Team Lease Employment Outlook Report: Half Yearly Special · Team Lease Employment Outlook Report:...

42

Team Lease Employment Outlook Report: Half Yearly Special Quarter-23, July-September 2012 A comprehensive and in-depth analysis of Employment and Business Outlook for the forthcoming half year; includes statistics for 8 cities and 8 sectors, literature review insights and depth-survey findings. inTouch analytics http://be-in-touch.com

Transcript of Team Lease Employment Outlook Report: Half Yearly Special · Team Lease Employment Outlook Report:...

Team Lease Employment Outlook

Report: Half Yearly Special Quarter-23, July-September 2012

A comprehensive and in-depth analysis of Employment and Business Outlook for the

forthcoming half year; includes statistics for 8 cities and 8 sectors, literature review insights and

depth-survey findings.

inT

ou

ch

an

aly

tics

http

://be-in

-tou

ch

.co

m

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

1

Literature Research & Depth Survey insights This edition of the Team

Lease Employment

Outlook Survey report

carries: a depth survey

that compiles thoughts

related to hiring and

talent retention which

respondents have shared

with us in addition to the

outlook for business and

hiring; anda literature

research

sectionthatstudies the

intensity of blue collar

workforce

employment,with the

help of an extensive

secondary research

exercise.

Preface

The TeamLease Employment Outlook Report is a forward looking tool

for human resource policy and decision makers, reflecting business

sentiment for hiring across cities and sectors. This report carries a

snapshot of business hiring sentiment for the next six months on the

basis of the survey and analysis carried out during the preceding 3

months.

The Employment Outlook Survey spans eight industry sectors and eight

cities across India. The survey covers small, medium and large

companies across these sectors, studies attrition and employment

trends, and gleans information on hiring sentiments, all this covering

different locations, hierarchical levels and functional areas.

As part of a recent feature we introduced, we have set out to invite

thoughts on hiring and talent retention from respondents that go

beyond hiring and business sentiment inputs we usually solicit from

them.

With the most critical drivers that influence hiring being tracked

continually, the Employment Outlook Report is the only one of its kind

seeking to deliver high impact hiring decision support to its

stakeholders – Business & HR heads, Senior Management as well as

industry policy makers.

The current edition also studies the intensity of blue collar workforce

employment across industries and investigates if it corresponds with

hiring intent, with the help of an extensive secondary research

exercise.

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

2

Contents

1. Executive Summary 2. Project Objectives 3. Index definitions

3.1. Employment Outlook Index 3.2. Business Outlook Index

4. Depth Survey findings: Hiring and Talent Retention 5. Employment Outlook

5.1. Net Employment Outlook 5.2. Net Employment Outlook Growth – by sector 5.3. Net Employment Outlook Growth – by city

6. Business Outlook 6.1. Net Business Outlook 6.2. Net Business Outlook Growth – by sector 6.3. Net Business Outlook Growth – by city

7. Hiring Intent 7.1. Hiring Intent by Location 7.2. Hiring Intent by Hierarchy 7.3. Hiring Intent by Functional Area

8. Other Trends 9.1. Employment Outlook Index – city-sector drilldown 9.2. Business Outlook Index – city-sector drilldown 9.3. Attrition trends by sector 9.4. Attrition trends by city

9. Annexure: Research Methodology 9.1. Sample Design 9.2. Respondent Selection 9.3. Data Collection 9.4. Secondary Sources

10. Sample Distribution 10.1. City-wise breakup 10.2. Business size-wise breakup

11. Reasons for Attrition – the employer perspective 11.1. By city 11.2. By sector

12. Insights: Literature Review

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

3

Executive Summary

The Apr-Sep, FY14 half year records a high level of optimism in terms of the hiring sentiment.There is a healthy growth of 4 percentage points in the Employment Outlook Index. Forecasts for the business sentiment are,comparatively mixed, with a marginal improvement of 2 percentage points in the Business Outlook Index.

Sectors wise frontrunners that post significant growth in both the Employment and Business Outlook indices are ITeS (5 and 4 points respectively) and Healthcare/Pharma (4 and 5 points respectively). Retail is projected to rise by 5 percentage points in Employment outlook. Meanwhile, the only sector that badly loses is Infrastructure – the business outlook here goes down by 5 percentage points.

City trends point to Mumbai as the leader, with a large increase of 5 and 7 percentage points,respectively, in Employment and Business outlook. The other gainers include Bangalore (4 percentage point increase in Employment outlook) and Delhi (5 percentage point increase in Business outlook).

Across geographies, Tier-II cities lead hiring intent, with a big rise of 4 points. Metros follow suit, however, with a marginal improvement of a single point. Hiring at the Middle and Junior levels is set to be more popular in the forthcoming half year(Apr-Sep, FY14), with a 6 and 4 point increase in hiring intent. Split by functional areas, Blue collar and Engineering are far ahead of the rest by registering an increase of 6 and 5 points respectively. And, both Sales & Marketing and IT witness a marginal increase of 2 points.

