SZ16071557-fmfd-bsdownload.cib.com.cn/netbank/download/en/20160912en.pdfthose of the end of 2010...

261

2015 2015 ANNUAL REPORT INDUSTRIAL BANK CO.,LTD. Green Finance , Better Tomorrow Add: No. 154 Hudong Road, Fuzhou, Fujian, P.R.C T e l : (86)591-87839338 F a x : (86)591-87842633 P. C : 350003 www.cib.com.cn THE FIRST EQUATOR BANK IN CHINA

Transcript of SZ16071557-fmfd-bsdownload.cib.com.cn/netbank/download/en/20160912en.pdfthose of the end of 2010...

2015

2015ANNUAL REPORT

IND

USTR

IAL BANK C

O.,LTD

.

Green Finance , Better Tomorrow

Add: No. 154 Hudong Road, Fuzhou, Fujian, P.R.CT e l : (86)591-87839338F a x : (86)591-87842633P. C : 350003www.cib.com.cn

THE FIRST EQUATOR BANK IN CHINA

1

CONTENTS

Chairman’s Statement 2

President’s Report 4

Important Notice 7

Definitions 10

CorporateProfileandKeyFinancialIndicators 11

BusinessOverviewoftheCompany 19

ManagementDiscussionandAnalysis 23

SignificantIssues 81

ShareCapitalChangesandShareholdersofOrdinaryShares 87

MattersRegardingPreferredShares 91

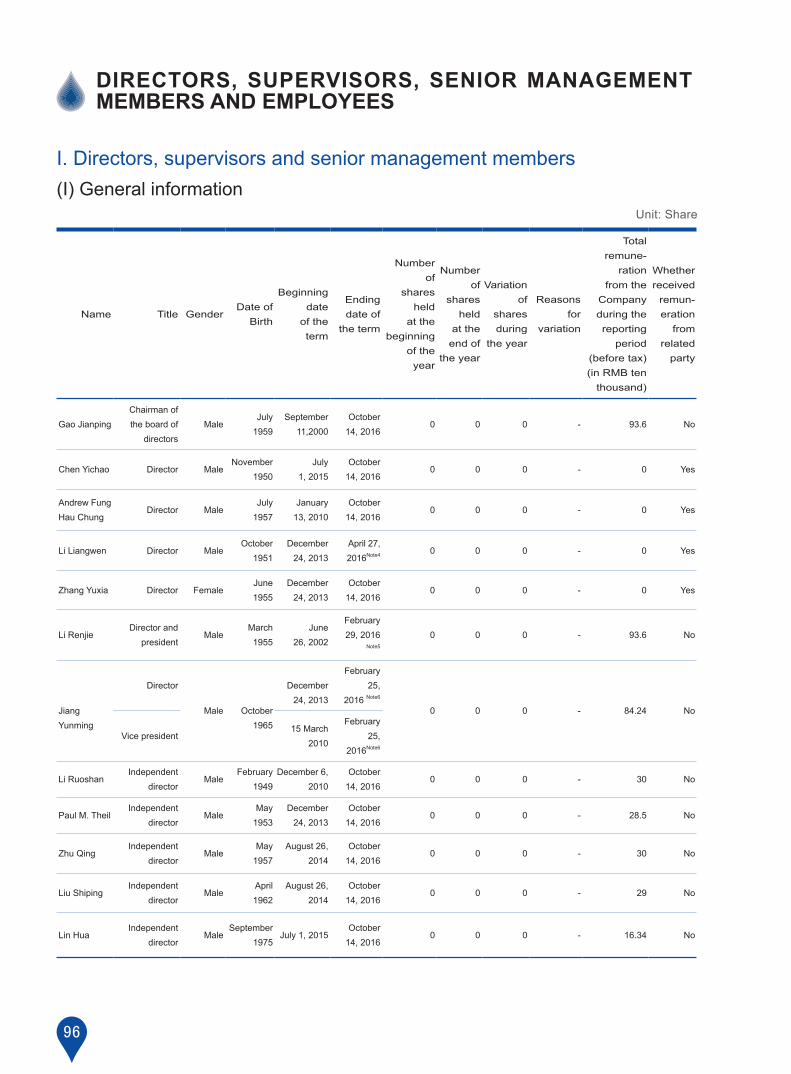

Directors,Supervisors,SeniorManagementMembersandEmployees 96

CorporateGovernance 107

FinancialStatements 115

DocumentsAvailableforInspection 115

Appendix:Auditors’ReportandFinancialStatements 116

TheCompany’sOrganizationalStructure 258

2

Theyear2015witnessedthesuccessfulcompletionof thisroundof thefive-yeardevelopmentplan.Over thepastfiveyears, facing thechallengesincluding theslowdown inmacro-economicgrowth,accelerated interest rate liberalization,cross-bordercompetition formatand intensifiedfinancialmarketfluctuation,theCompanyactivelyadaptedtothenewnormalofeconomicdevelopment,andimplementedforward-lookingstrategicdeployment,flexiblygraspedmarketopportunitiesanddeepenedreformandtransformationbyleveragingitsmarket-orientedsystemsandmechanismsandteamculture.Therefore,theCompanyachievedfruitfuloperatingresults.

Overthepastfiveyears, the industrypositionfurther improvedwiththekeyperformanceindicatorsdoubled.Asat theendof2015,theCompany’s totalassets,balanceofdeposits ,balanceof loans,equity interestattributable to theordinaryshareholdersof theparentcompanyamounted toRMB5.30trillion,RMB2.48trillion,RMB1.78trillion,andRMB287.743billionrespectively,being2.86times,2.19times,2.08times,and3.13timesofthoseoftheendof2010respectively,enablingittorankthetop10DomesticBanks,Top50GlobalBanks,Top500WorldEnterprises,andtakethe6thplaceinallAsianbankswithregardtocompetitivenessofAsianbanks.TheBankactivelyandfullydisclosedrisks.ThebalanceofNPLswrittenoffandtransferredduringthepastfiveyearsaccumulatedtoapproximatelyRMB80billion,andtheNPLratioattheendof2015was1.46%.Theassetsqualitywasoverallcontrollable.Onthatbasis,netprofitattributabletotheshareholdersoftheparentcompanyaccumulatedtoapproximatelyRMB200billion,cashdividendsdistributedwereoverRMB40billion,averagerateofreturnontotalassetswas1.17%,andaveragerateofreturnonnetassetswas22.72%duringthepastfiveyears.TheBankmaintainedastableandsoundfinancialpositionandwontheawardofthe“Asian Bank Offering the GreatestReturntoShareholders”.

Over thepast fiveyears, thepositionasamainbankinggroupwasestablishedwith thesmoothprogressofcomprehensiveoperating layout.FollowingtheestablishmentofIndustrialBankFinancialLeasingCo.,Ltd.in2010,theCompanymergedUnionTrustLimitedandrenameditasChinaIndustrialInternationalTrustLimitedin2011,establishedCIBFundManagementCo.,Ltd.in2013,andIndustrialConsumerFinanceCo.,Ltd.in2014,andpurchasedNingboShanliFuturesBrokerCo.,Ltd.andrenameditasCIBFuturesCo.,Ltd.in2014,establishedChinaIndustryDigitalFinancialService(Shanghai)Co.,Ltd.andIndustrialEconomicResearchandConsultingCo.,Ltd. in2015.Meanwhile, theCompanyconstantlyexpandeditsbusinessscopeviareinvestmentofsubsidiaries,andtheCompanyhasbecomeoneofthefewdomesticbankholdinggroupsthatpossessfullfinanciallicenses.TheBankinsistedongivingfullplaytotheadvantageofmulti-licenseoperation,andcontinuedtoexpandthescopeofthecollaborationandlinkagebetweenparentcompanyandsubsidiariesandbetweensubsidiaries,whileenablingthetheGrouptoimproveitsoverallcompetitioncapability,customerserviceabilityandbusinesscomprehensiverevenue.Meanwhile,theGroupwonthe“AnnualFinancialHoldingGroupAward2015”.

Over thepastfiveyears, theeffectivenessofoperational transformationgradually revealedwith theconsensusreachedoncapitalsavingconcept.Adheringtothecapitalsupplementationprincipleof“givingprioritytointernalaccumulationwithexternalsourcesasthesupplement”,theCompanysupplementedcoretieronecapitalofoverRMB150billionbyprofitretentionduringthepastfiveyears.TheCompanyfurtheroptimizedshareholderstructureandraisedcoretieronecapitalofRMB23.532billionthroughprivateplacementtoshareholdersincludingPICCandChinaNationalTobaccoCorporation.TheCompanyactivelycarriedoutcapital instrument innovation,became thefirstbatchofpreferredsharepilotbanks, raised tieronecapitalofRMB25.905billion,andcompletedtwosupplementationoftiertwocapitalofRMB30billionintotal, therebypromotingthesustainableandhealthydevelopmentof itsvariousbusinesses.Attheendof2015,theCompany’snetcapitalreachedRMB383.504billion,being3.43timesofthatof theendof2010,withcapitaladequacy ratioof11.19%andadequacy ratioofcore tieronecapitalof8.43%.TheCompanyestablished theall-roundandactivecapitalmanagementconcept,promoted transformationofoperationmodeandcultivationofstrategickeybusiness throughcapitalmanagement,builtcharacterizedoperationanddifferentiatedcompetitionadvantages.Currently,theCompanyhasbecomeamainstreamcompetitorin thedomesticurbanizationfinance,apioneer in thegreenfinance,a forerunner in the interbankbusinessfinanceandanadvocatorofpensionfinance.Moreover,theCompanytooktheleadinpositioningitselfformultiplemarkets,suchasmoneymarket,capitalmarket,preciousmetalsmarket,foreignexchangemarket,andderivativesmarket,etc.,therebyenjoyingfirst-moveradvantages.

Over thepastfiveyears, the reformofbusinessgovernancesystemconstantlydeepenedwith thestableoperationofcorporategovernance.TheCompanysmoothlycompleted theworkhandoverof thepresidentand two termsofchairmenof theboardofsupervisors,appointed fournewvicepresidents, thereby realizingastable transitionof theseniormanagement teamwhile following itsoperationstrategies.TheCompanysuccessfullycompleted thechangesof the8thsessionof theboardofdirectorsand resignandadditionofpartofdirectorsduringsuchsession,continued tostrengthen theconstructionofprofessionalabilityanddecision transmissionmechanismof theboardofdirectors, therebyenhancing thestrategymanagementandcontrolabilityaswellasstrategy implementationability.TheCompanywasconsecutivelygranted the“Award of the Board of Directors”byShanghaiStockExchange in2011and2012.Basedon thedevelopment trendofbanking industryandactualconditionsof theCompany, theCompanysuccessfully implemented theprofessional reformsoncorporatefinanceandfinancialmarket, furtherdeepened thereformof retailfinanceandsupporting reforms including the reformon riskmanagementsystem,enabling theBankatall levels toexperiencesignificantchangesintheorganizationsystemandpromotionmodeoftheoperationalmanagementandfurtherimprovetheprofessionaloperationability,internalgrowth impetusandrefinedmanagement level.TheCompanyadapted to thereformrequirementsbyestablishingHongKongBranch,which isoneessentialsteptointernationaldevelopment.Meanwhile,theCompanyadvancedstocknetworktransformationandcommunitybankconstructionafterbasicallycompletingthedeploymentofnationwidenetwork,accelerated integrated innovationof traditionalphysicalchannelsandInternetchannels,therebyfurtherenhancingitsspecializedservicescapability.

Lookingaheadintothe“13thFive-Year”,thedevelopmentenvironmentathomeandabroadwillremaincomplicated,theworldeconomyrecoverywillbeatortuousprocessinprofoundadjustment,thedomesticeconomywilldeepenreformtorealizeashift fromolddevelopmentmomentumintothenewoneand the industry transformationandupgrading.TheCompanywillproactivelyservenationalstrategies, insiston theoveralldirectionofmarketization, integrationand internationalization,adapt to thenewnormaleconomy, integrate itself intonewfinancialpattern, furtheremphasizesoundness, innovation,coordination, refinementandreformsofsystemsandmechanisms,consolidateandexpand thepositionandadvantagesoftraditionalbusinesses,andcultivateandexpandemergingstrategicbusinessboundaryandspace,aimingtofurtherenhancetheoverallstrengthoftheGroup,andcreategreatervalueforrelevantstakeholdersincludingcustomers,employeesandshareholders.

