The Devastation of Flooding - Gallagher · flood, commonly called the "hundred year flood." Base...

30

16BSD23491F © 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ The Devastation of Flooding How to Identify Properties in Flood Plains and What to Do Before and After A Flood STEVE BOYER – GALLAGHER BASSETT GARY WOOD – GALLAGHER BASSETT APPRAISALS NIGEL WILSON – DUFF & PHELPS AMPY JIMENEZ – ARTHUR J GALLAGHER TIM DRANEY – BMS CAT

Transcript of The Devastation of Flooding - Gallagher · flood, commonly called the "hundred year flood." Base...

16BSD23491F © 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

The Devastation of FloodingHow to Identify Properties in Flood Plains and

What to Do Before and After A Flood

STEVE BOYER – GALLAGHER BASSETTGARY WOOD – GALLAGHER BASSETT APPRAISALSNIGEL WILSON – DUFF & PHELPSAMPY JIMENEZ – ARTHUR J GALLAGHERTIM DRANEY – BMS CAT

16BSD23491F

Convocation 2016Flood Plan Issues

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 316BSD23491F

• Flooding is the most common and costly natural disaster in the United States, causing an average of $50 billion in economic losses each year. Most U.S. natural disasters declared by the president involve flooding.

• In order to improve the development of proper insurance coverage and avoid the risk of underinsuring, appraisal companies are now being asked to provide updated flood risk information.

FLOODING

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 416BSD23491F

• General and temporary condition of partial or complete inundation of 2+ acres or 2+ properties (at least one of which is your property) from:

– Overflow of inland or tidal waters– Unusual and rapid accumulation or runoff of surface waters from any source

• Mudflow - A river of liquid and flowing mud on the surfaces of normally dry land, as when earth is carried by a current of water

• Collapse or sinking of land along shore resulting from erosion or undermining caused by waves, or currents of water exceeding anticipated cyclical levels- RAPID erosion

A FLOOD IS . . .

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 516BSD23491F

• Base Flood Elevation (BFE) - The base flood is the 1%-annual-chance flood, commonly called the "hundred year flood." Base Flood Elevation is the water-surface elevation of the base flood. The depth of the base flood can be calculated by subtracting the ground elevation from the BFE. The probability is 1% that rising water will reach BFE height in any year; which compounds over a thirty-year period to 26% or more.

• In the flood zone - This term is used by most people to mean the property is in the Special Flood Hazard Area (SFHA), as depicted on the Flood Insurance Rate Map (FIRM). The NFIP flood zones are A and V zones and sometimes have letters or numbers following the A or V (e.g. AE, AH, AO, VE). The officially adopted FIRM is the basis for all flood insurance rating. The community may be using a more restrictive map with broader flood zones and higher flood standards for regulating floodplain development. The community's regulatory map also may include allowances for increased runoff, subsidence, failure of dams and levees, or sea level rise, which are not reflected on the FIRM.

FLOOD ZONE DEFINITIONS

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 616BSD23491F

• Too low- From an insurance-rating standpoint, "too low" means the elevation of the building is lower than the BFE. Building elevation in the A-zones is measured at the top of the lowest floor. Elevation in the V-zones is measured at the bottom of the lowest horizontal structural member of the foundation. Enclosures that are lower than the living space may be considered the "lowest floor" in some circumstances; machinery and equipment located below the living space may raise insurance rates. The following resources may be helpful:

– NFIP Elevation Certificate with lowest floor diagrams– FEMA Technical Bulletin 1-08: Openings in Foundation Walls and Walls of Enclosures

• From a practical standpoint, "too low" means the risk of flooding is higher, a fact that has been concealed till now by artificially low (subsidized) insurance rating. The lower you are relative to BFE, the higher your risk of flooding. Being “too low” in the flood zone can cause hardship for the owner if the building is substantially damaged by fire, flood, tornado, earthquake or other event and must be raised before it can be repaired. The cost of raising the building usually is not covered by home owners insurance, but may be offset to some extent by the Increased Cost of Compliance coverage of the NFIP policy.

FLOOD ZONE DEFINITIONS CONT.

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 716BSD23491F

• Can be captured on the buildings appraised. For flood zone determination, the appraisal company will provide the following information:

– The Zone– Community Number– Map Panel Number– Map Date– Letter Map Amendments if any

• The certified flood zone determinations for each building will be coordinated through a third party vendor. The certified flood zone determination letter is then added the clients COPE spreadsheet. The physical flood zone identifier certificate, is then kept in the clients correspondence file.

• A certified flood zone determination information provides protection in case of errors that may lead to the wrong flood zone determination letter and loss to the client.

