The Deutsche Bank Guide to · PDF file23 March 2017 Special Report: The Deutsche Bank Guide to...

45

Deutsche Bank Markets Research Global Special Report Economics Foreign Exchange Rates Date 23 March 2017 The Deutsche Bank Guide to Brexit ________________________________________________________________________________________________________________ Deutsche Bank AG/London DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016. Oliver Harvey UK Macro Strategist (+44) 20 754-51947 [email protected] Mark Wall Chief Economist (+44) 20 754-52087 [email protected] After Article 50 is triggered, sequencing is the key that opens all doors to Brexit. The current timeframe to conclude negotiations is unrealistic particularly if the deal requires ratification from all EU national parliaments (a mixed agreement). The UK and EU27 must find a way to conclude a transitional deal without a lengthy sign-off process or the UK will drop out of the EU in March 2019 with no deal. A transitional deal will be tricky but not impossible. Turkey shows the customs union is not intimately bound to the Single Market. The EEA Treaty might also provide a template. But the UK will have to accept budget contributions, pooling of sovereignty and compromise on freedom of movement. Politics is the main risk. Behind the bluster, Secretary of State Davis has struck a more moderate tone in parliamentary testimony. But we are concerned the current strategy for a broad-based trade deal by 2019 risks jeopardizing the chances of a transitional agreement. The government’s wafer-thin majority in parliament has also yet to be resolved. Eurosceptic Conservative MPs and the right-wing UK press will push for a clean break, constraining Prime Minister May’s ability to compromise. An early general election would dilute their influence. Politics will be equally problematic for the EU27. With populism increasingly felt across the continent, the EU must take account of the threat a successful Brexit would present of the European project. The differing national interests of EU27 states will be a theme of talks. Most importantly, Brexit negotiations are just one of several competing priorities for the EU over the next two years. Economically, the UK must prevent a sudden exit from the customs union in March 2019 or risk seeing huge disruption to existing business models. It is also in the UK and EU’s interest to seek short-term regulatory equivalence for financial services, but this will be unsustainable long term due to regulatory divergence and the risks the City would pose for the Eurozone. The future for other service industries, making up over thirty percent of UK exports, looks bleak unless an EEA approach is pursued. The UK’s ability to conduct third-country free trade deals is at best a red- herring and at worst a waste of time and energy. They will face political, technical and structural headwinds. The primary focus of the negotiations must be to conclude a deal with the EU. Only once this is achieved should attention be turned to the rest of the world. UK economic growth following last year’s referendum confounded pessimistic forecasts, but is unlikely to continue. There is growing evidence of the real income shock. The Bank of England seems to feel under pressure from rising inflation and robust growth to hike rates, but with little evidence of rising wages, caution on monetary policy is likely to prevail in the near term. Medium-term, the success of a post-Brexit UK will rest on the industrial strategy. This is particularly true if net migration begins to fall, weakening demographics. The strategy should maximize the UK’s strengths in high tech manufacturing and education, but is not yet ambitious enough. The market should hope for the best but plan for the worst. Time constraints, the scale and complexity of talks and the threat that a soft deal represents to EU means the UK faces an uphill battle to avoid a hard outcome. The political difficulties only look resolvable with an early UK general election. Our base case is that the UK will eventually compromise, but this will depend on a weakening economy and market pressure, with a full cliff-edge Brexit likely to be fully priced at some point in the next two years.

Transcript of The Deutsche Bank Guide to · PDF file23 March 2017 Special Report: The Deutsche Bank Guide to...

Deutsche Bank Markets Research

Global

Special Report

Economics Foreign Exchange Rates

Date 23 March 2017

The Deutsche Bank Guide to Brexit

________________________________________________________________________________________________________________

Deutsche Bank AG/London

DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016.

Oliver Harvey

UK Macro Strategist

(+44) 20 754-51947

Mark Wall

Chief Economist

(+44) 20 754-52087

After Article 50 is triggered, sequencing is the key that opens all doors to

Brexit. The current timeframe to conclude negotiations is unrealistic particularly if the deal requires ratification from all EU national parliaments (a mixed agreement). The UK and EU27 must find a way to conclude a transitional deal without a lengthy sign-off process or the UK will drop out of the EU in March 2019 with no deal.

A transitional deal will be tricky but not impossible. Turkey shows the customs union is not intimately bound to the Single Market. The EEA Treaty might also provide a template. But the UK will have to accept budget contributions, pooling of sovereignty and compromise on freedom of movement.

Politics is the main risk. Behind the bluster, Secretary of State Davis has struck a more moderate tone in parliamentary testimony. But we are concerned the current strategy for a broad-based trade deal by 2019 risks jeopardizing the chances of a transitional agreement. The government’s wafer-thin majority in parliament has also yet to be resolved. Eurosceptic Conservative MPs and the right-wing UK press will push for a clean break, constraining Prime Minister May’s ability to compromise. An early general election would dilute their influence.

Politics will be equally problematic for the EU27. With populism increasingly felt across the continent, the EU must take account of the threat a successful Brexit would present of the European project. The differing national interests of EU27 states will be a theme of talks. Most importantly, Brexit negotiations are just one of several competing priorities for the EU over the next two years.

Economically, the UK must prevent a sudden exit from the customs union in March 2019 or risk seeing huge disruption to existing business models. It is also in the UK and EU’s interest to seek short-term regulatory equivalence for financial services, but this will be unsustainable long term due to regulatory divergence and the risks the City would pose for the Eurozone. The future for other service industries, making up over thirty percent of UK exports, looks bleak unless an EEA approach is pursued.

The UK’s ability to conduct third-country free trade deals is at best a red-herring and at worst a waste of time and energy. They will face political, technical and structural headwinds. The primary focus of the negotiations must be to conclude a deal with the EU. Only once this is achieved should attention be turned to the rest of the world.

UK economic growth following last year’s referendum confounded pessimistic forecasts, but is unlikely to continue. There is growing evidence of the real income shock. The Bank of England seems to feel under pressure from rising inflation and robust growth to hike rates, but with little evidence of rising wages, caution on monetary policy is likely to prevail in the near term.

Medium-term, the success of a post-Brexit UK will rest on the industrial strategy. This is particularly true if net migration begins to fall, weakening demographics. The strategy should maximize the UK’s strengths in high tech manufacturing and education, but is not yet ambitious enough.

The market should hope for the best but plan for the worst. Time constraints, the scale and complexity of talks and the threat that a soft deal represents to EU means the UK faces an uphill battle to avoid a hard outcome. The political difficulties only look resolvable with an early UK general election. Our base case is that the UK will eventually compromise, but this will depend on a weakening economy and market pressure, with a full cliff-edge Brexit likely to be fully priced at some point in the next two years.

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 2 Deutsche Bank AG/London

Executive summary: Tempus fugit

Brexit is the most important political event for the UK since WW2, and will shape the UK economy for generations. In this report, we provide a comprehensive guide for investors for the months and years ahead. The report is structured around 44 of the most important questions concerning the Brexit process.

Stop all the clocks More than the economics, or even the politics, time will be the decisive factor in negotiations. Article 50 of the Lisbon Treaty was designed so no member state would contemplate triggering it. According to the EU Commission, an agreement will need to be concluded by October 2018, in just over eighteen months time.

The real timeframe will be shorter. Negotiations may not begin in earnest until after the French elections in June and important decisions deferred until after the next German government is formed in late autumn. Agreeing a wide-reaching new relationship in an eighth of the time it took to conclude the recent free trade agreement between Canada and the EU is highly optimistic. This is particularly true as EU attention will be taken up with the future direction of the European project.

Interim or out This means two things. First, a transitional arrangement is needed to buy more time. This is not the same as the implementation period currently suggested by the UK government. Second, this will need to be simple and largely off-the-shelf, not a complex agreement containing multiple carve-outs and much negotiation.

A transitional deal still raises a number of questions. Can it be incorporated into the UK’s divorce agreement with the EU27? If so, what will be its legal basis as EU law ceases to apply? Will a deal need to be signed off by national parliaments or just a majority in the EU Council? The closer we get to March 2019, the more the details of international and EU law will matter.

Politically challenged Negotiations will be conducted against a highly unstable political backdrop. In the UK, PM May must appease eurosceptic MPs who see limited risks from a clean break, or underweight them relative to demands for sovereignty. With the smallest parliamentary majority since the mid-1970s, there will be plenty of opportunities for rebellious MPs to undermine talks. A snap general election this year would result in a larger government majority and be bullish for the eventual outcome.

For the EU27, the UK cannot retain the benefits and spurn the obligations of EU membership without undermining the European project. While the EU Council will initially present a united front, national differences are likely to emerge as talks progress, leaving the UK to negotiate with a moving target.

Forget global Britain; focus on the EU A sudden exit from the customs union is the largest immediate risk for the UK and EU27, and would be very damaging for businesses that rely on frictionless cross-border trade. A transitional agreement is achievable given a common starting point and because the customs union is not intimately bound to the Single Market. But this will be binary: a sector-by-sector deal is not unachievable.

London’s role as Europe’s banker will diminish over time due to the differing regulatory priorities of the UK and EU27 and the reluctance of Eurozone authorities to tolerate an offshore financial centre with no political oversight. Short term, though, a transitional deal should maintain equivalence between the UK and EU27 to allow the financial industry more time to plan and adapt.

Neither access to the customs union nor equivalence for financial services will be of any comfort to other service industries. Single Market access is important to the legal, digital and airline sectors, among many others. A deal on services will require a mixed agreement from the EU27, meaning a transitional deal will be very difficult unless the UK pursues the EEA option.

The merits of WTO rules where the UK is free to conclude new trade deals with the rest of the world are overegged. The UK would need to rip up vast swathes of its existing regulatory architecture and still faces structural headwinds in negotiating new trade deals, such as its low share of global imports and the secular decline in world trade since the crisis. The UK should concentrate on securing a favorable deal with the EU first before devoting much energy to free trade deals elsewhere.

No such thing as a free Brexit Ultimately, any transitional deal will have to involve UK compromises, including some form of contribution to the EU budget, pooling of sovereignty, and limited checks on EU migration. The alternative is that the UK pays through lower trade and economic disruption.

The vote for Brexit was one against globalization. Yet, the UK will need to become more competitive to adapt to life outside the EU, particularly if a more restrictive migration policy sees demographics deteriorate. Resolving this will be the hardest challenge for UK politicians. An industrial strategy may be the answer. But so far, proposals are not ambitious enough.

Remain bearish GBP, other markets more nuanced For markets, sterling will continue to be the main shock-absorber for the Brexit talks. It is likely that the market prepares for a hard Brexit (no transitional deal) at some point in the next two years, even if the ultimate outcome is positive. This is not yet fully priced, and we remain bearish. The outlook for other assets is more nuanced.

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 3

Table of contents

The sequencing of talks and a transitional deal pp.4-8 1. Why is the short Article 50 timeline shorter than it appears?

2. Can parallel talks be conducted?

3. If time runs out, could agreement be extended?

4. Is Article 50 irreversible?

5. What are the positions of both sides on a transitional agreement?

6. What is the difference between a transition and implementation period?

7. What are the obstacles to a transitional deal?

8. Could EEA membership be used as a transitional agreement?

9. How could a transitional deal be constructed?

Divorce negotiations pp.9-11 10. What are the main contents of the divorce negotiations?

11. How high is the UK’s divorce bill likely to be?

12. Why is the divorce bill likely to prove so contentious?

13. Why are EU citizens rights not protected after Brexit?

14. What are the other aspects of the divorce negotiations?

A new relationship with the EU pp.11-22 15. What are the trade options for the UK with the EU after Brexit?

16. What is the economically least disruptive option?

17. Could the UK seek a sector-specific customs deal with the EU?

18. What other obstacles are there to access to the customs union?

19. How could a customs union deal be constructed?

20. What kind of deal could be reached for financial services?

21. Why is a transitional deal important for financial services?

22. What about other services?

23. What are the options for freedom of movement?

24. Why is immigration policy important for UK growth?

25. Who has got most leverage in negotiations?

26. Why are these issues not comprehensive?

UK trade outside the EU pp.23-26 27. Why is the WTO not a fallback option?

