Taxation (Cross-border Trade) Bill · PDF fileIn my view the provisions of the Taxation...

171

Bill 128 57/1 Taxation (Cross-border Trade) Bill EXPLANATORY NOTES Explanatory notes to the Bill, prepared by the Treasury, are published separately as Bill 128—EN. EUROPEAN CONVENTION ON HUMAN RIGHTS The Chancellor of the Exchequer has made the following statement under section 19(1)(a) of the Human Rights Act 1998: In my view the provisions of the Taxation (Cross-border Trade) Bill are compatible with the Convention rights.

Transcript of Taxation (Cross-border Trade) Bill · PDF fileIn my view the provisions of the Taxation...

Bill 128 57/1

Taxation (Cross-border Trade) Bill

EXPLANATORY NOTES

Explanatory notes to the Bill, prepared by the Treasury, are published separately asBill 128—EN.

EUROPEAN CONVENTION ON HUMAN RIGHTS

The Chancellor of the Exchequer has made the following statement under section19(1)(a) of the Human Rights Act 1998:

In my view the provisions of the Taxation (Cross-border Trade) Bill are compatiblewith the Convention rights.

Bill 128 57/1

Taxation (Cross-border Trade) Bill

CONTENTS

PART 1

IMPORT DUTY

The charge to tax

1 Charge to import duty2 Chargeable goods

Incurring of liability to import duty

3 Obligation to declare goods for a Customs procedure on import4 When liability to import duty incurred5 Goods not presented to Customs or Customs declaration not made

Person liable to import duty

6 Person liable to import duty

Amount of import duty: the customs tariff, preferences, safeguarding etc

7 Amount of duty: introduction8 The customs tariff9 Preferential rates: arrangements with countries or territories outside UK

10 Preferential rates given unilaterally11 Quotas12 Tariff suspension13 Dumping of goods, foreign subsidies and increases in imports14 Increases in imports or changes in price of agricultural goods15 International disputes etc

Amount of import duty: supplementary

16 Value of chargeable goods17 Place of origin of chargeable goods18 Currency

Reliefs

19 Reliefs

Taxation (Cross-border Trade) Billii

Administration etc

20 Notification and payment of import duty, etc21 Customs agents22 Authorised economic operators23 Approvals and authorisations granted under regulations24 Rulings as to application of customs tariff or place of origin

Supplementary

25 Disclosure of information26 Co-operation with other customs services27 Fees for exercise of functions in connection with import duty28 Requirement to have regard to international obligations29 Consequential amendments30 General provision for the purposes of import duty

UK's customs union

31 Territories forming part of a customs union with UK

Regulations etc

32 Regulations etc

Interpretation etc

33 Meaning of “domestic goods”34 Presentation of goods to Customs on import or export35 Exports made in accordance with applicable export provisions36 Outward processing procedure37 Minor definitions38 Table of definitions

PART 2

EXPORT DUTY

39 Charge to export duty40 Regulations under section 39: supplementary

PART 3

VALUE ADDED TAX

41 Abolition of acquisition VAT and extension of import VAT42 EU law relating to VAT43 Other VAT amendments connected with withdrawal from EU

PART 4

EXCISE DUTIES

44 Excise duties: postal packets sent from overseas45 General regulation making power for excise duty purposes etc

Taxation (Cross-border Trade) Bill iii

46 Exercise of information powers in connection with excise duty47 EU law relating to excise duty48 Regulations under ss. 44 to 4749 Sections 44 to 48: interpretation50 Excise duty amendments connected with withdrawal from EU

PART 5

OTHER PROVISION CONNECTED WITH WITHDRAWAL FROM EU

51 Power to make provision in relation to VAT or duties of customs or excise52 Subordinate legislation relating to VAT or duties of customs or excise53 Meaning of “excise duty”

PART 6

FINAL PROVISIONS

54 Consequential and transitional provision55 Commencement56 Short title

Schedule 1 — Customs declarationsSchedule 2 — Special Customs procedures

Part 1 — Entitlement to declare goods for special customs proceduresPart 2 — Storage procedurePart 3 — Transit procedurePart 4 — Inward processing procedurePart 5 — Authorised use procedurePart 6 — Temporary admission procedurePart 7 — Supplementary provisions

