The DRAM Market - Smithsonian Institution

35

1996 F ACTS 1997 FORECAST Market Size: $25,130 million Market Size: $21,485 million Shipments: 2,762 million Shipments: 3,064 million ASP: $9.10 ASP: $7.01 OVERVIEW Dynamic random access memory or DRAM is the main memory component of most computers and many electronic systems. From 1993-1995, industry observers were stunned and amazed as the DRAM market displayed relentless growth. Helping the DRAM market grow at its acceler- ated pace was the lack of sufficient memory production capacity available to meet the needs of the vigorous PC market. In 1996, a different scenario panned out for the DRAM market and its suppliers. In 1Q96, DRAM prices for 4Mbit devices plunged and continued to drop through the balance of the year. Furthermore, 16Mbit DRAM average selling prices (ASPs) also rapidly declined. Softer PC sales and a rather sudden glut of worldwide production capacity turned the DRAM market from one of the most lucrative to one of most difficult in which to participate. For 1997, ICE anticipates another soft year for the DRAM market. Although unit demand will remain strong and bit volume will continue to grow nicely, excess capacity will further erode aver- age selling prices. This will keep the market from growing at the rapid pace it experienced just a few years ago. THE DRAM MARKET The DRAM market has been through many up and down cycles as shown in Figure 2-1, but few suppliers recalled demand being so strong over such a long period of time as during the recent past few years. For the already huge DRAM market to grow by such large percentages over a sev- eral year period was quite remarkable. INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-1 2 THE DRAM MARKET

Transcript of The DRAM Market - Smithsonian Institution

1996 FACTS 1997 FORECAST

Market Size: $25,130 million Market Size: $21,485 million

Shipments: 2,762 million Shipments: 3,064 million

ASP: $9.10 ASP: $7.01

OVERVIEW

Dynamic random access memory or DRAM is the main memory component of most computersand many electronic systems. From 1993-1995, industry observers were stunned and amazed asthe DRAM market displayed relentless growth. Helping the DRAM market grow at its acceler-ated pace was the lack of sufficient memory production capacity available to meet the needs of thevigorous PC market.

In 1996, a different scenario panned out for the DRAM market and its suppliers. In 1Q96, DRAMprices for 4Mbit devices plunged and continued to drop through the balance of the year.Furthermore, 16Mbit DRAM average selling prices (ASPs) also rapidly declined. Softer PC salesand a rather sudden glut of worldwide production capacity turned the DRAM market from oneof the most lucrative to one of most difficult in which to participate.

For 1997, ICE anticipates another soft year for the DRAM market. Although unit demand willremain strong and bit volume will continue to grow nicely, excess capacity will further erode aver-age selling prices. This will keep the market from growing at the rapid pace it experienced just afew years ago.

THE DRAM MARKET

The DRAM market has been through many up and down cycles as shown in Figure 2-1, but fewsuppliers recalled demand being so strong over such a long period of time as during the recentpast few years. For the already huge DRAM market to grow by such large percentages over a sev-eral year period was quite remarkable.

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-1

2 THE DRAM MARKET

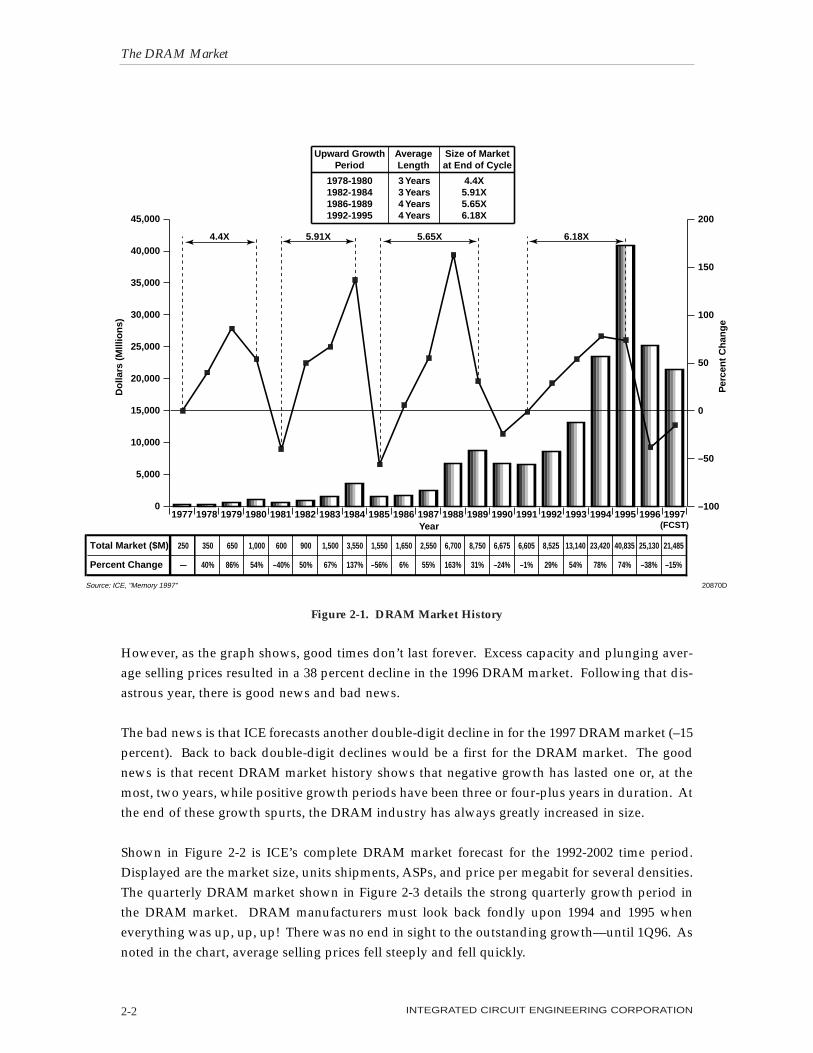

However, as the graph shows, good times don’t last forever. Excess capacity and plunging aver-age selling prices resulted in a 38 percent decline in the 1996 DRAM market. Following that dis-astrous year, there is good news and bad news.

The bad news is that ICE forecasts another double-digit decline in for the 1997 DRAM market (–15percent). Back to back double-digit declines would be a first for the DRAM market. The goodnews is that recent DRAM market history shows that negative growth has lasted one or, at themost, two years, while positive growth periods have been three or four-plus years in duration. Atthe end of these growth spurts, the DRAM industry has always greatly increased in size.

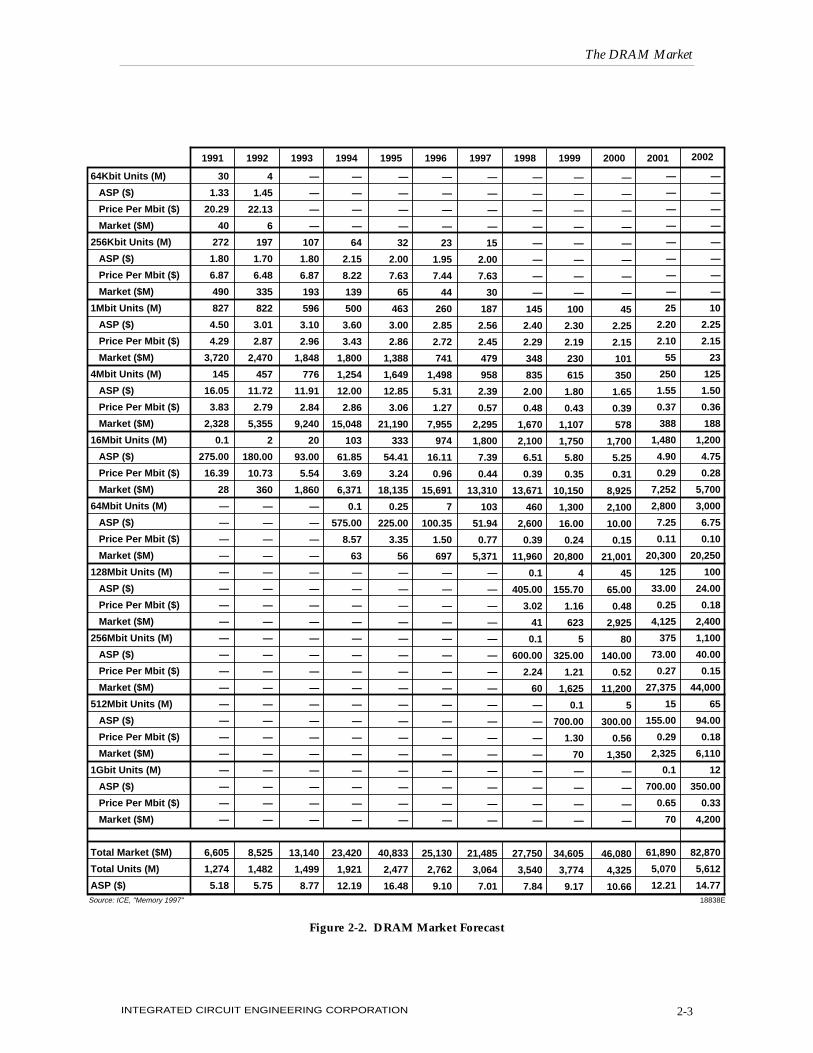

Shown in Figure 2-2 is ICE’s complete DRAM market forecast for the 1992-2002 time period.Displayed are the market size, units shipments, ASPs, and price per megabit for several densities.The quarterly DRAM market shown in Figure 2-3 details the strong quarterly growth period inthe DRAM market. DRAM manufacturers must look back fondly upon 1994 and 1995 wheneverything was up, up, up! There was no end in sight to the outstanding growth—until 1Q96. Asnoted in the chart, average selling prices fell steeply and fell quickly.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-2

Do

llars

(M

Illio

ns)

Per

cen

t C

han

ge

Year

20870DSource: ICE, "Memory 1997"

Total Market ($M)

Percent Change

350

40%

250

—

650

86%

1,000

54%

600

–40%

900

50%

1,500

67%

3,550

137%

1,550

–56%

1,650

6%

2,550

55%

6,700

163%

8,750

31%

6,675

–24%

6,605

–1%

8,525

29%

13,140

54%

23,420

78%

40,835

74%

25,130

–38%

21,485

–15%

Upward GrowthPeriod

AverageLength

Size of Marketat End of Cycle

1978-19801982-19841986-19891992-1995

3 Years3 Years4 Years4 Years

4.4X5.91X5.65X6.18X

4.4X 5.91X 5.65X 6.18X

(FCST)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

199719961995199419931992199119901989198819871986198519841983198219811980197919781977–100

–50

0

50

100

150

200

Figure 2-1. DRAM Market History

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-3

64Kbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

256Kbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

1Mbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

4Mbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

16Mbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

64Mbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

128Mbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

256Mbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

512Mbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

1Gbit Units (M)

ASP ($)

Price Per Mbit ($)

Market ($M)

Total Market ($M)

Total Units (M)

ASP ($)

30

1.33

20.29

40

272

1.80

6.87

490

827

4.50

4.29

3,720

145

16.05

3.83

2,328

0.1

275.00

16.39

28

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

6,605

1,274

5.18

4

1.45

22.13

6

197

1.70

6.48

335

822

3.01

2.87

2,470

457

11.72

2.79

5,355

2

180.00

10.73

360

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

8,525

1,482

5.75

—

—

—

—

107

1.80

6.87

193

596

3.10

2.96

1,848

776

11.91

2.84

9,240

20

93.00

5.54

1,860

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

13,140

1,499

8.77

—

—

—

—

64

2.15

8.22

139

500

3.60

3.43

1,800

1,254

12.00

2.86

15,048

103

61.85

3.69

6,371

0.1

575.00

8.57

63

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

23,420

1,921

12.19

—

—

—

—

32

2.00

7.63

65

463

3.00

2.86

1,388

1,649

12.85

3.06

21,190

333

54.41

3.24

18,135

0.25

225.00

3.35

56

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

40,833

2,477

16.48

—

—

—

—

23

1.95

7.44

44

260

2.85

2.72

741

1,498

5.31

1.27

7,955

974

16.11

0.96

15,691

7

100.35

1.50

697

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

25,130

2,762

9.10

—

—

—

—

15

2.00

7.63

30

187

2.56

2.45

479

958

2.39

0.57

2,295

1,800

7.39

0.44

13,310

103

51.94

0.77

5,371

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

21,485

3,064

7.01

—

—

—

—

—

—

—

—

145

2.40

2.29

348

835

2.00

0.48

1,670

2,100

6.51

0.39

13,671

460

2,600

0.39

11,960

0.1

405.00

3.02

41

0.1

600.00

2.24

60

—

—

—

—

—

—

—

—

27,750

3,540

7.84

—

—

—

—

—

—

—

—

100

2.30

2.19

230

615

1.80

0.43

1,107

1,750

5.80

0.35

10,150

1,300

16.00

0.24

20,800

4

155.70

1.16

623

5

325.00

1.21

1,625

0.1

700.00

1.30

70

—

—

—

—

34,605

3,774

9.17

—

—

—

—

—

—

—

—

45

2.25

2.15

101

350

1.65

0.39

578

1,700

5.25

0.31

8,925

2,100

10.00

0.15

21,001

45

65.00

0.48

2,925

80

140.00

0.52

11,200

5

300.00

0.56

1,350

—

—

—

—

46,080

4,325

10.66

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

—

—

—

—

—

—

—

—

25

2.20

2.10

55

250

1.55

0.37

388

1,480

4.90

0.29

7,252

2,800

7.25

0.11

20,300

125

33.00

0.25

4,125

375

73.00

0.27

27,375

15

155.00

0.29

2,325

0.1

700.00

0.65

70

61,890

5,070

12.21

2002

—

—

—

—

—

—

—

—

10

2.25

2.15

23

125

1.50

0.36

188

1,200

4.75

0.28

5,700

3,000

6.75

0.10

20,250

100

24.00

0.18

2,400

1,100

40.00

0.15

44,000

65

94.00

0.18

6,110

12

350.00

0.33

4,200

82,870

5,612

14.7718838E Source: ICE, "Memory 1997"

Figure 2-2. DRAM Market Forecast

It appears the overall DRAM market stabilized in the latter half of 1996 and into 1Q97. While themarket did stabilize, ICE forecasts further erosion of the market in 1997, but at a much moregradual pace.

