TECHNOLOGY the New Derivatives Landscape - J.P. … · In this issue, Navigating the New...

32

WINTER 2011 REGULATIONS COSTS TECHNOLOGY CENTRAL CLEARING Navigating the New Derivatives Landscape

Transcript of TECHNOLOGY the New Derivatives Landscape - J.P. … · In this issue, Navigating the New...

Winter 2011

REGULATIONS

COSTS

TECHNOLOGY

CENTRAL CLEARING

Navigating the New Derivatives Landscape

2 J.P. Morgan thought / Winter 2011

Thinking Out LoudAs we embark on a new year, the economic climate continues to

present our clients with opportunities and challenges. The changing

economy of the past two years has led to a significant volume of

financial services legislation that could potentially have a profound

impact on the way we do business. Throughout the changing

regulatory landscape, we remain committed to offering leadership

and vision to our clients and business partners.

In this issue, Navigating the New Derivatives Landscape, we focus

on the impact of new regulations on OTC Derivatives and the

ongoing dynamic challenges present in servicing these instruments.

We evaluate the impact the legislative reform will have on daily

business practices, valuation standards and financial reporting

disclosure, especially for fund services clients.

This issue also takes a look at the changing cost of derivatives

trading, post-execution trade management, collateral management

and trade reporting and transparency. We also introduce you to

DerivClear™, our new in-house OTC processing solution that

provides Web-based access to a broad range of operational services

across the OTC trade lifecycle. Finally, we review our Derivatives

Collateral Management service and best practices following the

implementation of central counterparties.

As the financial landscape continues to evolve, we will make the

necessary investments in our people, technology and infrastructure

to help your business succeed in this challenging environment.

Thank you for reading and, as always, your questions and comments

are welcome and can be sent to [email protected]

Conrad KozakCEOWorldwide Securities Services

Conrad Kozak

CEO Worldwide Securities Services

Throughout the changing

regulatory landscape, we remain

committed to offering leadership

and vision to our clients and

business partners.

Winter 2011 / J.P. Morgan thought 3

Winter 2011

J.P. MorganWorldwide Securities Services

tom ChristoffersonGlobal Sales and Client [email protected]

Mark KelleyWestern HemisphereSales and Client [email protected]

Laurence BaileyAsia-PacificSales and Client [email protected]

Francis JacksonEurope, Middle East and AfricaSales and Client [email protected]

About J.P. Morgan Worldwide Securities Services J.P. Morgan Worldwide Securities Services (WSS) is a premier securities servicing provider that helps institutional investors, alternative asset managers, broker dealers and equity issuers optimize efficiency, mitigate risk and enhance revenue. A division of JPMorgan Chase & Co., WSS leverages the firm’s global scale, leading technology and deep industry expertise to service investments around the world. It has $15.9 trillion in assets under custody and $6.7 trillion in funds under administration.

For more information, go to www.jpmorgan.com/wss.

4 10 2618 Valuations: Providing Accuracy and

independence New and enhanced regulatory requirements

include greater transparency and independence for the valuation of OTC derivative instruments.

20 Value-At-risk: Stress testing As portfolios have increased their

complexity through the use of derivatives, strong risk measurement has become more important than ever.

22 new “Best Practices for Collateral” In the OTC derivatives market, the daily

valuation of trades and exchange of collateral has assumed new, heightened importance in the aftermath of the global credit crisis.

24 Meeting the Challenge of regulatory reform: Derivatives Collateral Management

Swap dealers and major participants will be governed by new measures concerning mandatory clearing, exchange trading, reporting and enhanced segregation and margin requirements.

26 the Push for Collateralizing Derivatives trades in Asia Pacific

The use of collateral is becoming more widely recognized as an effective tool for managing counterparty credit risk.

28 Segregating independent Amounts to effectively Mitigate risk

With the specter of counterparty default fresh in their minds, many institutions increasingly seek to collateralize their derivatives trading activities to manage their risk.

4 riding the Waves of regulatory Change – Are You Prepared?

The significant reforms to OTC derivatives regulation will see unprecedented levels of change and an evolution of this industry.

6 the Changing Landscape of Global regulatory reform – Derivatives Disclosure and Valuation

We evaluate the impact of change in daily valuation standards and financial reporting disclosure.

10 Buy-Side Partnership Drives Beneficial Changes to OtC Derivatives Landscape

J.P. Morgan has collaborated with other major dealers and buy-side firms to create continued structural improvements in the global OTC derivatives markets.

12 the Changing Cost of Derivatives How we expect the various stages of post-execution processing to change.

14 the Path to Clearing OTC derivatives clearing is increasingly

critical as the direction of OTC derivatives markets is influenced by financial reform.

16 the Challenges of StP in OtC Derivatives Processing

The Financial Services Industry is facing major changes in the way OTC derivative products are traded and processed.

17 DerivClear™ DerivClear is J.P. Morgan’s in-house

OTC processing solution that provides Web-based access to a broad range of operational services across the OTC trade lifecycle.

4 J.P. Morgan thought / Winter 2011

Riding the Waves of Regulatory Change

Are You Prepared?

Winter 2011 / J.P. Morgan thought 5

While multiple global regulatory initiatives are in progress, two key reforms spearheading the wave of derivatives legislation are the Dodd-Frank Wall Street Reform and Consumer Protection Act, signed into law by President Obama on July 21, 2010 and the European Market Infrastructure Regulation currently under public consultation with a view for implementation in 2011.

These two initiatives are expected to have a significant transformational impact on the financial services industry with the common objectives of instilling greater discipline and governance to protect the public interest, manage systemic risk, have adequate capital and manage general economic welfare.

The key OTC related themes that have arisen from the legislative reforms, which will have buy-side impact are:

• CentrAL CLeArinG: to reduce the build up of large unfunded counterparty risk exposures that lead to failure

• BiLAterAL COLLAterALiSAtiOn: to streamline collateral dispute resolution and increase robust portfolio reconciliation between counterparties by adhering to reconciliation best practices

• trAnSPArenCY: to provide transparency to regulators requiring mandatory disclosure and reporting of OTC activity via trade repositories

• StAnDArDizAtiOn: to facilitate central clearing and potentially making complex OTC products exchange-tradable

• iMPrOVeD OPerAtiOnAL PerFOrMAnCe: to automate the end-to-end OTC derivatives post execution flow, increasing STP with the use of electronic work flow tools

The end of the legislative period is now to be followed by a lengthy period of rule making on the part of the relevant regulatory bodies. The key will be how each of these entities interprets legislation to which they have been tasked. Until such time, many questions remain, specifically in relation to the detail, or the

absence thereof, of how many of the above initiatives will be implemented and by extension, impact industry participants.

It is expected that much if not all of the rule making will be preceded by periods of industry engagement and consultation on the part of regulators. Given the potential pace and sheer volume of rule making (the Commodity Futures Trading Commission lists 30 areas of rule making to implement the Dodd-Frank Bill alone). How each of the industry participants, both buy-side and sell-side, engage and feed into this process will be instrumental in addressing existing uncertainty, in addition to determining its overall success.

Historically, this process has rested predominantly on the sell-side. “Buy-side firms must address this imbalance, by working through their related associations, professional networks or partnering with their service providers,” said Alvaro Zambrano Saez, Product Manager, J.P. Morgan Global Derivatives Services. “Buy-side firms must have a clear line-of-sight to potential regulations and the organisational governance, structure, resource and experience to determine business impacts, and the related effort to implement.” He adds, “There are very few areas within OTC derivatives services that will not be impacted by these changes or carry implementation risk.” In addition, firms, particularly those with a transatlantic offering, must be aware of differences between the EU and US regulations where those may exist, while in turn, not lose sight of the non-EU/US regulations in flight during this period.

OTC derivatives service providers, including J.P. Morgan Global Derivatives Services, will be instrumental in piloting their clients during this uncertain environment through understanding the detail, timing and impact (intended or otherwise) of Derivatives regulations over the coming year. Successful partnership will not be so much desired as required - identification and selection of an appropriate Derivatives service provider will in itself become equally critical.

