Systemwide Accounting Kelly Cox Year-End Legal Training May 2010.

43

Systemwide Accounting Kelly Cox Year-End Legal Training May 2010

-

date post

22-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Systemwide Accounting Kelly Cox Year-End Legal Training May 2010.

Systemwide Accounting

Kelly Cox

Year-End Legal Training

May 2010

Topics Covered• Systemwide Investment Fund – Trust (SWIFT)• Year-End Reserve Entry • General Fund Spend Down • Centralized Payroll Adjustments (CPA)• General Fund Appropriation Payroll SWAP • General Fund and Trust Fund Tie Points• ARRA• CSURMA Accounting

May 2010 2Year-End Legal Training

Systemwide Investment Fund – Trust (SWIFT)

• CSU Banking 101• Bank of CSU Statement Reconciliation• SWIFT Investments and Earnings• Appropriate SWIFT Balances• SWIFT Negative Balances• Cash Posting Orders (CPO)

May 2010 Year-End Legal Training 3

CSU Banking 101 The California State University Systemwide Investment

Fund‐Trust (SWIFT) was established on July 2, 2007 for the purpose of pooling university cash and investments, providing centralized cash and investment management services.

The campus’ cash management is centralized by using one bank, Wells Fargo Bank (WFB)

The surplus cash at the bank is invested with US Bank, aka Systemwide Investment Fund – Trust (SWIFT).

May 2010 Year-End Legal Training 4

CSU Banking 101 Cash Management Office (CMO) analyzes the

cash activity across the system to determine the CSU daily cash requirements. If there is a shortage, a redemption (wire transfer)

from US Bank to WFB is needed. If there is a surplus, CMO transfers funds to US Bank

from WFB. These transactions do not affect a campus’ over-all

cash/investment balance. May 2010 Year-End Legal Training 5

CSU Banking 101 Monthly Statements for SWIFT are produced

from the Bank of CSU database and distributed to each SWIFT participants.

ZBA Monthly Statements for WFB are produced by WFB distributed to each account holder.

FIRMS Object Code 101100 cash – Short Term Investments is used to record transactions that flow through the WFB and SWIFT.

May 2010 Year-End Legal Training 6

Bank of CSU Statement Reconciliation

• Deadline:• Bank of CSU Statements will be distributed by

July 7Th

• Bank of CSU statement is used for CPO transaction and WFB balance verification.• Campuses also receive statements from WFB to

reconcile detail transactions.

May 2010 Year-End Legal Training 7

Bank of CSU Statement Reconciliation Tips…..

• Discrepancies in monthly balances between the campus G/L and Bank of CSU statements are usually caused by bank adjustments • ACH disbursements adjustments such as ACH

rejects • Paper/controlled disbursements adjustments due

to fraud investigations or checks posted by Wells Fargo Bank as cash paid item

May 2010 Year-End Legal Training 8

SWIFT Investments and Earnings

• Campuses will receive a pass-down entry no later than the July 26th for their June net earnings and Changes in Unrealized Gain/Loss.• There is no legal entry required for the Changes

in Unrealized Gain/Loss. • http://www.calstate.edu/sfsr/gaap/

May 2010 Year-End Legal Training 9

SWIFT Investments and Earnings Con’t

• Record investment earnings in the Pooled Investment Fund (CSU Fund 541).• SWIFT net investment earnings should be then

allocated internally within campus funds according to that campus’ allocation policy.

• Net Income in the Pooled Investment Fund is zero (“no fund balance”) at end of fiscal year.

• See Chapter 2.2.4 for accounting entries

May 2010 Year-End Legal Training 10

Appropriate SWIFT Balances

• The State University Trust Fund (SCO 0948) is the only fund for which cash can be held locally within SWIFT. • Governmental funds (e.g.Capital Outlay) or other

Enterprise SCO funds (0576, 0578, etc) must be held at the State and cannot be within SWIFT. • Reconcile to ensure that no SWIFT cash is

recorded in non-0948 funds.

