The 2014 U.S Pharmaceutical · PDF file2014 Strategic management presentation . ... 7 Proton...

55

April 2013 IMS Health Overview The 2014 U.S Pharmaceutical Market: Trends, Issues & Outlook Prepared for GPhA By Doug Long VP Industry Relations [email protected] February 11, 2015

-

Upload

nguyenhuong -

Category

Documents

-

view

226 -

download

0

Transcript of The 2014 U.S Pharmaceutical · PDF file2014 Strategic management presentation . ... 7 Proton...

April 2013

IMS Health Overview

The 2014 U.S Pharmaceutical Market: Trends, Issues

& Outlook

Prepared for

GPhA

By Doug Long

VP Industry Relations

February 11, 2015

All reproduction rights, quotations, broadcasting, publications reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording, or any information storage and retrieval system, without express written consent of IMS HEALTH.

2014 Strategic management presentation

Top US Pharmaceutical events of 2014

• HEP C

• Double digit dollar growth is back caused by Innovation and

list price increases

• Patent Expiries

− the ones that didn’t happen and the ones that did

• Branded formulary blocks

• The “end” of the Inversion fad

• 42 NMEs launched (41 approved) most in more than a decade, and 18 orphans most in a year ever (and one more than last year’s record 17)

• The withdrawal of Incivek and Victrelis (i.e. launched in 2011 and done by late 2014 – a product’s life is not 10-15 years in these cases)

•

5.2%

1.1%

4.1%

0.7%

-2.8%

3.5%3.4%

1.4%

12.4%

1.9%

12.9%

1.7%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Sales TRx

2010 2011 2012 2013 MAT Nov 2014 YTD Nov 2014

US Market Sales and Dispensed Prescription growth

Source: IMS Health, National Sales Perspectives, Nov 2014 IMS Health, National Prescription Audit, Nov 2014

% Growth of sales and prescription of products Total market

12.4% 12.0%

14.2%

0%

5%

10%

15%

20%

25%

MAT Nov 2014

% G

RO

WTH

1.9%

-6.8%

4.0%

-10%

-5%

0%

5%

MAT Nov 2014 %

GR

OW

TH

Source: IMS Health, National Prescription Audit, Branded generics disaggregated, Nov 2014

Source: IMS Health, National Sales Perspectives, Branded generics disaggregated, Nov 2014

Twelve months ending Nov 2014 Twelve months ending Nov 2014 % Growth US$ % Growth TRx

Total market Brands Generics

Brands and Generics sales and TRx growth (MAT)

Specialty $ Growth is 25.1%

Reasons for Generic Price Inflation

Regulatory/Quality and other costs – with the increased scrutiny from the FDA, manufacturers need to invest more into their quality systems and when a quality / supply issue arises due to 483s, it creates the opportunity to increase prices to recoup part of their investment

Customer consolidation – with the increased purchasing power of the customers, manufacturers need to make up value on products where they can

Fewer new product launches – generic manufacturers make money by launching new products, reducing CGS, M&A activity and raising prices; with fewer launches, it puts more pressure on the “in-line” product portfolio which again is a driver to increase prices

What are people thinking about?

• Pharmacies

• Purchasing Alliances

• Controlled Substances abuse

• Access to Specialty Drugs

• Generic Price Inflation

• Track and Trace

• Wholesalers

• Purchasing Alliances

• Controlled Substances abuse

• Access to Specialty Drugs

• Generic Price Inflation

• Track and Trace

• Payors

• Soaring costs of Specialty Drugs

• Generic Price Inflation

• Pruning formularies

• Generic Manufacturers

• Purchasing Alliances

• Portfolio Optimization

• Brand drugs

• Proposed labeling changes

• Tax Inversion

• Brand/Specialty Manufacturers

• Price backlash

• Becoming more specialized

• Oral Specialty

• Orphan Drugs

• Tax Inversion

• Consumers

• Rising costs

• Specialty Tiers

• Losing Insurance

Top Molecules on a TRX Basis- 2014 (MAT November)

Rank Molecule TRx (000) Share Growth

1 ACETAMINOPHEN-HYDROCODONE 120,945 2.8% -6.5%

2 LEVOTHYROXINE 118,386 2.8% 3.4%

3 LISINOPRIL 102,975 2.4% 2.0%

4 METOPROLOL 84,397 2.0% 0.9%

5 ATORVASTATIN 80,207 1.9% 19.3%

6 AMLODIPINE 77,104 1.8% 5.0%

7 METFORMIN 76,082 1.8% 5.5%

8 OMEPRAZOLE 73,773 1.7% 5.1%

9 SIMVASTATIN 72,304 1.7% -9.2%

10 ALBUTEROL 66,362 1.5% 4.6%

TRx

Source: IMS Health, National Prescription Audit, November 2014

Which Molecules gained and lost TRX Volume in 2014?

TRX Gains Gain (Mil.) TRX Losses Loss (Mil.)

