Talent Solutions for Mutual Insurers - Health | Aon · Talent Solutions For Mutual Insurers...

38

Talent Solutions for Mutual Insurers January 25, 2017

Transcript of Talent Solutions for Mutual Insurers - Health | Aon · Talent Solutions For Mutual Insurers...

Talent Solutions for Mutual Insurers January 25, 2017

Talent Solutions For Mutual Insurers Proprietary & Confidential 2

Agenda

Introduction – Aon’s Integrated Approach

About Aon Hewitt & Ward Group Talent, Rewards and Performance

Industry Challenges and Initiatives

Human Capital Strategy Survey Review

Closing Summary and Q&A

Additional Resources and Contacts

Talent Solutions For Mutual Insurers Proprietary & Confidential 3

Introduction – Aon’s Integrated Approach

Jeff Rieder, CPA Partner and head of Ward Group +1.513.746.2400 [email protected]

Brian Ruggeberg, Ph.D. Partner, Aon Hewitt +1.516.342.2708 [email protected]

Chris Delhey Senior Managing Director, Aon Benfield Mutual Insurance Practice Group Leader +1.312.381.5566 [email protected]

Moderator:

Speaker:

Speaker:

Talent Solutions For Mutual Insurers Proprietary & Confidential 4

An Overview of Talent, Rewards & Performance

For most firms, talent is their largest expense and their greatest asset.

Recruit Assess Engage

Effectively determining reward strategies are critical to motivating and retaining a firm’s key talent.

What to pay How to pay it

Objectively measuring performance against internal goals and the external market is key to assessing the effectiveness of the reward strategy.

Benchmark Optimize Assess

Talent Solutions For Mutual Insurers Proprietary & Confidential 5

Industry Challenges and Initiatives

Talent Solutions For Mutual Insurers Proprietary & Confidential 6

Focus

An Active Industry

Speed of Change

Driving efficiency with new enterprise systems

Sales/Distribution strategy continues to evolve

Marketing and servicing efforts are changing to focus on the millennial generation

Product/Geographic expansion

Advanced analytics

Talent Solutions For Mutual Insurers Proprietary & Confidential 7

Management Perspective

Senior leadership becoming less optimistic about the state of the industry.

Source: Ward Group 2016 Business Environment Survey

2%

32%

54%

12%

4%

29%

50%

17%

0%

33%

59%

8%

0% 20% 40% 60% 80% 100%

Significantly worse

Moderately worse

About the same

Moderately better

State of the Industry in 2016 Compared to 2015

Commercial Lines Personal Lines Overall Benchmark

Talent Solutions For Mutual Insurers Proprietary & Confidential 8

-10%

-5%

0%

5%

10%

15%

20%

25%Total Personal Commercial

U.S. Quarterly Year-over-Year Direct Premium Change

2016 – Q3 marked the first time in 6 years total quarterly premium declined over prior year for commercial lines

Source: SNL Financial

Post 9/11 Post Katrina

Talent Solutions For Mutual Insurers Proprietary & Confidential 9

YTD Change in Direct Premium Through Q3 2016 (Versus YTD 2015)

3.6%

1.4%

5.6%

7.0%

4.6%

3.4%

2.5%

1.6%

0.6%

0.1%

-2.7%

-4% -2% 0% 2% 4% 6% 8%

All Lines

Commercial

Personal

Private Auto (Est.)

