TEFAF Art Symposium 2012

18

EMOTIONAL VALUE & ART INVESTMENT Friday, 16 March 2012, Maastricht ING ART MARKET SYMPOSIUM MAASTRICHT AMSTERDAM

-

Upload

tefaf -

Category

Economy & Finance

-

view

645 -

download

1

Transcript of TEFAF Art Symposium 2012

EMOTIONAL VALUE & ART INVESTMENT

Friday, 16 March 2012,

Maastricht

ING ART MARKET SYMPOSIUMMAASTRICHT AMSTERDAM

EMOTIONS, EMOTIONAL ASSETS, & ART INVESTMENT

• To what extent does being in a good mood affect art prices?

• Positive emotions affect our optimistic judgement

• Kirschsteiger, Rigotti and Rustichini (2006) - Good mood implies greater gift giving.

• Loewenstein, Hsee, Weber and Welch (2001) Inducing good mood increases the probability of good outcomes

• We like to give greater weight to the probability of ‘positive’ events, and discount ‘negative’ events.

BEHAVIOURAL FINANCE: WEATHER AFFECTS OUR MOOD

• Some evidence of mood affecting stock prices.

• Mood is proxied by the weather. – Cloudy days and NYSE - Saunders (1993);

– International - Hirschleifer&Shumway (2003);

– Effect driven by market makers - Goetzman& Zhu (2005);

• Seasonal Affective Disorder (SAD)– Stock returns correlate with the length of the day - Kamstra,

Kamer and Levi (2003)

• Cloud coverage and sunshine hours

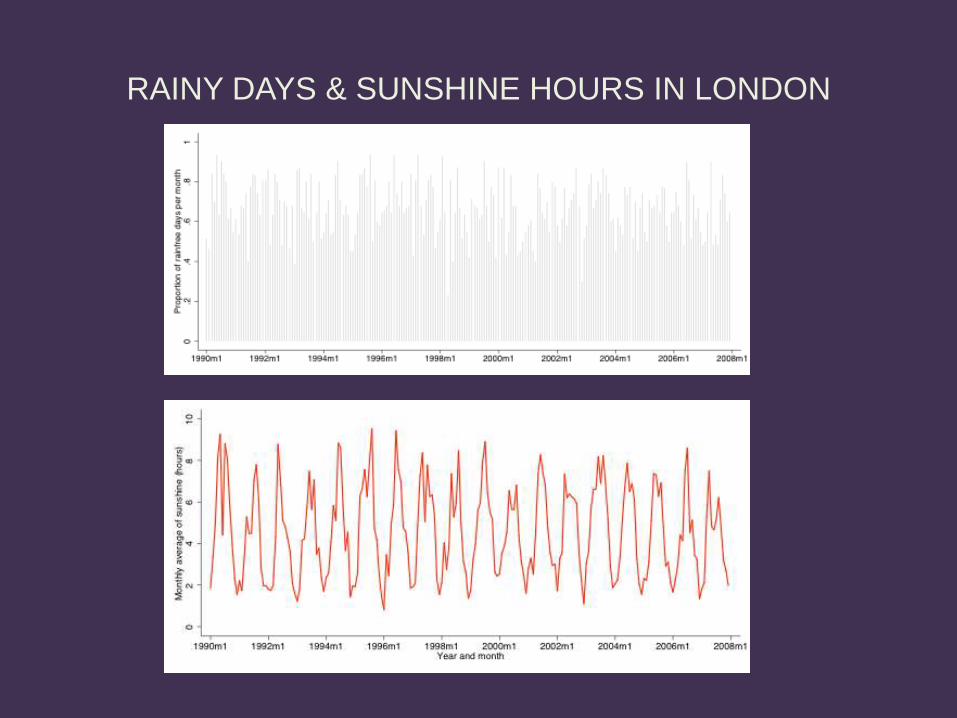

RAINY DAYS & SUNSHINE HOURS IN LONDON

LONDON ART PRICES

• Over 10,000 sales prices between 1990-2007

• High quality artworks and consistently high attendance

rates

• Dataset used is from the European Database for Art

Sales Prices

• Repeat Sales from this dataset:

London All Art Index© and the

Mei-Moses World All Art Index©

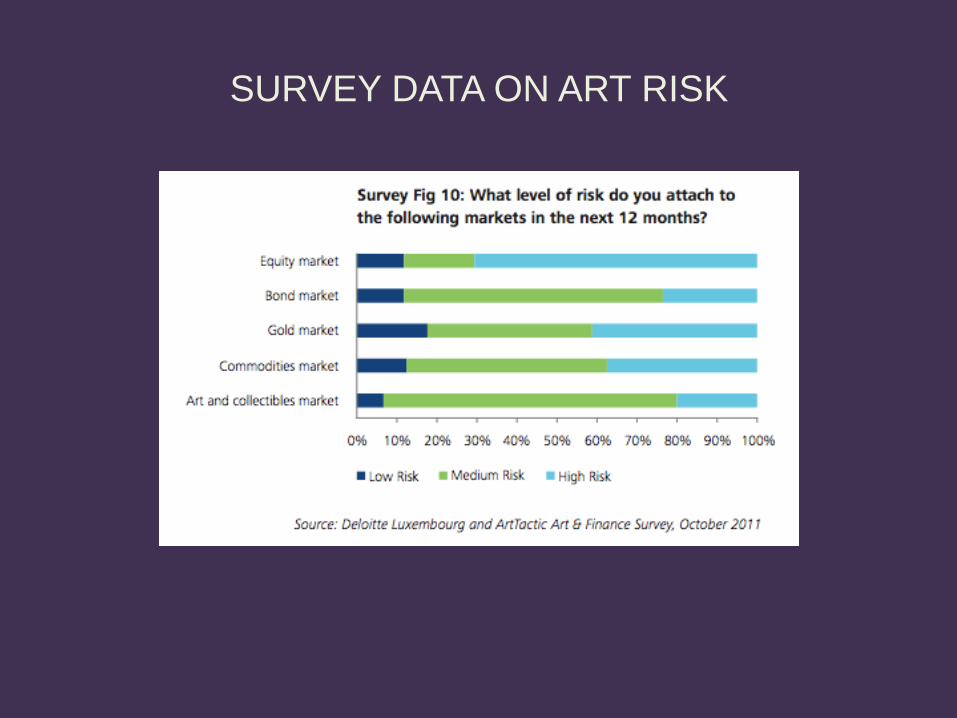

SURVEY DATA ON ART RISK

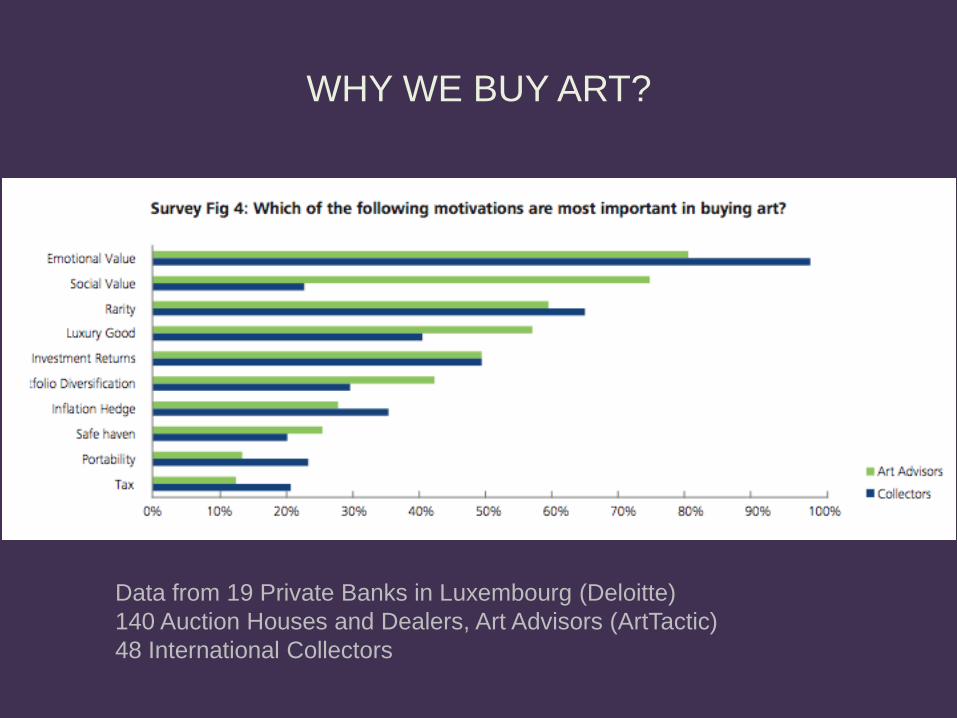

WHY WE BUY ART?