The recent financial crisis led governments and supervisors across the globe to undertake a comprehensive review of the inherent risks, regulation, governance and oversight of derivatives, specifically Over-The-Counter (OTC) Derivatives. The significant reforms to OTC derivatives regulation will see unprecedented levels of change and an evolution of this industry.

Riding the Waves of Regulatory Change

Are You Prepared?

6 J.P. Morgan thought / Winter 2011

Capital markets have recovered significantly from the lows of 2009, but investors are still seeking further signs of stabilization. Regulators and legislators are eager to assure participants that markets are safe, and are focused on implementing a wide ranging series of regulations designed to provide improved disclosure and transparency, particularly with respect to derivatives.

In fact, the breadth of these reforms is so sweeping that it is challenging for fund sponsors and other market participants to anticipate how these rules will be implemented.

As we evaluate the impact of these reforms on our clients’ business practices, daily valuation standards and financial reporting disclosure are two areas where we expect significant impact for our Fund Services clients.

deRivAtives disClosuRe And vAluAtion

the changing landscape of global regulatory reform

Daily Valuation StandardsToday, fund sponsors must focus not only on the increasing regulatory requirements for disclosure and transparency, but also on improving the standards for valuation. Gone are the days when firms could rely on the brokerage community to provide daily pricing of derivatives. Over a short period of time, independent pricing vendors have largely

Winter 2011 / J.P. Morgan thought 7

replaced broker or investment manager-supplied valuations for derivatives, setting the standard with the same scrutiny, data scrubbing and second-sourcing previously only typical for equities and bonds.

In keeping with the rapid pace of development and increasing complexity in the derivatives market, J.P. Morgan continues to enhance its centralized pricing unit by supporting multiple external vendors and offering an in-house valuation service to provide derivatives pricing coverage. Many of our clients are now using a combination of vendors for both primary and second-sourced prices, providing independence and robustness to the valuation process, to the benefit of investment fund boards, management companies and their pricing committees. Clients may also utilize customized reporting, which provides information such as price movement exceptions to help them better manage fund risk and support valuation oversight committees.

J.P. Morgan’s unique ability to leverage the depth of skills and expertise developed within our investment bank ensures we can keep pace with development of new derivatives and trends in

the market. This specialist approach, combined with the global strength and capability in our fund servicing locations, provides our clients with comprehensive coverage of the over-the-counter (OTC) derivatives market.

Financial reporting Disclosures J.P. Morgan Fund Services teams are engaged globally in the impact of regulatory changes to financial disclosure requirements for our clients. In the U.S., Topic 815 (formerly called FAS 161), “Disclosure about Derivatives Instruments and Hedging Activities” was issued to improve the disclosure requirements in financial reporting, giving investors a better understanding of the use of these instruments in investment portfolios. We utilized the Investment Company Institute (ICI) rule guidance as a foundation to help our clients deal with these rigorous new standards. We also created reports tailored specifically to address requirements for financial statements. The new requirements have been in effect for less than a year and there are already signs of additional changes to come.

8 J.P. Morgan thought / Winter 2011

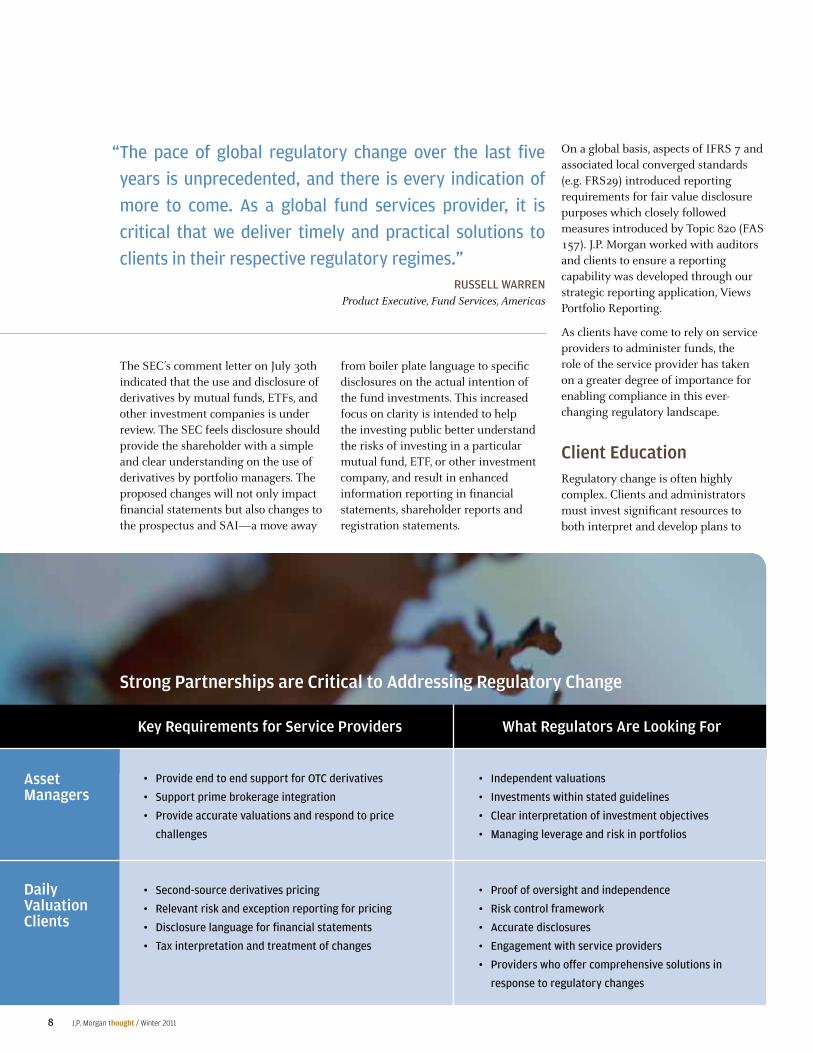

• ProvideendtoendsupportforOTCderivatives

• Supportprimebrokerageintegration

• Provideaccuratevaluationsandrespondtoprice

challenges

• Independentvaluations

• Investmentswithinstatedguidelines

• Clearinterpretationofinvestmentobjectives

• Managingleverageandriskinportfolios

Strong Partnerships are Critical to Addressing regulatory Change

The SEC’s comment letter on July 30th indicated that the use and disclosure of derivatives by mutual funds, ETFs, and other investment companies is under review. The SEC feels disclosure should provide the shareholder with a simple and clear understanding on the use of derivatives by portfolio managers. The proposed changes will not only impact financial statements but also changes to the prospectus and SAI—a move away

On a global basis, aspects of IFRS 7 and associated local converged standards (e.g. FRS29) introduced reporting requirements for fair value disclosure purposes which closely followed measures introduced by Topic 820 (FAS 157). J.P. Morgan worked with auditors and clients to ensure a reporting capability was developed through our strategic reporting application, Views Portfolio Reporting.

As clients have come to rely on service providers to administer funds, the role of the service provider has taken on a greater degree of importance for enabling compliance in this ever-changing regulatory landscape.

Client educationRegulatory change is often highly complex. Clients and administrators must invest significant resources to both interpret and develop plans to

Daily Valuation Clients

Asset Managers

What regulators Are Looking For

• Second-sourcederivativespricing

• Relevantriskandexceptionreportingforpricing

• Disclosurelanguageforfinancialstatements

• Taxinterpretationandtreatmentofchanges

• Proofofoversightandindependence

• Riskcontrolframework

• Accuratedisclosures

• Engagementwithserviceproviders

• Providerswhooffercomprehensivesolutionsin

response to regulatory changes

Key requirements for Service Providers

from boiler plate language to specific disclosures on the actual intention of the fund investments. This increased focus on clarity is intended to help the investing public better understand the risks of investing in a particular mutual fund, ETF, or other investment company, and result in enhanced information reporting in financial statements, shareholder reports and registration statements.

“ The pace of global regulatory change over the last five years is unprecedented, and there is every indication of more to come. As a global fund services provider, it iscritical that we deliver timely and practical solutions to clients in their respective regulatory regimes.”

