Syria - iuj.ac.jp · The Economist Intelligence Unit The Economist Intelligence Unit is a...

33

COUNTRY REPORT Syria The full publishing schedule for Country Reports is now available on our web site at http://www.eiu.com/schedule. 3rd quarter 1999 The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom

Transcript of Syria - iuj.ac.jp · The Economist Intelligence Unit The Economist Intelligence Unit is a...

COUNTRY REPORT

SyriaThe full publishing schedule for Country Reports is nowavailable on our web site at http://www.eiu.com/schedule.

3rd quarter 1999

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newsletters toannual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1000Fax: (44.20) 7499 9767E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2802 7288Fax: (852) 2802 7638E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU ElectronicNew York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Jeremy Eagle Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023

This publication is available on the following electronic and other media:

Online databases

FT Profile (UK)Tel: (44.20) 7825 8000

DIALOG (US)Tel: (1.415) 254 7000

LEXIS-NEXIS (US)Tel: (1.800) 227 4908

M.A.I.D/Profound (UK)Tel: (44.20) 7930 6900

NewsEdge Corporation (US)Tel: (1.718) 229 3000

CD-ROM

The Dialog Corporation (US)SilverPlatter (US)

Microfilm

World Microfilms Publications(UK)Tel: (44.20) 7266 2202

Copyright© 1999 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-7211

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

Syria 1

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Contents

3 Summary

4 Political structure

5 Economic structure

6 Outlook for 1999-2000

12 Review12 The political scene20 Economic policy and the economy24 Oil and gas27 Telecommunications28 Foreign trade and payments

30 Quarterly indicators and trade data

List of tables

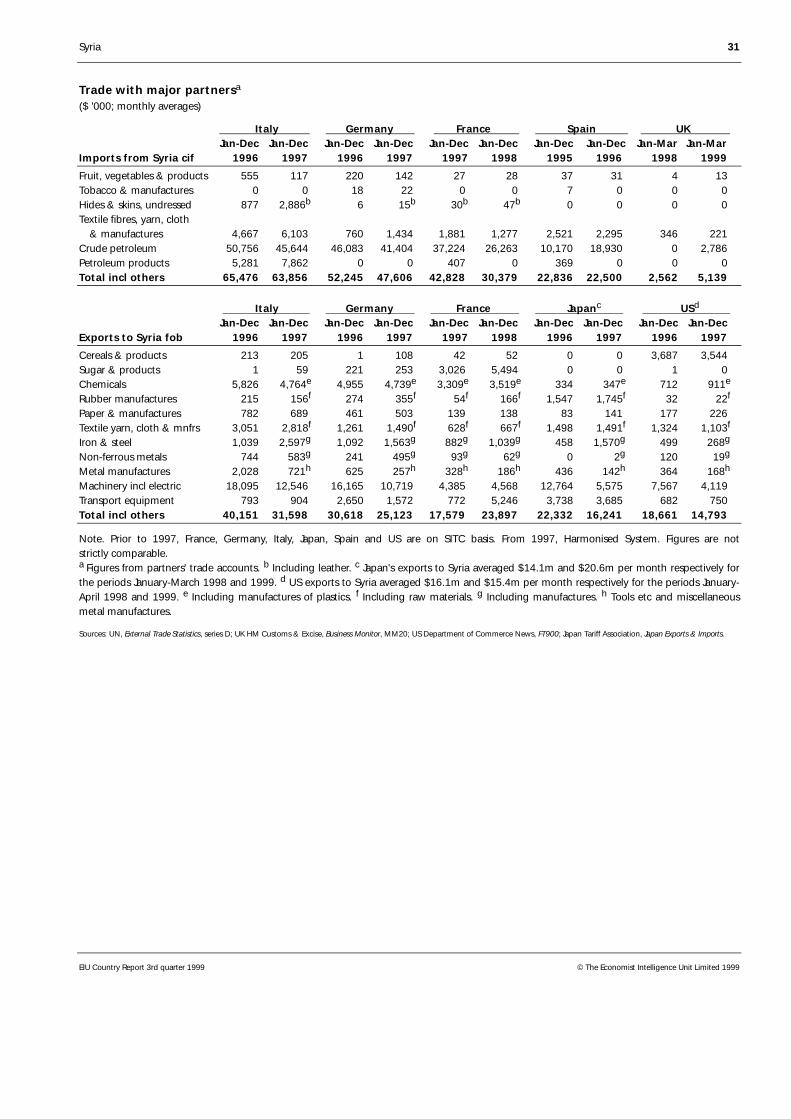

11 Forecast summary21 Cotton production24 Government finances25 Crude oil production28 Merchandise trade30 Quarterly indicators of economic activity31 Trade with major partners

List of figures

11 Gross domestic product11 Current-account balance21 Cotton prices25 Spot oil prices

.

Syria 3

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Summary

3rd quarter 1999

Outlook for 1999-2000: Syria will soon embark on peace talks with Israel,though negotiations will be slow and complex, and the timing of an eventualsettlement is impossible to predict. The delicate process of domestic politicalrealignment, aimed at boosting the position of the president’s son, Bashar al-Assad, will continue, though the success of this effort is largely dependent on thehealth of the president. All this will leave little time for major economic policyinitiatives, though a severe drought has prompted remedial measures. Syria willremain mired in recession this year, reflecting weak consumer confidence anddeclining oil output, though a return to growth is expected in 2000. The current-account deficit will continue to narrow, reaching 0.4% of GDP in 2000.

The political scene: The easing out of the political old guard has continuedwith the retirement or imprisonment of several senior regime figures, notablythe commander of the air force, Mohammed Kholi. Bashar al-Assad has been atthe forefront of an anti-corruption campaign. A new cabinet has still to benamed, though the current foreign minister, Farouq al-Shara, appears likely toreplace Mahmoud al-Zubi as prime minister. The president has exchangedpleasantries with the new Israeli prime minister, Ehud Barak, and the stageseems set for the start of peace talks. In a bid to strengthen his negotiatinghand, Mr Assad has visited Russia for talks on a possible arms purchase.

Economic policy and the economy: A rebound in oil prices has easedpressure for radical economic reform, though Syria’s worst drought for decadeshas necessitated some government help for the agricultural sector. Productionof cotton, wheat and barley have all suffered, and the government has beenforced to import barley for the first time in about a decade. The cabinet isreportedly discussing amendments to Law No. 10, though these are likely to beminimal, and an early unification of exchange rates now seems unlikely.

Oil and gas: Oil production has so far held steady at 540,000 barrels/day in1999, despite fears of continued decline. The government has opened uppreviously state-run fields to foreign participation. The Conoco/Elf gas deal hasbeen ratified with completion scheduled for mid-2001. New gas discoverieshave been made and plans to expand the pipe network are under way.

Telecommunications: A mobile telephone pilot scheme has been intro-duced, possibly as a prelude to a national network. Siemens of Germany haswon a contract to install 750,000 new telephone land lines in the final phaseof a nationwide expansion programme.

Foreign trade and payments: Syria has agreed to start repaying its $502mdebt to Iran, though details of the terms have not been revealed. A Germandelegation has failed to reach agreement on $909m in Syrian debt.

Editor: James ReeveAll queries: Tel: (44.20) 7830 1007 Fax: (44.20) 7830 1023

Next report: Our next Country Report will be published in November

July 23rd 1999

4 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

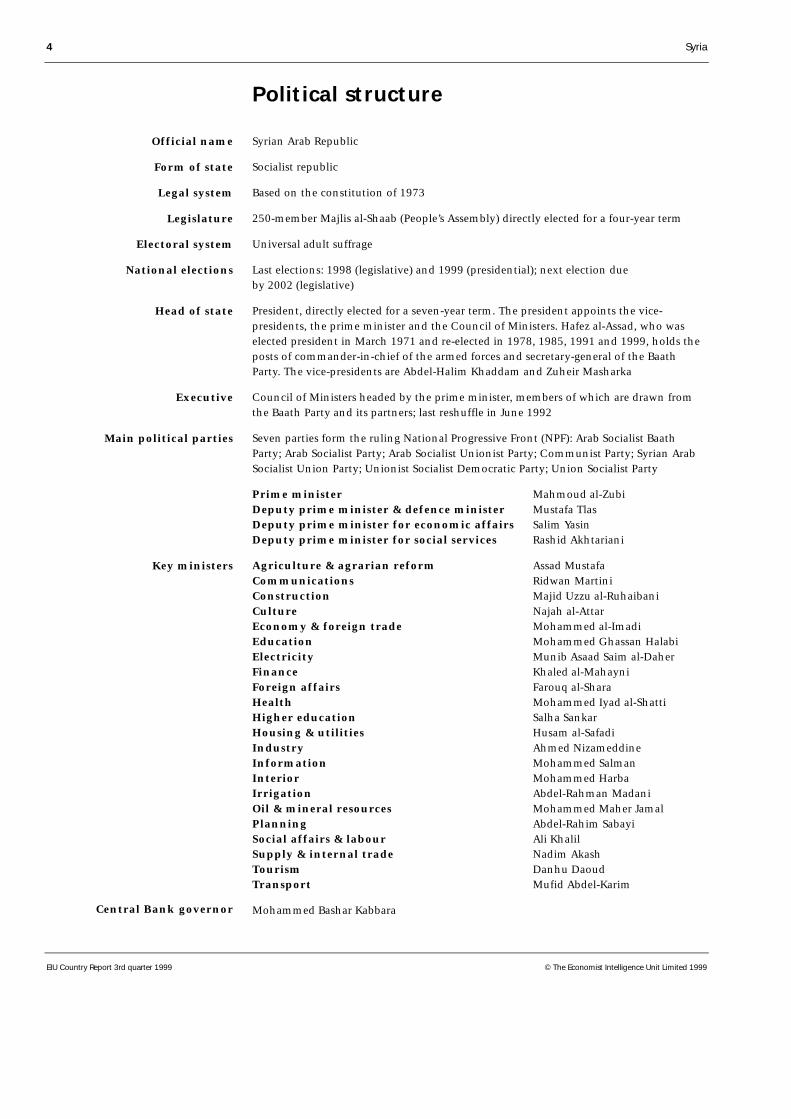

Political structure

Syrian Arab Republic

Socialist republic

Based on the constitution of 1973

250-member Majlis al-Shaab (People’s Assembly) directly elected for a four-year term

Universal adult suffrage

Last elections: 1998 (legislative) and 1999 (presidential); next election dueby 2002 (legislative)

President, directly elected for a seven-year term. The president appoints the vice-presidents, the prime minister and the Council of Ministers. Hafez al-Assad, who waselected president in March 1971 and re-elected in 1978, 1985, 1991 and 1999, holds theposts of commander-in-chief of the armed forces and secretary-general of the BaathParty. The vice-presidents are Abdel-Halim Khaddam and Zuheir Masharka

Council of Ministers headed by the prime minister, members of which are drawn fromthe Baath Party and its partners; last reshuffle in June 1992

Seven parties form the ruling National Progressive Front (NPF): Arab Socialist BaathParty; Arab Socialist Party; Arab Socialist Unionist Party; Communist Party; Syrian ArabSocialist Union Party; Unionist Socialist Democratic Party; Union Socialist Party

