The Consumer Financial Protection Agency and Other Financial Regulatory Reforms John P. Kromer...

22

The Consumer Financial Protection Agency and Other Financial Regulatory Reforms John P. Kromer Clinton R. Rockwell Jon David Langlois Washington, DC Los Angeles, CA Washington, DC Experienced Specialized Accomplished Cost- Effective Collaborative

-

Upload

imogen-bradley -

Category

Documents

-

view

216 -

download

0

Transcript of The Consumer Financial Protection Agency and Other Financial Regulatory Reforms John P. Kromer...

The Consumer Financial Protection Agency and Other Financial Regulatory Reforms

John P. Kromer Clinton R. Rockwell Jon David LangloisWashington, DC Los Angeles, CA Washington, DC

Experienced

Specialized

Accomplished

Cost-Effective

Collaborative

2

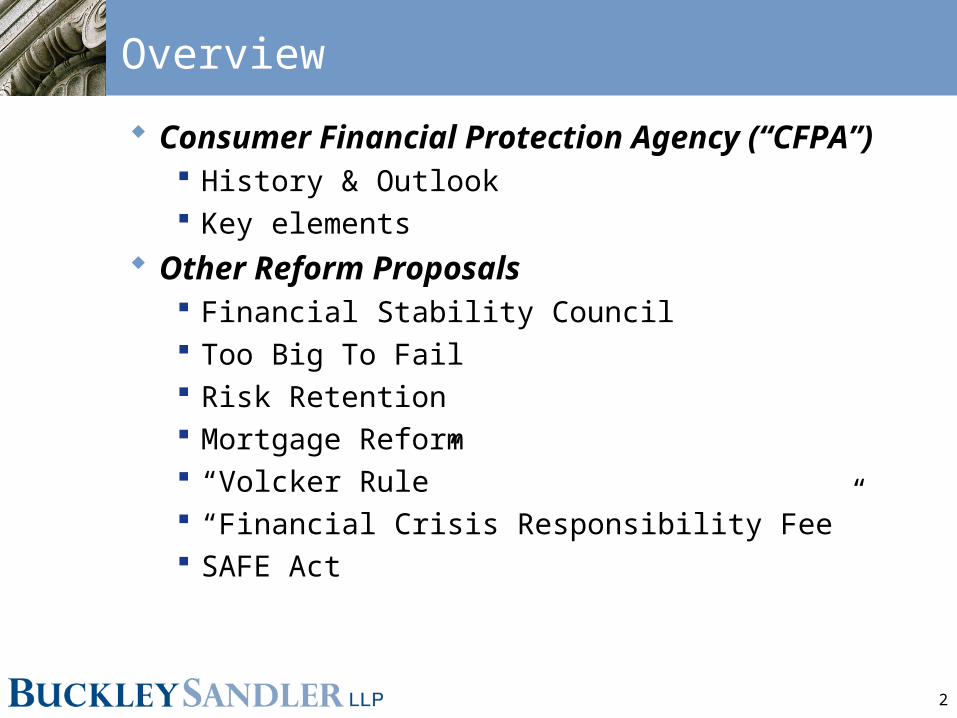

Overview

Consumer Financial Protection Agency (“CFPA”) History & Outlook Key elements

Other Reform Proposals Financial Stability Council Too Big To Fail Risk Retention Mortgage Reform “Volcker Rule” “Financial Crisis Responsibility Fee” SAFE Act

