Tgi conference call 3T13

30

TGI and Calidda Results and Key Developments 3Q 2013 Investor Conference Call November 7th 2013

-

Upload

empresa-de-energia-de-bogota -

Category

Investor Relations

-

view

78 -

download

2

Transcript of Tgi conference call 3T13

TGI and Calidda

Results and Key Developments

3Q 2013

Investor Conference Call

November 7th 2013

November 2013

Strictly Private and Confidential

TGI 3Q 2013 Results and Key Developments

3

Table of contents

1. TGI overview and history

2. Financial and operating highlights

3. Sizeable expansion projects are well underway

4. Questions and answers

Appendix

1. Economic, industry and regulatory environment

2. Shareholders and management team

3. EEB Overview

1. TGI overview and history

5

Overview

Stable and growing Colombian economy with sound investment environment

Constructive and stable regulatory framework

Largest natural gas pipeline system in Colombia

Stable and predictable cash flow generation, strongly indexed to the US Dollar

Strong and consistent financial performance

Experienced management team with solid track record in the sector

Expertise, financial strength and support of shareholders

Natural monopoly in a regulated environment

Strategically located pipeline network

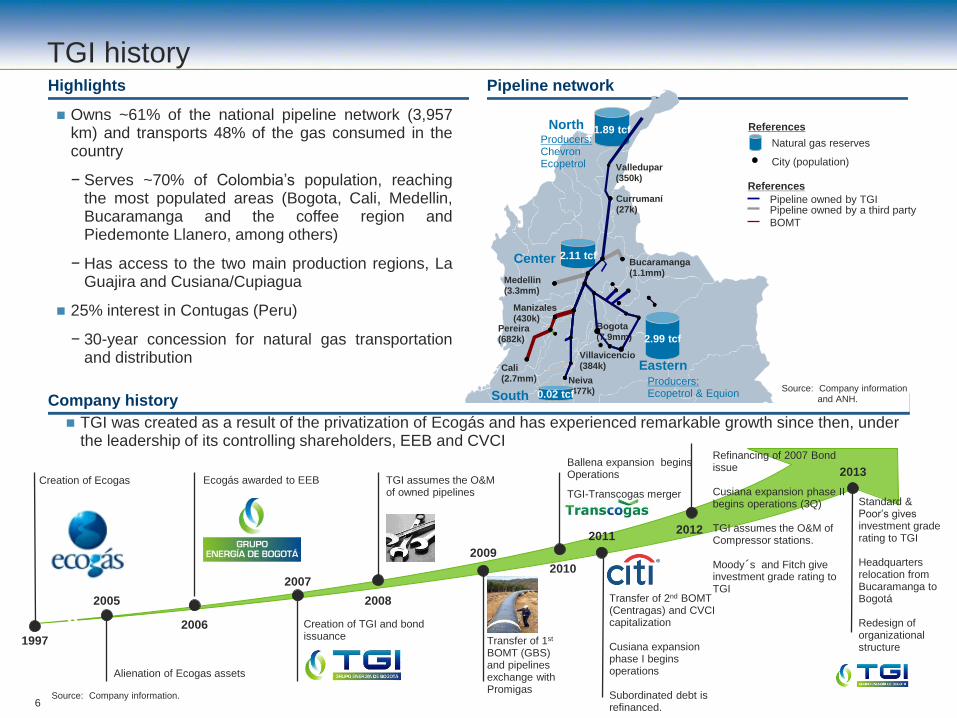

Company history

TGI history Pipeline network

Natural gas reserves

City (population)

References

Highlights

Source: Company information and ANH.

2.11 tcf Center

1.89 tcf North

2.99 tcf

Eastern

Producers: Chevron Ecopetrol

Producers: Ecopetrol & Equion South

Valledupar (350k)

Currumaní (27k)

Bucaramanga (1.1mm)

Bogota (7.9mm)

Neiva (477k)

Cali (2.7mm)

Pereira (682k)

Manizales (430k)

Medellin (3.3mm)

0.02 tcf

Pipeline owned by TGI Pipeline owned by a third party

References

BOMT

Owns ~61% of the national pipeline network (3,957 km) and transports 48% of the gas consumed in the country

− Serves ~70% of Colombia’s population, reaching the most populated areas (Bogota, Cali, Medellin, Bucaramanga and the coffee region and Piedemonte Llanero, among others)

− Has access to the two main production regions, La Guajira and Cusiana/Cupiagua

25% interest in Contugas (Peru)

− 30-year concession for natural gas transportation and distribution

TGI was created as a result of the privatization of Ecogás and has experienced remarkable growth since then, under

the leadership of its controlling shareholders, EEB and CVCI

Villavicencio (384k)

6

Creation of Ecogas

1997

2005

Alienation of Ecogas assets

2006

Ecogás awarded to EEB

2007

Creation of TGI and bond issuance Transfer of 1st

BOMT (GBS) and pipelines exchange with Promigas

Transfer of 2nd BOMT (Centragas) and CVCI capitalization

Cusiana expansion phase I begins operations

Subordinated debt is refinanced.

2009

2008

TGI assumes the O&M of owned pipelines

2012

Refinancing of 2007 Bond issue

Cusiana expansion phase II begins operations (3Q)

TGI assumes the O&M of Compressor stations.

Moody´s and Fitch give investment grade rating to TGI

2011

2010

Source: Company information.

Ballena expansion begins Operations

TGI-Transcogas merger

2013

Standard & Poor’s gives investment grade rating to TGI

Headquarters relocation from Bucaramanga to Bogotá

Redesign of organizational structure

2. Financial and operating highlights

8

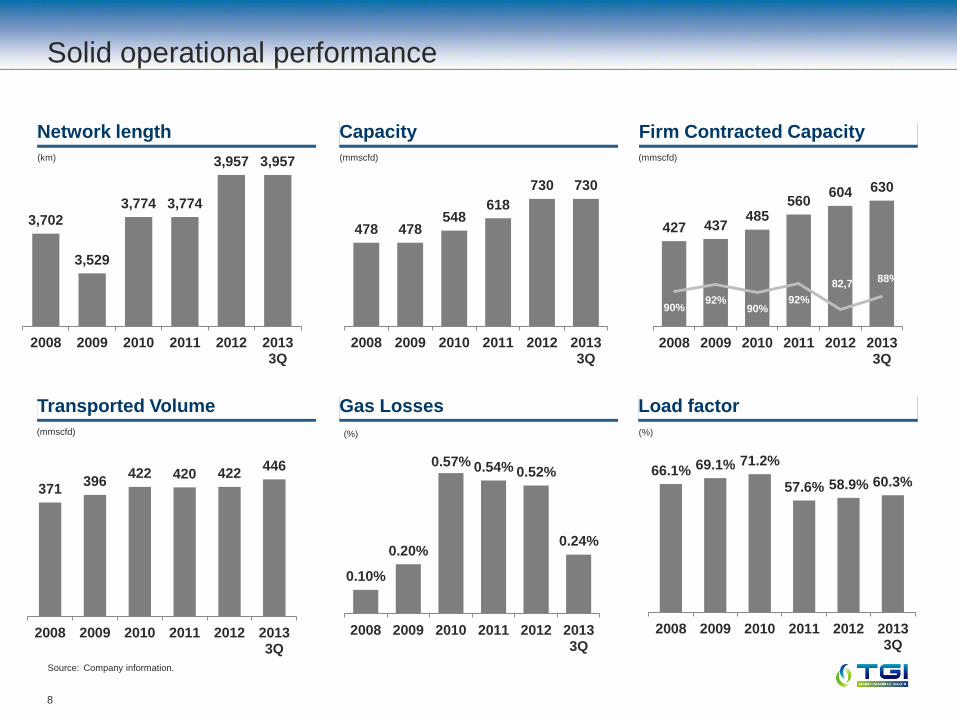

Solid operational performance

Source: Company information.

