THE EFECTIVENES OF MACROPRUDENTIAL INSTRUMENTS … MACROPRUDENTIAL... · CIR = Cost to Income Ratio...

13

Call for Paper Page 1 THE EFECTIVENES OF MACROPRUDENTIAL INSTRUMENTS AND BANKING MARKET STRUCTURE ON BANKS’ PERFORMANCE: EMPIRICAL EVIDENCE ON EMERGING COUNTRIES Yuli Teguh Hidayat, Tumpak Silalahi 1 , and Prof. Dr. Rina Indiastuti 2 Abstract: Recently, numerous Central Banks implement various macroprudential policies to complement monetary policy that have been established as a compulsory study at the Faculty of Economics and Business. However, macroprudential instruments are still relatively new. Its intended purpose is to achieve stability in the financial system while monetary policy is intended to achieve the objectives of macroeconomic stability. The structure of the banking industry affecting the effectiveness of macroprudential policy because the financial industry will respond to monetary policy and macroprudential policy would be well responded if the banking market structure can be identified in the early stage. Allegedly the differences that occur between the overly concentrated market structure as in the monopoly market and vice versa in a perfectly competitive market has a different effect when testing the effectiveness of monetary and macroprudential policies. This dissertation study aimed to explore the implications of macroprudential policy particularly the effect of banking market structure on the profitability of banks in Indonesia and how the interaction between macroprudential policy and market structure. Research methodology used is based on an econometric model with the model specification and the main purpose of research is to assess the performance of banks. There are two main models used in this study: firstly, using a longitudinal panel OLS regression analysis with a design that is analysis of longitudinal data modeling that consist of panel fixed effect model and random effect model is further equipped with a Hausman test. The second approach, complementary study was conducted with the model of Vector Auto Regression Model (VAR) to test cointegration, stationary test, Granger Causality Test, Impulse Response and Variance Decomposition. Key word: Macroprudential policy, Banking Structure, Commercial Bank Profitability. 1 Yuli Teguh Hidayat and Tumpak Silalahi, Student at the Faculty of Economics and Business, University of Padjdjaran, Bandung Indonesia, Working at Center for Central Banking Research and Education, Bank Indonesia, corresponding author: [email protected] or [email protected] 2 Co-author, lecture in Economics and Business Faculty, University of Padjdjaran, Bandung Indonesia, corresponding co- author: [email protected].

Transcript of THE EFECTIVENES OF MACROPRUDENTIAL INSTRUMENTS … MACROPRUDENTIAL... · CIR = Cost to Income Ratio...

Call for Paper Page 1

THE EFECTIVENES OF MACROPRUDENTIAL INSTRUMENTS AND BANKING MARKET STRUCTURE ON BANKS’ PERFORMANCE:

EMPIRICAL EVIDENCE ON EMERGING COUNTRIES

Yuli Teguh Hidayat, Tumpak Silalahi1, and Prof. Dr. Rina Indiastuti2

Abstract:

Recently, numerous Central Banks implement various macroprudential policies to complement monetary

policy that have been established as a compulsory study at the Faculty of Economics and Business. However,

macroprudential instruments are still relatively new. Its intended purpose is to achieve stability in the financial system

while monetary policy is intended to achieve the objectives of macroeconomic stability. The structure of the banking

industry affecting the effectiveness of macroprudential policy because the financial industry will respond to monetary

policy and macroprudential policy would be well responded if the banking market structure can be identified in the

early stage. Allegedly the differences that occur between the overly concentrated market structure as in the monopoly

market and vice versa in a perfectly competitive market has a different effect when testing the effectiveness of

monetary and macroprudential policies. This dissertation study aimed to explore the implications of macroprudential

policy particularly the effect of banking market structure on the profitability of banks in Indonesia and how the

interaction between macroprudential policy and market structure.

Research methodology used is based on an econometric model with the model specification and the main

purpose of research is to assess the performance of banks. There are two main models used in this study: firstly, using

a longitudinal panel OLS regression analysis with a design that is analysis of longitudinal data modeling that consist of

panel fixed effect model and random effect model is further equipped with a Hausman test. The second approach,

complementary study was conducted with the model of Vector Auto Regression Model (VAR) to test cointegration,

stationary test, Granger Causality Test, Impulse Response and Variance Decomposition.

Key word: Macroprudential policy, Banking Structure, Commercial Bank

Profitability.

