Tax on the Couch - NTAAntaa.com.au/downloads/TOTC June 2012 - Notes.pdf · Tax on the Couch –...

21

Tax on the Couch – June 2012 Tax on the Couch June 2012

Transcript of Tax on the Couch - NTAAntaa.com.au/downloads/TOTC June 2012 - Notes.pdf · Tax on the Couch –...

Tax on the Couch – June 2012

Tax on the Couch

June 2012

Tax on the Couch – June 2012

The information in this publication has been developed in consultation with the Australian Taxation Office.

ATO Disclaimer

This general advice has been prepared by the Australian Taxation Office ABN 52 824 753 556 and does not take account of your objectives or financial, legal or taxation situation or needs. Before acting on this general advice you should consider the appropriateness of the advice having regard to your situation. We recommend you obtain financial, legal and taxation advice in making an investment strategy and investing the assets of any fund.

This material has been prepared based on information believed to be accurate at the time of publication. Subsequent changes in circumstances may occur at any time and may impact the accuracy of the information.

This material or information is not intended as a form of financial advice and should not be treated as such. The Australian Taxation Office does not provide financial, legal or taxation advice.

The above disclaimer also applies to, and in respect of, the NTAA.

Disclaimer

The NTAA and their presenters do not hold an Australian Financial Services Licence to provide financial product advice under the Corporations Act 2001 (Cth). This material covers general taxation information which is only one of the factors to consider when making a decision on a financial product. If you are seeking financial product advice, you should contact a person who is licensed under the Corporations Act 2001 (Cth).

Tax on the Couch is intended to be a guide only. None of the comments contained in the presentation or notes are intended to be advice, whether legal, financial or professional. You should not act solely on the basis of the information contained in these notes because many aspects of the material have been generalised and the tax laws apply differently to different people in different circumstances. Further, as tax and related laws change frequently, there may have been changes to the law since the notes were written. Specific advice should always be obtained from a tax professional.

The NTAA, their directors, employees, consultants, presenters and authors expressly disclaim any and all liability to any person, whether a purchaser or not, for the consequences of anything done or omitted to be done by any such person relying on a part or the whole of the contents of this publication.

Copyright

© Copyright 2012 NTAA

All rights reserved. Except as permitted by the Copyright Act 1968, no part of these notes may be reproduced or published in any form or by any means, electronic or mechanical, including photocopying, recording, or by information storage or retrieval system, without prior written permission from the NTAA.

Feedback Please send any questions or feedback regarding Tax on the Couch to [email protected]

© Tax on the Couch: June 2012

Tax on the Couch – June 2012

Table of Contents Legislative Update....................................................................................................................................2 Bills of interest currently before Parliament (as at 19 May 2012) ............................................................2 Other legislative developments ................................................................................................................4 Rulings Update.........................................................................................................................................5 Rulings .....................................................................................................................................................5

Class Rulings ........................................................................................................................................5 Class Rulings – Notices ........................................................................................................................5 Goods and Services Tax Rulings – Notices ..........................................................................................5 Miscellaneous Tax Rulings....................................................................................................................5 Product Rulings .....................................................................................................................................6 Taxation Rulings – Notices....................................................................................................................6

Draft Rulings.............................................................................................................................................6 Draft Taxation Rulings...........................................................................................................................6

Determinations .........................................................................................................................................6 Taxation Determinations – Notices........................................................................................................6

Legislative Determinations .......................................................................................................................7 Excise....................................................................................................................................................7 Goods and Services Tax .......................................................................................................................7 Income Tax............................................................................................................................................7 PAYG Variations and Notices................................................................................................................7

ATO Interpretative Decisions....................................................................................................................7 New ATO Interpretative Decisions ........................................................................................................7 Withdrawn ATO Interpretative Decisions...............................................................................................8

Case Update ............................................................................................................................................9 Media Releases: Treasury Ministers and ATO.......................................................................................10 Speeches: Treasury, Treasury Ministers and ATO.................................................................................12 Other Developments ..............................................................................................................................13 Ju ne Hot Topic: 2012/13 Federal Budget ...............................................................................................14

© Tax on the Couch: June 2012 1

Tax on the Couch – June 2012

Legislative Update Bills of interest currently before Parliament (as at 19 May 2012)

If you experience any problems with the Parliament’s website, go to http://www.aph.gov.au/Parliamentary_Business/Bills_Legislation#a1 and click on “Bills before Parliament”.

Budget related legislation currently before parliament Family Assistance and Other Legislation Amendment (Schoolkids Bonus Budget Measures) Bill 2012This Bill has passed all stages of Parliament without amendment and awaits Royal Assent. Introduced the day after the budget, it introduces the Budget 2012-2013 proposal to introduce the ‘Schoolkids bonus’ to be paid to eligible families (those generally in receipt of Family Tax Benefit A) in 2 instalments in January and July of each year form the 2013 income tax year.

The Schoolkids bonus payment will not require any receipts and eligible parents will receive $410 for each primary school child and $820 for each secondary school child. This will replace the Education Tax Refund from 1 January 2013.

As a transitional rule, the government will pay the 2012 Education tax Refund entitlements as a lump sum payment in June 2012. This should reflect entitlements to $409 for each primary school child and $818 for each secondary school child.

Tax Laws Amendment (Medicare Levy and Medicare Levy Surcharge) Bill 2012 Following on from the 2012/13 Budget announcements, this bill proposes to increase the Medicare Levy low-income thresholds for individuals and families for the 2012 income tax year.

Other Bills Paid Parental Leave and Other Legislation Amendment (Dad and Partner Pay and Other Measures) Bill 2012This Bill amends the Paid Parental Leave Act 2010 to: extend the Paid Parental Leave scheme to certain working fathers and partners so that they receive two weeks’ dad and partner pay at the rate of the national minimum wage; and clarify provisions relating to: ‘keeping in touch days’; debt recovery; notices; and delegation of the secretary’s powers; and the Fair Work Act 2009 to: clarify unpaid parental leave arrangements in the event of a stillbirth or infant death; enable early commencement of unpaid parental leave; and enable employees who are on unpaid parental leave to perform permissible paid work for short periods (‘keeping in touch days’); and five Acts to make amendments consequential on the dad and partner payment

Tax Laws Amendment (Shipping Reform) Bill 2012This Bill is part of a package of five bills in relation to the Australian shipping industry, the bill amends the: ITAA97 to provide for: a new category of exempt income for ship operators under certain circumstances; an accelerated depreciation of shipping vessels through a cap of 10 years to the effective life of those vessels; roll-over relief from income tax for eligible ship owners; a refundable tax offset for employers of Australian resident seafarers in certain circumstances; and the disclosure of tax information.