FLOOD ZONE DETERMINATION

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 816BSD23491F

• In order to develop the proper flood zone determination, the appraisal company will first obtain the following information:

– The individual clients building name– Building address– COPE Data– Global Positioning System (GPS) coordinates or longitude/latitude

coordinates

• This data is then providing to a third party vendor to develop the certified flood zone determination letters.

FLOOD ZONE DETERMINATION

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 916BSD23491F

Component-Based Appraisal Methodology• Buildings - site inspection

– Review of available as-built plans– Measuring of dimensions– Determination of primary construction components– Opinion of quality of materials and construction – Review of building services, interior and exterior finishes, additional features, etc.– Photographing of each building– Development of replacement cost using local construction cost resources– Reporting of values and COPE data by building– Evaluation of land improvements (if required) - parking lots, signage, outdoor lighting,

etc.• We do not recommend trending building costs:

– High probability of capitalized renovations results in excessive replacement cost– Unable to break out original costs by individual building

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1016BSD23491F

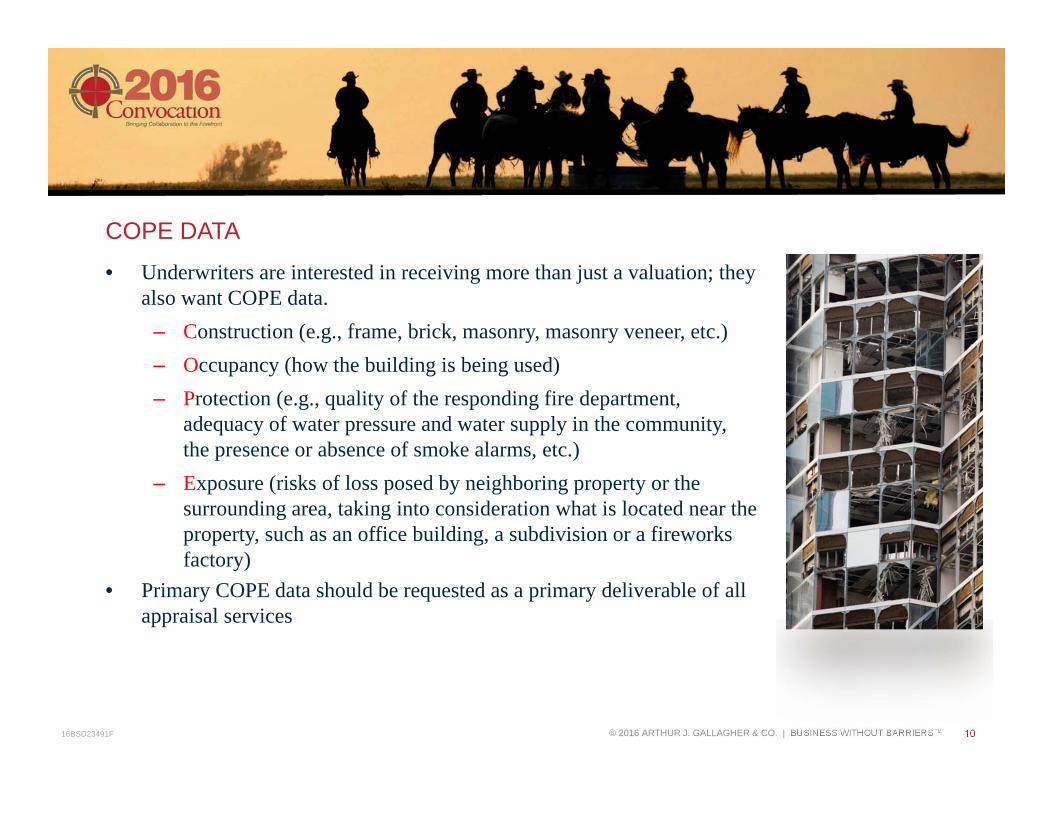

• Underwriters are interested in receiving more than just a valuation; they also want COPE data.

– Construction (e.g., frame, brick, masonry, masonry veneer, etc.)– Occupancy (how the building is being used)– Protection (e.g., quality of the responding fire department,

adequacy of water pressure and water supply in the community, the presence or absence of smoke alarms, etc.)

– Exposure (risks of loss posed by neighboring property or the surrounding area, taking into consideration what is located near the property, such as an office building, a subdivision or a fireworks factory)

• Primary COPE data should be requested as a primary deliverable of all appraisal services

COPE DATA

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1116BSD23491F

Standard COPE Data• Occupancy• Address• Class of construction• Year of construction• Square feet of space• Number of stories• Average story height• Wall construction• Roof construction• Heating system• Cooling system• Fire alarm• Sprinklers• Entry alarm• GPS coordinatesOptional COPE Data• Plot plans• Flood zone certification

Secondary Windstorm COPE Data: (more detailed structural/location specific data elements)• Construction quality• Roof covering• Roof age/condition• Roof geometry• Roof anchor• Roof equipment bracing• Basement• Appurtenant structures• Cladding type• Roof sheeting attachment• Frame/foundation attachment• Ground-level equipment• Opening protection• Flashing and coping quality• Content grade

