Tax Tables 2018/19 - Wizard Learning · Page 2 v 81.1 On 20 February 2018, the Scottish Government...

13

Page 1 v81.1 Assisting finance professionals to pass industry exams and helping meet their CPD requirements with our accredited CPD system © Wizard Learning Ltd Tax Tables 2018/19 1. Income Tax rates 2. Personal Allowances 3. Child Tax Credit 4. Working Tax credit 5. Company Cars 6. National Insurance Contributions 7. Capital Gains Tax 8. ISA Subscription Limits 9. Value Added Tax 10. Stamp Duties 11. Corporation Tax 12. Pension Contributions 13. Inheritance Tax 1. Income Tax Rates Each year, the rates of Income Tax are set in the annual budget. It is charged at increasing rates, depending on the amount of income an individual has and from where it has arisen. 2018/19 2017/18 Rate % Band Rate % Band 0 £1 - £5,000 * 0 £1 - £5,000 * 20 £1 - £34,500 20 £1 - £33,500 40 £34,500 - £150,000 40 £33,500 - £150,000 45 Over £150,000 45 Over £150,000 * The 0% starting rate is applied for savings income, applicable where non-savings taxable income after allowances is under £5,000. If non-savings taxable income exceeds £5,000 then the 0% starting rate for savings will not apply.

Transcript of Tax Tables 2018/19 - Wizard Learning · Page 2 v 81.1 On 20 February 2018, the Scottish Government...

Page 1 v81.1

Assisting finance professionals to pass industry exams and helping

meet their CPD requirements with our accredited CPD system

© Wizard Learning Ltd

Tax Tables 2018/19

1. Income Tax rates

2. Personal Allowances

3. Child Tax Credit

4. Working Tax credit

5. Company Cars

6. National Insurance Contributions

7. Capital Gains Tax

8. ISA Subscription Limits

9. Value Added Tax

10. Stamp Duties

11. Corporation Tax

12. Pension Contributions

13. Inheritance Tax

1. Income Tax Rates Each year, the rates of Income Tax are set in the annual budget. It is charged at

increasing rates, depending on the amount of income an individual has and from

where it has arisen.

2018/19 2017/18

Rate % Band Rate % Band

0 £1 - £5,000 * 0 £1 - £5,000 *

20 £1 - £34,500 20 £1 - £33,500

40 £34,500 - £150,000 40 £33,500 - £150,000

45 Over £150,000 45 Over £150,000

* The 0% starting rate is applied for savings income, applicable where non-savings

taxable income after allowances is under £5,000. If non-savings taxable income

exceeds £5,000 then the 0% starting rate for savings will not apply.

Page 2 v81.1

On 20 February 2018, the Scottish Government set the following income tax rates for

Scotland.

Bands Band name Rates (%)

Over £11,850*- £13,850 Starter Rate 19

Over £13,850-£24,000 Basic Rate 20

Over £24,000-£43,430 Intermediate Rate 21

Over £43,430-£150,000** Higher Rate 41

Above £150,000** Top Rate 46

* Assumes person is in receipt of the Standard UK Personal Allowance

** Personal Allowance is reduced by £1 for every £2 earned over £100,000.

In England and Wales, the 20% rate applies to income up to £34,500 in the current tax

year is known as the basic rate and the 40% rate on income in excess of £34,500 is

known as the higher rate. The 45% rate on income in excess of £150,000 is known as

the additional rate. A new Personal Savings Allowance (PSA) was introduced in the

2016/17 tax year on interest received from savings. Basic rate taxpayers have an

allowance of £1,000 on which no tax will be paid, and higher rate taxpayers have an

allowance of £500 on which no tax will be paid. Additional rate taxpayers have no

PSA and any interest received will be taxed in full.

Another change that took effect from the 2016/17 tax year onwards is the payment of

savings interest gross, i.e. with no income tax deducted at source. Prior to 6 April

2016, interest was paid net of 20% income tax. Higher rate and additional rate

taxpayers paid further income tax of 20% and 25% respectively of the grossed-up

interest, basic rate taxpayers had no further tax to pay on the interest, and non-

taxpayers could reclaim the tax already deducted.

