Sustainable Energy in Cities David Hawkey [email protected] .

40

-

Upload

olivia-hamilton -

Category

Documents

-

view

216 -

download

0

Transcript of Sustainable Energy in Cities David Hawkey [email protected] .

Overview

• What is district heating?• Development of heat networks• Organisational issues• Examples• UK context• Heat map exercise

Cities’ contribution to GHG emissions

• 75%–80% of anthropogenic GHG emissions?– Stern review, Clinton Climate Initiative, GLA, etc.

• What constitutes a city?– Production vs consumption– Location vs administration

• Cities are sites in regional, national, international flows of resources and waste

• Infrastructures enable various forms of circulation and metabolism

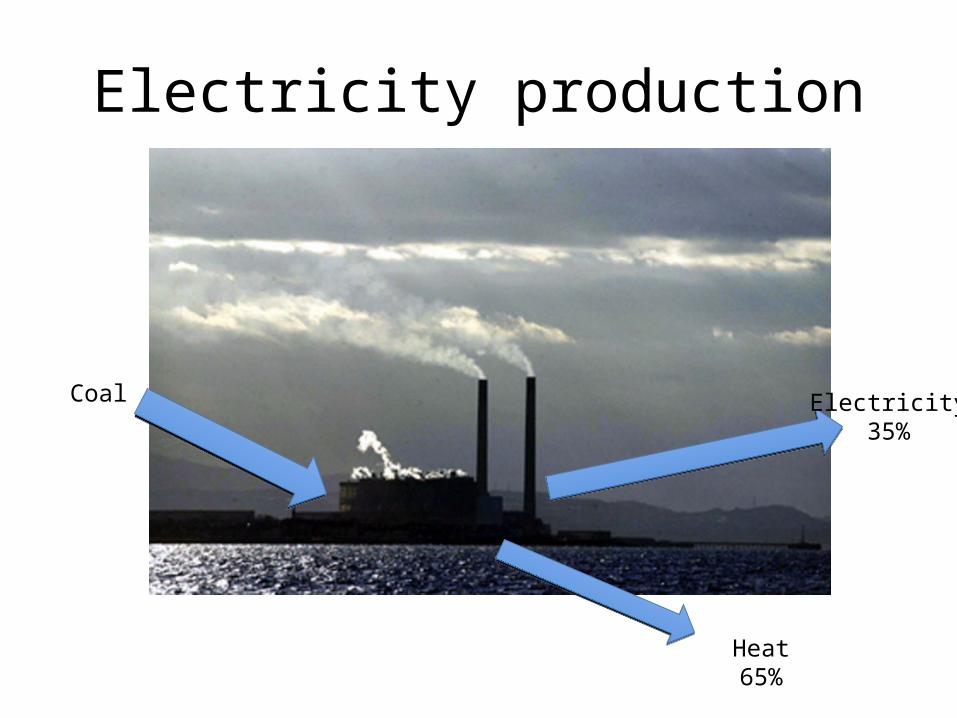

Electricity production

Coal Electricity35%

Heat65%

Building energy supply

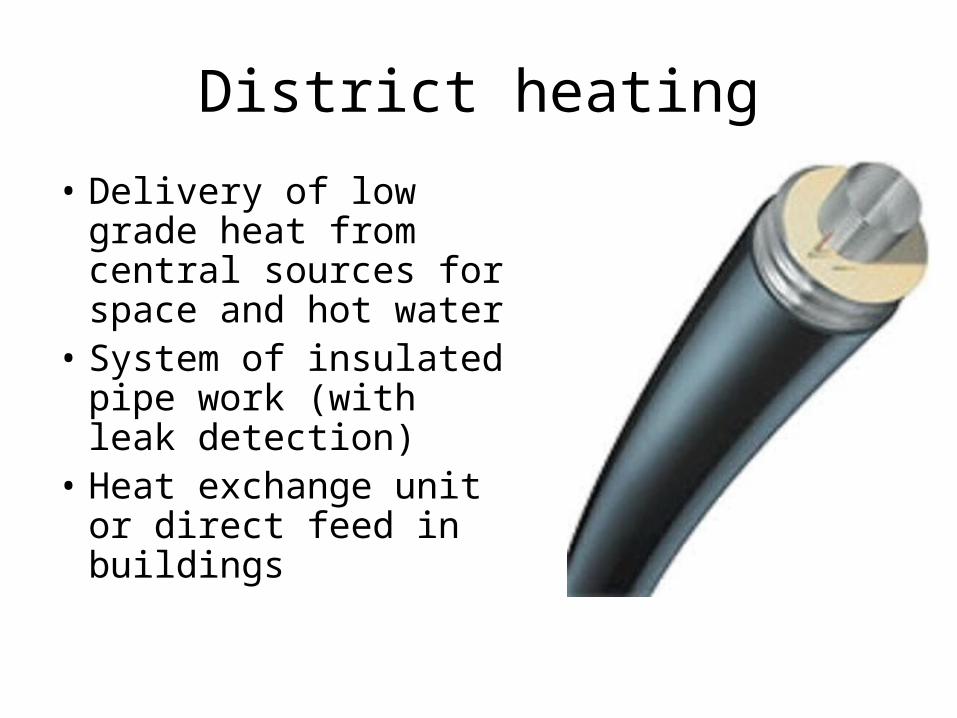

District heating

• Delivery of low grade heat from central sources for space and hot water

• System of insulated pipe work (with leak detection)