Network length

(km)

Capacity

(mmscfd)

Firm Contracted Capacity

(mmscfd)

Transported Volume Gas Losses Load factor

(mmscfd) (%) (%)

371 396

422 420 422 446

2008 2009 2010 2011 2012 20133Q

0.10%

0.20%

0.57% 0.54% 0.52%

0.24%

2008 2009 2010 2011 2012 20133Q

66.1% 69.1% 71.2%

57.6% 58.9% 60.3%

2008 2009 2010 2011 2012 20133Q

3,702

3,529

3,774 3,774

3,957 3,957

2008 2009 2010 2011 2012 20133Q

478 478 548

618

730 730

2008 2009 2010 2011 2012 20133Q

427 437 485

560 604 630

90% 92%

90% 92%

82,7% 88%

2008 2009 2010 2011 2012 20133Q

9

Source: UPME and Company information. (1) As of September 30, 2013. (2) 47,6% of market share of gas transported directly by TGI. Most of the 15% transported by “Others” is natural gas transported by TGI through the

TGI Pipeline System to other pipeline systems.

TGI is the largest natural gas transportation company in the country

− Holds 47.6%(2) market share in the Colombian natural gas transportation sector and owns ~61% of the pipeline network

TGI’s extensive pipeline network (3,957 km) allows the Company to take advantage of new business opportunities and participate in expansion projects in different regions

Other industry participants face high barriers of entry to access TGI’s gas transportation market in a cost-efficient manner

Natural gas transportation market share (1)

Natural gas transported volume (1)

(mmscfd)

(% of natural gas transported volume)

Largest natural gas pipeline system in Colombia

TGI has a dominant market position, holding a natural monopoly with high barriers of entry

Source: Natural gas transportation companies’ Electronic Bulletin of Operations

Source: Natural gas transportation companies’ Electronic Bulletin of Operations

TGI 47%

Promigas 38%

Others 15%

446.5

348.5

46.1 44.2 29.7 11.5 6.0

10

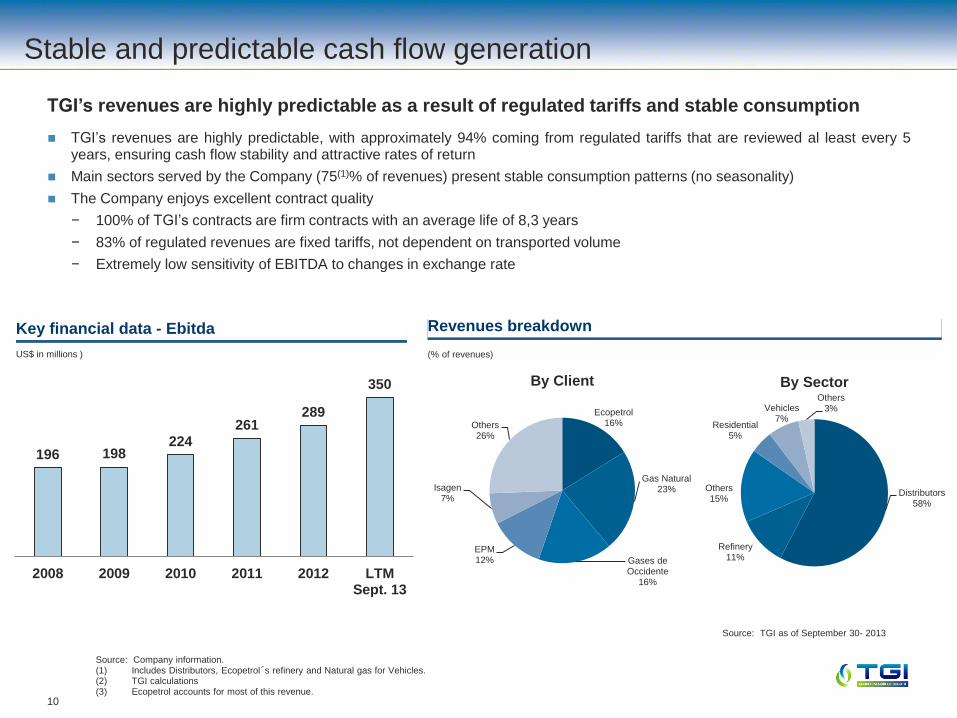

Stable and predictable cash flow generation

TGI’s revenues are highly predictable, with approximately 94% coming from regulated tariffs that are reviewed al least every 5 years, ensuring cash flow stability and attractive rates of return

Main sectors served by the Company (75(1)% of revenues) present stable consumption patterns (no seasonality)

The Company enjoys excellent contract quality

− 100% of TGI’s contracts are firm contracts with an average life of 8,3 years

− 83% of regulated revenues are fixed tariffs, not dependent on transported volume

− Extremely low sensitivity of EBITDA to changes in exchange rate

Revenues breakdown

(% of revenues)

Source: Company information. (1) Includes Distributors, Ecopetrol´s refinery and Natural gas for Vehicles. (2) TGI calculations (3) Ecopetrol accounts for most of this revenue.

