TBLI EUROPE 2015 - ESG Analyses and Indices - Gustavo Pimentel

11

TBLI Europe 2015 Workshop C1 ESG Analysis and Indices Gustavo Pimentel Managing Director [email protected] 20 Nov 2015

-

Upload

asn-bank -

Category

Economy & Finance

-

view

306 -

download

0

Transcript of TBLI EUROPE 2015 - ESG Analyses and Indices - Gustavo Pimentel

TBLI Europe 2015 Workshop C1 ESG Analysis and Indices

Gustavo Pimentel Managing Director [email protected]

20 Nov 2015

Specialists in Sustainable Finance and Responsible Investing § ESG Advisory for

Responsible Investors

§ LatAm-focused ESG research: sector and thematic

§ ESG Risk Mgmt for banks and insurers

11th best house, 2nd best SRI analyst worldwide

(Extel IRRI 2013)

Chair of ESG Integration WG PRI Brazil Network

Impact Investing IDB beyondBanking Award 2011

About SITAWI

EIRIS Sales and Research Partner (South America)

“Not everything that can be counted counts, and

not everything that counts can be counted”

(Albert Einstein OR William Bruce Cameron)

3

Collapse of Samarco tailings dam in Brazil (JV Vale / BHP)

4

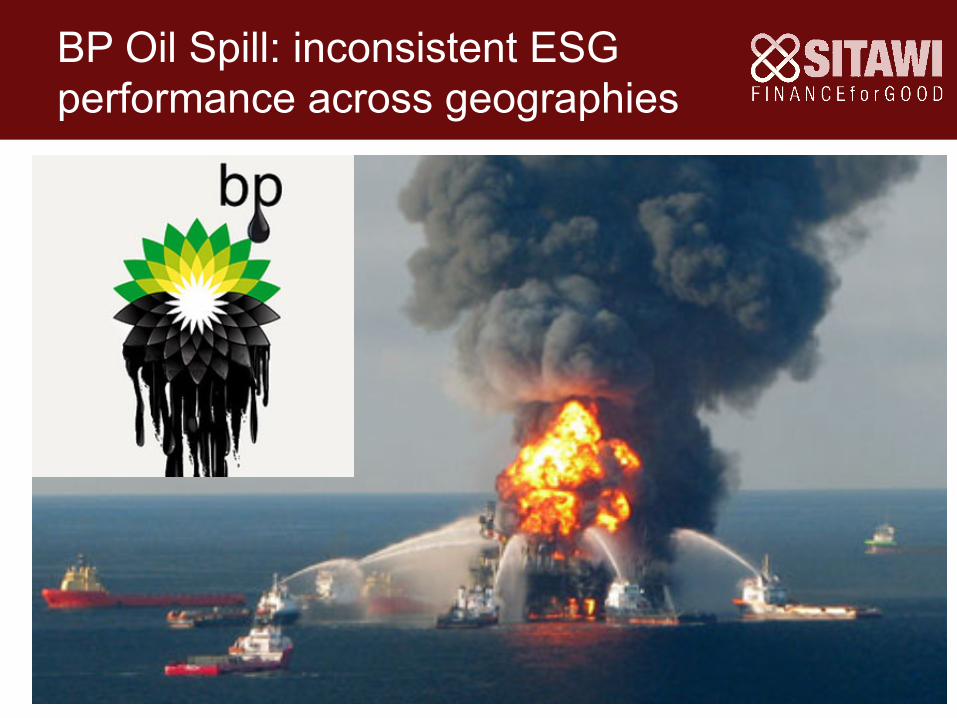

BP Oil Spill: inconsistent ESG performance across geographies

5

VW emissions scandal Can you trust self-reported data?

6

Petrobras corruption scandal

7

8

1.86

1.90

1.94

2.11

2.17

2.17

2.19

2.20

2.25

1.60 1.70 1.80 1.90 2.00 2.10 2.20 2.30

Specialized Consumer Services (Education)

Integrated Oil & Gas

Home Construction

Broadline Retail

General Mining

Transportation Services

Apparel Retail

Iron & Steel

Food Product

Average Relevance Score per Sector

Source: survey of Brazilian PRI signatories on materiality of EFFAS KPIs for ESG, 2013

O&G lower materiality: industry context in Brazil or problem with KPIs list?

