The Current Foreclosure Crisis – Trends and Roadblocks … · WOODSTOCK INSTITUTE | FEBRUARY 2011...

28

WOODSTOCK INSTITUTE | FEBRUARY 2011 American Planning Association February 22, 2011 The Current Foreclosure Crisis – Trends and Roadblocks to Recovery Geoff Smith | Senior Vice President Woodstock Institute | Chicago, Illinois [email protected] | www.woodstockinst.org

Transcript of The Current Foreclosure Crisis – Trends and Roadblocks … · WOODSTOCK INSTITUTE | FEBRUARY 2011...

WOODSTOCK INSTITUTE | FEBRUARY 2011

American Planning AssociationFebruary 22, 2011

The Current Foreclosure Crisis –Trends and Roadblocks to Recovery

Geoff Smith | Senior Vice PresidentWoodstock Institute | Chicago, [email protected] | www.woodstockinst.org

Woodstock Institute

• Chicago-based non-profit research and policy organization working locally, nationally, and internationally to promote economic development in lower-income communities and communities of color

• Work with financial institutions, community organizations, foundations, government agencies, and others.

• Areas of expertise include CRA and fair lending policies, financial and insurance services, small business lending, community development financial institutions, and economic development strategies.

• Key program area: Housing Policy and Practice

• Mortgage Lending

• Foreclosures

WOODSTOCK INSTITUTE | MONTH YEAR

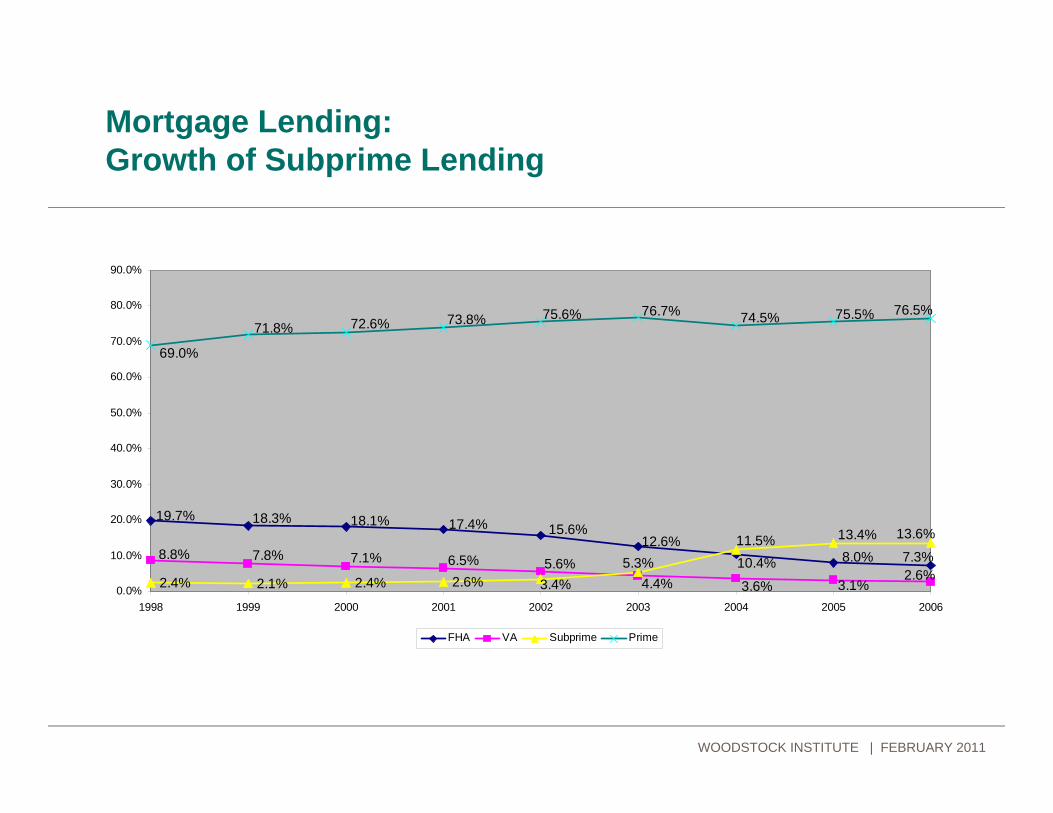

Mortgage Lending:Growth of Subprime Lending

2.4% 2.1% 2.4% 2.6%

8.0%10.4%12.6%

15.6%17.4%18.1%18.3%19.7%

7.3%

3.1%4.4%5.6%6.5%7.1%

3.6%

8.8% 7.8%2.6%

11.5%5.3%

3.4%

13.4% 13.6%

72.6% 73.8% 75.6% 76.7% 74.5% 75.5%

69.0%

71.8%76.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006

FHA VA Subprime Prime

WOODSTOCK INSTITUTE | FEBRUARY 2011

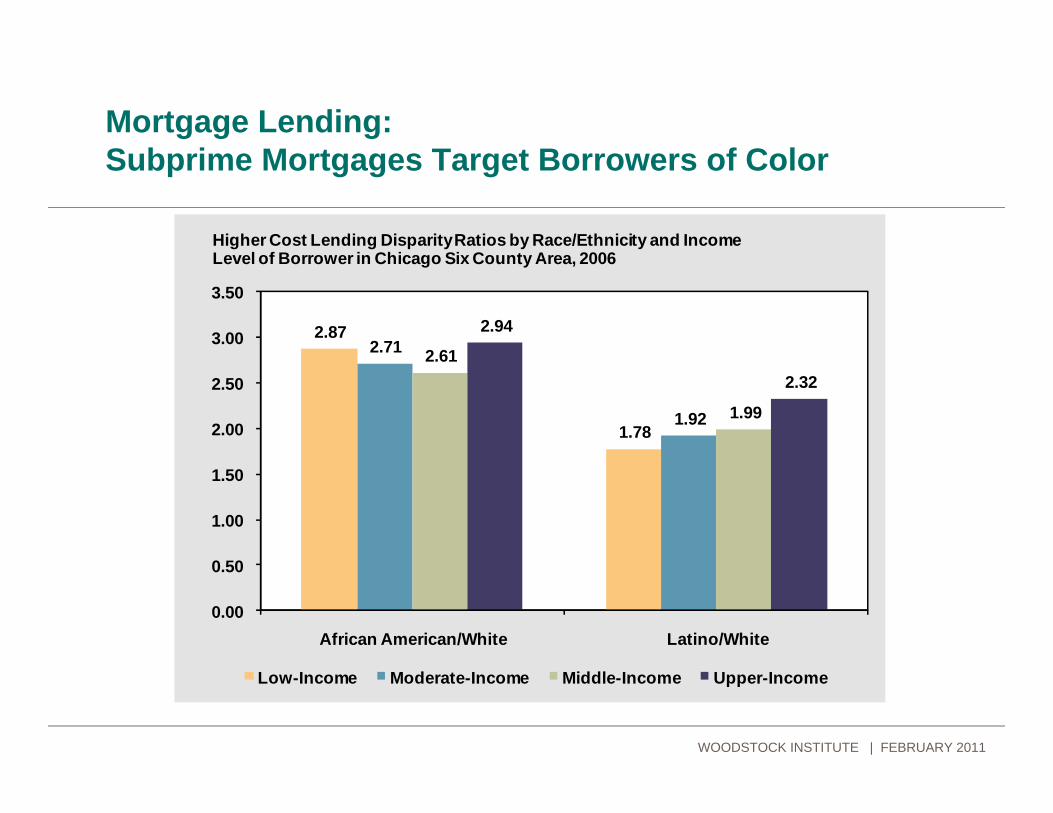

Mortgage Lending:Subprime Mortgages Target Borrowers of Color

2.87

1.78

2.71

1.92

2.61

1.99

2.94

2.32

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

African American/White Latino/White

Higher Cost Lending Disparity Ratios by Race/Ethnicity and Income Level of Borrower in Chicago Six County Area, 2006

