Switzerland Tax Guide - PKF

17

Switzerland Tax Guide 2013

Transcript of Switzerland Tax Guide - PKF

SwitzerlandTax Guide

2013

PKF Worldwide Tax Guide 2013 I

Fore

wor

d

foreword

A country’s tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed?

Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. This handy reference guide provides clients and professional practitioners with comprehensive tax and business information for over 90 countries throughout the world.

As you will appreciate, the production of the WWTG is a huge team effort and I would like to thank all tax experts within PFK member firms who gave up their time to contribute the vital information on their country’s taxes that forms the heart of this publication.

I hope that the combination of the WWTG and assistance from your local PKF member firm will provide you with the advice you need to make the right decisions for your international business.

Richard SackinChairman, PKF International Tax CommitteeEisner Amper LLP [email protected]

PKF Worldwide Tax Guide 2013II

Disclaimer

important disclaimer

This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication.This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication.

The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication.

Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances.

PKF International is a network of legally independent member firms administered by PKF International Limited (PKFI). Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions on the part of any individual member firm or firms.

PKF Worldwide Tax Guide 2013 III

Pref

ace

preface

The PKF Worldwide Tax Guide 2013 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world’s most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 1 January 2013, while also noting imminent changes where necessary.

On a country-by-country basis, each summary addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country’s personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments.

While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice.

In addition to the printed version of the WWTG, individual country taxation guides are available in PDF format which can be downloaded from the PKF website at www.pkf.com

PKF INTERNATIONAL LIMITEDMAY 2013

©PKF INTERNATIONAL LIMITEDALL RIGHTS RESERVEDUSE APPROVED WITH ATTRIBUTION

PKF Worldwide Tax Guide 2013IV

Introduction

about pKf international limited

PKF International Limited (PKFI) administers the PKF network of legally independent member firms. There are around 300 member firms and correspondents in 440 locations in around 125 countries providing accounting and business advisory services. PKFI member firms employ around 2,270 partners and more than 22,000 staff.PKFI is the 11th largest global accountancy network and its member firms have $2.68 billion aggregate fee income (year end June 2012). The network is a member of the Forum of Firms, an organisation dedicated to consistent and high quality standards of financial reporting and auditing practices worldwide.

Services provided by member firms include:

Assurance & AdvisoryInsolvency – Corporate & PersonalFinancial Planning/Wealth managementTaxationCorporate FinanceForensic AccountingManagement ConsultancyHotel ConsultancyIT Consultancy

PKF member firms are organised into five geographical regions covering Africa; Latin America; Asia Pacific; Europe, the Middle East & India (EMEI); and North America & the Caribbean. Each region elects representatives to the board of PKF International Limited which administers the network. While the member firms remain separate and independent, international tax, corporate finance, professional standards, audit, hotel consultancy and business development committees work together to improve quality standards, develop initiatives and share knowledge and best practice cross the network.

Please visit www.pkf.com for more information.

PKF Worldwide Tax Guide 2013 V

Stru

ctur

e

structure of country descriptions

a. taXes payable

FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER TAXES

b. determination of taXable income

CAPITAL ALLOWANCES DEPRECIATION STOCK/INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS LOSSES FOREIGN SOURCED INCOME INCENTIVES

c. foreiGn taX relief

d. corporate Groups

e. related party transactions

f. witHHoldinG taX

G. eXcHanGe control

H. personal taX

i. treaty and non-treaty witHHoldinG taX rates

PKF Worldwide Tax Guide 2013VI

Time Zones

AAlgeria . . . . . . . . . . . . . . . . . . . .1 pmAngola . . . . . . . . . . . . . . . . . . . .1 pmArgentina . . . . . . . . . . . . . . . . . .9 amAustralia - Melbourne . . . . . . . . . . . . .10 pm Sydney . . . . . . . . . . . . . . .10 pm Adelaide . . . . . . . . . . . . 9.30 pm Perth . . . . . . . . . . . . . . . . . .8 pmAustria . . . . . . . . . . . . . . . . . . . .1 pm