© Tax on the Couch: June 2012 2

http://www.aph.gov.au/Parliamentary_Business/Bills_Legislation/Bills_Search_Results/Result?bId=r4780

Tax on the Couch – June 2012

Superannuation Legislation Amendment (Trustee Obligations and Prudential Standards) Bill 2012This Bill amends the Superannuation Industry (Supervision) Act 1993 to: expand the duties for registrable superannuation entity (RSE) licensees; apply new trustee duties to RSE licensees of an RSE that offers a MySuper product; apply duties to the directors of corporate trustees; provide the Australian Prudential Regulation Authority with the power to issue prudential standards in relation to superannuation prudential matters; and make consequential amendments.

Tax and Superannuation Laws Amendment (2012 Measures No. 1) Bill 2012This Bill contains the following superannuation-related proposed amendments:

Disclosure of superannuation information – Schedule 5 permits the ATO to disclose details of an individual’s superannuation interests and benefits to a regulated super fund or public sector super scheme, an ADF, an RSA provider or their administrators (the bodies). This information will enable funds to assist their members to find and consolidate their superannuation interests. This measure is proposed to commence on Royal Assent.

Indexation of concessional contributions cap – Schedule 3 amends the ITAA 1997 to temporarily pause the indexation of the superannuation concessional contributions cap so that it will remain fixed at $25,000 up to and including the 2014 income year. This measure is proposed to take effect from 1 July 2013.

Refund of excess concessional contributions – Schedule 4 amends the ITAA 1997, the Superannuation (Government Co-contribution for Low Income Earners) Act 2003, the TAA 1953 and the Taxation (Interest on Overpayments and Early Payments) Act 1983 to allow eligible individuals to effectively have excess concessional contributions of $10,000 or less refunded to them. If the refund is accepted, the excess concessional contributions will be assessed as income for the year of the excess rather than paying excess contributions tax. These amendments are proposed to apply to excess concessional contributions of an eligible individual for the income year starting on 1 July 2011 and later years.

Payslip reporting – Schedule 6 amends the Superannuation Industry (Supervision) Act 1993 to require employers to report, on payslips, any information prescribed in the regulations about contributions. The regulations will in turn require employers to report the amount of contributions, and the date on which the employer expects to pay them. The regulations will also incorporate the existing requirements in Regulation 3.46 in the Fair Work Regulations 2009 to include the name, or name and number, of any fund to which the contribution is to be (or was) paid. These amendments are proposed to apply to contributions accrued after the date of Proclamation (or, if no proclamation date is set, 12 months after Royal Assent).

Tax Laws Amendment (2012 Measures No. 1) Bill 2012This Bill makes amendments to:

Ensure that expenses incurred in gaining or producing a rebatable benefit are not deductible;

Provide that complying superannuation entities cannot account for gains and losses on certain assets on revenue account using the trading stock exception;

Exempt from income tax ex-gratia payments to New Zealand non-protected special category visa holders for the floods that occurred in New South Wales and Queensland in early 2012; and

Commence the phase out of the dependent spouse tax offset by restricting eligibility for the offset to taxpayers with a dependent spouse born before 1 July 1952;

as well as technical amendments relating primarily to the minerals resource rent tax.

© Tax on the Couch: June 2012 3

http://www.aph.gov.au/Parliamentary_Business/Bills_Legislation/Bills_Search_Results/Result?bId=r4758

http://www.aph.gov.au/Parliamentary_Business/Bills_Legislation/Bills_Search_Results/Result?bId=r4758

Tax on the Couch – June 2012

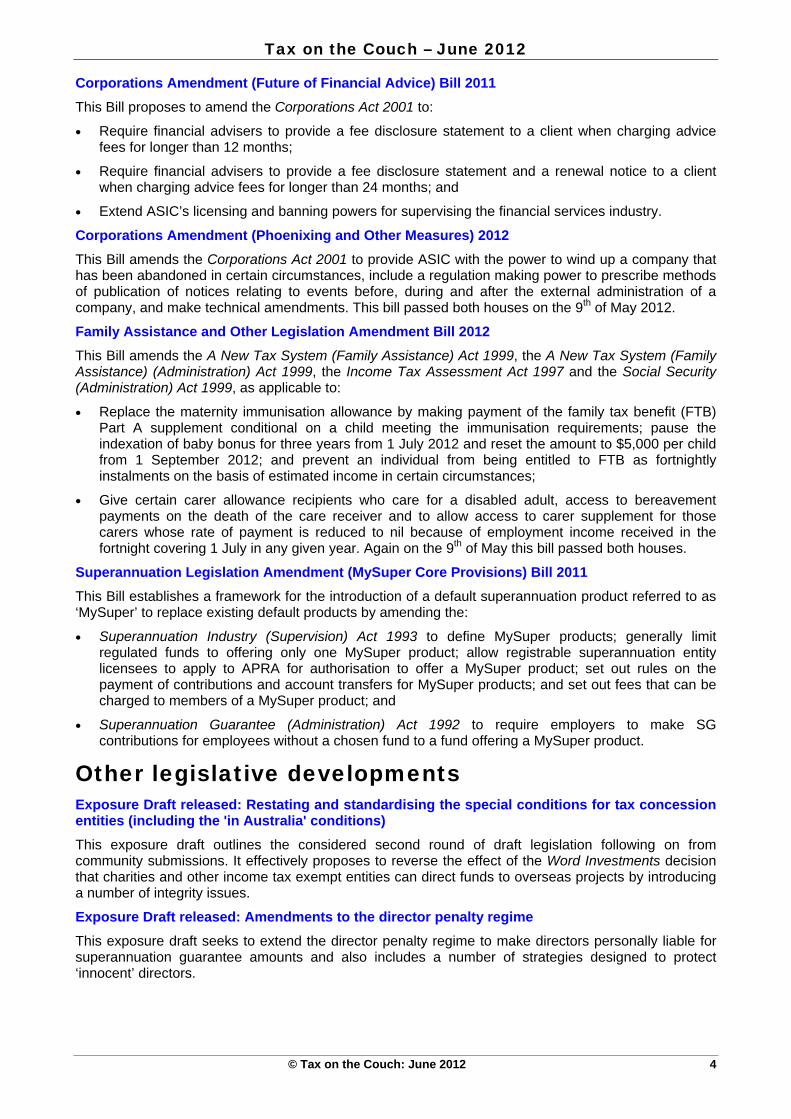

Corporations Amendment (Future of Financial Advice) Bill 2011This Bill proposes to amend the Corporations Act 2001 to:

Require financial advisers to provide a fee disclosure statement to a client when charging advice fees for longer than 12 months;

Require financial advisers to provide a fee disclosure statement and a renewal notice to a client when charging advice fees for longer than 24 months; and

Extend ASIC’s licensing and banning powers for supervising the financial services industry.