3

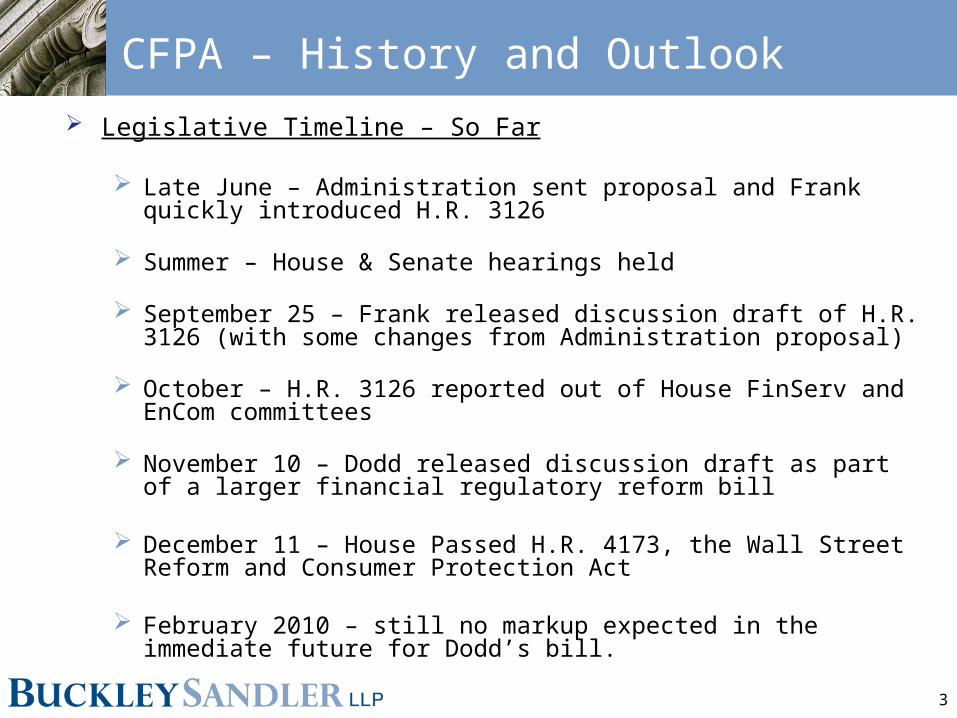

CFPA – History and Outlook

Legislative Timeline – So Far

Late June – Administration sent proposal and Frank quickly introduced H.R. 3126

Summer – House & Senate hearings held

September 25 – Frank released discussion draft of H.R. 3126 (with some changes from Administration proposal)

October – H.R. 3126 reported out of House FinServ and EnCom committees

November 10 – Dodd released discussion draft as part of a larger financial regulatory reform bill

December 11 – House Passed H.R. 4173, the Wall Street Reform and Consumer Protection Act

February 2010 – still no markup expected in the immediate future for Dodd’s bill.

4

Consumer Protection – The Arguments

Arguments for Creating CFPA Too many cooks in the kitchen: disparate authority

creates unequal regulation for similar products or services

Conflicting Missions: some regulators are also responsible for institution safety & soundness, and consumer protection has taken a back seat

Arguments Against the CFPA Separating safety and soundness regulation from

consumer protection regulation will hurt both missions Will create conflicting and overly burdensome

compliance directives from the CFPA and the safety and soundness regulator – whose directive rules?

5

The CFPA – House Proposal

Title IV of H.R. 4173 establishes the Consumer Financial Protection Agency (“CFPA”) Generally, the CFPA is tasked with regulating and

enforcing the “enumerated” consumer protection laws Enumerated laws include, among others, the Fair Credit

Reporting Act, the Federal Debt Collection Practices Act, the Homeowners Protection Act, the Home Mortgage Disclosure Act, the Real Estate Settlement Procedures Act, the SAFE Act, the Truth in Lending Act, the Equal Credit Opportunity Act and unfair and deceptive trade acts and practices for mortgages.

6

The CFPA – House Proposal

Title IV of H.R. 4173 establishes the Consumer Financial Protection Agency (“CFPA”) The CFPA would regulate "covered persons" and "related

persons" engaging in a "financial activity" or providing "consumer financial products or services.“ "Covered Persons" are those who engage directly or indirectly

in a financial activity, in connection with the provision of a consumer financial product or service. They would also include independent contractors, including attorneys, appraisers, or accountants, who knowingly or recklessly violate a consumer law or regulation or breach of duty.

"Related persons" include, among others, directors, officers, controlling stockholders, shareholders, and joint venturers.

A “service provider” means any person who provides a material service to a covered person in the provision of a consumer financial product or service, and includes persons who facilitate the design of, or operations relating to the provision of the product or service, have direct interaction with the consumer, or process transactions.

7

The CFPA – House Proposal

Applies to “financial activities” which include, among other things: Deposit-taking activities; Extending credit and servicing loans, including acquiring,

purchasing, selling, brokering, or servicing loans or other extensions of credit;

Collecting, analyzing, maintaining, and providing consumer report information or other account information by covered persons;

Debt collecting related to any consumer financial product or service;

Providing real estate settlement services; Acting as an investment or financial adviser (with some

exceptions); Money transmitting; Sale, provision or issuance of stored value products; Acting as a custodian of money or any financial instrument.

8

The CFPA – House Proposal

Structure of the CFPA Single Director vs. Board of Directors H.R. 4173 provides for a transitional structure

initially headed by a single director, but after 2 years transfers to a 5-member presidentially appointed commission.

Director (and subsequently, the Commission), will be advised by a Consumer Financial Protection Oversight Board on strategies, actions, and policies, including whether CFPA regulations are in line with prudential, market, or systemic objectives of the other regulators.

9

The CFPA – House Proposal

Funding appropriations from the Federal Reserve Board Assessments on entities regulated by CFPA

separately for depository and non-depository institutions and based on the size, complexity, and compliance record of the institution.

