The Checklist - 1. Risk drivers identification - High frequency

Upload

arpm-advanced-risk-and-portfolio-managementCategory

view

64download

1

The “Checklist” > 1. Risk drivers identification > Credit

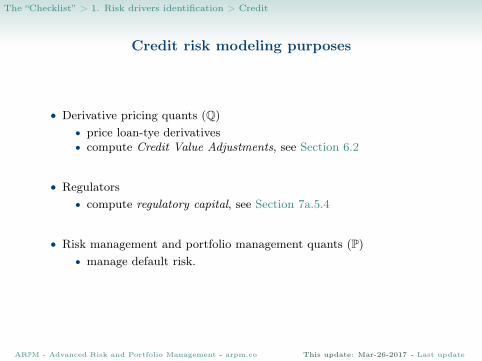

Credit risk modeling purposes

• Derivative pricing quants (Q)• price loan-tye derivatives• compute Credit Value Adjustments, see Section 6.2

• Regulators• compute regulatory capital, see Section 7a.5.4

• Risk management and portfolio management quants (P)• manage default risk.

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > Credit

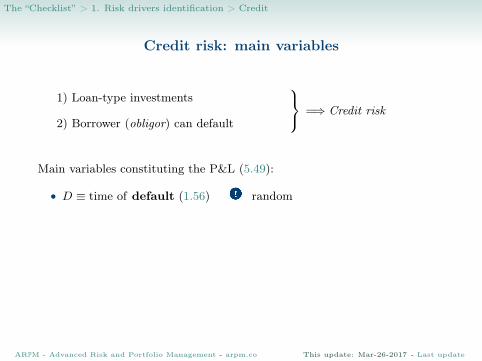

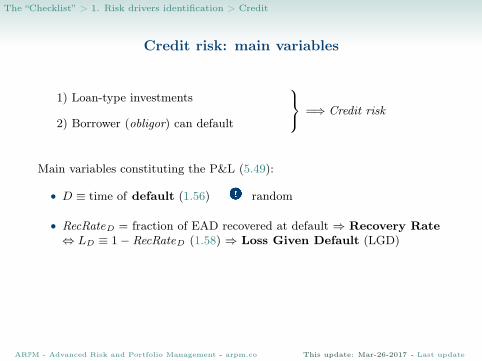

Credit risk: main variables

1) Loan-type investments

2) Borrower (obligor) can default

=⇒ Credit risk

Main variables constituting the P&L (5.49):

• D ≡ time of default (1.56) random

• RecRateD = fraction of EAD recovered at default ⇒ Recovery Rate⇔ LD ≡ 1− RecRateD (1.58) ⇒ Loss Given Default (LGD)

• Vt = market value of the defaultable instrument at time t (13.1)

• XposD ≡ max(0, VD−) (1.57) ⇒ Exposure At Default (EAD)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > Credit

Credit risk: main variables

1) Loan-type investments

2) Borrower (obligor) can default

=⇒ Credit risk

Main variables constituting the P&L (5.49):

• D ≡ time of default (1.56) random

• RecRateD = fraction of EAD recovered at default ⇒ Recovery Rate⇔ LD ≡ 1− RecRateD (1.58) ⇒ Loss Given Default (LGD)

• Vt = market value of the defaultable instrument at time t (13.1)

• XposD ≡ max(0, VD−) (1.57) ⇒ Exposure At Default (EAD)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > Credit

Credit risk: main variables

1) Loan-type investments

2) Borrower (obligor) can default

=⇒ Credit risk

Main variables constituting the P&L (5.49):

• D ≡ time of default (1.56) random

• RecRateD = fraction of EAD recovered at default ⇒ Recovery Rate⇔ LD ≡ 1− RecRateD (1.58) ⇒ Loss Given Default (LGD)

• Vt = market value of the defaultable instrument at time t (13.1)

• XposD ≡ max(0, VD−) (1.57) ⇒ Exposure At Default (EAD)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > Credit

Credit risk: main variables

1) Loan-type investments

2) Borrower (obligor) can default

=⇒ Credit risk

Main variables constituting the P&L (5.49):

• D ≡ time of default (1.56) random

• RecRateD = fraction of EAD recovered at default ⇒ Recovery Rate⇔ LD ≡ 1− RecRateD (1.58) ⇒ Loss Given Default (LGD)