Corporations Amendment (Phoenixing and Other Measures) 2012 This Bill amends the Corporations Act 2001 to provide ASIC with the power to wind up a company that has been abandoned in certain circumstances, include a regulation making power to prescribe methods of publication of notices relating to events before, during and after the external administration of a company, and make technical amendments. This bill passed both houses on the 9th of May 2012.

Family Assistance and Other Legislation Amendment Bill 2012 This Bill amends the A New Tax System (Family Assistance) Act 1999, the A New Tax System (Family Assistance) (Administration) Act 1999, the Income Tax Assessment Act 1997 and the Social Security (Administration) Act 1999, as applicable to:

Replace the maternity immunisation allowance by making payment of the family tax benefit (FTB) Part A supplement conditional on a child meeting the immunisation requirements; pause the indexation of baby bonus for three years from 1 July 2012 and reset the amount to $5,000 per child from 1 September 2012; and prevent an individual from being entitled to FTB as fortnightly instalments on the basis of estimated income in certain circumstances;

Give certain carer allowance recipients who care for a disabled adult, access to bereavement payments on the death of the care receiver and to allow access to carer supplement for those carers whose rate of payment is reduced to nil because of employment income received in the fortnight covering 1 July in any given year. Again on the 9th of May this bill passed both houses.

Superannuation Legislation Amendment (MySuper Core Provisions) Bill 2011This Bill establishes a framework for the introduction of a default superannuation product referred to as ‘MySuper’ to replace existing default products by amending the:

Superannuation Industry (Supervision) Act 1993 to define MySuper products; generally limit regulated funds to offering only one MySuper product; allow registrable superannuation entity licensees to apply to APRA for authorisation to offer a MySuper product; set out rules on the payment of contributions and account transfers for MySuper products; and set out fees that can be charged to members of a MySuper product; and

Superannuation Guarantee (Administration) Act 1992 to require employers to make SG contributions for employees without a chosen fund to a fund offering a MySuper product.

Other legislative developments Exposure Draft released: Restating and standardising the special conditions for tax concession entities (including the 'in Australia' conditions)This exposure draft outlines the considered second round of draft legislation following on from community submissions. It effectively proposes to reverse the effect of the Word Investments decision that charities and other income tax exempt entities can direct funds to overseas projects by introducing a number of integrity issues.

Exposure Draft released: Amendments to the director penalty regimeThis exposure draft seeks to extend the director penalty regime to make directors personally liable for superannuation guarantee amounts and also includes a number of strategies designed to protect ‘innocent’ directors.

© Tax on the Couch: June 2012 4

http://www.aph.gov.au/Parliamentary_Business/Bills_Legislation/Bills_Search_Results/Result?bId=r4753

Tax on the Couch – June 2012

Exposure Draft released: Fringe Benefits Tax (FBT) Reform living-away-from-home benefitsThe long awaiting reforms for the ‘Living Away from home allowances’ has been released. The bill seeks to treat LAFHA as part of an employee’s assessable income rather than as fringe benefits. It will also ensure that eligible employees must maintain a home in Australia for their own personal use and enjoyment at all times while required to live away from home for their work.

If they are eligible, employees will be able to claim a deduction for reasonable food and accommodation expenses against these allowances for a maximum period of 12 months.

Where employees are not eligible to claim an income tax deduction for these expenses, the employer will pay FBT on these benefits.

The reforms will apply form 1 July 2012. Transitional rules apply to permanent residents who have employment arrangements for LAFH allowances and benefits in place prior to 7.30PM (AEST) on 8 May 2012. Such arrangements will be permitted to continue until 1 July 2014.

For temporary residents, only those who are maintaining a home in Australia and have employment arrangements for LAFH allowances and benefits prior to the budget announcements will be able to continue their arrangements under the transitional rules.

Rulings Update The following lists the Rulings, Determinations, Practice Statements and Interpretative Decisions (and other related documents) issued by the ATO between 16 April 2012 to 15 May 2012.

Rulings Class Rulings CR 2012/25 Income tax: Insurance Australia Group Limited - issue of

convertible preference shares 18 April 2012

CR 2012/26 Income tax: scrip for scrip: merger of Adamus Resources Limited and Endeavour Mining Corporation

24 April 2012

CR 2012/27 Income tax: early retirement scheme BlueScope Steel Limited 2 May 2012 CR 2012/28 Fringe benefits tax and income tax: employer contributions to the

WA Construction Industry Redundancy (No. 2) Fund 9 May 2012

CR 2012/29 Income tax: PAYG withholding: payments made by local government bodies in Queensland for the transfer of long service leave entitlements to other local government bodies and to Queensland government agencies

9 May 2012

CR 2012/30 Income tax: early retirement scheme - Ambulance Victoria 9 May 2012 CR 2012/31 Income tax: Australian Government Sport Training Grant Scheme

payments provided by the Australian Sports Commission 9 May 2012

Class Rulings – Notices CR 2012/25ER - Erratum

Income tax: Insurance Australia Group Limited - issue of convertible preference shares

9 May 2012

Goods and Services Tax Rulings – Notices GSTR 2002/6A3 - Addendum

Goods and services tax: exports of goods, items 1 to 4 of the table in subsection 38-185 (1) of the A New Tax System (Goods and Services Tax) Act 1999

18 April 2012

Miscellaneous Tax Rulings MT 2012/1 Miscellaneous taxes: application of the income tax and GST laws

to immediate transfer farm-out arrangements 18 April 2012

MT 2012/2 Miscellaneous taxes: application of the income tax and GST laws to deferred transfer farm-out arrangements