Low-Income Moderate-Income Middle-Income Upper-Income

WOODSTOCK INSTITUTE | FEBRUARY 2011

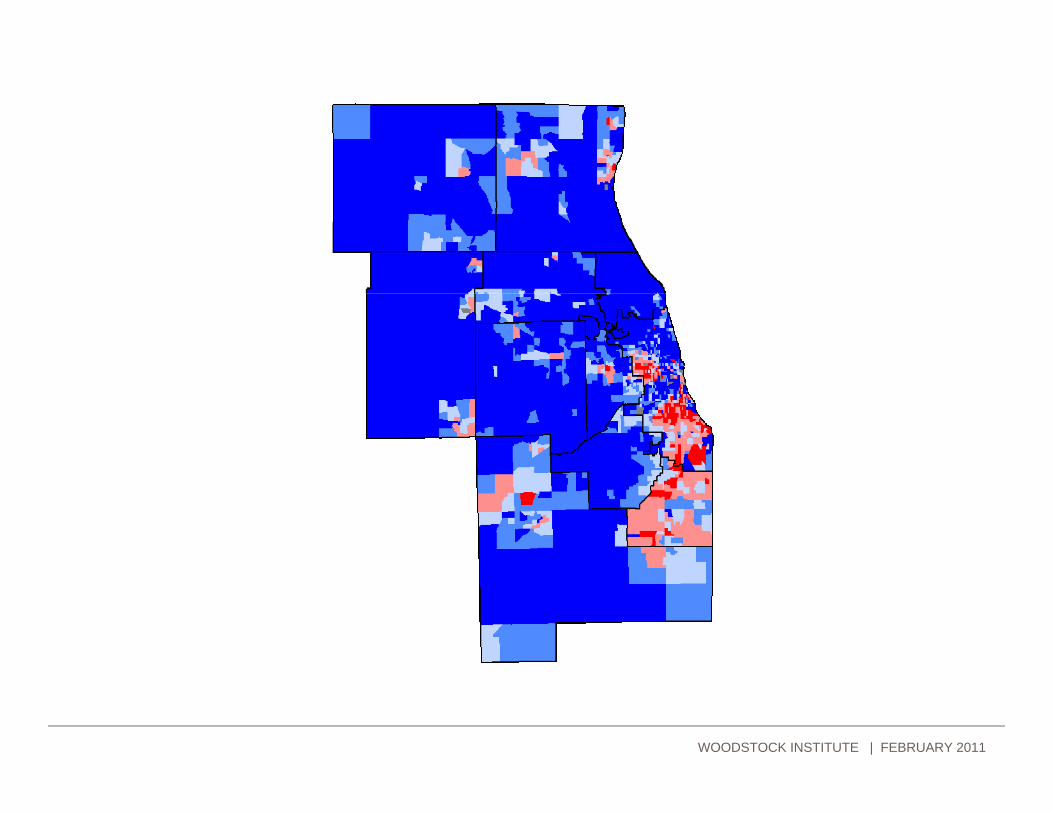

Mortgage Lending:Subprime Mortgages Concentrated in Communities of Color

WOODSTOCK INSTITUTE | FEBRUARY 2011

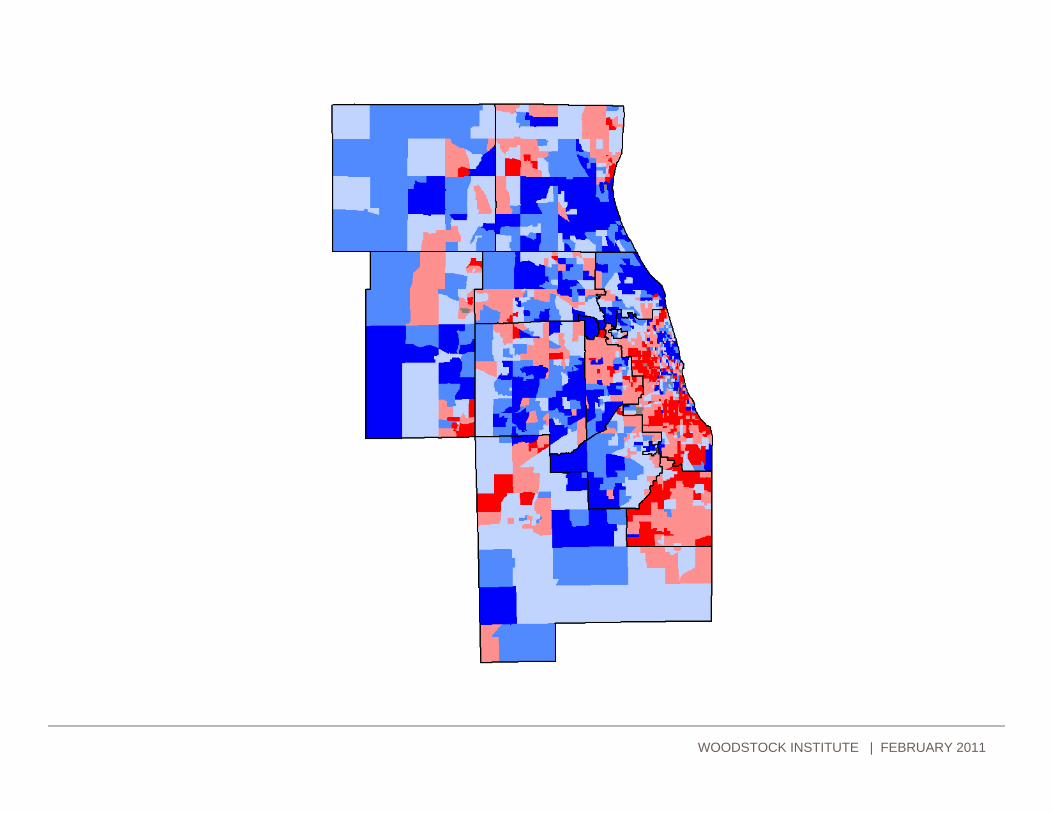

Regional Quarterly Trends in Foreclosure Filings, 2005 to 2010

WOODSTOCK INSTITUTE | FEBRUARY 2011

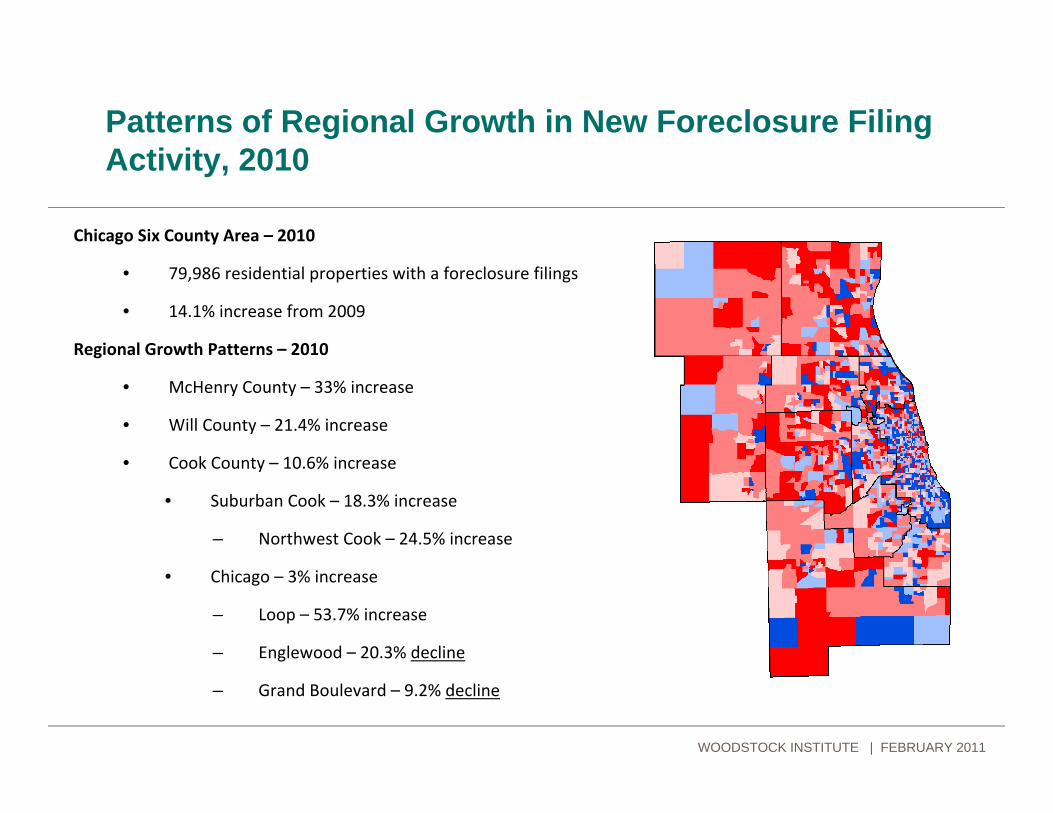

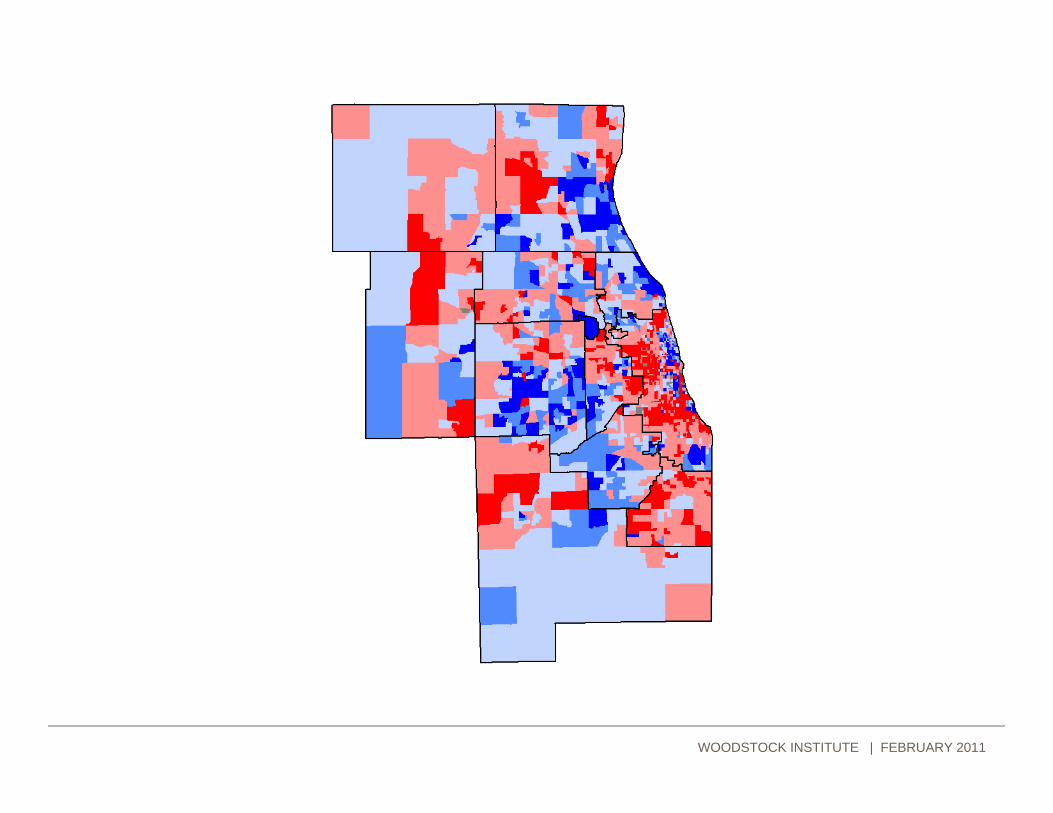

Patterns of Regional Growth in New Foreclosure Filing Activity, 2010

Chicago Six County Area – 2010

• 79,986 residential properties with a foreclosure filings

• 14.1% increase from 2009

Regional Growth Patterns – 2010

• McHenry County – 33% increase

• Will County – 21.4% increase

• Cook County – 10.6% increase

• Suburban Cook – 18.3% increase

– Northwest Cook – 24.5% increase

• Chicago – 3% increase

– Loop – 53.7% increase

– Englewood – 20.3% decline

– Grand Boulevard – 9.2% decline

WOODSTOCK INSTITUTE | FEBRUARY 2011

Emerging Issues – Condo Foreclosures in the Suburbs

Condo foreclosures continue to rise, expand to suburbs in 1H 2010

• Increase from 1‐3Q 2009:

• Region – 42.5%

• City of Chicago – 34.9%

• Share of total new foreclosure filings in 1‐3Q 2010:

• Region ‐ 19.5%

• City of Chicago – 26.6%

In certain suburban regions, a substantial share of newly filed foreclosures are on condos