Comm'l Auto Liab

Fidelity & Surety

Home / Farm

Workers' Comp

Comm'l Multi Prl

Med Prof Liab

Fire & Allied

Source: SNL Financial

Talent Solutions For Mutual Insurers Proprietary & Confidential 10

60.0%

57.1% 56.3% 56.2%

63.3%

65.3%

59.2%

65.9%

62.5% 61.0%

59.7%

64.1%

70.2%

63.4%

53.1%

51.0% 51.0% 52.2%

62.3%

60.1%

54.4%

2016-YTD201520142013201220112010

Total Personal Commercial

Direct Loss Ratio

Source: SNL Financial

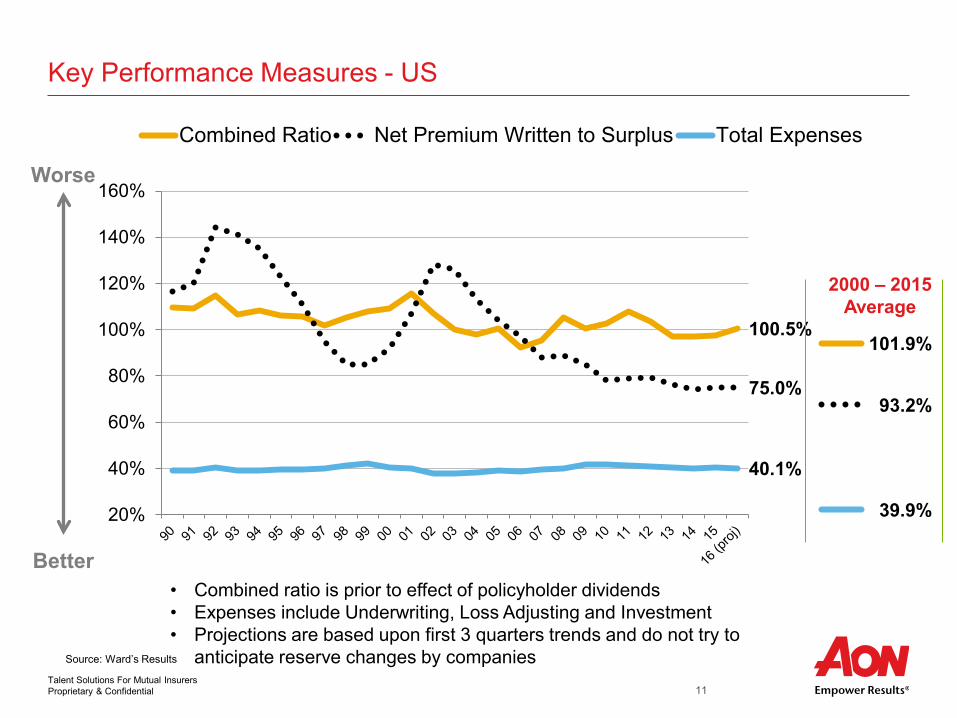

Talent Solutions For Mutual Insurers Proprietary & Confidential 11

100.5%

75.0%

40.1%

20%

40%

60%

80%

100%

120%

140%

160%

Combined Ratio Net Premium Written to Surplus Total Expenses

39.9%

93.2%

2000 – 2015 Average

Worse

Better

101.9%

Source: Ward’s Results

Key Performance Measures - US

• Combined ratio is prior to effect of policyholder dividends • Expenses include Underwriting, Loss Adjusting and Investment • Projections are based upon first 3 quarters trends and do not try to

anticipate reserve changes by companies

Talent Solutions For Mutual Insurers Proprietary & Confidential 12

Employee Costs on the Rise

10.8%

13.0%

7%

8%

9%

10%

11%

12%

13%

14%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Salaries & Benefits as % of Net Premiums Written

Ward's 50 Total Industry

Talent Solutions For Mutual Insurers Proprietary & Confidential 13

Hiring for Succession

The workforce is changing, 42% of workers are over 50 while millennials (those born after 1980) make up approximately 21% of the employee population.

<30 11.6%

31-40 19.5%

41-50 26.1%

51-60 31.3%

>60 11.4%

Employee Age Distribution

32.6% 34.3% 36.2% 38.4%

42.7%

2008 2010 2012 2014 2016

Percent of Workforce over 50

*Source Ward Group “HR and Employee Benefit Practices Study”, 2016

HR led employee training costs have increased 44% since 2013, from $421 per FTE to $606. Employee engagement has become more challenging. Remote workers expected to double in the next 3 years.

Talent Solutions For Mutual Insurers Proprietary & Confidential 14

Hiring for Innovation

Focus on recruiting a unique mix of talent and demographics; think about “out of the industry” talent.

81% of insurance executives are looking to hire a broader range of talent with different perspectives and diverse skills.

