The Antitrust Masters Course V ABA Section of Antitrust Law Plenary Session Slides October 1, 2010...

34

The Antitrust Masters Course V ABA Section of Antitrust Law Plenary Session Slides October 1, 2010 – Part I Principal Lecturers Professor Andrew I. Gavil Honorable William E. Kovacic Professor Steven C. Salop Williamsburg Lodge, Williamsburg, VA

-

Upload

caiden-merryman -

Category

Documents

-

view

216 -

download

0

Transcript of The Antitrust Masters Course V ABA Section of Antitrust Law Plenary Session Slides October 1, 2010...

The Antitrust Masters Course VABA Section of Antitrust Law

Plenary Session Slides October 1, 2010 – Part I

Principal Lecturers

Professor Andrew I. Gavil

Honorable William E. Kovacic

Professor Steven C. Salop

Williamsburg Lodge, Williamsburg, VA

Session Agenda

• Evolution of Merger Analysis: Historical Foundations

• The Influence of the Horizontal Merger Guidelines, Old and New– Competitive Effects– Conditions of Entry– Efficiencies

2

Part I:Evolution of Merger Analysis:

Historical Foundations

Clayton Act Section 7:Three Stages of Development

• Originated in Clayton Act of 1914– Sherman Act covers “combinations,” but no

specific merger prohibition

• Celler-Kefauver Amendments of 1950– Response to limitations in language of original Act

and narrow interpretations by SCT

• Hart-Scott-Rodino Amendments – 1976– Created pre-merger notification system– Converted law enforcement into regulatory system

4

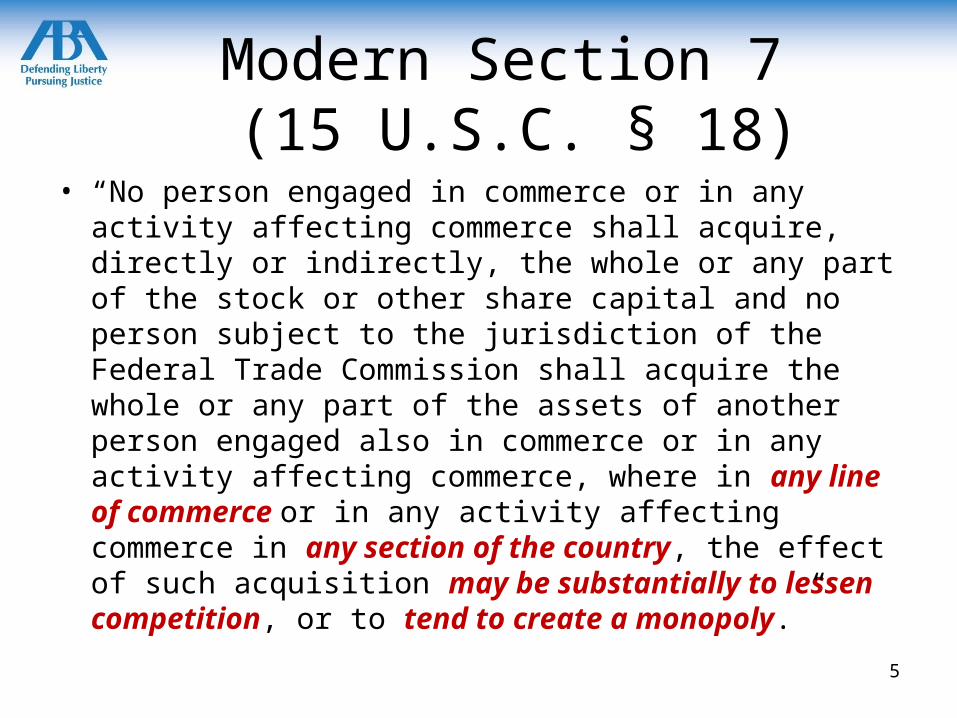

Modern Section 7 (15 U.S.C. § 18)

• “No person engaged in commerce or in any activity affecting commerce shall acquire, directly or indirectly, the whole or any part of the stock or other share capital and no person subject to the jurisdiction of the Federal Trade Commission shall acquire the whole or any part of the assets of another person engaged also in commerce or in any activity affecting commerce, where in any line of commerce or in any activity affecting commerce in any section of the country, the effect of such acquisition may be substantially to lessen competition, or to tend to create a monopoly.”