10

The CFPA – House Proposal

General Powers of the CFPA Examination power of all covered entities

To be done in coordination with examinations already conducted by the functional regulators and state bank supervisors

Enforcement power over the enumerated consumer protection laws includes ability to take action based upon consumer complaints. May take action to prevent an unfair, deceptive or abusive act or

practice related to the "offering" of a consumer financial product or service although such action must be consistent with the FTC Act.

Carve out: insured depositories and credit unions with assets under $10 billion will not be subject to CFPA-only examinations,

CFPA may include an examiner in every aspect of the primary regulator examination, and the primary regulator must provide reports to the CFPA. The CFPA may also, under certain circumstances, remove the primary regulator from an enforcement action.

11

The CFPA – House Proposal

Specific Powers of the CFPA prohibit or impose conditions or limitations on the use of mandatory

arbitration clauses; regulate consumer disclosures, including the costs, benefits, and risks

associated with any consumer financial product or service. implement a combined TILA/RESPA disclosure (unless HUD and the Fed

do it first). implement rules governing duties owed by a covered person, its

employees, agents and independent contractors to a consumer when that person deals or communicates directly with the consumer in the provision of a consumer financial product or service.

regulate the manner, setting, and circumstances for sales practices. monitor compensation practices to promote fair dealing with consumers. Adopt rules on appraisal independence requirements. Adopt rules on disclosure of overdraft fees and charges.

The CFPA may not, however, require that any particular product or service be offered to any consumer

12

The CFPA – House Proposal

Preemption Provisions Generally addresses federally-chartered banks and thrifts and their

operating subsidiaries. Key Conclusions of H.R. 4173:

Codifies the Barnett Bank standard for preemption of state laws for national banks and thrifts

National banks subject to state laws, unless (i) application would have a discriminatory effect on national banks in comparison with its effect on a state chartered bank; or (ii) the State consumer financial law prevents, significantly interferes with, or materially impairs the ability of a national bank to engage in the business of banking.

Preemption determinations under this subparagraph may be made by a court or by regulation or order of the OCC in accordance with applicable law on a case-by-case basis (meaning, a determination made by the OCC, in consultation with the CFPA, concerning the impact of a particular state law on any national bank subject to that law).

Effectively repeals the Watters decision and removes preemption protection for operating subsidiaries of national banks and thrifts.

Codifies the holding in Cuomo and expressly gives state attorneys general visitorial powers over national banks and federal thrifts.

Specifying that interest rate exportation of national banks is not affected; Removes Chevron deference for OCC determinations relating to applicability of state

laws, while generally preserving Chevron deference for interpretations of the National Bank Act; and

Clarifies that a state law is not inconsistent if it provides greater protection than what is provided under federal law.

13

Other Reform Proposals

Some other key reform proposals include: Financial Stability Council Too Big To Fail Risk Retention Mortgage Reform “Volcker Rule” “Financial Crisis Responsibility Fee” SAFE Act Implementation

14

Other Reform Proposals – Systemic Risk

Called the “Financial Stability Improvement Act” in HR 4173 Key Elements

In general, the bill subjects entities that are identified as systemically risky to increased scrutiny and regulation

Also sets up a process for resolving such institutions in case of a failure

Sets up the Financial Services Oversight Council (“FSOC”) to monitor financial markets and identify systemic risk issues and threats FSOC can recommend that regulators impose stricter

prudential standards on specific companies, and bill gives regulators the authority to implement and enforce such standards (and the Board to take prompt corrective action)

FSOC can take actions to mitigate systemic risks, including modifying prudential standards, terminating certain activities, and restricting ability to offer products or activities

Also attempts some consolidation of regulators to close “gaps” in regulation

15

Other Reform Proposals – Too Big to Fail

House bill (as reported from Financial Services Committee) FDIC may only lend to failing company for

purpose of unwinding it FDIC may not provide the kind of “open bank

assistance” to holding companies that it can now provide their subs

Senate Banking Committee expected to adopt similar provisions

Administration says both bills will ensure that government may only assist individual institution to ensure orderly failure

16

Other Reform Proposals – Credit Risk Retention

House systemic risk title requires retention of: Up to 5% on FHA or GSE loans Less if good underwriting/due diligence or safer

product (as established by federal banking agency and SEC regs)

More than 5% if underwriting/due diligence is insufficient

“Appropriate Agencies” may provide exemptions/adjust requirements

Note of Interest -- H.R. 1728, which passed House in May, would have exempted FHA and GSE loans from risk retention requirements

17

Other Reform Proposals – Mortgage Reform

HR 4173 includes the “Mortgage Reform and Anti-Predatory Lending Act” (H.R. 1728)