Ethics and corruption did not make the cut of the most material ESG issues…probably because of inadequate KPIs

9

76%

67%

67%

65%

60%

50%

12%

11%

22%

12%

30%

40%

0%

0%

0%

6%

10%

0%

12%

22%

11%

18%

0%

10%

Accidental oil/gas spills

Emissions to Water

Remediation

Leakages

GHG Emissions

Maintenance & Safety

Most material ESG themes for Integrated Oil & Gas

High Med Low Null

Source: survey of Brazilian PRI signatories on materiality of EFFAS KPIs for ESG, 2013

Corruption-related KPIs

Percentage of revenues in regions with Transparency International corruption index below 6.0

Contribution to political parties as a percentage of revenues

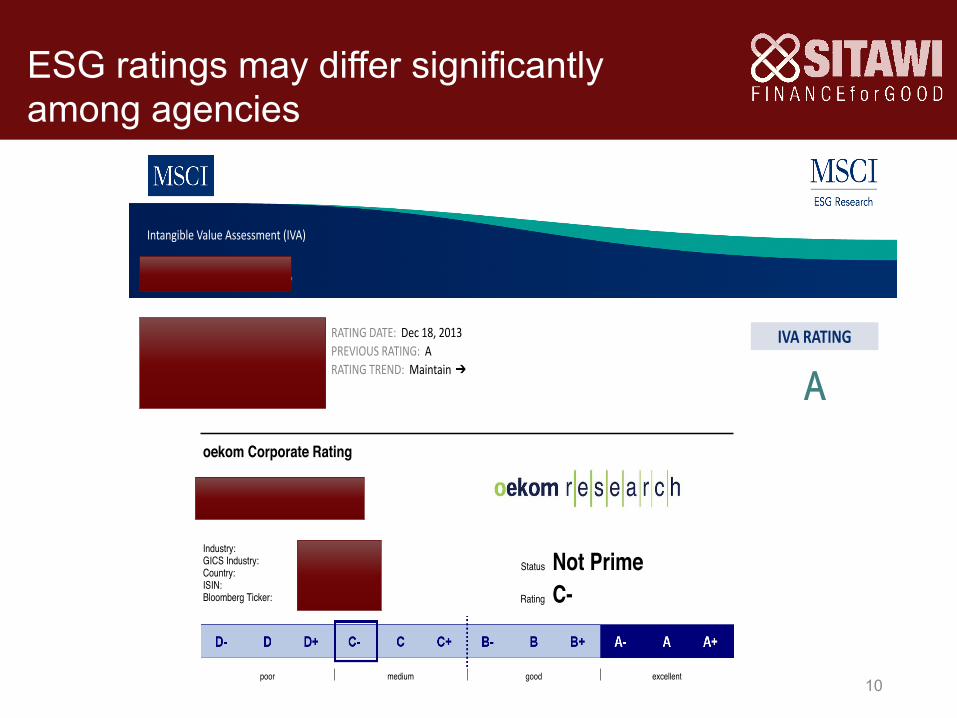

ESG ratings may differ significantly among agencies

10

��������

AA���������

�������������

��� �-�1&(�H2 1�5-& (2 8-�'�-&�� �3 H�HA �'� �.,/�-<H2 '<�1./.:�1C�.,(-�3�� &�-�1�5.-/.14.+(. �-� �+��31(�(3< �(231(�85.- ./�1�5.-2 '�+/ 3'� �.,/�-< ,�(-3�(- � 9�1< +.: .9�1�++��1�.- �-� 3.;(� 1�+��2� ..3/1(-3> 3'�1��< +.:�1(-& (32 �;/.281� 3. �22.�(�3�� 1�&8+�3.1< 1(2*2A �-3'� .3'�1 '�-�> (32 '(&' ��/�-��-�� .- '<�1.C/.:�1 �;/.2�2 (3 3. /.3�-5�+ ./�1�5.-�+ �(218/5.-1(2*2 .9�1 3'� +.-& 3�1, (- ��2� . 1��8��� :�3�1 �9�(+��(+(3<A ��� �-�1&(� F��� G (2 �,.-& 3'� �: �.,/�-(�2 (- 3'� /��1 2�3 3'�3 �1� 2(&-�3.1< 3. 3'� �� �+.��+ �.,/��3 �-� (3 '�2 '(&'C+�9�+�.,,(3,�-32 3. ,�-�&(-& (32 (,/��3 .- �(.�(9�12(3<> �.-2(��1(-& (32 ./�1�3�2 (- �1�=(+ :'(�' '�2�-��,(� 1(�'-�22 �-� �(9�12(3< . $.1� �-� �8-�A �'� �.,/�-< ��,.-231�3�2 231.-& ��/��(3<3. ,�-�&� (32 '8,�- 1�2.81��2 (- 3�1,2 . �,/+.<�� �-&�&�,�-3 �-� 31�(-(-&> �+3'.8&' (32�,/+.<�� 381-.9�1 (-�1��2�� 2'�1/+< �.,/�1�� 3. 3'� /1�9(.82 <��1> (-�(��5-& /.3�-5�+ &�/2 (-(,/+�,�-3�5.- . (32 /.+(�(�2A ��� �+2. 31�(+2 (-�8231< /��12 (- 3�1,2 . /1.9(�(-& 1�-�:��+��-�1&< .!�1(-&2 3. (32 �823.,�12> 3'�1��< -.3 8++< ��/(3�+(=(-& .- 3'� /.3�-5�+ &1.:3'.//.138-(5�2�(-�3'��1�-�:��+���-�1&<�2/���A