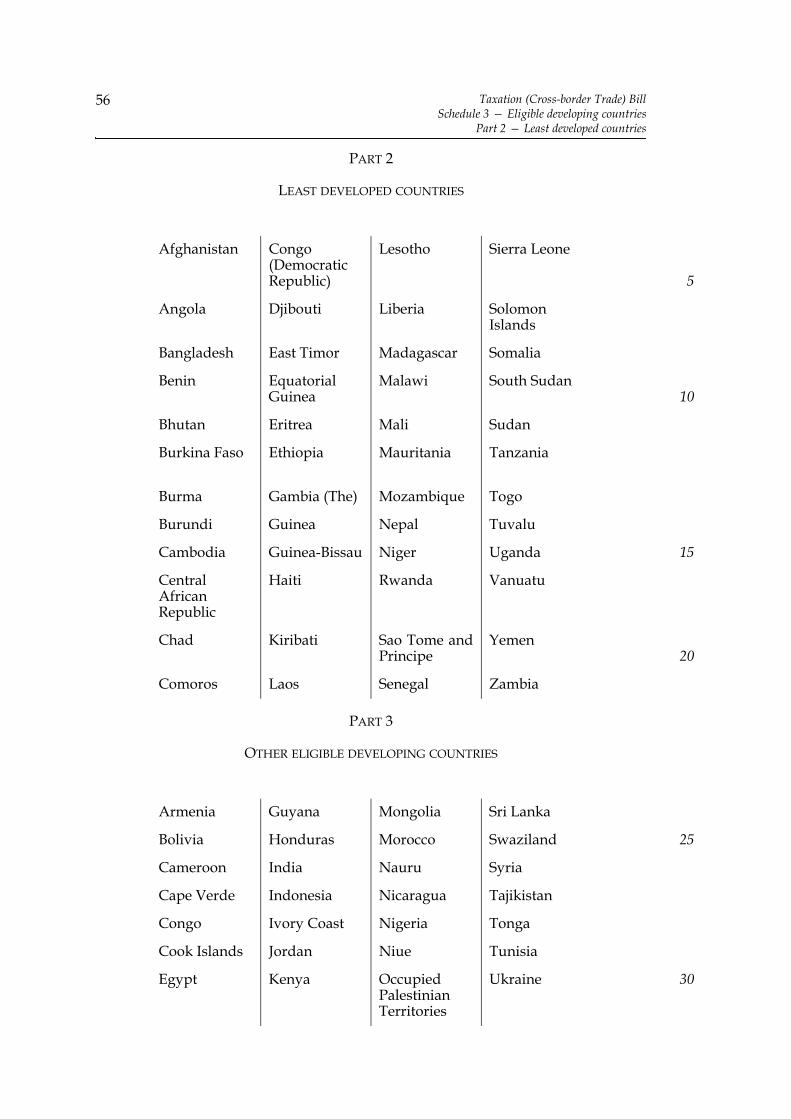

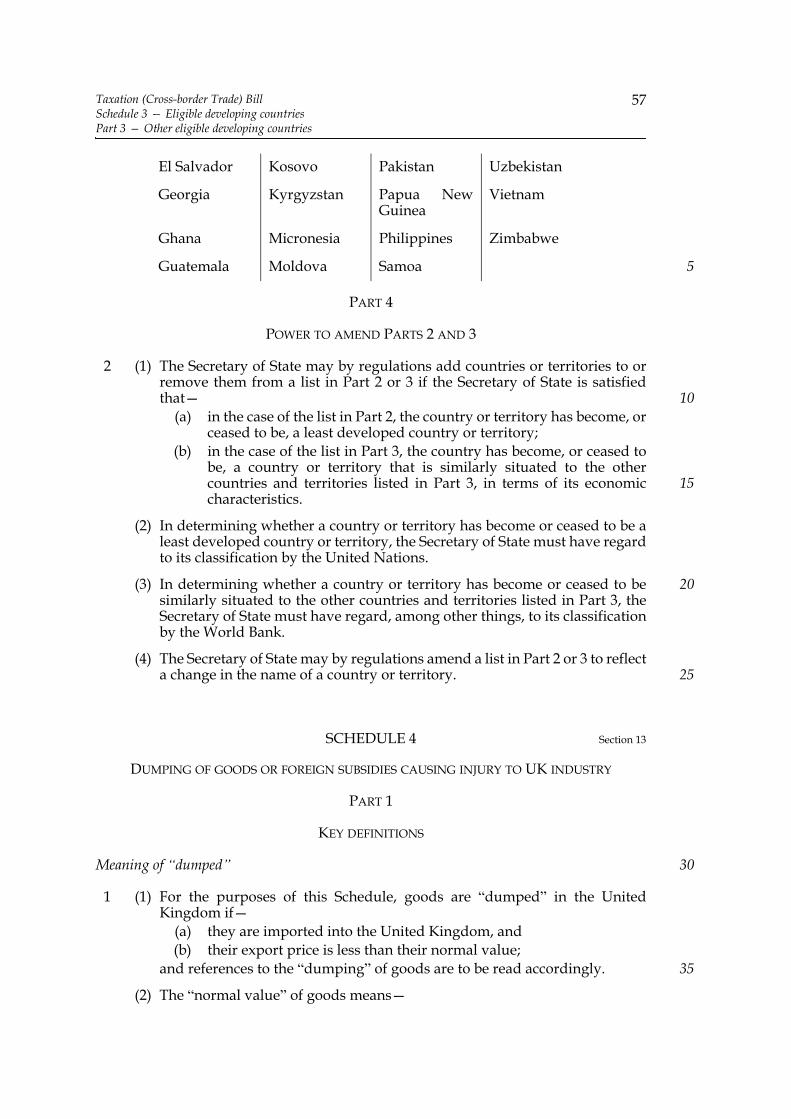

Schedule 3 — Eligible developing countriesPart 1 — IntroductionPart 2 — Least developed countriesPart 3 — Other eligible developing countriesPart 4 — Power to amend Parts 2 and 3

Schedule 4 — Dumping of goods or foreign subsidies causing injury to UKindustry

Part 1 — Key definitionsPart 2 — Dumping and subsidisation investigationsPart 3 — Provisional remedy: requiring a guaranteePart 4 — Definitive remedies: anti-dumping amount or countervailing

amountPart 5 — UndertakingsPart 6 — Supplementary

Schedule 5 — Increase in imports causing serious injury to UK producersPart 1 — Key definitionsPart 2 — Safeguarding investigationsPart 3 — Provisional remedy: provisional safeguarding amountPart 4 — Definitive remedies: definitive safeguarding amount & tariff

rate quotas

Taxation (Cross-border Trade) Billiv

Part 5 — SupplementarySchedule 6 — Import duty: notification of liability, payment etcSchedule 7 — Import duty: consequential amendments

Part 1 — Replacement of EU customs dutiesPart 2 — Amendments of CEMA 1979Part 3 — Amendments of other enactments

Schedule 8 — VAT amendments connected with withdrawal from EUPart 1 — Amendments of Value Added Tax Act 1994Part 2 — Amendments of other enactments

Schedule 9 — Excise duty amendments connected with withdrawal from EU

Bill 128 57/1

Taxation (Cross-border Trade) BillPart 1 — Import duty

1

A

B I L LTO

Impose and regulate a duty of customs by reference to the importation ofgoods into the United Kingdom; to confer a power to impose and regulate aduty of customs by reference to the export of goods from the United Kingdom;to make other provision in relation to any duty of customs in connection withthe withdrawal of the United Kingdom from the EU; to amend the lawrelating to value added tax, and the law relating to any excise duty on goods,in connection with that withdrawal; and for connected purposes.

Most Gracious Sovereign

E, Your Majesty’s most dutiful and loyal subjects, the Commons of the UnitedKingdom in Parliament assembled, towards raising the necessary supplies to

defray Your Majesty’s public expenses, and making an addition to the publicrevenue, have freely and voluntarily resolved to give and to grant unto Your Majestythe several duties hereinafter mentioned; and do therefore most humbly beseechYour Majesty that it may be enacted, and be it enacted by the Queen’s most ExcellentMajesty, by and with the advice and consent of the Lords Spiritual and Temporal, andCommons, in this present Parliament assembled, and by the authority of the same, asfollows:—

PART 1

IMPORT DUTY

The charge to tax

1 Charge to import duty

A duty of customs (to be known as “import duty”) is charged in accordancewith provision made by or under this Part by reference to the importation ofchargeable goods into the United Kingdom.

W

5

Taxation (Cross-border Trade) BillPart 1 — Import duty

2

2 Chargeable goods

Goods are “chargeable goods” for the purposes of this Part unless they aredomestic goods.

Incurring of liability to import duty

3 Obligation to declare goods for a Customs procedure on import

(1) Chargeable goods which are presented to Customs on import must be declaredfor a Customs procedure by the making of a Customs declaration.

(2) It is the Customs procedure for which the goods are declared that determineswhen a liability to import duty is incurred.

(3) The Customs procedures for which chargeable goods may be declared are asfollows—

(a) a procedure under which the goods are released for free circulation inthe United Kingdom (referred to in this Part as “the free-circulationprocedure”), or

(b) a special Customs procedure.

(4) In this Part “special Customs procedure” means—(a) a storage procedure,(b) a transit procedure,(c) an inward processing procedure, or(d) an authorised use procedure or temporary admission procedure.

(5) Schedule 1 makes provision about—(a) the period within which Customs declarations are required to be made

(and associated matters),(b) the making, amendment or withdrawal of Customs declarations, (c) the acceptance of Customs declarations by HMRC,(d) the verification of Customs declarations by HMRC officers, and(e) the release of goods to, and the discharge of goods from, Customs

procedures.

(6) Schedule 2 makes further provision about special Customs procedures.

4 When liability to import duty incurred

(1) If—(a) chargeable goods are declared for the free-circulation procedure, and(b) HMRC accept the declaration,

a liability to import duty is incurred at the time of the acceptance.

(2) If chargeable goods are declared for—(a) a storage procedure,(b) a transit procedure, or(c) an inward processing procedure,

the general rule is that a liability to import duty is not incurred by reference tothe importation of the goods.

(3) This rule is subject to the following two exceptions—

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

3

(a) if there is no entitlement to make the Customs declaration concerned, aliability to import duty is incurred at the time the (purported)declaration is made, and

(b) if there is a breach by any person of any requirement relating to theprocedure, a liability to import duty is incurred at the time at which thebreach first occurs.

(4) In the case of goods declared for an authorised use procedure or temporaryadmission procedure—

(a) a liability to import duty is incurred at the time the declaration isaccepted by HMRC,

(b) if there is an entitlement to make the declaration for the procedure, therate of import duty is lower than the normal rate (see section 19(4)),

(c) if there is no such entitlement, the liability is at the normal rate, and(d) if there is a breach of a requirement relating to the procedure, a further

liability to import duty arises at the time of the breach at the normal ratereduced to take account of the amount of any earlier liability.

(5) In the case of goods declared for a temporary admission procedure, see alsosection 19(5).

(6) In this section any reference to the breach of a requirement relating to a specialCustoms procedure is to—

(a) a breach, occurring while the procedure has effect, of the terms of thedeclaration for the procedure or of any other requirement imposed inrelation to the procedure by or under Schedule 2, or

(b) a breach, occurring at any time after the declaration was made, of anyother requirement imposed by an HMRC officer in relation to the goodsfor which the declaration was made.

(7) In this section “the normal rate” means the rate that, at the time of thedeclaration or breach (as the case may be), would be applicable if section 19(4)were ignored.

5 Goods not presented to Customs or Customs declaration not made

(1) If chargeable goods—(a) are imported into the United Kingdom, and(b) are not presented to Customs on import (if so required),

the goods are liable to forfeiture (as to which, see Part 11 of CEMA 1979) at thetime of importation.

(2) If goods are liable to forfeiture as a result of—(a) subsection (1), or(b) paragraph 1(5) or 3(4) of Schedule 1 (no Customs declaration made),

a liability to import duty is incurred at the time at which the goods becomeliable to forfeiture.

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

4

Person liable to import duty

6 Person liable to import duty

(1) If a Customs declaration is made in respect of any chargeable goods, the personin whose name the declaration is made is the person liable to import duty inrespect of the goods.