The total DRAM market for the period 1992-2002 is shown in Figure 2-4. Following four years ofoutstanding growth, the long-anticipated “recovery” in the market hit in 1996. ICE forecasts thatit will take the DRAM market a few more years (to the year 2000) to be at least the size it was in1995. From 1997 to the year 2002, ICE forecasts the DRAM market to have a cumulative averageannual growth rate of 31 percent.

Excess capacity will remain a fact of life for the DRAM suppliers in 1997. The potential for pricewars will continue as companies seek to grow or maintain their share of the market. As the decadecloses, however, ICE believes DRAM supply and demand will be better balanced. Early into the2000’s, ICE forecasts that demand will once again outstrip supply, causing the market to grow atan accelerated pace.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-4

DollarsUnitsASP

Mill

ion

s o

f U

nit

s, D

olla

rs

AS

P (

$)

20881ASource: ICE, "Memory 1997"

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1Q974Q963Q962Q961Q964Q953Q952Q951Q954Q943Q942Q941Q940.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

4,432

417

10.63

5,365

460

11.66

6,277

502

12.50

7,346

542

13.55

8,015

578

13.87

9,545

602

15.86

10,805

626

17.26

12,468

671

18.58

9,969

629

15.85

5,946

630

9.44

4,570

743

6.15

4,645

760

6.11

4,582

789

5.81

Market ($M)

Units (M)

ASP ($)

Quarter/Year

Figure 2-3. Quarterly DRAM Market

Displayed in Figure 2-5 is the DRAM market by density. In terms of dollar volume, the 16Mbitdensity was the largest in 1996 and is forecast to remain the biggest market in 1997 and 1998.However, ICE believes that market demand for the 64Mbit generation will develop in 1997 andgrow rapidly to challenge the 16Mbit market beginning in 1998. Meanwhile, the 4Mbit density isforecast to quietly slip closer to the obsolete phase in the product lifecycle—a distant “memory”of a grand time in the DRAM market.

DRAM UNIT SHIPMENTS

Shown in Figure 2-6 are quarterly DRAM shipments beginning in 1994 and continuing through1Q97. During the 13-quarter span, total DRAM shipments increased 89 percent. 4Mbit devices,which accounted for 61 percent of total shipments in 1Q94, represented 36 percent of shipmentsin 1Q97. Meanwhile, shipments of DRAMs with densities greater than 4Mbit grew rapidly inthe last three quarters shown. In 1Q97, these devices accounted for 57 percent of total DRAMunit shipments.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-5

Do

llars

(M

illio

ns)

Per

cen

t C

han

ge

Year

18857ESource: ICE, "Memory 1997"

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

20022001200019991998199719961995199419931992

–40

–20

0

20

40

60

80

Total Market ($M)

Percent Change

8,525

29

13,140

54

23,420

74

40,833

74

25,130

–38

21,485

–15

27,750

29

34,605

25

46,080

33

61,890

34

82,870

34

Total Market

Percent Change

Figure 2-4. DRAM Market Growth

Total DRAM unit shipments for the 1992-2002 time period are displayed in Figure 2-7. With theexception of 1993 when units increased a mere one percent, shipments of DRAMs grew wellthrough the first part of the 1990’s. From 1997-2002 units shipments are forecast to average annualgrowth of 13 percent.

DRAM shipments by density are graphed in Figure 2-8. Despite its dwindling market size, 4Mbitunits continued to be a popular selection among system designers in 1996—and for good reason.Although they started 1996 priced around $11.50, 4Mbit DRAMs ended the year priced at $2.55!

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-6

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������20022001200019991998199719961995199419931992

Year

Do

llars

(M

illio

ns)

20880BSource: ICE, "Memory 1997"

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

Total Market ($M)

—

—

23

188

5,700

20,250

2,400

44,000

6,110

4,200

82,870

6

335

2,470

5,355

360

—

—

—

—

—

8,525

—

193

1,848

9,240

1,860

—

—

—

—

—

13,140

—

139

1,800

15,048

6,371

63

—

—

—

—

23,420

—

65

1,388

21,190

18,135

56

—

—

—

—

40,834

—

44

741

7,955

15,691

697

—

—

—

—

25,128

—

30

479

2,295

13,310

5,371

—

—

—

—

21,485

—

—

348

1,670

13,671

11,960

41

60

—

—

27,750

—

—

230

1,107

10,150

20,800

623

1,625

70

—

34,605

—

—

101

578

8,925

21,001

2,925

11,200

1,350

—

46,080

—

—

55

388

7,252

20,300

4,125

27,375

2,325

70

61,890

������

������

���

���

���

����

������

Figure 2-5. Dollar Volume of Select DRAM Densities

With low pricing, designers employed these devices in great numbers in their systems.Consumers, who long awaited to upgrade the memory in their PCs also took advantage of thetremendously lower prices for 4Mbit DRAMs. As a result, unit shipments at this density remainedwell over one billion pieces during 1996.

A big jump in 16Mbit shipments is forecast for 1997. Nearly all the major Japanese and Koreanvendors ramped their output of this density to supply the world’s needs.

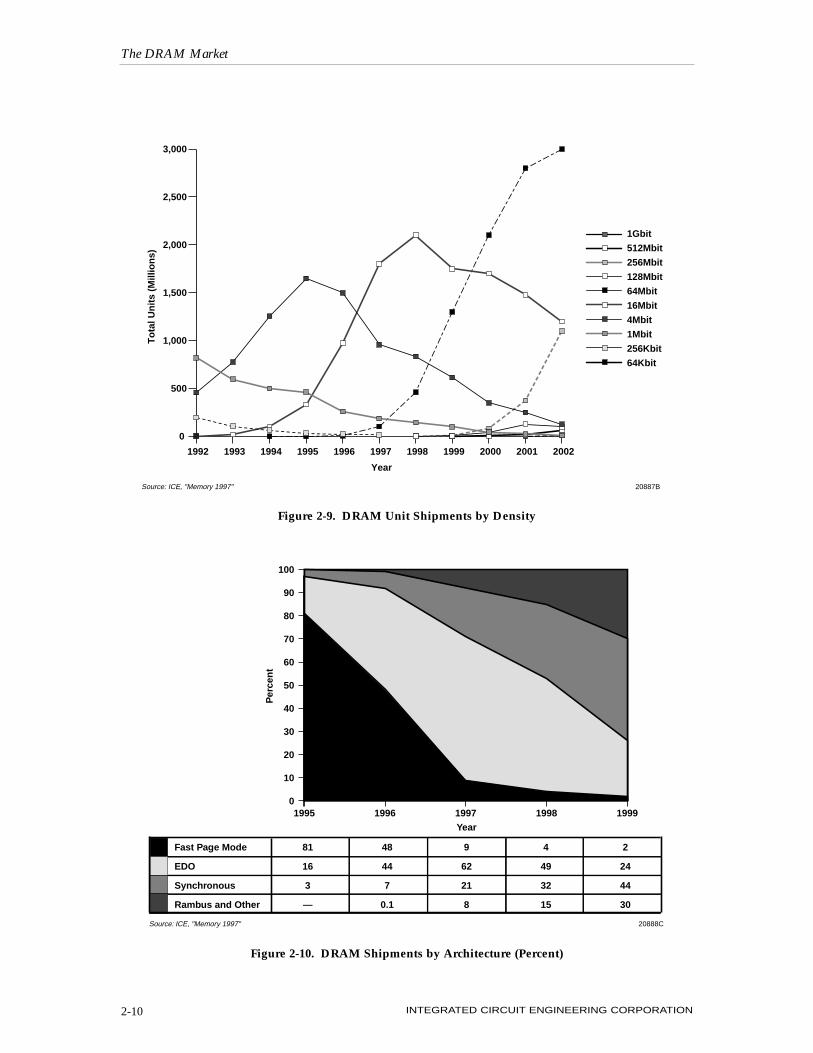

Figure 2-9 provides a look at the typical lifecycle curve for DRAM unit shipments. The 1Mbit den-sity took a long, slow decline on its way out of the market spotlight after peaking in 1991. 4Mbitshipments peaked in 1995, more than doubling the highest yearly 1Mbit output. Perhaps morethan any other generation to date, 4Mbit DRAMs enjoyed more time in the “spotlight,” which isthe mature/saturation phase of the product lifecyle.

16Mbit devices ramped up in 1996 and will be followed by the 64Mbit generation in 1997/1998.ICE forecasts that shipments of 16Mbit DRAMs will peak in 1998 and that 64Mbit devices will topout early in the next century. Whether by a few hundred million or several hundred million units,each successive DRAM generation ships more than its predecessor.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-7

0

100

200

300

400

500

600

700

800

���������������������������������������1Q974Q963Q962Q961Q964Q953Q952Q951Q954Q943Q942Q941Q94

Quarter/Year

20

135

253

9

417

17

128

292

23

460

14

122

335

31

502

12

115

375

40

542

11

124

393

50

578

8

122

407

65

602

7

114

417

88

626

6

76

388

160

629

6

103

432

130

671

5

68

365

192

630

6

62

406

268

743

5

54

340

361

760

5

52

284

448

789

≤256Kbit

1Mbit

4Mbit

≥4Mbit

Total Units (M)

Un

its

(Mill

ion

s)

20885ASource: ICE, "Memory 1997"

���������

Figure 2-6. Quarterly DRAM Shipments by Density

Unit Shipments by Architecture

Until recently, all DRAMs were made using the same fast-page mode (FPM) architecture.However, FPM devices can no longer keep pace with faster microprocessors, and, consequently,hamper overall system performance.

As a result of FPM DRAM’s inability to keep pace with high-speed microprocessors, and sincealmost three-fourths of all DRAMs wind up in PC systems with high-speed microprocessors,DRAM architectures have changed. Though there are numerous revolutionary and evolutionaryalternatives (reviewed in Section 7), three main architectures emerged that appear likely to con-tend for the largest share of 1997 and 1998 DRAM shipments. Figure 2-10 shows the three—extended data out (EDO) DRAM, synchronous DRAM (SDRAM), and Rambus DRAM—and howICE believes the market will be divided among these different architectures in the coming years.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-8

Total Units (M)

Percent Change

5,612

11

1,482

16

1,499

1

1,921

28

2,477

29

2,762

11

3,064

11

3,540

16

3,774

7

4,325

15

5,070

17

Year

Un

its

(Mill

ion

s)

Per

cen

t C

han

ge

0

1,000

2,000

3,000

4,000

5,000

6,000

200220012000199919981997199619951994199319920

5

10

15

20

25

30

20006CSource: ICE, "Memory 1997"

Total Units (M)

Percent Change

Figure 2-7. DRAM Unit Shipments

Most leading DRAM manufacturers curtailed production of their fast-page mode DRAMs in 1995and 1996 and now manufacture DRAMs based on EDO and SDRAM technology. EDO is a rea-sonably cheap and easy upgrade from fast page mode DRAMs. They represented a marginalimprovement over fast-page mode devices. While useful, the market for these devices was short-lived. Furthermore, the investment required to make further marginal performance gains in EDOmemory has made it impractical to continue using it in new PC platforms. As a result, the indus-try witnessed the transition from EDO to synchronous DRAM in 1996.

