Taxsutra Conclave 2015 – International Tax at Crossroads ... · Taxsutra Conclave 2015 –...

87

Transcript of Taxsutra Conclave 2015 – International Tax at Crossroads ... · Taxsutra Conclave 2015 –...

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page2

Page2

#ta

xsut

ra

#

LNEv

ent

ww

w.le

xisn

exis

.co.

in

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page3

Page3

#ta

xsut

ra

#

LNEv

ent

ww

w.le

xisn

exis

.co.

in

Table of Contents

1

BEPS 4 Taxsutra Brief Global Reactions 4 Experts’ Corner BEPS impact on inbound and outbound investment – an Indian perspective

- Punit Shah (Partner, Dhruva Advisors LLP) 8

Taxation of the Digital Economy – BEPS proposals and the Indian approach - Ajay Rotti (Partner, Dhruva Advisors LLP) & Hariharan Gangadharan (Associate Partner)

12

BEPS : India Insights - Sunil Shah (Partner, Deloitte India) & Pritin Kumar (Partner) 15

2

Goods & Services Tax (GST) 22 Taxsutra Brief Overview 22 Experts’ Corner GST – Through the Looking Glass

- L. Badrinarayanan (Partner, Lakshmikumaran & Sridharan, Attorneys) 24

GST and Out of Court Settlements - L. Badrinarayanan (Partner, Lakshmikumaran & Sridharan, Attorneys) 28

GST – India on the cusp of most awaited tax reform - Saloni Roy (Senior Director, Deloitte India) 32

3

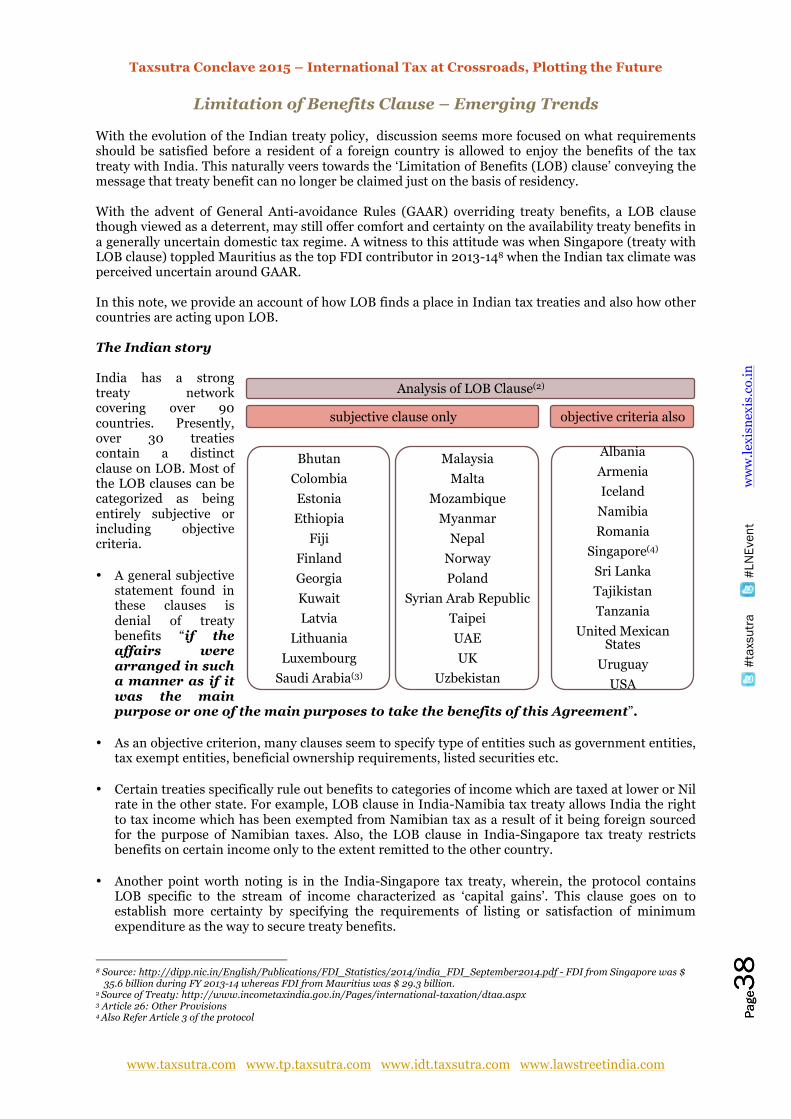

International Tax Policy 35 Taxsutra Brief Overview 35 Limitation of Benefits Clause – Emerging Trends 38 Experts’ Corner Making India’s International Tax Policy more certain

- Ashutosh Dikshit (Principal Advisor, BMR & Associates LLP) 40 Can we make ‘Make in India’ better?

- Kumar Kandaswami (Senior Director, Deloitte India) 44

4

Litigation Trends 48 Taxsutra Brief India’s Tax Dispute Resolution Scenario 48 Around the world – APA developments in 2014-15 73 Most Viewed Tax Rulings 76 Experts’ Corner Tax Litigation in India – Trends & Strategies

- Rohit Jain (Partner, Economic Laws Practice), Rahul Khurana (Associate Manager) & Divya Jeswant (Senior Associate)

51

Administrative law principles in tax litigation : Missing arrow in your quiver? - Sujit Ghosh (Partner & National Head, Advaita Legal) & Sudipta Bhattacharjee (Principal)

55

5

Transfer Pricing 58 Taxsutra Brief Marketing Intangibles - Analyzing litigation trends post Delhi HC verdict 58 Experts’ Corner Business Restructuring

- Nitin Jain (Partner, EY) 62

Identifying commercial or financial relations between Associated Enterprises for applying Arm’s Length Principle - Rajendra Nayak (Partner, EY)

66

6 Black Money The Black Money Act – Success of Failure?

- Ameet N Patel (Partner, Manohar Chowdhry & Associates, CAs) 71

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page4

Page4

#ta

xsut

ra

#

LNEv

ent

ww

w.le

xisn

exis

.co.

in

BEPS

Taxsutra Brief: Global Reactions

“Taxation is at the core of countries’ sovereignty, but the interaction of domestic tax rules in some cases leads to gaps and friction.” Quoting so, in July 2013, the Organization for Economic Co-operation and Development (OECD) released its Action Plan on Base Erosion and Profit Shifting (BEPS). The report garnered significant attention in the wake of countries combating high profile tax evasions due to anomalies in the international tax systems. Two years post the beginning of concerted efforts of countries to counter BEPS, the domino effect is being felt across Continents. By the time the first speakers take to the dias at the inaugural Taxsutra Conclave and you flip through the articles in this booklet, the final BEPS reports shall be in the public domain. OECD has already finalized Action Plan 13 dealing with Transfer Pricing: Country-By-Country (CbC) reporting and

has also released the implementation package. While BEPS aims a coordinated implementation of various BEPS action plans, rather than an individual-country effort, some of the countries have started selectively implementing a few of the BEPS solutions . A case in point – Diverted Profits Tax legislated by Britain. Captured below is a highlight of how India and some other countries have taken note of OECD recommendations on BEPS –

A. The Indian Scenario

The Indian Government has taken steps to protect its tax base as witnessed by its spree of execution of automatic information exchange agreements, agreement with the US under Foreign Account and Tax Compliance Act (FATCA), the Black Money Law with a one-time compliance window and the ongoing re-negotiation of the India-Mauritius tax treaty. Specifically on the BEPS project, Indian Competent Authority, Mr Akhilesh Ranjan in a recent interview with Taxsutra, asserted that India will wait for all the reports to be submitted to G-20 and thereafter initiate actions and that too strictly in accordance with the outcomes of the BEPS project.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page5

Page5

#ta

xsut

ra

#

LNEv

ent

ww

w.le

xisn

exis

.co.

in

With these legislative developments on one hand, the Tax Tribunals in India have had their share of discussion around BEPS in general and on OECD recommendations on BEPS Action Plans while deciding some of the cases. A gist of the recent rulings discussing BEPS / OECD’s work is provided below:

B. Asia The proportion of tax changes has been almost in conjunction with the relative size of the Asian continent. Almost, all the identified BEPS issues have had their share of limelight in the various tax proposals across the region. Prominent issues are digital economy, treaty abuse, anti-avoidance measures, Controlled Foreign Companies (CFC) etc.

