SYMC BUY REC

25

Symantec Corporation Jozsef Nemeth

-

Upload

jozsef-nemeth -

Category

Documents

-

view

124 -

download

0

Transcript of SYMC BUY REC

Symantec Corporation Jozsef Nemeth

[Jozsef Nemeth]

Student Research This report is published for educational purposes

only for the Roland George Investments

Program.

Industry: Software

Sector: Information Technology

Ticker: SYMC (NASDAQ) Recommendation: Buy

Price: $ 24.82 (as of 10/31/2014)

Fair Value: 29.11$

Undervalued by: 17.68%

Earnings/Share Jun. Sep. Dec. Mar. Year P/E Ratio

2011 $0.40 $0.39 $0.42 $0.38 $1.59 24.30

2012 0.43 0.45 0.45 0.44 1.77 11.78

2013 0.44 0.50 0.51 0.47 1.92 23.24

2014A/E* 0.44

0.45 0.48 0.57 1.94 15.01

2015E 0.50 0.48 0.54 0.53 2.04 14.26

Highlights

De-Merger: Symantec announced the de-merger of the company’s security and information management

segments, with completion expected in December 2015. They seek to create two companies that are better

able to pursue individualized growth opportunities that arise in their individual industries. Additionally,

many of the difficulties of splitting up sales teams and shared contracts has already been resolved as the

company began to optimize their company for margins. Management went as far as to say these

transitions are roughly 60% complete, and the December deadline will remain solely on SEC approval.

New Strategic Direction: Symantec’s new management team spent 2013 reviewing every aspect of the

company to improve growth in the fast evolving industry. By the end of the year Symantec announced

their new goal to target 30% operating margins and 5% organic growth by FY2015, something the

company has never done before. With a history of growing through acquisition, the new strategic

direction has shown to be much more effective in growing revenue as the company reported 50% revenue

growth year-over-year in Q1 2015.

Global Intelligence Network 2.0: Symantec collects telemetry about security threats at nearly 200,000

rows a second, in the largest privately run global intelligence network. Symantec has begun to use the

information collected in the global intelligence network to provide advance threat protection in all the

companies’ key products. This will make Symantec’s security products the standard of the industry and

thus increasing the company’s market share.

Dominating Information Management Industry: Symantec has maintained a market leading position

in the information management segment, as they capture over half of the Fortune 500 companies.

Additionally the information management segment has seen the recent release of innovative products that

will help spur growth for the segment in the future.

Stock Valuation: Due to their new strategic direction, dominating market position, and value of a de-

merged company, I estimate that Symantec stock has an expected return of 7.16%. Further, Symantec is

undervalued by 17.68% with a fair value of $29.21. The total return suggests that it is an attractive buy.

Date: 11/3/2014

$17.95-$25.53

5,143,560

0.99

690.31M

17.13 B

92.30%

0.25%

27%

15.11%

Institutional Holdings

Insider Holdings

Debt to Total Capital

Return on Equity

Market Profile

52-Week Price Range

Average Daily Volume

Beta

Shares Outstanding

Market Capitalization

SYMC

S&P 500

Industry

01/8/14 Roland George Investment Program

Stetson University Student Research

2

Exhibit 1: The Company

Exhibit 2: Product Revenue Breakdown

Exhibit 3: Segment Operating Margin

Exhibit 4: Segment Revenue Growth

Business Description

Company: Symantec Corp. (NASDAQ: SYMC) was founded in 1982 and has since become one of the

largest software companies in the world, with over 18,500 employees in more than 50 countries (Exhibit 1).

Headquartered in Mountain View, CA Symantec’s products and services protect people and information in

any environment from mobile devices and enterprise data centers to cloud-based systems. Symantec’s

recently announced a de-merger of their security and information management businesses, which will create

two market leading companies.

Products: Through its stores and resellers, the company offers the following products (% of all revenue):

Consumer Security (31%): Norton solutions, endpoint security and management, encryption and mobile

offerings.

Enterprise Security (31%): Endpoint security, endpoint management, encryption, mobile, secure socket

layers certificate, user authentication, mail, web and data center security, data loss prevention, hosted

security and managed security services.

Information Management (38%): Backup and recovery, archiving and eDiscovery, storage and high

availability solutions.

Over the past three years the revenue breakdown of Symantec has remained relatively stable, where the

largest source of revenue, Information Management, has the lowest operating margin of 23% (Exhibit 2). On

the other hand, Consumer Security, which has the highest operating margin of 45%, has the lowest revenue

share.

Growth Strategies: Symantec has four main growth strategies:

Manage Product Portfolio for Margin: Symantec has begun to optimize their businesses based on

growth potential and lifecycle. The company recognizes some businesses are ideal for achieving the

targeted 30% operating margins, while others will drive future growth (Exhibit 3). Symantec started by

optimizing their Norton brand, Storage Foundation, and Cluster Offerings segments for higher margins.

The first change was the creation of the new consumer segment for the Norton brand, with specialized

staff to improve product know-how. Norton brand product offerings were additionally simplified with the

release of Norton Security and Norton Security with backup, an all in one Norton Security software,

leading to less confusion for customers during product selection. Norton Small Business was released as

the first Norton solution for small businesses, which were the target of 30% of all cyber-attacks in 2013.

Meanwhile, Symantec has begun to streamline their channel strategy by exiting certain high cost and

unprofitable retail markets and OEM deals to improve their Storage Foundation segment. By streamlining

low growth segments for margins, Symantec is able to generate higher levels of free cash flow to invest in

high growth segments.

Focused R&D on High Growth Segments: To spur organic revenue growth Symantec’s has been

moving R&D dollars to backup appliances and selected security business (Exhibit 4). Symantec’s backup

appliances grew 35% year-over-year as they doubled the capacity of backup from 76-terabytes to 148-

terabytes, allowing for the targeting of the upper mid-market of the enterprise segments, essentially

doubling the company’s addressable market. Under backup appliances Symantec recently released

NetBackup 7.6 providing the first enterprise level backup product on the market, in a time when

enterprises are moving to software-defined data center architecture. In the security segment Symantec has

begun to leverage their four trillion threat indicators from millions of endpoints to reduce false positives,

which seriously compromised the value for customers. Symantec launched their managed Advance

Threat Protection (ATP) service that triangulates threat indicators to provide best in class comprehensive

threat detection. Symantec has additionally been launching multiple new services targeting enterprises

such as Incident Response, Managed Adversary, and Threat Intelligence. In addition to focusing on

organic growth, Symantec is considering making multiple acquisitions in technologies that strengthen

their capabilities or add new capabilities that fit growth objectives.

Reduce Cost and Improve Efficiency: Symantec is pursuing eight initiatives to grow revenue and

improve cost-efficiency. Symantec has recognized revenue inefficiencies in new customer acquisition

along with their renewal rates, requiring two initiatives targeting these shortfalls. Symantec has thus

created two dedicated teams to focus on renewals and new customers allowing for better coordination

among the sales groups. The third revenue efficiency initiative put in place is improving license

compliance, reducing complexity for customers so they do not fall out of compliance. The final revenue

efficiency initiative is pricing optimization, which incorporates customer feedback and market dynamics

Headquarters Mountain View, CA

Year Founded 1982

IPO Date 1989

No. of Employees 18,500

No. of Countries 50

No. of Patents 2,700

Consumer Security

Enterprise Security

Information Management

Consumer Security

Enterprise Security

Information Management

01/8/14 Roland George Investment Program

Stetson University Student Research

3

Exhibit 8: Security Industry Revenue

Exhibit 10: Information Management

Industry Revenue

Exhibit 9: Mobile Security Industry Revenue

Exhibit 5: Technology Revenue

Growth vs. GDP Growth

Exhibit 7: SYMC Revenue Growth vs.

