Tax Deduction at Source

62

Tax Deduction at Source Tax Deduction at Source

-

Upload

pallavisweet -

Category

Documents

-

view

35 -

download

1

Transcript of Tax Deduction at Source

Tax Deduction at Source Tax Deduction at Source

Tax Deduction At SourceTax Deduction At Source

MEANING:-MEANING:-

Person responsible for making payment of Person responsible for making payment of certain income of the income earners deduct certain income of the income earners deduct income tax at the prescribed rates on such income tax at the prescribed rates on such incomes before payment is made to them.incomes before payment is made to them.

The amount so deducted at source shall be The amount so deducted at source shall be deposited by the deductor in the deposited by the deductor in the Government Treasury within the prescribed Government Treasury within the prescribed time limit. time limit.

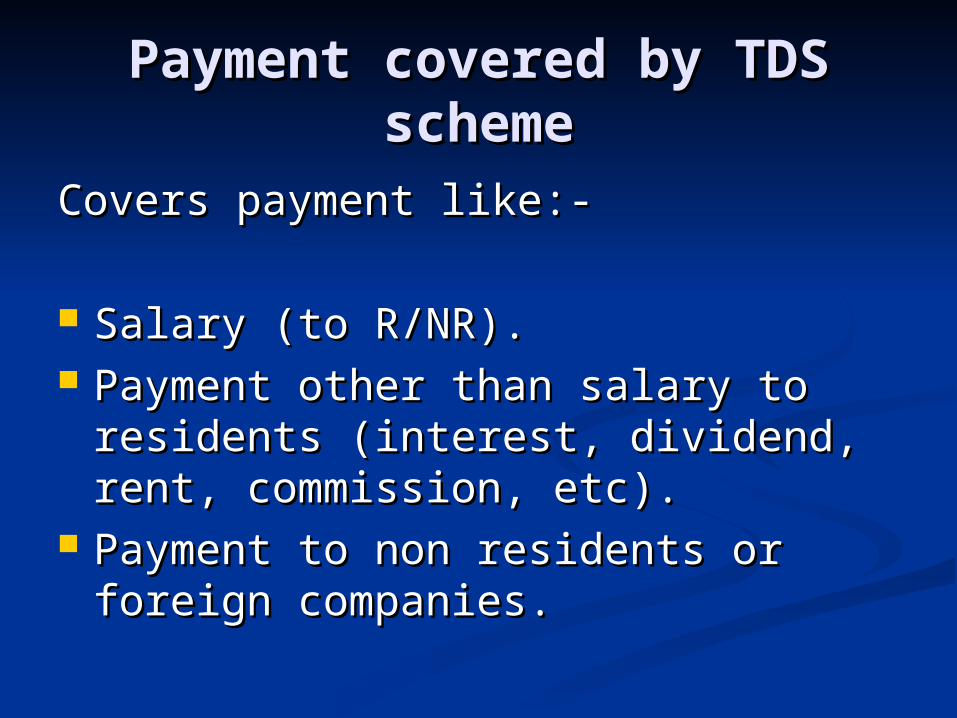

Payment covered by TDS Payment covered by TDS schemescheme

Covers payment like:-Covers payment like:-

Salary (to R/NR).Salary (to R/NR). Payment other than salary to Payment other than salary to

residents (interest, dividend, rent, residents (interest, dividend, rent, commission, etc).commission, etc).

Payment to non residents or foreign Payment to non residents or foreign companies.companies.

Salaries (Sec.192)Salaries (Sec.192)

Compute the income from salary as Compute the income from salary as discussed under the head “Income discussed under the head “Income from salaries”.from salaries”.

From such salary allow the From such salary allow the deductions u/s. 80C, 80CCC, 80CCD, deductions u/s. 80C, 80CCC, 80CCD, 80D, 80DD, 80E, 80GG and 80U.80D, 80DD, 80E, 80GG and 80U.

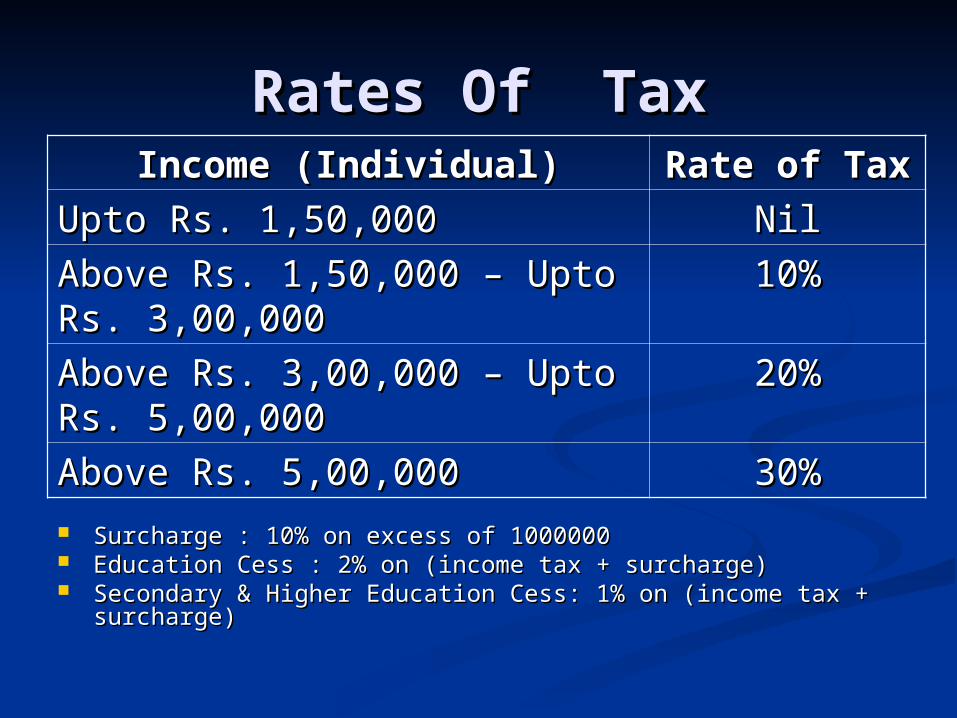

Rates Of TaxRates Of Tax

Surcharge : 10% on excess of 1000000 Surcharge : 10% on excess of 1000000 Education Cess : 2% on (income tax + surcharge)Education Cess : 2% on (income tax + surcharge) Secondary & Higher Education Cess: 1% on (income tax + Secondary & Higher Education Cess: 1% on (income tax +

surcharge)surcharge)

Income (Individual)Income (Individual) Rate of TaxRate of Tax

Upto Rs. 1,50,000Upto Rs. 1,50,000 NilNil

Above Rs. 1,50,000 – Upto Rs. Above Rs. 1,50,000 – Upto Rs. 3,00,0003,00,000

10%10%

Above Rs. 3,00,000 – Upto Rs. Above Rs. 3,00,000 – Upto Rs. 5,00,0005,00,000

20%20%

Above Rs. 5,00,000Above Rs. 5,00,000 30%30%

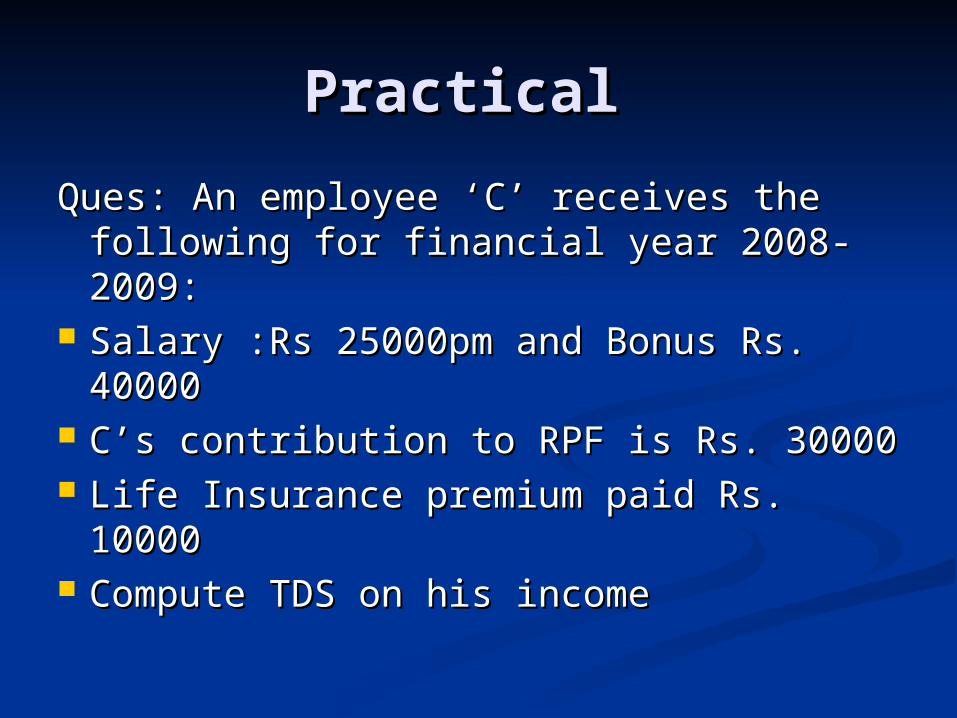

Practical Practical

Ques: An employee ‘C’ receives the Ques: An employee ‘C’ receives the following for financial year 2008-following for financial year 2008-2009:2009:

Salary :Rs 25000pm and Bonus Rs. Salary :Rs 25000pm and Bonus Rs. 4000040000

C’s contribution to RPF is Rs. 30000 C’s contribution to RPF is Rs. 30000 Life Insurance premium paid Rs. Life Insurance premium paid Rs.

1000010000 Compute TDS on his incomeCompute TDS on his income

Solution Solution Computation of salary income and TDS for the assessment year Computation of salary income and TDS for the assessment year

2009-2010 2009-2010 Rs.Rs.

Salary(25000*12) and bonusSalary(25000*12) and bonus = 340000= 340000Savings u/s 80C:Savings u/s 80C:L.I premium L.I premium 10000 10000Contri to RPF 30000Contri to RPF 30000 (40000)(40000)Salary Income Liable to TDS 300000Salary Income Liable to TDS 300000

Tax on Rs. 300000Tax on Rs. 300000Upto Rs. 1,50,000 Upto Rs. 1,50,000 Nil NilAbove Rs.1,50,000 – Upto Rs.3,00,000Above Rs.1,50,000 – Upto Rs.3,00,000 10% 15000 10% 15000 Add Surcharge Add Surcharge Nil Nil Add EC@2% 300Add EC@2% 300Add SHEC@1% 150Add SHEC@1% 150 Tax deductible at source 15450Tax deductible at source 15450

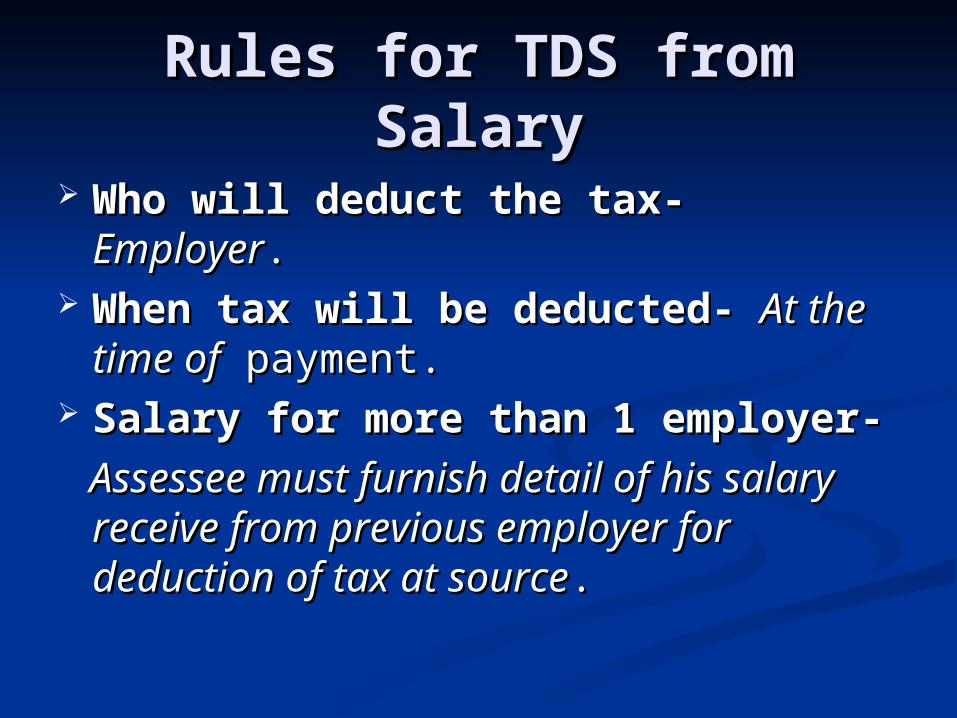

Rules for TDS from Rules for TDS from SalarySalary

Who will deduct the tax-Who will deduct the tax- EmployerEmployer.. When tax will be deducted-When tax will be deducted- At the At the

time oftime of payment. payment. Salary for more than 1 employer-Salary for more than 1 employer-

Assessee must furnish detail of his Assessee must furnish detail of his salary receive from previous employer salary receive from previous employer for deduction of tax at sourcefor deduction of tax at source. .

Rules Cont…Rules Cont…

Income from any other head-Income from any other head-

• An employee can furnish detail of this An employee can furnish detail of this other income to his employerother income to his employer

• Employer can deduct tax at source Employer can deduct tax at source from such incomes also.from such incomes also.

• Assessee cannot claim set-off any loss Assessee cannot claim set-off any loss from salary income except loss under from salary income except loss under the head “Income from House the head “Income from House Property”.Property”.

Rules Cont…Rules Cont…

Payment of salary in Foreign Payment of salary in Foreign currency-currency-

For the purpose of TDS on salary For the purpose of TDS on salary payable in foreign currency the payable in foreign currency the value in rupees of such salary shall value in rupees of such salary shall be calculated at the prescribed rate be calculated at the prescribed rate of exchange.of exchange.

Rules Cont…Rules Cont…

Tax on Perks paid by employers-Tax on Perks paid by employers-

• The employer has being given the The employer has being given the option to pay tax on income by way option to pay tax on income by way of perquisites (not provided by the of perquisites (not provided by the way of monetary payments).way of monetary payments).

• Such amount paid by employer shall Such amount paid by employer shall be deemed to have being paid by the be deemed to have being paid by the assessee.assessee.

Rules Cont…Rules Cont… Relief U/S 89(1)- Relief U/S 89(1)-

• If employee furnishes information in form no. 10E If employee furnishes information in form no. 10E to the employer relief u/s 89 should be given to the to the employer relief u/s 89 should be given to the concerned employee while deducting TDS u/s 192concerned employee while deducting TDS u/s 192..

• This facility is available for employees of:-This facility is available for employees of:-• government organization or company, government organization or company, • corporative society, corporative society, • local authority, local authority, • university, university, • institution, institution, • association or bodyassociation or body..

Rules Cont…Rules Cont…

Deposit of tax-Deposit of tax-

• Person responsible for paying the Person responsible for paying the salary is required to pay TDS as salary is required to pay TDS as under-under-

• Where deduction is made by or on behalf of Where deduction is made by or on behalf of Government- on same day.Government- on same day.

• In other case- within one week of the last day of In other case- within one week of the last day of the month in which deduction is made.the month in which deduction is made.

Rules Cont…Rules Cont…

Furnishing statement-Furnishing statement-

• Person responsible for paying salary Person responsible for paying salary shall furnish to the person who shall furnish to the person who receives a salary a statement giving receives a salary a statement giving particulars of perquisites or profit in particulars of perquisites or profit in lieu of salary( in form 12BA).lieu of salary( in form 12BA).

Is it possible to get salary Is it possible to get salary without tax deduction or without tax deduction or with lower tax deduction?with lower tax deduction?

YES,YES, Employee can make an Employee can make an application in form no. 13 to the application in form no. 13 to the assessingassessing officer to get a certificate officer to get a certificate of lower tax deduction or no tax of lower tax deduction or no tax deduction.deduction.

Interest on securities Interest on securities Sec. 193Sec. 193

(a)(a) Any person responsible for paying Any person responsible for paying an interest on securities to a resident an interest on securities to a resident is required to deduct tax at source at is required to deduct tax at source at the rates in force on amount of the rates in force on amount of interest payable.interest payable.

(b)(b) The Tax is required to be deducted The Tax is required to be deducted at the time of credit of such income at the time of credit of such income to the payees account or at the time to the payees account or at the time of payment of interest on securities of payment of interest on securities whichever is earlier.whichever is earlier.

