The Effects of MFA Quota Removal on Apparel...

215

Report No. 39994 - AFR VERTICAL AND REGIONAL INTEGRATION TO PROMOTE AFRICAN TEXTILES AND CLOTHING EXPORTS A CLOSE KNIT FAMILY? July 2007 Poverty Reduction and Economic Management 1 Southern Africa Africa region ___________________________________________________ _________

Transcript of The Effects of MFA Quota Removal on Apparel...

Report No. 39994 - AFR

VERTICAL AND REGIONAL INTEGRATIONTO PROMOTE AFRICAN TEXTILES AND CLOTHING EXPORTSA CLOSE KNIT FAMILY?

July 2007

Poverty Reduction and Economic Management 1Southern AfricaAfrica region

____________________________________________________________

Document of the World Bank________________________

ACRONYMS AND ABBREVIATIONS

ACP African Caribbean and Pacific AGOA African Growth and Opportunity ActATC WTO Agreement on Textiles and ClothingCMT Cut, make and trimCOMESA Common Market for Eastern and Southern AfricaEBA Everything but ArmsEPZ Export Processing ZoneFTAs Free trade agreementsGATT General Agreement on Tariffs and TradeGSP Generalized System of PreferencesLDCs Least Developed CountriesMFA Multifiber ArrangementMMTZ Malawi, Mozambique, Tanzania and ZambiaMUB Manufacture-under-bondROOs Rules of originSACU Southern African Customs UnionSADC Southern African Development CommunityT&C Textiles and clothingTCF Third-country fabricTMB Textiles Monitoring BodyWTO World Trade Organization

Vice President Obiageli K. EzekwesiliSector Manager Emmanuel AkpaTask Team Leaders Ian John Douglas Gillson, Caglar Ozden

2

TABLE OF CONTENTS

AcknowledgementsExecutive Summary

1. INTRODUCTION........................................................................................................................................1

2. PROTECTION AND PREFERENCES IN THE GLOBAL MARKET FOR TEXTILES AND CLOTHING......................................................................................................................................................3

2.1 THE AGREEMENT ON TEXTILES AND CLOTHING: QUOTAS HAVE GONE BUT HIGH TARIFFS REMAIN.....32.2 EU GSP AND EVERYTHING BUT ARMS..................................................................................................42.3 THE EU ACP/COTONOU AGREEMENT...................................................................................................52.4 US GSP AND THE AFRICAN GROWTH AND OPPORTUNITY ACT............................................................5

3. TRADE PATTERNS IN TEXTILES AND CLOTHING............................................................................7

3.1 CHINA DOMINATES IN WORLD EXPORTS OF TEXTILES AND CLOTHING..................................................73.2 TEXTILES AND CLOTHING EXPORTS ARE IMPORTANT TO SOME AGOA COUNTRIES..............................93.3 DEVELOPED COUNTRIES ARE THE MAIN MARKETS FOR IMPORTS OF TEXTILES AND CLOTHING............9

3.3.1 The US market for textiles and clothing is growing strongly but the sources of imports are changing................................................................................................................................................103.3.2 The EU market for textiles and clothing is fragmented and rules of origin are a constraint......11

4. APPAREL EXPORTS FROM AFRICA UNDER AGOA – PAST, PRESENT AND THE FUTURE....13

5. VERTICAL AND REGIONAL INTEGRATION IN AFRICAN TEXTILES AND CLOTHING TRADE........................................................................................................................................................................20

5.1 THE RATIONALE FOR VERTICAL AND REGIONAL INTEGRATION...........................................................205.2 INTRA-AGOA TRADE IN COTTON, YARN, FABRIC AND CLOTHING......................................................21

5.2.1 Cotton...........................................................................................................................................215.2.2 Yarn.............................................................................................................................................225.2.3 Fabric..........................................................................................................................................235.2.4 Clothing.......................................................................................................................................24

5.3 CONSTRAINTS TO VERTICAL AND REGIONAL INTEGRATION.................................................................255.3.1 Competitiveness and production capacity..................................................................................255.3.2 Quality and service delivery.......................................................................................................275.3.3 Lead times....................................................................................................................................285.3.4 Costs of production......................................................................................................................295.3.5 Rules of origin..............................................................................................................................335.3.6 Other policy constraints..............................................................................................................36

6. THE TEXTILES AND CLOTHING SECTOR IN SELECTED AFRICAN COUNTRIES.....................38

6.1 SOUTH AFRICA.....................................................................................................................................396.2 MAURITIUS...........................................................................................................................................436.3 MADAGASCAR......................................................................................................................................476.4 LESOTHO..............................................................................................................................................506.5 KENYA..................................................................................................................................................546.6 ZAMBIA................................................................................................................................................58

7. CONCLUSION..........................................................................................................................................61

REFERENCES...............................................................................................................................................63

LIST OF EXPERTS CONSULTED..............................................................................69

3

TABLES

TABLE 1: AFRICAN GROWTH AND OPPORTUNITY ACT ELIGIBLE COUNTRIES..........................6

TABLE 2: POTENTIAL REGIONAL SUPPLY CHAIN FOR T&C FOR AFRICAN COUNTRIES........25

TABLE 3: WAGE COSTS IN THE T&C SECTOR AMONG SELECTED AFRICAN COUNTRIES......30

TABLE 4: ELECTRICITY COSTS AMONG SELECTED COUNTRIES..................................................31

TABLE 5: FREIGHT COSTS AMONG SELECTED COUNTRIES...........................................................32

TABLE 6: WATER AND TELECOMMUNICATIONS COSTS AMONG SELECTED COUNTRIES....33

TABLE 7: NUMBER OF WORKERS AND FIRMS BY PRODUCT IN LESOTHO: 2004-2005..............52

TABLE 8: THE IMPACT OF AGOA ON CLOTHING EXPORTS FROM KENYA’S EPZ......................57

Table 9: Phase-out of quotas under the ATC.................................................................................................74

FIGURES

FIGURE 1: APPAREL EXPORTS TO THE US ($ MILLIONS).................................................................13

FIGURE 2: RELATIVE PRICES OF APPAREL EXPORTS (WEIGHTED BY EXPORT VALUE)........15

FIGURE 3: RELATIVE PRICES OF EXPORTS (WEIGHTED BY US IMPORT VALUE).....................16

FIGURE 4: MARKET SHARES OF APPAREL EXPORTERS TO THE US.............................................16

FIGURE 5: AVERAGE RELATIVE PRICES..............................................................................................17

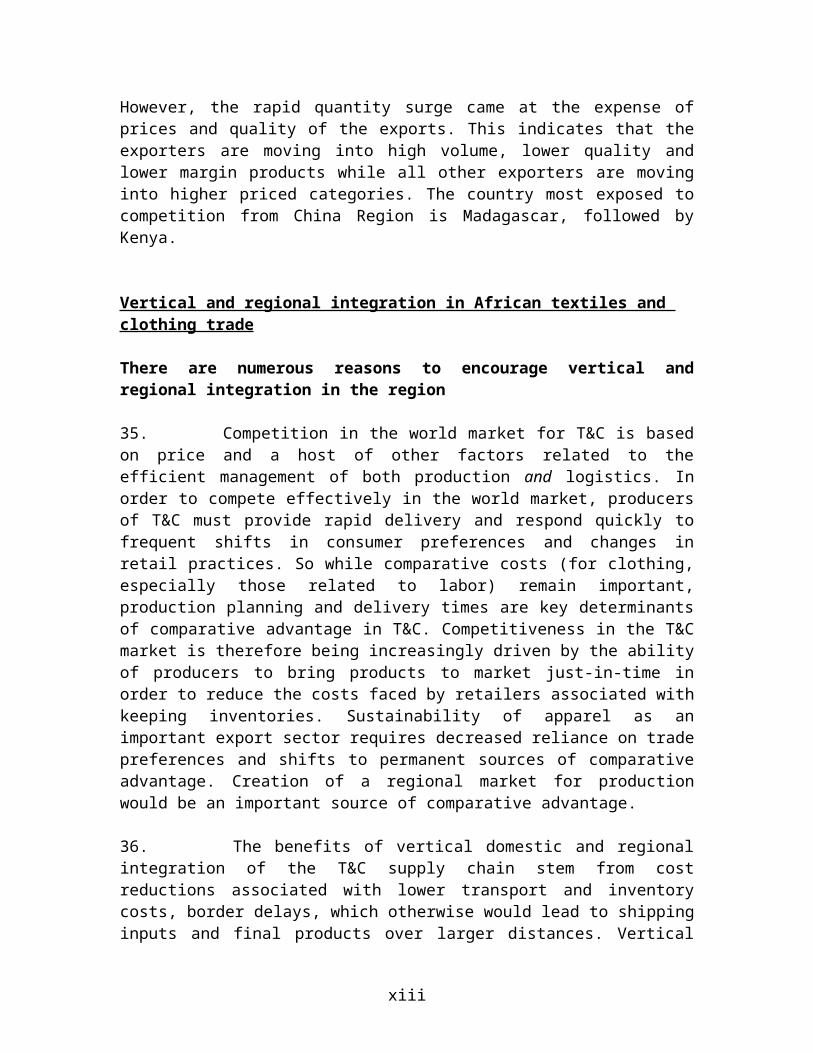

FIGURE 6: MARKET SHARES...................................................................................................................18