(2) If a liability to import duty is incurred as a result of section 5 in respect of anychargeable goods, any person who is in possession or control of the goodswhen they enter the United Kingdom is liable to import duty in respect of thegoods.

(3) In addition to any person liable as a result of subsection (1) or (2), each of thefollowing persons is liable to import duty—

(a) a person on whose behalf a Customs declaration is made,(b) a person liable as a result of provision made by section 21(6) (Customs

agents),(c) a person liable as a result of provision made under paragraph 21 of

Schedule 2 (special Customs procedures), and(d) a person otherwise involved in a breach of a relevant Customs

obligation.

(4) For this purpose a person is otherwise involved in a breach of a relevantCustoms obligation if—

(a) the person provides false information in connection with a chargeableCustoms declaration and the person knew, or ought reasonably to haveknown, that the information was false,

(b) the person (“A”) acted (whether as a Customs agent or otherwise) onbehalf of another person who breached a relevant Customs obligationand A knew, or ought reasonably to have known, of the breach by thatother person,

(c) the person participated in, or was otherwise involved in, a breach of arelevant Customs obligation and knew, or ought reasonably to haveknown, of the breach, or

(d) the person possesses or controls the goods at a time when there hasbeen a breach of a relevant Customs obligation and the person knew, orought reasonably to have known, of the breach.

(5) For the purposes of subsection (4)(a) a person (“P”) provides “false informationin connection with a chargeable Customs declaration” if—

(a) P provides information to another person to enable that other person tomake a Customs declaration,

(b) that other person makes the declaration, and(c) the information provided by P is false.

(6) For the purposes of subsection (4) there is “a breach of a relevant Customsobligation” if—

(a) there is a breach of a requirement imposed on any person that resultsin a liability to import duty, or

(b) circumstances otherwise arise that result in a liability to import duty,and, in a case within paragraph (b) of this subsection, references to knowledgeof the breach are to knowledge of those circumstances.

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 1 — Import duty

5

(7) If two or more persons are liable to import duty in any case, those persons arejointly and severally liable to import duty in that case.

Amount of import duty: the customs tariff, preferences, safeguarding etc

7 Amount of duty: introduction

(1) The amount of import duty applicable to any goods is to be determined inaccordance with the customs tariff (see section 8), as amended or adjusted byprovision made under any of the following sections—

(a) section 9 (preferential rates: arrangements with countries or territoriesoutside UK),

(b) section 10 (preferential rates given unilaterally),(c) section 11 (quotas),(d) section 12 (tariff suspension),(e) section 13 (dumping of goods, foreign subsidies and increases in

imports),(f) section 14 (increases in imports or changes in price of agricultural

goods), and(g) section 15 (international disputes etc).

(2) See also—(a) sections 16 to 18 (which deal with the valuation of goods, their place of

origin and cases where amounts are expressed in a foreign currency),and

(b) section 19 (which enables provision to be made for full or partial relieffrom import duty).

8 The customs tariff

(1) The Treasury must make regulations establishing, and maintaining in force, asystem which—

(a) classifies goods according to their nature, origin or any other factor,(b) gives codes to the goods as so classified,(c) specifies the rate of import duty applicable to goods falling within

those codes (whether by a formula or otherwise), and(d) contains rules for determining the amount of import duty applicable to

those goods.

(2) This system is referred to in this Part as the customs tariff.

(3) The customs tariff may provide for the amount of any import duty applicableto any goods falling within any code to be determined by reference to either orboth of the following—

(a) the value of the goods, and(b) the weight or volume of the goods or any other measure of their

quantity or size.

(4) The customs tariff may include provision as to the meaning of any expressionused in it.

(5) In considering the rate of import duty that ought to apply to any goods in astandard case, the Treasury must have regard to—

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

6

(a) the interests of consumers in the United Kingdom,(b) the desirability of maintaining and promoting the external trade of the

United Kingdom,(c) the desirability of maintaining and promoting productivity in the

United Kingdom, and(d) the extent to which the goods concerned are subject to competition.

(6) In considering the rate of import duty that ought to apply to any goods in astandard case, the Treasury must also have regard to any recommendationabout the rate made to them by the Secretary of State.

(7) In considering what recommendation to make, the Secretary of State must haveregard to the matters set out in subsection (5)(a) to (d).

(8) In this section “a standard case” means a case other than one to which any ofsections 9 to 15 or 19(4) apply (preferential rates, quotas, tariff suspension,safeguarding, etc).

9 Preferential rates: arrangements with countries or territories outside UK

(1) If—(a) Her Majesty’s government in the United Kingdom makes

arrangements with the government of a country or territory outside theUnited Kingdom, and

(b) the arrangements contain provision for the rate of import dutyapplicable to goods, or any description of goods, originating from thecountry or territory to be lower than the applicable rate in the customstariff in its standard form,

the Treasury may make regulations to give effect to the provision made by thearrangements (whether by amending the customs tariff or otherwise).

(2) The reference here to the customs tariff in its standard form is to the tariff as ithas effect without regard to any provision made under any of sections 10 to 15or section 19(4).

(3) The power of the Treasury to make regulations under this section is exercisableonly on the recommendation of the Secretary of State.

10 Preferential rates given unilaterally

(1) The Secretary of State may by regulations establish a scheme (“a tradepreference scheme”) under which the rate of import duty applicable to goods,or any description of goods, originating from an eligible developing country islower than the applicable rate in the customs tariff in its standard form.

(2) A trade preference scheme may—(a) apply to one or more eligible developing countries,(b) provide for the application of the lower rates to be subject to the

meeting of specified conditions, and(c) make provision about the variation, suspension and withdrawal of the

application of the lower rates.

(3) If a trade preference scheme is established under subsection (1), regulationsunder subsection (1)—

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

7

(a) must provide for a nil rate of import duty to be applicable to all goodsoriginating from a least developed country, except arms andammunition, and

(b) may make provision about the suspension and withdrawal of theapplication of the nil rate.

(4) In subsection (3)—(a) “arms and ammunition” has the meaning specified in regulations made

by the Secretary of State, and(b) “suspension” and “withdrawal” may include the application of another

rate that is lower than the applicable rate in the customs tariff in itsstandard form.

(5) The references in this section to the customs tariff in its standard form are tothe tariff as it has effect without regard to any provision made under any ofsection 9, sections 11 to 15 or section 19(4).

(6) In Schedule 3—(a) Part 1 defines “eligible developing country” and “least developed

country” for the purposes of this section,(b) Parts 2 and 3 contain lists for the purpose of those definitions, and(c) Part 4 confers power to amend those lists.

11 Quotas

(1) Regulations may make provision for determining the amount of import dutyapplicable to any goods that are subject to a quota.

(2) Goods are subject to a quota for the purposes of this section if—(a) Her Majesty’s government in the United Kingdom makes

arrangements with the government of a country or territory outside theUnited Kingdom and the arrangements contain provision for the goodsconcerned to be subject to a quota, or

(b) the Treasury otherwise consider that it is appropriate for the goodsconcerned to be subject to a quota.

(3) Regulations may make any provision that the person making them considersappropriate for the purposes of this section, including (for example)—

(a) provision specifying the factors by reference to which a quota is to bedetermined,

(b) provision imposing conditions subject to which a quota has effect,(c) provision for a quota in respect of specified goods to be subject to a

licensing or allocation system (see also subsection (4)), and(d) any other provision in relation to the administration of a quota.

(4) Regulations made under subsection (3) which make provision for a quota inrespect of specified goods to be subject to a licensing or allocation system mayinclude—

(a) provision authorising any public body to grant licences or determine asystem for allocating the quotas,

(b) provision specifying the cases in which a person is eligible to make useof a quota,

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

8

(c) provision specifying the conditions subject to which any person maymake use of a quota (including provision for the giving of a guaranteeof a specified amount),

(d) provision authorising the conditions to be imposed by a licence or otherdocument,

(e) provision requiring the payment of fees by any person in connectionwith any application for a licence or an allocation, and

(f) provision generally in relation to the administration of the licensing orallocation system.

(5) Any fees payable as a result of provision made under subsection (4)(e) must bepaid into the Consolidated Fund.