Interest on securities Interest on securities Sec. 193Sec. 193

RATE OF TAX:-RATE OF TAX:-a)a) If the recipient of interest is other than a If the recipient of interest is other than a

company:company: i) Securities issued by local authority or i) Securities issued by local authority or

statutory corporation-@10%+surcharge, if statutory corporation-@10%+surcharge, if any + education cess@2%+secondary and any + education cess@2%+secondary and higher education cess@1%;higher education cess@1%;

ii) Debentures issued by a company, where ii) Debentures issued by a company, where such debenture are listed in a recognised such debenture are listed in a recognised stock exchange in India-@10%+surcharge, stock exchange in India-@10%+surcharge, if any + education cess@2%+SHEC@1%;if any + education cess@2%+SHEC@1%;

iii)other securities-@20%+surcharge, if iii)other securities-@20%+surcharge, if any + education cess@2%+SHEC@1%.any + education cess@2%+SHEC@1%.

Interest on securities Interest on securities Sec. 193Sec. 193

b)If the recipient is a company:b)If the recipient is a company:

then it would be charged @20%then it would be charged @20%+surcharge, if any + education cess@2%+surcharge, if any + education cess@2%+SHEC@1%.+SHEC@1%.

TAX SHALL NOT BE DEDUCTED AT SOURCE TAX SHALL NOT BE DEDUCTED AT SOURCE FROM ANY INTEREST PAYABLE ON:-FROM ANY INTEREST PAYABLE ON:-

a)a) National Savings Certificates; orNational Savings Certificates; or

b)b) 8% Savings(Taxable)Bonds; or8% Savings(Taxable)Bonds; or

c)c) National Development Bonds; orNational Development Bonds; or

d)d) Any security of the central or state Any security of the central or state government.government.

Dividends Sec.194Dividends Sec.194(a)(a) The Principal Officer of the Indian The Principal Officer of the Indian

Company or a company, which has made Company or a company, which has made prescribed arrangements for declaration prescribed arrangements for declaration and payment of dividend in India is and payment of dividend in India is responsible for deducting tax at source responsible for deducting tax at source from dividend payable to a shareholder, from dividend payable to a shareholder, who is resident in India.who is resident in India.

(b) No tax is to be deducted at source u/s (b) No tax is to be deducted at source u/s 194 from Dividend payable to any 194 from Dividend payable to any individual shareholder if the dividend is individual shareholder if the dividend is paid by the company by an account payee paid by the company by an account payee cheque and the aggregate amount of cheque and the aggregate amount of dividend distributed/paid or likely to be dividend distributed/paid or likely to be distributed/paid during the financial year distributed/paid during the financial year does not exceed Rs.2,500/-.does not exceed Rs.2,500/-.

Dividends Sec.194Dividends Sec.194

(c) Dividend paid by domestic (c) Dividend paid by domestic companies u/s 115O are exempt companies u/s 115O are exempt from tax in the hands of the from tax in the hands of the recipients’ w.e.f. April 1, 2003.recipients’ w.e.f. April 1, 2003.

d)The rate of TDS on dividends are d)The rate of TDS on dividends are @ 20%+ surcharge, if any+ @ 20%+ surcharge, if any+ education cess@2%+SHEC@1%education cess@2%+SHEC@1%

INTEREST OTHER THAN INTEREST OTHER THAN ‘INTEREST ON SECURITIES’ Sec. ‘INTEREST ON SECURITIES’ Sec.

194A194A

Who will deduct the tax at sourceWho will deduct the tax at source

- An Individual or HUF, who is required An Individual or HUF, who is required to get his accounts audited u/s 44ABto get his accounts audited u/s 44AB

- A Company, firm, co-operative society, A Company, firm, co-operative society, local authority, AOP or BOI etc.local authority, AOP or BOI etc.

Payment made to whom: a resident of Payment made to whom: a resident of India.India.

RATE OF TAX:RATE OF TAX: 1.) Domestic Company:1.) Domestic Company:

@ 20% + Surcharge @ 10% + E.C. @ @ 20% + Surcharge @ 10% + E.C. @ 2%2%

2.)Other residents in India:2.)Other residents in India:

@ 10% + Surcharge, if any +E.C. @ 2 @ 10% + Surcharge, if any +E.C. @ 2 %%

Illustration Illustration

(Q) Calculate the amount of tax (Q) Calculate the amount of tax deducted at source from the deducted at source from the following incomes during the F.Y. following incomes during the F.Y. 2008-09.2008-09.

a.) Interest on unlisted debentures of a.) Interest on unlisted debentures of Y Ltd. Payable to T, a resident in Y Ltd. Payable to T, a resident in India Rs. 10,000.India Rs. 10,000.

b.) Interest on Delhi Govt. Securities b.) Interest on Delhi Govt. Securities payable to Mr. Z, a resident in India payable to Mr. Z, a resident in India Rs. 20,000.Rs. 20,000.

Income from Interest on Securities Income from Interest on Securities (listed)(listed)

Rs. 6,000.Rs. 6,000.

WINNINGS FROM LOTTERY OR WINNINGS FROM LOTTERY OR CROSSWORD PUZZLES ETC. Sec. CROSSWORD PUZZLES ETC. Sec.

194B194B

Who is the recipent : any personWho is the recipent : any person Payment covered: Winnings from Payment covered: Winnings from

lotteries/ crosswords puzzles/ card lotteries/ crosswords puzzles/ card games/ other games.games/ other games.

Max. amount which can be paid Max. amount which can be paid without tax deduction: if the amount without tax deduction: if the amount of payment is Rs. 5,000 or less than of payment is Rs. 5,000 or less than Rs. 5,000.Rs. 5,000.

Rate of tax deduction at source: 30%Rate of tax deduction at source: 30%

Illustration Illustration

During the F.Y. 2008-09 find out the During the F.Y. 2008-09 find out the tax to be deducted at source in the tax to be deducted at source in the following cases:following cases:

a.) payment regarding lottery a.) payment regarding lottery winnings Rs. 500winnings Rs. 500

b.) Lottery winnings of Rs. 1,00,000 b.) Lottery winnings of Rs. 1,00,000 payable to Mr.X , resident in India.payable to Mr.X , resident in India.

Winning From Winning From Horse RaceHorse Race

Tax will be deducted at source by bookmakers and Tax will be deducted at source by bookmakers and race clubs from winning from horse races, whenrace clubs from winning from horse races, when

The payment exceeds Rs 2500The payment exceeds Rs 2500The prescribed rate for deducting tax during the The prescribed rate for deducting tax during the previous year 2008-09 is 30% plus surcharge if anyprevious year 2008-09 is 30% plus surcharge if anyPlus education cess @3% in case of all assessee.Plus education cess @3% in case of all assessee.

Winning from lottery or crossword Winning from lottery or crossword puzzlespuzzles

Tax will be deducted if the amount exceeds Tax will be deducted if the amount exceeds byby

Rs 5000Rs 5000 The prescribed rate for deducting tax during the The prescribed rate for deducting tax during the

previous year 2008-09 is 30% plus surcharge if anyprevious year 2008-09 is 30% plus surcharge if any Plus education cess @3% in case of all assessee.Plus education cess @3% in case of all assessee.

Winning from lotteryWinning from lottery

Important points to be rememberImportant points to be remember

When the price is given partly in cash and partly in kind, When the price is given partly in cash and partly in kind, then income tax will be deducted with reference to the then income tax will be deducted with reference to the aggregate amount of the cash prize and the value of the aggregate amount of the cash prize and the value of the prize in kind. If the part in cash is not sufficient to meet the prize in kind. If the part in cash is not sufficient to meet the liability of deduction of tax in respect of the whole of the liability of deduction of tax in respect of the whole of the winning, the person responsible for paying shall before winning, the person responsible for paying shall before releasing the winning ensure that tax has been paidreleasing the winning ensure that tax has been paid

When the prize is given in installments, the tax will be When the prize is given in installments, the tax will be deducted only at the time of actual payment of each deducted only at the time of actual payment of each installments ie not in the lump sum in the end but at each installments ie not in the lump sum in the end but at each interval of installments.interval of installments.

Income tax is not deductible from the income by way of Income tax is not deductible from the income by way of bonus or commission paid to lottery agent or sellers of bonus or commission paid to lottery agent or sellers of lottery tickets on the sale made by them.lottery tickets on the sale made by them.