• Vt = market value of the defaultable instrument at time t (13.1)

• XposD ≡ max(0, VD−) (1.57) ⇒ Exposure At Default (EAD)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > Credit

Credit risk: main variables

1) Loan-type investments

2) Borrower (obligor) can default

=⇒ Credit risk

Main variables constituting the P&L (5.49):

• D ≡ time of default (1.56) random

• RecRateD = fraction of EAD recovered at default ⇒ Recovery Rate⇔ LD ≡ 1− RecRateD (1.58) ⇒ Loss Given Default (LGD)

• Vt = market value of the defaultable instrument at time t (13.1)

• XposD ≡ max(0, VD−) (1.57) ⇒ Exposure At Default (EAD)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > Credit

Credit risk: main variables

1) Loan-type investments

2) Borrower (obligor) can default

=⇒ Credit risk

Main variables constituting the P&L (5.49):

• D ≡ time of default (1.56) random

• RecRateD = fraction of EAD recovered at default ⇒ Recovery Rate⇔ LD ≡ 1− RecRateD (1.58) ⇒ Loss Given Default (LGD)

• Vt = market value of the defaultable instrument at time t (13.1)

• XposD ≡ max(0, VD−) (1.57) ⇒ Exposure At Default (EAD)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

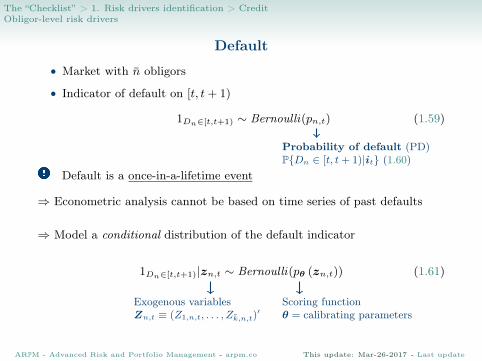

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Default

• Market with n̄ obligors

• Indicator of default on [t, t+ 1)

1Dn∈[t,t+1) ∼ Bernoulli(pn,t) (1.59)

Probability of default (PD)P{Dn ∈ [t, t+ 1)|it} (1.60)

Default is a once-in-a-lifetime event

⇒ Econometric analysis cannot be based on time series of past defaults

⇒ Model a conditional distribution of the default indicator

1Dn∈[t,t+1)|zn,t ∼ Bernoulli(pθ (zn,t)) (1.61)

Exogenous variablesZn,t ≡ (Z1,n,t, . . . , Zk̄,n,t)

′Scoring functionθ = calibrating parameters

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Default

• Market with n̄ obligors

• Indicator of default on [t, t+ 1)

1Dn∈[t,t+1) ∼ Bernoulli(pn,t) (1.59)

Probability of default (PD)P{Dn ∈ [t, t+ 1)|it} (1.60)

Default is a once-in-a-lifetime event

⇒ Econometric analysis cannot be based on time series of past defaults

⇒ Model a conditional distribution of the default indicator

1Dn∈[t,t+1)|zn,t ∼ Bernoulli(pθ (zn,t)) (1.61)

Exogenous variablesZn,t ≡ (Z1,n,t, . . . , Zk̄,n,t)

′Scoring functionθ = calibrating parameters

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

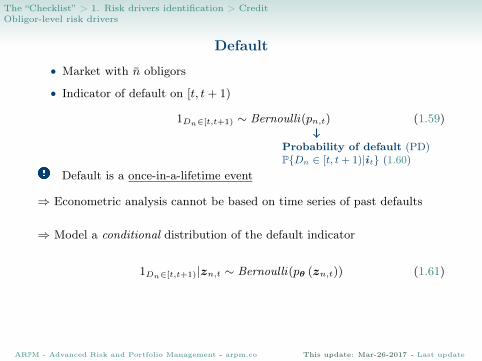

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Default

• Market with n̄ obligors

• Indicator of default on [t, t+ 1)

1Dn∈[t,t+1) ∼ Bernoulli(pn,t) (1.59)

Probability of default (PD)P{Dn ∈ [t, t+ 1)|it} (1.60)