TGI’s revenues are highly predictable as a result of regulated tariffs and stable consumption

Source: TGI as of September 30- 2013

Key financial data - Ebitda

US$ in millions )

196 198 224

261 289

350

2008 2009 2010 2011 2012 LTMSept. 13

Ecopetrol 16%

Gas Natural 23%

Gases de Occidente

16%

EPM 12%

Isagen 7%

Others 26%

By Client

Distributors 58%

Refinery 11%

Others 15%

Residential 5%

Vehicles 7%

Others 3%

By Sector

11

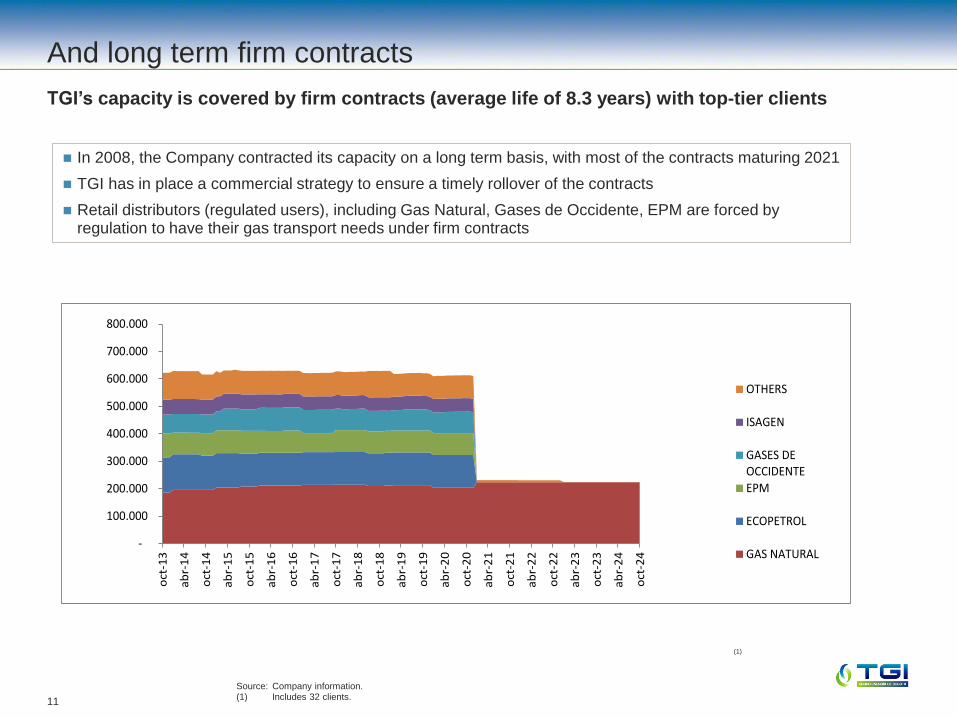

And long term firm contracts

Source: Company information. (1) Includes 32 clients.

TGI’s capacity is covered by firm contracts (average life of 8.3 years) with top-tier clients

(1)

In 2008, the Company contracted its capacity on a long term basis, with most of the contracts maturing 2021

TGI has in place a commercial strategy to ensure a timely rollover of the contracts

Retail distributors (regulated users), including Gas Natural, Gases de Occidente, EPM are forced by regulation to have their gas transport needs under firm contracts

-

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

oct

-13

ab

r-1

4

oct

-14

ab

r-1

5

oct

-15

ab

r-1

6

oct

-16

ab

r-1

7

oct

-17

ab

r-1

8

oct

-18

ab

r-1

9

oct

-19

ab

r-2

0

oct

-20

ab

r-2

1

oct

-21

ab

r-2

2

oct

-22

ab

r-2

3

oct

-23

ab

r-2

4

oct

-24

OTHERS

ISAGEN

GASES DEOCCIDENTE

EPM

ECOPETROL

GAS NATURAL

12

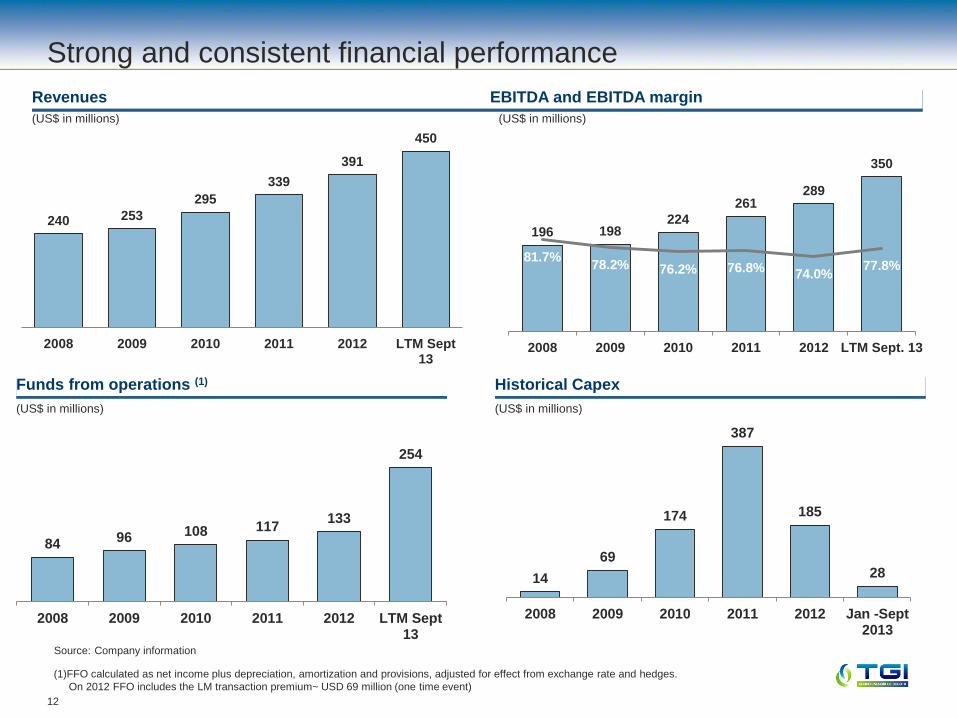

Strong and consistent financial performance

Revenues EBITDA and EBITDA margin

Funds from operations (1)

(US$ in millions)

Source: Company information

Historical Capex

(US$ in millions)

(US$ in millions) (US$ in millions)

(1)FFO calculated as net income plus depreciation, amortization and provisions, adjusted for effect from exchange rate and hedges.

On 2012 FFO includes the LM transaction premium~ USD 69 million (one time event)

