Term Investment Accounts Terms & Conditions and …...2 Contents About this document..... 3 3 About...

24

Term Investment Accounts Terms & Conditions and Fees & Charges Effective 20 January 2020 Contains the Terms & Conditions and Fees & Charges for our Term Investment Accounts. This document must be read together with our Accounts & Access Facilities Terms & Conditions document (which contains the terms & conditions relating to Access Facilities that may be used to access your Term Investment Account) and our Fees & Charges document (which contains the fees & charges relating to Access Facilities). People’s Choice Credit Union, a trading name of Australian Central Credit Union Ltd ABN 11 087 651 125, acts under its own Australian Financial Services Licence 244310 and Australian Credit Licence 244310.

Transcript of Term Investment Accounts Terms & Conditions and …...2 Contents About this document..... 3 3 About...

1

Term Investment Accounts Terms & Conditions and Fees & Charges

Effective 20 January 2020

Contains the Terms & Conditions and Fees & Charges for our Term Investment Accounts.

This document must be read together with our Accounts & Access Facilities Terms & Conditions document (which contains the terms & conditions relating to Access Facilities that may be used to access your Term Investment Account) and our Fees & Charges document (which contains the fees & charges relating to Access Facilities).

People’s Choice Credit Union, a trading name of Australian Central Credit Union Ltd ABN 11 087 651 125, acts under its own Australian Financial Services Licence 244310 and Australian Credit Licence 244310.

2

Contents

About this document ..................................................................................................................................................3

1. Definitions ............................................................................................................................................................ 4

2. Codes of Practice ............................................................................................................................................... 6

3. Privacy ....................................................................................................................................................................7

4. Term Investment Accounts ............................................................................................................................. 9

5. Complaints ..........................................................................................................................................................20

6. Financial Claims Scheme ...............................................................................................................................20

7. Summary of Term Investment Accounts................................................................................................... 21

8. Term Investment Fees & Charges ...............................................................................................................22

3

About this DocumentThis document sets out the Terms & Conditions and Fees & Charges for our Term Investment Accounts, along with any notices we give you about interest rates.

The Terms & Conditions that apply to Access Facilities which you may use to access your Term Investment Account are set out in our Accounts & Access Facilities Terms & Conditions document and the fees and charges associated with the Access Facilities are set out in our Fees & Charges document.

The information in this document will help you to:

• Understand how our Term Investments operate (including interest, Account statements etc.);

• Decide whether a People’s Choice Credit Union Term Investment will meet your needs; and

• Compare this product with other financial products you may be considering.

You should read this document before making a decision to open a Term Investment Account with People’s Choice Credit Union. Please keep this document in a safe place, as you may need to refer to it in the future. Alternatively, you can download this document by visiting our website at peopleschoicecu.com.au

Please note: by opening a Term Investment Account you agree to be bound by these Terms & Conditions.

4

1. Definitions 1.1 In this document:

Access Facility means the Access Facilities described in our “Accounts & Access Facilities Terms & Conditions” document which we allow you to use to access your Term Investment Account, including Internet Banking and Mobile Banking. We may change the Access Facilities we allow you to use to access your Term Investment Account from time to time;

Access Method means a method authorised by us for your use as a form of authentication, and accepted by us as your authority to make a transaction or to access or change information about your Account, that does not require a manual signature, and includes, but is not limited to any combination of a Card, Digital Wallet, Account Number, Card Details, expiry date, PIN, MAP, People’s Choice Secure Code and Access Code;

Account means a Term Investment Account with us;

Accountholder means the person(s) in whose name(s) an Account is held and if there is more than one Accountholder it means the Accountholders jointly and severally;

AML means Anti-Money Laundering and Counter Terrorism Financing Act 2006 (Cth) as amended, varied or substituted from time to time;

Business Day means, in the relevant place, a day that is not a Saturday, a Sunday or a public holiday. Where the relevant place is not clear, Business Day, means a day that is a Business Day in Sydney or Melbourne;

Court Order means probate, letters of administration or other orders of similar effect made by an Australian State or Territory Court in relation to the administration of the estate of a deceased person:

Deposit Guarantee means a guarantee from the Government for funds up to $250,000 held as eligible deposits;

Early Redemption means a full or partial withdrawal from a Term Investment Account prior to maturity of the investment;

Electronic Communication means a communication of information in the form of data, text or images by means of guided and/or unguided electromagnetic energy;

End of Day in respect of any calendar day means the earlier of:

• the time we commence our end of day processing, being not before 9.00pm South Australia time; and

• 11:29:59 pm in South Australia

Grace Period means a period of seven days from maturity of a Term Investment Account;

Internet Banking means:

• The service we provide through our Website which you can access using an internet browser software application, which enables you to deal with us electronically over the internet including receiving information from and giving information to us about your Accounts or Access Facilities and conducting transactions on your Accounts; and

• Mobile Banking;

Joint Account means an Account held in the name of more than one Member;

MAP means Member Access Password as defined in clause 4.17;

5

Member means a person who holds a Member share in the Credit Union;

Member Number means the number allocated to you by People’s Choice Credit Union to be used to assist us in identifying you and to allocate products and services you hold. You may be allocated more than one Member Number under your Membership;

Membership means holding one share in People’s Choice Credit Union entitling the Membership owner to products and services offered by People’s Choice Credit Union;

Minor means a person under the age of 18 years old. Special terms and conditions apply to Accounts held by minors;