ATORVASTATIN 12,981,907 ATENOLOL -1,880,428

GABAPENTIN 6,640,749 FLUTICASONE-SALMETEROL -2,066,815

LOSARTAN 5,733,362 CODEINE-GUAIFENESIN -2,186,187

FLUTICASONE 4,923,766 VALSARTAN -2,191,013

PANTOPRAZOLE 4,307,358 WARFARIN -2,377,544

METFORMIN 3,954,260 ESOMEPRAZOLE -2,868,577

LEVOTHYROXINE 3,884,443 ZOLPIDEM -2,896,754

AMLODIPINE 3,674,845 AZITHROMYCIN -3,761,959

OMEPRAZOLE 3,553,121 SIMVASTATIN -7,360,451

ESCITALOPRAM 3,402,867 ACETAMINOPHEN-HYDROCODONE -8,389,680

12 Months ending Nov. 2014

Source: IMS Health, National Sales Perspectives, Nov 2014

Top specialty products – MAT Nov 2014

Sales ($MN) Share Growth

U.S. Specialty Market 116,257 100.0% 25.1%

1 Sovaldi 7,570 6.5% - - -

2 Humira 7,005 6.0% 28.0%

3 Enbrel 5,419 4.7% 15.8%

4 Remicade 4,487 3.9% 8.9%

5 Copaxone 3,833 3.3% 2.6%

6 Neulasta 3,817 3.3% 7.0%

7 Rituxan 3,448 3.0% 4.1%

8 Atripla 2,956 2.5% 2.8%

9 Avastin 2,864 2.5% 5.9%

10 Tecfidera 2,477 2.1% 237.4%

Top 10 43,876 37.7% 40.6%

Source: IMS Health, National Sales Perspectives, Nov 2014

Top specialty products – MAT Nov 2014

Sales ($MN) Share Growth

11 Truvada 2,466 2.1% 9.6%

12 Epogen 2,413 2.1% 7.4%

13 Gleevec 2,269 2.0% 20.9%

14 Herceptin 2,165 1.9% 11.1%

15 Olysio 1,888 1.6% - - -

16 Stelara 1,422 1.2% 51.6%

17 Tysabri 1,407 1.2% 64.5%

18 Stribild 1,265 1.1% 133.1%

19 Gilenya 1,250 1.1% 19.1%

20 Alimta 1,217 1.0% 2.3%

Top 20 61,638 53.0% 39.8%

Products Company US$mn% Market

Share% Growth

US Industry 368,784 100.0 12.4

1 Abilify® OTS 7,725 2.1 19.7

2 Sovaldi® GS- 7,570 2.1

3 Humira® AV1 7,005 1.9 28.0

4 Nexium® AZN 6,016 1.6 -1.8

5 Crestor® AZN 5,808 1.6 9.0

6 Enbrel® AAI 5,419 1.5 15.8

7 Advair Diskus® GSK 4,857 1.3 -5.7

8 Remicade® JAN 4,487 1.2 8.9

9 Lantus Solostar® S.A 4,343 1.2 45.3

10 Copaxone® TVN 3,833 1.0 2.6

Top 10 57,062 15.5 29.5

MAT Nov 2014

Sales of leading products

Source: IMS Health, National Sales Perspectives, Nov 2014

Products Company US$mn% Market

Share% Growth

11 Neulasta® AAI 3,817 1.0 7.0

12 Rituxan® GTC 3,448 0.9 4.1

13 Januvia® MSD 3,393 0.9 19.5

14 Lantus® S.A 3,331 0.9 32.1

15 Spiriva Handihaler® B.I 3,311 0.9 9.5

16 Lyrica® PFZ 3,031 0.8 26.6

17 Atripla® BMG 2,956 0.8 2.8

18 Avastin® GTC 2,864 0.8 5.9

19 Celebrex® PFZ 2,583 0.7 15.8

20 Levemir® N-N 2,505 0.7 55.9

Top 20 88,302 23.9 24.1

MAT Nov 2014

Sales of 11-20 products

Source: IMS Health, National Sales Perspectives, Nov 2014

Products Company US$mn% Market

Share% Growth

21 Oxycontin® PUF 2,501 0.7 -3.1

22 Tecfidera® BGE 2,477 0.7 237.4

23 Truvada® GS- 2,466 0.7 9.6

24 Epogen® AAI 2,413 0.7 7.4

25 Gleevec® NVR 2,269 0.6 20.9

26 Symbicort® AZN 2,177 0.6 41.3

27 Herceptin® GTC 2,165 0.6 11.1

28 Vyvanse® SHI 2,055 0.6 17.6

29 Zetia® MU& 2,014 0.5 19.0

30 Xarelto® JAN 1,967 0.5 114.5

Top 30 110,805 30.0 25.0

MAT Nov 2014

Sales of 21-30 products

Source: IMS Health, National Sales Perspectives, Nov 2014

What do we mean by specialty pharmaceuticals? IMS has established an industry standard definition

• Initiated only by a specialist

• Generally not oral

• Require special handling

• Unique distribution

• High expense

• Warrants intensive patient counseling

• Requires reimbursement assistance

Medicines that treat specific, complex chronic diseases with four or more of the following attributes:

Top Specialty events to watch for!