28. Can the UK negotiate third country free trade deals during EU talks?

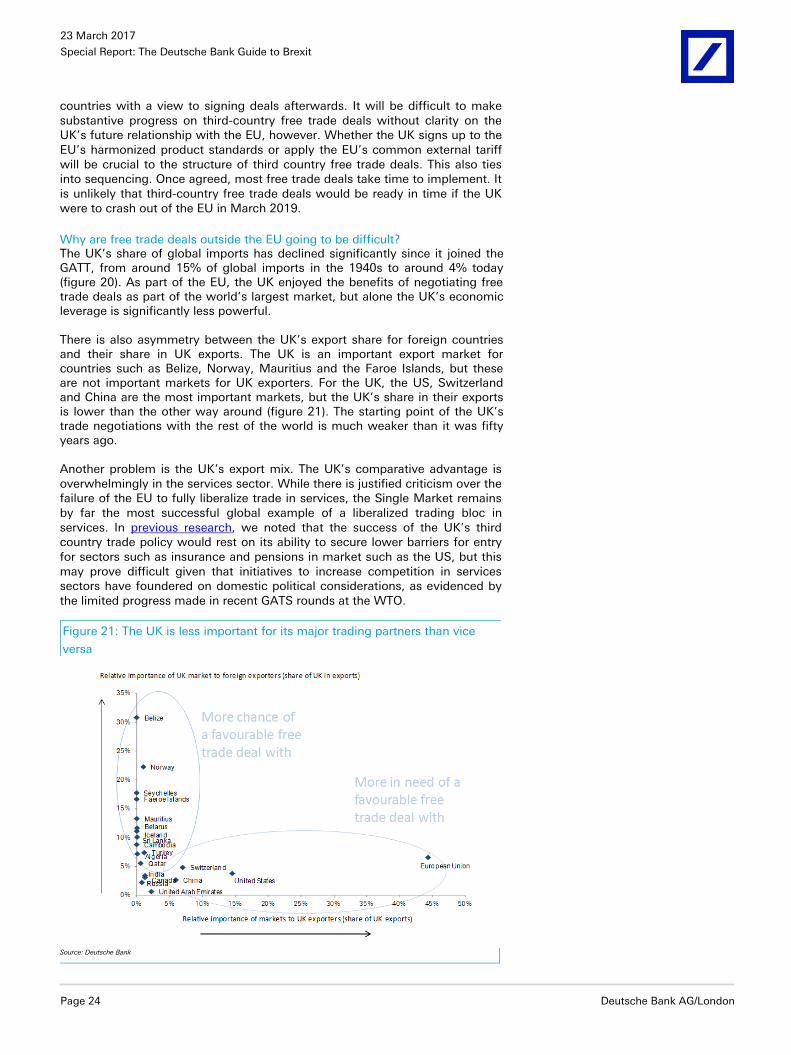

29. Why are free trade deals outside the EU going to be difficult?

30. Why should third country free trade deals be a low priority?

31. What free trade deals will the UK lose as part of its EU membership?

32. Could relaxing state aid rules mitigate a hard Brexit outcome?

Political risks pp.27-29 33. How easy will it be for May to compromise with the EU?

34. Why would a snap UK general election be a positive outcome?

35. What is the risk of Scottish independence?

36. To what extent will Brexit undermine the trust in UK institutions?

37. What are the main political risks for the EU27?

38. Why will Germany not be directing the agenda for the EU27?

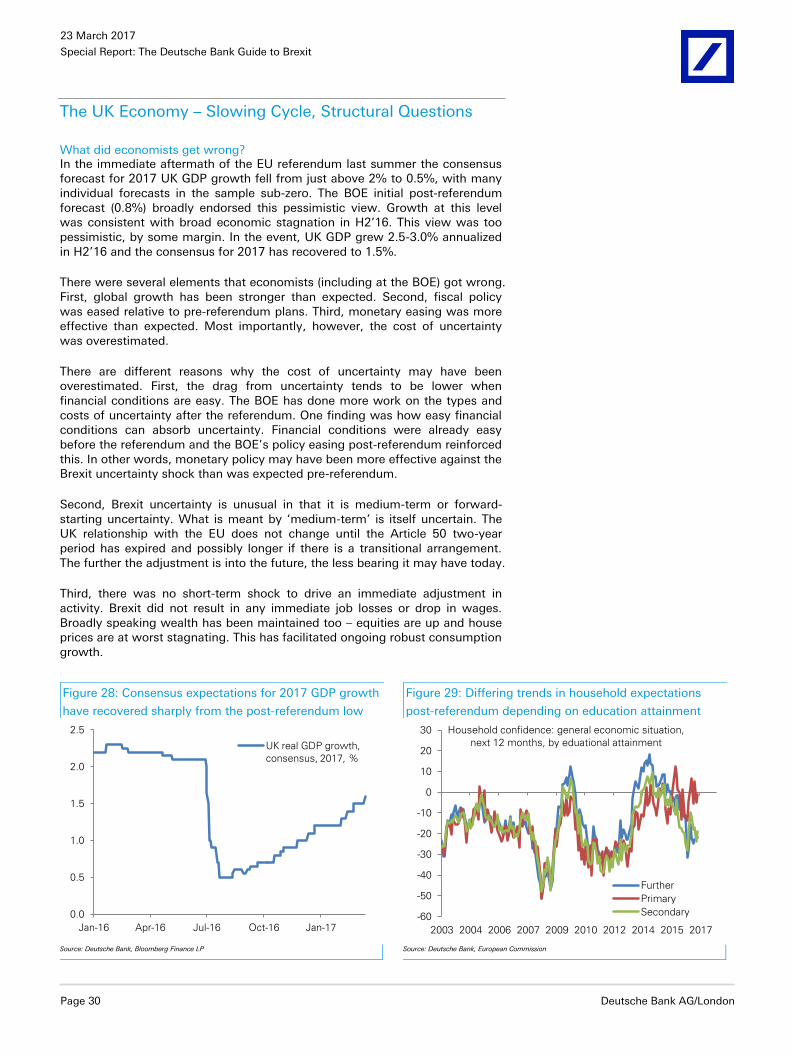

Brexit and the UK economy pp.30-37 39. What did economists get wrong?

