the - IARFC CPA, an authority on insurance ... [email protected] Derek D. Klock ... 31 Get Your...

36

the Vol. 7 No. 12 • December 2006 Official IARFC Publication www.IARFC.org Serving Financial Advisors Worldwide

Transcript of the - IARFC CPA, an authority on insurance ... [email protected] Derek D. Klock ... 31 Get Your...

the

Vol. 7 No. 12 • December 2006 Official IARFC Publication www.IARFC.org

Serving Financial Advisors Worldwide

IARFC Member Benefits and Professional ToolsPublications and Printed MaterialsThe Register – monthly membership magazine.

Journal of Personal Finance – our quarterly academic journal.

Financial Insider – 8 page client financial newsletter.

20/20 Newsletter – 4 page color client financial newsletter.

Press Releases – to announce receipt of RFCdesignation.

Probe newsletter – timely 4 pagenewsletter from Kissling org.

Research Press – by Vernon Jacobs,CLU, CPA, an authority on insuranceand tax planning.

Financial Services Online (FSO) –Internet publications: Online

Financial Services Journal Online –monthly publication, eight articles.

Financial E-News – Bi-weekly e-mail of about financial services developments.

RFC Consumer folder – 4 page full colorbrochure about RFC and advisor services.

RFC Small flyer – 3 panel full colorbrochure about RFC® and advisor services.

RFC flyer – two color brochureemphasizing ethics.

RFC Gold Foil Labels – add a touch of classto your envelopes and financial plans.

Business Source – monthly reviews ofimportant business and financial books; $32 yearly.www.thebusinesssource.com/subscribeiarfc1.htm

Educational Events and Practice ManagementFinancial Advisors Forum – three-day high level conference forfinancial practitioners. May 15-17, 2007, Bally’s Las Vegas.

Education Cruise/Conferences – CE-at-Sea. Depart fromVancouver, and journey to Anchorage, Alaska, August 17-24, 2007.

Website Partnership – Financial Visions helps you build a full-featured advisor website with NASD approved content.

Advisor Verification – confirmation at IARFC.org of education,designation, operations, services, products, photo and contact info.

Sponsor Association – access to National Heritage Foundation, adonor-advised/founder-involved charitable entity.

Wealth Management – Courses for advisors wishing to serveaffluent families — acquire the C3DWP designation.

Financial Calculators – online analytical, presentation andeducation tools for IARFC members, located on the IARFC website.

Professional Recognition ItemsYour Member Profile – IARFC.org has a very sophisticated profile,and currently the best, of all those in the financial services field.

The RFC® Certificate – Handsome 16” x 20” parchment diploma-type document designed for framing and display.

RFC® Confirmation Notice – A smallerrecognition notice for use in a folder orbinder 8.5” x 11”.

Formal Announcements – 4” x 5” formalcards proclaiming your RFC® conferment.

Professional Insignia – Gold RFC® orsilver RFA lapel pin; Men’s tie chain andkey; Ladies gold ring broach; Unisex goldRFC® cufflinks.

Financial Plan Binders – attractivepadded dark blue binders with 3slanted D rings.

Colorful Index Tab sets – for theassembly of quality financial plans.

Comprehensive Sample Plans – Fullplans including assembly andpresentation manual, preparedusing the Plan Builder software,supplemented by materials fromPractice Builder.

Client Appreciation – specialtydocument wallets and folders formemorable presentations.

Personal Note Cards – with goldRFC® Key on front for use with clients and prospects.

Document Filing Systems that will create natural cross-sellingdiscussions, by Boxes by Pandora.

IARFC Logos – for business cards, website and stationery.

Financial SoftwareIPS AdvisorPro software – Investment Policy Statements for youradvisory clients in accordance with RIA requirements, authored byNorm Boone & Linda Lubitz.

Practice Builder Financial software – Client RelationshipManagement (CRM) customized for the needs of financialprofessionals. Use technology to differentiate yourself, tocommunicate more often and maintain “Top of Mind Awareness.”

Plan Builder Financial software – for sophisticated,comprehensive and modular financial plans; more than 80financial variables. Results are graphically displayed. A planningtool to motivate your clients to take action Now!

Client Builder Financial – a presentation system in PowerPoint toclose the fee-based planning engagement, with full script andbackup letters, agendas and forms in Microsoft Word.

The Register • December 2006 Page 1

The Register is published monthly by the International Association of Registered Financial Consultants ©2006. It includes articles and advice on technical subjects,economic events, regulatory actions and practice management. The IARFC makes noclaim as to accuracy and does not guarantee or endorse any product or service that isadvertised or featured. Articles, comments and letters are welcomed by e-mail to: Wendy M. Kennedy, Editorial Coordinator, [email protected] SSN 1556-4045 POSTMASTER: Send address changes to, P.O. Box 42506, Middletown, Ohio 45042-0506

Financial Planning Building2507 North Verity Parkway

P.O. Box 42506Middletown, OH 45042-0506

800 532 9060 • Fax 513 424 5752www.IARFC.org

BOARD OF DIRECTORS

Edwin P. Morrow, Chairman & CEOCLU, ChFC, CFP®, CEP, RFC®

Judith Fisette-Losz, Executive [email protected]

Lester W. AndersonMBA, RFC®

H. Stephen Bailey, PresidentLUTCF, CEBA, CEP, CSA, RFC®

Jeffrey ChiewDBA, CLU, ChFC, CFP®, RFC®

Vernon D. GwynneCFP®, RFC®

Derek D. KlockMBA, RFC®

Edward J. LedfordCLU, RFC®

Constance O. LuttrellRFC®

Ruth LyttonMS, Ph.D., RFC®

James McCarty, SecretaryCLU, RHU, LUTCF, RFC®

Burnett Marus, TreasurerRFC®

Rosilyn H. OvertonMS, CFP®, RFC®

Ruben RuizChFC, CLU, MSFS, CSA, RFC®

Michael ZmistowskiRFC®

[email protected]_________________________________

Wendy M. Kennedy, Editorial [email protected]

Stephanie Langster, Administrative [email protected]

in this issue

2 The 2007 IARFC Calendar of Events

3 The Francis Family The Bermuda Financial Triangle

5 First RFC Class to be Launched Client Acquisition and Engagement

6 From the Chairman’s Desk A Scorecard on IARFC Progress in 2006by Ed Morrow

7 Financial Plan Competition Launched

8 In 2007, Keep Changing to Mirror the LTCI Market Place and Prospectsby Wilma Anderson

9 Taiwan RFC Growth

10 Do You Really Know Where Your E-mails Go? by Ed Morrow

11 Do You Say “Thanks” Often Enough? Use the RFC Note Cards to Enhance Your Image

12 Registered Education Planner (REP) A Window of Service Opportunities

13 Compliance-Friendly MarketingA Mom’s Letter to Her Children by Katherine Vessenes

16 Reflections from Southern Californiaby Ed Morrow and Mehdi Fakharzadeh

18 The New RMA — Registered Mortgage Advisorby Randy Luebke

21 Pitch, Polish or PersonalityImproving Your Phone Impactby Frances Scott

22 Life Insurance in Retirement PlanningA New Regulatory Environment for Life Insurance?by Ben G. Baldwin

25 Financial Advisors Forum — Las Vegas May, 2007

31 Get Your CE-at-Sea — Alaska Cruise Conference 2007

Page 2 The Register • December 2006

Register LettersWe welcome your comments, suggestions and ideas.Please direct correspondence to: [email protected] may be edited for length and clarity.

INTERNATIONALIARFC COORDINATORS

Jeffrey ChiewAsia Chair

DBA, CLU, ChFC, CFP®, RFC®

Liang Tien LungChina Development Organization (IMM)

RFC®

Ralph LiewPhilippines Chair

RFC®

[email protected] Balmori

Executive [email protected]

Jerry TanSingapore Chair

CIAM, CMFA, RFC®

Zhu Xu LongChina Chair, Shanghai

RFC®

Samuel W. K. Yung, MHChair, Hong Kong and Macao

CFP®, MFP, FChFP, CMFA, CIAM, RFC®

[email protected]. Teresa So

Advisor, Hong Kong and MacaoPhD, MFP, FChFP, CMFA, CIAM, RFC®

RFC®

Ng Jyi WeiMalaysia Chair

ChFC, CFP®, RFC®

Aidil Akbar Madjid Indonesia Chair

MBA, RFC®

[email protected] Soemarto

MA, RFC®

Jeffrey ChenTaiwan Chair

RFC®

Preecha SwasdpeeraThailand Chair

MPA, MM, RFC®

Demetre KatsabekisGreece Chair

MBA, Ph.D, RFC®

The IARFC Register is accepting articles of 300 to 1,500 words on planning and practice management topics. Submit via e-mail, along with an

electronic photo and short bio of less than 100 words to: [email protected]

Calendar of Events:

First RFC Course – Part ICovering Client Acquisition and Client Engagement January 16-17, 2007, Middletown, OH

RFC – Indonesia GraduationsDecember 7, 2006, Jakarta December 8, 2006, Surabaya

Organizational Launch MeetingsFebruary 19–23, 2007, AustraliaFebruary 24-28, 2007, New Zealand

MarketShare Leadership ConventionMarch 6-9, 2007, Las Vegas, NV

Financial ExpoMarch 22, 2007, Tampa, FL

APfinSA ConferenceApril 13-15, 2007, Taipei, Taiwan

Financial Advisors ForumMay 15-17, 2007, Las Vegas, NV

MDRT Annual MeetingJune 10-13, 2007, Denver, CO

International Dragon AwardsAugust 11-13, 2007, Xiamen, China

IARFC Cruise/Conference – AlaskaAugust 17-24, 2007Vancouver, BC to Anchorage, AK

RFC Forum – ChinaSeptember, 2007, Dalian, China

RFC Forum – MalaysiaSeptember, 2007, Kuala Lumpur

Do you refer advisors for IARFCmembership? You can do this easily bycalling in or mailing names to the IARFCstaff. We will follow up!