18 April 2012

MT 2012/3 Administrative penalties: voluntary disclosures 9 May 2012

© Tax on the Couch: June 2012 5

Tax on the Couch – June 2012

Product Rulings PR 2012/7 Income tax: tax consequences of changing the portfolio structure,

contributing to and partially redeeming an investment in a unit in the Perpetual WealthFocus Investment Advantage Fund

18 April 2012

PR 2012/8 Income tax: TFS Sandalwood Project 2012 2 May 2012 PR 2012/9 Income tax: National Viticulture Fund of Australia Project No. 4 (31

May 2005 Growers) 9 May 2012

PR 2012/10 Income tax: National Viticultural Fund of Australia Project No. 4 (1 July 2005 to 31 October 2005 Growers)

9 May 2012

PR 2012/11 Income tax: National Viticultural Fund of Australia Project No. 4 (1 November 2005 to 31 May 2006 Growers)

9 May 2012

PR 2012/12 Income tax: Heathcote Ridge Vineyard Project (May 2006 Growers)

9 May 2012

PR 2012/13 Income tax: Heathcote Ridge Vineyard Project (October 2006 Growers)

9 May 2012

PR 2012/14 Income tax: Heathcote Ridge Vineyard Project (May 2007 Growers)

9 May 2012

PR 2012/15 Income tax: AgriWealth 2012 Softwood Timber Project 9 May 2012

Taxation Rulings – Notices IT 2575W - Notice of Withdrawal

Income tax: Malaysian Government service pension - paragraph 18(2) Australia/Malaysia double taxation agreement

18 April 2012

IT 2665W - Notice of Withdrawal

Income tax: Swedish, Danish, Finnish, Dutch and Malaysian Government pensions paid to Australian residents

18 April 2012

TR 96/7 - Erratum Income tax: record keeping - section 262A - general principles 18 April 2012

Draft Rulings Draft Taxation Rulings TR 2012/D1 Income tax: meaning of 'income of the trust estate' in Division 6 of

Part III of the Income Tax Assessment Act 1936 and related provisions

28 March 2012

TR 2012/D3 Income tax: capital allowances: treatment of open pit mine site improvements

9 May 2012

Determinations Taxation Determinations – Notices TD 2008/29A1 - Addendum

Income tax: consolidation: capital gains: do the core consolidation rules in Division 701 of the Income Tax Assessment Act 1997 modify the effect of the CGT contract rules if an entity contracts to buy or sell a CGT asset and the contract settles after the entity becomes, or ceases to be, a member of a consolidated group?

24 April 2012

TD 2008/30A1 - Addendum

Income tax: consolidation: capital gains: for the purposes of Part 3-90 of the Income Tax Assessment Act 1997, is the CGT asset that an entity has contracted to buy from another taxpayer an asset of the entity at a time it joins or leaves a consolidated group, if the contract is not completed at that time?

24 April 2012

TD 2008/31A1 - Addendum

Income tax: consolidation: capital gains: for the purposes of Part 3-90 of the Income Tax Assessment Act 1997, is the CGT asset that an entity has contracted to sell to another taxpayer an asset of the entity at a time it joins or leaves a consolidated group, if the contract is not completed at that time?

24 April 2012

© Tax on the Couch: June 2012 6

Tax on the Couch – June 2012

Legislative Determinations Excise EXC 2012/2 Excise (Blending exemptions) Determination 2012 (No. 1) Dated this 12th day

of April 2012

Goods and Services Tax PAR 2012/1 A New Tax System (Goods and Services Tax) (Particular

Attribution Rules Where Supply or Acquisition Made Under a Contract Subject to Preconditions) Determination 2012

Dated: 12 April 2012

Income Tax Effective Life 2012/1

Income Tax (Effective Life of Depreciating Assets) Amendment Determination 2012 (No 1)

Dated this 3th day of May 2012

PAYG Variations and Notices Variation 34 Low income minors where no TFN or ABN provided Signed on 13 April 2012

ATO Interpretative Decisions New ATO Interpretative Decisions ATO ID 2012/29 Translation of foreign currency: when does a financial report

comply with the accounting standards under the Corporations Act 2001

20 April 2012

ATO ID 2012/30 Assessability of prize money derived by foreign resident horse trainer from a non treaty country

20 April 2012

ATO ID 2012/31 Thin Capitalisation: exemption - certain special purpose entities 27 April 2012 ATO ID 2012/32 Excess Contributions Tax: concessional contributions - reserves 4 May 2012 ATO ID 2012/33 Intra-group supply when an invoice is issued after recipient

leaves a GST group 4 May 2012

ATO ID 2012/34 Intra-group supply of services that is partly performed after the recipient leaves the GST group

4 May 2012

ATO ID 2012/35 Functional currency: requirement for a foreign resident to use the applicable functional currency to work out the amount of a capital gain or capital loss on indirect Australian real property interests.

4 May 2012

ATO ID 2012/36 Lease Document Expenses: deductibility when a property used partly for the production of assessable income

4 May 2012

ATO ID 2012/37 Division 250 - tax preferred use of an asset 4 May 2012 ATO ID 2012/38 Capital Allowances: depreciating assets - grant of indefeasible

right of use 4 May 2012

ATO ID 2012/39 Capital gains tax small business retirement exemption: deceased estate - choice by executor

4 May 2012

ATO ID 2012/40 Capital Allowances: hire purchase agreement - cost of the acquisition of the property

11 May 2012

ATO ID 2012/41 Consolidation: pre-joining history and TOFA balancing adjustment

11 May 2012

ATO ID 2012/42 Consolidation: inherited TOFA transitional balancing adjustment and cessation of financial arrangement

11 May 2012

ATO ID 2012/43 Consolidation: allocable cost amount and the TOFA transitional balancing adjustment

11 May 2012

ATO ID 2012/44 Assessments for the 2003-04 and earlier nil years: effect of transfer pricing determination on the period within which an original assessment can be made

11 May 2012

© Tax on the Couch: June 2012 7

Tax on the Couch – June 2012

Withdrawn ATO Interpretative Decisions ATO ID 2004/694 (Withdrawn)

GST and sale of land by Body Corporate in New South Wales 20 April 2012

ATO ID 2002/365 (Withdrawn)

CGT - Disposal of a trust asset to beneficiaries at less than market value

27 April 2012

ATO ID 2003/238 (Withdrawn)

CGT small business retirement exemption: deceased estate - choice by executor

4 May 2012

ATO ID 2007/11 (Withdrawn)