Blue Collar hiring is forecast to increase by a significant rate in the coming 6 months, as per the intent captured per functional areas. Our literature research investigates and finds that the sectors that have a higher incidence of informal workforce hiring are, indeed, the ones that have an increased intent to hire blue collar workers over the coming half year.

The depth survey findings reveal a hunt for superior grade talent combined with a reward-and-recognize mode organizations are stepping into over the next 6 months. This would mean an intense talent acquisition and retention tug-of-war greeting the first half of the next fiscal.

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

4

Project Objectives The Employment Outlook Report aims at –

Providing forward looking estimates of hiring sentiment and thus enabling its users with a tool to make effective hiring / people decisions for the immediate next quarter / half year.

Providing *Hiring Sentiment Intelligence* for different industry sectors, business sizes and geographies, as well as across hierarchical levels and functional areas.

Index Definitions Employment Outlook Index: The Employment Outlook Index is computed as the

difference in the proportion of respondents who report an increase in hiring needs and those who report a decline in hiring needs over the next three / six months.

Business Outlook Index: The Business Outlook Index is computed by subtracting the percentage respondents who say business in the next three / six months is likely to decrease from the percentage who says it will increase.

4. Depth Survey Findings

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

5

Main drivers of Hiring

With a mixed business sentiment pattern across industries and cities, we delved into

factors beyond business prospects for the industry and city to look at what drives

hiring for the next 6 months. Employers seem to be in the mood to cherry pick great

talent at bargain rates of salary in a mixed-mood market. This looks like an attempt

by the surveyed employers to consolidate their position in the talent market.

The desire to acquire valuable talent is aimed at four broad profile categories as

illustrated below.

Root causes of attrition; and the reasons for attrition this present Half Year

Attrition in the present Half Year was attributed to two major reasons – 1. a small

element of wrongly calibrated hiring in the past and 2. better market opportunities.

The first reason is all too familiar: bad choices become apparent after significant

monies have been spent on training and orientation and some of the hires leave.

The second reason is inevitable in a supply-constrained market.

24

11

9

6

Profile categories in demand for April-September, 2013-14 [# of respondents]

Engineers with > 5 years experience

Analysts & Business Consultants

Specialized Software Programmers

Digital Marketing Professionals

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

6

Talent retention strategy and steps to retain top talent

Retention initiatives are concentrated around rewards and recognition over the next

6 months. Organizations are in performance evaluation mode and the outcomes are

all about how valuable talent needs to be rewarded and retained.

Seen in conjunction with the aggressive talent hunt organizations are on, as stated in

the first section of this chapter, retention of top talent would take a lot more than in

the previous Half Years.

What makes employers prefer specific tier-2 and tier-3 locations to hire in

significant numbers

A variant response obtained during the surveys carried out for this edition was the

augmentation of customer service personnel by a few of the respondents that

indicated they would hire substantially from both tier-2 and tier-3 cities / towns.

These respondents believe that rural BPOs that have emerged at locations such as

Hosur, Kochi, Udupi, Falda and Chindwara are a good ground for hiring cost-effective

support staff.

