T2.1 Chapter Outline Chapter 2 Financial Statements, Taxes, and Cash Flow Chapter Organization...

41

T2.1 Chapter Outline Chapter 2 Financial Statements, Taxes, and Cash Flow Chapter Organization 2.1 The Balance Sheet 2.2 The Income Statement 2.3 Cash Flow 2.4 Taxes 2.5 Capital Cost Allowance 2.6 Summary and Conclusions CLICK MOUSE OR HIT SPACEBAR TO ADVANCE copyright © 2002 McGraw-Hill Ryerson,Ltd.

-

Upload

trevion-bartlett -

Category

Documents

-

view

214 -

download

0

Transcript of T2.1 Chapter Outline Chapter 2 Financial Statements, Taxes, and Cash Flow Chapter Organization...

T2.1 Chapter Outline

Chapter 2Financial Statements, Taxes, and Cash Flow

Chapter Organization

2.1 The Balance Sheet

2.2 The Income Statement

2.3 Cash Flow

2.4 Taxes

2.5 Capital Cost Allowance

2.6 Summary and Conclusions CLICK MOUSE OR HIT SPACEBAR TO ADVANCE

copyright © 2002 McGraw-Hill Ryerson,Ltd.

T2.1 Chapter Outline

Chapter 2Financial Statements, Taxes, and Cash Flow

Chapter Organization

2.1 The Balance Sheet

2.2 The Income Statement

2.3 Cash Flow

2.4 Taxes

2.5 Capital Cost Allowance

2.6 Summary and Conclusions CLICK MOUSE OR HIT SPACEBAR TO ADVANCE

copyright © 2002 McGraw-Hill Ryerson,Ltd.

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 3

T2.2 The Balance Sheet (Figure 2.1)

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 4

T2.2 The Balance Sheet

Components Assets (Current & Long-Term) Liabilities (Current & Long-Term) Owners Equity

Key concepts Liquidity Net Working Capital

• Current Assets minus Current Liabilities Debt vs. Equity Market vs. Book Value

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 5

Liquidity

refers to the speed and ease which an asset can be turned into cash

a highly liquid asset then is one which can be quickly sold and turned into cash - without a significant loss in value.

Assets are listed on the balance sheet in order of decrreasng liquidity

liquidity is important - running the day to day business and being in position to pay interest charges, retire loans, pay dividends, etc.

Trade-off - the more liquid an asset is the lower the return to that asset e.g. Cash balances vs inventory vs fixed assets

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 6

Debt v.s. Equity

Generally, when a firm borrows it gives the bondholder first claim on the firm’s cash flow and assets....equity holders receive the residual value or whatever is left after the creditors are paid.

Thus, shareholders equity is the residual difference between assets and liabilities.

The use of debt financing is called financial leverage - debt financing can magnify returns (gains and losses) to shareholders or equity holders

increases the potential return also increases the risk factor

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 7

Market Value vs Book Notes

Balance sheet values are book values GAAP requires assets to be shown at historical cost current asset book values can be very close to market value fixed assets can and often have major differences between

historical cost and market value

GAAP Accounting principles of objectivity and conservatism are the drivers behind historical cost.

• No argument about historical cost and because book is usually less than mkt. - they are also conservative( if mkt values fall along way below book - assets will be written down - good examples of this are the recent writedowns of assets by the likes of Nortel Cisco and many other high tech. firms

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 8

T2.3 Income Statement

Components Revenues Expenses

• Cash and non-cash

• Operating and non-operating Net Income Earnings per share Dividends

3 important concepts for Finance GAAP & Accrual Accounting & Matching Non-cash items Time and Costs

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 9

Cash Flow

Key concept in the study of Corporate Finance liquidity is about turning assets into cash investment analysis and capital budgeting is about discounted

cash flows valuation of securities is about future discounted cash flow at some

rate of discount e.g bonds - future interest payments and principle repayments discounted back at a certain rate

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 10

T2.4 Cash Flow

Cash flows are essential to valuation

In Finance, one of the main concern is the timing of cash flows. (another being the discount rate)

Since the income statement includes non-cash items, we will have to adjust it to get information on cash flows

Balance sheet activity plays an important role in the determination of the cash balance (e.g.)

Collections on accounts receivable

Borrowing on accounts payable

Work with reported financial statements to determine historical cash flow.