Payment to contractors and Payment to contractors and sub contractorssub contractors

Tax will be deducted at source if the sum exceeds Rs 20,000.Tax will be deducted at source if the sum exceeds Rs 20,000. and further where the aggregate of amount exceeds Rs. and further where the aggregate of amount exceeds Rs.

50,000.50,000. Everyone except an individual or HUF shall not deduct tax at Everyone except an individual or HUF shall not deduct tax at

source where such sum is made or credited to the contractor source where such sum is made or credited to the contractor exclusively for personal purposes of such individual or any exclusively for personal purposes of such individual or any member of HUF.member of HUF.

The authorities which will have to pay tax are:The authorities which will have to pay tax are:a)a) The central government or any state governmentThe central government or any state governmentb)b) Any local authorityAny local authorityc)c) Any statutory corporationAny statutory corporationd)d) Any companyAny companye)e) Any cooperative societyAny cooperative societyf)f) Any registered societyAny registered societyg)g) Any trustAny trusth)h) Any firmAny firmi)i) An individual or HUF who is required to get his accounts An individual or HUF who is required to get his accounts

audited under 44AB Actaudited under 44AB Act

Payment to contractors and Payment to contractors and sub contractorssub contractors

Rate of TDSRate of TDS When payee is a contractor, under sec 194CWhen payee is a contractor, under sec 194Ca)a) in case of advertising @1% plus surcharge, if any + in case of advertising @1% plus surcharge, if any +

education cess@3%education cess@3%b)b) In any other case @ 2%plus surcharge, if any + In any other case @ 2%plus surcharge, if any +

education cess @3%education cess @3% When payee is a sub contractor, under sec194 C2When payee is a sub contractor, under sec194 C2a)a) when payee is an individual or HUF contractor, who when payee is an individual or HUF contractor, who

is required to get his accounts audited under is required to get his accounts audited under sec40ABsec40AB

b)b) If sub contractor is resident, then the deduction is @ If sub contractor is resident, then the deduction is @ of 1% + surcharge, if any + education cess @ 3%of 1% + surcharge, if any + education cess @ 3%

Payment to contractors and Payment to contractors and sub contractorssub contractors

ExceptionsExceptions Tax will not be deducted during the Tax will not be deducted during the

course of business of plying, hiring course of business of plying, hiring or leasing good carriages, if such or leasing good carriages, if such contractor is an individual who has contractor is an individual who has not owned more than two carriages.not owned more than two carriages.

Insurance commissionInsurance commission

Tax will be deductedTax will be deducted If amount exceeds Rs 5000If amount exceeds Rs 5000 In case of person, resident of IndiaIn case of person, resident of Indiaa)a) 10% plus surcharge, if any10% plus surcharge, if any + education cess @3% + education cess @3% In case of domestic companyIn case of domestic companya)a) 20% plus surcharge, if any20% plus surcharge, if any +education cess @ 3%.+education cess @ 3%.

Section 194E – Payment to Non Section 194E – Payment to Non Resident Sportsman/Sports Resident Sportsman/Sports

AssociationAssociation (a) Any person responsible for paying any (a) Any person responsible for paying any income to a non resident sportsman including income to a non resident sportsman including an athlete who is not a Citizen of India or a an athlete who is not a Citizen of India or a non-resident Sports Association or Institution non-resident Sports Association or Institution is required to deduct tax at source.is required to deduct tax at source.

(b) The tax is required to be deducted at the (b) The tax is required to be deducted at the time of credit of such income to the account of time of credit of such income to the account of payee or at the time of payment in cash or by payee or at the time of payment in cash or by issue of cheque or draft or by any other mode issue of cheque or draft or by any other mode whichever is earlier.whichever is earlier.

Section 194EE – Payment in respect of Section 194EE – Payment in respect of deposits under Nationaldeposits under National

Savings SchemeSavings Scheme

(a) Any person responsible for paying to (a) Any person responsible for paying to any person any amount referred to in any person any amount referred to in Section 80CCA(2) is required to deduct Section 80CCA(2) is required to deduct Income Tax.Income Tax.

(b) No deduction is required to be made (b) No deduction is required to be made where the amount of such payment or the where the amount of such payment or the aggregate amount of such payments aggregate amount of such payments during the financial year is less than during the financial year is less than Rs.2,500/-.Rs.2,500/-.

Section 194F – Payment on account of Section 194F – Payment on account of Repurchase of Units by MutualRepurchase of Units by Mutual

Funds or UTIFunds or UTI

Any person responsible for paying to Any person responsible for paying to any person any amount referred to any person any amount referred to in Section 80CCB(2) is required to in Section 80CCB(2) is required to deduct tax at source at the time of deduct tax at source at the time of payment without any exemption.payment without any exemption.

Section 194G – Commission Section 194G – Commission etc. on the sale of Lottery etc. on the sale of Lottery

TicketsTickets

Any person who is responsible for Any person who is responsible for paying commission, remuneration or paying commission, remuneration or prize to any person who is or has prize to any person who is or has been stocking, distributing, been stocking, distributing, purchasing or selling lottery tickets purchasing or selling lottery tickets is required to deduct tax at source is required to deduct tax at source on such tickets on an amount on such tickets on an amount exceeding Rs.1,000/-.exceeding Rs.1,000/-.

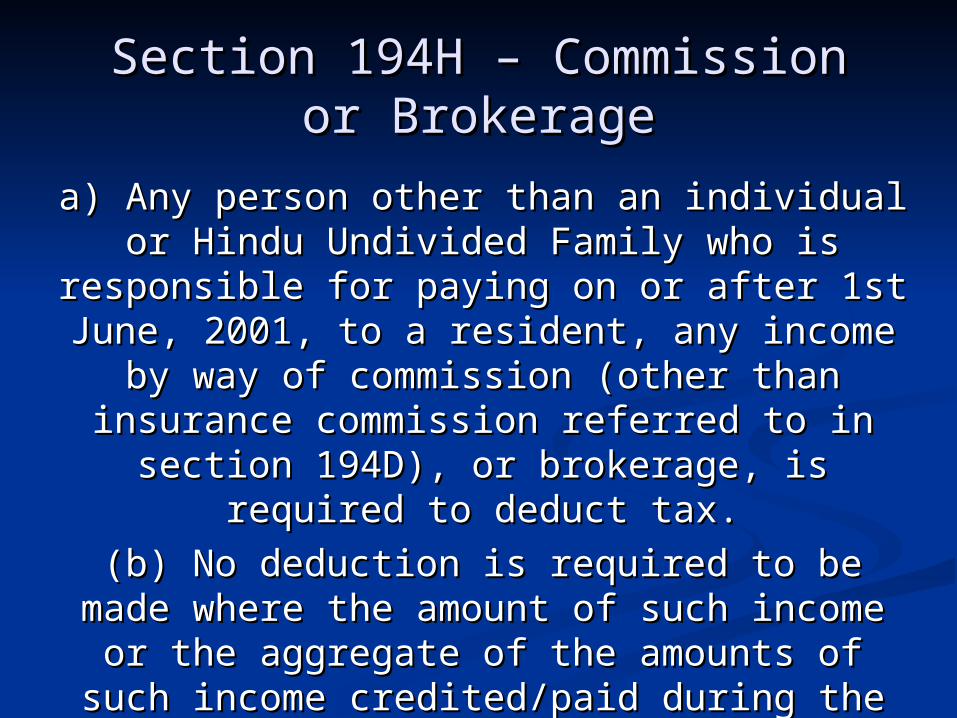

Section 194H – Commission or Section 194H – Commission or BrokerageBrokerage

a) Any person other than an individual or a) Any person other than an individual or Hindu Undivided Family who is responsible Hindu Undivided Family who is responsible for paying on or after 1st June, 2001, to a for paying on or after 1st June, 2001, to a

resident, any income by way of commission resident, any income by way of commission (other than insurance commission referred to (other than insurance commission referred to in section 194D), or brokerage, is required to in section 194D), or brokerage, is required to

deduct tax.deduct tax.

(b) No deduction is required to be made (b) No deduction is required to be made where the amount of such income or the where the amount of such income or the aggregate of the amounts of such income aggregate of the amounts of such income

credited/paid during thecredited/paid during the

financial year does not exceed Rs.2,500/-.financial year does not exceed Rs.2,500/-.