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

7

5. Employment Outlook

5.1 Net Employment Outlook 5.2 Net Employment Outlook Growth – by sector

5.3 Net Employment Outlook Growth – by city

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

8

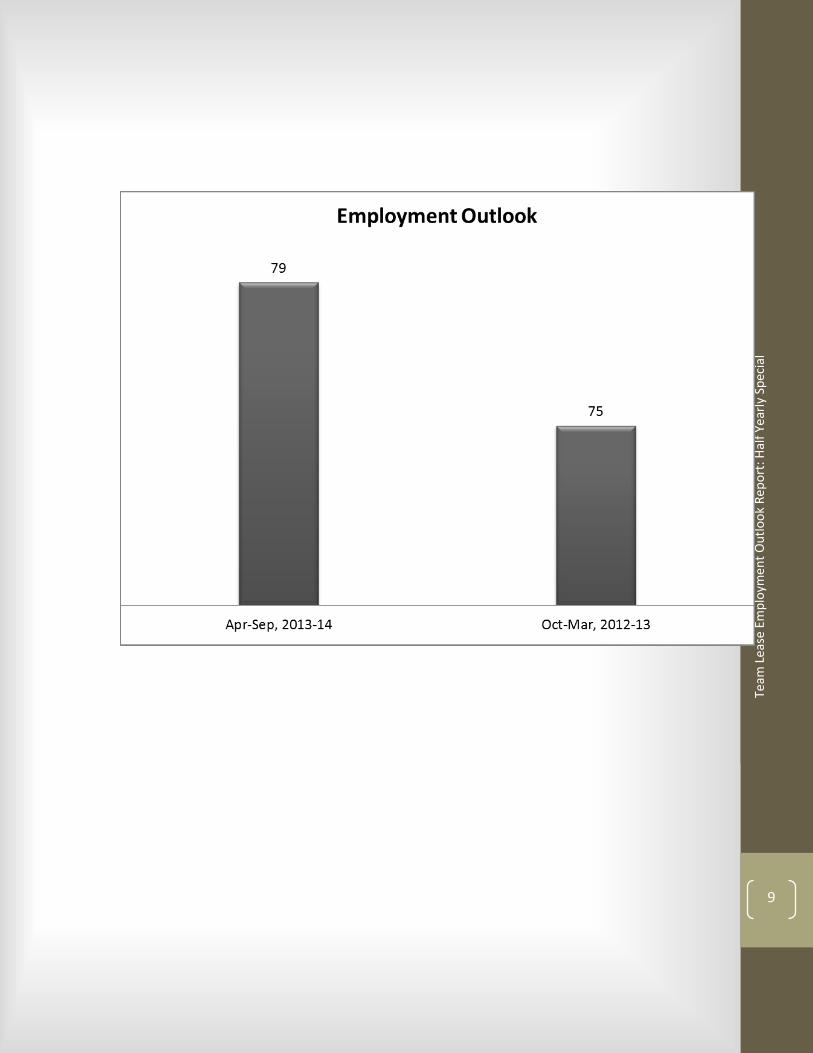

5.1 Net Employment Outlook

The half year period, Apr-Sep, FY14 sees a substantial increase of +4 points in the

net employment index. The Net Employment Outlook Indexis the difference in the

proportion of respondents reporting an increase in hiring needs and those reporting

a decline for the half year period in question.

Period (Figures in percentage)

Increase Decrease No Change Net Employment Outlook

Apr-Sep, FY14 84 5 11 +79

Oct-Mar,FY13 77 2 21 +75

More businesses have decided to hire over the forthcoming half year, compared

with the last half year).

Shaded cells have significant increases (gray) /decreases (red) in Index.

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

9

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

10

5.2 Net Employment Outlook Growth – by sector

Three sectors witness significant changes in the Net employment Outlook. The

outlook grows by +5 percentage points for ITeS and Retail. While, a four point

increase in the outlook is observed in Healthcare &Pharma.

Sector

(Figures in Percentage)

Half Year Net Increase /

Decrease Apr-

Sep,

FY14

Oct-

Mar,

FY13

IT 78 75 +3

ITES 79 74 +5

Financial Services [FS] 63 61 +2

Retail & FMCG [R&F] 81 76 +5

Infrastructure [INF] 60 63 -3

Manufacturing & Engineering [M&E] 51 53 -2

Telecom [TEL] 80 80 NC

Healthcare &Pharma [H&P] 75 71 +4

Four other sectors experience a marginal change in the Net employment Outlook-

the outlook grows by 3 and 2 percentage points for IT and Financial services

respectively and drops by 3 and 2 percentage points for Infrastructure and

Manufacturing respectively.

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

11

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

12

5.3 Net Employment Outlook Growth – by city

Mumbai and Bangalore, with a five and four percentage point growthin the

employment outlook lead the list in the forthcoming half year.

City

(Figures in Percentage)

Half Year Net Increase / Decrease Apr-Sep, FY14 Oct-Mar, FY13

Mumbai [Mum] 70 65 +5

Delhi [Del] 66 64 +2

Bangalore [Blr] 77 73 +4

Kolkata [Kol] 58 61 -3

Chennai [Chn] 65 66 -1

Pune [Pun] 71 68 +3

Hyderabad [Hyd] 59 61 -2

Ahmedabad [Ahd] 72 73 -1

A marginal increase in the outlook is noticed in Pune(+3 points) and Delhi(+2 points).

Four cities-Kolkata, Hyderabad, Ahmedabad and Chennai record a slight dip in the

outlook.

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

13

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

14

6. Business Outlook

6.1 Net Business Outlook 6.2 Net Business Outlook Growth – by sector

6.3 Net Business Outlook Growth – by city

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

15

6.1 Net Business Outlook

The coming half yearinches up the business outlook, although slightly by an increase

of two percentage points.

Period (Figures in percentage)

Increase Decrease No Change Net Business Outlook

Apr-Sep, FY14 81 7 12 +74

Oct-Mar, FY13 75 3 22 +72

The trend is characterised by a substantial growth in the number of respondents

reporting an increase as well asdecrease in the business sentiment.

[Shaded cells have significant increases (gray) /decreases (red) in Index.]

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

16

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

17

6.2 Net Business Outlook Growth – by sector

More than half of the sectors experience a growth in the business sentiment.

Amongst them, Healthcare &Pharma and ITeS have a significant growth of 5 and 4

percentage points respectively. While, the three sectors that have marginal growth

are Telecom, IT and Manufacturing.