FIGURE 7: MARKET SHARE OF THE CHINA REGION IN EXPORT CATEGORIES.........................18

FIGURE 8: MARKET SHARE OF QUOTA COUNTRIES IN EXPORT CATEGORIES.........................19

FIGURE 9: MAIN INTRA- AND EXTRA-REGIONAL FLOWS OF AGOA TRADE IN COTTON........21

FIGURE 10: MAIN INTRA- AND EXTRA-REGIONAL FLOWS OF AGOA TRADE IN YARN..........22

FIGURE 11: MAIN INTRA- AND EXTRA-REGIONAL FLOWS OF AGOA TRADE IN FABRIC.......23

Figure 12: Main intra- and extra-regional flows of AGOA trade in clothing................................................24

ANNEXES

ANNEX 1: THE WTO AGREEMENT ON TEXTILES AND CLOTHING................................................73

ANNEX 2: MFN TARIFFS ON INTERNATIONAL TRADE IN TEXTILES............................................75

ANNEX 3: MFN TARIFFS ON INTERNATIONAL TRADE IN CLOTHING..........................................76

ANNEX 4: THE EU’S GSP...........................................................................................................................77

ANNEX 5: EU TARIFFS ON TEXTILES AND CLOTHING PRODUCTS 2005......................................79

ANNEX 6: LIST OF LEAST DEVELOPED COUNTRIES.........................................................................80

ANNEX 7: EU TRADE ARRANGEMENTS WITH THE ACP COUNTRIES...........................................81

ANNEX 8: US TARIFFS ON TEXTILES AND CLOTHING PRODUCTS 2005......................................83

ANNEX 9: THE AFRICAN GROWTH AND OPPORTUNITY ACT.........................................................84

ANNEX 10: TRADE DATA AVAILABILITY............................................................................................85

ANNEX 11: MAJOR EXPORTERS OF TEXTILES 1994-2005 (EXCLUDING INTRA-EU TRADE)....87

4

ANNEX 12: AGOA EXPORTS OF TEXTILES 1994-2005.........................................................................88

ANNEX 13: WORLD EXPORTS OF CLOTHING 1994-2005 (EXCLUDING INTRA-EU TRADE)......89

ANNEX 14: AGOA EXPORTS OF CLOTHING 1994-2005.......................................................................90

ANNEX 15: THE IMPORTANCE OF AGOA EXPORTS OF T&C, 2004.................................................91

ANNEX 16: WORLD IMPORTS OF TEXTILES 1994-2005 (EXCLUDING INTRA-EU TRADE).........92

ANNEX 17: AGOA IMPORTS OF TEXTILES 1994-2005.........................................................................93

ANNEX 18: WORLD IMPORTS OF CLOTHING 1994-2005 (EXCLUDING INTRA-EU TRADE).......94

ANNEX 19: AGOA IMPORTS OF CLOTHING 1994-2005.......................................................................95

ANNEX 20: US IMPORTS OF TEXTILES 1994-2005...............................................................................96

ANNEX 21: AGOA EXPORTS OF TEXTILES TO US 1994-2005............................................................97

ANNEX 22: US IMPORTS OF CLOTHING 1994-2005..............................................................................98

ANNEX 23: AGOA EXPORTS OF CLOTHING TO US 1994-2005..........................................................99

ANNEX 24: EU IMPORTS OF TEXTILES 1994-2005 (EXCLUDING INTRA-EU TRADE)................100

ANNEX 25: AGOA EXPORTS OF TEXTILES TO EU 1994-2005..........................................................101

ANNEX 26: EU IMPORTS OF CLOTHING 1994-2005 (EXCLUDING INTRA-EU TRADE)..............102

ANNEX 27: AGOA EXPORTS OF CLOTHING TO EU 1994-2005........................................................103

ANNEX 28: SEED COTTON PRODUCTION IN AGOA COUNTRIES 1994-2005...............................104

ANNEX 29: AGOA COTTON LINT PRODUCTION AND EXPORTS 2003..........................................105

ANNEX 30: INTRA AGOA COTTON TRADE 2003 (US$ 1000S)..........................................................106

ANNEX 31: THE IMPORTANCE OF AGOA REGIONAL TRADE IN COTTON, YARN, FABRIC AND CLOTHING (2003)......................................................................................................................................108

ANNEX 32: INTRA AGOA YARN TRADE 2003 (US$ 1000S)...............................................................109

ANNEX 33: INTRA AGOA FABRIC TRADE 2003 (US$ 1000S)...........................................................111

ANNEX 34: INTRA AGOA CLOTHING TRADE 2003 (US$ 1000S).....................................................113

ANNEX 35: COSTS OF DOING BUSINESS.............................................................................................115

ANNEX 36: SEED COTTON YIELDS IN SOUTHERN AND EASTERN AFRICA 1994-2005............116

ANNEX 37: COTTON LINT EXPORTS FROM SOUTHERN AND EASTERN AFRICA 1994-2004...117

ANNEX 38: COTTON LINT IMPORTS FOR SOUTHERN AND EASTERN AFRICA 1994-2004.......118

5

ACKNOWLEDGMENTS

This report presents the results of research undertaken by the World Bank and close dialogue with the private sector and researchers in six African countries: Kenya, Lesotho, Madagascar, Mauritius, South Africa and Zambia.

The report was prepared by a team consisting of Ian Gillson (Task Team Leader, AFTP1), Caglar Ozden (Task Team Leader, DECRG) and Fahrettin Yagci (AFTP1). The team received strong support from Robert Keyfitz (AFTP1), Marie Sheppard (AFTPS), Mombert Hoppe (PRMTR), Lolette Kritzinger-van Niekerk (AFCRI), Shirley Faragher (AFCS1), Beatrice Abade (AFCE2) and Paula Lamptey (AFCS1). Matilde Bordon (AFTPS) provided outstanding advice for the Kenya component of the work. The peer reviewers were Sonia Plaza (AFCRI) and Paul Brenton (PRMTR).

The report was prepared under the supervision of Emmanuel Akpa, Sector Manager for AFTP1. He offered conceptual guidance, provided critical analytical advice and ensured quality control and management support. Assistance with editing, dissemination and budget management was provided by Rose Kumsinda (AFTP1).

On the private sector side the team would like to thank all of the textile and clothing firms we visited on field interviews in Kenya, Mauritius, South Africa and Zambia as well as business associations and local experts who provided important insights for this study. An exhaustive list of those consulted is included at the end of the report. The field interviews were facilitated by Joop de Voest who kindly provided details of firms in the region to approach.

6

EXECUTIVE SUMMARYIntroduction

1. Export diversification into higher value-added products and away from primary commodities with their associated price risks (volatility and long-term decline) remains a major trade policy objective for many African countries. Textiles and clothing (T&C) are sectors that provided an opportunity for a few African countries for export diversification. Clothing production is labor intensive, involving relatively low start-up costs and easily transferable technology. Labor requirements can be met with low and semi-skilled workers, especially women. Consequently, countries with competitive labor costs, especially in South and East Asia, have been able to capture significant shares of the world market. Despite the potential benefits and their various sources of comparative advantage, few African countries, until recently, have managed to establish a meaningful presence in the world clothing market. Consequently, despite being a net exporter of cotton Africa remains a net importer of textiles and clothing.