RuSSEllWARREnProduct Executive, Fund Services, Americas

Winter 2011 / J.P. Morgan thought 9

assure compliance. At J.P. Morgan, our regulatory experts release regular publications on current regulatory topics through our Trustee & Fiduciary bulletin in Europe and our Regulatory Alert in the United States.

However, regular updates may not always be sufficient to keep pace with the latest events, so we invest significant resources to produce more detailed responses to the latest regulatory changes, outlining the likely impact and J.P. Morgan’s proposed response. We also regularly host client webinars on such topical issues where the views of our experts are made available to our clients. We place much importance on engaging directly with clients to better understand their concerns and address individual issues.

“The pace of global regulatory change over the last five years is unprecedented, and there is every indication of more to come,” says Russell Warren, Product Executive, Fund Services, Americas. “As a global fund services provider, it is critical that we deliver timely and practical solutions to clients in their respective regulatory regimes.”

To further our understanding and impact on the regulatory environment and clarify the intent of the emerging regulatory reforms for our Fund Services clients, we participate in industry groups that are working closely with standard setters (e.g. FASB in the U.S., ASB in the U.K. and Ireland, and IASB globally). Meetings with the standard setters also provide J.P. Morgan with an opportunity to provide feedback on the impact (cost and effort) that the changes have on our industry that they may not have contemplated. In an effort to leverage the full resources of the firm, our regulatory teams also collaborate with our Corporate Accounting Policy Group. This group monitors and implements regulatory change for J.P. Morgan as a financial institution, asset manager and plan sponsor.

Looking ForwardIn response to the financial events over the past few years, governments and regulators globally have been eager to take action, and be seen to take action, by increasing regulatory oversight across the whole financial landscape. The ramifications of these new regulations are likely to touch almost the entire fund industry.

Measures to further regulate all investment funds marketed to European investors are being approved by the European Union through its Alternative Investment Fund Managers directive (AIFM). AIFM will apply to all fund managers established in Europe and the funds managed by them, regardless of whether the fund itself is incorporated within an EU Member State, to the extent that the fund does not already operate under harmonized legislation (e.g. UCITS).

AIFM outlines specific valuation requirements for impacted funds (AIFs), ensuring that appropriate procedures are in place to allow for the proper valuation of fund assets. It is proposed that the valuation process be performed by an external evaluator, or, at a minimum, a group functionally independent from the portfolio management function. Additionally, AIFM will require that AIFs have a depository with a duty to ensure that units of the AIF are accurately valued in accordance with applicable rules and legislation.

Other imminent European change measures include the implementation of the ‘recast’ UCITS directive (UCITS IV) which will enter into force on the 1st of July 2011. UCITS IV provides a number of opportunities for fund and management company rationalization through a number of measures facilitating arrangements such as master-feeder structures and passporting of management companies (the ability of a management company established in one European member state to use that authorization to

provide certain services (e.g. management of UCITS) in other EU states). UCITS IV introduces relatively few obligatory measures, however, where they exist, the recurring theme of transparency and prescription of valuation processes is evident. All UCITS must produce and provide investors with Key Investor Information in the form of the ‘KID’ (Key Investor Information Document). Additionally, organizational requirements under the UCITS legislation introduce obligations relating to the independent assessment of the value of OTC derivatives, and notes good practice measures relating to other financial instruments that may expose a UCITS to valuation risk.

President Obama has recently signed into law the most far-reaching U.S. financial reform legislation since The Great Depression, (1) and investors are still in the early stages of understanding how policy makers will draft these regulations to enforce the new law. As we consider the impacts to these changes, clarification is needed to understand the potential changes to such topics as leverage limit requirements for mutual funds and the impact of taxation on certain derivatives instruments.

Many U.S. clients are eager to understand the sensitivity analysis requirements for Level 3 securities (under Topic 820), an issue that is currently under debate by FASB. The IASB has also included similar requirements in IFRS 7, potentially increasing the likelihood of mandating testing of underlying assumptions inherent in pricing esoteric securities. Some speculate that this may move the FASB and IASB towards convergence on a global standard to improve disclosure on all financial instruments.

(1) Dodd-Frank Wall Street Reform and Consumer Protection Act, Press Release, June 29, 2010 http://financialservices.house.gov/press/PRArticle.aspx?NewsID=1306

russell Warren Product Executive, Fund Services, Americas

Marcel Guibout Product Director, Fund Services, EMEA

10 J.P. Morgan thought / Winter 2011

significant investment of resources and capital by the Dealer community and buy-side firms that are collaborating on such efforts.” Mr. Turkfeld added that the derivatives industry recognizes additional work still lies ahead, and that its leadership will be aggressively pursuing improvements based on five major performance objectives:

OBJeCtiVe 1To increase transparency and better understand transparency needs in the OTC derivatives market, the signatories will: (a) continue to advance the development of global data repositories; (b) provide relevant Supervisors with: (i) an inventory of existing forms of transparency in OTC derivatives markets by product and asset class; (ii) a study which describes and evaluates the spectrum of methods that can be used to increase transparency, analyzes the benefits and costs and attempts to identify to whom such benefits and costs accrue and (iii) relevant transaction data to support the Supervisors’ own analysis.

OBJeCtiVe 2To deliver robust, efficient and accessible central clearing to the OTC derivatives markets, the signatories make a strong commitment to increase: (a) the range of products eligible for clearing and (b) the proportion of open interest in the products that are cleared. In support of this commitment, where appropriate, the signatories will work towards the inclusion of users, either through direct access or through indirect client access, including extension of collateral segregation and portfolio portability in the event of a clearing member default.

Addressing credit, equity and interest-rate derivatives – and eventually encompassing commodities and FX – J.P. Morgan devoted 3 months to establishing newly defined targets and goals that would benefit all buy-side participants. The detailed recommendations were recently communicated in a three-page letter and summary document to the president of the U.S. Federal Reserve Bank, the Honorable William C. Dudley. http://search.newyorkfed.org/ny.

This industry-wide effort was undertaken in partnership with Federal Reserve Supervisors, buy-side companies, trade associations such as ISDA (the International Swaps and Derivatives Association), various technology platforms and an array of industry vendors. The resulting efforts reflected mutually agreed on desire for greater control, efficiency, transparency and increased automation throughout the derivatives trading and settlement process.

Brian Turkfeld, J.P. Morgan’s representative on the industry’s Operations Steering Committee (OSC), outlined how the derivatives markets will move to more robust automation and improved operational standards via key targets and industry-wide system enhancements. These measures will provide greater opportunity for real-time settlements via streamlined processes, rapid resolution of trade discrepancies and increased clearing eligibility through various methods.

“This new series of commitments represents not only a powerful statement of intent, but is also evidence of positive action from the entire derivatives industry,” Mr. Turkfeld noted. “The resulting communications with the regulatory community and supporting service providers reflect a

Buy-side Partnership drives Beneficial Changes to otC derivatives landscape

Aspartofourcommitmenttoproactivelylistentoclientsandintegratetheirperspectivesintoourday-to-dayoperations,J.P.Morganhascollaboratedwithothermajordealersandbuy-sidefirmstocreatecontinuedstructuralimprovements in the global OTC derivatives markets.

Winter 2011 / J.P. Morgan thought 11

Jan.

07

—

Apr.

07 —

Jul.

07 —

Oct

. 07

—

Jan.

08

—

Apr.

08 —

Jul.

08 —

Oct

. 08

—

Jan.

09

—

Apr.

09 —

Jul.

09 —

Oct

. 09

—

Jan.

10

—

Apr.

10 —

OBJeCtiVe 3 To drive a high level of product, processing and legal standardization in each asset class with a goal of securing operational efficiency, mitigating operational risk and increasing the netting and clearing potential for appropriate products (recognizing that standardization is only one of several criteria for clearing eligibility). Accordingly, workstreams have been established to analyze existing, and where appropriate, potential opportunities for further standardization by asset class and by product.

OBJeCtiVe 4 To continue to work to enhance bilateral collateralization arrangements to ensure robust risk management, including strong legal and market practices and operational frameworks. In particular, continue the work on resolution procedures for variation margin disputes arising out of bilateral derivatives transactions, and on publication and adoption of best practices among the Members and other signatories. Additionally, continue the consideration of the risks, mitigants and enhancements associated with initial margin.