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 11

Cash Flow

Cash flow from an historical perspective - calculated from financial statements - our focus in this chapter

how to calculate

projected cash flow - look at in later chapters as we move into the question of valuation of investments and securities

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 12

T2.4 GAAP versus Cash Flow Time Line

Revenue

recognized

and

matched

expenses

Sale of goods

on credit

Time

Pay Payroll Pay Collect

for checks utilities accounts

raw goodsissued receivable

Cash flowCash flowCash flow Cash flow

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 13

T2.6 Cash Flow Summary

I. The cash flow identityCash flow from assets = Cash flow to creditors (bondholders)

+ Cash flow to stockholders (owners)

This is based upon the balance sheet identity: Assets = Liabilities + Equity

The equivalent cash flow statement is: cash flow to creditors

Cash flow from assets = +

cash flow to stockholders

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 14

T2.6 Cash Flow Summary (cont’d)

II. Cash flow from assetsCash flow from assets = Operating cash flow

– Net capital spending – Additions to net working capital (NWC)

where Operating cash flow = Earnings before interest and taxes (EBIT)

+ Depreciation – Taxes Net capital spending = Ending net fixed assets –

Beginning net fixed assets+ Depreciation

Change in NWC = Ending NWC – Beginning NWC

III. Cash flow to creditorsCash flow to creditors = Interest paid – Net new borrowing

IV. Cash flow to stockholdersCash flow to stockholders = Dividends paid – Net new equity raised

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 15

T2.5 Cash Flow Example

Balance Sheet

Beg End Beg End

Cash $100 $150 A/P $100 $150

A/R 200 250 N/P 200 200

Inv 300 300 C/L 300 350

C/A $600 $700 LTD $400 $420

NFA 400 500 C/S 50 60

R/E 250 370

$300 $430

Total $1000 $1200 Total $1000 $1200

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 16

T2.5 Cash Flow Example (continued)