Initially, SDRAMs were tagged with a 10-15 percent price premium compared to a similarly pack-aged and configured EDO DRAM. That price premium will be essentially non-existent by thesecond half of 1997.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-9

0

1,000

2,000

3,000

4,000

5,000

6,000

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������

20022001200019991998199719961995199419931992Year

Un

its

(Mill

ion

s)

20886BSource: ICE, "Memory 1997"

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

Total Market (M)

—

—

10

125

1,200

3,000

100

1,100

65

12

5,612

4

197

822

457

2

—

—

—

—

—

1,482

—

107

596

776

20

—

—

—

—

—

2,981

—

64

500

1,254

103

0.1

—

—

—

—

1,921

—

32

463

1,649

333

0.3

—

—

—

—

2,477

—

23

260

1,498

974

7

—

—

—

—

2,762

—

15

187

958

1,800

103

—

—

—

—

3,063

—

—

145

835

2,100

460

0.1

0.1

—

—

3,540

—

—

100

615

1,750

1,300

4

5

0.1

—

3,774

—

—

45

350

1,700

2,100

45

80

5

—

4,325

—

—

25

250

1,480

2,800

125

375

15

0.1

5,070

������

������

���

���

���

����

������

Figure 2-8. Unit Volume of Select DRAM Densities

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-10

0

500

1,000

1,500

2,000

2,500

3,000

20022001200019991998199719961995199419931992

Year

To

tal U

nit

s (M

illio

ns)

20887BSource: ICE, "Memory 1997"

1Gbit

512Mbit

256Mbit

128Mbit

64Mbit

16Mbit

4Mbit

1Mbit

256Kbit

64Kbit

Figure 2-9. DRAM Unit Shipments by Density

Figure 2-10. DRAM Shipments by Architecture (Percent)

Fast Page Mode

EDO

Synchronous

Rambus and Other

81

16

3

—

48

44

7

0.1

9

62

21

8

4

49

32

15

2

24

44

30

0

10

20

30

40

50

60

70

80

90

100

19991998199719961995

Per

cen

t

Year

Source: ICE, "Memory 1997" 20888C

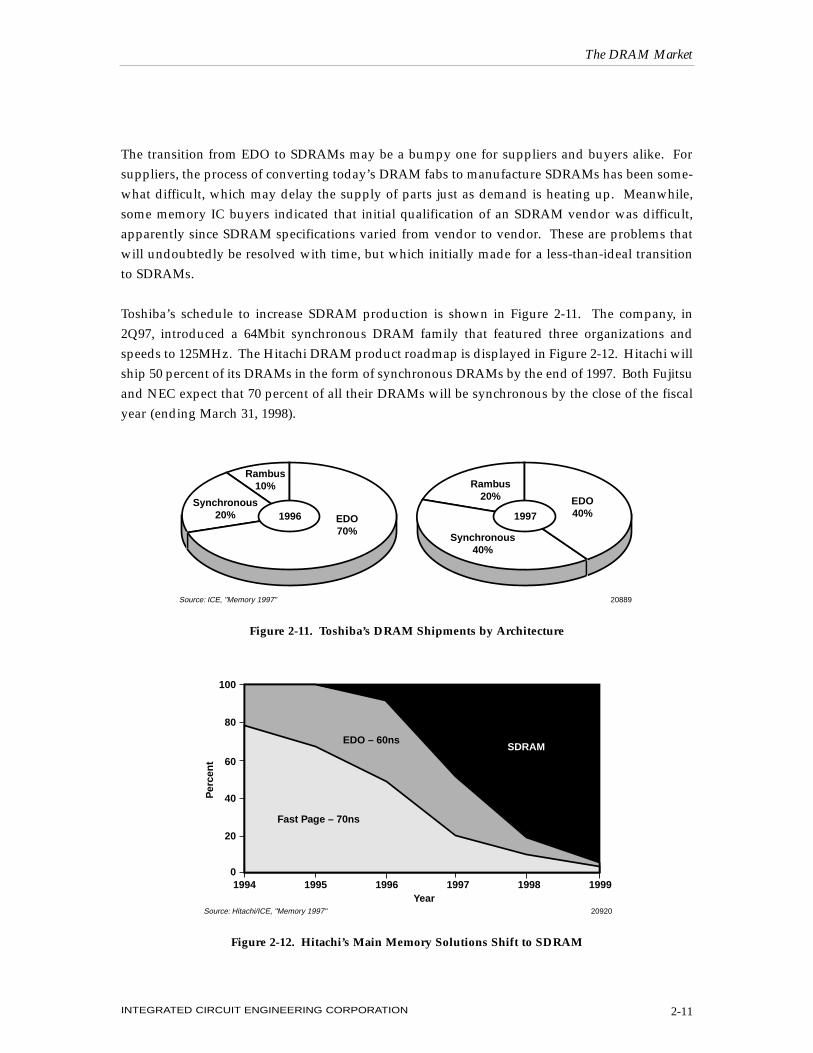

The transition from EDO to SDRAMs may be a bumpy one for suppliers and buyers alike. Forsuppliers, the process of converting today’s DRAM fabs to manufacture SDRAMs has been some-what difficult, which may delay the supply of parts just as demand is heating up. Meanwhile,some memory IC buyers indicated that initial qualification of an SDRAM vendor was difficult,apparently since SDRAM specifications varied from vendor to vendor. These are problems thatwill undoubtedly be resolved with time, but which initially made for a less-than-ideal transitionto SDRAMs.

Toshiba’s schedule to increase SDRAM production is shown in Figure 2-11. The company, in2Q97, introduced a 64Mbit synchronous DRAM family that featured three organizations andspeeds to 125MHz. The Hitachi DRAM product roadmap is displayed in Figure 2-12. Hitachi willship 50 percent of its DRAMs in the form of synchronous DRAMs by the end of 1997. Both Fujitsuand NEC expect that 70 percent of all their DRAMs will be synchronous by the close of the fiscalyear (ending March 31, 1998).

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-11

Rambus10%

Synchronous20% EDO

70%

20889Source: ICE, "Memory 1997"

1996

Rambus20%

Synchronous40%

EDO40%1997

Figure 2-11. Toshiba’s DRAM Shipments by Architecture

Figure 2-12. Hitachi’s Main Memory Solutions Shift to SDRAM

100

80

60

40

20

01994 1995 1996 1997 1998 1999

Year

Per

cen

t

Source: Hitachi/ICE, "Memory 1997" 20920

Fast Page – 70ns

EDO – 60nsSDRAM

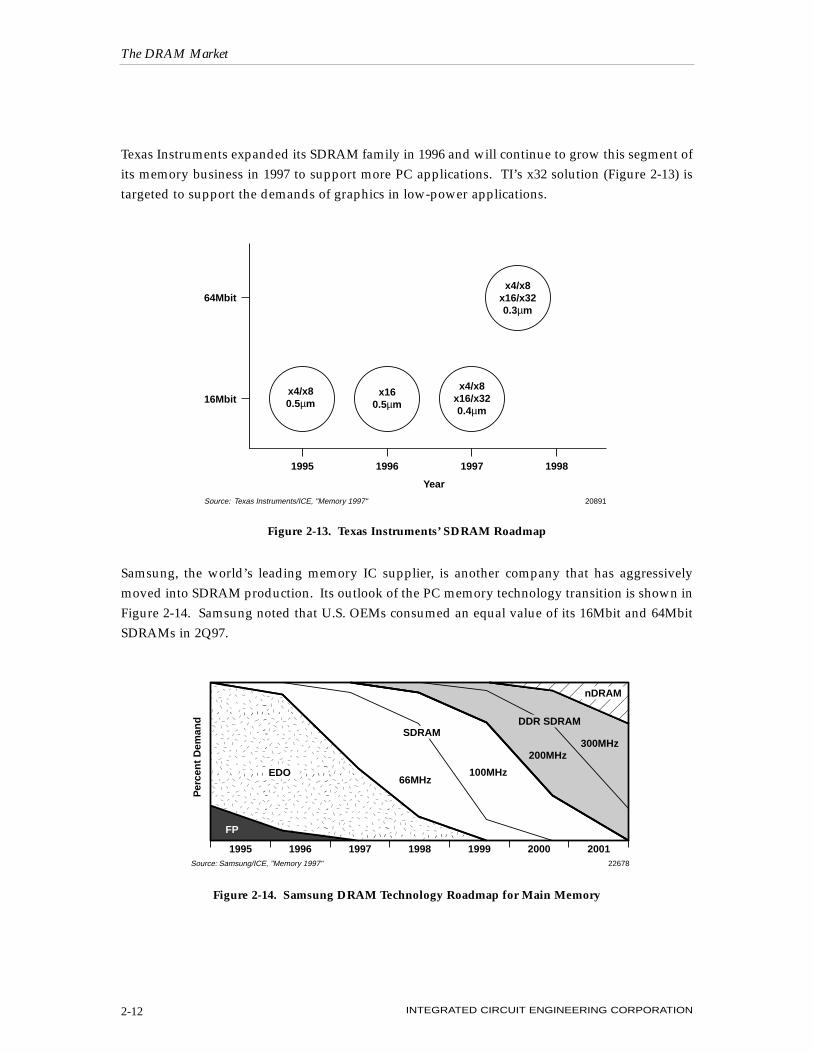

Texas Instruments expanded its SDRAM family in 1996 and will continue to grow this segment ofits memory business in 1997 to support more PC applications. TI’s x32 solution (Figure 2-13) istargeted to support the demands of graphics in low-power applications.

Samsung, the world’s leading memory IC supplier, is another company that has aggressivelymoved into SDRAM production. Its outlook of the PC memory technology transition is shown inFigure 2-14. Samsung noted that U.S. OEMs consumed an equal value of its 16Mbit and 64MbitSDRAMs in 2Q97.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-12

20891Source: Texas Instruments/ICE, "Memory 1997"

64Mbit

16Mbitx4/x80.5µm

x160.5µm

x4/x8x16/x320.4µm

x4/x8x16/x320.3µm

1995 1996

Year

1997 1998

Figure 2-13. Texas Instruments’ SDRAM Roadmap

Figure 2-14. Samsung DRAM Technology Roadmap for Main Memory��������������������

������������������

FP

EDO

SDRAM

66MHz100MHz

DDR SDRAM

200MHz300MHz

nDRAM

1995

Per

cen

t D

eman

d

1996 1997 1998 1999 2000 2001Source: Samsung/ICE, "Memory 1997" 22678

Beyond SDRAMs, Samsung is promoting double data rate (DDR) SDRAM, which doubles thetransfer rate of information compared to a standard SDRAM (which transfers almost twice as muchdata as an EDO DRAM device, Figure 2-15). Samsung believes the DDR SDRAM technology willextend the life of synchronous memory into the 300MHz range, thus directly competing with theRambus DRAM and perhaps delaying the day when vendors have to embrace a new architecture.

In 1996, it became obvious that standard SDRAMs would not be able to perform to the 1.5Gbit to3.0Gbit/second system bandwidth necessary to provide realistic 3D graphics and DVD process-ing. The Rambus DRAM (RDRAM) provides that solution. This technology provides a wide pathfor fast data transfer between the memory and the processing segments of a system.

Rambus licensed the top five DRAM manufacturers (and several others) to use its technology. Thecompany charges a flat “engineering fee” to customize its interface to a memory vendor’s exist-ing product. Vendors then pay royalties based upon the actual selling price of the Rambus DRAM.

Rambus scored a major win when it announced in 1Q97 that Intel would adopt the RambusDRAM architecture as its next-generation main-memory technology for PCs. If all goes accordingto Intel’s plan, Rambus DRAMs will begin to appear in high-end PCs in 1999 (Figure 2-16).