Chairman:

Chairman’s Statement

3

2 0 1 5 ANNUAL REPORT

Chairman:Gao Jianping

4

In2015,domesticmacroeconomycontinuedtoslide,financialmarketfluctuatedintensively,commercialbanksfacedgreatchallengesinitsoperationandmanagement.Facingthecomplexandseverebusinessenvironment,andcenteringonoperationtargetsdeterminedbytheboardofdirectorsatthebeginningoftheyear,theCompanyflexiblyadjusteditsoperatingstrategy,profoundlypromotedreformandtransformation,vigorouslyconsolidatedthedevelopment foundation,successfullywithstoodvarious internalandexternal tests,achievingoperating resultswhicharegenerallybetter thanexpectedandsuccessfullyconcluding this roundofFive-yearPlan.Asat theendof the reportingperiod, the totalassetsof theCompanyreachedRMB5,298.880billion,up20.25%fromthebeginningof the reportingperiod.Netprofitattributable toshareholdersof theparentcompany for theyearreachedRMB50.207billion,representingayear-on-yearincreaseof6.51%.Stickingtobroadensourcesofincomeandreduceexpenditurewhilestrengtheningcostcontrolandmanagement, theCompanymaintainedacost-to-incomeratioat21.59%,remainingata relatively lower levelwithintheindustry.Influencedbythedownturnofmacroeconomyandriskdisclosureofcertainindustriesandareas,theassetsqualitydecreasedslightly,withtheratioofNPLsattheendofthereportingperiodstandingat1.46%,representinganincreaseof0.36percentagepointascomparedwiththebeginningofthereportingperiod.However,theoverallassetsqualityremainedreasonableandcontrollable.TheCompanyincreasedprovision,withprovisionimpairmentlossesofassetsmadeduringthereportingperiodofRMB45.260billion,representingayear-on-yearincreaseof74.72%,whileprovisioncoveragewasadequateoverall,withprovisioncoverageratioat210.08%,andprovision-to-loanratioat3.07%.

In2015,theCompanyprofoundlypromotedgroupoperationsandfurtherstrengthenedmulti-marketoperationandcomprehensiveservicecapability.IndustrialEconomicResearchandConsultingCo.,Ltd.openedsmoothly,CIBDigitalFinancialServiceCo.,Ltd.officiallyestablished,and thesubsidiaries furtherdiversified.TheCompanyhasbecomeoneof thedomesticbankgroupswithmostabundantfinancial license resources.Eachsubsidiarymaintainedarapidbusinessdevelopment,andtheindustrialpositionandprofitcontributiontotheGroupcontinuedtoincrease.Supportingmechanismssuchasexaminationandassessment further improved,and intra-groupcooperationand linkagebecamesmoother.Trans-department,trans-line,trans-institution,andtrans-businesssegmentcooperationandlinkagehavebeenmoreintimateandefficient,andcooperationandlinkagebetweenparent-subsidiarycorporationsandamongsubsidiariescontinued toexpand.Theconstructionofcorebusinessclusterof theGroupmadesignificantachievement,and thebusiness formatof“sizeable investment,sizeableassetmanagementandsizeablewealthmanagement” further shaped.

In2015,theCompanypersistedinpromotingoperationaltransformationandfurtheroptimizedbusinessdevelopmentpattern.Basicservicesfocusingon transactionbanksachievedobviousprogress.Cashmanagementbusinessbasiswasstrengthenednotably,cross-bordersettlementbusinessrecordedastablegrowth,annualRMBandforeigncurrencycross-bordersettlementbusinessvolumereachedarecordhighofUSD122.394billion.AndTheCompanycontinuedtodevelopandapplynewtypepaymentandsettlementinstrumentsincluding“CloudQuickPass”,inter-bankpayrollservice,onlinecardsettlement,electronic foreignexchangesettlementandsale, therebysteadilypromoting thecompetitivenessof itspaymentandsettlementbusiness.TheCompanyvigorouslydevelopeddirectbanks,WeChatbanks,andremotebanks,andonlineandofflinechannel integrationandlinkagehavebeenmoreefficient.Keybusinessescharacterizedbylightcapitalandlightassetsmaintainedagooddevelopmentmomentum.Thescaleof theunderwritingofdebt issuingandfinancing instruments reachedRMB384.245billion, representingayear-on-year increaseof22.14%.DailyaveragestockbalanceoffinancialproductsreachedRMB1,347.641billion,representingayear-on-yearincreaseof60.27%.ThescaleofassetscustodyreachedRMB7,213.948billion, representingan increaseof52.64%ascomparedwith thebeginningof thereportingperiod.ThevolumeoftradeoffuturesexchangeswasRMB1,912.499billion,takingtheleadinthemarket.TheCompanycontinuedtoexploreandpromotetheinnovativeservices taking theserviceofcapitalmarketas theprimaryorientation,andmaintainedagooddevelopmentmomentum invariousbusinessesincluding industry funds,PPPbusiness,perpetual capital securities,asset securitization,privateplacementof listedcompaniesand financial

consultancy.

In2015, theCompanysteadilypromotedvariousreforms,and furtherconsolidated the foundation fordevelopment.TheCompanycomprehensivelydeployedanddeepenedthereformofriskmanagementsystemsandmechanisms,andorderlypromotedthereformofthecreditcardoperationandmanagementsystemsandmechanisms,comprehensivelyoptimized the labororganizationmodeofbusinesshalls,and further improved thereformof the franchisedmechanismof the inter-bankbusiness, therebyobviouslyenhancing theeffectivenessofmanagement.TheCompanysparednoeffortstopreventandcontrolnon-performingassets,soastoachieveoverallstableassetqualityatalllevelsoftheBank.TheCompanycontinuouslyenhanced innovations in riskmanagementmodeandoperation,andvigorouslysupported innovationbusinessdevelopment.TheCompanysolidlycarried out the “two enhancements, two containment” and “lookingback”special inspections,andprofoundlycarriedoutcheckingofemployeebehaviorrisk,therebyfurtherimprovingtheeffectivenessofcomplianceinternalcontrolmanagement.TheCompanycontinuedtoincreaseinvestmentin informationtechnologyconstruction,exploredtheleadingrolesofapplyingscienceandtechnologiesinthebusinessdevelopment,andconstantlyimprovedtheelectronic,informationandintelligentlevelsofthebusinessoperation.

Lookingahead into2016,moreuncertaintieswill continue toweighon theworldeconomy.Prominentcontradictionsandproblemsarising fromthedecline indomesticeconomicgrowth, industrialproductprice,entityenterpriseprofits,andfiscal revenuegrowthand increaseofprobabilityofoccurrenceofeconomicriskwillcontinue,creditrisk,exchangerateriskandinterestrateriskfacedbycommercialbankswillbelikelytoincrease,andtheoperatingpressurewillfurtherincrease.Meanwhile,theadvancementofstructuralreformsatthesupplyside,activecapitalmarket,developmentofnewtechnologiesandformatswillalsobringalotofnewstructuralopportunities,enablingcommercialbankstohavealargeroomtodevelop.Underthecorrectleadershipoftheboardofdirectorsandcaresandsupportfromallcommunities,themanagementoftheCompanywilladheretoenhancingadvantageswhileavoidingdisadvantages,notonlyproperlydealwithimpactsofavarietyofrisks,butalsostrivetograspnewmarketopportunities,aimingtoachievereasonablebusinessgrowth,maintainoverallstableassetqualityandprofitabilityinthenewyear,aswellascreateagoodstartforthenewroundoffive-yeardevelopment.

President’s Report

President:

5

2 0 1 5 ANNUAL REPORT

President: TaoYiping

6

Chairman of the Board of Supervisors :JiangYunming

7

2 0 1 5 ANNUAL REPORT

TheCompany’s board of directors, board of supervisors, directors, supervisors and senior management membersherebywarrant that the informationcontained in this report is free fromfalserepresentation,misleadingstatementormaterialomission,andassumejointandseveralliabilities.

TheCompany’sannual report2015and itsabstractwerereviewedandapprovedat the18thmeetingof the8thsessionof theboardofdirectorsonApril27,2016.Therewerenodirectors,supervisorsorseniormanagementmemberswhocouldnotwarrantordisagreedwith the truthfulness,accuracyandcompletenessofthecontentsofthisannualreport.

The financialdataand indicatorscontained in thisannual reportwereprepared incompliancewiththePRCGenerallyAcceptedAccountingPrinciples.Unlessotherwisespecified, they represented theconsolidateddata.ThemonetarysumsexpressedinRMBinthisannualreport.

DeloitteToucheTohmatsuCertifiedPublicAccountantsLLPhasaudited theCompany’s financialstatements2015 inaccordancewith theChineseAuditingStandards (“CAS”) and has issued a standard auditor’sreportwithunqualifiedopinions.

TheCompany’schairmanGaoJianping,presidentTaoYipingandgeneralmanagerof the financialdepartmentLi Jianherebywarrant that the financial statements in theannual report2015are true,accurateandcomplete.

Theplanofdividendsdistributionforordinaryshareforthereportingperiodconsideredbytheboardofdirectors:basedon the totalcapitalof19,052,336,751shares,cashdividendofRMB6.10(inclusiveoftax)shouldbedistributedforevery10ordinaryshares.

Theplanofdividendsdistribution forpreferredshares isas follows:proposeddividends forpreferredsharesareRMB1.147billion in total.Ofwhich, the total nominal valueof thepreferredsharesof“IndustrialBankP1”isRMB13billion,theinterestperiodwasfromJanuary1toDecember31,2015,proposeddividendsareRMB780millionwithanannualdividendyieldof6%;thetotalnominalvalueofthe preferred shares of “IndustrialBankP2”isRMB13billion,theinterestperiodwasfromJune24toDecember31,2015,proposeddividendsareRMB367millionwithanannualdividendyieldof5.40%.

Investorsareadvised to read the fullcontentof thisannual reportcarefully.Perspectiveand forward-lookingstatements regarding futurefinancialconditions,operatingperformance,businessdevelopmentandbusinessplancontainedinthisreportdonotconstituteanysubstantivecommitmentoftheCompanytoinvestors.Investorsshouldpayattentiontoinvestmentrisks.

Theboardofdirectorsspecially reminds investors that therisk factors theCompany issubject tohavebeen listed indetail in this report.Please refer to“ManagementDiscussionandAnalysis” for risk factortheCompanyissubjecttoandtheriskmanagementanalysis.

ImPoRtant notICe

8

9

2 0 1 5 ANNUAL REPORT

10

DefInItIonS

Inthisreport,unlessthecontextotherwisespecified,thefollowingtermshavethemeaningssetforthbelow:

IndustrialBank/theCompany IndustrialBankCo.,Ltd.

CentralBank ThePeople’s Bank of China

CSRC ChinaSecuritiesRegulatoryCommission

CSRCFujianBureau FujianBureauunderChinaSecuritiesRegulatoryCommission

CBRC ChinaBankingRegulatoryCommission

CBRCFujianBureau FujianBureauunderChinaBankingRegulatoryCommission

DeloitteToucheTohmatsu DeloitteToucheTohmatsuCertifiedPublicAccountantsLLP

IndustrialLeasing IndustrialBankFinancialLeasingCo.,Ltd.

IndustrialTrust ChinaIndustrialInternationalTrustLimited

IndustrialFund CIBFundManagementCo.,Ltd.

IndustrialConsumerFinance IndustrialConsumerFinanceCo.,Ltd.

IERCC IndustrialEconomicResearchandConsultingCo.,Ltd.

Newcapitalrequirements beingmeasured inaccordancewith theCapitalRules forCommercialBanks(Provisional)(Implementedfrom2013)ofCBRC

Yuan RMBYuan

11

2 0 1 5 ANNUAL REPORT

CoRPoRate PRofIle anD Key fInanCIal InDICatoRS

I.CorporateprofileLegalChinesename:兴业银行股份有限公司 (Abbreviation: 兴业银行 )

LegalEnglishname:INDUSTRIALBANKCO.,LTD.

Legalrepresentative:GaoJianping

Secretaryoftheboardofdirectors:ChenXinjianRepresentative of securities affairs: Chen Zhiwei

Address:154HudongRoad,Fuzhou,PRC

Postcode:350003

Tel:(86)591-87824863

Fax:(86)591-87842633

Email:[email protected]

Registeredaddress:154HudongRoad,Fuzhou,PRCOfficeaddress:154HudongRoad,Fuzhou,PRC

Postcode:350003

Website:www.cib.com.cn

Designatednewspapersforinformationdisclosure:ChinaSecuritiesJournal,ShanghaiSecuritiesNews,SecuritiesTimes,SecuritiesDaily

WebsitedesignatedbyCSRCforpublishingannualreports:www.sse.com.cn

Locationofannualreportsfiling:theCompany’sofficeoftheboardofdirectors

Companystockbriefintroduction:

Classesofstock The stock exchange Stock abbreviation Stock code

A shares Shanghai Stock Exchange IndustrialBank 601166

Preferred shares Shanghai Stock Exchange IndustrialBankP1 360005

Preferred shares Shanghai Stock Exchange IndustrialBankP2 360012

12

Otherrelatedinformation:CertifiedpublicaccountantsfirmengagedbytheCompany:DeloitteTouche

TohmatsuCertifiedPublicAccountantsLLP

Officeaddress:30thFloor,BundCenter,222YanAnEastRoad,Shanghai,PRC

Namesofthesigningaccountants:ShenXiaohong,ZhangHua

Sponsorperformingcontinuousmonitoring:CITICSecuritiesCo.,Ltd.,IndustrialSecuritiesCo.,Ltd.

