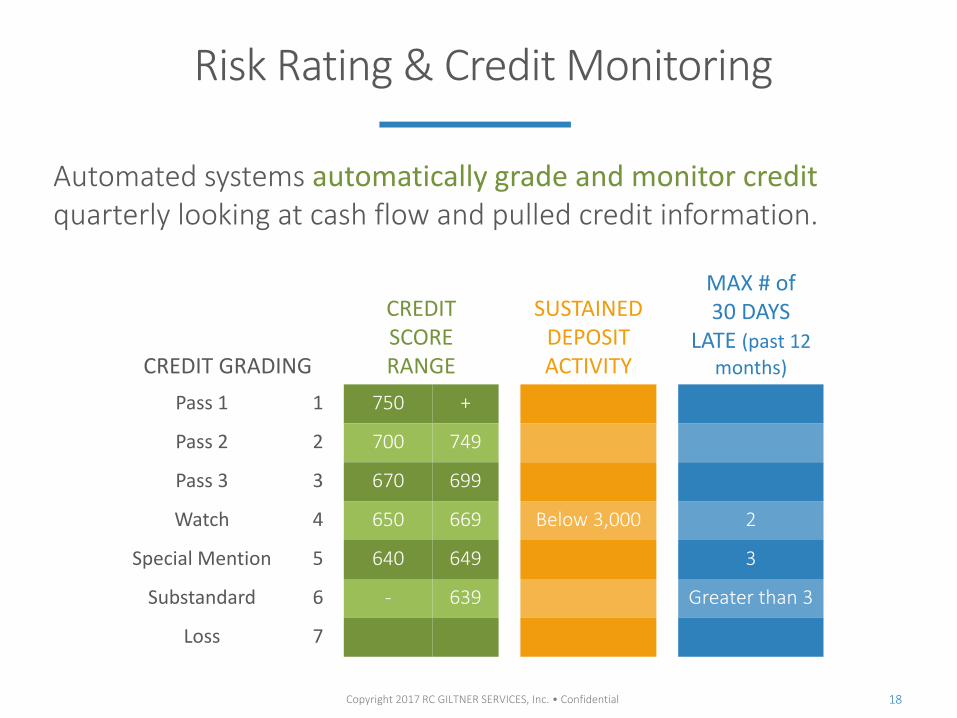

Automated systems automatically grade and monitor credit quarterly looking at cash flow and pulled credit information.

Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

Risk Rating & Credit Monitoring

CREDIT GRADING

CREDIT SCORE RANGE

SUSTAINED DEPOSIT ACTIVITY

MAX # of 30 DAYS

LATE (past 12 months)

Pass 1 1 750 +

Pass 2 2 700 749

Pass 3 3 670 699

Watch 4 650 669 Below 3,000 2

Special Mention 5 640 649 3

Substandard 6 - 639 Greater than 3

Loss 7

19 Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

Sales & Marketing

Sales All logins provided for sales management to assign leads to sales

Marketing Digital and Direct Marketing

Direct Mail Emails Digital Ads

Targeted Digital IP Addresses Target digital just like we

do with direct mail One-click to access digital

lending Collateral Material

Posters Counter cards Tent Cards Web Banner

SALES PROCESSES

DIGITAL TRACKING

SUPPORT

MARKETING TEMPLATES

Questions

May 9, 2017

Thank you for your time.

RCGILTNER Services, Inc.

For more info: Trevor Knott

SVP, BSG Financial Group

(781) 254-9647 [email protected]