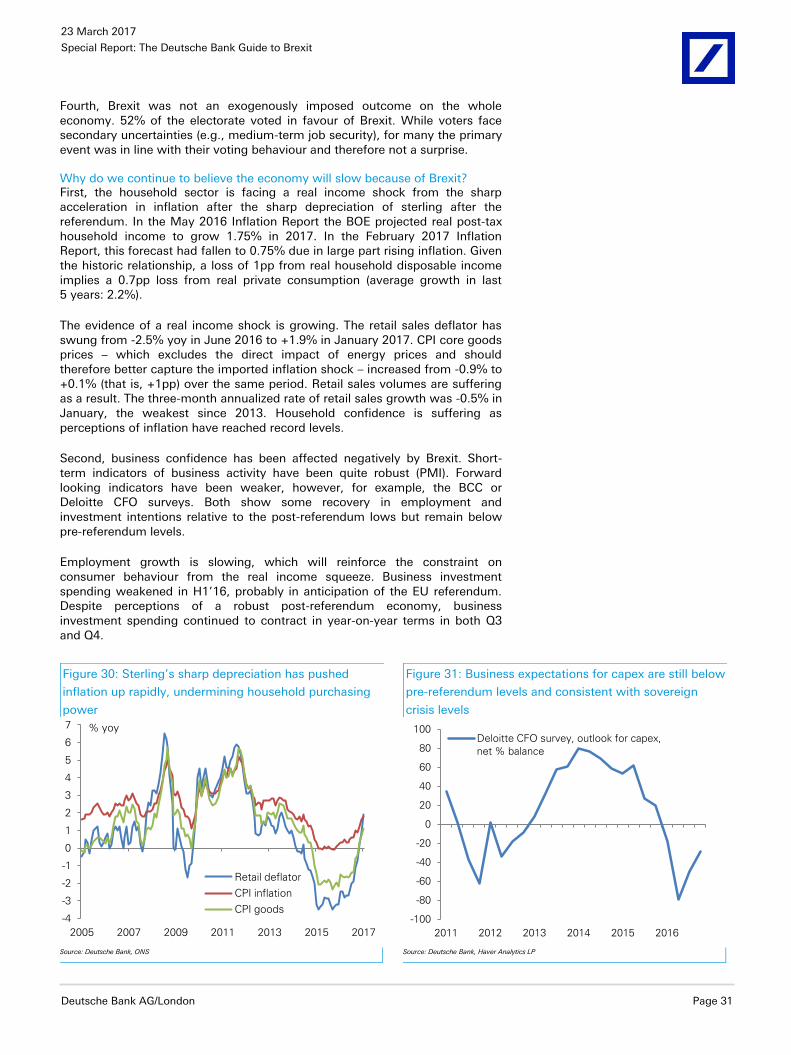

40. Why do we continue to believe the UK economy will slow?

41. Will the Bank of England have to tighten monetary policy despite Brexit?

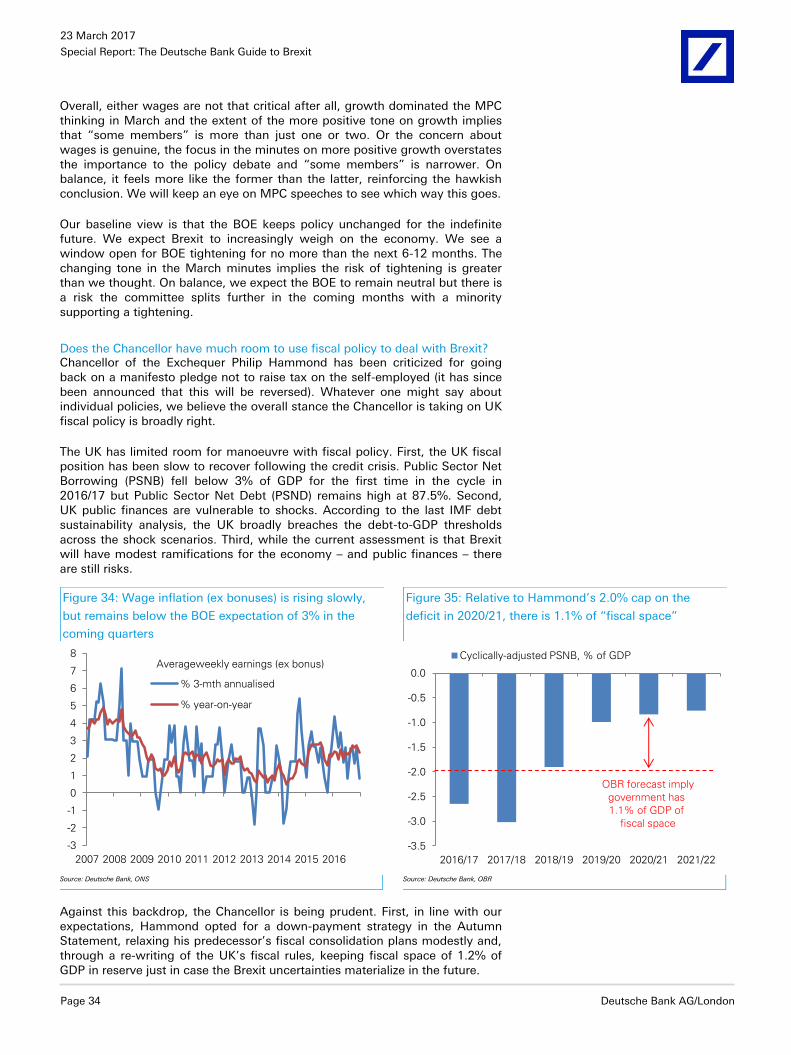

42. Does the Chancellor have much room to use fiscal policy to deal with Brexit?

43. Is the OBR’s 2% potential growth expectation too optimistic?

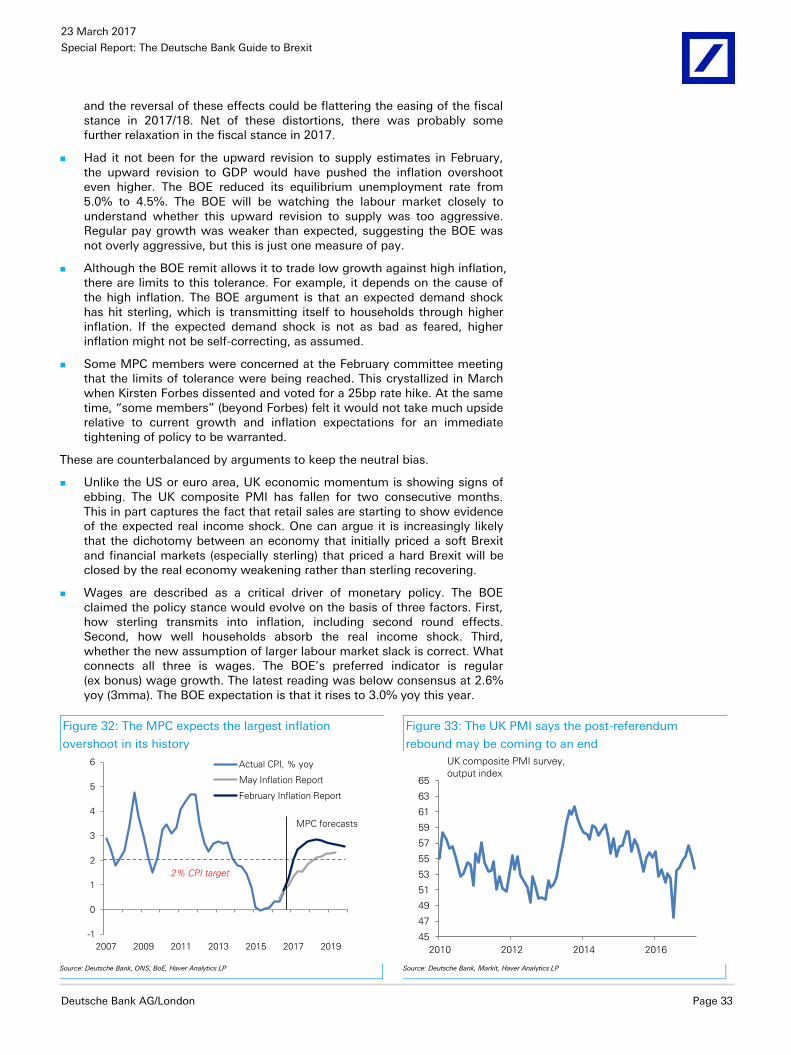

44. What are the market implications?

Conclusion, market implications and further reading pp.38-39

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 4 Deutsche Bank AG/London

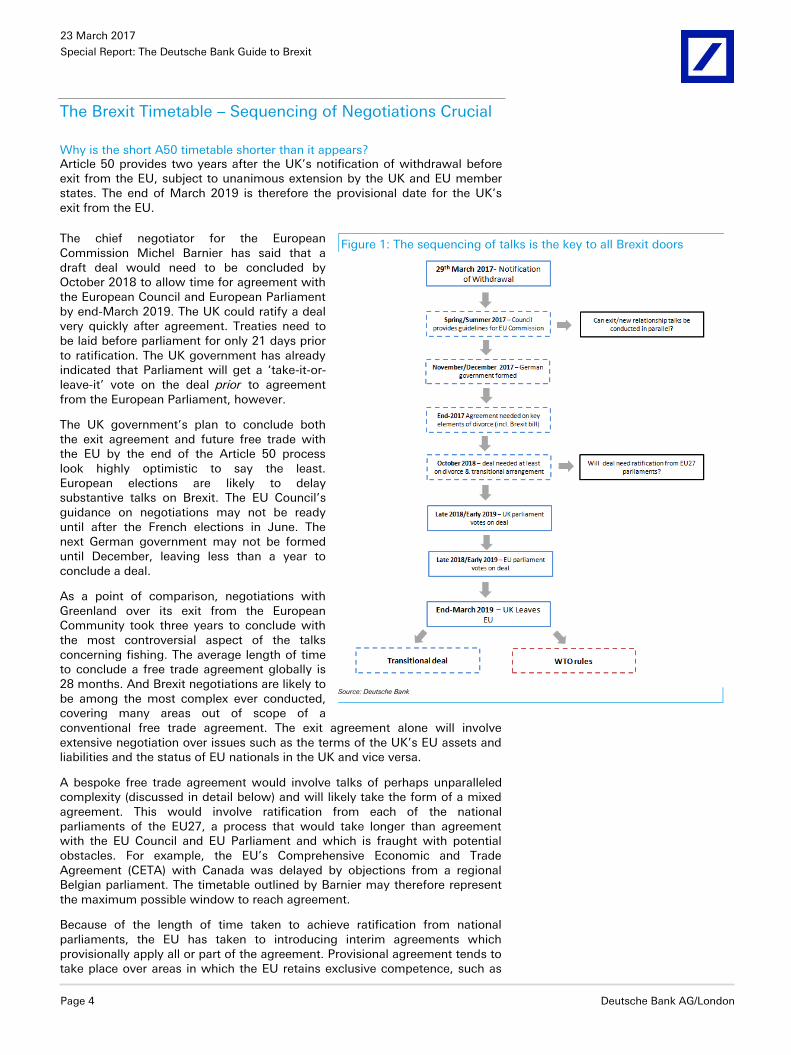

The Brexit Timetable – Sequencing of Negotiations Crucial

Why is the short A50 timetable shorter than it appears? Article 50 provides two years after the UK’s notification of withdrawal before exit from the EU, subject to unanimous extension by the UK and EU member states. The end of March 2019 is therefore the provisional date for the UK’s exit from the EU.

The chief negotiator for the European Commission Michel Barnier has said that a draft deal would need to be concluded by October 2018 to allow time for agreement with the European Council and European Parliament by end-March 2019. The UK could ratify a deal very quickly after agreement. Treaties need to be laid before parliament for only 21 days prior to ratification. The UK government has already indicated that Parliament will get a ‘take-it-or-leave-it’ vote on the deal prior to agreement from the European Parliament, however.

The UK government’s plan to conclude both the exit agreement and future free trade with the EU by the end of the Article 50 process look highly optimistic to say the least. European elections are likely to delay substantive talks on Brexit. The EU Council’s guidance on negotiations may not be ready until after the French elections in June. The next German government may not be formed until December, leaving less than a year to conclude a deal.

As a point of comparison, negotiations with Greenland over its exit from the European Community took three years to conclude with the most controversial aspect of the talks concerning fishing. The average length of time to conclude a free trade agreement globally is 28 months. And Brexit negotiations are likely to be among the most complex ever conducted, covering many areas out of scope of a conventional free trade agreement. The exit agreement alone will involve extensive negotiation over issues such as the terms of the UK’s EU assets and liabilities and the status of EU nationals in the UK and vice versa.

A bespoke free trade agreement would involve talks of perhaps unparalleled complexity (discussed in detail below) and will likely take the form of a mixed agreement. This would involve ratification from each of the national parliaments of the EU27, a process that would take longer than agreement with the EU Council and EU Parliament and which is fraught with potential obstacles. For example, the EU’s Comprehensive Economic and Trade Agreement (CETA) with Canada was delayed by objections from a regional Belgian parliament. The timetable outlined by Barnier may therefore represent the maximum possible window to reach agreement.

Because of the length of time taken to achieve ratification from national parliaments, the EU has taken to introducing interim agreements which provisionally apply all or part of the agreement. Provisional agreement tends to take place over areas in which the EU retains exclusive competence, such as

Figure 1: The sequencing of talks is the key to all Brexit doors

Source: Deutsche Bank

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 5

trade in goods and tariffs, although recent agreements between the EU and Georgia and the Ukraine were criticized as their provisional application concerned areas out of the scope of EU competence.1 The use of provisional application could shorten the time needed for the UK and EU to agree a deal.

Can parallel talks be conducted? According to Prime Minister Theresa May’s Lancaster House Speech, the UK government intends to conclude both the UK’s exit agreement and the future relationship with the EU by the end of the two-year Article 50 process. The terms of the UK’s exit from the EU and the establishment of a new relationship with the EU have been seen as legally separate agreements, although under Article 50 the exit agreement must ‘take account of the future relationship [of the leaving member state] with the union.’ The agreement on exit terms requires only a qualified majority vote in the EU Council and approval from the EU parliament, while a free trade agreement would take the form of a mixed agreement and would require unanimous approval from EU27 parliaments.

A crucial part of the UK strategy is the ability to coordinate negotiations over the two agreements in parallel. Negotiators from the EU Commission and EU Parliament have so far emphasized that the two must be sequenced one after the other. In his recent remarks to the EU parliament, Commission negotiator Barnier said no talks could take place over a future free trade deal before agreement is reached on the status of EU citizens, the UK’s financial obligations and the border arrangements with Northern Ireland.

If time runs out, could agreement be extended? Under Article 50, negotiations can be extended subject to unanimous agreement from all parties. The main problem with extension is political. There are European Elections in May 2019 and the appointment of a new European Commission. If agreement was reached to extend negotiations, the UK would be in the strange position of participating in the selection of the new EU Commission President and holding elections for the European Parliament.

Even if this obstacle were overcome, an extension of talks with the EU could prove politically disastrous for the UK government. Prime Minister May has promised that the UK will cease to be a member of the EU by 2019. The UK government is also required by law to call a new general election by May 2020. A change in government could lead to an entirely different approach to Brexit negotiations. For these reasons, an extension of negotiations is unlikely unless in the event of a significant external shock.

Is Article 50 irreversible? If UK public opinion were to change over the course of the Brexit negotiations, could the UK change its mind? The answer is unclear. Article 50 is silent on the issue and there are no precedents to draw from. In the court challenge on the UK government’s ability to trigger A50 without a parliamentary vote last October, government lawyers argued that they see Article 50 as irreversible. By contrast, Donald Tusk, president of the European Council, has said that he regards A50 as reversible, a view also shared by the head of the European Legal Service in an article in the Financial Times.2

The only institution with legal authority to rule on the matter is the ECJ. An ECJ ruling would be seen as highly political, however, given its implications for negotiations. A challenge from a British barrister in Ireland seeks to have the matter referred to the ECJ, with the case to be heard in the spring.

1 EU External Agreements: EU and UK procedures, 28th March 2016

2 “Article 50 is not forever and the UK could change its mind,” Jean-Claude Piris, FT, 1st September 2016

Figure 2: Key figures in the Brexit

process

Source: Deutsche Bank

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 6 Deutsche Bank AG/London

A Transitional Agreement – Necessary but Difficult

Given the challenge of concluding both an exit agreement and the new deal with the EU in such a short timeframe, there is increasing acknowledgement of the merits of a transitional deal to allow more time for both sides to conclude talks. We argued that an interim deal was necessary for a smooth Brexit in September, due to the timing difficulties of concluding a new deal and to mitigate the terms of trade shock for businesses both in the UK and in the EU27 if no deal was reached.

What are the positions of both sides on a transitional agreement? The Brexit White Paper described a ‘phased period of implementation…to prepare for the new arrangements’ as in the mutual interests of all parties. The Brexit Secretary David Davis has clarified that this period would merely enable the UK and EU27 time to implement an agreement rather than represent an extension of negotiations.

EU Commission negotiator Barnier has said that once broad parameters are agreed for a future relationship, a number of transitional deals may be necessary. Under this transitional period, the UK will remain subject to EU law. The EU parliament’s chief negotiator Guy Verhofstadt has said that under any transitional agreement the UK will remain fully subject to the jurisdiction of the ECJ and the EU’s four freedoms. Both Barnier and Verhofstadt’s comments stand in contrast to the UK government’s position which seeks a period where the UK’s relationship with the EU has already been fundamentally changed.

What is the difference between a transitional deal and implementation period? There is a key difference between a transitional deal and the implementation period described by the White Paper. A transitional deal acknowledges that Article 50 does not provide sufficient time to conclude a comprehensive new agreement, and provides more time to reach compromise. An implementation period implies that a deal can be concluded by March 2019 and represents a phasing in period for new arrangements.

This difference is sharply illustrated by different views on parallel talks. The UK wants talks to be conducted simultaneously on the terms of exit and a new free trade agreement. By contrast, Barnier envisages reaching a deal on the terms of exit, followed by talks on a new free trade agreement and transitional arrangements. A new free trade deal is unlikely to be concluded by March 2019, and the UK government’s strategy is therefore concerning. Either the implementation period is rhetoric designed to sooth concerns about the date of the UK’s exit from the EU, or it represents an unrealistic strategy. In the latter case, valuable time to agree on a transitional arrangement would be wasted.

