The Effect of Compensation Disclosure on Compensation ... effect of compensation... · 2 The Effect...

34

1 The Effect of Compensation Disclosure on Compensation Benchmarking: Evidence from China Wei Jiang Department of Accounting, School of Management Center for Management Accounting Research Jinan University Guangzhou 510275, China Email: [email protected] Xinxin Liao School of Business Sun Yat-Sen University Guangzhou 510275, China Email: [email protected] Bingxuan Lin College of Business Administration University of Rhode Island Kingston, RI 02881 Email: [email protected] 1-401-874-4895 Yunguo Liu* School of Business Sun Yat-Sen University Guangzhou 510275, China Email: [email protected] Wei Jiang acknowledges the financial support of the National Natural Science Foundation of China (71272212), the Humanities and Social Science Foundation of the China Ministry of Education (11YJC630076), Institute of Enterprise Development at Jinan University (2014ZD001) and the Fundamental Research Funds for the Central Universities at Jinan University (12JNYH003). * Contact Author

Transcript of The Effect of Compensation Disclosure on Compensation ... effect of compensation... · 2 The Effect...

1

The Effect of Compensation Disclosure on Compensation Benchmarking:

Evidence from China

Wei Jiang

Department of Accounting, School of Management

Center for Management Accounting Research

Jinan University

Guangzhou 510275, China

Email: [email protected]

Xinxin Liao

School of Business

Sun Yat-Sen University

Guangzhou 510275, China

Email: [email protected]

Bingxuan Lin

College of Business Administration

University of Rhode Island

Kingston, RI 02881

Email: [email protected]

1-401-874-4895

Yunguo Liu*

School of Business

Sun Yat-Sen University

Guangzhou 510275, China

Email: [email protected]

Wei Jiang acknowledges the financial support of the National Natural Science Foundation of China (71272212),

the Humanities and Social Science Foundation of the China Ministry of Education (11YJC630076), Institute of

Enterprise Development at Jinan University (2014ZD001) and the Fundamental Research Funds for the Central

Universities at Jinan University (12JNYH003).

* Contact Author

2

The Effect of Compensation Disclosure on Compensation Benchmarking:

Evidence from China

Abstract

Improved compensation disclosure might minimize unscrupulous compensation

behavior by entrenched executives, and it could allow better benchmarking against

peer groups. Meanwhile, with improved disclosure, executives can collectively defend

their high salaries by engaging in opportunistic peer selection behavior. Better

disclosure also forces companies to pay their executives market salaries. Using a

sample of Chinese companies, we find that industry benchmarking is prevalent in

China. Moreover, since the amended regulation for executive compensation

disclosure in 2005, executives whose compensations are above the industry average

have experienced much smaller pay raises, and executives whose compensations are

below the industry average have had much higher pay raises. The results of our study

are robust after controlling for various firm and industry characteristics. The results

also show that companies controlled by different entities (i.e., central government,

local government or non-government) behave very differently in response to

enhanced compensation disclosure. These findings highlight the importance for

policymakers of understanding how different firms react to improved disclosure, and

how various firms face different incentives concerning disclosure.

3

The demand for greater corporate compensation disclosure has increased

considerably in recent years, especially since the 2008 financial crisis. However,

studies on executive compensation disclosure have yielded many different results. On

the one hand, improved compensation disclosure is associated with better governance,

higher pay-for-performance sensitivity and improved monitoring by stakeholders (Lo,

2003; Perry and Zenner, 2001; Vafeas and Afxentiou, 1998). On the other hand,

compensation disclosure regulations appear to have very little effect in mitigating the

problems involved in corporate compensation practices (Faulkender and Yang, 2013).

There might also be unintended consequences of better disclosure, as disclosure may

aggravate agency problems and affect related costs (Hermalin and Weisbach, 2012).

Compensation disclosure in emerging markets can be especially difficult to analyze

due to weak corporate governance, lax enforcement of security laws and a poor

disclosure environment. Leuz and Wysocki (2008) point out that there have been

major changes in disclosure regulations in many emerging markets. However, these

regulations may have different effects in various markets due to the diversity of

institutional and economic factors.

Executive compensation disclosure in China is fairly limited. In 1998, the

China Security Regulatory Commission (CSRC) required listed firms in China to

disclose information about top executive compensation. However, this regulation only

required companies to report the total compensation for the three highest-paid

managers. As corporate governance in China slowly improved and demand for

corporate disclosure became greater, the CSRC issued new rules in 2005. Under the

4

new disclosure regulation, all listed firms are required to report the compensation,

including the salaries, bonuses, stipends and other benefits for the top three executives

separately. This disclosure regulation of 2005 is in many ways comparable to the

1992 United States Securities and Exchange Commission (SEC) revisions to its rules

governing disclosure of executive compensation.

Although the CSRC 2005 disclosure regulation does not require firms to

reveal their compensation peers (as the 2006 U.S. SEC rule does), it does give firms

access to peer compensation information at the individual level, which allows for

better benchmarking. The extant literature suggests that firms are likely to benchmark

against their peers, and the use of benchmarking has a significant effect on CEO

compensation (Bizjak et al., 2008; Bizjak et al., 2011; Albuquerque et al., 2013).

In this study, we examine how executive compensation benchmarking

behavior has changed in response to the new 2005 regulation. We find that under the

amended regulation, executives whose compensations are above the industry average

have experienced much smaller pay raises, and executives whose compensations are

below the industry average have seen much higher pay raises. The results of our study

are robust after controlling for various firm and industry characteristics. Furthermore,

we find that companies controlled by different entities (i.e., central government, local

government or non-government) behave very differently in response to enhanced

compensation disclosure. Specifically, executives whose compensations are above the

industry average generally receive lower pay increases in the subsequent year. After

2005, this effect has been stronger for firms controlled by the central government, but

5

weaker for firms controlled by local governments or non-government entities.

Meanwhile, executives whose compensations are below the industry average have

received higher pay increases in the subsequent year. This effect, however, has been

weaker for firms controlled by the central government and stronger for firms

controlled by local governments. Also, the 2005 regulation does not seem to have any

effect on firms controlled by private entities. Our findings suggest that due to agency

conflicts and labor market competition, firms controlled by different entities tend to

react differently to the disclosure policy change.

Our study contributes to the literature in the following ways. First, we provide

a direct analysis of the 2005 CSRC compensation disclosure, showing that increased

disclosure leads to both intended and unintended economic consequences that vary

among different types of firms. Although China has become the world’s largest

economy, its governance and disclosure environment remain weak (Fan et al., 2007;

Jiang et al., 2010). It is therefore important to understand how the requirement for

compensation disclosure might have varying effects on corporate behavior. Second,

we extend the study of Ezzamel and Watson (1998), which suggests that managers

who are paid more than their peers and managers who are paid less than their peers

face different pressures and incentives for inflating their pay, and they often do so by

using peer groups as benchmarks. Finally, we contribute to the growing literature that

examines CEO compensation in China. Previous studies on the Chinese market have

examined many aspects of executive compensation, including pay-for-performance

sensitivity (Firth et al., 2006; Gu et al., 2010), corporate governance (Conyon and He,

6

2011), managerial power and entrenchment (Chen et al., 2011; Lin and Lu, 2009) or

executive compensation in family firms (Cheng et al., 2014). However, very few

studies have explored benchmarking behavior in China. Our study fills this gap in the

research and shows how benchmarking behavior can change in response to the new

disclosure requirement.

The remainder of this study is organized as follows. Section 2 discusses the

related literature and introduces our hypotheses. Section 3 presents our sample

description, the variable definitions and the empirical methodology. Section 4 reports

our empirical analysis. Section 5 gives the results of robustness tests, and Section 6

offers conclusions from the study.

2. Literature Review and Hypotheses Development

Corporate disclosure regulation can result in both firm-specific benefits and

costs. On the one hand, greater disclosure is often associated with improved market

liquidity (Verrecchia, 2001), reduced agency cost (Shleifer and Wolfenzon, 2002) and

lower cost of capital (Lambert et al., 2007). On the other hand, improved disclosure

exposes firms to indirect costs, as firm-specific information can disclose the firm’s

disadvantages to competitors or regulators (Verrecchia, 1983; Feltham et al., 1992).

Ernstberger and Gruning (2013) show that a country’s regulatory environment

interacts with firm governance arrangements to affect the quality of disclosure. It is

therefore helpful to examine the pros and cons of disclosure in different regulatory

settings. Leuz and Wysocki (2008) review the literature on disclosure regulation and

7

suggest that the extant literature focuses heavily on regulatory changes in the U.S.

market, and that the major regulatory or enforcement changes in other countries are

largely ignored. Examining the effect of regulatory disclosure in China can therefore

provide us with new insights with respect to how regulatory disclosure might result in

different kinds of corporate behavior in regulatory environments outside the U.S.

