Take advantage of tax-deferred retirement savings. · this tax-advantaged retirement account. Who...

8

IRAs Take advantage of tax-deferred retirement savings.

Transcript of Take advantage of tax-deferred retirement savings. · this tax-advantaged retirement account. Who...

IRAsTake advantage of tax-deferred retirement savings.

IRAsWe’re living longer than ever before. Some of us may spend 20 years or more in retirement. That means more time to do what we like to do. But it also means making sure we find a way to pay for it.

Help your retirement savings go the distance.Finding ways to pay for up to 20 additional years of everyday living expenses — is a tough challenge. While you may have a retirement plan at work, it may not be enough to fund your living expenses in retirement.

That’s why one part of a sound financial plan is having solid goals for your retirement years.

Managing a Lifetime of Financial Goals

Note: These are just examples of how this might work for you.

EstatePlanning

OtherInsurance

Savings

- Checking Accounts- Savings Accounts- Money Markets

Umbrella LiabilityInsurance

Long TermCare Insurance

RetirementIncome Gifting

- IRAs- Stocks & Bonds- Employee Retirement Plans

HealthInsurance

AutoInsurance

Homeowners/PropertyInsurance

DisabilityIncome

Insurance

LifeInsurance

EmergencyFund

Wills/Trusts

- Annuities- College Planning- Mutual Funds

Investments

A practical way to address future financial goals.An Individual Retirement Arrangement (IRA) can help jumpstart your plan for future needs. It’s easy to set up and lets you be in control — you decide how much and where it is invested. By including IRAs in your retirement planning, you could help achieve the financial goals you’re working for that much sooner.

Choose the IRA that works for you.IRAs help make your retirement savings work harder through the valuable tax benefits they can provide. They also give you control and flexibility: you choose how your money is invested and you can change investments within your IRA as needed. Typical investments that can be made with IRA contributions include: mutual funds, stocks, bonds, certificates of deposit (CDs) and annuities.

Traditional IRA – more money to put to work now.Traditional IRAs allow your money to grow tax-deferred until you withdraw it. That means your account can grow faster and accumulate more money for retirement — especially if you have a long period of time to keep the money invested, such as 20 or 30 years.

What’s more, contributions to a traditional IRA may be tax-deductible, which puts more money in your pocket now — or to invest in your future. While the generous tax benefits you receive now do mean there’s a tax bill to pay later, those withdrawals will be taxed as ordinary income, which, at retirement may be at a lower tax rate.

Roth IRA – no taxes due later on.Roth IRAs also have tax benefits — but they are different from a traditional IRA. The money you put into a Roth IRA can not be deducted from your taxes. However, when time comes to withdraw money, you pay no taxes on your contributions or earnings.1 So, all of what you accumulate in your account is yours to keep. And, there is no age requirement to begin taking money out of your account — so you can leave more to your heirs, if that is a goal.

1 This only applies if the withdrawal is a qualified distribution. A distribution is qualified if the Roth IRA is held for five years and if made after 59½, upon death or disability, or as a first-time home purchase with a lifetime limit of $10,000.

Traditional vs. Roth IRAs.Here’s a more detailed comparison of a Traditional vs. Roth IRA. Your Allstate Agent can help you decide which one is right for you.

2 Generally, IRA withdrawals are treated as distributions of gain. Withdrawals of gain are taxed as ordinary income and, if taken prior to age 59½, may be subject to an additional 10% federal penalty tax.

3 Qualified distributions from a Roth IRA are tax-free. A distribution is qualified if the Roth IRA is held for five years and if made after 59½, upon death or disability, or as a first-time home purchase with a lifetime limit of $10,000.

Traditional IRA Roth IRA

Are contributions tax- deductible?

Contributions may be tax-deductible, depending on:

• Your adjusted gross income • Your marital status • Whether you and/or your

spouse participate in a retirement plan at work

Contributions are not tax-deductible

How are earnings taxed?

Earnings from your contributions grow tax-deferred; you pay no taxes until you withdraw the money2

Earnings from your contributions grow tax-free; you pay no taxes when you take a qualified distribution3

Is there a contribution age limit?

You may continue to make contributions at any age as long as you are still working. Otherwise, you many not make contributions after age 72.

You may continue to make contributions at any age as long as you are still working. Otherwise, you many not make contributions after age 72.

Is there a distribution requirement based on age?