GDP Growth

Exhibit 6: Revenue Growth Comparison

into more transparent pricing policies and more efficient selling processes. These four revenue initiatives

should help drive top line growth and support margin expansion.

The first cost-efficiency initiative is to optimize the Norton business, by streamline their product offerings

and supporting Symantec’s first growth strategy. Additionally, the sales and support teams have been

divided into security and information management, allowing for better product specialization and support

times, improving customer feedback. Symantec has also been reducing their global footprint, reducing

redundant positions and consolidating data centers. The final cost-efficiency Symantec plans to pursue

performance based incentives for sales and R&D teams.

Attract Top Talent: Symantec has seen a relatively high level of upper management turnover in the last

year, with a new CEO, CIO, CFO, and two new board members. Symantec announced the appointment of

CEO Michael Brown in September after an extensive search of over 100 candidates. Brown had been

serving as interim president and CEO since March 2013. Since Browns appointment as interim CEO

Symantec has returned to positive year-over-year revenue growth and consistently been exceeding

margins. In January Sheila Jordan was announced as Symantec’s CIO, with the focus of building and

supporting the global Information Technology effort at Symantec. Jordan joins Symantec after nine years

at Cisco where she managed IT services for Cisco’s global workforce. Symantec CFO Thomas Seifert

joined the company in April and has a long career as CFO for other technology companies such as

Brightstar and Advance Micro Devices. The newly appointed upper management and board provide the

Symantec with new direction and focus helping lead the company to grow revenue and improve operating

margins.

Competitors: Due to Symantec's two distinct operating segments of information management and security

the company does not have any direct competitors. However, Symantec may be compared to Gemalto (GTO),

a Netherlands based mid cap growth company that provides solutions & services related to mobile

communication, machine-to-machine, and secure transactions and security. Gemalto has a global reach in 44

different countries, supported by their 12,000 employees. Additional competitors to Symantec include

Microsoft along with newly listed companies such as Palo Alto Networks and FireEye.

Industry and Peer Group Overview

Symantec operates in the Technology industry, providing primarily software to their customers. The

technology industry revenue growth has a 93% correlation with GDP growth (Appendix 6, Exhibit 5).

Additionally, the software segment has an 83% correlation to the Technology industry revenue growth

(Appendix 7, Exhibit 6). This shows that as the economy continues to improve into 2015, so will the revenue

growth of the industry. I then ran a regression of Symantec’s revenue growth since 1988 compared to GDP

growth and found no significant correlation (Appendix 8, Exhibit 7). I attribute this to the revenue growth the

company being much more volatile than the industry, in addition to the extremely high growth the company

saw in its early years.

The Security market, of the technology industry, is an extremely fragmented industry that is evolving rapidly

with the recent influx of security company IPO's. The security market total revenue in 2013 was $23 billion

and is expected to expending to $38 billion in 2018, with a projected compounded annual growth rate or

CAGR of 10% (Exhibit 8). The combination of high growth and fragmented markets provides a ripe

opportunity for continued innovation. The three main trends Gartner sees forming in the security industry

moving forward are; mobile security, big data, and advance targeted attacks. Over the last year there has been

a 91% increase in targeted attacks with attacks lasting three times as long. Meanwhile, 38% of mobile users

have become victims of cyber crime, which will likely increase as Bring Your Own Device (BYOD) mega

trend continues in the workplace. In the last year hackers have been able to expose 552 million identities, in

coordinated mega breaches, proving cybercrime remains a real and damaging threat to consumers and

businesses alike. Thus with the rise of mega breaches there has been a shift toward managed security

services. This segment of the security market is projected to be a $10 billion market by 2018, growing at a

30% CAGR for 2013 to 2018 (Exhibit 9).

The Information Management market is a mature market that still has tremendous opportunity. The

Information Management market total revenue was $11 billion in 2013 expanding to $16 billion by 2018,

with a CAGR of 7% (Exhibit 10). Major trends of the market include mobile, virtualization, hybrid clouds

and now the Internet of Things, helping to drive exponential growth for the industry. However, as

organizations are adding more storage, virtualizing workloads, and adopting cloud solutions it is becoming

more challenging to find the right information making the need for technology to manage information even

more vital.

in billions

in billions

in billions

Technology

GDP Growth

Technology

Software

SYMC

GDP Growth

01/8/14 Roland George Investment Program

Stetson University Student Research

4

Exhibit 12: Time Line of Data Breach, 2013

Exhibit 11: Impact of Data Breach

Exhibit 13: De-Merger Benefit

Antivirus is Dead

A recent article came out saying with the increased sophistication of cybercriminals it has become apparent

that antivirus software is dead. However, antivirus is not dead, according to Symantec Antivirus software

captures 45% of all threats and is a key part to multi-layered Endpoint security. Companies that are able to

provide effective multi-layered security products will capture growth opportunity leading to increased market

share in the consumer segment.

Cybercriminals Innovation

The security segment is constantly facing evolving threats for hackers. In 2012 the majority of security

threats targeted small business and manufacturers in cyber espionage in an attempt to capture intellectual

property. Small business were targeted due to their weak security and ultimately as a way to reach larger

companies via “watering hole” techniques. Manufactures were targeted as the supply chain for large

companies tend to hold valuable intellectual property. In 2013 cybercriminals unleashed the most damaging

series of cyber-attacks in history, with 8 mega breaches in the span of 2 months (Exhibit 11). This significant

shift in cybercriminal behavior revealed that criminals are plotting for months before pulling off huge heists –

instead of executing quick hits with smaller rewards (Exhibit 12). One mega breach can be worth 50 smaller

attacks and with the great success of these attacks and potential for huge paydays means that large-scale

attacks are here to stay. The best way to help prevent the mega breaches comes from training employees

about security, track company data and implement a strong security infrastructure. Symantec already is

offering or will be offering services and products to meet all the needs of companies to protect against the

new era of mega attacks.

Competitive Positioning

De-Merger of Security and Information Management Segments

In 2005, Symantec acquired Veritas Software, an Information Management company, for $13.52 billion. On

October 09, 2014 Symantec’s CEO announced the company would be separating into a Security company

and Information Management Company, with a tax-free distribution to Symantec shareholders of 100% of

the Information Management businesses new publicly traded stock, with expected completion in December

2015. The separation comes after the newly appointed management reviewed both businesses for achieving

their four strategies for growth. As the growth for both markets has drastically accelerated both companies

require distinct strategies and dedicated investments along different core competencies. By creating two

industry leading companies Symantec positions itself well in the industry to capture growth. On an Enterprise

Revenue value splitting the company and achieving industry average EV/Sales will result in an increase of

$6,218 (Exhibit 13). The de-merger of Symantec will add value to shareholders and capture future growth in

the following three ways:

Improve Strategic Focus: A separation will allow each company to more effectively focus on its unique

growth opportunities and allow for tailored R&D investments, improving go to market capabilities. These

improvements should help each company grow their market share and capture more future growth. The

Symantec security company will focus on the growth opportunities in three areas: unified security,

cybersecurity services and a best in class portfolio. Unified security will deliver a security platform that uses

big data for superior threat detection. A focus on cybersecurity services includes the launch of capabilities to

span managed security, incident response, threat adversary intelligence, and simulation based training.