• Enhanced substance/ Permanent establishment requirements introduced in favorable tax regimes such as Mauritius, Singapore etc.

• China, Russia and Vietnam have all introduced anti-abuse rules and beneficial ownership rules, or guidance to restrict treaty benefits to conduit situations.

• Russia has introduced rules for CFC in 2014 targeting certain types of entities. • Indirect tax on digital services introduced in Japan, South Korea and Israel. • Several countries like Korea, Singapore, Malaysia etc. have implemented transfer pricing

documentation / CbC reporting in accordance with OECD requirements.

• Baker Hughes Singapore Pte. Ltd. [TS-214-ITAT-2015(DEL)]: The assessee was a non-resident company engaged in various services relating to oil exploration work and claimed taxation u/s 44BB of the Income-tax Act. Revenue alleged that such a view would amount to BEPS and assessee’s income is taxable u/s 44DA of the Act. ITAT observed that BEPS is merely a tax policy consideration for law making and has no role in judicial process and that the judicial process will infringe neutrality if it is to be swayed by such policy considerations.

• Watson Pharma Pvt. Ltd. [TS-3-ITAT-2015(Mum)-TP]: The assessee, a subsidiary of a US Company was engaged in contract manufacturing and research services. The transfer pricing officer worked out adjustment on location savings on the basis of transfer of manufacturing activity from US to India. The Tribunal deleted the addition on location savings while noting that India is part of G20 countries, and that all G20 countries have concurred to the position on no adjustment for location savings in cases where, reliable local market comparable are available and can be used to identify arm's length prices.

• Mitsubishi Corporation India Pvt. Ltd. [TS-330-ITAT-2014(DEL)-TP]: The assessee, a subsidiary of Japanese Corporation (Sogo Shosha establishment) carried out transactions of provision of services, purchase of goods and other transactions. TPO rejected use of ‘Berry ratio’ adopted by the assessee. One of the reasons cited was that the assessee was not suitably compensation for location savings. Referring to the “4-step process” as per OECD report titled “Guidance on Transfer Pricing Aspects of Intangibles”, ITAT rejected location savings in the absence of any identification/quantification effort by the revenue.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page6

Page6

#ta

xsut

ra

#

LNEv

ent

ww

w.le

xisn

exis

.co.

in

C. Europe , UK and Ireland The European region, not surprisingly has witnessed most of the activities around BEPS, coupled with developments under the European Union (EU). The major developments have been around implementing the three tier transfer pricing documentation and CbC reporting, taxation of digital services, tax information sharing and enhanced disclosure measures.

D. Australia & Africa Australia has also been proactive in addressing BEPS-issues with changes proposed in its 2015 budget. While the momentum is relatively moderate in the African continent, in a recently concluded African tax authorities meet, countries expressed the need to counter BEPS, to promote information sharing and resource enhancement. One of the concerns expressed was with respect to the higher threshold for

CbC reporting relative to their region and propose to explore a lower threshold.

• EU developments: o Amendments to the Parent Subsidiary directive to deny participation exemption on

distribution of profits that are deductible by the subsidiary, introduction of general anti-avoidance rules and deterrence against use of hybrid loan arrangements to benefit from double non-taxation.

o Sharing of tax rulings among the member states o Proposal to extend scope of CbC reporting to public disclosure along with financial

statements to the extent feasible. • Countries with already existing Patent box regimes such as Spain, have modified it in line with

OECD BEPS recommendations to Action Plan 5. Further, Ireland and Switzerland have initiated discussions for such a scheme.

• VAT on electronic services introduced in Luxembourg. Turkey, too has expressed its intent to introduce a similar tax.

• Several countries including Spain, UK have already approved the implementation of the three-tiered transfer pricing documentation and CbC reporting suggested by OECD w.e.f. January 2016.

• France, Austria and Spain have adopted rules to deny deduction to payments made to related parties and are subject to no or low taxation.

• Significant tax changes have been proposed in the UK in the Budget, 2015 and otherwise. The UK Government has introduced a new tax ‘Diverted profit tax’ at the rate of 25%, applicable to large multinationals with business in UK who enter into ‘contrived’ arrangements to divert profits from the UK by avoiding a UK taxable permanent establishment and/or by other ‘contrived’ arrangements between connected entities. Further enhanced disclosure mechanisms have been proposed for taxpayers to disclose their tax strategies, personal accountability of named board member to tax strategies etc.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page7

Page7

#ta

xsut

ra

#

LNEv

ent

ww

w.le

xisn

exis

.co.

in

E. Americas The billion dollar question hanging over the BEPS projecct is the adoption of the BEPS outcomes by the US and so far the super-power is playing a bit tough to get; going by its decision to keep away from the process of development of multilateral instrument. The silver lining though – statement made by US Treasury officials Mr. Robert Stack that despite concerns expressed by senior Republican Congressmen, the US Administration has the powers to implement CbC reporting. But this is a space to keep a close eye on…

• Proposed revisions to the US Model Income tax convention was released in May 2015. The revisions target exempt permanent establishments, special tax regime, expatriated entities, anti-treaty shopping measures of limitation of benefits article and subsequent changes in treaty partner’s tax law. Expanding the CFCs regime, it is proposed to impose a minimum tax on foreign earnings above a risk-free return on equity invested in active assets.

• Discussions on introduction of patent box regime • US has also executed agreements under FATCA with several countries including India for

information exchange • Tax havens such as Cayman Islands, British Virgin Islands and Cyprus have launched the FATCA

notification and reporting mechanisms. Information obtained by the respective tax authorities will then be shared with US revenue.

• Mexico & South American countries such as Ecuador have adopted the CbC reporting and transfer pricing documentation requirements.

• Companies in Brazil are required to report information on tax-planning structures that leads to avoidance, reduction or deferral of tax if the transaction has no business purpose and economic substance; is done in an unusual manner or is identified in the guidance to be issued by the tax authorities. Brazil has also amended its CFC regime for selective consolidation for tax purposes.

• Chile has introduced CFC rules and adopted transfer pricing regulations for business restructuring. • Argentinean city has introduced withholding tax on payments to foreign providers of digital media.

• Australia to adopt transfer pricing documentation and CbC reporting by 2016. Also proposed indirect tax on digital goods and services and multinational anti-avoidance law to counter BEPS related structures that seek to avoid a taxable presence. It has further reduced the thin-capitalisation ratio from 3:1 to 1.5:1. Recently, Australian Senate Committee issued its interim report on corporate tax avoidance setting out recommendations, including greater tax transparency measures.

