Michaelmas Term - Experimental Physiology Background and Debrief Sheets

1

1

Term Sheets for Advanced and Financing Rounds Pascal Honold

Bern, 24 October 2012

Bern, 24 October 2012 2

Introduction

The Speaker Handout – Term Sheet Template Raise your voice!

2

Bern, 24 October 2012 3

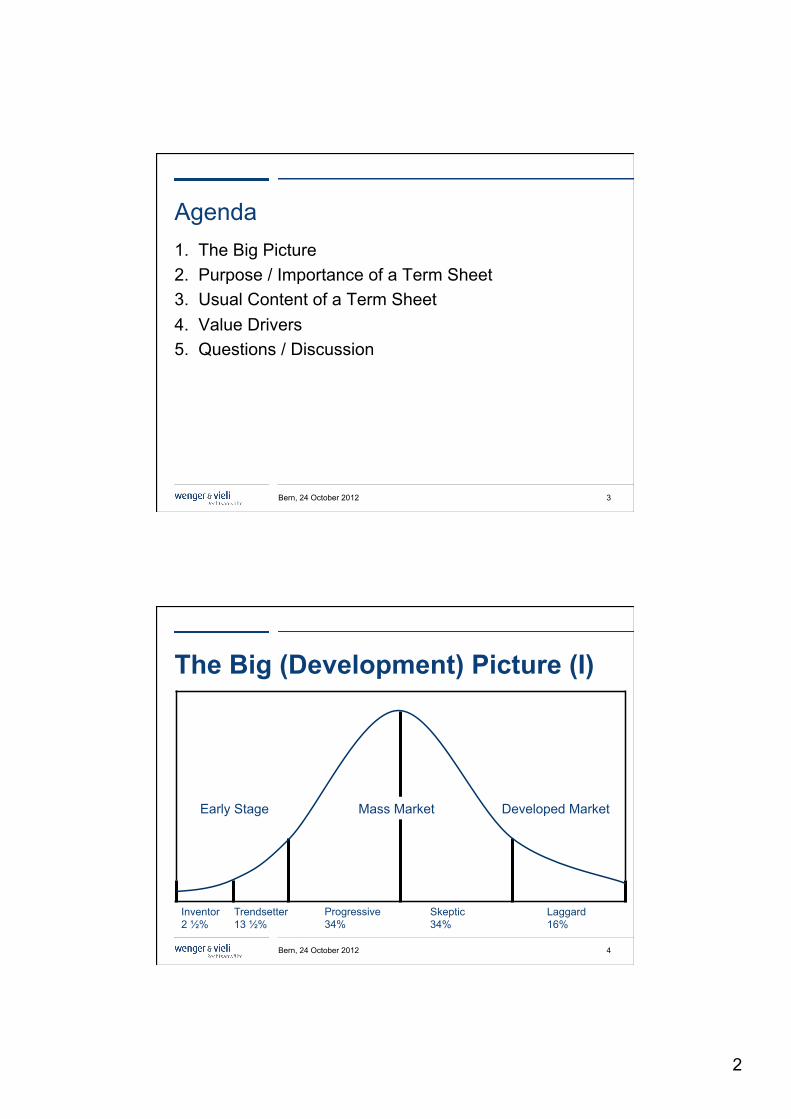

Agenda 1. The Big Picture 2. Purpose / Importance of a Term Sheet 3. Usual Content of a Term Sheet 4. Value Drivers 5. Questions / Discussion

4

The Big (Development) Picture (I)

Inventor 2 ½%

Trendsetter 13 ½%

Skeptic 34%

Laggard 16%

Early Stage Developed Market

Bern, 24 October 2012

Mass Market

Progressive 34%

3

5

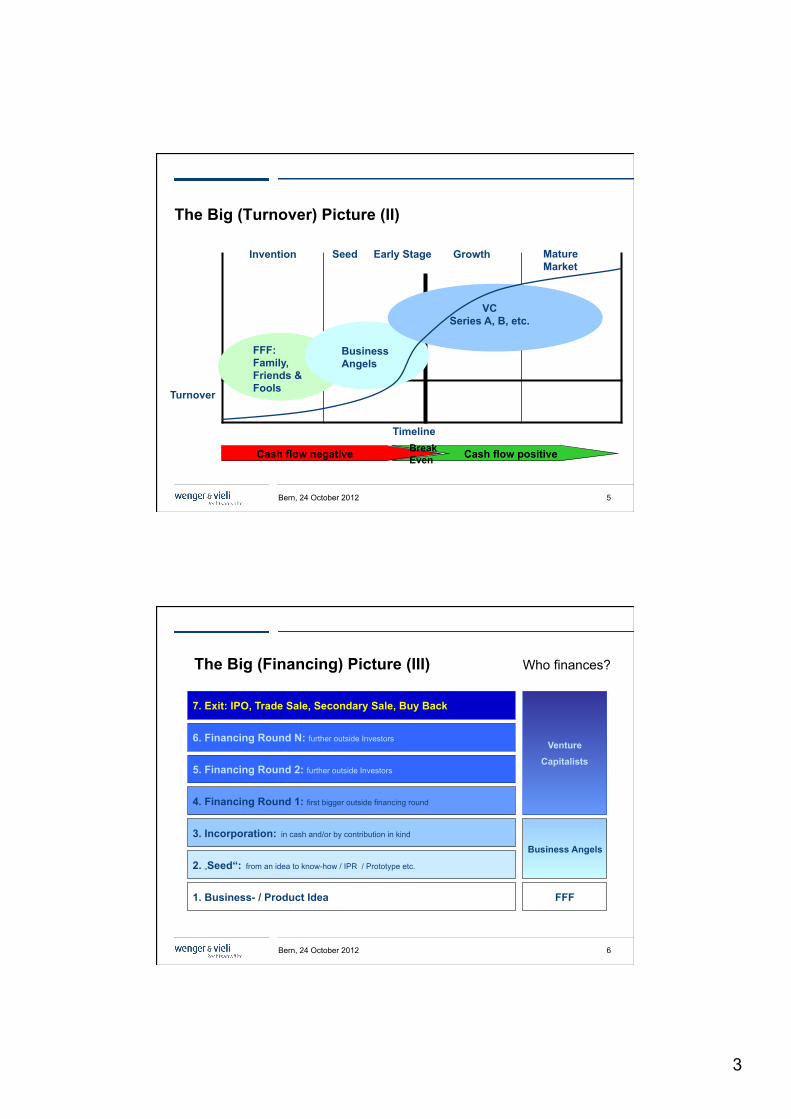

The Big (Turnover) Picture (II)

Turnover

Bern, 24 October 2012

Timeline

Business Angels

FFF: Family, Friends & Fools

VC Series A, B, etc.