2. Nevertheless, clothing exports from sub-Saharan Africa have expanded rapidly during the past decade mainly due to the unilateral market access preferences granted by the US and the EU. Since most other developing countries faced restrictive access to the European and US markets, due to quotas and high tariffs, the quota-free and duty-free access granted to African exporters of clothing led to rapid export growth. A main feature of these preferences, especially the Africa Growth and Opportunity Act (AGOA) of the US, has been the permission to use imports of third-country yarns and fabrics in the production of exports while maintaining eligibility for preferences. This allows cheap fabrics, often sourced from Asia, to be processed in Africa and exported to the US. Over 85% of the clothing exports currently eligible for AGOA preferences in the US market are made from third-country fabric. As a result, apparel exports from eligible AGOA countries to the US have increased threefold.

3. For the AGOA countries, the share of T&C exports in their total exports is rather low, at 0.5% and 2.8%, respectively. This is mainly due to the large share of raw materials, minerals and oil in the exports from the region. But for some individual countries, T&C form an important share of manufactured exports. These are Lesotho (accounting for 97% of total exports), followed by Mauritius (51%), Madagascar (41%), Cape Verde (39%), Swaziland (25%) and Kenya (12%).

4. The future of clothing production for export in sub-Saharan Africa is rather uncertain as it faces two major challenges:

increased competition from large and competitive producers such as China, Bangladesh, India, and Pakistan following the phase-out of the quotas after the expiration of the WTO Agreement on Textiles and Clothing (ATC); and,

expiration of the third-country fabric derogation under AGOA scheduled to occur in 2013.

5. After the expiration of the ATC in 2005, AGOA countries have seen their recent growth of exports turn into a decline. Many factories have closed, resulting in the loss of tens of thousands of jobs in Kenya, Lesotho, Madagascar, Mauritius, Namibia, South Africa and Swaziland. Producers in sub-Saharan Africa can no longer depend on displaced production from quota-bound countries to boost their exports. Instead, they need to be more cost competitive, deliver their products to market on-time, and, be prepared to meet higher quality and service requirements. The expiration of the third-country fabric derogation under AGOA will generate a further significant decline for the African clothing industry unless the region is able to supply all of the various yarns and fabrics that US buyers demand.

6. This study explores the options the region has to overcome these two challenges. In particular, it assesses the potential for and identifies challenges to the regional and vertical integration in the sector. Timing is crucial since both the EU and the US have recently imposed limited trade restrictions on China (until 2008) to protect certain domestic T&C industries. These safeguards might provide a brief opportunity for sub-Saharan African producers to integrate their T&C sector both domestically and regionally.

7. In terms of policy recommendations, in addition to sector-specific policies, the report suggests that African countries should implement economy-wide reforms for long-term competitiveness that would benefit all sectors. These would include i) addressing infrastructure and regulatory weaknesses that limit access to and raise the cost of backbone services: electricity, water, transport, telecommunications, ports and finance; ii) reviewing trade, tax and labor market policies that limit the incentives to invest in productive activities including external tariffs and rules of origin in regional trade agreements that limit access to the most appropriate and lowest cost inputs; and, iii) developing pro-active export and investment promotion policies to overcome informational barriers that limit access to foreign markets and investors.

8. For developed countries, the EU should implement non-restrictive rules of origin that support exports of clothing from Africa under the available preference schemes by allowing efficient sourcing of inputs. The US should broaden its coverage of textiles under AGOA (for all beneficiaries not just those classified as lesser developed) to encourage investment in African spinning and weaving. And all industrialized countries should provide aid for trade to support countries that implement well-defined competitiveness reform programs that address the key infrastructure and policy constraints that limit exports and investment in goods and services.

ii

Protection and preferences in the global market for textiles and clothing

With the removal of the ATC, quotas are gone but high tariffs remain

9. On January 1 2005, the ATC expired. The quotas that once shaped the global apparel trade were removed and tariffs were left as the only trade restrictions in place. The ATC and its predecessor, the Multi-Fiber Arrangement (MFA), had governed world trade in T&C by providing a framework for bilateral and unilateral restrictions and limiting imports into developed-country markets whose domestic industries were facing decline. Preferential access to protected markets favored exports from some developing countries (e.g. Kenya) while quotas restricted exports from others (e.g. India and China).

10. A key impact of the ATC is that restrictions on imports from the more competitive East and South Asian manufacturers (such as China, Japan, South Korea and Hong Kong) led to a displacement of clothing production to less developed but less competitive locations such as Mexico, Central America, Bangladesh, Sri Lanka and Mauritius. The initial driving force behind this process was large retailers such as Wal-Mart and brands such as Nike who began to outsource production to low-wage countries. For example, in the 1990s Korean and Taiwanese producers expanded their operations to the Caribbean and Sub-Saharan Africa.

11. While ATC required the eventual elimination of quotas, it did not mandate a reduction in tariff protection. Consequently, the global market for T&C products remains heavily distorted, especially in OECD markets for finished products. Average applied tariffs on imports of textiles are 6.7% in the EU and 7.5% in the US but are higher for imports of clothing at 11.5% and 10.8% respectively. However, in many categories, the US and the EU impose tariffs that are over 20% whereas their average tariffs on manufactured goods are below 3%. Tariff peaks on imports of certain T&C products can reach 32 percent in the US.

12. Since apparel exports are subject to some of the highest tariffs on manufactured goods in the major importing OECD countries, preferential access offered by the US and EU may still make a substantial positive impact on the export volumes of eligible countries. However, the rules of origin (ROO) in these preference programs, particularly in the EU, have imposed serious constraints on exporters.

AGOA is the most generous among the four preferential programs for sub-Saharan exports of textiles and clothing

13. There are four preferential arrangements.

EU and the US GSP. The EU implemented its Generalised System of Preferences (GSP) in 1971. The EU GSP can be used by all developing countries. For textiles, the general GSP reduces average EU import tariffs from 6.70% (under MFN) to 5.42% and, for clothing, from 11.54% to 9.23%. The most favourable

iii

arrangements under the EU’s GSP are reserved for LDCs. The US GSP program offers duty-free treatment for specified products from designated countries but excludes most T&C products. Consequently, the US GSP reduces average US import tariffs marginally since most categories are excluded. Tariffs are lowered for few eligible categories textiles from 7.5% (under MFN) to only 7.4% and, for clothing, from 10.8% to 10.6%.

EU Everything but Arms (EBA). With its Everything but Arms (EBA) amendment, effective from March 2001, the EU extended duty- and quota-free access to all products originating in LDCs, except arms and ammunition. This covers (where the ordinary GSP does not) all agricultural products, including ‘sensitive’ products (banana, rice, beef, sugar). In T&C, the African LDCs cannot benefit from the EBA initiatives because (a) the ROO require double transformation (two significant processes should be performed within the country), and (b) there is no cumulation provision for inputs originating in other African countries (clothing must be manufactured of fabrics made in the exporting country or the EU.)

The EU ACP/Cotonou Agreement. 77 African, Caribbean and Pacific (ACP) countries (excluding South Africa) have traditionally received more generous tariff preferences on a broader range of products than those covered under the EU’s GSP. The ACP/Cotonou Agreement eliminates import duties on clothing meeting its ROO. For textiles, it reduces average EU import tariffs from 6.7% (under MFN) to 0.3%. ROOs allow full ACP cumulation for almost all products.

US GSP and the African Growth and Opportunity Act. For sub-Saharan exporters, the US introduced AGOA in 2000 and expanded it three times afterwards. The current program extends until 2015. 37 of 48 Sub-Saharan African countries are AGOA-eligible. The main advantage is its extension of product coverage to include almost all clothing and textiles products. A second advantage is the eligibility guarantee for longer terms – up to eight years – whereas GSP needs to be renewed by the US congress every year. Finally, AGOA provides very generous and flexible ROOs for eligible LDCs. It requires only single transformation until 2013 - the third-country fabric (TCF) derogation. The only major countries that are currently ineligible for the use of the TCF derogation are Mauritius and South Africa.

Trade patterns in textiles and clothing

14. The pattern of trade in T&C has been shaped by two factors. First, the MFA/ATC regime served as a negative preference system, helping some developing country suppliers (such as Central American and sub-Saharan African countries) at the expense of others (many East and South Asian countries such as China and India). The current tariff levels and preference programs continue this pattern. In short, quotas in T&C shielded

iv

less competitive suppliers in Latin America and Africa from competition from Asian exporters.

15. Second, the emergence of global supply chains for T&C has provided retailers with the ability to increasingly manage their supply networks and dictate non-price conditions such as quality, delivery schedule and choices over raw materials.

China dominates in world exports of textiles and clothing

16. China region1 is the world’s largest exporter of T&C. Following the end of the ATC, China region’s world market share has risen from 32.8% in 2004 to 36.3% in 2005 for textiles and from 39.3% to 42.4% in the same period for clothing.