(6) The power to make regulations under this section providing for a quota inrespect of specified goods to be subject to a licensing or allocation system isexercisable by the Secretary of State.

(7) The power to make regulations under this section containing any otherprovision is exercisable by the Treasury; and, in considering what provision toinclude in the regulations, the Treasury must have regard to anyrecommendation made to them by the Secretary of State.

12 Tariff suspension

(1) The Treasury may by regulations make provision securing that, for a specifiedperiod, the rate of import duty applicable to specified goods is to be lower thanthe applicable rate in the customs tariff in its standard form.

(2) The regulations must provide that (subject to any exceptions) the Secretary ofState is obliged—

(a) to consider a request made by any person for goods to be specifiedgoods for the purposes of the regulations, and

(b) to make recommendations to the Treasury about the request.

(3) The regulations may—(a) make provision for extending the specified period (including by means

of a notice),(b) impose conditions on the application of the lower rate, and(c) make further provision about requests made to the Secretary of State

(including provision about the form and contents of a request and themanner, and date by which, a request is to be made).

(4) In this section the reference to the customs tariff in its standard form is to thetariff as it has effect without regard to any provision made under any ofsections 9 to 11, sections 13 to 15 or section 19(4).

(5) In considering what provision to include in any regulations under this section,the Treasury must have regard to any recommendation made to them by theSecretary of State.

13 Dumping of goods, foreign subsidies and increases in imports

(1) Functions relating to import duty are conferred on the Trade RemediesAuthority (“the TRA”) by—

(a) Schedule 4 (dumping and foreign subsidies causing injury to UKindustry), and

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 1 — Import duty

9

(b) Schedule 5 (increased imports causing serious injury to UK producers).

(2) If the Secretary of State accepts a recommendation by the TRA under provisionmade by or under Schedule 4 or 5 that an additional amount of import dutyshould be applicable to goods, the Secretary of State must by public noticemake provision giving effect to the recommendation.

(3) If the Secretary of State accepts a recommendation by the TRA under provisionmade by or under Schedule 5 that goods should be subject to a tariff rate quota,the Secretary of State must by public notice make provision for determining theamount of import duty applicable to the goods in order to give effect to therecommendation.

(4) If the Secretary of State accepts a recommendation by the TRA under provisionmade by or under Schedule 4 or 5 that—

(a) the application of an additional amount of import duty to goods underthis section should be suspended, varied or revoked, or

(b) the application of a quota to which goods are subject under this sectionshould be suspended, varied or revoked,

the Secretary of State must by public notice make provision giving effect to therecommendation.

(5) The Secretary of State may make regulations containing any provision that theSecretary of State considers appropriate for the purposes of subsections (3) and(4)(b); and section 11(3)(a) to (d), (4) and (5) apply to regulations under thissubsection as they apply to regulations under section 11(3).

14 Increases in imports or changes in price of agricultural goods

(1) The Treasury may by regulations make provision for an additional amount ofimport duty to be applicable to specified agricultural goods, or a specifieddescription of agricultural goods, if—

(a) the volume of imports of the specified goods, or goods of the specifieddescription, into the United Kingdom during a specified periodexceeds a specified trigger level, or

(b) the import price of the goods has fallen below a specified trigger price.

(2) The regulations may (among other things) make provision—(a) limiting the period for which an additional amount of import duty is

applicable;(b) for the suspension of the application of an additional amount of import

duty;(c) requiring the giving of a guarantee in respect of an additional amount

of import duty which is potentially applicable to goods, where therepresentative price for the goods has fallen below the specified triggerprice and the import price of the goods is higher than thatrepresentative price;

(d) specifying the representative price for goods or a description of goods,(whether by a formula or otherwise) and providing for representativeprices to be adjusted (whether by a formula or otherwise).

(3) The power of the Treasury to make regulations under this section is exercisableonly on the recommendation of the Secretary of State.

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 1 — Import duty

10

15 International disputes etc

(1) If—(a) a dispute or other issue has arisen between Her Majesty’s government

in the United Kingdom and the government of a country or territory,and

(b) Her Majesty’s government in the United Kingdom is authorised underinternational law to deal with the issue by varying the amount ofimport duty in the case of goods, or a description of goods, originatingfrom the country or territory,

the Secretary of State may make regulations varying the amount of importduty applicable to the goods or the description of goods.

(2) In exercising the power to make the regulations in the case of a disputeaffecting any goods, the Secretary of State must secure that the amount ofimport duty payable in that case takes account of any additional amount ofimport duty which—

(a) is payable under section 13 as a result of the goods being subsidised, or (b) would have been so payable had an undertaking not been accepted in

respect of the goods.

Amount of import duty: supplementary

16 Value of chargeable goods

(1) This section makes provision for determining the value of chargeable goods forthe purposes of this Part.

(2) The general rule is that the value of the goods is the transaction value of thegoods when sold for export to the United Kingdom.

(3) For this purpose “the transaction value” means the total amount of theconsideration—

(a) payable for the goods, or(b) payable in connection with the importation of the goods into the United

Kingdom,subject to the inclusion or exclusion of matters specified in regulations madeby the Treasury.

(4) The regulations may make provision for treating a matter to be of a specifiedamount or value.

(5) Regulations made by the Treasury may make provision for the value of goodsfor the purposes of this Part to be a value other than the transaction value.

(6) The following are examples of the kind of provision that may be made by theregulations—

(a) provision dealing with transactions between persons who are relatedto, or connected with, each other in a specified way, and

(b) provision dealing with cases where a transaction value cannot, orcannot readily, be determined.

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

11

17 Place of origin of chargeable goods

(1) This section makes provision for determining the place of origin of chargeablegoods for the purposes of this Part.

(2) Goods are to be regarded as originating from a country or territory if they arewholly obtained in the country or territory.

(3) If goods are obtained in two or more countries or territories, the goods are tobe regarded as originating from the last country or territory in whichsubstantial processing of them has taken place that is economically justified.

(4) Processing of any goods is to be regarded as substantial only if—(a) it results in the manufacture of a new product or represents an

important stage of manufacture, and(b) it takes place in an undertaking equipped for the purpose.

(5) It is for the person making a Customs declaration to show that goods originatefrom a particular country or territory.

(6) The Treasury may by regulations make provision for the purposes of thissection, including (for example) provision—

(a) for determining what constitutes, or does not constitute, processingthat is economically justified,

(b) for determining what constitutes, or does not constitute, an importantstage of manufacture,

(c) as to cases in which goods are, or are not, to be regarded as originatingfrom a country or territory, and

(d) as to the evidence which is to be required, or is to be sufficient, for thepurpose of showing that goods originate from a particular country orterritory.

(7) In relation to any case where the applicable rate of import duty is determinedunder section 9 or 10 (preferences), the provision that may be made byregulations under subsection (6) includes—

(a) provision for the place of origin of the goods to be determined inaccordance with the regulations,

(b) provision for regarding goods exported by or on behalf of personsapproved in accordance with the regulations as originating from acountry or territory or for regarding only goods exported by or onbehalf of approved persons as originating from a country or territory,

(c) provision for different categories of approved persons,(d) provision requiring the Treasury to publish a list of persons who are for

the time being approved persons and information about the category ofapproval, and

(e) other provision about approved persons.

(8) The power to make regulations under this section is exercisable only on therecommendation of the Secretary of State.

18 Currency

(1) The value of chargeable goods for the purposes of this Part must be calculatedand expressed in sterling.

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

12

(2) If an amount that is relevant for the purpose of calculating the value of goodsfor the purposes of this Part is expressed in a currency other than sterling, theamount must be converted into its sterling equivalent.

(3) The conversion must be made in accordance with provision contained in apublic notice given by HMRC Commissioners.

(4) The public notice may make provision—(a) specifying the exchange rate that must be used for the purposes of this

section,(b) for the conversion to be made by reference to an exchange rate (or rates)

applicable at any time (including a time earlier than that at which animportation took place) or by reference to the average exchange rate fora specified period,

(c) for the exchange rate determined in accordance with the notice to applyto transactions or other events taking place in a specified period,

(d) for adjusting the applicable exchange rate if the value of sterling againstthe currency concerned has increased or decreased by more than aspecified percentage, and

(e) for any conversion to be rounded up or down.

