Telecoms, Media & Technology abc -...

36

abc Global Research LED adoption in headlights to take off, doubling global auto LED sales by 2015 Korean, Taiwanese LED makers to gain; auto OP could surpass LCD BLU by 2015 Raise TPs of Epistar, Everlight and Seoul Semi; 2014 a good year for LED pricing The LED auto lighting market is set to grow 25-35% in 2014-15 as LED adoption in headlights rises to 12-15% of units (from less than 2% now). As LED headlight requires a substantial amount of LED, global auto LED revenue is likely to roughly double by 2015. Auto lighting is by far the most profitable of all applications for LED players, given the high entry barrier and long product life cycle. Industry structure favours LED adoption. Although the auto lighting market is only 25-30% the size of the global general lighting industry, market share is concentrated among a few top players (whereas general lighting is much more fragmented); this implies that adoption rates could surge rapidly, as relatively few decision makers are involved. Even entry-level vehicles, such as Toyota Corolla, are starting to adopt LED headlights, and we expect many to follow. Korean and Taiwanese LED makers stand to benefit from outsourcing by top LED makers and direct cooperation with global auto lighting suppliers. Although auto LED accounts for only 4% of sales in 2013e, we believe it could surpass LCD BLU in terms of operating profit contribution by 2015 and be on a par with general lighting by 2018, as margins are 20ppt+ higher than for general lighting. We raise our TP for Epistar to TWD76, for Everlight to TWD63, and for Seoul Semi to KRW39,000 (from TWD74, TWD56, KRW32,000) but keep it at KRW113,000 for LG Innotek. We reiterate our OW rating on Epistar, Everlight and LGI, but keep Seoul Semi at UW as we think positives are already priced in. Rising lighting and auto lighting demand should lead to a favourable pricing environment in 2014 while capacity additions should remain disciplined. Telecoms, Media & Technology Electronic Equipment Asia LED Auto lighting the next big driver 3 October 2013 Jerry Tsai* Analyst HSBC Securities (Taiwan) Corporation Limited +8862 6631 2863 [email protected] Brian Sohn* Analyst The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch +822 3706 8765 [email protected] Louis Cheng* Associate HSBC Securities (Taiwan) Corporation Limited +8862 6631 2865 [email protected] View HSBC Global Research at: http://www.research.hsbc.com *Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations Issuer of report: HSBC Securities (Taiwan) Corporation Limited Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of i t Financial and valuation summary Local TP HSBC ‘‘13e EPS _ ‘‘14e EPS _ ‘‘14e BVPS _ Target PB __ Company curr new/old rating New Old New Old New Old New Old Epistar TWD 76 / 74 OW 1.36 1.76 3.37 3.13 54.0 53.9 1.4x 2014e 1.4x 2H13e/ 1H14e Everlight TWD 63 / 56 OW 3.63 3.17 4.12 3.63 39.6 39.0 1.6x 2014e 1.4x 2H13e/ 1H14e LG Innotek KRW 113,000 OW 2,526 2,526 6,058 6,058 71,477 71,477 1.6x 2014e 1.6x 2014e Seoul Semi KRW 39,000 / 32,000 UW 1,083 1,079 1,619 1,291 12,806 11,332 3.0x 2014e 2.6x 2014e Aixtron † EUR 12.7 N(V) -0.94 -0.94 0.09 0.09 3.81 3.81 3.25x 2014e 3.25x 2014e † Covered by Christian Rath Key: OW = Overweight; UW = Underweight; N(V) = Neutral (Volatile) Source: HSBC estimates Financial and valuation summary Company Bloomberg ___ PE (x) ____ ___ PB (x) ____ __ ROE (%)___ ticker 2013e 2014e 2013e 2014e 2013e 2014e Epistar 2448 TT 41.2 16.7 1.1 1.0 2.7 6.4 Everlight 2393 TT 14.9 13.2 1.4 1.4 9.9 10.6 LG Innotek 011070 KS 35.0 14.6 1.4 1.2 3.9 8.9 Seoul Semi 046890 KS 38.4 25.7 3.7 3.2 10.0 13.4 Source: HSBC estimates

Transcript of Telecoms, Media & Technology abc -...

abcGlobal Research

LED adoption in headlights to take off,

doubling global auto LED sales by 2015

Korean, Taiwanese LED makers to gain; auto OP could surpass LCD BLU by 2015

Raise TPs of Epistar, Everlight and Seoul Semi; 2014 a good year for LED pricing

The LED auto lighting market is set to grow 25-35% in

2014-15 as LED adoption in headlights rises to 12-15% of

units (from less than 2% now). As LED headlight requires a

substantial amount of LED, global auto LED revenue is

likely to roughly double by 2015. Auto lighting is by far the

most profitable of all applications for LED players, given the

high entry barrier and long product life cycle.

Industry structure favours LED adoption. Although the

auto lighting market is only 25-30% the size of the global

general lighting industry, market share is concentrated

among a few top players (whereas general lighting is much

more fragmented); this implies that adoption rates could

surge rapidly, as relatively few decision makers are involved.

Even entry-level vehicles, such as Toyota Corolla, are starting

to adopt LED headlights, and we expect many to follow.

Korean and Taiwanese LED makers stand to benefit from

outsourcing by top LED makers and direct cooperation with

global auto lighting suppliers. Although auto LED accounts

for only 4% of sales in 2013e, we believe it could surpass

LCD BLU in terms of operating profit contribution by

2015 and be on a par with general lighting by 2018, as

margins are 20ppt+ higher than for general lighting.

We raise our TP for Epistar to TWD76, for Everlight to

TWD63, and for Seoul Semi to KRW39,000 (from TWD74,

TWD56, KRW32,000) but keep it at KRW113,000 for LG

Innotek. We reiterate our OW rating on Epistar, Everlight

and LGI, but keep Seoul Semi at UW as we think positives

are already priced in. Rising lighting and auto lighting demand

should lead to a favourable pricing environment in 2014

while capacity additions should remain disciplined.

Telecoms, Media & Technology Electronic Equipment

Asia LED

Auto lighting the next big driver

3 October 2013 Jerry Tsai* Analyst HSBC Securities (Taiwan) Corporation Limited +8862 6631 2863 [email protected]

Brian Sohn* Analyst The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch +822 3706 8765 [email protected]

Louis Cheng* Associate HSBC Securities (Taiwan) Corporation Limited +8862 6631 2865 [email protected]

View HSBC Global Research at: http://www.research.hsbc.com

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations

Issuer of report: HSBC Securities (Taiwan) Corporation Limited

Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

Financial and valuation summary

Local TP HSBC ‘‘13e EPS _ ‘‘14e EPS _ ‘‘14e BVPS _ Target PB __ Company curr new/old rating New Old New Old New Old New Old

Epistar TWD 76 / 74 OW 1.36 1.76 3.37 3.13 54.0 53.9 1.4x 2014e

1.4x 2H13e/1H14e

Everlight TWD 63 / 56 OW 3.63 3.17 4.12 3.63 39.6 39.0 1.6x 2014e

1.4x 2H13e/1H14e

LG Innotek

KRW 113,000 OW 2,526 2,526 6,058 6,058 71,477 71,477 1.6x 2014e

1.6x 2014e

Seoul Semi

KRW 39,000 / 32,000

UW 1,083 1,079 1,619 1,291 12,806 11,332 3.0x 2014e

2.6x 2014e

Aixtron† EUR 12.7 N(V) -0.94 -0.94 0.09 0.09 3.81 3.81 3.25x 2014e

3.25x 2014e

†Covered by Christian Rath Key: OW = Overweight; UW = Underweight; N(V) = Neutral (Volatile) Source: HSBC estimates

Financial and valuation summary

Company Bloomberg ___ PE (x) ____ ___ PB (x) ____ __ ROE (%)___ ticker 2013e 2014e 2013e 2014e 2013e 2014e

Epistar 2448 TT 41.2 16.7 1.1 1.0 2.7 6.4Everlight 2393 TT 14.9 13.2 1.4 1.4 9.9 10.6LG Innotek 011070 KS 35.0 14.6 1.4 1.2 3.9 8.9Seoul Semi 046890 KS 38.4 25.7 3.7 3.2 10.0 13.4

Source: HSBC estimates

2

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Global LCD TV panel, general lighting and auto lighting market sizes and top 8 player market shares

Global auto lighting revenue – LED versus non-LED

*LCD TV revenue refers only to panel portion; however, the top-8 rev refers to TV brands, which were the key decision makers driving the migration to LED

Source: HSBC estimates

Source: HSBC estimates

Gross margin comparison: auto LED the highest by far LED chip utilisation rate outlook positive

Source: HSBC Source: HSBC estimates

Asia LED operating profit breakdown by segment –-Auto could overtake BLU in 2015

Source: HSBC estimates

0

22

44

66

88

LCD TV PNL Lighting Auto lighting

Top 8 rev Outside top 8

(USDbn)

0

9

18

27

36

2001 2003 2005 2007 2009 2011 2013e 2015e

Non-LED auto-lighting revenue (USDbn) LED auto-lighting revenue(USDbn)

(USDbn)

0% 14% 28% 42% 56%

BLU

Lighting

Automotive 40-50%

20-30%

15-25%

GM (%)

Avg. opex of sales14.5%

0%

25%

50%

75%

100%

1Q09 4Q09 3Q10 2Q11 1Q12 4Q12 3Q13 2Q14

(%)

80%

0%

25%

50%

75%

100%

2013 2014 2015 2016 2017 2018

Auto lighting BLU Lighting Mobile Others

(%)

3

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

LED auto lighting is set to grow 25-35% in 2014-15 30% the size of general lighting, but a much more addressable opportunity

We believe the next major catalyst for global LED

demand is automotive lighting, which has been

met by LCD backlight and general lighting in

recent years. We expect this to drive sales growth

and, even more, to boost operating profit for the

leading Taiwanese and Korean LED makers

beginning in 2014.

While the USD26bn market is around 25-30% the

size of general lighting business, its concentrated

industry structure means adoption could be much

faster once the critical point is reached.

Global automotive lighting is controlled by a

handful of players: the top eight makers have a

combined global share of their segment more than

80% versus just 40% for the top 8 players in the

global lighting market.

We believe this high concentration is the reason

why LED penetration in TV jumped from

low-single-digit levels in 2009 to 80%-plus

(in 2012) in three years. The top eight TV brands

account for 65% of global shares (the concentration

is even higher if we consider panel makers) and the

decision on migration to new technology is

controlled by a few players.

Next major wave of LED adoption imminent

LED auto headlight adoption has been low (less than 2%), but

should take off soon thanks to an aggressive push by auto lighting

and automobile makers

LED dollar content in auto lighting is high and offers the best

margin due to high barriers to entry and long product life

We expect LED auto lighting to grow 25-35% in 2014-15; industry

concentration means adoption levels could surge

Global LCD TV panel, lighting and auto lighting market size and top 8 player market shares

*LCD TV revenue refers only to panel portion; however, the top-8 rev refers to TV brands, which were the key decision makers driving the migration to LED Source: HSBC estimates

0

22

44

66

88

LCD TV PNL Lighting Auto lighting

Top 8 rev Outside top 8

(USDbn)

4

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

The global lighting market is massive, but the tail

is very long, as lighting is a highly localised

business. We therefore believe automobile mobile

lighting could offer much more addressable

opportunities for LED makers, as each customer

and order win could have a much greater impact.

LED penetration within LED TV

Source: DisplaySearch, HSBC

Dollar content is high; ASP erosion likely the least among all applications

The price of LED is on a consistent downward

trend. Nevertheless, ASP erosion is less marked

for automotive lighting than for the other major

applications, owing to more favourable pricing

factors. While LED prices are typically declining

at rates of 13-20% per year for backlight and

lighting (assuming healthy supply and demand;

the level is much more if not), we expect an ASP

decline for auto lighting LED (especially those

used in headlights) of just 5% per annum.