5

Merger Policies – 1960s-70s“Trends Toward Concentration”

• Brown Shoe (1962)– Stop Mergers in industries with “trends toward

concentration”• Reliance on 1950 Legislative History

– Pabst (1966) & Von’s Grocery (1966)• Combined 4.5% and 7.5% market shares

• Stewart dissent in Von’s:– “The sole consistency that I can find is that in

litigation under §7, the Government always wins.”

6

Merger Policies – 1960s-70sThe Structural Presumption Emerges

• Philadelphia Nat’l Bank (1963)– “…[W]e think that a merger which produces a firm

controlling an undue percentage share of the relevant market, and results in a significant increase in the concentration of firms in that market is so inherently likely to lessen competition substantially that it must be enjoined in the absence of evidence clearly showing that the merger is not likely to have such anticompetitive effects.”

• Product of IO thinking at the time– Structure-Conduct-Performance Paradigm

7

Merger Policies – 1960s-70sEfficiencies as a Negative

• Brown Shoe (1962)– Efficiency as an “offense”

• Procter & Gamble (1967)– “Possible economies cannot be used as a defense

to illegality. Congress was aware that some mergers which lessen competition may also result in economies but it struck the balance in favor of protecting competition.” Citing Brown Shoe

8

Merger Policies – 1960s-70sRebutting the Presumption

• General Dynamics (1974)– Rebutting the structural presumption – Statistical case by government was rebutted by

evidence that past market shares were NOT probative of future market power

• Last word from the Supreme Court on substantive analysis of mergers

9

Incipiency – Two Approaches

• Stop “trend towards concentration”– Emphasized by Brown

Shoe & other earlier cases

– No longer a focus of enforcement policy

• Stop merger before consummation– Implemented by HSR

system

– “Incipiency” transformed into synonym for “prediction”

10

Two Formative Events

1976Creation of HSR Pre-Merger

Notification System(Procedural Reform)

1982Revised HMGs

(Substantive Analysis)

• Increased role of agency regulation• Accelerates time for review•Substitutes “prediction” for effects analysis • Requires new analytical tools• Standard in courts shifts from proof to likelihood of success

• Integrates traditional SCP paradigm with oligopoly theory and game theory• New approach to market definition (hypothetical monopolist SSNIP test)• Use of HHI instead of CR4•Focus on coordinated effects• Supports consideration of entry and later efficiencies to rebut prima facie case 11

Part II:The Influence of the Horizontal

Merger Guidelines, Old and New

13

Role of Merger Guidelines

• In U.S.– Horizontal Merger Guidelines (1968, 1982-97)

– Vertical Merger Guidelines (1984)

– Commentaries on Merger Guidelines (2006)

– New Horizontal Merger Guidelines (2010)

• In E.U.– Notice on Definition of Relevant Market (1997)

– Horizontal Merger Guidelines (2004)

– Implementing Regulation (2004)

– Non-Horizontal Merger Guidelines (2008)

• Many other jurisdictions as well

Then and Now:Some Defining Features

1982-1997 Guidelines• “Unifying theme”: market power

• But, suggested sequential analysis beginning with market definition

• HHI Thresholds – Replace CR2 and CR4

• Competitive Effects – Coordinated & Unilateral

• Entry and Repositioning– Timely, Likely, Sufficient

– Committed vs. uncommitted

– Two year threshold

• Efficiencies– Verifiable & merger-specific

2010 Guidelines• “Unifying theme”: market power

• Deemphasizes sequential analysis

• Emphasis on competitive effects – More broadly defined

– Explicit concern with exclusion

– Market definition less central

– Expanded treatment of unilateral effects

– More skeptical of buyer power

• Highlight latest economic tools• HHI Thresholds (Retained but raised)

• Entry and Repositioning– More skeptical view

– Committed/uncommitted redefined

– Explicit two year threshold dropped

• Efficiencies– Little change

14

Influence of 1982-97 HMGs in the Courts

• Still need to know the law as influenced by the old HMGs:

– The Structural Presumption• Heinz (2001)(Baby Food)

– Market Definition and Use of HHIs• Cardinal Health (1998)

– Coordinated Effects• HCA (1986); Arch Coal (2004); CCC

Holdings (2009)

– Unilateral Effects• Staples (1997); Oracle (2004); Whole Foods

(2008)

– Entry• Waste Management (1984); Baker Hughes

(1990)

– Efficiencies (No court success)• University Health (1991); Butterworth Health

(1996); Long Island Jewish Med. Cntr. (1997); Staples (1997); Heinz (2001)

Lower Courts Embraced and Followed HMGs:

- But agencies didn’t always prevail; and

- Courts held agencies to their own HMGs

15

Some Current Challenges

• 2010 HMGs are not that different from 1997 HMGs, or 2006 HMG Commentaries, BUT….– Different enough that gap between agency practice and law of mergers

in courts has grown

• Critical Issues for Future:– Will the agencies test the differences in court?