Income Statement

Sales $2000

Costs 1400

Depreciation100

EBIT 500

Interest 100

Taxable Income 400

Taxes 200

Net Income$200

Dividends 80

Addition to R/E $120

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 17

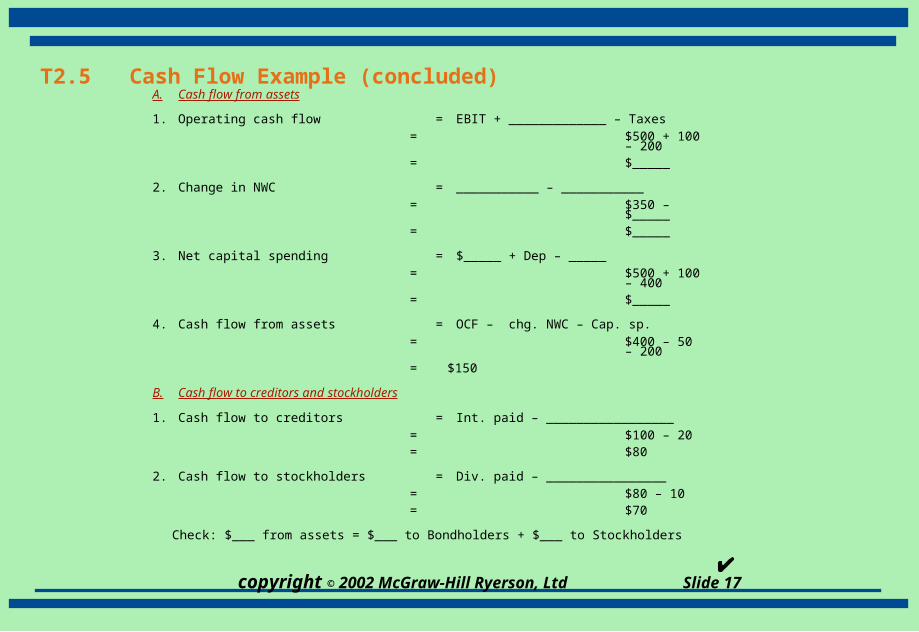

T2.5 Cash Flow Example (concluded)A. Cash flow from assets

1. Operating cash flow = EBIT + _____________ – Taxes= $500 + 100

– 200= $_____

2. Change in NWC = ___________ – ___________= $350 –

$_____= $_____

3. Net capital spending = $_____ + Dep – _____= $500 + 100

– 400= $_____

4. Cash flow from assets = OCF – chg. NWC – Cap. sp.= $400 – 50

– 200= $150

B. Cash flow to creditors and stockholders

1. Cash flow to creditors = Int. paid – _________________= $100 – 20= $80

2. Cash flow to stockholders = Div. paid – ________________= $80 – 10= $70

Check: $___ from assets = $___ to Bondholders + $___ to Stockholders

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 18

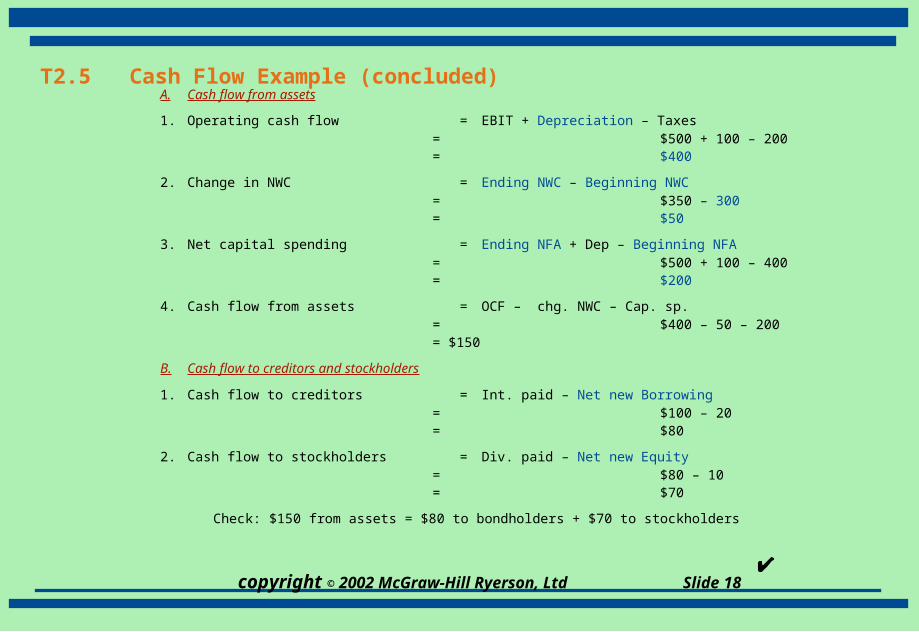

T2.5 Cash Flow Example (concluded)A. Cash flow from assets

1. Operating cash flow = EBIT + Depreciation – Taxes= $500 + 100 – 200= $400

2. Change in NWC = Ending NWC – Beginning NWC= $350 – 300= $50

3. Net capital spending = Ending NFA + Dep – Beginning NFA= $500 + 100 – 400= $200

4. Cash flow from assets = OCF – chg. NWC – Cap. sp.= $400 – 50 – 200= $150

B. Cash flow to creditors and stockholders

1. Cash flow to creditors = Int. paid – Net new Borrowing= $100 – 20= $80

2. Cash flow to stockholders = Div. paid – Net new Equity= $80 – 10= $70

Check: $150 from assets = $80 to bondholders + $70 to stockholders

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 19

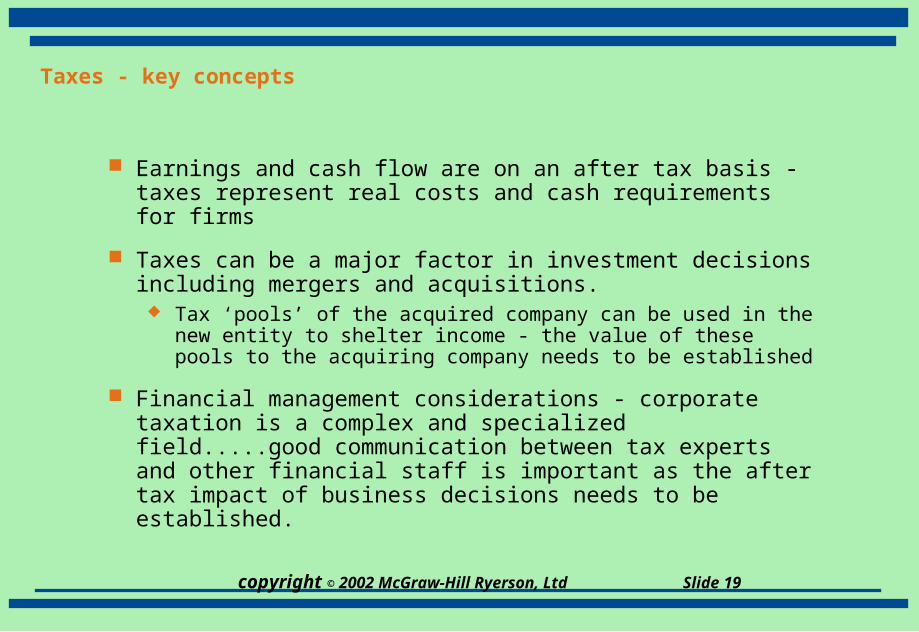

Taxes - key concepts

Earnings and cash flow are on an after tax basis - taxes represent real costs and cash requirements for firms