Symantec also plans to optimize their portfolio offerings by integrating diverse capabilities into their security

products.

The Information Management business will focus on resilient foundational products, reduced total cost of

ownership (TCO), and Information Fabric. A focus on resilient products will allow the business to deliver

Information Management capabilities in an ever changing environment to customers through software, cloud,

or integrated appliances. The Information Management business will focus on delivering solutions that

reduce the TCO by helping customers reduce the unmanaged proliferation of redundant and unused data. The

last focus of the Information Management business will be on creating an information fabric that enables

visibility, management, and control of organizations entire information landscape as a map.

Reduce Operational Complexity: With Symantec’s current merged business there is an immense amount

of complexity caused by the breadth of their product offerings. Sales, R&D, and management teams all faced

difficulties in communication, creating issues with getting product offerings to customers, lower customer

feedback scores, slower R&D go to market times, and increase difficulty delivering strategic plans. By de-

merging the company Symantec will be able to streamline these processes and simplify each organization

operations, in turn improving communication. This will make it easier for customers to do business with the

individual companies, with separate product offerings and improved specialization by sales and support

teams.

Incidents

Identities Exposed

Number of

Breaches

Total

Identities

Exposed

in million in thousand

in

million

Current De-Merged

Security $4,618.24 $5,195.52

Information

Managemetn $8,006.24 $13,647.00

Enterprise Value $12,624.48 $18,842.52

01/8/14 Roland George Investment Program

Stetson University Student Research

5

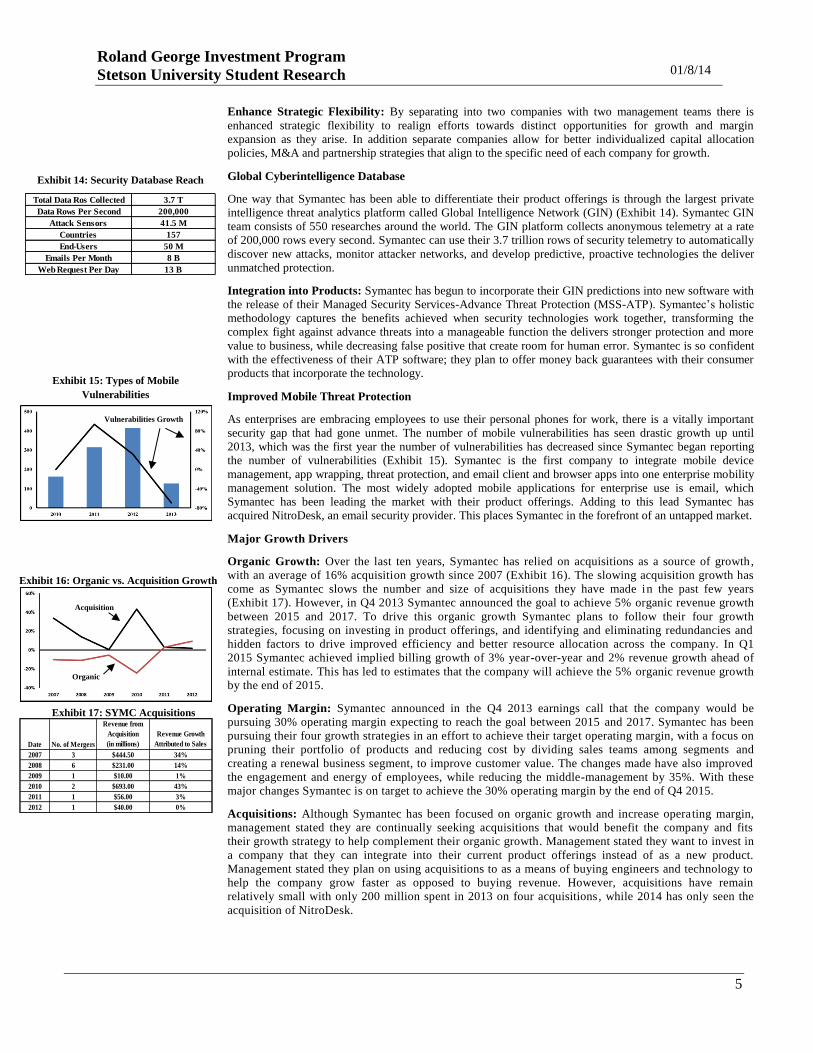

Exhibit 14: Security Database Reach

Exhibit 15: Types of Mobile

Vulnerabilities

Exhibit 16: Organic vs. Acquisition Growth

Exhibit 17: SYMC Acquisitions

Enhance Strategic Flexibility: By separating into two companies with two management teams there is

enhanced strategic flexibility to realign efforts towards distinct opportunities for growth and margin

expansion as they arise. In addition separate companies allow for better individualized capital allocation

policies, M&A and partnership strategies that align to the specific need of each company for growth.

Global Cyberintelligence Database

One way that Symantec has been able to differentiate their product offerings is through the largest private

intelligence threat analytics platform called Global Intelligence Network (GIN) (Exhibit 14). Symantec GIN

team consists of 550 researches around the world. The GIN platform collects anonymous telemetry at a rate

of 200,000 rows every second. Symantec can use their 3.7 trillion rows of security telemetry to automatically

discover new attacks, monitor attacker networks, and develop predictive, proactive technologies the deliver

unmatched protection.

Integration into Products: Symantec has begun to incorporate their GIN predictions into new software with

the release of their Managed Security Services-Advance Threat Protection (MSS-ATP). Symantec’s holistic

methodology captures the benefits achieved when security technologies work together, transforming the

complex fight against advance threats into a manageable function the delivers stronger protection and more

value to business, while decreasing false positive that create room for human error. Symantec is so confident

with the effectiveness of their ATP software; they plan to offer money back guarantees with their consumer

products that incorporate the technology.

Improved Mobile Threat Protection

As enterprises are embracing employees to use their personal phones for work, there is a vitally important

security gap that had gone unmet. The number of mobile vulnerabilities has seen drastic growth up until

2013, which was the first year the number of vulnerabilities has decreased since Symantec began reporting

the number of vulnerabilities (Exhibit 15). Symantec is the first company to integrate mobile device

management, app wrapping, threat protection, and email client and browser apps into one enterprise mobility

management solution. The most widely adopted mobile applications for enterprise use is email, which

Symantec has been leading the market with their product offerings. Adding to this lead Symantec has

acquired NitroDesk, an email security provider. This places Symantec in the forefront of an untapped market.

Major Growth Drivers

Organic Growth: Over the last ten years, Symantec has relied on acquisitions as a source of growth,

with an average of 16% acquisition growth since 2007 (Exhibit 16). The slowing acquisition growth has

come as Symantec slows the number and size of acquisitions they have made in the past few years

(Exhibit 17). However, in Q4 2013 Symantec announced the goal to achieve 5% organic revenue growth

between 2015 and 2017. To drive this organic growth Symantec plans to follow their four growth

strategies, focusing on investing in product offerings, and identifying and eliminating redundancies and

hidden factors to drive improved efficiency and better resource allocation across the company. In Q1

2015 Symantec achieved implied billing growth of 3% year-over-year and 2% revenue growth ahead of

internal estimate. This has led to estimates that the company will achieve the 5% organic revenue growth

by the end of 2015.