• South Africa has amended its CFC regime to exempt substantive business operations. It is also proposed to adopt the OECD CbC reporting with additional reporting requirements in relation to interest and royalty payments.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page8

Page8

#ta

xsut

ra

#

LNEv

ent

ww

w.le

xisn

exis

.co.

in

Experts’ Corner

BEPS impact on inbound and outbound investment – an Indian perspective

Punit Shah, Partner, Dhruva Advisors LLP

Cross-border investment structures (both inbound as well as outbound) have come under increased scrutiny around the world in recent years. This is aimed at countering practices such as treaty shopping and use of inefficiencies in treaty structures to achieve double ‘non-taxation’. In addition to steps that are being taken to address these issues at multilateral level under the aegis of the OECD’s BEPS project, several countries are also taking steps at the unilateral and bilateral level in this regard. The combined impact of such multilateral, bilateral

and unilateral steps on cross-border investments must be considered in order to better appreciate the framework within which businesses have to operate. Overview of BEPS in the context of cross-border investment structures: At the multilateral level, there are several areas of the BEPS initiative that have a bearing on inbound and outbound investments. Specifically, Action Item 6 (dealing with prevention of treaty abuse) and Action Item 3 (strengthening CFC Rules) need to be considered in this regard. As regards Action 6, a Report was issued by the OECD in 2014 which set out a three-pronged approach to tackling treaty abuse:

With the increasing scrutiny of cross-border investment structures, various multilateral, bilateral and unilateral steps are taken by countries to counter treaty shopping and use of inefficiencies in treaty structures to achieve double ‘non-taxation’. Punit Shah [Partner, Dhruva Advisors LLP] provides an incisive account of what this means for the Indian Investment climate. Talking about the BEPS proposals, the Author expresses concern that investment through Mauritius and Singapore could be hit hard and double-non taxation arising from the fact these countries do not levy tax on capital gains could also lead to a potential denial of treaty benefits. Discussing about the Indian actions in this regard, the Author concludes that access to favourable treaties may be increasingly restricted, and investors and foreign corporations seeking to invest in India will have to largely rely on their own country’s treaty with India.

BEPS Action Item 6 • Express statement in

treaties that contracting states intend to avoid double non-taxation/treaty shopping

• Specific anti-abuse rule based LOB Clause

• General anti-abuse rule based PPT

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page9

Page9

#ta

xsut

ra

#

LNEv

ent

ww

w.le

xisn

exis

.co.

in

a) The inclusion in treaties of an express statement that the Contracting States, when entering into a treaty, intend to avoid creating opportunities for non-taxation or reduced taxation through tax evasion or avoidance, including through treaty shopping arrangements

b) The inclusion in tax treaties of a specific anti-abuse rule based on the limitation-on-benefits

provisions included in treaties concluded by the United States and a few other countries (‘LOB’)(based on factors such as the legal nature, ownership, and general activities in the contracting state)

c) The introduction of a general anti-abuse rule based on a

Principal Purposes Test (‘PPT’) intended to address other forms of treaty abuse, including treaty shopping situations that would not be covered by the LOB rule described above

BEPS impact on India: Once implemented, the OECD BEPS proposals could have a significant bearing on how inbound investments into India are structured. For instance, investments through jurisdictions such as Mauritius and Singapore could be particularly hit hard. In addition to challenges that many investors may face in complying with stringent LOB provisions, double-non taxation arising from the fact that Mauritius and Singapore do not levy tax on capital gains could also lead to a potential denial of treaty benefits. To some extent, a specific LOB article may help in bringing an element of objectivity as to the availability of treaty benefits. However, compliance with the PPT could prove far harder, particularly mindful of the subjectivity involved. The inclusion of an express statement that the treaty is not intended to create opportunities for double non-taxation or for treaty shopping may also, in an Indian context, guide Courts and Tribunals towards a more purposive, rather than a strict textual interpretation of treaty provisions. From an outbound perspective as well, Indian corporations may find it difficult to route investments through multi-tier structures overseas, as these could significantly curtail the availability of treaty benefits. Given the potential for litigation, legitimate structures involving regional holding companies could also be adversely hit. The outcome of the OECD’s work on Action Item 3 in the context of CFCs could also be a key factor in the context of cross border investments. The implementation of robust CFC rules will limit the attractiveness of multi-tier structures and will limit the use of non-operating entities in cross-border investments. India had proposed to introduce a fairly comprehensive CFC regime as part of the Direct Taxes Code Bill, 2010 which lapsed recently. Any potential re-introduction of CFC norms by India may borrow from the work being done in the OECD on this topic. Unilateral and Bilateral measures: Simultaneously with the work being undertaken at the OECD, parallel efforts are being undertaken by India at a unilateral as well as bilateral level to counter treaty abuse. Specifically, at a bilateral level, India has been pushing hard for renegotiation of several key treaties with a view to plug abuse and treaty shopping. For instance, a protocol has been

“The inclusion of an express statement that the treaty is not intended to create opportunities for double non-taxation or for treaty shopping may also, in an Indian context, guide Courts and Tribunals towards a more purposive, rather than a strict textual interpretation of treaty provisions.”

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page10

Pa

ge10

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

signed with Singapore which sets out a LOB article in order to qualify for capital gains exemption. Reports indicate that the treaty with Mauritius is being renegotiated, particularly in respect of the capital gains exemption in India under the treaty. Additionally, most of the treaties that India has entered into in recent years or which have been modified through protocols provide for a LOB Article. Such LOB articles are not objective or comprehensive in nature and usually provide that treaty benefits shall not be available if the main purpose or one of the main purposes of setting up of such enterprise in the other contracting state is to obtain benefits under the treaty. Incidentally, such LOB clauses are somewhat akin to the PPT test that is contemplated as part of the BEPS project. Additionally, at a unilateral level as well, several steps are being undertaken by India which could have a bearing on the availability of treaty benefits in inbound situations. For instance, the Income-tax Act has been amended to make the availability of a Tax Residency Certificate mandatory for claiming treaty benefits. Additionally, a General Anti-Avoidance Rule (‘GAAR’) has been enacted (though not yet brought into force), which can be potentially invoked to deny treaty benefits. Additionally, it is provided that the provisions of GAAR will override tax treaties. At the field level too, the availability of treaty benefits, particularly in the context of Mauritius continues to pose practical challenges. There is a good deal of scrutiny of such claims under judicially evolved principles of anti-avoidance, which leads to litigation. This is notwithstanding favourable Circulars issued by the CBDT and several decisions from the judiciary upholding the availability of treaty benefits including the decision of the Supreme Court in the landmark AzadiBachaoAndolan case and more recently of the Punjab and Haryana High Court in the Serco BPO case. In conclusion, the tax treaty landscape, particularly in an Indian context, is likely to see far reaching changes in the years ahead. While a good part of such changes will be driven by developments at the OECD at a multilateral level, domestic law changes and bilateral renegotiations are likely to also play an equally significant role in this. Access to favourable treaties may be increasingly restricted, and investors and foreign corporations seeking to invest in India will have to largely rely on their own country’s treaty with India. Needless to mention, this could pose significant challenges, particularly in the context of collective investment vehicles and use of holding company structures. Existing structures too, will not be immune to such changes and may potentially have to be re-examined in the light of such changes.

“The tax treaty landscape, particularly in an Indian context, is likely to see far reaching changes in the years ahead. While a good part of such changes will be driven by developments at the OECD at a multilateral level, domestic law changes and bilateral renegotiations are likely to also play an equally significant role in this provisions.”