What are the obstacles to a transitional deal? There are numerous obstacles to a transitional agreement. The first is timing. A transitional agreement that redefines the UK’s access to the Single Market may require treaty changes and need to be ratified by the national parliaments of all 27 different member states. Not only is this unachievable in a two year timeframe, changes to the EU treaties to accommodate a transitional deal for the UK is highly unlikely.

The second is legal. If amendments to EU Treaties are practically impossible, what would govern the UK and EU’s legal status under a transitional deal? The UK government has announced a Great Repeal Bill to translate the EU acquis into UK domestic legislation at the date of exit from the EU. This would end the

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 7

supremacy of EU law in UK courts. Some have proposed using parallel EU secondary legislation and an Act of Parliament to get around this problem.3 A transitional deal would also need to be WTO compliant. WTO rules state that interim agreements are only permissible if the nature of the future trade deal has been sketched out and the interim agreement has a specified end-date. Under Article 24 of the WTO’s General Agreement on Tariffs and Trade (GATT), any transitional arrangement would be permitted for a maximum of 10 years.

Finally, there are political problems associated with a transitional agreement. The UK has promised to leave the EU by 2019, ceasing to be part of the customs union and no longer subject to ECJ authority. It is highly unlikely EU Member States would be willing to tolerate a transitional deal in which the UK remains part of the Single Market and customs union but repeals the EU acquis through the Great Repeal Bill and ceases to be subject to ECJ rules. This was confirmed by Commission negotiator Barnier in his recent remarks to the EU parliament. If the UK were to remain subject to the ECJ, on the other hand, this would enrage eurosceptic MPs within the Conservative Party and parts of the electorate that were promised exit from the EU by 2019.

Could EEA membership be used as a transitional arrangement? One model for a transitional agreement would be EEA membership. There are some advantages associated with this option. A large part of the UK’s existing economic relationship with the EU would remain intact, with the UK retaining Single Market Access and regulatory equivalence (although not access to the customs union). The UK government would also be meeting its commitment to have left EU by 2019 and would no longer be subject to ECJ authority. EEA membership would also be consistent de jure with the government’s Great Repeal Bill, which aims to transfer legal authority from the ECJ to domestic courts, albeit de facto relevant UK legislation would still need to be compliant with EU law via the oversight of the EFTA court. The EEA also has history as a stop-gap measure. EEA membership was seen as a temporary measure for Norway prior to full accession to the EU in 1992 before the rejection of full membership in a referendum in 1994.

A crucial question is whether an exit from the EU need necessarily entail an exit from the EEA or whether the UK must separately notify the EEA under Article 127 of the EEA Treaty. Legal opinion differs on this subject. The UK government has argued that the UK’s membership of the EEA derives from its membership of the EU, although this is a matter of dispute. 4 If the UK government is right, the UK would have to re-join EFTA as a third country, agree to the surveillance mechanism of the EEA and sign up to the EFTA court. This would require unanimous approval from existing EEA states. According to some experts, this process would take up to a year.5

An additional problem is that senior Brexit ministers have ruled out the prospect of EEA membership, arguing that it would represent a continuum of EU membership, including freedom of movement of labour. As we have argued previously, Article 112 of the EEA Treaty does provide scope for unilateral restrictions on the four freedoms, and could potentially be politically sellable as an alternative to EU membership, but this view does not appear to be shared by UK ministers.

3 University of Oxford, “How to Make a Transitional Brexit Arrangement,” Pavlos Eleftheriadis, 15th

February 2017 4 LSE blog: How Article 127 of the EEA Agreement could keep the UK in the Single Market, Gavin Barrett,

5 Brexit, “The Options for Trade,” House of Lords Select Committee

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 8 Deutsche Bank AG/London

Finally, approval for the UK’s reentry to the EEA should not be taken for granted either from existing EEA member states or the EU. The UK would be by far the largest economy in the EEA and could be seen as upsetting the power balance of the existing agreement. The EU could also perceive the UK’s entry into the EEA as undermining the solidarity of the EU; representing the thin end of the wedge for a larger exodus of EU member states into a ‘half-in, half-out’ option.

How could a transitional deal be constructed? If EEA membership is off the table, at a minimum the UK should seek an arrangement covering continued access to the customs union and some form of equivalence for financial services. The hurdle for the customs union may be lower, as it falls under the exclusive competence of the EU and therefore may not require revisions to the treaties or ratification from national parliaments. A broader transitional deal on services will be much more difficult to achieve for the opposite reason.

A transitional deal will be difficult to achieve but not impossible. The advantages of a transitional deal are manifold given the costs to both sides of a ‘cliff-edge’ exit from the EU in early-2019.

Any transitional deal will have to meet several criteria: have a pre-defined end-point, clearly sketch out the UK’s future relationship with the EU after the transitional period and be an ‘off-the-shelf’ rather than bespoke solution. The more complex the transitional deal, the less likely it is to be concluded. The legal basis for a transitional deal is established in the WTO and could be quickly ratified by the UK parliament, leaving EU law as the main obstacle. The question is whether a transitional deal could be signed-off without changes to EU treaties. With respect to the customs union at least, this could be possible. But the quid pro quo will be a constructive resolution of the UK’s financial liabilities to the EU (discussed in more detail below) as well as compromise on ECJ oversight. Most importantly, an attempt to conclude a comprehensive new relationship with the EU27 should not take precedence over settling the conditions for a transitional deal, or valuable time will be lost.

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 9

Negotiating the divorce – A Messy Settlement

What are the main contents of the divorce negotiations? The UK’s exit negotiations will cover the status of the UK’s financial assets and liabilities in the EU, the rights of EU citizens living in the UK and vice versa, common security arrangements such as the European Arrest Warrant (EAW), the UK’s participation in EU agencies and regulatory bodies such as the European Medicines Agency, the European Markets and Securities Agency and the European Investment Bank and border arrangements between Northern Ireland and the Republic of Ireland.

A future free trade deal is legally separate agreement and would cover the UK’s future economic relationship with the EU. Reports indicate that Commission negotiator Barnier envisages the negotiations between the UK and EU will be three tiered; agreement on the terms of the divorce, the transitional deal and a future free trade agreement. As we will see below, in practical terms it will be difficult to separate the three entirely.

How high is the UK’s divorce settlement bill likely to be? One of the earliest and most contentious areas of negotiations surrounds the status of the UK’s assets and liabilities in the EU. The so-called ‘divorce bill’ concerns the net liabilities that the UK has built up as part of its membership of the EU. According to press reports, the European Commission has settled on a figure of around GBP 50bn that the UK will need to pay for its exit agreement with the EU.6

According to analysis from the Centre for European Reform, the UK’s liabilities to the EU can be split into reste á liquidier unpaid budget appropriations (RAL), national allocations of investment spending for 2014-20 Multiannual Financial Framework (MFF) and the costs of the pension promises to EU officials.7 This is partly offset by the UK’s share of the EU’s assets, including property plant and equipment, the rebate and assets available for sale.

Within this framework, the assumptions governing the UK’s ultimate net liabilities are highly controversial. These include, among others, whether the UK’s liabilities are measured on the basis of its average gross contribution to the EU budget (15% of EU liabilities) or including the UK’s EU budget rebate (closer to 12%), how the UK’s share of the EU’s assets is calculated, whether the UK is responsible for the pension liabilities of its own citizens or should make a contribution based on its share of EU budget contributions, whether the UK should be responsible for the EU’s contingent liabilities and what the cut-off date is for the UK’s continuing liabilities under the EU budget’s unpaid budget allocations.

Why is the divorce bill likely to prove so contentious? The discussions are likely to prove politically contentious because rows over the UK’s budget contributions to the EU have been one of the recurring motifs of its membership. Among areas of potential disagreement include over the differing accounting methods between the EU (unfunded commitments), and UK (accruals basis) and pension liabilities. The Pension Scheme for European Officials (PESO) is run on an unfunded basis and is generous compared to other comparable schemes.

Nor can negotiations over the budget be separated from other aspects of the negotiations. For example, if the UK were to remain part of elements of the customs union, at least as part of a transitional agreement, agreement would

6 “European Commission ‘agrees GBP 48bn Brexit Bill” Independent, 10th February 2017

7 “The EUR60bn Brexit Bill,” Alex Barker, CER, February 2017

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 10 Deutsche Bank AG/London

need to be reached on the share of customs duties collected by the UK and EU. According to the government’s White Paper, the UK may also wish to remain part of specific EU programs, in which case it would continue to make financial contributions.

In terms of the enforceability of the EU’s claims on the UK, the House of Lords has concluded that if the UK were to leave the EU without a deal, it would not be liable for outstanding financial obligations.8 This would leave net budget contributors such as Germany or net budget recipients such as Poland, to foot the bill. As a share of gross national income, the additional burden would still be small, however, with previous Deutsche Bank research calculating an additional burden of just 0.09% of Germany’s GDP. The EU27 may conclude that the costs of no deal being reached for the UK would be far higher.

In short, negotiations over the UK’s divorce bill represent one of the largest risks to an agreement with the EU27. The wide range of estimates concerning the Brexit bill (between GBP 20bn to 60bn), the ample scope for interpretation over the UK’s commitments and the politically toxic nature of the debate, with the UK’s budget contributions featuring heavily in the referendum campaign and Prime Minister May having promised that significant payments to the EU budget were over, offer plenty of scope for a disorderly outcome.

Regardless, the UK will have to pay up one way or another. Under an EEA-style agreement or continued access to the customs union, the UK will have to make contributions to EU funds. If the UK were to walk away from its financial commitments, the prospects of a constructive outcome in EU talks would be slim to non-existent, and the cost would be felt through loss of trade. A GBP 50bn bill is roughly equivalent to four years continued EU membership. A deal on the EU budget could be sold politically as the price paid to reach a transitional agreement with the EU27.

Why are EU citizens rights not guaranteed after Brexit? Financial commitments will not be the only contentious area of negotiations. Another could surround the rights of EU citizens currently resident in the UK and UK citizens in the EU. The concept of ‘acquired rights’ under existing freedom of movement laws has come under increasing scrutiny since the referendum. The House of Lords has concluded the rights of citizens would need to be protected in the withdrawal agreement and given effect in the legal systems of both the UK and EU27.

Both the UK government and EU27 have signaled their willingness to reach a compromise on this issue, but neither has declared it will unilaterally protect the rights of each other’s citizens after Brexit. Partly, this is due to the politics of negotiations. The UK government sought assurances from the EU27 over citizens’ rights in December but was rebuffed on the basis that no pre-negotiations would take place before the UK had triggered Article 50.

There are several practical barriers to concluding a deal on EU citizens rights. In the first place, it may be difficult for EU citizens resident in the UK and vice versa to establish proof of residence. The UK’s current process for establishing residence involves an 85 page form and much supporting evidence which may prove impractical in the rush for EU citizens to establish proof of residence. A related point is when the cut-off date for current EU citizens’ rights is deemed to be. Recently, there has been speculation that the date for triggering Article 50 will be used as the cut-off for EU citizens to enjoy existing rights as part of their membership of the EU.

8 “Brexit and the EU budget,” House of Lords European Union Committee, 15th Report Session

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 11

This aspect of negotiations is inherently linked to a transitional agreement and the future of the UK’s relationship with the EU. For example, if under a transitional agreement the UK will continue to need to abide by the EU’s freedom of movement laws, there will need to be clarification over the legal status of EU27 citizens arriving under the transitional period.

What are the other aspects of the divorce negotiations? While the divorce bill and EU citizens’ rights are the most headline-grabbing of the exit negotiations, other aspects of the divorce negotiations are by no means trivial. These include the future of the UK’s position in security arrangements such as the EAW, participation in regulatory bodies and the future of the frictionless border between the Republic of Ireland (in the EU) and Northern Ireland (part of the UK). The status of the UK in EU regulatory bodies is of particular economic importance as many are linked to participation in the Single Market and the low non-tariff barriers UK industries enjoy. For example, participation in the European Medicines Agency ensures fast track approval of UK pharmaceutical exports across the EU.

A new deal for Britain and the EU - Costs and Benefits

What are the trade options for the UK with the EU after Brexit? Future trade options for the UK with the EU after Brexit can broadly be split into three alternatives: a close to status quo arrangement, a bespoke free trade deal and WTO rules.