Invention Seed Early Stage Growth Mature Market

Cash flow negative Cash flow positive Break Even

Bern, 24 October 2012 6

The Big (Financing) Picture (III) Who finances?

1. Business- / Product Idea

2. „Seed“: from an idea to know-how / IPR / Prototype etc.

3. Incorporation: in cash and/or by contribution in kind

4. Financing Round 1: first bigger outside financing round

5. Financing Round 2: further outside Investors

7. Exit: IPO, Trade Sale, Secondary Sale, Buy Back

6. Financing Round N: further outside Investors

FFF

Business Angels

Venture

Capitalists

4

7

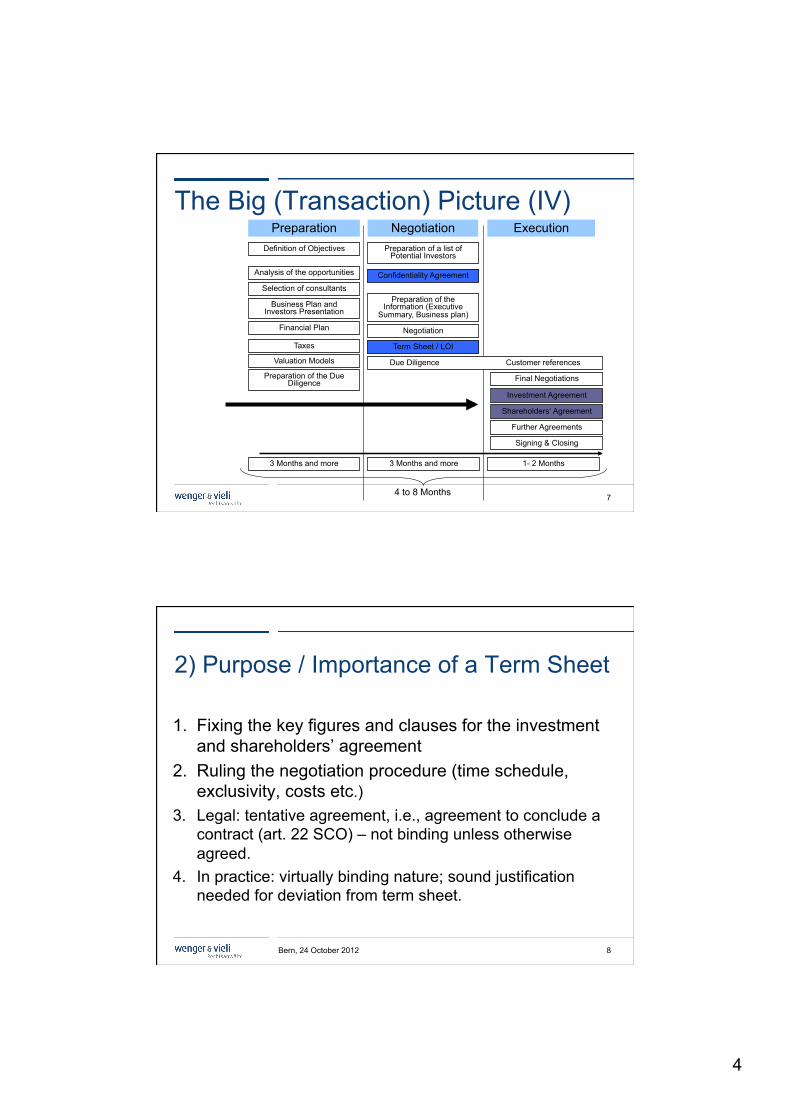

The Big (Transaction) Picture (IV)

Business Plan and Investors Presentation

Preparation of the Due Diligence

Analysis of the opportunities

Definition of Objectives

Selection of consultants

Financial Plan

Valuation Models

Taxes

Preparation of a list of Potential Investors

Preparation of the Information (Executive

Summary, Business plan)

Confidentiality Agreement

Term Sheet / LOI

Due Diligence Customer references

Investment Agreement

Shareholders‘ Agreement

Signing & Closing

Final Negotiations

Negotiation

Further Agreements

3 Months and more 3 Months and more 1- 2 Months

Preparation Negotiation Execution

4 to 8 Months

Bern, 24 October 2012 8

2) Purpose / Importance of a Term Sheet

1. Fixing the key figures and clauses for the investment and shareholders’ agreement

2. Ruling the negotiation procedure (time schedule, exclusivity, costs etc.)

3. Legal: tentative agreement, i.e., agreement to conclude a contract (art. 22 SCO) – not binding unless otherwise agreed.