May 2010 Year-End Legal Training 11

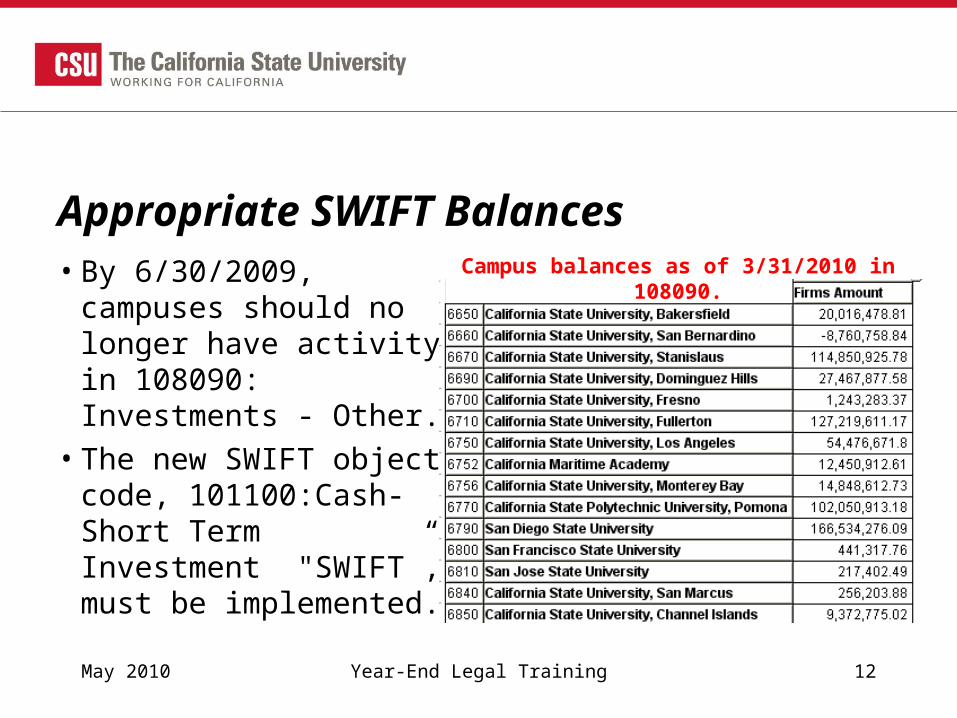

Appropriate SWIFT Balances• By 6/30/2009, campuses

should no longer have activity in 108090: Investments - Other.• The new SWIFT object

code, 101100:Cash-Short Term Investment "SWIFT”, must be implemented.

May 2010 Year-End Legal Training 12

Campus balances as of 3/31/2010 in 108090.

SWIFT Negative Balances

• At Year end, the Cash – Short Term Investments “SWIFT” accounts within each CSU fund should not be negative. • For non swap campuses, a year-end entry to

exchange 305022 Fund balance clearing (FBC) with101100 Cash – Short Term Investments “SWIFT” to correct negative balances is required.• See Chapter 2.2.6 for suggested process

May 2010 Year-End Legal Training 13

Cash Posting Orders (CPO)

• Preferred method to collect and disburse funds between campuses and the CO • To avoid year-end scramble request a CPO

rather than issuing invoices.• Contact Lilian Audet at [email protected] to

request a CPO to be executed. • See chapter 2.2.7 for more information.

May 2010 Year-End Legal Training 14

Cash Posting Orders (CPO)

• Two Contacts:• CPO Contact: Address questions regarding the

purpose of the CPO to the Cash Posting Order contact listed at the bottom of the CPO memo page.

• Accounting Contact: Address accounting related questions (FIRMS object codes or the journal entries) to the Accounting Entries contact listed at the bottom of the CPO memo page.

May 2010 Year-End Legal Training 15

Year-End Reserve Entry

• The entire fund balance in the CSU Operating Fund (485) and CERF (441) must be reserved via a “pre-closing” year-end memo entry in the ACTUALS ledger. • The Systemwide budget office uses the campus

entries to know how you plan to use the “excess” funds.

May 2010 Year-End Legal Training 16

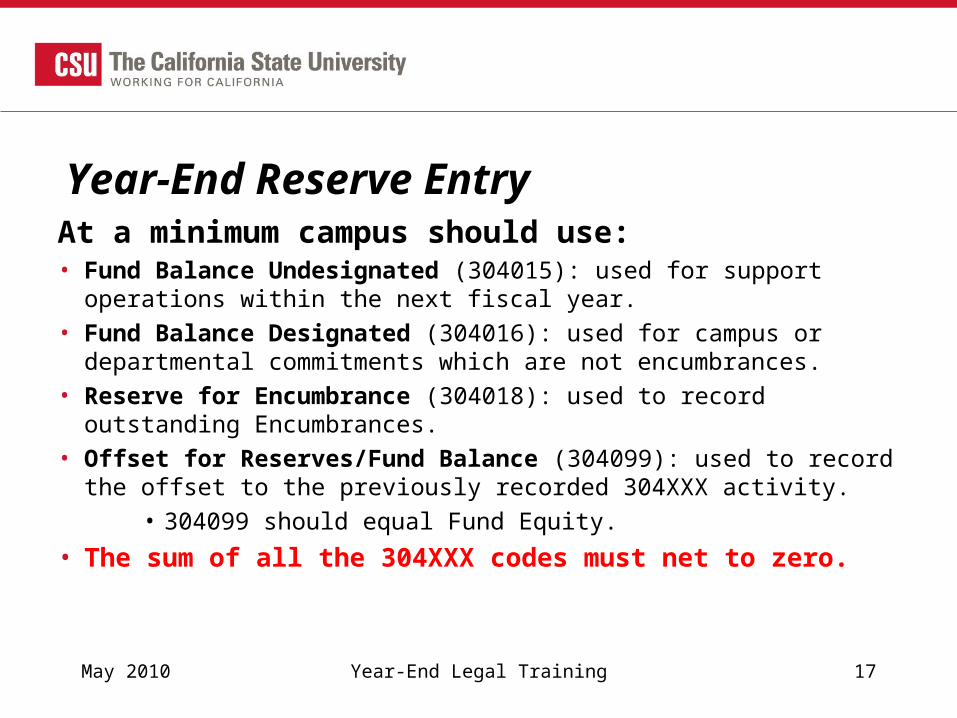

Year-End Reserve Entry At a minimum campus should use:• Fund Balance Undesignated (304015): used for support operations

within the next fiscal year.• Fund Balance Designated (304016): used for campus or

departmental commitments which are not encumbrances.• Reserve for Encumbrance (304018): used to record outstanding

Encumbrances.• Offset for Reserves/Fund Balance (304099): used to record the

offset to the previously recorded 304XXX activity. • 304099 should equal Fund Equity.

• The sum of all the 304XXX codes must net to zero.

