Term Sheet Negotiations (08.24.2015)

22

1 Term Sheet Negotiations August 24, 2015 Chris Austin, Partner, Orrick Liz Wessel, CEO WayUp Ellie Wheeler, Principal, Greycroft Partners

-

Upload

joyce-chuang -

Category

Small Business & Entrepreneurship

-

view

488 -

download

2

Transcript of Term Sheet Negotiations (08.24.2015)

1

Term Sheet NegotiationsAugust 24, 2015

Chris Austin, Partner, Orrick

Liz Wessel, CEO WayUp

Ellie Wheeler, Principal, Greycroft Partners

2

Anatomy of a Term Sheet: Agenda

• Key Points

• Pre-Financing Strategy

• Term Sheet Review

— Allocating Value

— Managing the Company

— Investors Rights

—Miscellaneous Terms

• Questions

3

Anatomy of a Term Sheet: Overview

• Allocating Value

—Valuation

—Capitalization

—Liquidation

—Dividends

• Managing the Company

—Board Composition

—Protective Provisions

—Drag Along Rights

• Investor Rights

—Anti-Dilution Protection

—Right of First Refusal & Co-Sale Right

—Redemption

• Miscellaneous Terms

4

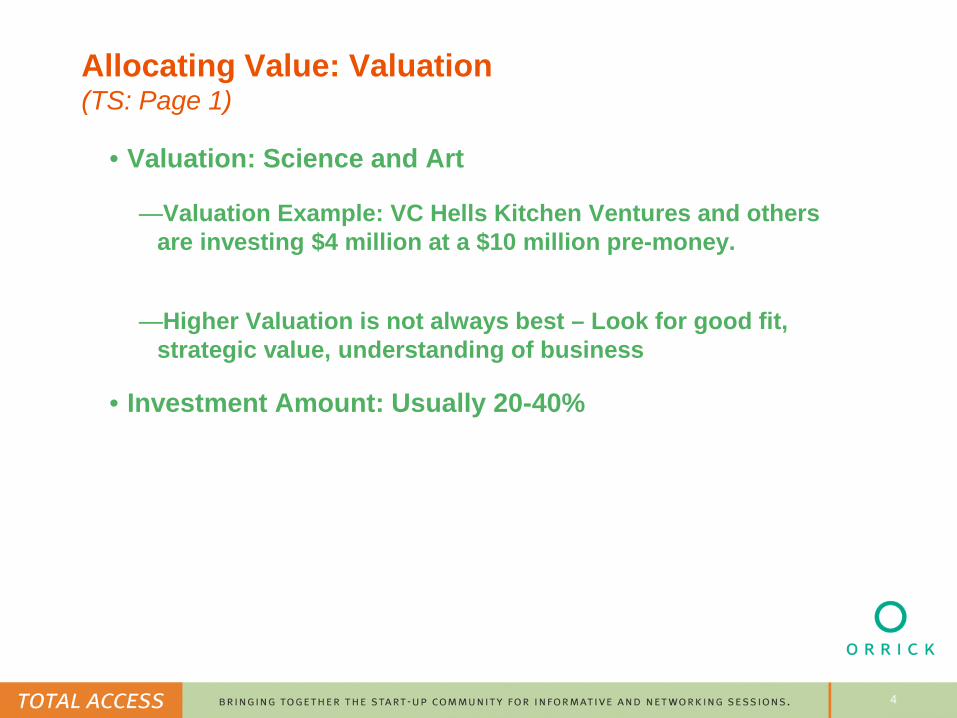

Allocating Value: Valuation(TS: Page 1)

• Valuation: Science and Art

—Valuation Example: VC Hells Kitchen Ventures and othersare investing $4 million at a $10 million pre-money.

—Higher Valuation is not always best – Look for good fit,strategic value, understanding of business

• Investment Amount: Usually 20-40%

5

Allocating Value: Capitalization(TS: Pages 1/2)

Founder Vesting

• Standard Schedule is a 4 year term with a 1 year cliff

• Acceleration – Single and Double Trigger

• Setup prior to VC negotiations and keep terms within

the market range (founder favorable side). You do not

want this to be a point of negotiation with VCs.