4. In practice: virtually binding nature; sound justification needed for deviation from term sheet.

5

Bern, 24 October 2012 9

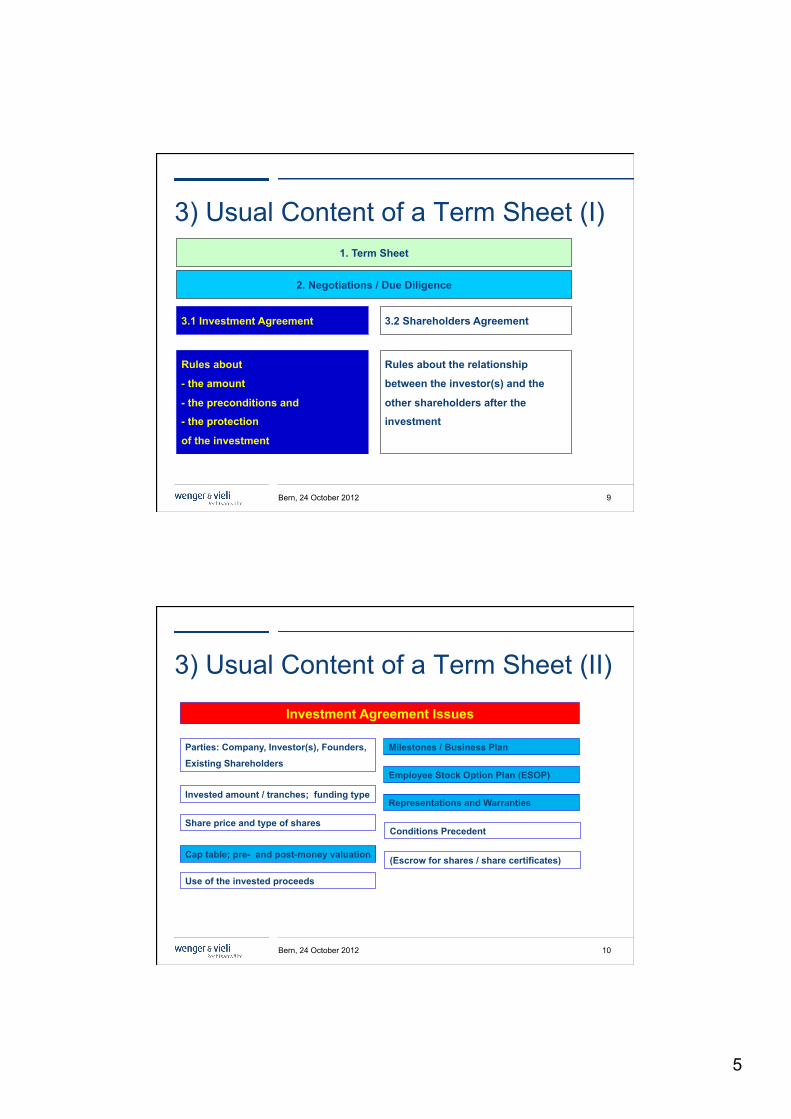

3) Usual Content of a Term Sheet (I)

3.1 Investment Agreement 3.2 Shareholders Agreement

Rules about

- the amount

- the preconditions and

- the protection

of the investment

Rules about the relationship

between the investor(s) and the

other shareholders after the

investment

1. Term Sheet

2. Negotiations / Due Diligence

Bern, 24 October 2012 10

3) Usual Content of a Term Sheet (II)

Parties: Company, Investor(s), Founders,

Existing Shareholders

Invested amount / tranches; funding type

Use of the invested proceeds

Employee Stock Option Plan (ESOP)

Share price and type of shares

Cap table; pre- and post-money valuation

Milestones / Business Plan

Representations and Warranties

Conditions Precedent

Investment Agreement Issues

(Escrow for shares / share certificates)

6

Bern, 24 October 2012 11

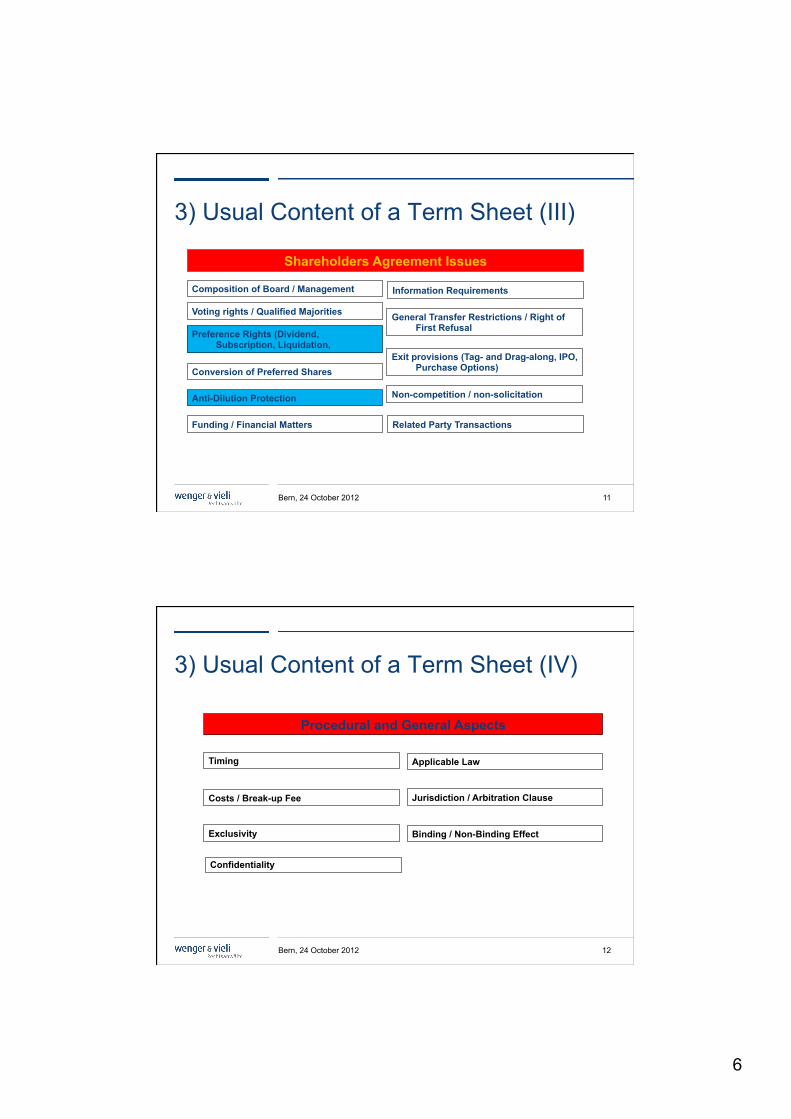

3) Usual Content of a Term Sheet (III)

Voting rights / Qualified Majorities

Composition of Board / Management Information Requirements

Conversion of Preferred Shares

Preference Rights (Dividend, Subscription, Liquidation,

General Transfer Restrictions / Right of First Refusal

Funding / Financial Matters Related Party Transactions

Exit provisions (Tag- and Drag-along, IPO, Purchase Options)

Shareholders Agreement Issues

Non-competition / non-solicitation Anti-Dilution Protection

Bern, 24 October 2012 12

3) Usual Content of a Term Sheet (IV)