We specifically focus on the effect of compensation disclosure on

compensation peer benchmarking in China1

. In the U.S., market compensation

disclosure has become a focal point of public interest since the early 1990s. The SEC

disclosure rules of 1992 and 2006 are major regulations that specify the information

to be released in company compensation disclosures. Many studies have shown that

better compensation disclosure results in improved corporate governance and better

pay-for-performance sensitivity (Franco et al., 2013; Vafeas and Afxentiou, 1998; Ke

et al., 1999; Lo, 2003). The SEC rule of 2006 requires firms to disclose the pay-

setting process by revealing which compensation peer groups are considered. This

disclosure allows researchers to look inside the black box and explore how firms pick

their peer groups. Faulkender and Yang (2010) analyze firms in the S&P 500 and the

S&P 400 Midcap firms. These researchers find that firms tend to select highly paid

peers to justify their CEO compensations. In a subsequent study, Faulkender and

Yang (2013) conclude that strategic peer benchmarking has remained prevalent since

the SEC 2006 disclosure requirement. The findings of these researchers suggest that

1 For a comprehensive review of compensation policy in China, please refer to Conyon and He (2011)

and Beaulier et al. (2012).

8

disclosure regulation does very little to mitigate the agency problems involved in

compensation practice. However, Cadman and Carter (2013) use a broader sample

and find that opportunism is not the main motive behind such peer group selection.

Compensation disclosure in China started in 1997, when the CSRC required

all listed firms to disclose compensation information for their executives. However,

the 1997 regulation was so vague that companies could often bury the compensation

disclosure amidst lengthy corporate annual reports. The CSRC modified its rule in

2001 and required a separate section in the annual report dedicated to compensation

disclosure. Furthermore, the CSRC 2001 rule required firms to disclose more specific

compensation information, such as the process of setting the compensation, the total

compensation, the sub-totals of compensation for the three most highly paid managers,

the allowance for independent directors and the intervals of compensation (Beaulieu

et al., 2012). In 2005, the CSRC issued another update and required that listed

companies report individual executive compensations, instead of the aggregate

compensations of the top three executives. Following the 2005 update, corporate

reports disclosed executive compensation at the individual level for the first time.

This change allowed companies to figure out the exact compensation earned by other

executives in firms of the same industry or of similar size.

Bizjak et al. (2008) show that the category of firms in the same industry is one

of the most popular benchmarks used by companies, and that managers usually target

their pay at or above the median (mean) level of their industry peers. We hypothesize

that Chinese companies normally use the industry average compensation as their

9

benchmark to set executive compensation. In many cases, we have observed

companies such as Shenzhen Wanke (ticker 000002) explicitly stating that they set

their executive compensation based on the compensation level in the same industry.

Given the more detailed disclosure requirements since 2005, firms have had easier

access to executive pay information about their peers. Therefore, many firms find it

convenient to benchmark against their peers in the same industry. Hence, we propose

the following hypotheses:

H1a: Chinese companies use industry benchmarking to determine executive

compensation.

H1b: This benchmarking behavior has grown more prevalent since 2005.

Compensation benchmarking might result in different outcomes for executives

who are paid above the benchmark and for those who are paid below it. Using social

comparison and equity theories, Ezzamel and Watson (1998, 2002) find that external

labor markets and internal pay comparisons are critical factors in determining

executive pay. Furthermore, these researchers find evidence that shows asymmetric

adjustment to prior-period pay anomalies. Specifically, the pay of relatively under-

paid executives displays much higher sensitivity to comparison with external market

pay levels. With greater compensation disclosure, we should expect that the under-

paid executives2 have a much stronger case for requesting higher pay. At the same

time, we should expect that the over-paid executives are under greater pressure to

2 In this study, the terms under-/over-paid refer to compensation levels below/above industry average.

10

curb excessive compensation. We therefore suggest the following additional

hypotheses:

H2a: Executives whose compensations are above the industry average will

receive lower pay increases in the subsequent year, and executives whose

compensations are below the industry average will receive higher pay

increases in the subsequent year.

H2b: The asymmetric adjustments in salary between the over-paid and under-

paid executives are more striking since 2005.

Adjustments in salary are also closely linked to various other factors such as

management incentives and labor market competition. One of the unusual

characteristics of Chinese companies is their diversity in forms of ownership control.

Firms can either be controlled by the government as state-owned enterprises (SOEs)

or owned by private entities. Among SOEs, there are also major differences between

SOEs affiliated with the central government (SOECGs) and SOEs affiliated with local

governments (SOELGs).

Chen et al. (2009) show that SOECGs are subject to strict supervision.

Executives in SOECGs are appointed by the central government, and many of them

eventually become vice ministers of state. The levels of compensation in these firms

are thus less important to the executives than their political careers. In extreme cases,

we can expect SOECG executives to sacrifice their compensation levels for the sake

of career advancement. Hence, we would expect the pay of SOECG executives to

11

adjust more slowly, even if they have been relatively under-paid in the past. When

compensation disclosure becomes more transparent after 2005, we expect managers in

SOECGs to have fewer incentives to increase their monetary compensation, since

they derive greater benefit from political advancement rather than direct

compensations. Meanwhile, the central government has also issued several

regulations to limit the compensation for SOECG executives, and this in turn would

create greater pressure for over-paid executives to receive lower pay increases (even

pay cut) if compensation information becomes public. Therefore, if there is greater

transparency in compensation disclosure after 2005, SOECG executives who were

over-paid compared to the industry average would expect to receive much lower pay

increases.

SOELGs, however, are subject to weaker supervision and management (Chen

et al., 2009). Jiang et al. (2010) find that tunneling behavior is more severe for

SOELGs than for SOECGs, which suggests a more severe agency problem for

SOELGs. We therefore hypothesize that executives of SOELGs are more likely to

engage in opportunistic benchmarking behavior. If peer compensation information

becomes available, SOELG executives can justify a higher pay raise using selective

benchmarks. We expect under-paid SOELG executives to increase their compensation

faster after 2005. For over-paid executives, we also expect their salaries to be less

responsive to the industry benchmarks, due to the heightened agency conflicts within

SOELGs. They will have greater incentives to engage in selective benchmarking

behavior in order to maintain their higher pay level.

12

For private non-SOE firms, the compensation for executives is more directly

driven by the competitive labor market, and we expect under-paid executives to have

greater salary increases after 2005 when peer compensation information becomes

more available. Overall, we propose the following hypotheses:

H3a: Over-paid (under-paid) executives in SOECGs will receive less (more)

pay increase in the following year; however, this pattern is more (less)

pronounced since 2005.

H3b: Over-paid (under-paid) executives in SOELGs and non-SOE firms will

receive less (more) pay increases in the following year, and this pattern is less

(more) pronounced since 2005.

3. Data, Variable Definition and Empirical Methodology

3.1 Data and Definitions of Variables

Our sample includes all firms listed in the China Stock Market and

Accounting Research (CSMAR) database during the period between 2003 and 2007.

We use data from the two years before and after 2005 to construct the sample for

comparison. We exclude firms in the financial sector, because their financial data are

not directly comparable to those of other firms. We also remove observations with

missing financial information, ownership data or compensation information, and firms

missing two consecutive years of information on managerial compensation, sales

growth, debt, ROA or firm size. To mitigate the influence of possible spurious outliers,

13

we also winsorize all variables at the 1% and 99% level. We obtain a final sample of

2878 firm-year observations.

One of the key variables of interest is the change in compensation from year t-

1 to year t. As companies only disclosed the sum of their top three executives’

compensations prior to 2005, we can only examine the compensation benchmarking

behavior for the top three executives as a whole. We define Compen as the total

compensation of the three highest-paid executives in the firm. ∆Compen is computed

as Compen in the current year (t) minus Compen in the previous year (t-1), scaled by

Compen in year t-1. To measure the effect of peer benchmarking, we first identify

peer firms as those operating in the same industry (as classified by the CSRC). We

then define the mean and the median of the total compensation reported by these firms

as PeerMean and PeerMed. The measure of peer benchmarking (BMark) is the

difference between company compensation and peer compensation, which are defined

as BmarkMean = (PeerMean-Compen)/PeerMean, or BmarkMed = (PeerMed-

Compen)/PeerMed. Hence, if executives are paid above the industry average,

BmarkMean and BmarkMed should be negative. To facilitate the interpretation of our

results, we use the absolute value of these variables when conducting the empirical

tests.