DRAM AVERAGE SELLING PRICES

The DRAM average selling price (ASP) from 1992 through 2002 is shown in Figure 2-17. Limitedproduction capacity and strong demand kept ASPs rising quickly during the first part of thedecade. To the contrary, added worldwide production capacity (i.e., greater supply) led to a crashin the DRAM ASP in 1996. ICE forecasts that an overcapacity condition will continue through1997, which will lead to further erosion of average selling prices. Demand should begin to matchsupply in 1998 and then gradually out-grow supply through the year 2002. Accordingly, DRAMASPs are forecast to climb during this time.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-13

22679Source: Samsung/ICE, "Memory 1997"

Bu

s C

lock

Sp

eed

(M

Hz)

175

150

125

100

75

50

25

0

1989 1991 1993 1995 1997 1999 2001

Fast Page(300Mbits/s)

EDO(500Mbits/s)

SDRAM(>500-800Mbits/s)

DDR SDRAM II(1.0-2.4Gbits/s)

Figure 2-15. Samsung Promotes DDR SDRAM to Match Bus Clock

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-14

�����������������������������������

��������������������

High EndDesktop

VolumeDesktop

Low CostDesktop

1994 20001995 1999199819971996

FP EDO66MHzSDRAM

100MHzSDRAM

DirectRDRAM

Source: Intel/Rambus/ICE, "Memory 1997" 22680

Figure 2-16. Intel’s Outlook for PC Platform Memory

Figure 2-17. DRAM Average Selling Price

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20022001200019991998199719961995199419931992–50

–40

–30

–20

–10

0

10

20

30

40

50

60

Year

20022DSource: ICE, "Memory 1997"

Total ASP ($)

Percent Change

14.77

21

5.75

11

8.77

52

12.19

39

16.48

35

9.10

–45

7.01

–23

7.84

12

9.17

17

10.66

16

12.21

15

AS

P (

$)

Per

cen

t C

han

ge

Total ASP (S)

Percent Change

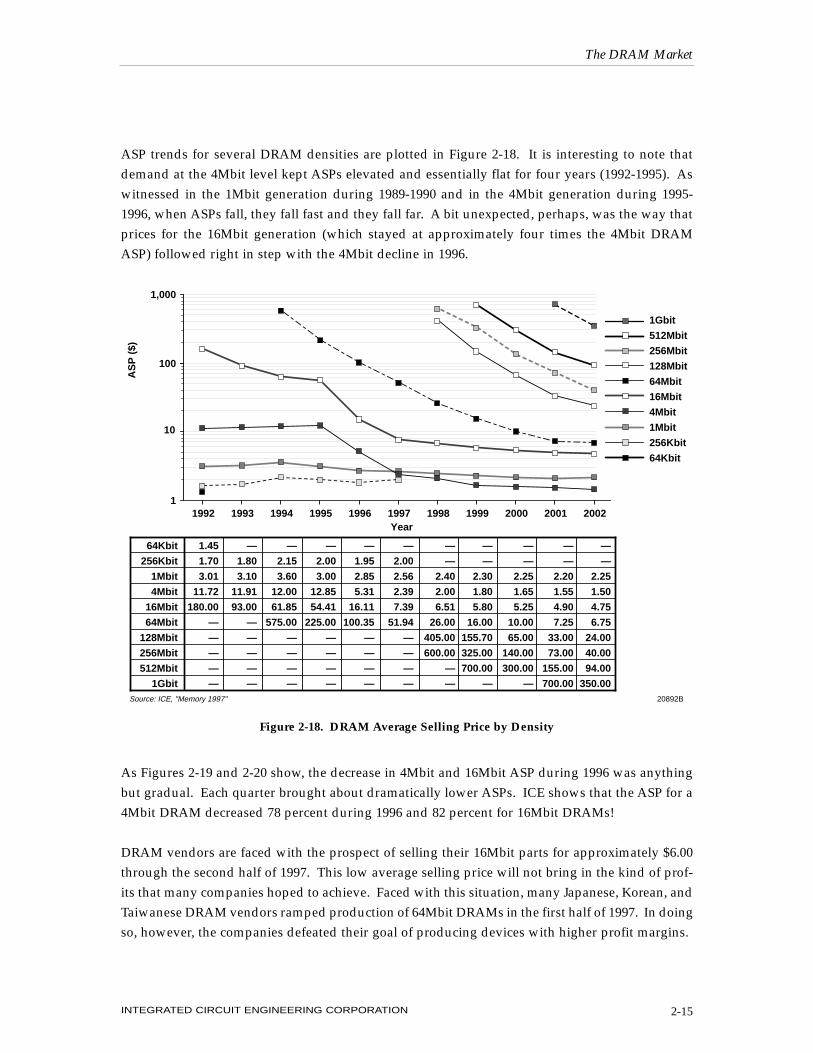

ASP trends for several DRAM densities are plotted in Figure 2-18. It is interesting to note thatdemand at the 4Mbit level kept ASPs elevated and essentially flat for four years (1992-1995). Aswitnessed in the 1Mbit generation during 1989-1990 and in the 4Mbit generation during 1995-1996, when ASPs fall, they fall fast and they fall far. A bit unexpected, perhaps, was the way thatprices for the 16Mbit generation (which stayed at approximately four times the 4Mbit DRAMASP) followed right in step with the 4Mbit decline in 1996.

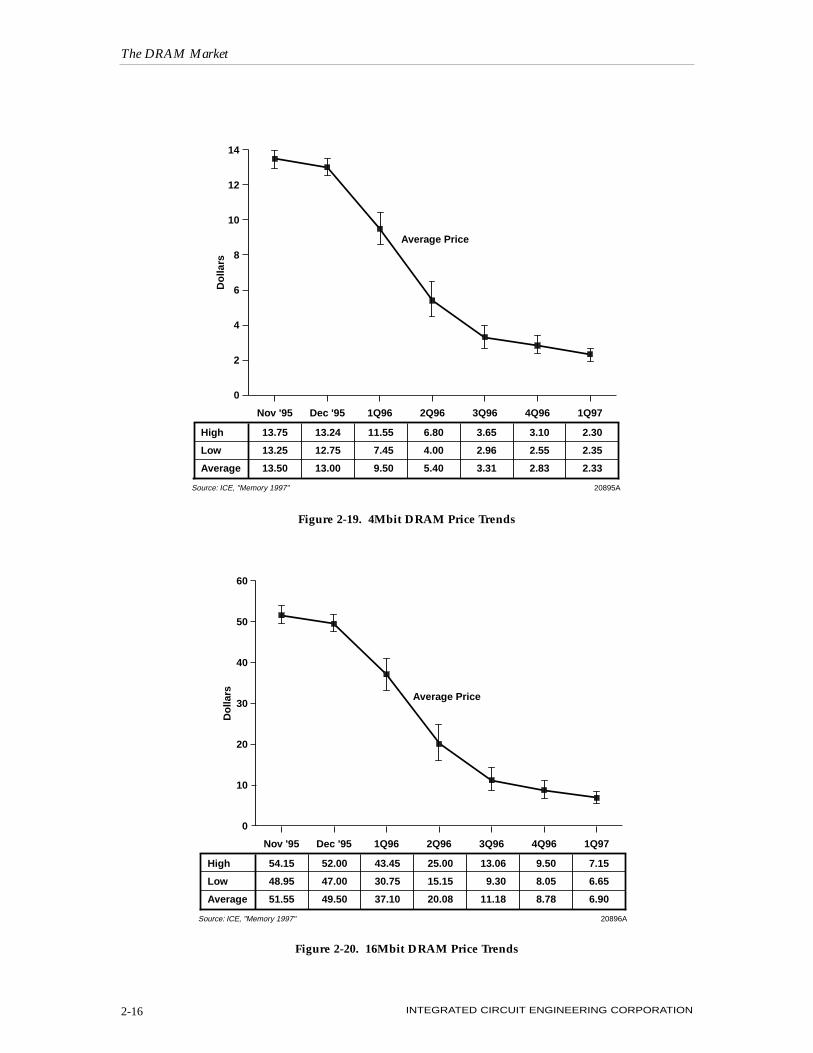

As Figures 2-19 and 2-20 show, the decrease in 4Mbit and 16Mbit ASP during 1996 was anythingbut gradual. Each quarter brought about dramatically lower ASPs. ICE shows that the ASP for a4Mbit DRAM decreased 78 percent during 1996 and 82 percent for 16Mbit DRAMs!

DRAM vendors are faced with the prospect of selling their 16Mbit parts for approximately $6.00through the second half of 1997. This low average selling price will not bring in the kind of prof-its that many companies hoped to achieve. Faced with this situation, many Japanese, Korean, andTaiwanese DRAM vendors ramped production of 64Mbit DRAMs in the first half of 1997. In doingso, however, the companies defeated their goal of producing devices with higher profit margins.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-15

Year

20892BSource: ICE, "Memory 1997"

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

1.45

1.70

3.01

11.72

180.00

—

—

—

—

—

—

1.80

3.10

11.91

93.00

—

—

—

—

—

—

2.15

3.60

12.00

61.85

575.00

—

—

—

—

—

2.00

3.00

12.85

54.41

225.00

—

—

—

—

—

1.95

2.85

5.31

16.11

100.35

—

—

—

—

—

2.00

2.56

2.39

7.39

51.94

—

—

—

—

—

—

2.40

2.00

6.51

26.00

405.00

600.00

—

—

—

—

2.30

1.80

5.80

16.00

155.70

325.00

700.00

—

—

—

2.25

1.65

5.25

10.00

65.00

140.00

300.00

—

—

—

2.20

1.55

4.90

7.25

33.00

73.00

155.00

700.00

—

—

2.25

1.50

4.75

6.75

24.00

40.00

94.00

350.00

20021992 1993 1994 1995 1996 1997 1998 1999 2000 2001

AS

P (

$)

1

10

100

1,000

1Gbit

512Mbit

256Mbit

128Mbit

64Mbit

16Mbit

4Mbit

1Mbit

256Kbit

64Kbit

Figure 2-18. DRAM Average Selling Price by Density

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-16

0

2

4

6

8

10

12

14

13.75

13.25

13.50

13.24

12.75

13.00

11.55

7.45

9.50

6.80

4.00

5.40

3.65

2.96

3.31

3.10

2.55

2.83

2.30

2.35

2.33

Do

llars

Nov '95 Dec '95 1Q96 2Q96 3Q96 4Q96 1Q97

High

Low

Average

20895ASource: ICE, "Memory 1997"

Average Price

Figure 2-19. 4Mbit DRAM Price Trends

0

10

20

30

40

50

60

54.15

48.95

51.55

52.00

47.00

49.50

43.45

30.75

37.10

25.00

15.15

20.08

13.06

9.30

11.18

9.50

8.05

8.78

7.15

6.65

6.90

Do

llars

Nov '95 Dec '95 1Q96 2Q96 3Q96 4Q96 1Q97

High

Low

Average

20896ASource: ICE, "Memory 1997"

Average Price

Figure 2-20. 16Mbit DRAM Price Trends

64Mbit DRAM ASPs followed the same path as 4Mbit and 16Mbit generations before them. At thebeginning of 1996, 64Mbit DRAMs sold for $250. By the end of the year, they sold for $90. In1Q97, the devices were offered for $60, and in 2Q97, the prices had dropped to less than $40. Asof 2Q97, there was more 64Mbit product than the niche application of high-performance work-stations could absorb.

ICE believes the DRAM buyers’ market will continue throughout 1997. Plenty of fab capacity willkeep prices flat or slightly down on all densities of DRAM during the upcoming year.

DRAM BIT VOLUME

DRAM bit volume is provided in Figure 2-21. The DRAM bit volume forecast provides a clear indi-cation that the DRAM market will remain vibrant through the year 2002. There will be demand formore bits. Annual bit volume growth from 1997 through the year 2002 is forecast to average 69 per-cent, with 64Mbit and 256Mbit devices serving as the backbone for that growth (Figure 2-22).