• Northwest Cook – 43.1% of all new FC filings

• 64.8% increase from 1‐3Q 2010

• North Cook – 29.9%

• 57.9% increase

• Southwest Cook – 23.4%

• 59.4% increase

• DuPage County – 22.3%

• 31.7% increase

WOODSTOCK INSTITUTE | FEBRUARY 2011

WOODSTOCK INSTITUTE | FEBRUARY 2011

WOODSTOCK INSTITUTE | FEBRUARY 2011

WOODSTOCK INSTITUTE | FEBRUARY 2011

WOODSTOCK INSTITUTE | FEBRUARY 2011

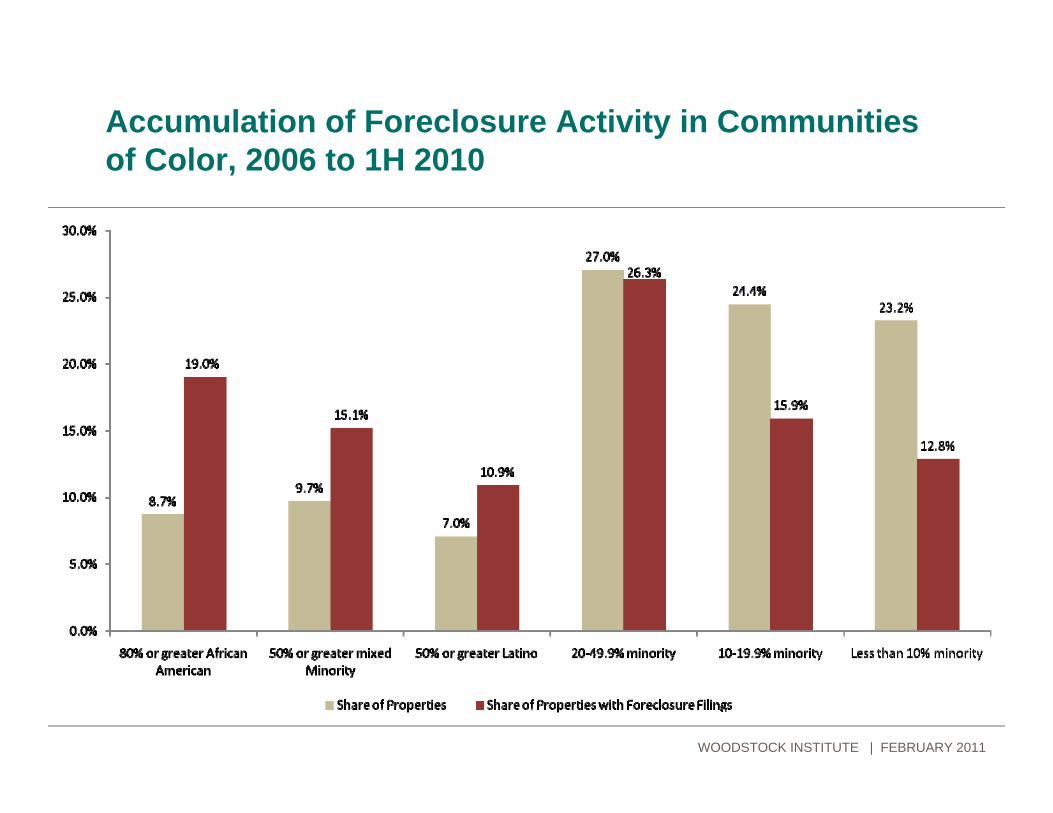

Accumulation of Foreclosure Activity in Communities of Color, 2006 to 1H 2010

WOODSTOCK INSTITUTE | FEBRUARY 2011

WOODSTOCK INSTITUTE | OCTOBER 2010

WOODSTOCK INSTITUTE | OCTOBER 2010

WOODSTOCK INSTITUTE | OCTOBER 2010

WOODSTOCK INSTITUTE | OCTOBER 2010

WOODSTOCK INSTITUTE | OCTOBER 2010

Patterns of Regional Growth in Completed Foreclosure Auction Activity, 2009 to 2010

Chicago Six County Area – 2010

• 30,981 residential properties completed foreclosure process

• 95.3% entered REO status

• 25.2% increase in completed auctions from 2009

Regional Growth Patterns – 2009 to 2010

• Will County – 24.8% increase

• Cook County – 27.8% increase

• Suburban Cook – 37.4% increase

– Northwest Cook – 66.1% increase

– Southwest Cook – 41.9% increase

• Chicago – 19.9% increase

WOODSTOCK INSTITUTE | FEBRUARY 2011

Impacts of Foreclosure

Homeowner

• Loss of shelter

• Loss of assets

• Displacement

• Damaged credit

• Family Stress

Communities

• Blight

• Neighborhood instability

• Increases in violent crime

• Decreases in property values

• Increased costs for municipalities and decreased revenues to manage those costs and to improve neighborhoods