Following previous studies, we control for corporate governance and company

financial characteristics. As in the studies by Albuquerque et al. (2013), Bizjak et al.

(2008; 2011) and Cadma and Carter (2014), we control for the ultimate owner of the

firm. Ownership equals 1 if a firm is controlled by the state, and 0 otherwise. We also

14

control for ownership by the largest shareholders. Topshare is measured as the

number of shares owned by the largest shareholder divided by the total shares

outstanding. Duality equals 1 if the CEO is also the chairman of the board, and 0

otherwise. Board independence (BIndepen) is proxied by the number of independent

directors in relation to the total number of directors. Board size (Bsize) is the natural

log of the number of directors on the board. ∆Growth represents change in sales

growth, with sales growth measured by (Salest-Salest-1)/Salest-1. ∆Lev represents

change in leverage, and is measured by (Levt-Levt-1)/Levt-1. Lev is defined as total

debts over total assets. ∆ROA represents change in return on total assets, and is

measured by NIt/Total Assett –NIt-1/Total Assett-1. ∆Size is the change in firm size, and

firm size is measured as the natural log of total assets. To control for the effect of the

2005 split-share structure reform (Liao et al., 2014), we also control for the number of

non-tradable shares (Ntradeshares) issued by the firm. Finally, we define a dummy

variable Period05 that equals 1 if the observation occurs after 2005, and 0 otherwise.

Insert Table 1 Here

Table 2 shows the summary of statistics for our sample. The mean (median)

value for the dependent variable, ∆Compen, is 0.0175 (0.0114). BmarkMean has a

mean of 0.0271 and a median of 0.0245. BmarkMed has very similar results,

suggesting that very little difference exists between the two industry peer benchmarks.

We also find that 69.85% of our observations are SOEs. We therefore further classify

our sample into SOEs controlled by the central government and SOEs controlled by

15

local governments. We classify 11.02% of our observations as SOECGs and 58.83%

as SOELGs.

Insert Table 2 Here

3.2 Empirical Models

Following Bizjak, Lemmom and Naveen (2008), we use the following two

models to test the effects of industry compensation benchmarking:

∆Compen = β0 + β1 |BMark| + β2 Period05 + β3 Ownership + β4 Topshare

+ β5 Duality + β6 BIndepen + β7 Bsize + β8 ∆Growth + β9 ∆Lev

+ β10∆ROA + β11 ∆Size + β12 Ntradeshares + Σ Year + Σ Industry (1)

∆Compen = β0 + β1 |Bmark| + β2 |Bmark| × Period05 + β3 Period05 + β4 Ownership

+ β5 Topshare + β6 Director + β7 Indepen + β8 Bsize + β9 ∆Growth

+ β10 ∆Lev + β11 ∆ROA + β12 ∆Size +β13 Ntradeshares + Σ Year

+ Σ Industry (2)

In both models we control for the year and industry fixed effects. The industry

benchmarking measure Bmark is either the mean compensation benchmark

(BmarkMean) or the median compensation benchmark (BmarkMed).

4. Empirical Results

16

The results for model 1 using the full sample are shown in Table 3. The

coefficient for BmarkMean (BmarkMed) is 0.1747 (0.1871) and is significant at the 1%

level. This result suggests that industry benchmarking is evident in the Chinese

market.

We then divide the full sample into two groups: those in which executives are

paid above the mean level of their industry peers, and those in which executives are

paid below that level. In general, increases in size and firm performance (∆ROA) are

associated with positive pay increases. It is worth noting that BmarkMean is negative

if the executives are paid more than their peers. To make interpretation easier, we use

the absolute value of BmarkMean in these tests. We can then interpret the negative

and significant coefficient for BmarkMean as evidence suggesting that executives

who are paid above the industry average tend to subsequently receive lower pay raises.

The coefficients for BmarkMean and BmarkMed are -0.4711 and -0.4823,

respectively. For the group of executives paid below the industry average, the

coefficients for BmarkMean and BmarkMed are both positive and they are significant.

These results suggest that the more an executive is under-paid, the greater a pay

increase she will receive in the subsequent year. These results are consistent with

hypotheses 1a and 2a.

Insert Table 3 Here

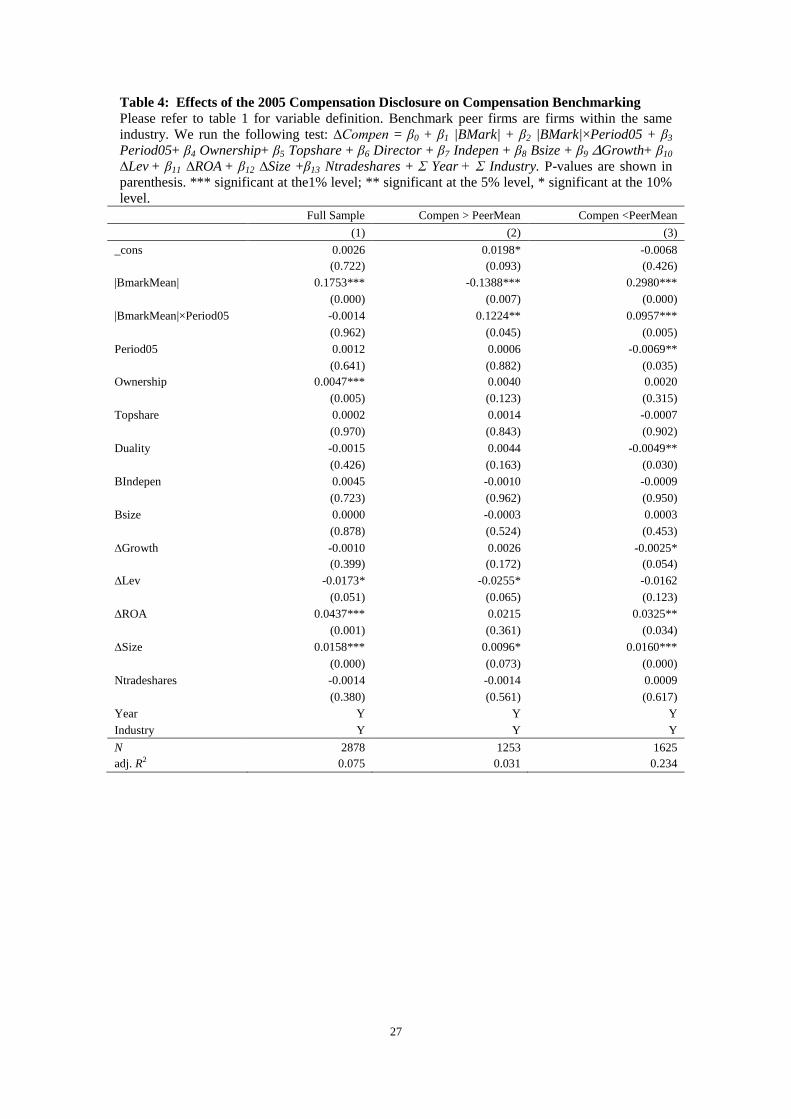

We next run model 2 and examine the effects of the 2005 compensation

disclosure requirement. The results are shown in Table 4. Interestingly, the

17

coefficients for BmarkMean3 are positive and significant for the full sample and for

two sub-samples. However, the coefficient for the interaction term between

BmarkMean and the Period05 dummy variable is insignificant, which suggests no

significant effect since the 2005 compensation disclosure requirement. Further

analysis using subsamples reveals that the coefficients for the interaction term are

both significant. If executives are paid above the industry average, they will thus

receive lower pay raises in the subsequent year (negative coefficient for BmarkMean).

However, this effect is weaker since 2005 (positive coefficient for the interaction

term). These findings suggest that in response to requirements for more transparent

disclosure, executives might engage in opportunistic benchmarking, and therefore

find it easy to maintain their high compensation levels. This result is also consistent

with a greater completion in the labor market after 2005. In order to retain talented

executives, firms have to offer a more competitive compensation package (Bryson et

al. 2014). Meanwhile, those executives who are paid below the industry average will

receive higher pay raises in the subsequent year (the coefficient for BmarkMean is

0.1753). After 2005, we observe a faster adjustment rate (the coefficient for the

interaction term is -0.0014). If an executive perceives her pay as below the market

average, then compensation disclosure by her peer companies allows her to justify a

greater increase in compensation. It is therefore important to realize that

compensation disclosure might have different effects on the benchmarking behavior

3 In the following analysis, the results using BmarkMean and BmarkMed are all qualitatively similar. Therefore,

we only report results using BmarkMean in the subsequent portions of our study.