1 Yuli Teguh Hidayat and Tumpak Silalahi, Student at the Faculty of Economics and Business, University of Padjdjaran,

Bandung Indonesia, Working at Center for Central Banking Research and Education, Bank Indonesia, corresponding author: [email protected] or [email protected] 2 Co-author, lecture in Economics and Business Faculty, University of Padjdjaran, Bandung Indonesia, corresponding co- author: [email protected].

Call for Paper Page 2

MACROPRUDENTIAL INSTRUMENTS EFECTIVENES AND BANK MARKET

CONCENTRATION ON BANKS’ PERFORMANCE:

(EMPIRICAL EVIDENCE ON INDONESIAN BANKING FIRM PROFITABILITY)

1. INTRODUCTION

Research on the banking industry became the topic of many resercher in depth at

present, it is inseparable from the phenomenon of the global financial crisis of 2008,

which makes a variety of changes to banking authority expects the model to corporate

banking which is sustainable and beneficial for the economy.

The emergence of bank failures due to the 2008 global crisis in the world banking

industry, that indicated from a number of banks in developed countries (developed

countries) to bail out, making the formulation of resilience in the banking industry is

indispensable. The resilience of the financial system of the pressure his own crisis

(financial resiliance) is influenced by various factors.

One of the factors the durability depends on the structure of the market owned by

a Contracting State on its financial system, are more oriented to financial or domination by

capital markets (Capital market orientation).

Indonesia's financial system is dominated by the banking sector which is reflected

by the bank's market share is more dominant than the capital markets and non-bank

financial institutions, therefore, highly relevant microeconomic deepening bank to do.

Call for Paper Page 3

Emerging countries such as Indonesia have a very much interest on banking sector since

bank interest margins as a measure of financial intermediation costs is particularly

pertinent in the absence of developed capital markets and the small presence of non-bank

financial institutions, households and firms largely depend on bank financing.

The role of macro prudential instruments belief to stabilize the financial system,

however on the individual banking institution those policy can affect the banking

profitability. On the other side, the effectiveness of macroprudential policy depend on the

bank market structure.

According to Arreguy et all (IMF WP -13/167), implementing macro prudential

will effect on the costs arise from an increase in the cost of intermediation and its effect on

long-run output. Even though, the benefit is derived from the resilience of the economy

from the policy measure—a reduction in the probability of a crisis and output losses in the

event of a crisis.

2. MOTIVATION OF THE STUDY

Study about macro prudential instruments become a new policy trend particularly

since the global financial crisis during 2008’s beside monetary policy that already long

exist in the economic theory. However, it is still premature to know precisely how the

interaction between monetary policy and macro prudential policy influence the business

strategy of the banking industry.

Based on explanation above, this research is intended to study the things as

follows:

Call for Paper Page 4

1. To review and analyze the impact on Indonesian macro prudential policies on

performance of commercial banks in Indonesia.

2. To study the impact of market power or market concentration on commercial bank

profitability.

3. To examine the relationship between economic cycle with commercial banks

performance.

4. To review and analyze interaction between market power or market concentration

and macro prudential policy in conjunction with the profitability of commercial banks

in Indonesia.

To achieve those objectives, research methodologies developed in this paper based on the

econometric model as a primarily tool using quarterly commercial bank data since 2007

until recently as a compliment to descriptive and statistical analysis.

3. THEORETICAL BACGROUND

Study of literature and research on micro-economic banking mostly refers to the

contribution Brucker and Klein (1971) and Bernard Shull (1963). At the level of

microeconomics, a production function of goods is relatively easy to explain but in the

production function model in the banking services industry is not as simple as the

production of goods. That's because the production on a bank deposit collection services

and disbursements of public funds which of course is more complicated to measure.

Several literature studies try to explain the level of productivity in the banking balance

sheet by way of diagnosis (balance sheet) a simple bank among others: Xavier et al (2008),

Mankiw, NG (1986) and Mishkin (2010), as follows:

Call for Paper Page 5

Assets Liabilities + Capital

Reserves Deposits

Loan Equity

On the assets side of the balance sheet there is a Reserve bank (R) is the difference between the

volume of deposits received by banks as well as the volume of loans disbursed by the notation

(D_it-L_ (it)). Reserve bank owned which symbol can be classified into two types, namely

Statutory Reserves (usually not given interest) with the notation SR with i interest rate and t

the period of bank portfolio position in the interbank market M(t) with the following model:

+ .......................................................... (1.1)

From the point of understanding or definition of a bank as a financial institution described

as an example, by Xavier et al (1998, p.1) that defines the operations of the bank as a

financial institution that guarantees loans and accept deposits from the public. While, Rose

and Hudgins (2005) defines a more comprehensive bank: first, the economic functions it

serves, both, the services it offers its customers and third, the legal basis for its existence.