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-17

0

100,000

200,000

300,000

400,000

500,000

600,000

200220012000199919981997199619951994199319920

10

20

30

40

50

60

70

80

90

100

Bit

s x

1012

Per

cen

t C

han

ge

Year

Total Bit Volume

Percent Change

2,864

85

4,243

48

7,536

78

13,019

73

23,370

80

41,363

77

69,797

69

121,219

74

200,896

66

339,411

69

578,476

70

20894CSource: ICE, "Memory 1997"

Bit VolumePercent Change

Figure 2-21. DRAM Bit Volume

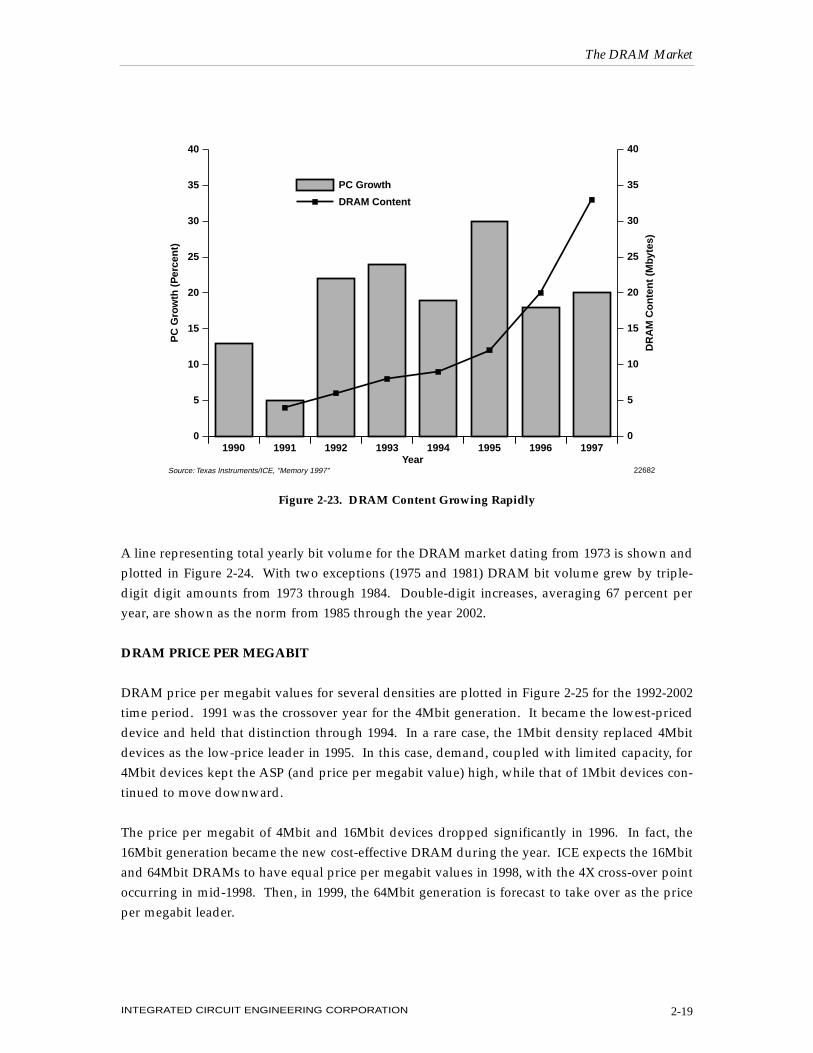

Much of the bit volume growth is due to the continued expansion of the PC industry. As noted inFigure 2-23, PC unit growth has been around 20 percent since about 1992. What is more interest-ing to note is the amount of DRAM used for main memory on the average new system. From amere 4Mbytes in 1991 to 20Mbytes in 1996 to a forecast of 32Mbytes in 1997, the amount of PCmain memory has increased eight-fold in six years. Price declines and new software capabilities(Netscape, Windows NT, etc.) contributed to the higher memory content.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-18

Year

20882BSource: ICE, "Memory 1997"

0.3

52

862

1,917

34

—

—

—

—

—

—

28

625

3,255

336

—

—

—

—

—

—

17

524

5,260

1,728

7

—

—

—

—

—

8

485

6,916

5,592

17

—

—

—

—

—

6

273

6,284

16,341

466

—

—

—

—

—

4

196

4,020

30,204

6,939

—

—

—

—

—

—

152

3,502

35,232

20,870

13

27

—

—

—

—

105

2,579

29,360

87,242

537

1,342

54

—

—

—

47

1,468

28,521

140,929

6,040

21,475

2,416

—

—

—

26

1,049

24,830

187,905

16,777

100,633

8,053

107

—

—

10

524

20,133

201,327

13,422

295,279

34,897

12,885

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Bit

s x

1012

0.10

1.00

100.00

10.00

1,000.00

10,000.00

100,000.00

1,000,000.00

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

1Gbit

512Mbit

256Mbit

128Mbit

64Mbit

16Mbit

4Mbit

1Mbit

256Kbit

64Kbit

Figure 2-22. DRAM Bit Volume by Density

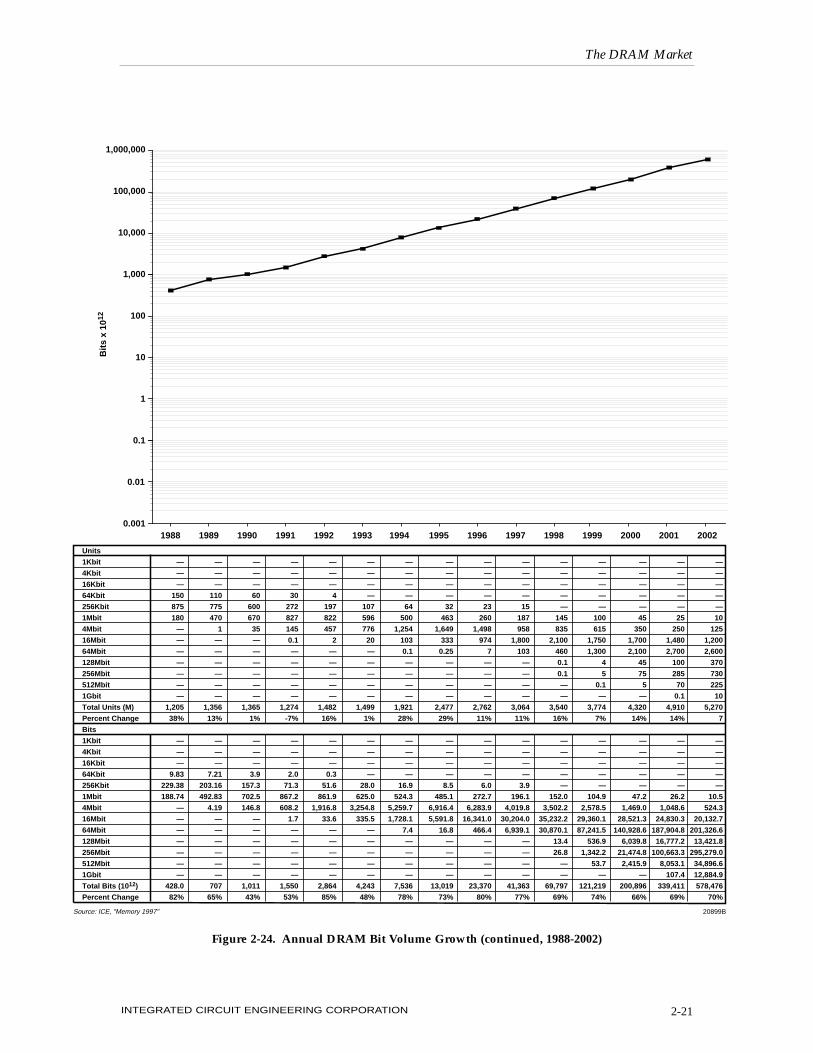

A line representing total yearly bit volume for the DRAM market dating from 1973 is shown andplotted in Figure 2-24. With two exceptions (1975 and 1981) DRAM bit volume grew by triple-digit digit amounts from 1973 through 1984. Double-digit increases, averaging 67 percent peryear, are shown as the norm from 1985 through the year 2002.

DRAM PRICE PER MEGABIT

DRAM price per megabit values for several densities are plotted in Figure 2-25 for the 1992-2002time period. 1991 was the crossover year for the 4Mbit generation. It became the lowest-priceddevice and held that distinction through 1994. In a rare case, the 1Mbit density replaced 4Mbitdevices as the low-price leader in 1995. In this case, demand, coupled with limited capacity, for4Mbit devices kept the ASP (and price per megabit value) high, while that of 1Mbit devices con-tinued to move downward.

The price per megabit of 4Mbit and 16Mbit devices dropped significantly in 1996. In fact, the16Mbit generation became the new cost-effective DRAM during the year. ICE expects the 16Mbitand 64Mbit DRAMs to have equal price per megabit values in 1998, with the 4X cross-over pointoccurring in mid-1998. Then, in 1999, the 64Mbit generation is forecast to take over as the priceper megabit leader.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-19

0

5

10

15

20

25

30

35

40

199719961995199419931992199119900

5

10

15

20

25

30

35

40

Year

PC

Gro

wth

(P

erce

nt)

DR

AM

Co

nte

nt

(Mby

tes)

PC Growth

DRAM Content

Source: Texas Instruments/ICE, "Memory 1997" 22682

Figure 2-23. DRAM Content Growing Rapidly

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-20

20898ASource: ICE, "Memory 1997"

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986

Bit

s x

1012

0.001

0.01

0.1

1

10

100

1,000

10,000

100,000

1,000,000

8

—

—

—

—

—

—

—

—

—

—

—

—

8

—

0.0082

—

—

—

—

—

—

—

—

—

—

—

—

0.0082

—

21

—

—

—

—

—

—

—

—

—

—

—

—

21

163%

0.0215

—

—

—

—

—

—

—

—

—

—

—

—

0.0215

163%

19

3

—

—

—

—

—

—

—

—

—

—

—

22

5%

0.0195

0.0123

—

—

—

—

—

—

—

—

—

—

—

0.0317

48%

13

24

—

—

—

—

—

—

—

—

—

—

—

37

68%

0.0133

0.0983

—

—

—

—

—

—

—

—

—

—

—

0.112

252%

10

50

2

—

—

—

—

—

—

—

—

—

—

62

68%

0.0102

0.2048

0.0328

—

—

—

—

—

—

—

—

—

—

0.248

122%

5

67

17

—

—

—

—

—

—

—

—

—

—

89

44%

0.0051

0.2744

0.2785

—

—

—

—

—

—

—

—

—

—

0.558

125%

1

70

71

—

—

—

—

—

—

—

—

—

—

142

60%

0.0010

0.2867

1.1633

—

—

—

—

—

—

—

—

—

—

1.5

160%

1

31

184

1

—

—

—

—

—

—

—

—

—

217

53%

0.0010

0.1270

3.0147

0.0655

—

—

—

—

—

—

—

—

—

3.2

121%

1

15

230

11

—

—

—

—

—

—

—

—

—

257

18%

0.0010

0.0614

3.7683

0.7209

—

—

—

—

—

—

—

—

—

4.6

42%

—

10

240

100

—

—

—

—

—

—

—

—

—

350

36%

—

0.0410

3.9322

6.5536

—

—

—

—

—

—

—

—

—

10.5

131%

—

5

220

330

2

—

—

—

—

—

—

—

—

557

59%

—

0.0205

3.6045

21.6269

0.5243

—

—

—

—

—

—

—

—

25.8

145%

—

—

120

820

40

—

—

—

—

—

—

—

—

980

76%

—

—

1.966

53.740

10.486

—

—

—

—

—

—

—

—

66.2

157%

—

—

35

500

240

—

—

—

—

—

—

—

—

775

-21%

—

—

0.573

32.768

62.915

—

—

—

—

—

—

—

—

96.3

45%

—

—

10

380

520

4

—

—

—

—

—

—

—

914

18%

—

—

0.164

24.904

136.315

4.194

—

—

—

—

—

—

—

165.6

72%

1987

—

—

—

150

680

45

—

—

—

—

—

—

—

875

-4%

—

—

—

9.83

178.26

47.19

—

—

—

—

—

—

—

235.3

42%

Units

1Kbit

4Kbit

16Kbit

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

Total Units (M)

Percent Change

Bits

1Kbit

4Kbit

16Kbit

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

Total Bits (1012)

Percent Change

Figure 2-24. Annual DRAM Bit Volume Growth (1973-1987)

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-21

20899BSource: ICE, "Memory 1997"

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Bit

s x

1012

0.001

0.01

0.1

1

10

100

1,000

10,000

100,000

1,000,000

Units

1Kbit

4Kbit

16Kbit

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

Total Units (M)

Percent Change

Bits

1Kbit

4Kbit

16Kbit

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

Total Bits (1012)