Officeaddress:CITICSecuritiesBuilding,No.8ZhongXinSanRoad,FutianDistrict,Shenzhen;No.268HudongRoad,Fuzhou

Namesofsigningrepresentativesofsponsor:WuLing,LuoZhongxing,TianJinhuo,QiaoJie

Periodforcontinuousmonitoring:FromSeptember10,2014toDecember31,2016

This report isprepared inbothChineseandEnglish.Should therebeanydiscrepancyininterpretation,theChineseversionshallprevail.

13

2 0 1 5 ANNUAL REPORT

II.Keyaccountingdataandfinancialindicatorsforlastthreeyears(1)Keyaccountingdataandfinancialindicators

Unit:RMBmillion

Item 2015 2014 Increase/decreasein2015comparedwith2014(%) 2013

Operating income 154,348 124,898 23.58 109,287

Profitbeforetax 63,244 60,598 4.37 54,261

Netprofitattributabletotheshareholdersoftheparentcompany 50,207 47,138 6.51 41,211

Netprofitattributabletotheshareholdersoftheparentcompany,afterdeductionofnon-recurringgainsandlosses

49,493 46,660 6.07 40,998

Basic EPS (RMB) 2.63 2.47 6.48 2.16

DilutedEPS(RMB) 2.63 2.47 6.48 2.16

BasicEPS,afterdeductionofnon-recurringgainsandlosses(RMB) 2.60 2.45 6.12 2.15

ROA(%) 1.04 1.18 Down0.14percentagepoint 1.20

WeightedaverageROE(%) 18.89 21.21 Down2.23percentagepoints 22.39

WeightedaverageROE,afterdeductionofnon-recurringgainsandlosses(%) 18.63 21.00 Down2.37percentagepoints 22.27

Cost-to-incomeratio(%) 21.59 23.78 Down2.19percentagepoints 26.71

Netcashflowfromoperatingactivities 818,693 682,060 20.03 209,119

Netcashflowpersharefromoperating activities (RMB) 42.97 35.80 20.03 10.98

December31,2015

December 31,2014

Increase/decreaseattheendof2015comparedwiththeendof

2014(%)

December 31,2013

Totalassets 5,298,880 4,406,399 20.25 3,678,304

Shareholders’equityattributabletotheshareholdersoftheparentcompany 313,648 257,934 21.60 199,769

Shareholders’equityattributabletotheordinaryshareholdersoftheparentcompany

287,743 244,976 17.46 199,769

Totalnumberofordinarysharesattheendof2015 19,052 19,052 - 19,052

Netassetspershareattributabletotheshareholdersoftheparentcompany(RMB) 15.10 12.86 17.46 10.49

NPLratio(%) 1.46 1.10 Up0.36percentagepoint 0.76

Provisioncoverageratio(%) 210.08 250.21 Down40.13percentagepoints 352.10

Provision-to-loanratio(%) 3.07 2.76 Up0.31percentagepoint 2.68

14

Note:1.BasicEPSandweightedaverageROEwerecalculatedbasedon“PreparationRulesforInformationDisclosurebyCompaniesOfferingSecurities to thePublicNo.9-CalculationandDisclosureofReturnonNetAssetsandEarningsPerShare” (2010Revision).

2.Asattheendof2015,theCompanyissuedanaggregateofRMB26billionpreferredshares(IndustrialBankP1andIndustrialBankP2)withnon-cumulativedividends.Thedividendsofthepreferredsharesfor2015havenotyetbeendistributed,whichwillbedistributedafterapprovalbythegeneralmeeting.

(2)2015quarterlyfinancialdataUnit:RMBmillion

Thefirstquarter(January-March)

Thesecondquarter(April-June)

Thethirdquarter(July-September)

Thefourthquarter(October-December)

Operating income 34,207 38,051 40,096 41,994

Netprofitattributabletotheshareholdersofthelistedcompany 14,790 12,954 13,477 8,986

Netprofitattributabletotheshareholdersofthelistedcompany,afterdeductionofnon-recurringgainsandlosses

14,686 12,822 13,281 8,704

Netcashflowfromoperatingactivities (53,728) 734,467 (73,713) 211,667

(3)Itemsandamountsofnon-recurringgainsandlossesUnit:RMBmillion

Item 2015 2014 2013

Gainsandlossesonthedisposalofnon-currentassets 9 83 (28)

Governmentgrantsrecognizedinprofitorloss 334 379 162

Write-backofassetswritten-offinpreviousyears 531 242 113

Netnon-operatingincomeandexpenseinadditionto the above 91 (54) 49

Impact on income tax (252) (172) (83)

Total 713 478 213

Non-recurringgainsandlossesattributabletotheshareholdersoftheparentcompany 714 478 213

Non-recurringgainsandlossesattributabletominorityshareholders (1) - -

15

2 0 1 5 ANNUAL REPORT

(4)SupplementaryfinancialdataUnit:RMBmillion

Item December31,2015 December31,2014 December31,2013

Totalliabilities 4,981,503 4,145,303 3,477,133

Placementsfrombanksandotherfinancialinstitutions 103,672 81,080 78,272

Totaldeposits 2,483,923 2,267,780 2,170,345

Incl:Demanddeposits 1,063,243 948,425 907,078

Time deposits 1,149,101 1,053,728 979,043

Other deposits 271,579 265,627 284,224

Totalloans 1,779,408 1,593,148 1,357,057

Incl:Corporateloans 1,197,627 1,179,708 988,808

Individualloans 511,906 385,950 353,644

Discountedbills 69,875 27,490 14,605

Loanlossprovisions 54,586 43,896 36,375

16

(5)CapitaladequacyratioUnit:RMBmillion

Keyindicator December31,2015 December31,2014 December31,2013

Netcapital 383,504 328,767 250,183

Incl:Coretieronecapital 289,769 246,484 201,153

Other tier one capita 25,909 12,958 -

Tiertwocapital 69,420 69,933 50,663

Deductions 1,594 608 1,633

Totalriskweightedassets 3,427,649 2,911,125 2,310,471

Capitaladequacyratio(%) 11.19 11.29 10.83

Tieronecapitaladequacyratio(%) 9.19 8.89 8.68

Coretieronecapitaladequacyratio(%) 8.43 8.45 8.68

Note:Data in this tablearecalculated inaccordancewith theCapitalRulesforCommercialBanks(Provisional)andbasedondatareportedtoregulatoryauthorities.

17

2 0 1 5 ANNUAL REPORT

(6)SupplementaryfinancialindicatorsUnit:%

Keyindicator Standardvalue December31,2015

December 31,2014

December 31,2013

Loan-to-depositratio(convertedtoRMB) ≤75 67.62 64.76 61.95

Liquidityratio(convertedtoRMB) ≥25 56.80 41.59 35.79

Proportionofloanstothelargestsingleborrower ≤10 2.11 8.26 7.06

Proportionofloanstothetoptenborrowers ≤50 12.62 20.44 23.72

Migrationratioofpassloans - 3.69 2.33 1.20

Migrationratioofspecialmentionloans - 52.96 42.16 30.48

Migrationratioofsubstandardloans - 87.33 93.77 97.63

Migrationratioofdoubtfulloans - 35.92 20.53 30.41

Note:1.Datainthistablearethosebeforeconsolidation,anddataofsubsidiariesarenotincludedinthistable.

2.Datainthistablearecalculatedbasedondatareportedtoregulatoryauthorities.

3.PursuanttoDocumentYJF[2010]No.112issuedbyCBRC,startingfrom2011,regulationofthedailyaverageloan-to-depositratiopermonthwasstrengthened.TheindicatoroftheCompany’sdailyaverageloan-to-depositratioofeverymonthduringthereportingperiodhasmetregulatoryrequirements.

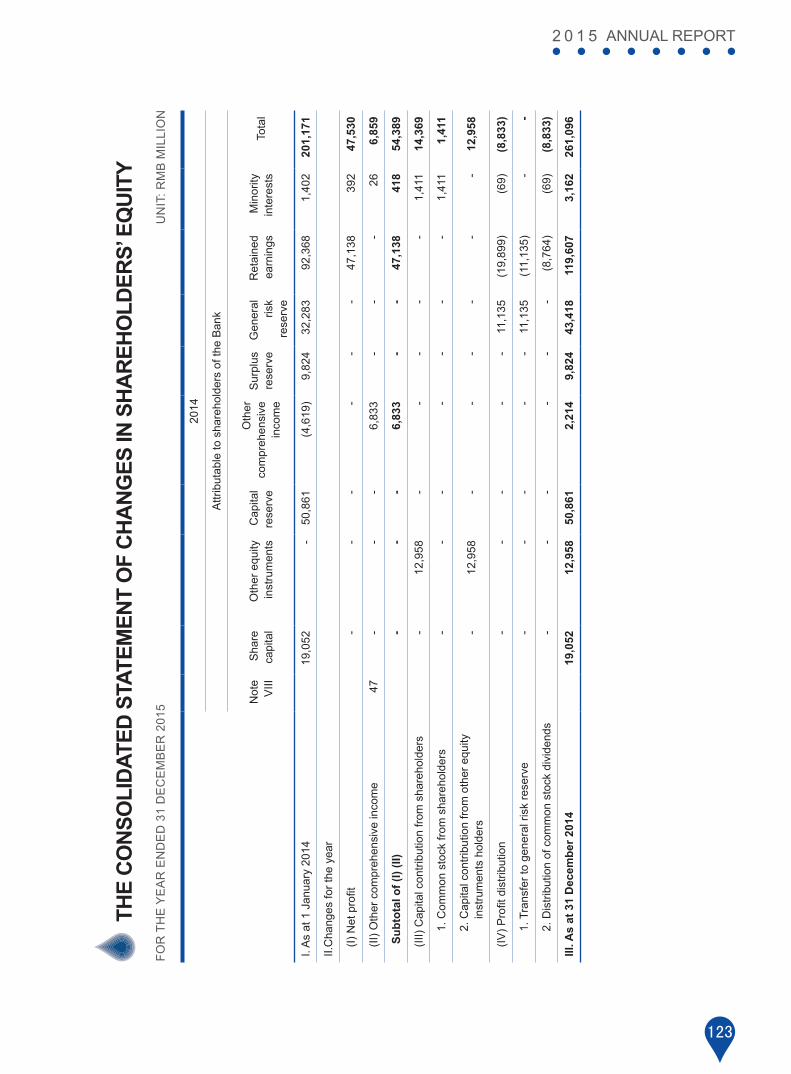

(7)Changesinshareholders’equityduringthereportingperiodUnit:RMBmillion

Item Beginningbalance Increase during the period

Decrease during the period Closingbalance

Sharecapital 19,052 - - 19,052

Preferred shares 12,958 12,947 - 25,905

Capitalreserve 50,861 - - 50,861

Other comprehensive income 2,214 3,471 - 5,685

Generalreserve 43,418 17,247 - 60,665

Surplusreserve 9,824 - - 9,824

Undistributedearnings 119,607 50,207 (28,158) 141,656

Shareholders’equityattributabletotheshareholdersoftheparentcompany 257,934 83,872 (28,158) 313,648

18

(8)ItemsmeasuredatfairvalueUnit:RMBmillion

Item December 31,2014

Gainsandlossesin the period

from changes in fairvalue

Accumulatedchanges in fair

valuerecognizedinequity

Provision for impairment

made in the period

December31,2015

Financialassetsatfairvaluethroughprofitorloss 44,435 (109) - - 128,685

Preciousmetals 7,456 (1,311) - - 41,964

Derivativefinancialassets 5,1422,781

- - 13,933

Derivativefinancialliabilities 4,498 - - 10,563

Available-for-salefinancialassets 407,752 7,699 1,095 426,304

Financialliabilitiesatfairvaluethroughprofitorloss 1,903 17 - 1

Note:1.Financialassetsatfairvaluethroughprofitorloss:primarilytheRMBbondsheldforthepurposeofmarketmakingtrading.TheCompanyadjustedthepositionofitsheld-for-tradingRMBbondsinadynamicalprocess,basedonthetradingactivitylevelinthebondmarketanditsjudgmentonthemarketmovement.Inthereportingperiod,theCompany’sinvestmentintheheld-for-tradingbondsincreased,andthechangesoffairvaluehadaminorimpactrelativetothescale.

2.Preciousmetals:beingsubjecttoimpactoftheproprietarypreciousmetaltradingstrategyandmarketmovement,theCompanyincreased itscashpositionofpreciousmetalduringthereportingperiod,and itsbalanceat fairvalue indomesticpreciousmetalsspottradingattheendofthereportingperiodincreasedbyRMB34.508billioncomparedwiththatatthebeginningoftheperiod.

3.Derivativefinancialassetsandliabilities:theabsolutevaluesofderivativefinancialassetsandliabilitiesdecreasedcomparedwiththoseat thebeginningof theperiod.Theoveralloffsetbalanceincreased,meaningthatgainsfromthechanges infairvalueofthefinancialderivativesinvestmentintheperiodincreased.

4.Available-for-sale financialassets: theCompany increased its investment inavailable-for-sale financialassetsduring thereportingperiodundertheneedofassetallocationandmanagement,aswellas its judgmentonthemarketmovementandanalysisoftheinter-bankmarketliquidity.