OBJeCtiVe 5 To build on improvements in operational performance, with a focus on moving away from manual processes and driving increased automation, straight-through-processing, and trade date matching, affirmation and processing.

Mr. Turkfeld also noted that in less than a year, the industry had taken the following steps towards achieving these key milestones:

• Implementation of a revised and formal ISDA Governance framework, with increased participation of the buy-side in developing the strategic agenda, policy formation and decision-making. The newly created ISDA Industry Governance Committee (IIGC), under the auspices of the ISDA Board, provides governance and strategic direction for the product level steering and working groups, and acts as a focal point for the Supervisors and legislators to engage effectively with the industry.

• Significant progress on product standardization for Credit Derivatives, including, the completion of the 2009 ISDA Credit Derivatives Determinations Committees, Auction Settlement and Restructuring CDS Protocol (often referred to as the “Small Bang”), which allowed existing Credit Derivative contracts to be modified to provide for Auction Settlement for Restructuring Credit Events.

• The successful launch of CDS clearing in Europe and the recent launch of Single Name clearing in Europe and North America.

• The initial extension of clearing services to the buy-side, with the launch of initial client access to the clearing of Credit Derivatives and Interest Rate Derivatives.

120%

100%

80%

60%

40%

20%

0%

Significant increase in electronic Processing Over the Past 3 Years electronically Confirmed vs. eligibility

electronically confirmed as a % of electronically eligible (Credit)

electronically confirmed as a % of electronically eligible (equity)

electronically confirmed as a % of electronically eligible (rates)

• Significant progress in the implementation of global data repositories, with the successful launch of coverage for Credit Derivative and Interest Rate Derivative products. In addition, the selection process for the global data repository for Equity Derivative products launched on schedule. Substantial progress has also been made in implementing global data repositories.

• Delivery of proposals for improvements to OTC bilateral collateral processes (please see accompanying article on “Best Practices for OTC Derivatives Collateral”.)

• Continued improvement in industry infrastructure, as measured by further reduction, and, in some cases, elimination, of unsigned transaction confirmation backlogs, and continued improvement in operating performance metrics.

“Our partnership has led to significant progress over a number of years and we plan to build upon the industry’s success,” states Mr. Turkfeld. “We also believe derivative products are a vital hedging instrument for the market. As an industry, we look forward to maintaining a solid partnership with the regulatory community to implement prudent enhancements to the product landscape.”

12 J.P. Morgan thought / Winter 2011

As a consequence of this review, governmental bodies and regulators have been assiduously prescribing remedies that will affect the end-to-end processing of an OTC transaction. Most of the foreseeable changes will incur costs in the provision of new service requirements, project implementation, and further staffing needs. This is in addition to the tangible expense of tying up capital to conform to prescribed collateral management principles.

This article will examine how we expect the various stages of post execution processing to change, and focuses primarily on trade management, collateral management, trade reporting and transparency, as well as highlighting any cost implications that OTC industry participants will need to consider in this changing environment.

time for “t Processing” The past decade has seen the OTC industry, primarily led by the sell-side, proactively move towards processing of OTC trades on trade date, or “T processing”, in order to execute legal contracts in a timely manner. The move towards standardised OTC derivatives contracts, with the ultimate aim of pushing these contracts to a central clearing party (“CCP”), will have a profound impact on post execution timeliness and efficiency.

The requirement for central clearing will expand the concept of “T processing” beyond today’s confirmations processing and matching on MarkitSERV DSMatch1. Decisions will need to be made promptly and activity completed within a matter of minutes of a trade being bilaterally agreed between a dealer and its counterparty. Any incomplete “T processing” could trigger fallback bilateral processes for trades that were initially intended for clearing. Therefore, technology infrastructure will need to be as present and resilient in post-execution activity as it is today in pre-execution for clearing to be a successful solution for any buy-side participant. “Middleware” platforms developed by industry vendors such as MarkitSERV, ICE and CME will become indispensible in navigating complex and time sensitive process flows that involve, at a minimum, the investment manager, a dealer, a clearing broker and a CCP. OTC transaction capture infrastructure for both position and lifecycle management is expected to entail the adoption of robust and scalable solutions that can analyse or identify transactions eligible for clearing, and consequently track and monitor their progress

Marketturmoiloverthe last fewyearshasdampenedenthusiasm in trading of Over-The-Counter (“OTC”) contracts and prompted both OTC industry insiders and outsiders to scrutinise various aspects of systemic risk.

ThE ChAngIng COSTOfDERIvATIvES

Winter 2011 / J.P. Morgan thought 13

towards expected acceptance by CCPs. Whether developed in-house or purchased through a vendor, the effort for integration within a firm’s technology architecture should not be underestimated.

In addition to infrastructure considerations, industry participants will need to re-assess their operating models and team structures. Responsibility for certain post execution processing such as affirmations with executing brokers, allocation and selection of transactions against appropriate clearing broker and CCP, may require closer realignment to front office desks and trade support teams.

Collateral is CallingCollateral management practices will change, mainly due to the expected requirement to utilise CCPs for eligible OTC transactions. Investment managers will need to revise bilateral agreements with their dealers, understand the margin processes that clearing brokers will implement and set up various forms of segregated accounts related to CCP processing. There will be new requirements for collateral to be posted at initial transaction. In addition to the opportunity cost presented by this upfront cashflow requirement, investors’ ability to dispute any ongoing collateral calls due to valuation fluctuations is expected to be limited, unlike today’s status quo. CCPs will dictate the margin calculation process using their own valuations, leaving no room for clearing brokers or the underlying investors to challenge any calls. It is therefore important that market participants will have the capability to reflect and source the appropriate valuation against each position, and clearly distinguish between cleared and non-cleared OTC transactions within their collateral management processes.

Automation and messaging will be the key to success. However, OTC collateralisation practices today are not performed under a common messaging standard. Through an ISDA-sponsored collateral committee, industry practitioners published “Standards for the Electronic Exchange of OTC Derivative Margin Calls”, in November 2009. With the advent of central clearing, it is expected that such recommendations will be expanded to include central clearing practices and gain momentum for industry adoption. Buy-side, sell-side and service providers will all have the equally shared responsibility of ensuring that investment is made available to adopt automated practices within their firms and therefore achieve collective benefit across the industry.

reporting that the Price is rightTransaction processing and collateral management are two of the relatively simpler areas to identify impact. The reality is that central clearing and associated OTC legislation will bring

with it a number of variables that buy-side participants will need to tackle.

Reporting is an obvious area of impact, whether for the purpose of producing net asset value or “NAV”, for feeding information to service providers, compliance and risk teams, or for any future regulatory transparency requirements. With so many parties now having a stake in what was traditionally a bilateral transaction, the dissemination of comprehensive and accurate information will be key to ensure that all needs are satisfied. Tactical or workaround solutions so far have served the purposes of OTC position and lifecycle management; however, smaller firms may struggle with the demands of what should be a dedicated, scalable and robust OTC infrastructure and operating model.

The move towards “third party” or “independent” valuations has been prevalent over recent years within the buy-side. There is no guidance to suggest that this will change in the near future. Each CCP will adopt its own valuation policies. This alone creates an inconsistency for a fund’s pricing methodology across bilateral and cleared trades that will only be compounded by the available choice of CCPs that will compete against each other to clear the same asset classes. Firms who have outsourced instrument pricing to valuation providers should not expect to cut their spending any time soon, unless they are prepared to increase resources of their internal teams appropriately to understand the changing landscape and implement their own price exploration and verification functions. In addition, fund pricing committees will need to re-evaluate the definition of the “right price” for a cleared OTC and its appropriate use for collateral margin and NAV calculations. For many firms, direction will need to be set without necessarily finding comfort in industry consensus from the outset.

the Final Stage If we transpose the Kübler-Ross model to our OTC industry which views the path from a crisis through the stages of ‘Denial’, ‘Anger’, ‘Bargaining’, ‘Depression’ to ‘Acceptance’, we must all be at the final stage. Denial should have been the first to go with Lehman’s collapse in 2008. Anger would have shortly ensued in the aftermath and through the 2009 recession. More recently, bargaining with governmental bodies and regulators has been the highlight of the first half of 2010, concurrently with depression as no one is spared from the impact of the forthcoming legislative changes. So at this final stage of acceptance, we must prepare and recognise the appropriate investment required in advance to achieve it all. Historically, buy-side institutions have lagged behind the pace of larger sell-side institutions when it comes to such change. Work should have already begun.