Taxes can be a major factor in investment decisions including mergers and acquisitions.

Tax ‘pools’ of the acquired company can be used in the new entity to shelter income - the value of these pools to the acquiring company needs to be established

Financial management considerations - corporate taxation is a complex and specialized field.....good communication between tax experts and other financial staff is important as the after tax impact of business decisions needs to be established.

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 20

T2.7 Taxes

Key issues: What is an average tax rate? What is a marginal tax rate? Why do we pay attention to marginal tax rates? What are corporate tax rates? What are individual tax rates? How does the difference between corporate and individual

tax rates affect corporate finance?

How do tax rates relate to the goal of corporate finance?

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 21

T2.7 Individual Tax Rates

FEDERAL

Taxable Income $ Tax Rate 0- 31677 16%

31678-63354 22%

63355-103000 26%

103001- UP 29%

Provincial

generally applied as a % of the Basic Federal Tax - exception Alberta

Alberta - 10%

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 22

T2.7 Marginal versus Average Tax Rates

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 23

T2.7 Individual Tax Rates

SELECTED PROVINCIAL(Table 2.5)

Resident of Percentage of Basic Federal Tax

Alberta 44%

Newfoundland 62

Prince Edward Island 57.5

Saskatchewan 48

Northwest Territories 45

Yukon Territory 50

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 24

Taxes on Investment Income

taxes on dividends and capital gains

dividends two clear goals -

• avoidance of double taxation with corporations paying dividends from after tax income and full taxation in the hands of shareholders -> dividend tax credit

• this tax shelter applies to dividends paid by Canadian Corporations thus encouraging Canadian investors to invest in Canadian firms

Capital Gains rates are coming down with 50% of the gain now being taxed - down

from 75% tax deferral from only realized gains being taxed results in lower

‘effective tax’

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 25

T2.8 ILLUSTRATION OF DIVIDEND TAX CREDIT FOR ALBERTA RESIDENTSMarginal Tax Rate 17% 24% 29%

Dividends $1,000 $1,000 $1,000

Gross up at 25% 250 250 250

Grossed up dividends 1250 1250 1250

Federal Tax on dividends 212.50 300.00 362.50

Less Dividend Tax Credit

(13.333% x $1,250) (166.67) (166.67) (166.67)

Federal Tax Payable 45.83 133.33 195.83

Provincial Tax at 44% of Federal Tax 20.17 58.67 86.17

Total Tax 66.00 192.00 282.00

Effective Combined Tax Rates 6.6% 19.2% 28.2%

NOTE: Marginal tax rates apply to incomes of less than 32,000 (17%), more than 32,000 but less

than 64000 (25%), and more than 64,000 (29%)

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 26

T2.9 Corporate Tax Rates

FEDERAL ALBERTA COMBINED

Basic Corporations 26.1 13.0% 39.1%

Manufacturing and Processing 22.1 13.0 35.1

All Small Corporations 13 4.5 17.5(Taxable Income below $200 thousand)

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 27

Taxable Income

taxable income is different from net income net income needs to conform to GAAP taxable income is calculated according to tax rules

established by the various taxing authorities e.g. book depreciation vs capital cost allowance

• book depreciation attempting to match revenues earned from the use of a tangible depreciable asset with the costs associated with the asset

• capital cost allowance - allowable deductions associated with various types of assets - patchwork of tax rules that often have stemmed from government budget and economic development objectives.