Section 194 I – RentSection 194 I – Rent

(a) Any person other than an individual (a) Any person other than an individual or Hindu Undivided Family responsible or Hindu Undivided Family responsible for paying rent to resident any income for paying rent to resident any income by way of rent is required to deduct taxby way of rent is required to deduct tax

a) 15% if the payee is individual or HUFa) 15% if the payee is individual or HUF

b) 20% in other cases.b) 20% in other cases.

This provision does not applicable if total This provision does not applicable if total rent not exceed Rs.1,20,000.rent not exceed Rs.1,20,000.

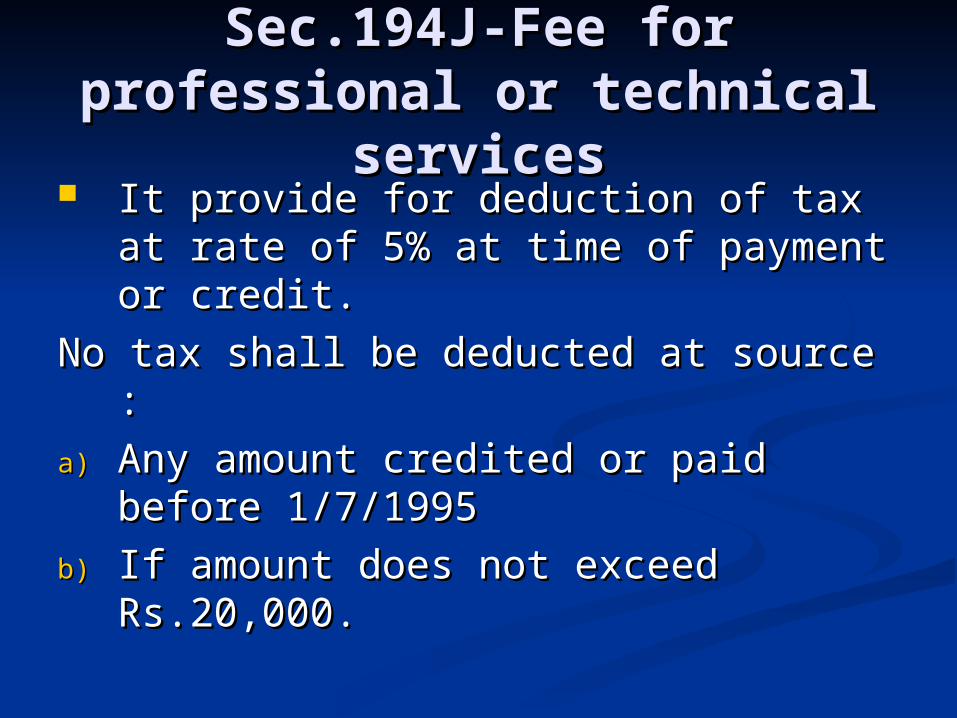

Sec.194J-Fee for Sec.194J-Fee for professional or technical professional or technical

servicesservices It provide for deduction of tax at It provide for deduction of tax at

rate of 5% at time of payment or rate of 5% at time of payment or credit.credit.

No tax shall be deducted at source :No tax shall be deducted at source :

a)a) Any amount credited or paid before Any amount credited or paid before 1/7/19951/7/1995

b)b) If amount does not exceed If amount does not exceed Rs.20,000.Rs.20,000.

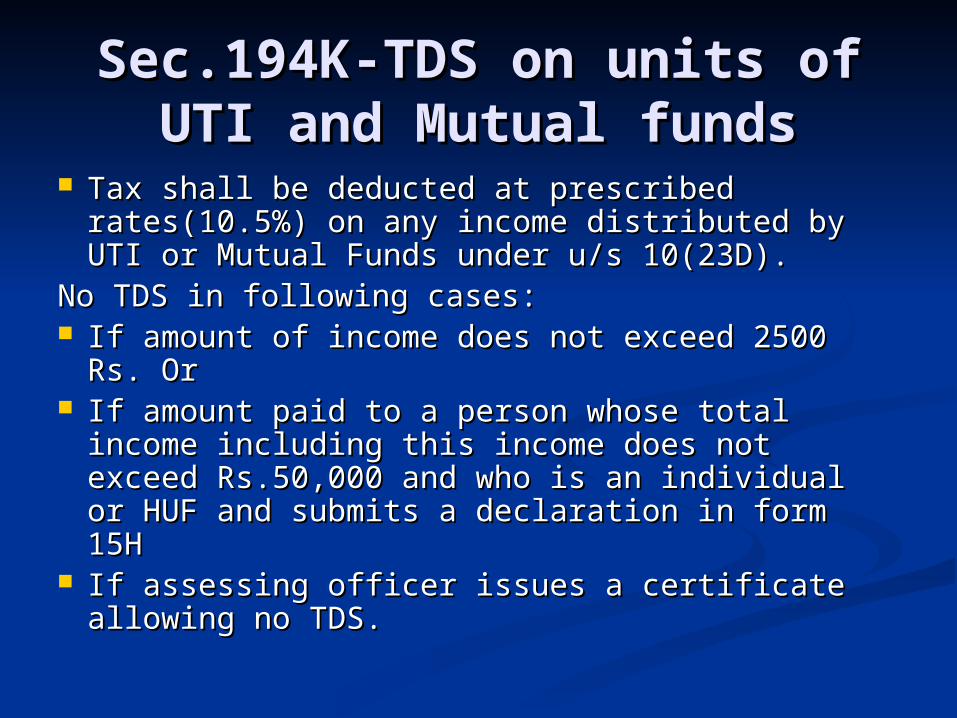

Sec.194K-TDS on units of Sec.194K-TDS on units of UTI and Mutual fundsUTI and Mutual funds

Tax shall be deducted at prescribed Tax shall be deducted at prescribed rates(10.5%) on any income distributed by UTI rates(10.5%) on any income distributed by UTI or Mutual Funds under u/s 10(23D).or Mutual Funds under u/s 10(23D).

No TDS in following cases:No TDS in following cases: If amount of income does not exceed 2500 Rs. If amount of income does not exceed 2500 Rs.

OrOr If amount paid to a person whose total income If amount paid to a person whose total income

including this income does not exceed including this income does not exceed Rs.50,000 and who is an individual or HUF Rs.50,000 and who is an individual or HUF and submits a declaration in form 15Hand submits a declaration in form 15H

If assessing officer issues a certificate allowing If assessing officer issues a certificate allowing no TDS.no TDS.

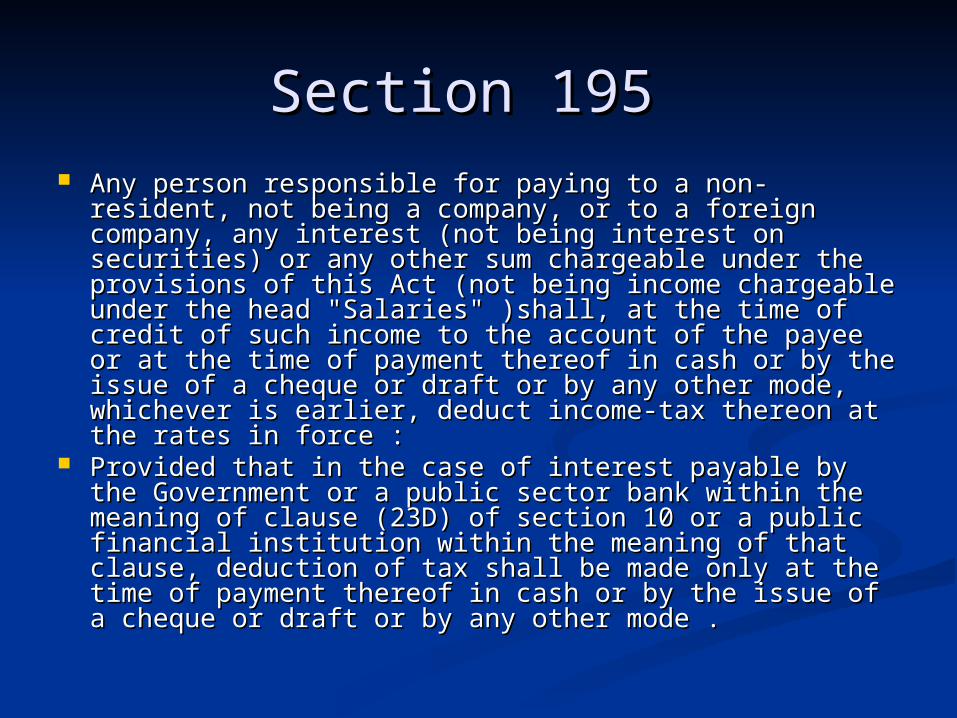

Section 195Section 195 Any person responsible for paying to a non-resident, Any person responsible for paying to a non-resident,

not being a company, or to a foreign company, any not being a company, or to a foreign company, any interest (not being interest on securities) or any other interest (not being interest on securities) or any other sum chargeable under the provisions of this Act (not sum chargeable under the provisions of this Act (not being income chargeable under the head being income chargeable under the head "Salaries" )shall, at the time of credit of such income to "Salaries" )shall, at the time of credit of such income to the account of the payee or at the time of payment the account of the payee or at the time of payment thereof in cash or by the issue of a cheque or draft or thereof in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, deduct by any other mode, whichever is earlier, deduct income-tax thereon at the rates in force : income-tax thereon at the rates in force :