In association with

22

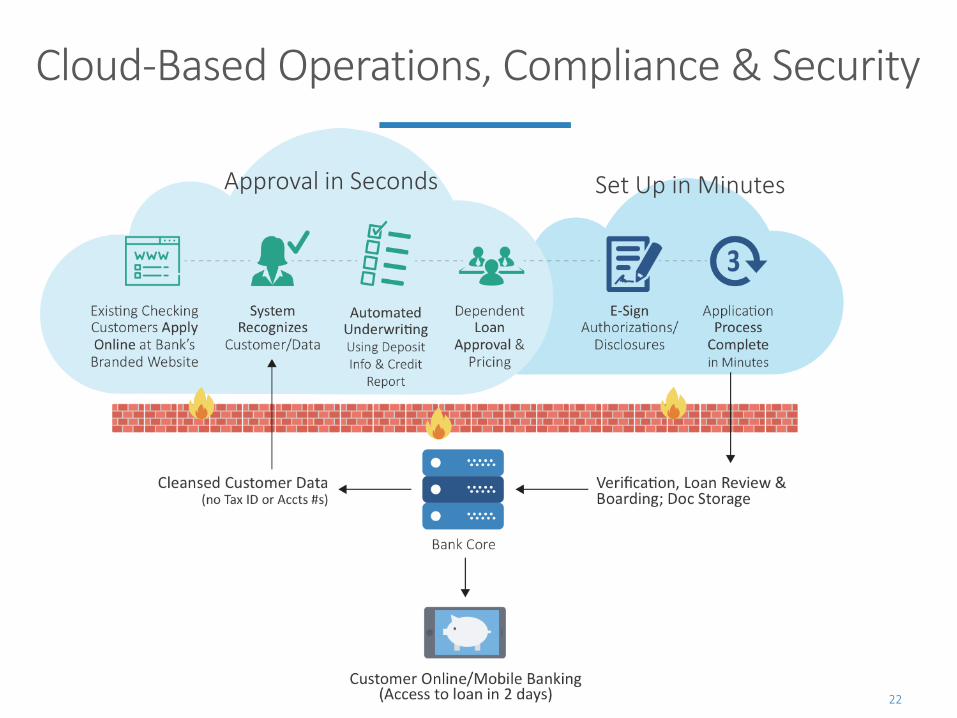

Cloud-Based Operations, Compliance & Security

Approval in Seconds Set Up in Minutes

23

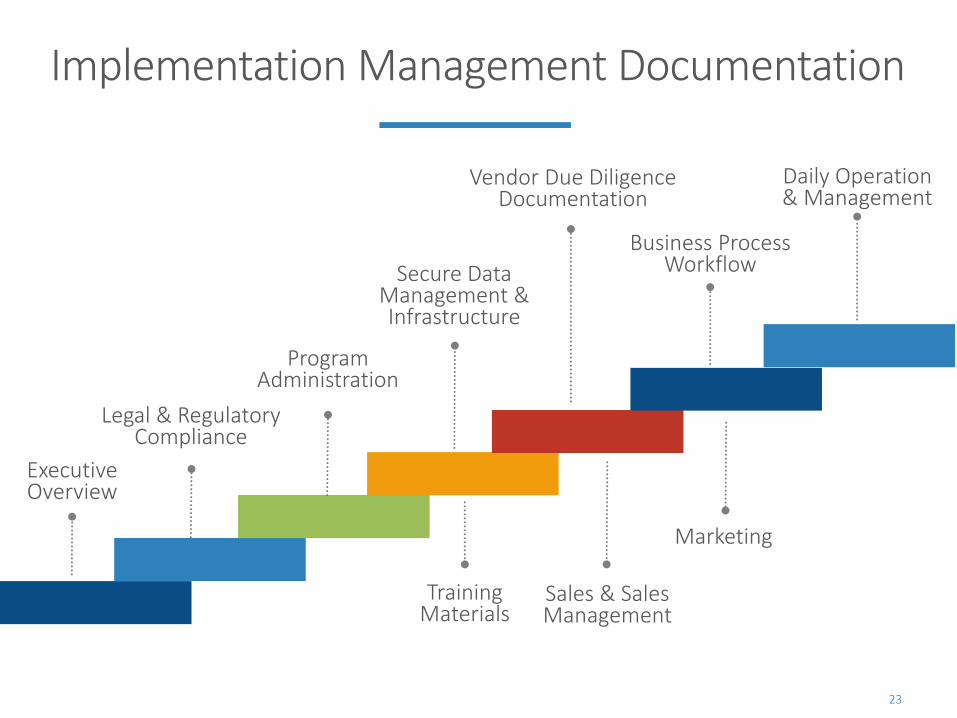

Implementation Management Documentation

Executive Overview

Legal & Regulatory Compliance

Program Administration

Secure Data Management & Infrastructure

Vendor Due Diligence Documentation

Business Process Workflow

Daily Operation & Management

Marketing

Sales & Sales Management

Training Materials

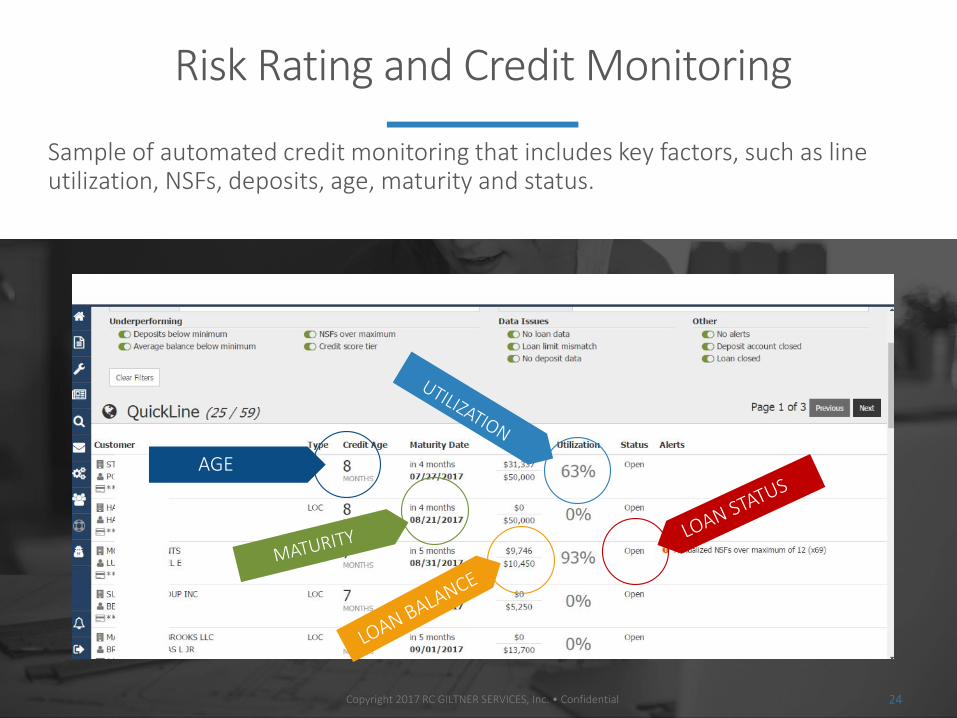