BBahamas . . . . . . . . . . . . . . . . . . .7 amBahrain . . . . . . . . . . . . . . . . . . . .3 pmBelgium . . . . . . . . . . . . . . . . . . . .1 pmBelize . . . . . . . . . . . . . . . . . . . . .6 amBermuda . . . . . . . . . . . . . . . . . . .8 amBrazil. . . . . . . . . . . . . . . . . . . . . .7 amBritish Virgin Islands . . . . . . . . . . .8 am

CCanada - Toronto . . . . . . . . . . . . . . . .7 am Winnipeg . . . . . . . . . . . . . . .6 am Calgary . . . . . . . . . . . . . . . .5 am Vancouver . . . . . . . . . . . . . .4 amCayman Islands . . . . . . . . . . . . . .7 amChile . . . . . . . . . . . . . . . . . . . . . .8 amChina - Beijing . . . . . . . . . . . . . .10 pmColombia . . . . . . . . . . . . . . . . . . .7 amCyprus . . . . . . . . . . . . . . . . . . . .2 pmCzech Republic . . . . . . . . . . . . . .1 pm

DDenmark . . . . . . . . . . . . . . . . . . .1 pmDominican Republic . . . . . . . . . . .7 am

EEcuador . . . . . . . . . . . . . . . . . . . .7 amEgypt . . . . . . . . . . . . . . . . . . . . .2 pmEl Salvador . . . . . . . . . . . . . . . . .6 amEstonia . . . . . . . . . . . . . . . . . . . .2 pm

FFiji . . . . . . . . . . . . . . . . .12 midnightFinland . . . . . . . . . . . . . . . . . . . .2 pmFrance. . . . . . . . . . . . . . . . . . . . .1 pm

GGambia (The) . . . . . . . . . . . . . 12 noonGermany . . . . . . . . . . . . . . . . . . .1 pmGhana . . . . . . . . . . . . . . . . . . 12 noonGreece . . . . . . . . . . . . . . . . . . . .2 pmGrenada . . . . . . . . . . . . . . . . . . .8 amGuatemala . . . . . . . . . . . . . . . . . .6 am

Guernsey . . . . . . . . . . . . . . . . 12 noonGuyana . . . . . . . . . . . . . . . . . . . .7 am

HHong Kong . . . . . . . . . . . . . . . . .8 pmHungary . . . . . . . . . . . . . . . . . . .1 pm

IIndia . . . . . . . . . . . . . . . . . . . 5.30 pmIndonesia. . . . . . . . . . . . . . . . . . .7 pmIreland . . . . . . . . . . . . . . . . . . 12 noonIsle of Man . . . . . . . . . . . . . . 12 noonIsrael . . . . . . . . . . . . . . . . . . . . . .2 pmItaly . . . . . . . . . . . . . . . . . . . . . .1 pm

JJamaica . . . . . . . . . . . . . . . . . . .7 amJapan . . . . . . . . . . . . . . . . . . . . .9 pmJordan . . . . . . . . . . . . . . . . . . . .2 pm

KKenya . . . . . . . . . . . . . . . . . . . . .3 pm

LLatvia . . . . . . . . . . . . . . . . . . . . .2 pmLebanon . . . . . . . . . . . . . . . . . . .2 pmLuxembourg . . . . . . . . . . . . . . . .1 pm

MMalaysia . . . . . . . . . . . . . . . . . . .8 pmMalta . . . . . . . . . . . . . . . . . . . . .1 pmMexico . . . . . . . . . . . . . . . . . . . .6 amMorocco . . . . . . . . . . . . . . . . 12 noon

NNamibia. . . . . . . . . . . . . . . . . . . .2 pmNetherlands (The) . . . . . . . . . . . . .1 pmNew Zealand . . . . . . . . . . .12 midnightNigeria . . . . . . . . . . . . . . . . . . . .1 pmNorway . . . . . . . . . . . . . . . . . . . .1 pm

OOman . . . . . . . . . . . . . . . . . . . . .4 pm

PPanama. . . . . . . . . . . . . . . . . . . .7 amPapua New Guinea. . . . . . . . . . .10 pmPeru . . . . . . . . . . . . . . . . . . . . . .7 amPhilippines . . . . . . . . . . . . . . . . . .8 pmPoland. . . . . . . . . . . . . . . . . . . . .1 pmPortugal . . . . . . . . . . . . . . . . . . .1 pmQQatar. . . . . . . . . . . . . . . . . . . . . .8 am