Mobile Banking means the Internet Banking service we provide through Mobile Banking software applications we make available for you to download on compatible Devices, which are designed for mobile Devices such as mobile phones and tablets, which enables you to deal with us electronically over the internet, including receiving information from and giving information to us about your Accounts and Access Facilities and conducting transactions on your Accounts but does not include Internet Banking accessed through an internet browser software application;

National Contact Centre means our call centre which can provide telephone assistance in relation to the products and services we offer;

Notification of Change Table means the table set out in clause 4.22.3;

Payment means a payment transacted using an Access Facility;

Phone Banking means a service we offer through telephone communication network which enables you to electronically receive information from us about your Accounts, or to transact on your Accounts;

Primary Email Address means the email address you have provided to us;

Privacy Act means the Privacy Act 1988 (Cth) as amended, varied or substituted from time to time;

Summary of Term Investment Accounts Table means the tables provided on page 18;

Terms & Conditions means:

• In relation to an Account, these Terms & Conditions and any notice we give you about current interest rates; and

• In relation to an Access Facility, our “Accounts & Access Facilities Terms & Conditions” document and our “Fees & Charges” document;

Third Party Operator means a person referred to in clause 4.11 including a person authorised by either a Member or the Guardianship Board to operate on an Account(s);

Website means our website accessible at peopleschoicecu.com.au;

We, us, our, People’s Choice Credit Union or the Credit Union refers to People’s Choice Credit Union, a trading name of Australian Central Credit Union Ltd ABN 11 087 651 125, Australian Financial Services Licence 244310 and Australian Credit Licence 244310;

You means, according to the context:

• The Accountholder; and • Any third party the Accountholder nominates to operate the Account.

6

2. Codes of Practice 2.1 Customer Owned Banking Code of Practice

2.1.1 The Customer Owned Banking Code of Practice seeks to foster good relations between customer owned banking institutions and their customers. The Customer Owned Banking Code of Practice also seeks to promote fair and consistent treatment of customers of customer owned banking institutions by setting down formal standards of disclosure and conduct that must comply with when dealing with their customers.

The Customer Owned Banking Code of Practice is administered by the Code Compliance Committee, an independent committee established by the Customer Owned Banking Association. People’s Choice Credit Union is a customer owned banking institution and is committed to the Customer Owned Banking Code of Practice.

The code contains 10 key promises:

• We will be fair and ethical in our dealings with you; • We will focus on our customers; • We will give you clear information about our products and services; • We will be responsible lenders; • We will deliver high customer service and standards; • We will deal fairly with any complaints; • We will recognise customers’ rights as owners; • We will comply with our legal and industry obligations; • We will recognise our impact on the wider community; and • We will support and promote the Customer Owned Banking Code of Practice

2.1.2 Our commitment to the Customer Owned Banking Code of Practice means that we will:

• Define standards of good practice and service; • Disclose information that is relevant and useful to our Members; • Clearly define the terms and conditions for all our products and services; and • Make a simple, effective complaints handling process available to our Members.

2.1.3 You can obtain a copy of the Customer Owned Banking Code of Practice upon request or from our Website. The Customer Owned Banking Code of Practice applies to all our Accounts.

7

3. Privacy 3.1 Collection of Personal Information

3.1.1 We collect personal information about you for the purposes of providing our products and services to you and for processing your Payments.

3.1.2 We owe you a duty to keep information about you confidential and in general, we will not disclose your information to other parties. However, we can disclose information we have about you in circumstances where:

• We are required to do so in order for us to provide you with your Account or Access Facility or to carry out your instructions in relation to an Account or Access Facility.

For example, disclosure to our service providers or payment intermediaries, such as CUSCAL.

• We are compelled to do so by law.

For example, disclosure to various Government departments and agencies such as the Australian Taxation Office of the amount of interest you have earned on your Account, and disclosure to the courts under subpoena.

• It is in the public interest to do so.

For example, where a crime, fraud or misdeed is committed or suspected by us, and in our reasonable discretion, disclosure is justified.

• We are permitted by law and it is in our interest to do so.

For example, disclosure to a court in the event of legal action to which we are a party, or if we are trying to recover a debt, we may have to inform solicitors, debt collectors or credit reference agencies.

• You ask us or agree for us to do so.

For example, when you open an Account or apply for a service, you may agree to us giving a reference or passing on information to a credit agency by signing an authority allowing us to do so.

3.1.3 You may have access to the personal information we hold about you at any time by asking us.

3.1.4 We must also comply with the Privacy Act which is an Act passed by the Australian Government that requires us not to disclose certain information about you unless that disclosure is allowed.

3.1.5 More detailed information on our privacy practices can be found in our Privacy Policy, which can be obtained from:

• any of our branches or Advice Centres; • by calling us on 13 11 82; or • our Website.

8

3.2 Anti-Money Laundering (AML) and Counter Terrorism Financing Requirements

3.2.1 We meet the regulatory and compliance obligations of AML and Counter-Terrorism Financing laws both in Australia and overseas. These obligations mean that:

• We will not allow a person to operate any Account(s) until his or her identity has been verified in accordance with any identification procedures we deem necessary to meet our obligations. This applies equally for all Account owners and authorised Third Party Operators;

• We may be required to obtain additional information from you where required by any law in Australia or any other country and you agree to provide us with that information;

• We may be required (and you authorise us) to disclose information provided to us or any other information where required by law in Australia or any other country. This includes the release of information regarding Internet Banking transactions to overseas regulators;

• Your transactions could be delayed, blocked or frozen if we believe on reasonable grounds that making a Payment may be in breach of the law in Australia or any other country;

• You release us from all liability to you if we delay or block any transaction, or refuse to pay any money or do anything else affecting a transaction or Payment in the reasonable belief that a transaction or Payment would contravene any law in Australia or any other country.