• Vesting for a portion of time served usually allowed

Stock Option Pool

• Key issue: What will you need to compensate your

employees between this round and the next? No one

answer – depends on current team

6

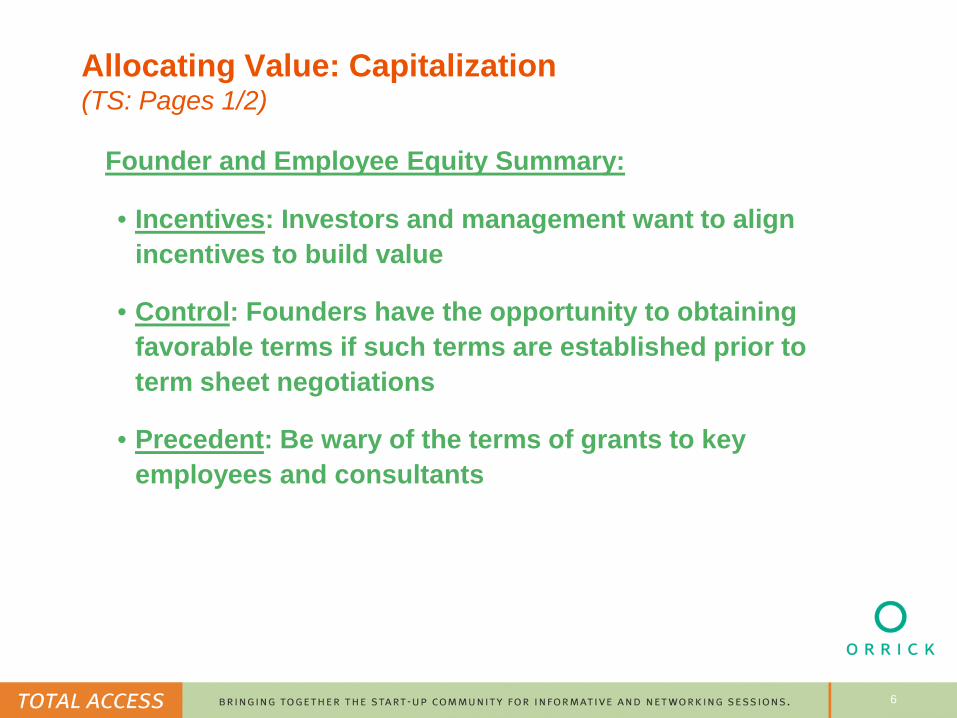

Founder and Employee Equity Summary:

• Incentives: Investors and management want to align

incentives to build value

• Control: Founders have the opportunity to obtaining

favorable terms if such terms are established prior to

term sheet negotiations

• Precedent: Be wary of the terms of grants to key

employees and consultants

Allocating Value: Capitalization(TS: Pages 1/2)

7

Allocating Value: Dividends(TS: Page 2)

• A key component of Preferred Stock ~ basically, it’s

interest.

• This is not a “coupon” investment. Keep at 8% or less

(8% is standard)

• Try to stay away from cumulative dividends. Current

market standard is “as, if and when declared” (which is

generally never…. So no dividends)

8

Allocating Value: Liquidation Preference(TS: Page 2)

• At Liquidation/Dissolution, VC gets:

—The right to receive the proceeds first - preference

—Piece of the remaining proceeds – participation – try to NOThave participating preferred

• Examples:

—Both liquidation multiples and participation will the VC’Sactual return

—$20 million investment for 25% of company, and later $50million exit

—Participating = $20 mm + 25% of $30 mm = $27.5 MM to VC,$22.5 to everyone else

—Non-participating = $20 MM to VC and $30 MM to everyoneelse

9

Allocating Value: Liquidation Preference(TS: Page 2)

Liquidation Summary:

• Incentives: Liquidation Preferences will guide incentives

toward liquidity

• Control: Even though the Common stockholders may own

the majority of the company, they may be excluded from

the liquidity proceeds

• Precedent: Subsequent rounds can lead to stacking

preferences

10

Managing the Company: Protective Provisions(TS: Page 3)

Protective Provisions

• Without the vote of a % of Preferred, Company will not

be able to take actions that affect equity/ownership.

For example:

—Authorize/Issue Preferred Stock

—Grant options beyond a certain limit

—Amend the charter

—Sell the Company

• These are in every deal – look to confirm that set of

restrictions is standard

11

Managing the Company: Board Structure(TS: Page 3)

Board Composition

• Generally at Series A, VC will ask for 1-2 seats

• VC will ask for special provisions ~ Preferred Director

consent

• At Series A, be sure VC is not board majority

12

Managing the Company: Drag Along Rights(TS: Page 5)

Drag-Along Rights

• Investors can force Common Stockholders to participate

in a sale of the Company.