Capital Allowances: depreciating asset - composite asset - open-cut mine pit haulage road

9 May 2012

ATO ID 2007/12 (Withdrawn)

Capital Allowances: depreciating assets - open-cut mine benches, batters, berms and catchberms

9 May 2012

ATO ID 2007/13 (Withdrawn)

Capital Allowances: depreciating asset - composite asset - all open-cut mine pit haulage roads

9 May 2012

ATO ID 2007/14 (Withdrawn)

Depreciating Assets: composite item - open-cut mine pit 9 May 2012

© Tax on the Couch: June 2012 8

Tax on the Couch – June 2012

Case Update Mehta and Commissioner of Taxation [2012] AATA 208 (13 April 2012) The AAT held that a taxpayer was a share trader during the 2009 income tax year based on the relevant facts. This was despite evidence that suggested the taxpayer did not carry out activities such as charting or noting trend lines and cyclic performance of stocks but instead relied upon various sources of advice such as newspapers, investment magazines and stock market reports.

Wong and Commissioner of Taxation [2012] AATA 254 (27 April 2012)Another example of where the taxpayer was successful at the AAT with respect to arguing that they were a share trader. A number of issues were considered by the AAT in coming to this conclusion, including: the nature of the activities and whether they had a purpose of profit-making, the complexity and magnitude of the undertaking and if there was any intention to engage in trade regularly, routinely or systematically etc.

Sent v Commissioner of Taxation [2012] FCA 382 (16 April 2012)The Federal Court dismissed a taxpayer’s appeal and reversed a partially favourable decision of the AAT by including all of the $11.6 million worth of bonuses that had been converted into interests under an Employee Share Trust as assessable income on fundamentally, a constructive receipts argument. The 50% administrative penalties were also found to be suitable by the appellant court.

Phillips and Commissioner of Taxation [2012] AATA 219 (17 April 2012) The AAT held that a taxpayer did not pass the CGT small business maximum net asset value test for the purpose of a capital gain triggered when they sold shares to a related trust. Effectively a liability incurred in relation to a loan made to the family trust was secured by way or a mortgage over assets owned by another related company. The tribunal found that for a liability to be taken into account under the maximum net asset value test, a relationship must exist between the liabilities and assets of the entity in use rather than assets held by other connected entities.

Kelly v Commissioner of Taxation [2012] FCA 423 (27 April 2012)A taxpayer was partly successful in arguing that they had assigned their interest in a partnership to their own discretionary family trust and to a holding trust where they could adequately demonstrate the assignment. This required evidence of the intention of the parties, consideration paid for the assignment and written evidence according to the state laws governing the transfer of property. Certain attempts to assign partnerships interests under a ‘retirement deed’ were held to be ineffective as there was insufficient evidence of any transfer, a lack of consideration and comments made that an assignment can generally only be made by a continuing rather than retiring partner.

Lake Fox Limited and Commissioner of Taxation [2012] AATA 265 (4 May 2012)The AAT held that an employer paying for the private health insurance policy of one of its employees was subject to FBT as it was not an exempt benefit. The taxpayer had tried to argue that such a payment could be an exempt benefit under S 58M of the FBT Act which related to ‘work-related medical examinations, screenings, preventative health care or counselling’. The tribunal found that there was insufficient connection between the payment of the premium and these work-related exempt benefits.

© Tax on the Couch: June 2012 9

Tax on the Couch – June 2012

Media Releases: Treasury Ministers and ATO Deputy Prime Minister and Treasurer – The Honourable Wayne Swan MP

021 17/04/2012 Release of CEFC Expert Review

022 18/04/2012 IMF World Economic Outlook

023 18/04/2012 Government responds to the Final Report of the Advisory Panel on the Economic Potential of Senior Australians

024 18/04/2012 Implementing G20 commitment on OTC derivative reforms

025 20/04/2012 Treasurer to Attend G20, IMF and World Bank Meetings

026 20/04/2012 Statement by Australia, Singapore, Republic of Korea and the United Kingdom on IMF Resourcing

027 23/04/2012 GST Distribution Review Interim Report

028 24/04/2012 Consumer Price Index - March Quarter 2012

029 04/05/2012 Prime Minister to host Economic Forum

030 05/05/2012 Expansion of program to fight bowel cancer

031 06/05/2012 Tax relief for businesses in our patchwork economy

032 06/05/2012 New flood victims exempt from flood levy

033 08/05/2012 Keeping low-income earners exempt from Medicare Levy

034 08/05/2012 2012-13 Budget builds on growing record of tax reform

035 08/05/2012 Resourcing ASIC to continue strong market supervision

036 08/05/2012 A stronger economy for a fair Australia

037 08/05/2012 Helping households with the cost of living

038 08/05/2012 Spreading the benefits of the Boom

Assistant Treasurer – The Honourable David Bradbury MP

015 17/04/2012 Consultation on Restating and Standardising the Special Conditions for Tax Concession Entities

016 18/04/2012 Protecting Worker's Entitlements and Strengthening Director Obligations

017 18/04/2012 Exposure Draft Legislation for Changes to the Income Tax Law Affecting Consolidated Groups

018 24/04/2012 Inspector-General's review into the Australian Taxation Office's compliance approaches to small and medium enterprises and high wealth individuals

019 24/04/2012 $40 million in assets seized including Rolls Royces, yachts, a Lamborghini and an Aston Martin

020 30/04/2012 Exemption for financial advisers providing tax advice extended

© Tax on the Couch: June 2012 10

Tax on the Couch – June 2012

021 02/05/2012 GST treatment of Australian taxes, fees and charges - exposure draft regulations

022 06/05/2012 Tax relief for businesses in our patchwork economy

023 08/05/2012 Resourcing ASIC to continue strong market supervision

024 08/05/2012 Maintaining the Cross-Agency Approach to Preventing Abuse of Secrecy Jurisdictions (Project Wickenby) and Other Tax Compliance Measures

025 08/05/2012 2012-13 Budget builds on growing record of tax reform

026 10/05/2012 Decision on the applications for declaration of jet fuel infrastructure facilities servicing Sydney airport

027 15/05/2012 Ms Delia Rickard appointed as a full-time Deputy Chairperson of the Australian Competition and Consumer Commission

028 15/05/2012 Expert Roundtable to assist in clarifying the operation of the Income Tax General Anti-avoidance rule

029 15/05/2012 Reform of Living-Away-From-Home Allowances and Benefits - Draft Legislation Released for Consultation

ATO

17 Apr 2012 Free tax support to help Darwin small businesses take control of their tax Small business people in the Darwin region can keep on track with their tax and superannuation obligations with free and confidential one-on-one information sessions in the next month.