Sample of automated credit monitoring that includes key factors, such as line utilization, NSFs, deposits, age, maturity and status.

24 Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

AGE

Risk Rating and Credit Monitoring

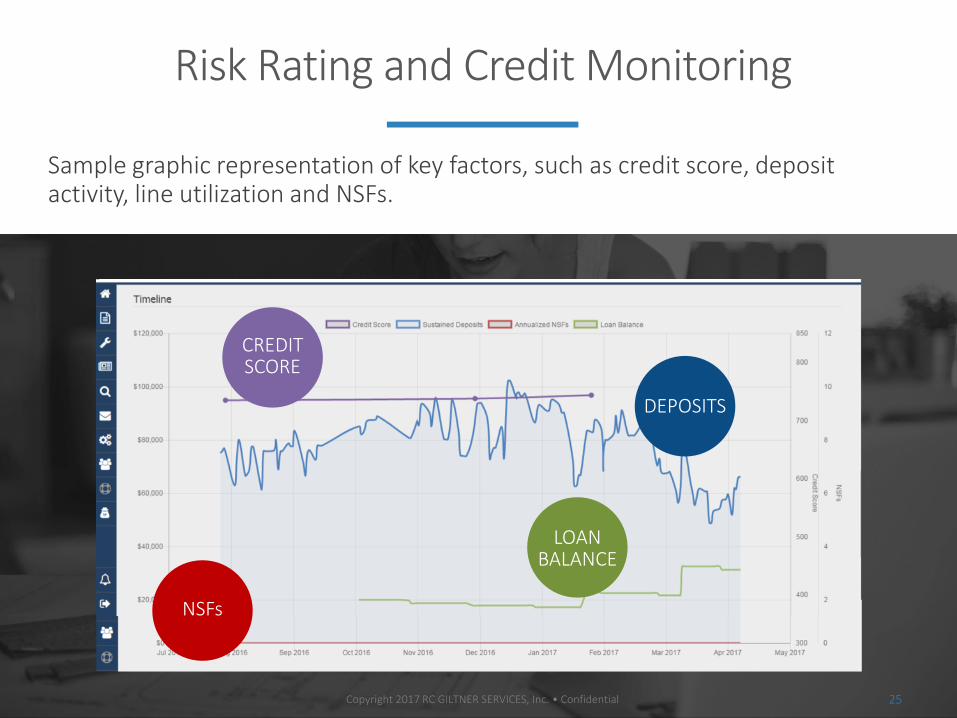

Sample graphic representation of key factors, such as credit score, deposit activity, line utilization and NSFs.

25 Copyright 2017 RC GILTNER SERVICES, Inc. • Confidential

Risk Rating and Credit Monitoring

CREDIT SCORE

DEPOSITS

NSFs

LOAN BALANCE