Prime minister Mahmoud al-ZubiDeputy prime minister & defence minister Mustafa TlasDeputy prime minister for economic affairs Salim YasinDeputy prime minister for social services Rashid Akhtariani

Agriculture & agrarian reform Assad MustafaCommunications Ridwan MartiniConstruction Majid Uzzu al-RuhaibaniCulture Najah al-AttarEconomy & foreign trade Mohammed al-ImadiEducation Mohammed Ghassan HalabiElectricity Munib Asaad Saim al-DaherFinance Khaled al-MahayniForeign affairs Farouq al-SharaHealth Mohammed Iyad al-ShattiHigher education Salha SankarHousing & utilities Husam al-SafadiIndustry Ahmed NizameddineInformation Mohammed SalmanInterior Mohammed HarbaIrrigation Abdel-Rahman MadaniOil & mineral resources Mohammed Maher JamalPlanning Abdel-Rahim SabayiSocial affairs & labour Ali KhalilSupply & internal trade Nadim AkashTourism Danhu DaoudTransport Mufid Abdel-Karim

Mohammed Bashar Kabbara

Official name

Form of state

Legal system

Legislature

Electoral system

National elections

Head of state

Executive

Main political parties

Key ministers

Central Bank governor

Syria 5

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

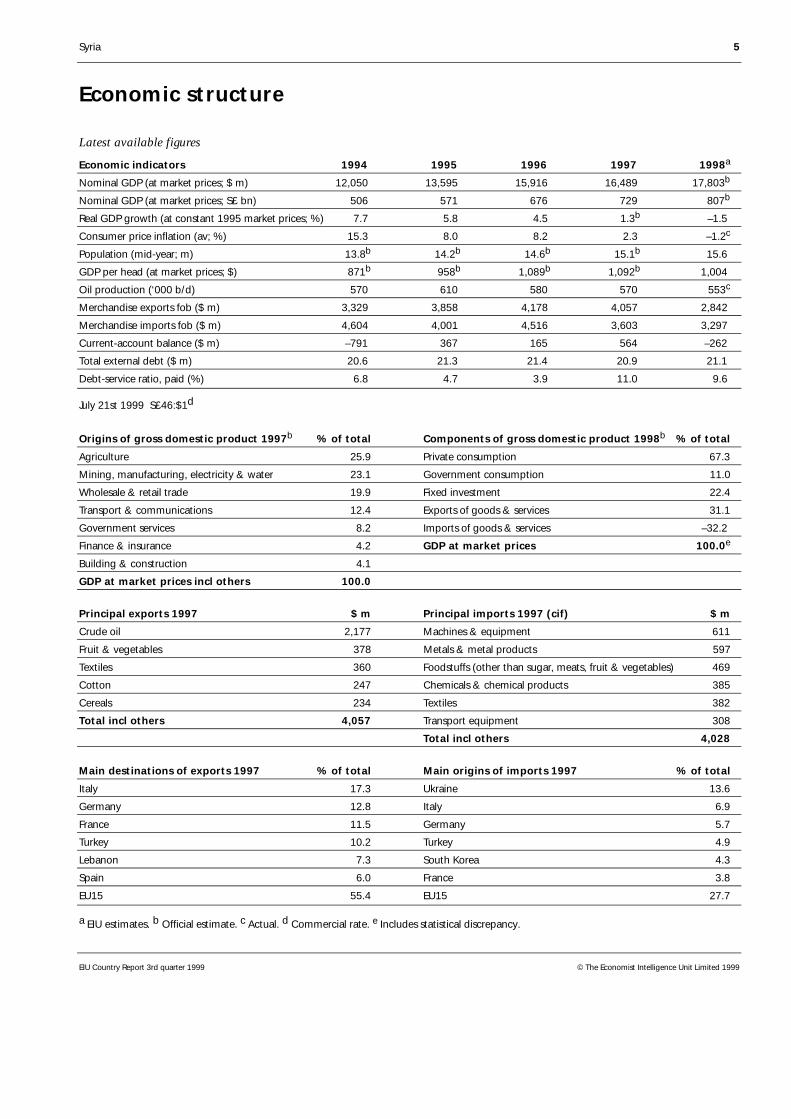

Economic structure

Latest available figures

Economic indicators 1994 1995 1996 1997 1998a

Nominal GDP (at market prices; $ m) 12,050 13,595 15,916 16,489 17,803b

Nominal GDP (at market prices; S£ bn) 506 571 676 729 807b

Real GDP growth (at constant 1995 market prices; %) 7.7 5.8 4.5 1.3b –1.5

Consumer price inflation (av; %) 15.3 8.0 8.2 2.3 –1.2c

Population (mid-year; m) 13.8b 14.2b 14.6b 15.1b 15.6

GDP per head (at market prices; $) 871b 958b 1,089b 1,092b 1,004

Oil production (‘000 b/d) 570 610 580 570 553c

Merchandise exports fob ($ m) 3,329 3,858 4,178 4,057 2,842

Merchandise imports fob ($ m) 4,604 4,001 4,516 3,603 3,297

Current-account balance ($ m) –791 367 165 564 –262

Total external debt ($ m) 20.6 21.3 21.4 20.9 21.1

Debt-service ratio, paid (%) 6.8 4.7 3.9 11.0 9.6

July 21st 1999 S£46:$1d

Origins of gross domestic product 1997b % of total Components of gross domestic product 1998b % of total

Agriculture 25.9 Private consumption 67.3

Mining, manufacturing, electricity & water 23.1 Government consumption 11.0

Wholesale & retail trade 19.9 Fixed investment 22.4

Transport & communications 12.4 Exports of goods & services 31.1

Government services 8.2 Imports of goods & services –32.2

Finance & insurance 4.2 GDP at market prices 100.0e

Building & construction 4.1

GDP at market prices incl others 100.0

Principal exports 1997 $ m Principal imports 1997 (cif) $ m

Crude oil 2,177 Machines & equipment 611

Fruit & vegetables 378 Metals & metal products 597

Textiles 360 Foodstuffs (other than sugar, meats, fruit & vegetables) 469

Cotton 247 Chemicals & chemical products 385

Cereals 234 Textiles 382

Total incl others 4,057 Transport equipment 308

Total incl others 4,028

Main destinations of exports 1997 % of total Main origins of imports 1997 % of total

Italy 17.3 Ukraine 13.6

Germany 12.8 Italy 6.9

France 11.5 Germany 5.7

Turkey 10.2 Turkey 4.9

Lebanon 7.3 South Korea 4.3

Spain 6.0 France 3.8

EU15 55.4 EU15 27.7

a EIU estimates. b Official estimate. c Actual. d Commercial rate. e Includes statistical discrepancy.

6 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Outlook for 1999-2000

Syria is entering an interesting, if unsettling, period both at home and abroad.Following the election of the relatively moderate Ehud Barak as Israel’s primeminister in May, Syria has a good chance of reclaiming the Golan Heights, lostto Israel during the 1967 war. However, this will involve compromise andchange, most notably in southern Lebanon, but also in how Syria defines itselfas a nation. At home, the ageing president, Hafez al-Assad, will continue thedelicate process of political realignment, in an attempt to secure the future ofhis family and clan. All this will require a firm but sensitive political touch, andtime, which his fragile health may yet deny him.

Mr Barak’s convincing election victory has revived talk of regional peace andterritorial compromise following four frustrating years of broken promisesand growing mutual suspicion between Israel and its Arab neighbours. For the69-year-old Mr Assad, the advent of Mr Barak appears to represent a finalchance to restore the Golan Heights to Syrian sovereignty. Regaining thissmall, but strategically important and agriculturally fertile strip of land is not,and never has been, Mr Assad’s political priority. He is more concerned withstaying in power and maintaining Syrian hegemony in neighbouring Lebanon.However, the Golan has a symbolic resonance for many Syrians which cannotbe ignored. As his country’s defence minister during the disastrous 1967 war,Mr Assad may also feel some personal responsibility for its loss.

Mr Assad is therefore willing to engage with Mr Barak as soon as possible. Therehave been unprecedented exchanges of compliments between the two men,and Syria has reportedly told “rejectionist” Palestinian groups based in theSyrian capital, Damascus, in no uncertain terms that they will not be allowed tojeopardise the putative negotiations. Mr Assad also recognises that these talkswill require more substantive compromises from Syria. Most importantly, it willeventually have to commit to reining in the Shia guerrilla group, Hizbullah,which has been engaged in a successful war of attrition against Israeli troopsoperating in southern Lebanon. Israel wants to withdraw these troops (itsmilitary losses are politically unsustainable), but will do so only with adequatesecurity guarantees from Syria. Damascus will therefore have to ensure thatHizbullah is disarmed—a messy business which Syria might leave to Lebanesetroops. Either way, Syria will be the ultimate guarantor of peace along theLebanese-Israeli border.

Syria will also have to change its political language. For as long as Mr Assad hasbeen in office, Syria has used Israel’s existence to define itself diplomatically. Asa self-styled “frontline state”, involved in sporadic military skirmishes withIsrael, Syria won popular respect and financial support from the Arab world.Domestically, too, Israel’s existence was useful, enabling Mr Assad’s politicalopponents to be labelled as “Zionist agents”, and despatched without trial.Peace with Israel will therefore involve a period of uneasy adjustment, andsome rhetorical habits will be difficult to drop completely. Syria’s militarypresence in Lebanon will also become more difficult to justify, although theEIU expects Syrian troops to be maintained there.

Syria enters a period ofchange—

—involving peace talkswith Israel—

Syria 7

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

In return for such sacrifices, Syria will demand the return of the Golan in itsentirety, based on the 1948 ceasefire line. It may agree to pull its troops furtherback towards Damascus, and will probably accept the involvement of aninternational peacekeeping force, but Israeli listening posts or early warningstations on the Golan are unlikely to be tolerated. Nor, probably, will anyIsraeli settler farmers, although how many of them will want to stay under aSyrian flag is not clear.

It is also unclear to which of the “tracks”—Palestinian or Syrian—Mr Barak willdevote most of his time and effort to solving. The pressure from Egypt andJordan is likely to be towards the former; however, Mr Barak’s militarybackground may incline him towards the Syrian/southern Lebanon track,which probably appears as a comparatively straightforward strategic problem.Given also his public commitment to have Israeli forces out of Lebanon byJune 2000, the Syrian option will become increasingly attractive. It is futile topredict when full peace between Israel and Syria will be achieved, butnegotiations should begin in earnest by September this year.

Mr Assad may also believe that securing peace with Israel will help toconsolidate the domestic position of his 34-year-old son, Bashar. Anything thatinvolves change is probably to Bashar’s advantage: peace with the “Zionistenemy” would leave the Baathist old guard, with its language of “resistance”and “steadfastness”, looking old-fashioned and inflexible. However, thepresident will not rely solely on a change of rhetoric. More practical measureswill include the forced retirement and, if necessary, the imprisonment, of thosemen who might one day decide to challenge Bashar’s meteoric rise.