5.Financial liabilitiesatfairvaluethroughprofitor loss:theCompany’sfinancial liabilitiesatfairvaluethroughprofitor lossaremainlysaleofbondsborrowedandshortsalegoldtransactions.Asattheendofthereportingperiod,thepositionwasmainlysaleofbondsborrowed.

19

2 0 1 5 ANNUAL REPORT

BuSIneSS oveRvIew of the ComPany

I.MainBusinessesandOperationModeoftheCompanyandConditionsoftheIndustry(I) Main businesses and operation mode Founded inAugust1988, theCompany isoneof thefirstgroupof joint-stockcommercialbanksapprovedby theStateCounciland thePeople’sBankofChina.OnFebruary5,2007, theCompanywas listedonShanghaiStockExchange,andhasnowdeveloped intoanational joint-stockcommercialbankwithsoundgovernance,distinctcharacteristicsandgoodservice,rankingtop50banksworldwide.

TheCompany ismainlyengaged incommercialbankservices, itsmainbusinessscope includes:deposits taking;provisionof short-,medium-and long-term loans;domesticand international settlement;billsacceptanceanddiscounting; issueof financialbonds;agency issue, cashingandunderwritingofgovernmentbonds; tradingofgovernmentbondsand financialbonds;agency issueofnegotiablesecuritiesexceptstock; tradingandagencytradingofnegotiablesecuritiesexceptstock;assetcustody; inter-bankborrowingand lending; tradingoragencytradingof foreignexchange; settlementandsalesof foreignexchange;bankcardbusiness;L/Cservicesandguarantee;agencycollectionsandpaymentsandagency insurance;safe-boxservices,financialconsulting,creditinvestigation,consulting,witnessbusinessandotherbankingactivitiesapprovedby theCBRC.TheCompanyhasestablished119branchesand1,787outlets inmajorcitiesacross thecountryandhasestablishedcorrespondentbank relationshipswithmore than1,500banksworldwide.TheBankhasestablishedanonlinebankingplatform“Online IB”,a telephonebankingplatform“95561”,amobilebankingsystem“Wireless IB” and the Direct Bankingplatform .TheCompanyconstantly improves itsservicenetworkcombiningvirtualityand reality,coveringChinaandconnectingdomesticandoverseasmarket.

Forover20yearssince itsestablishment, theCompanyhasbeenadvocatingthebusinessphilosophyof“Growing Together with Sincere Service”andendeavoring tooffercomprehensive, top-quality,andhigh-efficient financialservicesforcustomers. Itsmainbusinessesaredivided intothreesegments,namelycorporatefinance,retailbankingandfinancialmarket.Corporatefinancebusiness includescorporatedepositand loanbusiness, investmentbanking,tradefinancing,cashmanagement,environmentfinance,smallenterprisebusinessandinstitutionalbusiness,etc.Retailbankingbusiness includesretailbankingbusiness,creditcardbusinessandprivatebankingbusinessetc.Financialmarketbusinessincludesinterbankbusiness,treasurybusiness,assetsmanagementandassetscustody,etc.

TheCompanyactivelypromotesbusinesstransformation,consolidatesandstrengthensbasicbusinessfocusingontransactionbanks.Adhering to thedevelopmentdirectionof“sizeable investment,sizeablewealthmanagementandsizeableassetmanagement”andaccelerated thedevelopmentofkeybusinesses featuring lightassetandlightcapitalandpersistentlyexploredinnovativebusinesswithservingthecapitalmarketasthemaindirection.TheCompanyconstantlydeepensreformonriskmanagementsystemsandmechanisms, improvestheeffectivenessofcompliance, internalcontrolandoperational riskmanagementandstrives tomaintain theoverallsteadinessof thequalityofassets,andprovidesstrongsupport for innovation inbusinessdevelopment.TheCompanycontinues toworkhardonestablishingagroup,constantlyenhances thegroup-oriented layout,and improvesmarket-orientedoperationandcomprehensiveservice capability, enabling it tobecomeoneof thebankgroupswith themostabundantfinanciallicensesresourceinChina.

(II)ConditionsoftheindustryanddevelopmenttrendUnderthenewnormalofdomesticeconomy,thedevelopmentofbankingindustryinChinaisenteringanewstage.Specifically speaking, the impetusofeconomicgrowth ischanging,economicgrowth isslowingdown,and theoperationperformanceofcommercialbankshasswitchedfromhigh-speedgrowthtolowandmediumspeedgrowth.

20

Adjustmentofeconomicstructurecontinues,exposureofcredit risk intensifiesandqualityofassetsofcommercialbankscontinues todrop.Financialdisintermediation isbecoming increasingly fiercewith thebasiccompletionofthe reformof interest rate liberation,cross-boundarycompetition is turning intensifiedwith theopeningof industryaccess,andpressuresonbankoperation is increasing.Facedwith thechangesofsituation,commercialbanksacceleratedoperation transformationandacceleratedprovidingbetterservice to thegeneralpublicof traditionalbusinessandmadeefforts topromotesuchemergingbusinessesas investmentbank,assetmanagement,wealthmanagement,custodyand fortunemanagement.Steadyprogresshasbeenmade in integration,group-orientedlayoutand internationalizationof finance,andmaincommercialbanks formeddifferent typesof financialholdinggroups.Inthefuture,itwillbethethemeforcommercialbankstostrengthenriskdisposal,implementinnovationanddeepentransformationforacertainperiodoftime.TheCompanywillchangeinaccordancewiththesituation,makethebestuseof itsadvantagesandbypass thedisadvantages,studyand learn from theadvancedexperienceofmarketandplaninadvancetocircumventthemainrisks,anditwilltakethedevelopmentopportunitytoexploreandsticktothesustainabledevelopmentpathwithitsowncharacteristics.

II.ExplanationonMajorChangesofMainAssetsduringtheReportingPeriodAsat theendof thereportingperiod,thetotalassetsof theCompanystoodatRMB5,298.880billion,up20.25%%fromthefigureat thebeginningof theperiod,ofwhich loans increasedby11.69%fromthefigureat thebeginningof theperiod;financialassetsheldunderresaleagreementsdecreasedby68.30%comparedwith thefigureat thebeginningoftheperiod;andvariousnet investmentswereupby91.04%comparedwiththefigureatthebeginningof theperiod.Refer to“AnalysisofBalanceSheets” asdiscussedandanalyzed inChapter IVManagementDiscussionandAnalysis.

III.AnalysisofCoreCompetitivenessByactivelyimplementingthemacroeconomicpoliciesandfinancialregulationrequirements,theCompanyhasbeenpersistingingivingdevelopmentasitspriority,takingtransformationasthecorelineandreformasthefundamentalimpetus , andbuilding itself intoa“mainstream banking group with sound foundation, coordinated structure, prominentprofessionalism,vividdistinctiveness,solidstrength,andfullaccountability”,therebyconstantlyimprovingitscompetitiveness.

Promotingstandardizedoperationof theCompanyby improvinggoverningstructure.Since itsestablishment,theCompanyhasbeenconstantly improving its systemandmechanismstructure inaccordancewithmarket-orientedoperationmechanism, improving the internaloperationefficiencybystandardizedoperationandscientificmanagement, thereby formingastandardizedcompanystructurewithefficientmanagementanddifferentiatedspecialties.Onthebasisofgivingfullplaytothesystemadvantageofheadoffice,branchesandsub-brancheswhileadhering tobeingcustomer-oriented, theCompanyhasgraduallyestablishedvariousbusinesshandlingcentersormanagementcentersbypromoting itsoperationmanagement tobeclose to themarketand to thecustomers,accordingtotheprincipleofdelayering,professionalizationandcentralizationaswellasseparationoffront-,middle-andback-office.TheCompanyhasalsoestablishedamatrixmanagementmodebypromotingdual-lineoperationaccording to thedirectionofgradually formingbusinessdepartmentsbybusiness lines.Basedon theexistingmanagementofassetsandliabilities,comprehensiveoperationplan,risksandinternalcontrolofmoderncommercialbanks,theCompanyhasreorganizeditsflowprocessandrestructureditssystems,constantlydeepenedreformonoperationmanagementsystemsandmechanismsandacceleratedoperationtransformationtoholdahighgroundinmodernbankcompetitionandconstantlystimulatevigorousoperationenergy.

Creatingbrandproductsandholdinganadvantageouspositionintheindustrybybusinessinnovation.TheCompanyhasbeenengagedinfinancialmarketformanyyearsandhasbeenwell-knownforitsprominentinnovationcapabilityandaccurateforward-lookingjudgment.TheCompanyhastakenaleadingpositionininnovationinmanysegmented

21

2 0 1 5 ANNUAL REPORT

business areas and opens its own “blueocean”,withdistinctoperationcharacteristics.TheCompanyhasbuilttheentireIndustrialBankbrandbybusinessinnovationandestablishedawell-recognizedproductandservicebrandsystem.Abathofproductsandservicebrandsincluding“NaturalLife”, “EnjoyableLife”, “UniversalLife”, “IB Business Express”, “IBFortuneStar”, “IndustrialBankSesameBlooming”, “GreenFinance”, “theEquatorPrinciples”, “Bank-to-BankPlatform”, “E-banking”, “Hotline IB”, “QianDaMoneyManager” and “Direct Banking”arewidely recognized in thedomesticfinancialmarket.TheCompany followed themarketdevelopmenttrend, made great efforts in creating “onebodyand twowings” specializedservicesystem, centralized theresourceadvantagesof thegroupand focusingonurbanizationfinancialbusiness,environmentfinancebusiness,pension financebusiness,comprehensiveservicesbusiness forsmallandmediumbanking institutionsandnon-bankfinancial institutions,directfinancingbusiness incapitalmarket, investmentandcustodybusinessofassetsmanagementandtransactionbankingbusiness, itcreatedafinancialproductsystemwithclearpositioning,distinctcharacteristics,outstandingadvantagesandcomplete functions, formingadvantageousbrandandproductclusterwiththecharacteristicsofthegroup.

Promotingbusiness transformationbycomprehensiveoperation.TheCompanyhasbeenpersisting in themulti-market,multi-productandcomprehensivedevelopmentpathandactivelycreating itscapabilityoffinancialservicesformulti-market. Ithas formeda relativelycompletebusinesssystemcovering interbankbusiness,capital trading,assetsmanagementandassetscustody,andhas taken the lead inplanning itsbusiness in themonetarymarket,capitalmarket,bondmarket, inter-bankmarket,non-bank financial institutionmarket,preciousmetals, foreignexchangeandderivativeproducts trading.Through thecomprehensive layoutof recentyears, theCompanyhasbeen transformed fromasinglebank to“amoderncomprehensivefinancialservicegroupwithbankingbusinessas thecore,coveringbusinessareas including trust, leasing, funds, futures,assetmanagement, internet financeandresearchandconsultation”.TheHongKongbranchwasofficiallyopened in2014,markingakeystepfor theinternationalizationstrategiesof theCompany.Relyingon linkagebetween investmentand loan, linkagebetweenbusinessinandoutsidethestatements,linkagebetweenparentcompanyandsubsidiaries,theCompanyhasmetthediversifiedfinancialservicedemandofcustomers,andthebusinesscoordinationandlinkagedevelopmentcapabilitybetweenbranchesandsubsidiariesbothathomeandabroadhasbeenconstantlyimproved.

Promotingcontinuous improvementofoperationsupportingcapabilitybyscienceand technology.“Building theBank throughScienceandTechnology” is listedasoneof thekeystrategies for thebankingoperation.TheCompanyvaluedtracingandgraspedthedevelopmenttrendofmodernfinancialtechnology.Itincreasedinvestmentinscienceandtechnology topromote innovation infinancial technologiesandconstantly improvethe technologicalcontentoffinancialservice.TheCompanyisamongthefirstbatchofbanksbuildingmodernmanagementsystemsinaccordancewiththeprocessbankconcept,anditscentralizedbackofficeoperationsystemholdsaleadingpositionin the industry.Thecoreproductionsystemconstructionof theCompany isamongthebest in the industry,makingitoneofthefewbanksinthecountrythathaveindependentcoresystemresearchanddevelopmentcapabilityandproprietaryintellectualpropertyrights,aswellastheonlydomesticbankexportingcoresystemtechnology.Itisthefirst tobuildan integrateddisaster recoverysystem integrating themasterdatacenter,same-citydisaster recoveryanddifferent-citydisasterrecovery,andoneofthefirstbanksinthecountrythatcomplywiththeinternationaldisasterrecoverystandard(level-5)andtherequirementsofthedisasterrecoverystipulationsofPBOC.TheCompany’skeyindicators,suchaskey informationsystemavailabilityandgoldcardsystem transactionsuccess rate,havebeenamongthebestintheindustryovertheyears.