3.2.2 You agree that you will not initiate, engage in or effect a transaction or Payment that may breach any law in Australia or any other country. If you do so, you indemnify us against any loss or liability we may incur which arises from such transaction or Payment.

9

4. Term Investment Accounts 4.1 People’s Choice Credit Union Term Investment Accounts & Access Facilities

4.1.1 By opening an Account, you authorise us to permit you or any of the Member(s) linked to the Account (each an “Authorised Person”) to:

• operate the Account; • deposit money in the Account; • negotiate any cheques in your name; • withdraw all or any moneys standing to the credit of the Account; • obtain statements of the Account and any information concerning the Account generally; • provide renewal / reinvestment / redemption and interest payment instructions; • give a third party authority to a Third Party Operator to operate the Account; and • use any Access Facility or other means available to access or operate your Account, in accordance with these Terms & Conditions.

4.1.2 You indemnify us for any liability arising out of the use of the Account and as specified in clause 4.1.1, including where an Authorised Person acts without, or inconsistently with, your instructions.

4.1.3 In the event of your death, the credit balance in any Account held by you that is not a Joint Account will be deemed to be property located:

(a) if a Court Order has been made in relation to the administration of your estate and the original, or a certified copy, of that Court Order has been provided to us, in the State or Territory in which that Court Order was made; or

(b) otherwise, in the State of South Australia.

4.2 Becoming a Member

4.2.1 You will need to become a Member of the Credit Union before we can issue an Account to you.

To become a Member, you will need to do everything we ask of you including, without limitation, complete a Membership application form and purchase a $2.00 share in the Credit Union which is fully refundable should you ever resign your Membership.

4.2.2 You can open an Account jointly with another person, so long as you are both Members of the Credit Union.

4.2.3 Memberships can also be opened for non-personal use, trusts, clubs and societies, but must be opened in the name of a separate legal entity.

4.3 Providing Proof of Identity

4.3.1 The law requires us to verify your identity when you open an Account or Membership or when you become a Third Party Operator to an Account or Membership.

4.3.2 You agree to provide us with any documents we reasonably require from you in order for us to comply with our obligations under AML or any other relevant legislation. If you do not provide us with this information we may refuse to open an Account or Membership for you or allow you to become a Third Party Operator.

4.3.3 The regulations require all identification to be current and original documents or certified copies of the original documents must be used.

10

4.4 Opening and Operating an Account

You can open any combination of Accounts included in the Summary of Term Investment Accounts Table subject to the eligibility requirements of the Account type.

4.5 Fees & Charges

4.5.1 This document outlines the current fees and charges applicable to our Term Investment Accounts. Please refer to our “Fees & Charges” document to find out more information about the Fees & Charges relating to other products and services.

4.5.2 We may vary fees or charges on our Term Investment Accounts from time to time. Please see the Notification of Change Table for details of how and when we must notify you of any changes to those fees and charges.

4.6 Interest

4.6.1 To find out more information about the current interest rates applicable to our Term Investment Accounts, please refer to our “Transactions and Savings Interest Rates” document.

4.6.2 We calculate interest on the closing daily credit balance of your Account as at the End of Day, unless otherwise indicated in the Summary of Term Investment Accounts Table. We may vary interest rates from time to time. However, interest rates on Term Investment Accounts remain fixed for the agreed term. You can obtain information about current Term Investment interest rates from us at any time by visiting our Website.

4.7 Tax File Numbers and Taxation

4.7.1 Interest earned on an Account is income and may be subject to income tax.

4.7.2 When you apply for an Account we will ask you for your Tax File Number or exemption. We apply your Tax File Number to each Account. You are not obliged to disclose your Tax File Number to us. However, if you do not, and do not claim a valid exemption, we are obliged to deduct withholding tax from any interest you earn at the highest marginal taxation rate plus the Medicare levy rate. The withholding tax rate is set by the Government and may vary from time to time.

4.7.3 For a Joint Account, all holders must quote their Tax File Numbers and/or exemptions; otherwise withholding tax applies to the whole of the interest earned on the Joint Account.

4.7.4 For overseas residents, withholding tax may apply even though you have quoted us your Tax File Number.

4.7.5 For business Accounts and charities, you need only quote your ABN instead of your Tax File Number.

4.7.6 Your Tax File Number will be kept in accordance with the strict guidelines of the Privacy Act.

4.8 Joint Accounts

4.8.1 A Joint Account is an Account in the name of more than one person.

4.8.2 The important legal consequences of holding a Joint Account are:

• The right of survivorship – when one joint holder dies, the surviving joint holder(s) automatically take the deceased joint holder’s interest in the Account;

• Joint liability – each joint holder(s) is individually liable for the full amount owing on the Joint Account. This means we can recover all money owing from one or more of the Accountholders as we choose.

11

4.8.3 You can operate a Joint Account on the basis of:

• ‘all to sign’; or • ‘only one to sign’; or • specific signing authority, eg: ‘two of four joint holders to sign’.

All to sign means all joint holders must authorise any action on the Account, including closure of the Account. Only one to sign means any one joint holder can authorise any action on the Account, including closure of the Account.

Specific signing authority means the instruction for a signing authority to be followed in regard to any action on the Account, including closure of the Account.