Monetary authorities generally require commercial banks keep a portion of the public

funds in the bank as statutory reserves (reserve requirement) to be deposited in the

central bank in the form of cash or securities in vault. The amount of the reserve

requirement set each monetary authority and RR policies affect the ability of banks to lend

that ultimately affect the performance of the bank. Why banks must keep some funds in

Call for Paper Page 6

the banking industry has a RR for different legality of other non-bank industry is given the

mandate / business license to collect public funds (Giro, deposits and savings).

Because the banking industry is not controlled by a particular company, then the Monti-

Klein models easily explain models of imperfect competition (Cournot) among a number

of banks N is more a portrait of reality. To simplify the analysis, it is assumed there are N

number of banks that have a similar cost function, and linear:

( ) 1.2

The link between market structure, conduct and performance is described by the

company two paradigms is still a debate among academics. The first paradigm is

Hyphotesis Structure Conduct Performance (SCP) and the second, Hyphotesis Relative

Market Power (RMP). Traditional SCP Hyphotesis found the level of bank profitability is

affected by the level of market domination which concentrated market structure

(monopoly and oligopoly) with a market share effect on performance. While the RMP

Hyphotesis found diversified banking products became the market power which in turn

have an impact on improving the profitability of banks. Lubis (2012), examined the

behavior of Indonesian banks in influencing the price that shows how much market power

that empowered as an indicator of the level of competition in the market. The findings of

the study was the level of competition in the Indonesian banking credit market is still

quite high but can not be categorized as a perfectly competitive market. Parera (2010)

(market concentration bank in Sri Lanka), concluded in his research on SCP, which is

concentrated on bank structure impact on bank powers to set interest rates on loans and

higher and lower interest rates on deposits.

Call for Paper Page 7

4. RESEARCH METHODOLOGY

There are many factors that affect the performance of the banks. The factor such as

internal and external factors would be investigate for this research. Some research on the

impact of external factor on Net Interest margin (NIM) for Indonesian Financial Sector had

been done in a partial such as the effect of GDP and Inflation. Hoewever, the effect of

macro prudential instruments on NIM still rarely since the data is unpublish by the

Central Bank.

Furthermore, the model developed in this research based on econometric as follows:

Panel 1 Equation:

Panel 2 Equation:

Panel 3 Equation:

Description:

SRR = Riil Reserve Requirement Ratio

DLTV = Loan to Value Dummy

GDP = Growth Domestic Product

Infl = Inflation Rate

MS = Market Share Power

CR = Concentration Share Power

Aset = Bank Asset

CAR = Capital Adequacy Ratio

CIR = Cost to Income Ratio (Efficiency Perbankan

NPL = Rasio of Non Performing Loan

NIM = Net Interest Margin

= + + 𝐡 + + + + +

Call for Paper Page 8

Growth DPK = The Growth of Commercial Bank Funding.

The analysis will be performed refers to two types namely panel data modeling residual

Fixed Effects Model (Fixed Effect Model (FEM) and Random Effects Model Model (REM).

Electoral most appropriate model among the models of Fixed Effects or Random Effects Model is

based on the consideration that the model improper could cause bias. Therefore, using Hausman

test will examine the best model which is FEM or REM.

As a proxy for measuring the performance of the banking industry that bank

profitability that need to be investigated whether macro prudential policy and the level of market

share (market power) of a bank relative to the effect on the profitability of the banking industry.

In academic circles, there is still debate whether the market share (level of competition) lead to

market stability (stability Concentration hyphothesis) or market share actually cause market

instability (Concentration fragility hyphothesis). If the level of mastery of a dominant market

instability (fragility) and decreased levels of efficiency and profitability of the banking structure of

the Indonesian Banking implications settings need to be cautious.

Call for Paper Page 9

No Variables Description Source of Data

Expected

Sign.

