The changing economic landscape and the implications for ...

Upload

econsult-solutionsCategory

view

293download

3

DICK VOITH, ECONSULT SOLUTIONSOctober 23, 2015

The Changing Landscape of Economic Development:

Opportunities and Equity Issues

Presentation Overview• American Cities

– Urban Decline– Changing Landscape

• Philadelphia: Challenges and Opportunities– Tax Structure– Key Challenges– Opportunities

2

Changing Landscape of American Cities

• After 40 years or more of decline, most American cities have stabilized and begun to grow

3

Urban Decline

Decline in 1950 was inevitable:

• Development of highway system• Housing subsidies for new construction• Extremely cheap suburban development• Changing manufacturing technology and

globalization• Aging, disinvested city housing

4

Urban Decline

Exacerbated by:

• Social problems• Racial tensions

5

Urban DeclineFormation of a new “American Dream”

• Suburban house with lots of land• Cars equal freedom• Cities were only for the poor, living in the city was

essentially a failure

6

Urban Decline

American dream continuously reinforced:

• Movies, TV, commercials• Cities were the opposite of the dream

– Unsafe– Obsolete– Escape from New York (NYC was

declining and near bankrupt in the 70s)

• Potential positive benefits of cities were recognized by few..

7

Changing Landscape

8

By the 1990s The landscape began to change once again, in part driven by basic economic forces:

• Suburbs became expensive places to develop• Highway asset became expensive with transportation

expenditures focused on replacement rather than new capacity

• Cities began the transition towards knowledge centers• Production and consumption benefits of cities

appreciated once again

8

Changing Landscape

99

1950 1980 2000 20100%

10%20%30%40%50%60%

23%

45%50% 51%

% of People Live in Suburbs

Changing Landscape

10

Cultural shift in attitudes towards cities reflected in:

• Movies, TV, commercials

10

Changing LandscapeCity and Suburbs now on more even ground• Suburbs still growing but not fueled by city decline

11

Philadelphia

Philadelphia was on the verge of bankruptcy in 1991

• Rendell administration reforms– Union contracts– Spending– Tax policies

12

Philadelphia

13

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Popu

latio

n

Year

Philadelphia

Philadelphia

Key issues for Philadelphia:

• Tax structure• Schools• Public Safety• Transit• Water/Sewer

14

Philadelphia: Tax Structure

Addressing Philadelphia’s Tax Structure

• ESI involved since 2003 Tax Reform Commission

15

Philadelphia: Tax StructurePhiladelphia’s wage and business taxes have proven to have negative impacts on jobs

16

• Despite Phila’s population renaissance employment growth is modest at best

Philadelphia: Tax Structure• Lack of competitiveness can be seen in the

low rents for offices

17

NYC

San Fran

Was

h DC

Boston

Housto

n

Chicag

o

Denve

r

Philad

elphia

San D

iego

Atlanta

$0

$10

$20

$30

$40

$50

$60

$70

$80 $75

$63

$51 $45

$36 $33 $31 $27 $26 $25

CBD Rent per Square Ft Q4 2014 (source: Center City District)

Philadelphia Wage Tax

Reductions in Wage Tax:• Resident Wage Tax 1995: 4.96%• Resident Wage Tax 2016: 3.91%

Achieved through a series of incremental cuts

18

Philadelphia Tax Abatement

Real Estate Tax Abatement

• Since 2000, Philadelphia has offered a ten-year abatement on all real estate improvements– Owner continues to pay tax on the value

of the land and the prior value of the improvements during the 10 year period

19

Philadelphia Tax Abatement

20

• Pre abatement—virtually no residential construction• Post-abatement—construction on pace with suburbs

Philadelphia Tax Abatement

21

Category Code

Total Property

Count

Abated Property

Count

Percent Properties

Abated Abated LV Abated MVResidential 459,219 12,077 2.6% $389,325,957 $4,642,431,100Apartments 40,927 1,183 2.9% $123,471,227 $1,978,538,800Mixed Use 14,760 177 1.2% $17,521,180 $93,296,700Commercial 14,934 376 2.5% $342,288,819 $1,574,214,500Industrial 4,406 51 1.2% $22,058,800 $113,627,500Vacant Land 45,513 10 0.0% $321,600 $4,294,000Total 579,759 13,874 2.4% $894,987,583 $8,406,402,600

Philadelphia Tax Abatement

22

Abatement Issues

• Center on fairness• Superficially reasonable:

– Why shouldn’t those wealthy enough to develop be able to pay higher taxes?