Talent Solutions For Mutual Insurers Proprietary & Confidential 15

Hiring for Diversity

85% of organizations with a diversity-focused staffing strategy report

increased performance

Diversity is key to promoting innovation

and creativity

Bringing together diverse teams has proven to create

a culture of adaptability

and productivity

Talent Solutions For Mutual Insurers Proprietary & Confidential 16

Insurance Carrier Employment

1360

1380

1400

1420

1440

1460

1480

1500

1520

1540

In T

hous

ands

6.67%

Source: U.S. Bureau of Labor Statistics

94,700 new jobs since April 2011

Talent Solutions For Mutual Insurers Proprietary & Confidential 17

Job Openings in Finance and Insurance

121

176 162

182

220 224

253 274

0

50

100

150

200

250

300

2009 2010 2011 2012 2013 2014 2015 2016

In T

hous

ands

Source: U.S. Bureau of Labor Statistics

Talent Solutions For Mutual Insurers Proprietary & Confidential 18

12-Month Staffing Plans Increase vs. Expected Revenue Growth

56%

66% 65% 66%

75% 69%

77%

86% 81%

87% 85% 84% 79% 80% 79%

35%

44% 39%

44% 44% 51% 54% 56% 54%

62% 58%

66% 65% 66% 66%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Expected Revenue Growth Increase Employees

Talent Solutions For Mutual Insurers Proprietary & Confidential 19

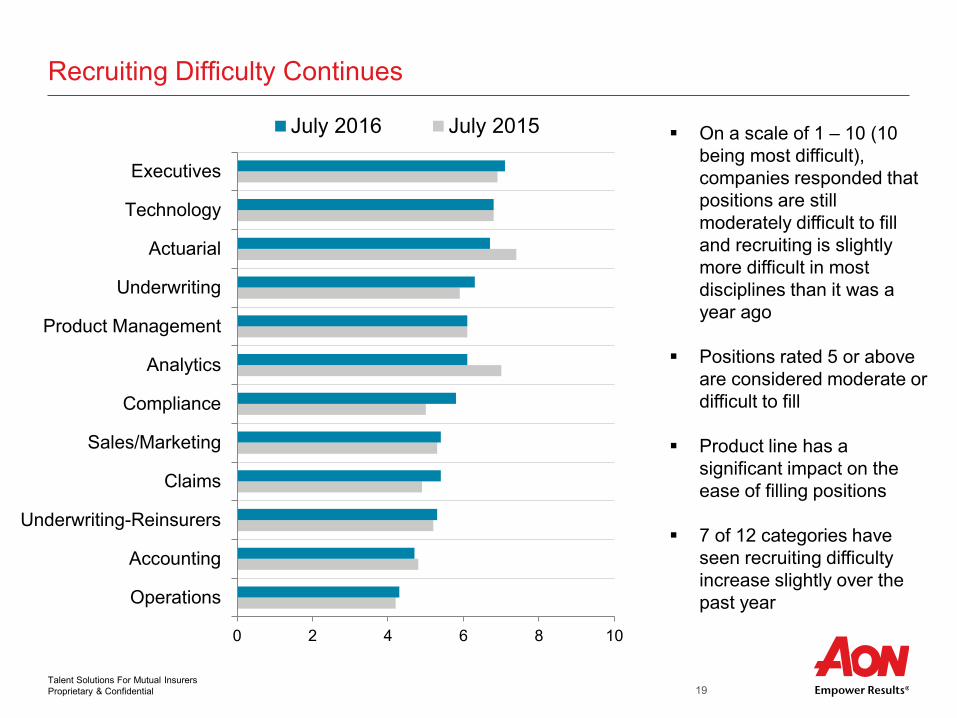

Recruiting Difficulty Continues

On a scale of 1 – 10 (10 being most difficult), companies responded that positions are still moderately difficult to fill and recruiting is slightly more difficult in most disciplines than it was a year ago

Positions rated 5 or above are considered moderate or difficult to fill

Product line has a significant impact on the ease of filling positions

7 of 12 categories have seen recruiting difficulty increase slightly over the past year

0 2 4 6 8 10

Operations

Accounting

Underwriting-Reinsurers

Claims

Sales/Marketing

Compliance

Analytics

Product Management

Underwriting

Actuarial

Technology

Executives

July 2016 July 2015

Talent Solutions For Mutual Insurers Proprietary & Confidential 20

Human Capital Strategy Assessment Survey

Talent Solutions For Mutual Insurers Proprietary & Confidential 21

Human Capital Strategy Assessment Survey

The Human Capital Strategy Assessment Survey assesses the human capital programs of insurance carriers to help determine how the talent spend is linked to business strategy

