Taxation in Latin America From words and data to policy action · PDF fileCosta Rica Chile...

21

Taxation in Latin America From words and data to policy action Angel Melguizo OECD Development Centre Wilson Center – Latin American Programme Washington DC, April 20 2017

Transcript of Taxation in Latin America From words and data to policy action · PDF fileCosta Rica Chile...

Taxation in Latin AmericaFrom words and datato policy action

Angel MelguizoOECD Development Centre

Wilson Center – Latin American ProgrammeWashington DC, April 20 2017

Open data for better policies

Revenue Statistics and Taxing Wages in LAC

• Detailed, internationally comparable data on tax revenues and labour tax laws (including a simulator by income and family composition) in 20+ Latin American and Caribbean (LAC) economies

• Based on OECD Revenue Statistics and OECD Taxing Wages methodologies, but adapted to Latin America

• Joint projects with the Economic Commission for Latin America and the Caribbean (ECLAC) , the Inter-American Centre for Tax Administrations (CIAT), and Inter-American Development Bank (IDB)

LAC countries continued their convergence

process towards OECD taxation levels, despite the

economic slowdown

Total tax revenues in LAC and OECD, 1990-2015(Percentage of GDP)

0

5

10

15

20

25

30

35

1990 91 92 93 94 1995 96 97 98 99 2000 01 02 03 04 2005 06 07 08 09 2010 11 12 13 14 2015

Difference B-A LAC (24) (A) OECD (35) (B)

Source: OECD/ECLAC/CIAT/IDB (2017), Revenue Statistics in Latin America and the Caribbean

Wide national variations exist across LAC

countries (‘Americas Latinas’)

Total tax revenues in LAC countries and OECD, 2015(Percentage of GDP)

0 5 10 15 20 25 30 35 40

OECD

LAC

Guatemala

Dominican Republic

Panama

Peru

El Salvador

Mexico

Paraguay

The Bahamas

Chile

Colombia

Nicaragua

Venezuela

Ecuador

Honduras

Costa Rica

Bolivia

Jamaica

Belize

Uruguay

Trinidad and Tobago

Barbados

Brazil

Argentina

Cuba

Source: OECD/ECLAC/CIAT/IDB (2017), Revenue Statistics in Latin America and the Caribbean

Tax structures continue to be based on indirect tax

receipts (VAT and other taxes on consumption)

Tax revenue composition in LAC and OECD, 2015(Percentage of GPD and total tax revenues)

1. Represents a group of 24 Latin American and Caribbean countries . Chile and Mexico are also part of the OECD (35) group.2. Represents the unweighted average for OECD member countries in the year 2014.Source: OECD/ECLAC/CIAT/IDB (2017), Revenue Statistics in Latin America and the Caribbean

6.2 p.p. (27%)

3.8 p.p.(16%)

0.8 p.p.(4%)

11.2 p.p.(49%)

0.9 p.p, (4%)

Taxes on income and profits Social security contributions Property

Taxes on goods and services Other taxes

11.5 p.p.(34%)

9.1 p.p.(27%)

1.9 p.p.(5%)

11.0 p.p. (32%)

0.7 p.p. (2%)

LAC (24)1 OECD (35)2

Despite recent increases, personal income tax

collection continues to be low (vs CIT)

Personal and Corporate income tax revenues in LAC and OECD, 2015(Percentage of GDP)

Note: the share on taxes on income and the share on taxes on profits may not add up to the total share on taxes on incomes and profits due to unallocable revenue. Only countries that could allocate 75% or more of revenue of taxes on incomes and profits into the sub categories taxes on income and taxes on profits are shown in the figure above.

Source: OECD/ECLAC/CIAT/IDB (2017), Revenue Statistics in Latin America and the Caribbean

0 3 6 9 12 15

LAC

OECD

The Bahamas

Bolivia

Paraguay

Guatemala

Dominican Republic

Colombia

Costa Rica

Chile

Panama

Peru

Honduras

Belize

Cuba

Brazil

El Salvador

Uruguay

Argentina

Mexico

Jamaica

Trinidad and Tobago

Barbados

PIT CIT

Fiscal revenues from non-renewable natural

resources are (too?) important sources of revenue

Fiscal revenues from non-renewable natural resources, 2015(in billions of dollars and percentage of GDP)

0 10 20 30 40 50 60 70

Jamaica

Suriname

Dominican Republic

Trinidad and Tobago

Peru

Chile

Bolivia

Ecuador

Colombia

Argentina

Venezuela

Brazil

Mexico6.1

As % of GDP

1.4

6.7

1.7

2.7

6.3

10.9

1.3

1.3

7.7

0.3

0.9

0.2

From data to policy action (I)

• Given the economic slowdown and weak commodity prices, a no-policy change scenario suggests that tax revenues will notincrease. Key to ensure the financing of education, infrastructure andsocial programmes.