If you turned 70½ prior to 12/31/19, you must start taking an annual RMD beginning 4/1/20. If you turn 70½ on or after 1/1/2020 you will have an RMD beginning date of 4/1 of the year following the year you turn 72. RMDs have been waived in 2020.

No distributions are required to be taken during the owner’s lifetime

Will I have to pay income tax or a penalty tax if I withdraw money before retirement?

You will have to pay taxes on withdrawals as ordinary income. If taken before age 591⁄2, withdrawals may be subject to an additional 10% federal penalty tax. However, you may not have to pay the 10% penalty tax in certain circumstances

As a general rule, you can withdraw your contributions from a Roth IRA at any time without paying any tax or penalty. If you take a distribution within five years from the period funds were converted from an IRA, then an early distribution penalty may apply even though the distribution isn’t taxable. If you withdraw earnings, and the withdrawal is not a qualified distribution, it may be subject to the 10% early distribution penalty.

5

How an IRA works.Before opening an IRA, it’s important to understand some of the basic facts about this tax-advantaged retirement account.

Who can contribute?Anyone earning an income can contribute to an IRA. If you are married filing jointly and do not work — but your spouse does — you may also contribute to an IRA. There are two benefits of doing this:

• You can double your family’s retirement savings power

• You each have retirement funds in your own names

How much can I contribute?For the 2020 tax year, you can contribute $6,000 per year to an IRA if you’re age 49 or under. For anyone 50 or older, a catch-up provision allows you to contribute up to $7,000 per year4.

When can I contribute?You can open an IRA for a tax year from January 1 of a given year until April 15 of the following year. Contributions of any amount (up to the annual maximum) can be made any time in between for a Roth, Traditional or combination of the two — as long as you earn enough income to qualify for the annual maximum.

When can I access the money?You are allowed to take withdrawals after age 59½ without incurring penalties. There are, however, certain exceptions5 that allow you to withdraw from your account before then, such as:

• First-time home purchase

• College expenses

• Medical expenses

Your Allstate Agent can help you with any issues you may have about withdrawal or contributions options.

4 Contribution limits are for either a Traditional, Roth or combination of the two.

5 Penalty-free withdrawals for first-time home purchase are limited to $10,000 lifetime. Penalty-free withdrawals for college expenses are allowed only for amounts used to pay qualified higher education expenses. Penalty-free withdrawals for unreimbursed medical expenses are allowed only on expenses in excess of the medical deduction percentage of your Adjusted Gross Income (AGI).

6

Option Pros

No taxes or penalties

Money continues to grow tax-deferred

Broad range of investment options

May incur small administrative charges

Any loans from employer’s plan must be paid immediately

No taxes or penalties

Money continues to grow tax-deferred

New plan may not accept funds from previous plan

Investment options and access to money may be limited

No taxes or penalties

Money continues to grow tax-deferred

Can transfer money to another plan or IRA later

Investment options and access to money may be limited

May incur administrative charges

Potential to have a large sum of money at your disposal

Taxes and penalties could severely reduce savings

Future tax-deferred growth is lost

Cons

Leave money in the plan

Transfer money to a new employer’s plan

Take some or all of the money in a lump sum cash payment

Roll over money to a Traditional IRA with a direct rollover

Changing jobs or retiring?

A Rollover IRA can keep your retirement savings working for you.If you’re changing jobs or retiring, it may be tempting to take your retirement benefits in a lump sum. But that might cost you unnecessary penalties and taxes. Keeping your money in a tax-deferred plan is almost always a better idea.

Your Allstate Agent can help you avoid the pitfalls of penalties or taxes that come with this important decision — and determine if a rollover IRA is your best option. Below are some of the typical options you have with a retirement plan distribution. Evaluate the pros and cons — and then contact your Allstate Agent.