Percent Change

—

—

—

150

875

180

—

—

—

—

—

—

—

1,205

38%

—

—

—

9.83

229.38

188.74

—

—

—

—

—

—

—

428.0

82%

—

—

—

110

775

470

1

—

—

—

—

—

—

1,356

13%

—

—

—

7.21

203.16

492.83

4.19

—

—

—

—

—

—

707

65%

—

—

—

60

600

670

35

—

—

—

—

—

—

1,365

1%

—

—

—

3.9

157.3

702.5

146.8

—

—

—

—

—

—

1,011

43%

—

—

—

30

272

827

145

0.1

—

—

—

—

—

1,274

-7%

—

—

—

2.0

71.3

867.2

608.2

1.7

—

—

—

—

—

1,550

53%

—

—

—

4

197

822

457

2

—

—

—

—

—

1,482

16%

—

—

—

0.3

51.6

861.9

1,916.8

33.6

—

—

—

—

—

2,864

85%

—

—

—

—

107

596

776

20

—

—

—

—

—

1,499

1%

—

—

—

—

28.0

625.0

3,254.8

335.5

—

—

—

—

—

4,243

48%

—

—

—

—

64

500

1,254

103

0.1

—

—

—

—

1,921

28%

—

—

—

—

16.9

524.3

5,259.7

1,728.1

7.4

—

—

—

—

7,536

78%

—

—

—

—

32

463

1,649

333

0.25

—

—

—

—

2,477

29%

—

—

—

—

8.5

485.1

6,916.4

5,591.8

16.8

—

—

—

—

13,019

73%

—

—

—

—

23

260

1,498

974

7

—

—

—

—

2,762

11%

—

—

—

—

6.0

272.7

6,283.9

16,341.0

466.4

—

—

—

—

23,370

80%

—

—

—

—

15

187

958

1,800

103

—

—

—

—

3,064

11%

—

—

—

—

3.9

196.1

4,019.8

30,204.0

6,939.1

—

—

—

—

41,363

77%

—

—

—

—

—

145

835

2,100

460

0.1

0.1

—

—

3,540

16%

—

—

—

—

—

152.0

3,502.2

35,232.2

30,870.1

13.4

26.8

—

—

69,797

69%

—

—

—

—

—

100

615

1,750

1,300

4

5

0.1

—

3,774

7%

—

—

—

—

—

104.9

2,578.5

29,360.1

87,241.5

536.9

1,342.2

53.7

—

121,219

74%

—

—

—

—

—

45

350

1,700

2,100

45

75

5

—

4,320

14%

—

—

—

—

—

47.2

1,469.0

28,521.3

140,928.6

6,039.8

21,474.8

2,415.9

—

200,896

66%

—

—

—

—

—

25

250

1,480

2,700

100

285

70

0.1

4,910

14%

—

—

—

—

—

26.2

1,048.6

24,830.3

187,904.8

16,777.2

100,663.3

8,053.1

107.4

339,411

69%

2002

—

—

—

—

—

10

125

1,200

2,600

370

730

225

10

5,270

7

—

—

—

—

—

10.5

524.3

20,132.7

201,326.6

13,421.8

295,279.0

34,896.6

12,884.9

578,476

70%

Figure 2-24. Annual DRAM Bit Volume Growth (continued, 1988-2002)

DRAM CONSUMPTION AND PRODUCTION

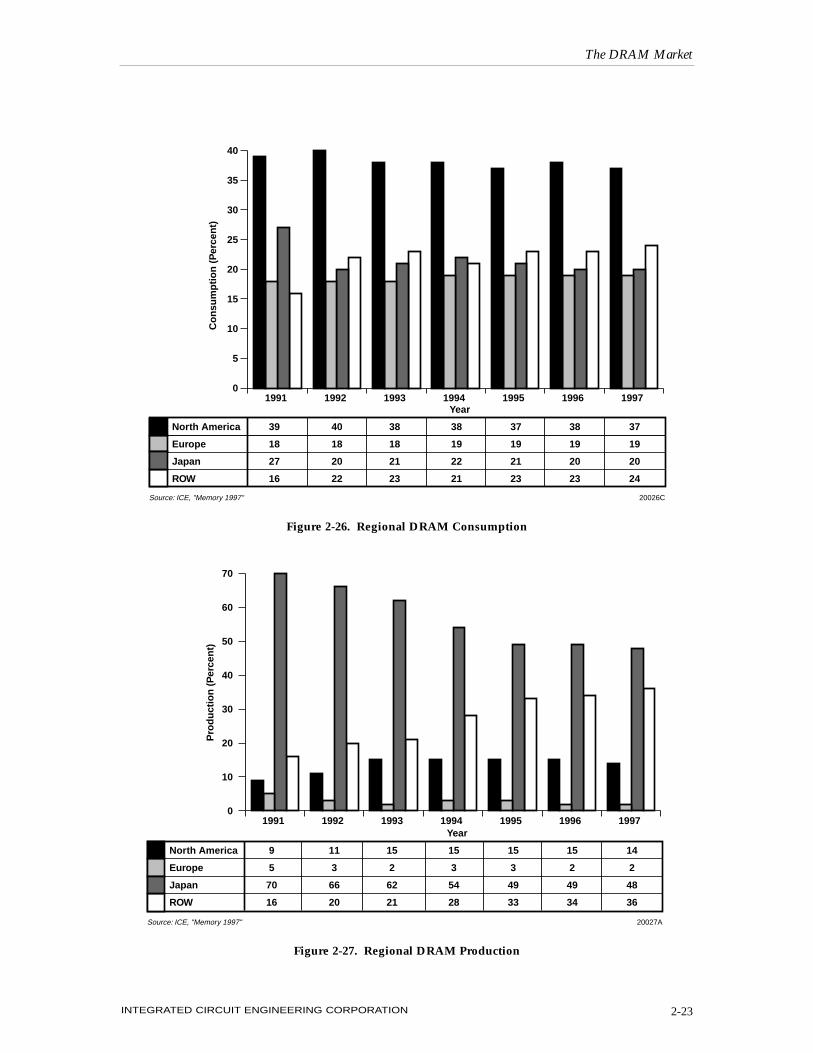

Throughout the 1990’s, the North American region has been the DRAM consumption leader(Figure 2-26). In 1996, it had 38 percent of the DRAM market. Consumption of DRAMs in theROW region (Asia-Pacific countries excluding Japan) first surpassed Japan’s consumption in 1992.Strong consumer electronic consumption in the developing economies of the region along withPC-related work (assembly, packaging, test) will lead to greater consumption in this region.

Although its marketshare dropped considerably since 1991, DRAM production has remainedfirmly in the hands of Japanese companies (Figure 2-27). The biggest threat to Japan’s productionlead comes from the ROW region (specifically, Korea), which continued to build more facilities athome and abroad to harvest additional marketshare.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-22

Year

20883BSource: ICE, "Memory 1997"

22.13

6.48

2.87

2.79

10.73

—

—

—

—

—

—

6.87

2.96

2.84

5.54

—

—

—

—

—

—

8.22

3.43

2.86

3.69

8.57

—

—

—

—

—

7.63

2.86

3.06

3.24

3.35

—

—

—

—

—

7.44

2.72

1.27

0.96

1.50

—

—

—

—

—

7.63

2.45

0.57

0.44

0.77

—

—

—

—

—

—

2.29

0.48

0.39

0.39

3.02

2.24

—

—

—

—

2.19

0.43

0.35

0.24

1.16

1.21

1.30

—

—

—

2.15

0.39

0.31

0.15

0.48

0.52

0.56

—

—

—

2.10

0.37

0.29

0.11

0.25

0.27

0.29

0.65

—

—

2.15

0.36

0.28

0.10

0.18

0.15

0.18

0.33

Pri

ce P

er M

bit

($)

1Gbit

512Mbit

256Mbit

128Mbit

64Mbit

16Mbit

4Mbit

1Mbit

256Kbit

64Kbit

64Kbit

256Kbit

1Mbit

4Mbit

16Mbit

64Mbit

128Mbit

256Mbit

512Mbit

1Gbit

20021992 1993 1994 1995 1996 1997 1998 1999 2000 20010.10

1.00

10.00

100.00

Figure 2-25. DRAM Price Per Mbit by Density

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-23

0

5

10

15

20

25

30

35

40

1997199619951994199319921991Year

Co

nsu

mp

tio

n (

Per

cen

t)

North America

Europe

Japan

ROW

39

18

27

16

40

18

20

22

38

18

21

23

38

19

22

21

37

19

21

23

38

19

20

23

37

19

20

24

20026CSource: ICE, "Memory 1997"

Figure 2-26. Regional DRAM Consumption

0

10

20

30

40

50

60

70

1997199619951994199319921991Year

Pro

du

ctio

n (

Per

cen

t)

North America

Europe

Japan

ROW

9

5

70

16

11

3

66

20

15

2

62

21

15

3

54

28

15

3

49

33

15

2

49

34

14

2

48

36

20027ASource: ICE, "Memory 1997"

Figure 2-27. Regional DRAM Production

Projecting out current trends in regional production through the year 2002, it appears that ROW-based manufacturers could very well be supplying a greater percentage of DRAMs to the world-wide market than their Japanese counterparts (Figure 2-28). World-class manufacturing prowess,generally lower labor costs, supportive governments, and a desire to quickly be a major player inthe microelectronics industry are factors that will contribute to the growth in DRAM productionin the ROW region.

DRAM SALES LEADERS

Shown in Figure 2-29 are the leading DRAM suppliers for 1996. As noted in the chart, no vendorwas spared from the huge decline in the DRAM market. Texas Instruments’ DRAM sales weredown 50 percent in 1996, while Samsung managed to control the bleeding with “only” a 26 per-cent decline in its DRAM sales for 1996. For most, the decline in DRAM revenue nearly matchedthat of the DRAM market itself (-38 percent).

Topping the list of DRAM suppliers was Samsung. Although its DRAM sales were down 26 per-cent in 1996, it easily remained the world’s leading supplier of DRAMs and showed no sign ofrelinquishing that position.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-24

0

10

20

30

40

50

60

70

200220012000199919981997199619951994199319921991

Japan

ROW

Year

Mar

kets

har

e (P

erce

nt)

Japan

ROW

70

16

66

20

62

21

54

28

49

33

49

34

48

36

44

40

42

42

40

44

40

45

46

38

20884ASource: ICE, "Memory 1997"

Figure 2-28. ROW to Overtake Japan in DRAM Production

One reason why the top ten players accounted for the overwhelming majority of the DRAMmarket (93 percent in 1996) was that many marginal players fled the market or switched to pro-ducing other ICs once DRAM profit margins became extremely lean. And why not? Even thoughthe loss was painful, large DRAM suppliers could afford to ship more DRAM units in 1996, yetcome up with about $1-$2 billion less in revenue. For the small or marginal DRAM supplier, aproportionate reduction in revenue would likely have been much more devastating.

4Mbit DRAMs

Although the 4Mbit DRAM market declined 62 percent in 1996, 4Mbit units out-shipped all otherDRAM densities. ICE estimates that 1.5 billion 4Mbit units were shipped in 1996, a decline ofnine percent from 1995.

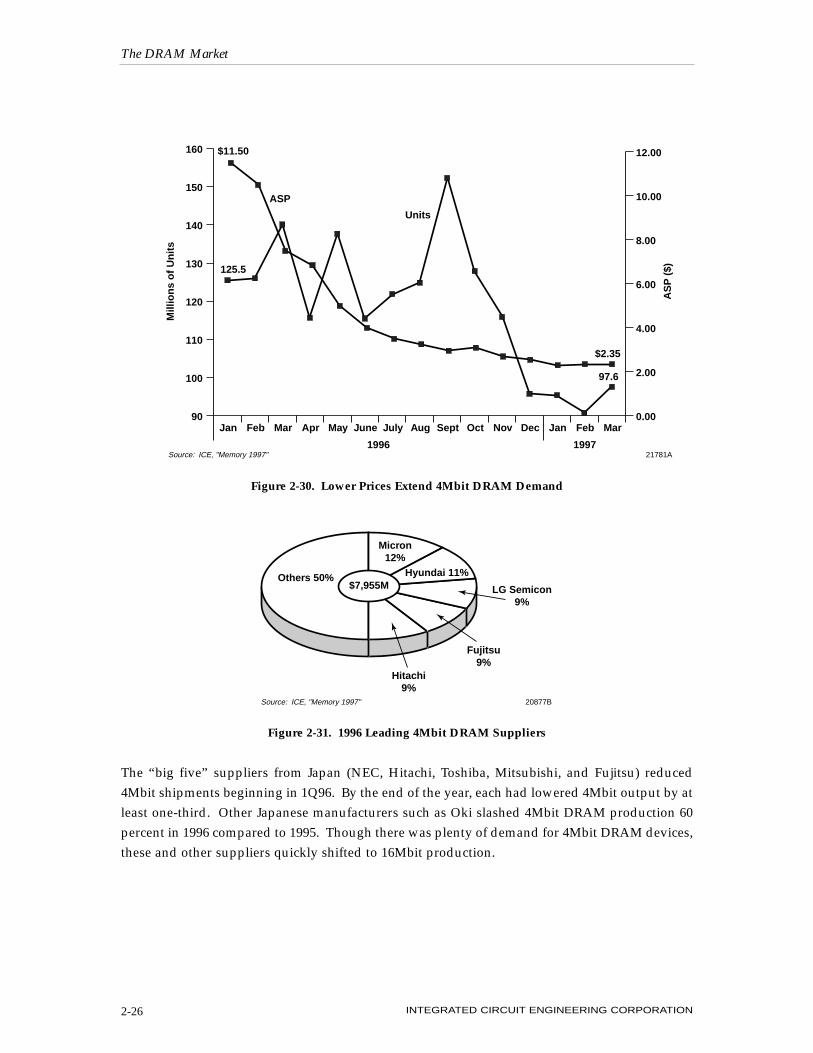

Though the luster faded from the 4Mbit market, PC OEMs and consumers wishing to upgrade theirsystem memory took advantage of the long-overdue low prices and filled their computers withadditional memory, which helped extend the demand for 4Mbit devices well into 1996 (Figure 2-30).