WOODSTOCK INSTITUTE | FEBRUARY 2011

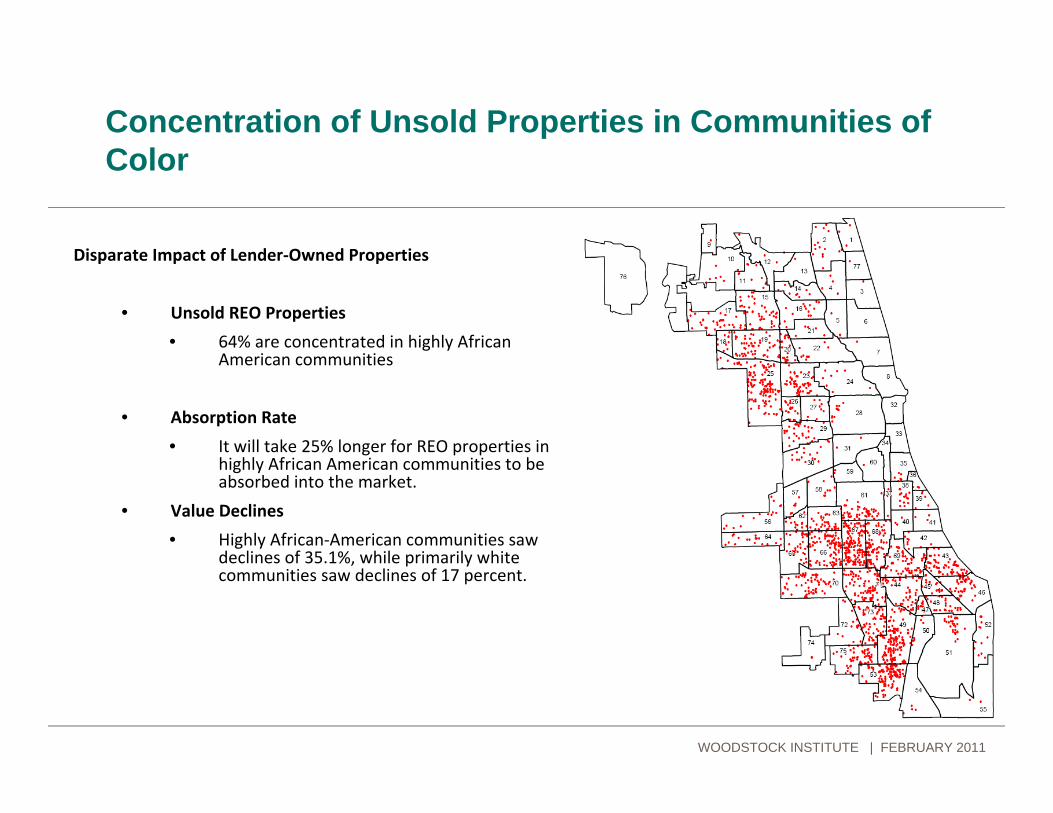

Concentration of Unsold Properties in Communities of Color

Disparate Impact of Lender‐Owned Properties

• Unsold REO Properties

• 64% are concentrated in highly African American communities

• Absorption Rate

• It will take 25% longer for REO properties in highly African American communities to be absorbed into the market.

• Value Declines

• Highly African‐American communities saw declines of 35.1%, while primarily white communities saw declines of 17 percent.

WOODSTOCK INSTITUTE | FEBRUARY 2011

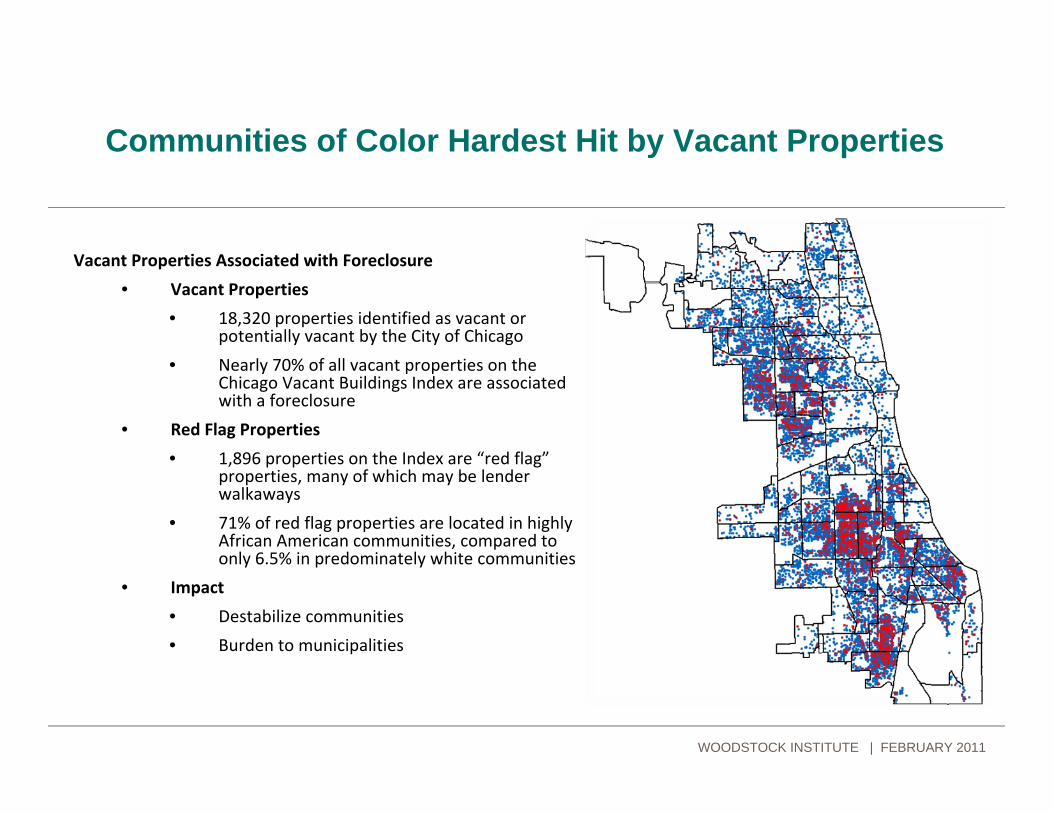

Communities of Color Hardest Hit by Vacant Properties

WOODSTOCK INSTITUTE | FEBRUARY 2011

Vacant Properties Associated with Foreclosure

• Vacant Properties

• 18,320 properties identified as vacant or potentially vacant by the City of Chicago