This process will involve a degree of subtlety: if the interference in theestablished order is too heavy-handed, resentment towards Bashar may bestored up for later. In addition, the president himself is a member of the “oldguard” and he has an often overlooked sense of loyalty to his old Baathist andmilitary cadres. Similarly, and somewhat ironically, the president is keen to usethe Baath Party to legitimise his son’s political elevation. Consequently, aconference of the Baath Party’s Regional Command will be convened, probablyin September, to anoint Bashar as one of its members. Constitutionally, onlymembers of the Regional Command can become a vice-president or presidentof the republic; it is a sign of the balance that needs to be struck that thepresident feels obliged to “play by the rules” in this way.

A new cabinet will probably be appointed in the wake of this conference.Syrian ministers are generously referred to as “technocrats”, a reflection of theirrelative political impotence rather than their qualifications. As such, none ofthem will have a major bearing on policy. However, it will still help Bashar if,as some expect, the current foreign minister, Farouq al-Shara, is elevated toprime minister. Mr al-Shara is considered a Bashar loyalist, with far fewer ties tothe Baathist establishment than the incumbent, Mahmoud al-Zubi.

Given this delicate process of domestic and regional political realignment, it isprobably too much to expect any major economic policy initiatives. The delayin appointing a new cabinet has only depressed business confidence further,

—and delicate domesticrealignment

Major economic policychanges are unlikely—

8 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

though a new prime minister, whoever he may be, will be unable to initiatesubstantive economic restructuring without the president’s approval. Basharand his associates recognise the need for a degree of economic liberalisation,and they may be allowed freedom to tinker with some aspects of theeconomy—the banking sector, for example—but the complex and opaquepatronage networks that have sustained the old guard and their partners inprivate business will be left largely intact, at least for the time being.

Consequently, the economy is likely to remain structurally rigid for the rest ofthe forecast period. For those businessmen without adequate politicalconnections, controls will remain in place on how much they can import, atwhat price and on what they can do with their export earnings. In a starkillustration of the type of statism that is still to be overcome, the economyminister, Mohammed al-Imadi, recently told a meeting of businessmen inDamascus that exchange-rate unification is “out of the question” as long asprivate businesses continue to import more than they export. He also rejectedtheir complaints that private-sector exporters have to hand over 25% of theirforeign-currency earnings.

Nor is it certain that peace with Israel, when it comes, will give a boost toeconomic liberalisation. Israel is certainly keen to include free trade in thedefinition of “normalisation”. However, while some of the more dynamicSyrian businessmen are keen to exploit the opportunities that peace mightbring, the majority remain suspicious. Protection from Israeli “economicimperialism” may even provide an excuse for the imposition of more rigidtrade controls.

That said, the ailing economy will require immediate remedial measures. Themost pressing problem is a drought, the worst in 25 years and, in some parts ofthe country, such as Daraa in the south, the most severe in 50 years (seeEconomic policy and the economy). Given that agriculture accounts for thelargest single share of GDP, and is the single greatest employer of labour, thedrought will have a pronounced impact on domestic demand this year at least(see below). The pain will also be felt in the external balances, since agriculturalexports, particularly cotton, wheat and livestock, are important foreign-exchange earners. With this in mind, the government has moved with atypicalspeed to help the beleaguered sector, for example by lifting all taxes on cottonand cotton-related products, and by selling fodder to livestock farmers atsubsidised prices.

Some of the pressure for serious economic reform has been lifted by the recentupturn in oil prices. Despite uncertain medium-term production prospects (seebelow), this sector still contributes some 50% of government revenue. Ourforecast for average International Energy Agency (IEA) crude prices has notchanged: we continue to expect an average IEA import price of $14/barrel thisyear, rising to $15.50/b in 2000. However, recent data showing an unexpect-edly strong commitment by OPEC member states to their new productionquotas have given a sharp boost to prices in the past few weeks, and all thepotential for our annual price assumption is on the upside.

—with stifling controls inplace on many private-

sector activities

An oil price rebound willallow an increase in

government spending—

Syria 9

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

This should enable the government to increase spending towards the end ofthe year. Most of this will be directed towards energy-related constructionwork, and increasingly towards the gas sector, as the government seeks toconvert its oil-thirsty power stations to gas feedstock in order to free up moreprecious oil for exports. For example, construction work on a $430m gasprocessing plant, involving Conoco of the US and France’s Elf Aquitaine, is setto begin soon. However, the oil sector itself will continue its gentle decline.Construction work aimed at streamlining and rationalising oil output willcontinue, and there should be a small boost to production next year, but majorfinds now seem a thing of the past.

Current spending will remain relatively high, but only through politicalnecessity, as the government attempts to find jobs for the estimated 50,000young Syrians who enter the employment market each year. With a populationgrowth rate of 3.3%, the government will struggle to find jobs for all, and theunemployment rate, independently estimated at some 15%, is likely to grow.The private sector is in no position to help: business confidence remainsextremely fragile and investment decisions are likely to be postponed until thepolitical map is more clearly defined. Drought will depress agricultural incomeseven further, increasing the level of migration from rural areas and puttinggreater strain on creaking urban infrastructure. Overall, therefore, we expectthe upturn in oil revenue to be offset by agricultural contraction, and we haveleft our real growth forecast for this year unchanged at –1.5%.

The performance of the economy will be better in 2000, though hardlydynamic. Another increase in global oil prices, combined with a marginal risein Syrian crude output, will boost export revenue, and will be augmented by anincrease in transfers from Gulf states, as they too begin to emerge fromrecession. There should also be an increase in remittances from Lebanon,particularly if peace is achieved between Syria and Israel. Lebanon, with itslaisser-faire economic management, is expected to attract an increase in foreigninvestment flows, from which the large number of Syrians employed in itsconstruction sector should benefit. Therefore, and on the assumption thatthere is no further drought, the increase in government and private-sectorspending should be just enough to drag the Syrian economy back into positivegrowth, although the overall rate will remain low.

Under these circumstances, inflation is expected to remain low in 1999 and2000. IMF data show that consumer prices in 1998 fell by an average 1.3%,confirming a trend begun in 1997, when real interest rates moved from beingnegative to positive—one reason why private-sector savings have increasedover the past 18 months or so. Ordinarily, recession this year would point tocontinued deflation; however, the drought is almost certain to put pressure onprices. The government’s complex system of subsidisation will minimise theimpact on consumer prices of food shortages, but it will, in effect, have to printmoney to achieve this, which is likely to have inflationary consequences.Imported inflation should remain subdued this year at least, with the globalprices of non-oil commodities expected to decline quite sharply. Nevertheless,and largely because of the drought, we expect the overall rate of inflation to

—but business confidence islikely to remain weak—

—and economic growthwill be minimal

Food shortages may havesome inflationary pressure

10 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

increase to 1.5% this year, unchanged from our previous forecast. A slightincrease to about 1.8% is expected next year, in line with a rise in global non-oil commodity prices and the more general recovery in economic activity. Afurther devaluation of the Syrian pound’s neighbouring countries’ rate, fromthe current S£46:$1 towards the free-market rate of about S£50:$1, would haveincreased imported inflationary pressures, but this seems less likely to happennow, given Mr Imadi’s criticism of the private sector (see above). We still expectthe process of exchange-rate unification to continue, but this is likely to bedragged out beyond the forecast period.

Mr Imadi’s concerns appear to be predicated on a deteriorating externalposition, though he is likely to have exaggerated this for political reasons.Despite the dip in crude production, oil export revenue should increase slightlythis year in line with improving prices. However, overall exports will declineslightly, as the slight gain in the oil sector is offset by the decline in agriculturalproduction. The severity of the drought appears greater than we assumedpreviously, and we have nudged upwards our projection of imports for thisyear to reflect higher levels of imported staples. Consequently, we now expectthe trade deficit to be somewhat wider than assumed previously, at justover $400m.

The value of exports should increase in 2000 to about $3.2bn, reflectingprincipally the increase in oil output and prices, but also a pick-up in agri-cultural production. Imports should also register a small gain as private-sectorconfidence recovers and government spending accelerates in line with higheroil export earnings. We have decided not to include Russian arms purchases innext year’s import projection (see The political scene)—nothing has beensigned yet, and there are a number of political and financial hurdles to beovercome before this happens. In any case, deals of this kind are oftenexpressed as services debits. The trade deficit is therefore expected to narrow toabout $169m in 2000.

Performance in other parts of the current account is likely to be mixed. Servicescredits, which are composed primarily of tourist receipts, are likely to continueto decline this year, mainly because of recession in neighbouring Lebanon, fromwhere the largest single group of tourists hails. There may be more visitors fromthe Gulf this year since Syria is seen as a cheaper holiday option, though they arelikely to spend less. This situation should improve in 2000 as Lebanon emergesfrom recession and, if a peace treaty is signed with Israel, as European visitornumbers pick up. Services debits are also likely to increase again, particularly in2000, in line with infrastructural development in the oil and gas sectors.

Income credits are likely to remain relatively minor and decline at a shallowrate in line with the downward movement in international interest rates.Income debits, which should, in theory, reflect mainly movements in oil prices(as foreign oil companies constitute the main source of repatriated profits), arelikely to show some relatively marked increases in 1999 and 2000 because ofthe government’s recent decision to meet interest payment arrears on some ofits external debt (see Foreign trade and payments). Current transfers credits are

There will be little growthin export values—

—although the current-account deficit willcontinue to narrow

Syria 11

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

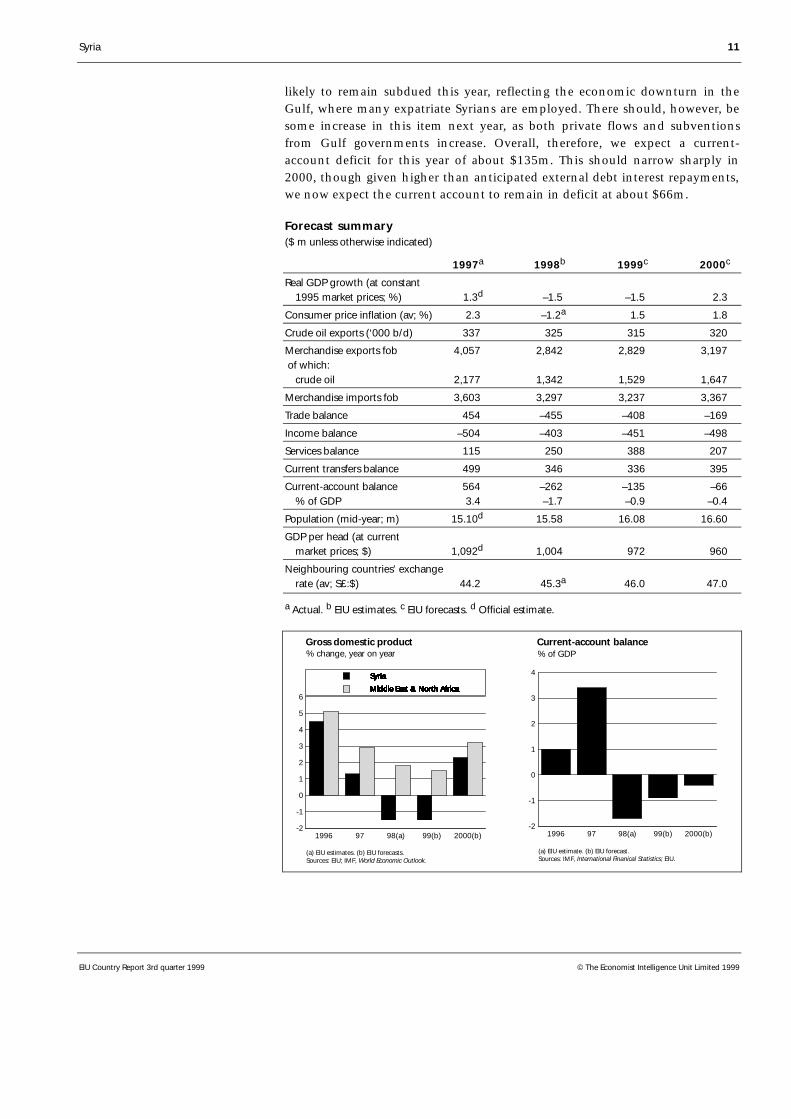

likely to remain subdued this year, reflecting the economic downturn in theGulf, where many expatriate Syrians are employed. There should, however, besome increase in this item next year, as both private flows and subventionsfrom Gulf governments increase. Overall, therefore, we expect a current-account deficit for this year of about $135m. This should narrow sharply in2000, though given higher than anticipated external debt interest repayments,we now expect the current account to remain in deficit at about $66m.