Default is a once-in-a-lifetime event

⇒ Econometric analysis cannot be based on time series of past defaults

⇒ Model a conditional distribution of the default indicator

1Dn∈[t,t+1)|zn,t ∼ Bernoulli(pθ (zn,t)) (1.61)

Exogenous variablesZn,t ≡ (Z1,n,t, . . . , Zk̄,n,t)

′Scoring functionθ = calibrating parameters

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

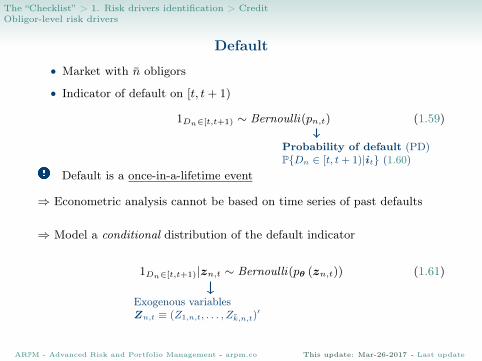

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Default

• Market with n̄ obligors

• Indicator of default on [t, t+ 1)

1Dn∈[t,t+1) ∼ Bernoulli(pn,t) (1.59)

Probability of default (PD)P{Dn ∈ [t, t+ 1)|it} (1.60)

Default is a once-in-a-lifetime event

⇒ Econometric analysis cannot be based on time series of past defaults

⇒ Model a conditional distribution of the default indicator

1Dn∈[t,t+1)|zn,t ∼ Bernoulli(pθ (zn,t)) (1.61)

Exogenous variablesZn,t ≡ (Z1,n,t, . . . , Zk̄,n,t)

′Scoring functionθ = calibrating parameters

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Default

• Market with n̄ obligors

• Indicator of default on [t, t+ 1)

1Dn∈[t,t+1) ∼ Bernoulli(pn,t) (1.59)

Probability of default (PD)P{Dn ∈ [t, t+ 1)|it} (1.60)

Default is a once-in-a-lifetime event

⇒ Econometric analysis cannot be based on time series of past defaults

⇒ Model a conditional distribution of the default indicator

1Dn∈[t,t+1)|zn,t ∼ Bernoulli(pθ (zn,t)) (1.61)

Exogenous variablesZn,t ≡ (Z1,n,t, . . . , Zk̄,n,t)

′Scoring functionθ = calibrating parameters

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Default

• Market with n̄ obligors

• Indicator of default on [t, t+ 1)

1Dn∈[t,t+1) ∼ Bernoulli(pn,t) (1.59)

Probability of default (PD)P{Dn ∈ [t, t+ 1)|it} (1.60)

Default is a once-in-a-lifetime event

⇒ Econometric analysis cannot be based on time series of past defaults

⇒ Model a conditional distribution of the default indicator

1Dn∈[t,t+1)|zn,t ∼ Bernoulli(pθ (zn,t)) (1.61)

Exogenous variablesZn,t ≡ (Z1,n,t, . . . , Zk̄,n,t)

′

Scoring functionθ = calibrating parameters

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Default

• Market with n̄ obligors

• Indicator of default on [t, t+ 1)

1Dn∈[t,t+1) ∼ Bernoulli(pn,t) (1.59)

Probability of default (PD)P{Dn ∈ [t, t+ 1)|it} (1.60)

Default is a once-in-a-lifetime event

⇒ Econometric analysis cannot be based on time series of past defaults

⇒ Model a conditional distribution of the default indicator

1Dn∈[t,t+1)|zn,t ∼ Bernoulli(pθ (zn,t)) (1.61)

Exogenous variablesZn,t ≡ (Z1,n,t, . . . , Zk̄,n,t)

′Scoring functionθ = calibrating parameters

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Exogenous variables driving the default

• Macroeconomic variables Zmacrot : GDP, inflation, employment

statistics...

• Book variables Zbookn,t : earnings, liabilities...

• Forward-looking market variables Zmktn,t : equity value, credit spread,

implied vol...

• Processed variables Zprocn,t : credit agency ratings, Altman’s z-score,

functions of the previous categories...