• HEP C Innovation and Pricing

• Patient as a Payer

− Specialty tiers in exchanges

• Growing demand for value driven metrics (CE and RWE)/adoption of guidelines

• Copaxone ® 3X weekly and Copaxone ® generic?

• Specialty space gets more crowded with new entrants and more orals are coming

• The first Biosimilar applications are filed

• Co Pay programs cooperation by payers

• Possible 340B changes

• Gene Therapies & Orphan drugs price discussions

US$mn% Market

Share% Growth

US Industry 368,784 100.0 12.4

1 Analogs of human insulin 18,360 5.0 36.6

2 Antiarth,biol resp mod 14,443 3.9 23.9

3 Antipsychotics,oth 14,177 3.8 17.9

4 Lipid regulators 12,877 3.5 4.7

5 Antineo monoclonal antib 10,766 2.9 12.2

6 Viral Hepatitis Products 10,607 2.9 678.0

7 Proton pump inhib 8,783 2.4 -8.2

8 HIV antiviral combination 8,624 2.3 17.5

9 Analeptics 8,261 2.2 -2.2

10 Steroid,inhaled bronch 8,084 2.2 8.9

Top 10 114,982 31.2 23.4

MAT Nov 2014

Leading classes

Sales of leading therapy classes

Source: IMS Health, National Sales Perspectives, Nov 2014

US$mn% Market

Share% Growth

11 Neurological disorders 7,949 2.2 36.6

12 GI anti-inflam 7,945 2.2 12.7

13 Anti-depressants 6,785 1.8 -23.9

14 Dpp-4 Inhib 6,342 1.7 23.6

15 Angiotensin II antagonists 5,870 1.6 -9.4

16 Tyrosine kinase inhibitor 5,383 1.5 27.4

17 Codeine & comb 5,281 1.4 9.0

18 Seizure disorders 5,163 1.4 14.9

19 Immunologic interferons 4,869 1.3 -5.3

20 Immune system adjuncts 4,809 1.3 4.9

Top 20 175,378 47.6 17.1

MAT Nov 2014

Leading classes

Sales of 11-20 therapy classes

Source: IMS Health, National Sales Perspectives, Nov 2014

DollarsAC

US$mn Total Rx dispensed

AC

TRxs mn

Viral Hepatitis Products 9243.5 Anti-depressants 13.0

Analogs of human insulin 4920.4 Seizure disorders 10.1

Antiarth,biol resp mod 2790.7 Antiarth,plain 4.4

Antipsychotics,oth 2147.8 Thyroid hormone,synth 4.1

Neurological disorders 2131.0 Anticoagulants, Other 4.0

Anticoagulants, Other 1402.4 Proton pump inhib 3.7

HIV antiviral combination 1282.0 Steroid,inhaled nasal 3.7

Monoclonal antibodies 1261.8 Biguanides 3.4

Dpp-4 Inhib 1211.4 Antinauseant 5HT3 antag 3.1

Antineo monoclonal antib 1166.5 Angiotensin II antagonists 2.9

Largest absolute growth by leading therapy classes, Sales & TRx (MAT)

Source: IMS Health, National Sales Perspectives, Nov 2014, National Prescription Audit, Nov 2014

DollarsAC

US$mn Total Rx dispensed

AC

TRxs mn

Hormones,androgens -187.2 Diuretics,comb -1.1

Anti-migraine -221.2 Antidopa phenothiazine -1.1

Immunologic interferons -272.1 Hormones -1.2

Tetracyclines -428.5 Osteoclast Inhibitors -1.4

Non-barb,oth -462.2 Antihyperlipidemic agt -1.4

Antihyperlipidemic agt -491.0 Ace inhibitors -1.6

Heparins -519.8 Vitamin K Antagonists -2.4

Angiotensin II antagonists -608.2 Non-barb,oth -3.3

Proton pump inhib -780.9 Macrolides & related -3.6

Anti-depressants -2125.6 Codeine & comb -7.9

Largest absolute neg growth by leading therapy classes, Sales & TRx (MAT)

Source: IMS Health, National Sales Perspectives, Nov 2014, National Prescription Audit, Nov 2014