26 Apr 2012 $40 million in assets restrained, tax evasion and money laundering scheme dismantled As part of Project Wickenby, the Australian Federal Police has charged a man with conspiring to dishonestly cause a loss to the Australian Tax Office and conspiring to deal in the proceeds of crime to the value of $63 million, dismantling a multi-million dollar tax evasion and money laundering scheme.

30 Apr 2012 Latest taxation statistics now available Taxation statistics 2009-10 - the latest edition of the ATO's most comprehensive statistical publication is now available.

01 May 2012 ATO warns investors about tax avoidance schemes The ATO today warned taxpayers to steer clear of tax avoidance schemes as they prepare to lodge their 2012 tax returns.

03 May 2012 Second arrest for dealing in $63 million in proceeds of crime The Australian Federal Police (AFP) has today charged a second man with conspiring to dishonestly cause a loss to the Australian Tax Office (ATO) and conspiring to deal in the proceeds of crime to the value of $63 million as part of an ongoing Project Wickenby investigation.

15 May 2012 Free tax support to help Darwin small businesses take control of their tax Small business people in the Darwin region can keep on track with their tax and superannuation obligations with free and confidential one-on-one information sessions in the next month.

15 May 2012 Company directors sentenced under Project Wickenby The courts continue to send a strong message about their low tolerance for tax cheats by imposing significant jail terms.

© Tax on the Couch: June 2012 11

Tax on the Couch – June 2012

Speeches: Treasury, Treasury Ministers and ATO Deputy Prime Minister and Treasurer – The Honourable Wayne Swan MP

009 25/04/2012 Address to the Geebung RSL ANZAC Day Dawn Service, Brisbane

010 09/05/2012 'The Budget and the Fair Go in the Asian Century' - National Press Club Post-Budget Address, Canberra

011 11/05/2012 'Productivity: The Untold Story of Budget 2012' - Address to the CEDA Post-Budget Luncheon, Brisbane

012 14/05/2012 'The Fair Go Budget' - Address to the ACOSS Post-Budget Luncheon, Melbourne

013 15/05/2012 'Spreading the boom through our patchwork economy' - address to the NSW Business Chamber of Commerce, Sydney

Treasury

11-05-2012 A decade of Intergenerational Reports: Contributing to long term fiscal sustainability Dr David Gruen

© Tax on the Couch: June 2012 12

Tax on the Couch – June 2012

Other Developments Withdrawal of the ATO’s Trust Resettlement - Statement of Principles As a result of the decision in Federal Commissioner of Taxation v. Clark and Anor (Clark) [2011] FCAFC 5 and the High Courts refusal to grant the Commissioner leave to appeal that decision, the ATO’s Statement of Principles from August 2001 has been withdrawn.

The ‘Statement of Principles’ with the relevant withdrawal statement can be found at http://www.ato.gov.au/businesses/PrintFriendly.aspx?ms=businesses&doc=/content/14283.htmFor more information refer to the Decision Impact Statement of Clark’s case at http://law.ato.gov.au/atolaw/view.htm?DocID=LIT/ICD/QUD1of2010/00001&PiT=99991231235958 ATO compliance activities re SMEs: Tax Inspector-General's report released The audit activities and competency of the ATO with respect to its SME audits have been scrutinised by the Inspector general. The IG review can be found at http://www.igt.gov.au/content/reports.asp?NavID=9

ATO’s Litigation Statistics The ATO has released its publication Your case matters 2012 which features key data and analysis regarding tax and super litigation from 1 July 2007 to 29 February 2012. The ATO said these statistics had been published for the first time. The relevant document is at http://www.ato.gov.au/content/00318105.htm

Year-end tax planning

Fatma has discussed some interesting and topical ‘year-end’ tax planning leading up to 30 June 2012.

© Tax on the Couch: June 2012 13

Tax on the Couch – June 2012

June Hot Topic: 2012/13 Federal Budget Also see the NTAA’s 2012/13 Federal Budget Review at www.ntaa.com.au

Many of the announced changes discussed below can be found within the relevant budget papers at http://www.budget.gov.au/2012-13/content/bp2/html/bp2_revenue-09.htm

1. Changes effective Budget night – 7.30pm AEST 8 May 2012

FBT – further reform of living-away-from-home allowances and benefits The Government has announced it will further reform the tax concession for living-away-from-home (‘LAFH’) allowances and benefits by better targeting it at people who are legitimately maintaining a second home in addition to their actual home for an initial period. In particular, this measure will:

Limit access to the tax concession to employees who maintain a home for their own use in Australia, that they are living away from for work; and

Provide the tax concession for a maximum period of 12 months in respect of an individual employee, for any particular work location.

This measure builds on previously announced reforms which include taxing LAFH allowances in the hands of the recipient (i.e., the employee) rather than through the FBT system as is currently the case. The employee would then be entitled to claim a tax deduction for certain LAFH expenses they incur.

In particular, the Budget reforms aim to prevent employers from being able to give the tax concession to employees who are not maintaining a second home, or are maintaining two homes indefinitely.

However, the reforms will not apply to:

The tax concession for ‘fly-in fly-out’ arrangements, as these employees will not be subject to the 12 month time limit; or

The tax treatment of travel and meal allowances that are provided to employees who have to travel away from their usual place of work for short periods (generally up to 21 days).

For arrangements entered into after 7.30pm (AEST) on 8 May 2012, the reforms will apply from 1 July 2012. For arrangements entered into prior to that time with respect to permanent residents, the reforms will apply from 1 July 2014. Temporary residents will still be required to maintain a home in Australia if they wish to rely on the transitional rules for current arrangements.

For the Exposure draft released after the date of filming please see:

http://www.treasury.gov.au/ConsultationsandReviews/Submissions/2012/Fringe-Benefits-Tax-FBT-Reform-living-away-from-home-benefits

FBT – reform of airline transport fringe benefits An ‘airline transport fringe benefit’ may arise when an employee of an airline or travel agent is provided with free or discounted travel on a stand-by basis. Currently, the taxable value of an airline transport fringe benefit is calculated as follows:

the stand-by value of the benefit (for both domestic and international travel, the stand-by value is 37.5% of the lowest publicly advertised economy airfare charged for that particular route); less

any employee contribution.