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

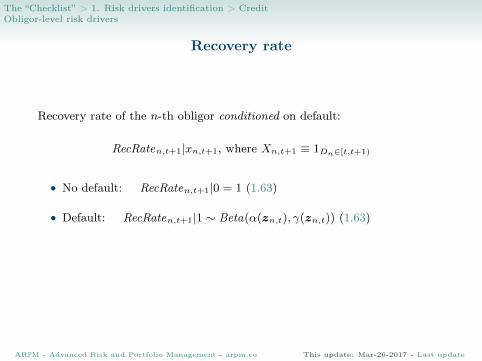

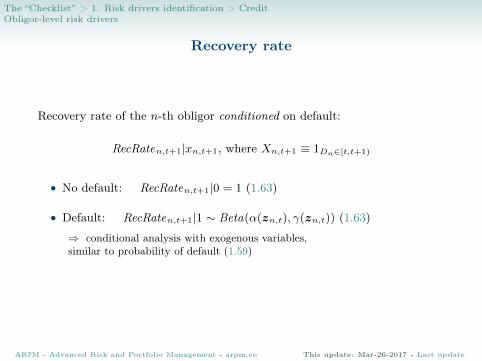

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Recovery rate

Recovery rate of the n-th obligor conditioned on default:

RecRaten,t+1|xn,t+1, where Xn,t+1 ≡ 1Dn∈[t,t+1)

• No default: RecRaten,t+1|0 = 1 (1.63)

• Default: RecRaten,t+1|1 ∼ Beta(α(zn,t), γ(zn,t)) (1.63)

⇒ conditional analysis with exogenous variables,similar to probability of default (1.59)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Recovery rate

Recovery rate of the n-th obligor conditioned on default:

RecRaten,t+1|xn,t+1, where Xn,t+1 ≡ 1Dn∈[t,t+1)

• No default: RecRaten,t+1|0 = 1 (1.63)

• Default: RecRaten,t+1|1 ∼ Beta(α(zn,t), γ(zn,t)) (1.63)

⇒ conditional analysis with exogenous variables,similar to probability of default (1.59)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Recovery rate

Recovery rate of the n-th obligor conditioned on default:

RecRaten,t+1|xn,t+1, where Xn,t+1 ≡ 1Dn∈[t,t+1)

• No default: RecRaten,t+1|0 = 1 (1.63)

• Default: RecRaten,t+1|1 ∼ Beta(α(zn,t), γ(zn,t)) (1.63)

⇒ conditional analysis with exogenous variables,similar to probability of default (1.59)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

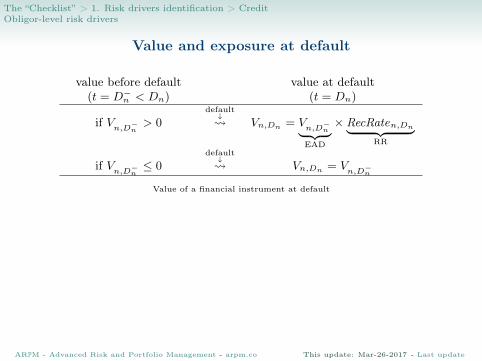

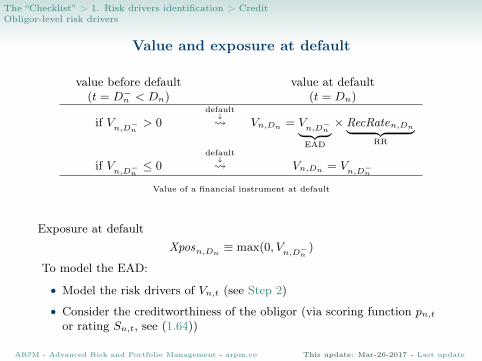

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Value and exposure at default

value before default(t = D−n < Dn)

value at default(t = Dn)

if Vn,D−n

> 0default↓ Vn,Dn = V

n,D−n︸ ︷︷ ︸EAD

× RecRaten,Dn︸ ︷︷ ︸RR

if Vn,D−n

≤ 0default↓ Vn,Dn = V

n,D−n

Value of a financial instrument at default

Exposure at defaultXposn,Dn

≡ max(0, Vn,D−n

)

To model the EAD:

• Model the risk drivers of Vn,t (see Step 2)

• Consider the creditworthiness of the obligor (via scoring function pn,t

or rating Sn,t, see (1.64))