Timing

Costs / Break-up Fee

Exclusivity

Applicable Law

Jurisdiction / Arbitration Clause

Binding / Non-Binding Effect

Procedural and General Aspects

Confidentiality

7

13

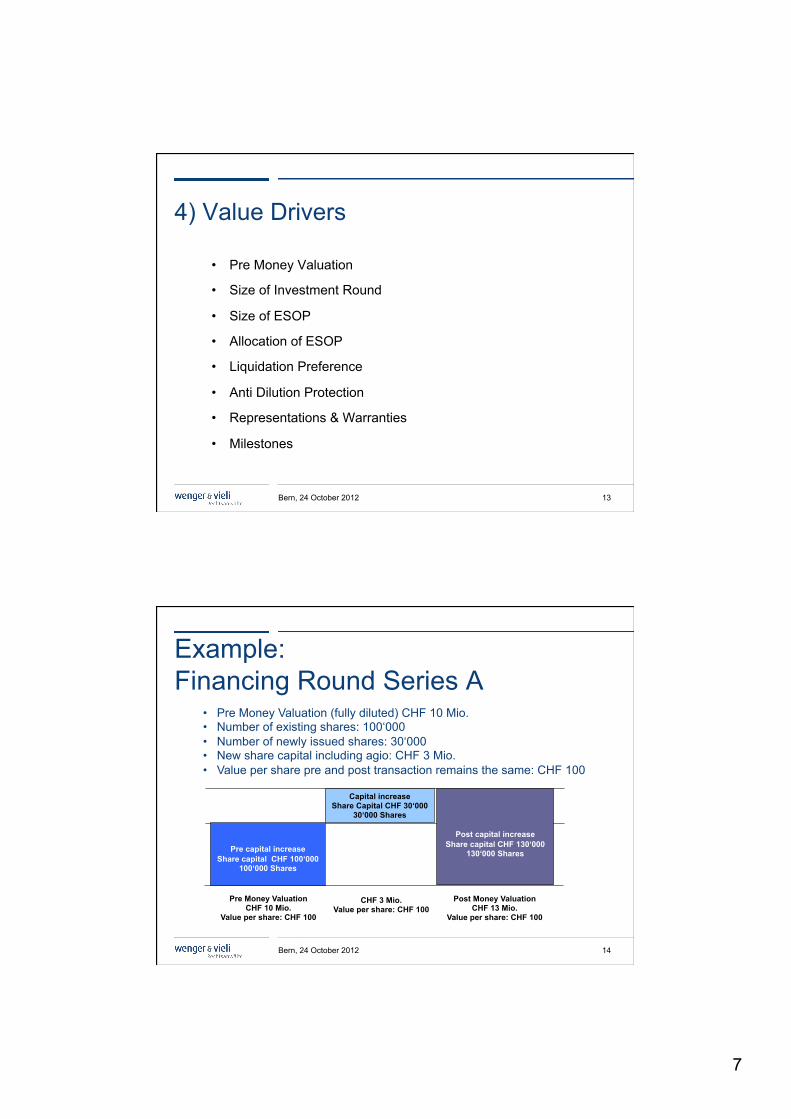

4) Value Drivers

• Pre Money Valuation

• Size of Investment Round

• Size of ESOP

• Allocation of ESOP

• Liquidation Preference

• Anti Dilution Protection

• Representations & Warranties

• Milestones

Bern, 24 October 2012

14

Example: Financing Round Series A

Pre capital increase Share capital CHF 100‘000

100‘000 Shares

Post capital increase Share capital CHF 130‘000

130‘000 Shares

Capital increase Share Capital CHF 30‘000

30‘000 Shares

Pre Money Valuation CHF 10 Mio.

Value per share: CHF 100

CHF 3 Mio. Value per share: CHF 100

Post Money Valuation CHF 13 Mio.

Value per share: CHF 100

• Pre Money Valuation (fully diluted) CHF 10 Mio. • Number of existing shares: 100‘000 • Number of newly issued shares: 30‘000 • New share capital including agio: CHF 3 Mio. • Value per share pre and post transaction remains the same: CHF 100

Bern, 24 October 2012

8

15

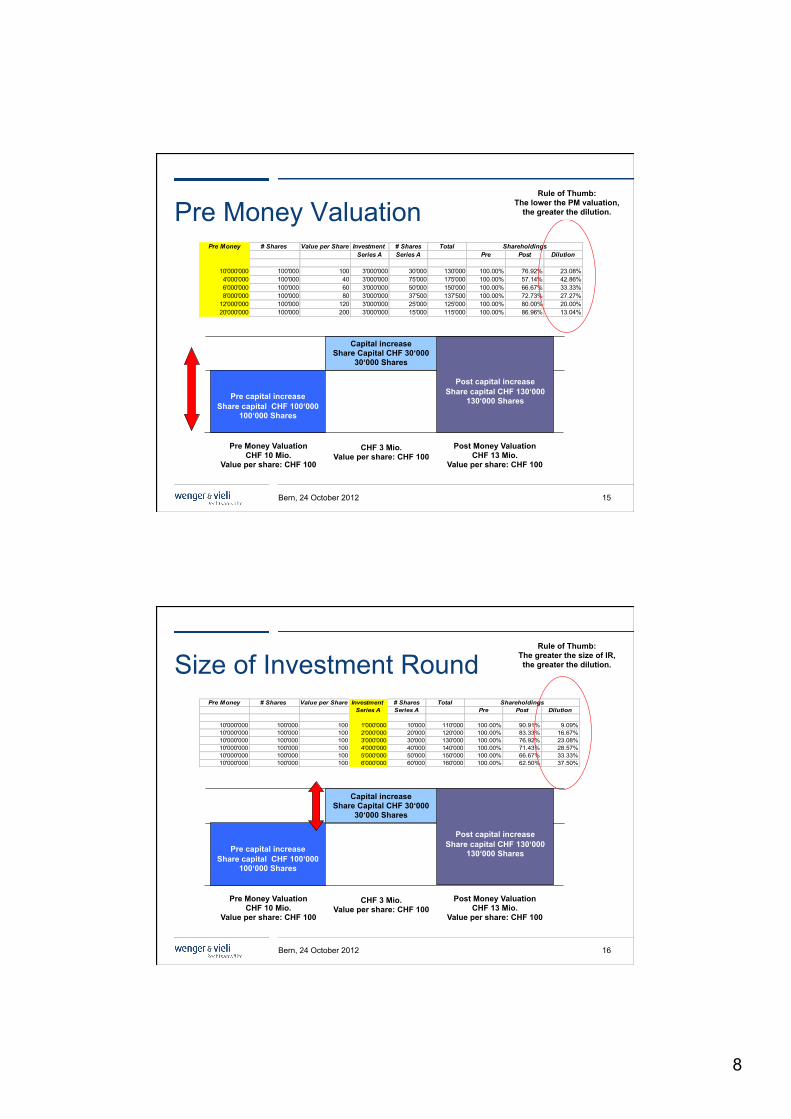

Pre Money Valuation

Pre capital increase Share capital CHF 100‘000

100‘000 Shares

Post capital increase Share capital CHF 130‘000

130‘000 Shares

Capital increase Share Capital CHF 30‘000

30‘000 Shares

Pre Money Valuation CHF 10 Mio.