Status quo: This would keep the UK’s current terms of trade with the EU intact as far as possible, and seek to replicate existing economic arrangements. The most obvious legal model would be continued membership of the EEA, in which the UK would continue to abide by the EU’s four freedoms of capital, labor, goods and services with a potential emergency brake. A status quo arrangement is only likely as part of a transitional deal as without a say in EU institutions, the UK will become a taker rather than giver of EU legislation and regulatory priorities could diverge over time. EEA membership does not entail UK inclusion in the EU customs union. A separate deal would be required in order to ensure continued access. Another form of status quo arrangement was proposed by Jean Pisani-Ferry and Norbert Rottgen among others on the blog Bruegel.9 This envisaged the UK entering into a continental partnership with the EU, in which the UK would continue to be part of the Single Market but with a quota system on migrants from the EU.

Bespoke arrangement: A bespoke trade agreement is the UK government’s preferred option for Brexit. According to the White Paper, the UK government will seek ‘an ambitious and comprehensive Free Trade Agreement and a new customs agreement’ with the EU. A bespoke arrangement could be analogous to the CETA deal concluded between the EU and Canada this year, which sees a reduction in tariffs and non-tariff barriers in goods but has more limited scope in services.

WTO rules: A third option for the UK after Brexit is full exit from the Single Market and the customs union and the UK adopting the multilateral framework of the WTO to conduct its trade with the EU. This would involve the UK being subject to the EU’s common external tariff and rules of origin checks. It would also mean no access to the Single Market in services. We discuss the merits and difficulties of the each option in more detail below.

9 “Europe after Brexit: A proposal for a continental partnership,” Breugel, 29th August 2016

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 12 Deutsche Bank AG/London

What is the economically least disruptive option? None of the UK’s potential future trade relations with the EU are economically costless, but some will be more disruptive than others.

The Institute of Directors has argued that a loss of customs union access would be the most economically disruptive outcome for UK businesses in the short term. Firms trading goods would feel an immediate impact of customs checks and tariffs, while services firms would feel the loss of Single Market Access only on a more ad-hoc basis. It is important to note that a loss of customs union access is important not because of the outright level of tariffs (which are relatively low), but because of much higher non-tariff barriers which relate to the Single Market’s harmonized regulatory regime, as well as the disruption caused at points of entry by the required checks on rules of origin and tariffs. In previous analysis, which focused on the impact only of tariffs, we calculated that the UK’s trade in goods with the EU would fall by around GBP 50bn in the event of the UK dropping out of the customs union.

In the medium-term, the UK’s loss of Single Market Access in services is likely to be more damaging. As shown by Figure 3, the UK’s comparative advantage is overwhelmingly concentrated in services industries. Thirty five percent of the UK’s services exports are destined for the EU, with the share larger in specific industries (40% in financial services). Non-tariff barriers in services are higher than tariffs on goods. One example is the ability of UK-based banks to passport into the EU. In previous research, we calculated that the costs to UK services trade with the EU under WTO rules would be in the region of GBP 20bn.

The picture for services is less clear in the long-term, however. If the UK were to remain a member of the Single Market in services, but lose its voice in EU

Figure 3: The UK’s comparative advantage is overwhelmingly concentrated in

services industries

Source: Deutsche Bank, UN Comtrade, International Trade Centre *revealed comparative advantage calculated as the share of a sector in total UK exports/share of the same sector in global exports. For more information, see World Bank trade indicators. Revealed comparative advantage calculations give numbers greater than or less than 1. For visual purposes, numbers less than one are shown here as negative

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 13

decision making, it would give up its ability to influence EU rule-making. The future of the UK as a taker rather than a giver of regulation could be prejudicial for the long term success of sectors such as financial services.

As well as trading arrangements, negotiations on the freedom of movement of workers between the UK and EU will be very important. EU citizens currently enjoy near frictionless access to the UK labor market. As we argued in a recent special report, this has been a fundamental driver of recent UK jobs growth and has papered over weakening demographic trends. Freedom of movement of labour is often seen as a political issue in the context of Brexit negotiations, but the more restrictive future arrangements between the UK and EU labour markets are, the more economically disruptive the outcome will be.

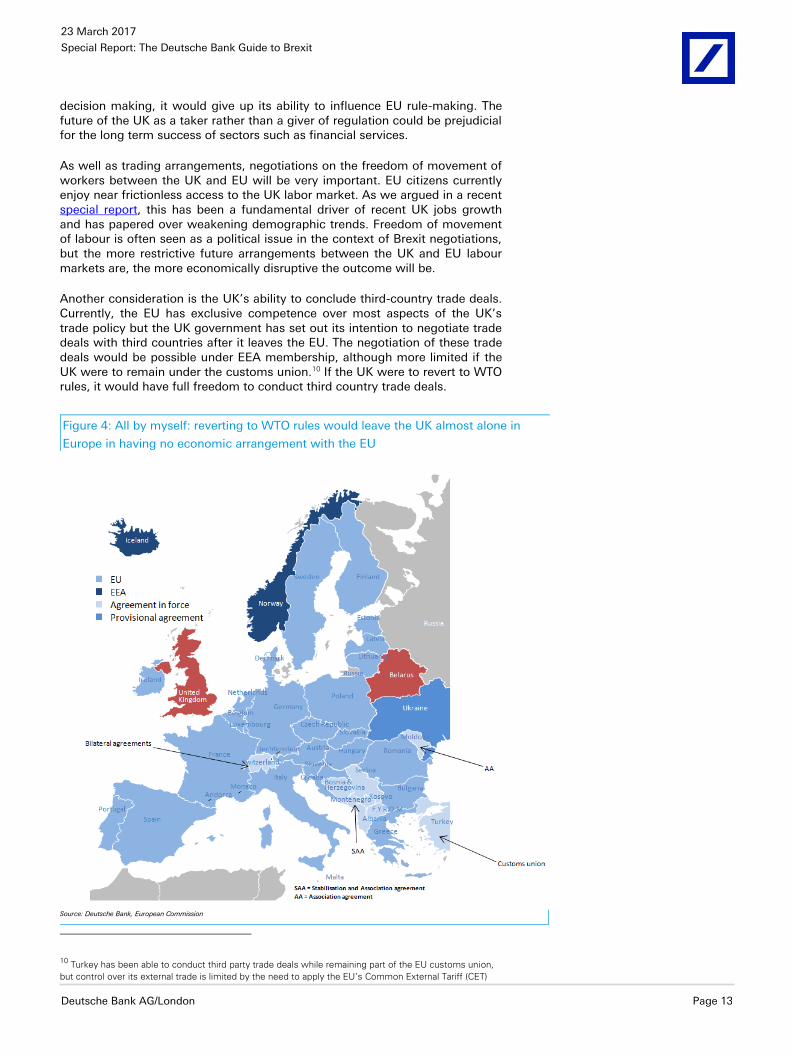

Another consideration is the UK’s ability to conclude third-country trade deals. Currently, the EU has exclusive competence over most aspects of the UK’s trade policy but the UK government has set out its intention to negotiate trade deals with third countries after it leaves the EU. The negotiation of these trade deals would be possible under EEA membership, although more limited if the UK were to remain under the customs union.10 If the UK were to revert to WTO rules, it would have full freedom to conduct third country trade deals.

10 Turkey has been able to conduct third party trade deals while remaining part of the EU customs union,

but control over its external trade is limited by the need to apply the EU’s Common External Tariff (CET)

Figure 4: All by myself: reverting to WTO rules would leave the UK almost alone in

Europe in having no economic arrangement with the EU

Source: Deutsche Bank, European Commission

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 14 Deutsche Bank AG/London

The least economically disruptive option would be a status quo arrangement based on EEA membership plus a separate deal on the customs union that allows UK companies to continue frictionless trade. Such a deal would also include continued free access for EU migrants into the UK labour market. The second least disruptive option would be no EEA agreement, or broad agreement on services, but continued access to the customs union.

The third least disruptive option would be a free trade agreement along the lines of CETA. This would not cover either Single Market access in services or solve the issue of border checks for goods although there may be some ways of mitigating the effects of the latter, such as signing up to the common transit procedure convention.11 Under a free trade agreement the UK is also likely to have more leeway to negotiate over freedom of movement of workers, although the introduction of significant barriers to reciprocal labour market access with the EU would be disruptive.

No trade deal would likely be very damaging to the UK’s current economic model. As shown by figure 4, the UK would also be alone in Europe in not pursuing some kind of trade deal with the EU, the world’s largest single market. We do not see the advantages of a deal with the EU as being even partially offset by the increased optionality provided by the ability to conduct third party trade deals. This is discussed in more detail in the section on third country trade below.

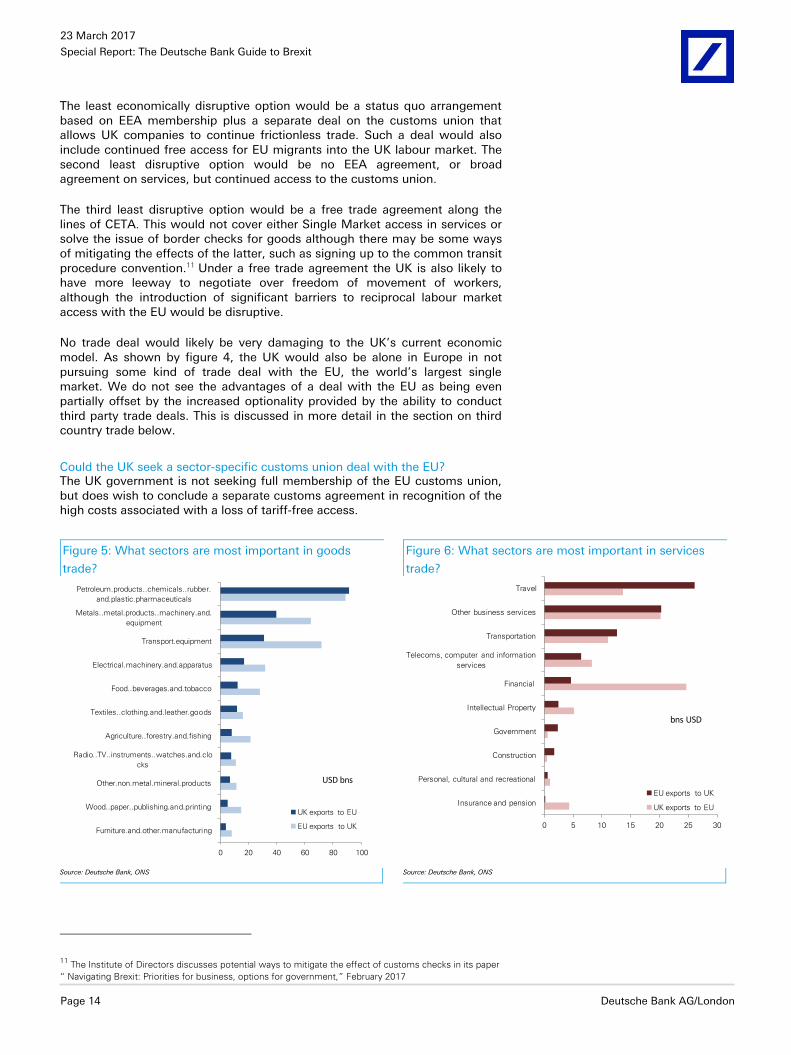

Could the UK seek a sector-specific customs union deal with the EU? The UK government is not seeking full membership of the EU customs union, but does wish to conclude a separate customs agreement in recognition of the high costs associated with a loss of tariff-free access.

11 The Institute of Directors discusses potential ways to mitigate the effect of customs checks in its paper

“ Navigating Brexit: Priorities for business, options for government,” February 2017

Figure 5: What sectors are most important in goods

trade?

Figure 6: What sectors are most important in services

trade?