1 Riil Reserve

Requrement The change of Reserve Reserve Requirement Ratio. Bank Indonesia(BI) -

2 LTV'S Dummy Event Study, reguation of Loan to Value =1 for the

period. Q-II 2012 since policy implementing and =0

other period. BI -

3 Market Power Level of market share compare to bank industries BI +

4 Concentration

(CR4,CR11) Concentration of 4 firms to industry BI +

5 Bank Asset(Asset) Total Aset of Firm

Bank Scope Bureau Vandijk +/-

6 Bank Capital Capital of bank proxy by Capital Adequacy

Ratio(CAR) BI +

7 Bank Efficiency (Cost to Income Ratio), notation: CIR BI -

8 (Credit Risk) Non-Performing Loan to Total Loan, Notation: NPL BI -

9 Net Interest margin Net Interest margin, Notation: NIM BI +

10 Deposit Growth Growth of bank funding BI +

11 GDP Economic Growth IFS +

12 Inflation Inflation IFS +

5. DATA AND STATISTIC DESCRIPTION

The data in this study will be obtained from a variety of sources of data that is owned

by Bank Indonesia (Indonesian Banking Directory), the privately run Bank Scope Bureau

Vandijk, Blomberg and data from the International Financial Statistics (IFS). By using

longitudinal panel regression as a primarily tool based on quarterly commercial bank data since

Q1 2005 until Q-IV 2012, allows this research to avoid multicolinearity test.

Call for Paper Page 10

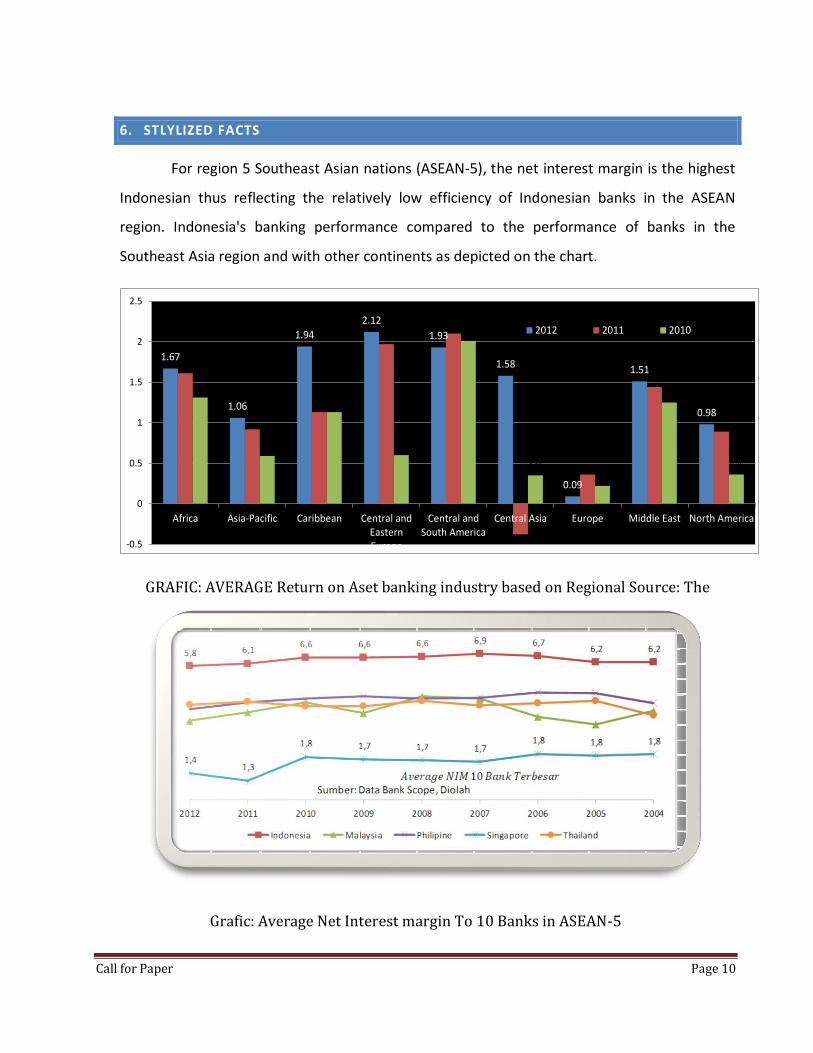

6. STLYLIZED FACTS

For region 5 Southeast Asian nations (ASEAN-5), the net interest margin is the highest

Indonesian thus reflecting the relatively low efficiency of Indonesian banks in the ASEAN

region. Indonesia's banking performance compared to the performance of banks in the

Southeast Asia region and with other continents as depicted on the chart.