4.8.4 If the Joint Accountholders omit to indicate the signing authority on the Account, the Account will default to ‘all to sign’.

4.8.5 All Joint Accountholders must consent to the Joint Account being operated on an ‘only one to sign’ basis. However, any one Joint Accountholder can alter this arrangement, making it ‘all to sign’.

4.8.6 If more than one signature is required this will limit the types of transactions you can perform. To perform transactions via Internet Banking the Account must be ‘only one to sign’.

4.9 Accounts Opened for Minors

4.9.1 An Account opened by a parent(s), legal guardian(s) or other adult(s) on behalf of a Minor must be in the Minor’s sole name – a Joint Account cannot be opened

4.9.2 Accounts opened independently by a Minor may be solely in the name of the Minor or be a Joint Account - A Minor may open a Joint Account with another Minor(s) aged 13 or over and/or an adult(s)

4.9.3 Accounts opened for Minors under the age of 13 (at time of Account opening):

• the Account can only be opened by a parent(s), legal guardian(s) or other adult(s) on behalf of the Minor.

• the person(s) who opens the Account must be a Third Party Operator(s) when the Account is opened and may operate the Account in that capacity subject to the terms of the Account operating authority, the other provisions of this clause 4.9.3, and the requirements of clause 4.11.

• the Minor may only operate the Account (while a Minor) with the express, written consent of the Third Party Operator(s) in a form we approve and in accordance with the Account operating authority. The Minor may then operate the Account in accordance with the Account operating authority (as varied to include the Minor) and the other provisions of this clause 4.9.3. Minors under the age of 10 years cannot be authorised to operate the Account.

• a Minor who has been given authority to operate the Account can, if the Account operating authority specifies ‘only one to sign’, unilaterally change the Account operating authority, appoint a Third Party Operator(s) and/or remove any Third Party Operator’s authority to operate the Account.

• we do not recommend the provision of Internet Banking access to Minors. However, Internet Banking access may be provided to a Minor aged 10 years or older with the express, consent of the Third Party Operator(s) given in accordance with an Account operating authority.

12

4.9.4 Accounts opened for Minors aged 13 years and over (at time of Account opening):

• the Account may be opened by a parent(s), legal guardian(s) or other adult(s) on behalf of the Minor. If it is, clause 4.9.3 will apply to the Account, except for the first bullet point.

• the Account may be opened by the Minor independently and without permission from any parent, legal guardian or other adult. If it is, the following provisions of this clause 4.9.4 will apply to the Account.

• subject to the other terms and conditions applying to the Account, a Minor will have unrestricted rights to operate the Account if the Account is in the Minor’s sole name and in accordance with the Account operating authority in the case of a Joint Account.

• a Minor may authorise, unilaterally if the Account is in the Minor’s sole name or in accordance with the Account operating authority in the case of a Joint Account, one or more Third Party Operators to operate the Account in writing in a form we approve. A Minor may, unilaterally if the Account is in the Minor’s sole name or in accordance with the Account operating authority in the case of a Joint Account, change the Account operating authority and/or remove any Third Party Operator’s authority to operate the Account.

• Internet Banking access by the Minor will be permitted.

4.9.5 Whether an Account is opened under clause 4.9.3 or the first bullet point of 4.9.4, the Minor will, upon attaining 18 years of age, obtain unrestricted access to the Account (including the right to remove any Third Party Operators) without the consent of any Third Party Operator(s).

4.9.6 A Third Party Operator must be an adult.

4.9.7 We will only open an Account at the independent request of a Minor, or grant Account access to a Minor at the request of a Third Party Operator(s), where the Minor is able to register a consistent specimen signature to our satisfaction.

4.9.8 We reserve the right to decline to open an Account for a Minor, or to grant Account access to a Minor at the request of a Third Party Operator(s), if we consider it reasonably necessary to decline in order to protect our interests, those of an Accountholder or those of a Minor.

4.9.9 We reserve the right to remove a Third Party Operator, restrict the ability of a Third Party Operator to operate on the Account of a Minor or otherwise change the Account operating authority of the Account of a Minor where we consider it reasonably necessary to do so in order to protect our interests, those of an Accountholder or those of the Minor.

4.9.10 In relation to an Account with a Minor Accountholder, each joint Accountholder who isn’t a Minor and each Third Party Operator on the Account agrees to indemnify us and keep us indemnified against all claims (including any claim made by the Minor), obligations, liabilities, expenses, losses, damages and costs that we may sustain or incur as a result of any transaction carried out on the Account while they are a joint Accountholder who isn’t a Minor or Third Party Operator (even if they are no longer a joint Accountholder or Third Party Operator at the time indemnity is sought) by:

• them

13

• a Minor;

• any joint Accountholder; and/or

• any Third Party Operator on the Account.

4.9.11 The indemnity in 4.9.10 does not require a joint Accountholder or Third party Operator to indemnify us for any claims, obligations, liabilities, expenses, losses, damages or costs to the extent they arise from any fraud, negligence or wilful misconduct by us or our officers, employees, contractors or agents

4.9.12 For the avoidance of doubt, any credit balance in a Minor’s Account is at all times the property of the Minor in the case of an Account in the sole name of a Minor and is the joint property of all the Accountholders (including each Minor) in the case of a Joint Account.

4.10 Trust Accounts

4.10.1 You can open an Account as a trust Account. However:

• We are not taken to be aware of the terms of the trust;

• We do not have to verify that any transactions you carry out on the Account are authorised by the terms of the trust.