Sector

(Figures in Percentage)

Half Year Net Increase / Decrease Apr-Sep,

FY14

Oct-Mar,

FY13

IT 74 72 +2

ITES 73 69 +4

Financial Services [FS] 60 62 -2

Retail & FMCG [R&F] 82 84 -2

Infrastructure [INF] 62 67 -5

Manufacturing & Engineering [M&E] 61 60 +1

Telecom [TEL] 59 56 +3

Healthcare &Pharma [H&P] 74 69 +5

Infrastructure turns out to be a laggard with a maximum drop of 5 percentage

points. Financial services and Retail slightly dip by 2 percentage points.

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

18

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

19

6.3 Net Business Outlook Growth – by city

Forthcoming half year sees Mumbai and Delhi contributing almost entirely to the

incremental growth in the business sentiment.

City

(Figures in Percentage)

Half Year Net Increase / Decrease Apr-Sep, FY14 Oct-Mar, FY13

Mumbai [Mum] 71 64 +7

Delhi [Del] 56 51 +5

Bangalore [Blr] 78 75 +3

Kolkata [Kol] 68 69 -1

Chennai [Chn] 82 80 +2

Pune [Pun] 80 80 NC

Hyderabad [Hyd] 72 73 -1

Ahmedabad [Ahd] 73 73 NC

Bangalore and Chennai report a marginal increase of 3 and 2 percentage points

respectively. The rest of the cities have little or no change in the business sentiment.

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

20

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

21

7. Hiring Intent

7.1 Hiring Intent by Geography 7.2 Hiring Intent by Hierarchy 7.3 Hiring Intent by Functional Area

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

22

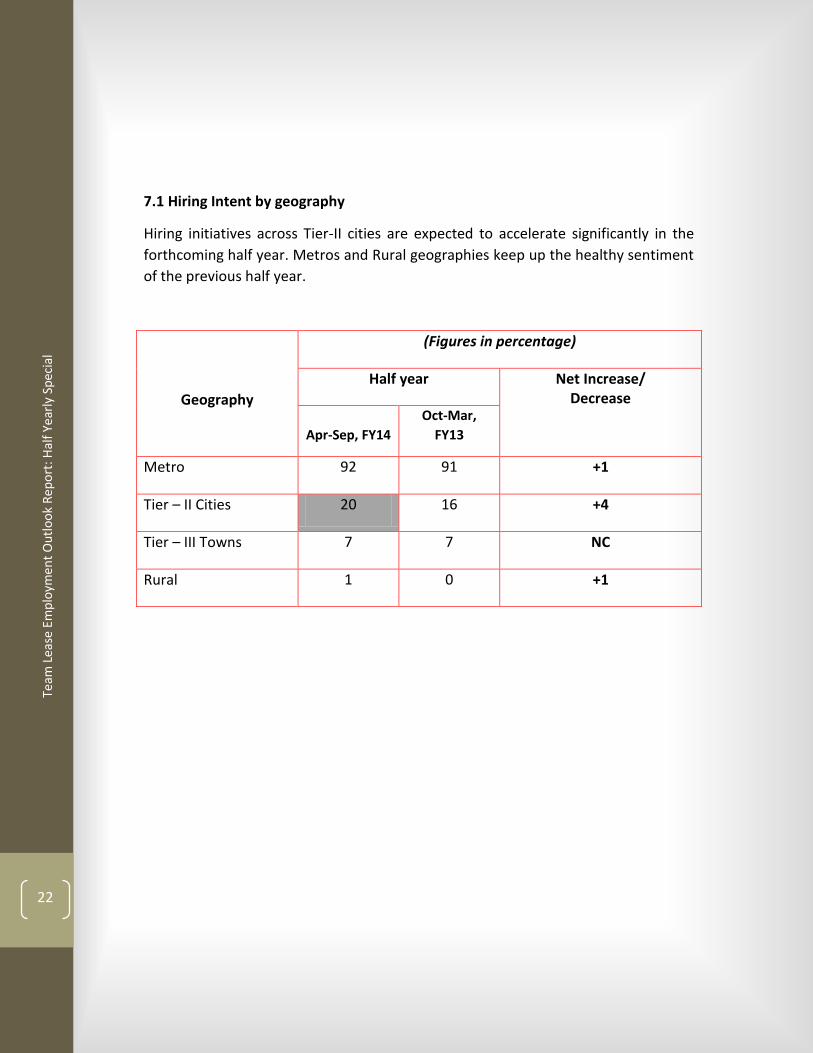

7.1 Hiring Intent by geography

Hiring initiatives across Tier-II cities are expected to accelerate significantly in the

forthcoming half year. Metros and Rural geographies keep up the healthy sentiment

of the previous half year.

Geography

(Figures in percentage)

Half year Net Increase/ Decrease

Apr-Sep, FY14

Oct-Mar,

FY13

Metro 92 91 +1

Tier – II Cities 20 16 +4

Tier – III Towns 7 7 NC

Rural 1 0 +1

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

23

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

24

7.2 Hiring Intent by Hierarchy

Businesses intend to increase hiring across organization levels, with a substantial

appreciation in the intent at the Middle and Junior levels. A negligible dip in hiring

intent is seen across Senior levels.