1 Formerly DTCC Deriv/SERV

14 J.P. Morgan thought / Winter 2011

OTC derivatives clearing will become increasingly critical as the future direction of OTC derivatives markets is being influenced by financial reform in both the United States and Europe. The Dodd-Frank Act in the U.S. and the European Markets Infrastructure Regulation (EMIR) in Europe are, in principle, similar with respect to the regulation of OTC derivatives markets. One component of both reform packages includes the mandatory clearing of OTC derivatives, including Credit Default Swaps (CDS) and Interest Rate Swaps (IRS), by most investors at central counterparties (CCPs).

the Path to Clearing

CLeArinG HOuSe

➤ Risk management/control➤ Segregationofinitialmargin➤ Default management➤ Impliedguaranteefundcontributions➤ Legal basis against hedges held bilaterally or in

other clearing houses➤ Timing and conditions of the clearing house

guarantee to be in force➤ Operational Readiness • Connectivitytomiddlewareandotherindustry

infrastructure • Abilitytoprocessproducts • Tradeeventprocessing

(e.g. coupons, credit events)

PresidentObama

signs bill

SEC/CfTCrule writing

period

EuropeanCommission

initiatesEMIR,Short-sellingandSovereignCDS

Legislation

EuropeanCommission

initiatesCRDIvLegislation

MifIDproposals on Transparency

and Trade Reporting

PoliticalAgreementinEuon

MandatoryClearing

SecondaryLegislation

July 2010

July 2011 – December 2011

September 2010

December 2010

February 2011

July 2011

December 2011

December 2012

May 2010

ImplementationDate

Senate bill

passes

MandatoryClearingeffectivethelaterof 360 days from signing – July 2011 OR 60 days after rule writing completion

Considerations When Choosing Your:

CLeArinG BrOKer and PriMe BrOKer

➤ Credit and Risk • Creditworthiness • Marginingregime • Crisismanagement➤ Operational readiness • Technologyinvestment • Connectivitytoclearinghouses,executingbrokersandclients • Knowledgeofoperationalstaffandabilitytoadviseclients • leadershipindefiningtheindustryoperatingmodeltobenefit

their clients➤ Abilitytoprovidetraditionalprimebrokerageservices,and

intermediate trades that cannot be cleared➤ Consolidated reporting across cleared and non-cleared trades➤ Singlepointofcontactforoperationsstaffacrossmultiple

clearing houses and non-cleared trades

Winter 2011 / J.P. Morgan thought 15

Dave OlsenGlobal Head of OTC Clearing

PrODuCt SCOPe

enD-uSerS requireD tO CLeAr

rePOrtinG OBLiGAtiOnS

MAnDAtOrY eLeCtrOniC trADinG

BACKLOADinG

riSK MitiGAtiOn FOr nOn-CLeAreD trADeS

u.S. (Dodd-Frank Act)

All categories of OTC derivatives, including interest rate, credit, foreign exchange, equities and commodities, but limited to derivatives on specified underlyings. Spot foreign exchange (FX) transactions appear to be excluded, as are commercial forward foreign exchange transactions and some kinds of physically settled commodities.

The clearing obligation applies to financial counterparties, which includes banks, investment firms, insurance companies, registered funds (UCITS), pension funds and alternative investment fund managers.

Financial counterparties must report the details of all their OTC derivative contracts to a registered trade repository.

No equivalent provisions in the proposed EU Regulation, but due to be addressed in a MiFID review in Q1 2011.

Required to submit to trade repositories.

Products not required to be cleared carry new obligations, in addition to reporting, including:• Electronic confirmation • Tracking of valuations • Reconciliation of portfolios• Proactively manage collateral• Link to capital requirementswhere applicable

A broad class of OTC derivatives that are commonly known as swaps. Spot FX does not appear to be included, and the Treasury Secretary has the ability to exempt both FX swaps and forwards from the clearing obligation (but not other obligations within the Act). Certain physically settled commodity transactions (but different from the EU exclusions) and certain physically settled forward transactions in securities are also excluded.

The clearing obligation applies to anyone who enters into a derivative subject to the clearing obligation, other than those end-users who are exempt (as described below).

Any swap must be reported to a registered trade repository.

The Bill requires that swaps eligible for clearing must be traded on an exchange or executed through a swap (or security-based swap) execution facility (“SEF”), if the relevant instrument is listed by an Exchange or traded on a SEF. The Bill defines a SEF as, generally, a trading system or platform in which multiple participants have the ability to execute or trade derivatives by accepting bids and offers made by other participants, including a facility that facilitates the execution of security-based swaps in particular. Swap Execution Facilities must be registered as such (or as a “designated contract market” under either the Commodity Exchange Act or the Securities Exchange Act) and comply with certain core principles (including timely publication of trade data to the extent prescribed by the relevant commission).

No clearing requirement, but required to submit to trade repositories.

Imposes capital and market requirements on swap dealers and major swap participants that enter into uncleared swap transactions. There are also provisions giving counterparties the right to require swap dealers or major swap participants to segregate initial margin on uncleared swaps.

eu (eMir)

uS Dodd-Frank Act and eu Legislation ComparisonIn this table we summarize how both the proposed EU legislation and the Dodd-Frank Act consider different categories of counterparties and highlight certain other differences between both texts in relation to the trading and clearing of OTC derivatives.

J.P. Morgan continues to monitor industry and regulatory developments and works to enhance our OTC clearing and intermediation services offering to enable our clients to meet these evolving commitments. We encourage clients to contact us for a more detailed conversation on the impact to clients and the wider industry.

Information correct as of November 17, 2010.

16 J.P. Morgan thought / Winter 2011

The Over-The-Counter (OTC) derivatives business is very dynamic, experiencing a significant growth in trading volumes over thelast ten years. This growth has been accompanied by an increase in the number of new products requiring technical support, regulatory changes and industry wide initiatives.

platform to meet the challenges posed by a greater need for OTC derivatives processing capabilities.

DerivClear™

DerivClear™ can provide connectivity for both technically advanced clients and clients with limited technical capacity. Technically advanced clients can take advantage of several electronic trade capture methods such as: FpML over SWIFT, Secure web services over the internet or point-to-point, guaranteed messaging. However, in some cases the investment to implement these solutions may not be viable. For low volume clients or those with limited technical capacity there are simpler options such as manual trade entry directly into the DerivClear™ web application, spreadsheet uploads or sending files using secure File Transfer Protocol (FTP).

Once connectivity is established all parties have to agree on the format of messages to be processed. While the standard message

the Challenges of stP in otC derivatives Processing

to providing STP solutions. The most demanding of these include:• Connectivity between parties• Standard message formats• Minimum data requirements• Common reference data• Performance and scalability

While these issues can be challenging for large market participants, they represent acute difficulties for smaller market participants that do not have large technology departments, or none at all that would allow them to support these new challenges. In response to this need, J.P. Morgan’s Global Derivative Services Group (GDS) has developed the DerivClear™

As a result of the financial crisis and subsequent regulatory reform, the Financial Services Industry is facing major changes in the way OTC derivative products are traded and processed. The three key themes of these changes are: contract standardization, central clearing and enhanced market transparency (via trade warehouses).

To support these initiatives there will be an increased need to focus on STP solutions. The imperative to effectively pass data between counterparties, central clearing houses, service providers and trade warehouses in a timely manner will undoubtedly necessitate enhanced STP capabilities. There are many challenges

Winter 2011 / J.P. Morgan thought 17

Clients that use OTC derivatives as a part of their strategy realize the value that J.P. Morgan offers in managing all or part of their derivative operation. J.P. Morgan provides OTC derivative processing services through the DerivClear™ platform, provided by Global Derivatives Services (“GDS”). GDS is part of the broader Global Fund Services product suite within J.P. Morgan Worldwide Securities Services and is integrated with other offerings, such as Fund Accounting.