Reliefs

19 Reliefs

(1) The Treasury may by regulations make provision for full or partial relief froma liability to import duty.

(2) The regulations may provide for the relief to be given by reference to anyfactor, for example—

(a) the nature or origin of goods or anything else by reference to whichgoods are classified in the customs tariff,

(b) anything in the customs tariff by reference to which the amount ofimport duty applicable to goods is determined,

(c) the purposes for which goods are imported,(d) the person by whom, or for whose benefit, goods are imported, and(e) the circumstances in which goods are imported.

(3) The regulations may provide for a relief to be conditional on (among otherthings) the export of goods in accordance with the applicable exportprovisions.

(4) In the case of goods that are declared for an authorised use procedure ortemporary admission procedure, the Treasury—

(a) must exercise the power to make regulations under this section so as tosecure that the rate of import duty applicable to the goods is lower thanthe applicable rate in the customs tariff in its standard form, and

(b) may secure that result by amending the customs tariff.

(5) If the regulations provide for partial relief in respect of goods declared for atemporary admission procedure, the regulations must secure that—

(a) the partial relief operates by way of additional charges to import dutyby reference to any period during which the procedure has effect, and

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

13

(b) the total of the additional charges does not exceed the amount of theliability in the absence of the partial relief.

(6) If the regulations provide for partial relief in any other case, the regulationsmay make provision corresponding to that mentioned in subsection (5)(a) and(b).

(7) The reference in this section to the customs tariff in its standard form is to thetariff as it has effect without regard to any provision made under any ofsections 9 to 15 (preferential rates, quotas, tariff suspension, safeguarding, etc).

Administration etc

20 Notification and payment of import duty, etc

Schedule 6 makes provision for—(a) the notification of any liability to pay import duty,(b) the payment of import duty,(c) the giving of guarantees in respect of any liability to pay import duty,(d) the repayment of import duty,(e) the remission of import duty, and(f) the recovery of import duty.

21 Customs agents

(1) A person (“the principal”) may appoint any other person (a “Customs agent”)to act on the principal’s behalf for the purposes of this Part, and—

(a) the agent may make Customs declarations in the name of the principal(and in that case the agent acts as a “direct agent”), or

(b) the agent may make Customs declarations in the agent’s own name(and in that case the agent acts as an “indirect agent”).

(2) The appointment of a person as a Customs agent, and the withdrawal of anappointment of a person as a Customs agent, must be disclosed to HMRC inaccordance with regulations made by HMRC Commissioners.

(3) The effect of an appointment of a person as a Customs agent is that anythingdone under, or otherwise for the purposes of, this Part by, or in relation to, theagent is regarded as done under, or otherwise for the purposes of, this Part by,or in relation to, the principal (and not by the agent).

(4) There is an exception to this rule if a Customs agent acts as an indirect agent(and see also section 37(8)(b)).

(5) In that case, the indirect agent is liable to import duty in accordance withsection 6(1) (and the principal is also liable to import duty in accordance withsection 6(3)(a)).

(6) If a Customs agent acts as a direct agent, the agent is also liable to import dutyif—

(a) the agent acts at time when the appointment has not been disclosed toHMRC as mentioned in subsection (2),

(b) the agent acts at a time when the appointment of the person as aCustoms agent has been withdrawn,

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

14

(c) the agent otherwise purports to act on behalf of the principal when theagent has no authority to do so, or

(d) a liability to import duty is incurred by reference to the importation ofgoods declared for a Customs declaration and the declaration was notmade in accordance with regulations under paragraph 9 of Schedule 1(simplified Customs declarations).

(7) HMRC Commissioners may by regulations make further provision aboutCustoms agents for the purposes of import duty.

(8) Each of the following is an example of the kind of provision that may be madeby the regulations—

(a) provision requiring persons to be eligible for appointment as Customsagents only if an HMRC officer has approved the appointment, and

(b) provision specifying the criteria for approving the appointment(including provision for the criteria to be specified in a public noticegiven by HMRC Commissioners).

22 Authorised economic operators

(1) HMRC Commissioners may by regulations make provision—(a) disapplying or simplifying specified requirements made by or under

this Part in relation to things required or authorised to be done byauthorised economic operators, or

(b) requiring HMRC to have regard to the status of a person as anauthorised economic operator when considering whether or not, orhow, to exercise any power or other function for the purposes of thisPart.

(2) For this purpose “authorised economic operators” means persons authorisedin accordance with provision made by or under the regulations.

(3) Regulations under this section may (for example)—(a) specify the criteria to be applied in determining whether or not any

person should be an authorised economic operator,(b) specify those criteria by reference to professional standards of

competence (as set by any specified person) or by reference to anythingelse (including the judgment of any person as to suitability),

(c) make provision for a person’s status as an authorised economicoperator to be subject to compliance with conditions specified in theregulations or in the authorisation, and

(d) establish different classes of authorised economic operator.

23 Approvals and authorisations granted under regulations

(1) This section applies in relation to approvals granted to any person underregulations made under this Part (whether in respect of premises or anythingelse) unless the regulations in question make alternative provision.

(2) In this section references to an approval include an authorisation.

(3) The regulations under which an approval is granted may—(a) require an application for approval to be made in a specified form and

in a specified manner and to contain specified information,(b) specify cases in which an application for approval may not be made,

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 1 — Import duty

15

(c) require HMRC to consider, within a specified period, whether or not anapplication, or purported application, for approval is, as a result ofprovision made by paragraph (a) or (b), one that falls to be determined,

(d) confer on the applicant a right of appeal to an appeal tribunal in a casewhere HMRC have failed to comply with paragraph (c),

(e) require HMRC to notify a person making a purported application forapproval that, as a result of provision made by paragraph (a) or (b), thepurported application does not fall to be determined, and

(f) make further provision about the notification.

(4) The provision that may be made under subsection (3)(d) includes—(a) provision for an appeal to be brought only if a period specified in the

regulations has ended, and(b) provision limiting the power of an appeal tribunal to the power to

direct HMRC, in a case where it is satisfied that HMRC have actedunreasonably, to consider the application as mentioned in subsection(3)(c) within such further period as is specified by the tribunal.

(5) An approval granted by HMRC is treated as if it had never been granted if—(a) the (purported) application for approval was deficient in some respect,(b) the applicant knew, or ought reasonably to have known, of the

deficiency,(c) HMRC consider that the approval would not have been granted if the

deficiency was known at the time it was granted by the person grantingit, and

(d) HMRC give a notice to the applicant under this subsection notifying theapplicant of the effect of this subsection.

(6) Regulations made by HMRC Commissioners may make any provision thatthey consider appropriate for the purposes of subsection (5), includingprovision specifying cases in which the approval is to continue to be treated asstill in force.

(7) An approval may be amended, suspended or revoked in cases specified in theregulations under which it was granted.

(8) The amendment, suspension or revocation of an approval takes effect from thedate specified in a notice given by HMRC to the person approved (and,accordingly, does not affect anything already done by any person before thatdate in reliance on the approval).

(9) HMRC—(a) may not specify a date before the notice is given unless HMRC and the

person both agree that such a date may be given, and(b) may not specify a date that falls more than one year after the date on

which the notice is given.

(10) In this section “an appeal tribunal” has the same meaning as in Chapter 2 ofPart 1 of the Finance Act 1994 (see section 7).

24 Rulings as to application of customs tariff or place of origin

(1) HMRC Commissioners must by public notice make provision establishing asystem under which persons apply for rulings given by HMRC officers for thepurpose of—

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 1 — Import duty

16

(a) determining any issue as to the code in the customs tariff applicable toany goods, or

(b) determining the place of origin of any goods for the purposes of thisPart.

(2) Each of the following is an example of the kind of provision that may be madeby the notice—

(a) provision specifying cases in which rulings need not be given,(b) provision about the making of the applications (including their form,

the information to be contained in them and any documents toaccompany them),

(c) provision requiring the applications to be determined within aspecified period,

(d) provision about the period for which, and other conditions subject towhich, the rulings are to have effect,

(e) provision about the form in which the rulings are to be given,(f) provision for the withdrawal or amendment of rulings,(g) provision determining the extent to which the rulings may be relied on

by applicants, and(h) provision requiring any person to whom a ruling has been given to

disclose that fact to HMRC.