Did you attend the 2006 Forum? Youcan register now for the 2007 Forum inLas Vegas — a great program in awonderful location.

Did you Get Your CE at Sea? Register forthe cruise on the Celebrity Summit toAlaska. Make your spouse happy!

Would you like to assist us? Help us witharticles, help at one of our, or teach theRFC courses when we roll them out nextyear. You can serve on an IARFCcommittee, recruit sponsors, be an eventspeaker or serve as a board member.

Call now to Get Active: 800 532 9060or e-mail: [email protected]

Get Involved: We welcome thesubmission of articles from IARFCpractitioners. This is a great way tocontribute to the profession.

Professional Articles: The Journalof Personal Finance is seekingarticles by practitioners that maydeal with the application offinancial planning techniques,marketing and practicemanagement. These are expectedto be very high level papers orarticles.

Publicity Opportunities: Naturally,we encourage published authors toadvise both their clients and themedia of their being published bysending a press release.

Contact Dr. Ruth LyttonE-mail: [email protected]: 540 231 6678

Call for Papers

Bermuda is an insurance and financialcenter, catering to institutions on a world-wide basis. But who serves the needs ofthe citizens and ex-patriot employees ofthis island nation only 650 miles off thecoast of North Carolina?

Unless you have visited Bermudapersonally (as well you should) you may notbe aware that it is not one island, but 138islands, many quite tiny. The six majorislands are bridged together, so thebusiness or tourist visitor tends to think ofit as a single island with beautiful whiteand pink sand beaches, wooded cliffs,calm bays and a coastline dotted by gailycolored houses and white roofs gleaming inthe bright sun. Bermuda is part of theBritish Commonwealth, but it is governedas a separate nation, with its own laws,elections, parliament and court system,serving the population of 65,000 residents.

The economy of Bermuda is tied moreclosely to the U.S. than to Britain, and theBermuda dollar is pegged to the U.S. dollar,though it is backed more solidly by goldreserves. The major industries areoffshore company registrations, insuranceand investments. There is not muchagriculture and no manufacturing. TheIsland has almost 100% employment rateand a 100% literacy rate. It is a great placeto visit, and an even finer place to live.

The Francis’ family history in Bermudagoes back several hundred years, and thefamily members are known to nearly allthe locals, having been quite involved inthe recent developments of the country.We caught up with the busy Arliss Francis,CLU, RFC® at the IARFC Cruise CE at SeaConference, where he and his wife, Arian,were relaxing on their tenth financialadvisor’s cruise.

What was your background beforeentering financial services?

I attended Goldsmith College, LondonUniversity, in the U.K. where I majored ingeography and received a TeachersCertificate from the Institute of Education.After my graduation in 1957, I returned toBermuda to teach geography and headthe physical education program at theCentral School.

Did you have a background in athletics?

I was actually a champion sprinter forBermuda when I was young. While

attending university Iexcelled in track andfield, and representedthe Amateur AthleticAssociation ofEngland in theUniversity Games.Track gave me anopportunity to travel,which is always a great experience.

Are you still athletic?

Well, I have played alot of golf, which isvery popular here in Bermuda. Ourcourses, which feature the famous “Bermuda grass” are playablefor the full year. But lately my involvementin athletics is limited to cheering on my10-year old granddaughter, Kyla Bolden,who is the 800-meter champion on theisland in her age group. For the last twoyears Kyla has competed and won against the best of U.S and Jamaica in the AAU National Club Championships,held at Disney’s Wide World of SportsComplex in Florida.

Did you enjoy teaching?

Yes, developing the minds and bodies ofthe kids was wonderful. I really enjoyedthe classroom experience, althougheventually I became disappointed with theadministrative bureaucracy of the schoolsystem. The structure here is not muchdifferent than the structure in the States.Plus, I found that advancement andcompensation were limited by the system.

How did you migrate from teaching into insurance?

I started selling life insurance part-timewith the highly respected Walter RobertsAgency, representing Empire LifeInsurance Company, and soon my part -time commissions were exceeding myteaching salary. When Mr. Robertsdecided to go into the hotel business, Ipurchased the agency from him, only tolater discover that Empire was planning tocease operations in Bermuda.

Shortly thereafter I started to representthe Bermuda Fire & Marine InsuranceCompany for life insurance. When thatfirm was bought out by the RoyalInsurance group, I started looking around again, and eventually formed

Diamond Company Limited as anindependent agency. I realized there wasa need to provide a continuity of identitythat was independent of the insurancecompanies represented.

Where are your offices?

Back in 1978 we leased second-flooroffices in the Outerbridge Building, which is on the main boulevard (anextension of Front Street), near the edge of the City of Hamilton. After nearlythirty years we’re still in the samelocation, and from my office window I can look out across Hamilton harbour and watch the cruise ships docking andletting off the tourists.

The commerce center of the city isactually quite small, so it is easy forclients to drop by, or for me to meet themfor lunch or dinner in town. The HamiltonPrincess, one of the Island’s premierhotels, is just half a block from our offices,and two blocks in the other direction you’ll find a selection of upscale shopsand fine restaurants.

How did you build your organization?

Over the years I watched a number ofagencies expand and contract as agentsstruggled to earn a consistent living. Irealized what was lacking, and what theagents needed: a good company torepresent, an opportunity to operate withmaximum independence, solid trainingand of course, motivation.

As a result of other changes, I signed onwith Equitable Life of Canada, whichoffered a full suite of life insuranceproducts suitable for our market. Policieswere issued in Bermuda currency (which

The Francis Family The Bermuda Financial Triangle

The Register • December 2006 Page 3

continued on page 4

continued from page 3 The Francis Family

is pegged in value to the US dollar), andalso in Canadian dollars. Gradually theoperation grew, and at one point we hadfive MDRT qualifiers within DiamondCompany Limited. We’ve since reducedour office staff somewhat, and my sonAntony now acts as the principal producerand office manager.

Have you been involved professionally?

I started off with the Life UnderwritersAssociation Training Course (LUATC), atwo-year course patterned after the LUTCFin the States, but taught by Canadians.Then, I took the Chartered LifeUnderwriter educational curriculum, andwas the first native of Bermuda to holdthe CLU designation.

I qualified for the Million Dollar RoundTable in 1975 and have attended theannual meetings nearly every year,generally carrying the Bermuda flag in theopening ceremony. At one of thosemeetings I met Ed Morrow, who asked meto join him in pioneering an organizationin financial services — ConfidentialPlanning Services (CPS).

I served on the CPS Board of Directors fortwelve years, and we were instrumental inhelping many prominent individuals makethe transition from life insurance tofinancial planning. Primarily, CPSdeveloped training courses and

Antony Francis, RFC®, on right working with a client

operational manuals on how to run afinancial planning operation.

In Bermuda I served two terms asPresident of the Life UnderwritersAssociation, now named the BermudaAssociation of Insurance and FinancialAdvisors — BAIFA. My son, Antony, hasalso served as president for two terms,and we take an active interest inpromoting good professional conduct on the Island.

While Bermuda is a small nation, it is verycosmopolitan. Most of us study abroad,and then return home where the economyis strong, property values are solid andthe society is very church-oriented. Wordtravels very fast. A great reputation takesa long time to build — but it can be swiftlydestroyed by a moment of carelessness,poor service or self-interest.

We have enjoyed watching the recentgrowth of the IARFC, and look forward tojoining other financial advisors at theForum meetings and Cruise Conferences.We frequently bring our friends and familyto join us on the cruises, and I suggestthat other RFCs consider doing that.Cruises are a great opportunity to bondwith clients and new friends. Theorganization is really moving forward,filling an international vacuum in the areaof training financial advisors with practicemanagement and marketing techniques.

Did you become involved in otheractivities in Bermuda?