Hierarchy

(Figures in percentage)

Half year Net Increase/ Decrease

Apr-Sep, FY14

Oct-Mar,

FY13

Entry Level [No Experience]

48 47 +1

Junior Level [1 – 3 years’ Experience]

71 67 +4

Middle Level [3 – 7 years’ Experience]

47 42 +5

Senior Level [> 7 years’ Experience]

24 25 -1

Not Hiring 12 12 NC

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

25

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

26

7.3 Hiring Intent by Functional Area

The upcoming half year(HY2) sees an incremental change in hiring intent across

various functional areas. Blue Collar and Engineering profiles beat the incremental

trend and grow by 5 and 4 percentage points respectively.

Functional Area

(Figures in percentage)

Half year Net Increase/ Decrease

Apr-Sep, FY14

Oct-Mar,

FY13

Sales / Marketing / Customer Service [SMC]

85 84 +1

IT 32 31 +1

Engineering [ENG] 45 41 +4

Accounts / Finance [A&F]

10 11 -1

Administration / HR / Office Service [AHO]

11 13 -2

Blue Collar [BC]* 47 42 +5

Other 5 5 NC

Not hiring 7 8 -1

*Previously included under ‘Others’

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

27

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

28

8. Other Trends

8.1 Employment Outlook Index – city-sector drilldown 8.2 Business Outlook Index – city-sector drilldown

8.3 Attrition trends by sector 8.4 Attrition trends by city

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

29

8.1 Employment Outlook Index – city-sector drilldown

City

Half

Year

Total

Sector

IT

ITeS

FS

RMF

INF

M&E

TEL

H&P

Mum

Apr-Sep,

FY14 70 10 8 13 12 5 7 6 9

Oct-

Mar,

FY13

65 9 6 11 12 6 7 6 8

Del

Apr-Sep,

FY14 66 5 5 13 14 5 7 9 8

Oct-

Mar,

FY13

65 6 4 13 14 4 6 9 9

Blr

Apr-Sep,

FY14 77 8 10 8 9 5 11 13 13

Oct-

Mar,

FY13

74 6 8 8 9 6 9 14 14

Kol

Apr-Sep,

FY14 58 4 5 11 8 6 6 3 15

Oct-

Mar,

FY13

61 5 4 12 9 6 4 3 18

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

30

Chn

Apr-Sep,

FY14 65 7 7 8 11 8 7 5 12

Oct-

Mar,

FY13

66 6 8 9 10 8 8 6 11

Pun

Apr-Sep,

FY14 71 6 12 5 6 11 10 10 11

Oct-

Mar,

FY13

69 6 10 6 6 12 11 9 9

Hyd

Apr-Sep,

FY14 59 3 10 9 7 4 11 6 9

Oct-

Mar,

FY13

61 4 11 11 6 5 10 5 9

Ahd

Apr-Sep,

FY14 72 4 4 18 7 4 12 10 13

Oct-

Mar,

FY13

73 3 3 18 8 4 14 9 14

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

31

9.2 Business Outlook Index – city-sector drilldown

City

Half

Year

Total

Sector

IT

ITeS

FS

RMF

INF

M&E

TEL

H&P

Mum

Apr-Sep,

FY14 71 5 4 10 7 18 10 6 11

Oct-

Mar,

FY13 64 6 5 8 5 17 9 5 9

Del

Apr-Sep,

FY14 56

3 4 8 10 7 6 8 10

Oct-

Mar,

FY13 51 4 2 6 11 8 6 6 8

Blr

Apr-Sep,

FY14 78

9 4 11 10 9 12 15 8

Oct-

Mar,

FY13 76 8 5 9 9 9 13 13 10

Kol

Apr-Sep,

FY14 68

10 5 6 12 9 5 10 11

Oct-

Mar,

FY13 69 9 4 7 12 10 4 11 12

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

