Taking Stock: Conducted by: secondary opportunities and ... · secondary opportunities and the...

12

Taking Stock: secondary opportunities and the agile future Conducted by: Supported by: An academic research survey conducted by Northumbria University Published August 2015

Transcript of Taking Stock: Conducted by: secondary opportunities and ... · secondary opportunities and the...

Taking Stock:secondary opportunities and the agile future

Conducted by:

Supported by:

An academic research survey conducted by Northumbria UniversityPublished August 2015

Executive SummaryThis research studied 27 towns and cities across England, Wales and Scotland.

21st Century businesses are agile. Tenants want less space, more from it and on their own terms.

34% of vacant secondary stock was built in the pre-war period while 37% was built during the 1960’s and 1970’s. Both eras of construction offer opportunities for the new economy.

Agile tenants have voted with their feet. Over 29m sq ft of offices are lying empty. Around 26 ½ m sq ft or 90% of the vacant office stock is in the secondary market. This could be the tip of the iceberg.

Geographical analysis indicates that secondary office property can be a niche investment class, part of a mix of office types or a disruptive alternative to traditional office development.

Landlords could miss out on £4.8bn of profit over the next 10 years. Landlords are loosing nearly £325m of losses on rent alone per year and are paying almost £170m in holding costs.

The world of work has changed

A new lease of life for secondary stock

Vacancy shockwave

The geography of resilience

£4.8bn office timebomb

Everyone is talking about the shortfall in prime office property and the urgent need to create new business space, but no one is discussing how the secondary office market can help to plug this shortfall, or the quality, value and variety of this stock.

When I came across some initial research by academics at Northumbria University, I was intrigued, and I wanted to know more. I was shocked to learn that the UK has vacant office space equalling double the total stock in Leeds, and as a result, landlords are likely to lose over £4.8bn in rent over the next ten years. Concerning me the most was the lack of awareness around the problem and the impact it has on business and the economy.

This ‘Office Timebomb’ really hit home and we supported the independent experts at Northumbria University to delve deeper into the issue. This research document is the first of what will be quarterly reports into this secondary office market and the huge threats and opportunities this brings.

Other factors we must consider with this research include business rates and empty property rate avoidance. Also, changes to permitted development rights for office to residential conversion is one of the single biggest threats to office provision. To accommodate the UK’s thriving businesses the secondary office market will become increasingly integral.

It makes truly compelling reading. The enlightened building owners who grasp the challenge of the agile future and the opportunity that secondary property presents, could benefit hugely.

Steve Jude, Chief Executive Officer, Citibase plc

£4.8bn

Commercial office stock in the Northumbria University database

SecondaryMarket

PrimeMarket

7

Aberdeen

Glasgow

Newcastle &Gateshead

Leeds

ManchesterLiverpool

Nottingham

Leicester

Cardiff

Exeter

Plymouth

Portsmouth

Southampton

Guildford

Croydon

Chelmsford

Ipswich

Cambridge

Reading

Oxford

Bath & NorthEast Somerset

Type No. of properties

Floorspace (m2)

Floorspace (Sqft)

Rateable Value(£)

Retail 560,150 118,151,000 1,271,304,760 £17,488,000,000

Office 355,990 9,272,000 99,766,720 £14,092,000,000

Industrial 450,910 323,101,000 3,476,566,760 £11,786,000,000

TOTAL 1,367,050 450,524,000 4,847,638,240 £43,366,000,000

Traditional assessments of the office market focus on estimates of take up and absorption, concentrating on the prime market. However, these studies rarely ground their findings in an appraisal of overall stock. In response, for the first time we present a representation of all vacant office stock.

We reveal an 18% average vacancy rate.

Astonishingly, the real rate could be double this figure if grey space is taken into account. Grey space describes those office properties that are leased but surplus to requirements and likely account for a further 20% of stock.