Forecast summary($ m unless otherwise indicated)

1997a 1998b 1999c 2000c

Real GDP growth (at constant 1995 market prices; %) 1.3d –1.5 –1.5 2.3

Consumer price inflation (av; %) 2.3 –1.2a 1.5 1.8

Crude oil exports (‘000 b/d) 337 325 315 320

Merchandise exports fob 4,057 2,842 2,829 3,197 of which: crude oil 2,177 1,342 1,529 1,647

Merchandise imports fob 3,603 3,297 3,237 3,367

Trade balance 454 –455 –408 –169

Income balance –504 –403 –451 –498

Services balance 115 250 388 207

Current transfers balance 499 346 336 395

Current-account balance 564 –262 –135 –66 % of GDP 3.4 –1.7 –0.9 –0.4

Population (mid-year; m) 15.10d 15.58 16.08 16.60

GDP per head (at current market prices; $) 1,092d 1,004 972 960

Neighbouring countries’ exchange rate (av; S£:$) 44.2 45.3a 46.0 47.0

a Actual. b EIU estimates. c EIU forecasts. d Official estimate.

-2

-1

0

1

2

3

4

5

6

1996 97 98(a) 99(b) 2000(b)

Gross domestic product% change, year on year

(a) EIU estimates. (b) EIU forecasts.Sources: EIU; IMF, World Economic Outlook.

Middle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North Africa

Syria

Middle East & North Africa

SyriaSyria

Middle East & North Africa

Syria

Middle East & North Africa

SyriaSyria

Middle East & North Africa

Syria

Middle East & North Africa

Syria

Middle East & North Africa

Syria

Middle East & North Africa

Syria

Middle East & North Africa

Syria

Middle East & North Africa

Syria

Middle East & North Africa

Syria

Middle East & North Africa

Syria

Middle East & North Africa

Syria

Middle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North AfricaMiddle East & North Africa

Syria

-2

-1

0

1

2

3

4

1996 97 98(a) 99(b) 2000(b)

Current-account balance% of GDP

(a) EIU estimate. (b) EIU forecast. Sources: IMF, International Finanical Statistics; EIU.

12 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

The overall financing requirements will probably be met by a combination ofconcessional loans from Japanese and Gulf institutions and, if necessary, bydrawing on Syrian commercial banks’ sizeable foreign assets. These reached$22.3bn in September 1998, according to the IMF. Data on foreign-exchangereserves are not published.

Review

The political scene

Syria has not escaped the political lethargy that traditionally accompanies theonset of summer in most Arab states. Accordingly, efforts by the president,Hafez al-Assad, to pave the way for his 34-year-old son, Bashar, for high officehave slowed following a burst of activity in the first few months of the year(2nd quarter 1999, pages 12-13). Nevertheless, there have been some changes tothe old guard, with the “retirement” of a number of senior cadres—mostnotably, the commander of the air force, General Mohammed Kholi. GeneralKholi has himself, on occasion, been viewed as a possible successor to the pres-ident. Others who are said to have been replaced include General Ibrahim Huja,a leading figure in air force intelligence, and Riyadh Shalish, who played animportant role in presidential security. Simultaneously, a number of previouslysenior regime figures are understood to have been imprisoned. General Bashiral-Najjar, who was replaced last year as head of civilian intelligence byMahmoud al-Saqqa, is said to have received a 25-year prison sentence, thoughthe charges have not been made public. Colonel Aziz Abbas, who was directorof Bashar al-Assad’s office at the presidential palace, has been jailed for sevenyears, according to reports, though again it is not clear on what grounds.

The issue of succession now appears to have become Mr Assad’s overridingdomestic concern, or as one Damascus-based diplomat puts it, “the prismthrough which everything is filtered”. Reports of the president’s state of healthare contradictory. If, as has been suggested, he is suffering from coronary andcarotid artery disease, chronic lymphocytic leukaemia and diabetes, then hisdays would appear to be numbered. However, following an interview withMr Assad in June, the veteran Syria-watcher Patrick Seale described him asbeing in good health. The impression of an active president has been reinforcedby his two-day visit to Russia in early July (see below) and his numerousappearances on the tarmac of Damascus airport to meet visiting dignitaries.

Despite this, many observers say that for a man who is, officially at least, notyet 70, Mr Assad appears older and frailer than he should. In recent meetingshe has seemed vague and absent-minded. Moreover, these meetings arebecoming rare events. Since December he has twice cancelled importantspeeches to parliament—the second in February, shortly after he was re-electedpresident for a fifth seven-year term.

The president hascontinued to make key

personnel changes—

—as he prepares the groundfor succession

Syria 13

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

The president’s son, by contrast, has continued to seek the limelight, mostnotably with an anti-corruption drive. Under Bashar’s direction, the usuallysupine Syrian media have set to work with great vigour to uncover corruptionand mismanagement within the public services. This would have left most ofthe civil service as potential targets, although, so far at least, most of thevictims appear to have been confined to the Syrian Telecommunications andPostal Corporation. A total of 25 senior executives from this organisation havebeen brought in front of the Economic Security Court on various charges.

This sort of campaign is typical of many autocracies. Designed to curb theworst excesses of the regime, while giving the public some sense ofinvolvement in government, they also help to boost the popular standing oftheir instigator. Previous campaigns in Syria were headed by Bashar’s popularbrother, Bassel al-Assad, before his untimely death in a car crash in 1994. In theabsence of an independent judiciary, however, the Syrian system is likely toremain endemically corrupt. This situation, which leaves the president as theultimate source of authority and largesse, is encouraged by Mr Assad.

Bashar’s anti-corruption campaign should make it easier for Mr Assad to confera more substantial political title on his son. (The only official position that hecurrently holds is that of colonel in the elite Presidential Guard.) This willprobably involve a “popular campaign”, orchestrated by the regime, possiblyinvolving some form of referendum, which will “demand” that Bashar beappointed to a senior position in the regime. This could then allow Mr Assad toput in place the legal structure to have Bashar appointed to one of the threevice-presidencies, for example. One of these remains vacant following thedismissal last year of Mr Assad’s younger brother, Rifaat. To do this, Mr Assadwould need the approval of the Baath Party Regional Command, the party’shighest decision-making body. This body has not convened since 1985, butBashar would probably have to be appointed to it before he could assumeeither the post of vice-president or, indeed, president.

These institutional changes will not, in themselves, guarantee Bashar’s eventualacceptance as president. Simultaneous changes in the power structure,involving the promotion of a younger generation of politicians and militaryofficers, will be more important to Bashar’s chances of retaining the presidencyfor any length of time after his father’s death (see Outlook for 1999-2000).

Meanwhile, there is still no sign of a new cabinet. Most observers expected amajor reshuffle, the country’s first for seven years, to be announced shortlyafter the presidential election in February. Mr Assad may have decided to delayhis decision until after the anti-corruption drive has run its course and theBaath Party’s Regional Command has been convened.

Whatever the reason for the delay, the reshuffle is still expected to go ahead,with the most significant change involving the replacement of the primeminister, Mahmoud al-Zubi. The likely successor is still a matter of debate.Some expect Ahmed Qabalan, the secretary of the Damascus Rural Area branchof the Baath Party, to be appointed; however, a more plausible candidateappears to be the current foreign minister, Farouq al-Shara, a supporter of

Bashar al-Assad heads ahigh-profile anti-

corruption campaign—

—which may help preparethe ground for political

office

A new cabinet is stillawaited—

—though there is a strongcandidate for prime

minister

14 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Bashar. If that were the case, the current Syrian ambassador to Washington,Walid al-Mu’allim, would probably fill the vacant post of foreign minister.Whoever becomes prime minister, the overall direction of government policywill continue to be driven from Mr Assad’s office. The sense of continuity willbe reinforced by the retention of several long-serving ministers close toMr Assad. Along with Mr al-Shara, these are likely to include the defenceminister, Mustafa Tlas, and the minister of information, Mohammed Salman.

Despite these domestic uncertainties, it is clear that Syria enjoys probably thebest chance yet of making peace with its long-standing enemy, Israel. Theoverwhelming victory of Ehud Barak, the Labour leader, in Israel’s presidentialelection in May, has provided fresh impetus to a peace process that hadbecome virtually moribund under his predecessor, Binyamin Netanyahu. Aspart of his election campaign, Mr Barak pledged to remove Israeli troops fromthe country’s self-styled “security zone” in southern Lebanon within a year.Given the control that Syria has over Lebanese affairs, and in particular itsinfluence over the Shia Muslim guerrilla group, Hizbullah—the prime reasonfor Israel’s presence in southern Lebanon—it is clear that Mr Barak is preparedto make concessions on the Golan Heights, which Israel captured from Syriaduring the 1967 war. Mr Barak has implied as much, emphasising that Israelismust be prepared to make “painful compromises” in order to effect the pull-out of troops from southern Lebanon.

The strategic imperative has been enhanced by an unprecedented exchange ofcompliments between Mr Barak and Mr Assad. In an interview with the Britishjournalist Patrick Seale in Tel Aviv, Mr Barak said that he considered Mr Assad’slegacy to be “a strong, independent, self-confident Syria”, which was “veryimportant” to the stability of the Middle East. In turn, Mr Assad described theIsraeli leader to Mr Seale as a “strong and honest man” who, it was clear, waskeen to reach a peace agreement with Syria. As the Israeli chief of staff,Mr Barak was intimately involved in negotiations between the two sides in themid-1990s. Although both sides have different interpretations of what wasachieved then, it is clear that a provisional agreement on the return of most ofthe Golan Heights to Syrian sovereignty was close. Unfortunately, negotiationswere suspended following the accession to power of Mr Netanyahu in 1996(although Mr Netanyahu claims that unofficial talks carried on, sporadically,for a number of years).

Meanwhile, external support for a Syrian-Israeli peace deal appears strong. TheUS president, Bill Clinton, who, behind the scenes, backed Mr Barak’s election,is keen to secure at least one peace agreement between Israel and eitherSyria/Lebanon, or the Palestinians, before he leaves office in early 2001. As aresult, senior US government members and former officials, including theformer secretary of state James Baker, and Edward Djerejian, a former USambassador to Damascus, have recently paid visits to Syria. The US secretary ofstate, Madeleine Albright, is also likely to visit Syria in August. The EuropeanUnion, represented by the Spanish prime minister, José María Aznar, and asenior French foreign ministry official, have also been to the Syrian capital.