Operating Margin: Symantec announced in the Q4 2013 earnings call that the company would be

pursuing 30% operating margin expecting to reach the goal between 2015 and 2017. Symantec has been

pursuing their four growth strategies in an effort to achieve their target operating margin, with a focus on

pruning their portfolio of products and reducing cost by dividing sales teams among segments and

creating a renewal business segment, to improve customer value. The changes made have also improved

the engagement and energy of employees, while reducing the middle-management by 35%. With these

major changes Symantec is on target to achieve the 30% operating margin by the end of Q4 2015.

Acquisitions: Although Symantec has been focused on organic growth and increase operating margin,

management stated they are continually seeking acquisitions that would benefit the company and fits

their growth strategy to help complement their organic growth. Management stated they want to invest in

a company that they can integrate into their current product offerings instead of as a new product.

Management stated they plan on using acquisitions to as a means of buying engineers and technology to

help the company grow faster as opposed to buying revenue. However, acquisitions have remain

relatively small with only 200 million spent in 2013 on four acquisitions, while 2014 has only seen the

acquisition of NitroDesk.

Total Data Ros Collected 3.7 T

Data Rows Per Second 200,000

Attack Sensors 41.5 M

Countries 157

End-Users 50 M

Emails Per Month 8 B

Web Request Per Day 13 B

Vulnerabilities Growth

Organic

Acquisition

Date No. of Mergers

Revenue from

Acquisition

(in millions)

Revenue Growth

Attributed to Sales

2007 3 $444.50 34%

2008 6 $231.00 14%

2009 1 $10.00 1%

2010 2 $693.00 43%

2011 1 $56.00 3%

2012 1 $40.00 0%

01/8/14 Roland George Investment Program

Stetson University Student Research

6

Exhibit 18: Antivirus Market Share

Exhibit 19: Geographic Revenue Source

Exhibit 20: Dividend Yield

Potential Improvements in Market Share

Antivirus: The antivirus market has become more fragmented in the past few years. In 2013 the top ten

antivirus software made up 74% of the market share, while in 2014 the top ten companies only accounted for

62% of the entire market share (Exhibit 18). The top two companies Microsoft (23%) and Avast (15.9%)

offer free antivirus software, which leads to their high market share. Symantec is in 5th place for market share

with 8% trailing behind AVG and ESET by 1% and 0.1% respectively. However, Symantec has recently

streamlined their nine core Norton product offerings into on flagship product called Norton Security, which

will boost sales and market share for the company in the antivirus market.

Leading Information Management Market: Symantec’s Information management business has a become a

market leader with #1 market share in backup with 30% market share, reaching 75% of Fortune 500

companies through their availability solutions. The business also has leading market share in enterprise

backup and storage management products, with their NetBackup appliance products achieving 36% market

share, which grew 27% year over year. With the positive market position and growth it is expected Symantec

Geographical Growth: In 2013 Symantec achieved rigorous foreign government certifications, allowing the

company to offer additional security products in two key regions; Russia and China. Symantec Endpoint

Protection Small Business Edition was added to the list of three previously approved products in Russia.

Currently the EMEA (E.U, Middle East, and Africa) makes up 29% of Symantec revenue however, it has

been growing as a percentage of sales since 2011 (Exhibit 19). In addition, thirteen products achieved

certification for China’s Ministry of Public Safety and the Ministry of Public Security of the People’s

Republic of China. 2013 marked the first year Symantec recognized the Asian Pacific and Japan as an

individual segment, and by Q1 2015 17%of Symantec’s revenues came from this segment. The global

segments have substantial growth potential and Symantec has assurance from government certifications to

provide confidence in companies and people as Symantec expands.

Leading Data Center

Symantec released their Storage Foundation software, which enables enterprises to leverage Solid State

Drives (SSDs) in their data centers. This will allow customers to access applications and data 400% faster

than traditional storages used, making it the only offering to provide this benefit. The software will also be

the only software that does not require enterprises to switch to a full SSD data center as the software detects

key data to store on the SSD, drastically reducing the cost of incorporating the software into current

infrastructure. This will help the Information Management segment of Symantec to continue to grow and

capture more market share into the future.

Returning Cash to Shareholders

Symantec’s management has remained committed to returning cash to shareholders. Symantec began paying

dividends in June 2013, with a $0.15 dividend per share. In June quarter Symantec paid a $0.15 dividend per

share, with a yield of 2.5%. The company dividend yield has been relatively in-line with the industry, only

outperforming in the last two quarters (Exhibit 20). Cash dividends totaled $104 million and were financed

directly through cash flow. Additionally, Symantec will continue to buy back shares as part of a $1 billion

dollar share repurchase program, of which $533 million remains. The company has been buying shares back

at an average quarterly amount of $125 million, or 6 million shares.

Investment Summary

De-Merging of Core Segments: In an effort to improve shareholder value Symantec is de-merging their

security and information management business. By separating into two companies it will allow for

improved strategic focus, reduced operational complexity, and enhanced flexibility. Operating as separate

companies will allow Symantec to better meet customers’ needs. As a result, the company will see positive

growth through renewed contracts and new customer acquisition. The separation will also allow Symantec

to reduce redundant positions and make doing business with the company more simplistic.

Exceeding Strategic Turnaround Timeline: In 2013 Symantec announced their strategic turnaround plan

to return the company to positive revenue growth and improved operating margins of 30%, with an estimated

completion in FY2015 - 2017. Since then the company has exceeded estimates and reported positive revenue

growth and improved operating margins in Q1 2015, ahead of internal estimates. This trend should continue

into the rest of the year as Symantec tend to have the best two quarters in Q3 and Q4. Thus Symantec is set to

reach 5% revenue growth and 30% operating margins by the end of FY2015.

Industry Growth: Symantec operates in two fast growing segments in the technology industry. The

technology industry as a whole has expected to grow at 6.2% annually for the next two years. The Security

segment is expected to achieve 10% annual growth, while the Information Management segment is expected

SYMC

Industry

01/8/14 Roland George Investment Program

Stetson University Student Research

7

Exhibit 21: Revenue Growth

Exhibit 22: EPS Growth

Exhibit 24: Earnings Growth

Exhibit 23: Earnings Surprise

to grow at 7% annually over the same period. Symantec is poised to capture this growth as they leverage their

market leading product line and improve their strategic focus under their new strategies for growth.

Capitalize on Intelligence Network: In an effort to improve growth in the security segment, Symantec has

begun to leverage their Global Intelligence Network to improve all their product offerings. In 2014 Symantec

incorporated their GIN predictions into Norton Small Business, Norton Security, and MSS-ATP, with

improved threat detection and a money back guarantee if you receive a virus. Symantec’s improved products

have helped drive their 7% revenue growth in enterprise security segment. The consumer segment is

estimated to receive roughly a 5% revenue growth driven by increase subscriptions for Norton Security.

Leverage Mature Market Cash Flow: In an effort to improve profit margin and promote growth,

Symantec management is focusing on leveraging their low growth and high cash flow products lines. This

is accomplished by shifting R&D away from mature markets and into high growth segments such as

enterprise security and services. This will allow Symantec to use the high cash flow of their mature

products to invest in future growth for 2015 and beyond, helping achieve the targeted 5% organic growth.