Creatingsoftcompetitivepowerbythepragmaticanddedicatedcorporateculture.Tofulfilltheenterprisemissionof“SincereWin-WinService”,adhering to thecorevalueof“Ration, Innovation,PeopleFirstandSharing” and theoperationpolicyof“operatinginaccordancewithlaw,steadyoperationandcivilizedoperation”,theCompanyimplements thestrategyofstrictbankingoperation,bankingoperationbyexperts,developingbankbyscienceandtechnologyandbankingestablishmentbyservice,upholds thecorporatespiritsof“Pragmatism,ProfessionalDedication, Entrepreneurship and Teamwork”, graduallybuildsasimpleandharmonious“homeculture”, a prudent and sound “riskculture”,ahard-working“diligenceculture”andasincerewin-win“serviceculture”, thereby formingstrongsoftcompetitivepowerand improving internalmanagement level inallaspects,effectivelyimprovingcorecompetitivenessandpromotingthehealthydevelopmentofallundertakings.

22

Fromlefttoright:

XueHefengChenXinjianTaoYipingLiWeiminChen Jinguang

Vicepresident:Director and vice president:

President: Vicepresident:Vicepresident:

23

2 0 1 5 ANNUAL REPORT

management DISCuSSIon anD analySIS

I.Situationofmajoroperationsduringthereportingperiod(I) Overview 1.Overalloperations

During the reportingperiod, facing the complicatedand fiercebusinessenvironment, theCompany rationallycoordinated thegoals in relation to“scale,qualityandefficiency”, flexiblyadjusted thebusinessstrategy,andpromotedbusinessstructureadjustmentand transformationandupgrading, therebymeetingexpectationsof itsoveralloperations.

(1)Thescaleofbusinesssteadilyandhealthily increased.Asat theendof thereportingperiod, thetotalassetsoftheCompanyreachedRMB5,298.880billion,representinganincreaseof20.25%fromthefigureatthebeginningofthereportingperiod; thebalanceofdomesticandforeigncurrencydepositwasRMB2,483.923billion, representingan increaseof9.53%fromthefigureat thebeginningof the reportingperiod; thebalanceofdomesticand foreigncurrencyloanreachedRMB1,779.408billion,representinganincreaseof11.69%fromthefigureatthebeginningofthereportingperiod.

(2)Profitabilitycapabilitymaintainedrelativelygoodstatus.Duringthereportingperiod,therealizedoperatingincomewasRMB154.348billion,up23.58%year-on-year,ofwhichfeeandcommissionincomereachedRMB33.592billion,up18.23%year-on-year.NetprofitattributabletotheshareholdersoftheparentcompanyforthewholeyearreachedRMB50.207billion,representingayear-on-yearincreaseof6.51%.Duringthereportingperiod,weightedaveragenetassets returns ratiowere18.89%, representingayear-on-yeardecreaseof2.32percentagepoints, total returnonassetsreached1.04%,representingayear-on-yeardecreaseof0.14percentagepoint.

(3)Thequalityofassetswascontrollableoverall.Asattheendofthereportingperiod,thebalanceofnon-performingloansof theCompanywasRMB25.983billion,upRMB8.439billion; the ratioofnon-performing loansstandingat1.46%, representingan increaseof0.36percentagepoint fromthefigureat thebeginningof the reportingperiod.Duringthereportingperiod,theprovision-to-loanratiowas3.07%attheendofthereportingperiod,andtheprovisioncoverageratiowas210.08%.

(4)Marketstatusandbrand imagewerecontinuouslyenhanced.TheCompanycontinued tobeamong the top50worldbanks,global500companies,and top150 listedworldenterpriseswith rankingssteadilyclimbing.Over thepastyear, theCompanywonhonors including the“AnnualFinancialHoldingGroupAward2015”, “The Most InfluentialNationalBank”, “AsianBankOfferingtheGreatestReturn toShareholders”, “The Best Green Bank Award”inaseriesofappraisalactivitiesofauthoritiesbothathomeandabroad.

2.Compositionofoperatingincomeandoperatingprofit

Duringthereportingperiod,operatingincomeoftheCompanywasRMB154.348billion,anditsoperatingprofitwasRMB62.810billion.

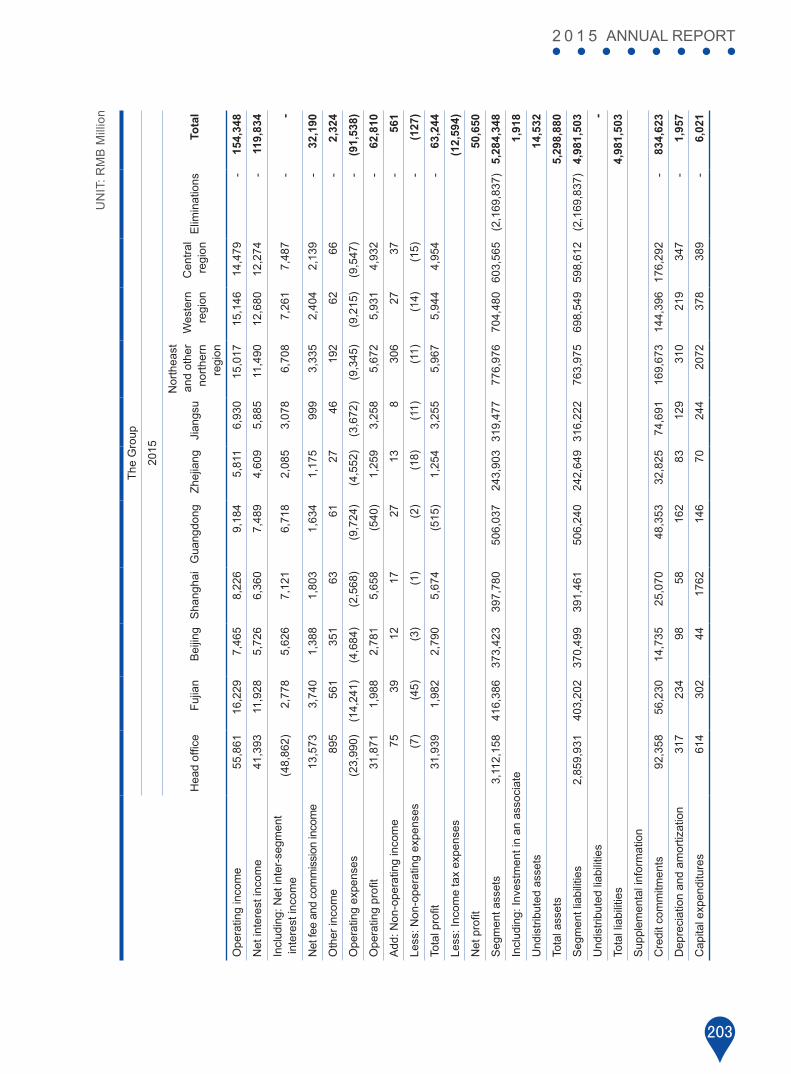

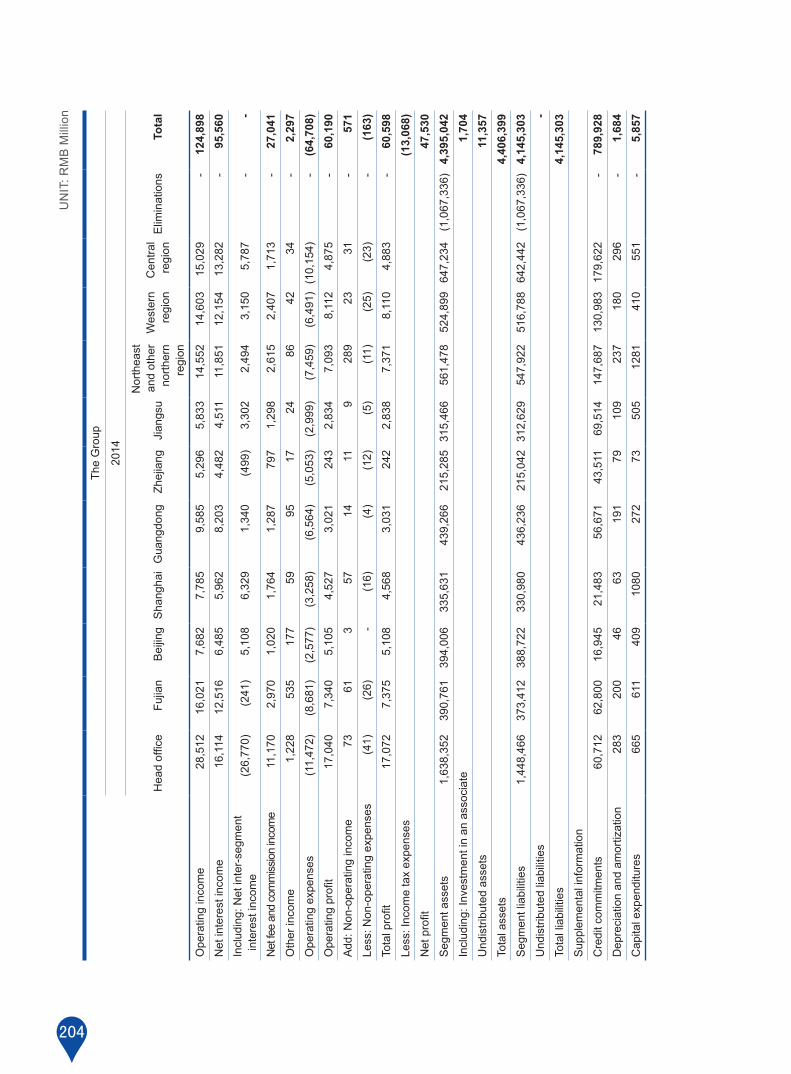

(1)TheCompanydivided its regionalbranches into tensegmentsby importanceandcomparability,namely,headoffice(includingtheheadquartersanditsaffiliatedoperatingunits),Fujian,Beijing,Shanghai,Guangdong,Zhejiang,Jiangsu,Northeastandother regions inNorthernChina,WesternChinaandCentralChina.Operating incomeandoperatingprofitofvariousregionsaresetoutasfollows:

24

Unit:RMBmillion

Region Operating income Change over previousyear(%) Operatingprofit Change over

previousyear(%)

Headoffice 55,861 95.92 31,871 87.04

Fujian 16,229 1.30 1,988 (72.92)

Beijing 7,465 (2.82) 2,781 (45.52)

Shanghai 8,226 5.66 5,658 24.98

Guangdong 9,184 (4.18) (540) (117.87)

Zhejiang 5,811 9.72 1,259 418.11

Jiangsu 6,930 18.81 3,258 14.96

Northeast and other regions 15,017 3.20 5,672 (20.03)

WesternChina 15,146 3.72 5,931 (26.89)

CentralChina 14,479 (3.66) 4,932 1.17

total 154,348 23.58 62,810 4.35

(2)Theamount,proportionandyear-on-yearchangesoftheitemsofoperatingincome

Unit:RMBmillion

Item Amount Percentageintotaloperatingincome(%)

Increase/decreaseyear-on-year(%)

Interestincomefromloans 101,750 34.86 8.95

Interestincomefromplacements 2,095 0.72 (54.90)

Interest income from amount due fromtheCentralBank 6,497 2.23 4.71

Interest income from amount due from banksandotherfinancialinstitutions 3,894 1.33 (18.57)

Interestincomefromfinancialassetsheldunderresaleagreements 27,382 9.38 (51.39)

Gainandloss,andinterestincomefrom investment 111,501 38.20 124.27

Feeandcommissionincome 33,592 11.51 18.23

Interestincomefromfinancinglease 5,367 1.84 33.14

Other income (190) (0.07) (107.30)

total 291,888 100 16.70

25

2 0 1 5 ANNUAL REPORT

3.Financialpositionandoperatingresults

(1)Changesofkeyfinancialindicatorsanddescriptions

Unit:RMBmillion

Item December31,2015

December31,2014

Increase/decrease over previousyear-end(%)

Brief description

Totalassets 5,298,880 4,406,399 20.25 Steadyandhealthygrowthofvariousasset businesses

Totalliabilities 4,981,503 4,145,303 20.17 Steadyandhealthygrowthofvariousliabilitybusinesses

Shareholders’equityattributabletotheshareholdersoftheparentcompany

313,648 257,934 21.60Transferof thenetprofitearned in thecurrent period and issuance of preferred shares

Item 2015 2014Increase/decrease

over previousyear-end(%)

Brief description

Netprofitattributabletotheshareholdersoftheparentcompany

50,207 47,138 6.51

Stable interestmargin,growth indailyaverageinterest-bearingassets;growthin fee and commission income and cost-to-incomeratiomaintainedatalowlevel

WeightedaverageROE(%) 18.89 21.21

Down2.32percentage points

Duetotheretainedprofitsandincreasedchangeinfairvalueofavailable-for-salefinancialassets,thegrowthinnetprofitwasslowerthanthegrowthinweightednet assets

Netcashflowfrom operating activities 818,693 682,060 20.03

Optimizebusinessstructure, leadingtohealthyandsteadygrowth invariousbusinesses and increase in investment allocationbysizingmarketopportunity