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page11

Pa

ge11

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page12

Pa

ge12

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Taxation of Digital Economy – BEPS proposals and the Indian approach

Ajay Rotti, Partner Hariharan Gangadharan, Dhruva Advisors LLP Associate Partner

It is now increasingly recognized that the current international tax regime which has evolved over the course of the last century is inadequate to deal with rapid changes that are taking place in global marketplace. Thanks to the increased digitisation of business, the difficulties in applying the traditional rules and principles designed in the context of a brick and mortar economy to the digital world are becoming increasingly widespread and affect both taxpayers as well as tax administrators. While businesses (both pure technology companies as well as companies that use technology to expand their geographical reach) face serious uncertainties on the tax front, Governments perceive an erosion of the tax base through transactions undertaken in the borderless digital world. The OECD’s BEPS Action 1 on addressing the tax challenges of the digital economy as part of the BEPS initiative is largely an outcome of this recognition. India is a part of this initiative and is expected to play a crucial role in influencing the ultimate outcome of this exercise. The BEPS proposals The BEPS initiative in relation to the digital economy focused on identifying the difficulties involved in applying existing international tax rules to the digital economy and to develop detailed options (both from a direct and indirect tax perspective) to address these difficulties. The Report released in September 2014 in this regard contains a detailed overview of the key features of the digital economy,

Global businesses speeding into the digital era has necessitated the need to reform the traditional tax concepts. Ajay Rotti [Partner, Dhruva Advisors LLP] and Hariharan Gangadharan [Associate Partner] trace the taxation of digital economy in India along with an analysis of the BEPS proposals. The Authors state that the initiative to address these challenges must not be viewed as a zero-sum negotiation game involving a conflict between ‘residence’ and ‘source’ based taxation. Finally, the Authors call for a for a wider debate as to whether India’s interests lie solely in gathering additional revenue, or in ensuring that the global rules for taxing the digital economy do not hamper the growth of India promising digital sector or block the penetration of new technologies and digital businesses in India.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page13

Pa

ge13

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

• Cannot ring-fence digital economy for tax purposes

• Development of ‘virtual PE’

• VAT, CFC and artificial avoidance of PE

various existing business models which present challenges from a tax perspective as well as potential options to address them. While no final conclusions emerged from this Report, the following key findings are nonetheless indicative of the approach being adopted to address this issue: a) The digital economy cannot be ring-fenced for tax purposes b) The development of a ‘virtual PE’ standard as an alternative

theory of nexus for digital commerce operations was considered, but not currently recommended

c) Other issues of relevance in relation to the digital economy are

to be addressed as part of other initiatives on VAT, CFC, and artificial avoidance of PE etc. d) The OECD task force on the digital economy is expected to continue its work and issue a

supplementary report by December 2015

The Indian approach Indians are increasingly becoming voracious consumers of digital goods and services and the Government tends to view the revenue implications of this trend with some concern. To counter this, India has long adopted an aggressive ‘source’ based approach to the digital economy. This inter alia entails:

a) Seeking to tax foreign companies in India by treating websites as permanent establishments b) Characterising payments for digital goods/services as royalties or technical fees c) Widening the scope of withholding payments for digital goods and services

Courts in India are now dealing with several such cases, and it is only likely that such cases will increase in number and complexity in the years ahead. Most of such cases are currently at the level of the Income-tax Appellate Tribunal (‘ITAT’), but are expected to be taken in further appeals to the High Courts and the Supreme Court. For instance, in the case of ITO vs. Right Florists Pvt. Ltd. (154 TTJ 142), the ITAT held that a website could not per se be regarded as a permanent establishment of a foreign company, unless the servers are located in India. It is

relevant to note that the Commentary to the OECD’s Model Convention states that where an enterprise carries on business through a website hosted on its server (leased or owned), the place where such server is located could constitute a permanent establishment of the enterprise if the other requirements of Article 5 are met. India has stated that it does not agree with such an interpretation. It is of the view that a website may constitute a permanent establishment in certain circumstances. However, it has not spelt out the circumstances under which it would consider a website as constituting a permanent establishment. The ITAT in the Right Florists case took note of the above reservations made by India. However, it concluded that such reservations made to the commentary would be relevant only for interpreting tax treaties entered into by India after expressing such reservations. In other words, it found that these reservations would not have any impact in interpreting the meaning of the term permanent establishment under treaties that India has entered into prior to 2008 (which is when such reservations were expressed).

“India has long adopted an aggressive ‘source’ based approach to the digital economy”

“In the case of ITO vs. Right Florists Pvt. Ltd. (154 TTJ 142), the ITAT held that a website could not per se be regarded as a permanent establishment of a foreign company, unless the servers are located in India”

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page14

Pa

ge14

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

The characterisation of payments for digital goods and services as royalties or fees for technical services is also becoming the subject matter of litigation in India. Specifically disputes surrounding characterisation of payments for access to digital databases, e-learning courses etc. are also coming up before the Courts with increasing frequency. Media reports indicate that India is advocating such a source based approach in relation to the digital economy at the OECD as well. The way forward The multilateral initiative to address tax challenges arising from a digital economy is in its essence an attempt to build a global consensus for reforming the international tax regime. It must not be viewed as a zero-sum negotiation game involving a conflict between ‘residence’ and ‘source’ based taxation. Indeed, the very need for this exercise stems from the fact that the traditional concepts of ‘residence’ and ‘source’ are difficult to apply in the digital world. While India’s interests undoubtedly need to be protected, there is a need for a wider debate as to whether India’s interests lie solely in gathering additional revenue, or in ensuring that the global rules for taxing the digital economy do not hamper the growth of India promising digital sector or block the penetration of new technologies and digital businesses in India. Specifically, in the context of the Prime Minister’s ambitious ‘Digital India’ initiative, one would expect that India’s positions on the tax front, both domestically as well as in multilateral forums such as the OECD are geared to support the long term vision to transform India into a digitally empowered society and knowledge economy.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page15

Pa

ge15

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

BEPS: India Insights

Sunil Shah, Partner Pritin Kumar, Partner Deloitte India

Backdrop

The G20 had initiated the Base Erosion and Profit Shifting (‘BEPS’) project to ensure that profits are taxed where economic activities are performed and where value is created. At the request of the G-20, the Organisation for Economic Co-operation and Development (‘OECD’) developed an action plan to tackle BEPS in a comprehensive manner. India, being part of the G20, is bound by the final announcements on BEPS. In September 2014, the OECD published seven papers as a first tranche of deliverables under the BEPS project. There have been some revised papers and new discussion drafts issued in the past year and the eight papers forming the second tranche of deliverables is expected shortly.

Action items The OECD has identified 15 action points to combat BEPS as summarised in the table below.

Action 1: Address the tax challenges of the digital economy

“Gaps” Establishing international coherence of corporate income taxation

“Frictions” Restoring the full effects and benefits of international standards

“Transparency” Ensuring transparency while promoting increased certainty and predictability

In recent times, discussions on tax remain incomplete without reserving time for BEPS. Two years into its development, it is time for the curtains to be raised or perhaps already risen by the time you are reading this. While BEPS is of significance for the entire world, Sunil Shah [Partner, Deloitte] and Pritin Kumar [Partner, Deloitte] capture its essence in the Indian context. The Authors give an account of the relevance of each action plan vis-à-vis the present Indian tax regime. Further the Authors draw inference on India’s position out of the recent tax developments and India’s response to the UN questionnaire on BEPS. They also note the key actions in the tax world as a result of BEPS action plans such as LOB rule, deferment of GAAR, tribunal notings, etc. Stressing upon the need to be abreast with BEPS developments, the Authors conclude that constant change in tax policy matters affecting taxpayers’ rights and obligations provides taxpayers an opportunity to have a relook at their operational arrangements and investment structures and to assess the impact of the BEPS project on their business.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page16

Pa

ge16

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Action 2: Neutralize the effects of hybrid mismatch arrangements

Action 6: Prevent treaty abuse

Action 11: Establish methodologies to collect and analyze data on BEPS and the actions to address it

Action 3: Strengthen controlled foreign company (CFC) rules

Action 7: Prevent the artificial avoidance of PE status

Action 12: Require taxpayers to disclose their aggressive tax planning arrangements

Action 4: Limit base erosion via interest deductions and other financial payments

Assure that transfer pricing outcomes are in line with value creation

Action 8: Intangibles

Action 13: Re-examine transfer pricing documentation

Action 5: Counter harmful tax practices more effectively, taking into account transparency and substance

Action 9: Risk and capital

Action 14: Make dispute resolution mechanisms more effective

Action 10: Other high-risk transactions

Action 15: Develop a multilateral instrument

Action 1, dealing with digital economy cuts across all actions and impacts, and is in turn impacted by, all the other action points. Action 15 binds all the action items together and proposes a multilateral instrument, which would have the same effect as simultaneous renegotiation of the 3,000+ bilateral treaties that are currently in effect, for implementation of the BEPS actions.