• Drag-Along rights are not present in every deal, but

becoming more frequent

• Try to make is so that majority common + majority

preferred required – then it’s used to clean up little

holders

13

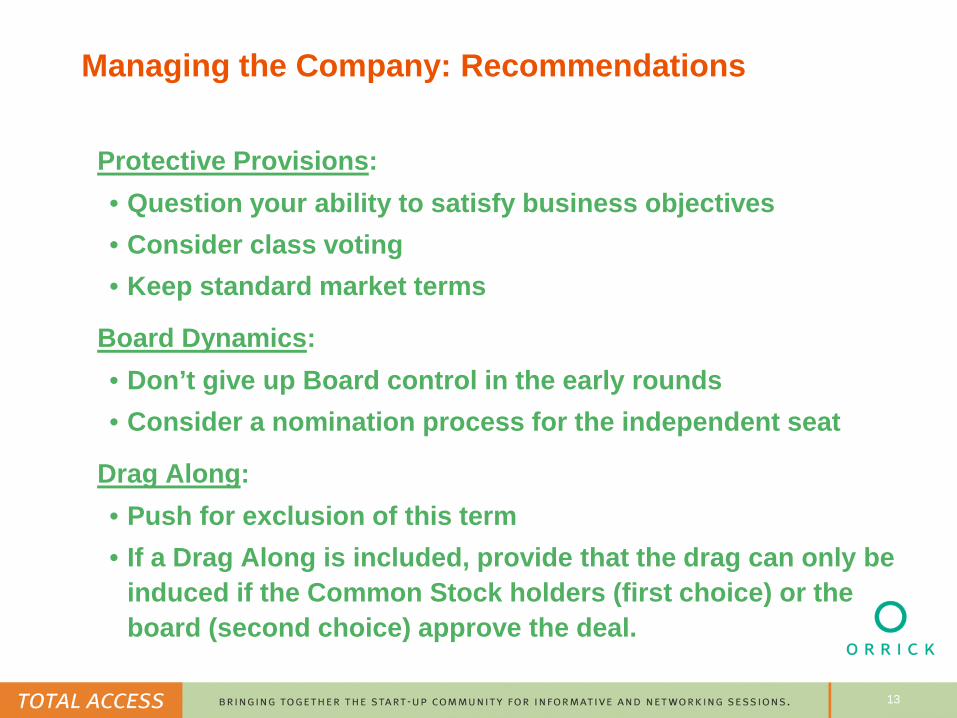

Managing the Company: Recommendations

Protective Provisions:

• Question your ability to satisfy business objectives

• Consider class voting

• Keep standard market terms

Board Dynamics:

• Don’t give up Board control in the early rounds

• Consider a nomination process for the independent seat

Drag Along:

• Push for exclusion of this term

• If a Drag Along is included, provide that the drag can only be

induced if the Common Stock holders (first choice) or the

board (second choice) approve the deal.

14

Investor Rights

Further Protection for the VC: Reducing Risk

• Right of First Offer (TS: Page 4)

• Anti-Dilution Protection (TS: Page 2)

• Right of First Refusal & Co-Sale Right (TS: Page 5)

• Redemption (TS: Page 3)

• Registration Rights (TS: Page 4)

15

Investor Rights: Right of First Offer(TS: Page 4)

• With certain standard exceptions, if the company

issues stock, VC has the right to maintain its pro rata

percentage ownership of the company.

—This measurement should be based on the fully-dilutedvalues, not the outstanding values

• ROFO is a standard term, but limit who has the right

16

Investor Rights: Antidilution Protection(TS: Page 2)

• If the Company subsequently issues cheaper stock

(subject to standard exceptions), conversion ratio is

adjusted so that upon conversion to common, they get

more than 1:1

• A few methods (Broad/Narrow/Ratchet); varying levels

of punishment

• Broad-based is overwhelmingly the market trend

17

Investor Rights: Right of First Refusal and Co-Sale(TS: Page 5)

Right of First Refusal

• Before Founder can sell, he must give Company and

Investors right to buy

Co-Sale Right

• If the Investors and the Company decline to buy, then

the Founder must give Investors a right to participate

in that sale

18

Investor Rights: Right of First Refusal and Co-Sale(TS: Page 5)

Recommendations

• Right of First Refusal & Co-Sale is completely standard

• Be sure to limit who has the right with a share threshold.

• Be wary of carve-outs for founders---example of why your

attorney should draft the documents

19

Investor Rights: Redemption(TS: Page 3)

• Force the Company to return the money to investors at

specified time (i.e., in 7 years, VC can ask for money

back)

• Push for exclusion of this term (very bad precedent);

however, if it is included confirm that the terms provide:

—Enough runway (5-10 years)

—Redeeming investors only receive what they paid +dividends

—Higher approval threshold (other Investors must consent)

20

Investor Rights: Registration Rights(TS: Page 4)

Registration Rights

• Investors can make the company file for IPO, follow-on

offerings

• Don't spend too much time on this section

21

Term Sheets: Miscellaneous Terms

• Information and Management Rights: Opening the books

• Legal Fees: Investor Counsel fees $25k-35k

• No-Shop (“Exclusivity”): Reasonable term

![SWIFIA template term sheet - EPA · 2021. 6. 25. · july 2020 [template term sheet – swifia – srfs without capital markets debt] this template term sheet is not a contract or](https://static.fdocuments.net/doc/165x107/61403a391664f15185589edd/swifia-template-term-sheet-epa-2021-6-25-july-2020-template-term-sheet-a.jpg)