TRxs mn% Market

Share% Growth

US Industry 4,277 1.0 1.9

1 Anti-depressants 294 6.9 4.6

2 Lipid regulators 258 6.0 0.5

3 Codeine & comb 194 4.5 -3.9

4 Ace inhibitors 174 4.1 -0.9

5 Seizure disorders 144 3.4 7.5

6 Proton pump inhib 135 3.2 2.8

7 Beta blockers 135 3.1 -0.8

8 Thyroid hormone,synth 121 2.8 3.5

9 Calcium blockers 109 2.5 2.3

10 Antiarth,plain 98 2.3 4.7

Top 10 1,661 38.8 1.7

MAT Nov 2014

Leading therapy class

Dispensed prescriptions of leading therapy classes

Source: IMS Health, National Prescription Audit, Nov 2014

TRxs mn% Market

Share% Growth

11 Angiotensin II antagonists 94 2.2 3.2

12 Benzodiazepines 94 2.2 -0.4

13 O/C estrogen/progestogen 83 2.0 1.4

14 Biguanides 79 1.8 4.6

15 Beta agonists 70 1.6 2.8

16 Hormones,cort plain,oral 62 1.5 3.8

17 Penicillins 61 1.4 -1.5

18 Mus relx,non-surg 61 1.4 3.8

19 Analeptics 59 1.4 4.9

20 Macrolides & related 59 1.4 -5.7

Top 20 2,384 55.7 1.7

MAT Nov 2014

Leading therapy class

Dispensed prescriptions of 11-20 therapy classes

Source: IMS Health, National Prescription Audit, Nov 2014

Biologicals future loss of exclusivity

Twelve compounds will present a US$ 73 billion opportunity by 2020

Not considered existing biosimilars such as Epoetin Alfa expired in EU, but still patent protected in the US

Source: IMS MIDAS, 09/2013, IMS Patent focus

EU expiry date US expiry date

2018 2016

2015 2028 (extended)

2014 2018

2014 2015

Expired 2018

2019 2019

Expired Expired

2015 2016

2014 2019

2017 2014

2015 2015

2016 2016

5 0 10

Etanercept (Enbrel)

Adalimumab (Humira)

4.3

Infliximab (Remicade)

5.6

5.6

Trastuzumab (Herceptin)

4.8

5.1

7.5

Insulin Glargine (Lantus)

Interferon Beta-1A (Avonex, Rebif)

7.5

6.2

Ranibizumab (Lucentis)

Insulin Aspart (Novomix, Novorapid)

Pegfilgrastim (Neulasta)

Bevacizumab (Avastin)

Glatiramer Acetate (Copaxone)

Rituximab (Mabthera)

7.8

5.4

9.4

4.3

Global Sales (MAT 09/2013), US$ billion

Total ~ US$ 73

billion

Despite biosimilars gradually emerging

2012

ROW

Europe

2013

Italy, largest Biosimilars

market in EU*

Mar Jun

Biosimilar G-CSF (Zarzio)

prescribed more than originator

N° of Biosimilar applications

(EMA) all-time high (8)

Lilly & BI submission for insulin glargine

biosimilar

Market trends

Regulatory

2nd GSF approved in Japan

Inflectra# (Infliximab Biosimilar)

approved EU

2014

Market trends

Regulatory

Source: Secondary research. List not exhaustive. (*) at ex-manufacturer price levels, not including rebates and discounts. (#) Recommended for RA (Rheumatoid arthritis), CD (Crohn’s disease), UC (Ulcerative colitis), AS (Ankylosing spondylitis), PA (Psoriasis), PsA (Psoriatic arthritis)

Follitropin alfa biosimilar approved

Jul

FDA approved Tbo-filgrastim but filed in the

U.S. as BLA

Remsima (Infliximab Biosimilar)

launched in Korea

Teva announce launch of

GRANIX in USA

Nov

Sandoz Omnitrope to be sole subsidised

somatropin from Jan 2015 in NZ

Herzuma (Trastuzumab bs)

approved in Korea

In Europe, biosimilar uptake exhibits different paces

A few countries have reached or approached the maturity stage

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Mar-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13

% U

pta

ke,

SU

Biosimilar uptake across Europe MAT 03/2007 – 12/2013 (Volumes, SU)

AUSTRIA BELGIUM FRANCE GERMANY HUNGARY

ITALY ROMANIA SPAIN SWEDEN UK

Total 10 countries 425M €

MAT 12/2013 Fast uptake at launch, now mature

Consistent uptake

Slow uptake, cultural resistance

Fast growing due to faster growing market trend

Payers incentivized Biosimilars

Source: IMS MIDAS, MAT Sep 2013

The global playing field continues to expand with players finding niches

Players differ not only in geographical spread but also a wider biologic portfolio

Emerging markets players

Domestic players

Serving domestic market only*

Serving 2+ countries

# Pharmerging markets only

Source: IMS Health, MIDAS, MAT Dec 2012. (*) restricted to MIDAS sales data and recombinant and synthesised prods only.

© 2013, IMS HEALTH

International Reach

Government backed players

0%

5%

10%

15%

20%

25%

30%

$0

$10

$20

$30

$40

$50

$60

$70

2010 2011 2012 2013 MAT Nov 2014

% G

RO

WTH

US$

US$BN

Generics Growth

Source: IMS Health, National Sales Perspectives, Branded generics disaggregated, Nov 2014

Generics Sales are $65 Billion and Growth is 14.2%

0%

5%

10%

15%

20%

25%

30%

2700

2800

2900

3000

3100

3200

3300

3400

3500

3600

2010 2011 2012 2013 MAT Nov

2014

% G

RO

WTH

TRx

TRx m

n

Generics Growth

Source: IMS Health, National Sales Perspectives, Branded generics disaggregated, Nov 2014