BEPS in the Indian Context From a corporate tax perspective, the most important action is Action 6 dealing with treaty abuse. Broadly speaking, Action 6 proposes a principal purposes test [PPT] rule or a limitation on benefits [LOB] rule supplemented by a PPT rule. From an Indian standpoint, India has already legislated a general anti-avoidance rule [GAAR] in its domestic tax law – the GAAR empowers the tax authorities to look through arrangements, the main purpose of which is to obtain a tax benefit and which inherently lack commercial justification, amongst other conditions. The GAAR and LOB / PPT rule may, inter alia, impact intermediate holding companies for investing into India, which lack substance and have been interposed only to avail tax treaty benefits. Similarly, such rules may challenge and aggressive tax structures put in

place in India using intermediate companies in favourable treaty jurisdictions. Incidentally, Mauritius has been a popular intermediary jurisdiction for investing into India in view of the capital gains exemption – newspaper reports indicate that India is actively trying to renegotiate the tax treaty with Mauritius.

Corporate tax perspective: Action 6: “The GAAR and LOB / PPT rule may, inter alia, impact intermediate holding companies for investing into India, which lack substance and have been interposed only to avail tax treaty benefits.” Action 7: “India is ahead of the OECD on this Action.” Action 2: “the possibility of the tax authorities questioning hybrid financial instruments, especially imported mismatch arrangements (i.e. interposing an intermediate finance company leading to a hybrid mismatch), cannot be ruled out.”

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page17

Pa

ge17

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Action 7 dealing with preventing the artificial avoidance of permanent establishment [PE] status is also an important action from an Indian perspective. Interestingly, some of the tightening of norms under Action 7that are mentioned below are: (a) already in place under many of India’s tax treaties; or (b) the interpretation followed by tax authorities; or (c) India’s stated position in respect of the OECD model convention. Accordingly, India is ahead of the OECD on this Action. • Wide interpretation of the term ‘conclude contracts’

• Strengthening of the requirements for an agent to be considered ‘independent’ only if it acts on

behalf of various persons (and not only group companies)

• Exclusion of ‘delivery’ from the specific activity exemptions • Inclusion of insurance companies within the purview of PE Another interesting action from a corporate tax perspective is Action 2 dealing with hybrid mismatches –such hybrid mismatches could be on account of hybrid entities or hybrid financial institutions. Historically, hybrids have not been much of an issue from a tax perspective in India. A popular instrument that could be regarded as a hybrid in certain situations is compulsorily convertible debentures. With Action 2 of BEPS, the possibility of the tax authorities questioning hybrid financial instruments, especially imported mismatch arrangements (i.e. interposing an intermediate finance company leading to a hybrid mismatch), cannot be ruled out. From a Transfer Pricing (TP) standpoint, Action 13 is the most significant action from an Indian perspective – this action provides for a three-tiered approach to TP documentation:

(1) a Country-by-Country [CbC] report to provide a global financial snapshot; (2) a master file to provide a high-level view of a company’s business operations and important information on company’s global transfer pricing policies, with respect to intangibles and financing; and (3) a local file to provide an entity and transaction level transfer pricing analysis. Whilst the Indian transfer pricing regulations broadly cover the content of a local file, the regulations presently do not provide maintenance of the information contemplated in the master file and CbC template. It is pertinent to note that the new guidance will provide tax authorities with substantial information to assess if there is any transfer pricing risk resulting in artificial shifting of taxable income in tax advantaged jurisdictions. Accordingly, taxpayers that currently do not follow consistent transfer pricing policies on a global basis may find a need to do so in the near future along with centralised management, implementation and documentation of a group’s transfer pricing policies Action item 8, 9 & 10 deal with the aspects to assure that transfer pricing outcomes are in line with value creation. It includes special measures respectively (1) to ensure that inappropriate returns will not accrue to an entity solely because it has contractually assumed risks or has provided capital (2) to clarify the circumstances in which transactions can be re-characterised, and (3) special measures for transfers of hard-to-value intangibles.

Transfer pricing Perspective: Action 13: “the new guidance will provide tax authorities with substantial information to assess if there is any transfer pricing risk resulting in artificial shifting of taxable income in tax advantaged jurisdictions.” Action 8: “while the revised guidance does not provide for any additional compensation for group synergies, provision of centralised services and subsequent allocation of costs and benefits have been a controversial issue in India.” Action 9: “is extremely open-ended and vague and may result in multiple interpretations resulting in increased TP disputes” Action 10:“Given the significant litigation in India in respect of intra-group services, this action is of immense significance for Indian tax authorities as well as the taxpayers.”

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page18

Pa

ge18

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Action 8 deals with guidance on TP aspects of intangibles. In determining compensation for use or transfer of intangibles, importance is given to contribution of the group companies in Development, Enhancement, Maintenance, Protection and Exploitation (‘DEMPE’) of intangible. While the Indian TP provisions have wider definition of intangibles, most of the guidance provided on

intangible by the OECD is in line with the practices followed by the Indian tax authorities. For instance, in the revised guidance on intangible, conduct of group companies is considered important than contractual arrangement between them for appropriate compensation in an intangible transaction. Similar approach has been followed in Circular No. 6/ 2013 (‘Circular’) issued by the Central Board of Direct Taxes (‘CBDT’) which deals with classification of Indian contract Research and Development (R&D) centres of overseas MNE entities bearing insignificant risks. It also emphasizes on conduct of the parties than contractual arrangement and considers the performance of significant people functions and control over service providers by foreign principal as important factors for determining the contribution of Indian R&D centre in the development of intangibles and its related

compensation. Jurisprudence in case of intangible transactions is still at a nascent stage in India. Tax authorities have, in recent audits, raised the issue of arm’s length returns to entities that are not legal owners of intangible assets but are seen to have economic ownership. However, there are certain views of tax authorities that contradict with position in the OECD guidance. The OECD guidance provides that no separate compensation for location savings / location specific advantages is required if there exist local comparable uncontrolled transactions. But, it is a belief of Indian tax authorities that such an approach may not consider the benefit of location savings which can be computed by taking into account the cost difference between costs in the low cost country and in the high cost country from where the business activity was relocated. Further, definition of intangible as provided in the revised guidance on intangible does not consider assembled workforce whereas the Indian TP regulations considers trained and organised work force as an intangible property requiring compensation for any related transaction. Moreover, while the revised guidance does not provide for any additional compensation for group synergies, provision of centralised services and subsequent allocation of costs and benefits have been a controversial issue in India. Action 9 relating to risk and re-characterization lays emphasis on ‘value creation’ and examination of ‘options realistically available” in identifying the commercial and financial relations between the AEs. The rules to be developed require alignment of returns with value creation. Further, it also provides that a transaction between AEs should have the “fundamental economic attributes of arrangements between unrelated parties” else, the tax authorities may resort to non-recognition or re-characterization of such transaction. This will involve adopting transfer pricing rules or special measures to ensure that inappropriate returns will not accrue to an entity solely because it has contractually assumed risks or has

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page19

Pa

ge19

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

provided capital. Action 9 is extremely open-ended and vague and may result in multiple interpretations resulting in increased TP disputes. Therefore, it is imperative that OECD may consider providing concrete and detailed definition or guidance to avoid arbitrary application and aggressive interpretations by the tax authorities. OECD Discussion Draft on Action 10 proposes a simplified transfer pricing approach for low value-adding intra-group services. The aim of this Discussion Draft is to reduce base erosion through excessive management fees and head office expenses, particularly in developing countries. In the said draft, the OECD has defined low value-adding intra-group services as those which are supportive in nature, are not part of the core business of the group and do not use or create unique and valuable intangibles involving significant risk. The draft recognises that the arm’s length price of such intra-group services is closely related to costs and provides mechanism to allocate the costs of providing each category of such services to those group companies which benefit from such services using consistent group-wide allocation keys with an associated consistent small mark-up. In Indian context, tax authorities have been closely scrutinised numerous cases on intra-group services and challenging the payments for such services based on factors such as demonstrating actual receipt of services, their benefits, their need, willingness to pay, lack of proper documentation, etc. In this regard, the proposed simplified approach to low-value adding services will be helpful for some MNE groups. However, India, in its response to the United Nations’ questionnaire on BEPS has indicated that one of the major ways in which base erosion takes place is through excessive payments to foreign affiliated companies in respect of service charges, management and technical fees, royalties and interest.