May 2010 Year-End Legal Training 17

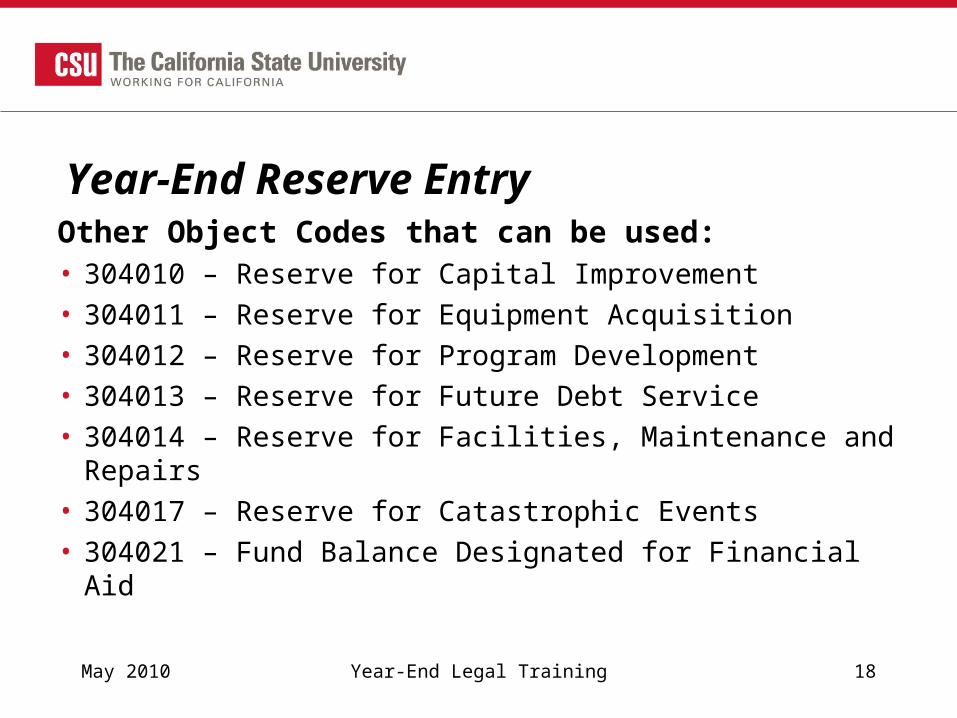

Year-End Reserve Entry Other Object Codes that can be used:• 304010 – Reserve for Capital Improvement• 304011 – Reserve for Equipment Acquisition• 304012 – Reserve for Program Development• 304013 – Reserve for Future Debt Service • 304014 – Reserve for Facilities, Maintenance and

Repairs• 304017 – Reserve for Catastrophic Events• 304021 – Fund Balance Designated for Financial Aid

May 2010 Year-End Legal Training 18

General Fund Spend Down

• The primary objective of RMP was to define the State University Trust Fund (SCO 0948) as their primary operating fund. • All payroll was then directed to State Fund 0948.

Plan of Financial Action (PFA) is submitted to move payroll expenditures from Trust to General Fund in order to “spend down” the general fund.

• This process is called the Centralized Payroll Adjustments (CPA).

May 2010 Year-End Legal Training 19

Centralized Payroll Adjustments (CPA)

• CMO determines campus draw down of state support to fund payroll.• Campus are to record this PFA as:• Credit to 690003 in the CSU Operating Fund,

CSU Fund 485 and a debit to 305022• Debit the same account, 690003, in the General

Fund SCO Fund 0001 and a credit to 305022

May 2010 Year-End Legal Training 20

Centralized Payroll Adjustments (CPA)Con’t

• CMO then determines campus draw down of remaining non-state funded payroll• Campus are to record this CPO as: • Credit to 101100 Cash – Short Term Investments

“SWIFT”• debit to 305022 Fund Balance Clearing

• By the 3rd quarter, the remaining months will totally be funded by the campuses SWIFT funds

May 2010 Year-End Legal Training 21

General Fund Appropriation Payroll SWAP

• To accomplish the goal of “spending down” the General Fund, some campuses need to exchange General Fund appropriation with SWIFT dollars. • During the 3rd quarter of each fiscal year the

SWAP will occur.