Philadelphia Tax Abatement

23

Theoretical Basis for Abatement

• Lowers tax on mobile capital—increases the rate of investment in the city– Half way to a land tax—but can tax the

capital once it is fixed• Investment makes the city so much more

attractive that demand increases hugely• Available to anyone—not subject to political

manipulation

Philadelphia Tax Abatement

24

Theoretical Basis for Abatement

• Increases the supply of housing at all levels• Result is greater housing opportunity for all,

regardless of income level– This is not true only if 100% of the people

looking for housing are new to the city • Multi-family rental supply increases,

lowering rent costs for tenants

25

• “Lost revenue” is only relevant if investment would have occurred anyway

• Benefit taxes—high income people generate more revenue than they use—which results in more money available for basic services

Theoretical Basis for Abatement

Philadelphia Tax Abatement

Philadelphia Tax Abatement

26

Empirical Issues

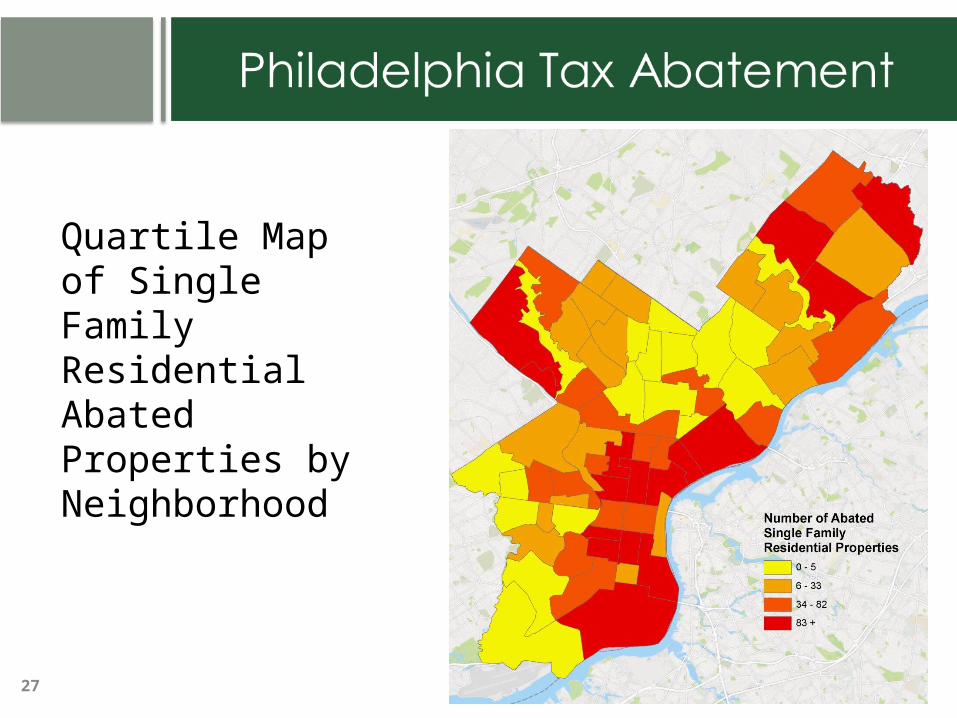

with Abatement

• Concentrated in Center City but appear all over

Quartile Map of Single Family Residential Abated Properties by Neighborhood

27

Philadelphia Tax Abatement

28

Empirical Issues

with Abatement

• Both rental and owner-occupied housing

Philadelphia Tax Abatement

29

Empirical Issues

with Abatement

• Significant use of abatement for low/moderate income units

Philadelphia Tax Abatement

30

Empirical Issues with Abatement

• Abated properties have been turning back to the tax roles– Approximately $1 billion per year (1% of taxable

value)• Now property tax revenue are increasing at a faster rate

than they otherwise would have• Careful studies have shown that the abatement

generates more revenue to the city than it forgoes

Philadelphia Tax Abatement

31

Equity and the Abatement

• Important to look at the total tax package– High wage and school taxes paid by high income

people mean that their revenues exceed the cost of producing services for them—especially since they place little burden on schools

• Philadelphia’s homestead exemption means that property tax rates are considerably lower for low and moderate income people (distribution of house values, and implied tax rates with the homestead invention)