Until 2015/16, dividend income was paid with a 10% tax credit. This was

representative of the tax already paid by the company on its profits and, although not

income tax, it was deemed to satisfy the basic rate tax liability to income tax on

dividends. So, the tax rates for dividend income were 10% (income up to the basic

rate), 32.5% (higher rate) and 37.5% (additional rate). Higher rate and additional rate

taxpayers paid an additional 22.5% and 27.5% respectively of the grossed-up

dividend. Basic rate taxpayer had no further tax liability, nor did non-taxpayers,

although this 10% tax credit was not reclaimable, not by anyone.

This changed from the start of the 2016/17 tax year. The 10% tax credit was removed

and dividends are now paid gross. In 2018/19, all individuals have a dividend

allowance of £2,000 on which no income tax will be charged. Dividend income in

excess of £2,000 in the tax year will be charged at 7.5% for basic rate taxpayers,

32.5% for higher rate taxpayers and 38.1% for additional rate taxpayers.

Page 3 v81.1

2. Personal Allowances

2018/19 2017/18

Personal * £11,850 £11,500

Married couples (and civil partners) allowance

(born before 6/4/1935) minimum at 10% **

£3,360 £3,260

Married couples (and civil partners) allowance

(born before 6/4/1935) maximum at 10%**

£8,695 £8,445

Marriage Allowance*** £1,190 £1,100

Age related allowances reduced by £1 for every

£2 of income over: (Married, born before

6/4/35)**

£28,900 £28,000

Rent-a-room £7,500 £7,500

Blind Persons Allowance £2,390 £2,320

Enterprise Investment Scheme relief limit at 30% £2,000,000**** £1,000,000

Venture Capital Trust relief limit at 30% £200,000 £200,000

Seed Enterprise Investment Scheme at 50% £100,000 £100,000

Seed Enterprise Investment Scheme CGT

reinvestment relief

50% 50%

Social Investment Tax Relief 30% £1,000,000 /

£1,500,000 for

enterprises up

to 7 years old

£1,000,000

* The Personal Allowance will be reduced by £1 for every £2 where net income exceeds

£100,000 with no personal allowance above £123,700 in 2018/19 (was £123,000 in 2017/18)

** Married couples and civil partners where at least one of the couple was born before

6/4/1935 are entitled to the married couples allowance. This is a restricted allowance, i.e. it

does not increase the amount of income that can be received before tax is payable; instead it

reduces the tax bill by 10% of the amount of allowance the individual is entitled to. It is

subject to the income limit of £28,900, which means that those with income under this

amount will receive the full married couples allowance However, this allowance is lost at a

rate of £1 for every £2 of income that exceeds £28,900. When income reaches £39,570, the

married couples allowance is reduced to its lowest level of £3,360.

*** Available for those born after 5 April 1938 – a basic rate or non-taxpayer can transfer up

to 10% of the personal allowance (£1,190 2018/19) to a spouse or civil partner who is not a

higher or additional rate taxpayer.

**** Above £1,000,000 must be in knowledge intensive companies

Certain Income Tax reliefs are capped at the greater of £50,000 or 25% of income.

This excludes charitable donations.

An additional tax charge applies to claw back child benefit (by 1% for every £100 of

income) where one income in a household exceeds £50,000, with full claw back by

£60,000.

Page 4 v81.1

3. Child Tax Credit MAXIMUM

AMOUNT 2018/19

Family element - the basic payment if responsible for one or

more children

£545

Child element - for each child under 16, paid on top of the

family element

£2,780

Disabled child element (additional to child element) £3,275

Severely disabled child element, paid on top of any disability

element

£1,325

A qualifying young person is a person aged under 20 in full-time non-advanced

education or on an approved unwaged job-related training scheme. A family can only

receive one family element regardless of the number of children. Child tax credit may

not be paid if there is one child and the annual income is more than £40,000, there are

two children and the annual income is more than £55,000, or there are three children

and the annual income is more than £65,000. If the household does not have childcare

costs to take into account, the limits are £25,000, £35,000 and £40,000 respectively.

Payments are made in relation to each individual’s unique personal circumstances.

4. Working Tax Credit MAXIMUM IN 2018/19

Basic £1,960

Second adult in family £2,010

Lone parent £2,010

30 hour element (where one person works

at least 30 hours)

£810

Disability (for each disabled worker) £3,090

Severe disability (for each disabled

worker)

£1,330

Childcare: one child Entitled to 70% of eligible childcare

costs, which are capped at £175/week

(max entitlement £175 x 70% = £122.50)

Childcare: two or more children Entitled to 70% of eligible childcare

costs, which are capped at £300/week

(max entitlement £300 x 70% = £210)

All the elements of both child and working tax credit are tapered by reference to the

claimant’s’ circumstances. The maximum amounts payable are initially calculated

without reference to income. A reduction is then made with reference to the amount of

income. For child tax credit, where income exceeds £16,105 it will be reduced by

41%. For working tax credit, it is also reduced by 41% for income over £6,420.