4.10.2 You agree to indemnify us against any claim made upon us in relation to, or arising out of, that trust.

4.11 Third Party Operators

4.11.1 You may nominate another person or persons to operate your Account (a “Third Party Operator”) by completing the relevant form, available at any of our branches. Third Party Operators may be required to provide proof of identity as explained in clause 4.3.

4.11.2 By authorising a Third Party Operator to have access to your Account you are instructing us to allow the persons nominated to operate on your Account, without necessarily becoming a Member, in the following ways (please refer to table):

Third Party Operator to a

Non-Minor

Third Party Operator to

a Minor

Third Party Operator to

Business

Create a new Term Investment (excludes reinvesting to a new term) X 3 3

Give instructions as to where interest is to be paid on a Term Investment

3 3 3

Reinvest and add additional deposits to Term Investment 3 3 3

Term Investment Redemptions X 3 3

Obtain statements of the Account 3 3 3

Change personal details of the Account owner X 3 3

Open or close an Account or Membership X 3 3

Authorise another person to be a third party operator on the Account. X 3 3

14

4.11.3 You are responsible for all transactions your Third Party Operator carries out on your Account. You should ensure the person you authorise to operate on your Account(s) is a person you trust fully.

4.11.4 You may revoke the Third Party Operator’s authority at any time by giving us written notice.

4.11.5 We will comply with any notice given to us to revoke the Third Party Operator’s authority within 48 hours of receiving the request.

4.11.6 We will not be liable for any transaction completed or purported to be completed (including any deductions from your Account) by a Third Party Operator prior to the expiry of the period set out in clause 4.11.5.

4.11.7 We are not liable for any loss or damage caused to you by Third Party Operators except where it arises from fraudulent or negligent conduct by our agent or employee or if we are liable under a statute or the ePayments Code.

4.12 Deposits

4.12.1 Deposits may be made to open the Account, or added to your Account balance at renewal, by any of the following methods, unless otherwise indicated in the Summary of Term Investment Accounts Table:

• By cash or cheque at any branch (please see clause 4.13 for more details regarding cheque deposits); or

• By transfer from another Account with us.

4.12.2 Under Australian law we are required to report all cash deposits or withdrawals of $10,000 or more.

4.12.3 We may refuse to accept any cheque for deposit at our absolute discretion.

4.12.4 You may not deposit additional funds into a Term Investment Account at any time during the term of the investment. However, upon maturity of a Term Investment Account you may deposit additional funds at any time during the Grace Period. There is no minimum required amount for additional deposits.

4.13 Cheque Deposits

4.13.1 You can only access the proceeds of a cheque when it has cleared. This usually takes three Business Days. The drawing bank has a right to request an additional day’s clearance. Overseas cheques of $10,000 or less may take up to 30 Business Days to clear, and overseas cheques of above $10,000 are cleared upon receipt of payment confirmation from the third party service provider we use to present the cheque.

4.13.2 Cheques deposited at a branch can normally only be deposited into the Account of the person or entity named as payee on the cheque. If you are depositing a cheque to your Account where you are not the person or entity named, ownership of the cheque must be transferred to you by having the payee sign the back of the cheque in the following manner:

Please pay [your Account name], signed [payee’s signature]. If we are not satisfied you are the rightful owner of the cheque (for any reason), in our sole discretion we may refuse to accept the deposit.

15

4.14 Withdrawals

4.14.1 You may make a partial withdrawal of funds from your Term Investment Account once during the term of the investment, annually if the term of the investment is greater than one year or within the Grace Period, provided that you withdraw a minimum of $1,000, or if your balance is less than $1,000, withdraw all funds from your Term Investment Account. If you need to withdraw further funds from your Term Investment Account during the remainder of the term where the term of the Investment is one year or less, or within the same annual period for terms greater than one year, you will be required to withdraw all funds from and close your Term Investment Account.

4.14.2 If you withdraw all or part of your funds from the Term Investment Account prior to maturity (Early Redemption), we may charge you an Early Redemption fee. Please refer to Term Investment Fees & Charges within this document. You must give us not less than thirty one (31) days notice if you wish to make an Early Redemption. In our discretion, we may waive this notice period in the event you are experiencing financial difficulty.

4.14.3 If a partial withdrawal during the term of the investment or within the Grace Period would cause the balance of your Term Investment Account to fall below the minimum balance required, you must redeem the Term Investment Account in full.

4.14.4 If you redeem your Term Investment in full and it is your only Account you will also have to resign your Membership, in which case you will be refunded your $2.00 share. Resigning your Membership must be in writing with your signature.

4.14.5 If you make a partial Early Redemption, the term and interest rate applicable to the Term Investment Account will continue.

4.15 Maturity of Term Investment Accounts

4.15.1 Prior to the end of your term for a Term Investment Account, you will receive a written notice from us advising you of your investment maturity date.

4.15.2 You must advise us of your requirements prior to expiry of the Grace Period. If we do not hear from you before expiry of the Grace Period, your funds will be automatically reinvested for the same term at the prevailing rate.

4.15.3 If your investment is automatically renewed and you wish to withdraw the funds prior to the new maturity date, the withdrawal will be treated as an Early Redemption as explained in clause 4.14.1.

415.4 If you perform a full redemption during the Grace Period, we will not pay you any interest for the Grace Period including the maturity date.

4.16 Corporate Cheques

4.16.1 You may request us to issue a corporate cheque, payable to the person you nominate, for a fee, as explained in the “Fees & Charges” document. A corporate cheque is similar to a bank cheque, but may not be treated as such by all third parties. A bank cheque can be organised for an additional charge. Please refer to the “Fees & Charges” document for applicable fees.