May 2010 Year-End Legal Training 22

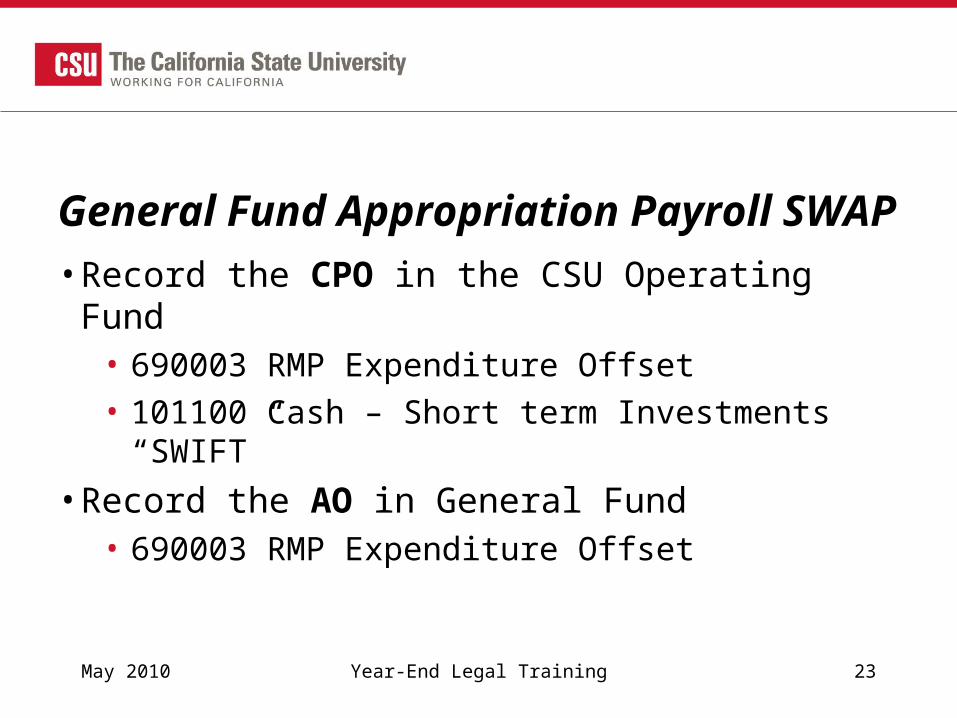

General Fund Appropriation Payroll SWAP

• Record the CPO in the CSU Operating Fund• 690003 RMP Expenditure Offset • 101100 Cash – Short term Investments “SWIFT”

• Record the AO in General Fund• 690003 RMP Expenditure Offset

May 2010 Year-End Legal Training 23

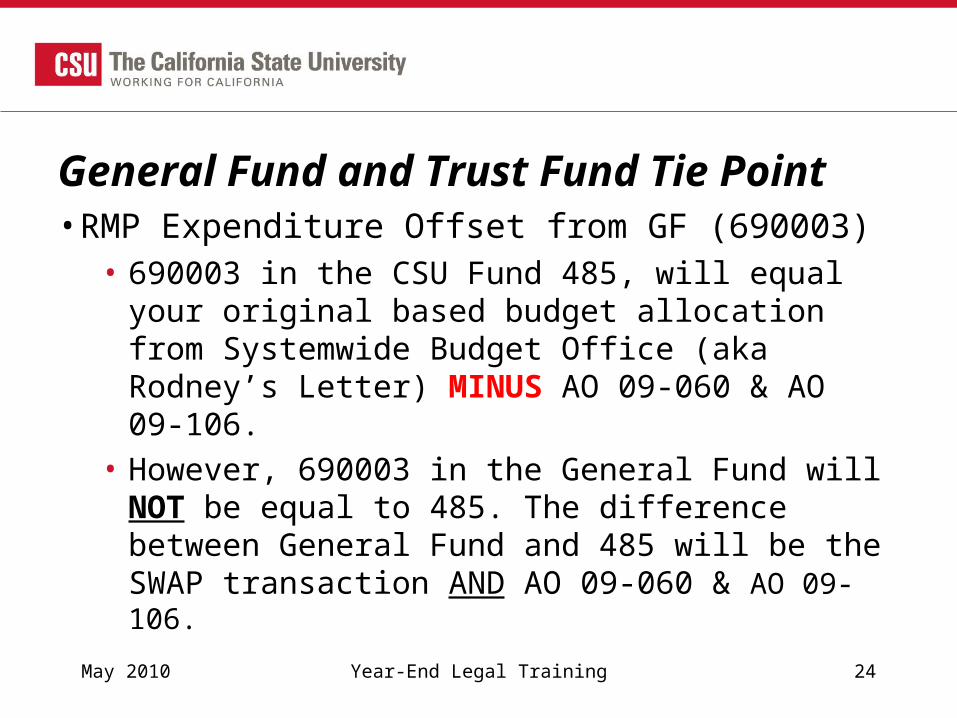

General Fund and Trust Fund Tie Point• RMP Expenditure Offset from GF (690003)• 690003 in the CSU Fund 485, will equal your

original based budget allocation from Systemwide Budget Office (aka Rodney’s Letter) MINUS AO 09-060 & AO 09-106.

• However, 690003 in the General Fund will NOT be equal to 485. The difference between General Fund and 485 will be the SWAP transaction AND AO 09-060 & AO 09-106.