During my time as a teacher, and early onin my insurance career, I was very activein the Jaycees International, and I wasfortunate to be elected a Senator and lifemember. Participating actively in theJaycees gave me an opportunity to meetother business owners and top executivesin Bermuda and around the world.

I served for several years on theInsurance Advisory Committee, anorganization that assists the BermudaDepartment of Insurance in promotinggood conduct and effective licensing ofagents and companies. I still serve on thecountry’s Hospital Insurance Committee,which is somewhat analogous to the U.S.Social Security and Medicare system.

I was pleased to serve for 12 years on theboard of the Bermuda Commercial Bankand Trust Company, the International TrustCompany of Bermuda, and then later withthe Winchester Global Trust Company.This lead to my connection with OlympiaCapital (BDA) Ltd., a global investmentmanagement company headed up byOskar Lewnowski.

How did your son, Antony, becomeinvolved in business with you?

Antony started out by attending theSchool of Insurance at Howard Universityin Washington, D.C. and interning in theUS with Prudential Insurance. Aftergraduation, he returned to Bermuda,where he became involved with Diamond Company Limited, primarilyadministering the policy service for themany clients who had purchased propertyand casualty insurance over the years.Over time his interest and involvementprogressed to include life insurance andfinancial services.

Now Antony is involved in every aspect ofDiamond Company Limited; selling moreinsurance as well as mastering thefinancial planning areas. On a personallevel, my son is very active in Martial Arts,particularly Thai Chi, and Antony alsotakes time out to manage the parish’ssoccer team.

What about the rest of your family?

We’ve always resided fairly close to oneanother. My father was a small landdeveloper and builder, and now Antony

Page 4 The Register • December 2006

continued on page 5

continued from page 4 The Francis Family

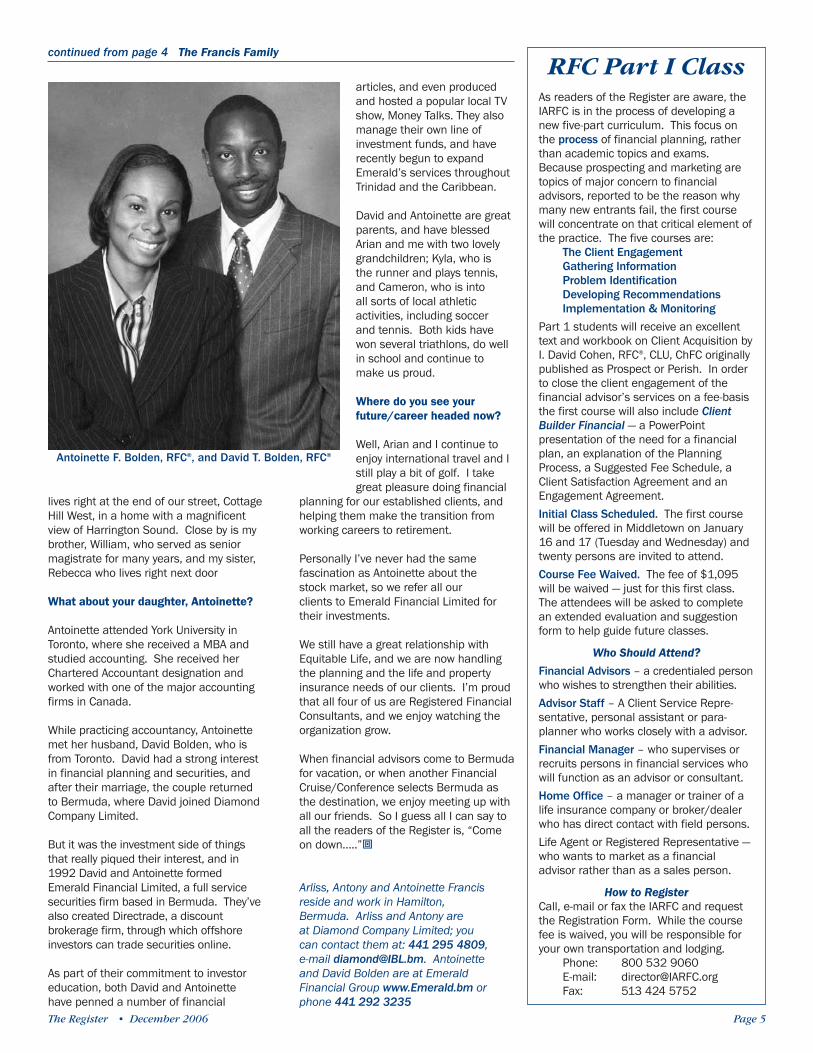

lives right at the end of our street, CottageHill West, in a home with a magnificentview of Harrington Sound. Close by is mybrother, William, who served as seniormagistrate for many years, and my sister,Rebecca who lives right next door

What about your daughter, Antoinette?

Antoinette attended York University inToronto, where she received a MBA andstudied accounting. She received herChartered Accountant designation andworked with one of the major accountingfirms in Canada.

While practicing accountancy, Antoinettemet her husband, David Bolden, who isfrom Toronto. David had a strong interestin financial planning and securities, andafter their marriage, the couple returnedto Bermuda, where David joined DiamondCompany Limited.

But it was the investment side of thingsthat really piqued their interest, and in1992 David and Antoinette formedEmerald Financial Limited, a full servicesecurities firm based in Bermuda. They’vealso created Directrade, a discountbrokerage firm, through which offshoreinvestors can trade securities online.

As part of their commitment to investoreducation, both David and Antoinettehave penned a number of financial

articles, and even producedand hosted a popular local TVshow, Money Talks. They alsomanage their own line ofinvestment funds, and haverecently begun to expandEmerald’s services throughoutTrinidad and the Caribbean.

David and Antoinette are greatparents, and have blessedArian and me with two lovelygrandchildren; Kyla, who is the runner and plays tennis,and Cameron, who is into all sorts of local athleticactivities, including soccer and tennis. Both kids havewon several triathlons, do wellin school and continue tomake us proud.

Where do you see yourfuture/career headed now?

Well, Arian and I continue toenjoy international travel and Istill play a bit of golf. I takegreat pleasure doing financial

planning for our established clients, andhelping them make the transition fromworking careers to retirement.

Personally I’ve never had the samefascination as Antoinette about the stock market, so we refer all our clients to Emerald Financial Limited fortheir investments.

We still have a great relationship withEquitable Life, and we are now handlingthe planning and the life and propertyinsurance needs of our clients. I’m proudthat all four of us are Registered FinancialConsultants, and we enjoy watching theorganization grow.

When financial advisors come to Bermudafor vacation, or when another FinancialCruise/Conference selects Bermuda asthe destination, we enjoy meeting up withall our friends. So I guess all I can say toall the readers of the Register is, “Comeon down…..”

Arliss, Antony and Antoinette Francisreside and work in Hamilton, Bermuda. Arliss and Antony are at Diamond Company Limited; you can contact them at: 441 295 4809, e-mail [email protected]. Antoinette and David Bolden are at EmeraldFinancial Group www.Emerald.bm orphone 441 292 3235

The Register • December 2006 Page 5

Antoinette F. Bolden, RFC®, and David T. Bolden, RFC®

As readers of the Register are aware, theIARFC is in the process of developing anew five-part curriculum. This focus onthe process of financial planning, ratherthan academic topics and exams.Because prospecting and marketing aretopics of major concern to financialadvisors, reported to be the reason whymany new entrants fail, the first coursewill concentrate on that critical element ofthe practice. The five courses are:

The Client EngagementGathering InformationProblem IdentificationDeveloping RecommendationsImplementation & Monitoring

Part 1 students will receive an excellenttext and workbook on Client Acquisition byI. David Cohen, RFC®, CLU, ChFC originallypublished as Prospect or Perish. In orderto close the client engagement of thefinancial advisor’s services on a fee-basisthe first course will also include ClientBuilder Financial — a PowerPointpresentation of the need for a financialplan, an explanation of the PlanningProcess, a Suggested Fee Schedule, aClient Satisfaction Agreement and anEngagement Agreement.Initial Class Scheduled. The first coursewill be offered in Middletown on January16 and 17 (Tuesday and Wednesday) andtwenty persons are invited to attend.Course Fee Waived. The fee of $1,095will be waived — just for this first class.The attendees will be asked to completean extended evaluation and suggestionform to help guide future classes.

Who Should Attend?Financial Advisors – a credentialed personwho wishes to strengthen their abilities.Advisor Staff – A Client Service Repre-sentative, personal assistant or para-planner who works closely with a advisor.Financial Manager – who supervises orrecruits persons in financial services whowill function as an advisor or consultant.Home Office – a manager or trainer of alife insurance company or broker/dealerwho has direct contact with field persons.Life Agent or Registered Representative —who wants to market as a financialadvisor rather than as a sales person.

How to RegisterCall, e-mail or fax the IARFC and requestthe Registration Form. While the coursefee is waived, you will be responsible foryour own transportation and lodging.