0 20 40 60 80 100

Furniture.and.other.manufacturing

Wood..paper..publishing.and.printing

Other.non.metal.mineral.products

Radio..TV..instruments..watches.and.clo

cks

Agriculture..forestry.and.fishing

Textiles..clothing.and.leather.goods

Food..beverages.and.tobacco

Electrical.machinery.and.apparatus

Transport.equipment

Metals..metal.products..machinery.and.

equipment

Petroleum.products..chemicals..rubber.

and.plastic.pharmaceuticals

USD bns

UK exports to EU

EU exports to UK

0 5 10 15 20 25 30

Insurance and pension

Personal, cultural and recreational

Construction

Government

Intellectual Property

Financial

Telecoms, computer and information

services

Transportation

Other business services

Travel

bns USD

EU exports to UK

UK exports to EU

Source: Deutsche Bank, ONS Source: Deutsche Bank, ONS

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 15

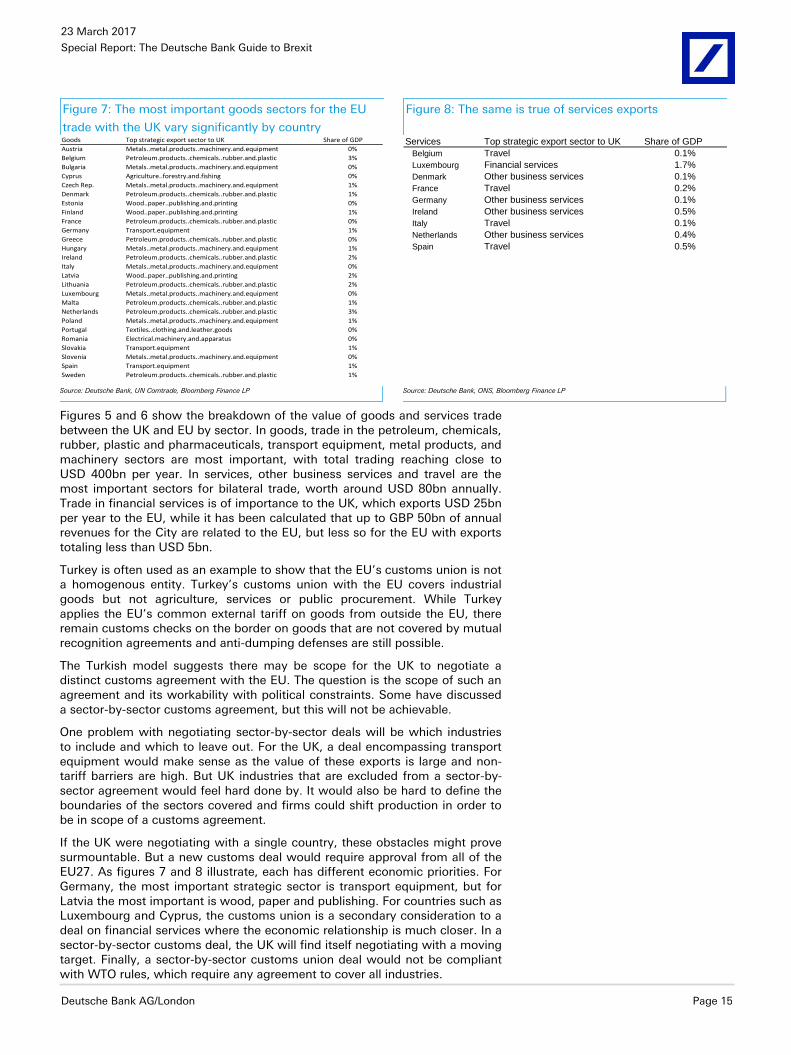

Figures 5 and 6 show the breakdown of the value of goods and services trade between the UK and EU by sector. In goods, trade in the petroleum, chemicals, rubber, plastic and pharmaceuticals, transport equipment, metal products, and machinery sectors are most important, with total trading reaching close to USD 400bn per year. In services, other business services and travel are the most important sectors for bilateral trade, worth around USD 80bn annually. Trade in financial services is of importance to the UK, which exports USD 25bn per year to the EU, while it has been calculated that up to GBP 50bn of annual revenues for the City are related to the EU, but less so for the EU with exports totaling less than USD 5bn.

Turkey is often used as an example to show that the EU’s customs union is not a homogenous entity. Turkey’s customs union with the EU covers industrial goods but not agriculture, services or public procurement. While Turkey applies the EU’s common external tariff on goods from outside the EU, there remain customs checks on the border on goods that are not covered by mutual recognition agreements and anti-dumping defenses are still possible.

The Turkish model suggests there may be scope for the UK to negotiate a distinct customs agreement with the EU. The question is the scope of such an agreement and its workability with political constraints. Some have discussed a sector-by-sector customs agreement, but this will not be achievable.

One problem with negotiating sector-by-sector deals will be which industries to include and which to leave out. For the UK, a deal encompassing transport equipment would make sense as the value of these exports is large and non-tariff barriers are high. But UK industries that are excluded from a sector-by-sector agreement would feel hard done by. It would also be hard to define the boundaries of the sectors covered and firms could shift production in order to be in scope of a customs agreement.

If the UK were negotiating with a single country, these obstacles might prove surmountable. But a new customs deal would require approval from all of the EU27. As figures 7 and 8 illustrate, each has different economic priorities. For Germany, the most important strategic sector is transport equipment, but for Latvia the most important is wood, paper and publishing. For countries such as Luxembourg and Cyprus, the customs union is a secondary consideration to a deal on financial services where the economic relationship is much closer. In a sector-by-sector customs deal, the UK will find itself negotiating with a moving target. Finally, a sector-by-sector customs union deal would not be compliant with WTO rules, which require any agreement to cover all industries.

Figure 7: The most important goods sectors for the EU

trade with the UK vary significantly by country

Figure 8: The same is true of services exports

Goods Top strategic export sector to UK Share of GDP

Austria Metals..metal.products..machinery.and.equipment 0%

Belgium Petroleum.products..chemicals..rubber.and.plastic 3%

Bulgaria Metals..metal.products..machinery.and.equipment 0%

Cyprus Agriculture..forestry.and.fishing 0%

Czech Rep. Metals..metal.products..machinery.and.equipment 1%

Denmark Petroleum.products..chemicals..rubber.and.plastic 1%

Estonia Wood..paper..publishing.and.printing 0%

Finland Wood..paper..publishing.and.printing 1%

France Petroleum.products..chemicals..rubber.and.plastic 0%

Germany Transport.equipment 1%

Greece Petroleum.products..chemicals..rubber.and.plastic 0%

Hungary Metals..metal.products..machinery.and.equipment 1%

Ireland Petroleum.products..chemicals..rubber.and.plastic 2%

Italy Metals..metal.products..machinery.and.equipment 0%

Latvia Wood..paper..publishing.and.printing 2%

Lithuania Petroleum.products..chemicals..rubber.and.plastic 2%

Luxembourg Metals..metal.products..machinery.and.equipment 0%

Malta Petroleum.products..chemicals..rubber.and.plastic 1%

Netherlands Petroleum.products..chemicals..rubber.and.plastic 3%

Poland Metals..metal.products..machinery.and.equipment 1%

Portugal Textiles..clothing.and.leather.goods 0%

Romania Electrical.machinery.and.apparatus 0%

Slovakia Transport.equipment 1%

Slovenia Metals..metal.products..machinery.and.equipment 0%

Spain Transport.equipment 1%

Sweden Petroleum.products..chemicals..rubber.and.plastic 1%

Services Top strategic export sector to UK Share of GDP

Belgium Travel 0.1%

Luxembourg Financial services 1.7%

Denmark Other business services 0.1%

France Travel 0.2%

Germany Other business services 0.1%

Ireland Other business services 0.5%

Italy Travel 0.1%

Netherlands Other business services 0.4%

Spain Travel 0.5%

Source: Deutsche Bank, UN Comtrade, Bloomberg Finance LP Source: Deutsche Bank, ONS, Bloomberg Finance LP

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 16 Deutsche Bank AG/London

What other obstacles are there to access to the customs union? Other difficulties concern the ability to square a deal on the customs union with political constraints. Turkey is not subject to the direct supervision of the ECJ, with disputes governed by a common resolution mechanism, although in practice the country has incorporated much relevant EU legislation into Turkish law in order to remove technical barriers to trade. Whatever agreement the UK reaches with the EU, however, will necessarily involve some pooling of sovereignty as every international trade deal incorporates some form of joint dispute resolution.

A further question will be the status of the UK in third country free trade deals. By entering into a customs union with the EU, the UK would have to accept the EU’s common external tariff (CET) for goods from outside the EU, which would reduce, although not eliminate, its scope for third country trade deals. Turkey has also found itself bound by third country trade agreements agreed by the EU, but with little input into their negotiation, although the country has introduced some border checks on imports from third countries such as Mexico and South Africa to defend domestic producers.12

How could a customs union deal be constructed? A customs union deal between the UK and EU, at least in the short term, will be tricky but not impossible. The EU’s relationship with Turkey shows that the customs union is not inherently part of the Single Market. The starting point is also a major positive in that UK product standards are already harmonized with the EU. The main issue concerns the ability of the UK to pick and choose elements of the customs union under a sector-by-sector deal. This will prove challenging due to the conflicting interests of different sectors and countries. As per negotiations over a transitional deal, then, any deal over the customs union should focus on the scope to leverage an existing relationship as opposed to using up time rewriting the rules.

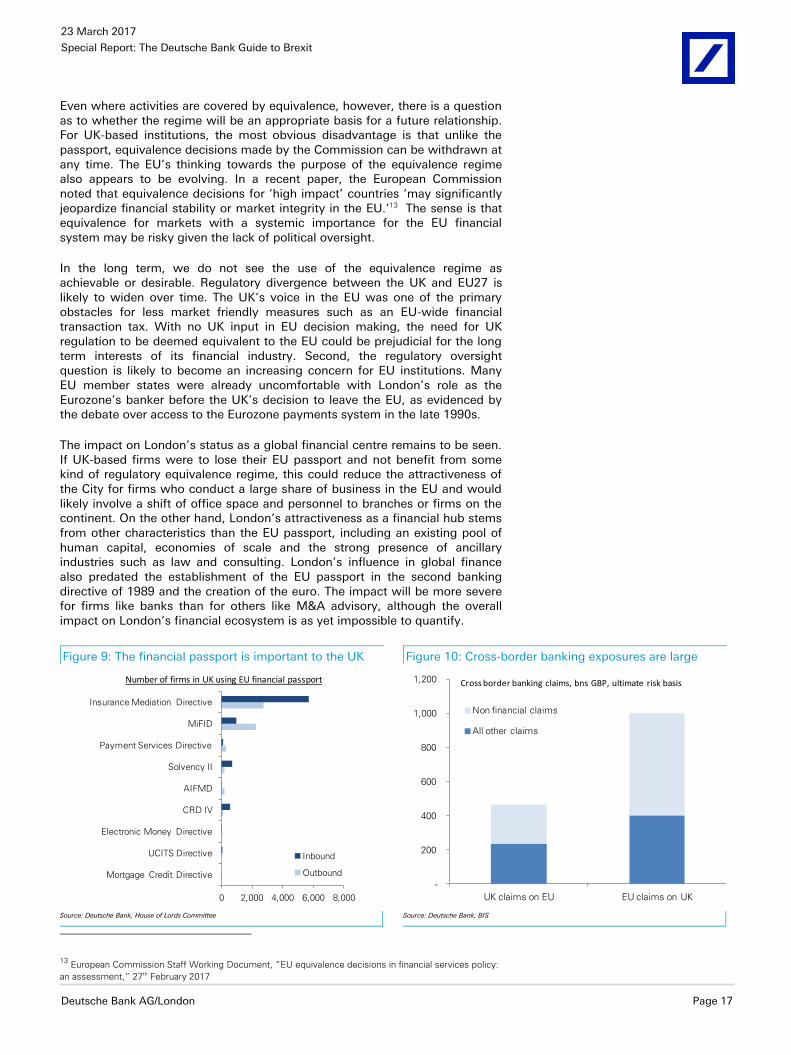

What kind of deal could be reached for financial services? One area of negotiations that has dominated Brexit headlines is financial services. Financial services are one of the most important sectors of the UK economy, and a large proportion of revenues are linked to trade with the EU. The UK is also important to the EU’s financial system. London is the largest centre for the trading and clearing of euro derivatives, for example, and processes a third of wholesale banking for large EU companies.

One of the main issues concerns the EU’s passport, under which firms are able to provide financial services in the Single Market either directly from their home country, or via branches, without a separately regulated subsidiary. Passporting is only possible as part of EU or EEA membership. If the UK were to leave both, UK-based firms would be subject to the EU’s third-country equivalence regime. This allows third-country firms to operate on similar terms, but covers a smaller range of financial activities, is subject to European Commission approval (and withdrawal) and generally provides more limited market access.