• Tax reforms have to come, hand in hand, with improvements in their management. Latin American governments need to strive for more efficient, transparent and innovative services

• In focus – tax reform and labour markets

Source: IDB (2015), Sistema de Indicadores de Mercado Laboral y Seguridad Social (SIMS)

Informality is pervasive, also within the emerging

middle class. Could tax reform help?

Labour informality in Latin America(Percentage of workers contributing to pensions, 2013)

85%

64%

42%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

GTM HND PER PRY NIC BOL COL ECU SLV MEX PAN DOM ARG VEN BRA URY CRI CHL

Quintil 1 Promedio Q2 - Q4 Quintil 5 Promedio ALC Q1 Promedio ALC Q2-Q4 Promedio ALC Q5

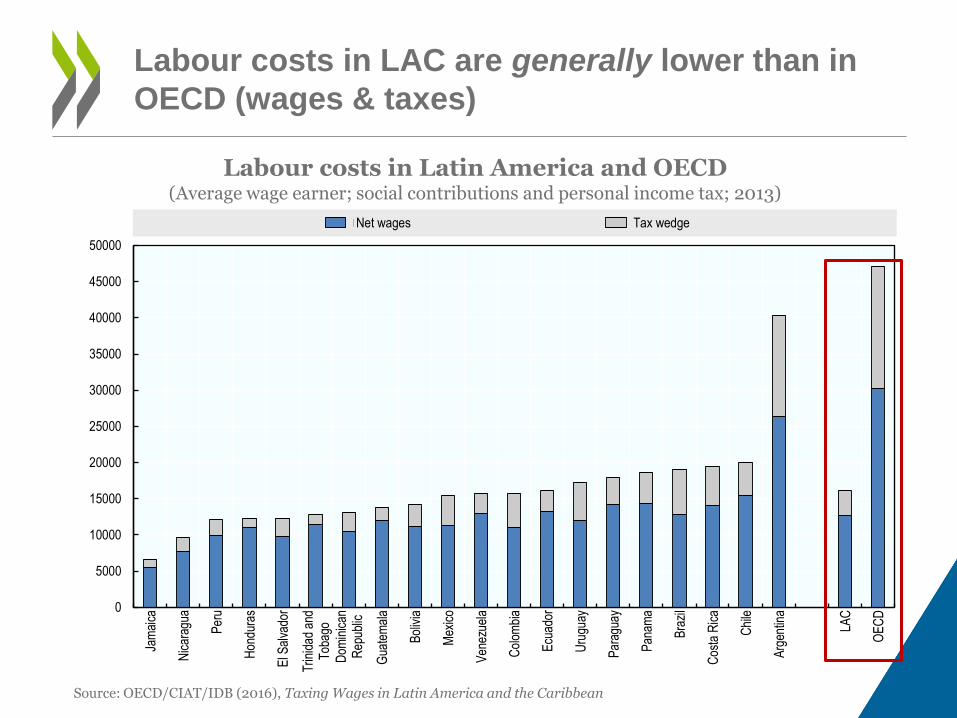

Labour costs in LAC are generally lower than in

OECD (wages & taxes)

Labour costs in Latin America and OECD(Average wage earner; social contributions and personal income tax; 2013)

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

Jam

aica

Nic

arag

ua

Per

u

Hon

dura

s

El S

alva

dor

Trin

idad

and

Tob

ago

Dom

inic

anR

epub

lic

Gua

tem

ala

Bol

ivia

Mex

ico

Ven

ezue

la

Col

ombi

a

Ecu

ador

Uru

guay

Par

agua

y

Pan

ama

Bra

zil

Cos

ta R

ica

Chi

le

Arg

entin

a

LAC

OE

CD

Net wages Tax wedge

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

Labour costs are relatively low due to low taxes on

wages (22% vs 36%)…

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

… explained by the personal income tax (average

formal worker is exempted)

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

Personal income tax only taxes the top deciles…

Single worker, no children Married couple, two children

Tax wedge by level of income in Latin America(Percentage of labour costs, 2013)