Phone: 800 532 9060E-mail: [email protected]: 513 424 5752

RFC Part I Class

Our association is finishing the year with a mixed scorecard – somewhat like a trackmeet where the team has done well in some events, and not so well in others. Let’slook at the results as we near the end of 2006.

Financial Advisor Forum. The attendees all rated the event a solid B. In format, wegot an A because the speakers were great, the old Manchester Inn did a fine job andeveryone enjoyed the reception and the Dunton dinner. But we rated a C- forattendance. It was a real shame, since some of the speakers were truly unique –like Mehdi Fakharzadeh, Norm Levine and Charlie “Tremendous” Jones. Greatbreakout speakers also. For those who attended, an unforgettable event!

Cruise/Conference. Just completed, from New York City harbor to the provinces ofnortheastern Canada. The weather was beautiful, the seas calm, the foliage juststarting to turn and the crew did their best to fatten us all. The program was wellreceived, and for the first time we delivered all the manuscripts on a CD-Rom.

Publications. The “sprint” event: our academic Journal of Personal Finance, editedby the tireless Dr. John Grable. Clearly an A+. And likely to be a repeat winnerunder the new editorship of Dr. Ruth Lytton. Fine articles from academia and somenice ones from the membership. Dr. Ruth needs more from the members next year.

The “distance” event: The Register magazine, probably rates an A- score, but clearlyfinishing the year strongly. The publication grew in size, added more color, and hasincluded some great articles. The Register Editor is incorporating more designsophistication, and our printers, SunGraphics, have held the costs down. Lots ofletters from readers tell us that the publication is being well read. What we clearlyneed next year are more articles from the members — and some advertising.

Cost Control — publication mailings. Here we must give the United States PostalService a clear grade of F — Failure! We applied November 2005 for a periodicalmailing permit to reduce costs substantially. USPS bounced our application betweenMansfield, Akron, Toledo, New York City, Cincinnati and Middletown. It was pass thebuck — our buck, your buck! We circled the one year mark with no progress. Nowwe are nearing the 13th month anniversary and no savings. (We are mailing copiesof this to the postmasters in the faint hope that shame will get some results.)

Website — www.IARFC.org. Mixed scores. The Financial Advisor Profiles are well-liked and clearly the best in financial services. However, many members have notupgraded their own profile and uploaded their photo, although more are gettingaround to it. On the other hand, the book store isn’t in operation and we are stilltrying to get a cleaner look and a more consistent system of uploading files. A clearlow score for our failure to add online CE programs featuring the wealth of talentwithin the association membership. Lots of room for improvement.

International Operations. Resounding firsts to our stars — the organizers in each of the countries: Liang Tien Lung, Jeffrey Chiew, Ralph Liew, Adil Madjid,Preecha Swadspeera, Samuel Yung and Teresa So, Allan Wan, Jerry Tan andDemetre Katsabekis. In each country there are more players on the team who alldeserve ribbons.

Domestic Growth. We are doing well in membership growth, especially since manyorganizations are losing members. A very reassuring note is that most all domesticmembers are coming as referrals – rather than from advertising or other recruiting.

Financial. We aren’t rolling in the dough, but with strong attendance (membershipgrowth) we are getting stronger. We keep expanding the member benefits andimproving the publications — with no debt.

Now, Score Yourself. Have you referred members to the IARFC, submitted articles,attended a meeting, or offered to help at the Forum? Think about 2007….

From theChairman’s Desk...

Page 6 The Register • December 2006

YOUR MOST IMPORTANTNEW YEAR’S RESOLUTION…

Get a Web Site For Your Business!

Do-not-call lists, do-not-email legislationand increasingly web-savvy customersmake the web a “must have” marketingtool for your practice. Gain more referrals,close more sales, and enhance yourprofessional image. Make 2007 your“Year of the Web.”

* AN ESSENTIALMARKETING TOOL

* A SITE THAT REFLECTSYOUR PRACTICE

* EASY TO USE

* JUST OVER $1/DAY!

1.800.593.9228

Use a Year -EndPlanning Memo

• Reaffirm your professional image • Clear, concise communications• Combat competitive pressures • Relieve client anxiety and doubt• Show your clients you care• Address their questions

Are you considering changes to yourmarketing plan? Would you like to seebetter results? If so, you owe it to yourselfto evaluate the ease and effectiveness ofClient Relationship Management.

To check out your IARFC member discount benefit

Call 800 666 1656E-mail: [email protected]

Visit: www.FinancialSoftware.com

Powered by:

SPONSORSHIP: The Plan Competition willhave a corporate sponsor, who will beinvolved in presentation of the awards tothe winning students. An officer will bepleased to announce the participation oftheir firm.

We believe that by emphasis on thewritten Plan and its presentation before a discriminating audience of advisors, the quality of financial plans at theeducational institutions will be improved.

This will be of long term benefit to the academic programs and to thefinancial advisor community. The IARFC is pleased to launch this important andtimely effort to uplift the financialplanning profession.

RECOGNITION: Each school will receive a walnut plaque recognizing thesubmission of a winning plan and a grant to offset the costs of attending the Forum. Each student will receive a parchment certificate and walnut wall plaque.

PREPARATION: Plans may be the product of a single student or a team of up to four students, each of whommust be enrolled as a full-timeundergraduate student in a U.S. basedcollege or university in a financialplanning/services curriculum.

Students may not receive assistance from faculty members or outside financial advisors.

10 THINGS TO ENSURE YOUR SUCCESS IN THE FINANCIAL SERVICES INDUSTRY

PRESENTATION: Each plan may bepresented by one or more students at the Financial Advisors Forum, andattending students and a faculty advisorfrom each school will receive acomplimentary registration for the entireprofessional conference.

PLAN FORMAT: The plan must be placed in a single three-ring binder and accompanied by a CD-ROMcontaining the client files as entered bythe students, including file copies ofsupplemental reports which may beprepared in Word, Excel, PowerPoint or inPDF files if output from a third-partysoftware application.

BASIC PLAN SOFTWARE: The IARFC willpresent to the participating schoolssufficient copies of the Plan BuilderFinancial software, which will be used forthe basic structure of the Plan. It shouldbe noted the Plan Builder softwareorganizes, analyzes and projects numbers— it does not provide recommendations.

PLAN FACT STITUATION: This will beprovided to the faculty advisors andstudents in an unstructured Word file.The students must organize and enter thedata into Plan Builder.

USE IN TEACHING: A college or universityinstructor may use the plan submission asan assignment or for supplemental creditwithin their course. However, theseevaluations or grades will not influencethe IARFC Plan Evaluation Board.

Financial Plan Competition Launched

The first national Financial Plan Competition has just beenlaunched by the IARFC and invitations have gone out tomore than 90 educational institutions. The competition isopen to undergraduate students enrolled in a curriculum ofpersonal financial planning or financial services. It requiresthe submission of a comprehensive personal financial planto be evaluated by a national Plan Evaluation Board of veryexperienced and highly credentialed financial advisors.

The three best plans, and the plan will be invited to present their plans atthe Financial Advisors Forum on May 15-17, 2007 at Bally’s in Las Vegas.Following the presentation of the three finalist plans, the audience ofadvisors will vote as to their evaluation. The winner or winners will beannounced on the final day of the Forum. These student will be primeprospective associates for those advisors seeking personnel growth.

The Register • December 2006 Page 7

DEADLINE: Since the three finalists willbe announced on May 1, 2007 the Plans(with the supporting CD) must be receivedby the IARFC prior to March 15, 2007.

PUBLICATIONS: Two articles will appearin The Register, one when the threefinalist plans are selected, and afterwardan article with photos of the winning plan writer (which may be an individual or team).

The IARFC will also publish a paper in itsacademic publication, Journal of PersonalFinance to be prepared by the planauthor(s), consisting of a summary of thecase, including a balance sheet, incomeand expense, family facts and goalsummary, and the recommendationsmade by the award winner.

FACULTY PARTICIPATION: Each collegeor university will designate one facultymember to accept the responsibility for distribution of materials andcommunications to students and otherfaculty advisors.

SOFTWARE GRANT: This can becomputed by multiplying the retail cost per copy of Plan Builder softwaretimes the number of authorized users at each university.

(Example: 24 x $1,195 = $28,680).

The IARFC has arranged for the Plan Builder software donation fromFinancial Planning Consultants, Inc, andthe IARFC will cover all incidental andcommunication expenses for the Plancompetition, including the judging of theplans submitted.

LOCAL RFC INVOLVEMENT: If anymembers of the IARFC are involved as adjunct or part time instructors at a university we would like to have them participate in distributing the information to their schools, and to encourage the students in theirplan preparation.