17. This increase in market share, largely in the US and EU, has led to the imposition of safeguards on Chinese T&C products until December 2008. Other countries, such as Turkey, Argentina, Brazil and South Africa have also imposed safeguards on imports of Chinese T&C products or have taken steps to be able to use them. After these safeguards are removed, many analysts expect the country’s market share to grow to more than 50%. According to some projections, the elimination of quotas have transformed T&C manufacturing so drastically that it will eventually resemble footwear and toys, in which over 90% of all global trade is imported from China.

18. Other major exporters of textiles are the EU, US, India and South Korea. In 2004, the largest AGOA exporters of textiles were South Africa, followed by Mauritius, Nigeria and Tanzania, accounting for 82% of total exports from the region.

19. In the clothing sector, the major exporters (in addition to the China region) are the EU, Turkey, Bangladesh, Mexico and India. In 2004, the largest AGOA exporters of clothing were Mauritius, followed by Madagascar, Lesotho, Kenya and South Africa, jointly accounting for 86% of total exports from the region.

Developed countries are the main markets for imports of textiles and clothing

20. In 2004, the largest importer of textiles in the world was the EU (17%) followed by the US (16%). AGOA countries are net importers of textiles, accounting for 1.7% of world imports in 2000 which increased to 2.4% in 2004.

21. For the clothing sector, the largest importer was the US (34%) followed by the EU (33%) in 2004. Although there is a rather small and specialized clothing industry left in the US and Japan, a significant domestic clothing sector remains in the EU, especially in Southern Europe. AGOA countries account for 0.5% of world clothing imports.

1 China region includes China, Taiwan (China), Hong Kong and Macao which is treated as a single entity for the purposes of this report.

v

The US market for textiles and clothing is growing strongly but the sources of imports are changing

22. The growth rate of US imports of textiles during 1994-2005 was 7.8% per year in nominal dollar terms. The second half of the 1990s witnessed important changes in the source of US imports of T&C. While Mexico, China region (the largest supplier of textiles to the US market with a share of 35%), India and Pakistan have increased their shares, the EU and South Korea have lost market share.

23. US imports of clothing grew more slowly than imports of textiles during 1994-2005, at an average annual rate of 6.5% in nominal dollar terms. The shares of China (24%) and Mexico increased, while the shares of the EU and South Korea decreased. US clothing imports from the Caribbean and Central America remained relatively stable.

24. The majority of sub-Saharan African clothing exports to the US have entered under AGOA, the principal mechanism stimulating and maintaining clothing production in these countries. Eligible sub-Saharan African countries shipped over 90% of their clothing exports to the US under AGOA preferences. Following the introduction of AGOA in 2000, the share of AGOA countries in US clothing imports increased from 1.1% in 1999 to 2.7% in 2004 before falling to 2.1% in 2005. Imports of textiles (not covered under AGOA until 2007) from the eligible countries remained largely unchanged (about 0.2%).

The EU market for textiles and clothing is fragmented and rules of origin are a constraint

25. Intra-EU trade accounted for 68% of EU’s textile imports in 1994, falling to 59% in 2004. Extra-EU imports of textiles grew by an average of 4.5 percent per year in nominal dollar terms over the same period. Behind this import growth is a substantial shift from intra-EU trade to imports from lower cost suppliers. Turkey’s market share, following the introduction of the EU-Turkey customs union in 1996, rose from 7.1% in 1994 to 15.0% in 2005. China region increased its market share of EU textile imports from 14.0% in 1994 to 24.0% in 2004, reaching 28.7% in 2005. Among those countries that lost market share are Switzerland, South Korea, Indonesia and the US. AGOA countries maintained their EU market share, accounting for 1.3% of total extra-EU imports of textiles.

26. Intra-EU imports of clothing as a share of the total EU imports fell from 46% to 31% over the same period with imports from third-country suppliers growing by an average of 7.8% per year. China region is largest supplier of clothing to the EU market: its share in total extra-EU clothing imports decreased from 31.0% in 1994 to 29.1% in 2004, but increased to 35.7% in 2005. Turkey is the second largest supplier and its share of extra-EU clothing imports rose from 11.2% to 14.9% over the same period. Romania has more than doubled its market share, from 3.2% in 1994 to 7.3% in 2004. In comparison to textiles, the share of imports from AGOA countries in total extra-EU imports of clothing fell from 2.3% in 1994 to 1.4% in 2004. Mauritius is the largest

vi

exporter of clothing to the EU, followed by Madagascar. South African exporters supply specialized clothing to the UK market.

27. A key factor in explaining why exports to the US have grown much faster than those to the EU is the ROOs of the preference programs. The EU rules do not allow producers in African LDCs the flexibility they (currently) have under the AGOA to source fabrics from anywhere.

Clothing exports under AGOA

28. The initial performance of the export sectors that targeted the US market under AGOA was remarkable. However, when the ATC quotas faced by South and East Asian countries were removed, exports from many AGOA eligible countries declined sharply. This pattern indicates the relative fragility of the apparel export industries in these countries and their over-reliance on the restrictions imposed on competing exporters from other developing countries.

29. An interesting picture emerges on the impact of AGOA preferences and of the recent removal of ATC quotas faced by major exporters in South and East Asia. A detailed analysis of the data for 1996-2006 shows the following characteristics of the apparel exports to the US:

AGOA benefited only a handful of countries, although a large number of countries are eligible.

30. Apparel exports from the region to the US increased rapidly after the implementation of AGOA in 2000. However, only a handful of the eligible countries really took advantage of these preferences. Even though dozens of countries were eligible, over 95 percent of the apparel exports to the US since 2000 were from Lesotho, Kenya, Madagascar, Mauritius, Swaziland and South Africa. Of these countries, South Africa and Mauritius were existing exporters before AGOA. In other words, AGOA really benefited Lesotho, Kenya, Madagascar and Swaziland. The vast majority of the apparel exports from these countries go to the US which implies exporters in these countries completely rely on AGOA preferences and AGOA failed to create strong apparel industries which can compete in other markets (such as the EU).

The sharp decline in exports under AGOA is due to the expiry of the ATC and the changes in the apparel industry.

31. Apparel exports to the US peaked in 2003 for Mauritius and South Africa and in 2004 for the other exporters. Since then, the decline in exports has been rather dramatic for some of these countries. For example, South African and Mauritian exports declined by 65 percent and 50 percent, respectively. Other countries weathered slightly better with declines ranging from 25 percent (Swaziland and Madagascar) to 15 percent in Lesotho and 5 percent in Kenya.

vii

32. A key factor for the decline is the change in the nature of apparel industry. Apparel retail became dominated by large chains (such as Wal Mart, Carrefour, GAP) and labels (such as Polo, Levi’s) which do not produce any of their merchandise. In many cases they design the product and outsource the production to a manufacturer. They have strict requirements for the fabric, other raw materials as well as logistics details such as delivery frequency, location and schedule. Most retailers prefer to carry low inventories and require merchandise to be delivered in small quantities as they are sold. In short, exporters that manage to integrate themselves into the supply chains of the major retailers, deliver the products on short notice and satisfy all the requirements earn superior profits. Countries with well established textiles industries and low transportation costs have natural advantages and, unfortunately, this is not the case with most sub-Saharan African countries that suffer from infrastructure shortcomings and relatively underdeveloped industries.

The data show that African exporters of apparel are moving into higher quality T&C products while China Region concentrates on lower quality, lower margin, high volume products.

33. Despite the sharp decline in export volumes during the last three years, relative prices of exports particularly from Mauritius, South Africa and Madagascar increased which indicates that these exporters are moving into higher quality products.

34. China Region captured significant market share from other exporters over the last several years, mostly at the expense of the preference recipients in Latin America. However, the rapid quantity surge came at the expense of prices and quality of the exports. This indicates that the exporters are moving into high volume, lower quality and lower margin products while all other exporters are moving into higher priced categories. The country most exposed to competition from China Region is Madagascar, followed by Kenya.