To ensure consistency of colour and brightness,

clients tend to retain the LED supplier they

originally select for an auto lighting modules

throughout the product’s life. If we combine that

with the 5% ASP pressure and the annual cost

down of LED chip makers (at a rate much higher

than 5% a year), we believe the auto lighting

business is highly lucrative for LED makers.

Meanwhile the LED dollar content of automotive

lighting is high in terms of chip area, as headlight

consumes at least 10x more LED chips than a

typical LED bulb (60w replacement). Moreover,

given the harsh operating environment and

demanding durability standard, the chip is also

more expensive on a like-for-like basis (20-50%

we believe).

0%

22%

44%

66%

88%

1Q09 4Q09 3Q10 2Q11 1Q12 4Q12

(%)

Automotive lighting breakdown

Source: HSBC

LED segment comparison: factor of pricing pressure

Auto lighting Lighting Backlight Implications on pricing pressure/margin

Customization Very high Mid-high Low High customization means lower pricing pressure Product life cycle 2.5-3 yrs 1-1.5 yrs 1 yr Long product life cycle means better marginLED as % of BOM 14-18% 25-35% 10% Lower % suggests lower pricing pressureOperating requirement Very high High limited High requirement means lower pricing pressure

Source: HSBC

5

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Owing to the higher entry barrier we believe

Chinese LED makers have little chance to share

this opportunity. So far, all the LED chips found

on Chinese automobiles have come from

international LED makers. This makes irrational

behaviour in the segment less likely.

Adoption kicking into high gear LED: the next-generation light source for auto headlights

LED is the ideal light source for auto lighting, owing

to its low power consumption, fast switch-on/-off

and durability. However, blended adoption is still

low at around 7%. While the cost premium over

current technologies, such as HID (high intensity

discharge) and halogen plays a part in this, we

believe the conservative nature of the auto

component industry and the stringent certification

process are actually the greatest challenges to LED

adoption. Nevertheless auto lighting suppliers

becoming aggressive, so we expect the migration

will start to accelerate.

LED adoption of automotive lighting*

*Blended is based on lumens; the rest are in units

Source: HSBC estimates

The adoption of LED in rear exterior lighting

(brake, signal, tail light) is already as high as

25% already, but the amount of light needed in

these fixtures is only modest. In our view,

headlight are the truly untapped opportunity for

LED (only 1.5% adoption in 2013), and the

amount of light output required (corresponding

directly to LED usage) is 4-5x the level needed

for exterior lights found on the rear of vehicle.

The current mainstream light source for

headlights on regular vehicles is halogen, while

HID, which is twice as expensive as halogen, now

accounts for 20% of the market (mostly premium

vehicle). We believe LED, which is still more

than twice as expensive as HID, will reach a 12-

15% unit share in auto headlights in the next

three years.

LED to be adopted in headlights

Until very recently, LED headlights were found

only in high-end cars such as Lexus, Mercedes

and Audi. However, we are starting to see them

appearing on regular vehicles. Toyota’s new

Corolla, the best-selling vehicle in the world, will

adopt LED for its low-beam headlight. Meanwhile

Peugeot (308), Ford (Mondeo) and Spain’s SEAT

(Leon) are all making full LED headlights

available – the last two as a standard option.

While the target of a 12-15% share by 2015 may

look aggressive given the current low adoption

rate, we believe it is an achievable goal, as a

tipping point is approaching for new auto

headlight technology and LED cost reduction.

0%

8%

16%

24%

32%

Break light Tail light Parking light Head light Blended

(%)

Global auto lighting revenue – LED versus non-LED

Source: HSBC estimates

0

9

18

27

36

2001 2003 2005 2007 2009 2011 2013e 2015e

Non-LED auto-lighting revenue (USDbn) LED auto-lighting revenue(USDbn)

(USDbn)

6

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

LED auto-lighting revenue breakdown

Source: HSBC estimates

Headlights undergoing a “smart” revolution –

and LED is the best light source

The value-added aspect is boosted by the fact that

major auto lighting makers are aggressively

promoting AFS (advanced front-lighting system),

which allows drivers to leave the high beam on

when driving (thereby extending visibility), but

can make an instantaneous adjustment when

oncoming traffic appears to avoid blinding the

oncoming driver. This plays to one of LED’s

strengths: fast switch-on/-off.

Vast improvement in cost, weight and heat

management

The first LED headlight to be commercially

produced was for the Lexus LS600h in 2007.

However, the cost was extremely high – reportedly

well over USD1,000. This is not attributable so

much to the LED itself – although high, its cost still

dwarfed by the total bill of materials (BOM) – as to

the heat emission from the LED. Lack of scale is

also a factor.

As the LED chips used to be much less efficient,

they previously generated considerable heat

(twice the level they emit today). The current

LED headlight module now uses a less complex

heat management system, which is a key reason

for the weight reduction of more than 60% for the

entire module in the past three to four years. As a

result, the price has come down significantly.

LED lumen per watt rising, reducing heat generation

Source: HSBC

The BOM for LED headlights is now 2-3 times that

of HID/halogen headlights, or less than USD100.

We believe that by 2015 the gap between LED

and HID – the current mainstream for high-end

vehicles – will be around 50%. In absolute terms

it will be less than USD20 on our estimates.

0

4

8

12

16

2001 2003 2005 2007 2009 2011 2013e 2015e

Back lights Daytime running lights Front lights

(USDbn)

0

50

100

150

200

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

(lm/w)

Lighting sources comparison

LED HID Halogen

Introduced 2007 1991 1961 Average life (hrs) 20,000 2,500 1,000

Cost Highest (4-5x) Medium to high (2x)

Lowest (1x)

Ignition time Instant <5 sec reaching

full intensity 15 sec reaching

full intensity Luminous efficacy 80-90 lm/W 60 lm/W 20-25 lm/W Power consumption

Lowest (35%) Medium (55%) High (100%)

Illumination colours Varying whites White-blue Slightly yellow

Source: HSBC

Headlight BOM cost comparison

HID-2013 LED-2013 LED-2015

Whole sale OEM ASP 56.8 120.0 83.0 BOM 41.5 80.0 54.0 Overhead 7.5 14.5 11.5 Labour 7.0 11.5 10.0 Main mechanical 7.0 12.0 8.0 Other mechanical/electrical 4.0 10.0 6.0 Optical/refractor 6.0 8.0 6.0 Heat management 8.0 4.0 light source 10.0 16.0 8.5

Source: HSBC estimates

7

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

LED adoption driven by aggressive push from entire supply chain

We believe players in all segments have strong

incentives for migrating to LED headlight:

Automotive lighting makers

In addition to the higher ASP (2-5x) and margin

(potentially 10-15ppt above regular headlights on

our estimates), LED offers auto lighting suppliers

an opportunity to penetrate new customer bases.

The relationship between automobile makers and

automotive lighting makers is typically stable.

However LED auto lighting, which requires

completely new expertise in the optical design to

maximize the benefit from LED, could alter the

landscape as automobile makers will be keen to

work with new suppliers that have these strengths.

The transition from halogen to HID was less

revolutionary, since HID is still a bulb-based light

source, whereas LED packages will be arranged

as an array in the auto lighting module, giving

more room for design flexibility.

We believe this is why LED headlights are

showcased on the corporate webpages of all major

Japanese and European automotive lighting makers

despite the very small adoption rate to date.

Automakers

LED headlights distinguish the vehicle after dark,

since the LED array can be arranged to show a

unique pattern. The lights on Audi and Mercedes

vehicles have a distinctive look. According to the

JD Power survey in April, LED headlights are the

most desirable new car technology for consumers,

ahead of voice activation and wireless connectivity.

We believe there is also another added benefit: the

light source (HID/halogen bulb) of current

headlights can easily be replaced at local shops

when it fails. Since LED lighting consists of an

array, any repairs are more complex and will

probably have to be conducted at the dealership.

This represents incremental service revenue.

Daytime running light also a key driver

Daytime running light (DRL) was introduced more

than decade ago and we are now seeing a surge in

demand since the EU made this a mandatory feature

on all vehicles sold (February 2011 for passenger;

August 2012 for commercial vehicles). Outside

Europe, more and more auto makers are making

DRL, which has been proven to reduce accidents

by around 20%, a standard feature.

DRL has been a key catalyst for LED demand in

the automobile segment. Although some DRL

uses HID/halogen as a light source, we believe

LED currently accounts for most DRL installed in

new cars, owing to its strengths in the areas of

energy conservation and longevity. Meanwhile

the ASP is among the highest for any lamp type.

DRL shipments

Source: HSBC estimates

Current ASP comparison (blended average)

Source: HSBC estimates

0

23

46

69

92

2001 2003 2005 2007 2009 2011 2013e 2015e

(mn units)

0

8

16

24

32

HeadLight

DRL TailLight

FogLight

ParkingLight

Directionindicator

Brakelight

(USD)

8

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Global automotive lighting model

2008 2009 2010 2011 2012 2013e 2014e 2015e

Global auto-lighting market value (USDm) – Total 23,807 21,954 23,660 24,897 26,047 27,185 29,260 31,809 Head light 8,448 7,740 8,241 8,567 8,892 9,222 10,103 11,635 Tail light 6,193 5,776 6,256 6,610 6,902 7,111 7,363 7,548 Parking light 1,488 1,367 1,459 1,521 1,569 1,612 1,675 1,725 Direction indicator 3,596 3,292 3,502 3,640 3,744 3,905 4,116 4,287 Fog light 1,736 1,594 1,702 1,775 1,830 1,880 1,954 2,012 Brake light 1,770 1,650 1,787 1,888 1,972 2,045 2,132 2,195 Daytime running light 576 535 713 896 1,139 1,410 1,918 2,406 Global auto-lighting market value (USDm) – LED only 3,806 3,849 4,562 5,221 5,994 6,871 8,784 11,832 Head light 347 355 413 462 604 693 1,602 3,710 Tail light 2,037 2,067 2,409 2,714 3,001 3,244 3,496 3,705 Parking light 142 144 168 190 210 234 260 282 Direction indicator 162 164 191 215 238 385 530 661 Fog light 166 168 196 221 245 273 304 329 Brake light 582 591 688 776 857 951 1,047 1,129 Daytime running light 370 359 496 643 839 1,090 1,545 2,014 LED penetration rate by products (%) Head light 0.6% 0.7% 0.8% 0.9% 1.2% 1.6% 4.5% 13.5% Tail light 15.0% 16.9% 18.8% 20.6% 22.5% 25.0% 27.5% 30.0% Parking light 3.7% 4.1% 4.6% 5.0% 5.5% 6.3% 7.2% 8.0% Direction indicator 1.7% 1.9% 2.1% 2.3% 2.5% 4.2% 5.8% 7.5% Fog light 3.7% 4.1% 4.6% 5.0% 5.5% 6.3% 7.2% 8.0% Brake light 15.0% 16.9% 18.8% 20.6% 22.5% 25.7% 28.8% 32.0% Daytime running light 33.3% 37.5% 41.7% 45.8% 50.0% 56.7% 63.3% 70.0% Blended 6.5% 7.4% 8.2% 9.0% 9.9% 11.5% 14.3% 20.4% Global automotive lighting shipments breakdown by products (m units) Head light 334 300 312 318 321 326 329 333 Tail light 483 438 461 474 483 491 504 515 Parking light 238 215 227 233 237 241 248 253 Direction indicator 594 539 569 587 598 608 626 641 Fog light 196 178 188 194 198 202 208 213 Brake light 255 232 245 252 257 262 270 276 Daytime running light 22 20 26 32 40 49 66 83 Total 2,905 2,623 2,736 2,783 2,791 2,797 2,880 2,952