196 198 224

261 289

350

81.7% 78.2% 76.2% 76.8%

74.0% 77.8%

2008 2009 2010 2011 2012 LTM Sept. 13

14

69

174

387

185

28

2008 2009 2010 2011 2012 Jan -Sept2013

84 96 108 117 133

254

2008 2009 2010 2011 2012 LTM Sept13

240 253

295

339

391

450

2008 2009 2010 2011 2012 LTM Sept13

13

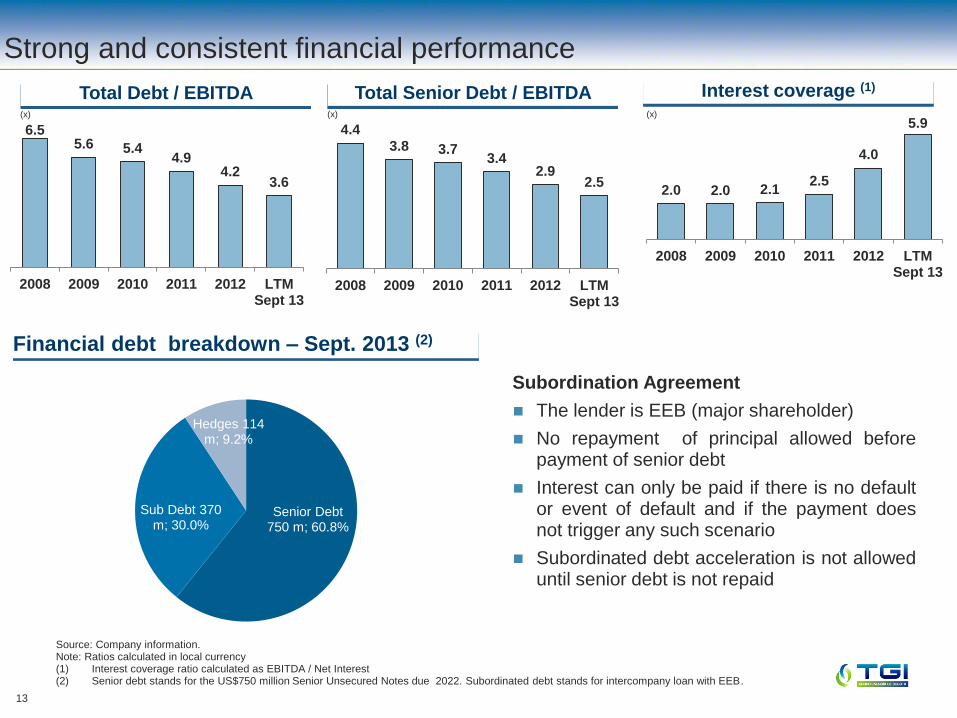

Financial debt breakdown – Sept. 2013 (2)

Subordination Agreement

The lender is EEB (major shareholder)

No repayment of principal allowed before payment of senior debt

Interest can only be paid if there is no default or event of default and if the payment does not trigger any such scenario

Subordinated debt acceleration is not allowed until senior debt is not repaid

Source: Company information. Note: Ratios calculated in local currency (1) Interest coverage ratio calculated as EBITDA / Net Interest (2) Senior debt stands for the US$750 million Senior Unsecured Notes due 2022. Subordinated debt stands for intercompany loan with EEB.

Strong and consistent financial performance

Total Debt / EBITDA (x)

Total Senior Debt / EBITDA (x)

Interest coverage (1)

(x)

6.5 5.6 5.4

4.9 4.2

3.6

2008 2009 2010 2011 2012 LTMSept 13

4.4 3.8 3.7

3.4 2.9

2.5

2008 2009 2010 2011 2012 LTMSept 13

2.0 2.0 2.1 2.5

4.0

5.9

2008 2009 2010 2011 2012 LTMSept 13

Senior Debt 750 m; 60.8%

Sub Debt 370 m; 30.0%

Hedges 114 m; 9.2%

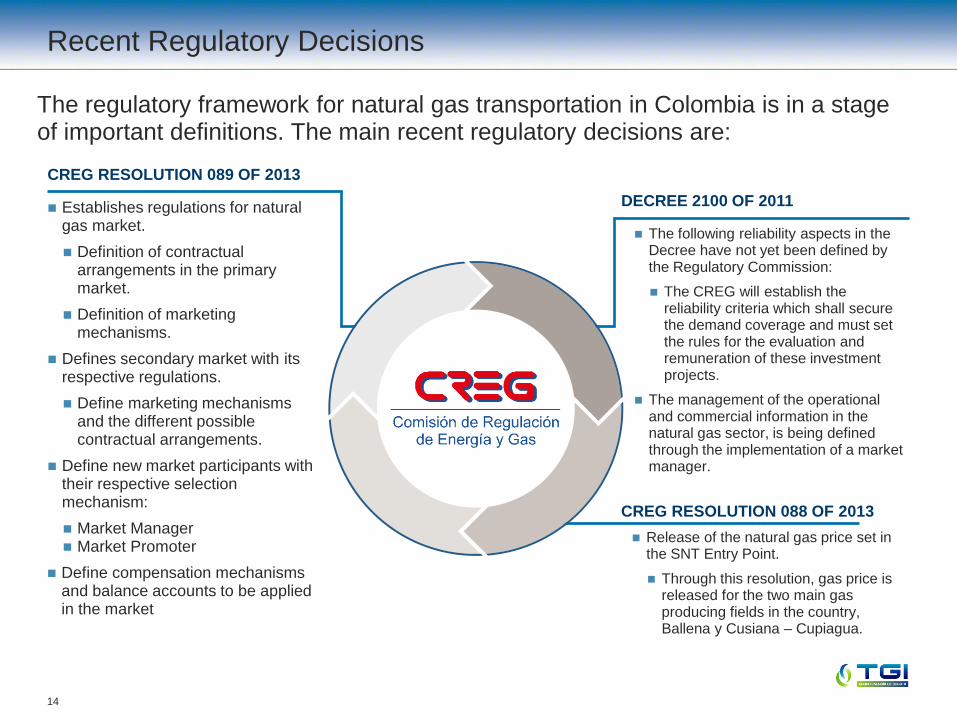

Release of the natural gas price set in the SNT Entry Point.

Through this resolution, gas price is released for the two main gas producing fields in the country, Ballena y Cusiana – Cupiagua.

CREG RESOLUTION 088 OF 2013

Establishes regulations for natural gas market.

Definition of contractual arrangements in the primary market.

Definition of marketing mechanisms.

Defines secondary market with its respective regulations.

Define marketing mechanisms and the different possible contractual arrangements.

Define new market participants with their respective selection mechanism:

Market Manager Market Promoter

Define compensation mechanisms and balance accounts to be applied in the market

The following reliability aspects in the Decree have not yet been defined by the Regulatory Commission:

The CREG will establish the reliability criteria which shall secure the demand coverage and must set the rules for the evaluation and remuneration of these investment projects.

The management of the operational and commercial information in the natural gas sector, is being defined through the implementation of a market manager.

DECREE 2100 OF 2011

Recent Regulatory Decisions

The regulatory framework for natural gas transportation in Colombia is in a stage of important definitions. The main recent regulatory decisions are:

CREG RESOLUTION 089 OF 2013

14

15

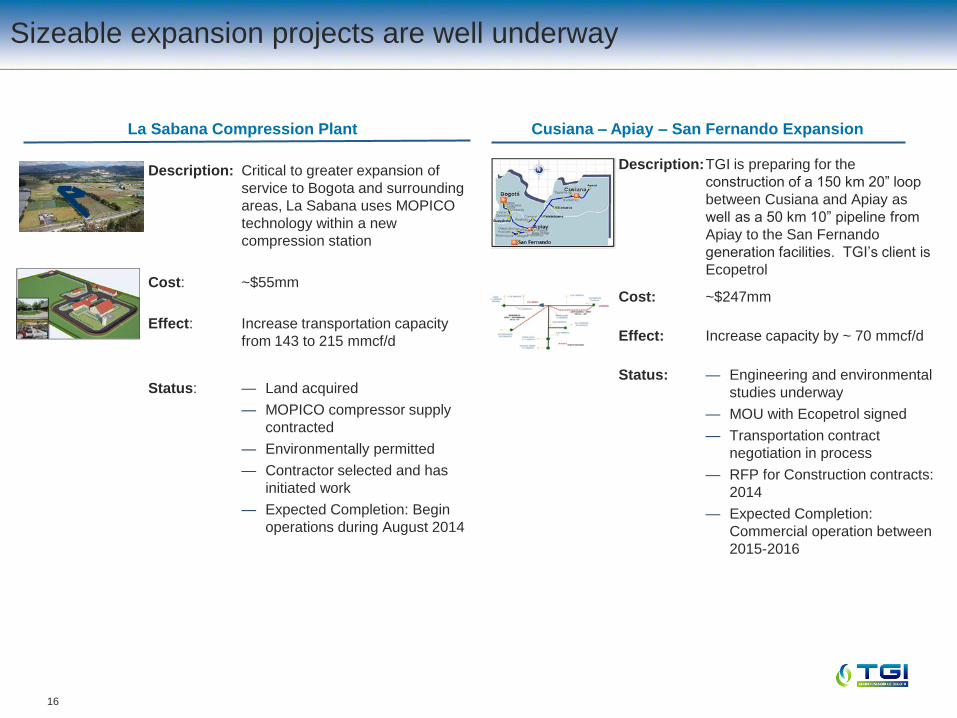

3. Sizeable expansion projects are well underway

16

Cusiana – Apiay – San Fernando Expansion La Sabana Compression Plant

Description: Critical to greater expansion of

service to Bogota and surrounding

areas, La Sabana uses MOPICO

technology within a new

compression station

Cost: ~$55mm

Effect: Increase transportation capacity

from 143 to 215 mmcf/d

Status: — Land acquired

— MOPICO compressor supply

contracted

— Environmentally permitted

— Contractor selected and has

initiated work

— Expected Completion: Begin

operations during August 2014

Description: TGI is preparing for the

construction of a 150 km 20” loop

between Cusiana and Apiay as

well as a 50 km 10” pipeline from

Apiay to the San Fernando

generation facilities. TGI’s client is

Ecopetrol

Cost: ~$247mm

Effect: Increase capacity by ~ 70 mmcf/d

Status: — Engineering and environmental

studies underway

— MOU with Ecopetrol signed

— Transportation contract

negotiation in process

— RFP for Construction contracts:

2014

— Expected Completion:

Commercial operation between

2015-2016

Sizeable expansion projects are well underway

17

Eje Cafetero Branches

Description: TGI will increase existing capacity

of Armenia and Chinchina

branches with the construction of

two new loops; Armenia Branch:

37.5 km 8” loop parallel to exiting

6” pipeline and Chinchina – Santa

Rosa – Dosquebradas Branch:

7.5km 3” loop parallel to existing

3” pipeline

Cost: ~$28mm

Effect: Additional revenues from pipeline

from Cusiana to this region.

Status: — Planning stage

— Expected Completion: 2015

Sizeable expansion projects are well underway

La Belleza – Vasconia Expansion

Description: Adapt compression stations in

Vasconia to increase maximum

transport capacity in La Belleza –

Vasconia segment by 230 mmcf/d

Cost: ~$14mm

Expected

Completion: 2014-2015

Adjustments for Venezuela Imports

Description: Adapt infrastructure at Ballena field

to connect the Ballena-

Barrancabermeja pipeline with

PDVSA’s cross-border natural gas

pipeline, enabling the transportation

of natural gas to come from

Venezuela to the central region of

Colombia

Cost: ~$5mm

Effect: Increase system reliability by

making Venezuela’s massive natural

gas reserves available to the largest

consumption centers in Colombia

Expected

Completion: 2014

Bucaramanga

Bogotá

Neiva

Cali

Medellin

2.99 tcf

0.02 tcf

2.11 tcf

EasternProducers:

EcopetrolEquion

Upper Magdalena Valley

1.89 tcf

Ballena

Cusiana

Barrancabermeja Refinery

Llanos Orientales

Sinu

Tumaco

Choco

Cordillera Oriental

Catatumbo

Guajira

Maracaibo

VenezuelaColombia

Cupiagua

Main Oil & Gas Basin

TGI Pipelines

Promigas Pipelines

PDVSA Pipelines

La Belleza – Vasconia Expansion

Description: Adapt compression stations,

delivery and receipt locations

along the Ballena -

Barrancabermeja pipeline so

that it can transport natural gas

in both directions, in order to

allow natural gas to be

transported from the central

region to the north

Cost: ~$20mm

Expected

Completion: 2016

Ballena

Barrancabermeja

18

4. Questions and answers

19

Investor Relations

For more information about TGI contact our Investor Relations team:

http://www.tgi.com.co

http://www.grupoenergiadebogota.com.co

Santiago Pardo de la Concha

CFO

+57 (1) 3138400 - ext 2320

Fabian Sánchez Aldana

Investor Relations Advisor GEB

+57 (1) 3268000 – ext 1897

Antonio Angarita

Investor Relations Officer GEB

+57 (1) 3268000 - ext 1546

Sergio Andrés Hernández Acosta

Finance Director

+57 (1) 3138400 - ext 2450

20

Appendix 1 – Economic and Industry Environment

21

Source: IMF, World Bank, Colombian Central Bank, National Administrative Department of Statistics and Bloomberg 1 2013E corresponds to the the average of the period January 2013 - September 2013.

Foreign Currency Reserves Increasing Foreign Direct Investments

High Real GDP Growth, Resilient to Global Setbacks Low Inflation & Country Risk Coupled with Strong Currency

1.7%

2.5%

3.9%

5.3%

4.7%

6.7% 6.9%

3.5%

1.7%

4.0%

6.6%

4.0% 4.1% 4.5%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Re

al

GD

P G

row

th (

% c

hg

yo

y)

GDP per

Capita

(US$ ‘000)

2.4 2.4 2.3 2.8 3.4 3.7 4.7 5.5 5.2 6.3 7.3 7.9

7.7%

3.0%

602

153

$2,291

$1,900

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

0%

2%

4%

6%

8%

10%

12%

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

E

20

14

E

Inflation (EOP) EMBI+¹ (Avg) FX Rate (EOP)

21

$2 $3

$10

$7

$9

$11

$7 $7

$13

$16

1.8% 2.6%

7.0%

4.1% 4.4% 4.3% 3.0% 2.4%

4.0% 4.2%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Foreign Direct Investments (US$bn) FDI / GDP (%)

8.2 8.4

Colombia did not

enter into recession

during the last

global financial

crisis

Stable and growing Colombian economy with sound investment environment

9 10 11 11 14 15 15

21 24 25

28 32

37 41

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

5

10

15

20

25

30

35

40

45

20002001200220032004200520062007200820092010201120122013(e)