• Nearly 70% of all vacant properties on the Chicago Vacant Buildings Index are associated with a foreclosure

• Red Flag Properties

• 1,896 properties on the Index are “red flag”properties, many of which may be lender walkaways

• 71% of red flag properties are located in highly African American communities, compared to only 6.5% in predominately white communities

• Impact

• Destabilize communities

• Burden to municipalities

Roadblocks to Recovery

Weakness in Impacted Local Real Estate Markets

• Accumulation of vacant properties

• A foreclosure reduces a property’s value by 27 percent, on average

• A foreclosure reduces surrounding property values by .9 percent

• Inventory absorption

• Underwater Homeowners

• 19.7 percent of Illinois mortgages underwater in 2Q 2010

Other Barriers

• Foreclosure process and disposition of foreclosed properties

• Disproportionately high unemployment

Credit Pullback

• Disproportionate lending declines

• 68.8 percent decline in home purchase lending in 2008 in region’s African American communities, compared to 54 percent regionally – 44 percent decline in predominately white communities

• Tighter underwriting and uncertain appraisals

• Credit scores and income issues

WOODSTOCK INSTITUTE | FEBRUARY 2011

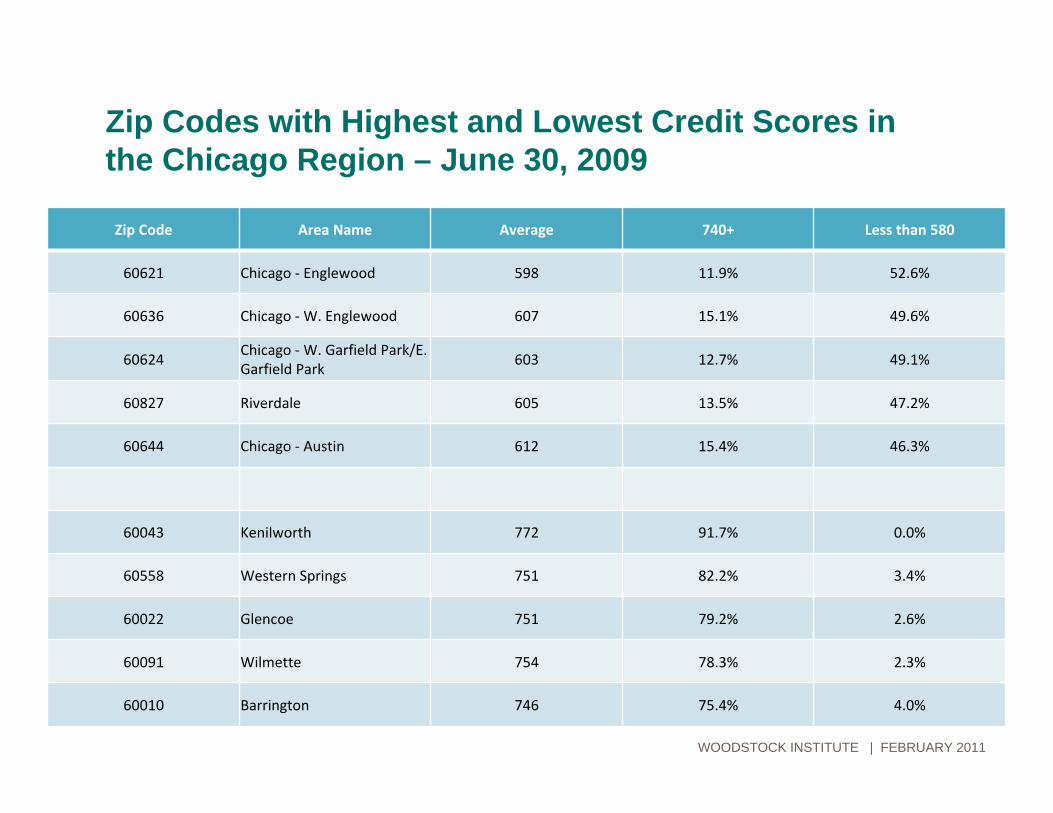

Zip Codes with Highest and Lowest Credit Scores in the Chicago Region – June 30, 2009