(3) The system established by the notice must secure that an application may bemade for a ruling even if an HMRC officer considers that the ruling is not, ormay not be, required to resolve a doubt as to the issue being determined.

Supplementary

25 Disclosure of information

(1) HMRC (or anyone acting on their behalf) may disclose information relating toimport duty for customs duty purposes.

(2) In this section “customs duty purposes” means purposes in connection with, orotherwise incidental to, the imposition, enforcement or other regulation ofimport duty.

(3) A person who receives information as a result of this section may not furtherdisclose the information except with the consent of the HMRC Commissioners(which may be general or specific).

(4) A person who receives information as a result of this section may use theinformation only for customs duty purposes.

(5) If a person discloses information in contravention of subsection (3) whichrelates to a person whose identity—

(a) is specified in the disclosure, or(b) can be deduced from it,

section 19 of the Commissioners for Revenue and Customs Act 2005 (offence ofwrongful disclosure) applies in relation to that disclosure as it applies inrelation to a disclosure in contravention of section 20(9) of that Act.

(6) This section does not limit the circumstances in which information may bedisclosed under section 18(2) of the Commissioners for Revenue and CustomsAct 2005 or under any other enactment or rule of law.

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 1 — Import duty

17

(7) Nothing in this section authorises the making of a disclosure which—(a) contravenes the Data Protection Act 1998, or (b) is prohibited by any of Parts 1 to 7 or Chapter 1 of Part 9 of the

Investigatory Powers Act 2016.

26 Co-operation with other customs services

(1) HMRC may cooperate with other customs services on matters of mutualconcern with a view to securing (by the exchange of information orotherwise)—

(a) the administration of the import duty system,(b) the prevention or detection of evasion or other fraud relating to import

duty, and(c) the prevention, reduction or elimination of avoidance of a liability to

import duty.

(2) Section 25(3) to (7) apply in relation to information disclosed as a result of thissection.

27 Fees for exercise of functions in connection with import duty

(1) The Treasury may by regulations authorise the charging of fees in respect ofthe exercise of any specified function of HMRC, or of an HMRC officer, for thepurposes of, or otherwise in connection with, import duty.

(2) The power may be exercised by the Treasury only if they consider that—(a) its exercise is consistent with arrangements between Her Majesty’s

government in the United Kingdom and any other government or anyinternational organisation or authority, and

(b) the circumstances in which the specified function is, or is likely to be,exercised are such that it is fair and reasonable for the charge to bemade.

28 Requirement to have regard to international obligations

(1) In exercising any function under any provision made by or under this Part—(a) the Treasury,(b) the Secretary of State,(c) HMRC, (d) the TRA, and(e) any other public body,

must have regard to international arrangements to which Her Majesty’sgovernment in the United Kingdom is a party that are relevant to the exerciseof the function.

(2) This section is not to be read as affecting the circumstances in which anyobligation to have regard to such matters would otherwise have arisen.

29 Consequential amendments

(1) Schedule 7 contains amendments consequential on the provision made by thisPart.

(2) The amendments made by that Schedule include amendments dealing with—

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

18

(a) reviews or appeals of decisions in relation to import duty (see sections13A to 16 of, and Schedule 5 to, the Finance Act 1994), and

(b) penalties in relation to breaches of requirements in relation to importduty (see Part 3 of the Finance Act 2003).

30 General provision for the purposes of import duty

The Treasury may by regulations—(a) make provision supplementing provision made in relation to import

duty by or under this Part or any other enactment, or (b) make other provision generally for the purposes of import duty.

UK's customs union

31 Territories forming part of a customs union with UK

(1) This section applies if arrangements are entered into between—(a) Her Majesty’s government in the United Kingdom, and(b) the government of a country or territory outside the United Kingdom,

establishing a customs union between the United Kingdom and the country orterritory.

(2) Arrangements establish a “customs union” between the United Kingdom anda country or territory if—

(a) they provide that no duty is to be chargeable by reference tomovements of goods, or goods of a specified description, between theUnited Kingdom and the country or territory, and

(b) they provide for the same, or substantially the same, rules for chargingduty on imports of goods, or goods of a specified description, fromplaces outside the United Kingdom or the country or territory.

(3) For this purpose—“duty” means—

(a) import duty, or(b) any duty (however described) imposed by the law of the

country or territory that is of a similar character to import duty,and

“specified” means specified in the arrangements.

(4) If Her Majesty by Order in Council declares that it is expedient that thearrangements should have effect for the purposes of import duty, thearrangements have effect for those purposes despite any enactment.

(5) HMRC Commissioners may make regulations generally for carrying out anyarrangements having effect in accordance with this section.

(6) Among other things, the regulations may—(a) modify or disapply provision made by or under this Part or any other

Act,(b) treat anything done by the government of a country or territory as if

done by the appropriate authority or person in the United Kingdom,and

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

19

(c) apply or replicate, with or without modifications, provision relating toduty under the law of a country or territory as that provision has effectfrom time to time.

(7) Examples of the kind of provision within subsection (6)(b) are—(a) provision treating an agreement entered into by a country or territory

as if it were entered into by Her Majesty’s government in the UnitedKingdom, and

(b) provision treating a system for determining the amount of dutyestablished under the law of a country or territory as if it were thecustoms tariff mentioned in section 8.

Regulations etc

32 Regulations etc

(1) Regulations under this Part are to be made by statutory instrument.

(2) A statutory instrument containing—(a) the first regulations under section 8, or(b) any other regulations under that section the effect of which is an

increase in the amount of import duty payable under the customs tariffin a standard case (within the meaning of that section),

must be laid before the House of Commons, and, unless approved by thatHouse before the end of the period of 28 days beginning with the date on whichthe instrument is made, ceases to have effect at the end of that period.

(3) The fact that a statutory instrument ceases to have effect as a result ofsubsection (2) does not affect—

(a) anything previously done under the instrument, or(b) the making of a new statutory instrument.

(4) In calculating the period for the purposes of subsection (2), no account is to betaken of any time—

(a) during which Parliament is dissolved or prorogued, or(b) during which the House of Commons is adjourned for more than 4

days.

(5) A statutory instrument containing regulations made under this Part other thanregulations to which subsection (2) applies is subject to annulment inpursuance of a resolution of the House of Commons.

(6) Any power to make regulations under this Part may be exercised—(a) either in relation to all cases to which the power extends, or in relation

to those cases subject to specified exceptions, or in relation to anyspecified case or description of case, or

(b) so as to make different provision for different purposes or areas.

(7) Any power to make regulations under this Part includes—(a) power conferring a discretion on any specified person to do anything

under, or for the purposes of, the regulations,(b) power to make provision by reference to things specified in a notice

published in accordance with the regulations,

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

20

(c) power to make supplementary, incidental and consequential provision,and

(d) power to make transitional or transitory provision and savings.

(8) Any power to make regulations under any provision of this Part does notrestrict the width of any power to make subordinate legislation under—

(a) any other provision of this Part, or(b) CEMA 1979 or any other enactment.

(9) Subsections (6) to (8) apply in relation to any public notice under this Part; andany provision that may be made by a public notice under this Part may bemade by regulations.

(10) An Order under section 31—(a) is not to be submitted to Her Majesty in Council unless a draft of the

Order has been laid before, and approved by a resolution of, the Houseof Commons, and

(b) if it revokes an earlier Order under that section, may containtransitional or transitory provision and savings.

(11) After it is established, the Secretary of State must consult the TRA beforemaking regulations under Schedule 4 or 5.

(12) Any power of HMRC Commissioners to make regulations under this Part isexercisable concurrently by the Treasury.

Interpretation etc

33 Meaning of “domestic goods”

(1) Goods are domestic goods for the purposes of this Part if—(a) they are wholly obtained in the United Kingdom, or(b) they have been subject to a chargeable Customs procedure.

(2) For the purposes of this section goods have been “subject to a chargeableCustoms procedure” if—

(a) the goods were declared for the free-circulation procedure and theprocedure has been discharged, or

(b) the goods were declared for an authorised use procedure and theprocedure has been discharged.

(3) Goods cease to be domestic goods if—(a) they are exported from the United Kingdom, and(b) the export is one which is required to be made in accordance with the

applicable export provisions,and the goods are then chargeable goods until such time (if any) as they arenext subject to a chargeable Customs procedure.