Provided that in the case of interest payable by the Provided that in the case of interest payable by the Government or a public sector bank within the Government or a public sector bank within the meaning of clause (23D) of section 10 or a public meaning of clause (23D) of section 10 or a public financial institution within the meaning of that clause, financial institution within the meaning of that clause, deduction of tax shall be made only at the time of deduction of tax shall be made only at the time of payment thereof in cash or by the issue of a cheque or payment thereof in cash or by the issue of a cheque or draft or by any other mode . draft or by any other mode .

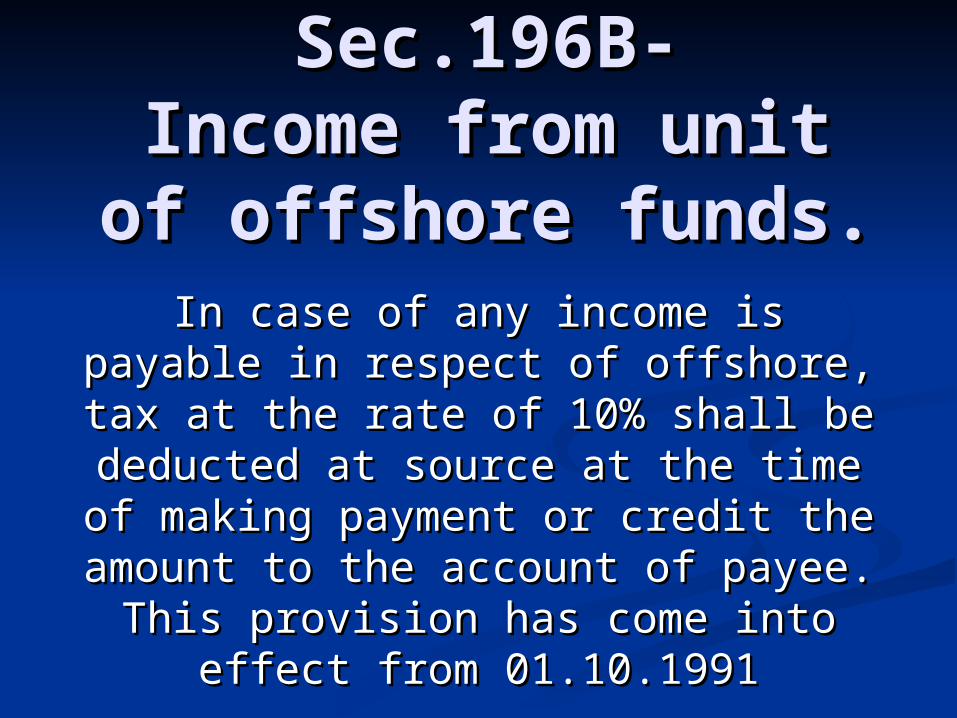

Sec.196B-Sec.196B-Income from unit Income from unit of offshore funds.of offshore funds.

In case of any income is payable in In case of any income is payable in respect of offshore, tax at the rate of respect of offshore, tax at the rate of 10% shall be deducted at source at 10% shall be deducted at source at

the time of making payment or credit the time of making payment or credit the amount to the account of payee. the amount to the account of payee. This provision has come into effect This provision has come into effect

from 01.10.1991from 01.10.1991

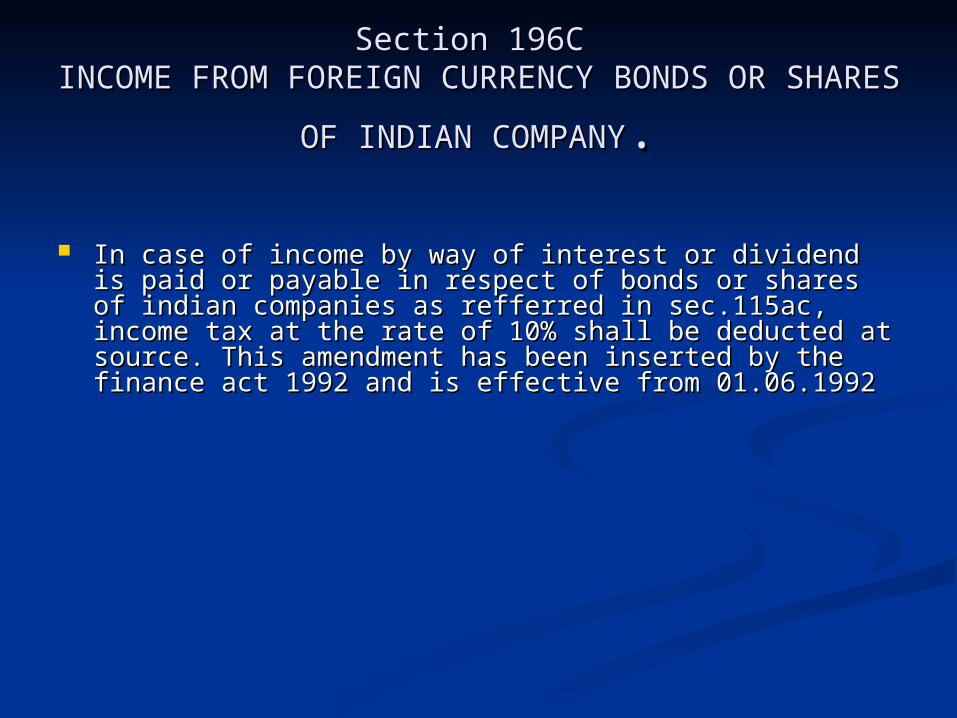

Section 196C Section 196C INCOME FROM FOREIGN CURRENCY BONDS OR INCOME FROM FOREIGN CURRENCY BONDS OR

SHARES OF INDIAN COMPANYSHARES OF INDIAN COMPANY..

In case of income by way of interest or dividend is paid or In case of income by way of interest or dividend is paid or payable in respect of bonds or shares of indian companies payable in respect of bonds or shares of indian companies as refferred in sec.115ac, income tax at the rate of 10% as refferred in sec.115ac, income tax at the rate of 10% shall be deducted at source. This amendment has been shall be deducted at source. This amendment has been inserted by the finance act 1992 and is effective from inserted by the finance act 1992 and is effective from 01.06.199201.06.1992

Section Section 196D 196D Income of Foreign Institutional Investors Income of Foreign Institutional Investors

from securitiesfrom securities.. (1) Where any income in respect of securities referred to in (1) Where any income in respect of securities referred to in clause (a) of sub-section (1) of clause (a) of sub-section (1) of section 115ADsection 115AD is payable to is payable to a Foreign Institutional Investor, the person responsible for a Foreign Institutional Investor, the person responsible for

making the payment shall, at the time of credit of such making the payment shall, at the time of credit of such income to the account of the payee or at the time of income to the account of the payee or at the time of

payment thereof in cash or by issue of a cheque or draft or payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax by any other mode, whichever is earlier, deduct income-tax

thereon at the rate of twenty per cent.thereon at the rate of twenty per cent.(2) No deduction of tax shall be made from any income, by (2) No deduction of tax shall be made from any income, by way of capital gains arising from the transfer of securities way of capital gains arising from the transfer of securities

referred to in referred to in section 115ADsection 115AD, payable to a Foreign , payable to a Foreign Institutional Investor.Institutional Investor.