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Value and exposure at default

value before default(t = D−n < Dn)

value at default(t = Dn)

if Vn,D−n

> 0default↓ Vn,Dn = V

n,D−n︸ ︷︷ ︸EAD

× RecRaten,Dn︸ ︷︷ ︸RR

if Vn,D−n

≤ 0default↓ Vn,Dn = V

n,D−n

Value of a financial instrument at default

Exposure at defaultXposn,Dn

≡ max(0, Vn,D−n

)

To model the EAD:

• Model the risk drivers of Vn,t (see Step 2)

• Consider the creditworthiness of the obligor (via scoring function pn,t

or rating Sn,t, see (1.64))

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

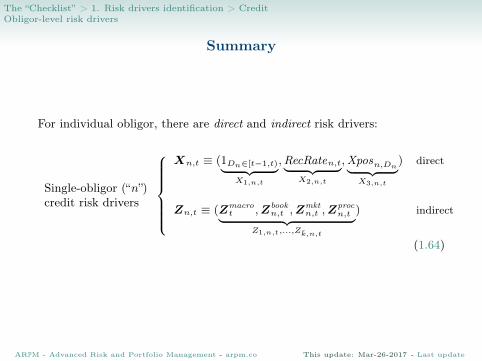

The “Checklist” > 1. Risk drivers identification > CreditObligor-level risk drivers

Summary

For individual obligor, there are direct and indirect risk drivers:

Single-obligor (“n”)credit risk drivers

Xn,t ≡ (1Dn∈[t−1,t)︸ ︷︷ ︸X1,n,t

,RecRaten,t︸ ︷︷ ︸X2,n,t

,Xposn,Dn︸ ︷︷ ︸X3,n,t

) direct

Zn,t ≡ (Zmacrot ,Zbook

n,t ,Zmktn,t ,Z

procn,t︸ ︷︷ ︸

Z1,n,t,...,Zk̄,n,t

) indirect

(1.64)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

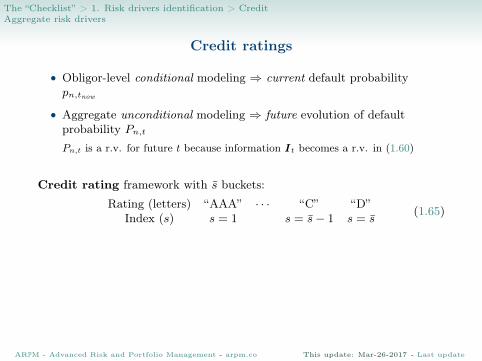

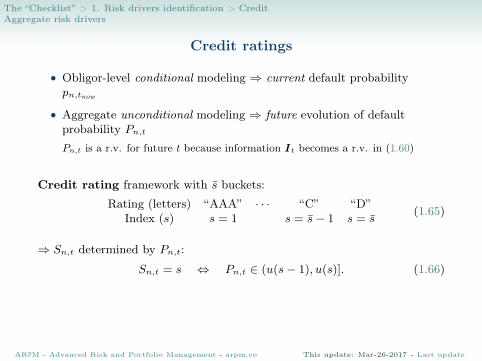

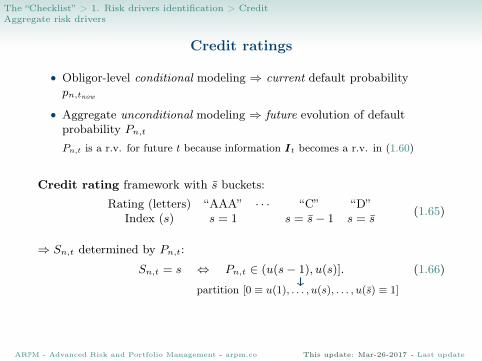

The “Checklist” > 1. Risk drivers identification > CreditAggregate risk drivers

Credit ratings

• Obligor-level conditional modeling ⇒ current default probabilitypn,tnow

• Aggregate unconditional modeling ⇒ future evolution of defaultprobability Pn,t

Pn,t is a r.v. for future t because information It becomes a r.v. in (1.60)

Credit rating framework with s̄ buckets:

Rating (letters) “AAA” · · · “C” “D”Index (s) s = 1 s = s̄− 1 s = s̄

(1.65)