If you are involved in any way with aninstitution, please communicate with the IARFC at: [email protected] or 800 532 9060

If you look around the LTCI landscape,you’ll see many changes have occurredduring the past two years. Someinsurance companies got out of themarket, some companies have hadsignificant premium rate changes, andnow your prospects are getting moresavvy about how to buy this insurance andwill ask key questions about LTCI and thecompanies which you represent.

It’s not possible to stand still. As advisorswe have to look to 2007 and welcomethese changes in products and how to sellthem effectively, because those changesare not going away. You can’t sell LTCI thesame way you did 5 or 10 years ago. Youcan’t promise the client that there won’tbe rate increases. And, you can’t promisea client that the cost of healthcare won’tcontinue to skyrocket.

When you’re creating your prospectingplan, scramble your marketing strategy abit. There isn’t a sure-fire solution forevery marketplace or prospect, no matterwhat the advertisers tell you. Try directmail; give talks to your local Rotary, Lion’sClub, or women’s investment groups. Putan ad in the paper or take some time onCable TV to do an Infomercial. Give anafternoon tea and dessert event to ask your clients for feedback. Ask 10 key clients to be on your AdvisoryBoard each year. They’ll certainly tell you about the competitors they see in your marketplace and what theylike or don’t like about them. Thisinformation is SO valuable to yoursuccessful marketing efforts! Clients love to help and will feel very honored that you want their input. Use it to your advantage.

Next, when you’re working with clients,don’t assume that every individual needsthe same type of LTCI plan. The averageperson who buys an LTCI policy today ismuch more informed than they were 5yeas ago. Yes, the average person stillneeds about 3 years of coverage as aminimum, but that’s not the only solution.Every person wants to believe that they’llnever need to use their LTCI plan, andwe’re living longer than ever.

Denial will always be a factor in the LTCIsale and no matter how good the productsare your healthy client does not want toimagine their health changing so muchthat they would actually have to use thebenefits of an LTCI policy. Beprepared to address theirfears calmly andproceed throughyour salespresentation.And, by allmeans, don’tignore whatthe clientsays to you.Otherwise,you mightnot be ableto close later on.

As advisors, weneed to look atthe client’s completefinancial picture, inaddition to the questionsyou’ll always ask about theirhealth and family’s longevity factors.When you prepare some proposals foryour client, factor in the client’sguaranteed income factors, inquire abouttheir life insurance and determinewhether some of the life plan’s deathbenefits could be used to pay for any carein the future. Ask your client couple aboutthe preparations they have made for achange in income when the first onepasses on. Some advisors even considerLTCI to be a portfolio protection plan.

For clients who can’t health-qualify forLTCI coverage, be prepared to offer somealternative solutions. Their familymembers may need to give input, andthose same family members can becomeyour next clients when they watch youprepare and offer solutions to their Mom and Dad.

Whatever situation you have with a client and their financial picture, you can find a solution that will fitperfectly for them. It probably won’t be the solution that you’ve been selling on a regular basis though. The days of selling only the stand-alone LTCIpolicies are just about over. The Advisorwho learns the basics of selling LTCI andthen fine-tunes their sales presentation to encompass the client’s financialsituation will be the Advisor who WINSconsistently in 2007.

Join Wilma Anderson in Las Vegas atthe 2007 Financial Advisors

Forum during herpresentation

“Matching LTCOptions for the

More-SavvyProspect &Client,” andlearn how tofine-tuneyour sellingskills forthe more-savvyprospect and

client!Skillfully meet

the needs of the50 year olds who

may not see theneed for LTC right now,

learn how to open theGroup sales market in your

area, and learn how to offer the non-traditional plans to the 60 or better-agedclient/prospect.

Wilma G. Anderson, RFC®, is known in the industry as The LTC Coach, and is a practicing producer and InvestmentAdvisor Representative in Littleton, CO.Through the LTC Coach, Wilma offerssales workshops. DVDs and sales systems that help Advisors to boost their LTC and annuity sales to the senior market. She can be reached [email protected], or 720 344 0312. www.theLTCcoach.com

In 2007, Keep Changing to Mirror the LTCI Market Place & Prospects

Wilma G. Anderson, RFC®

Page 8 The Register • December 2006

At a recent ContinuingEducation session of the IARFC-Taiwan,certificates were presentedto the most recent 80graduates in the publicauditorium of the CentralNewspaper Building.

Over 300 RegisteredFinancial Consultants wereassembled for the half dayeducational event. Therecent accomplishmentswere saluted by IARFCChair, Ed Morrow, who wason hand for the ceremonyand was one of the CE presenters.

The IARFC has establishedregular RFC classes in thefollowing cities: Taipei,Kaohsiung, Taichung,Tainan, Hualien andTaoyun. It has also heldclasses in the trainingfacilities of fifteeninsurance and insurancebrokerage organizations.Local RFC clubs meet on amonthly basis to exchangeideas and participate incase studies. This is inaddition to quarterly CE events sponsored by IARFC-Taiwan in major cities.

Each RFC in Taiwan nowhas access to a websitewww.IARFC.org.tw thatprovides communicationand distribution services.On a regular basis eachmember also receives anelectronic newsletter.Quarterly there isdistribution of a 48 page printed magazine/newslettercalled the Register — and persons alsoreceive the monthly Advisers magazine

The number of Registered FinancialConsultants in Taiwan has increased from150 in March 2004 to 1,100 in March2006 and by end of year the number ofRFCs in Taiwan will reach 1,300 based oncurrent class enrollment in six cities.

Nearly 200 articles in Taiwanesepublications with subjects related tofinancial planning have been aimed ateducating local citizens in Taiwan to

understand the importance of financialplanning and hiring a professional advisor.

IARFC-Taiwan has formed a strategicalliance with the Economic Daily, Taiwan’smost important financial newspaper,causing the IARFC to become well knownin financial circles. RFC members cannow have their articles published inEconomic Daily every two weeks toprovide financial information, and topromote the designation to the public.

The RFC has become the leading brand offinancial certificate in Taiwan, far beyondthe competing designations andeducational programs.

Agreements have beenexecuted with the followinginstitutions to promoteRFC: ShinKong LifeInsurance, ING Life Insurance, Fubon LifeInsurance, AEGON Life Insurance, GAMCInternational FinancialGroup, PCA Life Insurance,Insurance Brokers’Association, HonestyInsurance Broker Company,Rock Financial RiskServices, HoyaworldInsurance Broker Company, Kon Hsin Insurance BrokerCompany, Ho Tai Insurance Broker Company, WeiLin Insurance BrokerCompany and ChiayiInsurance Union. Theseorganizations haveendorsed the RFC coursesfor their associates andthey strongly encouragecontinuing education.

An RFC ElectronicNewspaper is delivered to all Taiwanese RFCmembers with the purposeof providing updatedinformation and news.Each month RFC membersin Taiwan also receiveAdvisers magazine, a 120 page publicationfeaturing articles forfinancial advisors andinsurance agents, oftenincluding articles by RFCs.

The new IARFC-Taiwanwebsite www.IARFC.org.twprovides various data to allRFC members Each majorcity in Taiwan now has an

“RFC Club” as a platform for all membersto interact and communicate with eachother so as to expand each one’sprofessional network and exchangeplanning techniques.

IARFC-Taiwan is under thecapable leadership of RichardWu, RFC® who can be reached

Taiwan RFC Growth

The Register • December 2006 Page 9

Addressing the most recent RFC Graduation Ceremony and CE session inTaipei is Mr. Liu Chung Sheng, the General Manager of Polaris Securitiesof Hong Kong and Polaris Holdings of Taiwan. He addressed the group onFinancial Planning and Investments in the Golden Triangle of Taiwan,Hong Kong and Macau. Mr Liu is also the publisher of two prominentmagazines, Financial World and Info on Wealth that are widely read.

How do you forward e-mails? A recentsurvey of sophisticated business users ofthe Internet revealed that having to glanceat and delete all those pesky messages atleast 50% do not! In fact nearly 100% donot follow “good forwarding” procedureson a consistent basis

Do you wonder why you get viruses orjunk mail? Don’t you hate it? One of theculprits may be you — and the way you areforwarding e-mail messages.

Every time you forward an e-mail there isinformation left over from all the peoplewho got the message before you, namelytheir e-mail addresses and names. As themessages get forwarded along, the list ofaddresses builds, and builds, and builds.All it takes is for some poor sap to get avirus, and then his or her computer cansend that virus to every E-mail addressthat has come through his computer. Or,someone can take all of those addressesand sell them to a junk mail marketer inthe hopes that you will go to their site andhe will make five cents for each hit.That’s right, all of that inconvenience overa nickel! How do you stop it? Well, thereare several easy steps:

1. When you forward an e-mail, DELETEall of the other addresses that appear inthe body of the message (at the top).That’s right, DELETE them. This is quiteeasy — just highlight them and deletethem, backspace them, cut them,whatever it is you know how to do. It onlytakes a second. However, you MUST clickthe “Forward” button first and then youwill have full editing capabilities againstthe body and headers of the message. If

you don’t click on “Forward” first, youwon’t be able to edit the message at all.