Source: HSBC estimates

9

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

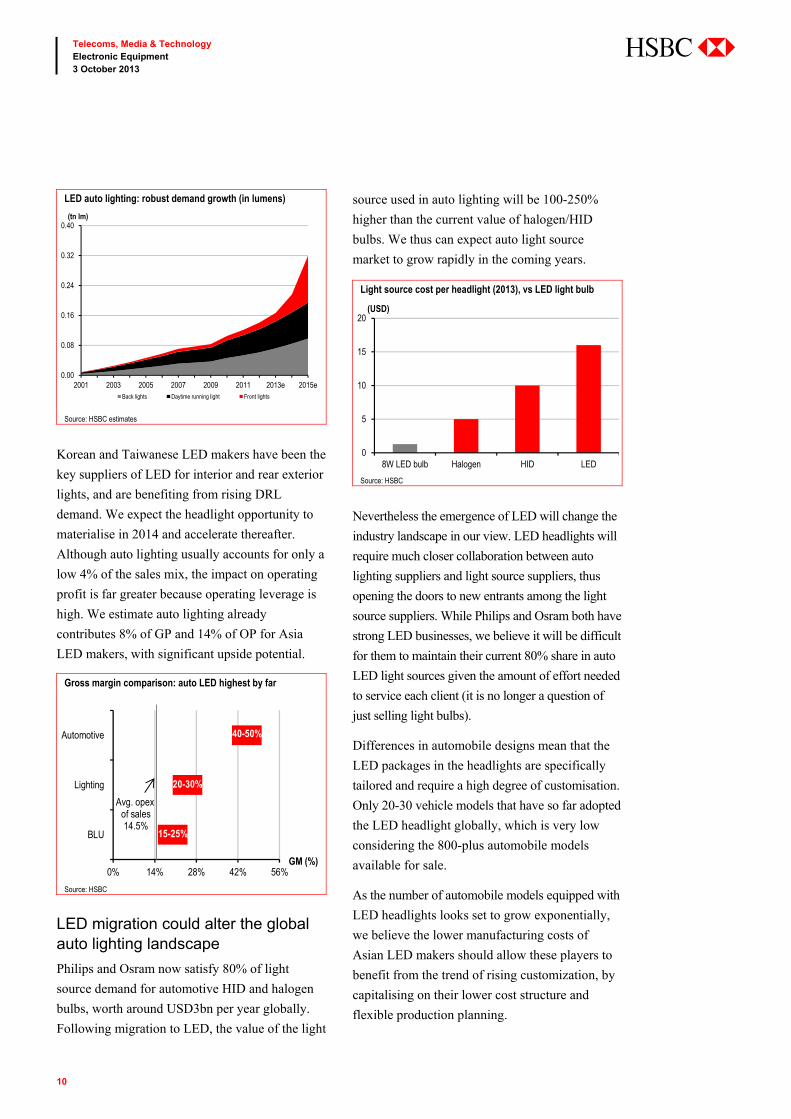

Asia LED makers positioned for outsourcing trend Automotive lighting accounts for about 6-7% of

global LED revenue (at the LED package level),

or USD800-850m. We expect the global auto

LED package revenue to almost double (+85%) in

the next two years, driven by adoption of LED

headlights and DRL.

While the majority of auto lighting LED packages

are supplied by the globally leading Japanese and

European LED makers – notably Nichia, Philips and

Osram (Three of the “Big Five” LED players

globally) – we see outsourcing manufacturing

opportunities for Asian names in the coming years.

The LED capex of most top-tiered LED makers

has been very modest, as many are adopting the

outsourcing model. As global LED chip shipment

still growing at a rate of 20% a year (driven by

rising lighting, while size/pixel migration is

underpinning BLU demand), new incremental

demand from auto segment should create further

supply tightness. We therefore expect outsourcing

orders to benefit Asian LED players.

Small revenue, big profit

The auto LED package market is worth just under USD1bn, but is

set to double by 2015; migration to LED should open doors to new

entrants

Global leaders to increase outsourcing to Asian makers; revenue

contribution is just 4% now, but OP to surpass BLU by 2015, and …

… to be on a par with general lighting by 2017-18 due to 20ppt+

higher margins, high operating leverage, and long product life cycle

Global LED package market value

Source: HSBC estimates

Global LED chip demand for all segments (2010 = 100)

Source: HSBC estimates

0

4

8

12

16

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Others Sign Mobile BLU Lighting Auto

(USDbn)

0

120

240

360

480

2010 2011 2012 2013e 2014e

(index as of 2010)

10

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Korean and Taiwanese LED makers have been the

key suppliers of LED for interior and rear exterior

lights, and are benefiting from rising DRL

demand. We expect the headlight opportunity to

materialise in 2014 and accelerate thereafter.

Although auto lighting usually accounts for only a

low 4% of the sales mix, the impact on operating

profit is far greater because operating leverage is

high. We estimate auto lighting already

contributes 8% of GP and 14% of OP for Asia

LED makers, with significant upside potential.

Gross margin comparison: auto LED highest by far

Source: HSBC

LED migration could alter the global auto lighting landscape

Philips and Osram now satisfy 80% of light

source demand for automotive HID and halogen

bulbs, worth around USD3bn per year globally.

Following migration to LED, the value of the light

source used in auto lighting will be 100-250%

higher than the current value of halogen/HID

bulbs. We thus can expect auto light source

market to grow rapidly in the coming years.

Nevertheless the emergence of LED will change the

industry landscape in our view. LED headlights will

require much closer collaboration between auto

lighting suppliers and light source suppliers, thus

opening the doors to new entrants among the light

source suppliers. While Philips and Osram both have

strong LED businesses, we believe it will be difficult

for them to maintain their current 80% share in auto

LED light sources given the amount of effort needed

to service each client (it is no longer a question of

just selling light bulbs).

Differences in automobile designs mean that the

LED packages in the headlights are specifically

tailored and require a high degree of customisation.

Only 20-30 vehicle models that have so far adopted

the LED headlight globally, which is very low

considering the 800-plus automobile models

available for sale.

As the number of automobile models equipped with

LED headlights looks set to grow exponentially,

we believe the lower manufacturing costs of

Asian LED makers should allow these players to

benefit from the trend of rising customization, by

capitalising on their lower cost structure and

flexible production planning.

0% 14% 28% 42% 56%

BLU

Lighting

Automotive 40-50%

20-30%

15-25%

GM (%)

Avg. opex of sales14.5%

LED auto lighting: robust demand growth (in lumens)

Source: HSBC estimates

Light source cost per headlight (2013), vs LED light bulb

Source: HSBC

0.00

0.08

0.16

0.24

0.32

0.40

2001 2003 2005 2007 2009 2011 2013e 2015eBack lights Daytime running light Front lights

(tn lm)

0

5

10

15

20

8W LED bulb Halogen HID LED

(USD)

11

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Auto lighting the long-term margin driver for Asia LED Auto could be a greater earnings driver than BLU by 2015

The revenue of Korean and Taiwanese LED

makers has a 4% exposure to the auto sector –a

step below the global average. This is

understandable, as Nichia, Philips and Osram

have high shares in this segment. Nevertheless we

expect a long-term growth rate of 30% for auto

LED in coming years, driven by increasing

outsourcing orders from the leaders.

Although we expect the contribution of auto LED

to the revenue mix of Korean and Taiwanese LED

makers to remain small – around 9% by 2016 and

15% by 2018 (practically the smallest of all

segments) – the contribution to profitability

should be far greater:

In terms of gross profit, the contribution of auto

LED for Korean/Taiwan LED makers should

be similar to that of backlights by 2016.

However, given the very high operating

leverage, auto LED could surpass BLU in terms

of its operating profit contribution by 2015.

By 2018, the operating profit contribution of

auto LED could be similar to that of general

lighting, if LED headlight adoption turns out

to be broader based (+40%).

As we mentioned earlier, LED chip demand

should still grow at a rate of more than 25% in the

coming years. However revenue growth has

always been much less impressive owing to ASP

erosion. As auto LED is likely the segment with

(1) by far the highest margin; and (2) by far the

least ASP erosion in the product life cycle, it is

one of the biggest drivers of incremental earnings

growth (along with LED lighting), despite the

small revenue base.

This is why we believe investors should focus less

on Asia’s LED revenue growth, which is

plateauing, and more on the margin expansion and

earnings growth story, as higher-margin segments

account for a larger share of the product mix.

Asia LED operating profit breakdown by segment – auto could overtake BLU in 2015

Source: HSBC estimates

Margin trend in Asia LED, assuming 30% growth for auto

Source: HSBC estimates

0%

25%

50%

75%

100%

2013 2014 2015 2016 2017 2018

Auto lighting BLU Lighting Mobile Others

(%)

0%

8%

16%

24%

32%

2013 2014 2015 2016 2017 2018

Gross margin (%) Operating margin (%)

(%)

12

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Our scenario analysis shows that, even if auto

lighting grows at a slower rate of 20%, there is

still a good chance that the auto segment will play

a more critical role than the BLU segment from

the profit perspective.

Opportunity in Korea The LED market in the auto lighting industry

is also an important opportunity for Korean

LED manufacturing companies, as (1) Korean

car companies are growing faster than other

auto makers, and (2) applications for LED

lights are expanding via premium strategies

and improvements in energy efficiency.

Only 1-2% of automobiles now have LED

headlights installed, but this market is

expected to grow as they begin to be installed

in small and medium-size vehicles, too.

For example, Hyundai Motors previously

installed LED headlamps only on luxury

models, but has now extended this option to

small and medium-size vehicles to promote

its differentiation strategy (eg it was first

installed in new models of Equus, Genesis,

and K9, and has now been extended into the

2014 Sonata and Avante models).

German and Japanese companies currently

dominate the LED headlight segment, while

Korean companies have solid positions in

back lights, fog lights, and indoor lights,

where safety issues are of lesser importance.

However, we forecast a gradual increase in

the Korean companies’ market shares as they

penetrate the LED headlamp segment.

Opportunity in Taiwan Taiwan has a very small domestic automobile

manufacturing base, with a global market

share of less than 1%. However, several

Taiwanese companies playing key roles in the

global auto lighting world in both the AM

(after-market) and OEM space.

Scenario analysis: gross profit contribution under different auto growth assumptions

Segment gross profit % of total gross profit _ 2013 2014 2015 2016 2017 2018

Base case Auto lighting 8% 10% 13% 16% 20% 23% BLU 25% 22% 19% 17% 14% 12% Lighting 26% 29% 31% 33% 34% 36% Mobile 15% 13% 11% 9% 7% 6% Others 26% 26% 26% 26% 25% 23% Bull case Auto lighting 8% 11% 14% 18% 22% 27% BLU 25% 22% 19% 16% 14% 11% Lighting 26% 28% 31% 32% 33% 34% Mobile 15% 13% 11% 9% 7% 6% Others 26% 26% 26% 25% 24% 22% Bear case Auto lighting 8% 10% 11% 13% 15% 17% BLU 25% 22% 20% 17% 15% 13% Lighting 26% 29% 31% 34% 36% 39% Mobile 15% 13% 11% 9% 8% 7% Others 26% 26% 27% 26% 26% 25%

Source: HSBC estimates

Scenario analysis assumptions summary

___ Revenue growth y-o-y _____ GM Opex/sales Base case Bull case Bear case

Auto lighting 45% 18% 30% 35% 20% BLU 20% 13% -10% -10% -10% Lighting 25% 15% 12% 12% 12% Mobile 18% 13% -12% -12% -12% Others 23% 17% 3% 3% 3%

Source: HSBC

Scenario analysis: operating profit contribution under different auto growth assumptions

___ Segment operating profit % of total OP ____ 2013 2014 2015 2016 2017 2018

Base case Auto lighting 14% 17% 21% 26% 30% 35% BLU 24% 21% 18% 15% 12% 10% Lighting 29% 31% 32% 33% 34% 34% Mobile 11% 9% 8% 6% 5% 4% Others 22% 21% 21% 20% 19% 17% Bull case Auto lighting 14% 18% 23% 28% 33% 39% BLU 24% 21% 18% 14% 12% 9% Lighting 29% 30% 32% 33% 33% 32% Mobile 11% 9% 8% 9% 5% 4% Others 22% 21% 20% 19% 18% 16% Bear case Auto lighting 14% 16% 19% 21% 24% 27% BLU 24% 21% 18% 16% 13% 11% Lighting 29% 31% 33% 35% 37% 39% Mobile 11% 10% 8% 7% 6% 5% Others 22% 22% 21% 21% 20% 19%

Source: HSBC estimates

13

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Meanwhile the industry has a unique

structure, in which many players specialise

solely in chip making, creating opportunities

for outsourcing opportunities. As some auto

light source/auto lighting players actually

have their own LED packaging divisions,

they may wish to source the LED chips from

these chip makers. Epistar is already

supplying the global light source leaders and

is also working directly with a top five auto

lighting supplier.