18

of over-paid and under-paid executives. Overall, our results as shown in Table 4

support hypotheses 2b.

Insert Table 4 Here

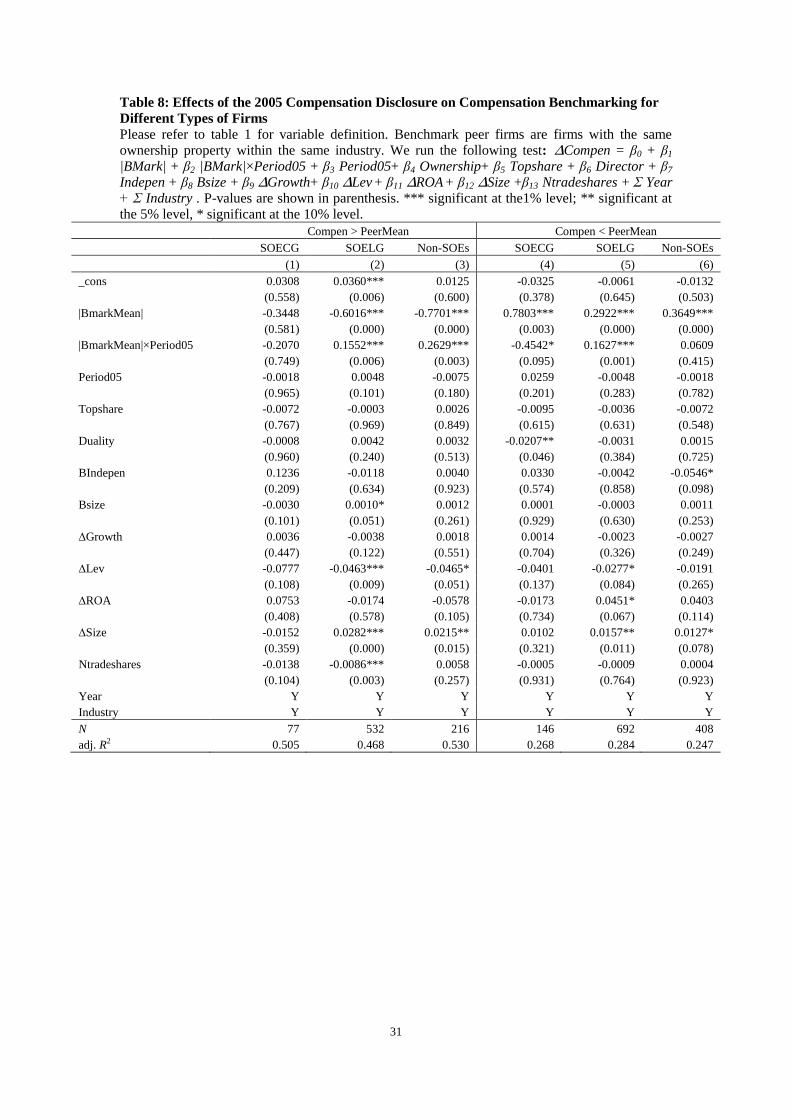

Our final test examines the differences in benchmarking behavior among

SOECG, SOELG and Non-SOE firms. As the over-paid and under-paid executives

display different benchmarking characteristics, we first divide our sample into these

two groups. Then we run the tests for the SOECG, SOELG and Non-SOE samples

separately. In Table 5, we see that if executives are paid above the industry average,

they will receive lower pay increases subsequently (the coefficients for BmarkMean

are negative for all three sub-samples). Interestingly, the interaction term between

BmarkMean and Period05 is negative for the SOECG sample. This result shows the

executives of SOECGs have received lower increases in compensation since the

improved disclosure requirement of 2005. This finding is consistent with the common

observation that SOECGs are highly monitored, and their executives are not mainly

incentivized by levels of compensation. However, the opposite situation applies for

SOELGs and Non-SOEs. It seems that executives in these types of firms are more

likely to engage in opportunistic benchmarking to secure their higher pay levels. For

the under-paid executives, we see in Column B of Table 5 that the coefficients for

BmarkMean are all positive, which suggests an upward pay adjustment in the

subsequent year. Although the executives of SOECGs received lower pay raises after

2005, the executives of SOELGs received greater increases in pay. For Non-SOEs,

the coefficient for the interaction term is insignificant. The striking differences among

19

the SOECG, SOELG and Non-SOE firms suggest that different agency issues and

incentives directly affect the outcomes of the disclosure policy. Specifically,

transparency in compensation deters executives in SOECGs from acquiring excessive

compensation, but executives in SOELGs and Non-SOEs may use the disclosed

information to engage in opportunistic peer benchmarking.

Insert Table 5 Here

5. Robustness Check

In the previously reported tests, we use all firms in the same industry as

benchmark firms. Some observers, however, might argue that firms tend to

benchmark against peers with the same ownership types. To ensure that our results are

robust, we re-run all of the tests using only firms with the same ownership types

within the same industry as benchmark firms. Although this method reduces the

number of peer firms in the same industry, our results as shown in Tables 6 through 8

are very similar to those reported in Tables 3 through 5.

Instead of using all firms in the same industry, we follow the approach taken

by Brookman and Thistle (2013) and define peer companies as firms of comparable

size (0.5-2 times the firm size) in the same industry. The results, shown in Tables 9,

10 and 11 are also very similar to those reported earlier.

6. Conclusions

20

Improved compensation disclosure allows firms to better benchmark executive

compensation against their peers. However, such benchmarking can also result in

opportunistic behavior in which managers strategically choose their peers to inflate

their overall compensation. Studies on the 2006 SEC regulation have found mixed

evidence with respect to the effect of greater disclosure on compensation contracting.

As the pros and cons of disclosure are closely related to institutional and market

conditions, we examine the effects of the compensation disclosure rule in China as

issued by the CSRC in 2005. We find evidence suggesting industry peer

benchmarking in China. Over-paid executives tend to receive lower pay increases in

the subsequent year. However, it seems that these over-paid executives have been able

to use peer disclosure to justify their compensation and to reduce the effect of

downward pay adjustment. We find that under-paid executives tend to receive

significant pay increases in the subsequent period, and this pattern has grown stronger

since 2005 when detailed information on executive compensation became available.

Overall, it seems that improved compensation disclosure has had an overall positive

effect on the levels of executive compensation.

More importantly, we show that firms with different ownership types behave

differently toward compensation disclosure. We provide additional evidence showing

that executives in SOECGs are under stricter monitoring, and both the under-paid and

over-paid executives have been more likely to reduce their pay increases since 2005.

However, executives of SOELG and non-SOE firms are more likely to use improved

compensation disclosure to secure higher pay.

21

Our study explores the effect of compensation disclosure in an emerging

market, and the results show how firms with different forms of ownership benchmark

executive compensation differently for their under- or over-paid executives. In future

studies, it would be interesting to examine whether China continues to improve its

compensation disclosure and how compensation contracting, specifically

benchmarking behavior, might further evolve as more and more Chinese companies

are listed on foreign exchanges.

22

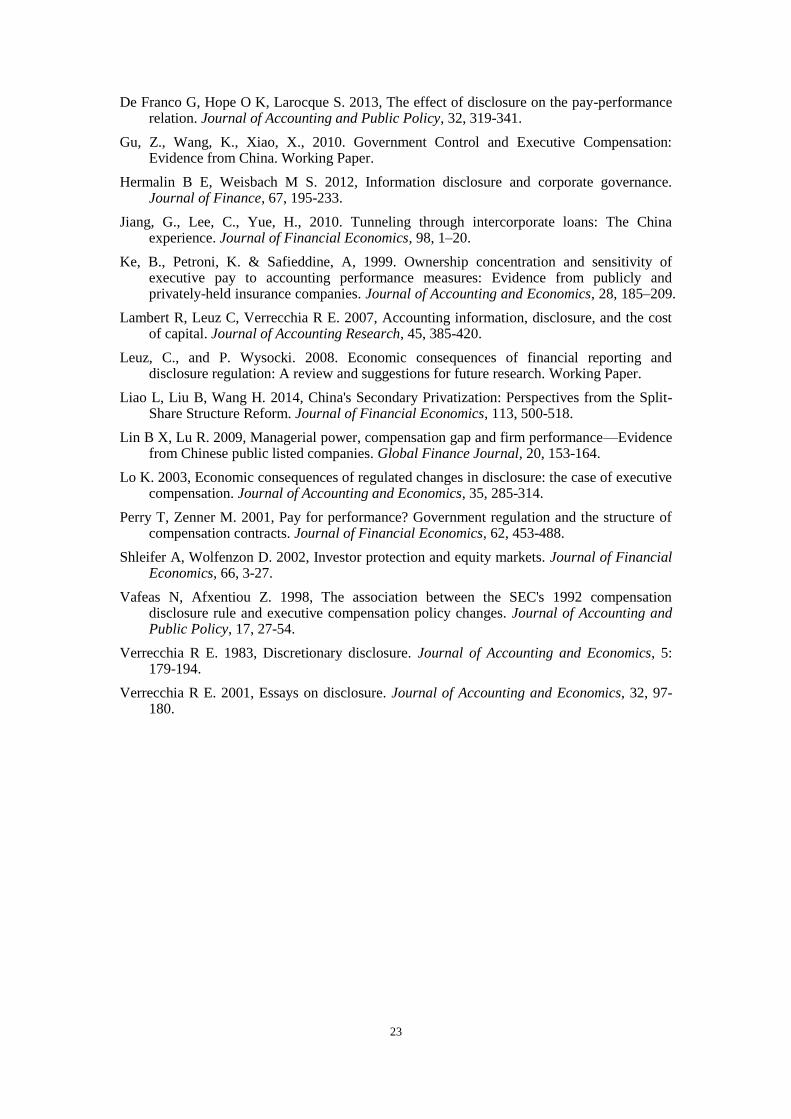

References:

Albuquerque, A., Franco, G. and Verdi, R., 2013, Peer Choice in CEO Compensation. Journal of Financial Economics, 108, 160-181.

Beaulieu P, Ding S, Qu B. 2012, Compensation disclosure in China., Asia-Pacific Journal of Accounting & Economics, 19, 253-277.

Bizjak, J., Lemmom, M. and Naveen, L., 2008, Does the Use of Peer Groups Contribute to Higher Pay and Less Efficient Compensation? Journal of Financial Economics, 90, 152-168.

Bizjak, J., Lemmom, M. and Nguyen,T., 2011, Are All CEOs above Average? An Empirical Analysis of Compensation Peer Groups and Pay Design. Journal of Financial Economics, 100, 538-555.

Brookman J T, Thistle P D. 2013, Managerial compensation: Luck, skill or labor markets? Journal of Corporate Finance, 21, 252-268.

Bryson A, J Forth and M Zhou (2014), "Same or Different? The CEO Labour Market in China's Public Listed Companies", The Economic Journal, 124, F90-F108

Cadman B, Carter M E. 2013, Compensation peer groups and their relation with CEO pay. Journal of Management Accounting Research, 26, 57-82.

Chen, G, Firth, M, Xu, L ,2009. Does the type of ownership control matter? Evidence from China’s listed companies. Journal of Banking and Finance, 33, 171-181.

Chen, J., Ezzamel M. and Cai, Z., 2011, Managerial power theory, tournament theory, and executive pay in China., Journal of Corporate Finance, 17, 1176–1199.

Cheng, M.Y, Lin, B.X., and Wei. M.H., 2014, Executive compensation in family firms: The effect of multiple family members., Journal of Corporate Finance, forthcoming.

Conyon, M. and He, L., 2011. Executive compensation and corporate governance in China Journal of Corporate Finance, 17, 1158–1175.

Ernstberger, J. and Grüning, M., 2013. How do Firm- and Country-Level Governance Mechanisms Affect Firms’ Disclosure? Journal of Accounting and Public Policy , 32, 50-67.

Ezzamel M., and Watson, R., 1998, Market Comparison Earnings and the Bidding-Up of Executive Cash Compensation: Evidence from the United Kingdom. Academy of Management Journal, 41, 221-231.

Ezzamel M, Watson R. 2002, Pay comparability across and within UK boards: An empirical analysis of the cash pay awards to CEOs and other board members. Journal of Management Studies, 39, 207-232.

Fan, J., Wong, T. and Zhang, T., 2007, Politically connected CEOs, corporate governance, and Post-IPO performance of China’s. Journal of Financial Economics, 84, 330-357.

Faulkender, M., and Yang, J., 2010, Inside the Black Box: the Role and Composition of Compensation Peer Groups. Journal of Financial Economics, 96, 257-270.

Faulkender, M., and Yang, J., 2013. Is Disclosure an Effective Cleansing Mechanism? The Dynamics of Compensation Peer Benchmarking. Review of Financial Studies, 20, 806-839.

Feltham, G.A. and Xie J.Z., 1992, Voluntary financial disclosure in an entry game with continua of types. Contemporary Accounting Research, 9, 46-80.

Firth, M., Fung, P., & Rui, O. M. 2006. Corporate performance and CEO compensation in China. Journal of Corporate Finance, 12, 693–714.

23

De Franco G, Hope O K, Larocque S. 2013, The effect of disclosure on the pay-performance relation. Journal of Accounting and Public Policy, 32, 319-341.

Gu, Z., Wang, K., Xiao, X., 2010. Government Control and Executive Compensation: Evidence from China. Working Paper.

Hermalin B E, Weisbach M S. 2012, Information disclosure and corporate governance. Journal of Finance, 67, 195-233.

Jiang, G., Lee, C., Yue, H., 2010. Tunneling through intercorporate loans: The China experience. Journal of Financial Economics, 98, 1–20.

Ke, B., Petroni, K. & Safieddine, A, 1999. Ownership concentration and sensitivity of executive pay to accounting performance measures: Evidence from publicly and privately-held insurance companies. Journal of Accounting and Economics, 28, 185–209.

Lambert R, Leuz C, Verrecchia R E. 2007, Accounting information, disclosure, and the cost of capital. Journal of Accounting Research, 45, 385-420.

Leuz, C., and P. Wysocki. 2008. Economic consequences of financial reporting and disclosure regulation: A review and suggestions for future research. Working Paper.

Liao L, Liu B, Wang H. 2014, China's Secondary Privatization: Perspectives from the Split-Share Structure Reform. Journal of Financial Economics, 113, 500-518.

Lin B X, Lu R. 2009, Managerial power, compensation gap and firm performance—Evidence from Chinese public listed companies. Global Finance Journal, 20, 153-164.

Lo K. 2003, Economic consequences of regulated changes in disclosure: the case of executive compensation. Journal of Accounting and Economics, 35, 285-314.

Perry T, Zenner M. 2001, Pay for performance? Government regulation and the structure of compensation contracts. Journal of Financial Economics, 62, 453-488.

Shleifer A, Wolfenzon D. 2002, Investor protection and equity markets. Journal of Financial Economics, 66, 3-27.

Vafeas N, Afxentiou Z. 1998, The association between the SEC's 1992 compensation disclosure rule and executive compensation policy changes. Journal of Accounting and Public Policy, 17, 27-54.

Verrecchia R E. 1983, Discretionary disclosure. Journal of Accounting and Economics, 5: 179-194.

Verrecchia R E. 2001, Essays on disclosure. Journal of Accounting and Economics, 32, 97-180.

24

Table 1: Variable Definition

Variables Definition

∆Compen

computed as Compen in the current year (t) minus Compen

the previous year (t-1), and scaled by Compen in year t-1,

where Compen is the total compensation of the three highest-

paid executives in the firm

The difference

between

managerial pay

and industry

peers

BmarkMean

(PeerMean-Compen)/PeerMean, where PeerMean is the mean

of the total compensation reported by firms operating in the

same industry

BmarkMed

(PeerMed-Compen)/PeerMed, where PeerMed is the median

of the total compensation reported by firms operating in the

same industry

Period05 dummy variable, taking the value 1 if the year is 2006 or

2007, and 0 otherwise

Ownership dummy variable, taking the value 1 if the ultimate controller

is the state, and 0 otherwise

SOECG dummy variable, taking the value 1 if the ultimate controller

is the central-government, and 0 otherwise

SOELG dummy variable, taking the value 1 if the ultimate controller

is the local-government, and 0 otherwise

Topshare proportion of shareholdings of the largest shareholder

Duality dummy variable, taking the value 1 if CEO is the Chairman,

and 0 otherwise

BIndepen ratio of number of independent directors to number of total

directors

Bsize natural log size of the board

∆Growth

change of sales growth during period t and period t-1, where

sales growth is change of sales during period t and period t-1,

and scaled by sales in year t-1

∆Lev change of leverage during period t and period t-1, where

leverage is the ratio of total debts to total assets

∆ROA change of ROA during period t and period t-1, where ROA is

the ratio of net incomes to total assets

∆Size change of firm size during period t and period t-1, where firm

size is the natural log of total assets

Ntradeshares

dummy variable, taking the value 1 if non-tradable shares of

the firm are above the mean of all firms in the same industry,

and 0 otherwise

25

Table 2: Descriptive Statistics

Please refer to table 1 for variable definitions. The total number of observation for the sample is

3830. We report the minimum (Min), maximum (Max), mean, median and standard deviation

(STD) for the complete sample here.