Vertical and regional integration in African textiles and clothing trade

There are numerous reasons to encourage vertical and regional integration in the region

35. Competition in the world market for T&C is based on price and a host of other factors related to the efficient management of both production and logistics. In order to compete effectively in the world market, producers of T&C must provide rapid delivery and respond quickly to frequent shifts in consumer preferences and changes in retail practices. So while comparative costs (for clothing, especially those related to labor) remain important, production planning and delivery times are key determinants of comparative advantage in T&C. Competitiveness in the T&C market is therefore being increasingly driven by the ability of producers to bring products to market just-in-time in order to reduce the costs faced by retailers associated with keeping inventories.

viii

Sustainability of apparel as an important export sector requires decreased reliance on trade preferences and shifts to permanent sources of comparative advantage. Creation of a regional market for production would be an important source of comparative advantage. 36. The benefits of vertical domestic and regional integration of the T&C supply chain stem from cost reductions associated with lower transport and inventory costs, border delays, which otherwise would lead to shipping inputs and final products over larger distances. Vertical integration, in particular, can also increase control over production and the ability to sample fabrics and clothing more quickly. For these reasons retailers are increasingly sourcing from companies that are vertically integrated or located in regions that house the whole industry.

37. While these arguments would favor the development of a fully integrated African T&C sector in order to benefit from proximity to the region’s abundant supply of cotton and other raw materials, such regional integration has not materialized. For example, while AGOA countries are traditional suppliers of seed cotton, accounting for 4.6% of world production, they have failed to become significant processors of raw cotton into T&C products. They account for less than 1% of world exports in such products and just three countries - Mauritius, South Africa and Lesotho - account for three-quarters of total volume.

38. Similarly, domestic cotton production in some but not all T&C producing countries.2 Cotton can be shipped long distances and stored without significant degradation in quality. Certain cotton-producing countries are relatively unattractive locations for manufacturing investment and they lack the workforce capabilities necessary to develop a T&C sector. Thus, it is economically desirable to promote intra-AGOA regional trade in cotton, yarn, fabric and clothing and establish an integrated industry.

Intra-AGOA trade in cotton, yarn, fabric and clothing

39. Cotton: As a group, AGOA countries export 83% of their cotton lint production, accounting for 9% of world exports. The largest producers (Cameroon, Côte d’Ivoire and Mali) export virtually all of their production. Nigeria is the only large producer of cotton lint in the region that domestically consumes most of its production (80%).

40. Over one-third of AGOA cotton exports go to China and the EU while only 8% of AGOA cotton exports are to the other countries in the region and this is only half of all cotton imported by the region. South Africa imports 61% of AGOA cotton traded regionally. Mauritius’ imports of cotton account for a further 13% and Nigeria 9%. Almost half of intra AGOA trade in cotton comes from Zambia and virtually all of this is exported to South Africa.

2 For example, while China has integrated its cotton sector through textiles to clothing, supplying over 90% of its cotton lint requirements, Mexico (a much smaller cotton producer) imports virtually all of its cotton to supply the T&C sector.

ix

41. Other major exporters to the other countries in the region include Benin (12%, mostly to Nigeria), Malawi (8%, to South Africa and Zambia), Mozambique (6%, to South Africa) and Mali (6% to Mauritius).

42. Yarn: As a group, AGOA countries are net importers of yarn (both cotton and man-made). One third of AGOA yarn imports are from the EU, US and China. While one-fifth of AGOA yarn exports are to the region they comprise less than 10% of all yarn imports to the region. Mauritius’ imports of yarn from AGOA countries account for one half of intra-regional trade in these products. South African imports of yarn account for a further 19%, followed by Uganda (6%) and Kenya (4%).

43. Two-fifths of intra AGOA trade in yarn is sourced from South Africa (mostly to Mauritius but also to other AGOA countries). Other major exporters in and to the region include Zambia (30%, to South Africa, Mauritius and Malawi), Kenya (10%, mostly to Uganda but also South Africa) and Madagascar (9%, virtually all to Mauritius but also to South Africa).

44. Fabric: AGOA countries are net importers of fabrics (cotton and man-made). Over half of AGOA fabric imports are from the EU, US and China. While 37% of AGOA fabric exports are to the region, only 5% of AGOA fabric imports are sourced regionally. One-third of AGOA fabric exports go to the EU (10% to the US, and virtually nothing to China). One-sixth of intra AGOA trade in fabric is accounted for by Mauritian imports from the region. Benin imports of fabric account for a further 15%, followed by Namibia (10%) and Malawi (6%).

45. Almost half fabric of fabric traded regionally is sourced from South Africa (mostly to Mauritius, Namibia and Malawi but also to other AGOA countries). Other major exporters in and to the region include Nigeria (13%, mostly to Benin), Côte d’Ivoire (11%, mostly to Benin but also Niger), Ghana (8%, to Nigeria and Benin) and Mauritius (7% to Madagascar and South Africa).

46. Clothing: AGOA countries are net exporters of clothing, accounting for 1% of world exports in 2003. Less than 5% of AGOA clothing exports are to the region, while 11% of AGOA clothing imports are sourced regionally (see Annex 34). 59% of AGOA clothing exports go to the US (34% to the EU, virtually nothing to China).

47. Nearly one-third of intra AGOA trade in clothing is accounted for by Namibian imports from the region. South African imports of clothing account for a further 19%, followed by Zambia (10%). Over one-half of intra AGOA trade in clothing is sourced from South Africa (mostly to Namibia, Zambia and Mozambique but also to other AGOA countries). Other major exporters to the region include Malawi (15%, almost exclusively to South Africa), Kenya (10%, mostly to Uganda and Tanzania), and Côte d’Ivoire (7% mostly to West and Central Africa).

Potential for vertical and regional integration exists …

x

48. The previous section shows that intra-AGOA trade in inputs required by the region’s clothing industry is low (less than 40% for fabrics and 20% for yarns) and more limited for products further up the cotton-clothing value chain (yarn production is more capital intensive than fabric production). But assuming the TCF derogation under AGOA expires in 2013 and is not extended, this will require African exporters to use regionally (or US) sourced yarn and fabric to maintain AGOA-eligibility for their clothing exports to the US market. Although AGOA beneficiaries will not necessarily need to develop their own cotton, spinning, weaving, knitting, dyeing, cutting and assembly operations, they will need to source these from other AGOA countries in order for exports to qualify for preferences. And there may be potentially significant competitiveness gains from this by reducing transport and logistics costs and shortening lead times through more coordinated planning, production and shipping.

49. Coughlin et al. (2001) propose the following possible supply chains for basic clothing for 11 African countries. They conclude that no country in the region has an absolute advantage in all stages of production and that the most competitive supply chain is a regional one.

Potential Regional Supply Chain for T&C for African Countries

Production stage Countries

Spinning Botswana, Lesotho, Mozambique, Mauritius, Namibia, South Africa, Swaziland, Malawi, Zambia, Zimbabwe, Tanzania

Knitting Botswana, Lesotho, Malawi, Mauritius, Namibia, South Africa, Swaziland, Zambia Zimbabwe

Weaving Botswana, Namibia, Lesotho, Mauritius, South Africa, Zimbabwe Zambia, Malawi

Dying and finishing Lesotho, Mauritius, South Africa, Zimbabwe, Zambia, Malawi

Basic clothing Lesotho, Mozambique, Malawi, Zambia, Zimbabwe, Tanzania

Fashion clothing Botswana, Mauritius, Swaziland, Namibia, South Africa

Product design, marketing Mauritius, South Africa

….. but challenges to realize this potential are daunting

50. Only if the clothing sector has long-term viability in Africa can there be any chance of developing sustainable backward and forward linkages. Interventions that compromise the competitiveness of the clothing sector (trade policies that raise the domestic cost of intermediate inputs, policies in overseas markets, especially ROOs that limit access to those markets) will not be conducive with the emergence of integrated production in Africa. In other words, investments will not be made in spinning and

xi

weaving if there is uncertainty concerning the viability of the downstream sources of demand: the clothing producers. In the modern global clothing market, those best able to perceive profitable opportunities for additional investments in other segments of the value chain, especially in small economies with limited domestic demand, are likely to be the clothing exporters. T&C firms in these countries must, therefore, determine their strategies depending on their position in the supply chain, their links to the international market and the type and value of products they export. For firms with unique, niche products (e.g. high quality suits in Mauritius) the best option may be to pursue branding to secure greater rents associated with the product’s uniqueness, or to enter a product niche (e.g. workwear in Zambia) where demand does not vary significantly throughout the year and there are fewer competitors. For large firms, with many operations offering standardized products (e.g. knitwear in Lesotho and menswear in Kenya), increased vertical integration within the country or regional integration with producers in other countries may be the best strategy for reducing costs associated with profit margins and transport costs and for controlling risks that delay shipments. But this will require significant investment in the region’s textile sector to develop production capacity and improve quality. Efforts will also be required to obtain buyer approval for new regional sources of yarns and fabrics. The alternative model, where a significant proportion of total output is destined for sale to the domestic market (e.g. as in South Africa) is not likely to be successful or sustainable, especially in small economies where domestic demand is limited or where competition is fierce from large Asian competitors that benefit from economies of scale or subsidies to their T&C industries. Domestic demand may also be limited where sales of second-hand clothing have already captured the low-middle range of the clothing market, failing to support the higher prices required by local manufacturers.