RRomania . . . . . . . . . . . . . . . . . . .2 pm

international time Zones

AT 12 NOON, GREENwICH MEAN TIME, THE STANDARD TIME ELSEwHERE IS:

PKF Worldwide Tax Guide 2013 VII

Tim

e Zo

nes

Russia - Moscow . . . . . . . . . . . . . . .3 pm St Petersburg . . . . . . . . . . . .3 pm

SSingapore . . . . . . . . . . . . . . . . . .7 pmSlovak Republic . . . . . . . . . . . . . .1 pmSlovenia . . . . . . . . . . . . . . . . . . .1 pmSouth Africa . . . . . . . . . . . . . . . . .2 pmSpain . . . . . . . . . . . . . . . . . . . . .1 pmSweden . . . . . . . . . . . . . . . . . . . .1 pmSwitzerland . . . . . . . . . . . . . . . . .1 pm

TTaiwan . . . . . . . . . . . . . . . . . . . .8 pmThailand . . . . . . . . . . . . . . . . . . .8 pmTunisia . . . . . . . . . . . . . . . . . 12 noonTurkey . . . . . . . . . . . . . . . . . . . . .2 pmTurks and Caicos Islands . . . . . . .7 am

UUganda . . . . . . . . . . . . . . . . . . . .3 pmUkraine . . . . . . . . . . . . . . . . . . . .2 pmUnited Arab Emirates . . . . . . . . . .4 pmUnited Kingdom . . . . . . .(GMT) 12 noonUnited States of America - New York City . . . . . . . . . . . .7 am Washington, D.C. . . . . . . . . .7 am Chicago . . . . . . . . . . . . . . . .6 am Houston . . . . . . . . . . . . . . . .6 am Denver . . . . . . . . . . . . . . . .5 am Los Angeles . . . . . . . . . . . . .4 am San Francisco . . . . . . . . . . .4 amUruguay . . . . . . . . . . . . . . . . . . .9 am

VVenezuela . . . . . . . . . . . . . . . . . .8 am

ZZimbabwe . . . . . . . . . . . . . . . . . .2 pm

PKF Worldwide Tax Guide 2013 1

switZerland

Currency: Swiss Francs Dial Code To: 41 Dial Code Out: 00 (CHF)

Member Firm:City: Name: Contact Information:Zurich Daniel Carotta 41 44 285 75 00 [email protected]

Zug Daniel Carotta 41 41 711 86 85 [email protected]

Geneva Jean-Claude Roder 41 22 301 54 40 [email protected]

Lugano Claudio Massa Cortesi 41 91 911 11 11 [email protected]

a. taXes payable

FEDERAL AND CANTONAL TAxES AND LEVIESTaxes are governed in Switzerland by federal law and 26 different cantonal tax laws. The cantonal tax laws were harmonised with effect from 1993. Tax declaration procedures and the determination of the taxable income in the various cantons are similar and in line with the federal law. However, the cantons do set their own tax rates. The presence of different tax legislation means that the fiscal burden on a Swiss company depends not only on the size of its income and assets but, to a considerable degree, also on the location of its registered office, its business objects and the nature of its operations. Taxation may vary significantly from one canton to another. In general, the cantonal laws are flexible and include tax privileges for special purpose companies e.g. holding companies.

CORPORATE TAxCorporate income tax is payable by Swiss resident companies on corporate net profit (i.e. on the profit after taxes). Exceptions to this rule may be found in some cantons where a special tax on capital gains realised on the sale of immovable property may be levied. Income of Swiss resident companies from business operations, permanent establishments and immovable property situated abroad is exempt from income tax but included in calculating progressive corporate income tax rates.

Each resident taxpayer has to file an annual tax return. As a rule, non-resident taxpayers have to file tax returns only if they maintain a permanent establishment or own immovable property in Switzerland including gains on the sale of such property and on income from debts secured by real estate situated in Switzerland.