The structure of global auto lighting Auto lighting makers

Car makers mostly rely auto lighting makers to

design and manufacture various exterior lights. As

a rule of thumb, Japanese auto lighting makers

tend to have strong relations with the US and

Japanese automakers, while European firms rely

more on US and European car makers. However,

both Japanese and European players are active in

China, setting up joint ventures with various local

partners. Some of these JVs are sizeable:

Shanghai Koito has already reached annual

revenue of USD1bn.

As these lights are endorsed by the automakers,

they are deemed to be OEM auto parts. For

replacement purposes, the products of auto

lighting OEMs (known as original equipment

suppliers, or OESs, in this context) can also be

purchased through distributors, albeit at a very

high premium (2-3x, by our estimates) to the

wholesale price (the cost auto makers paid to

install the equipment on the new cars).

Lighting source suppliers

The biggest auto light source suppliers globally

are Osram and Philips. We estimate that they have

a combined global market share of 80%. The light

source generally accounts for some 15-20% of the

auto lighting module.

We have seen some small companies bundle LED

packages into a filament shape, and use this as

replacement bulb – the consumer can simply

replace the HID/halogen with the LED light

source. However, we believe this design does not

fully exploit the benefits of LED.

After market (AM)

The auto component industry also has an after-

market (AM) segment. Companies in this area

manufacture parts that will fit a vehicle, without

approval from the OEM or the car makers.

Although these products are 50%-plus cheaper

than if purchased from the OES, AM is typically

more common in developing countries, as

developed countries such as the US have more

stringent insurance policies, which require the

products of OES to be used for repairs.

Global automotive lighting market

Source: HSBC

New Car Original Equipment Manufacturer (OEM)

Original Equipment Supplier (OES)Replacement

Aftermarket Parts (AM)

14

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Global lighting supply chain

Company Ticker Nationality Main products Main customers 2012 auto-lighting revenue

Industry position

Auto lighting makers

Koito 7276 JP Japan Automotive lighting Toyota, Nissan, Honda, Mazda

USD4.8bn Global No.1 auto-lighting maker;The biggest automotive lighting maker in China (37% market share); 20% owned by Toyota

Hella unlisted Germany Automotive lighting, street lights, auto parts

VW, GM Shanghai, Hyundai USD3.6bn

Top 3 auto-lighting maker and top 100 German industrial company; family-owned company with 70 locations in more than 30 countries

Stanley 6923 JP Japan

Automotive lighting, Street lights, electric/applied products

Honda USD2.2bn Revenue breakdown: 70% auto lighting, 20% electric/applied products, 10% components; 5% owned by Honda

Automotive Lighting unlisted Italy Automotive lighting Fiat, Ford USD3.1bn

Automotive lighting division of Magneti Marelli, which is a subsidiary of Fiat Group

Valeo FR FP France Automotive lighting, electric/applied products

Audi, BMW, Hyundai, Aston Martin

USD2.4bn Established in 1923. 15% revenue from auto lighting; operating more than 120 production sites in 28 countries

Delphi DLPH US United States

Automotive lighting, electric/applied products, Auto parts

GM, Ford, VW USD1.6bn Spun off from General Motors in 1999. Operating more than 150 production sites in 38 countries

SL 005850 KS

Korea Automotive lighting, Chassis, Moulds

Hyundai Motors, GM USD545m 4% global lighting market share;Revenue breakdown: 53% headlight, 30% moulds, 17% chassis

Hyundai Mobis

012330 KS Korea Module, After-sale

Hyundai Motors, Kia Motors

USD27.3bn (total revenue)

Revenue breakdown: 79% module, 18% after-sale, 33% Korea headlight market share; 17% owned by Kia Motors

Lighting source suppliers

Philips PHG US Netherlands

Light bulb, LED, Consumer electronics, Domestic appliances

All auto lighting makers, retail USD1.1bn

Global No.1 lighting source supplier; Established in 1891; Operating in more than 60 countries

Osram OSR GR Germany

Light bulb, LED, Light engines, Lighting management systems

All lighting makers, retail

USD1.4bn

Global top 3 lighting source supplier; Spun off from Siemens in 2012; Supplying customers in more than 150 countries

AM market/OEM manufacturer

Depo 6605 TT Taiwan Automotive lighting GM, Chrysler, USD0.4bn

Top AM auto-lighting maker (no.1 in Taiwan) with owned brand DEPO; More than 90% of revenue comes from AM auto lighting; sales in North America are made through self-owned subsidiary, Maxzone

TYC 1522 TT Taiwan Automotive lighting, Street lights

Ford, Ducati, Suzuki, Isuzu, GM

USD0.5bn

Top AM auto-lighting maker (No.2 in Taiwan); Above 95% of revenue comes from auto-lighting; Revenue breakdown: 45% from North America, 15% from Europe, 10% from South America, 10% from Asia

Tayih 1521 TT Taiwan Automotive lighting Ford, Chrysler, Mazda, Suzuki USD1.1bn

Top auto-lighting maker with OEM focus; Revenue breakdown: 80% auto lighting, 10% mould, 10% components

LED auto lighting module maker

Laster Tech 3346 TT Taiwan

LED auto lighting module, LED chips, LED industrial lighting

Koito, TYC, Tokaidenso, Audi, GM, BYD

USD40.9m

Distributors for Philips and Osram LED; Revenue breakdown: 67% from auto lighting, 23% from LED chips, 10% from industrial/general lighting

Source: Company data, HSBC

15

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

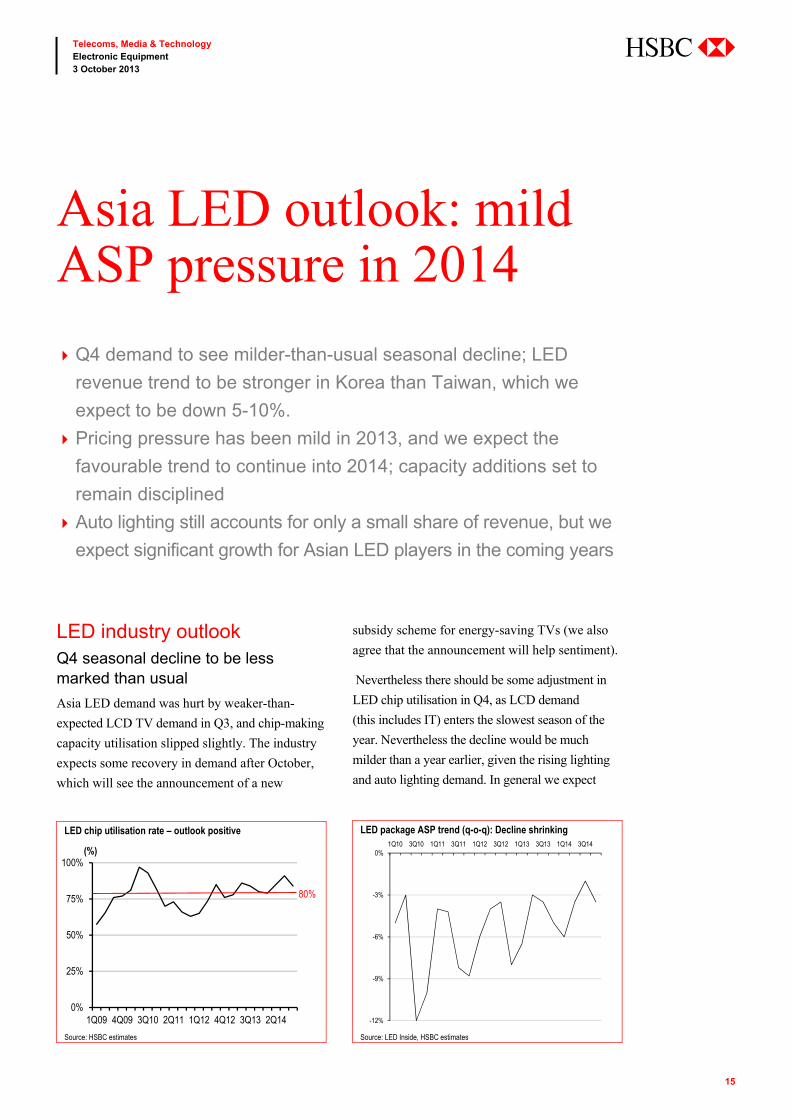

LED industry outlook Q4 seasonal decline to be less marked than usual

Asia LED demand was hurt by weaker-than-

expected LCD TV demand in Q3, and chip-making

capacity utilisation slipped slightly. The industry

expects some recovery in demand after October,

which will see the announcement of a new

subsidy scheme for energy-saving TVs (we also

agree that the announcement will help sentiment).

Nevertheless there should be some adjustment in

LED chip utilisation in Q4, as LCD demand

(this includes IT) enters the slowest season of the

year. Nevertheless the decline would be much

milder than a year earlier, given the rising lighting

and auto lighting demand. In general we expect

Asia LED outlook: mild ASP pressure in 2014

Q4 demand to see milder-than-usual seasonal decline; LED

revenue trend to be stronger in Korea than Taiwan, which we

expect to be down 5-10%.

Pricing pressure has been mild in 2013, and we expect the

favourable trend to continue into 2014; capacity additions set to

remain disciplined

Auto lighting still accounts for only a small share of revenue, but we

expect significant growth for Asian LED players in the coming years

LED chip utilisation rate – outlook positive

Source: HSBC estimates

LED package ASP trend (q-o-q): Decline shrinking

Source: LED Inside, HSBC estimates

0%

25%

50%

75%

100%

1Q09 4Q09 3Q10 2Q11 1Q12 4Q12 3Q13 2Q14

(%)

80%

-12%

-9%

-6%

-3%

0%1Q10 3Q10 1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14 3Q14

16

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Korean firms to perform better than Taiwan LED

players, owing to the captive customer supports: flat

to slightly up versus a 5-10% decline for Taiwan.

Pricing pressure has been mild, and should remain so into 2014

We foresee some price erosion in Q4 (5-6%).

However, the LED chip makers that can improve

their product mix should still be able to achieve

margin expansion. We also expect the pricing

environment to be favourable for most of 2014 (with

a greater drop in Q1), as capacity expansions in the

industry (outside China) remained disciplined. We

continue to take the view that Chinese capacity will

be unable to serve most of the product segments,

owing to outdated technology and quality issues.

LG Innotek The auto lighting business still makes an

insignificant contribution to LG Innotek’s revenue.

However, we expect it to become meaningful

once LG Group’s EV component business takes

off from H2 2014, since LG Group selected this

business as a new growth catalyst and it is in the

process of product bundles with its related

businesses to supply to auto OEMs. The related

businesses include (1) LG Chemicals’ battery

business, (2) LG Electronics’ car audio, motors,

communication device and navigation business,

(3) LG U+’s telecommunication service, (4) LG

Innotek’s sensor and LED light chip business.

Seoul Semi Seoul Semi is consolidating its position in the

street light business via Achrich, an A/C type

LED, and is expected to extend the use of this

product to the automobile segment as well.

Currently, automotive LED contributes 7-8% of

the company’s total sales, and we believe

headlights will cause a greater improvement in

profitability than in revenues.