Meanwhile, spending less R&D in mature markets will grow operating margin for these products, helping

to achieve the targeted 30% operating margin for the company.

Attractive Valuation Indicates a BUY: The various valuations we performed reveal a consensus that

Symantec’s stock is undervalued. Our fair value estimate is around $29.21, which suggests an undervaluation

of the current stock price by 17.68%. Furthermore, Symantec is in the process of de-merging their Security

and Information Management businesses, providing substantial growth opportunity. The easiest way for

individuals to invest in future growth is to buy Symantec stock.

Financial Analysis

Revenue and Earnings

Revenue: Symantec reported record revenue of $1.74 billion in Q1 2015, up 2% year-over-year, and the first

quarter or positive revenue growth since the reorganization of the company’s sales force in 2013. Revenue

growth was driven by a 3% implied billing growth year-over-year. Enterprise subscription grew 7% year-

over-year accounting for 16% of total revenue. Symantec’s consumer product revenue increased by 1.79%

driven primarily by growth of Information Security segment that saw revenue increases 2% year-over-year,

with revenue of $345 million. Information Management revenue was flat year-over-year at $650 million.

Since 2011 Symantec has been growing revenue at an annual rate of 2.55% (Exhibit 21). In fiscal 2014

Symantec delivered revenue of $6.7 billion at the high end of guidance, a year-over-year decline of 3%, as

the company completed and implemented their go-to market changes. In 2014, productivity & protection

segment declined 3 % to $2.87 billion, driven by weakness in endpoint management offset by strength in

mobile and enterprise solutions. The Information Security segment increase 1% to $1.13 billion as there was

continued growth in authentication and data loss prevention. The Information Management segment declined

4% to 2.5 billion due to weakness in Backup Exec ahead of a new release.

In 2015 Symantec was forecasted to achieve 7.19% revenue growth, as their growth strategies begin to affect

earnings. Growth is expected to be driven primarily through their organic growth, with Consumer security

expected to increase 9.4% as Symantec streamlines their product offerings and begins to target the untapped

small business market. Enterprise security is expected to closely follow as a driver of revenue growth with an

expected year-over-year growth of 8.33%, attributed to new service and product offerings. Information

Management is forecasted to achieve 4.42% revenue growth for the year of 2015, primarily attributed to

growth of NetBackup and improved renewal activity.

Earnings: The Software industry has experienced relatively high earnings growth over the past 3 years with

average annual earnings per share growth of 6.35%. However, in the past three years Symantec has been

outpacing the industry with an average annual EPS growth of 8.2% (Exhibit 22).When looking at the last four

quarters Symantec has shown strength in growing EPS with an average quarterly growth of 8.3% showing

improving revenue growth. Additionally, Symantec has developed a reputation for regularly beating earnings

with an average EPS surprise of 3.22% in the last 5 quarters (Exhibit 23). The improving EPS growth is

attributed to record Q1 revenue of $330 million, driven by the company’s strategies of increase operating

margins and improving organic growth.

Earnings for Symantec have also see improving growth, as the company has experienced an average annual

earnings growth of 16.44% since 2010, compared to the industry average of 11.58% (Exhibit 24). For 2014

Symantec reported net profit of $898, an 18.9% increase year-over-year. The trend of high earnings growth

has continued into 2015, with Q1 net profit of $236 million, or a 50.32% increase year-over-year. Looking

forward, I am optimistic in terms of earnings growth as Symantec’s efforts to focus on operating margins and

organic growth have begun gain momentum and begin to positively affect earnings growth. Looking forward,

SYMC

SYMC

SYMC

Industry

SYMC

Industry

Industry

Industry

01/8/14 Roland George Investment Program

Stetson University Student Research

8

Exhibit 25: Operating Margin

Exhibit 26: Profit Margin

Exhibit 27: Gross Margin

Exhibit 28: Return on Equity

Exhibit 29: Return on Assets

2016

Q1 Q2 Q3 Q4 FY 2014 Q1 Q2 Q3 Q4 FY 2015 Q1

Net Sales (Projected)

Consumer Security $524 $518 $517 $504 $2,063 $533 $548 $572 $604 $2,257 $563

Enterprise Security $544 $517 $528 $511 $2,100 $552 $568 $580 $592 $2,292 $596

Information Management $641 $602 $660 $610 $2,513 $650 $654 $658 $662 $2,624 $658

Total Revenue $1,709 $1,637 $1,705 $1,625 $6,676 $1,735 $1,770 $1,810 $1,858 $7,173 $1,817

Cost of Goods Sold $300 $284 $283 $282 $1,149 $309 $289 $281 $260 $1,139 $254

Gross Profit $1,409 $1,353 $1,422 $1,343 $5,527 $1,426 $1,481 $1,529 $1,598 $6,034 $1,563

Operating Expenses $979 $903 $913 $919 $3,714 $999 $1,027 $1,021 $1,026 $4,073 $1,086

Operating Income

Consumer Security $224 $225 $224 $255 $928 $268 $281 $307 $336 $1,192 $293

Enterprise Security $58 $80 $107 $69 $314 $70 $80 $104 $135 $389 $91

Information Management $148 $145 $178 $100 $571 $89 $93 $97 $101 $380 $93

Total Operating Income $430 $450 $509 $424 $1,813 $427 $454 $508 $572 $1,961 $477

Reconciling Items

Stock based compensation $39 $38 $34 $43 $154 $43 $35 $36 $37 $151 $36

Amortization of intangible assets $86 $42 $41 $41 $210 $42 $43 $44 $46 $175 $45

Restructuring and transition $81 $122 $29 $32 $264 $20 $17 $18 $14 $69 $12

Other Expenses $4 -$3 $18 $10 $29 $17 $9 $9 $10 $45 $9

Taxes/Expense $63 $10 $104 $81 $258 $69 $43 $73 $83 $268 $69

Net Profit $157 $241 $283 $217 $898 $236 $307 $328 $382 $1,253 $306

EPS $0.44 $0.50 $0.51 $0.47 $1.92 $0.44 $0.45 $0.48 $0.57 $1.94 $0.46

2014 2015

I am optimistic in terms of earnings growth with FY2015 forecasted to grow earnings 39.71% with annual

earnings of $1.245 billion.

Pro Forma

Based on the assumptions that (1) the company revenue will achieve 5% organic growth by the end of

FY2015, (2) the operating margin will be improve to 30%, (3) acquisitions will account for 1-2% growth, I

estimate the Q2 2015 EPS to be $0.45, beating earnings estimates of $0.44 (Appendix 1D). For the fiscal

year 2015, EPS is expected to be $1.94, a 40% increase from 2014. Keeping with this upward trend, earnings

are expected to grow by an average of 15.54 % per quarter in 2015 and 29.66% year-over-year in Q1 2016.

Following previous sections, for 2014, we attribute 7.44% of EPS growth to revenue growth and 8.1% to

margin expansion.

Profitability

Operating Margin: The operating margin for Symantec has steadily been increasing over the past four years

at an annual rate of 9.57%, while the industry has seen operating margins decrease an average -4.1% annually

(Exhibit 25). In the past four years Symantec's operating margin increased from 15.6% to 24.6%, as the

company targets 30% operating margin by the end of FY2015. The increasing operating margin has been

attributed to increased improved efficiency, lower sales and marketing costs, and improved R&D allocation.