4.16.2 If a corporate cheque is lost or stolen, you can ask us to stop payment on it. You will need to complete a form giving us evidence of the loss or theft of the cheque. You will also have to give us an indemnity – the indemnity protects us if someone else claims that you wrongfully directed us to stop the cheque.

16

4.16.3 We cannot stop payment on our corporate cheque if you used the cheque to buy goods or services and you are not happy with them. We are not responsible for any defects with goods or services you buy with our corporate cheque. You acknowledge that all complaints about goods and services must be addressed to the relevant supplier of those goods and services.

4.17 Member Access Password (MAP)

4.17.1 You may give us a password that we may accept as proof of your identity and your authority to carry out transactions on your Accounts.

Use

4.17.2 Your MAP may be used by us to establish your identity for certain dealings and transactions with us.

4.17.3 We will tell you from time to time the type of dealings and transactions in which we will accept your MAP to establish the identification of the person we are dealing with.

4.17.4 We reserve the right to not register a particular MAP at our absolute discretion (ie, if we consider it to be offensive).

Reliability

4.17.5 If we state that we accept MAP for a certain service or transaction to establish identity, if your MAP is given to us for that service or transaction, we may accept your MAP as conclusively establishing your identity. We do not need to undertake any other checks to verify your identity.

Security

4.17.6 You must not disclose your MAP to anyone (other than an authorised People’s Choice Credit Union representative).

4.17.7 You must tell us as soon as you think someone else knows your MAP or has used it without your consent. You should immediately reset your MAP.

4.17.8 We suggest you memorise your MAP.

4.17.9 We may cancel your MAP at any time without notice for security reasons.

4.17.10 You must not write your MAP, or carry it or keep a record of it, unless you have taken reasonable steps to disguise your MAP or prevent unauthorised access to your MAP.

4.17.11 You must not select a MAP that represents your birth date or a recognisable part of your name.

4.17.12 If you no longer wish to use your MAP, you can either write or telephone us and request that your MAP be cancelled.

Responsibility and Liability

4.17.13 Except where (and until) your MAP is cancelled by us or by you, or you have notified us that some unauthorised person may be using your MAP:

(a) We are not liable to you for any loss you suffer through unauthorised use of your MAP;

(b) You must pay us any loss we incur as a result of your use of or any unauthorised use by a third party of your MAP.

4.17.14 You must also indemnify us against any loss or damage we may suffer due to any claim, demand or action of any kind brought against us arising directly or indirectly because you did not comply with your obligations under “Security” above.

17

4.17.15 We are liable for any loss you incur because of a transaction after you or we cancel your MAP and where the loss is as a result of our fraud or negligence or that of our employees or agents.

4.17.16 Despite any of the above provisions, if you use your MAP as part of conducting an EFT Transaction (as defined in our Accounts & Access Facilities Terms & Conditions document), responsibility (and liability) is determined under our EFT Conditions of Use (refer your Accounts & Access Facilities Terms & Conditions document).

Cancellation

4.17.17 We may at any time without notice cancel your ability to use your MAP if we suspect you or someone else may use it inappropriately or in a fraudulent manner.

4.17.18 You may cancel your MAP, or notify us if you suspect someone else is using it without authorisation, at any time by sending us written notice or phoning us on 13 11 82.

4.18 Account Statements

4.18.1 We will provide you a statement of Account at the frequency stated in the Summary of Term Investment Accounts Table.

4.18.2 We may, at our discretion, send you Account statements more frequently. If you request to have an Account statement provided to you more frequently or if you ask us for an Account statement at any time, we may charge the fee applying from time to time as outlined in the Fees & Charges section.

eStatements

4.18.3 We may give you Account statements electronically (eStatements) for all Accounts you hold with us if:

• We have notified you that we will give Account Statements to you electronically, or you register to use Internet Banking on or after 1 August 2014 and you have not elected to receive statements by post instead of eStatements (refer to clause 4.18.9);

• You hold a Zip Account (as it is a condition of holding a Zip Account that you must receive eStatements). If you hold a Zip Account and no longer wish to receive eStatements, you will be required to either switch your Zip Account to an alternative Account which enables you to receive paper statements or close your Zip Account or;

• You are a Third Party Operator on a business account. A paper statement may continue to be produced on the Business Membership in addition to the eStatement;

Unless we are legally required to give them to you in another way.

4.18.4 We will notify you when a new eStatement is available. You must use Internet Banking to view your eStatements.

4.18.5 If we give your Account statements electronically, you will not receive paper statements by post and you will also receive other information about your Accounts and Access Facilities, such as notices about changes in rates, fees, and terms and conditions, electronically where the information is given as ‘messages’ within your statement or alongside your eStatement, in a downloadable form.

4.18.6 Unless you have elected to receive paper Account statements by post, you must regularly check for notifications from us that a new eStatement is available. You should check your eStatement as soon as it is available.

18

4.18.7 You must ensure we have your current details such as email address , mobile phone number etc. unless you have elected to receive paper Account statements by post. If we become aware that your details are invalid and we are unable to notify you when a new eStatement is available, we may send you paper statements by post until such time as your details are updated. If you change your details, let us know immediately. You can notify us of a change to your email address using Internet Banking or by contacting us.

4.18.8 Your eStatements and other information will be available to view using Internet Banking for 12 months. You can print or save your eStatements and other information provided with your eStatements during this period. You may request a paper copy of any eStatement to be sent to you by post up to six months after you receive notification the eStatement is available. A fee may be charged if you request a replacement paper statement.