Further, as per the Discussion Draft, proposed provisions shall be applicable even in cases where the low value-adding services may be the core business activity of the legal entity providing the service (e.g. a shared service centre); as long as the same is not the core activity from the perspective of the operations of the MNE group. Accordingly, from a service provider point of view, many of such services provided by the shared service centres /captive back offices may classify as low value adding intra-group services and therefore, may qualify for the simplified approach and a suggested mark-up of 2% to 5% for such provision of services. However, the Indian tax authorities would challenge the arm’s length nature of the service fee earned by these entities which is much lower than the Safe Harbour rates prescribed by in India. Further, the mark-up required to be earned by service providers has been a contentious issue wherein Indian tax authorities expect significantly high mark-ups. Therefore, the suggested approach in this draft of classifying the said services as low value-adding and the proposed mark-ups may not find favour with the Indian tax authorities. Given the significant litigation in India in respect of intra-group services, this action is of immense significance for Indian tax authorities as well as the taxpayers.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page20

Pa

ge20

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Last but not the least, is the development of a multilateral instrument in terms of Action 15 that binds the BEPS project. India, in its response to the UN questionnaire on BEPS (see the discussion in the section ‘India’s stated position on BEPS’ below), has indicated that developing a multilateral instrument is a high priority action because a multilateral instrument that is binding on all countries is of utmost necessity to combat tax treaty abuse, which is one of the primary concerns of developing countries like India. It is also interesting to note that India is a signatory to the SAARC limited multilateral agreement on avoidance of double taxation and mutual administrative assistance in tax matters and has recently signed the Multilateral Competent Authority Agreement on Automatic Exchange of Financial Account Information.

India’s stated position on BEPS The UN Subcommittee on BEPS invited developing countries to provide feedback on experiences regarding BEPS issues in the form of a questionnaire. India, in its response to the UN questionnaire, has identified the following as the most common practices and structures from a BEPS perspective: • Excessive payments to foreign affiliated companies in respect of interest, service charges,

management and technical fees and royalties (this is despite the fact that India follows source-based taxation in relation to royalties and fees for technical services and imposes a withholding tax).

• Aggressive transfer pricing, including supply chain restructuring that contractually allocates risks and profits to affiliated companies in low tax jurisdictions.

• Digital enterprises facing zero or no taxation in view of the principle of residence-based taxation.

• Artificial avoidance of permanent establishment status.

• Treaty shopping.

• Incentives in the tax laws for attracting investment.

• Assets situated in India are owned and sold by companies located in low tax jurisdictions with no substance.

Another area highlighted by the administration is the fact that it is extremely difficult to obtain the relevant information needed to assess and address BEPS concerns, and to accurately apply the relevant transfer pricing rules. It’s been indicated that the lack of transparency on the part of the multinational firms, and the lack of adequately trained resources are the two biggest hurdles in determining whether a firm has reported the correct profits for taxation in India.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page21

Pa

ge21

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Level of activity in India on account of BEPS

In the 2015 Budget, the GAAR, which was slated to be implemented from 1 April 2015, has been deferred by two years to 1 April 2017. One of the key reasons cited for the deferment of GAAR is that India is an active participant in the BEPS project and the reports on various BEPS action plans and recommendations regarding the measures to counter it are awaited – it is therefore proposed to implement GAAR as part of a comprehensive regime to deal with BEPS and aggressive tax avoidance. It is pertinent to note that India has already started re-jigging the existing bilateral tax treaties to prevent treaty shopping by insertion of PPT and LOB rules. Similarly, most of the new tax treaties of India typically contain a PPT / LOB rule. Incidentally, India has a special provision in its tax law that empowers the government to impose additional tax

burden and compliance requirements for certain notified countries if there is lack of effective exchange of information. Cyprus has been notified in terms of these provisions. Interestingly, Action 3 of the BEPS project deals with Controlled Foreign Corporation [CFC] rules. India does not have CFC rules in its legislature –going by the logic on GAAR, it is likely that India may introduce CFC rules after the finalisation of Action 3. The Delhi Tribunal in a recent ruling in the case of Baker Hughes has made some interesting observations in the context of BEPS. The Tribunal has observed that BEPS is a tax policy consideration which is relevant for the process of law making, but it cannot have a role in the judicial decision making process because judicial process will infringe neutrality if it is to be swayed by such policy consideration. It also observed that judicial authorities are to interpret the law as it exists and not as it ought to be in the light of certain underlying value notions. It is however pertinent to note that apart from the above, there has not been much development on the legislative front in the context of BEPS. On the contrary, the Indian legislature appears to be waiting for the BEPS actions to be finalised before taking any significant unilateral action. Conclusion BEPS seems largely targeted at getting the tax haven jurisdictions to tighten up their tax and disclosure laws. India as a large market and importer of capital has already independently put in place several anti-avoidance measures to counteract BEPS. The other requirements of the OECD BEPS initiative such as CbC reporting, hybrid instruments, etc. are not unique to India and will need to be implemented by all countries. Having said this, taxpayers need to be aware of and constantly monitor the ongoing BEPS Actions as well as the changes that India is bringing about in its domestic law and tax treaties. It will also be interesting to see how the Indian judiciary deals with the concepts of GAAR, LOB and PPT as well as other BEPS actions. Constant change in tax policy matters affecting taxpayers’ rights and obligations provides taxpayers an opportunity to have a relook at their operational arrangements and investment structures and to assess the impact of the BEPS project on their business.

“The Delhi Tribunal in a recent ruling in the case of Baker Hughes has made some interesting observations in the context of BEPS. The Tribunal has observed that BEPS is a tax policy consideration which is relevant for the process of law making, but it cannot have a role in the judicial decision making process because judicial process will infringe neutrality if it is to be swayed by such policy consideration.”

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page22

Pa

ge22

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Goods & Services Tax (GST)

Taxsutra Brief: Overview Since implementation of MODVAT (now CENVAT) in 1986 and VAT in 2005, GST will be by far, be the most significant indirect tax reform in India. Scope / features of current GST model in India: The “dual” structured GST, first envisioned by the Empowered Committee of State Finance Ministers in 2009, seeks to subsume both Central as well as State taxes as follows: • Central Excise Duty, Additional Excise Duties, Service

Tax, Additional Customs Duty (CVD) and Special Additional Duty of Customs (SAD), Central Sales Tax, Central Surcharges & Cesses etc. in CGST;

• VAT / Sales Tax, Entertainment Tax not levied by local bodies, Octroi & Entry Tax, Purchase Tax, Luxury Tax, Taxes on Lottery, betting & gambling, Taxes on advertisements etc. under SGST.