Value per share: CHF 100

CHF 3 Mio. Value per share: CHF 100

Post Money Valuation CHF 13 Mio.

Value per share: CHF 100

Bern, 24 October 2012

Pre Money # Shares Value per Share Investment # Shares Total ShareholdingsSeries A Series A Pre Post Dilution

10'000'000 100'000 100 3'000'000 30'000 130'000 100.00% 76.92% 23.08%4'000'000 100'000 40 3'000'000 75'000 175'000 100.00% 57.14% 42.86%6'000'000 100'000 60 3'000'000 50'000 150'000 100.00% 66.67% 33.33%8'000'000 100'000 80 3'000'000 37'500 137'500 100.00% 72.73% 27.27%12'000'000 100'000 120 3'000'000 25'000 125'000 100.00% 80.00% 20.00%20'000'000 100'000 200 3'000'000 15'000 115'000 100.00% 86.96% 13.04%

Rule of Thumb: The lower the PM valuation,

the greater the dilution.

16

Size of Investment Round

Pre capital increase Share capital CHF 100‘000

100‘000 Shares

Post capital increase Share capital CHF 130‘000

130‘000 Shares

Capital increase Share Capital CHF 30‘000

30‘000 Shares

Pre Money Valuation CHF 10 Mio.

Value per share: CHF 100

CHF 3 Mio. Value per share: CHF 100

Post Money Valuation CHF 13 Mio.

Value per share: CHF 100

Bern, 24 October 2012

Pre Money # Shares Value per Share Investment # Shares Total ShareholdingsSeries A Series A Pre Post Dilution

10'000'000 100'000 100 1'000'000 10'000 110'000 100.00% 90.91% 9.09%10'000'000 100'000 100 2'000'000 20'000 120'000 100.00% 83.33% 16.67%10'000'000 100'000 100 3'000'000 30'000 130'000 100.00% 76.92% 23.08%10'000'000 100'000 100 4'000'000 40'000 140'000 100.00% 71.43% 28.57%10'000'000 100'000 100 5'000'000 50'000 150'000 100.00% 66.67% 33.33%10'000'000 100'000 100 6'000'000 60'000 160'000 100.00% 62.50% 37.50%

Rule of Thumb: The greater the size of IR, the greater the dilution.

9

17

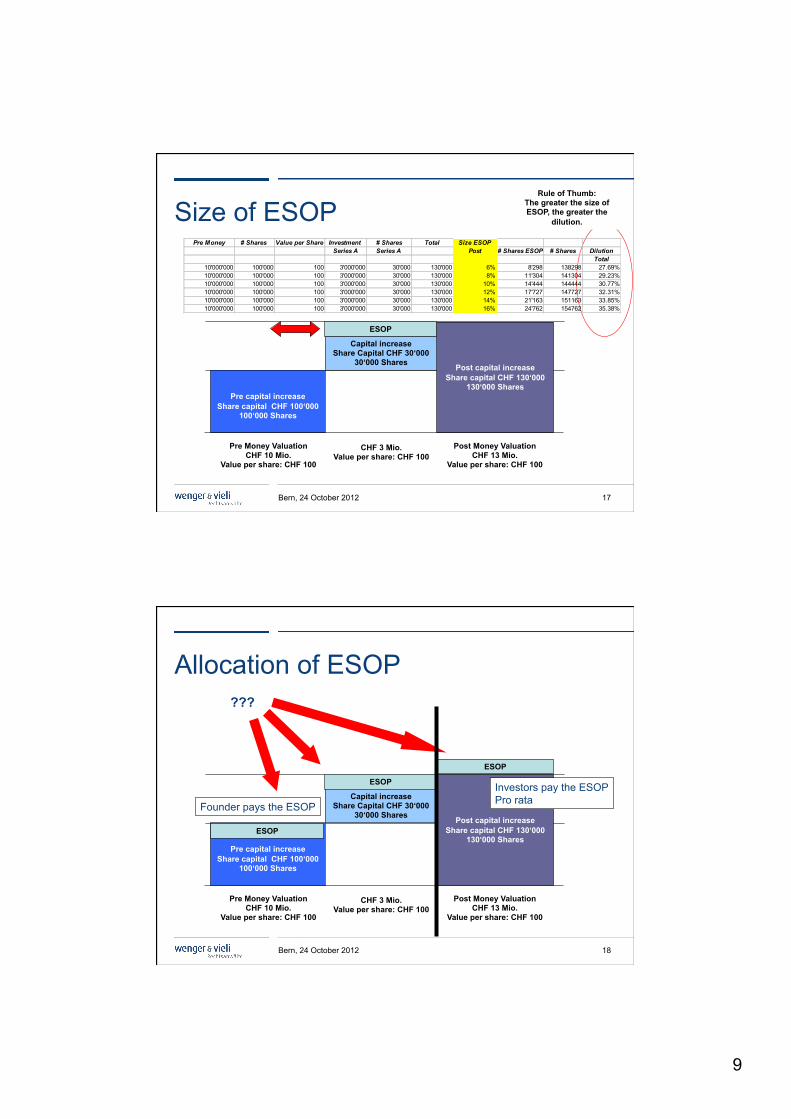

Size of ESOP

Pre capital increase Share capital CHF 100‘000

100‘000 Shares

Post capital increase Share capital CHF 130‘000

130‘000 Shares

Capital increase Share Capital CHF 30‘000

30‘000 Shares

Pre Money Valuation CHF 10 Mio.