Generics TRx are 3.5 Billion and Growth is 4.2%

30.1

%

69.9

%

2010

18.0

%

82.0

%

MAT Nov 2014 87.3

%

12.7

%

2010

82.4

%

17.6

%

MAT Nov 2014

Source: IMS Health, National Sales Perspectives, Nov 2014, National Prescription Audit, Nov 2014, Branded generics disaggregated

sales: $315.7bn

sales: $368.8bn

TRx: $4bn

TRx: $4.3bn

% MARKET SHARE US$ % MARKET SHARE TRx

Generics

Brands

Share of Sales & TRx brands and generics

-200

-100

0

100

200

300

400

2010 2011 2012 2013 MAT Nov 2014 YTD Nov 2014

AC T

Rxs M

N

Generics Brands

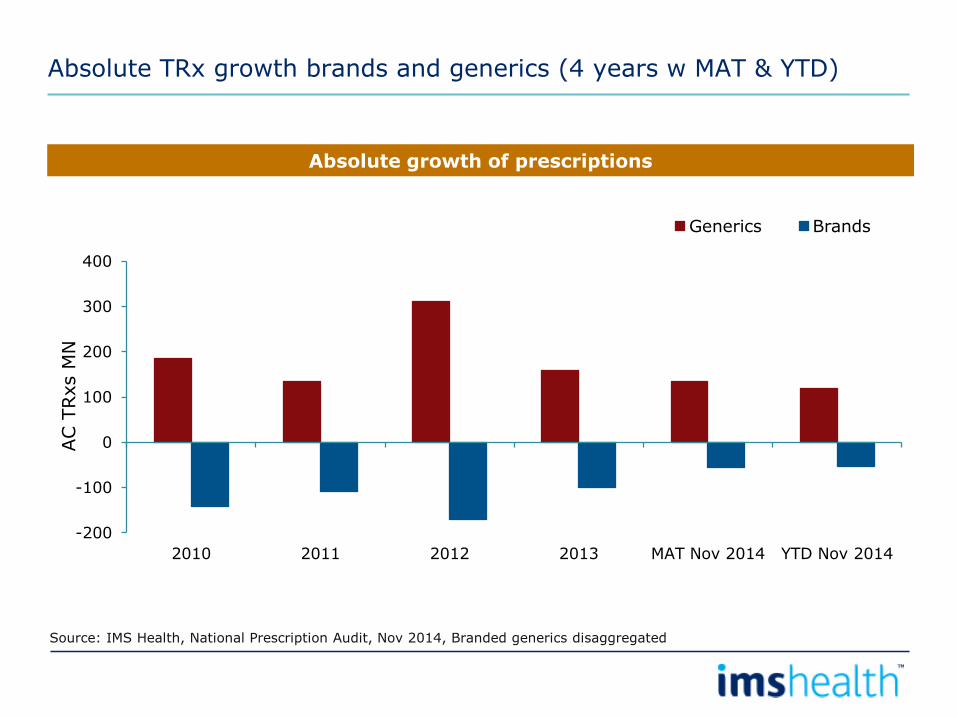

Source: IMS Health, National Prescription Audit, Nov 2014, Branded generics disaggregated

Absolute growth of prescriptions

Absolute TRx growth brands and generics (4 years w MAT & YTD)

Top US Generics events

• Generic Price Inflation

• Mergers

• How does the Generic Labeling Rule Play Out?

• Copaxone ® & Nexium ® Generics- When?

• Abilify ®

• FDA Guidance on Biosimilars (Naming, etc.)

• Rx to OTC Switches (Nexium) Flonase

• Impact of Consolidated Global Generic Purchasing

Products facing LOE in the next 4 years are valued at $78.4Bn

$17.8

$15.4 $16.6

$32.8

$10.3 $11.0

$27.7

$18.9

$11.1

$20.7

$0

$5

$10

$15

$20

$25

$30

$35

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Nexium, Abilify and Namenda face generic competition in 2015

U.S. Patent Expiry Exposure

Sales from year-prior to expiry for years 2009-14; sales in MAT Sep 2014 used for years 2015-18