Key Elements Places new standards on the origination of mortgage loans – a

“duty of care” Sets up new underwriting requirements to ensure loans meet the

“duty of care” standards Imposes new minimum standards for mortgage loans Prohibits certain loan practices for all loans, and additional

practices for “high cost” mortgages Requires new disclosures Imposes new requirements on mortgage servicers Implements new requirements on appraisal practices Does NOT repeal the RESPA reform rule

18

Other Reform Proposals – “Volcker Rule”

On January 21, President Obama announced the "Volcker Rule“: Restricts the size and scope of banks and financial

institutions. Generally, prevents banks or financial institutions that contain a

bank from owning, investing in, or sponsoring a hedge fund, private equity fund, or proprietary trading operations for their own profit and unrelated to servicing customers

broadens limitations on growth of liabilities at the largest financial firms, akin to the current deposit cap

When announced, the President intended that the proposal be included in the regulatory reform legislation

No details on the plan yet.

19

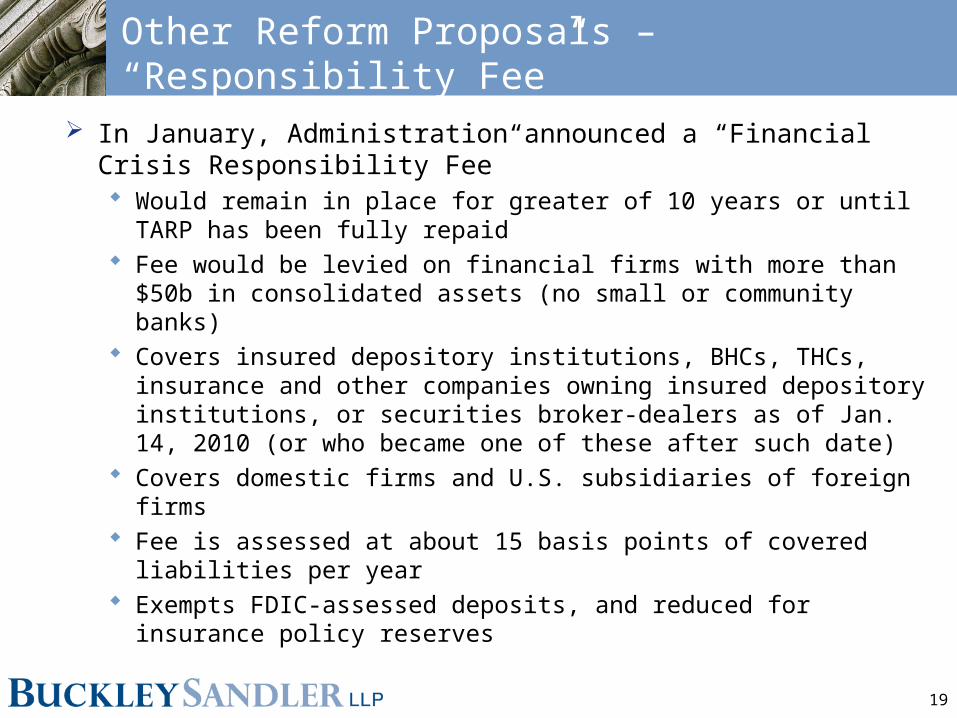

Other Reform Proposals – “Responsibility Fee”

In January, Administration announced a “Financial Crisis Responsibility Fee” Would remain in place for greater of 10 years or until TARP has

been fully repaid Fee would be levied on financial firms with more than $50b in

consolidated assets (no small or community banks) Covers insured depository institutions, BHCs, THCs, insurance

and other companies owning insured depository institutions, or securities broker-dealers as of Jan. 14, 2010 (or who became one of these after such date)

Covers domestic firms and U.S. subsidiaries of foreign firms Fee is assessed at about 15 basis points of covered liabilities per

year Exempts FDIC-assessed deposits, and reduced for insurance

policy reserves

20

Other Reform Proposals – SAFE Act

Mortgage Loan Origination Licensing and Registration Dual track: State Licensing and Federal Registration States have begun licensing MLOs HUD has issued Proposed Regulations applicable to

State licensing system Federal Banking Agencies are in process of finalizing

regulation

21

Other Reform Proposals – SAFE Act

Major Issues Unlevel playing field between State and Federal

systems Licensing of loan modification specialists Overlap of State and Federal systems for bank

subsidiaries Implementation issues

22

For further information contact:

John P. Kromer, Esq. Clinton R. Rockwell

BuckleySandler LLP BuckleySandler LLP

1250 24th Street, NW 1801 Century Park East

Suite 700 Suite 2240

Washington, DC 20037 Los Angeles, CA 90067

[email protected]@buckleysandler.com

Jon David Langlois

BuckleySandler LLP

1250 24th Street, NW

Suite 700

Washington, DC 20037