Cantonal income tax rates are predominantly flat rates. Some cantons use graduated rates. The federal income tax is 8.5% (statutory tax rate applicable on taxable income after taxes, effective tax rate is 7.83%).

Effective ordinary corporate tax rates on income vary significantly from one canton to another (from approximately 12% up to a maximum of approximately 24% in 2012.

An annual capital tax is due at the cantonal and communal level on taxable capital which is usually at least the value of paid in share capital. The effective ordinary capital tax rates vary from 0.01% to 0.52%depending on the canton of residence.Reduced rates are usually applicable for special purpose companies.

There are a number of special purpose companies in Switzerland, i.e. domiciliary and holding companies.

Domiciliary companies only have administrative activities in Switzerland and are exclusively engaged in international business. Companies qualifying for domiciliary status are completely exempt from cantonal tax on dividend income and on capital gains from qualifying participation. Other Swiss-sourced income is taxed at ordinary income tax rates whereas profits from trading outside are usually also subject to tax at reduced rates. Swiss federal tax does not provide for any particular relief for domiciliary companies.

Holding companies are exempt from cantonal and communal corporate income tax and are often also subject to capital tax at reduced rates. Holding companies may own real estate in Switzerland. However, as an exception, any income or capital gains generated from such real estate is subject to ordinary taxation. Federal income tax is levied at ordinary corporate income tax rates.

Switzerland

PKF Worldwide Tax Guide 20132

CAPITAL GAINS TAxCapital gains on real estate for direct federal tax and several cantonal tax purposes are aggregated with and taxed as part of ordinary income. In other cantons, recaptured depreciation is taxed with ordinary income, while the realised increase in value is subject to a special real estate gains tax.

Capital gains realised on the sale of investments are (partially) tax exempt, provided:(1) the sales price exceeds the (historical) acquisition costs of the investment(2) the securities sold amount to at least 10% of the sold company’s share capital

or entitle the purchaser to at least 10% of the profit or reserves of the sold company

(3) the investment was held for a period of at least one year.

BRANCH PROFITS TAxForeign branch income of a Swiss corporation is exempt from Swiss taxation. Swiss branches of foreign companies are assessed on the profit and capital attributable to the branch. Branches of foreign companies are treated for income tax purposes basically in the same way as those of local corporations. Some cantons apply special rules to Swiss finance branches of foreign companies. The finance branches are subject to reduced income tax rates (a reduced tax basis applies due to special deemed interest deductions) and usually also reduced annual capital tax rates.

VALUE ADDED TAx (VAT)VAT is charged on the domestic delivery of goods and rendering of services and a tax on the importation of goods and services into Switzerland. The VAT rate is usually 8%. Special lower rates (2.5% or 3.8%) apply for various services and goods. In addition, various exemptions exist.

LOCAL TAxESThe municipalities levy income taxes, mostly in the form of annually determined surcharges on the cantonal taxes. The tax rates may differ from one community to another.

OTHER TAxESThere are no taxes on income other than the federal, cantonal and communal taxes as mentioned above. In many cantons the churches also levy an income tax, generally based on a percentage of cantonal taxes.

SOCIAL SECURITyCompulsory old age and survivors’ insurance / unemployment insurance / children allowance / on gross salaries are payable at 12.5% (6.25% payable by the employer and employee respectively). Contributions to compulsory pension plans vary in accordance with the benefits covered and are usually shared by employer and employee. The employer generally has to bear at least half. Health insurance has to be organised and paid on a private basis.

ISSUANCE STAMP DUTy TAxThe issuance and increase of the nominal capital of the following securities are generally subject to issuance stamp duty tax:

Rate (%)

Shares of Swiss corporations 1*

Quotas of Swiss private limited companies 1*

Shares in Swiss co-operative societies 1*

* Nil % up to a paid-in capital of CHF 1,000,000.

Further, capital contributions made by shareholders and credited to reserves (capital surplus) are subject to 1% issuances stamp duty tax.

Since 1 March 2012 issuance stamp duty tax is no longer due on the issuance of debentures and money market papers.