Milton Keynes

Hemel Hempstead

Windsor & Maidenhead

Luton

Watford

Welwyn & Hatfield

Locations surveyed in this study

SWO

T

Secondary Swot Analysis

STRENGTHS• Lots of it (which means there is discriminatory choice)

• Often have good accessibility/proximity to transport networks

• Often in prestigious locations

• Convenient proximity to service and social amenities

• Lots of the these buildings have identity recognition

• Often have better parking provision associated with historical infrastructure

WEAKNESSES• Market overhang (which means lots of availability)

• Loss of rent and holding cost (opportunity to reverse and maximise)

• Perception of functional redundancy (counteracted by the emergence of new technology such as WIFI and flexible working practices)

• Perception of economic redundancy (the potential buoyant rental levels in central locations counteract this situation)

OPPORTUNITIES• To change a negative story into a positive

future (instead of Empty Property Rates [EPR] avoidance promote a climate of new business entrepreneurialism)

• Transformation (within and across use)

• There has been a revalorisation of commercial office space. Tenants want less of it and more from what they get.

• The agile tenant is small, creative and flexible and want office space that reflects their cultural taste and status

THREATS• Write down of property book value

(Stranded assets trapped in inertia)

• Empty property rates

• 2018 Minimum Energy Performance Standard (MEPS) legislation

• 2017 statutory valuation exercise uncertainty. This could be both positive and negative. In prime areas high property values are likely to be locked in. However, elsewhere the value of secondary assets are likely to fall (the last valuation exercise took place at the top of the market in 2008). This will make secondary assets more attractive as business rates will fall for tenants (and empty property rates for landlords)

The secondary office market is often overlooked and seen as the Cinderella of the property market. Perceptions of weaknesses and threats are often used to justify new office development.

However, the genuine strengths and exciting opportunities that these office properties present often outweigh this pessimism. The purpose of this report is to illustrate this situation.

Changing Business Practices:The world of work has changed forever

The old way The new way

inflexible agilespacious fast turnaround

good locationflexibleover specified

over resourced

expensiveleases

There has been a fundamental change in the nature of business: occupiers need less space and are more discerning in their demands.

The big question is, does the conventional office market and its institutional apparatus provide the business space for the 21st Century? Outside of the superheated Central London office market the answer is a resounding NO.

Office developers and investors are continuing to provide business space for the 20th Century. Large open plan spaces with large floor plates with long and restrictive leases are not what the SMEs and entrepreneurs of this new agile economy are demanding.

They need to be totally flexible in their work and they are demanding this from all aspects of their supply partners, this is relatively common place in IT and telecoms but less so in office accommodation.

This is a missed opportunity and one that has a critical bearing on economic growth, entrepreneurialism and growth.

The need for a new approach: ‘The agile future’ At its most productive, new development only accounts for 2% of supply in any given year. This means that in the short to medium term the prime market only accounts for 5-10% of office supply, yet it receives all of the attention. This means that 90% of the office market is underexploited and relatively unknown — hence the reason for this publication series.

How we use, maintain, and manage our existing office properties in order to satisfy our appetite for new ways of working, could define the cities of the future. Yes, there are plenty of empty property rate avoidance measures, and increasingly in certain locations, schemes to convert underperforming office properties into new use through permitted development legislation.

However, empty office property exploitation strategies that recognise the enduring potential of these offices in their current use, are few and far between. This is a missed opportunity. The UK does not need to build new office properties, they already exist in abundance.

Secondary office properties can provide a viable future for the new economy which is based on small business and entrepreneurialism. Small businesses, tech and creative industries do not want large floor plates, high specifications and restrictive lease covenants. Business in the 21st Century expect their business property to work for them.