Philadelphia Tax Abatement

32

Equity and the Abatement• Philadelphia’s homestead exemption means that

property tax rates are considerably lower for low and moderate income people

Market Value of Property

Abated Property Count

Percent of Abated Properties

< $124,999 1,465 10.6%

$125,001 to $250,000 3,317 23.9%

$250,001 to $500,000 6,129 44.2%

> $500,000 2,963 21.4%

Total 13,874 100.0%

Philadelphia Tax Abatement

33

Equity and the Abatement• Philadelphia’s homestead exemption means that

property tax rates are considerably lower for low and moderate income people

Market Value of Property

Abated Residential

Property Count

Percent of Abated Residential Properties

Total Residential Property Count

Percent of Total

Residential Properties

< $124,999 1,256 10.4% 264,956 57.7%

$125,001 to $250,000 3,062 25.4% 145,914 31.8%

$250,001 to $500,000 5,490 45.5% 39,875 8.7%

> $500,000 2,269 18.8% 8,474 1.8%

Total 12,077 100.0% 459,219 100.0%

Philadelphia: Tax StructurePhiladelphia Growth Coalition Proposal

• Lower wage tax• Lower net income tax• Increase commercial property tax

34

Fiscal Year Wage Tax – Resident

Wage Tax – non Resident

Real Estate Tax –

Residential

Real Estate Tax -

Commercial

BIRT – Gross

ReceiptsBIRT –

Net Income

2016 3.9102% 3.4828% 1.3998% 1.3998% 0.1415% 6.3900%

2026 3.0000% 2.5000% 1.3998% 1.6098% 0.1415% 3.0000%

Philadelphia: Tax StructurePhiladelphia Growth Coalition Proposal

35

Philadelphia Key Issues: Transit

SEPTA, once a drag on the city because of declining service, failing infrastructure, and uncertain funding is finally on solid footing

• TFRC (2002-07) led to act 44• More recently and more importantly Act 89—put

SEPTA on solid footing• Ridership is growing• More importantly, investments are being made take

advantage of SEPTA service creating a more viable, equitable and sustainable form of development

36

Philadelphia Key Issues: Water/Sewer

Philadelphia is a world leader in green infrastructure

• Saving billions by approaching the costs of its aging combined sewer system through pricing and incentives to limit runoff, rather than making huge capital investments

37

Philadelphia Key Issues: Water/Sewer

Philadelphia is a world leader in green infrastructure

• Saving billions by approaching the costs of its aging combined sewer system through pricing and incentives to limit runoff, rather than making huge capital investments

38

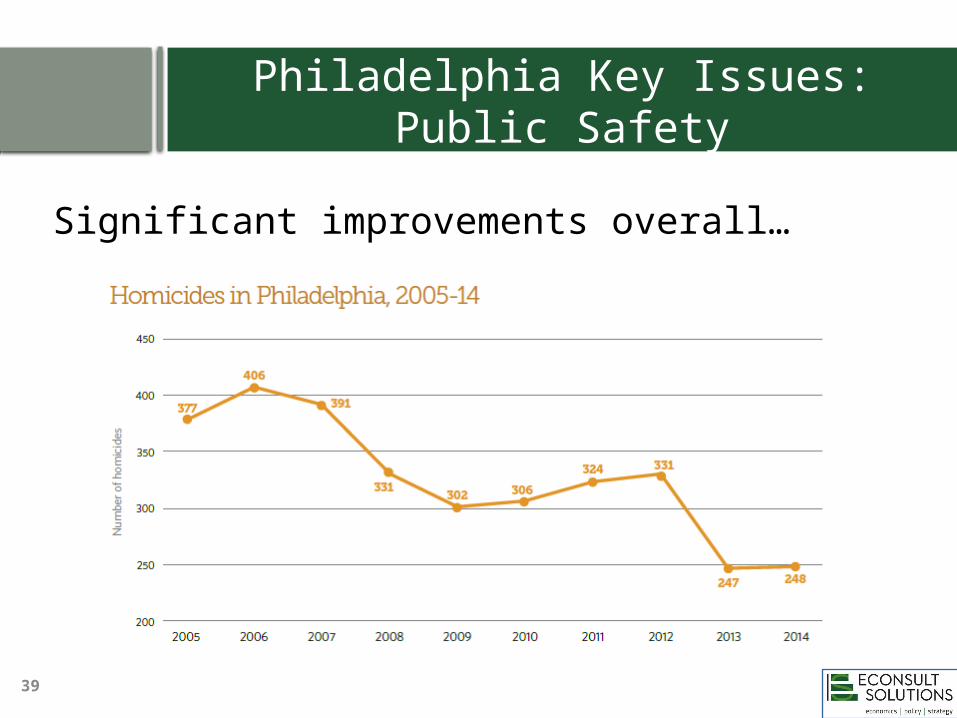

Philadelphia Key Issues: Public Safety

Significant improvements overall…

39

Philadelphia Key Issues: Public Safety

But geographically and demographically uneven…

40

Philadelphia Key Issues: SchoolsSchools remain a challenge for the City• Needy population• Fiscal challenges

41

OpportunitiesDelaware River Waterfront

42

OpportunitiesSchuylkill River Waterfront• Innovation Districts/Higher Ed tie-ins

43

Q & A