This method was developed when stand-by travel was a feature of commercial airline pricing and staff could be displaced from a flight up to the time of boarding. However, the concept of stand-by travel is no longer commercially relevant as airlines now use discounted pricing to optimise passenger levels.

As a result, the Government will update the method of determining the taxable value of airline transport fringe benefits provided after 7.30pm (AEST) on 8 May 2012 from stand-by value to market value.

© Tax on the Couch: June 2012 14

Tax on the Couch – June 2012

Non-residents – removal of the 50% CGT discount The Government will remove eligibility for the 50% discount on capital gains accrued by non-residents on taxable Australian property such as real estate, after 7.30pm (AEST) on 8 May 2012.

However, non-residents will still be entitled to the CGT discount on capital gains accrued before this time, provided they choose to obtain a market valuation of assets as at 8 May 2012.

Non-residents – changes to personal income tax rates

The Government will adjust the personal income tax rates and thresholds that apply to the Australian sourced income of non-residents, as follows:

From 1 July 2012, the first two marginal tax rate thresholds will be merged into a single threshold, with all taxable income below $80,000 subject to tax at 32.5% (currently, taxable income from $0 to $37,000 is taxed at 29%, and taxable income from $37,001 to $80,000 is taxed at 30%); and

From 1 July 2015, the same marginal rate will rise from 32.5% to 33%.

Increase in managed investment trust final withholding tax rate The Government will increase the managed investment trust (‘MIT’) final withholding tax rate from 7.5% to 15%, with effect from 1 July 2012.

This measure will return the withholding tax for MITs to the original 2007 election commitment of 15%.

The Government believes this rate is competitive with current rates applying in other countries (e.g., Japan and the US at 15%) and is significantly lower than the 30% non-final withholding rate under the previous government. The 15% rate strikes the right balance between attracting foreign investment and ensuring Australia receives a fair return on profits to be made in Australia.

Medicare levy low-income thresholds The Government will increase the Medicare levy low-income thresholds to $19,404 for individuals and $32,743 for families for 2011/12 (up from $18,839 and $31,789 respectively for 2010/11).

The additional amount of threshold for each dependent child or student will also increase to $3,007 (up from $2,919 for 2010/11). The Medicare levy threshold for single pensioners below Age Pension age will increase to $30,451 for 2011/12 (up from $30,439 for 2010/11).

Superannuation – reduction of higher tax concession for contributions of high income earners The Government will reduce the tax concession received by people with income over $300,000 on their concessional contributions, so it is more in line with that received by average income earners.

From 1 July 2012, individuals with ‘income’ greater than $300,000 (i.e., those who pay tax at the top marginal rate of 45%, excluding the Medicare levy) will have their concessional contributions taxed at 30% and not at 15%.

The definition of ‘income’ for the purposes of this measure includes concessional contributions (including notional employer contributions for members of defined benefit funds). If an individual’s income excluding their concessional contributions is less than the $300,000 threshold, but the inclusion of their concessional contributions pushes them over the threshold, the 30% rate will only apply to the part of the contributions that is in excess of the threshold.

The 30% rate will not apply to concessional contributions which exceed the concessional contributions cap and are therefore subject to ‘excess contributions tax’ (as these contributions are effectively taxed at the top marginal tax rate).

© Tax on the Couch: June 2012 15

Tax on the Couch – June 2012

Changes to the Net Medical Expenses tax offset The Government will introduce a means test for the net medical expenses tax offset (‘NMETO’) from 1 July 2012. For taxpayers with adjusted taxable income (‘ATI’) above the Medicare levy surcharge thresholds (i.e., $84,000 for singles and $168,000 for couples or families in 2012/13):

the threshold above which a taxpayer may claim the NMETO will be increased to $5,000 (currently $2,000); and

the rate of the tax offset will be reduced to 10% (currently 20%) for eligible out of pocket expenses incurred.

Better targeting of ETP tax offset – crackdown on golden handshakes The Government will apply a ‘whole of income’ cap to tax concessions provided to the recipients of certain employment termination payments (‘ETPs’), which include ‘golden handshakes’.

Currently, the ETP tax offset can be used to reduce tax payable on payments included in remuneration packages such as ‘golden handshakes’ (up to the relevant ETP cap amount – e.g., $165,000 for 2011/12).

From 1 July 2012, only that part of an affected ETP (e.g., a ‘golden handshake’) that takes a person’s total annual taxable income (including the ETP) to no more than $180,000 will receive the ETP tax offset. Amounts above this ‘whole of income’ cap will be taxed at marginal rates. That is, the ‘whole of income’ cap will complement the existing ETP cap (i.e., $175,000 for 2012/13).

Existing arrangements will be retained for certain ETPs relating to genuine redundancy (including to those aged 65 and over), invalidity, compensation due to an employment related dispute and death.

Phasing out the Mature Age Worker tax offset From 1 July 2012, the Government will phase out the mature age worker tax offset (‘MAWTO’) for taxpayers born on or after 1 July 1957. Access to the MAWTO will be maintained for taxpayers who are aged 55 years or older in the 2011/12 year.

To help older Australians who wish to continue working, the Government will provide a Jobs Bonus of $1,000 to 10,000 employers who recruit and retain a worker aged 50 years or over for over three months.

Consolidating the dependency offsets into a single tax offset From 1 July 2012, eight existing dependency tax offsets will be consolidated into a single, streamlined and non-refundable offset that is only available to taxpayers who maintain a dependant who is genuinely unable to work due to disability or carer obligations.

The offsets to be consolidated are the invalid spouse, carer spouse, housekeeper, housekeeper (with child), child-housekeeper, child-housekeeper (with child), invalid relative and parent/parent in law tax offsets. The new consolidated offset will be based on the highest rate of the existing offsets it replaces.

Taxpayers who are currently eligible to claim more than one offset amount in respect of multiple dependants who are genuinely unable to work will still be able to do so.

Converting the Education Tax Refund into a new ‘School kids Bonus’ From the 2012/13 year, the Government will transform the Education Tax Refund into a ‘School kids Bonus’ that will automatically be paid to eligible families, through the family payments system, to provide timely assistance with the costs of educating their children. As a result of this reform, families will not have to wait until tax time to claim this concession, and will not have to keep receipts during the busy back-to-school period.