space smart

Whole Market m2

Whole Market Sqft

RateableValue

Vacancy Rate %

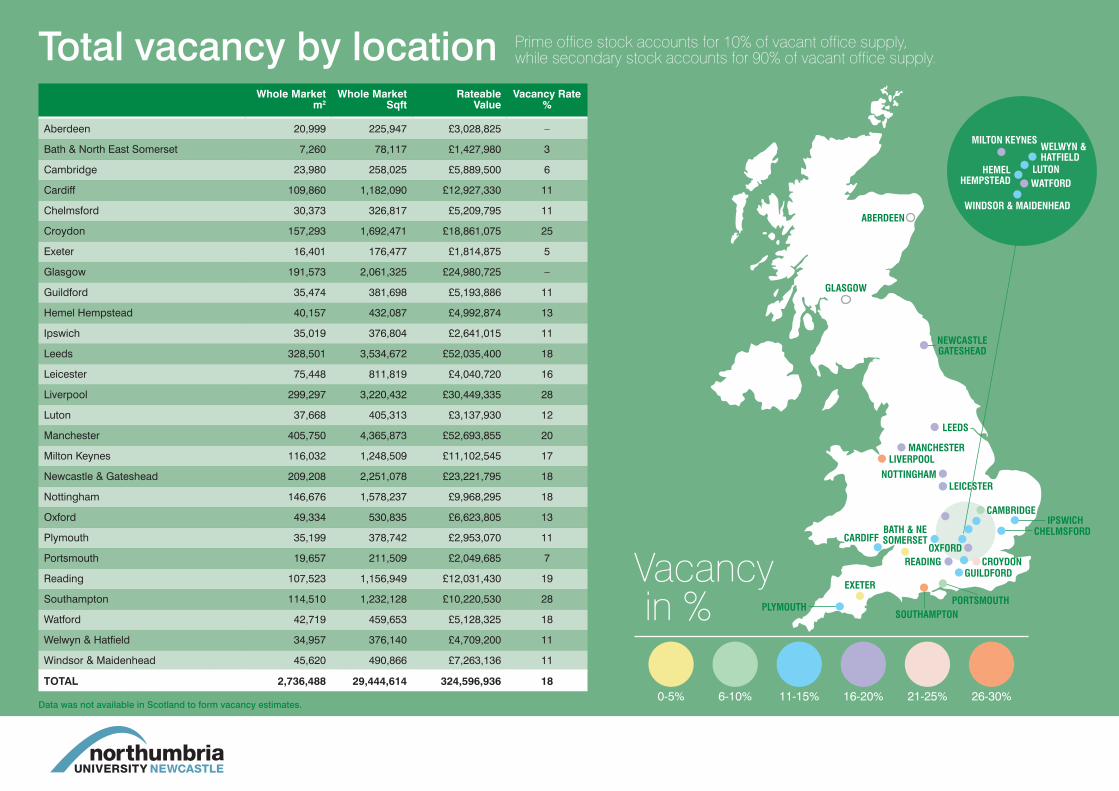

Aberdeen 20,999 225,947 £3,028,825 –

Bath & North East Somerset 7,260 78,117 £1,427,980 3

Cambridge 23,980 258,025 £5,889,500 6

Cardiff 109,860 1,182,090 £12,927,330 11

Chelmsford 30,373 326,817 £5,209,795 11

Croydon 157,293 1,692,471 £18,861,075 25

Exeter 16,401 176,477 £1,814,875 5

Glasgow 191,573 2,061,325 £24,980,725 –

Guildford 35,474 381,698 £5,193,886 11

Hemel Hempstead 40,157 432,087 £4,992,874 13

Ipswich 35,019 376,804 £2,641,015 11

Leeds 328,501 3,534,672 £52,035,400 18

Leicester 75,448 811,819 £4,040,720 16

Liverpool 299,297 3,220,432 £30,449,335 28

Luton 37,668 405,313 £3,137,930 12

Manchester 405,750 4,365,873 £52,693,855 20

Milton Keynes 116,032 1,248,509 £11,102,545 17

Newcastle & Gateshead 209,208 2,251,078 £23,221,795 18

Nottingham 146,676 1,578,237 £9,968,295 18

Oxford 49,334 530,835 £6,623,805 13

Plymouth 35,199 378,742 £2,953,070 11

Portsmouth 19,657 211,509 £2,049,685 7

Reading 107,523 1,156,949 £12,031,430 19

Southampton 114,510 1,232,128 £10,220,530 28

Watford 42,719 459,653 £5,128,325 18

Welwyn & Hatfield 34,957 376,140 £4,709,200 11

Windsor & Maidenhead 45,620 490,866 £7,263,136 11

TOTAL 2,736,488 29,444,614 324,596,936 186-10% 11-15% 16-20% 21-25%0-5% 26-30%

Total vacancy by location Prime office stock accounts for 10% of vacant office supply, while secondary stock accounts for 90% of vacant office supply.