51. The use of trade policy instruments (high duties on clothing, textiles and yarns in African countries; restrictive ROOs for preferences in the EU market, even with regional cumulation) have not been successful in supporting the clothing sector in Africa or in encouraging linkages with different part of the clothing chain. What is necessary is that Governments in Africa address the availability and cost of key backbone services that undermine the competitiveness of all sectors, improve the business climate and ensure that domestic firms have access to inputs at global prices. There may also be scope for pro-active sector specific policies that address critical constraints related to labor skills and market information.

xii

1. Introduction

Diversification into higher-value added export products away from commodities continues to be a major development and trade policy objective for many developing countries. During the last decade, textiles and apparel were presented as potential export sectors that would create such opportunities. Apparel production is especially labor intensive, with low start-up investments and easily transferable technology. Furthermore, the labor requirements can be easily met with low and semi-skilled workers, especially women. As a result, many countries with competitive labor costs, especially in South and East Asia, have captured significant shares in the world market during the last four decades. Despite the potential development benefits and their various sources of comparative advantage, few African countries have managed to establish a presence in the global textiles and apparel markets until recently. As a result, Africa as a whole, remains a net importer of textiles and clothing even though it is a net exporter of cotton.

The biggest boost to the African apparel sector came through the unilateral market access preferences granted by the US and the European Union via the African Growth and Opportunity Act (for the US) and Cotonou, EBA (for the EU) initiatives. Since the vast majority of the main apparel exporters in other developing countries faced rather restrictive access to the European and US markets (due to ATC quotas and high tariffs), the unilateral quota and tariff-free access granted to African countries led to rapid growth of exports from the region. The main feature of the preference programs, especially AGOA, was the permission to use fabric from third-countries which is not granted in other US bilateral and unilateral preference programs. This allows cheap fabrics, especially from Asia, to be processed in Africa and exported to the US – a process which is not allowed under the rules of origin under other preferential market access programs. The growth of apparel exports from Africa has been praised and identified as a success of unilateral preference programs.

The future of apparel exporters in sub-Saharan Africa is, however, rather uncertain as they face two major challenges for their products: i) increased competition from large, low-wage producers such as India, China, Bangladesh and Pakistan following the phase-out of quotas after the expiry of the ATC; and, ii) the expiration of the third-country fabric derogation under AGOA scheduled for 2013.

Since the expiration of the ATC in 2005, Africa has seen its recent growth of exports transformed into a decline. Many factories have closed, resulting in the loss of tens of thousands of jobs in Kenya, Lesotho, Madagascar, Mauritius, Namibia, South Africa and Swaziland. Producers in sub-Saharan Africa can no longer depend on displaced production from quota-bound countries to boost their exports. In order to attract buyers, they must be cost competitive (within the margins of preference they receive in developed country export markets); able to deliver to market on-time; and, be prepared to meet quality and service requirements.

The African clothing industry faces many challenges as it struggles to maintain its recently-found place in the global market. One of the main developments is increasing demands by retailers for faster lead times from their suppliers to satisfy changing fashions and to reduce the inventory costs. In other words, fast production is becoming the norm in an industry which favors countries that have flexible supply chains and lower transportation costs to main consumer markets in the West. Secondly, there is increased need for a large and nearby supplier base for raw materials. National clothing industries can no longer rely exclusively on distant sources of yarns and fabrics to satisfy clothing industry demand. But no national textile industry can survive without local clothing manufacturers as a demand base for their production.

Unilateral preference programs such as AGOA promote the development of regional yarn and fabric production capacity via a yarn-forward rule which requires yarn and fabric to be locally supplied. This requirement enhances regional development by encouraging more of the production to be done locally as well as discouraging transshipment. However it fails to fully capture the realities of today’s global market. It is both unrealistic and inefficient to force any regional textile sector to supply all of the various yarns and fabrics that US buyers specify, especially in small and poorer countries with less developed domestic markets. Even China, a diversified textiles producer, imports a significant portion of the needed yarns and fabrics to satisfy its buyers’ wide range of demands. Therefore, AGOA’s objective to develop a vertically integrated textiles-to-clothing supply chain within the region could deny African clothing manufacturers access to yarns and fabrics specified by their US customers if such inputs are unavailable in the region and the third country fabric derogation expires. This would generate a significant decline for the African clothing industry. Currently, over 85% of clothing exports currently eligible for preferences in the US market are made from third-country fabric.

This study explores the potential for regional and vertical integration to overcome these challenges and identifies obstacles to this. Timing is important since both the EU and the US have recently imposed trade restrictions on China (until 2008) to protect their domestic textiles and clothing industries. These safeguards provide a brief opportunity for sub-Saharan African producers to integrate their textiles and clothing industries both domestically and regionally.

2

2. Protection and preferences in the global market for textiles and clothing

2.1 The Agreement on Textiles and Clothing: quotas have gone but high tariffs remain

On 1 January 2005, the WTO Agreement on Textiles and Clothing (ATC) expired. The quotas that once shaped the global apparel trade were removed and tariffs were left as the only trade restrictions in place (see Annex 1). The Multifiber Arrangement (MFA) that preceded the ATC governed trade in textiles and clothing (T&C) by providing a framework for bilateral and unilateral restrictions limiting imports into developed-country markets whose domestic industries were facing decline. Preferential access to protected markets (see Section 2.2) served to protect exports from some developing countries (e.g. Kenya) while quotas restricted others (e.g. India and China).

Under the MFA, quotas fundamentally affected the production and trade of T&C in two ways (Cline, 1990; Hamilton, 1990; Minor, 2002). First, for exporting countries, quotas imposed a limit on exports but also secured market access, providing an incentive for producers to geographically diversify their export markets. The quota regime led production of T&C to spread to a larger number of countries. Secondly, importing countries were forced to source from exporting countries that had been allocated quotas that remained unfilled. For example, at the beginning of the 1990s half of T&C exports from Hong Kong would have gone to other countries had there been no quotas (Lande et al., 2005). Restrictions on imports from the more competitive East Asian manufacturers (such as China, Japan, South Korea and Hong Kong) led to a displacement of clothing production to less developed but less competitive locations such as Bangladesh, Indonesia, Sri Lanka and Mauritius. The initial driving force behind this process was the larger retailers such as Wal-Mart and brands such as Nike who began to outsource production to low-wage countries. While they carried out no production of their own, they maintained control over design and marketing of products, standard setting and sourcing of raw materials, distributing them globally and then importing the final products (Morris, 2006). This was followed by the establishment of ‘triangular production networks’, where countries with established relationships with these brands and retailers began to outsource their own production to (lower waged) countries (Gereffi, 1999). For example, in the 1990s Korean and Taiwanese producers expanded their operations to the Caribbean and Sub-Saharan Africa and the Mauritian clothing sector had developed operations in Madagascar.

While ATC required the eventual elimination of quotas, it did not mandate a reduction in tariff protection. Consequently, the global market for these products remains heavily distorted, especially in developed country markets for finished products and in those developing countries that produce clothing. Average applied tariffs on imports of textiles to the largest markets are 6.70% for the EU and 7.54% for the US (see Annex 2) but are higher for imports of clothing at 11.54% and 10.76% respectively (see Annex 3). However, in many categories, the US and the EU impose over 20% tariffs whereas their average tariffs on manufactured goods are below 3%. Tariff peaks on imports of T&C products can reach 32 percent in the US. Average tariffs on imports of T&C products in

3

many developing countries are also high, sometimes averaging over 20 percent with peaks of over 100 percent for certain products.

Since apparel exports are subject to some of the highest tariffs on manufactured goods in the major importing developed countries, preferential access offered in the US and EU can have a substantial positive impact on the eligible countries. However, the rules of origin in these preference programs can impose serious constraints on exporters.