32

Chn

Apr-Sep,

FY14 82

9 11 12 9 10 9 8 14

Oct-

Mar,

FY13 81 8 9 10 9 12 9 9 15

Pun

Apr-Sep,

FY14 80 11 14 7 10 13 12 9 4

Oct-

Mar,

FY13 80 9 14 8 9 14 10 10 6

Hyd

Apr-Sep,

FY14 72 9 6 13 11 7 8 6 12

Oct-

Mar,

FY13 73 10 6 12 10 7 9 7 12

Ahd

Apr-Sep,

FY14 73 9 4 10 9 8 12 4 17

Oct-

Mar,

FY13 73 8 3 11 10 8 12 5 16

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

33

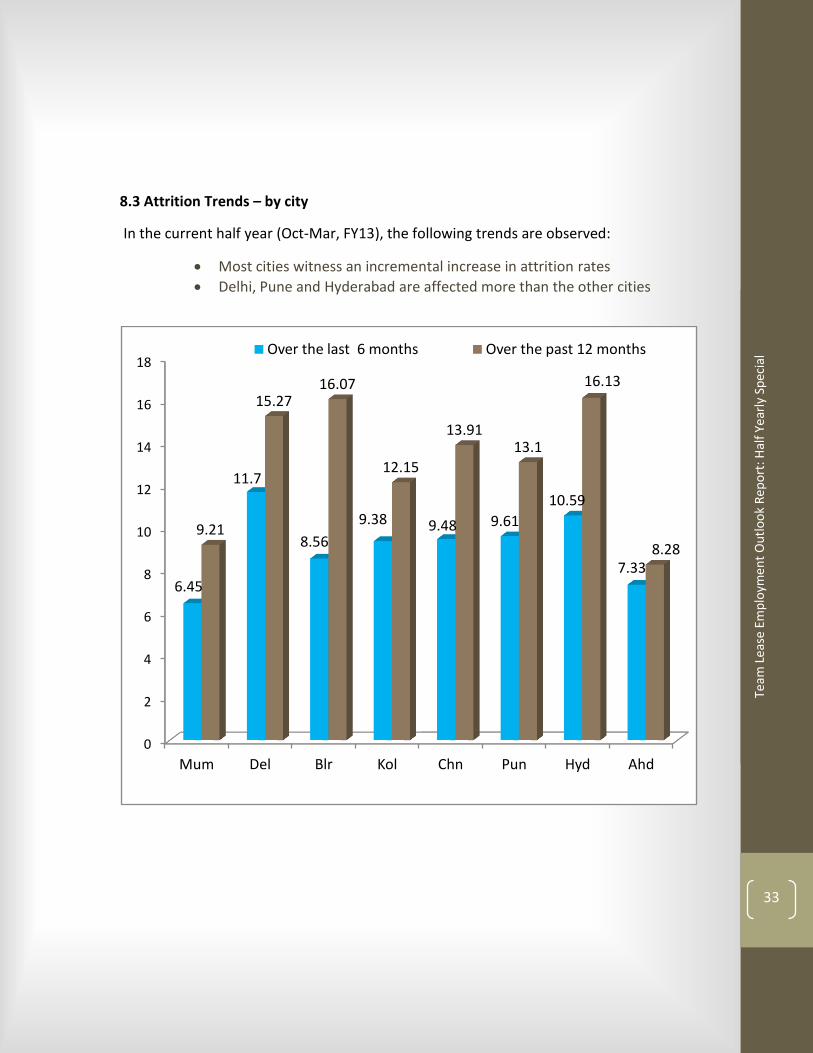

8.3 Attrition Trends – by city

In the current half year (Oct-Mar, FY13), the following trends are observed:

Most cities witness an incremental increase in attrition rates

Delhi, Pune and Hyderabad are affected more than the other cities

0

2

4

6

8

10

12

14

16

18

Mum Del Blr Kol Chn Pun Hyd Ahd

6.45

11.7

8.56

9.38 9.48 9.61

10.59

7.33

9.21

15.27 16.07

12.15

13.91 13.1

16.13

8.28

Over the last 6 months Over the past 12 months

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

34

Attrition Trends – by sector

In the current half year, Oct-Mar, FY13, most sectors report modest increases in

attrition. Infrastructure and ITeS are sectors contributing most toward both half

yearly and annual attrition.

0

2

4

6

8

10

12

14

16

M&E R&F FS IT ITES INF TEL H&P

8.9 9.56

8.65

9.71 10.12

10.97

9.56

8.57

10.96

13.78 13.28 13.11

15.52 15.07

11.24 11.25

Over the last 6 months Over the past 12 months

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

35

10.Annexure Research Methodology

The Employment Outlook Survey follows a rigorous and statistically validated process as detailed below.

10.1 Sample Design

Random sampling technique was used to identify respondents for the survey. Data sources used to collect contact data were:

1. Kompass directory for small, medium and large sized companies in the private sector. To ensure continuity with the baseline measurement, the core random sample was drawn from this database.

2. NASSCOM database for IT companies

3. Companies registered withbpo.india.org in the case of ITES and

4. Financial companies registered with the Bombay Stock Exchange (BSE).

10.2 Respondent Selection

Target respondents for the study were Business & HR Heads as well as Senior Managers with hiring mandates. The databases offered a contact name for each company listed. Interviewers called into each of these companies and obtained the names of the appropriate individuals who were responsible for hiring decisions.

10.3 Data Collection

The survey instrument was then administered to the target respondents using the CATI (Computer Aided Telephonic Interview) methodology. Appropriate computer software was used for data collection and tabulation. Please refer the following section named ‘Sample Distribution’ for details on city and business size-wise breakup of the sample.