Families who receive income support, income-based jobseekers allowance and

pension credit are automatically entitled to the full child tax credit without reference

to income.

A couple with children are required to work at least 24 hours between them in order to

qualify, in addition to the requirement that one of the couple works at least 16 hours

per week, although payment depends on individual circumstances.

Page 5 v81.1

4A Tax credits income thresholds The tax credits income thresholds and withdrawal rates are shown below.

Income thresholds and withdrawal rates - £ per year (unless stated)

2018/19 2017/18

Rates and Thresholds

First income threshold £6,420 £6,420

First withdrawal rate (per cent) 41% 41%

Second income threshold Withdrawn Withdrawn

First threshold for those entitled to Child Tax

Credit only

£16,105 £16,105

Income rise disregard £2,500 £2,500

Income fall disregard £2,500 £2,500

5. Company Cars

Car benefit

Calculated as a percentage of the list price based on the vehicles’ CO2 emissions.

CO2 emissions – grams

per kilometre

Percentage charge

Petrol

Percentage Charge

Diesel

0 - 50 13% 17%

51 - 75 16% 20%

76 - 94 19% 23%

95 - 99 20% 24%

100 -104 21% 25%

105 -109 22% 26%

110 - 114 23% 27%

115 - 119 24% 28%

120 - 124 25% 29%

125 - 129 26% 30%

130 - 134 27% 31%

135 - 139 28% 32%

140 - 144 29% 33%

145 - 149 30% 34%

150 - 154 31% 35%

155 - 159 32% 36%

160 - 164 33% 37%

165 - 169 34% 37%

170 - 174 35% 37%

175 - 179 36% 37%

180 and over 37% 37%

Zero emission cars (e.g. electric) have no taxable benefit.

Fuel benefit:

Calculated as a percentage of £23,400

Percentage used is from the above table.

Page 6 v81.1

Minimum at 13% £3,042

Maximum at 37% £8,658

Private Vehicles Used For Work:

Cars

On the first 10,000 business miles in tax year 45p per mile

Each business mile above 10,000 business miles 25p per mile

Motor Cycles 24p per mile

Bicycles 20p per mile

Qualifying passenger 5p per mile

6. National Insurance Contributions

Thresholds and rates

Thresholds 2018/19 Weekly Monthly Yearly

Lower Earnings Limit (LEL) £116 £503 £6,032

Primary earnings threshold (employees) £162 £702 £8,424

Secondary earnings threshold (employers) £162 £702 £8,424

Upper earnings limit (UEL) £892 £3,863 £46,350

Class 1 employee contribution rates

Total earnings per week

Rates

Up to £162.00 Nil

£162.01 – £892.00 12%

Above £892.00 2%

Class 1 employer contribution rates 2018/19 based on earnings above

the employers’ secondary earnings threshold of £162 per week.

13.8%

From April 2014, businesses and charities can claim a reduction of up to £3,000

(2018/19) of their employers’ contributions (NIC employment allowance). This is not

available if a director is the sole employee.

In 2018/19, no employer’s contributions are payable in respect of weekly earnings up

to £892 paid to employees under age 21 or age 25 for apprentices.

Page 7 v81.1

Reduced rate Class 1 (married women)

Employee:

£162 - £892 per week 5.85%

Above £892 per week 2%

Employer: 13.8%

Class 1A contributions: Flat rate of 13.8%.

Maximum Class 1 contributions from multiple employments

53 x £730 (£892 - £162) x 12% = £4,642.80

Class 2 (self-employed) Flat rate - £2.95 per week / £153.40 per year where

earnings exceed £6,205

Class 3 (voluntary) Flat rate - £14.65 per week / £761.80 per year

Class 4 (self-employed) 9% on profits between £8,424 and £46,350

plus 2% on profits above £46,350.