May 2010 Year-End Legal Training 24

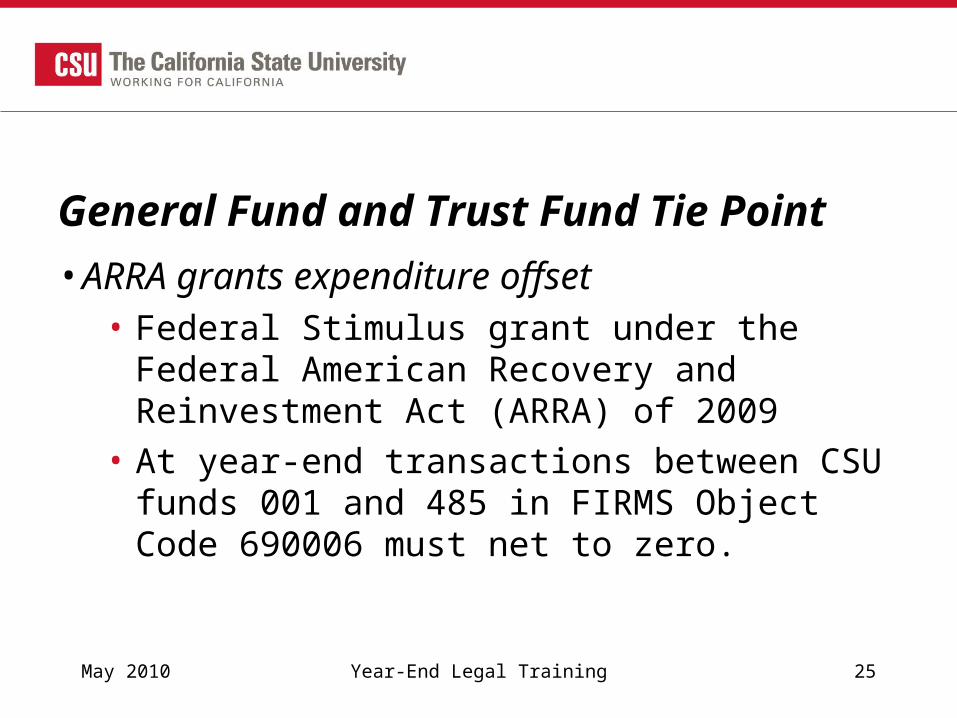

General Fund and Trust Fund Tie Point

• ARRA grants expenditure offset• Federal Stimulus grant under the Federal

American Recovery and Reinvestment Act (ARRA) of 2009

• At year-end transactions between CSU funds 001 and 485 in FIRMS Object Code 690006 must net to zero.

May 2010 Year-End Legal Training 25

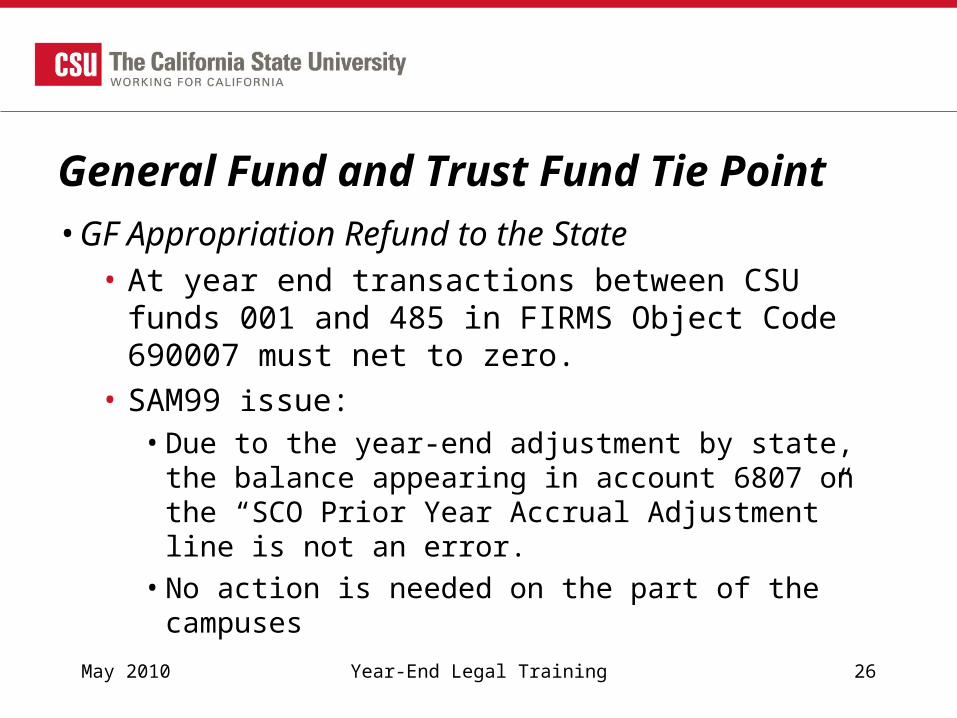

General Fund and Trust Fund Tie Point

• GF Appropriation Refund to the State• At year end transactions between CSU funds 001

and 485 in FIRMS Object Code 690007 must net to zero.

• SAM99 issue: • Due to the year-end adjustment by state, the

balance appearing in account 6807 on the “SCO Prior Year Accrual Adjustment” line is not an error. • No action is needed on the part of the campuses