⇒ Sn,t determined by Pn,t:

Sn,t = s ⇔ Pn,t ∈ (u(s− 1), u(s)]. (1.66)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

⇒ Fundamental assumption: Sn,t proxied by St (obligor-independent)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditAggregate risk drivers

Credit ratings

• Obligor-level conditional modeling ⇒ current default probabilitypn,tnow

• Aggregate unconditional modeling ⇒ future evolution of defaultprobability Pn,t

Pn,t is a r.v. for future t because information It becomes a r.v. in (1.60)

Credit rating framework with s̄ buckets:

Rating (letters) “AAA” · · · “C” “D”Index (s) s = 1 s = s̄− 1 s = s̄

(1.65)

⇒ Sn,t determined by Pn,t:

Sn,t = s ⇔ Pn,t ∈ (u(s− 1), u(s)]. (1.66)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

⇒ Fundamental assumption: Sn,t proxied by St (obligor-independent)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditAggregate risk drivers

Credit ratings

• Obligor-level conditional modeling ⇒ current default probabilitypn,tnow

• Aggregate unconditional modeling ⇒ future evolution of defaultprobability Pn,t

Pn,t is a r.v. for future t because information It becomes a r.v. in (1.60)

Credit rating framework with s̄ buckets:

Rating (letters) “AAA” · · · “C” “D”Index (s) s = 1 s = s̄− 1 s = s̄

(1.65)

⇒ Sn,t determined by Pn,t:

Sn,t = s ⇔ Pn,t ∈ (u(s− 1), u(s)]. (1.66)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

⇒ Fundamental assumption: Sn,t proxied by St (obligor-independent)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditAggregate risk drivers

Credit ratings

• Obligor-level conditional modeling ⇒ current default probabilitypn,tnow

• Aggregate unconditional modeling ⇒ future evolution of defaultprobability Pn,t

Pn,t is a r.v. for future t because information It becomes a r.v. in (1.60)

Credit rating framework with s̄ buckets:

Rating (letters) “AAA” · · · “C” “D”Index (s) s = 1 s = s̄− 1 s = s̄

(1.65)

⇒ Sn,t determined by Pn,t:

Sn,t = s ⇔ Pn,t ∈ (u(s− 1), u(s)]. (1.66)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

⇒ Fundamental assumption: Sn,t proxied by St (obligor-independent)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditAggregate risk drivers

Credit ratings

• Obligor-level conditional modeling ⇒ current default probabilitypn,tnow

• Aggregate unconditional modeling ⇒ future evolution of defaultprobability Pn,t

Pn,t is a r.v. for future t because information It becomes a r.v. in (1.60)

Credit rating framework with s̄ buckets:

Rating (letters) “AAA” · · · “C” “D”Index (s) s = 1 s = s̄− 1 s = s̄

(1.65)

⇒ Sn,t determined by Pn,t:

Sn,t = s ⇔ Pn,t ∈ (u(s− 1), u(s)]. (1.66)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

⇒ Fundamental assumption: Sn,t proxied by St (obligor-independent)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditAggregate risk drivers

Credit ratings

• Obligor-level conditional modeling ⇒ current default probabilitypn,tnow

• Aggregate unconditional modeling ⇒ future evolution of defaultprobability Pn,t

Pn,t is a r.v. for future t because information It becomes a r.v. in (1.60)

Credit rating framework with s̄ buckets:

Rating (letters) “AAA” · · · “C” “D”Index (s) s = 1 s = s̄− 1 s = s̄

(1.65)

⇒ Sn,t determined by Pn,t:

Sn,t = s ⇔ Pn,t ∈ (u(s− 1), u(s)]. (1.66)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

⇒ Fundamental assumption: Sn,t proxied by St (obligor-independent)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditAggregate risk drivers

Aggregate risk drivers

• Ns,t: number of obligors in rating s at time t

• Ns→s′,t: cumulative number of migrations from s to s′ up to t

Ns→s′,t ≡∑l≤t,n

1(Sn,l−1=s,Sn,l=s′), s 6= s′ (1.67)

• P̄t: cross-sectional sample median of default probabilities

P̄t ≡ M̂ed{P1,t, . . . , Pn,t, . . . , Pn̄,t} (1.68)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditAggregate risk drivers