Variable Min Max Mean Median STD

Compen

(ten thousands RMB) 18 1400 73 54 75

∆Compen -0.0795 0.1431 0.0175 0.0114 0.0344

BmarkMean -0.1729 0.2047 0.0271 0.0245 0.0655

BmarkMed -0.1682 0.2097 0.0330 0.0298 0.0654

Ownership 0.0000 1.0000 0.6985 1.0000 0.4590

SOECG 0.0000 1.0000 0.1102 0.0000 0.3132

SOELG 0.0000 1.0000 0.5883 1.0000 0.4922

Topshare 0.0899 0.7678 0.3928 0.3721 0.1631

Duality 0.0000 1.0000 0.1151 0.0000 0.3192

BIndepen 0.0000 0.5455 0.3445 0.3333 0.0521

Bsize 5.0000 15.0000 9.5961 9.0000 2.0385

∆Growth -2.9544 2.7859 0.0263 0.0191 0.5858

∆Lev -0.2219 0.2910 0.0171 0.0111 0.0835

∆ROA -0.2493 0.1760 -0.0009 0.0008 0.0532

∆Size -0.4192 0.9642 0.1230 0.0962 0.2121

Ntradeshares 0.0000 1.0000 0.4962 0.0000 0.5000

26

Table 3: Test on Compensation Industry Benchmarking

Please refer to table 1 for variable definition. Benchmark peer firms are firms within the same

industry. We run the following model here ∆Compen = β0 + β1 |BMark| + β2 Period05 + β3 Ownership + β4 Topshare + β5 Duality + β6 BIndepen + β7 Bsize + β8 ∆Growth + β9 ∆Lev +

β10∆ROA +β11 ∆Size +β12 Ntradeshares +Σ Year +Σ Industry . P-values are shown in parenthesis.

*** significant at the1% level; ** significant at the 5% level, * significant at the 10% level.

Full sample Compen >

PeerMean

Compen >

PeerMed

Compen <

PeerMean

Compen <

PeerMed

(1) (2) (3) (4) (5) (6)

_cons 0.0026 0.0009 0.0196** 0.0187** -0.0127 -0.0117

(0.716) (0.897) (0.027) (0.032) (0.121) (0.158)

|BmarkMean| 0.1747*** -0.4711*** 0.3573***

(0.000) (0.000) (0.000)

|BmarkMed| 0.1871*** -0.4823*** 0.3404***

(0.000) (0.000) (0.000)

Period05 0.0011 0.0020 0.0047* 0.0063** 0.0014 0.0020

(0.556) (0.278) (0.057) (0.013) (0.512) (0.356)

Ownership 0.0047*** 0.0049*** 0.0012 0.0010 0.0021 0.0016

(0.005) (0.003) (0.547) (0.607) (0.274) (0.402)

Topshare 0.0002 0.0002 -0.0016 -0.0010 -0.0016 -0.0047

(0.970) (0.964) (0.762) (0.861) (0.768) (0.369)

Duality -0.0016 -0.0016 0.0054** 0.0053** -0.0041* -0.0042*

(0.424) (0.406) (0.022) (0.030) (0.058) (0.053)

BIndepen 0.0045 0.0058 0.0038 0.0031 0.0006 0.0001

(0.723) (0.645) (0.809) (0.851) (0.965) (0.992)

Bsize 0.0000 0.0001 0.0010*** 0.0011*** 0.0004 0.0003

(0.879) (0.743) (0.006) (0.003) (0.359) (0.389)

∆Growth -0.0010 -0.0011 -0.0003 -0.0001 -0.0025** -0.0026**

(0.399) (0.350) (0.817) (0.966) (0.043) (0.041)

∆Lev -0.0173* -0.0179** -0.0449*** -0.0428*** -0.0137 -0.0163*

(0.051) (0.041) (0.000) (0.000) (0.175) (0.097)

∆ROA 0.0437*** 0.0430*** -0.0076 0.0026 0.0343** 0.0388***

(0.001) (0.001) (0.669) (0.892) (0.020) (0.007)

∆Size 0.0158*** 0.0166*** 0.0239*** 0.0194*** 0.0156*** 0.0176***

(0.000) (0.000) (0.000) (0.000) (0.000) (0.000)

Ntradeshares -0.0014 -0.0015 -0.0030* -0.0032* 0.0010 0.0015

(0.380) (0.338) (0.096) (0.082) (0.579) (0.401)

Year Y Y Y Y Y Y

Industry Y Y Y Y Y Y

N 2878 2878 1253 1147 1625 1731

adj. R2 0.075 0.086 0.445 0.453 0.293 0.272

27

Table 4: Effects of the 2005 Compensation Disclosure on Compensation Benchmarking

Please refer to table 1 for variable definition. Benchmark peer firms are firms within the same

industry. We run the following test: ∆Compen = β0 + β1 |BMark| + β2 |BMark|×Period05 + β3 Period05+ β4 Ownership+ β5 Topshare + β6 Director + β7 Indepen + β8 Bsize + β9 ∆Growth+ β10 ∆Lev + β11 ∆ROA + β12 ∆Size +β13 Ntradeshares + Σ Year + Σ Industry. P-values are shown in

parenthesis. *** significant at the1% level; ** significant at the 5% level, * significant at the 10%

level.

Full Sample Compen > PeerMean Compen <PeerMean

(1) (2) (3)

_cons 0.0026 0.0198* -0.0068

(0.722) (0.093) (0.426)

|BmarkMean| 0.1753*** -0.1388*** 0.2980***

(0.000) (0.007) (0.000)

|BmarkMean|×Period05 -0.0014 0.1224** 0.0957***

(0.962) (0.045) (0.005)

Period05 0.0012 0.0006 -0.0069**

(0.641) (0.882) (0.035)

Ownership 0.0047*** 0.0040 0.0020

(0.005) (0.123) (0.315)

Topshare 0.0002 0.0014 -0.0007

(0.970) (0.843) (0.902)

Duality -0.0015 0.0044 -0.0049**

(0.426) (0.163) (0.030)

BIndepen 0.0045 -0.0010 -0.0009

(0.723) (0.962) (0.950)

Bsize 0.0000 -0.0003 0.0003

(0.878) (0.524) (0.453)

∆Growth -0.0010 0.0026 -0.0025*

(0.399) (0.172) (0.054)

∆Lev -0.0173* -0.0255* -0.0162

(0.051) (0.065) (0.123)

∆ROA 0.0437*** 0.0215 0.0325**

(0.001) (0.361) (0.034)

∆Size 0.0158*** 0.0096* 0.0160***

(0.000) (0.073) (0.000)

Ntradeshares -0.0014 -0.0014 0.0009

(0.380) (0.561) (0.617)

Year Y Y Y

Industry Y Y Y

N 2878 1253 1625

adj. R2 0.075 0.031 0.234

28

Table 5: Effects of the 2005 Compensation Disclosure on Compensation Benchmarking for

Different Types of Firms

Please refer to table 1 for variable definition. Benchmark peer firms are firms within the same

industry. We run the following test: ∆Compen = β0 + β1 |BMark| + β2 |BMark|×Period05 + β3 Period05+ β4 Ownership+ β5 Topshare + β6 Director + β7 Indepen + β8 Bsize + β9 ∆Growth+ β10 ∆Lev + β11 ∆ROA+ β12 ∆Size +β13 Ntradeshares + Σ Year + Σ Industry . P-values are shown in

parenthesis. *** significant at the1% level; ** significant at the 5% level, * significant at the 10%

level.