Through DerivClear™, clients have web-based access to a broad range of operational services across the OTC trade lifecycle including trade capture, lifecycle management, confirmation, settlement, independent valuation management and reconciliations. The platform supports all the major OTC asset classes consisting of various individual instrument types, and DerivClear™ is able to fully support the majority of buy-side firms’ OTC processing requirements.

Dedicated highly skilled GDS teams across the globe support the DerivClear™ platform through our processing powerhouse centres in Bournemouth, London, New York and Mumbai, to help ensure that clients receive a best in class solution. Our Valuation Control Group (‘VCG’) offers flexible in-house production, verification and valuation transparency of OTC valuations. In addition, VCG maintains partnerships with a number of third party valuation providers for comprehensive valuation coverage on clients’ portfolios.

J.P. Morgan’s ongoing investment in the GDS proprietary infrastructure, combined with access to the leading OTC utilities and services and close collaboration with the J.P. Morgan Investment Bank, enables GDS to keep our offering up-to-date at a time of unprecedented industry change.

Clients choose DerivClear™ to help them achieve increased efficiency. Historically, clients may have employed

several different applications to support OTC portfolios for several reasons. For example, different OTC asset classes (i.e. rates vs. credit) or operational processes (settlements vs. confirmations) may each be supported in a different system. DerivClear™ provides clients with a single system to capture a client’s entire OTC portfolio, regardless of asset class or process. Having a single repository for all OTC positions and processes allows for greater STP rates that mitigates the risk of manual errors.

A key driver for a DerivClear™ client is the advantage of a controlled settlement process. Cashflows are calculated based on trade terms captured on the platform. Customized settlement rules (netting agreements, SSI retention) are applied to generate actual OTC flows with each of a client’s OTC counterparty. DerivClear™ offers clients a robust, controlled approval process, where authorized flows are automatically instructed via an electronic interface with the bank or custody. There is a reconciliation in place to ensure that expected settlements occur.

Clients also experience a reduced cost basis by utilizing DerivClear™, avoiding the high capital investment associated with building their own platform and employing a large technical and operational support staff. DerivClear™ costs are variable and are based on the clients’ actual activity volumes.

Finally, through DerivClear™, clients gain access to market confirmation and reconciliation platforms like DTCC, Markit PortRec, and other utilities built into the platform as workflow tools. All this allows clients to focus on core investment and risk decisions, and leave the operational component to GDS through the DerivClear™ platform.

DerivClear™ Won The Banker “Innovation in Custody and Securities” Award, 2009.

DerivClear™ An OtC Processing Solution through Advanced technology

format in the industry is FpML, there are many different versions of the standard and clients have different interpretations of where to provide the data within the message schema. DerivClear™ leverages a proprietary solution called Information Exchange (IX) to transform such messages into a format that it can process. The IX tool can also be configured to handle non-standard spreadsheets or file based formats.

The data requirements for OTC derivative trades are highly complex and vary for different financial products. Many clients struggle to capture and provide the prerequisite level of detail on every trade. DerivClear™ provides the capability for clients to set up and utilize trade templates which enable the system to default necessary information that is not provided as a matter of course on individual trades. Common reference data such as trade or security identifiers and counterparty names can also present a challenge. Identifiers must agree as part of the on-boarding process and setup to be useable by both client and GDS. DerivClear™ has the ability to store and utilize multiple identifiers as part of the trade record, thus allowing clients to reconcile to their own internal systems.

SummaryIn order to successfully support STP for OTC derivatives, processing systems must be robust and scalable. As past experience indicates, these products can have tremendous growth potential. While they may start out as low volume niche products, specific OTC instrument types can quickly become high volume products. DerivClear™ is built on a robust architecture that can easily be expanded to respond to increased volume and demand.

Both buy-side and sell-side participants in the OTC derivatives market should consider the need to build these new capabilities in-house or leverage a service provider for a solution. For those that choose to go with a service provider the STP and scalable capabilities of the provider should be a major factor in their decision.

18 J.P. Morgan thought / Winter 2011

The implementation of the UCITS Product Directive in November 2002, coupled with market and industry pressures resulting from events during and since the financial crisis precipitated by the collapse of Bear Stearns and Lehman Brothers in 2008, have increased the focus of legislative and regulatory bodies on Over-The-Counter (“OTC”) derivatives, especially for fund managers. In addition to existing requirements in relation to the timeliness and accuracy of OTC valuations, there are new and enhanced regulatory requirements which include the provision of greater transparency and independence in relation to the valuation of OTC derivative instruments. Regulators and investors have challenged the hitherto existing protocols regarding the use of unverified counterparty valuations in determining the NAV of fund holdings. As a result of the confluence of interests of regulators, investors fund managers and fund administrators have had to adapt and find solutions for sourcing independent valuations. J.P.Morgan’s Global Derivative Services (“GDS”) offers clients the ability to address such requirements through its Valuation Control Group (“VCG”) and the DerivClear™ platform.

What We DoLeveraging the expertise of the Global GDS team with locations in London, New York, Bournemouth, Sydney and Mumbai, VCG offers the in-house production of transparent and verifiable OTC valuations of its client portfolios. VCG also maintains partnerships with a number of Third Party Valuation (“TPV”) providers to ensure comprehensive valuation coverage of clients’ portfolios.

There are three critical areas of focus in the valuation process:1. Independence 2. Accuracy3. Transparency

To facilitate the first of these processes – independence – GDS created the

In addition, both J.P. Morgan and TPV valuation models are subject to quality and appropriateness tests to determine their suitability to produce valuations. The testing is undertaken by the GDS OTC Research & Development (R&D) team. Tests around J.P. Morgan models consist of a calculation verification step and a valuation validation, stress testing and benchmarking sign-off. For a TPV sourced model a comprehensive valuation benchmarking exercise is performed by GDS R&D. Subject to product and model complexity, the model review process will be conducted on a risk rated basis, reviewing complex models more frequently than vanilla models. To ensure that best practice is observed for both the initial and ongoing model review, VCG shares all model documentation testing procedures and results with J.P. Morgan’s bank-wide Model Risk Group (MRG). Model and market data documentation is also distributed to clients in the interests of transparency.

Strong process management and specialist training relating to the regular valuation service are critical. These include robust and scalable upfront trade capture controls, a thorough understanding of the trade terms based on an in-depth knowledge of derivative instruments and timely and effective trade life-cycle processing. Furthermore, VCG perform day-on-day valuation movement monitoring against pre-determined thresholds, while the GDS reconciliation team performs daily trade detail and valuation reconciliations against the counterparty on the trade to capture material differences. Any material valuation differences will be investigated by VCG to ensure the integrity of the GDS valuation.

Finally, DerivClear™ functionality allows for automated feeds from multiple vendors. This permits the sourcing of valuations from multiple providers for the same trade every day. Having access to a choice of in-house and vendor pricing packages enables GDS to compare valuations from multiple independent valuation sources alongside

DerivClear™ platform, which was designed to deliver trade capture, lifecycle management, confirmations, settlements, independent valuation management and reconciliation functionality for OTC instruments. It also acts as a depository for multiple valuations. The platform has been built to have direct links to the J.P.Morgan Fund Accounting, Derivatives Collateral Management and Investment Analytics business units.

How We Do itVCG provides independent valuations for OTC derivatives with interest rate, equity, credit, FX, commodity, and property underlyings. VCG’s focus offers a ‘best of breed’ service by utilising the in-house valuation platform coupled with a network of TPV providers covering a comprehensive range of both vanilla and exotic instruments.