Income is taxed differently across various industries with the ‘rules’ continually changing

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 28

Capital Cost Allowance

Key concepts and terms: Classes of assets Asset purchases and sales

• net acquisitions are used if multiple purchases

• one half year rule applies to net acquisitions

• sale - the balance in the pool is reduced by the lesser of sale price or original cost

Termination of asset pool

• terminal loss occurs when there is remaining UCC after the last asset disposal - this amount is fully tax deductible

• recaptured CCA occurs with a negative UCC after the last asset disposal - this amount is fully taxable

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 29

T 2.10 Capital Cost Allowance - Depreciation for tax purposes

Class Rate Assets

1 4% Buildings acquired after 1987

8 20% Furniture, photocopiers

10 30% Vans, trucks, tractors and computer equipment

13 Straight-line Leasehold improvements

16 40% Taxicabs and rental cars

22 50% Pollution control equipment

43 30% Manufacturing equipment

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 30

T2.11 CCA Example

Depreciation on $22,000 Photocopier (CCA Class 8)

Year UCC t CCA UCC t+1

1 11,000 2,200 $8,800

2 19,800 3,960 15,840

3 15,840 3,168 12,672

4 12,672 2,534 10,138

5 10,138 2,028 8,110

6 8,110 1,622 6,488

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 31

T2.12 Hermetic, Inc. Balance Sheet

as of December 31($ in thousands)

Assets 1998 1999

Current assets

Cash $ 45 $ 50

Accounts receivable 260 310

Inventory 320 385

Total $ 625$ 745

Fixed assets

Net plant and equipment 985 1100

Total assets $1610 $1845

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 32

T2.12 Hermetic, Inc. Balance Sheet (concluded)

Liabilities and equity 1998 1999

Current liabilities

Accounts payable $ 210 $ 260

Notes payable 110 175

Total $ 320$ 435

Long-term debt 205 225

Stockholders’ equityCommon stock and

paid-in surplus 290 290

Retained earnings 795 895

Total $1085 $1185

Total liabilities and equity $1610 $1845

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 33

T2.13 Hermetic, Inc. Income Statement

($ in thousands)

Net sales $710.00

Cost of goods sold 480.00

Depreciation 30.00

Earnings before interest and taxes $200.00

Interest 20.00

Taxable income 180.00

Taxes 53.45

Net income $126.55

Dividends 26.55

Addition to retained earnings $100.00

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 34

T2.14 Hermetic, Inc. Cash Flow from Assets

Cash flow from assets: Operating cash flow:

EBIT $ 200.00

+ Depreciation + 30.00

– Taxes – 53.45

$ 176.55 Change in net working capital:

Ending net working capital $ 310.00

– Beginning net working capital – 305.00

$ 5.00 Net capital spending:

Ending net fixed assets $ 1,100.00

– Beginning net fixed assets – 985.00

+ Depreciation + 30.00

$ 145.00

Cash flow from assets:

$ 26.55

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 35

T2.14 Hermetic, Inc. Cash Flow from Assets (concluded)

Total cash flow to creditors and stockholders:

Cash flow to creditors:

Interest paid $ 20.00

– Net new borrowing – 20.00

$ 0.00

Cash flow to stockholders:

Dividends paid $ 26.55

– Net new equity raised 0.00

$ 26.55

Cash flow to creditors and stockholders $ 26.55

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 36

T2.16 Solution to Problem 2.12

The December 31, 1999 balance sheet Pearl Jelly, Inc. showed long-term debt of $2 million, and the December 31, 2000 balance sheet showed long-term debt of $2.9 million. The 2000 income statement showed interest expense of $700,000. What was cash flow to creditors during 1999?

Cash flow to creditors = Interest paid – Net new borrowing

Interest paid = $700,000

Net new borrowing = $_______ – 2 million = $_______

Cash flow to creditors = $700,000 – (_______)

= _______

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 37

T2.16 Solution to Problem 2.12

The December 31, 1999 balance sheet Pearl Jelly, Inc. showed long-term debt of $2 million, and the December 31, 2000 balance sheet showed long-term debt of $2.9 million. The 2000 income statement showed interest expense of $700,000. What was cash flow to creditors during 1999?

Cash flow to creditors = Interest paid – Net new borrowing

Interest paid = $700,000

Net new borrowing = $2.9 million – 2 million = $900K

Cash flow to creditors = $700,000 – 900,000

= –$200,000

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 38

T2.17 Solution to Problem 2.13

The December 31, 1999 balance sheet Pearl Jelly, Inc. showed $500,000 in the common stock account, and $6.6 million in the additional paid-in surplus account. The December 31, 1999 balance sheet showed $550,000 and $7.0 million in the same two accounts. If the company paid out $300,000 in cash dividends during 2000, what was the cash flow to stockholders for the year?