The scope of the EU’s third party equivalence regime and therefore importance of the EU passport is heavily Balkanized across different types of financial services. Investment services, including sales and trading, are covered under MiFID II/MiFIR, as are reinsurance activities under Solvency II and fund management under AIFMD. Retail banking and deposit taking are not as CRD IV does not contain an equivalence regime for these activities.

12 Evaluation of the EU-Turkey Customs Union, World Bank, March 28th 2014

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 17

Even where activities are covered by equivalence, however, there is a question as to whether the regime will be an appropriate basis for a future relationship. For UK-based institutions, the most obvious disadvantage is that unlike the passport, equivalence decisions made by the Commission can be withdrawn at any time. The EU’s thinking towards the purpose of the equivalence regime also appears to be evolving. In a recent paper, the European Commission noted that equivalence decisions for ‘high impact’ countries ‘may significantly jeopardize financial stability or market integrity in the EU.’13 The sense is that equivalence for markets with a systemic importance for the EU financial system may be risky given the lack of political oversight.

In the long term, we do not see the use of the equivalence regime as achievable or desirable. Regulatory divergence between the UK and EU27 is likely to widen over time. The UK’s voice in the EU was one of the primary obstacles for less market friendly measures such as an EU-wide financial transaction tax. With no UK input in EU decision making, the need for UK regulation to be deemed equivalent to the EU could be prejudicial for the long term interests of its financial industry. Second, the regulatory oversight question is likely to become an increasing concern for EU institutions. Many EU member states were already uncomfortable with London’s role as the Eurozone’s banker before the UK’s decision to leave the EU, as evidenced by the debate over access to the Eurozone payments system in the late 1990s.

The impact on London’s status as a global financial centre remains to be seen. If UK-based firms were to lose their EU passport and not benefit from some kind of regulatory equivalence regime, this could reduce the attractiveness of the City for firms who conduct a large share of business in the EU and would likely involve a shift of office space and personnel to branches or firms on the continent. On the other hand, London’s attractiveness as a financial hub stems from other characteristics than the EU passport, including an existing pool of human capital, economies of scale and the strong presence of ancillary industries such as law and consulting. London’s influence in global finance also predated the establishment of the EU passport in the second banking directive of 1989 and the creation of the euro. The impact will be more severe for firms like banks than for others like M&A advisory, although the overall impact on London’s financial ecosystem is as yet impossible to quantify.

13 European Commission Staff Working Document, “EU equivalence decisions in financial services policy:

an assessment,” 27th February 2017

Figure 9: The financial passport is important to the UK Figure 10: Cross-border banking exposures are large

0 2,000 4,000 6,000 8,000

Mortgage Credit Directive

UCITS Directive

Electronic Money Directive

CRD IV

AIFMD

Solvency II

Payment Services Directive

MiFID

Insurance Mediation Directive

Number of firms in UK using EU financial passport

Inbound

Outbound

-

200

400

600

800

1,000

1,200

UK claims on EU EU claims on UK

Cross border banking claims, bns GBP, ultimate risk basis

Non financial claims

All other claims

Source: Deutsche Bank, House of Lords Committee Source: Deutsche Bank, BIS

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 18 Deutsche Bank AG/London

Why is a transitional deal important for financial services? The relationship between the UK and EU in financial services is likely to change significantly in the long-run, but a transitional agreement is in the mutual interests of both the EU and UK.

The legal uncertainty created for firms in the EU by a cliff-edge Brexit in which current passporting arrangements cease to function could negatively impact financial stability.14 The debate about the future of the UK’s status as the centre of euro derivative trading and clearing goes to the heart of this issue. The UK’s success in challenging the ECB’s attempt to relocate large-scale euro derivative clearing to the Eurozone in 2011 would have been impossible without the UK’s membership of the EU. Brexit therefore raises the prospect that Eurozone authorities could renew attempts to relocate euro clearing outside of London. But economies of scale are fundamental to the clearing business, and a revocation of London-based CCPs authorization to provide clearing services without alternative arrangements could cause a drying up of liquidity in euro-denominated derivatives.

Another concern is over wholesale banking. The UK is the leading centre in the EU for wholesale banking. BIS data in figure 10 shows around GBP 500bn of UK cross-border banking claims on EU countries and GBP 1,000 trillion EU claims on the UK, of which non financial claims amount to GBP 600bn. One estimate of the time banks will need to relocate has been calculated at two years, although this will vary significantly by how well established banks are already in the EU27. If wholesale activities are not covered by an equivalence declaration under MiFID and MiFIR, this could lead to a sudden relocation of activities to the continent and result in a lending bottleneck.

A managed transition in financial services is therefore in the best interests of both the UK and EU. This could involve an early commitment to maintain regulatory equivalence for defined activities for a specified period of time after the UK leaves the EU in March 2019, perhaps including the establishment of a joint financial regulatory committee as proposed by Open Europe, to ensure a regular dialogue between regulators. This would give financial firms a longer window in which to plan for changes to the UK and EU’s current relationship.

What about a deal other service industries? The financial sector is not the only services industry that would be affected by a loss of Single Market Access. Over thirty percent of UK exports are made up of non-financial services. Despite justified criticism, the EU has made large strides in lowering barriers to trade in services. Many UK companies benefit from harmonized regulations across the EU, rights of establishment and access to skilled labour through freedom of movement.

Other business services make up the largest share of UK exports to the EU after finance. This encompasses legal, accounting, consultancy and public relations professions among others. A loss of Single Market access could be very prejudicial to firms that benefit from freedom of establishment under the EU Services Directive. Another key export sector for the UK is information and communication. As the House of Lords noted, the contribution of digital services to UK growth is likely understated in GDP data.15 Among many issues facing the digital industry after Brexit will be an adequacy decision on data protection standards that allows data to travel freely between the UK and EU

14 In evidence to the TSC Committee Bank of England Governor Mark Carney noted that the UK’s financial

sector played an important role in the EU’s financial system. A sharp break in that liquidity and support

could be detrimental to financial stability in the EU. See BBC “Carney warns EU on risks of Brexit,” 11th

January 2011 15

“Brexit: trade in non-financial services,” House of Lords European Union Committee, 14th March 2017

Figure 11: How is trade regulated

across the EU?

Source: Deutsche Bank

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 19

and continued access to high skilled labour from the EU. Transport is the next most important sector for UK services exports. The success of the UK budget airlines industry is closely tied to efforts to liberalize air travel across the EU. The Single Aviation Market enables UK airlines to fly without restriction across the EU and within EU countries. The EU-US bilateral Open Skies agreement has extended this to US routes. Neither agreement would apply after the UK’s exit from the EU. This is far from comprehensive. For telecommunications, the abolition of roaming charges by mobile operators in the EU would cease to apply, unless reestablished under a new free trade agreement. For the creative services industry, broadcasters would no longer be able to rely on a domestic license to broadcast throughout the EU.

Any decision on continued access to the Single Market in services is not under EU competence. A deal will require a mixed agreement and ratification from the national parliaments of each the EU27. A transitional deal on non-financial services will therefore be difficult to achieve. Even with a free trade deal, it is very unlikely the UK will continue to enjoy its current market access as many forms of services trade are excluded from free trade agreements. The loss of access should not be underestimated. The NIESR have calculated that with no deal, the UK would face a 60% loss in services exports to the EU. Non-financial services have been seen as a key driver of future jobs growth. The lack of UK participation in EU initiatives to liberalize services such as the Digital Single Market strategy will likely present a large missed opportunity for UK firms.

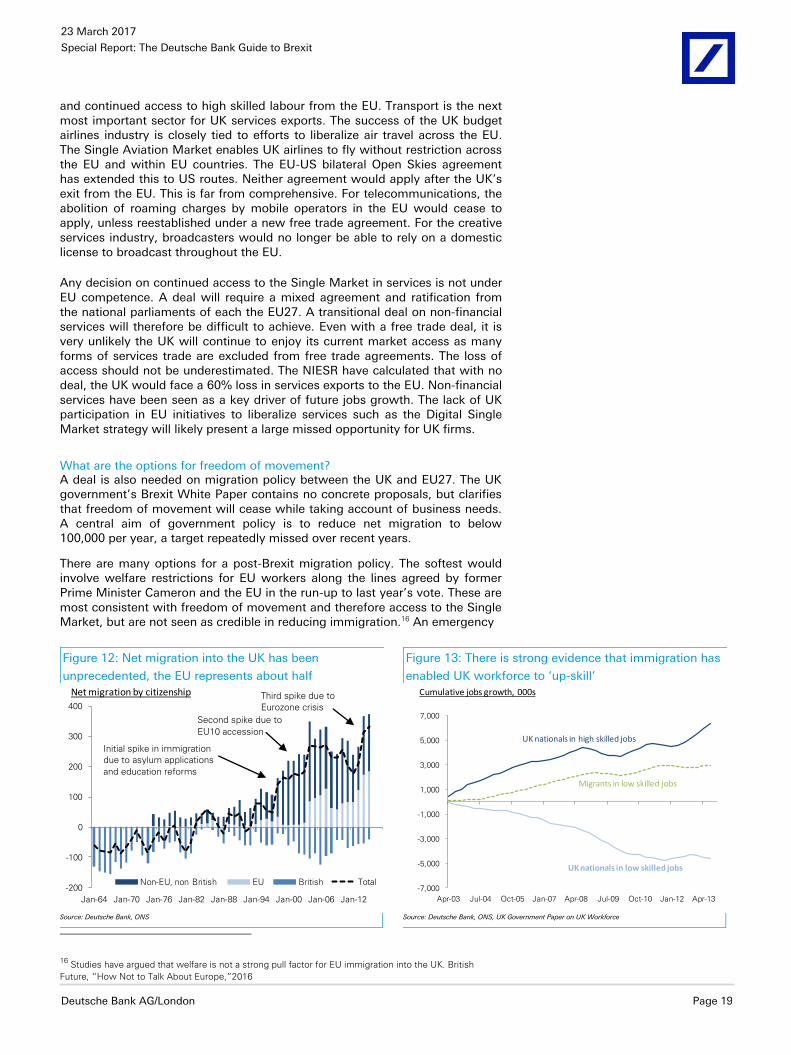

What are the options for freedom of movement? A deal is also needed on migration policy between the UK and EU27. The UK government’s Brexit White Paper contains no concrete proposals, but clarifies that freedom of movement will cease while taking account of business needs. A central aim of government policy is to reduce net migration to below 100,000 per year, a target repeatedly missed over recent years.

There are many options for a post-Brexit migration policy. The softest would involve welfare restrictions for EU workers along the lines agreed by former Prime Minister Cameron and the EU in the run-up to last year’s vote. These are most consistent with freedom of movement and therefore access to the Single Market, but are not seen as credible in reducing immigration.16 An emergency

16 Studies have argued that welfare is not a strong pull factor for EU immigration into the UK. British

Future, “How Not to Talk About Europe,”2016

Figure 12: Net migration into the UK has been

unprecedented, the EU represents about half

Figure 13: There is strong evidence that immigration has

enabled UK workforce to ‘up-skill’

-200

-100

0

100

200

300

400

Jan-64 Jan-70 Jan-76 Jan-82 Jan-88 Jan-94 Jan-00 Jan-06 Jan-12

Net migration by citizenship

Non-EU, non British EU British Total

-7,000

-5,000

-3,000

-1,000

1,000

3,000

5,000

7,000

Apr-03 Jul-04 Oct-05 Jan-07 Apr-08 Jul-09 Oct-10 Jan-12 Apr-13

Cumulative jobs growth, 000s

UK nationals in high skilled jobs

Migrants in low skilled jobs

UK nationals in low skilled jobs

Source: Deutsche Bank, ONS Source: Deutsche Bank, ONS, UK Government Paper on UK Workforce

Third spike due to

Eurozone crisis

Second spike due to

EU10 accession

Initial spike in immigration

due to asylum applications

and education reforms

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Page 20 Deutsche Bank AG/London

brake on EU migration was also discussed prior to the negotiations last year. While discarded, this is conceptually similar to Articles 112-114 of the EEA treaty, which allows member states to suspend freedom of movement where severe ‘economic, societal or environmental difficulties’ can be established. An emergency brake could provide policy flexibility, but would be contentious as none of the EEA states have ever applied it with the exception of Lichtenstein.