2.2 EU GSP and Everything but Arms

The EU implemented its Generalised System of Preferences (GSP) in 1971. The range of beneficiaries were gradually expanded, graduation criteria for the higher income developing countries were introduced and greater benefits for the LDCs in the scheme were offered (see Annex 4). In 2003, EU imports under GSP (for all goods) totalled US$59 billion, compared to US$18 billion under the US GSP (see section 2.4). The EU GSP can be used by all developing countries except Myanmar (which has been suspended). For textiles, the general GSP reduces average EU import tariffs from 6.70% (under MFN) to 5.42% and, for clothing, from 11.54% to 9.23% for clothing (see Annex 5). The most favourable arrangements under the EU’s GSP is reserved for LDCs (see Annex 6). With its Everything but Arms (EBA) amendment, effective from March 2001, the EU extended duty- and quota-free access to all products originating in LDCs, except arms and ammunition. This includes (where the ordinary GSP does not) all agricultural products, including ‘sensitive’ products.3

Rules of origin (ROOs) under EU preferential trade agreements vary widely. In general, EU ROOs under its GSP require two significant processes be performed within a country in order to confer origin and eligibility for the tariff preference. In many cases ‘significant’ processing requires a product to be reclassified from one four-digit tariff heading to another. In industry terms for clothing, this means that production, including cutting and sewing, must be combined with another process, such as manufacture of fabrics or yarns. In other words, dying and finishing is not sufficient to confer origin under the EU’s GSP. A 10 percent tolerance for third country content for trimmings and non-originating fibers and yarns is allowed. All exports for which preferential treatment is sought must be shipped directly to the EU without entering another country, although there is provision for transhipments as long as they are stored solely for onward freight. For African producers, there is no cumulation provision under the GSP for inputs originating in other African countries. Clothing must be constructed of fabrics made (including drying and finishing) in the country or the EU. However, a number of Asian countries eligible for GSP (Indonesia, Cambodia, Vietnam, Bangladesh and Pakistan) benefit from a regional cumulation rule that allows producers to source fabric and yarns from each other and from large textile producing countries such as India, as long as the 3 Only three most sensitive agricultural products were not liberalised immediately for LDCs: bananas, rice and sugar. For bananas, EBA provides for full liberalisation between 1 January 2002 and 1 January 2006 by reducing the full (out-of-quota) tariff by 20% every year. For rice and sugar, duty-free quotas have increased by 15 percent each year from base levels of 2,517 tons (for rice) and 74,185 tons (for sugar) in 2001/02 and will continue to do so until 2009, when all quota restrictions will be eliminated. Rules of origin still apply but (unlike preferences under the ordinary GSP) EBA does not expire.

4

fabric originates in the region and certain value-added criterion have been met (China and India have graduated from GSP and face full MFN tariffs). ROOs under EBA are also more restrictive for sub-Saharan African countries than for LDCs in South and South East Asia. Asian LDCs may use fabrics from neighboring countries as long as 51 percent of the value of the final product is added in the making up process and the fabrics come from designated partner countries. Moreover a temporary derogation (in place until 31 December 2006) for Cambodia, Laos and Nepal eliminates the value added rule (Minor, 2006). African LDCs should petition the EU for cumulation rules under EBA comparable to their counterparts in Asia.

2.3 The EU ACP/Cotonou Agreement

The group of African, Caribbean and Pacific (ACP) countries, now 77 (excluding South Africa), have traditionally received more generous tariff preferences on a broader range of products than those covered under the EU’s GSP (see Annex 7 for a chronology). The ACP/Cotonou Agreement eliminates import duties on clothing meeting its ROO (see Annex 5). For textiles, it reduces average EU import tariffs from 6.70% (under MFN) to 0.34%. ROOs specify that articles of clothing, including those made cotton, wool and manmade fibers, must be constructed from ACP yarn or fabrics i.e. full cumulation is allowed. As with ROOs under AGOA (see Section 2.4), the yarn used in knit-to-shape garments must be spun in an ACP country, in addition to the fabric construction and making-up. Exceptions to this general ROO exist for products containing significant embroidery or impregnated fabrics. Non-ACP fabrics can be used in made-up clothing if the fabrics are printed in an ACP country and the printing adds at least 52 percent of the value to the fabric – a significant barrier for basic garments. A 15 percent tolerance for non-ACP content including trimmings and non-originating fibers and yarns is allowed.

2.4 US GSP and the African Growth and Opportunity Act

The US GSP took effect in 1976 and was initially intended to operate until 1985, although it continues to function to the present day. The US GSP offers duty-free treatment for specified products from designated countries but excludes most T&C products. Consequently, the US GSP reduces average US import tariffs marginally since most categories are excluded. Tariffs are lowered for textiles from 7.54% (under MFN) to only 7.36% and, for clothing, from 10.76% to 10.64% (see Annex 8).

For African imports, the US introduced AGOA in 2000, and expanded it three times afterwards. In order to be eligible to receive tariff preferences under AGOA, countries must also be eligible under its GSP. Although GSP eligibility does not necessarily imply AGOA eligibility, the majority (45 of 48) of sub-Saharan African countries are currently GSP-eligible and 37 of these are also AGOA-eligible (see Table 1 for the dates of eligibility).

5

Table 1: African Growth and Opportunity Act eligible countries

Country Date declared AGOA eligible

Date declared eligible for apparel provisions

Country Date declared AGOA eligible

Date declared eligible for apparel provisions

Angola 30 December 2003 Lesotho 2 October 2000 23 April 2001Benin 2 October 2000 28 January 2004 Madagascar 2 October 2000 6 March 2001Botswana 2 October 2000 27 August 2001 Malawi 2 October 2000 15 August 2001Burkina Faso 10 December 2004 4 August 2006 Mali 2 October 2000 11 December 2003Burundi 1 January 2006 Mauritius 2 October 2000 18 January 2001Cameroon 2 October 2000 1 March 2002 Mozambique 2 October 2000 8 February 2002Cape Verde 2 October 2000 28 August 2002 Namibia 2 October 2000 3 December 2001Chad 2 October 2000 26 April 2006 Niger 2 October 2000 17 December 2003Congo 2 October 2000 Nigeria 2 October 2000 14July 2004Democratic Republic of Congo 31 December 2002 Rwanda 2 October 2000 4 March 2003

Djibouti 2 October 2000 Sao Tome and Principe 2 October 2000

Ethiopia 2 October 2000 2 August 2001 Senegal 2 October 2000 23 April 2002Gabon 2 October 2000 Seychelles 2 October 2000 Gambia 31 December 2002 Sierra Leone 2 October 2000 5 April 2004Ghana 2 October 2000 20 March 2002 South Africa 2 October 2000 7 March 2001Guinea 2 October 2000 Swaziland 2 October 2000 26 July 2001Guinea-Bissau 2 October 2000 Tanzania 2 October 2000 4 February 2002

Kenya 2 October 2000 18 January 2001 Uganda 2 October 2000 23 October 2001Zambia 2 October 2000 17 December 2001

The main advantage of AGOA is its extension of product coverage of GSP to include an additional 1,835 items. Notably, AGOA includes some clothing products (normally excluded from US preferences) with the requirement that countries (i) have procedures in place to prevent trans-shipments and use of counterfeit documents and (ii) meet rules of origin requirements (see Annex 9). AGOA also includes (from 2007) textiles products from eligible lesser developed African countries (defined as sub-Saharan African countries with a per capita GNP of less than US$1,500 in 1998). A second advantage is the eligibility guarantee for longer terms – up to eight years – whereas GSP needs to be renewed by the US congress every year.

AGOA, when compared to other preference programs of the US (such as NAFTA with Mexico or CBI with the Central American countries) provides more flexible ROOs for lesser developed countries. It requires only single transformation until 2013 (although this has been extended twice: initially scheduled for 20 September 2004 and then 30 September 2007). Simply put, the third-country fabric (TCF) derogation makes eligible for preferences clothing made from non-AGOA imported yarn or cloth, that (from 2007) is not deemed to be in abundant supply within the region (e.g. denim - see Annex 9). Of the 37 AGOA-eligible countries, 26 are eligible for apparel benefits and 24 for the TCF derogation. The only major countries that are ineligible for the use of the TCF derogation are Mauritius and South Africa. The US Congress approved legislation in November 2004 that included Mauritius, for a period of one year, under the TCF derogation. Mauritius had previously been excluded from the list (and is once again now), as a result of its relatively high income per capita. Currently, clothing exports from Mauritius have to be produced using regionally or US-sourced raw materials in order to qualify for AGOA preferences. Less than 50% of its exports to the US meet these requirements.