2. Whenever you send an e-mail to more than one person, unless it is to very select persons with whom you doregular business, do NOT use the To:or Cc: fields for adding e-mail addresses.This placement adds their names visiblyto all other recipients, and exposes them,and you, to the interest of the “e-mailaddress collectors.”

3. Always use the Bcc (blind carbon copy) field for listing the additional e-mail addresses. This way the peopleyou send to will only see their own e-mailaddress. If you don’t see your Bcc: option click on where it says To: and your address list will appear. Highlight the address and choose BCC and that’s it, it’s that easy. When you send toBcc your message will automatically say“Undisclosed Recipients in the “TO:” fieldof the people who receive it.

4. Remove any “FW:” text in the subjectline. You can re-name the subject if youwish or even fix the spelling. “FW” in the subject line is a field that attracts the attention of e-mail collectors, because it often is accompanied by listsof e-mail recipients.

5. Always hit your Forward button fromthe actual e-mail you are reading. Everget those e-mails that you have to open10 pages to read the one page with theinformation on it? By forwarding from justthe actual page you wish someone toview, you stop them from having to openmany e-mails just to see what you sent.

Do You Really Know Where Your E-Mails Go?

6. Have you ever gotten an e-mail that isa petition? It states some political orreligious position and asks you to addyour name and address and to forward itto 10 or 15 people or even to send it toyour entire address book. This petition e-mail can be forwarded on and on andcan collect thousands of names and e-mail addresses. The completed petitionis actually worth a couple of bucks to aprofessional spammer because of thewealth of valid names and e-mailaddresses contained therein. If you reallywant to support the petition, send it asyour own personal letter to the intendedrecipient. Your position may carry moreweight as a personal letter than whenaccompanied by a laundry list of namesand e-mail address on a petition.

7. Be wary of the e-mails that say thatsomething like, “Send this e-mail to 10people and you’ll see something great runacross your screen” or “If you forward thisnow, you’ll receive good luck or 200prayers.” Or sometimes they’ll just teaseyou by saying “something really cute willhappen.” It won’t happen! There is nomechanism for counting all those whoforwarded an e-mail and sending themsome sort of congratulatory message,photo, or prayer.

8. Before you forward an ‘Amber Alert’ ora ‘Virus Alert’, or some of the other onesfloating around nowadays, check them outbefore you forward them. Most of themare junk mail that’s been circling the netfor years! Just about everything youreceive in an e-mail that is in question canbe checked out at Snopes. Just go towww.snopes.com. It’s really easy to findout if the warning message is real or not.If it’s not, don’t pass it on.

9. Just use a little extra care whenforwarding messages. Already, there areenough pirates, hackers, spammers, andmalicious operators on the webs. Theydon’t need our help!

10. If your colleagues, compatriots, family and friends need to receive thismessage, e-mail [email protected],request the Forwarding Memo and we will reply with an electronic copy you canthen forward — using BCC, of course!

Ed Morrow, CLU, ChFC, CT, CFP®, CEP,RFC®, is chairman and chief executive ofthe International Association ofRegistered Financial Consultants.

Page 10 The Register • December 2006

Your prospects andclients have onething in common —each is hungry forsincere appreciation.Most feel that othersdo not recognize orappreciate their trueworth. Praise andappreciation canwork wonders inbuilding long lasting,viable relationships.Here’s an interestingillustration:

In the fall of 1860,the steamship “Lady Elgin” set out with atotal of 393 passengers and crewmembers, to make the trip from Chicagoto Milwaukee. Just off the shore ofEvanston, she was rammed by a lumberschooner and sank. As a result, 279 ofthe passengers and crew members died.Of those who were saved, 17 of themwere saved by a student at NorthwesternUniversity, Edward W. Spence. Spencemade 16 trips in all fromthe shore to the sinkingship and back again,saving the 17 lives.

Because of physicalexertion and the coldnessof the water, Spence was inshock at the end of the16th trip. It was reportedthat as they carried him tothe hospital, he kept askingthe question, Did I do my best?

Unfortunately, as a result of the incident,Edward Spence spent the remainder ofhis life as an invalid in a wheelchair.

Fifty years later, Northwestern Universitygranted him a Bachelor of Arts degree,not because he ever finished the classwork — he didn’t. He was awarded thedegree because they decided he deservedit. A bronze plaque commemorating hisheroism was placed on the wall of the oldCoast Guard Station at the southeastcorner of the campus — and it hangsthere yet today.

When he was 80 years old, on theanniversary of the sinking of the “LadyElgin,” Edward Spence was interviewed byChicago newspaper reporters. They askedhim, What is your most vivid memory ofthat tragic fall day when the “Lady Elgin”went down off the coast of Evanston?

Mr. Spence’s answer was, Not one of the17 people whose lives I saved ever cameback to say thank you — not one.

There is not enough appreciation in this world. Maybe people feel a bituncomfortable saying, Thanks. Maybe they feel that somehow peoplealways know they appreciate a gesture.They don’t!

The IARFC has developed a wonderful toolfor advisors to use in expressingappreciation — the Personal Note Card,with the Gold IARFC key on the front andthe Code of Ethics on the back. They areinexpensive, but when completed with ahandwritten message of just ten or fifteenwords — terribly effective. They areavailable in boxes of 250 for $100, andwe’ll even include a Blue Gel Pen in acomplimentary color, dark blue. Foradded impact, you can seal the envelopeswith a one- inch IARFC gold seal that costs$30 for 250.

The above article was adapted from theMonday Morning Message, distributedelectronically by Kinder BrothersInternational of Dallas. Jack Kinder, GarryKinder and Bill Moore are all RFCs andactive members of the IARFC. For moreinformation on their services, see:www.KBIgroup.com

Do You Say “Thanks” Often Enough?

The Register • December 2006 Page 11

Look for opportunities to express appreciation.People want recognition as individuals more thanany other single thing — even those who neverperform a heroic act.

Client appreciation requires tangibleactions that set you apart in the eyes ofclients as an individual who truly cares.And that’s Boxes by Pandora’s solemission: To help you demonstrate clientappreciation in a noteworthy andaffordable way!

From specialty document wallets andfolders that will make your presentationsmemorable, to worry-free documentfiling systems that will create naturalcross-selling discussions — you’ll findthem all here!

Our specialized manufacturing andproduction facility can personalize all ofour products with engraved brassnameplates, as well as your name andcompany logo.

If you’d like your VIP clients to thinkpositively about the services you provideon almost a daily basis, then our custom-made, personally imprinted clientappreciation boxes — created from selectwoods — are for you! Their rich, functionaldesigns will have all your clientsshowcasing them on desks, credenzas,and display cases.

Boxes by Pandora has special pricingfor IARFC members. For additionalinformation, a full brochure orto order call: 800 232 6937 orvisit: www.BoxesByPandora.com

Go Ahead and Impress Your Clients

The Registered Education Planner (REP®)preparation study course and examinationis offered by the First Financial EducationCentre, a 501(c)(3), education non- profitcorporation. The many opportunities forcommunity service available to RFC’s incollaboration with FFEC will be discussedin future articles. You may browse theirwebsite at 1fec.org if you wish tocollaborate on a project now.

What is the Designation?

The Register Education Planner (REP®) isa professional designation awarded by theInternational Association of RegisteredFinancial Consultants to those financialadvisors who can meet the highstandards of education, experience andintegrity required of all its members. Thisstudy course provides a resource toFinancial Advisors who want to offereducation planning services and productsto parents in preparation to pay foreducation and addressing the collegeadmissions process.

You may be wondering “who needs aRegistered Education Planner?” Oneanswer may well be approximately 13 million families!

These families need the help of a memberof the IARFC who has completed theeducation requirement for the professionaldesignation; Registered Education Planner.Another may be Baby Boomers, 50% ofthe Boomers are between the ages of 40-50 and 50% are between the ages of 50-60. Their children are either in college, orin the process of attending college. Manyof these people are already a client of anRFC. Many need help finding solutions toavoid using retirement savings to pay fortheir children’s education; this is a veryemotional issue.

Let’s look at some very startling facts:According to the College Board’s,www.collegeboard.org, 2005-2006analysis of college costs, the averageannual cost to attend a four-year publicuniversity is now $15,556 and a four-yearprivate school is $31,916. Elite privatecolleges like Harvard can approach$50,000 per year!

College costs are generally paid for with after-tax dollars, which means in the 28% tax bracket you must actuallyearn $18,655 to pay the public university$12,500. Remember, this is the cost for ONE year for ONE child. Using the tax benefits available to pay for aneducation provided by the government isa very important part of the overalleducation plan.

So what is the purpose of the program?