May 2010 Year-End Legal Training 26

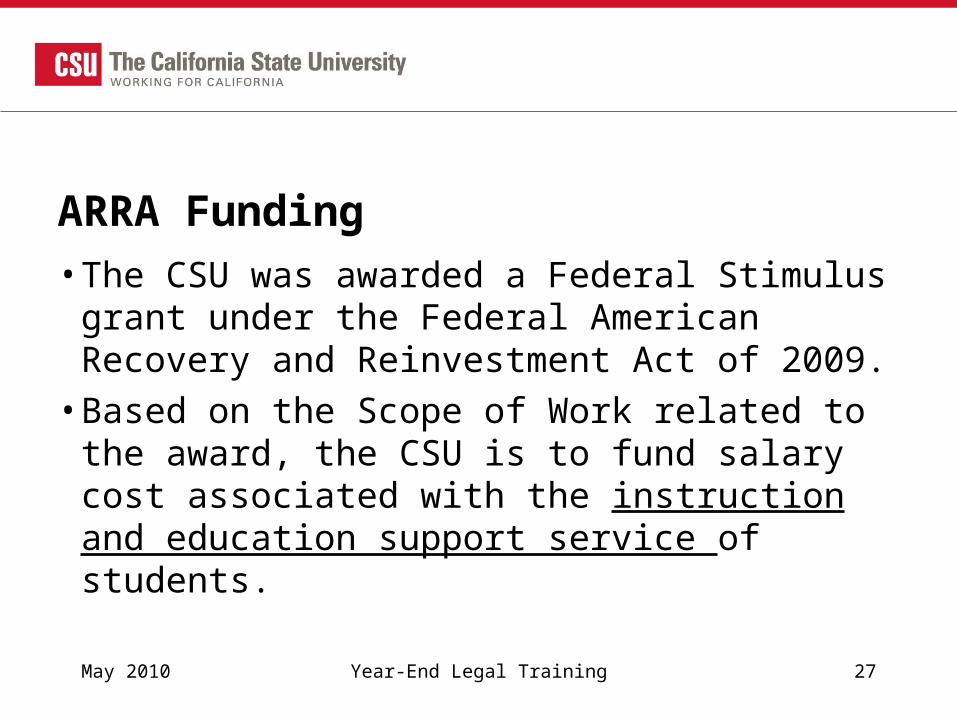

ARRA Funding

• The CSU was awarded a Federal Stimulus grant under the Federal American Recovery and Reinvestment Act of 2009. • Based on the Scope of Work related to the

award, the CSU is to fund salary cost associated with the instruction and education support service of students.

May 2010 Year-End Legal Training 27

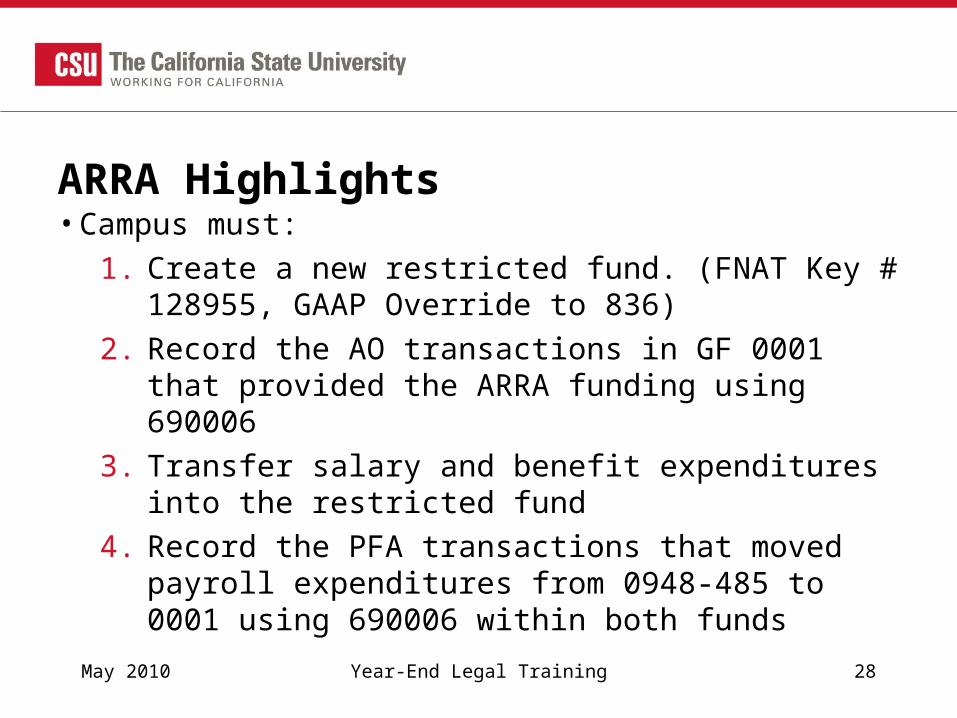

ARRA Highlights• Campus must:

1. Create a new restricted fund. (FNAT Key # 128955, GAAP Override to 836)

2. Record the AO transactions in GF 0001 that provided the ARRA funding using 690006

3. Transfer salary and benefit expenditures into the restricted fund

4. Record the PFA transactions that moved payroll expenditures from 0948-485 to 0001 using 690006 within both funds

May 2010 Year-End Legal Training 28

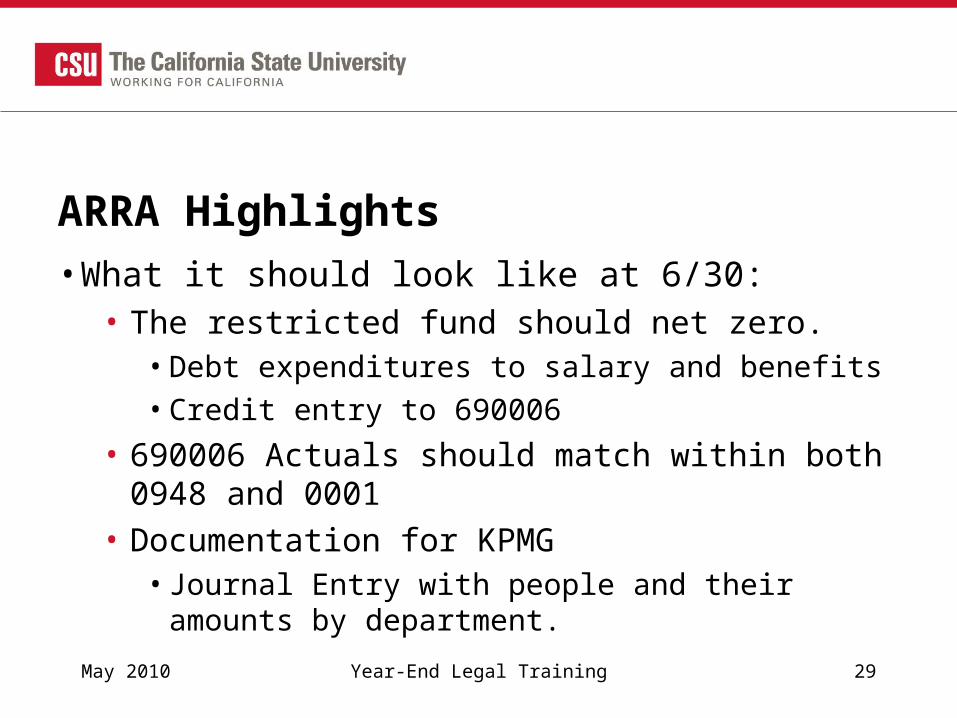

ARRA Highlights

• What it should look like at 6/30:• The restricted fund should net zero.• Debt expenditures to salary and benefits• Credit entry to 690006

• 690006 Actuals should match within both 0948 and 0001

• Documentation for KPMG• Journal Entry with people and their amounts by

department. May 2010 Year-End Legal Training 29

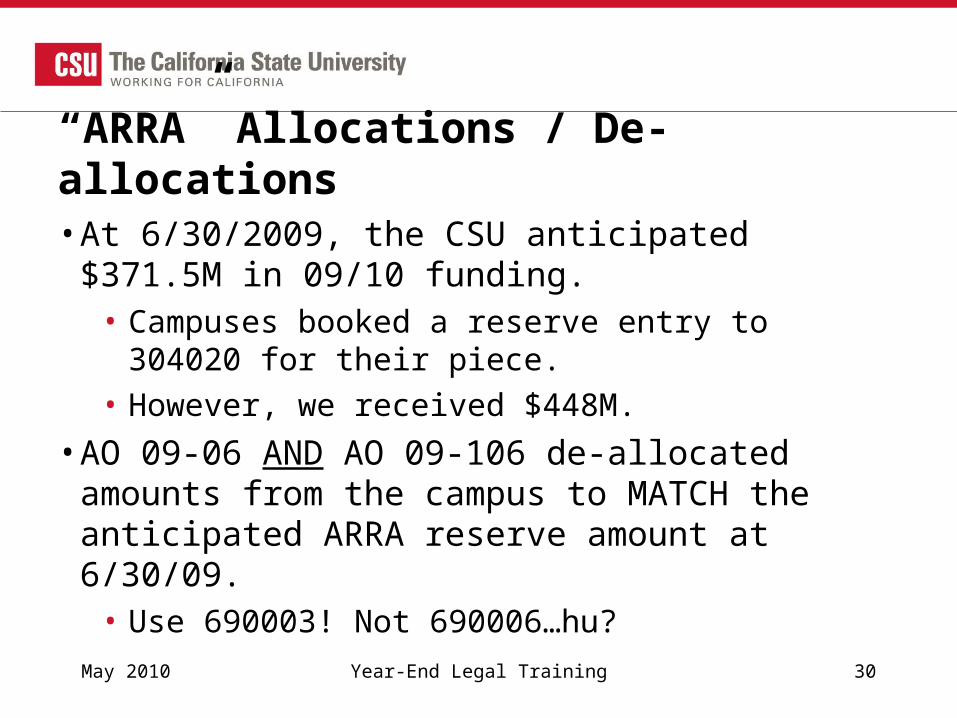

“ARRA” Allocations / De-allocations• At 6/30/2009, the CSU anticipated $371.5M in

09/10 funding. • Campuses booked a reserve entry to 304020 for

their piece. • However, we received $448M.

• AO 09-06 AND AO 09-106 de-allocated amounts from the campus to MATCH the anticipated ARRA reserve amount at 6/30/09.• Use 690003! Not 690006…hu?

May 2010 Year-End Legal Training 30

CSU Risk Management Accounting

• Organization• Accounting Tips• Dividend Change• Accruals• Outstanding Invoices• IDL/NDI/UI

• Deductible Recovery

May 2010 Year-End Legal Training 31

CSU Risk Management Accounting –Organization

• A joint power authority (JPA) composed of CSU campuses and its Auxiliary Organizations to protect member resources through broad insurance coverage programs and quality risk management services.

May 2010 Year-End Legal Training 32

CSU Risk Management Accounting-Accounting Tips CSURMA expenditures need to be consistently

recorded across the CSU First , The Industrial Disability Leave (IDL), Non-

Industrial Disability Leave (NDI) and Unemployment Insurance (UI) Program is designed for CSU campuses to cover their CSU employee’s disability leave and unemployment.