Talent Solutions For Mutual Insurers Proprietary & Confidential 22

Profile of Participating Organizations

Number of Participants 69

2015 Direct Premium Written (in Millions)

Property and Casualty $523,792

Life and Health $166,573

Financial Metrics

2015 Average Revenue (in Millions) $500,368

2015 Average Premium Growth 2.5%

2015 Average Return on Equity 7.1%

2015 Average Return on Revenue 8.0%

2015 Average Expense Ratio (P&C) 43.1%

2015 Average Expense Ratio (L&H) 33.3%

2015 Average Combined Ratio (P&C) 97.5

Employee Statistics

Annual employee turnover 8.8%

Average tenure of employee population 10.5

Survey was conducted from May through July, 2016

Talent Solutions For Mutual Insurers Proprietary & Confidential 23

Top Business Priorities

1%

7%

7%

10%

14%

17%

19%

28%

35%

36%

39%

57%

57%

57%

70%

Organizational Restructuring

Improve/Manage Captial Adequacy

Mergers & Acquisitions

Product Expansion

Geographic Expansion

Risk and Regulatory Compliance

Improve Loss Performance

Competitive Positioning/Gaining Market Share

Innovation Product or Technology

Executing on Major Investments/Initiatives

Revenue Growth

Customer/Client Service

Operational Efficiency/Cost Management

Technology Implementation

Human Capital/Talent Management

70% of companies indicated that Human Capital/Talent Management is one of their top five business priorities over the next three years

Talent Solutions For Mutual Insurers Proprietary & Confidential 24

Effectiveness of Human Capital Programs and Processes

Strengths

75% or more respondents consider the following programs and processes to be effective, highly effective, or exceptionally effective within their organizations.

Opportunities

52% or more respondents consider the following programs and processes to be ineffective or only moderately effective within their organizations.

Benefits 90%

Compensation 81%

Retention of Top Talent 80%

Organization Culture 77%

Sourcing and Recruiting 75%

Human Capital Analytics 83%

Career Pathing and Mobility 65%

Succession Planning 62%

Leadership and Development 54%

Diversity and Inclusion 52%

Note: Full rating scale for effectiveness is Exceptionally Effective, Highly Effective, Effective, Moderately Effective, Ineffective

+ ̶

Talent Solutions For Mutual Insurers Proprietary & Confidential 25

Effectiveness of Human Capital Programs and Processes

0% 25% 50% 75% 100%

Human Capital Analytics

Career Pathing and Mobility

Succession Planning

Leadership and Development

Diversity and Inclusion

High Potential Development

Reward and Recognition

Performance Management

Employee Training

Employee Assessment and Selection

Employee Engagement

Onboarding

Communication and Feedback

Sourcing and Recruiting

Organization Culture

Retention of Top Talent

Compensation

Benefits

Ineffective Moderately Effective Effective Highly Effective Exceptionally Effective

Talent Solutions For Mutual Insurers Proprietary & Confidential 26

Program Support and Alignment with Strategic Business Priorities

Many organizations agree that human capital programs and processes – regardless of effectiveness – are not highly supportive of or aligned with strategic business priorities:

Note: For the purposes of this reporting, the midpoint of the rating scale was excluded. The full supportive/aligned scale is: Not at all supportive or aligned; Somewhat supportive and aligned; Reasonably supportive and aligned; Highly supportive and aligned; Completely supportive and aligned

40%

41%

48%

49%

52%

Sourcing and Recruiting

Compensation

Organization Culture

Benefits

Retention of Top Talent

7%

13%

28%

29%

29%

Human Capital Analytics

Career Pathing and Mobility

Diversity and Inclusion

Retention of Top Talent

Leadership and Development

Top Five Most Effective

Top Five Least Effective

Human Capital Programs and Process Percent of respondents rating as highly / completely supportive and aligned

7%-29% of respondents rated the top five least effective HC programs and process as highly or completely supportive and aligned.

Only 40%-52% of respondents rated the top five most effective HC programs and processes as highly or completely supportive and aligned.