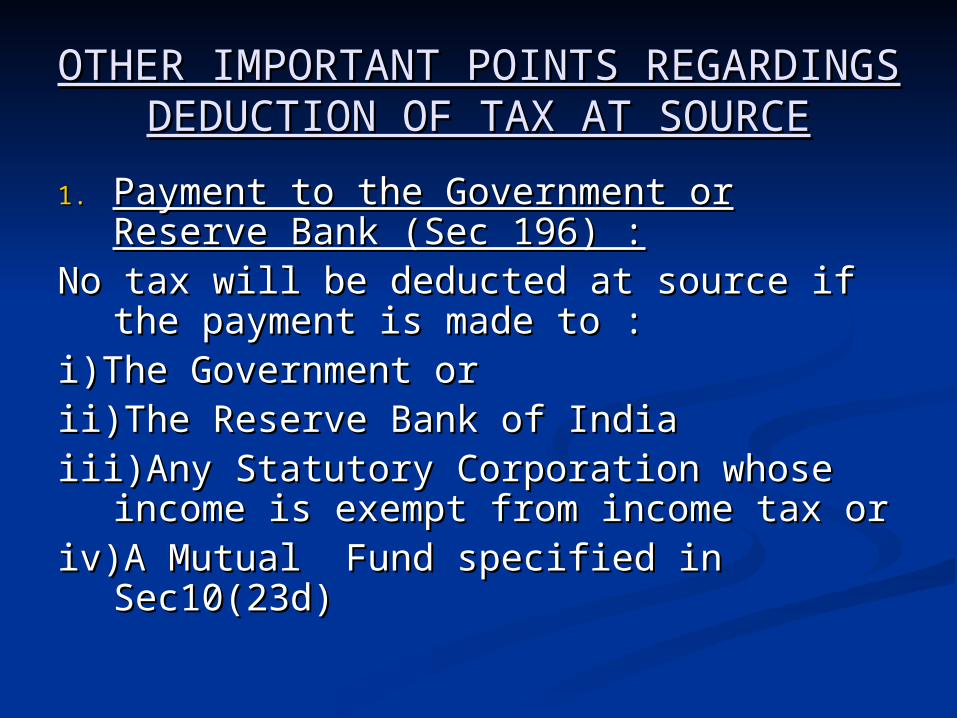

OTHER IMPORTANT POINTS OTHER IMPORTANT POINTS REGARDINGS DEDUCTION OF TAX REGARDINGS DEDUCTION OF TAX

AT SOURCEAT SOURCE1.1. Payment to the Government or Payment to the Government or

Reserve Bank (Sec 196) :Reserve Bank (Sec 196) :No tax will be deducted at source if the No tax will be deducted at source if the

payment is made to :payment is made to :i)The Government ori)The Government orii)The Reserve Bank of India ii)The Reserve Bank of India iii)Any Statutory Corporation whose iii)Any Statutory Corporation whose

income is exempt from income tax orincome is exempt from income tax oriv)A Mutual Fund specified in iv)A Mutual Fund specified in

Sec10(23d)Sec10(23d)

2.2. Tax deductionTax deduction at lower rate (Sec 197 at lower rate (Sec 197) :) :In case of any income of any person underIn case of any income of any person underSections 192 to 195 on an application beingSections 192 to 195 on an application beingmade by an assessee,the Assessing Officer,made by an assessee,the Assessing Officer,may if satisfied,issue a certificate that eithermay if satisfied,issue a certificate that eitherhis income is not taxable or taxable at lowerhis income is not taxable or taxable at lowerrate . In such a case the person making therate . In such a case the person making thepayment shall either not deduct tax at all or payment shall either not deduct tax at all or

deductdeductit at lower rate stated in the certificateit at lower rate stated in the certificate

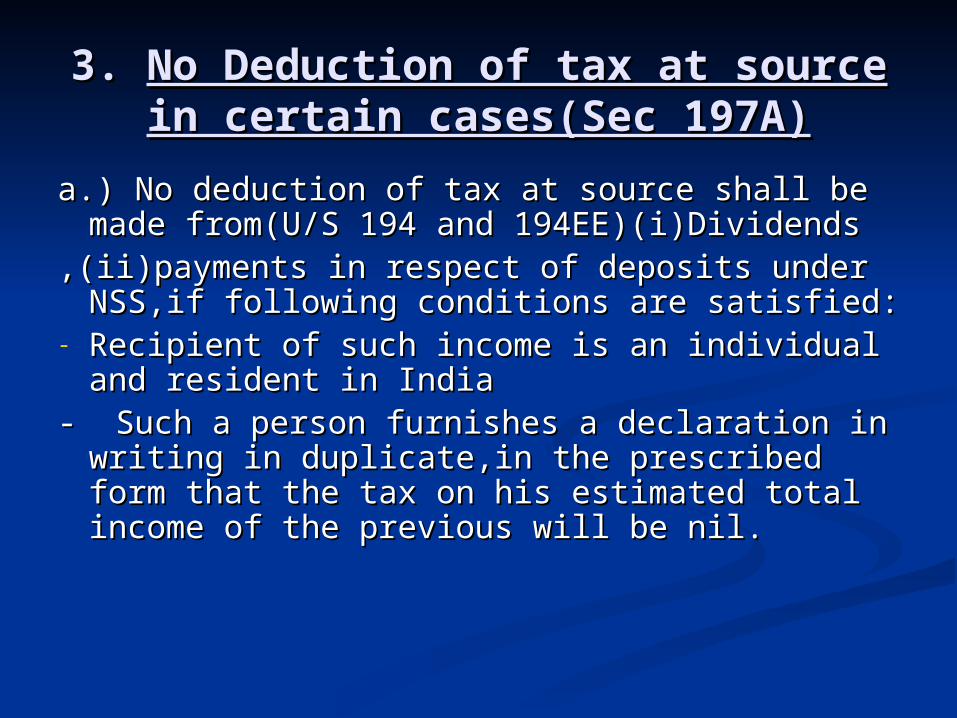

3. 3. No Deduction of tax at source in No Deduction of tax at source in certain cases(Sec 197A)certain cases(Sec 197A)

a.) No deduction of tax at source shall be a.) No deduction of tax at source shall be made from(U/S 194 and 194EE)made from(U/S 194 and 194EE)(i)Dividends(i)Dividends

,(ii)payments in respect of deposits under ,(ii)payments in respect of deposits under NSS,if following conditions are satisfied:NSS,if following conditions are satisfied:

- Recipient of such income is an individual Recipient of such income is an individual and resident in India and resident in India

- Such a person furnishes a declaration in - Such a person furnishes a declaration in writing in duplicate,in the prescribed form writing in duplicate,in the prescribed form that the tax on his estimated total income that the tax on his estimated total income of the previous will be nil.of the previous will be nil.

b) No deduction of tax at source shall be b) No deduction of tax at source shall be made from(U/S 193 and 194A) (i)interestmade from(U/S 193 and 194A) (i)interest

on securities ii)interest other than on securities ii)interest other than securities , if following conditions are securities , if following conditions are satisfied:satisfied:

- Recipient of such income is a person not Recipient of such income is a person not being a company or a firmbeing a company or a firm

- Such a person furnishes a declaration in - Such a person furnishes a declaration in writing in duplicate, in prescribed form writing in duplicate, in prescribed form that the tax on his estimated total income that the tax on his estimated total income of the previous year will be nil of the previous year will be nil

c.)If the income of a person is unconditionally exempt u/s c.)If the income of a person is unconditionally exempt u/s 10 and who is not required to file return of income u/s 10 and who is not required to file return of income u/s 139,there would be no requirement for TDS since the 139,there would be no requirement for TDS since the income is exemptincome is exempt

d.)No deduction of tax shall be made if the following d.)No deduction of tax shall be made if the following conditions are satisfied:conditions are satisfied:

- The assessee is an individual and resident of india The assessee is an individual and resident of india - He is of the age of 65 years or more at any time during He is of the age of 65 years or more at any time during

previous year previous year - He furnishes a declaration in prescribed form in He furnishes a declaration in prescribed form in

duplicate to the person responsible for paying any duplicate to the person responsible for paying any income of the following nature stating that the tax on his income of the following nature stating that the tax on his estimated total income for the relevant previous year is estimated total income for the relevant previous year is nil:nil:

- Interest on securities- Interest on securities - dividends- dividends - interest other than interest on securities- interest other than interest on securities - payment in respect of deposit under NSS - payment in respect of deposit under NSS

e.) No deduction of tax shall be made by the Offshore e.) No deduction of tax shall be made by the Offshore Banking Unit from the interest paid:Banking Unit from the interest paid:

- On deposit made after 31.3.2005 by a non resident On deposit made after 31.3.2005 by a non resident or a person not ordinarily resident in india or a person not ordinarily resident in india

- On borrowing after 31.3.2005 from a non resident On borrowing after 31.3.2005 from a non resident or a person not ordinarily resident in india or a person not ordinarily resident in india

The payer of the income aforesaid will deliver to the The payer of the income aforesaid will deliver to the Chief Commissioner or Commissioner of Income Tax Chief Commissioner or Commissioner of Income Tax one copy of the declaration on or before the 7 one copy of the declaration on or before the 7thth day day of the month next following month in which the of the month next following month in which the declaration is furnished . If he fails to do so he will declaration is furnished . If he fails to do so he will be liable to a penalty of Rs 100 per day during be liable to a penalty of Rs 100 per day during which the default continues which the default continues

4) 4) Tax deducted is income (Sec 198)Tax deducted is income (Sec 198) The tax deducted at source is deemed to be The tax deducted at source is deemed to be

the income of the person from whose the income of the person from whose income the tax has been deducted at sourceincome the tax has been deducted at source

5) 5) Credit for tax deductedCredit for tax deducted : : The tax deducted at source and paid to the The tax deducted at source and paid to the

central government is deemed to have been central government is deemed to have been paid on behalf of the person from whose paid on behalf of the person from whose income the deduction was made or the income the deduction was made or the owner of the security , or of the depositor owner of the security , or of the depositor or of the owner of property ,or of the unit or of the owner of property ,or of the unit holder .or the shareholder, as the case may holder .or the shareholder, as the case may bebe

6.)6.)Duty of tax payerDuty of tax payer : :It is the duty of the person responsible for It is the duty of the person responsible for

deducting tax at source that he must pay it to deducting tax at source that he must pay it to the government within the prescribed limitthe government within the prescribed limit

7.) 7.) Issue of certificateIssue of certificate (Sec 203): (Sec 203): The person deducting the tax at source or The person deducting the tax at source or

the employer paying the tax on the value of the employer paying the tax on the value of perquisites,has to issue a certificate of perquisites,has to issue a certificate of deduction/payment to the assessee stating deduction/payment to the assessee stating the amount of tax deducted at source or paid the amount of tax deducted at source or paid in the prescribed Form No.16/16AA in case in the prescribed Form No.16/16AA in case of salaries and Form No. 16A in all other of salaries and Form No. 16A in all other sourcessources

8.)8.)Tax deduction and collection account Tax deduction and collection account number (Sec 203A)number (Sec 203A) : :

Every person, deducting tax or collecting Every person, deducting tax or collecting tax at source, who has not been alloted a tax tax at source, who has not been alloted a tax deduction account number or a tax deduction account number or a tax collection account number,shall apply in collection account number,shall apply in duplicate in Form No. 49B within one month duplicate in Form No. 49B within one month from the end of the month in which the tax from the end of the month in which the tax was deducted or collected to the A.O for the was deducted or collected to the A.O for the allotment of a tax collection account number allotment of a tax collection account number

9.)9.)Furnishing of statement of tax deduction(Sec Furnishing of statement of tax deduction(Sec 203AA)203AA) : :

The Director General of Income Tax or the person The Director General of Income Tax or the person authorised by him shall,within prescribed time authorised by him shall,within prescribed time after the end of each financial year beginning on after the end of each financial year beginning on or after 1.4.2008 prepare and deliver to every or after 1.4.2008 prepare and deliver to every person from whose income the tax has been person from whose income the tax has been deducted or in respect of whose income tax has deducted or in respect of whose income tax has been a statement in the prescribed form been a statement in the prescribed form specifying the amount of tax deducted or paid or specifying the amount of tax deducted or paid or collected at sourcecollected at source

10.)10.)Bar against direct demand from assessee(Sec Bar against direct demand from assessee(Sec 205)205)::

Where tax has been deducted at source, the Where tax has been deducted at source, the assessee shall not be liable to pay tax himself to assessee shall not be liable to pay tax himself to the extent it has been deducted even the deductor the extent it has been deducted even the deductor has failed to pay it to the government .has failed to pay it to the government .

Persons responsible for deducting Persons responsible for deducting

tax at source ( Section 204)tax at source ( Section 204) In case of salaries In case of salaries In case of interest on securities In case of interest on securities

payable by a person other than State payable by a person other than State or Central Governmentor Central Government

In case of any other sum paid or In case of any other sum paid or credited under the provisions of the credited under the provisions of the ActAct

Tax deduction Tax deduction account number account number section (203A)section (203A)

Every person who is Every person who is responsible for deducting tax responsible for deducting tax at source is allotted a TAN at source is allotted a TAN

number number

Such account number shall be Such account number shall be quoted on following documentsquoted on following documents

- all the challans for payment of tax- all the challans for payment of tax - all tax deductions at source - all tax deductions at source

certificatescertificates - any other documents so prescribed - any other documents so prescribed

NUMERICALNUMERICAL

Ascertain amount of Tax deducted at source from Ascertain amount of Tax deducted at source from the following incomes/receipts during the the following incomes/receipts during the financial year 2008-09financial year 2008-09

Lottery winnings of Rs 100000 payable to Mr. X, Lottery winnings of Rs 100000 payable to Mr. X, resident in Indiaresident in India

Winnings from horse race Rs 50000 payable to Winnings from horse race Rs 50000 payable to Mr. Y , non resident in IndiaMr. Y , non resident in India

Dividends from a domestic company Rs 40000 Dividends from a domestic company Rs 40000 Insurance commission payable by resident of Insurance commission payable by resident of

India Rs. 14000India Rs. 14000 Commission to lottery agent Rs. 15000Commission to lottery agent Rs. 15000 Income from interest on securities Rs. 6000Income from interest on securities Rs. 6000

SOLUTIONSOLUTION

CONCLUSIONCONCLUSION

TDS is one of the modes of TDS is one of the modes of collecting Income-tax from the collecting Income-tax from the assesses in India.assesses in India.

Tax deducted at source needs to be Tax deducted at source needs to be deposited in the Government deposited in the Government treasury and assigned to the Central treasury and assigned to the Central Government, within a stipulated Government, within a stipulated time period time period

SECTION OF THE ACTSECTION OF THE ACT NATURE OF NATURE OF PAYMENTSPAYMENTS

RATES IN % FOR RATES IN % FOR COMPANIESCOMPANIES

RATES IN % FOR RATES IN % FOR OTHERSOTHERS

192192 SalariesSalaries

193193 Interest ON Interest ON SecuritiesSecurities

2020 1010

194 A194 A Interest other Interest other than interest on than interest on securitiessecurities

2020 1010

194BB194BB Winning from Winning from horse racehorse race

3030 1010

194D194D Insurance Insurance commissioncommission

1010 1010

194 H194 H Commission on Commission on brokeragebrokerage

55 55

194i194i Income from Income from rent>120000rent>120000

2020 15 & 20 15 & 20

194 B194 B Winnings from Winnings from lottery> 5000lottery> 5000

3030 3030

![Information about deduction of Income Tax at Source [TDS]nbr.gov.bd/uploads/publications/227.pdf · 1 | P a g e Information about deduction of Income Tax at Source [TDS] No. Heads](https://static.fdocuments.net/doc/165x107/5a9e1b587f8b9ad2298d589a/information-about-deduction-of-income-tax-at-source-tdsnbrgovbduploadspublications227pdf1.jpg)

![ADVANCE TAX, TAX DEDUCTION AT SOURCE AND … · advance tax [Section 207 to 208] Collection of tax at source [Section 206C] Computation of advance tax [Section 209] Installments of](https://static.fdocuments.net/doc/165x107/5fa63a289ca1172a0e527830/advance-tax-tax-deduction-at-source-and-advance-tax-section-207-to-208-collection.jpg)

![Deduction, Collection and Recovery of · PDF file28 Deduction, Collection and Recovery of Tax 28.1 Deduction and Collection of Tax at Source and Advance Payment [Section 190] The total](https://static.fdocuments.net/doc/165x107/5aadf0d27f8b9adb688bae6c/deduction-collection-and-recovery-of-deduction-collection-and-recovery-of-tax.jpg)