As Symantec continues to pursue their growth strategies the company will remain ahead of the industry

operating margin of 16.6% in 2013. Profit Margin: In 2013 the profit margin for Symantec was 10.9%, which is slightly lower than the industry

average of 13.13%. This is due in part to Symantec information management segment that produces a few

physical products that provide much lower operating margins. However, as the company focuses on

improved operating margin it will improve profit margin in the years to come. Additionally Symantec has

shown more stable profit margin compared to the industry, which has become negative in 2014 (Exhibit 26).

Gross Margin: Since 2010, gross margin in the technology industry have been relatively flat growing an

average -0.34% year-over-year. Although gross margins have been on decline for the industry Symantec has

been growing their gross margins and 0.62% annually. As of 2014 Symantec had a gross margin of 83%,

much higher than the industry average of 77.2% (Exhibit 27). As Symantec streamlines their product

offerings and focuses R&D on key growth opportunities their gross margins should be positively impacted.

Return on Equity: The current return on equity for Symantec is 15.11%, which is above the industry

average of -8.54% (Exhibit 28). Since 2011, Symantec's return on equity has been growing at an average rate

of 8.5%, outpacing the industry average growth of -3.88%. The growth of Symantec's ROE is expected to

continue to improve as the company recognizes the benefits of the strategic changes that have made in the

past year, and continue to leverage R&D into their high growth segments.

Return on Assets: In 2013 Symantec had a return on assets of 7.3%, which is slightly lower than the

industry average of 7.68. In 2014 Symantec is estimated to outperform the industry with an ROA of 8.2%,

compared to the industry average of -3.46% (Exhibit 29). However, over the past 4 years Symantec has been

able to grow their ROA at an average rate 13.08%, compared to the industries negative growth of 0.99%.

This shows that Symantec has again been able to leverage their product line and brand name to improve their

return when compared with the industry.

SYMC

SYMC

SYMC

SYMC

SYMC

Industry

Industry

Industry

Industry

Industry

01/8/14 Roland George Investment Program

Stetson University Student Research

9

Exhibit 30: Free Cash Flow Growth

Cash Flow

Total Net Cash Flow: Since the economic recession Symantec has experienced operating cash flow decrease

at an annual rate of -3.07%, due primarily to a decrease of the amount of depreciation accounted for each

year. When not accounting for the change in depreciation levels Symantec was able to grow operating cash

flow at an average 5.45% annually. Cash flow from financing activities for 2013 was $-1.7 billion, which was

negatively impacted by the enactment of the company’s first dividend payout, along with an enormous $1.18

billion long-term debt repayment. Cash flow from investment activities was negative $583 million for 2013,

as Symantec has been spending an average $278 million on purchases of property and equipment. Although

the company has been experiencing a period of negative cash flow growth, in FY2015 the company is

estimated to have positive year-over-year growth. This will be driven by the improved revenue and lower

costs associated with restructuring the company for the new growth strategies.

Free Cash Flow: Symantec had free cash flow of $201 million in Q1 2015, down 18.77% year-over-year

slightly above the industry decrease of -34.81% (Exhibit 30). The drastic decrease in year-over-year free cash

flow was driven primarily from a one-time tax deposit of $104 million, related to the previous year IRS audit.

However, the company offset some of the one-time expense with improved collections driven by the new

sales team structure. This positions the company to experience substantial free cash flow growth in the

following year, as they have fewer expenses and higher net income.

Debt

Debt to Equity: Currently, Symantec has $2.1 billion in long-term debt outstanding. Compared with the Peer

Group, Symantec carries a significantly higher amount of long-term debt, with and peer average of only $371

million. In 2013, Symantec’s debt to equity ratio was 0.56, while the Peer Group was 0.43. This shows that

although Symantec has a much larger amount of debt the company also is competing against much smaller

companies. Additionally, the majority of the debt issued was to fund the Veritas merger, which the company

is now de-merging from. As the de-merger completes in December it will be likely that Symantec will be

able to lower their debt level, while maintaining their investment grade rating.

Debt to EBITDA: More importantly, it is informative to look at Symantec’s debt-to-EBITDA ratio because

it shows the amount of time it will take the company to pay off its debt. Symantec’s current debt to EBITDA

is 1.08, compared to the industry average of 2.15. The debt to EBITDA suggests that the company is less

capable of paying its debts compared to their peers.

Solvency: Symantec’s first term loan facility of $600 million will come due in 2017. Symantec historically

has relied on free cash flow to satisfy liquidity needs. In Q4 2014 Symantec had cash equivalents and short-

term investments of $4 billion. Additionally Symantec has an unused revolving credit facility of $1 billion,

amended to extend into 2017. This provides Symantec with a liquidity position of roughly $5 billion, which

is plenty of cash to meet any loan facilities.

Valuations

In this section, I estimate the fair values of Symantec’s stock. It should be noted that all input data were

derived from historical company data and pro forma estimates.

Growth Duration Model: The Growth Duration valuation, a relative P/E model, is often used to compare a

company with significant growth potential to its stable industry. It is a relevant model for Symantec because

they have experienced a higher volatility in growth compared with the average firm in the Industry Peer

Group. Using earnings growth rates between 5% and 11% in the simulation, the median fair value for

Symantec is estimated to be $31.11, undervalued by 25.34% (Appendix 3).

Franchise Value Model: The Franchise valuation is often used when dealing with companies that are able to

produce significant franchise value, i.e. repeating its business model at a higher return on equity. This model

distinguishes between a company’s current return on equity and the return on equity that can be derived from

future opportunities. The underlying assumption for Symantec’s is that it will be able to improve its return

on equity by leveraging their current technological know-how, reputation, and existing intangibles. Using its

current return on equity of 15.11% and our expected future return on equity of 17.24%, I determined the

median fair value for Symantec to be $29.52, undervalued by 18.92% (Appendix 4).

Residual Income Model: The residual income model uses a combination of a company’s current book value

per share and expected future residual income. This is a relevant model for Symantec because they have

negative historical cash flow growth in the past and will likely not pay dividends in their information

management business. The median fair value for Symantec is $27, which shows that Symantec is

undervalued by 8.79% (Appendix 5).

SYMC

Industry

01/8/14 Roland George Investment Program

Stetson University Student Research

10

Average Fair Value: The summary estimates a fair value of $29.21, undervalued by 17.68%, which is

derived from the combined simulation results. This information recommends a strong position to BUY

Symantec.

Investment Risk

Inherent Risk in De-Merger: With Symantec's announcement of a planned demerger there is inherent risk

involved. First by demerging Security and Information Management Symantec faces potential changes in

taxation, which could make the demerger for the company uneconomical. Demergers also raise risk of

operational difficulties related to staffing and more importantly the potential loss of synergies. The last major

risk associated with a de-merger is the cost associated with the process. Costs of de-mergers can be separated

into one-time cost and ongoing cost. Ongoing costs associated with de-merger are essentially the additional

costs associated with the loss in synergies.

Potential Loss of Sales and Distribution Channels: Symantec sells products to customers around the world

through multi-tiered sales and distribution networks. Sales through each different channel involve distinct

risks. Direct Sales is a significant portion of enterprise product revenue, however, tends to consist of longer

sales cycles and difficulties in hiring and training new employees. Indirect Sales Channels is a significant

portion of revenue especially in end-user products. This distribution method provides Symantec with little

control over product delivery, minimum sale requirements, and preventing distribution of competing

products. Additionally, with the consolidation of the electronics retailer market, Symantec has seen a

decrease in their negotiating power. Finally, the OEM Sales channels raises the risk that revenues from this

segment could decrease if demand for OEM products decrease as well. Additionally, OEM agreements may

require Symantec to engage in additional product development, which could become costly for the company.