Seoul Semiconductor sales mix estimates

Source: HSBC estimates

Epistar While auto-related sales contribute only 3-4% to

revenue, we believe their GP/OP contribution is

well above that level owing to the extremely high

margin (likely the most profitable segment).

Management is suggesting the share of auto-related

revenue could rise to the 5-10% range in 2014.

0

400

800

1,200

1,600

2013e 2014e

Handset/Tablet TV General lighting and others Monitor Auto

(KRW bn)

Auto: 74bnAuto: 76bn

LG Innotek sales mix estimates

Source: HSBC estimates

Epistar sales mix estimates

Source: HSBC estimates

0

2,000

4,000

6,000

8,000

2013e 2014eLED DNCamera Module PCBPackage Substrate Material

(KRW bn)

Auto: 362bnAuto: 415bn

0

5

10

15

20

25

2013e 2014eOthers BLU Consumer Lighting Auto

(TWDbn)

Auto: TWD0.7bnAuto: TWD1.7bn

17

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Epistar is working with several auto lighting

leaders such as Stanley, which sources Epistar

chips for its auto-related LED packages. We

expect Epistar’s close ties with Toyoda Gosei

(a key subsidiary of Toyota) will allow it to

capture more opportunities in the future.

Everlight Everlight now generates a low-single-digit

percentage of its total revenue from auto-related

LED applications. Management suggests that the

segment should grow faster than the company as a

whole, as it continues to capture more customers

for interior and exterior auto lighting. Everlight is

working on headlight LED products. We believe

they have a chance to penetrate the AM market in

the coming year.

Everlight sales mix estimates

Source: HSBC estimates

0

7

14

21

28

2013e 2014eOthers BLU Consumer Lighting Auto

(TWDbn)

Auto: TWD0.7bn Auto: TWD1.2bn

18

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

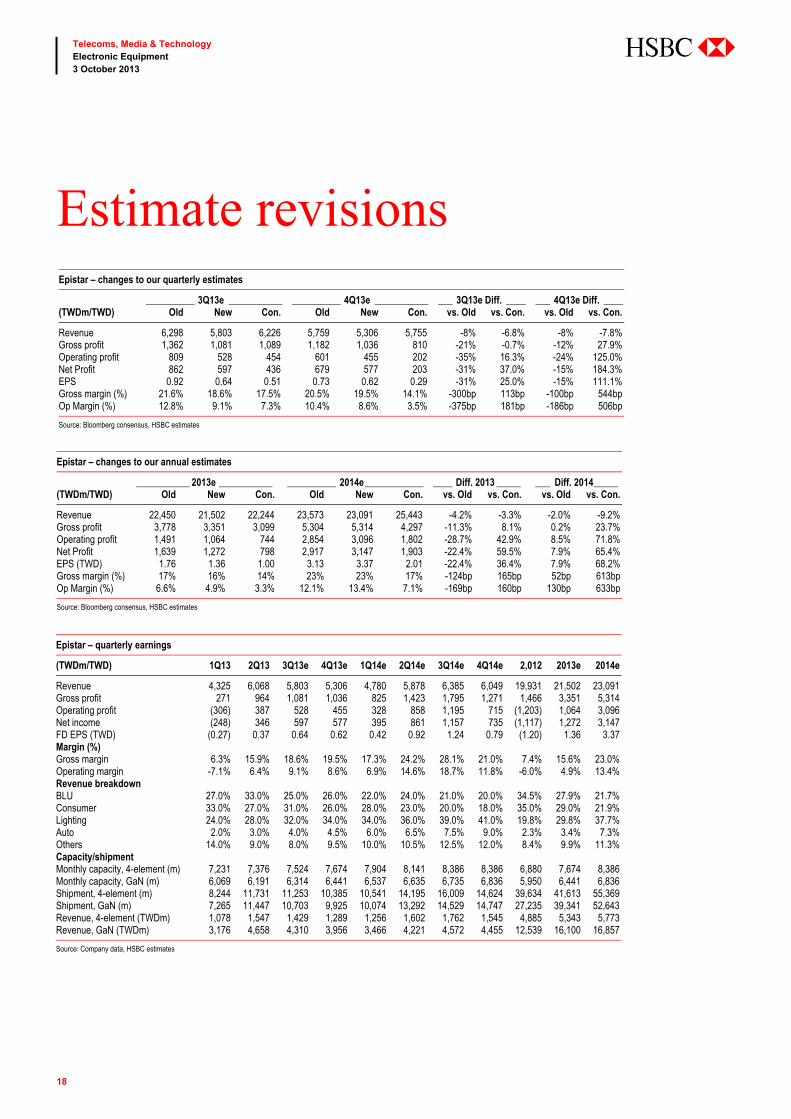

Epistar – changes to our annual estimates

___________ 2013e ___________ __________ 2014e ____________ ____ Diff. 2013 _____ ___ Diff. 2014 _____ (TWDm/TWD) Old New Con. Old New Con. vs. Old vs. Con. vs. Old vs. Con.

Revenue 22,450 21,502 22,244 23,573 23,091 25,443 -4.2% -3.3% -2.0% -9.2% Gross profit 3,778 3,351 3,099 5,304 5,314 4,297 -11.3% 8.1% 0.2% 23.7% Operating profit 1,491 1,064 744 2,854 3,096 1,802 -28.7% 42.9% 8.5% 71.8% Net Profit 1,639 1,272 798 2,917 3,147 1,903 -22.4% 59.5% 7.9% 65.4% EPS (TWD) 1.76 1.36 1.00 3.13 3.37 2.01 -22.4% 36.4% 7.9% 68.2% Gross margin (%) 17% 16% 14% 23% 23% 17% -124bp 165bp 52bp 613bp Op Margin (%) 6.6% 4.9% 3.3% 12.1% 13.4% 7.1% -169bp 160bp 130bp 633bp

Source: Bloomberg consensus, HSBC estimates

Estimate revisions

Epistar – quarterly earnings

(TWDm/TWD) 1Q13 2Q13 3Q13e 4Q13e 1Q14e 2Q14e 3Q14e 4Q14e 2,012 2013e 2014e

Revenue 4,325 6,068 5,803 5,306 4,780 5,878 6,385 6,049 19,931 21,502 23,091 Gross profit 271 964 1,081 1,036 825 1,423 1,795 1,271 1,466 3,351 5,314 Operating profit (306) 387 528 455 328 858 1,195 715 (1,203) 1,064 3,096 Net income (248) 346 597 577 395 861 1,157 735 (1,117) 1,272 3,147 FD EPS (TWD) (0.27) 0.37 0.64 0.62 0.42 0.92 1.24 0.79 (1.20) 1.36 3.37 Margin (%) Gross margin 6.3% 15.9% 18.6% 19.5% 17.3% 24.2% 28.1% 21.0% 7.4% 15.6% 23.0% Operating margin -7.1% 6.4% 9.1% 8.6% 6.9% 14.6% 18.7% 11.8% -6.0% 4.9% 13.4% Revenue breakdown BLU 27.0% 33.0% 25.0% 26.0% 22.0% 24.0% 21.0% 20.0% 34.5% 27.9% 21.7% Consumer 33.0% 27.0% 31.0% 26.0% 28.0% 23.0% 20.0% 18.0% 35.0% 29.0% 21.9% Lighting 24.0% 28.0% 32.0% 34.0% 34.0% 36.0% 39.0% 41.0% 19.8% 29.8% 37.7% Auto 2.0% 3.0% 4.0% 4.5% 6.0% 6.5% 7.5% 9.0% 2.3% 3.4% 7.3% Others 14.0% 9.0% 8.0% 9.5% 10.0% 10.5% 12.5% 12.0% 8.4% 9.9% 11.3% Capacity/shipment Monthly capacity, 4-element (m) 7,231 7,376 7,524 7,674 7,904 8,141 8,386 8,386 6,880 7,674 8,386 Monthly capacity, GaN (m) 6,069 6,191 6,314 6,441 6,537 6,635 6,735 6,836 5,950 6,441 6,836 Shipment, 4-element (m) 8,244 11,731 11,253 10,385 10,541 14,195 16,009 14,624 39,634 41,613 55,369 Shipment, GaN (m) 7,265 11,447 10,703 9,925 10,074 13,292 14,529 14,747 27,235 39,341 52,643 Revenue, 4-element (TWDm) 1,078 1,547 1,429 1,289 1,256 1,602 1,762 1,545 4,885 5,343 5,773 Revenue, GaN (TWDm) 3,176 4,658 4,310 3,956 3,466 4,221 4,572 4,455 12,539 16,100 16,857

Source: Company data, HSBC estimates

Epistar – changes to our quarterly estimates

__________ 3Q13e ___________ __________ 4Q13e ___________ ___ 3Q13e Diff. ____ ___ 4Q13e Diff. ____ (TWDm/TWD) Old New Con. Old New Con. vs. Old vs. Con. vs. Old vs. Con.

Revenue 6,298 5,803 6,226 5,759 5,306 5,755 -8% -6.8% -8% -7.8% Gross profit 1,362 1,081 1,089 1,182 1,036 810 -21% -0.7% -12% 27.9% Operating profit 809 528 454 601 455 202 -35% 16.3% -24% 125.0% Net Profit 862 597 436 679 577 203 -31% 37.0% -15% 184.3% EPS 0.92 0.64 0.51 0.73 0.62 0.29 -31% 25.0% -15% 111.1% Gross margin (%) 21.6% 18.6% 17.5% 20.5% 19.5% 14.1% -300bp 113bp -100bp 544bp Op Margin (%) 12.8% 9.1% 7.3% 10.4% 8.6% 3.5% -375bp 181bp -186bp 506bp