The ground is laid forpeace talks with Israel—

Syria 15

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

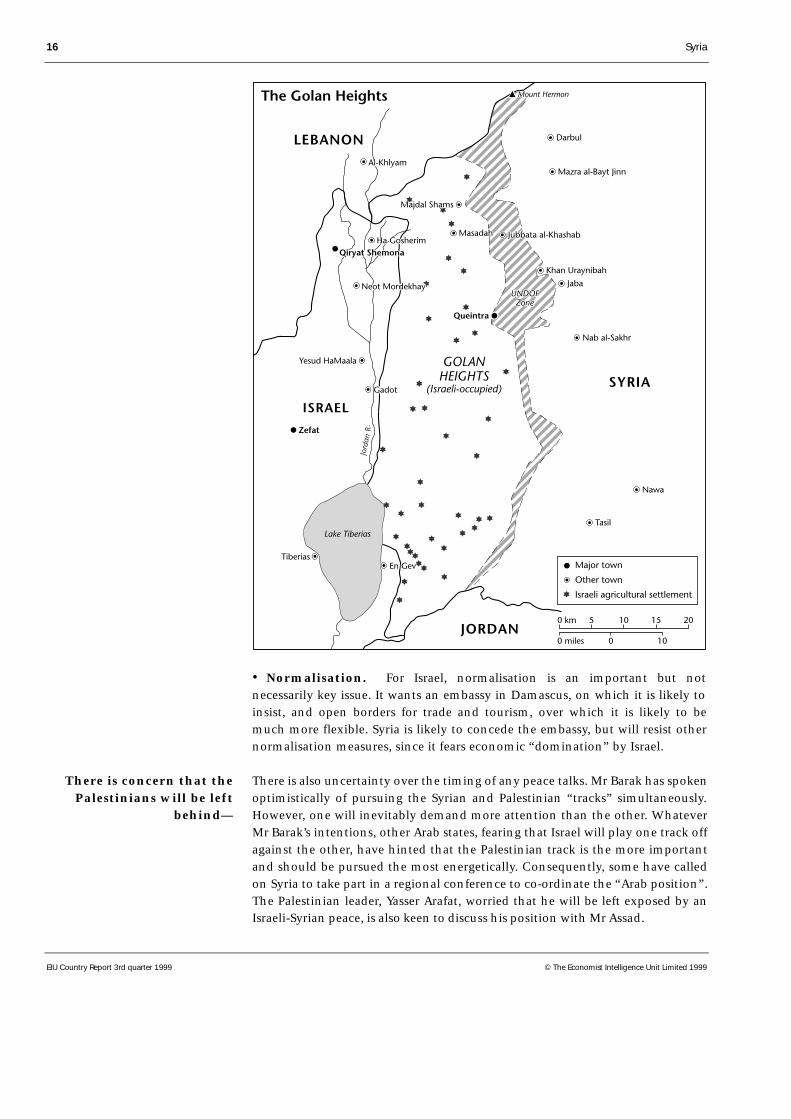

Despite this encouragement, negotiations promise to be long and complex.The major points of contention are as follows.

• Border deployment. Israel’s major concern will focus on securityarrangements for southern Lebanon, where Hizbullah has been engaged in aremarkably successful war of attrition against Israel and its surrogate SouthLebanon Army. To effect Hizbullah’s neutralisation, Syrian and/or regularLebanese troops will need to be deployed near the border with Israel. This isironic, given that Israel’s other principle concern will be to ensure that thereare as few Syrian troops as possible, if any, on the Golan Heights. Here Israelwill probably insist on a “mirrored” withdrawal, whereby Syrian and Israelitroops both pull back an equal distance from the new border. The vacuumwould then be filled by some form of international force. Israel will probablyinsist on US troops, since it has little faith in the UN, while Syria is likely topush for a French role. The timing of the withdrawal will also have to beagreed. In 1996 negotiations between the two sides are understood to havestalled on the insistence of the then Israeli leader, Yitzhak Rabin, that a limitedIsraeli withdrawal be followed by a lengthy period of normalisation to testSyria’s commitment to peace.

• Communications monitoring. Israel’s likely insistence on an advancedearly warning system in Syrian territory will be particularly contentious. Itcurrently operates a large and highly sophisticated electronic listening post ontop of Mount Hermon (Jebel el-Sheikh), which enables Israel to monitorcommunications within Damascus. Syria will probably insist that this isremoved under any peace deal.

• Arms reductions. Israel is keen to see a reduction in Syria’s armaments,specifically in its chemical weapons and ballistic missiles, but also in tank andaircraft levels. Syria will no doubt argue that, given Israel’s superior militarystrength and nuclear capability, it should be the one to disarm. In any case, theintrusive monitoring that would be required to confirm any reduction inmilitary capability is likely to be fiercely resisted by Israel. In addition, Syria’spolitical dynamics tend to work against disarmament and troop reduction. Themilitary and security services have long supported Mr Assad’s regime; reducingtheir resources will be difficult to undertake in a time of domestic politicalchange (see above).

• Border demarcation. The final border between the two countries is alsoopen to question. Syria insists on the ceasefire line that existed between 1948and June 6th 1967, while Israel is keen to revert to the 1948 border drawn upby the British during their mandatory hold on Palestine. The ceasefire linegives Syria three small pockets of additional territory (reflecting gains made inthe 1948 war), including access to the shores of the Sea of Galilee, somethingthat Israel will resist.

• Water. Access to Galilee is important for Syria since it opens up a source offresh water. Meanwhile, much of Israel’s northern water supply originates in theSyrian and Lebanese highlands, to which Israel will want continued indirectaccess. The water issue is now even more sensitive because of the severe droughtafflicting the region (see below, and Economic policy and the economy).

—which must overcome anumber of obstacles

16 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

• Normalisation. For Israel, normalisation is an important but notnecessarily key issue. It wants an embassy in Damascus, on which it is likely toinsist, and open borders for trade and tourism, over which it is likely to bemuch more flexible. Syria is likely to concede the embassy, but will resist othernormalisation measures, since it fears economic “domination” by Israel.

There is also uncertainty over the timing of any peace talks. Mr Barak has spokenoptimistically of pursuing the Syrian and Palestinian “tracks” simultaneously.However, one will inevitably demand more attention than the other. WhateverMr Barak’s intentions, other Arab states, fearing that Israel will play one track offagainst the other, have hinted that the Palestinian track is the more importantand should be pursued the most energetically. Consequently, some have calledon Syria to take part in a regional conference to co-ordinate the “Arab position”.The Palestinian leader, Yasser Arafat, worried that he will be left exposed by anIsraeli-Syrian peace, is also keen to discuss his position with Mr Assad.

There is concern that thePalestinians will be left

behind—

Syria 17

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Relations between Mr Assad and Mr Arafat have traditionally been poor. Syria,which, officially at least, has long been the main champion of the Palestiniancause, was deeply offended by Mr Arafat’s decision to break ranks and sign theOslo agreement with Israel in 1993. Egypt and Jordan have also signed separateagreements with Israel, and their insistence on a “unified” stance will ring alittle hollow in Damascus. Nevertheless, Mr Assad recognises the value in adegree of co-ordination, if only to put maximum pressure on Israel. In anapparent gesture of goodwill, in late July the Syrian vice-president, Abdel-Halim Khaddam, reportedly “asked” a number of radical Palestinian groupsbased in Damascus to drop the armed struggle against Israel. An official of oneof these groups (who are all opposed to the 1993 Oslo accords) told the newsagency Reuters that Mr Khaddam had been frank with them, explaining thatarmed attacks launched from Syria, or indeed Lebanon, were no longer viable.The reference to Lebanon generated a flurry of speculation that Syria hadintended the warning for Hizbullah as well. However, this seems unlikely, sincethe Shia guerrillas’ ability to inflict casualties on Israeli troops will be one ofSyria’s strongest cards in the forthcoming negotiations. A Hizbullah officialdismissed the idea as “talk which does not merit a response”.

Mr Khaddam’s visit to the Palestinian groups may have been well-intentioned,aimed at easing pressure on Mr Arafat and allowing him to forge some sense ofunity among the various Palestinian factions. However, the uncertainty thatthe request generated about Syria’s attitude towards Hizbullah’s activities willalso have helped Mr Khaddam personally. Any reference, no matter howoblique, to Lebanon will be an irritant to Bashar al-Assad, Mr Khaddam’s rival.For much of last year Bashar and Mr Khaddam were locked in a struggle forcontrol of Lebanon, a contest that Bashar eventually won. However,Mr Khaddam remains a contender to succeed Hafez al-Assad, and he mayregard the uncertainty generated by this episode as a small victory.

Syria’s hand in peace negotiations with Israel should also be strengthened byits vastly improved relations with Jordan. This follows the death earlier thisyear of King Hussein and the accession to the throne of his 37-year-old son,Abdullah. Mr Assad took the unexpected step of attending King Hussein’sfuneral in February, and this was followed by a visit to the Jordanian capital,Amman, by Bashar al-Assad in March. A reciprocal visit to Damascus by KingAbdullah in April appears to have opened a new chapter in Syrian-Jordanianrelations, which plummeted after Jordan made peace with Israel in 1994.

There is more than symbolic value in the exchange of visits. King Abdullah’svisit has paved the way for a series of economic and political agreementsbetween the two countries, the most important of which has seen Syria agreeto supply drought-ridden Jordan with drinking water from one its southerndams. In May Syria begin to pump 8m cubic metres of water for four monthsto its southern neighbour, a commitment that involves an element of sacrificesince Syria, too, is suffering from a severe drought. Israel has refused to supplywater to Jordan because of its own shortages.

—although Syria appearskeen to keep them involved

Syria’s hand isstrengthened by better

relations with Jordan—

18 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

The water is being pumped from the Bassel al-Assad dam near the southerntown of Daraa, close to the border with Jordan. From the Yarmouk river, whichmarks part of the border between the two countries, the water is directed to theAbdullah Canal and on to Amman. It does not appear that Jordan is having topay for the water, since Syrian government officials have described it as a“donation” from Mr Assad.

The two countries have also agreed to revive a 1987 agreement to build theUnity (Wahda) dam on the Yarmouk, at a cost of $211m. While Jordan wouldtake most of the water from the proposed dam, Syria would take some 75% ofthe electricity generated by a proposed hydroelectric power station. It appearsthat financing has been left up to the Jordanians. The two countries also agreedon a timetable for a long-running plan to link their electricity grids. Thisshould now be completed by the end of this year.

The two sides have also been investigating ways of easing travel across theirmutual border, on which there have been severe restrictions since Jordan’speace treaty with Israel in 1994. It now appears that Jordan has agreed to keepa close eye on Syrian Muslim Brotherhood members, who found exile inAmman in the 1980s after a failed rebellion against the Assad regime, whileSyria has pledged to keep a lid on criticism of Jordan by radical Palestiniangroups based in Damascus. Some 60% of Jordan’s population are Palestinian.