Compen > PeerMean Compen < PeerMean

SOECG SOELG Non-SOEs SOECG SOELG Non-SOEs

(1) (2) (3) (4) (5) (6)

_cons 0.0375 0.0288** 0.0121 -0.0312 -0.0081 0.0004

(0.165) (0.013) (0.525) (0.269) (0.430) (0.980)

|BmarkMean| -0.2794*** -0.5873*** -0.6196*** 0.4735*** 0.2741*** 0.3876***

(0.006) (0.000) (0.000) (0.000) (0.000) (0.000)

|BmarkMean|×Period05 -0.1891* 0.1834*** 0.1522** -0.2005* 0.1895*** 0.0624

(0.079) (0.000) (0.011) (0.068) (0.000) (0.246)

Period05 -0.0106 0.0060* -0.0037 0.0243** -0.0118*** -0.0002

(0.423) (0.052) (0.476) (0.040) (0.003) (0.964)

Topshare 0.0029 0.0005 0.0019 0.0020 -0.0008 -0.0057

(0.845) (0.940) (0.855) (0.916) (0.892) (0.602)

Duality 0.0227* 0.0041 0.0030 -0.0018 -0.0047 0.0001

(0.092) (0.219) (0.414) (0.822) (0.106) (0.985)

BIndepen -0.0188 -0.0123 0.0212 -0.0044 0.0085 -0.0308

(0.674) (0.541) (0.535) (0.946) (0.617) (0.265)

Bsize 0.0003 0.0010** 0.0016* 0.0009 0.0001 0.0003

(0.715) (0.040) (0.076) (0.480) (0.762) (0.694)

∆Growth 0.0034 -0.0034 0.0007 -0.0040 -0.0013 -0.0030

(0.280) (0.120) (0.758) (0.375) (0.492) (0.107)

∆Lev 0.0096 -0.0550*** -0.0601*** -0.0318 -0.0241* 0.0004

(0.670) (0.001) (0.001) (0.418) (0.087) (0.983)

∆ROA 0.0808** -0.0129 -0.0609** -0.0008 0.0404* 0.0289

(0.045) (0.635) (0.041) (0.988) (0.053) (0.218)

∆Size 0.0065 0.0310*** 0.0254*** -0.0003 0.0195*** 0.0169**

(0.440) (0.000) (0.000) (0.988) (0.000) (0.012)

Ntradeshares 0.0057 -0.0050** 0.0020 -0.0078 0.0023 0.0013

(0.226) (0.046) (0.603) (0.255) (0.372) (0.693)

Year Y Y Y Y Y Y

Industry Y Y Y Y Y Y

N 188 727 338 145 976 504

adj. R2 0.455 0.448 0.517 0.188 0.286 0.344

29

Table 6 Test on Compensation Industry Benchmarking

Please refer to table 1 for variable definition. Benchmark peer firms are firms with the same

ownership property within the same industry. We run the following model here ∆Compen = β0 +

β1 |BMark| + β2 Period05 + β3 Ownership + β4 Topshare + β5 Duality + β6 BIndepen + β7 Bsize +

β8 ∆Growth + β9 ∆Lev + β10∆ROA +β11 ∆Size +β12 Ntradeshares +Σ Year +Σ Industry . P-values

are shown in parenthesis. *** significant at the1% level; ** significant at the 5% level, *

significant at the 10% level.

Full Sample Compen > PeerMean Compen < PeerMean

(1) (2) (3)

_cons -0.0004 0.0192* -0.0165*

(0.963) (0.071) (0.094)

|BmarkMean| 0.1959*** -0.4954*** 0.3800***

(0.000) (0.000) (0.000)

Period05 0.0044** 0.0035 0.0052**

(0.024) (0.146) (0.016)

Ownership 0.0057*** 0.0058** 0.0039*

(0.005) (0.024) (0.078)

Topshare -0.0038 -0.0028 -0.0073

(0.450) (0.648) (0.199)

Duality -0.0007 0.0067** -0.0031

(0.754) (0.013) (0.230)

BIndepen -0.0014 0.0002 -0.0166

(0.929) (0.992) (0.342)

Bsize 0.0001 0.0011** 0.0003

(0.771) (0.012) (0.562)

∆Growth -0.0017 0.0006 -0.0022

(0.224) (0.730) (0.132)

∆Lev -0.0250** -0.0452*** -0.0204*

(0.011) (0.000) (0.052)

∆ROA 0.0338** -0.0214 0.0426***

(0.030) (0.328) (0.008)

∆Size 0.0146*** 0.0192*** 0.0144***

(0.000) (0.000) (0.000)

Ntradeshares -0.0008 -0.0053** 0.0004

(0.684) (0.023) (0.833)

Year Y Y Y

Industry Y Y Y

N 2071 825 1246

adj. R2 0.080 0.464 0.267

30

Table 7: Effect of the 2005 Compensation Disclosure on Compensation Benchmarking

Please refer to table 1 for variable definition. Benchmark peer firms are firms with the same

ownership property within the same industry. We run the following test: ∆Compen = β0 + β1 |BMark| + β2 |BMark|×Period05 + β3 Period05+ β4 Ownership+ β5 Topshare + β6 Director + β7 Indepen + β8 Bsize + β9 ∆Growth+ β10 ∆Lev + β11 ∆ROA+ β12 ∆Size +β13 Ntradeshares + Σ Year + Σ Industry . P-values are shown in parenthesis. *** significant at the1% level; ** significant at the

5% level, * significant at the 10% level.

Full Sample Compen > PeerMean Compen < PeerMean

(1) (2) (3)

_cons 0.0014 0.0220** -0.0123

(0.878) (0.038) (0.216)

|BmarkMean| 0.1648*** -0.6314*** 0.3142***

(0.000) (0.000) (0.000)

|BmarkMean|×Period05 0.0476 0.1763*** 0.1067***

(0.190) (0.000) (0.006)

Period05 0.0015 0.0011 -0.0022

(0.601) (0.658) (0.517)

Ownership 0.0057*** 0.0056** 0.0040*

(0.005) (0.027) (0.069)

Topshare -0.0037 -0.0047 -0.0069

(0.464) (0.441) (0.229)

Duality -0.0008 0.0066** -0.0033

(0.710) (0.014) (0.198)

BIndepen -0.0014 -0.0019 -0.0168

(0.931) (0.925) (0.336)

Bsize 0.0001 0.0010** 0.0003

(0.766) (0.019) (0.498)

∆Growth -0.0016 0.0004 -0.0021

(0.232) (0.821) (0.146)

∆Lev -0.0248** -0.0425*** -0.0203*

(0.012) (0.001) (0.052)

∆ROA 0.0335** -0.0261 0.0429***

(0.031) (0.230) (0.008)

∆Size 0.0146*** 0.0196*** 0.0145***

(0.000) (0.000) (0.000)

Ntradeshares -0.0008 -0.0049** 0.0001

(0.680) (0.032) (0.955)

Year Y Y Y

Industry Y Y Y

N 2071 825 1246

adj. R2 0.080 0.473 0.271

31

Table 8: Effects of the 2005 Compensation Disclosure on Compensation Benchmarking for

Different Types of Firms

Please refer to table 1 for variable definition. Benchmark peer firms are firms with the same

ownership property within the same industry. We run the following test: ∆Compen = β0 + β1 |BMark| + β2 |BMark|×Period05 + β3 Period05+ β4 Ownership+ β5 Topshare + β6 Director + β7 Indepen + β8 Bsize + β9 ∆Growth+ β10 ∆Lev + β11 ∆ROA + β12 ∆Size +β13 Ntradeshares + Σ Year

+ Σ Industry . P-values are shown in parenthesis. *** significant at the1% level; ** significant at

the 5% level, * significant at the 10% level.

Compen > PeerMean Compen < PeerMean

SOECG SOELG Non-SOEs SOECG SOELG Non-SOEs

(1) (2) (3) (4) (5) (6)

_cons 0.0308 0.0360*** 0.0125 -0.0325 -0.0061 -0.0132

(0.558) (0.006) (0.600) (0.378) (0.645) (0.503)

|BmarkMean| -0.3448 -0.6016*** -0.7701*** 0.7803*** 0.2922*** 0.3649***

(0.581) (0.000) (0.000) (0.003) (0.000) (0.000)

|BmarkMean|×Period05 -0.2070 0.1552*** 0.2629*** -0.4542* 0.1627*** 0.0609

(0.749) (0.006) (0.003) (0.095) (0.001) (0.415)

Period05 -0.0018 0.0048 -0.0075 0.0259 -0.0048 -0.0018

(0.965) (0.101) (0.180) (0.201) (0.283) (0.782)

Topshare -0.0072 -0.0003 0.0026 -0.0095 -0.0036 -0.0072

(0.767) (0.969) (0.849) (0.615) (0.631) (0.548)

Duality -0.0008 0.0042 0.0032 -0.0207** -0.0031 0.0015

(0.960) (0.240) (0.513) (0.046) (0.384) (0.725)

BIndepen 0.1236 -0.0118 0.0040 0.0330 -0.0042 -0.0546*

(0.209) (0.634) (0.923) (0.574) (0.858) (0.098)

Bsize -0.0030 0.0010* 0.0012 0.0001 -0.0003 0.0011

(0.101) (0.051) (0.261) (0.929) (0.630) (0.253)

∆Growth 0.0036 -0.0038 0.0018 0.0014 -0.0023 -0.0027

(0.447) (0.122) (0.551) (0.704) (0.326) (0.249)