MANCHESTER

NEWCASTLE GATESHEAD

MILTON KEYNES

LUTON

WELWYN & HATFIELD

HEMEL HEMPSTEAD WATFORD

WINDSOR & MAIDENHEADABERDEEN

GLASGOW

LEEDS

LIVERPOOL

CARDIFFBATH & NE SOMERSET

SOUTHAMPTONPLYMOUTH

EXETER

PORTSMOUTH

GUILDFORDCROYDONREADING

CHELMSFORD

CAMBRIDGE

OXFORD

NOTTINGHAMLEICESTER

IPSWICH

Vacancy in %

Data was not available in Scotland to form vacancy estimates.

PRIMARY MARKET SECONDARY MARKET

m2 Sqft m2 Sqft

Aberdeen 2,017 21,705 18,982 204,241

Bath & North East Somerset 716 7,704 6,544 70,413

Cambridge – 0 23,980 258,025

Cardiff 11,549 124,266 98,311 1,057,824

Chelmsford 628 6,757 29,745 320,060

Croydon – 0 157,293 1,692,471

Exeter 846 9,099 15,556 167,377

Glasgow 29,802 320,670 161,771 1,740,656

Guildford 1,008 10,841 34,466 370,857

Hemel Hempstead 7,572 81,473 32,585 350,615

Ipswich 194 2,087 34,825 374,717

Leeds 55,985 602,403 272,516 2,932,269

Leicester 4,105 44,173 71,343 767,646

Liverpool 20,893 224,805 278,404 2,995,627

Luton 1,942 20,893 35,727 384,419

Manchester 44,644 480,373 361,106 3,885,500

Milton Keynes 13,656 146,944 102,376 1,101,565

Newcastle & Gateshead 21,033 226,315 188,175 2,024,763

Nottingham 5,576 59,992 141,101 1,518,245

Oxford 1,881 20,241 47,453 510,594

Plymouth 4,474 48,140 30,725 330,602

Portsmouth 4,122 44,353 15,535 167,157

Reading 20,042 215,654 87,481 941,295

Southampton 6,847 73,674 107,663 1,158,454

Watford 7,381 79,416 35,338 380,237

Welwyn & Hatfield 1,677 18,047 33,280 358,093

Windsor & Maidenhead 11,222 120,751 34,397 370,116

TOTAL 279,812 3,010,776 2,456,676 26,433,837

Our findings indicate that there is a clear divide between the prime and secondary office market.

Primary and secondary market vacancy

25% 50% 75% 100%

ABERDEE

N

BATH

& N

ORTH

EAS

T SO

MER

SET

CAM

BRID

GE

CARD

IFF

CHEL

MSF

ORDCROYDONEXETER

GLASGOWGUILDFORD

HEMEL HEMPSTEADIPSWICH

LEEDS

LEICESTER

LIVERPPOOL

LUTON

MANCHESTE

R

MILT

ON K

EYNE

S

NEW

CAST

LE &

GAT

ESHE

AD

NOTT

INGH

AM

OXFORD

PLYMOUTH

PORTSMOUTH

READING

SOUTHAMPTON

WATFORD

WELWYN & HATFIELD

WINDSOR & MAIDENHEAD

SECONDARY MARKET VACANCY26.4m sqft

90%

Secondary Market

% SPLIT OF TOTAL VACANCY’