7. Capital Gains Tax

Exemptions

2018/19 2017/18

Individuals, estates etc £11,700 £11,300

Trusts generally £5,850 £5,650

Chattels proceeds (5/3 excess gain is taxable) £6,000 £6,000

Rates

Nil and Basic Rate taxpayers 10%* 10%

Higher and additional rate taxpayers 20%* 20%

Trusts and estates 20%*

20%

* Rates of capital gains tax remain at 18% and 28% for gains made from property. For

all other gains, the rates of capital gains tax are 10% and 20% (2018/19)

The amount of gain is added to the individual's other income in the tax year to

establish the rate of tax to be paid. Any part of the gain falling into the basic income

tax rate band is charged at the lower rate and any excess is charged at the higher rate.

Entrepreneur’s Relief

Gains made from 23/6/2010 that qualify for the relief are taxed at the flat rate of 10%.

From 05/04/11 the lifetime limit has been set at £10,000,000.

For trading businesses and companies (minimum 5% employee shareholding) held for

1 year or more.

Page 8 v81.1

8. ISA Subscription Limits

ISA 2018/19 * £20,000

Junior ISA 2018/19 ** £4,260

Lifetime ISA £4,000

Help to Buy ISA (from 1 Dec 2015) £1,000 initial and £200/month

* Investment can be in cash or shares.

** From April 2015, cash in a Child Trust Fund can be transferred to a Junior ISA.

9. Value Added Tax

Standard Rate 20%

Reduced rate 5%

Zero-rate 0%

Annual registration limit £85,000

De-registration threshold £83,000

Flat rate scheme turnover limit £150,000

Cash and annual accounting schemes turnover limit £1,350,000

10. Stamp Duties

Stamp Duty Land Tax

England and Wales

Non Residential Land and Buildings

Property Value:

£ 0 - £150,000 0%

£150,001 - £250,000 2%

Over £250,000 5%

Residential Land and Buildings (rates applied cumulatively from 4 December 2014)

Property value:

Up to £125,000 0%

£125,001 - £250,000 2%

£250,001 - £925,000 5%

£925,001 - £1,500,000 10%

Over £1,500,000 12%

Page 9 v81.1

Rates for first-time buyers purchasing properties worth £500,000 or less

Property value Rate (on portion of value above threshold)

applicable to completions on or after 22

November 17 if purchase qualifies for first-

time buyer relief

0 to £300,000 0%

£300,000 to £500,000 5%

Over £500,000 Standard rates above apply

Scotland – Land & Buildings Transaction Tax (LBTT)

Non Residential Land and Buildings (from 1 April 2015)

Property value:

£0 - £150,000 0%

£150,001 - £350,000 3%

Over £350,000 4.5%

Residential Land and Buildings (from 1 April 2015)

Property value:

£0 - £145,000 0%

£145,001 - £250,000 2%

£250,001 - £325,000 5%

£325,001 - £750,000 10% *

Over £750,000 12%

* For residential properties purchased by companies (or similar entities) over

£500,000 the rate is 15%.

Second properties over £40,000 – add 3% to each band of Stamp Duty Land Tax and

Land & Buildings Transaction Tax from 1/4/16.

Stamp Duty and Stamp Duty Reserve Tax

Shares and Securities - Standard rate 0.5% of the consideration paid *

Stamp Duty Reserve Tax 0.5% / 1.5% (depending on whether electronic or paper

transaction)

* No charge unless amount due exceeds £5

Both taxes were abolished from 30 March 2014 on recognised growth markets,

including AIM and ISDX.

Page 10 v81.1

11. Corporation Tax Financial Year Year to 31/3/2019

Full rate on profits 19%

Diverted profits 25%

Capital Allowances

Plant & machinery 100% annual investment allowance (1st year) * £200,000

Writing down allowance

Plant & machinery, patent rights, know-how (reducing balance) per annum 18%

Plant and machinery in certain enterprise zones (max €125m per investment project)

100%

Energy-saving and water efficient plant and machinery 100%

Renovation of business premises (disadvantaged areas) 100%

*There is a 100% annual investment allowance on the first £200,000 tranche per annum of

capital expenditure incurred on or after 1 January 2016, per group of companies or related

entities, on plant and machinery including long life assets and integral features, but excluding

cars.