International reserves Debt as % of GDP

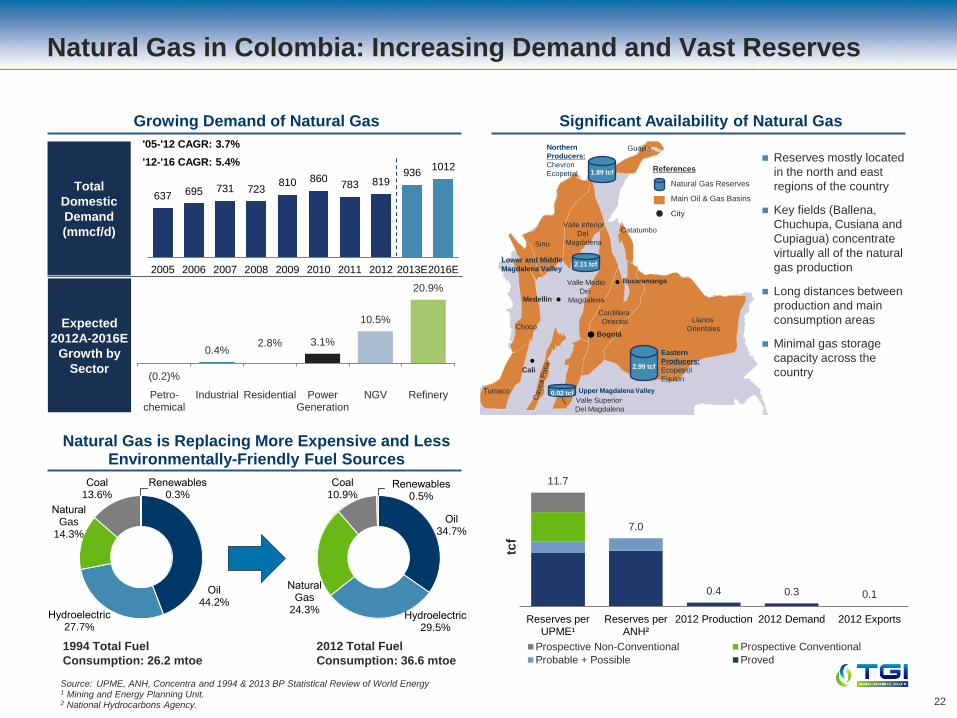

Source: UPME, ANH, Concentra and 1994 & 2013 BP Statistical Review of World Energy 1 Mining and Energy Planning Unit. 2 National Hydrocarbons Agency.

Natural Gas is Replacing More Expensive and Less Environmentally-Friendly Fuel Sources

Growing Demand of Natural Gas Significant Availability of Natural Gas

Reserves mostly located

in the north and east

regions of the country

Key fields (Ballena,

Chuchupa, Cusiana and

Cupiagua) concentrate

virtually all of the natural

gas production

Long distances between

production and main

consumption areas

Minimal gas storage

capacity across the

country

Total

Domestic

Demand

(mmcf/d)

Expected

2012A-2016E

Growth by

Sector

1994 Total Fuel

Consumption: 26.2 mtoe

2012 Total Fuel

Consumption: 36.6 mtoe

22

Natural Gas in Colombia: Increasing Demand and Vast Reserves

(0.2)%

0.4% 2.8% 3.1%

10.5%

20.9%

Petro-chemical

Industrial Residential PowerGeneration

NGV Refinery

Bucaramanga

Bogotá

Cali

Medellín

2.99 tcf

0.02 tcf

2.11 tcf

Eastern

Producers:

Ecopetrol

Equion

Upper Magdalena Valley

Lower and Middle

Magdalena Valley

Northern

Producers:

Chevron

Ecopetrol References

Natural Gas Reserves

Main Oil & Gas Basins

City

1.89 tcf

Llanos

Orientales

Catatumbo

Guajira

Sinu

Tumaco

Choco

Valle Superior

Del Magdalena

Cordillera

Oriental

Valle Inferior

Del

Magdalena

Valle Medio

Del

Magdalena

11.7

7.0

0.4 0.3 0.1

Reserves perUPME¹

Reserves perANH²

2012 Production 2012 Demand 2012 Exports

tcf

Prospective Non-Conventional Prospective Conventional

Probable + Possible Proved

Oil34.7%

Hydroelectric29.5%

Natural Gas

24.3%

Coal10.9%

Renewables0.5%

Oil44.2%

Hydroelectric27.7%

Natural Gas

14.3%

Coal13.6%

Renewables0.3%

637 695 731 723810 860

783 819936

1012

2005 2006 2007 2008 2009 2010 2011 2012 2013E2016E

'05-'12 CAGR: 3.7%

'12-'16 CAGR: 5.4%

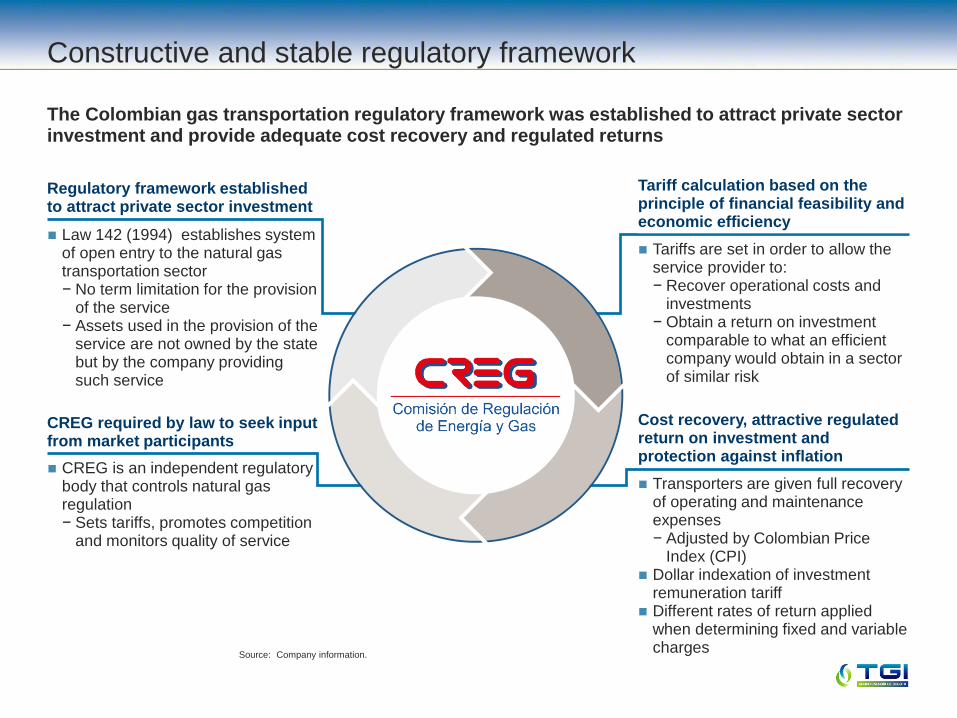

Regulatory framework established to attract private sector investment

Law 142 (1994) establishes system of open entry to the natural gas transportation sector − No term limitation for the provision

of the service − Assets used in the provision of the

service are not owned by the state but by the company providing such service

CREG required by law to seek input from market participants

CREG is an independent regulatory body that controls natural gas regulation − Sets tariffs, promotes competition

and monitors quality of service

Tariff calculation based on the principle of financial feasibility and economic efficiency

Tariffs are set in order to allow the service provider to: − Recover operational costs and

investments − Obtain a return on investment

comparable to what an efficient company would obtain in a sector of similar risk

Cost recovery, attractive regulated return on investment and protection against inflation

Transporters are given full recovery of operating and maintenance expenses − Adjusted by Colombian Price

Index (CPI) Dollar indexation of investment

remuneration tariff Different rates of return applied

when determining fixed and variable charges

Constructive and stable regulatory framework

Source: Company information.