10.4 Secondary Data Sources:

- Major sources of Indian and international research about informal workforce employment trends in India

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

36

10. Sample Distribution

10.1 City-wise breakup

10.2 Business Size Breakup

Small [Up to 249 employees]

Medium [250 – 999 employees]

Large [1,000 or more employees]

Mumbai 11 50 13

Delhi 11 52 10

Bangalore 14 52 13

Kolkata 14 50 14

Chennai 15 48 17

Pune 12 55 16

Hyderabad 12 52 16

Ahmedabad 13 42 12

Sectors / City

Mumbai Delhi Bangalore Kolkata Chennai Pune Hyderabad Ahmedabad Total

M&E 6 5 10 10 10 10 9 8 68

R&F 10 10 9 9 11 11 10 8 78

FS 11 10 12 7 9 11 10 5 75

IT 10 10 9 12 10 10 10 10 81

ITeS 9 11 10 10 12 10 10 9 81

INF 10 9 10 10 10 10 11 10 80

TEL 8 8 9 10 8 11 11 6 71

H&P 10 10 10 10 10 10 9 11 80

Total 74 73 79 78 80 83 80 67 614

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

37

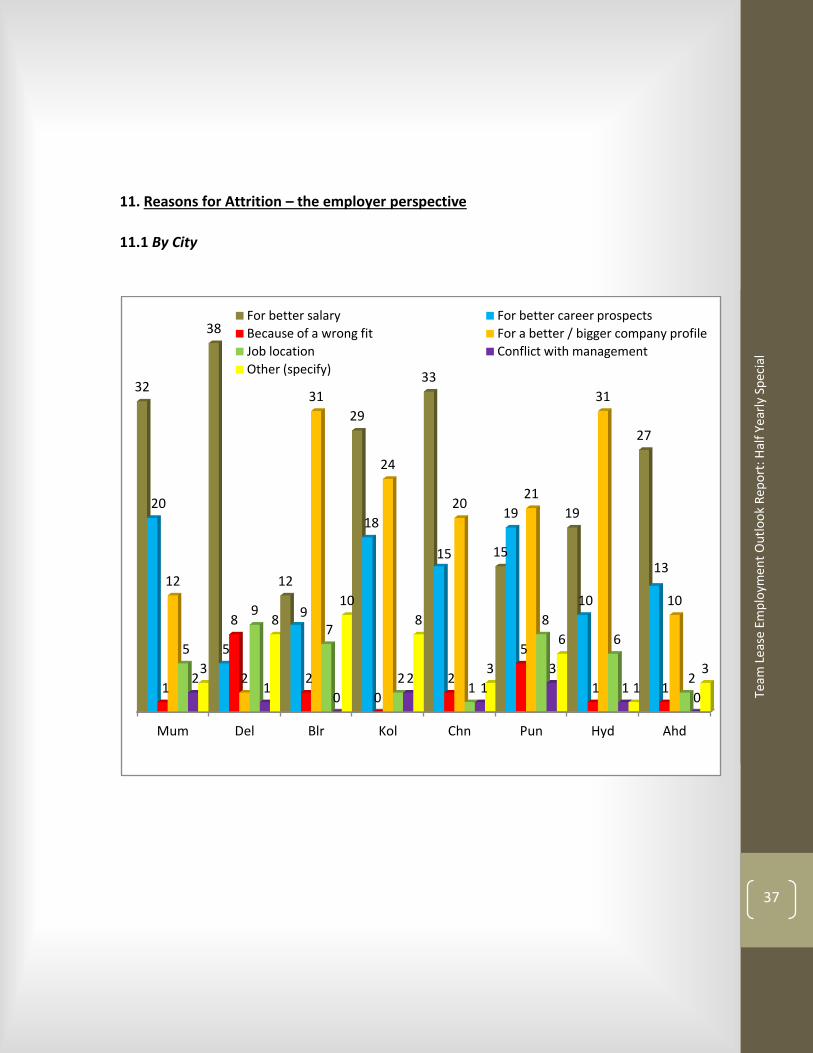

11. Reasons for Attrition – the employer perspective

11.1 By City

Mum Del Blr Kol Chn Pun Hyd Ahd

32

38

12

29

33

15

19

27

20

5

9

18

15

19

10

13

1

8

2

0

2

5

1 1

12

2

31

24

20 21

31

10

5

9

7

2 1

8

6

2 2 1

0

2 1

3

1 0

3

8

10

8

3

6

1

3

For better salary For better career prospects

Because of a wrong fit For a better / bigger company profile

Job location Conflict with management

Other (specify)

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

38

11.2 By Sector

0

5

10

15

20

25

30

35

M&E R&F FS IT ITES INF TEL H&P

22

13

29

19

22

31

22

17

11

14

25

23

26

16

9

21

1 1 0

3 4

5 6

5

17

22

9

17

8

14

12

28

0

8

4 5

3

1

9

11

1 0 0 0 0

2

0 0

9 8

7

10

5

3

1

5

For better salary For better career prospects Because of a wrong fit For a better / bigger company profile Job location Conflict with management Other (specify)