Source: Bloomberg consensus, HSBC estimates

19

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

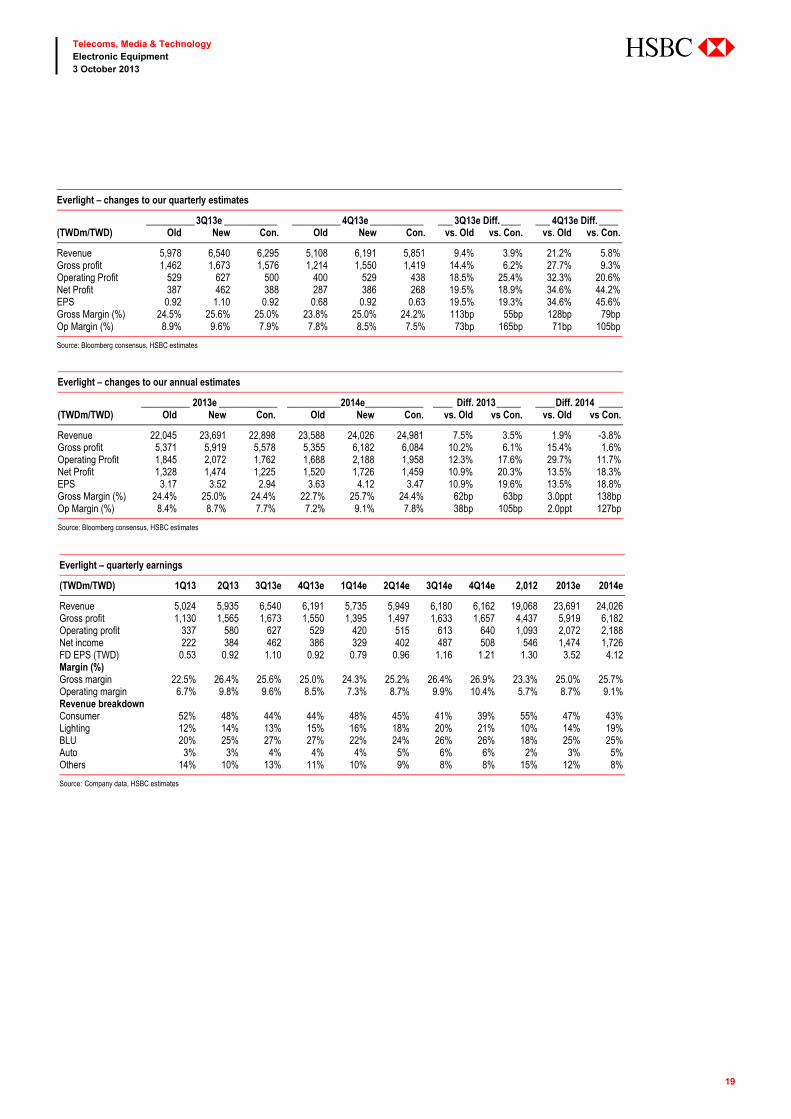

Everlight – quarterly earnings

(TWDm/TWD) 1Q13 2Q13 3Q13e 4Q13e 1Q14e 2Q14e 3Q14e 4Q14e 2,012 2013e 2014e

Revenue 5,024 5,935 6,540 6,191 5,735 5,949 6,180 6,162 19,068 23,691 24,026 Gross profit 1,130 1,565 1,673 1,550 1,395 1,497 1,633 1,657 4,437 5,919 6,182 Operating profit 337 580 627 529 420 515 613 640 1,093 2,072 2,188 Net income 222 384 462 386 329 402 487 508 546 1,474 1,726 FD EPS (TWD) 0.53 0.92 1.10 0.92 0.79 0.96 1.16 1.21 1.30 3.52 4.12 Margin (%) Gross margin 22.5% 26.4% 25.6% 25.0% 24.3% 25.2% 26.4% 26.9% 23.3% 25.0% 25.7% Operating margin 6.7% 9.8% 9.6% 8.5% 7.3% 8.7% 9.9% 10.4% 5.7% 8.7% 9.1% Revenue breakdown Consumer 52% 48% 44% 44% 48% 45% 41% 39% 55% 47% 43% Lighting 12% 14% 13% 15% 16% 18% 20% 21% 10% 14% 19% BLU 20% 25% 27% 27% 22% 24% 26% 26% 18% 25% 25% Auto 3% 3% 4% 4% 4% 5% 6% 6% 2% 3% 5% Others 14% 10% 13% 11% 10% 9% 8% 8% 15% 12% 8%

Source: Company data, HSBC estimates

Everlight – changes to our quarterly estimates

__________ 3Q13e ___________ __________ 4Q13e ___________ ___ 3Q13e Diff. ____ ___ 4Q13e Diff. ____ (TWDm/TWD) Old New Con. Old New Con. vs. Old vs. Con. vs. Old vs. Con.

Revenue 5,978 6,540 6,295 5,108 6,191 5,851 9.4% 3.9% 21.2% 5.8% Gross profit 1,462 1,673 1,576 1,214 1,550 1,419 14.4% 6.2% 27.7% 9.3% Operating Profit 529 627 500 400 529 438 18.5% 25.4% 32.3% 20.6% Net Profit 387 462 388 287 386 268 19.5% 18.9% 34.6% 44.2% EPS 0.92 1.10 0.92 0.68 0.92 0.63 19.5% 19.3% 34.6% 45.6% Gross Margin (%) 24.5% 25.6% 25.0% 23.8% 25.0% 24.2% 113bp 55bp 128bp 79bp Op Margin (%) 8.9% 9.6% 7.9% 7.8% 8.5% 7.5% 73bp 165bp 71bp 105bp

Source: Bloomberg consensus, HSBC estimates

Everlight – changes to our annual estimates

__________ 2013e ____________ ___________2014e ____________ ____ Diff. 2013 _____ ____ Diff. 2014 _____(TWDm/TWD) Old New Con. Old New Con. vs. Old vs Con. vs. Old vs Con.

Revenue 22,045 23,691 22,898 23,588 24,026 24,981 7.5% 3.5% 1.9% -3.8% Gross profit 5,371 5,919 5,578 5,355 6,182 6,084 10.2% 6.1% 15.4% 1.6% Operating Profit 1,845 2,072 1,762 1,688 2,188 1,958 12.3% 17.6% 29.7% 11.7% Net Profit 1,328 1,474 1,225 1,520 1,726 1,459 10.9% 20.3% 13.5% 18.3% EPS 3.17 3.52 2.94 3.63 4.12 3.47 10.9% 19.6% 13.5% 18.8% Gross Margin (%) 24.4% 25.0% 24.4% 22.7% 25.7% 24.4% 62bp 63bp 3.0ppt 138bp Op Margin (%) 8.4% 8.7% 7.7% 7.2% 9.1% 7.8% 38bp 105bp 2.0ppt 127bp

Source: Bloomberg consensus, HSBC estimates

20

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

LG Innotek – quarterly earnings trend

(KRWbn) 1Q13 2Q13 3Q13e 4Q13e 1Q14e 2Q14e 3Q14e 4Q14e 2012 2013e 2014e

Sales LED 256.9 315.7 309.4 301.8 307.8 310.9 317.1 320.3 998.2 1,183.70 1,256.00 DN 180.8 173.9 182.6 188.1 191.8 195.7 199.6 203.6 904.9 725.3 790.6 Camera Module 641.1 557.4 641 660.3 647 666.5 693.1 707 1,661.50 2,499.80 2,713.60 PCB 102.8 75.5 81.5 101.9 109.1 110.2 116.8 117.9 430.4 361.8 453.9 Package Substrate 108.2 125.5 128 132.5 133.8 136.5 137.8 143.3 431.3 494.1 551.4 Material 177.1 186.6 205.3 211.4 213.5 217.8 220 228.8 505.9 780.4 880.1 Automotive 87.3 89.4 84 101.2 102.2 103.2 104.2 105.3 353.6 361.9 414.9 Total 1,554.20 1,524.00 1,631.80 1,697.10 1,705.20 1,740.60 1,788.60 1,826.10 5,285.80 6,407.00 7,060.60 Operating profit LED -28.3 -22.4 -24.8 -15.1 -9.2 -6.2 -3.2 3.2 -102 -90.5 -15.4 DN 5.9 8 8.1 10.7 9.2 10.1 9.6 10.6 29.7 32.7 39.5 Camera Module 24.4 26.2 44.9 44.9 35.6 40 38.1 42.4 55.6 140.3 156.1 PCB 1.9 -3.4 -4.1 -3.1 -2.2 -1.1 0 1.2 38.9 -8.7 -2.1 Package Substrate 2.2 13.1 13.2 10.7 7.2 7.8 7.6 8.8 11 39.1 31.4 Material 7.7 9.2 16.3 13.3 12 11.7 12.9 10.5 40 46.4 47.1 Automotive 2.1 5.1 1.8 1.5 1.5 1.7 1.4 1.3 1.8 10.5 6 Total 15.8 35.7 55.4 62.9 54.1 64 66.5 78 75 169.9 262.5 OP margin LED -11.0% -7.1% -8.0% -5.0% -3.0% -2.0% -1.0% 1.0% -10.2% -7.6% -1.2% DN 3.3% 4.6% 4.4% 5.7% 4.8% 5.2% 4.8% 5.2% 3.3% 4.5% 5.0% Camera Module 3.8% 4.7% 7.0% 6.8% 5.5% 6.0% 5.5% 6.0% 3.3% 5.6% 5.8% PCB 1.8% -4.5% -5.0% -3.0% -2.0% -1.0% 0.0% 1.0% 9.0% -2.4% -0.5% Package Substrate 2.0% 10.4% 10.3% 8.1% 5.4% 5.7% 5.5% 6.1% 2.6% 7.9% 5.7% Material 4.3% 4.9% 7.9% 6.3% 5.6% 5.4% 5.9% 4.6% 7.9% 5.9% 5.3% Automotive (not LED) 2.4% 5.7% 2.2% 1.5% 1.5% 1.7% 1.3% 1.2% 0.5% 2.9% 1.4% Total 1.0% 2.3% 3.4% 3.7% 3.2% 3.7% 3.7% 4.3% 1.4% 2.7% 3.7%

Source: Company data, HSBC estimate (DN: display & network, PCB: printed circuit board)

Seoul Semiconductor – quarterly earnings outlook

(KRWbn) 1Q13 2Q13 3Q13e 4Q13e 1Q14e 2Q14e 3Q14e 4Q14e 2012 2013e 2014e

Sales Handset/Tablets 35 40 41 43 41 46 47 49 128 159 183 TV 65 74 77 80 77 86 88 92 239 296 342 General lighting 95 109 113 117 115 128 132 137 351 433 511 Monitor 21 24 25 26 25 27 28 29 77 95 110 Auto 16 19 19 20 19 21 22 23 60 74 76 Total sales 231 266 276 285 274 305 315 328 855 1,057 1,223 Operating profit Handset 0.9 3.5 1.5 1.5 1.1 1.3 1.5 1.3 0.8 7.4 5.3 TV 3 7.2 6.3 5.5 5.5 6.8 5.6 5.7 1.6 21.9 23.6 General lighting and others 7.2 16.7 13.4 10.1 13.6 17.9 20.8 22.7 13 47.3 75 Home appliance and others 1 1.8 1.2 1.1 0.9 1.1 1.1 1.1 1.2 5.2 4.2 Total OP 12.2 29.2 22.4 18.2 21.2 27.1 29 30.9 16.5 81.9 108.1 OP margin Handset 2.90% 9.90% 5.00% 4.70% 3.70% 3.80% 4.30% 3.70% 0.70% 5.80% 3.90% TV 3.90% 8.30% 7.20% 6.20% 6.50% 7.40% 6.00% 6.00% 0.60% 6.50% 6.50% General lighting and others 7.40% 13.50% 10.30% 7.40% 10.30% 12.20% 13.40% 13.80% 3.50% 9.70% 12.60% Home appliance and others 3.60% 8.70% 4.20% 4.00% 3.20% 3.10% 3.30% 3.40% 1.00% 4.90% 3.30% Total OP margin 5.30% 11.00% 8.10% 6.40% 7.70% 8.90% 9.20% 9.40% 1.90% 7.70% 8.80%

Source: Company data, HSBC estimate

Seoul Semiconductor – changes to our earnings estimates

(KRWbn) _____________ Old _____________ ____________ New _____________ __________ % change ___________ 2013e 2014e 2015e 2013e 2014e 2015e 2013e 2014e 2015e

Sales 1,057 1,201 1,313 1,057 1,223 1,414 0.0% 1.8% 7.7% Operating profit 82 84 108 82 108 138 0.3% 28.2% 27.4% Net income 63 75 96 63 94 120 0.3% 25.4% 25.3% OP margin 7.70% 7.00% 8.20% 7.70% 8.80% 9.80% 0.0%pt 1.8%pt 1.5%pt NP margin 5.90% 6.30% 7.30% 6.00% 7.70% 8.50% 0.0%pt 1.5%pt 1.2%pt

Source: HSBC estimates

21

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Seoul Semiconductor (046890 KS) Valuation methodology

We raise our 2014 earnings by 28% to capture

improving profitability in the general lighting

business. Our 2014 earnings estimate is 3% below

consensus. We raise our target price to KRW39,000

(from KRW32,000) after factoring in our earnings

revision and to reflect a change in valuation base,

as we shift from 2013e to 2014e. Our new target

PB multiple of 3.0x therefore now reflects the

average for the past three years: 2011-13 versus

2010-12 (2.6x) previously. As the LED lighting

industry is at an early stage of development, we

believe the average multiple for the past three

years reflects the full business cycle for the LED

BLU industry from the beginning to maturity. We

remain Underweight as we think there is limited

upside because (1) the share price already reflects

the company’s potential in general lighting, (2) it

is hard for the company to achieve higher margins

than its peers given the faster rate of price erosion

as more players enter the general lighting market,

and (3) the valuation is already stretched, as the

company is the most expensive LED stock

globally, trading at a 2013e of PB3.7x, compared

with 1.0-2.3x for its peers.