The Colombian gas transportation regulatory framework was established to attract private sector investment and provide adequate cost recovery and regulated returns

Appendix 2 – Shareholders and management team

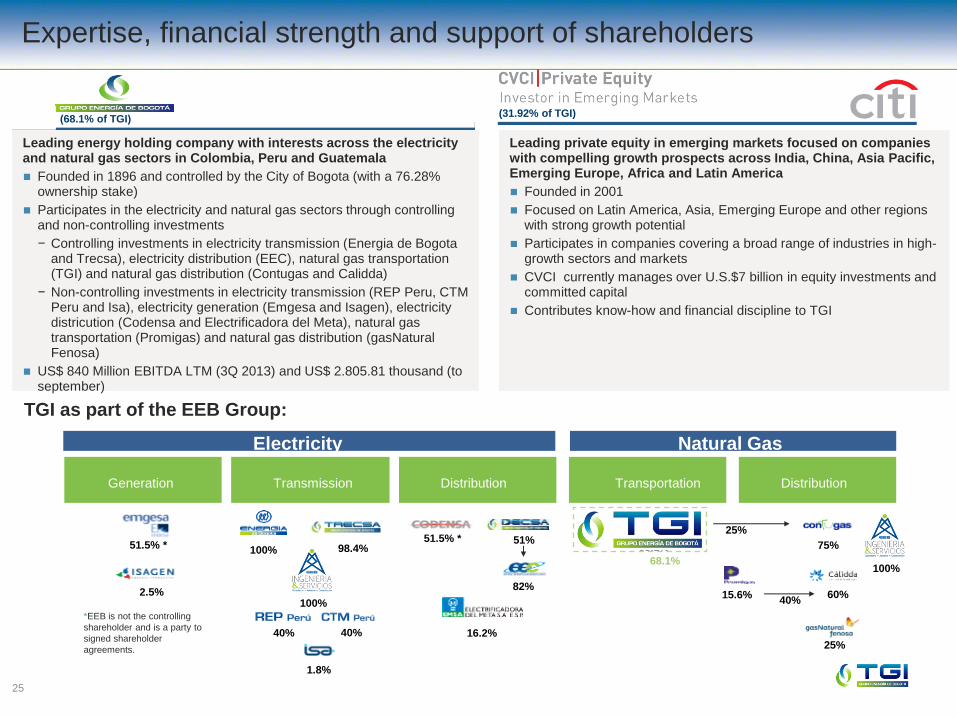

(68.1% of TGI)

Leading energy holding company with interests across the electricity and natural gas sectors in Colombia, Peru and Guatemala

Founded in 1896 and controlled by the City of Bogota (with a 76.28% ownership stake)

Participates in the electricity and natural gas sectors through controlling and non-controlling investments

− Controlling investments in electricity transmission (Energia de Bogota and Trecsa), electricity distribution (EEC), natural gas transportation (TGI) and natural gas distribution (Contugas and Calidda)

− Non-controlling investments in electricity transmission (REP Peru, CTM Peru and Isa), electricity generation (Emgesa and Isagen), electricity districution (Codensa and Electrificadora del Meta), natural gas transportation (Promigas) and natural gas distribution (gasNatural Fenosa)

US$ 840 Million EBITDA LTM (3Q 2013) and US$ 2.805.81 thousand (to september)

Leading private equity in emerging markets focused on companies with compelling growth prospects across India, China, Asia Pacific, Emerging Europe, Africa and Latin America

Founded in 2001

Focused on Latin America, Asia, Emerging Europe and other regions with strong growth potential

Participates in companies covering a broad range of industries in high-growth sectors and markets

CVCI currently manages over U.S.$7 billion in equity investments and committed capital

Contributes know-how and financial discipline to TGI

(31.92% of TGI)

Expertise, financial strength and support of shareholders

25

68.1%

25%

15.6%

Electricity

Transmission

40% 40%

1.8%

98.4%

Generation

51.5% *

2.5%

Distribution

51.5% *

16.2%

51%

82%

Distribution Transportation

Natural Gas

75%

60%

100%

*EEB is not the controlling

shareholder and is a party to

signed shareholder

agreements.

40%

25%

68.1%

TGI as part of the EEB Group:

100%

100%

26

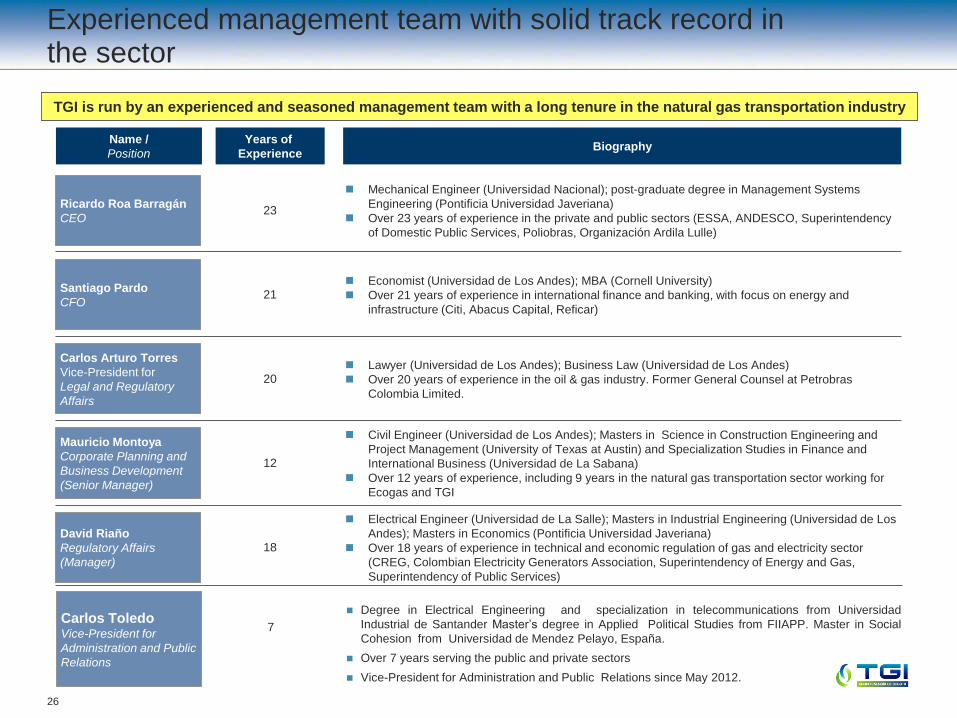

TGI is run by an experienced and seasoned management team with a long tenure in the natural gas transportation industry