Source: IMS Health, Dec 2014

US$mn% Market

Share% Growth

US Industry 368,784 100.0 12.4

1 Novartis (incl Sandoz) 19,625 5.3 3.2

2 Astrazeneca 19,453 5.3 7.9

3 Johnson & Johnson 18,719 5.1 36.6

4 Pfizer (incl Greenstone) 17,996 4.9 7.0

5 Roche (incl Genentech) 17,450 4.7 5.5

6 Merck & Co 17,358 4.7 6.5

7 Teva 17,294 4.7 12.5

8 Gilead Sciences 16,980 4.6 128.5

9 Amgen Corporation 16,264 4.4 10.9

10 Sanofi Aventis 14,380 3.9 20.0

Top 10 175,521 47.6 17.1

MAT Nov 2014

Leading corporations

Sales of leading corps

Source: IMS Health, National Sales Perspectives, Nov 2014

US$mn% Market

Share% Growth

11 Actavis US 13,824 3.7 -1.3

12 Abbvie Inc 12,449 3.4 3.0

13 GlaxoSmithKline 12,230 3.3 -3.8

14 Lilly 11,893 3.2 -22.6

15 Novo Nordisk 10,147 2.8 26.5

16 Mylan Labs, Inc. 8,642 2.3 9.2

17 Boehringer Ingelheim 8,198 2.2 6.2

18 Otsuka America Ph 8,084 2.2 20.9

19 Biogen Idec Corp 6,002 1.6 66.1

20 Shire US Corp 4,984 1.4 18.8

Top 20 271,974 73.7 12.3

MAT Nov 2014

Leading corporations

Sales of 11-20 corps

Source: IMS Health, National Sales Perspectives, Nov 2014

US$mn% Market

Share% Growth

US Industry 64,040 17.4 14.5

1 Teva 8,275 12.9 21.9

2 Mylan Labs, Inc. 7,009 10.9 4.9

3 Actavis US 5,737 9.0 -8.2

4 Sandoz (Novartis) 5,076 7.9 19.8

5 Sun Pharma 2,654 4.1 14.5

6 Par Pharm Corp 1,906 3.0 -10.9

7 Endo Pharm Inc. 1,845 2.9 63.0

8 Lupin Pharma 1,809 2.8 29.9

9 Dr Reddy Inc 1,687 2.6 22.2

10 Hospira Inc 1,438 2.2 6.4

Top 10 37,436 58.5 11.2

MAT Nov 2014

Sales of unbranded generics by leading

corporations

Sales of leading corps in Unbranded Generics

Source: IMS Health, National Sales Perspectives, Nov 2014

US$mn% Market

Share% Growth

11 Apotex Corp 1,378 2.2 11.2

12 Perrigo Inc 1,335 2.1 11.7

13 Mallinckrodt 1,333 2.1 29.3

14 Greenstone (Pfizer) 1,258 2.0 2.9

15 Roxane (BI) 1,245 1.9 24.6

16 Amneal Inc 1,223 1.9 43.8

17 Prasco Labs 1,025 1.6 50.5

18 Global Pharm Corp 944 1.5 40.7

19 Fresenius Kabi 892 1.4 -4.8

20 Glenmark Pharma 837 1.3 -2.7

Top 20 48,905 76.4 12.8

MAT Nov 2014

Sales of unbranded generics by

leading corporations

Sales of 11-20 corps in Unbranded Generics

Source: IMS Health, National Sales Perspectives, Nov 2014

TRxs mn% Market

Share% Growth

US Industry 4,277 100.0 1.9

1 Teva 538 12.6 -4.3

2 Mylan Labs, Inc. 342 8.0 -7.8

3 Novartis (incl Sandoz) 304 7.1 13.6

4 Actavis US 301 7.0 -9.2

5 Endo Pharma Inc. 237 5.5 13.6

6 Lupin Pharma 187 4.4 7.4

7 Amneal Inc 149 3.5 9.2

8 Pfizer (incl Greenstone) 133 3.1 -8.3

9 Zydus Pharma 116 2.7 15.8

10 Aurobindo Pharma 106 2.5 12.5

Top 10 2,413 56.4 0.9

MAT Nov 2014

Leading corporations

Dispensed prescriptions by leading corps

Source: IMS Health, National Prescription Audit, Nov 2014

TRxs mn% Market

Share% Growth

11 Dr Reddy Inc 99 2.3 7.2

12 Boehringer Ingelheim 92 2.1 5.8

13 Apotex Corp 92 2.1 17.0

14 Camber Pharma 80 1.9 18.9

15 Sun Pharma 64 1.5 7.2

16 Mallinckrodt 63 1.5 -24.0

17 Daiichi Sankyo 62 1.4 -18.1

18 Astrazeneca 60 1.4 -4.6

19 Internatl Labs 58 1.4 13.8

20 GlaxoSmithKline 50 1.2 -10.5

Top 20 3,134 73.3 0.9

MAT Nov 2014

Leading corporations

Dispensed prescriptions by 11-20 corps

Source: IMS Health, National Prescription Audit, Nov 2014

Dollars AC US$BN TRx AC TRx mn

Gilead Sciences 9.5 Novartis (incl Sandoz) 36.3

Johnson & Johnson 5 Endo Pharma Inc. 28.5

Biogen Idec Corp 2.4 Zydus Pharma 15.8

Sanofi Aventis 2.4 Legacy Pharma Pkg 15.3

Novo Nordisk 2.1 Apotex Corp 13.3

Teva 1.9 Accord Healthcare 13.1

Amgen Corporation 1.6 Lupin Pharma 12.9

Astrazeneca 1.4 Camber Pharma 12.8

Otsuka America Ph 1.4 Amneal Inc 12.6

Pfizer (incl Greenstone) 1.2 Aurobindo Pharma 11.8

Largest absolute growth by leading corporations, Sales & TRx (MAT)

Source: IMS Health, National Sales Perspectives, Nov 2014, National Prescription Audit, Nov 2014

Global Generic Dollars sales are approaching $200 Billon while Standard Units now are over 1 Trillion

$165,000

$170,000

$175,000

$180,000

$185,000

$190,000

$195,000

$200,000

2013 2014

Dollar Volume

Billion

940,000

950,000

960,000

970,000

980,000

990,000

1,000,000

1,010,000

1,020,000

1,030,000

2013 2014

Standard Units

12 Months ending Sept. 2014 vs. 12 Months ending Sept. 2013

10% 5%

Copyright IMS Health

Global Generic Rx market, Value, US$ at ex-mnf price

before rebates and discounts

The US and Pharmerging markets generate most of generic value sales; volume growth rate is declining