Data from 19 Private Banks in Luxembourg (Deloitte)

140 Auction Houses and Dealers, Art Advisors (ArtTactic)

48 International Collectors

DICHOTOMY OF INVESTING IN ART

• Investors

– Want financial return

– Pecuniary benefits

• Collectors

– Want emotional returns

– Non-pecuniary

– Expressive benefits

• Both investors and collectors have affective responses

• Valuation framework which encompasses these values

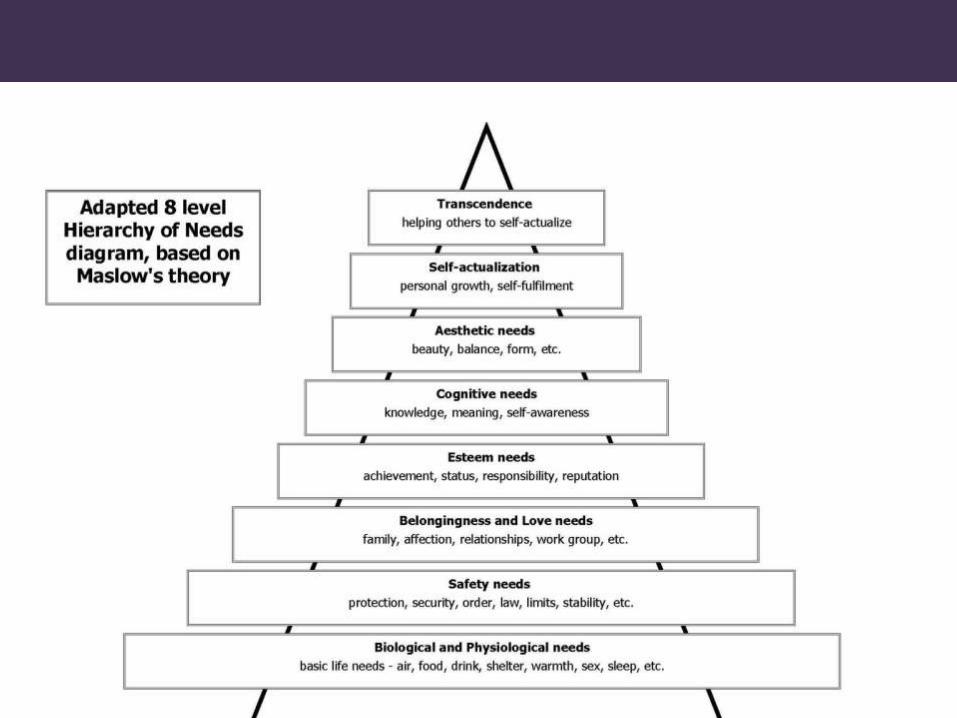

MASLOW: HIERACHY OF NEEDS

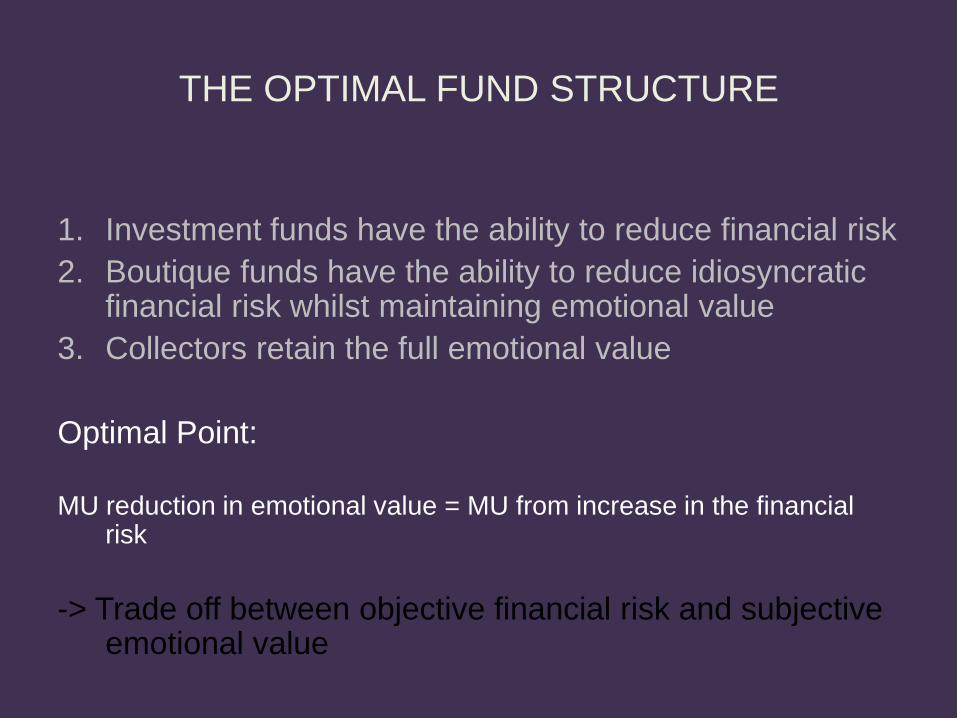

THE OPTIMAL FUND STRUCTURE

1. Investment funds have the ability to reduce financial risk

2. Boutique funds have the ability to reduce idiosyncratic financial risk whilst maintaining emotional value

3. Collectors retain the full emotional value

Optimal Point:

MU reduction in emotional value = MU from increase in the financial risk

-> Trade off between objective financial risk and subjective emotional value

LONDON HEDONIC PRICE INDEX

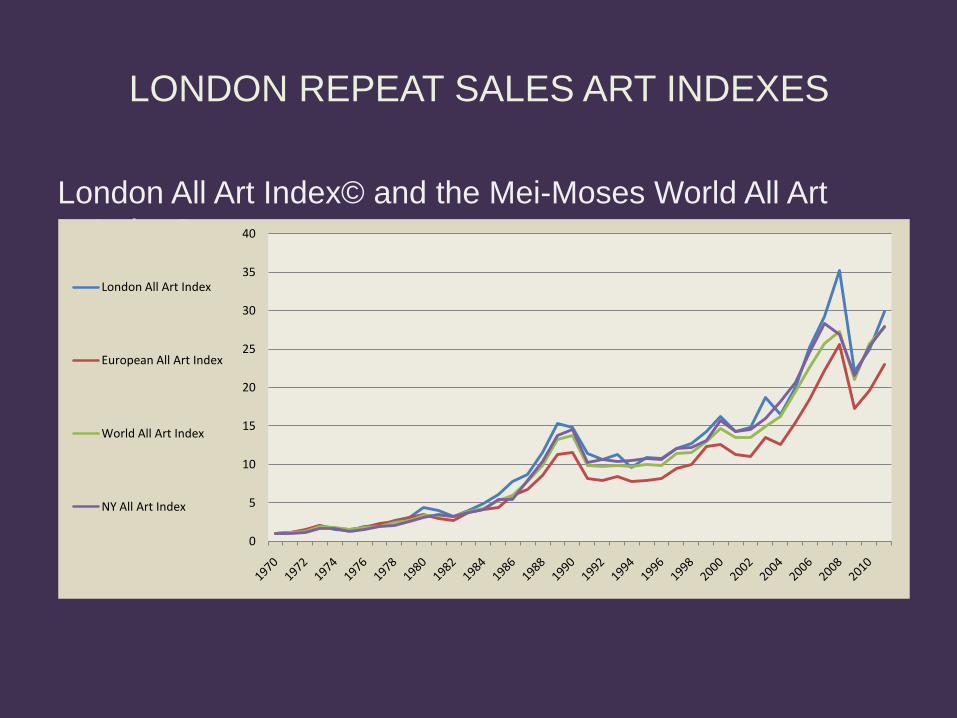

LONDON REPEAT SALES ART INDEXES

London All Art Index© and the Mei-Moses World All Art

Index©

0

5

10

15

20

25

30

35

40

London All Art Index

European All Art Index

World All Art Index

NY All Art Index

EMOTIONS AND INVESTMENT

1. How emotions affect art prices

2. How assets with emotional elements affect

us

3. Private and Common Value to art prices

4. Art Price Index – how art prices change

over time

5. Art returns reflect changing tastes and

fashion

6. Cannot predict the future

7. Investors care about financial and

emotional value

8. For love and for money!