Primary Market

Vacancy levels by

floorspace

Aber

deen

Bath

& N

orth

E

ast S

omer

set

Cam

brid

ge

Card

iff

Chel

msf

ord

Croy

don

Exet

er

Glas

gow

Guild

ford

Hem

el

Hem

pste

ad

Ipsw

ich

Leed

s

Leic

este

r

Live

rpoo

l

Luto

n

Man

ches

ter

Milt

on K

eyne

s

New

cast

le &

G

ates

head

Notti

ngha

m

Oxfo

rd

Plym

outh

Port

smou

th

Read

ing

Sout

ham

pton

Wat

ford

Welw

yn &

Hat

field

Win

dsor

&

Mai

denh

ead

Aber

deen

Bath

& N

orth

E

ast S

omer

set

Cam

brid

ge

Card

iff

Chel

msf

ord

Croy

don

Exet

er

Glas

gow

Guild

ford

Hem

el

Hem

pste

ad

Ipsw

ich

Leed

s

Leic

este

r

Live

rpoo

l

Luto

n

Man

ches

ter

Milt

on K

eyne

s

New

cast

le &

G

ates

head

Notti

ngha

m

Oxfo

rd

Plym

outh

Port

smou

th

Read

ing

Sout

ham

pton

Wat

ford

Welw

yn &

Hat

field

Win

dsor

&

Mai

denh

ead

TOTALOverall Market

£324,596,936 per year

TOTALSecondary Office

£273,134,952 per year

10

20

30

0

40

10

50

20

30

60

MIL

LIO

NS

£M

ILLI

ON

S £

Rent loss and holding costsRent landlords are missing out on per year

Holding cost per year1+1+3+6+3+9+1+12+3+2+1+25+2+15+2+26+5+11+5+3+1+1+6+5+3+2+41+1+3+5+2+9+1+10+2+2+1+18+2+14+2+22+5+10+5+3+1+1+4+4+2+2+3Whole Market

KEY

Secondary Market

Prime Market

KEY

Secondary Market

Aber

deen

Bath

& N

orth

E

ast S

omer

set

Cam

brid

ge

Card

iff

Chel

msf

ord

Croy

don

Exet

er

Glas

gow

Guild

ford

Hem

el

Hem

pste

ad

Ipsw

ich

Leed

s

Leic

este

r

Live

rpoo

l

Luto

n

Man

ches

ter

Milt

on K

eyne

s

New

cast

le &

G

ates

head

Notti

ngha

m

Oxfo

rd

Plym

outh

Port

smou

th

Read

ing

Sout

ham

pton

Wat

ford

Welw

yn &

Hat

field

Win

dsor

&

Mai

denh

ead

Aber

deen

Bath

& N

orth

E

ast S

omer

set

Cam

brid

ge

Card

iff

Chel

msf

ord

Croy

don

Exet

er

Glas

gow

Guild

ford

Hem

el

Hem

pste

ad

Ipsw

ich

Leed

s

Leic

este

r

Live

rpoo

l

Luto

n

Man

ches

ter

Milt

on K

eyne

s

New

cast

le &

G

ates

head

Notti

ngha

m

Oxfo

rd

Plym

outh

Port

smou

th

Read

ing

Sout

ham

pton

Wat

ford

Welw

yn &

Hat

field

Win

dsor

&

Mai

denh

ead

Compound Loss

The £4.8bn office timebomb

Compound Loss Per Year (Whole market)

Compound Loss Per Year (Secondary market)