In particular, eligible families will receive the new School kids Bonus of $410 for each child in primary school and $820 for each child in high school. The bonus will be paid in two equal instalments in January and July each year, starting from January 2013.

As a transitional measure, the full Education Tax Refund for the 2011/12 year will be paid in June 2012.

© Tax on the Couch: June 2012 16

Tax on the Couch – June 2012

Company loss ‘carry-back’ tax relief The Government will provide tax relief for companies (and entities taxed like companies) by allowing them to ‘carry-back’ revenue tax losses so they receive a refund against tax previously paid, as follows:

For 2012/13 – Tax losses incurred in 2012/13 can be carried back and offset against tax paid in respect of the 2011/12 year only; and

For 2013/14 and later years – Tax losses can be carried back and offset against tax paid up to two years earlier.

Companies will be able to carry-back up to $1 million of revenue tax losses each year, providing a cash benefit of up to $300,000 a year (i.e., $1 million x 30% company tax rate).

The measure will be subject to integrity rules, and limited to a company’s franking account balance.

3. Other budget announcements

SMSF auditor registration The Government will provide $10.7 million to the Australian Securities and Investments Commission (‘ASIC’) to develop and maintain an online registration system for auditors of self-managed superannuation funds (‘SMSFs’). As part of the registration process, ASIC will develop a competency exam for SMSF auditors. ASIC will also be responsible for the deregistration of non-compliant auditors.

Auditors may begin to register with ASIC from 31 January 2013.

The Government will also provide $10.6 million to the ATO to police registered auditors, check their compliance with competency standards set by ASIC and refer auditors to ASIC, for enforcement action.

The cost of this measure will be offset by increases in the SMSF levy and fees charged by ASIC for sitting the competency exam.

Additional funding for compliance activities The Government has announced that it will provide the following levels of funding for the ATO’s compliance activities:

$195.3 million in 2014/15 and 2015/16 to continue a range of activities that promote voluntary GST compliance.

$76.8 million over three years (to the ATO and other Project Wickenby agencies) to continue the Government’s fight against tax evasion, avoidance and related crimes.

$106 million over four years to improve the management of outstanding taxation debts and superannuation guarantee charges.

4. Other measures previously announced, and proceeding

Changes to marginal income tax rates and thresholds – The following marginal tax rates were recently introduced from the 2012-13 year, as part of the Government’s household assistance package under the Clean Energy laws:

Marginal tax rates and thresholds 2011/12 2012/13 2015/16

Threshold Rate Threshold Rate Threshold Rate $6,001 15.0% $18,201 19.0% $19,401 19.0% $37,001 30.0% $37,001 32.5% $37,001 33.0% $80,001 37.0% $80,001 37.0% $80,001 37.0% $180,001 45.0% $180,001 45.0% $180,001 45.0%

© Tax on the Couch: June 2012 17

Tax on the Couch – June 2012

Low-income tax offset (‘LITO’) – From 1 July 2012, individuals will be entitled to receive the LITO if their taxable income is below $66,667. The maximum value of the LITO will be reduced from $1,500 to $445 and will be phased out at the rate of 1.5 cents (previously 4 cents) for every dollar of taxable income over $37,000. Together with the other changes, this will mean low-income earners will have an effective tax-free threshold of $20,542.

The phase-out arrangements for the LITO are summarised in the following table.

Low income tax offset 2011-12 From 1 July 2012 From 1 July 2015

Offset amount $1,500 $445 $300 Lower income limit $30,000 $37,000 $37,000 Upper income limit $67,500 $66,667 $67,000 Phase-out rate 4.0% 1.5% 1.0%

This is the rate at which an individual’s entitlement to LITO reduces for every dollar of taxable income over the lower income limit, and cuts out if taxable income reaches the upper income limit. Eg, if taxable income is $40,000 for the 2011/12 year, their entitlement to the maximum offset of $1,500 will be reduced by $400 (i.e., the reduction amount = ($40,000-$30,000) x 4% = $400) to $1,100 (i.e., $1,500 - $400).

Replacement of the Entrepreneurs Tax Offset with better incentives for small business – The Government will replace the Entrepreneurs Tax Offset with simpler and supposedly more effective measures (e.g., simplified depreciation measures below).

Simplified depreciation measures – The Government will simplify tax for small businesses by:

allowing small businesses to instantly write off each and every business asset costing less than $6,500 that is purchased from 1 July 2012;

replacing the two depreciation pools that currently exist, with a single depreciation pool; and

introducing an immediate deduction for the first $5,000 of the cost of a motor vehicle purchased from 1 July 2012.

Increasing the Superannuation Guarantee (‘SG’) rate from 9% to 12% The Government will boost retirement savings, by progressively increasing the rate of the SG from 9% to 12% progressively over the next few years, starting at an initial increase to 9.5% from 1 July 2013.

Increase in the Superannuation Guarantee age limit – The Government has removed the age limit for the superannuation guarantee.

5. Other measures previously announced but deferred

Superannuation – deferral of higher concessional contributions cap The Government will defer the start date of the measure to increase, by $25,000, the concessional contributions cap for individuals over age 50 with superannuation balances below $500,000 from 1 July 2012 to 1 July 2014. The two-year deferral means that, for 2012/13 and 2013/14, the concessional contributions cap will be $25,000 per year for all individuals, regardless of their age.

In 2014/15, the general cap is likely to increase to $30,000 through indexation, and the higher cap would then commence at $55,000.

© Tax on the Couch: June 2012 18

Tax on the Couch – June 2012

Taxation agent services regime – financial advice exemption The Government has extended the financial advisers exemption from compliance with the Tax Agent Services Act 2009 up until and including 30 June 2013, to allow for the details of the regulatory model to be settled and help resolve implementation issues associated with bringing financial planners under the scope of the Tax Agent Services regime.

6. Other measures previously announced, but not proceeding

Company tax cut not proceeding The Government will not proceed with the measure to lower the company tax rate from the 2013/14 year, nor implement an early start to the company tax rate cut for small businesses from the 2012/13 year.

50% tax discount for interest income not proceeding The Government will not proceed with the 2010/11 Budget measure to introduce a 50% discount for interest income, which was due to commence on 1 July 2013.

Standard deduction not proceeding The Government will not proceed with the 2010/11 Budget measure to introduce a standard deduction for work related expenses and the cost of managing tax affairs, which was due to start on 1 July 2013.

© Tax on the Couch: June 2012 19