Talent Solutions For Mutual Insurers Proprietary & Confidential 27

HR Function Components

While many organizations agree that key components of their HR Functions are effective, less than half rated their HR Functions as supportive of or aligned with strategic business priorities: Over 70% of respondents rated key components of their HR Functions as effective, highly effective, or exceptionally

effective However, less than 42% of respondents believe that their HR Function components are supportive of and aligned with

their business priorities – HR Technology and HR Processes represent specific risk areas

Note: For the purposes of this reporting, the midpoint of the rating scale was excluded. The full supportive/aligned scale is: Not at all supportive or aligned; Somewhat supportive and aligned; Reasonably supportive and aligned; Highly supportive and aligned; Completely supportive and aligned

71%

41%

74% 82% 82%

24% 16%

32%

41% 39%

0%

20%

40%

60%

80%

100%

HR Processes HRTechnology

HROrganization

Design

HRCapabilities

HRGovernance

% of respondents rating HRcomponent as effective, highlyeffective, or exceptionallyeffective

% of respondents rating HRcomponent as highly /completely supportive andaligned

Talent Solutions For Mutual Insurers Proprietary & Confidential 28

Assessment of Organizational Capabilities

Extent to which participants agreed or disagreed that the following organizational capabilities and skills met their organization's future business priorities.

0% 25% 50% 75% 100%

Analytics and big datacompetency

Innovation

Developing integrated solutionsacross business units

Sales accumen

Technology aptitude

Operational efficiency

Policyholder understanding andintimacy

Strongly Disagree Disagree Neutral Agree Strongly Agree

Talent Solutions For Mutual Insurers Proprietary & Confidential 29

Capabilities Required to Meet Current and Future Business Priorities

Strengths

Meeting Current Business Priorities:

62-76% of respondents strongly agree or agree that they have the following organizational capabilities and skills required to meet current business priorities

Opportunities

Meeting Current Business Priorities:

12-18% of respondents strongly disagree or disagree that they have the following organizational capabilities and skills required to meet current business priorities

Policyholder understanding and intimacy 76%

Technology aptitude 72%

Developing integrated solutions across business units 62%

Analytics and big data competency 18%

Sales acumen 13%

Developing integrated solutions across business units 12%

Meeting Future Business Priorities:

63-71% of respondents strongly agree or agree that they have the following organizational capabilities and skills required to meet future business priorities

Meeting Future Business Priorities:

13-25% of respondents strongly disagree or disagree that they have the following organizational capabilities and skills required to meet future business priorities

Policyholder understanding and intimacy 71%

Operational efficiency 65%

Technology aptitude 63%

Analytics and big data competency 25%

Developing integrated solutions across business units 18%

Technology aptitude 13%

Note: For the purposes of this reporting, the midpoint of the rating scale was excluded. The full scale is: Strongly Disagree; Disagree; Neutral; Agree; Strongly Agree

+ ̶

Talent Solutions For Mutual Insurers Proprietary & Confidential 30

30%

32%

38%

49%

49%

54%

60%

61%

64%

The chart demonstrates number of participant’s that agreed or strongly agreed that their organization had the practices to meet their organization's future business priorities.

My Company Has Practices Required to Meet Future Business Priorities

Employee value proposition helps to attract and retain the employees

Company has an attractable organizational culture

Workforce composition is appropriate and adequate

Appropriate organizational structure and spans of control are in place

Current workforce has sufficient skills and capabilities

Current workforce has ample geographic mobility

Organization has requisite change management processes and capabilities

Organization has a defined Human Capital Strategy

Have talent pools and leadership pipeline needed to fill key roles

Talent Solutions For Mutual Insurers Proprietary & Confidential 31

Meeting Future Business Priorities:

60-64% of respondents strongly agree or agree that they have the following company-wide priorities required to meet future business priorities

Practices Required to Meet Current and Future Business Priorities

Strengths

Meeting Current Business Priorities:

74-80% of respondents strongly agree or agree that they have the following company-wide priorities required to meet current business priorities

Opportunities

Meeting Current Business Priorities:

19-32% of respondents strongly disagree or disagree that they have the following company-wide priorities required to meet current business priorities

Current workforce has sufficient skills and capabilities 80%

Workforce composition is appropriate and adequate 75%

Company has an attractable organizational culture 74%

Have talent pools and leadership pipeline needed to fill key roles 32%

Organization has requisite change management processes and capabilities 20%

Organization has a defined Human Capital Strategy 19%

Meeting Future Business Priorities:

28-45% of respondents strongly disagree or disagree that they have the following company-wide required to meet future business priorities Employee value proposition helps to attract

and retain the employees 64%

Company has an attractable organizational culture 61%

Workforce composition is appropriate and adequate 60%

Have talent pools and leadership pipeline needed to fill key roles 45%

Organization has a defined Human Capital Strategy 30%

Organization has requisite change management processes and capabilities 28%

Note: For the purposes of this reporting, the midpoint of the rating scale was excluded. The full scale is: Strongly Disagree; Disagree; Neutral; Agree; Strongly Agree

+ ̶

Talent Solutions For Mutual Insurers Proprietary & Confidential 32

Critical Needs for the Future

Participants were asked what will be the most critical business needs for the future. Top 5 Most Common Themes

Analytics / Data

Customer Centricity Talent Technology Leadership

Talent Solutions For Mutual Insurers Proprietary & Confidential 33

Practices to Start, Continue and Stop

Participants were asked what activities the human resources organizational should Start, Continue and Stop in order to meet future needs

Activities to Start 1. Planning 2. Talent Development 3. Succession Planning 4. Leadership Development 5. Organizational Analytics

Activities to Continue 1. Talent Development 2. Employee Training 3. Focus on Culture 4. Employee Engagement 5. Succession Planning

Activities to Stop 1. Manual/Outdated Processes 2. Rigid Performance Evaluations 3. Operate on Old Technology 4. Eliminate Paper

Talent Solutions For Mutual Insurers Proprietary & Confidential 34

Implications and Q&A

Financial results are losing steam more quickly.

Expense management is becoming a greater priority with market headwinds.

Finding and retaining top talent is more difficult than ever.

Data analytics driving more company-wide decisions but companies indicate weakness in their capabilities.

The labor market is very competitive and expected to remain that way.

Many companies feel a need for new technology and updated processes in order to be successful in the future.

Human Capital/Talent Management is a top priority of most organizations to ensure proper alignment to business strategy to help meet current and future business objectives.

What questions do you have?

Talent Solutions For Mutual Insurers Proprietary & Confidential 36

For more information or to schedule a one-on-one meeting:

Visit Aon Benfield’s Mutual Insurance webpage for an overview of our offerings including:

– Growth strategies – Industry leading analytics – Capital solutions – Operational consulting and benchmarking – Innovative reinsurance

Aon Benfield inquiries, contact:

– Chris Delhey at +1.312.381.5566 or [email protected]

Ward Group inquiries, contact:

– Jeff Rieder, CPA at +1.513.746.2400 or [email protected]

Aon Hewitt inquiries, contact: – Brian Ruggeberg, Ph.D. at +1.516.342.2708

Download Aon’s Talent Solutions Info Sheet

Talent Solutions For Mutual Insurers Proprietary & Confidential 37

Biographies

Chris Delhey - Leader of Aon Benfield's Mutual Insurance Practice Group Jeff Rieder - Partner and Head of Ward Group

Brian J. Ruggeberg, Ph.D. – Partner, Aon Hewitt

Chris has 30 years of industry experience including servicing a highly diverse book of business: general casualty/CMP, personal lines, national and regional property, workers’ compensation, professional liability, directors and officers, financial institutions, fidelity/surety, and miscellaneous errors and omissions. One point of concentration within Chris’s current client partnerships is reinsurance specific to carriers insuring non-profits, mutual insurance companies, and other cooperative financial institutions.

Jeff has 22 years of experience in the insurance industry with expertise in the property-casualty and life segments. He has been involved with over 400 projects for domestic and international insurance companies, covering a range of performance and strategic evaluations. Jeff leads Aon’s global performance benchmarking practice for insurance and the U.S. insurance compensation practice.

Dr. Ruggeberg has 25 years of consulting experience and has been involved in the development and implementation of various assessment and selection, leadership assessment and development, performance management, and training programs. He also serves as the Talent Enablement leader for Aon Hewitt’s Talent practice.

Talent Solutions For Mutual Insurers Proprietary & Confidential 38

About Aon

Aon plc (NYSE:AON) is a leading global provider of risk management, insurance brokerage and reinsurance brokerage, and human resources solutions and outsourcing services. Through its more than 72,000 colleagues worldwide, Aon unites to empower results for clients in over 120 countries via innovative risk and people solutions. For further information on our capabilities and to learn how we empower results for clients, please visit: http://aon.mediaroom.com.

© Aon plc 2017. All rights reserved.

The information contained herein and the statements expressed are of a general nature and are not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.