(4) For the purposes of subsection (3), every export of goods is required to be madein accordance with the applicable export provisions unless an exceptionprovided for by regulations made by HMRC Commissioners applies to theexport.

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

21

(5) HMRC Commissioners may by regulations make provision for goods exportedfrom the United Kingdom in accordance with the applicable export provisionsto retain their status as domestic goods if—

(a) the goods merely pass through places outside the United Kingdombefore arriving at their ultimate destination in the United Kingdom, or

(b) the goods otherwise remain outside the United Kingdom for atemporary period.

(6) The provision that may be made by the regulations includes—(a) provision requiring conditions to be met in relation to the goods while

they are outside the United Kingdom, and(b) provision requiring the making of a declaration in connection with

their subsequent import into the United Kingdom.

(7) Goods that are in the United Kingdom are presumed to be domestic goodsunless the contrary is shown.

(8) The Treasury may by regulations make provision—(a) as to cases in which goods are, or are not, to be regarded as domestic

goods for the purposes of this Part,(b) for reversing the presumption that goods are domestic goods in

specified cases (so that they are presumed not to be domestic goodsunless the contrary is shown), and

(c) as to the evidence which is to be required, or is to be sufficient, for thepurpose of showing that goods are domestic goods.

34 Presentation of goods to Customs on import or export

(1) For the purposes of this Part, goods are presented to Customs on import if—(a) the goods are lawfully imported into the United Kingdom, and(b) notification of their importation into the United Kingdom is given to

HMRC in accordance with provision made by regulations made byHMRC Commissioners.

(2) The time at which goods are presented to Customs on import is the later of—(a) the time at which the notification of importation in accordance with the

regulations is received by HMRC, and(b) the time at which the goods are imported into the United Kingdom.

(3) For the purposes of this Part, goods are presented to Customs on export ifnotification of their export from the United Kingdom is given to HMRC inaccordance with provision made by regulations made by HMRCCommissioners.

(4) The notification must be given before the export of goods unless provision ismade by regulations made by HMRC Commissioners authorising thenotification to be given at a later time.

(5) Regulations made by HMRC Commissioners may make provision for thepurposes of this section.

(6) Each of the following is an example of the kind of provision that may be madeby regulations under this section—

(a) provision requiring a notification to be accompanied by documents ofa description specified in the regulations or in a public notice given byHMRC Commissioners,

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 1 — Import duty

22

(b) provision authorising a public notice given by HMRC Commissionersto make provision about the form and contents of a notification,

(c) provision authorising a public notice given by HMRC Commissionersto require notification to be made in accordance with provision madeby the notice,

(d) provision requiring or authorising, in specified cases, notification of animportation of goods to be given before the importation,

(e) provision deeming a notification to have been given in specified cases,and

(f) provision requiring a notification to disclose the location of the goods.

35 Exports made in accordance with applicable export provisions

(1) This section defines for the purposes of this Part what is meant by an export ofgoods from the United Kingdom being in accordance with the applicableexport provisions.

(2) The export of the goods is made in accordance with the applicable exportprovisions if—

(a) the goods are presented to Customs on export, and(b) the export is subsequently made in accordance with a procedure

provided for by regulations made by HMRC Commissioners.

(3) The regulations may—(a) provide for the procedure to involve the making of a declaration by the

person making the export or any specified person,(b) provide for requirements to be imposed on any person at any time

while the goods are subject to the procedure,(c) make provision specifying, or otherwise determining, the period

during which the goods are to be regarded as subject to the procedure,(d) deem, in specified cases, the export to have been made in accordance

with the procedure, and(e) provide for goods to be subject to the control of any HMRC officer from

a specified time.

(4) The provision which may be made as a result of subsection (3)(a) includesprovision applying or replicating the effect of—

(a) any provision made by or under Schedule 1 (Customs declarations), or(b) any other provision made by or under this Part that operates (to any

extent) by reference to a Customs declaration,with or without modifications.

36 Outward processing procedure

(1) This section applies if—(a) domestic goods have been presented to Customs on export, and(b) the goods are declared for an outward processing procedure.

(2) A declaration of goods for “an outward processing procedure” is adeclaration—

(a) that the goods are to be exported from the United Kingdom in order tobe processed outside the United Kingdom,

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

23

(b) that the processing is to take place during a temporary period at the endof which the goods are to be imported into the United Kingdom, and

(c) that the processing is to be carried out in accordance with requirementsimposed on any person by or under regulations made by HMRCCommissioners.

(3) The temporary period during which the processing is to take place is the periodspecified in a notice given to the person making the declaration by an HMRCofficer.

(4) That period may be subsequently extended (or further extended) by anothernotice given as mentioned in subsection (3).

(5) If goods are declared for an outward processing procedure—(a) the export of the goods is not one which is required to be made in

accordance with the applicable export provisions, but(b) HMRC Commissioners may by regulations make provision in relation

to any export under an outward processing procedure correspondingto the provision that may be made by regulations under section 35.

(6) If the processing of the goods under an outward processing procedure consistsin their repair by any person without charge, the goods continue to be regardedas domestic goods but only if, while the procedure has effect—

(a) there is no breach of the terms of the declaration for the procedure, and(b) there is no breach of any other requirement in relation to the procedure.

(7) If the processing of the goods under an outward processing procedure consistsin anything else, the goods are to be regarded as chargeable goods, but if—

(a) the goods are imported in accordance with the procedure, and(b) there is no breach of the terms of the declaration for the procedure, or

of any other requirement in relation to the procedure, while theprocedure has effect,

the value of the goods is to be reduced to take account of so much of that valueas can be attributed to the goods as they stood before being exported.

(8) HMRC Commissioners may make regulations for the purposes of this section.

(9) Each of the following is an example of the kind of provision that may be madeby the regulations—

(a) provision specifying cases in which goods may not be declared for anoutward processing procedure,

(b) provision imposing requirements on any person in relation to anoutward processing procedure,

(c) provision for determining the reduction in the value of any goods forthe purposes of subsection (7),

(d) provision authorised or required to be made by any regulations underSchedule 2, and

(e) other provision made by or under this Part of this Act that has effect inrelation to a special Customs procedure.

37 Minor definitions

(1) In this Part—

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 1 — Import duty

24

“approved guarantee”, in relation to goods declared for the free-circulation procedure, means any guarantee given in accordance withregulations made under paragraphs 6 and 7 of Schedule 6,

“arrangements” includes an understanding of any kind,“CEMA 1979” means the Customs and Excise Management Act 1979,“directions” means directions in electronic form or otherwise in writing,“guarantee” includes any indemnity, surety, security and undertaking of

any kind,“HMRC” means Her Majesty’s Revenue and Customs,“HMRC Commissioners” means the Commissioners for Her Majesty’s

Revenue and Customs,“HMRC officer” means an officer of Revenue and Customs,“notice”, except in the expression “public notice”, means a notice in

electronic form or otherwise in writing,“specified”, in relation to any regulations or public notice, means specified

in, or determined in accordance with, the regulations or public notice,“subordinate legislation” has the same meaning as in the Interpretation

Act 1978, and“the WTO” means the World Trade Organisation.

(2) In this Part any reference to a rate of duty includes a nil rate.

(3) In this Part any reference to goods being wholly obtained in any country orterritory includes—

(a) any case where the goods are grown, produced or manufactured onlyin the country or territory, and

(b) any other cases specified in regulations made by the Treasury.

(4) In this Part any reference to the processing of any goods includes the followingactivities—

(a) the erection, assembly, fitting or other working of the goods,(b) the repair of the goods,(c) the use of the goods for the purpose of facilitating the production or

manufacture of any other goods, and(d) the destruction of the goods.

(5) Any reference in any provision of this Part to a public notice is to a noticepublished by the Secretary of State, or (as the case may be) HMRCCommissioners, in such manner as the person giving the notice considersappropriate for the purposes of that provision.

(6) In this Part—(a) references to a territory outside the United Kingdom include the

European Union or any other international organisation or authoritycomprising territories outside the United Kingdom, and

(b) expressions relating to a territory outside the United Kingdom (such asthe government of a territory outside the United Kingdom or the law ofa territory outside the United Kingdom) are to be read accordingly withthe necessary modifications.