Value per share: CHF 100

CHF 3 Mio. Value per share: CHF 100

Post Money Valuation CHF 13 Mio.

Value per share: CHF 100

Bern, 24 October 2012

ESOP

Pre Money # Shares Value per Share Investment # Shares Total Size ESOPSeries A Series A Post # Shares ESOP # Shares Dilution

Total10'000'000 100'000 100 3'000'000 30'000 130'000 6% 8'298 138298 27.69%10'000'000 100'000 100 3'000'000 30'000 130'000 8% 11'304 141304 29.23%10'000'000 100'000 100 3'000'000 30'000 130'000 10% 14'444 144444 30.77%10'000'000 100'000 100 3'000'000 30'000 130'000 12% 17'727 147727 32.31%10'000'000 100'000 100 3'000'000 30'000 130'000 14% 21'163 151163 33.85%10'000'000 100'000 100 3'000'000 30'000 130'000 16% 24'762 154762 35.38%

Rule of Thumb: The greater the size of ESOP, the greater the

dilution.

18

Allocation of ESOP

Pre capital increase Share capital CHF 100‘000

100‘000 Shares

Post capital increase Share capital CHF 130‘000

130‘000 Shares

Capital increase Share Capital CHF 30‘000

30‘000 Shares

Pre Money Valuation CHF 10 Mio.

Value per share: CHF 100

CHF 3 Mio. Value per share: CHF 100

Post Money Valuation CHF 13 Mio.

Value per share: CHF 100

Bern, 24 October 2012

ESOP

ESOP

ESOP

???

Founder pays the ESOP

Investors pay the ESOP Pro rata

10

19

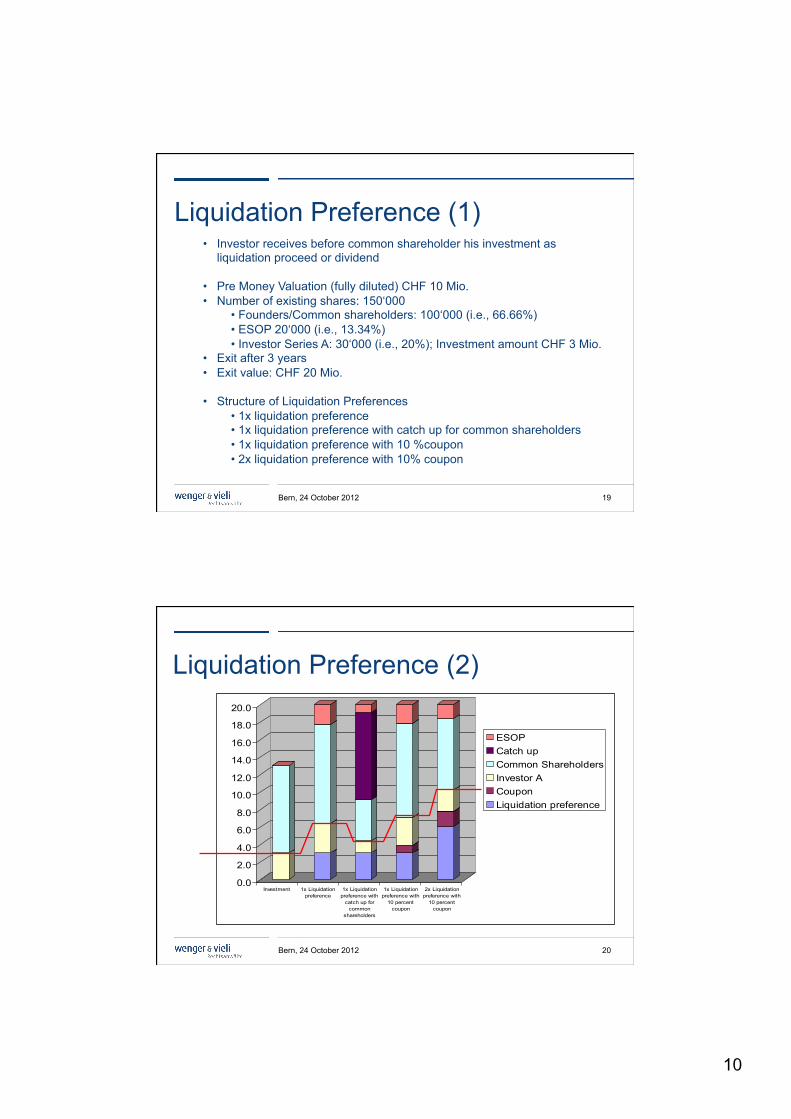

Liquidation Preference (1)

Bern, 24 October 2012

• Investor receives before common shareholder his investment as liquidation proceed or dividend

• Pre Money Valuation (fully diluted) CHF 10 Mio. • Number of existing shares: 150‘000

• Founders/Common shareholders: 100‘000 (i.e., 66.66%) • ESOP 20‘000 (i.e., 13.34%) • Investor Series A: 30‘000 (i.e., 20%); Investment amount CHF 3 Mio.

• Exit after 3 years • Exit value: CHF 20 Mio.

• Structure of Liquidation Preferences • 1x liquidation preference • 1x liquidation preference with catch up for common shareholders • 1x liquidation preference with 10 %coupon • 2x liquidation preference with 10% coupon

20

Liquidation Preference (2)

Bern, 24 October 2012

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Investment 1x Liquidationpreference