-5

0

5

10

15

20

25

30

1 2 3 4 5 6 7 8 9 10

Deciles de ingreso

Transferencias monetarias Impuesto a la renta CSS empleado CSS empleador

-10

-5

0

5

10

15

20

25

30

1 2 3 4 5 6 7 8 9 10

Deciles de ingreso

Transferencias monetarias Impuesto a la renta CSS empleado CSS empleador

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

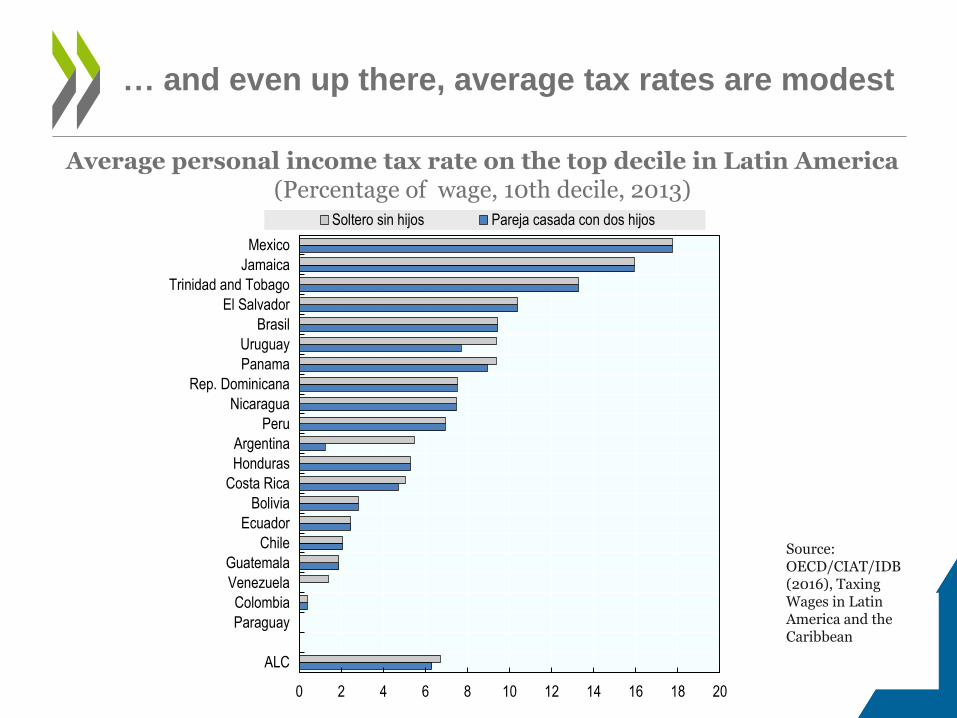

… and even up there, average tax rates are modest

Average personal income tax rate on the top decile in Latin America(Percentage of wage, 10th decile, 2013)

0 2 4 6 8 10 12 14 16 18 20

ALC

Paraguay

Colombia

Venezuela

Guatemala

Chile

Ecuador

Bolivia

Costa Rica

Honduras

Argentina

Peru

Nicaragua

Rep. Dominicana

Panama

Uruguay

Brasil

El Salvador

Trinidad and Tobago

Jamaica

Mexico

Soltero sin hijos Pareja casada con dos hijos

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

0% 5% 10% 15% 20% 25% 30%

OECD

LAC

Chile

Honduras

Trinidad y Tobago

Peru

Guatemala

Ecuador

Jamaica

Bolivia

Venezuela

El Salvador

Panamá

Paraguay

Dominican Rep

Nicaragua

Uruguay

Mexico

Costa Rica

Argentina

Colombia

Brazil

Employer contributions are alike in LAC and OECD

Employer social contributions in Latin America and OECD(Average wage earner; % labour costs; 2013)

What about those who are informal? Calculating

(tax) costs of formalisation

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Tasa de informalidad Costo teórico de formalización

Informality and theoretical tax costs of formalisation in LAC(Average LAC wage earner by income decile; % wages; 2013)