May 2010 Year-End Legal Training 33

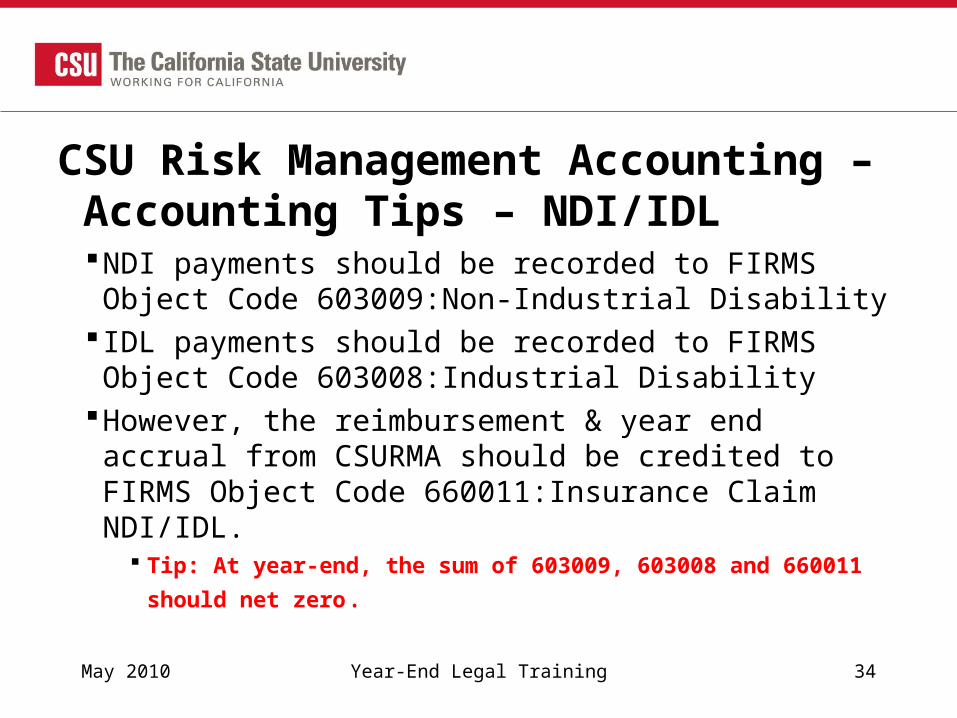

CSU Risk Management Accounting – Accounting Tips – NDI/IDL

NDI payments should be recorded to FIRMS Object Code 603009:Non-Industrial Disability

IDL payments should be recorded to FIRMS Object Code 603008:Industrial Disability

However, the reimbursement & year end accrual from CSURMA should be credited to FIRMS Object Code 660011:Insurance Claim NDI/IDL.

Tip: At year-end, the sum of 603009, 603008 and 660011 should

net zero.

May 2010 Year-End Legal Training 34

CSU Risk Management Accounting - Accounting Tips - UI

Unemployment Insurance (UI) payments to EDD should be coded to 603010: Unemployment Compensation AND the reimbursement & year end accrual from CSURMA should be a credited to 603010.

Tip: At year-end, 603010 should net zero

May 2010 Year-End Legal Training 35

CSU Risk Management Accounting - Accounting Tips – Deductible Recovery• Second, Deductible Recovery.• Throughout the policy year CSURMA makes payment

on claims on behalf of the campus. Quarterly campuses are to reimburse CSURMA up to their deductible limit. • This function is referred to as the Deductible Recovery

process. • Payments for deductible amounts should be recorded to

660012: Insurance Claim Deductible. • Tip: Account should tie back to all 4 quarter deductible amounts plus

any property deductible entries made.

May 2010 Year-End Legal Training 36

CSU Risk Management Accounting –Dividend

• Record the annual dividend to FIRMS Object Code 580092:CSURMA Dividend• The Chancellor’s office is to record to FIRMS

Object Code 660013• For GAAP reporting, both the campus and the

CO object codes map to GASB35 Natural Class code 723006 for systemwide elimination.

• See Chapter 2.3.4 for more information

May 2010 Year-End Legal Training 37

CSU Risk Management Accounting – Accrual• CSURMA and the campuses accounting transaction must

be in sync to avoid FIRMS errors. • The timing of the payments and receipts should be

monitored extensively so that the CSU consolidated reports are accurately presented.• Always communicate to CSURMA the campus CSU

Fund in which the transaction is recorded.• When recording in 0948, the campus entry would be

131547, Due from CSU 547 - TF CSU Risk Mgmt.

May 2010 Year-End Legal Training 38

CSU Risk Management Accounting –Outstanding Invoices• Please process a wire transfer rather than issuing a

check • Checks are hard to track down and a slow! • If a check must be cut, please mail checks out by

Monday, 6/21.• Please email Mandy Wong at [email protected] to

verify that we have received the payment. • The CO will follow this same practice when paying

campus outstanding invoices.

May 2010 Year-End Legal Training 39

CSU Risk Management Accounting – IDL/NDL/UI Accrual• In order to report all four quarters of IDL/NDL/UI within

the appropriate fiscal year, a legal accrual is needed. • This is an ugly process since this accrual can not be

communicated until the first week of July. • Email actual scanned invoices or estimated accruals to

Mandy ([email protected]) by 7/1

• Include amounts by program IDL, NDI or UI & campus CSU Fund.

• When recording in 0948, the campus entry would be 131547, Due from CSU 547 - TF CSU Risk Mgmt

May 2010 Year-End Legal Training 40

CSU Risk Management Accounting – Accruals• Tips for a clean ITT FIRMS Edit

• Wire Transfer instead of Checks

• Contact Mandy ([email protected])

• include campus CSU Fund.

• When recording in 0948, the campus entry would be 131547, Due from CSU 547 - TF CSU Risk Mgmt

• All Accruals will be included on the CO Interagency Transaction Report published on or before July 7th

May 2010 Year-End Legal Training 41

CSU Risk Management Accounting – Deductible Recovery• The CSURMA Deductible Recovery is getting easier!!! • This year we will process a CPO instead of an ADNOAT• However, it will still be late. We will be posted no later

than the end of business on Tuesday, July 6th • The campus entry will be Cash not Due to 547.• NO FIRMS EDIT ISSUES!!!

May 2010 Year-End Legal Training 42

www.calstate.edu

May 2010 43Year-End Legal Training