Dependency on Non-Contractual Revenue: A large portion of Symantec’s revenue is derived from

arrangements for maintenance, subscriptions, managed security services, and SaaS offerings, yet existing

customers have no contractual obligation to purchase additional solutions after the initial subscription or

contract time. Additionally, given the short operating history under these revenue sources it is difficult to

accurately predict customer’s renewal rates. Symantec’s customers’ renewal rates may decline or fluctuate as

a result of a number of factors, including the level of their satisfaction with the company’s customer support,

customer budgets and the pricing of the company’s solutions compared with the solutions offered by

competitors, any of which may cause the company’s revenue to grow more slowly than expected.

Accordingly, the company must invest significant time and resources in providing ongoing value to their

customers, or risk losing renewals.

Additional Acquisition Equals Additional Risk: Since in the past acquisitions has been a major source of

growth for Symantec a number of risks could arise from future acquisitions of other businesses, business

units and technologies. Specific risks associated with acquisitions include; complexity in integrating the

acquired businesses, diversion of management attention, assumption of liabilities, and potential dilution of

stock ownership. In the worst situation the acquired business would be unsuccessfully integrated leading to

additional unseen costs.

Exposure to International Risk: Symantec derives a substantial portion of revenues from customers located

outside of the U.S. and has multiple operations outside of the U.S. As the company continues to target

expansion into international regions they increase the risk associated with international operations. The risks

associated with international operations for Symantec include loss of intellectual property due to less

protective laws in foreign countries. International operations also increase the cost for the company as they

must provide support and products in multiple languages. However, the largest risk associated with

international operations is currency exchange fluctuations, which could decrease profits or increase costs of

doing business.

11

Table of Contents

Appendix 1A: Income Statement 12

Appendix 1B: Balance Sheet 13

Appendix 1C: Statement of Cash Flow 14

Appendix 1D: Income Statement Pro Forma 15

Appendix 2: Capital Asset Pricing Model 16

Appendix 3: Residual Income Model 17

Appendix 4: Growth Duration Model 18

Appendix 5: Franchise Value Model 19

Appendix 6: Technology Revenue Growth vs GDP Growth 20

Appendix 7: Software Revenue vs GDP Growth 21

Appendix 8: SYMC Revenue Growth vs. GDP Growth 22

12

Appendix 1A: Historic Income Statements Source: Yahoo Finance

4-Jul-14 28-Mar-14 27-Dec-13 27-Sep-13

1,735,000 1,625,000 1,705,000 1,637,000

309,000 282,000 283,000 284,000

1,426,000 1,343,000 1,422,000 1,353,000

Research Development 308,000 277,000 252,000 247,000

Selling General and Administrative 747,000 699,000 705,000 705,000

Non Recurring 20,000 33,000 32,000 124,000

Others 29,000 28,000 28,000 29,000

Total Operating Expenses 1,104,000 1,037,000 1,017,000 1,105,000

322,000 306,000 405,000 248,000

Total Other Income/Expenses Net 4,000 11,000 2,000 23,000

Earnings Before Interest And Taxes 326,000 317,000 407,000 271,000

Interest Expense 21,000 19,000 20,000 20,000

Income Before Tax 305,000 298,000 387,000 251,000

Income Tax Expense 69,000 81,000 104,000 10,000

Minority Interest - - - -

Net Income From Continuing Ops 236,000 217,000 283,000 241,000

Discontinued Operations - - - -

Extraordinary Items - - - -

Effect Of Accounting Changes - - - -

Other Items - - - -

236,000 217,000 283,000 241,000

- - - -

236,000 217,000 283,000 241,000

Net Income

Preferred Stock And Other Adjustments

Net Income Applicable To Common Shares

Operating Income or Loss

Income from Continuing Operations

Period EndingTotal Revenue

Cost of Revenue

Gross Profit

Operating Expenses

Non-recurring Events

13

Appendix 1B: Historic Balance Sheets Source: Yahoo Finance

4-Jul-14 28-Mar-14 27-Dec-13 27-Sep-13

Cash And Cash Equivalents 3,067,000 3,707,000 3,813,000 3,727,000

Short Term Investments 982,000 377,000 77,000 105,000

Net Receivables 834,000 1,149,000 1,062,000 747,000

Inventory 11,000 14,000 13,000 16,000

Other Current Assets 394,000 405,000 351,000 375,000

5,288,000 5,652,000 5,316,000 4,970,000

- - - -

1,140,000 1,116,000 1,110,000 1,091,000

5,871,000 5,858,000 5,856,000 5,859,000

735,000 768,000 809,000 852,000

- - - -

112,000 124,000 138,000 114,000

18,000 21,000 29,000 28,000

13,164,000 13,539,000 13,258,000 12,914,000

Accounts Payable 563,000 647,000 644,000 561,000

Short/Current Long Term Debt - - - -

Other Current Liabilities 3,416,000 3,659,000 3,505,000 3,346,000

3,979,000 4,306,000 4,149,000 3,907,000

2,095,000 2,095,000 2,094,000 2,094,000

218,000 335,000 316,000 284,000

1,034,000 1,006,000 941,000 972,000

- - - -

- - - -

7,326,000 7,742,000 7,500,000 7,257,000

- - - -

- - - -

- - - -

7,000 7,000 7,000 7,000

-912,000 -1,148,000 -1,316,000 -1,599,000

- - - -

6,547,000 6,744,000 6,885,000 7,066,000

196,000 194,000 182,000 183,000

5,838,000 5,797,000 5,758,000 5,657,000

-768,000 -829,000 -907,000 -1,054,000

Total Stockholder Equity

Net Tangible Assets

Preferred Stock

Common Stock

Retained Earnings

Treasury Stock

Capital Surplus

Other Stockholder Equity

Total Liabilities

Stockholders' Equity

Misc Stocks Options Warrants

Redeemable Preferred Stock

Total Current Liabilities

Long Term Debt

Other Liabilities

Deferred Long Term Liability Charges

Minority Interest

Negative Goodwill

Total Assets

Liabilities

Current Liabilities

Property Plant and Equipment

Goodwill

Intangible Assets

Accumulated Amortization

Other Assets

Deferred Long Term Asset Charges

Period Ending

Assets

Current Assets

Total Current Assets

Long Term Investments

14

Appendix 1C: Historic Statement of Cash Flows Source: Yahoo Finance

4-Jul-14 28-Mar-14 27-Dec-13 27-Sep-13236,000 217,000 283,000 241,000

117,000 115,000 111,000 111,000

61,000 79,000 -11,000 39,000

308,000 -115,000 -320,000 180,000

-446,000 206,000 257,000 -437,000

3,000 -1,000 3,000 2,000

14,000 -52,000 6,000 55,000

293,000 449,000 329,000 191,000

-92,000 -77,000 -65,000 -57,000

-613,000 -298,000 27,000 -67,000

-19,000 - - -17,000

-724,000 -375,000 -38,000 -141,000

-104,000 -104,000 -104,000 -105,000

-102,000 -74,000 -102,000 -19,000

-18,000 - - -

5,000 -13,000 -2,000 -5,000

-216,000 -187,000 -208,000 -125,000

7,000 7,000 3,000 53,000

-640,000 -106,000 86,000 -22,000

Other Cash Flows from Financing Activities

Total Cash Flows From Financing Activities

Effect Of Exchange Rate Changes

Change In Cash and Cash Equivalents

Total Cash Flows From Investing Activities

Financing Activities, Cash Flows Provided By or Used In

Dividends Paid

Sale Purchase of Stock

Net Borrowings

Investing Activities, Cash Flows Provided By or Used In

Capital Expenditures

Investments

Other Cash flows from Investing Activities

Changes In Accounts Receivables

Changes In Liabilities

Changes In Inventories

Changes In Other Operating Activities

Total Cash Flow From Operating Activities

Period EndingNet Income

Operating Activities, Cash Flows Provided By or Used In

Depreciation

Adjustments To Net Income

15

Appendix 1D: Pro Forma Income Statement Source: Personal Estimates

16

Appendix 2: Capital Asset Pricing Model Source: Reuters, Internal Student Estimates