The REP education program introduces abusiness process that will provide afoundation for a planning and advisingrelationship on financial matters. Theplanning focus is on training advisors todeveloping a clientele. In this process theadvisor will grow as his/her clients grow.In many situations a RFC will use anintern to assist in offering educationplanning to serve his/her clientele and thecommunity. This is a great benefit tocollege students who are interested in acareer as a financial advisor.

The Ethics Pledge of the IARFC isapplicable to all who complete the REPcourse. The experience requirement is aprofessional financial planner who isactive in financial planning and wishes toadd education planning and funding toservices they already offer. Theparticipant in the program receivesapproximately 150 pages of course

materials, bound in a study notebook,plus various handout pages developed by the instructor to share common areas of interest expressed by thestudents, along with Excel spreadsheets.For more information visit the FFECwebsite at 1fec.org.

Attendees must pass a writtenexamination at completion of the REPcourse and then will be granted the REPprofessional designation. Then they usethe term Registered Education Planner(REP®) on their brochures, stationery andbusiness cards. (John Advisor, REP orJohn Advisor, REP®, RFC®)

A Registered Education Planner (REP®)must complete 10 hours of professionalcontinuing education in college planning,grants, loans and financing annually inorder to maintain the designation as aRegistered Education Planner (REP®).This would also qualify for RFC, so it doesnot increase the RFC’s CE requirement.

Persons successfully completing allrequirements will become members of the International Association of Registered Financial Consultants (a non-profit professional education and practice support organization) and their names will be published on the IARFC website www.IARFC.org alongwith additional professional qualificationsand background.

The Registered Education Planner is not a degree, but a professionaldesignation, certifying that the individualhas satisfactorily completed all therequirements of the IARFC for thatprofessional designation. The term willnot be used in connection with anyproduct or service offered to the public or in commerce.

Registered Education Planner (REP)A Window of Service Opportunities

Display the IARFC Code of EthicsPlaque For Your Business!

Where does the IARFC stand? We solidly re-affirm our Code of Ethics. Thesimple, straightforward yet thorough Code is easily and clearly understood byconsumers as well as other advisors. Proudly Display Your Code of Ethics Wall Plaque in the entrance of your office,waiting area or in the room where you meet with clients. Handsomely placedbehind clear plastic on a walnut base

(8.5” x 13” — with some assembly required)Call Today and order the IARFC Code of Ethics wall plaque at a cost of $50plus $10 shipping: 800 532 9060

Page 12 The Register • December 2006

at any price. In short, create such valuethat a client would be lost without yourinvaluable services.

2. Place a high value on your peopleskills, your emotional intelligence.Many years ago Dale Carnegie discoveredthat the reason over 90% of all employeeslost their jobs had nothing to do with their innate ability for doing the work, but had everything to do with their peopleskills, or their ability to get along withother people.

You will also find that whether you arebeing selected and hired into a positionas an employee, or whether a client wantsto secure your services as a consultant,most people will not hire you unless theylike you. So your day in, day out, messageneeds to emanate “you can like mebecause you trust me”.

Although we are in an industry that has ahigh focus on technical issues and logicalconclusions, never forget that people buyon emotion and justify it with logic.Whenever you make a recommendation toa boss, a client or customer, make sureyou can relate it to the right hemisphereof their brain, the emotional half. Oncethey are excited about the outcome, thengo through with the logic and reasoning tojustify the decision.

If this is a weak area for you, read a booksuch as Dale Carnegie’s, How to WinFriends and Influence People or take acourse on emotional intelligence. It willprobably be the best continuing educationyou will ever get.

3. Give 110%, or under promise and over deliver. I sometimes think that your generation has been completelycast as “slackers”. Sure, there are a few slackers out there, but I see a lot of very dedicated young people, anxious to do whatever is necessary to accomplish their goals. Nevertheless it does seem that high quality service has become a thing of the past! Ifrequently feel as if I am living in AynRand’s book, Atlas Shrugged andeventually our whole infrastructure willdecay and it will be impossible to get a car or train or plane to go anywhere safely or on time.

A Mom’s Letter to Her ChildrenBy Katherine Vessenes, JD, CFP®, RFC®

Dear Loved Ones:

As you are completing college and starting in your career, you will be facing a lot of challenges and many wonderfulopportunities. I have often felt in my career that I was crawling through the jungle with a flashlight and amachete. Perhaps I was blazing the trail for you. Let me give you the advice I wish someone had been able to give meearly in my career. It would have made ahuge difference.

Here are the ten lessons that I think areabsolutely crucial for your achievingsuccess in the financial services industry:

1. Make yourself indispensable.We are currently facing an unprecedentedmedia glut of information in all areas of our life. It is particularly pronounced in the financial area. Our clients andcustomers are absolutely overwhelmedwith a mind-boggling array of details, data and conflicting information abouttheir finances.

A crucial part of your mission is to makesense out of nonsense, to work your waythrough the glut of information andsimplify it into a few clear choices for yourclients. An important part of your job is tomake life easier for your clients. Inwhatever way you do that, make sure thatyou become absolutely indispensable forthem, whatever you provide for yourclients, they could not get any other place,

This malaise over excellence puts you in agreat position. Remember, most of thecountry has seen the world class serviceof Disney World. It is the kind of servicethey would like to expect in every part oftheir lives, and are all too disappointednot to receive. If you can give that worldclass service consistently you will becomeindispensable to your clients and they willmake you very successful.

4. Figure out what the client wants and give it to them. As you take on your new position, it is important for youto think in terms of who is the client? Ifyou are being hired into a corporation,part of who is the client will definitely beyour boss or your superior. If you areworking as a consultant or an advisor,your client is a person who wants to retain your services.

Few people have figured out this basicconcept. I was talking to a large brokerdealer recently and they said to meproudly, “We finally figured out who theclient is!” I looked at them with light in myeyes thinking maybe somebody has finallygotten the picture. He continued, “Weknow our client is the investor,” he saidproudly. I was really dismayed becausehe had missed who his real client was.His real client was the rep! His realmission was to help the rep serve therep’s client, the investor.

The first step in this process is figuring outwho your client really is. Then discoverwhat they really want and how can yougive it to them.

Here are a few questions that you can askthat client: in three years what will makethis relationship worth your time andmoney? How would you define asuccessful relationship? What can I do tomake this relationship work better foryou? What do you really expect of me?Once you have the client’s expectationsclearly in mind, remember your goal andyour mission is to exceed thoseexpectations 100% of the time.

5. Take time to play. Yes, I know youcannot believe this is coming from yourmother, but a well balanced life not only

continued on page 14

Katherine Vessenes, JD, CFP®, RFC®

The Register • December 2006 Page 13

continued from page 13 Compliance-Friendly Marketing

brings you the energy to serve yourclients, but the inspiration you need tostay at the top of your game.

6. Make friends. “When you need afriend it’s too late to make one,” saidMark Twain. This industry has been,amazingly generous to me. I have hadpeople offer me money during thin times.I have had others who generously calledand said, “Katherine I’ve got a newbusiness venture for you. This is what Ithink you should do, and I’ll be your firstclient. After you’re finished with me, I’llhelp sell this idea to others.” In short, Icould never have survived in this industrywithout my many generous friends. Isometimes think we get far too involvedon the “work”, crunching the numbers orreviewing the alternatives, and spend toolittle time on the intangibles, makingfriends for life.

The best way to make a friend is to beone. Go out of you way to be kind. I try toalways ask, “What can I do to help youout?” Sometimes it is something assimple as introducing them to anotherfriend where the synergy could be goodfor both of their businesses.

7. Be honest, even if it hurts. You know we have always believed thathonesty is the best policy, but it was really put to the test a few years ago. I was just finishing up my first book, The Compliance and Liability Handbook,where I included a section on how tochoose a good insurance company andhow to choose a broker dealer. By thattime I had left the financial planningpractice and was lecturing and writing onthe subject, when I got a notification thatone of my former clients was planning towithdraw all of the money from his lifeinsurance policy.

Normally this would not have caused me any alarm. In this particular case the clients were a couple who had been friends of mine. It had been mypractice, dating from my years of legal experience, to always make husband and wife joint owners of any life insurance policy. This meant thatneither person could cancel a policy orwithdraw the cash without the other’spermission, which was designed to protectthem if they should divorce. In this case,Hubby, after 30 years of marriage walksout and moves to Alaska with Bambi. The wife, a hard worker, labored for years to pay off his debts and diligentlywas making payments on this whole life insurance policy on her husband.

Apparently, Bambi could not supportHubby in the style to which he wanted to become accustomed and he wanted to take the money out of the policy, which of course, had all been put there by his wife.

When I looked into the policy in greaterdetail I discovered that the insurancecompany had made a mistake and hadnot made them joint owners as I hadoriginally instructed. Naively, I call them up, explain the situation andexpected them to rectify it. After all, it was the right and honorable thing to do.They basically told me to kiss off.Ironically, my own insurance companycompletely failed the checklist I waswriting about in my book. It took all myenergy not to threaten to expose theirsorry behavior. I kept my mouth shut andtheir guilty secret will go to the grave.Step two was to crank up the people skillswe described in number 2. I eventuallyconvinced them that they should give meat least a week to see what I couldarrange on my end of the deal beforereleasing the money.