SOURCE: IMS HEALTH MIDAS Q2 2014

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

20

40

60

80

100

120

140

160

180

200

US

$ B

illi

on

s

Japan Pharmerging

ROW Top 5 Europe

US Pharma Growth

Generics Growth

Global Generic Rx market, Volume, SU

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

100

200

300

400

500

600

700

800

900

1,000

SU

Bil

lion

s

Japan Pharmerging

ROW Top 5 Europe

US Pharma Growth

Generics Growth

Copyright IMS Health

Top 10 Countries- Generic Dollar Value

Rank Country 2014 Volume

Market Share

Growth Absolute Change

Share of AC

Total Global 195,491,675,832 100% 10% 18,495,911,166 100.0%

1 US 64,908,401,739 29.3% 13% 7,535,049,346 40.7%

2 CHINA

23,906,352,664 10.9% 12% 2,510,348,439 13.6%

3 BRAZIL

10,898,527,967 4.8% 17% 1,580,639,532 8.5%

4 GERMANY 8,098,148,591 3.9% 5% 392,832,681 2.1%

5 FRANCE 7,218,739,038 3.7% -1% - 83,238,350 -0.5%

6 INDIA 6,882,357,031 3.2% 10% 653,840,471 3.5%

7 UK 6,076,419,529 2.9% 7% 403,282,641 2.2%

8 JAPAN 5,807,038,450 2.6% 14% 712,582,493 3.9%

9 CANADA 4,837,061,349 2.5% 0% 17,167,797 0.1%

10 ITALY 4,170,373,909 2.0% 7% 288,427,520 1.6%

Top 10 142,803,420,267 65.9% 11%

14,010,932,570 75.8%

12 months ending September 2014

Copyright IMS Health

Top 10 Countries- Generic Standard Units Volume

Rank Country 2014 Volume

Market Share

Growth Absolute Change

Share of AC

Total Global Total

1,017,003,480,555 100.0% 5% 45,252,127,400 100.0%

1 US

187,022,717,303 18.4% 3% 6,280,257,616 13.9%

2 INDIA

158,396,370,553 15.6% 6% 9,348,699,801 20.7%

3 CHINA

48,109,182,184 4.7% 8% 3,761,480,764 8.3%

4 JAPAN

43,734,396,861 4.3% 13% 5,086,684,951 11.2%

5 GERMANY

40,735,545,153 4.0% 3% 1,125,416,011 2.5%

6 UK

40,225,783,723 4.0% 5% 1,801,080,646 4.0%

7 BRAZIL

37,605,396,328 3.7% 11% 3,668,599,720 8.1%

8 PAKISTAN

34,205,392,455 3.4% 5% 1,569,781,422 3.5%

9 RUSSIA

30,837,136,751 3.0% 4% 1,157,718,669 2.6%

10 BANGLEDESH

27,034,037,988 2.7% 4% 921,024,493 2.0%

Top 10

647,905,959,299 63.7% 6% 34,720,744,093 76.7%

12 months ending September 2014

Copyright IMS Health

Generics are taking an increased share in all markets

REGIONAL GENERIC VOLUME MARKET SHARE (SU) 2004 VS. 2013, RX. RETAIL MARKET

LATAM : 46% 58%

USA: 52% 78%

Africa/Middle East: 46% 58%

Asia/Australasia : 34% 45%

Europe : 41% 56%

Canada: 56% 61%

Copyright IMS Health

61%

57%

31%

72%

27%

27%

58%

16%

12%

16%

11%

12%

World

Rest of the

world

Pharmerging

Developed

Brand Generic Other

Generics will represent a larger share of the market in value terms

Global spending, 2012 and 2017

2012

52%

52%

26%

67%

36%

31%

63%

21%

12%

17%

11%

12%

2017

$622Bn $650-680Bn

$224Bn $370-400Bn

$120Bn $125-155Bn

$965Bn $1,170-1,200Bn

Source: IMS Health Thought Leadership, September 2013

Copyright IMS Health

Buyers are for the first time exercising leverage on the Global market

RATIONALE FOR COMPANY MERGERS/CONSOLIDATION

Walgreen’s – Alliance Boots

- AmerisourceBergen

“...streamline the distribution of pharmaceuticals to Walgreens’ stores and

leverage global supply chain efficiencies while

improving patient access to affordable pharmaceuticals to increase the efficiency of the

healthcare system.”

Source: AmerisourceBergen Press Release March 2013

McKesson – Celesio –RITE AID

“A Celesio acquisition will allow McKesson to buy as much as $10 billion a year in generic

drugs for distribution, compared with $6 billion to $7

billion on its own”

Source:

http://www.bloomberg.com January 2014

CVS – Cardinal Health

“This partnership will enable us to maintain our leadership role

in navigating the dynamic U.S. generics market. With its combined volume and capabilities, the joint venture

will develop innovative purchasing strategies with generic manufacturers and

enhance supply chain efficiencies.”