Zip Code Area Name Average 740+ Less than 580

60621 Chicago ‐ Englewood 598 11.9% 52.6%

60636 Chicago ‐W. Englewood 607 15.1% 49.6%

60624Chicago ‐W. Garfield Park/E. Garfield Park

603 12.7% 49.1%

60827 Riverdale 605 13.5% 47.2%

60644 Chicago ‐ Austin 612 15.4% 46.3%

60043 Kenilworth 772 91.7% 0.0%

60558 Western Springs 751 82.2% 3.4%

60022 Glencoe 751 79.2% 2.6%

60091 Wilmette 754 78.3% 2.3%

60010 Barrington 746 75.4% 4.0%

WOODSTOCK INSTITUTE | FEBRUARY 2011

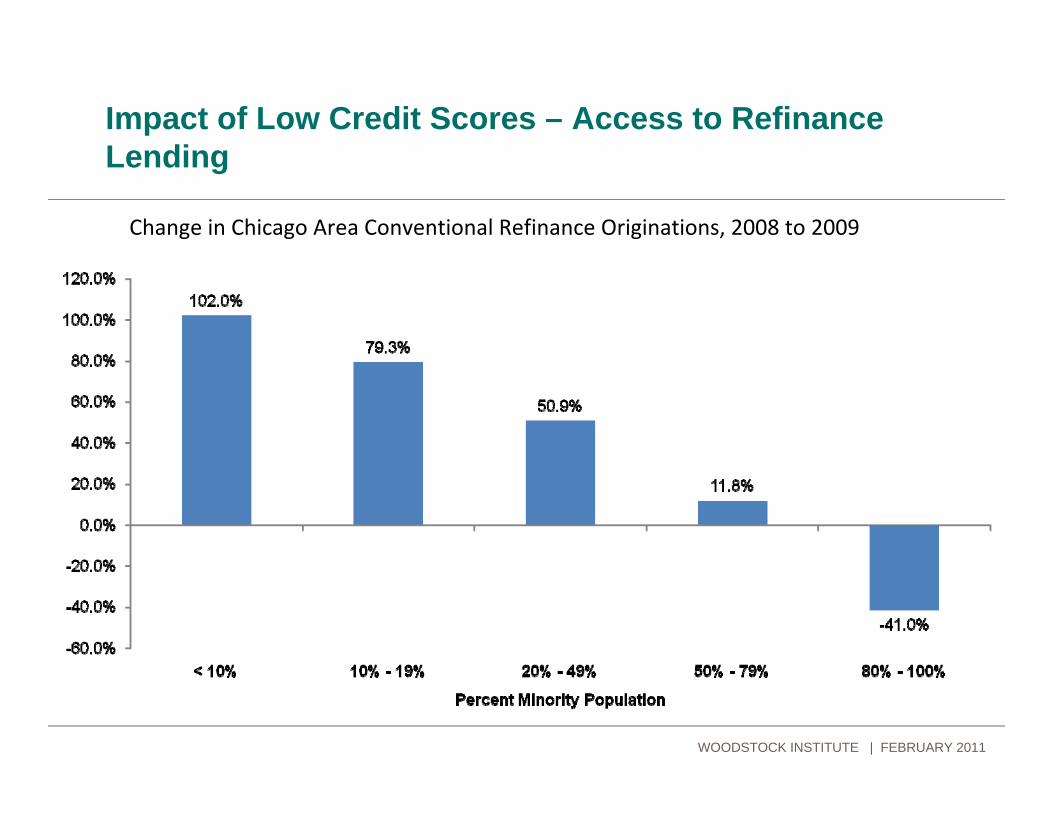

Impact of Low Credit Scores – Access to Refinance Lending

Change in Chicago Area Conventional Refinance Originations, 2008 to 2009

WOODSTOCK INSTITUTE | FEBRUARY 2011

Interventions:Helping Homeowners

• Home Affordable Modification Program (HAMP)

• Projected to help 3‐4 million

• Fell short of goals, actually has helped a little more than .5 million helped

• Challenges addressing emerging roadblocks

• Limited mortgage servicer accountability

• Proprietary modification

• Servicers completed 696,992 proprietary modifications from 3Q 2009 to 3Q 2010

• Lower monthly payments are not guaranteed as in HAMP

• Limited oversight and transparency

• Higher redefault rates (after six months ‐ 22.8% for proprietary mods, 10.8% for HAMP mods)

• Court mortgage foreclosure mediation programs: Philadelphia

• Facilitates communication between borrower and lender

• 30 percent of homeowners who participated in Philadelphia were able to reach a settlement

• Foreclosure counseling

• 45 percent of homeowners who complete counseling are able to stay in their homes

• Serious gaps in counseling capacity in areas of high foreclosure activity

WOODSTOCK INSTITUTE | FEBRUARY 2011

Interventions:Helping Communities and Looking to the Future

• Neighborhood Stabilization Program (NSP)

• Illinois has received $362.8 million in NSP funds from three rounds of funding

• Challenges: competing with investor purchases

• Weak demand in re‐sale market

• Municipal response to vacant properties

• Early warning databases, vacant property registry, liens and land banking

• Increased servicer accountability around vacant properties

• Boston Community Capital SUN program

• Uses borrowed funds to purchases REO properties, sells back properties to original owners

• CRA Modernization

• Ensures access to credit

• Updates CRA to reflect practices of the current financial landscape

• Financial Reform

• Foreclosure crisis has roots in discriminatory lending practices

• Financial reform keeps bad products out of neighborhoods

WOODSTOCK INSTITUTE | FEBRUARY 2011

American Planning AssociationFebruary 22, 2011

The Current Foreclosure Crisis –Trends and Roadblocks to Recovery

Geoff Smith | Senior Vice PresidentWoodstock Institute | Chicago, [email protected] | www.woodstockinst.org

WOODSTOCK INSTITUTE | FEBRUARY 2011