SECURITIES TRANSFER STAMP DUTy TAxThe transfer of taxable deeds (securities, debentures) is generally subject to securities transfer stamp duty tax if a Swiss securities dealer is involved. The tax rate is 0.15% for Swiss taxable deeds and 0.3% for foreign taxable deeds. Various exemptions exist.

Except from Swiss banks and brokers, capital companies with taxable deeds of more than CHF 10 million in their balance sheet qualify as a Swiss securities dealer with regard to stamp duty law.

Switzerland

PKF Worldwide Tax Guide 2013 3

b. determination of taXable income

The starting point for determining taxable income of corporate entities is the net income reported as per the statutory accounts. This means all types of income, including capital gains, are part of the taxable income. The reported profit may be adjusted for tax purposes by adding back, e.g. expenses that are not commercially justified such as excessive depreciation and provisions, hidden profit distributions and costs in connection with the purchase or improvement of fixed assets.

DEPRECIATIONDepreciation of tangible and intangible assets is allowed where ‘commercially justified’ and recorded in the books. For tax purposes, both the straight-line and the declining-balance methods may be used. The use of one method should be constant over the years and should only be changed if absolutely necessary. Safe haven rates have been published by the federal tax authorities, which are considered commercially justified.

STOCK/INVENTORyInventories must be carried at the lower of cost or market value. Cost is generally determined using the FIFO or average method. As a concession, a reserve against stock contingencies may be set up in the books. If this reserve does not exceed one-third of the lower of cost or market value of the inventory at the balance sheet date, it will be admitted by all tax authorities without enquiry.

CAPITAL GAINS AND LOSSESSee discussion above. As a rule, capital gains realised by corporations are not taxed separately but are added to any other income in the year of realisation and taxed at ordinary tax rates. Exceptions may apply to capital gains realised on the disposal of immovable property.

The sale of an investment of at least 20% in another company’s share capital by a Swiss company to a foreign or Swiss group company may, under certain circumstances, be made at either book value (tax- exempt restructuring) or fair market value. The sale of an investment of less than 20% in another company’s share capital to a foreign affiliated entity or to a Swiss company regardless of the investment may only be completed at fair market value.

Capital gains realised by a foreign shareholder on the sale of a Swiss subsidiary company are not subject to Swiss taxation, except for the sale of Swiss real estate companies, which would be considered as a direct sale of the Swiss properties owned by such companies.

DIVIDENDSDividends received are classified as business income but federal law and all cantonal laws allow a relief of taxes payable if the shareholding company owns more than 10% of the share capital or is entitled to at least 10% of the profit or reserves of the dividend distributing company or if the investment has a fair market value of more than CHF 1 million (qualifying investment). If the recipient of a dividend is a holding company, dividend income is exempt from corporate income taxes at cantonal and communal level.

Dividends paid from Swiss capital companies to Swiss residents and non-residents are subject to 35% Swiss withholding tax. Shareholders resident in Switzerland may apply for the notification procedure under certain circumstances or can reclaim the withholding tax. Shareholders resident abroad may obtain relief under the appropriate double taxation treaty or the tax savings agreement between Switzerland and the EU.

INTEREST DEDUCTIONSA company may generally deduct all interest paid or accrued during a business year, although loan arrangements between related parties must be made on an arm’s length basis. If the funds raised by interest bearing loans are loaned-on to affiliates, an interest spread of one-quarter to one-half per cent is basically required for the Swiss company if lending and on-lending are made in the same currency. Safe haven rates are published annually by the Swiss Federal Tax Administration for loans from and to affiliates.

Thin capitalisation rules apply to reduce the deduction available where the interest relates to monies borrowed from related parties. The Swiss Federal Tax Administration has issued thin capitalisation guidelines in a Circular Letter (“Kreisschreiben”). In general, any interest paid on loans from related parties that are classified as hidden equity are treated as hidden profit distributions, i.e. may be added back to taxable income and be subject to withholding tax. The excessive portion of the loan, reclassified as equity, may be subject to capital tax.

Switzerland

PKF Worldwide Tax Guide 20134

LOSSESA limited loss carry forward mechanism is available (for seven years) for federal and cantonal income taxes (there is an unlimited use of loss carry forward in certain recapitalisation scenarios “Sanierung”). Swiss tax law provides neither for loss carry back nor for the consolidation of profitable and unprofitable group companies.