Choose from these typical retirement plan distribution options

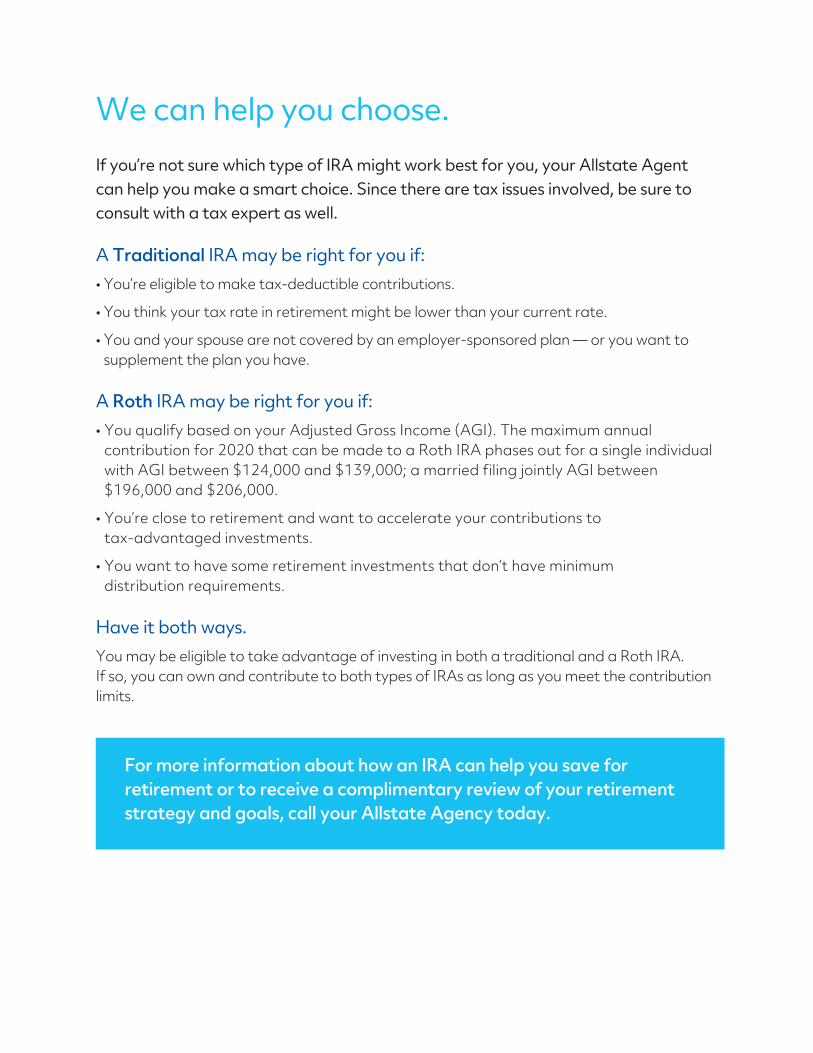

We can help you choose.If you’re not sure which type of IRA might work best for you, your Allstate Agent can help you make a smart choice. Since there are tax issues involved, be sure to consult with a tax expert as well.

A Traditional IRA may be right for you if:• You’re eligible to make tax-deductible contributions.

• You think your tax rate in retirement might be lower than your current rate.

• You and your spouse are not covered by an employer-sponsored plan — or you want to supplement the plan you have.

A Roth IRA may be right for you if:• You qualify based on your Adjusted Gross Income (AGI). The maximum annual

contribution for 2020 that can be made to a Roth IRA phases out for a single individual with AGI between $124,000 and $139,000; a married filing jointly AGI between $196,000 and $206,000.

• You’re close to retirement and want to accelerate your contributions to tax-advantaged investments.

• You want to have some retirement investments that don’t have minimum distribution requirements.

Have it both ways.You may be eligible to take advantage of investing in both a traditional and a Roth IRA. If so, you can own and contribute to both types of IRAs as long as you meet the contribution limits.

For more information about how an IRA can help you save for retirement or to receive a complimentary review of your retirement strategy and goals, call your Allstate Agency today.

Securities offered by Personal Financial Representatives through Allstate Financial Services, LLC (LSA Securities in LA and PA). Registered Broker-Dealer. Member FINRA, SIPC. Main Office: 2920 South 84th Street, Lincoln, NE 68506. (877) 232-2142. Check the background of this firm on FINRA’s BrokerCheck website http://brokercheck.finra.org.

This material is intended for general educational purposes only. Please note that neither Allstate nor any of its agents or representatives can give legal or tax advice. The brief discussion of taxes in this brochure may not be complete or necessarily current. The tax laws and regulations are complex and subject to change. For complete details, consult your attorney or tax advisor.

©2020 Allstate Insurance Company allstate.com 4/20

ALR82-4

You have more than a policy. You have Allstate.

Caring for customers and communities has always been a top priority for Allstate. Whether you’re looking for answers or advice you can trust, your Allstate agency is close to home and ready to help.

Allstate is committed to making insurance better. Along with fast and fair claim service, we have innovative tools, apps and extras to make everyday life easier for you.

Talk to your Allstate agency today and see what we mean when we say “You’re in good hands.®”