Source: Cardinal health press

release1

84% of the US generic market consolidated to 4 buying consortia 15% of Europe added to the US consortia

SOURCE: 1http://ir.cardinalhealth.com/files/doc_news/2013/CAH%20Press%20Release%2012.10.13.pdf

Copyright IMS Health

All markets are potentially addressable – the issue is business model and profitability

• What is current addressable market?

• What changes are required to expand the addressable market?

• Who retains the “margin” – wholesaler or pharmacy?

• What will happen with generic prices and industry over time?

• How will generic manufacturers play with a consolidating supply chain?

Wh

o s

ele

cts

th

e m

an

ufa

ctu

rer?

Patient

Pre

scriber

Pharm

acy

/WH

S

Payer

How are prices set?

Tender Free pricing

Regulated

1

2 3

4

5

1. Tender markets

2. Regulated price & dispensing choice

3. Market driven pricing & dispensing choice

4. Regulated price & prescribing choice

5. Out of Pocket markets

Copyright IMS Health

Product mix is a result of payer actions and manufacturer responses in a given market

Volume dynamics (SU) of products in the Statin market

SOURCE: IMS HEALTH MIDAS YEAR 2013

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q4 2000

Q1 2001

Q2 2001

Q3 2001

Q4 2001

Q1 2002

Q2 2002

Q3 2002

Q4 2002

Q1 2003

Q2 2003

Q3 2003

Q4 2003

Q1 2004

Q2 2004

Q3 2004

Q4 2004

Q1 2005

Q2 2005

Q3 2005

Q4 2005

Q1 2006

Q2 2006

Q3 2006

Q4 2006

Q1 2007

Q2 2007

Q3 2007

Q4 2007

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Volum

e m

arket share

Volume dynamics of products in the Irish C10A1 market

LIPITOR(atorvastatin)

CRESTOR(rosuvastatin)

PRAVACHOL(pravastatin)

ZOCOR(simvastatin)

GENERIC PRAVASTATIN

GENERICATORVASTATIN

GENERICSIMVASTATIN

LESCOL (fluvastatin)

LIPOBAY(cerviastatin)

GENERICROSUVASTATIN

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q4 2000

Q1 2001

Q2 2001

Q3 2001

Q4 2001

Q1 2002

Q2 2002

Q3 2002

Q4 2002

Q1 2003

Q2 2003

Q3 2003

Q4 2003

Q1 2004

Q2 2004

Q3 2004

Q4 2004

Q1 2005

Q2 2005

Q3 2005

Q4 2005

Q1 2006

Q2 2006

Q3 2006

Q4 2006

Q1 2007

Q2 2007

Q3 2007

Q4 2007

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Volum

e m

arket share

Volume dynamics of products in the UK C10A1 market

INTRODUCTION OF CATEGORY M

LIPITOR(atorvastatin)

CRESTOR

PRAVACHOL(pravastatin)

ZOCOR(simvastatin)

GENERIC PRAVASTATIN

GENERICATORVASTATIN

GENERICSIMVASTATIN

LESCOL (fluvastatin)

LIPOBAY(cerviastatin)

Copyright IMS Health

What drives the ability to negotiate prices?

Type of formulation

• Complexity

− Oral solids the easiest

− Injectables & inhalers the most difficult

Time as generic

• Initial period hardest

• 2 – 10 years period highest opportunity

• >10 years more un-predictable

In addition to the relative size of the buyer, there is a series of factors that determine the ability to negotiate down price

Number of viable suppliers

• A high number (4+) essential for low prices

Copyright IMS Health

Target segment for international negotiations

The top 200 U.S./European generic molecules accounting for 88% of total value

9%

4%

Source: IMS MIDAS 2013

Highest Potential

Highest Potential

Europe only

target market for negotiations (63%)

U.S. only

Pre-2003

2003-11

2012-13

7%

34%

22%

7%

14% 9%

4%

1% 1%

% of sales for each category split by those products only present in the US, only present in Europe, present in both

% of sales for age band of products versus 1st US generics

Both

Copyright IMS Health

Conclusions

• Dollar growth is improving in the developed markets and softening a bit in Pharmerging markets

• As the small molecule opportunity drought hits and the specialty drug wave accelerates, payers will be desperate to get cost savings somewhere…

− Generics

− Biosimilars

− Better pricing

• Generic share will continue to grow but there will be more regulatory oversight

• Generics are the best solution

Key imperatives for Generic companies

• Quality, Quality, and Quality

• Control costs − Vertical integration

− Portfolio optimization

• Ample inventory

• New product launches − First to File

− Exclusive positions

− High barriers to entry products

• Ex US Tax treatment

• Geographical footprint

• M&A

• Brand/Specialty products

• Strategic pricing

The Big 5 to watch for

• The HEP C market

• Generic Price Inflation

• Biosimilars are closer than they have ever been in the US

• Regulation and Reimbursement Issues

• Tax Inversion

Generics are a great Solution!

• Generics saved the US $239 billion in 2013

• 14% increase over 2012

• $1.5 Trillion in savings from 2004-2013