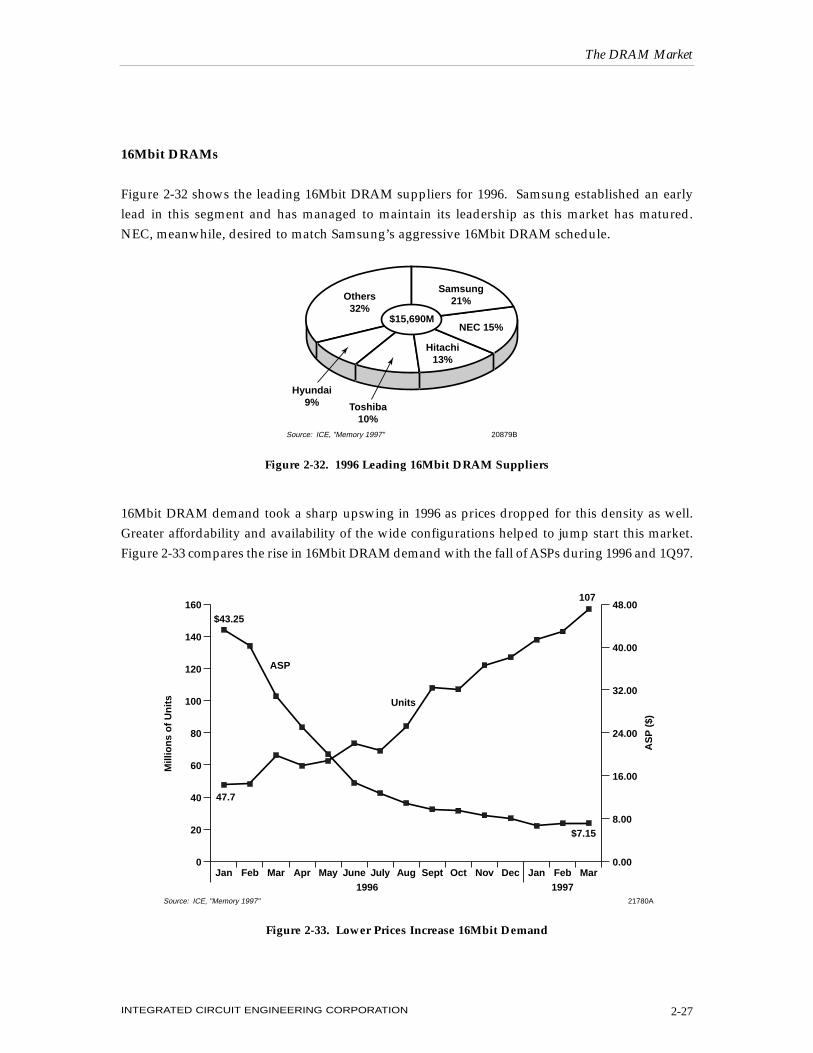

ICE’s estimate of the top 4Mbit DRAM suppliers in 1996 is shown in Figure 2-31. Revenue gen-erate by 4Mbit DRAM suppliers in 1996 dropped sharply. Watching ASPs fall and realizing rev-enue would be several hundred million (even more than one billion) dollars less than the previousyear had to sting many of the 4Mbit DRAM suppliers in 1996.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-25

20875CSource: ICE, "Memory 1997"

Samsung

NEC

Hitachi

Hyundai

Toshiba

LG Semicon

TI

Micron

Mitsubishi

Fujitsu

Others

Total

4,805

3,175

2,805

2,300

2,235

2,005

1,600

1,575

1,400

1,350

1,880

25,130

–26

–33

–37

–34

–40

–33

–50

–37

–37

–35

–62

–38

1995Sales($M)

1996/1995PercentChange

6,462

4,740

4,439

3,500

3,725

3,005

3,200

2,485

2,215

2,065

4,999

40,835

1996Sales($M)

Company

Figure 2-29. 1996 DRAM Sales Leaders

The “big five” suppliers from Japan (NEC, Hitachi, Toshiba, Mitsubishi, and Fujitsu) reduced4Mbit shipments beginning in 1Q96. By the end of the year, each had lowered 4Mbit output by atleast one-third. Other Japanese manufacturers such as Oki slashed 4Mbit DRAM production 60percent in 1996 compared to 1995. Though there was plenty of demand for 4Mbit DRAM devices,these and other suppliers quickly shifted to 16Mbit production.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-26

Source: ICE, "Memory 1997" 21781A

90

100

110

120

130

140

150

160

MarFebJanDecNovOctSeptAugJulyJuneMayAprMarFebJan0.00

2.00

4.00

6.00

8.00

10.00

12.00

1996 1997

AS

P (

$)

Mill

ion

s o

f U

nit

s

Units

ASP

$11.50

125.5

97.6

$2.35

Figure 2-30. Lower Prices Extend 4Mbit DRAM Demand

Figure 2-31. 1996 Leading 4Mbit DRAM Suppliers

$7,955M

Source: ICE, "Memory 1997" 20877B

Others 50%

Micron12%

Hyundai 11%

LG Semicon9%

Fujitsu9%

Hitachi9%

16Mbit DRAMs

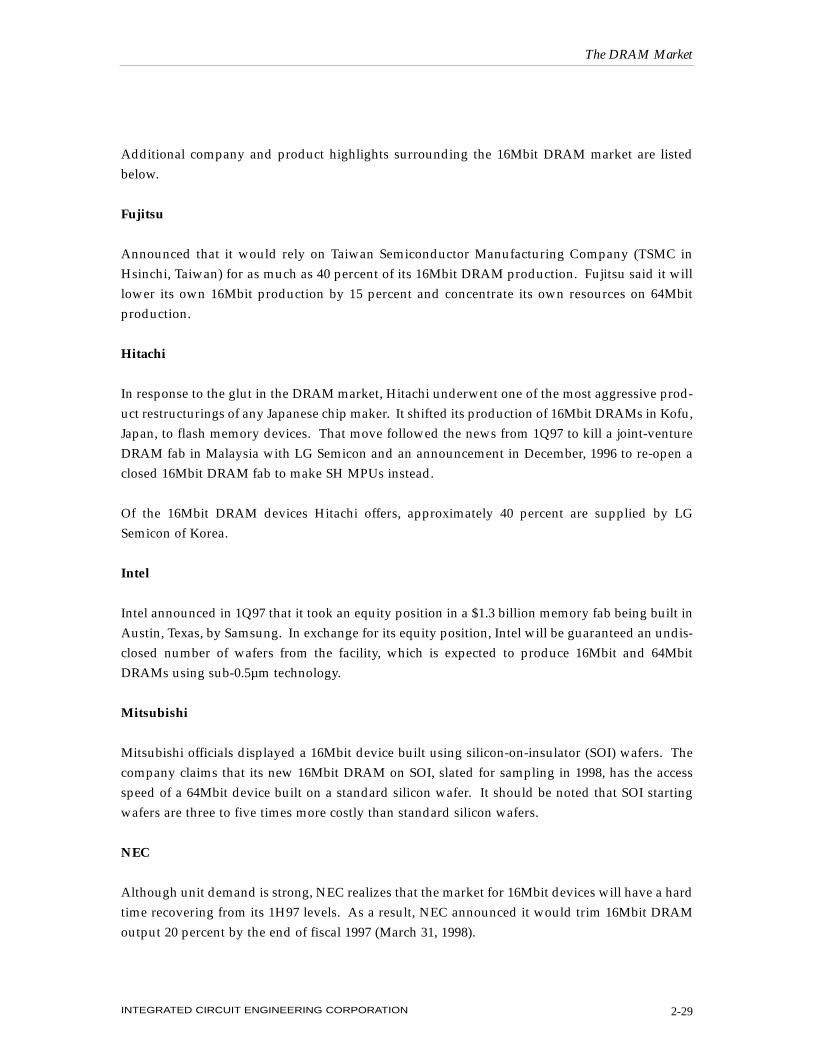

Figure 2-32 shows the leading 16Mbit DRAM suppliers for 1996. Samsung established an earlylead in this segment and has managed to maintain its leadership as this market has matured.NEC, meanwhile, desired to match Samsung’s aggressive 16Mbit DRAM schedule.

16Mbit DRAM demand took a sharp upswing in 1996 as prices dropped for this density as well.Greater affordability and availability of the wide configurations helped to jump start this market.Figure 2-33 compares the rise in 16Mbit DRAM demand with the fall of ASPs during 1996 and 1Q97.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-27

$15,690M

Source: ICE, "Memory 1997" 20879B

Others32%

Samsung21%

NEC 15%

Toshiba10%

Hitachi13%

Hyundai9%

Figure 2-32. 1996 Leading 16Mbit DRAM Suppliers

Figure 2-33. Lower Prices Increase 16Mbit Demand

Mill

ion

s o

f U

nit

s

AS

P (

$)

Source: ICE, "Memory 1997" 21780A

ASP

Units

$43.25

$7.15

107

47.7

0

20

40

60

80

100

120

140

160

MarFebJanDecNovOctSeptAugJulyJuneMayAprMarFebJan0.00

8.00

16.00

24.00

32.00

40.00

48.00

1996 1997

With the rapid decline of 16Mbit ASPs, Korean DRAM vendors capped or reduced their output of16Mbit devices in the first half of 1997 by as much as 30 percent. In 2Q97, Samsung reduced itsmonthly 16Mbit output from 18 million units to 16 million. A few Japanese suppliers (NEC,Toshiba, Oki, et al) took similar action. Prices fell so far that the business was no longer profitableand threatened their ability to invest in future products.

Despite the slim profit margins, talk of reduced output, and the move to the 64Mbit generation,production of 16Mbit DRAMs began in earnest in Taiwan during 4Q96. Nan Ya Technologystarted volume shipments of a 16Mbit (4Mbit x 4) EDO DRAM family from its new 200mm fab.The devices were manufactured using 0.4µm technology. The company plans additional configu-rations for 1997. Although it obtained its technology from Oki and will produce DRAMs for theJapanese company, Nan Ya will also sell its products on the merchant market using its own logo.

Taiwan’s Powerchip Semiconductor also initiated 16Mbit EDO DRAM production in 1996.Powerchip, formed in late 1994, obtained its 16Mbit and 64Mbit DRAM technology fromMitsubishi. It will sell 50 percent of its output to the Japanese company, with the remainder ded-icated to several Taiwanese-based firms.

Hyundai is bullish on the synchronous DRAM market and in 4Q96 released its 16Mbit SDRAM.Configured in x16, x8, or x4 versions, the device is expected to help improve Pentium Pro perfor-mance by as much as 20 percent compared to conventional EDO DRAM. Hyundai planned toexpand its SDRAM product line in 1H97 with the introduction of a 64Mbit SDRAM.

To cut production costs, several Taiwan-based DRAM suppliers shifted their 16Mbit productionlines to 0.35µm process technology in 2Q97. Among the companies moving to the finer processgeometry were TI-Acer, Vanguard International, United Semiconductor, Mosel-Vitelic, andPowerchip Semiconductor.

In another cost-cutting move, Fujitsu accelerated its drive to shrink 16Mbit DRAM size in orderto lower its production costs. The company currently manufactures 60mm-square chips usinga 0.36µm process. It hopes to reduce that to a 40mm-square chip using a 0.28µm process byearly 1998.

Some DRAM suppliers looked to more lucrative opportunities such as combining memory andlogic on a single chip. Though there are several crucial technology and manufacturing hurdles toovercome, the idea of memory and logic on one chip is intriguing to OEMs and suppliers.Immediate benefits of incorporating both technologies on one chip include higher bandwidth(great for graphics applications) and the obvious board space savings. Section 7 (DRAMTechnology) and Section 11 (Embedded Memory) further discuss the concept of DRAM and logicon the same chip.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-28

Additional company and product highlights surrounding the 16Mbit DRAM market are listedbelow.

Fujitsu

Announced that it would rely on Taiwan Semiconductor Manufacturing Company (TSMC inHsinchi, Taiwan) for as much as 40 percent of its 16Mbit DRAM production. Fujitsu said it willlower its own 16Mbit production by 15 percent and concentrate its own resources on 64Mbitproduction.

Hitachi

In response to the glut in the DRAM market, Hitachi underwent one of the most aggressive prod-uct restructurings of any Japanese chip maker. It shifted its production of 16Mbit DRAMs in Kofu,Japan, to flash memory devices. That move followed the news from 1Q97 to kill a joint-ventureDRAM fab in Malaysia with LG Semicon and an announcement in December, 1996 to re-open aclosed 16Mbit DRAM fab to make SH MPUs instead.