Syria has also sought to bolster its negotiating position by improving ties withRussia, its former cold war patron. Although Mr Assad abruptly cancelled aplanned trip to Moscow in April (2nd quarter 1999, page 15), speculation thatSyria is intending to purchase $2bn of Russian weapons was rekindled by a visitto Moscow in early July. Syria’s shopping list is said to include the Sukhoi-27fighter aircraft, T-80 tanks and the S-300 anti-aircraft/anti-missile system. Syriais also keen to upgrade its ageing MiG-21 and MiG-23 fighter planes, and securespare parts for its MiG-29 aircraft, which it acquired in the late 1980s and early1990s. In return, Syria is said to be considering offering the Russian navy a baseon its Mediterranean coast. The two sides also recently agreed in principle thatRussia should help Syria build two nuclear reactors, for electricity generation.

Finance is likely to be the main stumbling block. The Russian Treasury is saidto be extremely reluctant to engage in any deal, given that Syria still owes theformer Soviet Union $12bn, most of it relating to previous military deliveries.Russia’s foreign ministry, however, has taken a different tack. It recognises thatSyria is unlikely to make anything more than a token downpayment for freshmilitary supplies, but believes that the strategic advantage to be gained fromregaining Syria’s favour is more than adequate compensation.

The proposed deal is likely to face tough opposition from the US and Israel. InApril the US government punished Russian firms with financial sanctions forallegedly selling sophisticated anti-tank weapons to Syria (although it is notclear whether these Kornet-3 weapons have actually been delivered). Syria haspointed to a recent US decision to supply Israeli with 50 Lockheed Martin F-16fighter jets as evidence of double standards by the US on this issue.

—as Syrian drinking waterflows to Amman

Improved ties with Russiawill also help Syria’s

position—

—although any arms deal islikely to face strong Israeli

and US opposition

Syria 19

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

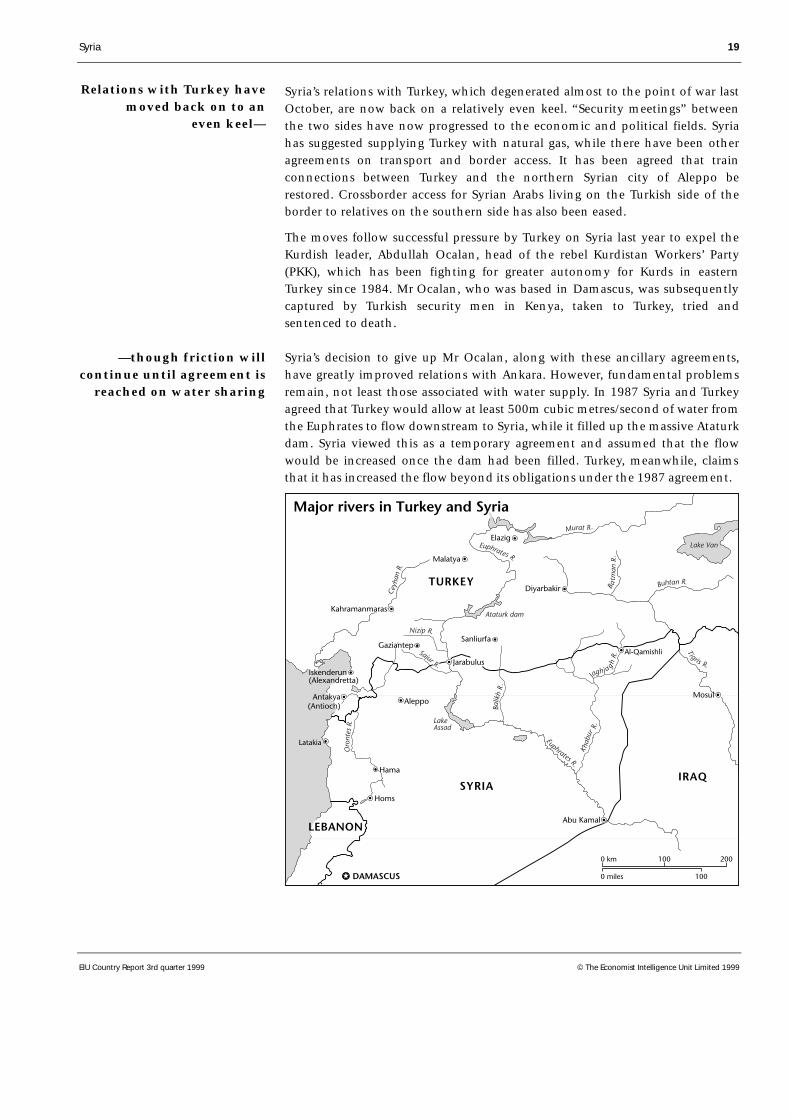

Syria’s relations with Turkey, which degenerated almost to the point of war lastOctober, are now back on a relatively even keel. “Security meetings” betweenthe two sides have now progressed to the economic and political fields. Syriahas suggested supplying Turkey with natural gas, while there have been otheragreements on transport and border access. It has been agreed that trainconnections between Turkey and the northern Syrian city of Aleppo berestored. Crossborder access for Syrian Arabs living on the Turkish side of theborder to relatives on the southern side has also been eased.

The moves follow successful pressure by Turkey on Syria last year to expel theKurdish leader, Abdullah Ocalan, head of the rebel Kurdistan Workers’ Party(PKK), which has been fighting for greater autonomy for Kurds in easternTurkey since 1984. Mr Ocalan, who was based in Damascus, was subsequentlycaptured by Turkish security men in Kenya, taken to Turkey, tried andsentenced to death.

Syria’s decision to give up Mr Ocalan, along with these ancillary agreements,have greatly improved relations with Ankara. However, fundamental problemsremain, not least those associated with water supply. In 1987 Syria and Turkeyagreed that Turkey would allow at least 500m cubic metres/second of water fromthe Euphrates to flow downstream to Syria, while it filled up the massive Ataturkdam. Syria viewed this as a temporary agreement and assumed that the flowwould be increased once the dam had been filled. Turkey, meanwhile, claimsthat it has increased the flow beyond its obligations under the 1987 agreement.

Relations with Turkey havemoved back on to an

even keel—

—though friction willcontinue until agreement is

reached on water sharing

20 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Further Turkish damming projects have only added to the friction. Syria andIraq are both downstream of Turkey’s Great Anatolian Project (GAP), a series ofdams for the Euphrates river. Full implementation of the GAP system couldresult in a 40% reduction in the flow of the Euphrates into Syria, and a 80%reduction in its flow into Iraq. Syria says that such a reduction would restrict thepower output from its Tabqa dam to a mere 12% of its capacity. The GAP schemealso promises to increase salinity and other forms of pollution in the Euphrates.

Syrian co-ordination with Iraq on this issue has been stronger than mostobservers expected. Syria has reportedly formally asked the UK not to supportTurkish plans to build the $1.5bn Ilisu dam on the Tigris river, even though theTigris does not actually flow through Syria.

Relations with Iraq are therefore likely to remain reasonably good, at least untilthe water issue with Turkey has been resolved. There is also a separate econ-omic rationale to an improvement in ties: the two sides have now set upinterest sections in their respective capitals, and have begun to discuss ways ofrestoring rail links. There is essentially only one crossborder rail link, atYaroubiyah, but this has been closed for two decades. Another link exists atAbu Kamal, but the railway line is only complete on the Iraqi side of the border.

Despite the lack of rail links, transport contact between the two sides has con-tinued to grow in line with the UN administered oil-for-food deal, which allowsIraq to export oil in exchange for certain commodities. However, there havealso been reports of increased smuggling involving Iraqi fuel oil and diesel. Thenumber of road tankers crossing the border each week is now said to run intothe hundreds. UN officials, who monitor Iraqi trade, seem powerless to stop theflow, largely because they operate at just one of three border crossings withSyria and are only mandated to search vehicles travelling into Iraq.

Economic policy and the economy

Pressure on the government to take decisive action on economic reform haseased over the past few months in line with the recovery in oil prices. In lateJuly Syrian Light, the country’s main export blend, was trading at about$18.50/barrel, compared with a paltry $10/b at the beginning of 1999. This isalso a substantial improvement over 1998, when Syrian Light averaged $11.90/b.

Oil is a vital earner for Syria, accounting for around 60% of export earnings,and nearly half of government revenue. The recovery in oil prices maytherefore partly explain the lack of any major economic initiatives, althoughdomestic and regional political considerations are probably more to blame forthe inertia. This has added to the sense of gloom among local businessmen,who bemoan the lack of meaningful liberalisation in recent years. However, itis unclear whether the appointment of a new cabinet (which is supposed to beimminent) would lead to an overhaul of existing business legislation, similar tothat in 1991, which helped boost business confidence and economic activity inthe early 1990s. Reports that Ahmed Qabalan is to become the next primeminister do not augur particularly well, given his background in rural BaathParty politics (see The political scene).

Smuggling between Syriaand Iraq is growing

Pressure for reform haseased as oil prices recover—

Syria 21

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

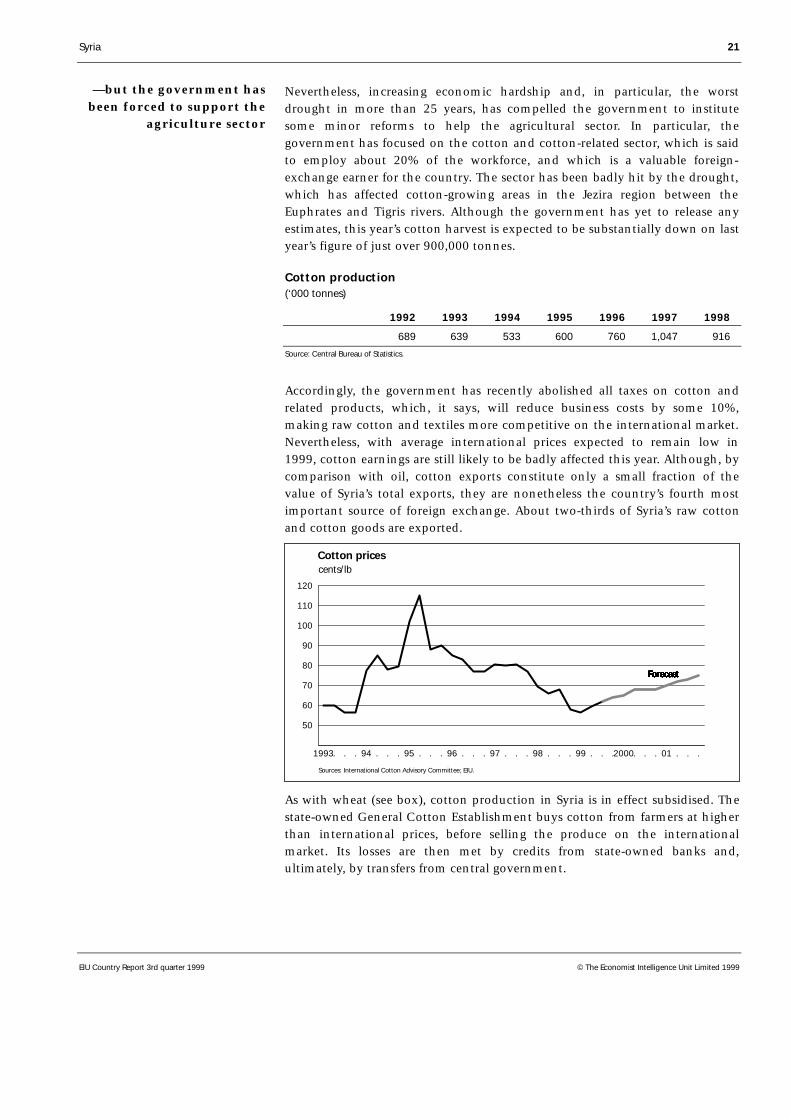

Nevertheless, increasing economic hardship and, in particular, the worstdrought in more than 25 years, has compelled the government to institutesome minor reforms to help the agricultural sector. In particular, thegovernment has focused on the cotton and cotton-related sector, which is saidto employ about 20% of the workforce, and which is a valuable foreign-exchange earner for the country. The sector has been badly hit by the drought,which has affected cotton-growing areas in the Jezira region between theEuphrates and Tigris rivers. Although the government has yet to release anyestimates, this year’s cotton harvest is expected to be substantially down on lastyear’s figure of just over 900,000 tonnes.