FOREIGN SOURCED INCOMESwitzerland has no controlled foreign company legislation and a foreign company may be treated as a conduit only in instances where it is used for tax avoidance purposes. All income reported by a Swiss company is, in principle, subject to Swiss federal, cantonal and communal taxes (exception see e.g. domiciliary companies).

INCENTIVESTax incentives are granted on a case-by-case basis and their extent and duration largely depend on the size of the investment and the importance attributed to the economic development of the canton or region concerned by the cantonal and federal governments. Such an incentive may be either relief or exemption from income and annual capital tax for up to ten years.

Provisions for future expenses relating to research and development payable to third parties are tax deductible up to a maximum of 10% of the net profit, with a ceiling of CHF 1m.

Under certain conditions, companies are allowed to set up a tax privileged ‘recession reserve’ up to an amount of 20% of the company’s annual gross salaries paid. The amounts are deductible for federal, cantonal and communal tax purposes.

Accelerated write-down on fixed asset investments is granted in certain cantons. A wide variety of non-tax incentives are granted by these regions, such as cash grants, participation in project costs, partial or entire assumption of interest expenses on loans required for realisation of the project, subsidies for training personnel etc.

c. foreiGn taX relief

Double tax relief is granted by means of tax exemption of foreign branch and real property income and by the deduction of any non-recoverable foreign withholding taxes. Based on most double taxation agreements, a credit against Swiss income taxes is granted for the unrelieved portion of foreign withholding taxes on dividends, interest and royalties or similar fees but not for underlying income taxes on dividends received from subsidiaries.

The tax credit is granted for taxes derived from treaty countries under which Switzerland has committed itself to such a tax credit. Foreign taxes of these countries are creditable only if they are irrecoverable and actually paid or, in respect of treaties that provide for a tax-sparing credit, if they are deemed to be paid.

d. corporate Groups

Each entity in Switzerland is subject to taxes independent from the corporate group and tax returns have to be filed for each Swiss subsidiary and branch. Revenue and capital losses cannot be transferred within a corporate group.

e. related party transactions

Intra-group transactions are not challenged by the tax authorities if they are made on an arm’s length basis. There are neither provisions in tax laws nor any administrative practices that would challenge a transaction solely on the grounds of being made between related parties. However, intra-group transactions, where the consideration paid for goods or services is higher than what an independent third party would be willing to pay or the consideration for goods or services sold is less than what an independent third party would require, may be deemed as hidden profit distributions and be adjusted for determining taxable income. Hidden profit distributions are, in addition, subject to withholding tax in the same way as dividends.

Payments to foreign affiliates in respect of management fees, research and development, general and administrative expenses are deductible, if made on an arm’s length basis. They should, however, be specific and identifiable as a commercially justified charge to the Swiss entity.

f. witHHoldinG taX

The company must withhold a tax of 35% and remit this amount to the tax authorities on all cash dividends and dividends in kind, including bonus shares and surplus

Switzerland

PKF Worldwide Tax Guide 2013 5

liquidation proceeds. As per 1 January 2011 reserves that have been paid in directly by shareholders can be distributed withholding tax free. This tax is in general levied at source. However, it can be applied through the notification procedure under certain circumstances. Most treaties provide for a reduction of the normal 35% rate.

Withholding tax on interest is levied at a rate of 35% but only on bonds, bond-like loans and deposits accepted by Swiss banks from non-bank clients. No withholding tax is levied on inter-company loans.

There is no withholding tax on royalties.

G. eXcHanGe control

There are, at present, no currency restrictions on inward investments, and the Swiss franc is freely convertible into any other currency. Bank accounts may be maintained in local or foreign currencies either in or outside Switzerland without restriction. There is no distinction between resident and non-resident accounts.

If the Swiss accounts are kept in a currency other than Swiss francs (i.e. in a functional currency), exchange gains or losses from the conversion of the functional currency accounts to CHF accounts are no longer taxable or tax deductible since the issuance of a respective federal court law decision in October 2009.