Certain long-life assets, integral features of buildings (reducing balance)

per annum 8%

Enterprise zone, commercial and industrial buildings** 100%

Motor cars

CO2 75g/km or less (new cars in first year) 100%

CO2 51 - 130g/km (reducing balance) 18%

CO2 over 130g/km or more (reducing balance) 8%

New and unused zero emissions goods vehicles 100%

Patent rights and know how *** 25%

Research & Development

Capital expenditure 100%

Tax credits SME scheme 230%

Tax credits large companies scheme 12%

Film Tax relief:

Limited budget (up to £20 million) 25%

Large budget (over £20 million)

25% on the first £20 million, 20% on additional expenditure.

Until April 2016, a ‘wear and tear allowance’ equivalent to 10% of the rental income was

given to landlords to reflect the cost of the upkeep of rented property. In April 2016, this was

abolished and now Replacement Relief exists, allowing landlords to offset the actual cost of

replacement items, capped at the cost of a modern equivalent if the new items improves the

old one.

** All enterprise zone designation periods have now ended. A balancing charge is made if the

building is sold within 25 years of its first use.

Page 11 v81.1

12. Pension Contributions Lifetime Allowance Annual Allowance* 2017/18 £1 million 2017/18 £40,000**

2018/19 £1,030,000 2018/19 £40,000**

* In some circumstances ‘carry forward’ may also be allowed from the previous three

tax years, by reference to a limit of £40,000 per annum (since the annual allowance

has remained at a constant £40,000 since 2014/15).

** Subject to 50% taper down to £10,000 if threshold income over £110,000 and net

adjusted income over £150,000.

Money Purchase Annual Allowance 2017/18 £4,000

2018/19 £4,000

Annual allowance charge Between 20% to 45% tax charge (depending on taxable income) on the amount of

total pension input in excess of the annual allowance

Lifetime allowance charge

55% of excess over lifetime allowance if taken as a lump sum.

25% of excess over lifetime allowance if taken in the form of income, which is

subsequently taxed under PAYE.

Unauthorised payment charge

A 40% income tax charge will be levied on the recipient of the payment and the

scheme would also be charged income tax normally at 15% of the unauthorised

payment. A surcharge of 15% income tax is payable in addition where the

unauthorised payment is more than 25% of the fund value.

Minimum pension age

The minimum pension age is 55. Increasing to 57 in 2028. For members with

protected retirement ages under 50, the lifetime allowance is reduced by 2.5% for

each year below the normal pension age except for some public service schemes such

as Police and Armed Forces. No reduction for ill health early retirement.

Triviality

Small pension funds can be paid as one-off lump sums, 25% tax free and 75% taxable

as income from age 55.

Maximum value of triviality lump sum is £30,000.