6

3. Trade patterns in textiles and clothing

This section analyzes global trade in T&C during the period 1994-2004, using the most recent data for 2005 where available (see Annex 10).4

The MFA/ATC regime served as a negative preference system, helping some developing country suppliers at the expense of others (especially East and South Asian countries such as China and India). Quotas in T&C shielded less competitive suppliers in Latin America and Africa from competition. The MFA, therefore, induced the expansion of T&C industries across a wide range of countries which did not necessarily have comparative advantage in these sectors. Over time, as quotas became more restrictive in certain products and exporters, investment flowed to unconstrained countries. Initially T&C production for export was concentrated in Japan, then spreading to Hong Kong, South Korea and Taiwan (China). Thereafter it relocated rapidly throughout Southeast Asia, the Indian subcontinent and to Turkey, Brazil, the Middle East Gulf and Mauritius. Exports of T&C from China and Vietnam grew rapidly once these countries received MFN status and have increased further following the removal of quotas under the ATC.

The emergence of global supply chains for T&C has provided retailers with the ability to increasingly manage their supply networks and dictate non-price conditions such as quality, delivery schedule and choices over raw materials (Flanagan, 2003; Kaplinsky, 2005). In 2001, the largest 5 US retailers accounted for over three-quarters of clothing sales, while in the UK the largest 10 retailers accounted for 52% of sales (Weathers, 2003; Gibbon, 2002). By 2010 it is predicted that the largest 10 retailers in the world will account for 25-30% of world T&C trade (Morris, 2006). Retailer power has also been increasing for two other reasons. First, consumers demand for varieties is increasing which is leading to shorter product seasons, faster product cycles and smaller orders (Salinger et al, 1998). Secondly, mergers and acquisitions have led to a greater concentration of retailers in developed countries (Morris and Sedowski, 2006).

3.1 China dominates in world exports of textiles and clothing

China is the country most likely to gain market share following the end of the ATC. The China region5 was the world’s largest exporter of both T&C in 2004. Its world market share (excluding intra-EU trade) of both textiles and clothing remained relatively constant between 1994 and 2004 at for textiles 33.0% and 32.8% respectively (see Annex 11) and for clothing at 39.5% and 39.3% over the same period (see Annex 13) for clothing. China currently offers the cheapest cost of production because of low (but increasing) wages, economies of scale and high productivity of its producers. The availability of cheap, high quality fabric, both domestically and from neighboring Asian countries, is also an advantage (Kaplinsky, 2005). China continues to expand its range of T&C products and has improved its capacity to meet international quality standards

4 Textiles are defined here as ISIC Rev.3 section 17 (excluding components relating to HS chapter 61) and clothing is defined as HS chapters 61-62 respectively.5 China region includes China, Taiwan (China), Hong Kong and Macao which is treated as a single entity.

7

(Morris, 2006). A large increase in exports from China followed the country’s accession to the WTO in 2001, as quotas were lifted or expanded on a number of China’s T&C products. Upon its membership of the WTO, China benefited not only from the third phase of integration under the ATC on 1 January 2002 but also from the integration of T&C products (granted to other WTO members when China was not a member) during the first two phases. Consequently, on 1 January 2002, 29 categories of quotas were removed on imports from China. Some of the highest import growth rates were in eight categories of products containing cotton. According to the National Cotton Council, US imports of products from China covered by these eight categories grew by an average of more than 640% in 2002.

Following the final phase of the ATC, figures for 2005 show that China region’s world market share has risen to 36.3% for textiles and 42.4% for clothing. This increase in exports from China, largely to the US and EU, has led to the imposition of safeguards on Chinese T&C products. Temporary quotas, agreed under the special T&C safeguard clause of China’s WTO accession, limit the (volume) growth in imports of certain T&C products to 7.5 percent per annum until December 2008. In June 2005, the EU concluded a bilateral agreement that further limits imports of T&C from China until the end of 2007, covering one-third of T&C products. And in November 2005, the US concluded a similar bilateral agreement limiting 22 clothing categories (or one-fifth) of T&C imports from China to an increase of between 10-17% per year until December 2008 (de Voest, 2006). The safeguards cover some 90 percent of T&C products integrated under the final stage of the ATC (IMF, 2006). Other countries, such as Turkey, Argentina, Brazil and South Africa (see Section 6.1) have also imposed safeguards on imports of Chinese T&C products or have taken steps to be able to use them.

After China is freed of bilateral constraints, many analysts expect the country’s market share of T&C to grow to more than 50%. Others believe that the elimination of quotas will transform T&C manufacturing so drastically that it will eventually resemble footwear and toys, in which upwards of 90% of all merchandise is imported from China.

Other major exporters of textiles are the EU, US, India and South Korea (see Annex 11). Developed countries, therefore dominate in world textile exports. The world export share in textiles of countries eligible for AGOA’s clothing provisions (hereafter simply defined as AGOA countries) fell from 0.52%, in 2000 to 0.45% in 2004, while increasing slightly to 0.47% in 2005. In 2004, the largest AGOA exporters of textiles were South Africa, followed by Mauritius, Nigeria and Tanzania, accounting for 82% of total textiles exports from the group (see Annex 12).

In the clothing sector, the major exporters (in addition to the China region) were the EU, Turkey, Bangladesh, Mexico and India (see Annex 13). The world export share in clothing for all AGOA countries rose from 1.24%, in 2000, to 1.43% in 2004 before falling to 1.22% in 2005 (see Annex 14). Exports from the region are mainly low-price basic items such as trousers, T-shirts and sweaters that typically have long production runs and few styling changes (ITC, 2004; EIU, 2004). In 2004, the largest AGOA exporters of clothing to the world were Mauritius, followed by Madagascar, Lesotho,

8

Kenya and South Africa, jointly accounting for 86% of total clothing exports from the group.

3.2 Textiles and clothing exports are important to some AGOA countries

For the AGOA group of countries as a whole the share of T&C exports in total exports is low, at 0.54% and 2.77% respectively (see Annex 15). But for some individual countries within the AGOA group, clothing exports are an important component of foreign exchange. Exports of clothing are most important for Lesotho (accounting for 97.24% of total exports), followed by Mauritius (51.45%), Madagascar (41.19%), Cape Verde (39.48%), Swaziland (24.58%) and Kenya (11.97%).

In 2004, the EU took the largest share of AGOA countries’ textiles exports (47.18%) followed by the US (6.69%). For clothing exports from AGOA countries, the US market accounts for 62.64% of total clothing exports, followed by the EU (33.53%).

The Canadian and Japanese markets are far less important for AGOA countries. In 2004, Canada and Japan accounted for 1.30% and 1.74%, respectively, of textile exports from AGOA countries while their share of clothing exports was 0.98% and 0.22%. For textiles, the Canadian market is most important for South Africa (accounting for 1.96% of South Africa’s textile exports) while Japan is most important for Tanzania (4.60%) and Mali (4.24%). Turning to clothing, Canada is most significant for Burkina Faso (accounting for 17.45% of its clothing exports and Nigeria (14.19%) while the Japanese market is most significant for Cameroon (14.06%) and Niger (6.49%).

3.3 Developed countries are the main markets for imports of textiles and clothing

In 2004, the largest importer of textiles was the EU followed by the US. Since 1994, the share of the ATC countries (EU, US and Canada) in world imports of textiles (excluding intra-EU trade) has increased from 31.1% to 35.8% in 2004. The increase was mainly due to an increase in the share of the EU and US from 16.7% to 17.0% and from 11.2% to 15.9%, respectively (see Annex 16). Canada’s share of world textiles imports has remained stable throughout the period at about 3%. AGOA countries are net importers of textiles, accounting for 1.65% of world imports in 2000, increasing to 2.37% in 2004 (see Annex 17).

For the clothing sector, the largest importer is the US followed by the EU and Japan. Although there is virtually no clothing industry left in the US or Japan, a significant domestic clothing sector remains in the EU, especially Southern Europe (Morris et al., 2006). Since 1994 the ATC countries’ combined shared of world imports has increased from 63.3% to 69.2%. The world share of clothing imports for the US and Canada increased marginally from 32.8% to 33.7% and from 2.1% to 2.3%, respectively, between 1994 and 2004 (see Annex 18). By contrast, the EU share of world clothing imports rose sharply from 28.4% to 33.2% over the same period. AGOA countries accounted for 0.30% of world clothing imports in 2000, increasing to 0.47% in 2004 (see Annex 19).

9

Given the larger share of ATC countries in world imports of clothing, these countries are relatively more important markets for exporters of clothing than for exporters of textiles.

3.3.1 The US market for textiles and clothing is growing strongly but the sources of imports are changing