26

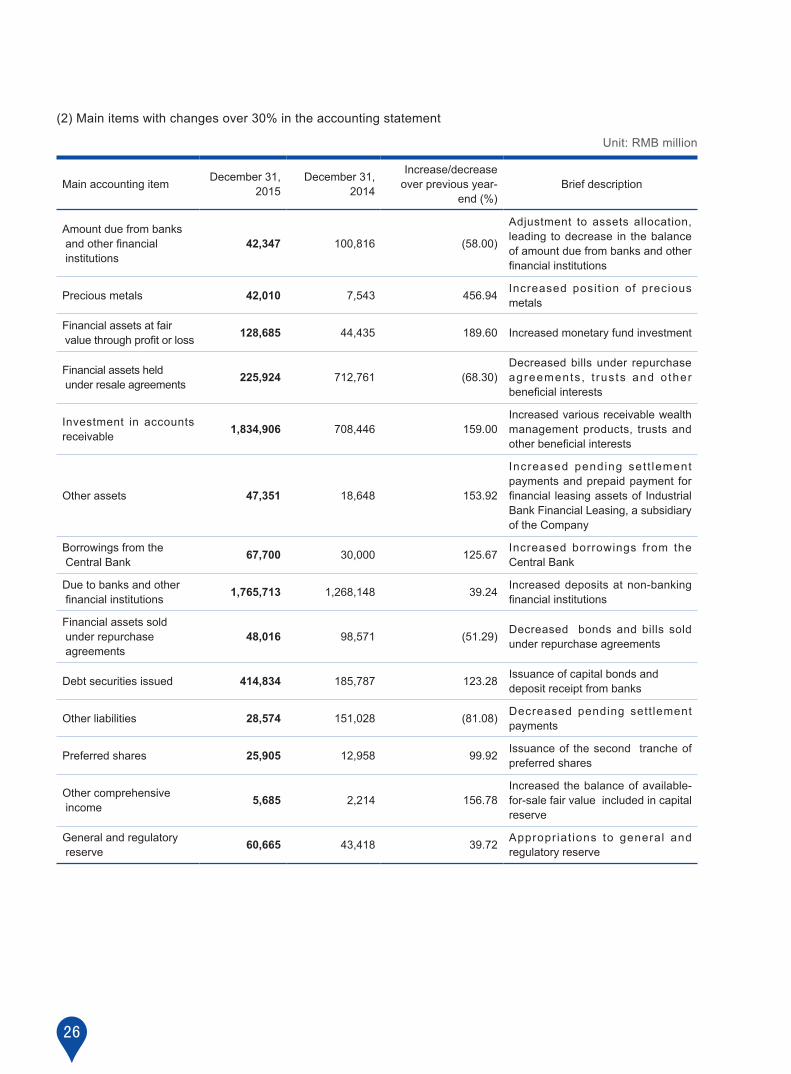

(2)Mainitemswithchangesover30%intheaccountingstatement

Unit:RMBmillion

Main accounting item December31,2015

December31,2014

Increase/decreaseoverpreviousyear-

end(%) Brief description

Amount due from banks andotherfinancial institutions

42,347 100,816 (58.00)

Adjustment to assets allocation,leading todecrease in thebalanceof amount due from banks and other financialinstitutions

Preciousmetals 42,010 7,543 456.94 Increased posit ion of precious metals

Financialassetsatfairvaluethroughprofitorloss 128,685 44,435 189.60 Increasedmonetaryfundinvestment

Financialassetsheldunderresaleagreements 225,924 712,761 (68.30)

Decreasedbillsunder repurchaseagreements , t rus ts and o ther beneficialinterests

Investment in accounts receivable 1,834,906 708,446 159.00

Increasedvariousreceivablewealthmanagement products, trusts and otherbeneficialinterests

Other assets 47,351 18,648 153.92

Increased pending set t lementpaymentsandprepaidpayment forfinancial leasingassetsof IndustrialBankFinancialLeasing,asubsidiaryoftheCompany

Borrowings from theCentralBank 67,700 30,000 125.67 Increased borrowings from the

CentralBank

Due to banks and other financialinstitutions 1,765,713 1,268,148 39.24 Increaseddepositsatnon-banking

financialinstitutions

Financialassetssold under repurchase agreements

48,016 98,571 (51.29) Decreased bondsandbills soldunder repurchase agreements

Debt securities issued 414,834 185,787 123.28 Issuanceofcapitalbondsanddeposit receipt from banks

Otherliabilities 28,574 151,028 (81.08) Decreased pending sett lementpayments

Preferred shares 25,905 12,958 99.92 Issuance of the second tranche of preferred shares

Other comprehensive income 5,685 2,214 156.78

Increasedthebalanceofavailable-for-salefairvalueincludedincapitalreserve

Generalandregulatory reserve 60,665 43,418 39.72 Appropr iat ions to general and

regulatoryreserve

27

2 0 1 5 ANNUAL REPORT

Main accounting item 2015 2014 Increase/decreaseoverpreviousyear(%) Brief description

Investment(losses)gains 3,482 (96) Negative in thesameperiodoflastyear Being h ighly in terre lated, the

overallgainsof these three itemsafter consolidation amounted toRMB2.010billion,downby9.74%

Gains(losses)fromchangeinfairvalue 1,378 1,631 (15.51)

Foreignexchangegains (2,850) 692 (511.85)

Business tax and surcharges 12,955 9,105 42.28 Business growth, the business tax andadditionalincreasesaccordingly

Impairmentlossesofassets 45,260 25,904 74.72Increased provision being made andgrowth in impairment lossesofloansandinvestments

Other comprehensive income 3,466 6,859 (49.47)The gains from the changing of available-for-salefairvaluereducedduring the reporting period

(II)Analysisofthebalancesheet1.Assets

Asat theendof the reportingperiod, the totalassetsof theCompanystoodatRMB5,298.880billion,up20.25%fromthefigureat thebeginningof theperiod,ofwhich loans increasedbyRMB186.260billionor11.69%fromthefigureat thebeginningof theperiod; financialassetsheldunder resaleagreementsdecreasedbyRMB486.837billionor68.30%comparedwiththefigureatthebeginningoftheperiod;andvariousnetinvestmentsincreasedbyRMB1,238.504billionor91.04%comparedwiththefigureatthebeginningoftheperiod.ThecompositionofthetotalassetsoftheCompanyisshowninthetablebelow:

Unit:RMBmillion

ItemDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Netloansandadvancestocustomers 1,724,822 32.55 1,549,252 35.16

Investment note(1) 2,598,945 49.05 1,360,441 30.87

Financialassetsheldunderresale agreements 225,924 4.26 712,761 16.18

Financeleasereceivables 74,146 1.40 58,254 1.32

Due from banks 42,347 0.80 100,816 2.29

Placementswithbanksandotherfinancialinstitutions 56,336 1.06 51,149 1.16

Cashandbalanceswithcentralbank 417,911 7.89 491,169 11.15

Other note (2) 158,449 2.99 82,557 1.87

total 5,298,880 100 4,406,399 100

Note: (1) Included the financialassetsat fairvalue throughprofitor loss,available-for-sale financialassets, receivableaccountinvestments,held-to-maturityinvestmentsandlong-termequityinvestments.

(2) Includedpreciousmetals,derivativefinancialassets, interest receivable,fixedassets,construction inprogress, intangibleassets,goodwill,deferredtaxassetsandotherassets.

28

Thedetailsofloansaresetoutasfollows:

(1)Classificationofloans

Unit:RMBmillion

Type December31,2015 December31,2014

Corporateloans 1,197,627 1,179,708

Personalloans 511,906 385,950

Discountedbills 69,875 27,490

total 1,779,408 1,593,148

Asat theendof the reportingperiod, theproportionofcorporate loanswas67.30%,down6.74percentagepointsfromthefigureatthebeginningoftheperiod.Theproportionofpersonalloansincreasedby4.54percentagepointsto28.77%,and theproportionofdiscountedbills increasedby2.20percentagepoints to3.93%,comparedwiththatatthebeginningoftheperiod.TheCompanyproactivelydealtwiththenewnormaleconomyandnewfinancialpattern,adheredtothemainprinciplesofstabilizingdevelopment,ensuringsafety,andpromotingtransformation” in itswork,rationallycoordinatedthegoalsinrelationto“scale,qualityandefficiency”,flexiblyadjustedthebusinessstrategy, furtherdeepened reformand transformation,vigorouslydevelopedandconsolidated the foundation fordevelopment,rationallydeterminedthedirectionandtempoforcreditgrant,soastomaintainasteadyandbalanceddevelopmentofvariousbusinesses.

29

2 0 1 5 ANNUAL REPORT

(2)Loandistributionbyindustry

Asattheendofthereportingperiod,thetopfiveindustriesthatreceivedthelargestproportionofbankloanswere:personal loans,manufacturing,wholesaleand retail, realestate,andwaterconservation,environmentandpublicfacilityadministration.Thedetailsondistributionbyindustryaresetoutasfollows:

Unit:RMBmillion

IndustryDecember31,2015 December31,2014

Loanbalance

Percentage (%)

NPLratio(%)

Loanbalance

Percentage (%)

NPLratio(%)

Agriculture,forestry,husbandryandfishery 6,407 0.36 2.09 5,751 0.36 0.00

Mining 66,930 3.76 1.68 53,743 3.37 0.93

Manufacturing 295,358 16.60 2.95 293,739 18.44 2.29

Productionandsupplyofpower,heat, gas and water 53,808 3.02 0.02 47,638 2.99 0.01

Construction 73,226 4.12 1.10 80,352 5.04 0.28

Transportation,logisticsandpostal service 60,575 3.40 0.64 56,777 3.56 0.02

Information transmission, software and IT service 8,782 0.49 0.83 8,172 0.51 1.03

Wholesaleandretail 205,299 11.54 4.63 239,606 15.04 2.63

Accommodation and catering 5,572 0.31 1.90 5,586 0.35 0.69

Finance 7,058 0.40 0.56 3,808 0.24 0.01

Realestate 201,366 11.32 0.02 189,843 11.92 0.00

Leasingandcommercialservices 90,505 5.09 0.42 88,290 5.54 0.40

Scientificresearchandtechnicalservice 4,735 0.27 5.26 4,633 0.29 4.24

Waterconservation,environmentandpublicfacilityadministration 92,518 5.20 0.00 79,168 4.97 0.06

Residentialservices,repairandotherrelatedservices 1,511 0.08 0.75 2,173 0.13 0.04

Education 2,788 0.16 0.07 2,178 0.14 0.09

Sanitationandsocialservices 9,517 0.53 0.11 5,535 0.35 0.00

Culture,sportingandentertainment 5,730 0.32 0.00 4,072 0.26 0.00

Publicadministration,socialsecurityandsocialorganizations 5,942 0.33 0.00 8,644 0.54 0.00

Personalloans 511,906 28.77 0.86 385,950 24.23 0.79

Discountedbills 69,875 3.93 0.00 27,490 1.73 0.00

total 1,779,408 100 1.46 1,593,148 100 1.10

30

Following theprincipleof“riskcontrollable, resourceconservationandsustainabledevelopment”, theCompanypromoted the reasonablearrangementandbalanceddevelopmentofcredit resources in the industry,customers,products,etc.,continuouslyexecuted the“protected,controlledandstressful”difference loanpolicy,speededup thedevelopmentofsmallandmedium-sized,microandretailbusinessesunder thepremiseofmeetingaccessconditionsandeffectivelycontrolling risks, fullyuncoveredbusinessopportunities in free tradezones, industrialparks,reformtestareasandotherareaswithspecialsupportpoliciesgrantedbythecountry, increasedsupportforenvironmentalprotection,medicalcare,education, tourism,communicationsandotherweakperiodicandgreenfinance,andpeople’slivelihoodconsumptionindustries,effectivelycompressedandwithdrewbackwardproductivityprojects,andcontinuouslyadjustedandoptimizedthecreditassetstructure.

NPLratios for themanufacturing,wholesaleand retail industriesslightly increased from thoseat thebeginningoftheperiod,mainlyattributabletotheimpactsoftheslowdowninmacroeconomicgrowth,theadjustmentofindustrialstructureand thedecrease inmarketdemand.Certainenterprisessuffered fromoperationdifficultyanddecreaseof repaymentability, certain industrieswithexcesscapacityandbulkcommodity tradesuffered from increasedrisks,whilenegative factorsofprivate lendingandguaranteed financing repaymentdidnot show fundamentalimprovements,resultinginincreasedcreditrisks.

(3)Loandistributionbygeographicalregion

Unit:RMBmillion

RegionDecember31,2015 December31,2014

Loanbalance Percentage(%) Loanbalance Percentage(%)

Headoffice 90,589 5.09 81,928 5.14

Fujian 251,630 14.14 235,059 14.75

Guangdong 174,734 9.82 163,696 10.28

Jiangsu 133,444 7.50 107,073 6.72

Zhejiang 122,778 6.90 118,680 7.45

Shanghai 99,581 5.60 99,549 6.25

Beijing 95,586 5.37 97,591 6.13

Northeast and other regions 237,929 13.37 197,426 12.38

WesternChina 277,343 15.59 235,395 14.78

CentralChina 295,794 16.62 256,751 16.12

total 1,779,408 100 1,593,148 100

TheCompany’s loan distribution by geographical region remained stable.TheCompany encouragedeachbranch combining thenational regional development strategybyexecuting the regional differential policy of“helpandcontrol”,gave fullplay to the regionalcomparativeadvantage, formulatedcreditpolicywith regionalcharacteristics, adjustedandoptimized regional credit structureunder theunifiedcredit policyofheadoffice,according tocomprehensive factors including thecharactersof region, industryecology, industrialstructureandcreditenvironment.