Flexible Access Drawdown (FAD) from 6 April 2015

Maximum tax free cash lump sum 25% of fund from age 55

Maximum income – unlimited from age 55

Uncrystallised Fund Pension Lump Sum (UFPLS) – 25% tax free, 75% taxable as

income

Maximum GAD limited for Capped Drawdown plans started before 5 April 2015

Page 12 v81.1

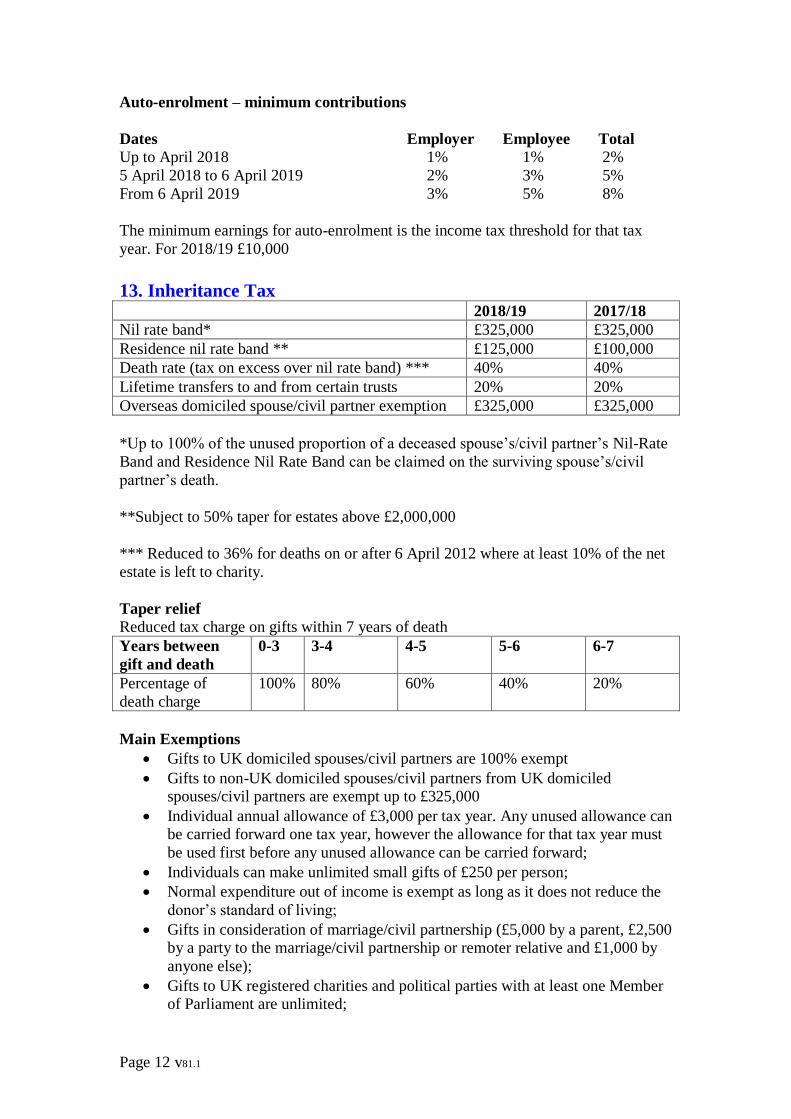

Auto-enrolment – minimum contributions

Dates Employer Employee Total

Up to April 2018 1% 1% 2%

5 April 2018 to 6 April 2019 2% 3% 5%

From 6 April 2019 3% 5% 8%

The minimum earnings for auto-enrolment is the income tax threshold for that tax

year. For 2018/19 £10,000

13. Inheritance Tax 2018/19 2017/18

Nil rate band* £325,000 £325,000

Residence nil rate band ** £125,000 £100,000

Death rate (tax on excess over nil rate band) *** 40% 40%

Lifetime transfers to and from certain trusts 20% 20%

Overseas domiciled spouse/civil partner exemption £325,000 £325,000

*Up to 100% of the unused proportion of a deceased spouse’s/civil partner’s Nil-Rate

Band and Residence Nil Rate Band can be claimed on the surviving spouse’s/civil

partner’s death.

**Subject to 50% taper for estates above £2,000,000

*** Reduced to 36% for deaths on or after 6 April 2012 where at least 10% of the net

estate is left to charity.

Taper relief Reduced tax charge on gifts within 7 years of death

Years between

gift and death

0-3 3-4 4-5 5-6 6-7

Percentage of

death charge

100% 80% 60% 40% 20%

Main Exemptions

Gifts to UK domiciled spouses/civil partners are 100% exempt

Gifts to non-UK domiciled spouses/civil partners from UK domiciled spouses/civil partners are exempt up to £325,000

Individual annual allowance of £3,000 per tax year. Any unused allowance can be carried forward one tax year, however the allowance for that tax year must

be used first before any unused allowance can be carried forward;

Individuals can make unlimited small gifts of £250 per person;

Normal expenditure out of income is exempt as long as it does not reduce the

donor’s standard of living;

Gifts in consideration of marriage/civil partnership (£5,000 by a parent, £2,500 by a party to the marriage/civil partnership or remoter relative and £1,000 by

anyone else);

Gifts to UK registered charities and political parties with at least one Member of Parliament are unlimited;

Page 13 v81.1

Gifts for public benefit/national purposes may also be exempt;

Gifts for the maintenance of a family (subject to conditions).

Reliefs

Business relief:

100% - available for interests in unincorporated businesses, sole traders and partnerships. Shareholdings of any size in unquoted and AIM companies.

50% - available for controlling shareholdings in fully listed companies. Land,

buildings, plant and machinery used wholly or mainly in connection with a

company controlled by the transferor or a partnership in which the transferor

was a partner.

Agricultural relief:

100% - available for owner occupied farms and farm tenancies.

50% - available for interest of landlords in let farmlands. The 50% relief is increased to 100% for land let under tenancies exceeding 12 months that

started after 31 August 1995.

The information provided is based on our understanding of UK law and HMRC

practice at the date of production, which may be subject to immediate change. Wizard

Learning are not responsible for any arrangements entered into on the basis of the

information in this document.