It was at that point that my entire lifepassed before me. I could see the wifesuing me for loosing the $300K lifeinsurance policy when her husband died, and I was frankly wondering howlong it was going to take to bankrupt us. I spent a couple days scurrying around to get things fixed to no avail. I alsodiscovered this company no longer hadE&O insurance on me and I realized I was going to have to call the wife andexplain to her the situation. She is highly emotional and I knew it was notgoing to be easy. I took a deep breath,got caught up on my prayer life, and called her. I explained what had gone on and also went on to outline that she had a couple choices. I explained the first choice was that she could filethat long awaited divorce and get thecourt to issue a temporary restrainingorder, preventing Hubby from withdrawingthe funds. She could do nothing, and loose all the money. She could sue the insurance company, or, (and Itook a deep breath), she could sue me. I felt I had to give her all the alternatives.At first she laughed, and then she cried. Eventually she got an attorney and got a restraining order against herhusband. She never did sue me. In factshe was so pleased with how I handledthe affair and how hard I worked on herbehalf that she sent me a gift certificatefor a massage. So, always be honest,even when it hurts.

8. Become an expert at something.Part of becoming indispensable andabsolutely invaluable to your clients is tolearn a particular area of information thatis critical and in high demand. I know oneperson in this industry who specializes inhelping the very wealthy who haveinherited their money. She is the onlyperson I know in this area. By the way inthe unlikely event that your father and Ileave you vast sums of money, I hope youwill go to her to work it out.

I came across this concept of expertise quite by accident in 1991 when I was working with the IAFP tocomplete my first book. One wise soul,who has since become one of my manydear friends, suggested that a uniqueangle would be to take all the complianceissues and weave them with a marketingspin. It was an absolutely revolutionarythought and I have made the most of itever since. Now my focus is themarketing and compliance issues facingthe industry. Although there are a fewcompliance people in the industry andlots of marketing types, I do not know ofanyone else who does what I do: turncompliance into a powerful marketingtool. I did not realize I had become anexpert until last year when BloombergPress was promoting my second book, Protecting Your Practice, and called me “America’s best knownauthority on the legal, ethical andcompliance issues facing financialadvisers.” I looked at this statement for a full ten minutes trying to figure outwho they were talking about.

A corollary to this rule is that if subjectmatter you want to become an expert at is unpleasant but also critical, so much the better. Other people are notgoing to take the time to learn it, and youwill get a chance to excel. One law firm Iknow really used this point well. Theytook a small area of insurance law andwrote a ten page report of the ins andouts of this particular portion of theirbusiness. They sent it to all of theirclients and prospects. Every year theyupdated it and it kept getting larger and larger. It is now a 300 page bookthat is absolutely critical to the industry if you really want to understand this areaof law. They found a niche; they becamean expert.

9. Identify your gifts. Dan Sullivan of theStrategic Coach has done a great job ofgetting his clients to focus on their

Page 14 The Register • December 2006

continued on page 15

continued from page 14 Compliance-Friendly Marketing

“unique ability”. Your unique abilities are those things for which you areunusually gifted. When you do theseactivities, you get energized and you reap extraordinary results. I know one of my gifts is communication, particularlyto audiences. I love giving theminformation that will make their livesbetter. It energizes me and we getextraordinary results.

Regrettably, a lot of our life has beenworking outside our unique abilities, in theareas Sullivan would call incompetence,competence, and excellence. I have foundapplying this principle brings far greaterresults. Life is easier and a whole lotmore fun. This can only lead to yourlongevity, if you are working in your unique gifts.

So now is the time to start thinking abouthow you are uniquely gifted. This willbecome more clear to you over your nextfew years of employment. Eventuallywhen you are old, wise, and say over 40,your goal will be to work at least 80% ofyour time in your unique ability.

10. Remember Whom you serve.I could sum up all of these thoughts inthis last concept. It helps for us not to gettoo high an opinion of ourselves andrealize we are only servants. We may beserving a boss, a corporation, or a client.Our role, in addition to making sense outof nonsense and making their life easier,is to serve them.

Ultimately though, we have anotherPerson we serve. We serve the Creator ofthe Universe, He who created honesty,truth, and your unique abilities. So yourMom’s final advice to her three lovedones: remember that everything you doshould reflect the attributes of thisCreator and God bless you. I am veryproud of you.

Love and kisses, Mom.

Maybe you ought to consider writing asimilar letter to your children...

Katherine Vessenes, JD, CFP®, RFC®, is anationally known author and speaker,focusing on sales, marketing, complianceand practice management issues forbroker/dealers and advisors. Look forher latest book: Become a MultimillionDollar Financial Advisor. She can bereached at [email protected].

The Register • December 2006 Page 15

Implement strategic steps to improve your practice — to help you work on your practice instead of working for your practice.

Save $200Save $200 when you mention this ad

Develop high quality comprehensive financial plans — Retirement Planning,Insurance Needs, Education Funding Create unlimited “what-if scenarios”— including Monte Carlo simulationsPresent product solutions powerfully and swiftlyEasily justify a substantial planning fee to help you work on your practice instead ofworking for your practice

Track prospects, clients, follow-ups, appointments, Select from hundreds of lettersand articlesRun Targeted Drip Marketing CampaignsIdentify clients and prospects by needed products, services or items of interestImplement Due Diligence and Liability Protection

The presentation system for financial advisors that motivates the prospect to engageyour services on your preferred basis. It is ideal for helping you charge a separate feefor the financial plan. A sample (editable) Plan Fee Schedule is included.

Solutions creatively designed, continuously enhanced, well-trained and supported to help build your success.

[email protected] 800 666 1656www.FinancialSoftware.com

Following our recent trips to China andIndia we had an opportunity to join upagain, this time in the playground of therich and famous of America, PalmSprings, California. Actually we werenearby in Palm Desert at the convocationof the Top of the Table, the signatoryevent of the Million Dollar Round Table.Over 400 of the world’s most successfulinsurance sales persons were gathered innearly palatial surroundings, sculptedponds, waterfalls and walkwayssurrounded, as you would expect, by palmtrees. About half the attendees were fromoutside the United States, reflecting thegrowing number of professionals and thegrowing size of their affluent constituencyaround the world.

In China, the atmosphere of the generalpopulation had been one of confidentcommercial exuberance and rampantconstruction. Everywhere people werebusy — industriously at work,communicating constantly by cell phone,text messages or computer. The messageseemed to be, “how can we do businesstogether, quickly and profitably?” Theattitude of agents and advisors at theconference was, “Tell me more, quickly!”

In India, the pace was slower and withoutthe same passion for organizationalstructure, order and cleanliness. Theatmosphere had been one of capitalismand friendliness. Smiling and caring facesrose above the more colorful dressmaking quick eye contact, with a messageof “You seem to be an interesting personI’ll like to become friends…perhaps wecan find away to do business together?”The agents and advisors were more open, “I’m looking for techniques andmarketing skills!”

However, in the bastion of rampant andsuccessful capitalism, we found everyonebusy at their task — whether it be work,leisure or travel. In prosperous selfconfidence the beautiful people ofSouthern California, and those who servedthem and visited them, all seemed to say,“I’m very diligent, decisive and successful— and I’m moving forward to new heights,but there is a possibility I can take sometime out to help you, if you’re interested?”The attitude of the leading producers was,“Tell me more about what you’redoing…and let me tell you what I’m doing.”Sharing needed to be a two-way street.

We are pleased to report that thepredicted demise of the life insurance

career is premature. Successfulproducers are growing even moresuccessful. But as Tony Gordon, pastpresident of MDRT and a native ofEngland indicated, “The times arechanging and the insurance business ischanging rapidly.”

Those who are adapting to these changes,and in fact those who are creating anddriving those changes, were wellrepresented at the Top of the Table.

Some, of course, were enjoying successbecause they are using efficiencies to merely do more of the same thingthey’ve been doing for recent years. But this is not the norm. Most of the top producers are aggressively seekingout new economic opportunities, newproducts and new operating models. One cannot really call this group “lifeinsurance sales men and women.” They are that, but now they are muchmore, as most of their business cardsindicate. Very few had the logo or nameof a life insurer on their cards. Their titleswere not “agent” “senior agent” or“district manager.” Their company wasusually a reflection of diverse financialinterests such as: “Regional FinancialGroup” or “Smith Financial Success.” The logo was not a familiar icon ofinsurance but often an amorphousacronym or initials. Their title was usually“President”, “CEO” or “Principal.”

But there were designations abounding —the prominent ones being CFP®, ChFC, andRFC®. But there were also some with CLU,

CFA, and CPA. A surprising numbersported degrees; MBA, MSF, J.D. and LL.M.