4.18.9 If you do not wish to receive Account Statements and other information provided with Account statements electronically, you may elect to receive paper Account statements by post by contacting us or using Internet Banking. If you decide to receive paper Account statements by post you will no longer be able to view your previous eStatements using Internet Banking. You should print or save a copy of your eStatements before requesting to receive paper Account statements by post.

4.18.10 Accountholders and Third Party Operators that have elected to receive Account statements by post cannot access eStatements for both personal and non-personal Membership Accounts via Internet Banking.

4.19 Change of Address

If you change your address or contact details, including email, please let us know immediately.

4.20 Account Combination

4.20.1 If you are in default under or breach any term of any agreement with us (including these Terms & Conditions) or you are not using your Accounts in accordance with the rules that apply to them, despite any other agreement between us we may without prior notice to you:

• combine the balances of any of your Accounts; or

• apply any credit balance or available funds in any of your Accounts, or any amount we otherwise may owe you, towards satisfying any amount that you owe us, in any order we choose;

4.20.2 This provision applies to all amounts, whether due or not or due contingently. This provision does not apply to formal trust Accounts.

4.21 Closing Accounts

4.21.1 We can close any Account in our absolute discretion by giving you at least 14 days written notice at the last address provided and paying you the balance of your Account.

4.21.2 If you are closing your only Account and you have no other deposit accounts or loans with us you will also have to resign your Membership, in which case you will be refunded your $2.00 share. Resigning a membership must be in writing with your signature.

4.21.3 If you do not abide by the terms and conditions applicable to an Account, we reserve the right to swap your account to an alternative Account type or close your Account as per clause 14.21.1 above.

19

4.22 Changes to Terms & Conditions

4.22.1 We may change these Terms & Conditions and any fees, charges, interest rates and other information at any time. The Notification of Change Table sets out whether we are required to give you advance notice of a change and how we may notify you of any change.

4.22.2 We are not obliged to give you advance notice if a change will result in a reduction in your obligations, if the change is necessary to restore or maintain the security of our systems or an Access Facility, or if the change is required to comply with our legal obligations.

4.22.3 Notification of Change Table

Type of change Notice we must give

Manner of giving notice

a) increasing any fee or charge 30 days See clause 4.23

b) adding a new fee or charge 30 days See clause 4.23

c) changing the method by which interest is calculated 20 days See clause 4.23

d) changing the frequency with which interest is credited 20 daysSee clause 4.23 or notice in a newspaper

e) changing interest rates (other than interest rates linked to money market rates or some external reference rate) day of change

See clause 4.23 or notice in a newspaper

f) changing any other term or condition 30 daysSee clause 4.23 or notice in a newspaper

4.23 Notices and Electronic Communication

4.23.1 We may give you information and notices (each a ‘communication’) in any way the law allows us to. This includes by:

• post, to your address recorded in our membership records or to a mailing address you have given us;

• if you are a registered Internet Banking user, notification or message sent to you within Internet Banking;

• if you have downloaded one of our Mobile Banking apps, notification or message sent to you in the app;

• email; or

• SMS.

4.23.2 We may also give you a communication by making it available electronically (for example, by publishing it on our website) and notifying you that we have done so and how you can obtain the communication. However, we will not give you a communication in this way if you have notified us that you do not want to receive communications from us in this way. You can notify us that you do not want to receive communications from us in this way by contacting us. Unless you have elected to receive paper Account statements by post, you may still receive communications from us electronically

20

where we include the communication in or with an Account statement which is given to you as an eStatement (see clause 4.18 for more information about eStatements).

4.23.3 You must promptly notify us of any changes to your contact details and ensure the contact details we have for you are always current and correct.

5. Complaints 5.1 Internal Dispute Resolution Process

5.1.1 We have a dispute resolution policy to deal with any complaints you may have in relation to our financial services or us. Our dispute resolution policy requires us to deal with any complaint in an efficient manner.

5.1.2 If you want to make a complaint, contact us and indicate you would like to make a complaint or visit our Website. Our staff must advise you of our complaint handling process and the expected time frame for handling your complaint (“Internal Dispute Resolution Process”)

5.2 External Dispute Resolution Process

5.2.1 If you are not satisfied with the outcome of our Internal Dispute Resolution Process or if we are not able to resolve your complaint to your satisfaction within 45 days, then you may escalate your complaint in accordance with clauses 5.2.2 and 5.2.3 below.

5.2.2 If your complaint relates to a breach of the Customer Owned Banking Code of Practice and you have not suffered loss or detriment, you can report it to the Compliance Manager of the Code Compliance Committee on local call: 1300 780 808.

5.2.3 For all other complaints, you may refer the matter to the Australian Financial Complaints Authority (AFCA):

Australian Financial Complaints Authority, GPO Box 3, Melbourne VIC 3001

Free call: 1800 931 678

Email: [email protected]

6. Financial Claims Scheme 6.1 The Financial Claims Scheme (FCS) is an Australian Government scheme that provides protection to deposits in banks, building societies and credit unions in the unlikely event that one of these financial institutions fails. The FCS can only come into effect if it is activated by the Australian Government. Under the FCS, deposits are protected up to a limit of $250,000 for each account holder. The FCS limit of $250,000 is applied to the combined amount of deposits for each account holder. For joint accounts, deposits are shared equally between the account holders.

For more information visit www.fcs.gov.au or phone the APRA hotline on 1300 558 849.