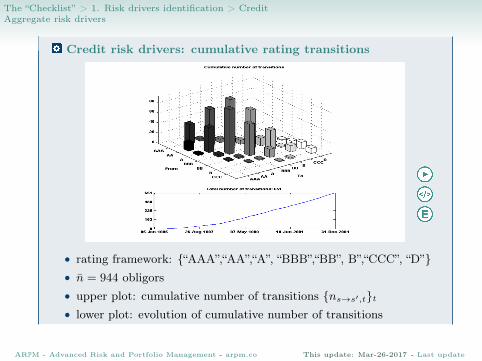

Credit risk drivers: cumulative rating transitions

• rating framework: {“AAA”,“AA”,“A”, “BBB”,“BB”, B”,“CCC”, “D”}• n̄ = 944 obligors• upper plot: cumulative number of transitions {ns→s′,t}t• lower plot: evolution of cumulative number of transitions

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

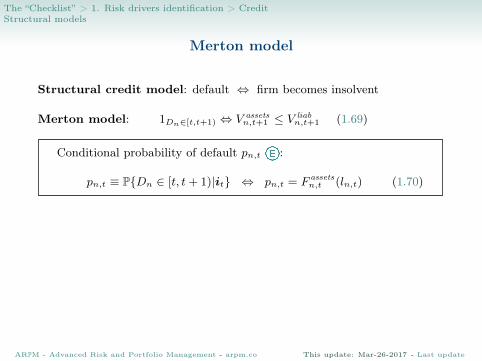

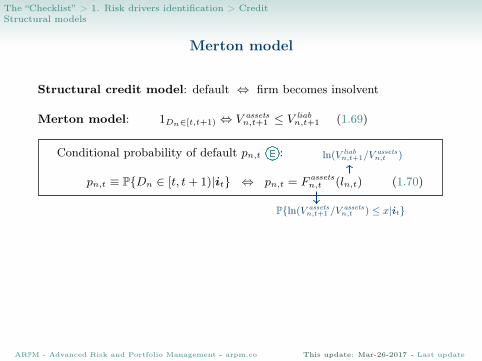

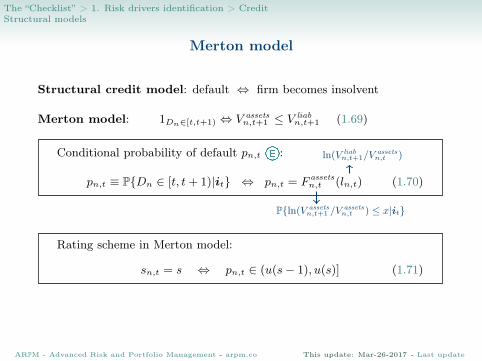

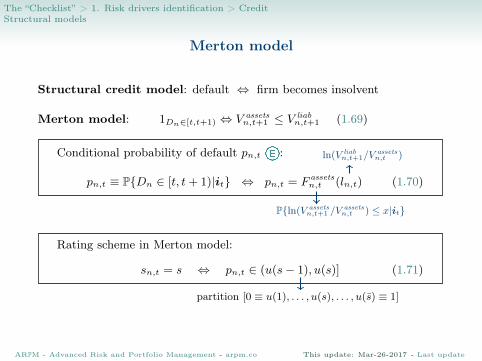

The “Checklist” > 1. Risk drivers identification > CreditStructural models

Merton model

Structural credit model: default ⇔ firm becomes insolvent

Merton model: 1Dn∈[t,t+1) ⇔ V assetsn,t+1 ≤ V liab

n,t+1 (1.69)

Conditional probability of default pn,t :

pn,t ≡ P{Dn ∈ [t, t+ 1)|it} ⇔ pn,t = F assetsn,t (ln,t) (1.70)

ln(V liabn,t+1/V

assetsn,t )

P{ln(V assetsn,t+1 /V

assetsn,t ) ≤ x|it}

Rating scheme in Merton model:

sn,t = s ⇔ pn,t ∈ (u(s− 1), u(s)] (1.71)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditStructural models

Merton model

Structural credit model: default ⇔ firm becomes insolvent

Merton model: 1Dn∈[t,t+1) ⇔ V assetsn,t+1 ≤ V liab

n,t+1 (1.69)