Aberdeen £4,512,949 £4,000,836

Bath & North East Somerset

£2,127,690 £2,001,413

Cambridge £8,775,355 £8,775,355

Cardiff £19,158,303 £16,469,499

Chelmsford £7,762,595 £7,295,852

Croydon £28,103,002 £28,103,002

Exeter £2,704,164 £2,525,811

Glasgow £37,221,280 £29,074,407

Guildford £7,738,890 £6,930,565

Hemel Hempstead £7,439,382 £6,127,804

Ipswich £3,935,112 £3,905,163

Leeds £77,532,746 £54,690,972

Leicester £6,020,673 £5,239,242

Liverpool £45,369,509 £41,396,908

Luton £4,675,516 £4,584,477

Manchester £78,513,844 £66,873,621

Milton Keynes £16,542,792 £14,353,833

Newcastle & Gateshead £34,600,475 £29,456,548

Nottingham £14,852,760 £14,042,945

Oxford £9,869,469 £9,815,606

Plymouth £4,400,074 £3,536,955

Portsmouth £3,054,031 £2,035,914

Reading £17,926,831 £13,107,873

Southampton £15,228,590 £13,910,312

Watford £7,641,204 £5,868,142

Welwyn & Hatfield £7,016,708 £5,067,043

Windsor & Maidenhead £10,822,073 £7,780,983

TOTAL £483,546,016 £406,971,078

Our research has revealed that taking the 27 towns and cities in the study, landlords could miss out on an astonishing £4.8bn in potential earnings and savings over a 10 year period.

In the secondary market alone this figure is an eye-watering £4.1bn.

£4.8bn landlord loss over 10 years

for the whole market

£4.1bn landlord loss over 10 years for the secondary market

Compound loss is an estimation of the total cost of vacancy based upon combined rental loss and holding cost payments.

Secondary office property has the potential to challenge its Cinderella status in a variety of ways. The following regional segmentation demonstrates these opportunities. This segmentation is broad and the authors recognise that there will be considerable inter and intra regional variation due to the relative conditions in each location.

Furthermore, it is highly likely, especially outside of Central London, that each location will contain a variety of all three scenarios. However, regardless of the variable characteristics of location, the message is out: occupiers want flexibility and secondary office property is waiting to be exploited in all three types of location.

Redundant locations: Typically redundant locations do not have the rental levels to support capital expenditure or the presence of economic demand to justify a conventional commercial building strategy. Nevertheless, these locations have a rapidly degrading commercial office stock which demands attention. These locations are attractive to business start-ups and those looking for low rental levels and flexibility and therefore demand office building solutions which account for these business trajectories.

Stranded locations: These locations (like Cardiff or secondary areas of regional cores like Leeds) do not have rental levels sufficient to justify the development of prime office supply or the refurbishment of secondary property into contemporary specification in the conventional sense (they may also not have the available space to construct new property).

However, these areas still have demonstrable economic potential (these locations are also suffering the impact of conversion into alternative use) and must make the most of their existing property assets which mostly fall into the secondary asset category through creative re-use measures and disruptive innovation.

Premium locations: Central London and elements of the regional cores: Such areas have buoyant rental markets and are even beginning to see the benefit of secondary property as an investment class, even creating speculative ‘shabby chic’ and so called ‘foundspace’. These areas report very low supplies of prime office supply and a lot of secondary has been lost to other uses through conversion.

Our findings indicate that some of these areas still have significant quantities of underutilised secondary properties which could be brought forward/repurposed to fill the deficit in property supply. For example the top three cities for secondary vacancy in our survey – Manchester, Liverpool and Leeds – alone had over 9.8m sq ft of empty secondary office space.

Building types: opportunities and challenges 34% of these properties were built before

the war and offer an enticing opportunity

for the agile businesses of the future. These

properties are often located in prominent

locations with buoyant rental levels and a

transferable identity based on rich cultural

history. Often these opportunities exist in

close proximity to transport infrastructure

and public transport networks and have great

walkability to a host of nearby amenities.

Towns and cities in the UK are crying out

for new office property to accommodate the

resurgent economy. Encouragingly, with

narrow floor plates, good access to light and

accessible servicing arrangements, these

buildings can be turned around for the new

economy with relative ease.

37% of properties were built during the

1960’s and 1970’s. Although these properties

can suffer from aggressive exteriors and

a degree of aesthetic stigma, they share

many of the same positive characteristics as

those built in the post war period in terms

of buoyant rental levels, accessibility and

proximity to amenities. Although suffering

from a certain degree of ‘Ugly Betty’

syndrome, many of these buildings have the

capacity to be reinvigorated through creative

transformation.