The provision of independent valuations is based on industry standard models and valuation techniques and the timely and comprehensive capture of market data across multiple asset classes (data capture extends to 50,000+ data points, daily, as required by asset class and currency). The instrument valuation process follows a rigorous pricing policy which adheres to the following steps:

a) Conduct initial and ongoing model validation reviews in order to ensure that valuations are produced in accordance with market standards. This involves reviewing the pricing model from first principles to ensure that VCG has the correct model for the instrument.

b) Conduct initial and ongoing market data reviews to ensure there is consistently accurate input into the valuation process.

c) Perform daily market data and valuation controls in order to check market data and valuation moves against defined tolerances and ensure that values move in line with underlying market data moves or trade lifecycle events.

vAluATIOnSProviding Accuracy and Independence

Winter 2011 / J.P. Morgan thought 19

counterparty and clients’ own valuations to ensure appropriate robustness in the valuation process.

Challenges & DevelopmentsWhile valuation models are available from a multitude of sources, the biggest challenge in relation to producing accurate independent valuations is obtaining quality market data. Data quality is critical to the valuation process and poor data will lead to less accurate valuation results. Furthermore, specific financial instruments can provide different data challenges and, sourcing extensive volatility surfaces and correlation data can be challenging and also costly.

In addition to data quality, data transparency is of crucial importance. Knowledge of what valuation models and data sources are used and what constitutes the process of how a valuation is produced are of paramount importance to understanding the utility of a given valuation.

The ongoing review of market data providers and model governance is critical to stay abreast of market developments. VCG works closely with the GDS client relationship managers to ensure the GDS instrument range stays abreast of fund manager requirements. As asset managers diversify their portfolios, VCG will continue to partner with them to ensure new instrument requirements are understood and managed in a timely manner.

Future StateThe provision of OTC derivative valuations is moving more in line with the long established process in the securities market where it is common to receive ‘prices’ from multiple valuation providers and a pricing hierarchy for any given ‘instrument’. Ever increasing numbers of specialised independent OTC derivative valuation providers are making this approach feasible for derivatives. GDS co-operates with such

providers in order to offer its clients as much choice as possible in obtaining and comparing independent valuations.

Through increased regulation and competitive pressures, transparency in how the value of any particular derivative has been determined is also increasing. This focus on price transparency should give client pricing committees and risk

InterestRatesSwaps OverviewAninterestrateswap(IRS)isanagreementwheretwocounterpartiesagreetoaperiodicexchangeofcashflowsforasetlengthoftimebasedonaprincipalamount.Onecashflowisbasedonafixedinterestrateandtheotheronafloatingrate.Thefixedrateissetatthecontract’sinceptionandthefloatingrateisreferencedtoaratethatvariesovertimesuchasthelondonInterbankOfferedRate(lIBOR),butotherreferencerateindicesmayalsobeused.

Ontheswapeffectivedate,thevalueoftheswapistypicallyzeroandnofundsareexchanged.Thetimespanbetweentheeffectivedateandtheterminationdateisdividedintopaymentperiods.Thefirstdateineachperiodistheresetdate;thevalueofthefloatingindexonthisdateisusedtodeterminethefloatingrateusedforpaymentsmadeattheendoftheperiod.Thefloatingrateisusuallyreseteverythreeorsixmonthsoverthelifeoftheswap.Thediagrambelowshowsthepaymentsthatcompriseatypicalorplainvanillaswap.WhileIRSdo not strictly adhere to these guidelines, most follow them as a general principal. The non-generic,morecomplicatedswapsvaryintiming,treatmentofprincipalandcashflows.

Bycomparingthefloatingratewiththefixedrate,paymentsaredeterminedbasedonanotionalamountandthedifferencebetweenthetworatesisnettedandthevalueispaidbetweencounterparties.forexample,iflIBORisbelowthefixedrate,thenthebuyer(fixed-ratepayer)paysthedifferencetotheseller;iflIBORisabovethefixedrate,thentheseller(fixed-ratereceiver)paysthedifferencetothebuyer.

Valuation Approachforaplainvanillaswap,thepresentvaluesofthefixedandfloatinglegsareaddedtogether.Allswaps have the same basic valuation function, as shown in the equation below:

managers the information they need to demonstrate successful oversight of their fund valuations. VCG engages with clients, either through visits, or the provision of pricing models, with the aim of ensuring that the independent valuations produced by GDS are clearly understood.

The rising prominence and importance of central counterparties will change current valuation delivery standards. We expect increased demand for same day valuations rather than the traditional T+1 approach. In addition, even with central counterparties supplying valuations for collateral purposes, we still expect the need for additional independent values to ensure that asset managers are able to price consistently across their entire portfolio and provide comparison and/or verification points.

PartyA PartyBFloating Payment LiBOr

Fixed Payments

PvofIRS=fixed*dft—floating t*dft

t=T

Σt=1

t=T

Σt=1

20 J.P. Morgan thought / Winter 2011

idea of the “sensitivity” of the equities compared to the other asset classes in the portfolio.

At that point, it is possible to determine a range of larger increments to analyze how the sensitivity evolves as the risk factors are shocked more dramatically. Sensitivity Analysis can provide some information on how the VaR reacts to shocks of various amplitudes on various risk factors. Furthermore, it is feasible to shock various factors at the same time within the same scenario. But without running individual shocks first, it will be hard to interpret which factor explains most of the new VaR estimate as correlations might have changed. In this instance, the risk manager needs to think as an economist more than as a quantitative analyst or to work with colleagues in the Research department to integrate their view on various asset classes, regions, currencies, etc.

It is also interesting to shock these risk factors over a longer period of time than only at the end of the analysis horizon (generally, one day or one month). This way, you can generate different shocks that will apply to some risk factors over a few time horizons. For instance, we can recalculate a VaR on a portfolio where we have amended the exchange rates amongst the two main currencies with the following shocks: -10%, +5%, and -15%. Studying the historical movements of these two currencies can provide some information to project various scenarios on how the market could evolve over the next few time intervals. This is where Sensitivity Analysis meets with Scenario Analysis as this last approach could be seen as a Customized Stress Test.

Despite its simplicity, this methodology also has some pitfalls. The risk manager needs to exercise some judgment in determining the optimal size of each shock which may differ from one asset class to another. These shocks must also be reassessed on a regular basis to avoid missing a change in the

VaR attempts to answer the question of how much a portfolio may lose if it remains unchanged over a given time horizon under normal market conditions at a given level of confidence. But VaR does not measure how adversely a portfolio may be affected if a sharp unfavorable movement occurs in these so-called normal markets, so it should not be taken for the panacea of risk measures. It is a starting point that we should tweak, distort and stress in order to better understand its behavior as we amend the assumptions it relies on. It is a tool that requires further tuning to provide a richer view of the risk of a portfolio.

Although VaR is one of the most widely discussed and evaluated risk measures, stress testing may be one of the most critical risk analyses that complement VaR. Stress testing is a tuning process by which we can explore how the portfolio would react to small (Sensitivity Analysis) or more drastic (Scenario Analysis) changing conditions in the markets. We review in this article various approaches to stress a portfolio and derive the pros and cons of each methodology in terms of time, complexity, cost, resources, level of reporting, frequency and specific needs (regulatory requirements, for instance). Table 1 provides a summary of the various forms of stress tests.

Sensitivity AnalysisSensitivity Analysis consists of shocking various risk factors of the portfolio with small upward or downward increments. It is very simple to implement and can be quickly automated in a systematic way. Examples of shocks are imposing a fall of all equity prices in the portfolio or proceeding to a parallel shift of the yield curve to shock the bonds included in the portfolio. In the former example, we will impose all equities to have a price 10% lower than they are at the moment. We rerun our VaR calculation and compare it with the VaR without the 10% equity shock. That might give us a rough

As portfolios have increased their complexity through the use of derivatives, strong riskmeasurement has become more important than ever. During times of high market volatility, risk measurement techniques and methodologies typically face greater scrutiny and analysis. Numerous approaches to measuring downside risk have been developed and fine-tuned in recent years.Oneofthemoredebatedriskmeasurementcalculationshasbeenvalue-at-Risk(vaR).

value-At-Risk: stress testing

Winter 2011 / J.P. Morgan thought 21

fail. This is an appealing idea in the sense that instead of starting from the existing standpoint and seeing how close we can go towards the edge of the cliff without falling, reverse stress testing tells you what risks you could take to fall directly off the cliff. However, the main problem with reverse stress testing is “how” to do it? There are so many reasons why an institution would fail that it may take some time to determine meaningful stress tests. When we conduct other types of stress testing, we always start from the known: the portfolio itself and its VaR and try to progress more or less in the dark to gauge the risks ahead. With Reverse Stress Testing, we start from the unknown and try to figure out how we became lost on the way. This intellectually challenging thought could soon become a tedious task where one tries to assess which events could have triggered the failure and how this event has contaminated the entire system. There is no easy answer to this problem but there are forms of statistical analysis that could be a starting point.