GRAFIC: AVERAGE Return on Aset banking industry based on Regional Source: The

Grafic: Average Net Interest margin To 10 Banks in ASEAN-5

1.67

1.06

1.94

2.12

1.93

1.58

0.09

1.51

0.98

1.31

0.59

1.13

0.6

2.01

0.35

0.22

1.25

0.36

-0.5

0

0.5

1

1.5

2

2.5

Africa Asia-Pacific Caribbean Central andEasternEurope

Central andSouth America

Central Asia Europe Middle East North America

2012 2011 2010

Call for Paper Page 11

7. RESULTS AND SUMMARY

The profitability of bank is influence by net interest rate margin, operational expenditure,

policy rate and credit risk. The economic growth have significant effect statitistically on

profitability on lag 3 that mean the commercial bank will respon to the economic cycle within

3 quarter.

In addtion, this paper provides some conclusion and policy recommendation, firstly, as

Bank Indonesia is a legal authority of monetary and banking suversion till now, so Bank

Indonesia needs to understand the determinants of bank performance. Secondly,

investigating the impact of macro prudential should aware with the market share of the each

industry. Failure to understand the relationship the interaction between macro prudential

instruments and market power will pose a risk to financial stability. These conclusion have

policy implications both direcly and indericly on designing macro prudential instruments.

Therefore, coordination and joint research between the monetary and fiscal policy will

benefit to provide a finacial stability.

Based on Panel 1 equation as describing on research methodology, the result of eviews-8

as follows:

Call for Paper Page 12

Call for Paper Page 13

REFERENCE:

1. Arreguy et all (IMF WP -13/167), Implementing Macroprudential, IMF

2. Indranarin Ramlall (2009), Bank Specific, Industry Specific and Macroeconomic Determinants of Profitability in Taiwanese Banking System: Under Panel Data Estimation, International Research Journal of Finance and Economics, Euro Journals Publishing, Inc 2009.

3. Beim dan Calomiries (2001), Emerging Financial market, 2nd edition, McGraw-Hill/Irwin.

4. Christobal M.Pagoso(2010), Money, Credit and Banking, Rex Book Store, Philipines.www.rexpublishing.com.ph

5. Demircuc-Kunt, Asli and Enrica(1998), The Determinats of banking crises in develop and depeloping countries, IMF Working Paper, vol. 45 No.1, Washington DC.

6. Yener Altunbas, Lynne Evans, Philip Molyneux (2001), Bank Ownership and Efficiency, Journal of Money, Credit and Banking, Vol.33. No.4, The Ohio State University.

7. Thierno Amadou Barry, Santos Jose Dacanay III, Laetitia Lepeti, Amine Tarazi(2008), paper presented for the European Commision Asia –Link project B7-3010/2005/105-139.

8. M.Anwar dan Aldrin Herwany (2006), The Determinants of Sucessful Bank Profitability in Indonesia: Empirical study for Provincial Governments Banks and Private Non-Foreign Banks.

9. Sujoko dan Ugy Soebiantoro (2007), Pengaruh struktur kepemilikan saham, leverage, factor Intern dan Faktor Ekstern terhadap nilai perusahaan,(Studi empiric pada perusahaan manufaktur dan non manufaktur di Bursa Efek Jakarta).

10. Peter S. Rose and Sylvia C. Hudgins (2005), Bank Management and Financial

Services, 6th edition, McGraw Hill International Edition.

11. J. Soedradjad Djiwandono (2001), Bergulat denganj krisis dan Pemulihan Ekonomi Indonesia, Pustaka Sinar Harapan Indonesia.

12. Michael P. Todaro and Stephen C. Smith (2009), Economic Development, 10ed, Addison Wesley, Pearson Education.

13. Todaro dan Smith (2009), Economic Development, Harlow, London: Addison Wesley/Pearson Education.

14. Kaminsky dan Reinhart (2000), Bank Lending and Contagion:Evidence From the Crisis,Department of Economics, George Washington University,Washington DC 20052.

15. Grigorian dan Manole (2002), Determinant of Commercial Bank Performance in Transtion Economies: An Application of Data Envelopment Analysisis, The World bank, WP 2850.

16. Sabine Herman and Dubravko Mihaljek (2010), The Determinants of Cross-Border bank flows to emerging markets: new empirical evidence on the spread of financial crises, BIS Working Papaers No.315.

17. Harald Finger and Heiko Hesse(2009), Lebabon-Determinats of Commercial Bank Deposits in Regional Financial Center, IMF Working Paper WP/09/195.