Cotton production(‘000 tonnes)

1992 1993 1994 1995 1996 1997 1998

689 639 533 600 760 1,047 916

Source: Central Bureau of Statistics.

Accordingly, the government has recently abolished all taxes on cotton andrelated products, which, it says, will reduce business costs by some 10%,making raw cotton and textiles more competitive on the international market.Nevertheless, with average international prices expected to remain low in1999, cotton earnings are still likely to be badly affected this year. Although, bycomparison with oil, cotton exports constitute only a small fraction of thevalue of Syria’s total exports, they are nonetheless the country’s fourth mostimportant source of foreign exchange. About two-thirds of Syria’s raw cottonand cotton goods are exported.

50

60

70

80

90

100

110

120

1993. . . 94 . . . 95 . . . 96 . . . 97 . . . 98 . . . 99 . . .2000. . . 01 . . .

Cotton pricescents/lb

Sources: International Cotton Advisory Committee; EIU.

ForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecastForecast

As with wheat (see box), cotton production in Syria is in effect subsidised. Thestate-owned General Cotton Establishment buys cotton from farmers at higherthan international prices, before selling the produce on the internationalmarket. Its losses are then met by credits from state-owned banks and,ultimately, by transfers from central government.

—but the government hasbeen forced to support the

agriculture sector

22 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Subsidising wheat

A confidential 1998 IMF report on the Syrian economy showsthat government efforts since the late 1980s to boostdomestic wheat production and reach self-sufficiency (whichwas achieved in 1992) are continuing to cost the governmentheavily in subsidies. According to the report, the GeneralEstablishment for Cereal Processing and Trade (GECPT) boughta total of 1.8m tonnes of wheat from farmers in 1997, at acost of S£11,300/tonne. This compared with an inter-national market rate of S£8,300/t (cif import basis at anexchange rate of S£50:$1). By extension, the IMF calculates,the GECPT would have saved S£5.4bn—equivalent tosome 0.8% of GDP—had it imported its wheat rather thanbought it locally.

The GECPT then sold the bulk of the wheat to local mills, withthe remainder exported. For the wheat it sold to the mills, theGECPT charged some S£17,700/t, representing the cost of thewheat, plus transport and distribution costs of some S£6,600/t.The mills then produced about 1.7m tonnes of flour at anaverage cost of S£22,900/t, but then sold it to the bakeries ata fixed price of S£7,100/t, incurring a loss of around S£26.5bn,or the equivalent of 3.8% of GDP.

All these losses were subsequently met by budgetary transfersand credits from state-owned banks. About S£4.7bn,equivalent to 0.7% of GDP, was budgeted for and transferred

from the Ministry of Finance to the GECPT to help cover itsexport losses. The mills’ losses were covered by the GECPT andwere met by monies from the government’s Price StabilisationFund (PSF), which finances consumer subsidies on wheat, sugarand rice. The PSF has two sources of revenue: one fromsurcharges earmarked specifically for it on a number of goods,such as TV sets, carpets and refrigerators; the other from directbudgetary transfers.

In 1997 the PSF received a total of S£7.5bn from these twosources, far less than the S£26.5bn it needed to cover thefinancial losses on wheat sales, and the S£2.5bn it needed tomeet rice and sugar subsidies. To bridge the gap, the PSFborrowed from the state-run Commercial Bank of Syria, a loanwhich itself was refinanced by the Central Bank of Syria.

Since 1994, the last time that bread prices were raised, wheatsubsidies have risen markedly with every increase in the harvest,from the equivalent of 3.5% of GDP to 5.3% in 1997, accordingto the IMF. Of this 5.3%, most has been used to cover subsidiesto the consumer, with the remainder given to farmers and asexport subsidies. To reduce the fiscal burden of these payments,the IMF has advised the Syrian government to raise prices onsubsidised foods. However, for a government that places such ahigh priority on social stability, this seems unlikely in the short tomedium term.

The government has also been forced to extend help to other parts of the agri-cultural sector, particularly wheat, barley and livestock farmers. The drought,which in some parts of the country, such as Daraa in the south, has been theseverest for 50 years, has decimated the barley crop and forced the governmentto import barley for the first time in around a decade. Last year, for example,local barley production stood at about 1.6m tonnes, of which some 1m tonneswent towards domestic consumption, with the bulk of that as animal feed.

This year the barley crop is expected to fall dramatically, to some 365,000 tonnes,well below local consumption needs. Most of the shortfall—some 500,000tonnes—is expected to be met from stored reserves. Nevertheless, the govern-ment admits that some barley (it does not say how much) will be imported, eitherto meet the shortfall directly or replenish reserves. Import taxes on the crop,designed to protect domestic production, have now been lifted. The governmenthas also sold fodder to livestock farmers at subsidised prices and has extendedthem free medicine and interest-free loans. An export ban on male cattle has alsobeen lifted to boost livestock prices. In times of fodder shortages livestock isusually killed—in 1989, for example, the last time that Syria was hit by drought,up to 50% of domestic livestock were slaughtered. Government officials areconfident that these measures will discourage farmers from culling their stock.

The government importsbarley for the first time in

a decade—

Syria 23

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

The wheat sector has also been badly hit by the shortage of water. This year’sharvest is expected to be down by some 35% to 2.66m tonnes, compared with4.1m tonnes in 1998. Domestic consumption is estimated at a little over3m tonnes, leaving a shortfall this year of around 340,000 tonnes. Again, thisdeficit is expected to be met by dipping into stored reserves, which areestimated at more than 2m tonnes.

There have been precious few other economic policy initiatives in the past fewmonths. According to local reports, a ministerial committee has recentlyapproved a series of amendments to Investment Law No. 10. These areunderstood to include allowing foreign investors to own the land on whichthey operate their projects, and some proposals on easing foreign-exchangerestrictions, though details have not been spelt out. The amendments areunder discussion by the full cabinet and, if agreement is reached, will then besent on to parliament for approval.

But even if these discussions eventually result in fresh legislation, there havealso been indications of a less flexible attitude to reform. The economyminister, Mohammed al-Imadi, has told a meeting of private-sectorbusinessmen that exchange-rate unification is out of the question as long asprivate businesses continue to import more than they export. Addressingbusiness leaders in Damascus on July 5th, Mr Imadi blamed the private sectorfor bringing in imports worth more than S£32,600m ($2,904m at the officialexchange rate) in 1998, while the value of their exports reached just S£9,100m($812m). The minister also rejected business leaders’ complaints that private-sector exporters need further incentives. The government has eased someaspects of the foreign-exchange regime in recent years, but exporters are stillobliged to change 25% of their earnings at local state-owned banks for a“commercial” exchange rate of S£46:$1. This compares with a black-marketrate of about S£50:$1.

The government had still not approved the 1999 budget as this report went toprint, though leaks suggest that expenditure will be set at just over S£255bn,up by some 7.3% on the IMF’s estimate of actual expenditure in 1998.However, there is no indication yet of expected revenue or deficit projectionsfor the year. In the meantime, government finances are being conductedaccording to the 1998 budget.

Government budget figures are, in any case, of limited value in determiningthe efficacy of fiscal policy, given that the government never publishes its out-turn data. The IMF has provided such data, but these numbers are suspiciouslysimilar to the budgeted figures. It should also be noted that the IMF’sprojections for 1998 government revenue were made relatively early in theyear; given the decline in oil prices during the course of 1998, actual revenue islikely to have been significantly smaller than that predicted by the Fund.

—but doubt is cast onfurther exchange-rate

liberalisation

Government expenditurelooks set to rise in 1999—

—though official figuresare largely unhelpful

—and dips into wheatreserves to satisfy domestic

demand

There has been sometinkering with

Law No. 10—

24 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

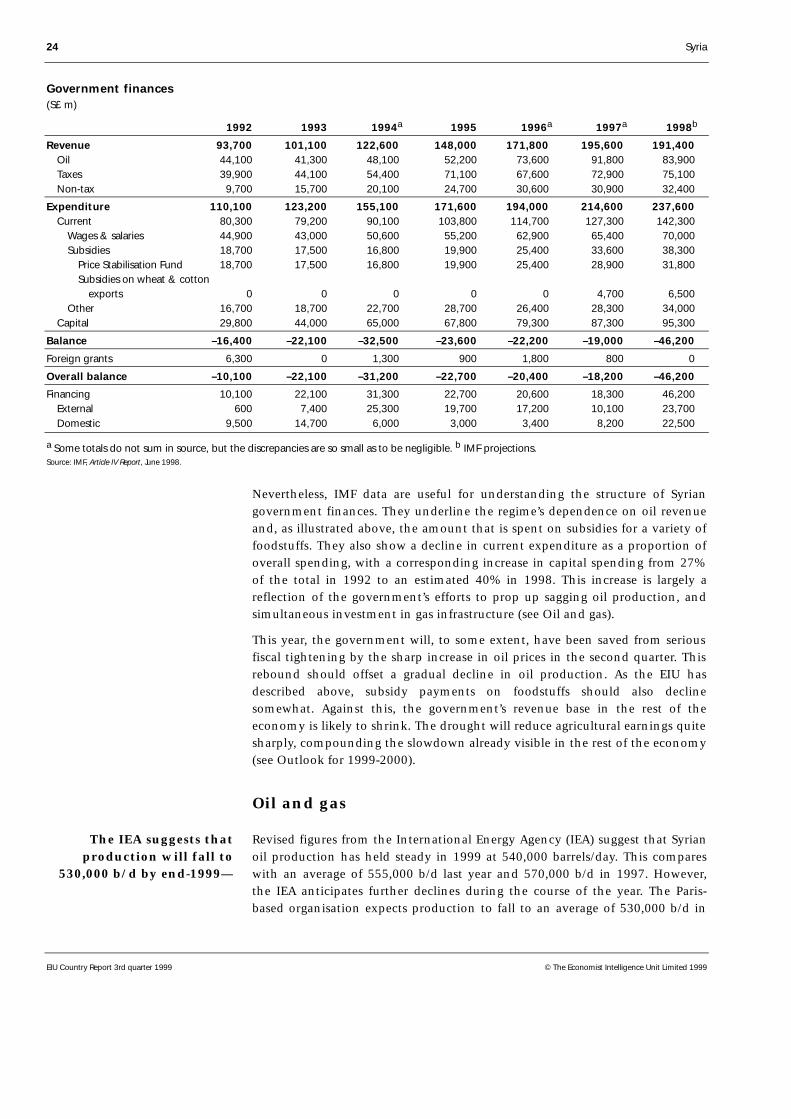

Government finances(S£ m)