( )

Rf Risk Free Rate 2.28%

Rm Market Return 7%

Β Beta 1.03

Required Rate of Return: 7.16%

Appendix 3: Residual Income Model Source: Reuters, Internal Student Estimates

BPS Current book value per share $8.34

k Current required rate of return 7.16%

G Current BPS growth rate 3.6%

ROE ROE Symantec 2014 15.11%

P* Fair value of Symantec using BPS $27.00

Undervalued by: 8.79%

18

Appendix 4: Growth Duration Model Source: Reuters, Internal Student Estimates

System Software Gemalto

P/E 16.3 P/E 16.15

Estimated Growth Next Year 13.00% Estimated Growth Next Year 7.29%

Dividend Yield 1.50% Dividend Yield 0.62%

SYMC Est. EPS Fiscal $1.93 SYMC Est. EPS Fiscal $1.93

Pessimistic Scenario Pessimistic Scenario

SYMC Earnings Growth 5.78% SYMC Earnings Growth 5.78%

P/E SYMC 1 +.0578 + 0.025 P/E SYMC 1 +.0578 + 0.025

P/E Sector 1 + .13 + 0.015 P/E Gemalto 1 + .0729 + 0.0062

SYMC Fair P/E = (0.9457)(16.3) = 15.4147 SYMC Fair P/E = (1.0034)(16.15) = 16.2056

Fair Value = (15.4147)(1.93) = $29.75 Fair Value = (16.2056)(1.93) = $31.28

Anticipated Scenario Anticipated Scenario

SYMC Earnings Growth 7.44% SYMC Earnings Growth 7.44%

P/E SYMC 1 + .0744 + 0.025 P/E SYMC 1 + .0744 + 0.025

P/E Sector 1 + .13 + .015 P/E Gemalto 1 + .0729 + 0.0062

SYMC Fair P/E = (.9602)(16.3) = 15.6505 SYMC Fair P/E = (1.0188)(16.15) = 16.4535

Fair Value = (15.6505)(1.93) = $30.21 Fair Value = (16.4535)(1.93) = $31.76

Optimistic Scenario Optimistic Scenario

SYMC Earnings Growth 10.07% SYMC Earnings Growth 10.07%

P/E SYMC 1 + .1007 + 0.025 P/E SYMC 1 + .1007 + 0.025

P/E Sector 1 + .13 + .015 P/E Gemalto 1 + .0729 + 0.0062

SYMC Fair P/E = (0.9832)(16.3) = 16.0257 SYMC Fair P/E = (1.0432)(16.15) = 16.8479

Fair Value = (16.0257)(1.93) = $30.93 Fair Value = (16.8479)(1.93) = $32.52

Average Fair Price vs. Sector = $30.33 Average Fair Price vs. Sector = $31.89

Average Fair Price for Symantec Corporation $30.33 Average Fair Price for Symantec Corporation $31.89

Undervalued by: 22.21% Undervalued by: 28.48%

Competitor

= = 0.9457 = = 1.0034

= = 0.9832 = = 1.0432

= = 0.9602 = = 1.0188

Sector

Fair Value: $31.11

Undervalued By: 25.34%

19

Appendix 5: Franchise Value Mode Source: Bloomberg, Internal Student Estimates

(

) (

)

g Growth of book value per share 3.6% k Required rate of return 7.16% BPS Current book value per share $8.34 ROE Current return on equity 15.11% R New business return on equity 17.24%

P* Fair value for the stock $29.52

Undervalued By: 18.92%

20

Appendix 6: Technology Revenue Growth vs GDP Growth Source: Internal Student Estimates

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.934225047

R Square 0.872776438

Adjusted R Square 0.847331726

Standard Error 0.009199663

Observations 7

ANOVA

df SS MS F Significance F

Regression 1 0.002903015 0.002903015 34.30089628 0.002056496

Residual 5 0.000423169 8.46338E-05

Total 6 0.003326184

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept 0.001769885 0.005686334 0.311252345 0.768167591 -0.012847301 0.01638707 -0.012847301 0.01638707

X Variable 1 0.555219793 0.094800844 5.856696704 0.002056496 0.311526464 0.798913122 0.311526464 0.798913122

21

Appendix 7: Software Revenue Growth vs GDP Growth Source: Internal Student Estimates

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.892937434

R Square 0.79733726

Adjusted R Square 0.756804713

Standard Error 0.018532711

Observations 7

ANOVA

df SS MS F Significance F

Regression 1 0.006756411 0.006756411 19.6715307 0.006794745

Residual 5 0.001717307 0.000343461

Total 6 0.008473718

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept -0.022999729 0.016446263 -1.398477517 0.220832821 -0.065276193 0.019276736 -0.065276193 0.019276736

X Variable 1 0.997152905 0.224824006 4.435259936 0.006794745 0.4192244 1.575081411 0.4192244 1.575081411

22

Appendix 8: SYMC Revenue Growth vs. GDP Growth Source: Internal Student Estimates

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.282024473

R Square 0.079537803

Adjusted R Square 0.037698613

Standard Error 0.019217537

Observations 24

ANOVA

df SS MS F Significance F

Regression 1 0.000702079 0.000702079 1.901035895 0.181821427

Residual 22 0.008124902 0.000369314

Total 23 0.008826981

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept 0.041039529 0.00561152 7.313442432 2.53237E-07 0.029401949 0.05267711 0.029401949 0.05267711

X Variable 1 0.022838181 0.016564043 1.378780583 0.181821427 -0.011513542 0.057189905 -0.011513542 0.057189905

23

Sources:

Reuters

Baseline

Bloomberg

Morningstar

Yahoo Finance

Google Finance

Symantec 10-Q

Symantec 10-K

Symantec Announcements

Symantec Transcripts

Symantec Conference Calls

Disclosures:

Ownership and material conflicts of interest: The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company.

The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might

bias the content or publication of this report.

Receipt of compensation: Compensation of the author(s) of this report is not based on investment banking revenue.

Position as a officer or director: The author(s), or a member of their household, does not serve as an officer, director or advisory board member of the subject company.

Market making:

The author(s) does not act as a market maker in the subject company’s securities.

Disclaimer: The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s)

to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute

investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by any indi vidual affiliated with CFA Society of Orlando, CFA Institute or the CFA Institute Research Challenge with

regard to this company’s stock.