H. personal taX

A Swiss resident individual is subject to Swiss federal, cantonal and communal taxes on his worldwide income and net wealth, with the exception of income from investments in foreign permanent establishments and real estate situated abroad. Basically, foreigners are regarded as resident from date of registration (usually within one week of arrival where the individual intends to stay permanently in Switzerland). The cantons levy a wage source tax on salaries paid by domestic employers to expatriates. The tax is deducted monthly from the expatriate’s gross income, including any benefits in kind, based on the cantonal tax table.

Persons resident abroad and drawing income from or owning net assets in the form of a permanent establishment or real estate in Switzerland are subject to Swiss taxes thereon at the rates that would apply to their worldwide taxable income or net assets. The tax liability is, however, limited to their Swiss taxable income and net assets.

Income tax is payable on assessable income less allowable deductions. The assessable income must include, in gross income, all compensation received as salary, living and housing allowances, tax reimbursements and the fair market value of any benefits in kind.

The tax rates of direct federal tax on income and all cantonal taxes on income and net wealth are on a progressive basis.

The federal tax rates apply separately to single and married taxpayers. These rates are valid as per 1 January 2013. The married taxpayers’ rate also applies to registered couples of the same sex living together and to widowed, separated and divorced or single persons living with children who are minors and studying at their expense.

The tax rates for unmarried taxpayers are as follows:

If taxable income is between

Tax on lower amount is

Tax on excess is

(CHF) (CHF) (CHF) (%)

0 – 14,500 – 0

14,500 – 31,599 – 0.77

31,600 – 41,399 131.65 0.88

41,400 – 55,199 217.00 2.64

55,200 – 72,499 582.20 2.97

72,500 – 78,099 1,096.00 5.94

78,100 – 103,599 1,428.60 6.60

103,600 – 134,599 3,111.60 8.80

134,600 – 175,999 5,839.60 11.00

Switzerland

PKF Worldwide Tax Guide 20136

If taxable income is between

Tax on lower amount is

Tax on excess is

(CHF) (CHF) (CHF) (%)

176,000 – 755,199 10,393.60 13.20

755,200 – . . . 86,848.00

If taxable income exceeds CHF 755,200 the exceeding income is subject to a flat rate of 11.50%.

The tax rate for married taxpayers is as follows:

If taxable income is between

Tax on lower amount is

Tax on excess is

(CHF) (CHF) (%)

0 – 28,300 – 0

28,300 – 50,899 – 1

50,900 – 58,399 226 2

58,400 – 75,299 376 3

75,300 – 90,299 883 4

90,300 – 103,399 1,483 5

103,400 – 114,699 2,138 6

114,700 – 124,199 2,816 7

124,200 – 131,699 3,481 8

131,700 – 137,299 4,081 9

137,300 – 141,199 4,585 10

141,200 – 143,099 4,975 11

143,100 – 144,999 5,184 12

145,000 – 895,799 5,412 13

895,800 – 103,016 11.5

* If taxable income exceeds CHF 895,800, the exceeding income is subject to a flat rate of 11.50%.

In addition, cantonal and municipal taxes are payable which are considerably higher. The tax rates are dependent on the canton in which the individual is resident. There are also net wealth taxes, inheritance and gift taxes levied by most cantons.

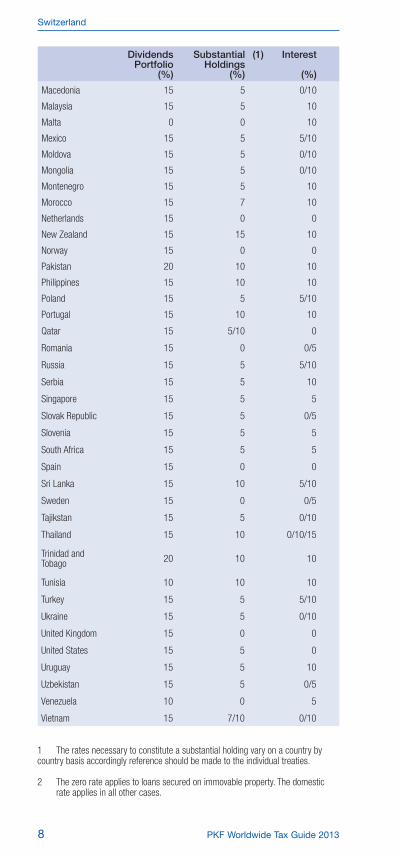

i. treaty and non-treaty witHHoldinG taX rates

Ordinarily the rate of Swiss withholding tax is 35%. Relief, when granted, is generally by way of refund. The table below stipulates the remaining tax for the recipient for each type of income. The information contained therein is valid as at 10 October 2012.