Building era:

PREMIUM

STRANDED

REDUNDANT

KEY 2000+ 1990s 1980s 1960/70 Post War Pre WarA new lease of life for secondary office properties

Bath & North East Somerset Cambridge Cardiff Chelmsford Croydon Exeter

Guildford Hemel Hempstead Ipswich Leeds Leicester Liverpool

Luton Manchester Milton Keynes Newcastle & Gateshead Nottingham Oxford Plymouth

Portsmouth Reading Southampton Watford Windsor & Maidenhead

Aberdeen

Glasgow

Welwyn & Hatfield

Conducted by:

About Citibase

Citibase offers fully serviced business centres for cost–conscious SMEs in over 40 locations nationwide.

Their unique disruptive business model brings together both clients and customers. Over the last 21 years they have been commissioned by some of the largest and smallest names in the UK property market to help execute a plan for their under-utilised office space.

They provide solutions to property owners, by taking over the management of the building, allowing building owners to generate a cash income from secondary office space with minimum stress whilst providing SME customers with cost–effective office solutions.

Citibase also offers building owners who have short-term voids a smart way of enjoying the hassle-free cash which only Citibase can generate by launching one of their unique pop–up business centres. It’s easy–in and easy–out, and Citibase will manage the entire process.

Citibase concentrates on town and city centre locations and offers their customers over 1 million sq. ft. under management. Founded in 1993, the business has at its heart the ‘Freedom at Work’ philosophy; a deep-routed commitment to support and nurture cost-conscious SMEs whether they are setting out for the first time or taking bigger steps on the path to growth. Being in a Citibase centre gives SMEs the independence to be freed from expensive rents and rates, inflexible terms, service charges, hidden costs and corporate restrictions. By taking the stress of running a building off business’s hands, Citibase allows SMEs to focus on growing a successful business.

Want to know more? Request an exploratory conversation with Steve Jude, Chief Executive Officer, email [email protected]

For more information on Citibase visit www.citibase.com

About R3Intelligence, Northumbria University

R3Intelligence is dedicated to supplying high quality impartial commercial real estate research and advice. Our multi–disciplinary team offers services and expertise for investors, landlords, businesses and organisations who want to understand how commercial real estate can work more efficiently for them. We are a team of industry specialists and academics based at a UK university offering commercial consultancy and contract research.

We offer clients commercial real estate exploitation strategies, commercial property market intelligence and spatial analysis and modelling services. In other words we have the advice and the evidence to back it up. Our expertise is in the following areas:

• Physical appraisal and value engineering in relation to the refurbishment, repositioning and conversion into alternative use of commercial real estate assets

• Commercial real estate asset stock picking

• Surplus commercial floor space planning

• Empty property rates strategies

• Employment land and premises assessments

• Land and property use planning

• Economic development and inward investment strategies

• Monitoring and simulation of contemporary methods of urban finance such as Business Rates Retention, Tax Increment Financing, Enterprise Zones, Accelerated Development Zones and Business Improvement Districts

Interested in getting your commercial property working better for you? Request an exploratory meeting with either Dr Paul Greenhagh or Kevin Muldoon-Smith

Dr Paul Greenhalgh, R3Intelligence Lead, Tel: 0191 227 4593, [email protected]

Kevin Muldoon-Smith, R3Intelligence Consultant, Tel: 07739 321643 [email protected]

www.R3Intelligence.co.uk

Supported by:

![GOVERNMENT OF PUDUCHERRY€¦ · Bachelor of Physiotherapy [B.P.T.)] one of the subject courses must have passed H.Sc. (Academic) examination conducted by the Board of Higher Secondary](https://static.fdocuments.net/doc/165x107/60185143c93cce14a3726c62/government-of-puducherry-bachelor-of-physiotherapy-bpt-one-of-the-subject.jpg)