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

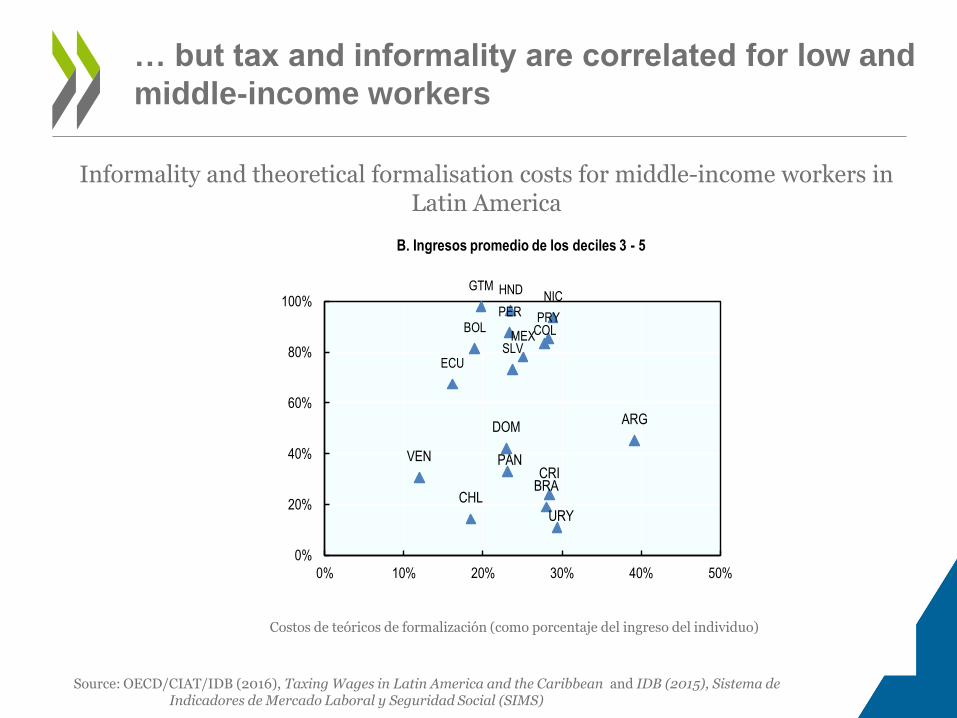

… but tax and informality are correlated for low and

middle-income workers

Costos de teóricos de formalización (como porcentaje del ingreso del individuo)

Informality and theoretical formalisation costs for middle-income workers in Latin America

URY

CHLBRACRI

VEN PAN

DOMARG

ECUSLV

MEXBOL COL

PRYPERNIC

HNDGTM

0%

20%

40%

60%

80%

100%

0% 10% 20% 30% 40% 50%

B. Ingresos promedio de los deciles 3 - 5

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean and IDB (2015), Sistema de Indicadores de Mercado Laboral y Seguridad Social (SIMS)

From data to policy action (and II)

• Boosting good jobs (protected & productive) should be a centralelement of the policy (also fiscal) agenda

• Personal income tax can be strengthen (revising minimumexempted) and made more progressive (tax deductions, rates?)

• Revision of non-wage labour costs – notably for low- and low-middleincome workers should be evaluated. Progressive subsidies on socialcontributions?

From data and words to policy action

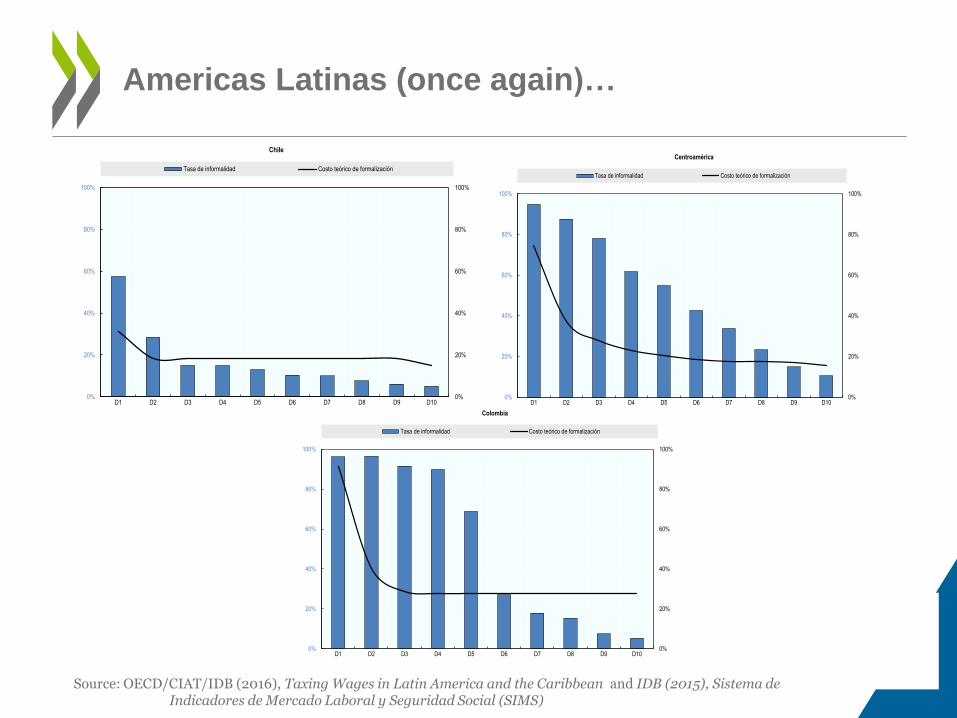

Americas Latinas (once again)…

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean and IDB (2015), Sistema de Indicadores de Mercado Laboral y Seguridad Social (SIMS)

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Chile

Tasa de informalidad Costo teórico de formalización

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Centroamérica

Tasa de informalidad Costo teórico de formalización

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Colombia

Tasa de informalidad Costo teórico de formalización