The Comerica Economic Outlook The Mid-Cycle U.S. Economy in a Multi-Speed World Robert A. Dye Chief...

18

The Comerica Economic Outlook The Mid-Cycle U.S. Economy in a Multi-Speed World Robert A. Dye Chief Economist, Comerica Bank January 2015

-

Upload

austin-watkins -

Category

Documents

-

view

214 -

download

0

Transcript of The Comerica Economic Outlook The Mid-Cycle U.S. Economy in a Multi-Speed World Robert A. Dye Chief...

The Comerica Economic Outlook

The Mid-Cycle U.S. Economy in a Multi-Speed World

Robert A. Dye Chief Economist, Comerica Bank

January 2015

2

Hits and Misses from 2014

Hits

• U.S. endogenous growth

• GDP expansion

• Falling unemployment rate

• Consumer re-emerges

• Low inflation

• Monetary policy unwind

Misses

• Oil prices

• Eurozone weaker

• Long-term rates lower

• Housing metrics

subdued

3

The U.S. and Global Economies in 2015, Many Moving Parts

• The U.S. economy is mid-cycle

• Labor metrics are improving

• Manufacturing conditions remain favorable

• However, U.S. economic growth remains hindered by wealth

destruction, risk aversion and tight housing credit

• Housing metrics remain range bound

• Oil prices have eased, creating winners and losers

• Inflation remains well contained

4

Global Momentum Slowed in 2014H2

• Global growth challenged by Europe, China and Japan

• Europe data softer, some leading indicators improving

• China vulnerable to credit bubble and weaker exports

• Japan still struggling for sustained lift-off

• Russia faces recession and possible default

5

The End of an Era for Global Monetary Policy

2007-2014 Globally coordinated extraordinary monetary policy

Very low interest rates

Special programs

Expanded currency swap lines

Asset purchases

2015- De-synchronization

Bank of Japan aggressive easing, beginning late 2012

U.S. Federal Reserve pivots

Bank of England tightens

European Central Bank doubles down

6

Foreign Exchange Rates Moved by Monetary Policy

7580859095100105110115120125

0.68

0.70

0.72

0.74

0.76

0.78

0.80

0.82

2011 2012 2013 2014

The Dollar, the Euro and the Yen

Euro/$ (L)

Yen/$ (R)

$

7

Fed Policy: Countdown to Interest Rate Lift-off

• Labor market metrics are improving

• Fiscal drag easing

• Strong consensus for solid 2015 GDP growth

• Falling oil prices and rising dollar complicate inflation outlook

• Next step in Fed pivot…forward guidance, started in December

• Yellen brackets lift-off…April-December 2015

• Interest rate lift-off around mid-year 2015

• Shallow trajectory, rates may not “normalize” before next recession

8

Recent Job Growth is Strong

4

5

6

7

8

9

10

-800

-600

-400

-200

0

200

400

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16

+252k in December, U. Rate 5.6 Percent

Forecast

Payroll Employment, avg monthly diff, ths (L)

Unemployment Rate, percent (R)