1992 1993 1994a 1995 1996a 1997a 1998b

Revenue 93,700 101,100 122,600 148,000 171,800 195,600 191,400 Oil 44,100 41,300 48,100 52,200 73,600 91,800 83,900 Taxes 39,900 44,100 54,400 71,100 67,600 72,900 75,100 Non-tax 9,700 15,700 20,100 24,700 30,600 30,900 32,400

Expenditure 110,100 123,200 155,100 171,600 194,000 214,600 237,600 Current 80,300 79,200 90,100 103,800 114,700 127,300 142,300 Wages & salaries 44,900 43,000 50,600 55,200 62,900 65,400 70,000 Subsidies 18,700 17,500 16,800 19,900 25,400 33,600 38,300 Price Stabilisation Fund 18,700 17,500 16,800 19,900 25,400 28,900 31,800 Subsidies on wheat & cotton exports 0 0 0 0 0 4,700 6,500 Other 16,700 18,700 22,700 28,700 26,400 28,300 34,000 Capital 29,800 44,000 65,000 67,800 79,300 87,300 95,300

Balance –16,400 –22,100 –32,500 –23,600 –22,200 –19,000 –46,200

Foreign grants 6,300 0 1,300 900 1,800 800 0

Overall balance –10,100 –22,100 –31,200 –22,700 –20,400 –18,200 –46,200

Financing 10,100 22,100 31,300 22,700 20,600 18,300 46,200 External 600 7,400 25,300 19,700 17,200 10,100 23,700 Domestic 9,500 14,700 6,000 3,000 3,400 8,200 22,500

a Some totals do not sum in source, but the discrepancies are so small as to be negligible. b IMF projections.Source: IMF, Article IV Report, June 1998.

Nevertheless, IMF data are useful for understanding the structure of Syriangovernment finances. They underline the regime’s dependence on oil revenueand, as illustrated above, the amount that is spent on subsidies for a variety offoodstuffs. They also show a decline in current expenditure as a proportion ofoverall spending, with a corresponding increase in capital spending from 27%of the total in 1992 to an estimated 40% in 1998. This increase is largely areflection of the government’s efforts to prop up sagging oil production, andsimultaneous investment in gas infrastructure (see Oil and gas).

This year, the government will, to some extent, have been saved from seriousfiscal tightening by the sharp increase in oil prices in the second quarter. Thisrebound should offset a gradual decline in oil production. As the EIU hasdescribed above, subsidy payments on foodstuffs should also declinesomewhat. Against this, the government’s revenue base in the rest of theeconomy is likely to shrink. The drought will reduce agricultural earnings quitesharply, compounding the slowdown already visible in the rest of the economy(see Outlook for 1999-2000).

Oil and gas

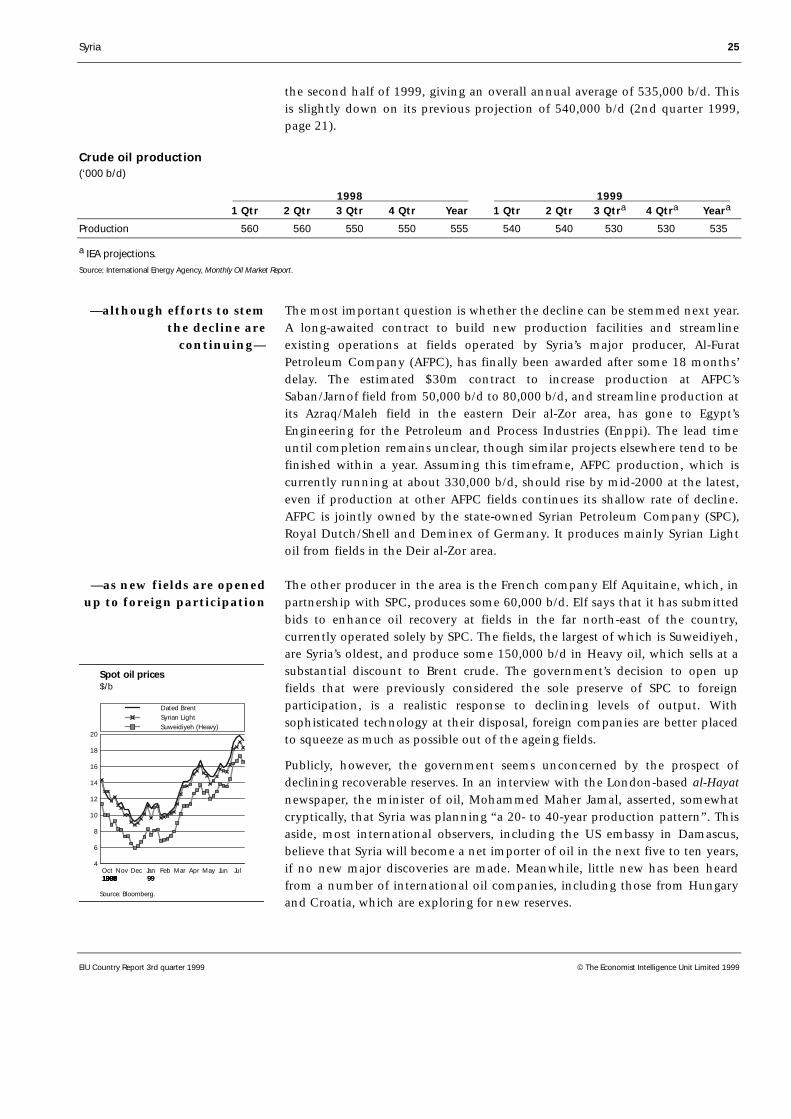

Revised figures from the International Energy Agency (IEA) suggest that Syrianoil production has held steady in 1999 at 540,000 barrels/day. This compareswith an average of 555,000 b/d last year and 570,000 b/d in 1997. However,the IEA anticipates further declines during the course of the year. The Paris-based organisation expects production to fall to an average of 530,000 b/d in

The IEA suggests thatproduction will fall to

530,000 b/d by end-1999—

Syria 25

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

the second half of 1999, giving an overall annual average of 535,000 b/d. Thisis slightly down on its previous projection of 540,000 b/d (2nd quarter 1999,page 21).

Crude oil production(‘000 b/d)

1998 1999 1 Qtr 2 Qtr 3 Qtr 4 Qtr Year 1 Qtr 2 Qtr 3 Qtra 4 Qtra Yeara

Production 560 560 550 550 555 540 540 530 530 535

a IEA projections.Source: International Energy Agency, Monthly Oil Market Report.

The most important question is whether the decline can be stemmed next year.A long-awaited contract to build new production facilities and streamlineexisting operations at fields operated by Syria’s major producer, Al-FuratPetroleum Company (AFPC), has finally been awarded after some 18 months’delay. The estimated $30m contract to increase production at AFPC’sSaban/Jarnof field from 50,000 b/d to 80,000 b/d, and streamline production atits Azraq/Maleh field in the eastern Deir al-Zor area, has gone to Egypt’sEngineering for the Petroleum and Process Industries (Enppi). The lead timeuntil completion remains unclear, though similar projects elsewhere tend to befinished within a year. Assuming this timeframe, AFPC production, which iscurrently running at about 330,000 b/d, should rise by mid-2000 at the latest,even if production at other AFPC fields continues its shallow rate of decline.AFPC is jointly owned by the state-owned Syrian Petroleum Company (SPC),Royal Dutch/Shell and Deminex of Germany. It produces mainly Syrian Lightoil from fields in the Deir al-Zor area.

The other producer in the area is the French company Elf Aquitaine, which, inpartnership with SPC, produces some 60,000 b/d. Elf says that it has submittedbids to enhance oil recovery at fields in the far north-east of the country,currently operated solely by SPC. The fields, the largest of which is Suweidiyeh,are Syria’s oldest, and produce some 150,000 b/d in Heavy oil, which sells at asubstantial discount to Brent crude. The government’s decision to open upfields that were previously considered the sole preserve of SPC to foreignparticipation, is a realistic response to declining levels of output. Withsophisticated technology at their disposal, foreign companies are better placedto squeeze as much as possible out of the ageing fields.

Publicly, however, the government seems unconcerned by the prospect ofdeclining recoverable reserves. In an interview with the London-based al-Hayatnewspaper, the minister of oil, Mohammed Maher Jamal, asserted, somewhatcryptically, that Syria was planning “a 20- to 40-year production pattern”. Thisaside, most international observers, including the US embassy in Damascus,believe that Syria will become a net importer of oil in the next five to ten years,if no new major discoveries are made. Meanwhile, little new has been heardfrom a number of international oil companies, including those from Hungaryand Croatia, which are exploring for new reserves.

—although efforts to stemthe decline are

continuing—

—as new fields are openedup to foreign participation

4

6

8

10

12

14

16

18

20

Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Dated BrentSyrian LightSuweidiyeh (Heavy)

Spot oil prices$/b

Source: Bloomberg.

19981998199819981998199819981998 999919981998 99

26 Syria

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

The effect of declining output has been partly offset by a substantial reboundin world crude prices. By late July Dated Brent had reached $19.52/b as themarket absorbed fresh data showing greater commitment to productioncutbacks among OPEC member states than had been anticipated. Syrian Lightwas priced at some 80 cents below this benchmark.

In any case, the government is increasingly turning its attention to the gassector. Important developments in the past few months include fresh gasdiscoveries in the northern Homs area and the confirmation of a $430mproject, involving Elf Aquitaine and Conoco of the US, to gather, treat anddistribute gas previously flared off from AFPC oilfields in the Deir al-Zor area(4th quarter 1998, page 17).

The government’s letter of intent with Conoco and Elf, which was signed lastNovember, was recently ratified by the Syrian government and parliament.This paves the way for the construction of a large gas treatment plant near Deiral-Zor, with a capacity to process 5m cubic metres/day. The plant is scheduledto be completed around mid-2001. Other elements of the development includean additional $30m project to develop the nearby gas/gas-condensate field atTabiyeh, though the projected capacity of this plant is not known.

SPC, meanwhile, has continued exploration in the gas-rich areas of Palmyraand Homs, in the centre and west of the country, and has announced thediscovery of another gas deposit in the al-Faydh field, close to Homs. The fieldhad been abandoned by a previous prospector, Marathon of the US, which hadspent years of fruitless search in Syria. The government claims that the newdeposit has the capacity to produce 1m cu metres/d of gas. The Abu Rabahfield, which is next to the new discovery, is said to produce 2m cu metres/d.Total Syrian gas production, all of which is currently used locally to feed powerstations, and for industrial and residential purposes, is put at 10-12m cumetres/d. Planned and current construction projects are expected to increaseoutput to around 18m cu metres/d by about 2001.