31

2 0 1 5 ANNUAL REPORT

(4)Formsofloanguarantee

Unit:RMBmillion

SecuritytypeDecember31,2015 December31,2014

Loanbalance Percentage(%) Loanbalance Percentage(%)

Unsecuredloans 309,261 17.38 281,107 17.65

Guaranteedloans 401,035 22.54 382,267 23.99

Securedbymortgage 826,016 46.42 712,332 44.71

Securedbycollateral 173,221 9.73 189,952 11.92

Discountedbills 69,875 3.93 27,490 1.73

total 1,779,408 100 1,593,148 100

Asat theendof the reportingperiod, theproportionof theCompany’sunsecured loansdecreasedby0.27percentagepointascomparedwith the figureat thebeginningof theperiod; theproportionofguaranteed loansdecreasedby1.45percentagepointsascomparedwith thatat thebeginningof theperiod; theproportionof loanssecuredbymortgageandcollateraldecreasedby0.48percentagepointascomparedwiththefigureatthebeginningof theperiod,while theproportionof loanssecuredbydiscountedbills increasedby2.20percentagepointsascomparedwiththefigureatthebeginningoftheperiod.

(5)Loansgrantedtothetoptenborrowers

Unit:RMBmillion

Customer December31,2015 Percentageintotalloans(%)

Customer A 7,600 0.43

Customer B 5,285 0.30

Customer C 4,932 0.28

Customer D 4,594 0.26

Customer E 4,426 0.25

CustomerF 4,236 0.24

Customer G 4,000 0.22

CustomerH 3,529 0.20

Customer I 3,500 0.20

Customer J 3,410 0.19

total 45,512 2.56

Asat theendof the reportingperiod, the loanbalanceof theCompany’s largestsingleborrowerwasRMB7,600million,accountingfor2.11%oftheCompany’snetcapitalbeforeconsolidation,whichconformedtotherequirementby the regulatorydepartments that theproportionof loanbalanceofasingleborrowercouldnotexceed10%ofabank’snetcapital.

32

(6) Structureofpersonalloans

Unit:RMBmillion

ItemDecember31,2015 December31,2014

Loanbalance

Percentage(%)

NPLratio(%)

Loanbalance

Percentage(%)

NPLratio(%)

Personalresidentialandbusinessmortgageloans 298,309 58.27 0.34 198,769 51.50 0.32

Personalbusinessloans 67,216 13.13 2.17 72,879 18.88 1.61

Credit cards 77,960 15.23 1.53 66,364 17.20 1.59

Others 68,421 13.37 1.08 47,938 12.42 0.41

total 511,906 100 0.86 385,950 100 0.79

TheCompany further adjustedandoptimized its structureof personal loansand steppedup support for thedevelopmentof personalmortgage loanbusiness. Influencedby the slowdown in thegrowthof thedomesticeconomy,theNPLratioofpersonal loansslightlywentupasat theendof thereportingperiod,but theoverall riskremainedcontrollable.

TheCompanycontinued tostrengthenriskpreventionandcontrolofpersonal loanbusiness.Firstly, theCompanystrengthenedpre-controlandpost-evaluation,riskmonitoringandwarningofpersonal loanbusiness.Secondly, theCompanystrengthenedriskcontrolforthekeypersonalloanvarieties,andcarriedoutstrictmanagementofcustomeraccessandduration.Thirdly,theCompanycontinuedtocarryoutriskscreening,andacceleratedriskmitigationanddisposal.

33

2 0 1 5 ANNUAL REPORT

Thedetailsofinvestmentaresetoutasfollows:

(1)Analysisoftotalinvestment

Asat theendof the reportingperiod, thenet investmentof theCompanystoodatRMB2,598.945billion, upRMB1,238.504billionor91.04%fromthefigureatthebeginningoftheperiod.Thespecificcompositionofinvestmentissetoutasfollows:

①Classificationbasedonaccountingitem

Unit:RMBmillion

ItemDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Financialassetsatfairvaluethroughprofitorloss 128,685 4.95 44,435 3.27

Available-for-sale 426,634 16.42 408,066 30.00

Receivable 1,834,906 70.60 708,446 52.07

Held-to-maturity 206,802 7.96 197,790 14.54

Long-termequityinvestments 1,918 0.07 1,704 0.12

total 2,598,945 100 1,360,441 100

Duringthereportingperiod,theCompanyincreasedtheinvestmentscale,particularlyinvestmentsthathadrelativelyhighabsoluteyieldsandcontrollablerisks.Attheendofthereportingperiod,thereceivablessubstantiallyincreasedmainlyduetotheinvestmentofwealthmanagementproducts,thetrustbeneficiaryrightandassetmanagementplan.

②Classificationbasedonissuer

Unit:RMBmillion

TypeDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Government bonds 421,475 16.22 268,683 19.75

Centralbankbillsandfinancialbonds 60,343 2.32 63,898 4.70

Corporate bonds 170,508 6.56 179,731 13.21

Other investments 1,944,701 74.83 846,425 62.22

Long-termequityinvestments 1,918 0.07 1,704 0.12

total 2,598,945 100 1,360,441 100

During the reportingperiod, theCompanyseized themarketopportunities.Firstly, theCompanystressedon theincreaseofholdinggovernmentbondsand localgovernmentbondswith taxdeductionandexemption, riskcapitalsavingandhighliquidity.Secondly,theCompanyincreasedtheinvestmentsthathadrelativelyhigherabsoluteyieldsandcontrollablerisks.

34

(2)Long-termequityinvestments

Asattheendofthereportingperiod,thebookvalueoftheCompany’slong-termequityinvestmentswasRMB1.918billion,andthedetailsaresetoutasfollows:

①TheCompanyheld223.20millionsharesofJiujiangCityCommercialBankCo.,Ltd.withaproportionofequityinterestof14.72%andabookvalueofRMB1.720billion.

② IndustrialTrustheld19.00%equity interest inChongqingMachineryandElectronicsHoldingGroupFinanceCompanyLimitedwithabookvalueofRMB147million.

③CIBGuoxinAssetManagementCo.,Ltd.heldthebookvalueofotherlong-termequityinvestmentofRMB51millionintotalattheendofthereportingperiod.

Depositswithbanksandotherfinancialinstitutionsaresetoutasfollows:

Asattheendofthereportingperiod,theCompanyhadabalanceofRMB42.638billionindepositswithbanksandotherfinancial institutions,decreasedRMB58.469billionor57.98%fromthefigureat thebeginningof theperiod.Themainreasonisthatthecompanyadjustedtheassetallocationandreduceddepositswithbanks.

Unit:RMBmillion

TypeDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Deposits with domestic banks 28,082 66.28 89,212 88.47

Depositswithotherdomesticfinancialinstitutions 1,187 2.80 715 0.71

Deposits with foreign banks 13,099 30.92 10,910 10.82

total 42,368 100 100,837 100

Detailsoffinancialassetsheldunderresaleagreementsaresetoutasfollows:

Asattheendofthereportingperiod,theCompanyrecordedabalanceofRMB225.924billioninfinancialassetsheldunderresaleagreements,representingadecreaseofRMB486.837billionor68.30%fromthefigureatthebeginningof theperiod. Inaccordancewith regulatory requirements, thereshouldbenoadditionalnon-standard financialassetsheldunderresaleagreements,andthefinancialassetsheldunderresaleagreementsattheendoftheperioddecreasedaccordinglyastheexistingonesreachedmaturity.

Unit:RMBmillion

TypeDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Bonds 51,550 22.82 25,077 3.52

Bills 97,839 43.31 364,923 51.20

Trustsandotherbeneficialinterests 76,535 33.87 322,359 45.23

Credit assets - - 300 0.04

Financialleasereceivables - - 102 0.01

total 225,924 100 712,761 100

35

2 0 1 5 ANNUAL REPORT

2.Liabilities

Asattheendofthereportingperiod,thetotalliabilitiesoftheCompanystoodatRMB4,981,503million,representinganincreaseofRMB836,200millionor20.17%fromthefigureatthebeginningoftheperiod.ThecompositionofthetotalliabilitiesoftheCompanyisshowninthetablebelow:

Unit:RMBmillion

ItemDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Duetobanksandotherfinancialinstitutions 1,765,713 35.45 1,268,148 30.59

Placementsfrombanksandotherfinancialinstitutions 103,672 2.08 81,080 1.96

Financialassetssoldunderrepurchaseagreements 48,016 0.96 98,571 2.38

Due to customers 2,483,923 49.86 2,267,780 54.71

Debt securities issued 414,834 8.33 185,787 4.48

Otherliabilitiesnote 165,345 3.32 243,937 5.88

total 4,981,503 100 4,145,303 100

Note:IncludedduetoCentralBank,financialliabilitiesatfairvaluethroughprofitorloss,derivativefinancialliabilities,employeebenefitspayable,taxpayable,interestpayableandotherliabilities.

Thespecificcompositionofcustomerdepositsissetoutasfollows:

Thecompany’scustomerdepositsgrewsteadily, thebalanceofcustomerdepositswasRMB2,483,923million,anincreaseofRMB216,143millionor9.53%comparedwiththefigureatthebeginningoftheperiod.

Unit:RMBmillion

ItemDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Demand deposits 1,063,243 42.80 948,425 41.82

Incl:Corporate 868,426 34.96 786,745 34.69

Personal 194,817 7.84 161,680 7.13

Time deposits 1,149,101 46.27 1,053,728 46.47

Incl:Corporate 973,107 39.18 847,319 37.36

Personal 175,994 7.09 206,409 9.11

Other deposits 271,579 10.93 265,627 11.71

total 2,483,923 100 2,267,780 100

36

Thedepositsfrombanksandotherfinancialinstitutionsaresetoutasfollows:

Asattheendofthereportingperiod,theCompanyhadabalanceofRMB1,765,713millionindepositsfrombanksandotherfinancialinstitutions,anincreaseofRMB497,565millionor39.24%fromthefigureatthebeginningoftheperiod.ThemainreasonfortheincreasewastheCompanyorganizedmulti-channelliabilitysources,reinforcedtheexpansionofliabilitiesofnon-depositfinancialinstitutionssoastomitigatevolatilityofmarketliquidity.

Unit:RMBmillion

Transaction counterpartDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Deposits from banks 547,734 31.02 550,267 43.39

Depositsfromotherfinancialinstitutions 1,217,979 68.98 717,881 56.61

total 1,765,713 100 1,268,148 100

Detailsoffinancialassetssoldunderrepurchaseagreementsaresetoutasfollows:

Asat theendof the reportingperiod, theCompany recordedabalanceofRMB48,016million in financialassetssoldunderrepurchaseagreements,representingadecreaseofRMB50,555millionor51.29%fromthefigureatthebeginningof theperiod,mainlydue to thecompanyadjusted liabilitiesallocationand reducedselling repurchaseassets.