Conditional probability of default pn,t :

pn,t ≡ P{Dn ∈ [t, t+ 1)|it} ⇔ pn,t = F assetsn,t (ln,t) (1.70)

ln(V liabn,t+1/V

assetsn,t )

P{ln(V assetsn,t+1 /V

assetsn,t ) ≤ x|it}

Rating scheme in Merton model:

sn,t = s ⇔ pn,t ∈ (u(s− 1), u(s)] (1.71)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditStructural models

Merton model

Structural credit model: default ⇔ firm becomes insolvent

Merton model: 1Dn∈[t,t+1) ⇔ V assetsn,t+1 ≤ V liab

n,t+1 (1.69)

Conditional probability of default pn,t :

pn,t ≡ P{Dn ∈ [t, t+ 1)|it} ⇔ pn,t = F assetsn,t (ln,t) (1.70)

ln(V liabn,t+1/V

assetsn,t )

P{ln(V assetsn,t+1 /V

assetsn,t ) ≤ x|it}

Rating scheme in Merton model:

sn,t = s ⇔ pn,t ∈ (u(s− 1), u(s)] (1.71)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditStructural models

Merton model

Structural credit model: default ⇔ firm becomes insolvent

Merton model: 1Dn∈[t,t+1) ⇔ V assetsn,t+1 ≤ V liab

n,t+1 (1.69)

Conditional probability of default pn,t :

pn,t ≡ P{Dn ∈ [t, t+ 1)|it} ⇔ pn,t = F assetsn,t (ln,t) (1.70)

ln(V liabn,t+1/V

assetsn,t )

P{ln(V assetsn,t+1 /V

assetsn,t ) ≤ x|it}

Rating scheme in Merton model:

sn,t = s ⇔ pn,t ∈ (u(s− 1), u(s)] (1.71)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditStructural models

Merton model

Structural credit model: default ⇔ firm becomes insolvent

Merton model: 1Dn∈[t,t+1) ⇔ V assetsn,t+1 ≤ V liab

n,t+1 (1.69)

Conditional probability of default pn,t :

pn,t ≡ P{Dn ∈ [t, t+ 1)|it} ⇔ pn,t = F assetsn,t (ln,t) (1.70)

ln(V liabn,t+1/V

assetsn,t )

P{ln(V assetsn,t+1 /V

assetsn,t ) ≤ x|it}

Rating scheme in Merton model:

sn,t = s ⇔ pn,t ∈ (u(s− 1), u(s)] (1.71)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

The “Checklist” > 1. Risk drivers identification > CreditStructural models

Merton model

Structural credit model: default ⇔ firm becomes insolvent

Merton model: 1Dn∈[t,t+1) ⇔ V assetsn,t+1 ≤ V liab

n,t+1 (1.69)

Conditional probability of default pn,t :

pn,t ≡ P{Dn ∈ [t, t+ 1)|it} ⇔ pn,t = F assetsn,t (ln,t) (1.70)

ln(V liabn,t+1/V

assetsn,t )

P{ln(V assetsn,t+1 /V

assetsn,t ) ≤ x|it}

Rating scheme in Merton model:

sn,t = s ⇔ pn,t ∈ (u(s− 1), u(s)] (1.71)

partition [0 ≡ u(1), . . . , u(s), . . . , u(s̄) ≡ 1]

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update

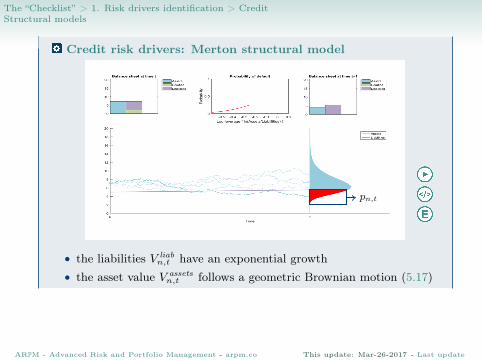

The “Checklist” > 1. Risk drivers identification > CreditStructural models

Credit risk drivers: Merton structural model

• the liabilities V liabn,t have an exponential growth

• the asset value V assetsn,t follows a geometric Brownian motion (5.17)

pn,t

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-26-2017 - Last update