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

39

12. Insights: Literature Review

Blue Collar workforce:

Hiring Sentiment versus Employment Intensity

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

40

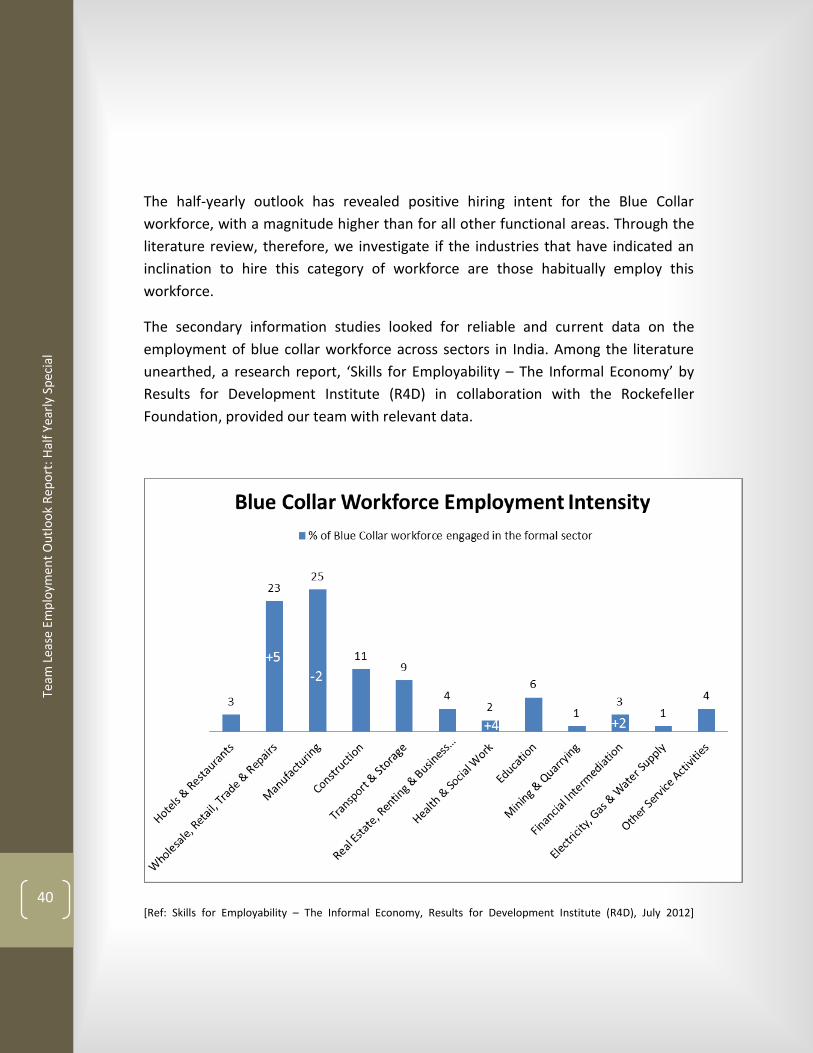

The half-yearly outlook has revealed positive hiring intent for the Blue Collar

workforce, with a magnitude higher than for all other functional areas. Through the

literature review, therefore, we investigate if the industries that have indicated an

inclination to hire this category of workforce are those habitually employ this

workforce.

The secondary information studies looked for reliable and current data on the

employment of blue collar workforce across sectors in India. Among the literature

unearthed, a research report, ‘Skills for Employability – The Informal Economy’ by

Results for Development Institute (R4D) in collaboration with the Rockefeller

Foundation, provided our team with relevant data.

[Ref: Skills for Employability – The Informal Economy, Results for Development Institute (R4D), July 2012]

Team

Lea

se E

mp

loym

ent

Ou

tlo

ok

Rep

ort

: Hal

f Ye

arly

Sp

ecia

l

41

The above chart illustrates the intensity of employment of blue collar workforce

across the formal sector in India. Of the 11 industry categories the research quotes,

we found 4 that directly correspond to those in the TeamLease Employment Outlook

Survey. Two of the four industry categories – Wholesale, Retail, Trade & Repairs and

Manufacturing – have high incidence of employment intensity of blue collar

workforce.

In terms of Business sentiment, Healthcare is the only industry with a significantly

high sentiment growth among the above four.

The Hiring sentiment scene is greener though. Three of the four industry categories

that correspond to the industries we research and report on are found to be having

increased inclination (two, significantly high) to hire blue collar workforce over the

next 6 months; only one – Manufacturing – is found to have a slightly reduced level

of hiring inclination.

Historical evidence of higher incidence of blue collar workforce employment in the

industries that responded with higher inclination to hire reinforces this forecast. The

informal workforce is the functional category to watch over the next 6 months.