9

Potential For Wage Inflation

0

2

4

6

8

10

12

'70 '80 '90 '00 '10

Sub-5.5 Percent Unemployment Rate Associated with Accelerating Wages

Unemployment Rate, percent

Avg Hourly Earnings, Prod Workers, pchya

10

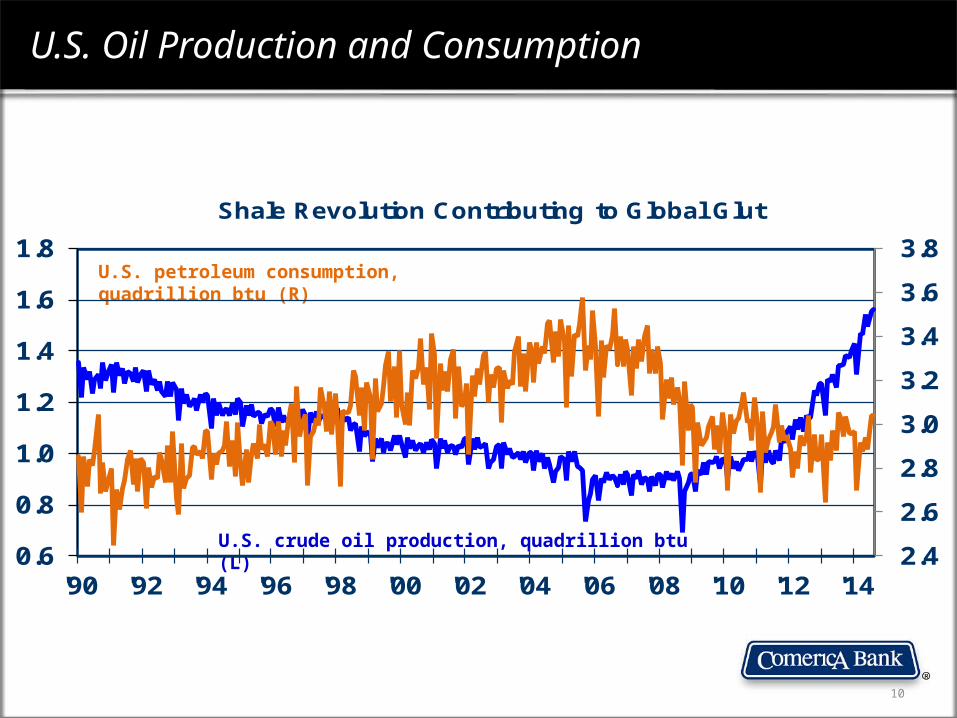

U.S. Oil Production and Consumption

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

0.6

0.8

1.0

1.2

1.4

1.6

1.8

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14

Shale Revolution Contributing to Global Glut

U.S. crude oil production, quadrillion btu (L)

U.S. petroleum consumption, quadrillion btu (R)

11

500

1000

1500

2000

20406080

100120140160

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

WTI Crude Price Through October 2014

WTI Crude Oil Spot Price at Cushing, $/barrel (L)

Falling Crude Oil Prices Complicate Inflation OutlookAnd Pose a Downside Risk for Oil Producing Regions

Average Active Rotary Rigs, Total Number U.S. (R)

12

Lower Gasoline Prices Boost Auto Sales

9,000,000

10,000,000

11,000,000

12,000,000

13,000,000

14,000,000

15,000,000

16,000,000

17,000,000

18,000,000

2008 2009 2010 2011 2012 2013 2014 2015

U.S. Auto Sales, total SAAR

History Forecast

13

Home Sales Supported by Job Growth, Low Rates

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

5,500,000

2008 2009 2010 2011 2012 2013 2014 2015 2016

New and Existing Home Sales

Existing Home Sales, (L)

New Home Sales, (R)

14

GDP Forecast Through 2015, Ongoing Moderate Expansion

(9)

(7)

(5)

(3)

(1)

1

3

5

2008 2009 2010 2011 2012 2013 2014 2015

U.S. Real GDP Growth, annualized rate

History Forecast

15

Interest Rates Face Upward Pressure with Monetary Policy Unwind

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Yield, percent

Fed Funds

10-Year Treasury Bonds

16

Forecast Risks

Downside Risks• Crude oil prices • China, Japan, Eurozone,

Russia, MENA • Consumer spending

languishes• Housing market stalls• Job growth weakens• Strong dollar hurts exports• Monetary policy stumbles• Fiscal policy failure, rating

downgrade

Upside Risks• Lower gasoline and product

prices• Consumer/Business confidence

surges• Strong job growth • Households unleash pent-up

demand• Easing underwriting for home

mortgages • Increased defense spending • Manufacturing renaissance• Europe and Japan turn the

corner

17

Michigan Labor Markets Are Improving

3,800

3,900

4,000

4,100

4,200

4,300

-10

-5

0

5

10

15

2008 2009 2010 2011 2012 2013 2014

Unemployment Rate, percent, U.S. Michigan (L)

Job Growth, y/y percent, U.S. Michigan (L)

Payroll employment, ths, Michigan (R)

Robert A. Dye

Subscribewww.comerica.com/economics

Follow on Twitter@Comerica_Econ