As per the Constitution (122nd Amendment) Bill 2014 passed by Lok Sabha in May 2015, alcoholic liquor for human consumption shall be exempt, while GST will not apply to (a) petroleum crude, (b) high speed diesel, (c) motor spirit (petrol), (d) natural gas, and (e) aviation turbine fuel, till a later date. Tobacco and tobacco products will be subject to GST with Centre empowered to impose excise duty additionally thereon. States shall have power to levy taxes on these items, except in case of imports and inter-state trade. Responding to the expectations of Revenue Neutral Rate (RNR) i.e. the rate at which there will be no loss to States after GST implementation, to be pegged at 27%, Union Finance Minister Arun Jaitley has assured Parliament that same would be much lower. As per the Bill, States where goods originate can levy 1% additional non-VATable tax over GST to make up any revenue loss for the first 2 years.

GST worldwide: With the increase of international trade in services, GST has become a preferred global standard. All OECD countries, except the US, follow this tax structure. GST was introduced in Australia in 2000. Whilst the rate is currently set at 10%, there are many domestically consumed items that are effectively zero-rated (GST-free) such as fresh food, education, and health services, as well as exemptions for Government charges and fees that are themselves in the nature of taxes.

Milestones in India’s indirect tax regime 1934 : Wide range of new articles brought within scope of central excise duty, alongwith sugar, matches and steel ingots 1956 : Central Sales Tax (CST) introduced to tax inter-state supply of goods 1986: MODVAT Scheme introduced to allow set-off of duty paid on purchased inputs against output liability 1994 : Service tax levied on certain services under Chapter V of Finance Act 2005 : Replacing the sales tax regime, Value Added Tax (VAT) implemented in most of the States 2016: GST ?

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page23

Pa

ge23

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Canada introduced GST in 1991 at a rate of 7%, later reduced to current rate of 5%. A Harmonised Sales Tax (HST) which is combined GST and provincial sales tax, is collected in some of the provinces of Canada. Common zero-rated items include basic groceries, prescription drugs, inward/outbound transportation and medical devices. Tax-exempt items include long term residential rents, health and dental care, educational services, day-care services, legal aid services, and financial services. Hong Kong failed to implement GST amidst political protests, where plan was finally withdrawn in December 2006 owing to lack of public support. Jersey, Channel Islands implemented GST in 2008. Current rate is 5% and businesses (predominantly in financial services sector) may be exempt if they obtain approval for International Services Entity (ISE) status. GST has been implemented in Malaysia w.e.f. April 2015 on most supply of goods and services, with 6% rate. Like India, GST Bill 2009 was delayed amid mounting criticism but was finally announced by Malaysian Prime Minister during Budget 2014. Agricultural products like paddy, fresh & chilled vegetables, essential foodstuff such as oil, salt & flour, eggs, livestock, and first 300 units of electricity for domestic use have been zero-rated; while sales / lease / rental of residential land / property, domestic mass public transportation, land for general use, private healthcare, education and diesel, RON95 petrol & LPG have been exempted from GST. All businesses with annual sales turnover of more than RM 500,000 were mandated to register under GST before December 31, 2014, while for those with lesser revenue, registration was optional. Rebate of RM 1,000 in the form of e-voucher had been given to company who purchased GST Accounting Software. Maldives adopted GST in 2011 with a rate of 3.5% from October to December 2011 and 6% from January 2012 to December 2012. From January 2013 to October 2014, the GST rate on tourism sector was at 8%, which has increased to 12% from November 2014 onwards.

New Zealand introduced GST way back in 1986 and is currently levied at 15%. From July 1989 to September 2010, GST was levied at 12.5%, and prior to that at 10%. In Singapore, GST was implemented in 1994 at single rate of 3%, with an assurance that it would not be raised for at least five years. The same was increased to 4% in 2003, to 5% in 2004, accompanied by an offset package to make average Singaporean household overall better off, even after accounting for additional costs imposed by the increase in GST rates. The rate was increased once again to 7% w.e.f. July 2007.

Country Implemented on

Australia 1 July 2000

Canada 1 January 1991 Jersey, Channel Islands 6 May 2008

Malaysia 1 April 2015

Maldives 2 October 2011

New Zealand 1 October 1986

Singapore 1 April 1994

Administered by:

Australia – Australian Taxation Office

Canada – Canada Revenue Agency

Jersey, Channel Islands – Comptroller of Taxes

Malaysia – Royal Malaysian Customs Department

Maldives – Maldives Inland Revenue Authority

New Zealand – Inland Revenue and New Zealand Customs

Singapore – Inland Revenue Authority of Singapore

In India, GST would be administered by both, CBEC at Union level & Commercial Tax departments at State level. GST Council, comprising of Union Finance Minister, Union Minister of State for Revenue and State Finance Ministers will recommend rates of tax, period of levy of additional tax, principles of supply, special provisions for certain states, etc.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page24

Pa

ge24

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Experts’ Corner

GST - Through the Looking Glass

L. Badrinarayanan, Partner, Lakshmikumaran & Sridharan, Attorneys

The talk of the town today is GST (Goods and Services Tax). GST has been touted as solution to all the ills that plague our current taxing regimes. It is supposed to be progressive, clear and easy to comply. GST in whatever form is implemented in India can only be for the better. But before we really appreciate what is GST, we must understand what is the GST we are talking about and what it holds for us as companies and us as consumers. This article seeks to explain what it means to us and what we must be prepared for.

The Goods and Services Tax (‘GST’) has been one of the most ‘popular’ taxes in the world. In the last 50 years, it has spread to over 160 countries across the world. While there are variations, the economic concept has remained the same. The tax is a multi-stage destination based consumption tax. The legal concept continues to remain tax on ‘supply’ with credit of taxes paid at an earlier stage. By making consumption the centrepiece of the tax, GST reflects accurately the taxes that a State must receive. Any other basis i.e. tax on business or a particular event (eg. Manufacture, import,

entry, etc) can lead to a distortion in tax entitlement by tax avoidance at that stage or event. GST on the other hand disincentives distortions of this nature and is consequently successful. For India as a Federal State, GST is its biggest disruptor. GST has far-reaching (and unpredictable) consequences for the individual States. GST has attracted both love and hate. GST has pushed the States to seek assurances from the Centre. GST fundamentally changes the way States earn their revenue from taxes. Gone will be the days of origin-based VAT where producing States enjoyed the fruits of their investment. Goods,

GST, one of the most popular taxes adopted by over 160 countries in the world, has been marred by uncertainty in India. While Centre has succeeded to bring majority of States on board, there still remains few niggles, that are yet to be addressed. In this must read article, the Author L. Badrinarayanan [Partner, Lakshmikumaran & Sridharan, Attorneys] explains what this most sought after reform has in store for the corporates and the consumers, by way of an illustration. The Author highlights the current distortions to an ideal GST regime in the country such as conflicting views with regard to RNR as also levy of 1% additional levy on interstate supplies. However, Author believes that all the players who are not ultimate consumers for a particular goods or service would benefit as the actual cost of goods in their hands would go down; and exports made at any stage would become zero-rated, thereby fostering economic growth of the country.

“The Goods and Services Tax (‘GST’) has been one of the most ‘popular’ taxes in the world. In the last 50 years, it has spread to over 160 countries across the world.”

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page25

Pa

ge25

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

Services & taxes will move to the State of consumption. Hailed by the Industry as being progressive, States are now tuned to introducing these tax reforms. With additional revenues in the form of tax on services and assurances from the Centre, the States look towards GST more favourably but not without doubts. The travails of the States are well documented and reported. The benefit to the Industry is well understood. But the implications for the end-consumer are not so clear. In a broad sense, it is assumed that it would be beneficial to the consumer. The rate also is discussed in terms of being revenue neutral, i.e. it is to reflect the current taxes collected by the authorities. Therefore, the general sense is that end-consumer is likely to not endure any increase except to face a higher absolute tax on his bills. It is this aspect that this article seeks to understand further. In order to achieve this, basic GST concepts are outlined and then their implications in form of an illustration are discussed.