Unit:RMBmillion

TypeDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Bonds 39,980 83.26 78,188 79.32

Bills 8,036 16.74 19,864 20.15

Others - - 519 0.53

total 48,016 100 98,571 100

37

2 0 1 5 ANNUAL REPORT

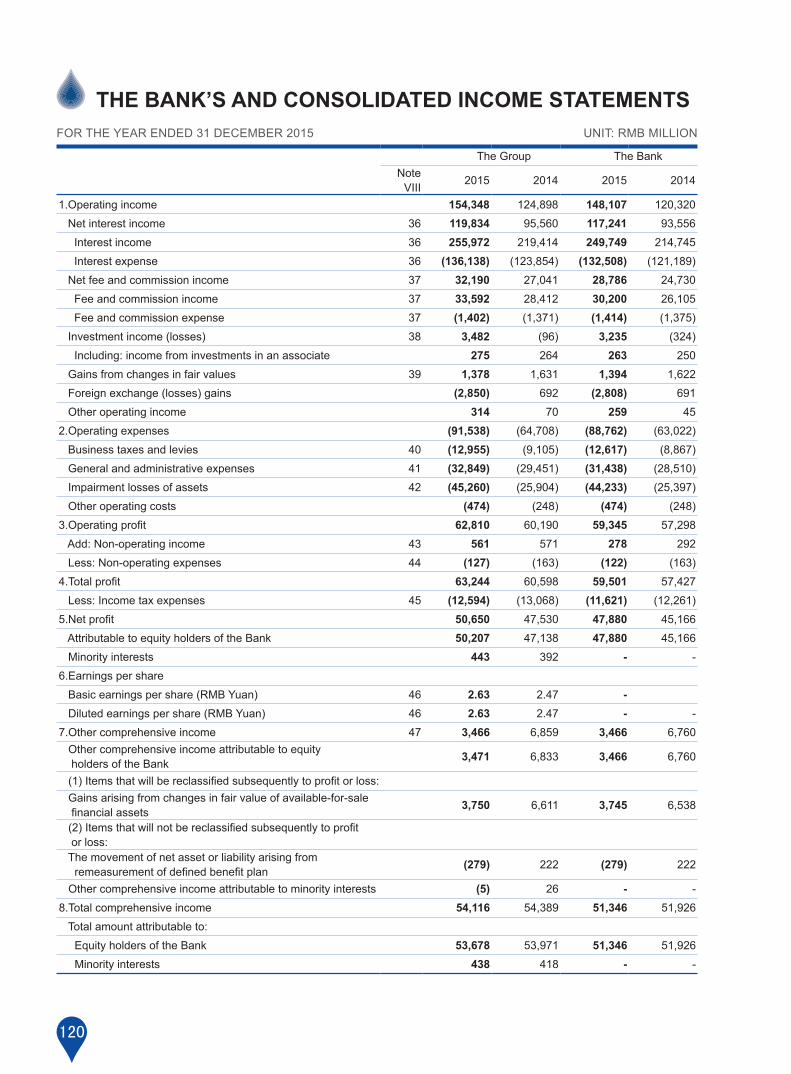

(III)AnalysisoftheincomestatementDuring the reportingperiod, theCompanydeliveredsteadyandhealthygrowth invariousbusinesses,withsteadygrowth in interest-bearingassets.TheCompany flexiblyallocatedassetsbycapturingmarketopportunitiesandincreasedtheyieldsofinterest-bearingassets,withstablenetincreasemargin.Therewasasustainedgrowthinfeeandcommissionincome.Thecost-to-incomeratiowasmaintainedatarelativelylowlevel.ThenetprofitattributabletoshareholdersoftheparentcompanyreachedRMB50,207million,up6.51%year-on-year.

Unit:RMBmillion

Item 2015 2014 Increase/DecreaseYoY(%)

Operating income 154,348 124,898 23.58

Net interest income 119,834 95,560 25.40

Netnon-interestincome 34,514 29,338 17.64

Business tax and surcharges (12,955) (9,105) 42.28

Operating and administrative expense (32,849) (29,451) 11.54

Impairmentlossofassets (45,260) (25,904) 74.72

Other operating costs (474) (248) 91.13

Netnon-operatingincomeandexpense 434 408 6.37

Profitbeforetax 63,244 60,598 4.37

Income tax (12,594) (13,068) (3.63)

Netprofit 50,650 47,530 6.56

Profitandlossofminorityshareholders 443 392 13.01

Netprofitattributabletotheshareholdersoftheparentcompany 50,207 47,138 6.51

1.Netinterestincome

Duringthereportingperiod,thenetinterestincomeoftheCompanywasRMB119,834million,upRMB24,274millionor25.40%year-on-year,mainlybecause interest-bearingassetsgrowth.Ononehand, the interestmarginof theCompanydecreasedslightly,thenetinterestmargindownby0.03percentagepointto2.45%.Ontheotherhand,thebusinessmaintainedasteadyandrapidgrowth,dailyaveragescaleof interest-bearingassetsup26.71%year-on-year.

TheinterestincomeincreasedRMB36,558millionor16.66%year-on-year.TheinvestmentinterestincomeincreasedbyRMB58,205millionor116.84%year-on-year,mainlydue to the investmentdailyaveragescaleup135.90%year-on-yearandholding resale interest incomedecreasedbyRMB28,953millionor51.39%year-on-year,mainlybecausedailyaveragescaleunderrepurchaseagreementsdown43.43%year-on-year.

TheinterestexpensesincreasedRMB12,284millionor9.92%year-on-year.Amongthem,thebondinterestspendingwasupRMB7.537billionor146.75%year-on-year,mainlyduetoissuingdepositreceiptandfinancialbonds,issuingbondsdailyscale rose173.59%year-on-year.Deposit interestexpenses increasedbyRMB5.143billionor9.84%year-on-year,mainlybecauseofthesizeofthedepositsdailyaverageroseby13.03%year-on-yearand10BPsdropininterestrates.

38

Thecompositionofinterestincomeandinterestexpenseduringtheperiodissetoutasfollows:

Unit:RMBmillion

Item2015 2014

Amount Percentage(%) Amount Percentage(%)

Interest income

Interestincomefromcorporateandpersonalloans 99,797 38.99 91,411 41.66

Interestincomefromdiscountedbills 1,953 0.76 1,982 0.90

Interest income from investments 108,019 42.20 49,814 22.70

Interest income from the amount due from theCentralBank 6,497 2.54 6,205 2.83

Interestincomefromplacementswithbanksandotherfinancialinstitutions 2,095 0.82 4,645 2.12

Interestincomefromresaleagreements 27,382 10.70 56,335 25.68

Interest income from deposits in banks and other financialinstitutions 3,894 1.52 4,782 2.18

Interestincomefromfinancialleasing 5,367 2.10 4,031 1.84

Other interest income 968 0.38 209 0.09

Subtotalofinterestincome 255,972 100 219,414 100

Interest expense

InterestexpenseonloansfromtheCentralBank 1,801 1.32 210 0.17

Interest expense on deposits 57,422 42.18 52,279 42.21

Interest expense on bonds issuance 12,673 9.31 5,136 4.15

Interest expense on deposits from banks and other financialinstitutions 57,897 42.53 57,565 46.48

Interestexpenseonplacementsfrombanksandotherfinancialinstitutions 3,785 2.78 3,546 2.86

Interest expense on repurchase agreements 2,427 1.78 4,969 4.01

Other interest expenses 133 0.10 149 0.12

Subtotalofinterestexpense 136,138 100 123,854 100

Net interest income 119,834 95,560

39

2 0 1 5 ANNUAL REPORT

Unit:RMBmillion

Item2015 2014

Average balance

Averageyield(%)

Average balance Averageyield(%)

Interest-bearingassets

Corporateandpersonalloansandadvances 1,710,902 6.00 1,432,788 6.52

Basedonloantype:

Corporateloans 1,349,597 5.97 1,133,841 6.50

Personalloans 361,305 6.11 298,947 6.59

Basedonloanterm:

Generalshort-termloans 835,668 5.87 778,948 6.51

Mediumandlong-termloans 828,768 6.23 623,019 6.53

Discountedbills 46,466 4.20 30,821 6.43

Investments 1,957,950 5.52 829,982 6.01

DepositsintheCentralBank 429,324 1.51 414,041 1.50

Depositsinandplacementswithbanksandotherfinancialinstitutions(includingfinancialassetsheldunderresaleagreements)

697,977 4.81 1,120,909 6.10

Financialleasing 92,771 5.79 60,657 6.65

total 4,888,924 5.24 3,858,377 5.69

Item2015 2014

Average balance

Average cost ratio(%)

Average balance

Average cost ratio (%)

Interest-bearingliabilities

Deposit taking 2,423,159 2.33 2,143,895 2.43

Corporate deposits 2,047,405 2.37 1,799,477 2.49

Demand deposits 686,645 0.67 711,260 0.64

Time deposits 1,360,760 3.22 1,088,217 3.69

Personaldeposits 375,754 2.14 344,418 2.15

Demand deposits 169,573 0.36 150,624 0.40

Time deposits 206,181 3.59 193,794 3.50

Depositsinandplacementsfrombanksandotherfinancialinstitutions(includingfinancialassetssold under repurchase agreements)

1,804,817 3.61 1,324,701 5.00

BorrowingsfromtheCentralBank 52,088 3.46 6,000 3.50

Bondspayable 299,328 4.23 109,408 4.69

total 4,579,392 2.97 3,584,004 3.45

Net interest spread - 2.26 - 2.23

Net interest margin - 2.45 - 2.48

40

2.Netnon-interestincome

During the reportingperiod, thenetnon-interest incomeof theCompanywasRMB34,514million,accounting for22.36%oftheoperatingincome,representinganincreaseofRMB5,176millionor17.64%year-on-year.Thespecificcompositionissetoutasfollows:

Unit:RMBmillion

Item 2015 2014

Net fee and commission income 32,190 27,041

Gainandlossfrominvestment 3,482 (96)

Gainandlossfromchangesinfairvalue 1,378 1,631

Gainandlossfromexchange (2,850) 692

Income from other businesses 314 70

total 34,514 29,338

Duringthereportingperiod,theCompanyrealizedfeeandcommissionincomeofRMB32,190million,upRMB5,149millionor19.04%year-on-year. Items likegainand loss from investment,gainand loss fromchanges in fairvalueandgainandlossfromexchangewerehighlyinterrelated.Afterthereclassificationbasedontheirbusinessnature,thegainrecognizedreachedRMB2,010million,downRMB217millionyear-on-year.

Thespecificcompositionoffeeandcommissionincomeissetoutasfollows:

Unit:RMBmillion

Item2015 2014

Amount Percentage(%) Amount Percentage(%)

Feeandcommissionincome:

Feeincomefrompaymentandsettlement 658 1.96 743 2.62

Feeincomefrombankcards 6,376 18.98 5,653 19.90

Feeincomefromagencybusiness 3,394 10.10 2,789 9.82

Feeincomefromguaranteecommitment 1,787 5.32 1,794 6.31

Feeincomefromtradingbusiness 198 0.59 133 0.47

Feeincomefromcustodybusiness 4,316 12.85 4,211 14.82

Feeincomefromconsultingservice 13,242 39.42 10,512 37.00

Feeincomefromtrustbusiness 1,631 4.86 1,376 4.84

Feeincomefromleasebusiness 931 2.77 534 1.88

Other fee income 1,059 3.15 667 2.34

Sub-total 33,592 100 28,412 100

Feeandcommissionexpense 1,402 1,371

Net fee and commission income 32,190 27,041

41

2 0 1 5 ANNUAL REPORT

3.Operatingandadministrativeexpense

Duringthereportingperiod,theoperatingexpenseoftheCompanywasRMB32.849billion,upRMB3.398billionor11.54%year-on-year.Thespecificcompositionissetoutasfollows:

Unit:RMBmillion

Item2015 2014

Amount Percentage(%) Amount Percentage(%)

Accruedpayroll 19,784 60.23 17,369 58.98

Depreciationandamortization 1,937 5.90 1,684 5.72

Leaseexpense 2,608 7.94 2,387 8.10

Othergeneralandadministrativeexpenses 8,520 25.93 8,011 27.20

total 32,849 100 29,451 100

During the reportingperiod, tomeet theneedsof thebusinessdevelopmentand institutionalexpansion,operatingexpenses increasedcorrespondingly.Operating incomerose23.58%year-on-yearduring thisperiod, thecost-to-incomeratiofell2.19%year-on-year,maintainingatalowlevelof21.59%,withexpensesmaintainingatareasonablelevel.

4.Impairmentlossofassets

Duringthereportingperiod,theCompany’simpairmentlossofassetswasRMB45,260million,upRMB19,356millionor74.72%year-on-year.Thespecificcompositionofimpairmentlossofassetsissetoutasfollows:

Unit:RMBmillion

Item2015 2014

Amount Percentage(%) Amount Percentage(%)

Impairmentlossofloans 37,093 81.96 19,651 75.86

Impairmentlossoninvestmentinaccountsreceivable 5,039 11.13 4,151 16.02

Impairmentlossonavailable-for-salefinancialassets 1,095 2.42 1,228 4.74

Impairmentlossonfinancialleasingreceivable 425 0.94 358 1.38

Impairmentlossonotherassets 1,608 3.55 516 2.00

total 45,260 100 25,904 100

During the reportingperiod, theCompanyaccrueda loan impairment lossofRMB37,093million,upRMB17,442millionyear-on-year,mainlybecauseoftheincreaseinscaleofloans.TheCompanymadeprovisionforimpairmentbasedonthepredictedpresentvalueofdiscountedfuturecashflowsdeterminedaspertheoriginaleffectiveinterestratesoftheloans,pursuanttotherelevantrequirementsoftheAccountingStandardsforBusinessEnterpriseswithindustryriskstakenintoaccount.

42

5.Incometax

Duringthereportingperiod,theeffectiveincometaxrateoftheCompanywas19.91%.Thedifferencebetweentheincometaxexpenseandtheamountcalculatedbasedonthe25%statutorytaxrateissetoutasfollows:

Unit:RMBmillion

Item 2015

Profitbeforetax 63,244

Statutorytaxrate(%) 25

Incometaxcalculatedatstatutorytaxrate 15,811

Effectontaxduetoadjustmentonthefollowingitems:

Tax-exemptincome (3,549)

Non-deductibleitems 226

Adjustmentonthetaxofpreviousyears 106

Income tax expense 12,594

(IV)AnalysisofthecashflowstatementUnit:RMBmillion

Item 2015 2014

Cashflowsfromoperatingactivities 818,693 682,060

Cashflowsfrominvestingactivities (1,078,507) (566,235)

Cashflowsfromfinancingactivities 213,791 114,322