On 1 July 2005 the agreement on the taxation of savings income between Switzerland and the EU came into effect. A limited company with a direct participation of 25% or more which is held longer than two years can file a request for the application of the declaration procedure. In this case, a 0% rate results.

DividendsPortfolio

(%)

SubstantialHoldings

(%)

(1) Interest

(%)

Resident corporations and individuals 0 0 0

Non-resident corporations and individuals

Non-Treaty Countries: 35 35 35

Treaty Countries:

Albania 15 5 5

Switzerland

PKF Worldwide Tax Guide 2013 7

DividendsPortfolio

(%)

SubstantialHoldings

(%)

(1) Interest

(%)

Algeria 15 5 0/10

Argentina 15 10 12

Armenia 15 5 0/10

Azerbaijan 15 5 10

Australia 15 15 10

Austria 15 0 0

Belarus 15 5 0/5/8

Belgium 15 10 0/10

Bangladesh 15 10 0/10

Bulgaria 15 5 0/10

Canada 15 5 0/10

Chile 15 15 15/5

China 10 10 0/10

Colombia 15 0 10

Croatia 15 5 0/5/10

Czech Republic 15 5 0

Denmark 15 0 0

Ecuador 15 15 0/10

Egypt 15 5 0/15

Estonia 15 5 0/10

Finland 10 0 0

France 15 0 0

Georgia 10 10 0

Germany 26,375/15 0 0

Ghana 15 5 10

Greece 15 5 7

Hungary 10 0 0

Iceland 15/18/20 5 0

India 10 10 10

Indonesia 15 10 10

Iran 15 5 0/10

Ireland, Republic of 0 0 0

Israel 15 5 0/5/10

Italy 15 15 12.5

Ivory Coast 15 15 0/15

Jamaica 15 10 5/10

Japan 10 1/5 0/10

Kazakhstan 15 5 0/10

Korea, Republic of 15 10 0/10

Kyrgyzstan 15 5 5

Kuwait 15 15 10

Latvia 15 5 10

Liechtenstein – – 0/– (2)

Lithuania 15 5 10

Luxembourg 15 0 0/10

Switzerland

PKF Worldwide Tax Guide 20138

DividendsPortfolio

(%)

SubstantialHoldings

(%)

(1) Interest

(%)

Macedonia 15 5 0/10

Malaysia 15 5 10

Malta 0 0 10

Mexico 15 5 5/10

Moldova 15 5 0/10

Mongolia 15 5 0/10

Montenegro 15 5 10

Morocco 15 7 10

Netherlands 15 0 0

New Zealand 15 15 10

Norway 15 0 0

Pakistan 20 10 10

Philippines 15 10 10

Poland 15 5 5/10

Portugal 15 10 10

Qatar 15 5/10 0

Romania 15 0 0/5

Russia 15 5 5/10

Serbia 15 5 10

Singapore 15 5 5

Slovak Republic 15 5 0/5

Slovenia 15 5 5

South Africa 15 5 5

Spain 15 0 0

Sri Lanka 15 10 5/10

Sweden 15 0 0/5

Tajikstan 15 5 0/10

Thailand 15 10 0/10/15

Trinidad and Tobago 20 10 10

Tunisia 10 10 10

Turkey 15 5 5/10

Ukraine 15 5 0/10

United Kingdom 15 0 0

United States 15 5 0

Uruguay 15 5 10

Uzbekistan 15 5 0/5

Venezuela 10 0 5

Vietnam 15 7/10 0/10

1 The rates necessary to constitute a substantial holding vary on a country by country basis accordingly reference should be made to the individual treaties.

2 The zero rate applies to loans secured on immovable property. The domestic rate applies in all other cases.

Switzerland

www.pkf.com