Under our research model, for stocks without a

volatility indicator, the Neutral band is 5ppt above

and below the hurdle rate for Korean stocks of

10%. Our target price implies a potential return of

-6%, which is below the Neutral band of our

model; therefore, we reiterate our Underweight

rating. Potential return equals the percentage

difference between the current share price and the

target price, including the forecast dividend yield

when indicated.

Risks to our view

Key upside risks include government subsidy, a

higher-than-expected earnings contribution from

Acrich and faster-than-expected lighting market

growth driven by promotions from retailers.

LG Innotek (011070 KS) Valuation methodology

We use a target PB multiple of 1.6x (on an

average of 2013-14e BVPS), which is the stock’s

five-year historical average. We believe this is

more appropriate as it reflects all of the

businesses, such as camera modules and substrate,

in addition to LED. On this basis we derive a

target price of KRW113,000 (unchanged). We

reiterate our Overweight rating, as we think the

stock price reflects the potential of the general

lighting business, but is relatively cheap compared

with other LED names.

Under our research model, for stocks without a

volatility indicator, the Neutral band is 5ppt above

and below the hurdle rate for Korean stocks of

10%. Our target price of KRW113,000 implies a

potential return of 28% (excluding forecast

dividend yield), which is above the Neutral band;

therefore, we are reiterating our Overweight

rating. Potential return equals the percentage

difference between the current share price and the

target price, including the forecast dividend yield

when indicated.

Valuation and risks

22

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Risks to our view

Downside risks include (1) a weaker-than-

expected overall TV and handset demand further

lowers its utilisation, (2) raw material prices

increase due to tight supply, and (3) unfavourable

FX rate reduces profit.

Epistar (2448 TT) Valuation methodology

Our new target price of TWD76.0 (previously

TWD74.0) is based on an unchanged multiple of

1.4x, but rolled forward to 2014e BVPS

(previously H2 2013e/H1 2014e). The 1.4x PB

multiple is at the point in the stock’s historical

trading band when ROE tends to reach c7%.

Under our research model, for stocks without a

volatility indicator, the Neutral band is 5ppt above

and below the hurdle rate for Taiwanese stocks of

9%. Our target price implies a potential return of

35%, above the Neutral band; therefore, we

reiterate our Overweight rating. Potential return

equals the percentage difference between the

current share price and the target price, including

the forecast dividend yield when indicated.

Risks to our view

The key downside risk is that Chinese competitors

could adopt an aggressive pricing strategy.

Everlight (2393 TT) Valuation methodology

Our new target price of TWD63.0 (previously

TWD56.0) is based on a 1.6x (previously 1.4x)

2014e BVPS (rolled forward from H2 2013e/H2

2014e). The new PB multiple of 1.6x is at the

point in its historical trading band where ROE

tends to reach double digits, as we are modelling

10.6% ROE in 2014 (prior 9.5%).

Under our research model, the Neutral band for

non-volatile stocks is 5ppt above and below the

hurdle rate for Taiwan stocks of 9%. Our target

price implies a potential return of 16%, which is

above the Neutral band; we therefore reiterate our

Overweight rating. Potential return equals the

percentage difference between the current share

price and the target price, including the forecast

dividend yield when indicated.

Risks to our view

The main downside risk is a severe LCD

inventory adjustment.

Epistar 12-month forward trading band, PB Everlight 12-month forward trading band, PB

Source: Company data, TEJ, HSBC estimates Source: Company data, TEJ, HSBC estimates

-30%

-10%

10%

30%

50%

0

40

80

120

160

Sep-03 Sep-05 Sep-07 Sep-09 Sep-11 Sep-13

RoE2.2x

1.4x

1.8x

1.0x

Epistar Share price (LHS, TWD) RoE (RHS, %)

1.6x2.0x

2.4x

2.8x

1.2x

-30%

-10%

10%

30%

50%

0

40

80

120

160

Sep-03 Sep-05 Sep-07 Sep-09 Sep-11 Sep-13

Everlight Share price (LHS,TWD) RoE (RHS, %)

ROE

Teleco

ms, M

edia &

Tech

no

log

y E

lectron

ic Eq

uip

men

t 3 O

ctob

er 2013

23

ab

c

HSBC global automobile demand model

Region 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013e 2014e 2015e

Western Europe 16,652 16,219 15,976 16,454 16,504 16,695 16,839 15,372 15,014 14,465 14,411 13,140 12,612 12,950 13,412 Germany 3,516 3,414 3,405 3,445 3,510 3,658 3,366 3,309 3,970 3,113 3,407 3,302 3,140 3,298 3,377 UK 2,706 2,830 2,882 2,896 2,762 2,666 2,735 2,421 2,181 2,253 2,202 2,284 2,472 2,472 2,447 Italy 2,644 2,579 2,456 2,488 2,455 2,543 2,728 2,379 2,359 2,151 1,938 1,518 1,382 1,405 1,575 France 2,681 2,544 2,385 2,415 2,482 2,436 2,523 2,505 2,673 2,666 2,631 2,280 2,105 2,171 2,291 Spain 1,706 1,590 1,672 1,841 1,909 1,904 1,882 1,323 1,062 1,101 913 777 805 824 901 Eastern Europe 1,492 1,484 1,825 2,465 2,729 3,061 3,863 4,219 2,285 2,912 3,894 4,112 4,082 4,237 4,348 Russia 1,149 1,128 1,224 1,447 1,612 1,944 2,594 2,952 1,468 1,899 2,678 2,934 2,822 2,921 2,936 Turkey 182 160 358 684 702 606 575 478 546 747 855 766 810 856 918 Ukraine 96 138 177 234 300 405 574 652 174 174 238 232 232 240 270 Others 65 58 66 100 115 106 120 137 96 92 123 179 219 220 224 Central Europe 1,072 1,093 1,206 1,246 1,272 1,352 1,551 1,539 1,082 1,009 971 924 868 929 994 Poland 350 328 383 354 271 281 347 378 362 374 320 312 297 316 335 Other EU 27 countries 265 285 311 378 468 541 646 605 354 302 317 290 273 286 304 Other Non-EU-27 countries 118 116 120 127 142 157 176 188 117 100 95 72 65 82 95 North America 19,587 19,483 19,195 19,502 19,689 19,324 18,923 15,920 12,653 13,970 15,268 17,161 18,415 18,683 18,900 USA 17,119 16,813 16,636 16,870 16,956 16,568 16,157 13,245 10,437 11,590 12,779 14,499 15,596 15,836 16,010 Canada 1,557 1,696 1,587 1,531 1,582 1,616 1,654 1,636 1,461 1,558 1,586 1,676 1,746 1,737 1,745 Mexico 912 974 972 1,101 1,151 1,140 1,112 1,039 755 822 903 986 1,073 1,110 1,145 South America 2,274 2,095 2,030 2,497 2,871 3,327 4,233 4,422 4,302 5,074 5,552 5,819 5,971 6,073 6,293 Brazil 1,467 1,391 1,321 1,524 1,616 1,833 2,353 2,660 3,004 3,317 3,412 3,628 3,647 3,714 3,859 Argentina 184 91 134 268 355 416 529 574 493 637 832 806 842 833 823 Middle East/Africa 2,363 2,499 2,716 3,078 3,725 4,097 4,378 4,468 4,206 4,870 5,018 4,621 4,527 4,661 4,917 Iran 352 504 614 804 1,072 1,132 1,140 1,158 1,420 1,635 1,665 1,026 815 927 1,076 Greater China 2,020 2,776 3,816 4,306 5,121 6,211 7,324 7,765 11,856 15,607 16,560 17,608 19,387 20,950 22,460 China 1,659 2,391 3,415 3,838 4,619 5,854 6,972 7,521 11,557 15,270 16,161 17,216 19,003 20,559 22,063 ASEAN + India 1,820 2,050 2,380 2,929 3,267 3,284 3,549 3,784 3,863 5,132 5,542 6,541 6,329 6,746 7,461 India 708 722 868 1,084 1,172 1,438 1,624 1,701 1,992 2,646 2,900 3,229 3,079 3,328 3,829 Others 7,868 8,058 7,775 7,642 7,736 7,618 7,440 7,094 6,865 7,402 6,642 7,834 7,547 7,437 7,401 Japan 5,628 5,585 5,497 5,541 5,536 5,416 5,088 4,847 4,472 4,801 4,048 5,164 4,816 4,633 4,572 South Korea 1,411 1,585 1,290 1,067 1,131 1,160 1,219 1,176 1,417 1,514 1,530 1,491 1,506 1,543 1,551 Oceania (Australia, New Zealand) 828 889 989 1,034 1,068 1,042 1,132 1,071 976 1,087 1,063 1,180 1,225 1,261 1,278 Global 55,148 55,759 56,919 60,120 62,913 64,969 68,099 64,583 62,127 70,442 73,858 77,760 79,740 82,667 86,187

Source: HSBC estimates

Appendix

24

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Financials & valuation: Epistar Corp Overweight Financial statements

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Profit & loss summary (TWDm)

Revenue 19,931 21,502 23,091 24,246EBITDA 3,099 6,226 9,292 10,662Depreciation & amortisation -4,302 -5,163 -6,195 -7,435Operating profit/EBIT -1,203 1,064 3,096 3,227Net interest -195 -136 -120 -120PBT -2,184 1,320 3,616 3,687HSBC PBT -2,184 1,320 3,616 3,687Taxation -146 -190 -429 -442Net profit -1,117 1,272 3,147 3,245HSBC net profit -1,117 1,272 3,147 3,245

Cash flow summary (TWDm)

Cash flow from operations 2,302 8,175 8,069 10,209Capex -2,942 -2,000 -2,500 -2,499Cash flow from investment -4,893 -3,137 -1,932 -1,988Dividends -945 -441 -763 -1,888Change in net debt 3,316 -4,647 -5,257 -6,216FCF equity -1,021 5,403 5,165 7,368

Balance sheet summary (TWDm)

Intangible fixed assets 4,625 4,532 4,442 4,353Tangible fixed assets 28,662 27,228 25,867 24,574Current assets 27,410 31,277 37,590 44,347Cash & others 12,135 16,782 22,040 28,256Total assets 67,017 70,406 74,615 79,398Operating liabilities 7,519 10,077 11,901 15,328Gross debt 12,349 12,349 12,349 12,349Net debt 214 -4,434 -9,691 -15,907Shareholders’ funds 47,149 47,980 50,364 51,721Invested capital 41,042 36,178 33,958 29,690

Ratio, growth and per share analysis

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Y-o-y % change

Revenue -9.3 7.9 7.4 5.0EBITDA -16.2 100.9 49.2 14.7Operating profit -5,385.0 – 191.1 4.2PBT – – 174.1 2.0HSBC EPS -313.6 – 147.4 3.1

Ratios (%)

Revenue/IC (x) 0.5 0.6 0.7 0.8ROIC -3.0 2.4 7.8 8.9ROE -2.3 2.7 6.4 6.4ROA -2.8 2.0 4.6 4.4EBITDA margin 15.5 29.0 40.2 44.0Operating profit margin -6.0 4.9 13.4 13.3EBITDA/net interest (x) 15.9 45.8 77.4 88.8Net debt/equity 0.5 -9.2 -19.2 -30.8Net debt/EBITDA (x) 0.1 -0.7 -1.0 -1.5CF from operations/net debt 1078.0 – – –

Per share data (TWD)

EPS Rep (diluted) -1.20 1.36 3.37 3.48HSBC EPS (diluted) -1.20 1.36 3.37 3.48DPS 0.54 0.82 2.02 2.09Book value 53.86 51.44 54.00 55.45

Key forecast drivers

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Global LCD TV shipment (m) 208 206 221 –Global LCD monitor shipment (m) 190 175 177 –Global LED packaging rev (USDm) 13,894 14,212 14,553 15,121