21

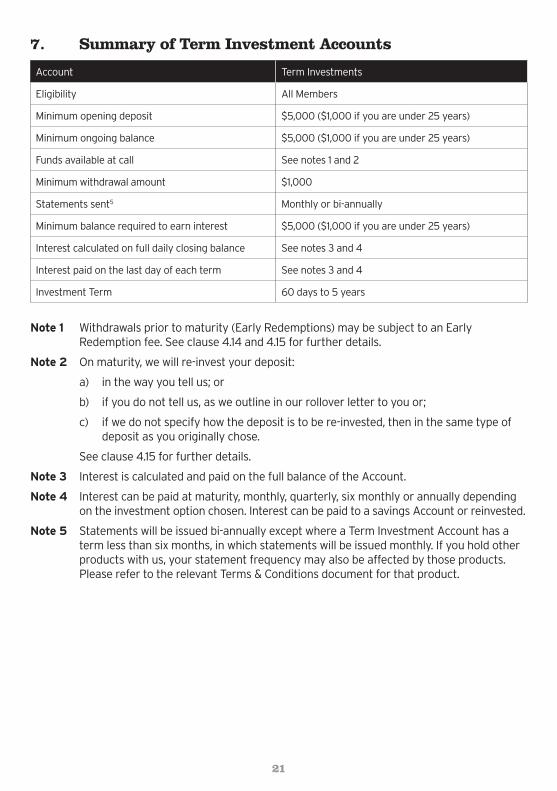

7. Summary of Term Investment Accounts

Account Term Investments

Eligibility All Members

Minimum opening deposit $5,000 ($1,000 if you are under 25 years)

Minimum ongoing balance $5,000 ($1,000 if you are under 25 years)

Funds available at call See notes 1 and 2

Minimum withdrawal amount $1,000

Statements sent5 Monthly or bi-annually

Minimum balance required to earn interest $5,000 ($1,000 if you are under 25 years)

Interest calculated on full daily closing balance See notes 3 and 4

Interest paid on the last day of each term See notes 3 and 4

Investment Term 60 days to 5 years

Note 1 Withdrawals prior to maturity (Early Redemptions) may be subject to an Early Redemption fee. See clause 4.14 and 4.15 for further details.

Note 2 On maturity, we will re-invest your deposit:

a) in the way you tell us; or

b) if you do not tell us, as we outline in our rollover letter to you or;

c) if we do not specify how the deposit is to be re-invested, then in the same type of deposit as you originally chose.

See clause 4.15 for further details.

Note 3 Interest is calculated and paid on the full balance of the Account.

Note 4 Interest can be paid at maturity, monthly, quarterly, six monthly or annually depending on the investment option chosen. Interest can be paid to a savings Account or reinvested.

Note 5 Statements will be issued bi-annually except where a Term Investment Account has a term less than six months, in which statements will be issued monthly. If you hold other products with us, your statement frequency may also be affected by those products. Please refer to the relevant Terms & Conditions document for that product.

22

8. Term Investment Fees & Charges The following fees and charges are payable in relation to Term Investment Accounts. We may debit the fees and charges to your Account when they become payable.

Early Redemption Fee

In the instance of an early withdrawal or redemption of your Term Investment Account, you will be required to pay an Early Redemption Administration Fee of $30.00 and the interest otherwise payable on the amount withdrawn from the Term Investment Account will be reduced. The amount by which the interest will be reduced is set out below and will depend on the percentage of the term that has elapsed as at the date of the withdrawal of funds from the Term Investment.

% through the term Interest otherwise payable on the withdrawn amount is reduced by

Less than 20% 80%

20% to less than 40% 60%

40% to less than 60% 40%

60% to less than 80% 20%

80% and over 10%

The Early Redemption Administration Fee will not be payable to the extent that the fee exceeds the interest payable on the withdrawn amount, this means that in some cases this fee may only be charged partially or not at all.

Service Fees Related to Term Investments

Company and Business Name Verification

Company and Business Name Search… ...................................................................................................$20.00

Applies to each Company or Business Name Search completed.

General

Documentation Requests .................................................................................................$15.00 per 15 minutes

Applies when you request that we provide copies of documentation held by People’s Choice Credit Union for Accounting or Audit requests or requests for information under the Privacy Act.

Signature Verification… .................................................................................................…$5.00 per verification

Applies when you request to withdraw funds without sufficient identification.

Statement Fees

Duplicate/replacement Statement… ..............................................................................$10.00 per statement

Applies when you request us to provide a copy of a statement that has already been issued (including where you request a paper copy of an eStatement). Charged at the time the statement is requested.

Replacement Interest Statement ....................................................................$10.00 per interest summary

Applies when you request us to provide a copy of an interest statement that has already been issued. Charged at the time the statement is requested.

23

Frequent Statement Fee .................................................................................$2.00 per additional statement

This fee applies to members who request a statement more regularly than the statement cycle specified in the Summary of Term Investment Accounts table in Chapter 7. Excludes eStatements, which are free of charge.

24

People’s Choice Credit Union, a trading name of Australian Central Credit Union Ltd ABN 11 087 651 125, acts under its own Australian Financial Services Licence 244310 and Australian Credit Licence 244310. BRC 8.6.148 V3.1-0320

How to contact usYou can contact us in any of the following ways:

• T 13 11 82

• F 1300 365 775

• peopleschoicecu.com.au

• In person at any of our branches

• Post to People’s Choice Credit Union

GPO Box 1942, Adelaide S.A. 5001