��'*�&�/+,*3��*��&-$� ��" !, ��'*��0+7��0�*� �

&�/+,*3��*��&-$� �'&,*'0�*+"�+ ��" !,

�&0"*'&%�&,�$ SAN TT3' UOASW ��*�'&��%"++"'&+ UN23 �.-� NSARW

��,�*��,*�++ QS3' �.-� NOAQW

�"'�"0�*+",3�>���&���+� TU3' �.-� OQAUW

�'2"���%"++"'&+�>���+,� VN23 �.-� NSARW

�(('*,/&"-�+�"&���&�1��$���&�* 3 OS3' �.-� NOAQW

�'�"�$ SAQ RT3' NOAQW /%�&���(",�$���0�$'(%�&, SS3' �.-� NOAQW

�'0�*&�&�� TAM OM3' RAMW �'*('*�,���'0�*&�&�� OM3' �.-� RAMW

�����@ ����P ����������@ ����NU>�OMNP����������@ �5+(5�2 �������������@ ��������C�������@ �+��31(���5+(5�2 �����������@ ��(-3�(-�������@ ��

����� ��������������

VAMSAU

QAQQAS

RAUQAM

TANQAS

PARQAS

SAQRAP

TAMTAV

��� � �� ��� � �� ���

�������������

&�/+,*3���-& ��"+,*"�/-'&<

OW

OMW ONWNTW @GI

NOWTW

�'(�B��'%(�&"�+

��������������>���A ���

�-�,��A/A�A ���

�.-(-*+()*���./�*��A�A ���

�'.'%�B��'%(�&"�+

������������������ �

�.*<.��+��31(���.:�1��.,/�-<>-�.1/.1�3�� ���

����������������>���A ���

-3�-&(�+����+8���22�22,�-3�F��G

������&�* "���7�7

&���������� �������������������������������"������������������!�������������$����������������������������#��������������� �����������������������������������������������#%

LOMNQ����>�-�A��&� N . OM

oekom Corporate Rating / Last Modification: 2013-11-29 1 © oekom research AG

oekom Corporate Rating

CPFL Energia SA

Industry:GICS Industry:Country:ISIN:Bloomberg Ticker:

UtilitiesElectric UtilitiesBrazilBRCPFEACNOR0CPFE3 BZ Equity

Status Not PrimeRating C-

poor medium good excellent

Strengths and Weaknesses

+ electricity generation almost entirely based on renewable energy sources+ very low carbon intensity of electricity generation

- recurring accidents with several fatalities in company operations in the lastthree years

- only limited information on measures to ensure the sustainable operation ofhydropower stations

- comparatively long duration of average interruption of power supply per yearper customer

- no information on measures to ensure the sustainable production of biomass

Rating History

Company Profile

CPFL Energia S.A., through its subsidiaries, distributes, generates and commercializes electricity in Brazil. The Company also commercializeselectricity and provides electricity-related services to its affiliates as well as unaffiliated parties.

Industry

Universe Results Key ESG Issues in the Industry

• Climate protection through increased useof renewable energies and energyefficiency

• Environmentally sound operation of plantsand infrastructure

• Secure and reliable energy and watersupply for all parts of the population

• Fair business practices• Worker safety and accident prevention

Rating UniverseScouting Universe

11

§ Global KPI / metrics are good starting points: suitable to large universes

§ Ratings disaggregation is critical to uncover tail risk

§ (Mis) leading indicators vs. KPI optimum range

§ Company specific analysis and materiality (“nothing compares to you”)

§ Integration into DCF is a strong trend: suitable for smaller universes

§ Be careful with the data fetish

Thoughts

Gustavo Pimentel

[email protected] +55 21 2247 1136

SITAWI

Av. Ataulfo de Paiva 658 / 401 - Leblon

Rio de Janeiro – RJ