∆Lev -0.0777 -0.0463*** -0.0465* -0.0401 -0.0277* -0.0191

(0.108) (0.009) (0.051) (0.137) (0.084) (0.265)

∆ROA 0.0753 -0.0174 -0.0578 -0.0173 0.0451* 0.0403

(0.408) (0.578) (0.105) (0.734) (0.067) (0.114)

∆Size -0.0152 0.0282*** 0.0215** 0.0102 0.0157** 0.0127*

(0.359) (0.000) (0.015) (0.321) (0.011) (0.078)

Ntradeshares -0.0138 -0.0086*** 0.0058 -0.0005 -0.0009 0.0004

(0.104) (0.003) (0.257) (0.931) (0.764) (0.923)

Year Y Y Y Y Y Y

Industry Y Y Y Y Y Y

N 77 532 216 146 692 408

adj. R2 0.505 0.468 0.530 0.268 0.284 0.247

32

Table 9 Test on Compensation Industry Benchmarking

Please refer to table 1 for variable definition. Benchmark peer firms are firms with size 0.5 to 2

times the size of the company. We run the following model here ∆Compen = β0 + β1 |BMark| + β2 Period05 + β3 Ownership + β4 Topshare + β5 Duality + β6 BIndepen + β7 Bsize + β8 ∆Growth +

β9 ∆Lev + β10∆ROA+β11 ∆Size +β12 Ntradeshares +Σ Year +Σ Industry . P-values are shown in

parenthesis. *** significant at the1% level; ** significant at the 5% level, * significant at the 10%

level.

Full sample Compen > PeerMean Compen < PeerMean

(1) (2) (3)

_cons 0.0000 0.0207** -0.0112

(0.996) (0.018) (0.209)

|BmarkMean| 0.0701*** -0.2664*** 0.1709***

(0.000) (0.000) (0.000)

Period05 -0.0052*** -0.0092*** -0.0020

(0.000) (0.000) (0.264)

Ownership -0.0021 -0.0017 -0.0038**

(0.124) (0.339) (0.035)

Topshare -0.0027 -0.0073 0.0001

(0.501) (0.164) (0.976)

Duality -0.0007 0.0016 0.0004

(0.656) (0.411) (0.850)

BIndepen 0.0188 0.0023 0.0268

(0.141) (0.886) (0.102)

Bsize 0.0002 0.0001 0.0007**

(0.478) (0.672) (0.046)

∆Growth -0.0003 0.0035** -0.0022

(0.770) (0.017) (0.141)

∆Lev 0.0110 0.0039 0.0068

(0.137) (0.702) (0.456)

∆ROA 0.0280** 0.0259* 0.0204

(0.010) (0.076) (0.131)

∆Size -0.0051* 0.0001 -0.0008

(0.065) (0.971) (0.815)

Ntradeshares 0.0023* 0.0009 0.0027

(0.068) (0.602) (0.110)

Year Y Y Y

Industry Y Y Y

N 2105 1042 1063

adj. R2 0.023 0.266 0.114

33

Table 10 Effect of the 2005 Compensation Disclosure on Compensation Benchmarking

Please refer to table 1 for variable definition. Benchmark peer firms are firms with size 0.5 to 2

times the size of the company. We run the following test: ∆Compen = β0 + β1 |BMark| + β2 |BMark|×Period05 + β3 Period05+ β4 Ownership+ β5 Topshare + β6 Director + β7 Indepen + β8 Bsize + β9 ∆Growth+ β10 ∆Lev + β11 ∆ROA + β12 ∆Size +β13 Ntradeshares + Σ Year + Σ Industry .P-values are shown in parenthesis. *** significant at the1% level; ** significant at the 5%

level, * significant at the 10% level.

Full sample Compen > PeerMean Compen < PeerMean

(1) (2) (3)

_cons 0.0003 0.0243*** -0.0103

(0.966) (0.006) (0.247)

|BmarkMean| 0.0641*** -0.3329*** 0.1460***

(0.005) (0.000) (0.000)

|BmarkMean|×Period05 0.0092 0.1028*** 0.0383

(0.746) (0.001) (0.223)

Period05 -0.0057*** -0.0136*** -0.0035

(0.005) (0.000) (0.105)

Ownership -0.0021 -0.0017 -0.0038**

(0.124) (0.350) (0.034)

Topshare -0.0027 -0.0078 0.0002

(0.498) (0.135) (0.967)

Duality -0.0007 0.0016 0.0004

(0.652) (0.420) (0.860)

BIndepen 0.0189 0.0029 0.0273*

(0.139) (0.860) (0.096)

Bsize 0.0002 0.0001 0.0007**

(0.479) (0.814) (0.047)

∆Growth -0.0003 0.0034** -0.0022

(0.769) (0.020) (0.144)

∆Lev 0.0110 0.0043 0.0066

(0.138) (0.666) (0.468)

∆ROA 0.0280** 0.0252* 0.0202

(0.010) (0.082) (0.135)

∆Size -0.0051* 0.0003 -0.0008

(0.065) (0.930) (0.805)

Ntradeshares 0.0023* 0.0009 0.0027

(0.068) (0.588) (0.111)

Year Y Y Y

Industry Y Y Y

N 2105 1042 1063

adj. R2 0.022 0.274 0.114

34

Table 11: Effects of the 2005 Compensation Disclosure on Compensation Benchmarking for

Different Types of Firms

Please refer to table 1 for variable definition. Benchmark peer firms are firms with size 0.5 to 2

times the size of the company. We run the following test: ∆Compen = β0 + β1 |BMark| + β2 |BMark|×Period05 + β3 Period05+ β4 Ownership+ β5 Topshare + β6 Director + β7 Indepen + β8 Bsize + β9 ∆Growth+ β10 ∆Lev + β11 ∆ROA+ β12 ∆Size +β13 Ntradeshares + Σ Year + Σ Industry . P-values are shown in parenthesis. *** significant at the1% level; ** significant at the 5% level, *

significant at the 10% level.

Compen > PeerMean Compen < PeerMean

SOECG SOELG Non-SOEs SOECG SOELG Non-SOEs

(1) (2) (3) (4) (5) (6)

_cons 0.0213 0.0098 0.0234 -0.0132 -0.0016 0.0126

(0.529) (0.256) (0.208) (0.630) (0.863) (0.507)

|BmarkMean| -0.5708*** -0.0597** -0.3699*** 0.5149*** 0.0580** 0.1440**

(0.000) (0.045) (0.000) (0.000) (0.026) (0.012)

|BmarkMean|×Period05 0.1392 0.1155*** 0.1353** -0.2291** 0.0707** 0.1115

(0.156) (0.001) (0.014) (0.030) (0.025) (0.120)

Period05 -0.0332*** 0.0038 -0.0209*** -0.0113 -0.0035 -0.0040

(0.000) (0.136) (0.000) (0.159) (0.115) (0.390)

Topshare 0.0282 -0.0105* -0.0101 -0.0048 0.0030 -0.0070

(0.150) (0.056) (0.328) (0.807) (0.566) (0.522)

Duality -0.0002 0.0028 0.0034 -0.0060 0.0000 0.0057

(0.976) (0.230) (0.328) (0.555) (0.989) (0.201)

BIndepen 0.0751 -0.0076 0.0156 0.0376 0.0107 -0.0145

(0.278) (0.657) (0.620) (0.537) (0.526) (0.676)

Bsize -0.0031*** 0.0003 0.0003 0.0024* 0.0001 -0.0003

(0.007) (0.362) (0.694) (0.067) (0.731) (0.735)

∆Growth 0.0058 0.0021 0.0046* 0.0062 -0.0029* -0.0051**

(0.139) (0.236) (0.062) (0.265) (0.099) (0.044)

∆Lev 0.0384 -0.0106 0.0021 0.0140 -0.0030 0.0231

(0.210) (0.385) (0.893) (0.675) (0.766) (0.183)

∆ROA 0.0289 -0.0101 0.0267 -0.0026 0.0048 0.0422*

(0.558) (0.580) (0.218) (0.961) (0.749) (0.080)

∆Size -0.0113 -0.0017 -0.0072 0.0082 -0.0004 -0.0020

(0.314) (0.712) (0.245) (0.514) (0.920) (0.775)

Ntradeshares -0.0014 0.0013 0.0123*** -0.0058 0.0019 0.0189***

(0.772) (0.456) (0.001) (0.310) (0.258) (0.000)

Year Y Y Y Y Y Y

Industry Y Y Y Y Y Y

N 125 604 313 138 602 323

adj. R2 0.704 0.129 0.367 0.338 0.116 0.187