Name /

Position

Years of

Experience

23 Ricardo Roa Barragán

CEO

Mechanical Engineer (Universidad Nacional); post-graduate degree in Management Systems

Engineering (Pontificia Universidad Javeriana)

Over 23 years of experience in the private and public sectors (ESSA, ANDESCO, Superintendency

of Domestic Public Services, Poliobras, Organización Ardila Lulle)

Biography

Santiago Pardo

CFO

Economist (Universidad de Los Andes); MBA (Cornell University)

Over 21 years of experience in international finance and banking, with focus on energy and

infrastructure (Citi, Abacus Capital, Reficar)

Carlos Arturo Torres

Vice-President for

Legal and Regulatory

Affairs

Lawyer (Universidad de Los Andes); Business Law (Universidad de Los Andes)

Over 20 years of experience in the oil & gas industry. Former General Counsel at Petrobras

Colombia Limited.

Mauricio Montoya

Corporate Planning and

Business Development

(Senior Manager)

Civil Engineer (Universidad de Los Andes); Masters in Science in Construction Engineering and

Project Management (University of Texas at Austin) and Specialization Studies in Finance and

International Business (Universidad de La Sabana)

Over 12 years of experience, including 9 years in the natural gas transportation sector working for

Ecogas and TGI

David Riaño

Regulatory Affairs

(Manager)

Electrical Engineer (Universidad de La Salle); Masters in Industrial Engineering (Universidad de Los

Andes); Masters in Economics (Pontificia Universidad Javeriana)

Over 18 years of experience in technical and economic regulation of gas and electricity sector

(CREG, Colombian Electricity Generators Association, Superintendency of Energy and Gas,

Superintendency of Public Services)

21

20

12

18

Experienced management team with solid track record in the sector

Carlos Toledo Vice-President for

Administration and Public

Relations

Degree in Electrical Engineering and specialization in telecommunications from Universidad

Industrial de Santander Master’s degree in Applied Political Studies from FIIAPP. Master in Social

Cohesion from Universidad de Mendez Pelayo, España.

Over 7 years serving the public and private sectors

Vice-President for Administration and Public Relations since May 2012.

7

27

Appendix 3 – EEB Overview

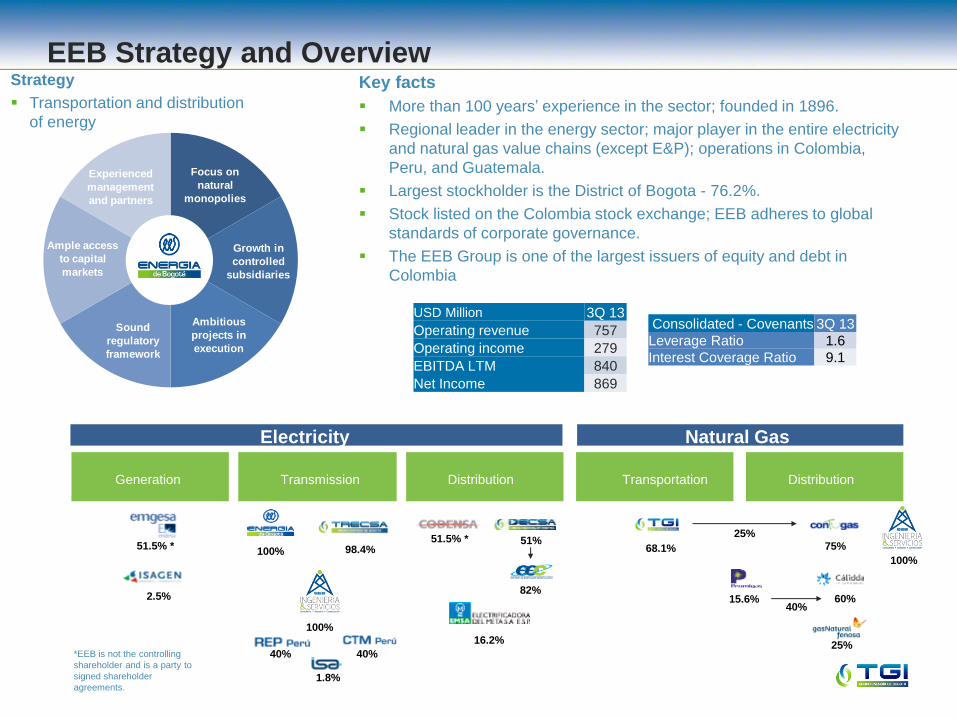

EEB Strategy and Overview Strategy

Transportation and distribution

of energy

Key facts

More than 100 years’ experience in the sector; founded in 1896.

Regional leader in the energy sector; major player in the entire electricity

and natural gas value chains (except E&P); operations in Colombia,

Peru, and Guatemala.

Largest stockholder is the District of Bogota - 76.2%.

Stock listed on the Colombia stock exchange; EEB adheres to global

standards of corporate governance.

The EEB Group is one of the largest issuers of equity and debt in

Colombia

USD Million 3Q 13

Operating revenue 757

Operating income 279

EBITDA LTM 840

Net Income 869

Consolidated - Covenants 3Q 13

Leverage Ratio 1.6

Interest Coverage Ratio 9.1

68.1%

25%

15.6%

Electricity

Transmission

40% 40%

1.8%

98.4%

Generation

51.5% *

2.5%

Distribution

51.5% *

16.2%

51%

82%

Distribution Transportation

Natural Gas

75%

60%

100%

*EEB is not the controlling

shareholder and is a party to

signed shareholder

agreements.

40%

25%

100%

100%

Focus on

natural

monopolies

Ample access

to capital

markets

Ambitious

projects in

execution

Growth in

controlled

subsidiaries

Sound

regulatory

framework

Experienced

management

and partners

Disclaimer

This presentation contains statements that are forward-looking within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements are only predictions and are not guarantees of future performance. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements include, among other things, statements concerning the potential exposure of TGI, its consolidated subsidiaries and related companies to market risks and statements expressing management’ expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as “anticipate”, “believe”, “could”, “estimate”, “expect”, “intend”, “may”, “plan”, “objectives”, ”outlook”, “probably”, “project”, “will”, “seek”, “target”, “risks”, “goals”, “should” and similar terms and phrases. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Although TGI believes that the expectations and assumptions reflected in such forward-looking statements are reasonable based on information currently available to TGI’s management, such expectations and assumptions are necessarily speculative and subject to substantial uncertainty, and as a result, TGI cannot guarantee future results or events. TGI does not undertake any obligation to update any forward-looking statement or other information to reflect events or circumstances occurring after the date of this presentation or to reflect the occurrence of unanticipated events.