ConclusionJ.P. Morgan believes that stress testing is more important than calculating the VaR in isolation. Of course, a minimum of effort needs to be put in place to compute an accurate VaR estimate, but at least an equal amount of time and effort must be spent to analyze its sensitivity to various shocks and stress events. We like to think that we construct a view of the risk profile of a portfolio by estimating VaR, a single number which helps manage the portfolio at a high level. But we should deconstruct this estimate with stress testing to obtain a more granular understanding of its sensitivity and weaknesses.

pattern of one specific asset (sudden and brief increase in volatility) or a correlation increasing between two assets. Also, since we only shock one factor at a time and with a very small change, the analysis is very local.

Scenario AnalysisScenario Analysis aims to identify extreme events that could trigger catastrophic losses in a given portfolio. Per definition, the shocks that are applied to the portfolio are of much greater amplitude than those used in a standard Sensitivity Analysis. Mainly, there are three types of Scenario Analysis: historical, customized and reverse stress testing.

Historical scenarios intend to test the healthiness of a portfolio by analyzing what would happen to the portfolio if particularly adverse and unexpected movements which occurred in the past would hit the portfolio in the near future. Some well-known examples of historical scenarios are the Russian Crisis of 1998, the attacks of 9/11, and more recently the Sub-Prime Crisis. The main advantage of these types of scenarios is that they really did happen! But even if the temptation is great to use these historical scenarios off the shelf and to systematically apply them on any types of portfolio, the risk manager should choose historical scenarios very carefully and review them on a regular basis as the composition of the portfolio changes, but also because of a few dangers.

First, we need to select the historical scenarios that are the most relevant to the portfolio. Second, we should determine the start and end dates of the historical scenario. Third, what do we do with the instruments that will reach maturity during the re-enactment of these events? You can roll them over or

decide not to, depending on your strategy or on the size of these positions. In either case, cash flows need to be taken into account appropriately. Fourth, do you apply an absolute or a relative shock to the risk factors? Generally, we perform relative shocks but that depends on the risk factor (for instance, it is better to shock volatility on a relative basis). Fifth, what do we do about missing instruments? What is the point of applying the Black Monday scenario to a portfolio of CDS? Further, if historical data are not available on all risk factors, one should either proxy them or proceed to an interpolation (more relevant to fixed income instruments where the term structure may need to be filled in and out throughout). Finally, we should point out that historical scenarios produce a loss estimate and not a VaR. Therefore, the likelihood of seeing a historical scenario come true remains unknown.

In order to fix some of these drawbacks, one can design some specific stress tests based on historical scenarios or on areas of vulnerability in the portfolio. These stress tests are called customized since they respond to a particular purpose such as shocking correlations, stressing a liquidity squeeze, or creating a scenario which is more likely to impact a portfolio than historical scenarios would. These scenarios can be economic, political or financial. The complexity of the scenario depends on various factors such as number of risk factors, period of time the pre-defined scenario is expected to last, complexity of the portfolio, number of positions in the portfolio, running time, staff, cost, etc. In a nutshell, there must be a trade-off between the constraints of establishing a complete program of customized stress tests and the desired outcome.

Reverse Stress Tests attempt to identify the risks that would lead an institution to

table 1 – Stress testing Methodologies

Methodology Forms Pros Cons

SensitivityAnalysis Incremental flexibility,automation localexploration

ScenarioAnalysis historical Actualevents limitedrelevance Customized flexibility,automation Resourcesandtimerequirement Reverse “How to break down the house” Difficult to implement

22 J.P. Morgan thought / Winter 2011

Because derivative trading is bilateral by nature, even slight timing differences in trade life cycle events can have negative repercussions for both parties when exchanging collateral.

It is in the margin-call process, where each firm values its transactions independently, that collateral disputes can occur due to these seemingly subtle differences in operational process. [See diagram on facing page] These factors, when viewed through the lens of a regulator, can combine with other operational or valuation issues to create unnecessary risk and reduced liquidity among all participants.

As part of our rigorous culture of risk man-agement, J.P. Morgan continues to be a global leader in addressing these collateral issues, in partnership with the International Swaps and Derivatives Association (ISDA). Chartered in 1985, ISDA is among the world’s largest global financial trade associations with more than 820 member institutions from 57 countries on six continents. Members include most of the world’s major institutions that deal in privately negotiat-ed derivatives, as well as many of the businesses, governmental entities and other end users that rely on OTC derivatives to manage the financial market risks inherent in their core economic activities.

The industry group’s notable accomplishments include developing the ISDA Master Agreement; publishing a wide range of related documentation materials and instruments covering a variety of transaction types; producing legal opinions on the enforceability of netting and collateral arrangements; securing recognition of the risk-reducing effects of netting

new“BestPracticesforCollateral”

In the OTC derivatives market, the daily valuation oftrades and exchange of collateral has assumed new,heightened importance in the aftermath of the global credit crisis. Transparency and the need to reduce systemic risk now play a central role in how regulators seek to monitor risk in the market. This focus has increasingly taken center stage as traders seek to profit from derivative transactions, while firms simultaneously seektominimizetheircounterpartycreditexposure.

Winter 2011 / J.P. Morgan thought 23

in determining capital requirements; promoting sound risk management practices, and advancing the understanding and treatment of derivatives and risk management from both public policy and regulatory capital perspectives.

ISDA’s newly published June 30, 2010 “Best Practices for the OTC Derivatives Collateral Process” is intended to harmonize operational and collateralization practices for all current market practitioners, as well as establish expectations and standards for new participants. Firms should strive to use these guidelines as a benchmark to compare against their own internal policies and procedures as they look for gaps between internal and identified best practices.

These “Best Practices for Collateral” are the result of the collaborative efforts of a working group of buy-side and sell-side market participants, under the auspices of the ISDA Collateral Steering Committee, and will be updated periodically. J.P. Morgan chaired the industry effort by organizing meetings, soliciting feedback, building consensus and guiding the process through to its timely completion.

“J.P. Morgan is proud of its collaboration with the industry to advance best practices, improve processes and promote risk management which is the culture in which we operate every day for our clients”, says Arthur Magnus, global head of Credit Risk, Client and Reference Data Operations, J.P. Morgan Investment Bank.

The document also integrates additional ISDA industry work streams and initiatives, such as Portfolio Reconciliation, Collateral Dispute Resolution and Electronic Messaging. J.P. Morgan’s clients benefit from the new industry guidelines for collateral in several ways:

• Increased efficiency by leveraging operational standards across the collateral space and pushing for increased use of automation, especially for collateral calls and portfolio reconciliation.

• Mitigated risk by proactively reconciling portfolios to identify trade breaks causing collateral disputes and working in partnership with clients to more speedily resolve breaks.

• Maximizing security by migrating margin call distribution and response from e-mail to a secure web-based messaging platform.

The entire “Best Practices for Collateral” document can be viewed at http://www.isda.org/c_and_a/collateral.html. Topics covered by the document include:• CSA Set Up and Long Form Confirmations• Margin Requirement Calculations• Call Issuance and Response• Settlement of Call• Collateral Dispute Resolution• Fails• Assignments• New Trades/Unwinds/Credit Events/Compressions• Rehypothecation and Substitution• Collateralized Portfolio Reconciliation• Interest Processing• Tri-Party Reconciliation

For questions about any aspect of ISDA “Best Practices for Collateral” contact Mark Demo, Vice President, Investment Banking Collateral at [email protected] or Nichole Framularo, ISDA Head of Market Infrastructure at [email protected].

OPerAtiOnAL riSK

MitiGAtiOn

COnSISTEnTOPERATIOnAlPROCESSES

DATASTAnDARDSfORRECOnCIlIATIOn