(7) For the purposes of this Part any reference to goods being subject to the controlof an HMRC officer includes control being exercised by—

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 1 — Import duty

25

(a) requiring the goods to be handled, or otherwise dealt with, inaccordance with instructions given by an HMRC officer (whether givenorally or in any other way), or

(b) requiring the goods to be kept in any place specified by an HMRCofficer.

(8) In the case of any reference in this Part to a person who makes a Customsdeclaration—

(a) the reference is to the person actually making the declaration even if thedeclaration is made on behalf of another person, and

(b) if a Customs declaration is made by a Customs agent in the name of theprincipal, the reference is to the agent despite the provision made bysection 21(3).

38 Table of definitions

The following table sets out some of the expressions used in this Part, showingwhere they are defined or otherwise explained—

acceptance (of a Customs declaration) paragraphs 11(2) and 13(4)of Schedule 1

the applicable export provisions section 35

approved guarantee (in relation to goodsdeclared for the free-circulation procedure)

section 37(1)

arrangements section 37(1)

an authorised use procedure paragraph 13 of Schedule 2

CEMA 1979 section 37(1)

chargeable goods section 2

control of HMRC officer section 37(7)

Customs agent section 21

Customs procedures section 3

customs tariff section 8

directions section 37(1)

domestic goods section 33

export (time of) section 5 of CEMA 1979

the free-circulation procedure section 3

guarantee section 37(1)

HMRC section 37(1)

HMRC Commissioners section 37(1)

HMRC officer section 37(1)

5

10

15

20

25

30

35

Taxation (Cross-border Trade) BillPart 1 — Import duty

26

PART 2

EXPORT DUTY

39 Charge to export duty

(1) The Treasury may by regulations make provision for, and in connection with,the charging of a duty of customs (to be known as “export duty”) by referenceto the export of goods from the United Kingdom.

(2) The regulations may provide for export duty to be chargeable by reference tothe export of —

(a) all goods, or

import (time of) section 5 of CEMA 1979

import duty section 1

an inward processing procedure paragraphs 9 and 11 ofSchedule 2

notice (except in the expression “public notice”) section 37(1)

origin (of goods) section 17

person making a Customs declaration section 37(8)

presented to Customs on export section 34(3)

presented to Customs on import section 34(1) and (2)

processing (of goods) section 37(4)

public notice section 37(5)

rate of duty section 37(2)

special Customs procedure section 3

specified (in relation to regulations or publicnotices)

section 37(1)

a storage procedure paragraph 2 of Schedule 2

subordinate legislation section 37(1)

a temporary admission procedure paragraph 15 of Schedule 2

territory outside the United Kingdom (andrelated expressions)

section 37(6)

the TRA section 13

a transit procedure paragraph 5 of Schedule 2

value (of chargeable goods) section 16

wholly obtained (in the case of goods) section 37(3)

the WTO section 37(1)

5

10

15

20

25

30

Taxation (Cross-border Trade) BillPart 2 — Export duty

27

(b) goods of a description specified in the regulations.

(3) The regulations—(a) may provide for export duty to be chargeable in accordance with a tariff

specified in the regulations (“the export tariff”),(b) may provide for export duty to be chargeable by reference to value,

weight or volume or other measure of quantity or size, and(c) may provide for the value of the goods and the other matters

mentioned in paragraph (b) to be determined in accordance with theregulations.

(4) In considering whether to impose export duty, and, if so, the rate of duty thatought to apply to any goods, the Treasury must have regard to—

(a) the interests of consumers in the United Kingdom,(b) the desirability of maintaining and promoting the external trade of the

United Kingdom,(c) the desirability of maintaining and promoting productivity in the

United Kingdom, and(d) the extent to which the goods concerned are subject to competition.

(5) In considering whether to impose export duty, and, if so, the rate of duty thatought to apply to any goods, the Treasury must also have regard to anyrecommendation about the rate made to them by the Secretary of State.

(6) In considering what recommendation to make, the Secretary of State must haveregard to the matters set out in subsection (4)(a) to (d).

(7) The provision that may be made by regulations under this section includesprovision replicating or applying, with or without modifications, anyprovision made by or under—

(a) Part 1, or(b) any other enactment relating to import duty.

(8) Paragraph 1 of Schedule 7 (replacement of EU customs duties) applies inrelation to this Part as it applies in relation to Part 1 (reading any reference toimport duty as a reference to export duty).

(9) In this section “specified” means specified in, or determined in accordancewith, the regulations.

40 Regulations under section 39: supplementary

(1) Regulations under section 39 are to be made by statutory instrument.

(2) A statutory instrument containing—(a) the first regulations under that section, or(b) any other regulations under that section the effect of which is an

increase in the amount of export duty payable,must be laid before the House of Commons, and, unless approved by thatHouse before the end of the period of 28 days beginning with the date on whichthe instrument is made, ceases to have effect at the end of that period.

(3) The fact that a statutory instrument ceases to have effect as a result ofsubsection (2) does not affect—

(a) anything previously done under the instrument, or(b) the making of a new statutory instrument.

5

10

15

20

25

30

35

40

45

Taxation (Cross-border Trade) BillPart 2 — Export duty

28

(4) In calculating the period for the purposes of subsection (2), no account is to betaken of any time—

(a) during which Parliament is dissolved or prorogued, or(b) during which the House of Commons is adjourned for more than 4

days.

(5) A statutory instrument containing regulations under section 39 other thanregulations to which subsection (2) applies is subject to annulment inpursuance of a resolution of the House of Commons.

(6) Any power to make regulations under section 39 may be exercised—(a) either in relation to all cases to which the power extends, or in relation

to those cases subject to specified exceptions, or in relation to anyspecified case or description of case, or

(b) so as to make different provision for different purposes or areas.

(7) Any power to make regulations under section 39 includes—(a) power conferring a discretion on any specified person to do anything

under, or for the purposes of, the regulations,(b) power to make provision by reference to things specified in a notice

published in accordance with the regulations,(c) power to make supplementary, incidental and consequential provision,

and(d) power to make transitional or transitory provision and savings.

PART 3

VALUE ADDED TAX

41 Abolition of acquisition VAT and extension of import VAT

(1) The Value Added Tax Act 1994 is amended as follows.

(2) In section 1 (imposition of charge to value added tax), in subsection (1)—(a) omit paragraph (b) (which charges VAT on the acquisition in the

United Kingdom of goods from other member States), and(b) for paragraph (c) substitute—

“(c) on the importation of goods into the United Kingdom,”.

(3) For section 15 substitute—

“15 Meaning of “importation of goods” into the United Kingdom

(1) This section determines for the purposes of this Act when, and bywhom, goods are imported into the United Kingdom.

(2) Goods are imported when they are declared for a Customs procedureunder Part 1 of TCTA 2018.

(3) But—(a) in the case of goods declared under TCTA 2018 for a storage

procedure, a transit procedure or an inward processingprocedure, the goods are imported when a liability to importduty is, or on the relevant assumptions would be, incurred inrespect of them under section 4 of that Act, and

5

10

15

20

25

30

35

40

Taxation (Cross-border Trade) BillPart 3 — Value added tax

29

(b) in the case of goods which are liable to forfeiture as a result ofsection 5(1) of, or paragraph 1(5) or 3(4) of Schedule 1 to, thatAct (goods not presented to Customs or Customs declarationnot made), the goods are imported when they become liable toforfeiture as a result of those provisions.

(4) Each person who is, or on the relevant assumptions would be, liable toimport duty in respect of goods imported into the United Kingdom is aperson who has imported the goods.

(5) For the purposes of this section “the relevant assumptions” are—(a) an assumption that a liability to import duty at a nil rate is

replaced by a liability to import duty at a higher rate, and(b) an assumption that no relief from import duty is available.

(6) If two or more persons are regarded as importing goods, those personsare jointly and severally liable to any VAT that is payable on theimportation.

(7) The preceding provisions of this section are to be ignored in readingany reference to importation or to an importer in anything applied forthe purposes of this Act by section 16(1) or (2).

(8) But subsection (7) does not apply so far as the context otherwiserequires or provision to the contrary is contained in regulations undersection 16(3).”

42 EU law relating to VAT