What is GST? GST is a tax on the supply of goods and services. In the existing taxation regime different events in the lifecycle of a goods or service, like manufacture, sale, entry, etc., are taxed by the Central or the State Government in accordance with the powers conferred by the Constitution of India, the GST is a simultaneous levy of tax

by both the Governments on the ‘SUPPLY’ of goods or services or both. The tax levied by the Centre would be called Central GST (‘CGST’) and that by the State would be called State GST (‘SGST’). The interstate supply would attract Integrated GST (‘IGST’). CGST and SGST would apply simultaneously on intra-state supplies and IGST would be attracted on inter-state supply. The myriad taxable events would be a thing of the past and ‘SUPPLY’ will be the order of the day. Though ‘supply’ has not been defined as yet, reference to foreign jurisprudence would show that supply means making available either goods or services. Distortions to an ideal GST The reason I use the word ‘ideally’ is because, we are once again facing a situation where a band rate for standard rated goods is a distinct possibility. Some essential goods and services are likely to be taxed at a lower rate and some to be exempted. The Government is unable to settle on a Revenue Neutral Rate (‘RNR’). The RNR is a rate which would ensure the present level of revenue collection to the Government when GST is implemented. Present conflicting views place the RNR anywhere between 18 to 27 percent. This is an area of concern that shall affect the ultimate consumer the most. The relief from the 2% CST cost has been cut short by the additional levy of 1% on interstate supply for a consideration. This is not the ideal GST, but it is far better off than

where we are today. GST credit mechanism As mentioned earlier, credit of CGST, SGST and IGST paid on all goods and services would be available barring a few excluded items. The credit of IGST can be used for the payment of IGST, CGST and SGST and vice versa. The credit of SGST

used for payment of IGST shall be transferred by the exporting state to the Centre and likewise, the amount of IGST credit used for the payment of SGST would be paid by the Centre to the respective State Government. Cross utilization between CGST and SGST would not be allowed. The final redistribution of GST amongst the States would be made by the Centre depending upon the actual consumption of goods and services. This is the plan to unify India into a single market.

“This is not the ideal GST, but it far better off than where we are today.”

“The myriad taxable events would be a thing of the past and ‘SUPPLY’ will be the order of the day.”

“GST fundamentally changes the way States earn their revenue from taxes. Gone will be the days of origin-based VAT where producing States enjoyed the fruits of their investment.”

“Present conflicting views place the RNR anywhere between 18 to 27 percent. This is an area of concern that shall affect the ultimate consumer the most.”

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page26

Pa

ge26

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

A closer look at GST Coming back to the question, whether GST is capable of delivering its promise? In transformations of such scale, the macro picture often overshadows the micro picture. A quick simulation of the GST model would throw light on the financial aspects of GST from both the business and consumer point of view. Let us assume a simple situation where a manufacturer produces goods in Maharashtra for Rs. 100, adds a Rs. 20 margin and stock transfers to say Madhya Pradesh against Form F without paying CST. Thereon, he sells it to a distributor. Assume the total VAT and local levies amount to 14.5%. The Excise duty is assumed to be 12.5%. The distributor adds margin of Rs. 20 and sells to a local retailer who adds further Rs. 30 margin and sells to the end customer. The numbers would look something like this: Maharashtra Madhya Pradesh

Manufacturer Depot Distributor Retailer Landed Cost 100

Landed Cost 136

Landed Cost 161

Landed Cost 184

Margin 20

Depot Cost 5

VAT Credit 20

VAT Credit 23 Excise Duty 16

Margin -

Actual Cost 141

Actual Cost 161

CST -

VAT 20

Margin 20

Margin 30 Final Price 136

Final Price 161

VAT 23

VAT 28

Final Price 184

Final Price 218

Note: Reversal of input tax credit on stock transfer of goods under Form F has not been considered. Assume GST to replace the existing tax regime. The same transaction with same margins would look as follows: Maharashtra Madhya Pradesh

Manufacturer Depot Distributor Retailer Landed Cost 100

Landed Cost 152

Landed Cost 159

Landed Cost 184

Margin 20

IGST Credit 32

CGST Credit 15

CGST Credit 17 IGST 32

Actual Cost 120

SGST Credit 19

SGST Credit 22

1% Levy -

Depot Cost 5

Actual Cost 125

Actual Cost 145 Final Price 152

Margin -

Margin 20

Margin 30

CGST 15

CGST 17

CGST 21

SGST 19

SGST 22

SGST 26

Final Price 159 Final Price 184 Final Price 222

Note: The landed cost for manufacturer may be lower in the GST regime due to removal of cascading effect. The same has not been considered in the illustration. The important points that need a close look are: Present Regime -‐ Excise duty becomes a cost for the onward transactions

-‐ The Central Government collection is limited to Rs. 16 and no share in onward value additions in

sale transactions

-‐ The total State Government collection is 28. Total imputed tax cost in price to consumer is Rs. 43 out of Rs. 218.

Taxsutra Conclave 2015 – International Tax at Crossroads, Plotting the Future

www.taxsutra.com www.tp.taxsutra.com www.idt.taxsutra.com www.lawstreetindia.com

Page27

Pa

ge27

#

taxs

utra

#LN

Even

t w

ww

.lexi

snex

is.c

o.in

GST Regime -‐ Both the Centre and States get a chunk of the

pie at each stage of movement of the goods till the final consumer.

-‐ The Central levy does not cascade and is available to be utilised against output liability at stages subsequent to manufacture.

-‐ The actual cost of goods at the depot, distributor and retailer stage in the GST regime is lower at Rs. 120, 125 and 145 as opposed to Rs. 136, 141 and 161 in the present regime.

-‐ The working capital blockage is higher in the GST regime. In the present regime, goods can be stock transferred (F Form) simply on payment of excise duty @ 12.5% against GST @ 27%.

-‐ Total tax collection in the GST regime for Centre is Rs. 21 and the States is Rs. 26 totalling Rs. 47 which is Rs. 4 higher than the present regime.

-‐ Though the States seem to be losing out on revenue as their collection on goods comes down to Rs. 26 from Rs. 28, the opportunity of taxing services would eventually lead to a net gain. The RNR must be decided accordingly

-‐ The price to the final consumer is Rs. 4 higher in the GST regime.

In spite of assuming the standard rate of Excise and VAT as 12.5% and 14.5% respectively, the goods for the final consumer gets costlier by Rs. 4. The lower rated goods in the present regime would be impacted to a greater degree. To add to the confusion, the Government is totally unclear about the RNR and the political debate is hinged upon it. A perusal of the National Institute of Public Finance and Policy report on RNR further highlights the lack of accurate data without which a just and exact

RNR cannot be determined. The cost of services for the ultimate consumer would definitely go up unless the benefit of erstwhile blocked credit exceeds the increase in tax rate and the industry passes on the benefit to the consumer. The benefits of GST would indeed trickle down to the ultimate consumer only if a correct RNR is agreed upon. Certain benefits of GST The brighter aspects of the proposed GST in its current shape are that all the players who are not ultimate consumers for a particular goods or service would benefit as the actual cost of goods in their hands would go down. Likewise, the exports made at any stage would be more competitive as they would be zero rated i.e. no output tax on export. The incentive to maintain the credit chain would create a larger tax base. Lowering of tax influence on business decisions, like setting up warehouses for avoiding a CST sale, would foster economic growth and more efficient use of the factors of production. GST may seem disadvantageous to consumer if the same supply chain is