16BSD23491F

Convocation 2016A Flood Is…

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1316BSD23491F

ELIGIBLE BUILDINGS• A structure with two or more outside rigid walls and a fully secured roof, that is affixed to a

permanent site;

• Special Flood Hazard Areas (SFHAs):

– Zones A, A1-A30, AE, AH, AO, A99, AR, V, V1-V30, VE– Mandatory purchase applies

• Non-Special Flood Hazard Aarea(Moderate/Minimal Flood Risks)

– Zones B, C, X– 25 - 30% claims paid in these zones– Insurance optional - highly recommended

FLOOD ZONES

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1416BSD23491F

• Flood mappings are constantly being re-zoned• Annual Flood determination on your schedule of locations• Avoid E&O’s- Property policies wording :

- Deductible: should be Excess of available coverage from NFIP weather purchased or not.

- Flood Zone determination: It is hereby agreed and understood that for the purpose of applying the flood deductible, flood sublimit and flood aggregate, the flood zone determination for locations whole or partially located in a Special Flood Hazard (SFHA) as determined by FEMA will be the determination as listed on the SOV at time of binding and will be used for the duration of the policy. With respects to locations added after binding, the flood zone determined at the time of addition will be applicable zone for the duration of the policy term.

WHAT YOUR AGENT SHOULD BE DOING FOR YOU

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1516BSD23491F

• What you need in order to receive FEMA reimbursement• Who is not covered by FEMA

NFIP

Are you prepared:

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1616BSD23491F

FLOODSMART.GOV

For customers wanting more information on:

• Flood Risks• Map Changes• Coverages• Exclusions

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1716BSD23491F

Here Comes The FloodNow What Do I Do?

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1816BSD23491F

• Remove Contents – If Possible• Move Contents From Lower Level To Higher Areas• Focus On Valuable Papers & Records• Focus On Valuable Artifacts• Check Sump Pumps To Insure They Are Working• Identify Restoration Contractor

PRE FLOOD PLANNING

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 1916BSD23491F

HERE IT COMES

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2016BSD23491F

SOMETIMES YOU’RE LUCKY…

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2116BSD23491F

…AND SOMETIMES YOU’RE NOT!

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2216BSD23491F

• Shut Off Main Electrical Switcho Water In The Buildingo Down Power Lines

• Shut Off Basement Furnace And Outside Gas Value

• Evacuating Buildingo Do Not Walk In Moving Watero Do Not Return Until Water Has Receded

THE FLOOD HAS ARRIVED

The Flood Has Arrived

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2316BSD23491F

My Home Town – Again And Again!!

16BSD23491F

THE CLEAN UP

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2516BSD23491F

• Recovery is a Process– Implement your recovery plan– Stabilize the property – Limit the Damage (your responsibility)

• Electrical issues• Water leakage/structural issues• Security• Replacement equipment• Contents/documents

– Determine the scope of restoration and repairs– Agree with adjuster, time line for work, initiate activity– Document for claim presentation

STEPS TO RECOVERY

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2616BSD23491F

• Emergency services to stabilize and limit damage– Remove water, stop source of water, begin muck out of

structure, emergency power, security, board up– Determine need for drying, desiccant vs room units –

moisture map, mobilize equipment– Pull moisture attackers (carpet, insulation, drywall, celling

tiles, particle board)– Look for special items, books/records, paper, art work,

things that YOU NEED TO PROTECT– POC/contractor/adjuster, consultant meetings daily

STEP 1: MITIGATION

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2716BSD23491F

• Recovery begins– Agree on scope, coverage issues discussed, estimate of costs,

time line – Drying continues and is monitored, moisture readings are taken,

can’t dry to fast, microbial issues– Controlled demo per the scope, not just cut and go– Pull carpet/pad and dispose, discard debris, – Sanitize, seal, clean furniture, equipment, – Freeze drying of paper items– Complete per scope, daily meetings, look at “put back” and the

approach– Sign off on work complete

STEP 2: RESTORATION, REMEDIATION

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2816BSD23491F

• Final part to reopen structure– Scope and estimate of repair– Going back the way it was, remodel, coverage– Award contract to GC– Monitor GC progress, change orders required, update

meetings

STEP 3: “PUT BACK” RECONSTRUCTION

© 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™ 2916BSD23491F

• Implement your contingency recovery plan• Daily meetings on large projects is critical• Make sure the scope is accurate, changes documented in

writing• Keep adjuster aware of issues• Remodeling may be out of the scope of coverage• Document everything• Patience, recovery is an arduous task but with the right

partners and planning it can go smoothly

WRAP UP

16BSD23491F © 2016 ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Thank You