– Will the courts embrace or reject?

– Note: Courts first rejected, then widely embraced 1982 HMGs in significant ways

We next turn to a more in-depth examination

of the approach of the new HMGs…

16

“Unifying Theme”

• Section 1: – “The unifying theme of these Guidelines is that

mergers should not be permitted to create, enhance, or entrench market power or to facilitate its exercise.” (new language)

– “A merger enhances market power if it is likely to encourage one or more firms to raise price, reduce output, diminish innovation, or otherwise harm customers as a result of diminished competitive constraints or incentives.” (broader focus?)

17

Organization of Guidelines• Expansion from 5 to 13 sections:

1. Overview (old section §0)

2. Evidence of Adverse Competitive Effects (New)

3. Targeted Customers and Price Discrimination (Expanded)

4. Market Definition (old § 1)

5. Market Participants, Market Shares, and Market Concentration (old § § 1.3-5)

6. Unilateral Effects (old §2.2) (Note reversal of order and expansion)

7. Coordinated Effects (old §2.1)

8. Powerful Buyers (New)

9. Entry (old §3)

10. Efficiencies (old §4)

11. Failure and Exiting Assets (old §5)

12. Mergers of Competing Buyers (New)

13. Partial Acquisitions (New)

New: 24 examples sprinkled throughout. 18

In General:

• Fewer changes from 1992 than some claim– Most of the more controversial points are in the

2006 Commentaries

• Easier to read and less formalistic than 1992

• “Performance” not “design” standards

Market Definition:

• Market definition an imperfect exercise

• Narrow markets generally more appropriate, as long as satisfy the SSNIP test

• Not tied to old algorithm of starting with single product then mechanically expanding market to next-closest substitute, which is a recipe for error

• Soften “smallest market” principle

• Greater acceptance of price discrimination markets

Some Observations from

5,000 Feet

19

Market Definition (continued):

• Characterization of High Margins– Do not by themselves prove monopoly power, but– Indicate either reduced price sensitivity by customers or

coordination– Apparently provocative to lawyers, but correct to economists– Query: What is the alternative explanation?

• Critical Loss in New HMGs– Explicitly use approach that infers reduced price sensitivity

from margin– Uses Diversion Ratio (DR) and Recapture Ratio (RR)– DR is the fraction of sales lost by one merging firm

to the other merging firm, when the price of one product is increased

– RR is the fraction of sales lost by one merging firm to all other firms in the proposed relevant market, when the price of one product is increased

– Outcome of SSNIP test is closely related to the GUPPI score used for unilateral effects

• Measuring DR– DR is related to the own-elasticity of demand and the cross-

elasticity of demand– Relies on buyer substitution evidence as discussed in 1992

HMGs

Some Observations from

5,000 Feet

2020

Market Definition (continued):

• Types of Evidence of Buyer Substitution *– Past responses of buyers to changes in relative price

– Buyer surveys as to likely responses to price increases

– Inferences drawn from characteristics of products and geographic locations known to matter to buyers

– Conduct of industry participants (how buyer substitution is monitored and understood by sellers)

– Industry experts

Some Observations from

5,000 Feet

21

*Source: Jonathan B. Baker, Market Definition: An Analytical Overview, 74 Antitrust L.J. 129 (2007).

21

Competitive Effects:

• Unilateral– Elimination of 35% threshold, but HHI safe harbors apply

– Market shares are not key; diversion ratio and value of diverted sales are key

– GUPPI score as quantitative measure• No efficiency offset

• No explicit equation in text

– Quasi-safe harbor for “small” GUPPI score

– No explicit anticompetitive presumption based on GUPPI• Possible implicit presumption if GUPPI implies that merging

firms by themselves satisfy SSNIP test

– Skeptical of entry and repositioning, absent historical evidence

• Cross-market balancing – Narrow Markets will put greater pressure on allowing

cross-market balancing

– Guidelines indicate increased willingness to consider balancing and evaluate consumer welfare across all “inextricably linked” markets.