Another option is a points system for EU migrants along the lines of Australia or New Zealand. This would discriminate between migrants based on factors like professional qualifications and work experience. This option appears to be unpopular with Prime Minister May because it doesn’t place hard checks on migrant numbers. Tougher options would include work permits, which could be capped either in aggregate, by skill, or by sector. The UK’s current multi-tier immigration policy for workers outside the EU involves a mixture of points-based and work permit criteria. Both these options would be incompatible with continued Single Market Access. A deal on migration is also likely to be reciprocal, with the EU27 applying similar controls on migrants from the UK.17

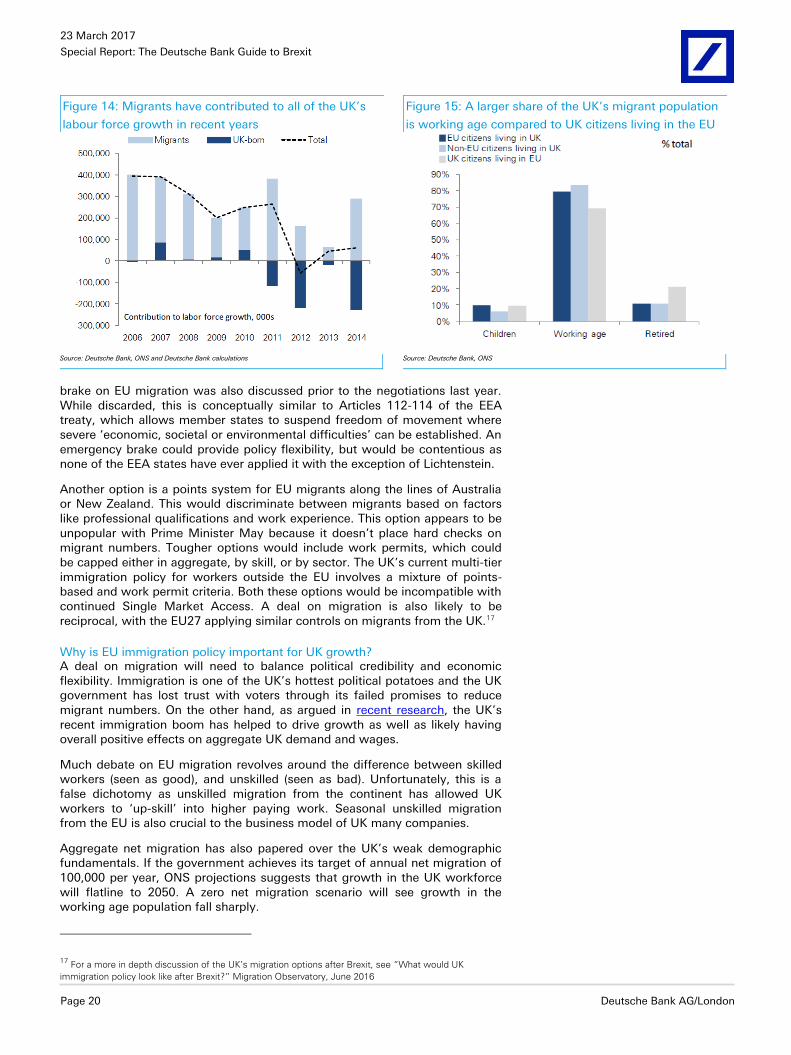

Why is EU immigration policy important for UK growth? A deal on migration will need to balance political credibility and economic flexibility. Immigration is one of the UK’s hottest political potatoes and the UK government has lost trust with voters through its failed promises to reduce migrant numbers. On the other hand, as argued in recent research, the UK’s recent immigration boom has helped to drive growth as well as likely having overall positive effects on aggregate UK demand and wages.

Much debate on EU migration revolves around the difference between skilled workers (seen as good), and unskilled (seen as bad). Unfortunately, this is a false dichotomy as unskilled migration from the continent has allowed UK workers to ‘up-skill’ into higher paying work. Seasonal unskilled migration from the EU is also crucial to the business model of UK many companies.

Aggregate net migration has also papered over the UK’s weak demographic fundamentals. If the government achieves its target of annual net migration of 100,000 per year, ONS projections suggests that growth in the UK workforce will flatline to 2050. A zero net migration scenario will see growth in the working age population fall sharply.

17 For a more in depth discussion of the UK’s migration options after Brexit, see “What would UK

immigration policy look like after Brexit?” Migration Observatory, June 2016

Figure 14: Migrants have contributed to all of the UK’s

labour force growth in recent years

Figure 15: A larger share of the UK’s migrant population

is working age compared to UK citizens living in the EU

Source: Deutsche Bank, ONS and Deutsche Bank calculations Source: Deutsche Bank, ONS

23 March 2017

Special Report: The Deutsche Bank Guide to Brexit

Deutsche Bank AG/London Page 21

The political sting may be partly salved by the fact net migration from the EU is likely to fall regardless. The influx in inbound migration from the EU over the last decade was due to the failure to introduce transitional controls to A10 accession countries in 2004, which saw migrants from the former Soviet Union pulled by the UK’s higher wages, and the recent Eurozone crisis which saw migrants from the peripheral states pushed by high unemployment rates. Neither is likely to prove so significant, as income levels in Eastern Europe converge with the west and the ongoing Eurozone recovery sees unemployment fall. This could provide much needed cover for the political salability of a softer migration deal.

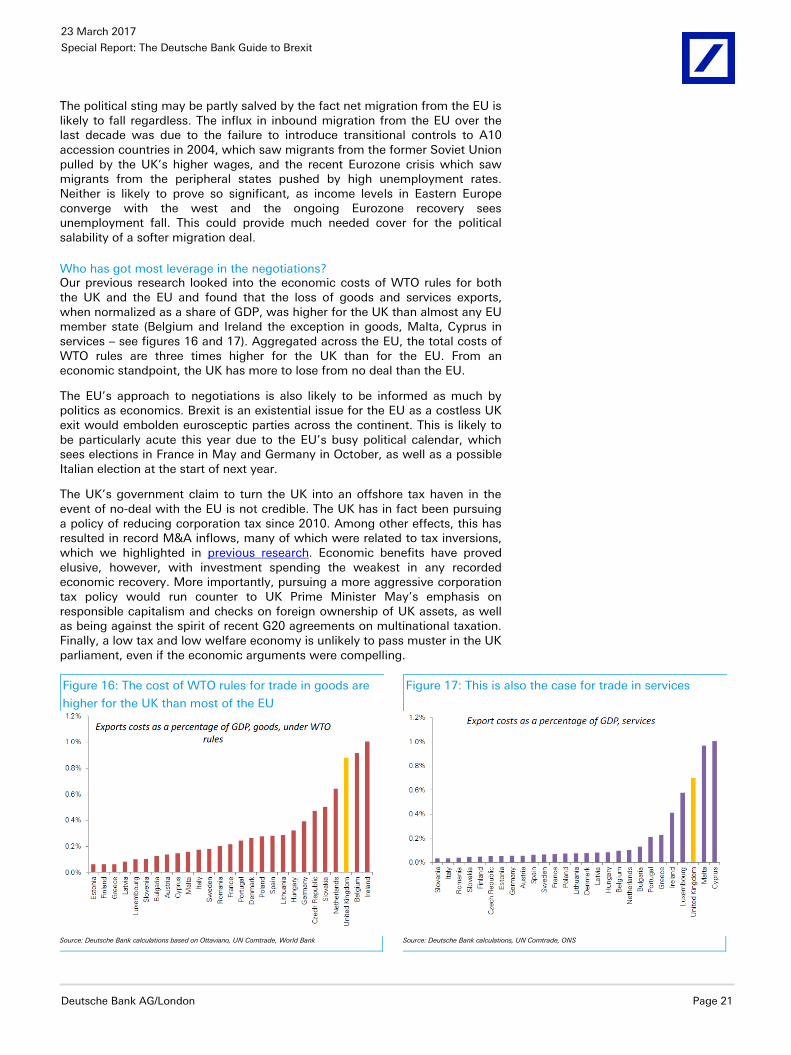

Who has got most leverage in the negotiations? Our previous research looked into the economic costs of WTO rules for both the UK and the EU and found that the loss of goods and services exports, when normalized as a share of GDP, was higher for the UK than almost any EU member state (Belgium and Ireland the exception in goods, Malta, Cyprus in services – see figures 16 and 17). Aggregated across the EU, the total costs of WTO rules are three times higher for the UK than for the EU. From an economic standpoint, the UK has more to lose from no deal than the EU.

The EU’s approach to negotiations is also likely to be informed as much by politics as economics. Brexit is an existential issue for the EU as a costless UK exit would embolden eurosceptic parties across the continent. This is likely to be particularly acute this year due to the EU’s busy political calendar, which sees elections in France in May and Germany in October, as well as a possible Italian election at the start of next year.

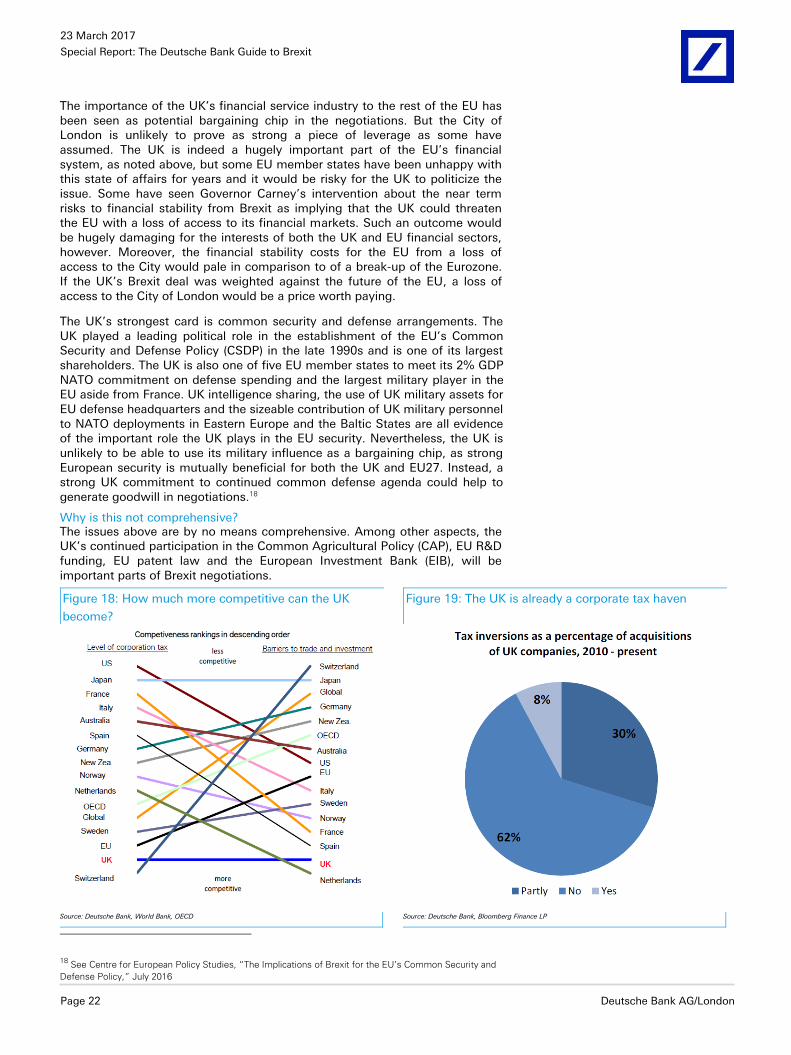

The UK’s government claim to turn the UK into an offshore tax haven in the event of no-deal with the EU is not credible. The UK has in fact been pursuing a policy of reducing corporation tax since 2010. Among other effects, this has resulted in record M&A inflows, many of which were related to tax inversions, which we highlighted in previous research. Economic benefits have proved elusive, however, with investment spending the weakest in any recorded economic recovery. More importantly, pursuing a more aggressive corporation tax policy would run counter to UK Prime Minister May’s emphasis on responsible capitalism and checks on foreign ownership of UK assets, as well as being against the spirit of recent G20 agreements on multinational taxation. Finally, a low tax and low welfare economy is unlikely to pass muster in the UK parliament, even if the economic arguments were compelling.

Figure 16: The cost of WTO rules for trade in goods are

higher for the UK than most of the EU