Cash flow to stockholders = Dividends paid – Net new equity Dividends paid = ________ Net new equity = (________+________) – ________ + ________)

Cash flow to stockholders = ________– ________ = ________

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 39

T2.17 Solution to Problem 2.13

The December 31, 1999 balance sheet Pearl Jelly, Inc. showed $500,000 in the common stock account, and $6.6 million in the additional paid-in surplus account. The December 31, 1999 balance sheet showed $550,000 and $7.0 million in the same two accounts. If the company paid out $300,000 in cash dividends during 2000, what was the cash flow to stockholders for the year?

Cash flow to stockholders = Dividends paid – Net new equity Dividends paid = $300,000 Net new equity = ($550,000 + 7m) – ($500,000 + 6.6m) = $450,000

Cash flow to stockholders = $300,000 – 450,000 = –$150,000

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 40

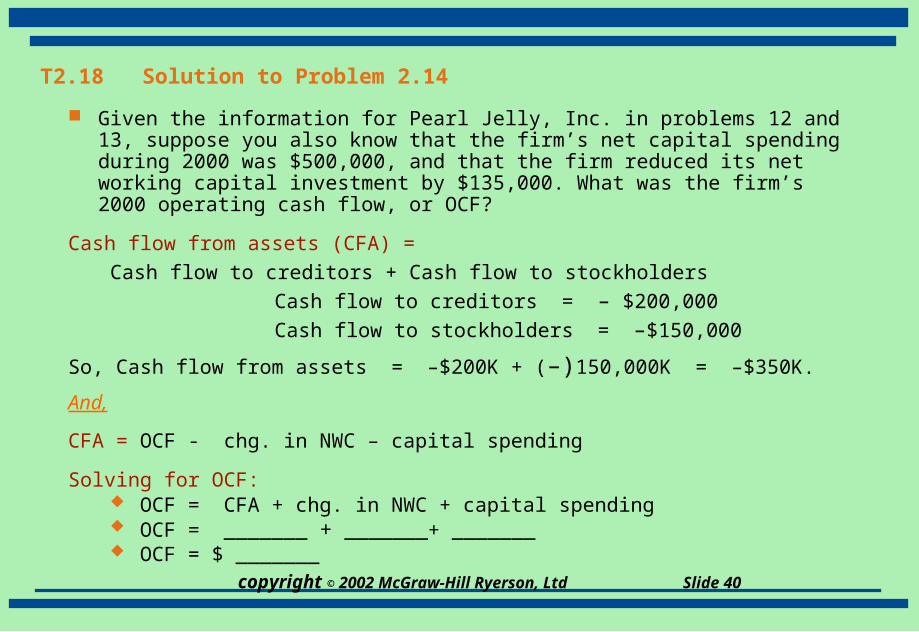

T2.18 Solution to Problem 2.14

Given the information for Pearl Jelly, Inc. in problems 12 and 13, suppose you also know that the firm’s net capital spending during 2000 was $500,000, and that the firm reduced its net working capital investment by $135,000. What was the firm’s 2000 operating cash flow, or OCF?

Cash flow from assets (CFA) =

Cash flow to creditors + Cash flow to stockholders

Cash flow to creditors = – $200,000

Cash flow to stockholders = –$150,000

So, Cash flow from assets = –$200K + (–)150,000K = –$350K.

And,

CFA = OCF - chg. in NWC – capital spending

Solving for OCF: OCF = CFA + chg. in NWC + capital spending OCF = _______ + _______+ _______ OCF = $ _______

copyright © 2002 McGraw-Hill Ryerson, Ltd Slide 41

T2.18 Solution to Problem 2.14

Given the information for Pearl Jelly, Inc. in problems 12 and 13, suppose you also know that the firm’s net capital spending during 2000 was $500,000, and that the firm reduced its net working capital investment by $135,000. What was the firm’s 2000 operating cash flow, or OCF?

Cash flow from assets (CFA) =

Cash flow to creditors + Cash flow to stockholders

Cash flow to creditors = – $200,000

Cash flow to stockholders = –$150,000

So, cash flow from assets = –$200K + (–)150,000K = –$350K.

And,

CFA = OCF – Chg. in NWC – Capital spending

Solving for OCF: OCF = CFA + Chg. in NWC + Capital spending OCF = –$350K + (– 135,000) + 500,000 OCF = $15,000