Some Observations from

5,000 Feet

2222

Competitive Effects (continued)

• Coordinated– More stress on history of collusion

– Avoid straightjacket of having to prove detection and punishment in detail

• Apparent view that evidentiary pendulum has swung too far

– More emphasis on “parallel accommodative responses”

• Buyer-Side Market Power:– More concern when buyers merge

– More skeptical that big buyers can protect entire market from price increases

Some Observations from

5,000 Feet

2323

A Closer Look at the “Value of Diverted Sales”

and the GUPPI Score

For Additional Explanation, see Salop & Moresi:

http://www.crai.com/uploadedFiles/Publications/Commentary-on-the-GUPPI.pdf

The GUPPI Score• Gross Upward Pricing Pressure Index

• A measure of the impact of the merger on the pricing incentives of the merging firms– Also used for market definition (hypothetical monopolist SSNIP test)

• Depends on several factors– Diversion Ratios– Price-Cost Margins– Prices

• Only a rough gauge. Does not take into account all the relevant factors, including: – Efficiencies – Repositioning and entry– Rate at which higher costs lead to higher prices– Other merging product price reactions– Rivals’ Price reactions

• GUPPI is described in words in the 2010 HMGs25

Value of Diverted Sales (VDS)• VDS measures the extra profits obtained post-merger from a unilateral

price increase, relative to the pre-merger world

• When firm-1 raises price of product-1, some sales are diverted to product-2– Pre-merger world: simply lost profits of firm-1– Post-merger world: those profits recaptured after merger

“Value of diverted sales” when raise price of product-1 equals

“Number of units diverted to product-2,” times

“Price-cost margin on product-2 (measured in dollars)”

• GUPPI is the “value of diverted sales” scaled into a percentage

26

Deriving the GUPPI Score

GUPPI = “scaled” measure of “value of diverted sales”

GUPPI equals

“Value of diverted sales”divided by

“Value of revenue on sales lost from price increase”

Putting this all together ….. 27

GUPPI Score Formula

GUPPI = DR12 x M2 x PR

• DR12 – “Diversion Ratio” – measure of closeness of substitution

• Provides a measure of “Reasonable Interchangeabilty” as derived from “cross-price elasticity of demand” (DuPont)

– Diversion Ratio definition: percentage of sales lost by product-1 that move to product-2, when raise price of product-1

– Estimate DR with the same consumer substitution evidence as used for market definition

• DRs measured product-by-product

28

GUPPI Score Formula (con’t)

GUPPI = DR12 x M2 x PR

• M2– Percentage Margin of product-2 (price minus cost,

expressed as a percentage of price)– Gauges increased profits (margin) on sales diverted to

product-2

• PR – Price ratio of product-2 relative to product-1– Serves as a scaling factor

29

GUPPI Example

• DR12 = 15%– If the price of product-1 is increased, 15% of the customers

that leave product-1 would substitute to product 2• M2=30%

– Product-2 earns a margin of 30% (modest)• PR =1

– Products 1 and 2 have equal prices

• GUPPI = DR12 x M2 x PR

– GUPPI = 15% x 30% x 1 = 4.5%

30

Calibrating GUPPIs• HMGs suggest a quasi-safe harbor for a “small” GUPPI

– Does “small” = 5%? – HMGs do not say

• If GUPPI>10% (and demand is linear), then the two merging products by themselves would comprise a relevant merger to monopoly market– GUPPI>10% means that a hypo. Monopolist that owned the two

products would have the incentive to raise price by more than 5%.– Thus, potential “anticompetitive presumption” level, though not

defined as such in the HMGs

– Silence is golden! It is premature to create a strong presumption.

31

2010 HMGs:Some Additional Issues

• More accurately reflect or change enforcement practices?– Have we abandoned concern for 6-5 mergers?

– Economic tools for analysis tried and true?

– Will enforcement be more like 1989? or 1999? or 2007?

• Will emphasis on unilateral effects stick?

• Will new HMGs be effective in pushing back against losses in cases like Arch Coal and Oracle? If so, any risks?

• What are the most controversial changes that could reach courts? How will they fare?

• What are likeliest next areas of evolution?– Relevance and utility of 1984 Vertical Merger Guidelines?

32

Recent Merger Challenges of Interest

• Whirlpool – import of foreign entry and potential for expansion

• XM-Sirius – changing technology and likely future entry

• CCC Holdings – First FTC PI in some time

– Split level standards for agency review? (Whole Foods)

• Google - AdMob – Apple's entry as a game changer

• Ovation – Does Market definition still rule?

33

Day 2, Session 1The End!