Valuation data

Year to 12/2012a 12/2013e 12/2014e 12/2015e

EV/sales 2.4 2.0 1.6 1.3EV/EBITDA 15.5 6.8 4.0 3.0EV/IC 1.2 1.2 1.1 1.1PE* 41.2 16.7 16.2PB 1.0 1.1 1.0 1.0FCF yield (%) -2.1 11.6 10.9 15.4Dividend yield (%) 1.0 1.5 3.6 3.7

*Based on HSBC EPS (diluted)

Issuer information

Share price (TWD)56.20 Target price (TWD) 76.00 3

5.2

Reuters (Equity) 2448.TW Bloomberg (Equity) 2448 TTMarket cap (USDm) 1,773 Market cap (TWDm) 52,408Free float (%) 70 Enterprise value (TWDm) 42,291Country Taiwan Sector SemiconductorsAnalyst Jerry Tsai Contact +8862 6631 2863

Price relative

Source: HSBC Note: Priced at close of 27 September 2013

29

49

69

89

109

129

29

49

69

89

109

129

2011 2012 2013 2014Epistar Corp Rel to TAIWAN WEIGHTED INDEX

25

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

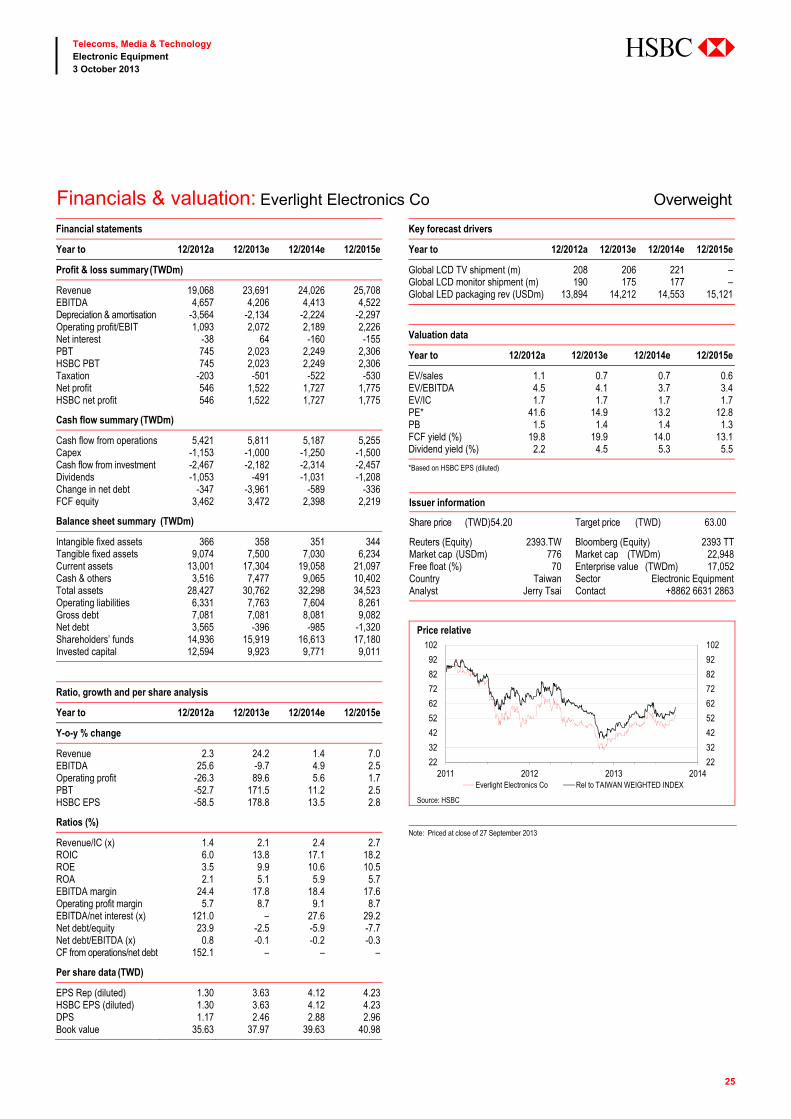

Financials & valuation: Everlight Electronics Co Overweight Financial statements

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Profit & loss summary (TWDm)

Revenue 19,068 23,691 24,026 25,708EBITDA 4,657 4,206 4,413 4,522Depreciation & amortisation -3,564 -2,134 -2,224 -2,297Operating profit/EBIT 1,093 2,072 2,189 2,226Net interest -38 64 -160 -155PBT 745 2,023 2,249 2,306HSBC PBT 745 2,023 2,249 2,306Taxation -203 -501 -522 -530Net profit 546 1,522 1,727 1,775HSBC net profit 546 1,522 1,727 1,775

Cash flow summary (TWDm)

Cash flow from operations 5,421 5,811 5,187 5,255Capex -1,153 -1,000 -1,250 -1,500Cash flow from investment -2,467 -2,182 -2,314 -2,457Dividends -1,053 -491 -1,031 -1,208Change in net debt -347 -3,961 -589 -336FCF equity 3,462 3,472 2,398 2,219

Balance sheet summary (TWDm)

Intangible fixed assets 366 358 351 344Tangible fixed assets 9,074 7,500 7,030 6,234Current assets 13,001 17,304 19,058 21,097Cash & others 3,516 7,477 9,065 10,402Total assets 28,427 30,762 32,298 34,523Operating liabilities 6,331 7,763 7,604 8,261Gross debt 7,081 7,081 8,081 9,082Net debt 3,565 -396 -985 -1,320Shareholders’ funds 14,936 15,919 16,613 17,180Invested capital 12,594 9,923 9,771 9,011

Ratio, growth and per share analysis

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Y-o-y % change

Revenue 2.3 24.2 1.4 7.0EBITDA 25.6 -9.7 4.9 2.5Operating profit -26.3 89.6 5.6 1.7PBT -52.7 171.5 11.2 2.5HSBC EPS -58.5 178.8 13.5 2.8

Ratios (%)

Revenue/IC (x) 1.4 2.1 2.4 2.7ROIC 6.0 13.8 17.1 18.2ROE 3.5 9.9 10.6 10.5ROA 2.1 5.1 5.9 5.7EBITDA margin 24.4 17.8 18.4 17.6Operating profit margin 5.7 8.7 9.1 8.7EBITDA/net interest (x) 121.0 – 27.6 29.2Net debt/equity 23.9 -2.5 -5.9 -7.7Net debt/EBITDA (x) 0.8 -0.1 -0.2 -0.3CF from operations/net debt 152.1 – – –

Per share data (TWD)

EPS Rep (diluted) 1.30 3.63 4.12 4.23HSBC EPS (diluted) 1.30 3.63 4.12 4.23DPS 1.17 2.46 2.88 2.96Book value 35.63 37.97 39.63 40.98

Key forecast drivers

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Global LCD TV shipment (m) 208 206 221 –Global LCD monitor shipment (m) 190 175 177 –Global LED packaging rev (USDm) 13,894 14,212 14,553 15,121

Valuation data

Year to 12/2012a 12/2013e 12/2014e 12/2015e

EV/sales 1.1 0.7 0.7 0.6EV/EBITDA 4.5 4.1 3.7 3.4EV/IC 1.7 1.7 1.7 1.7PE* 41.6 14.9 13.2 12.8PB 1.5 1.4 1.4 1.3FCF yield (%) 19.8 19.9 14.0 13.1Dividend yield (%) 2.2 4.5 5.3 5.5

*Based on HSBC EPS (diluted)

Issuer information

Share price (TWD)54.20 Target price (TWD) 63.00 1

6.2

Reuters (Equity) 2393.TW Bloomberg (Equity) 2393 TTMarket cap (USDm) 776 Market cap (TWDm) 22,948Free float (%) 70 Enterprise value (TWDm) 17,052Country Taiwan Sector Electronic EquipmentAnalyst Jerry Tsai Contact +8862 6631 2863

Price relative

Source: HSBC Note: Priced at close of 27 September 2013

22

32

42

52

62

72

82

92

102

22

32

42

52

62

72

82

92

102

2011 2012 2013 2014Everlight Electronics Co Rel to TAIWAN WEIGHTED INDEX

26

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Financials & valuation: LG Innotek Co Overweight Financial statements

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Profit & loss summary (KRWbn)

Revenue 5,316 6,380 7,016 7,597EBITDA 549 656 715 751Depreciation & amortisation -471 -486 -452 -425Operating profit/EBIT 77 170 263 326Net interest -103 -109 -107 -108PBT -18 66 157 219HSBC PBT -18 66 157 219Taxation -7 -15 -35 -49Net profit -25 51 122 170HSBC net profit -25 51 122 170

Cash flow summary (KRWbn)

Cash flow from operations 301 712 785 812Capex -350 -350 -350 -350Cash flow from investment -383 -381 -377 -380Dividends 0 0 0 -4Change in net debt 6 -202 -280 -299FCF equity -14 98 172 198

Balance sheet summary (KRWbn)

Intangible fixed assets 145 145 145 145Tangible fixed assets 2,631 2,499 2,401 2,330Current assets 2,073 2,689 3,174 3,661Cash & others 353 624 904 1,203Total assets 4,886 5,376 5,771 6,197Operating liabilities 1,450 1,819 2,091 2,352Gross debt 2,168 2,238 2,238 2,238Net debt 1,815 1,613 1,334 1,034Shareholders’ funds 1,268 1,319 1,441 1,607Invested capital 3,046 2,889 2,724 2,581

Ratio, growth and per share analysis

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Y-o-y % change

Revenue 16.8 20.0 10.0 8.3EBITDA 46.8 19.6 9.0 5.0Operating profit – 119.9 54.6 24.3PBT – – 139.8 39.0HSBC EPS – – 139.8 39.0

Ratios (%)

Revenue/IC (x) 1.7 2.2 2.5 2.9ROIC 4.8 5.2 8.0 10.3ROE -1.9 3.9 8.9 11.1ROA 3.1 2.9 3.9 4.4EBITDA margin 10.3 10.3 10.2 9.9Operating profit margin 1.5 2.7 3.7 4.3EBITDA/net interest (x) 5.3 6.0 6.7 7.0Net debt/equity 143.1 122.3 92.5 64.4Net debt/EBITDA (x) 3.3 2.5 1.9 1.4CF from operations/net debt 16.6 44.1 58.9 78.5

Per share data (KRW)

EPS Rep (diluted) -1,239.94 2,526.05 6,058.17 8,418.56HSBC EPS (diluted) -1,239.94 2,526.05 6,058.17 8,418.56DPS 0.00 0.00 0.00 200.00Book value 62,892.66 65,418.79 71,477.16 79,696.00

Valuation data

Year to 12/2012a 12/2013e 12/2014e 12/2015e

EV/sales 0.7 0.5 0.4 0.4EV/EBITDA 6.5 5.1 4.3 3.7EV/IC 1.2 1.2 1.1 1.1PE* 35.0 14.6 10.5PB 1.4 1.4 1.2 1.1FCF yield (%) -0.8 5.6 9.9 11.5Dividend yield (%) 0.0 0.0 0.0 0.2

*Based on HSBC EPS (diluted)

Issuer information

Share price (KRW)88,500 Target price (KRW) 113,000 2

7.7

Reuters (Equity) 011070.KS Bloomberg (Equity) 011070 KSMarket cap (USDm) 1,660 Market cap (KRWbn) 1,785Free float (%) 47 Enterprise value (KRWbn) 3354Country Korea Sector Electronic EquipmentAnalyst Brian Sohn Contact +822 3706 8765

Price relative

Source: HSBC Note: Priced at close of 27 September 2013

45225

65225

85225

105225

125225

145225

45225

65225

85225

105225

125225

145225

2011 2012 2013 2014LG Innotek Co Rel to KOSPI INDEX

27

Telecoms, Media & Technology Electronic Equipment 3 October 2013

abc

Financials & valuation: Seoul Semiconductor Underweight Financial statements

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Profit & loss summary (KRWbn)