1x Liquidationpreference with

catch up forcommon

shareholders

1x Liquidationpreference with

10 percentcoupon

2x Liquidationpreference with

10 percentcoupon

ESOPCatch upCommon ShareholdersInvestor ACouponLiquidation preference

11

21

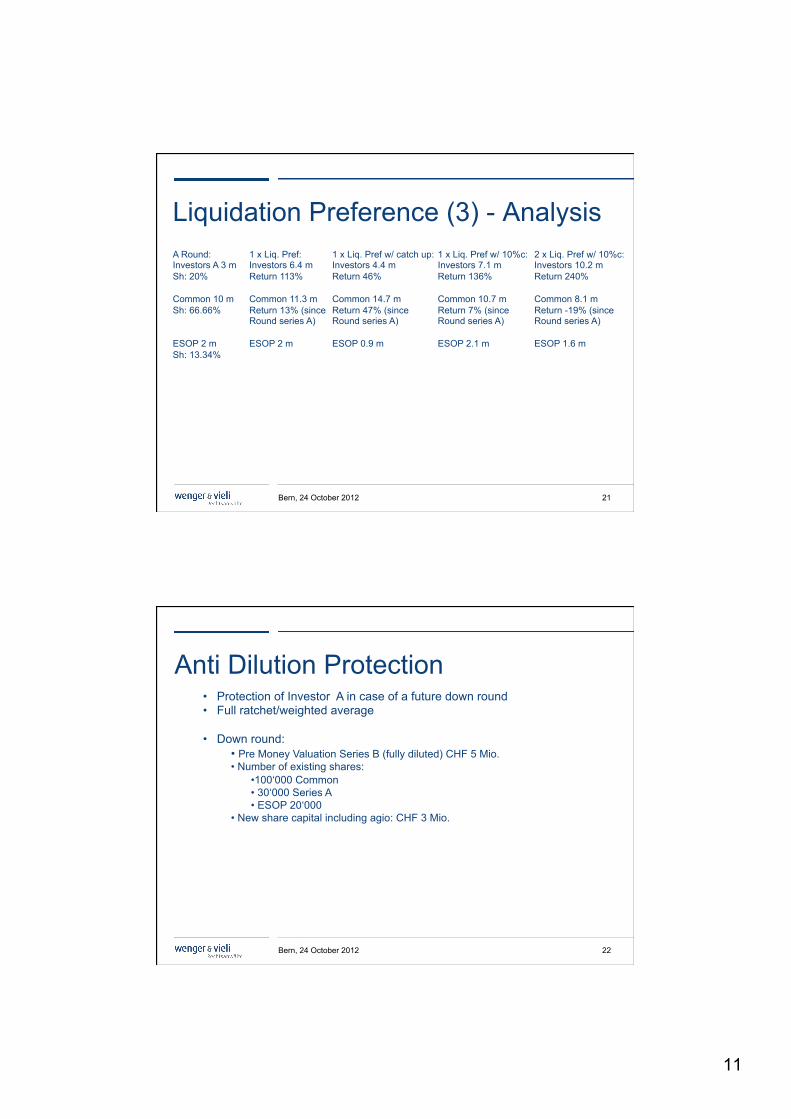

Liquidation Preference (3) - Analysis

Bern, 24 October 2012

A Round: Investors A 3 m Sh: 20% Common 10 m Sh: 66.66% ESOP 2 m Sh: 13.34%

1 x Liq. Pref: Investors 6.4 m Return 113% Common 11.3 m Return 13% (since Round series A) ESOP 2 m

1 x Liq. Pref w/ catch up: Investors 4.4 m Return 46% Common 14.7 m Return 47% (since Round series A) ESOP 0.9 m

1 x Liq. Pref w/ 10%c: Investors 7.1 m Return 136% Common 10.7 m Return 7% (since Round series A) ESOP 2.1 m

2 x Liq. Pref w/ 10%c: Investors 10.2 m Return 240% Common 8.1 m Return -19% (since Round series A) ESOP 1.6 m

22

Anti Dilution Protection

Bern, 24 October 2012

• Protection of Investor A in case of a future down round • Full ratchet/weighted average

• Down round: • Pre Money Valuation Series B (fully diluted) CHF 5 Mio. • Number of existing shares:

• 100‘000 Common • 30‘000 Series A • ESOP 20‘000

• New share capital including agio: CHF 3 Mio.

12

23

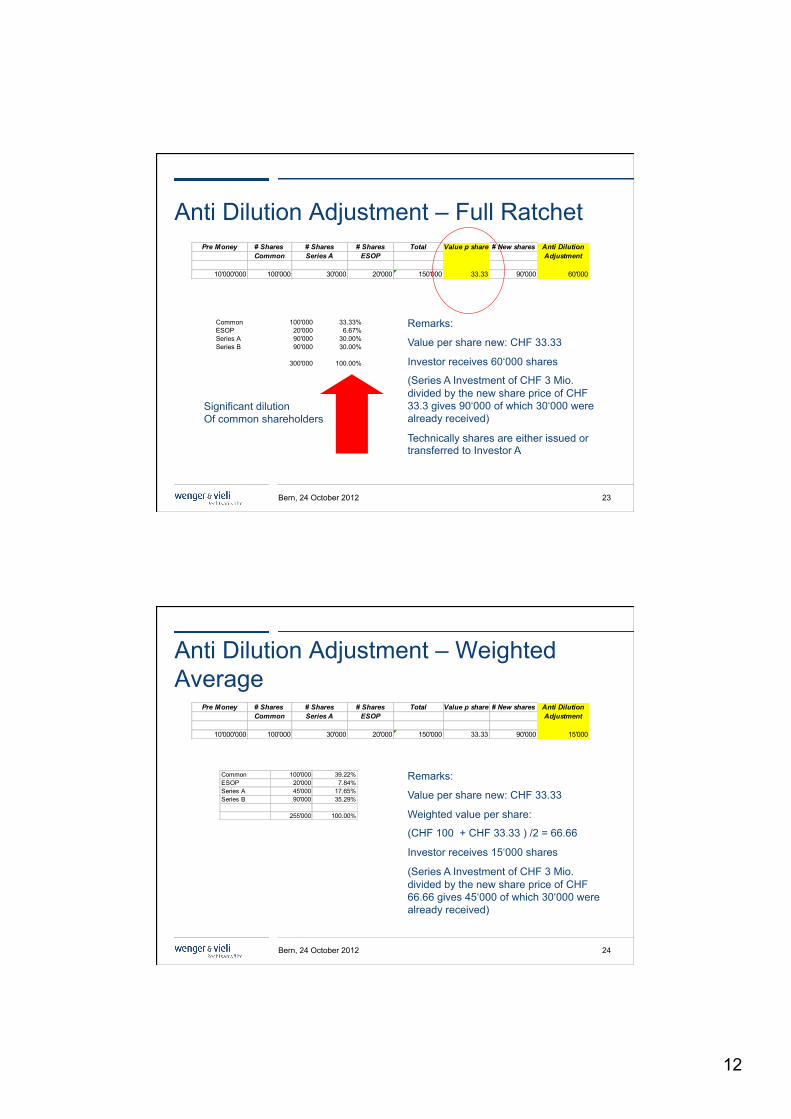

Anti Dilution Adjustment – Full Ratchet

Common 100'000 33.33%ESOP 20'000 6.67%Series A 90'000 30.00%Series B 90'000 30.00%