Of the 16Mbit DRAM devices Hitachi offers, approximately 40 percent are supplied by LGSemicon of Korea.

Intel

Intel announced in 1Q97 that it took an equity position in a $1.3 billion memory fab being built inAustin, Texas, by Samsung. In exchange for its equity position, Intel will be guaranteed an undis-closed number of wafers from the facility, which is expected to produce 16Mbit and 64MbitDRAMs using sub-0.5µm technology.

Mitsubishi

Mitsubishi officials displayed a 16Mbit device built using silicon-on-insulator (SOI) wafers. Thecompany claims that its new 16Mbit DRAM on SOI, slated for sampling in 1998, has the accessspeed of a 64Mbit device built on a standard silicon wafer. It should be noted that SOI startingwafers are three to five times more costly than standard silicon wafers.

NEC

Although unit demand is strong, NEC realizes that the market for 16Mbit devices will have a hardtime recovering from its 1H97 levels. As a result, NEC announced it would trim 16Mbit DRAMoutput 20 percent by the end of fiscal 1997 (March 31, 1998).

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-29

Oki

Oki invested $700 million to build a 16Mbit/64Mbit DRAM production facility in the U.S. The0.35µm 200mm wafer processing line will be located in Oregon.

Toshiba

Toshiba off-loaded a small portion of its 16Mbit DRAM production to Taiwan-based WinbondCorporation, which also expects to make 64Mbit DRAM for Toshiba. Additionally, the companylowered its own 16Mbit DRAM output by 15 percent in 1Q97.

64Mbit DRAMs

64Mbit DRAMs arrived on the market in volume in the first half of 1996—a time when overallDRAM prices were dropping quickly. With hopes of capturing some of the hefty profits that eludedthe 16Mbit generation, several companies disclosed plans to ramp up 64Mbit DRAM production.

With many companies jumping into the lucrative 64Mbit DRAM market, an oversupply situationwas created, which defeated DRAM manufacturers’ goal of producing chips with higher profitmargins. Once again, DRAM vendors deprived each other of the high margins they came toexpect at the beginning of the DRAM product life cycle.

The rapid drop in average selling price is premature for this new-generation of devices. From apricing standpoint, the 1997 market for 64Mbit devices is forecast to remain very fragile.Producers will try to maintain higher prices, but there could well be dissension among the ranks,which may result in even lower prices by the end of 1997.

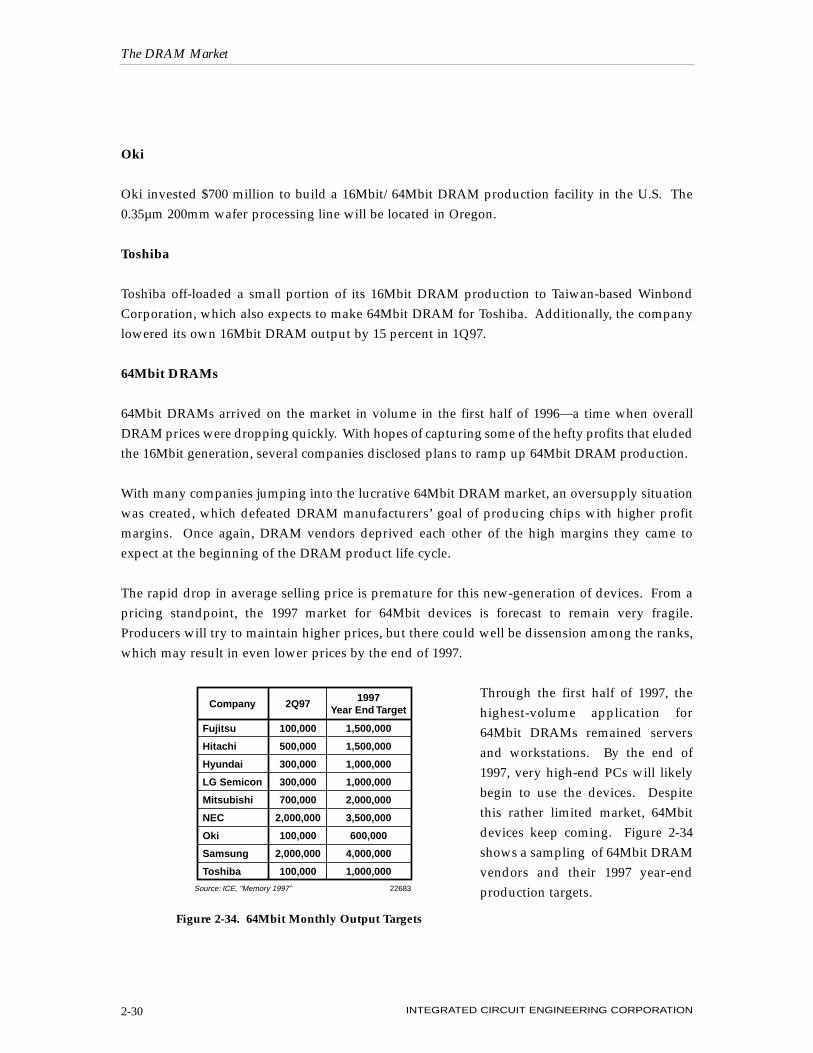

Through the first half of 1997, thehighest-volume application for64Mbit DRAMs remained serversand workstations. By the end of1997, very high-end PCs will likelybegin to use the devices. Despitethis rather limited market, 64Mbitdevices keep coming. Figure 2-34shows a sampling of 64Mbit DRAMvendors and their 1997 year-endproduction targets.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION2-30

Company 2Q971997

Year End Target

Fujitsu

Hitachi

Hyundai

LG Semicon

Mitsubishi

NEC

Oki

Samsung

Toshiba

100,000

500,000

300,000

300,000

700,000

2,000,000

100,000

2,000,000

100,000

1,500,000

1,500,000

1,000,000

1,000,000

2,000,000

3,500,000

600,000

4,000,000

1,000,000

Source: ICE, "Memory 1997" 22683

Figure 2-34. 64Mbit Monthly Output Targets

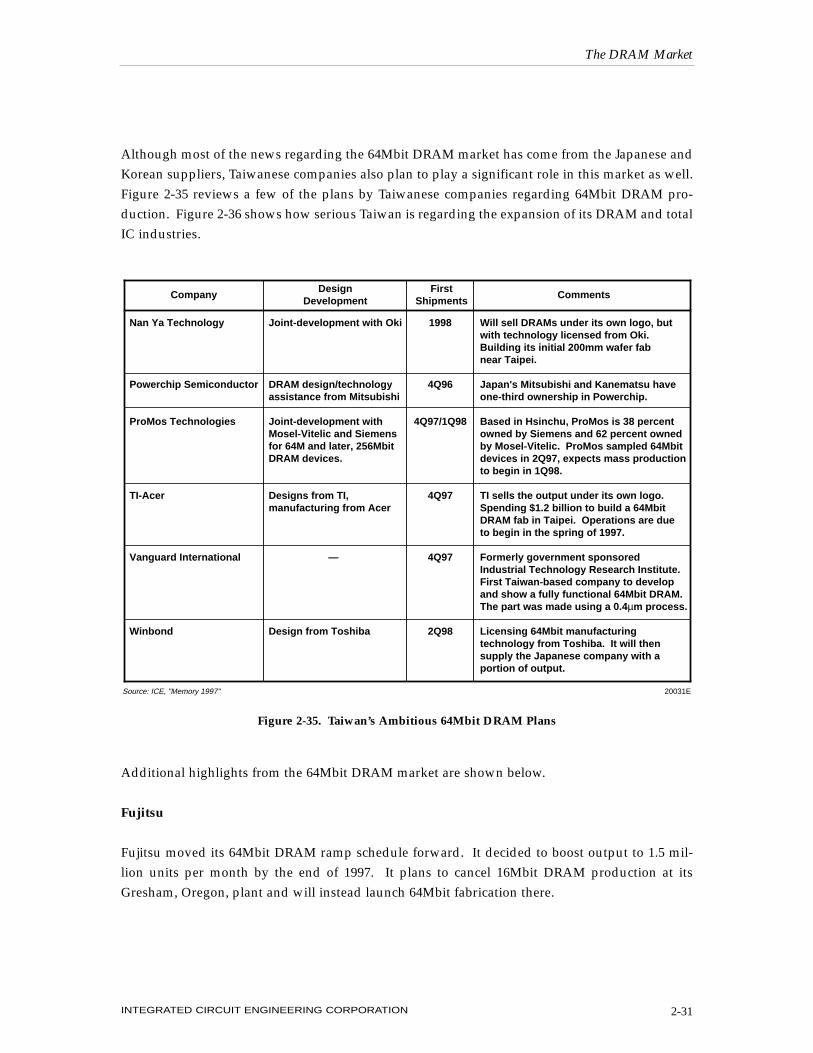

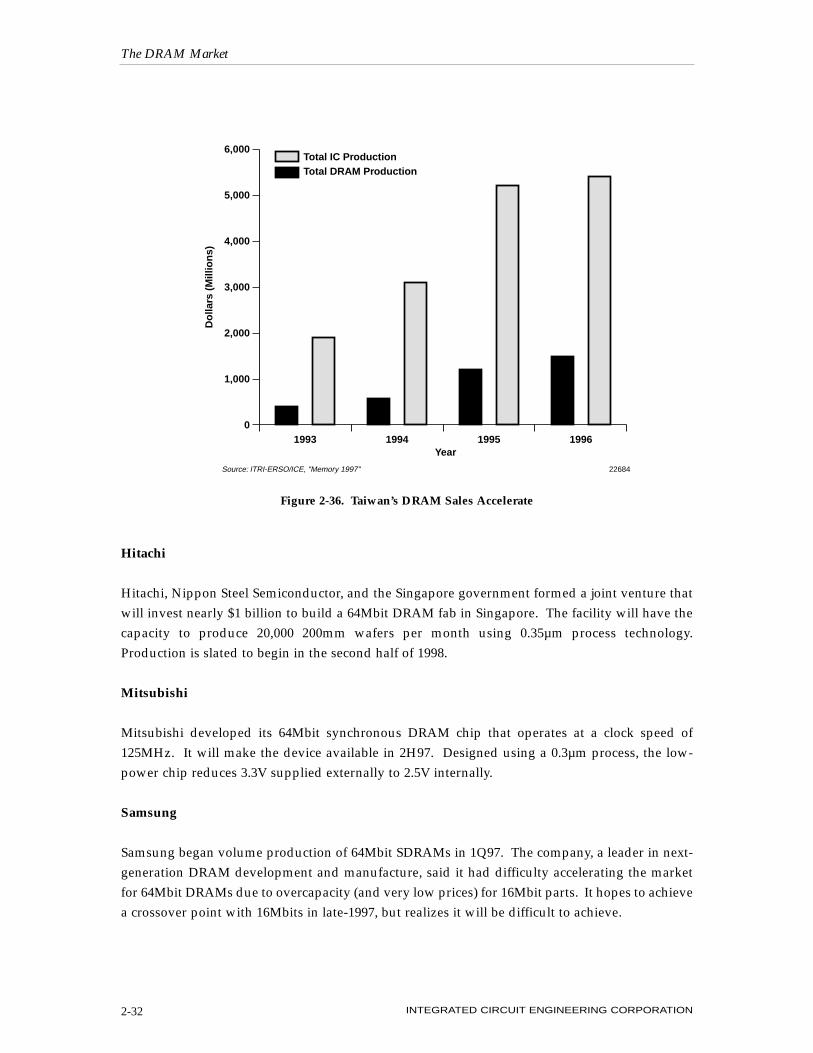

Although most of the news regarding the 64Mbit DRAM market has come from the Japanese andKorean suppliers, Taiwanese companies also plan to play a significant role in this market as well.Figure 2-35 reviews a few of the plans by Taiwanese companies regarding 64Mbit DRAM pro-duction. Figure 2-36 shows how serious Taiwan is regarding the expansion of its DRAM and totalIC industries.

Additional highlights from the 64Mbit DRAM market are shown below.

Fujitsu

Fujitsu moved its 64Mbit DRAM ramp schedule forward. It decided to boost output to 1.5 mil-lion units per month by the end of 1997. It plans to cancel 16Mbit DRAM production at itsGresham, Oregon, plant and will instead launch 64Mbit fabrication there.

The DRAM Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-31

CompanyDesign

DevelopmentFirst

ShipmentsComments

Will sell DRAMs under its own logo, butwith technology licensed from Oki.Building its initial 200mm wafer fabnear Taipei.

Japan's Mitsubishi and Kanematsu haveone-third ownership in Powerchip.