300'000 100.00%

Bern, 24 October 2012

Remarks:

Value per share new: CHF 33.33

Investor receives 60‘000 shares

(Series A Investment of CHF 3 Mio. divided by the new share price of CHF 33.3 gives 90‘000 of which 30‘000 were already received)

Technically shares are either issued or transferred to Investor A

Pre Money # Shares # Shares # Shares Total Value p share # New shares Anti DilutionCommon Series A ESOP Adjustment

10'000'000 100'000 30'000 20'000 150'000 33.33 90'000 60'000

Significant dilution Of common shareholders

24

Anti Dilution Adjustment – Weighted Average

Common 100'000 39.22%ESOP 20'000 7.84%Series A 45'000 17.65%Series B 90'000 35.29%

255'000 100.00%

Bern, 24 October 2012

Remarks:

Value per share new: CHF 33.33

Weighted value per share:

(CHF 100 + CHF 33.33 ) /2 = 66.66

Investor receives 15‘000 shares

(Series A Investment of CHF 3 Mio. divided by the new share price of CHF 66.66 gives 45‘000 of which 30‘000 were already received)

Pre Money # Shares # Shares # Shares Total Value p share # New shares Anti DilutionCommon Series A ESOP Adjustment

10'000'000 100'000 30'000 20'000 150'000 33.33 90'000 15'000

13

25

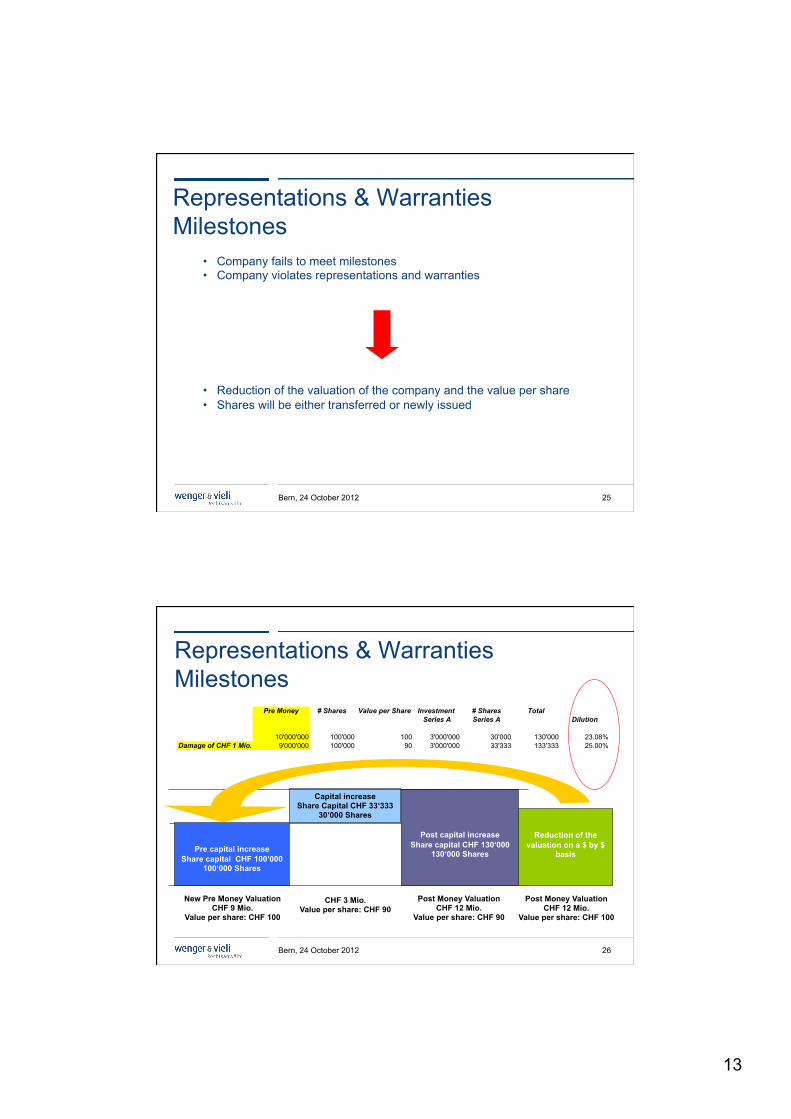

Representations & Warranties Milestones

Bern, 24 October 2012

• Company fails to meet milestones • Company violates representations and warranties

• Reduction of the valuation of the company and the value per share • Shares will be either transferred or newly issued

26

Representations & Warranties Milestones

Pre capital increase Share capital CHF 100‘000

100‘000 Shares

Post capital increase Share capital CHF 130‘000

130‘000 Shares

Capital increase Share Capital CHF 33‘333

30‘000 Shares

New Pre Money Valuation CHF 9 Mio.

Value per share: CHF 100

CHF 3 Mio. Value per share: CHF 90

Post Money Valuation CHF 12 Mio.

Value per share: CHF 90

Bern, 24 October 2012

Reduction of the valuation on a $ by $

basis

Post Money Valuation CHF 12 Mio.

Value per share: CHF 100

Pre Money # Shares Value per Share Investment # Shares TotalSeries A Series A Dilution

10'000'000 100'000 100 3'000'000 30'000 130'000 23.08%Damage of CHF 1 Mio. 9'000'000 100'000 90 3'000'000 33'333 133'333 25.00%

14

Bern, 24 October 2012 27

Any Questions?

28

Thanks.

Pascal Honold Wenger & Vieli Ltd. Dufourstrasse 56 8034 Zurich Phone: 058 / 958 58 58 E-mail: [email protected]

Bern, 24 October 2012

15

THANK YOU FOR YOUR ATTENDANCE!

Bern, 25 October 2011

Wenger & Vieli Ltd. Dufourstrasse 56, PO Box 1285, 8034 Zurich Phone +41 (0)58 958 58 58, www.wengervieli.ch