• Heat exchange unit or direct feed in buildings

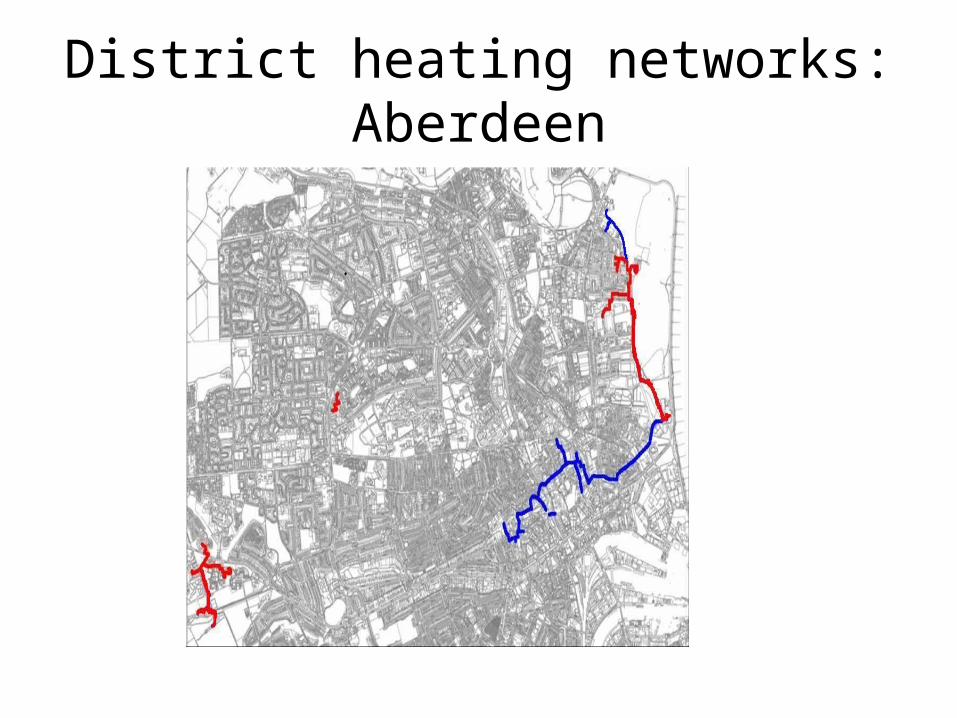

District heating networks: Aberdeen

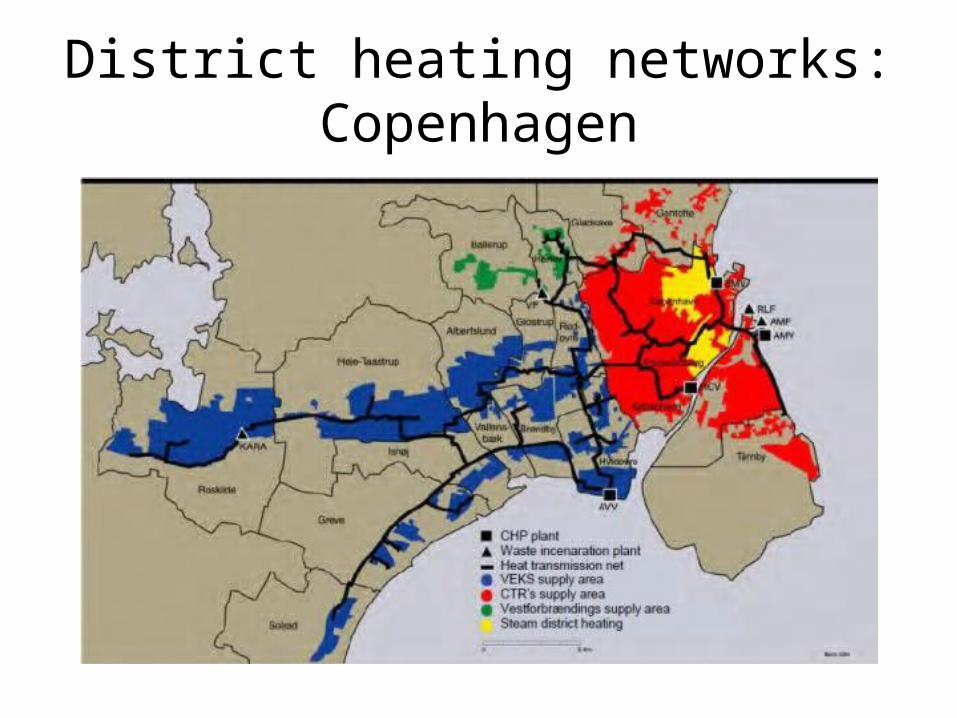

District heating networks: Copenhagen

District Heating – sources• Low carbon• Low cost• Renewable• Waste heat and heat from

waste• Efficiency• Local pollution• Flexibility• Energy security• Community participation• Electricity balancing• …

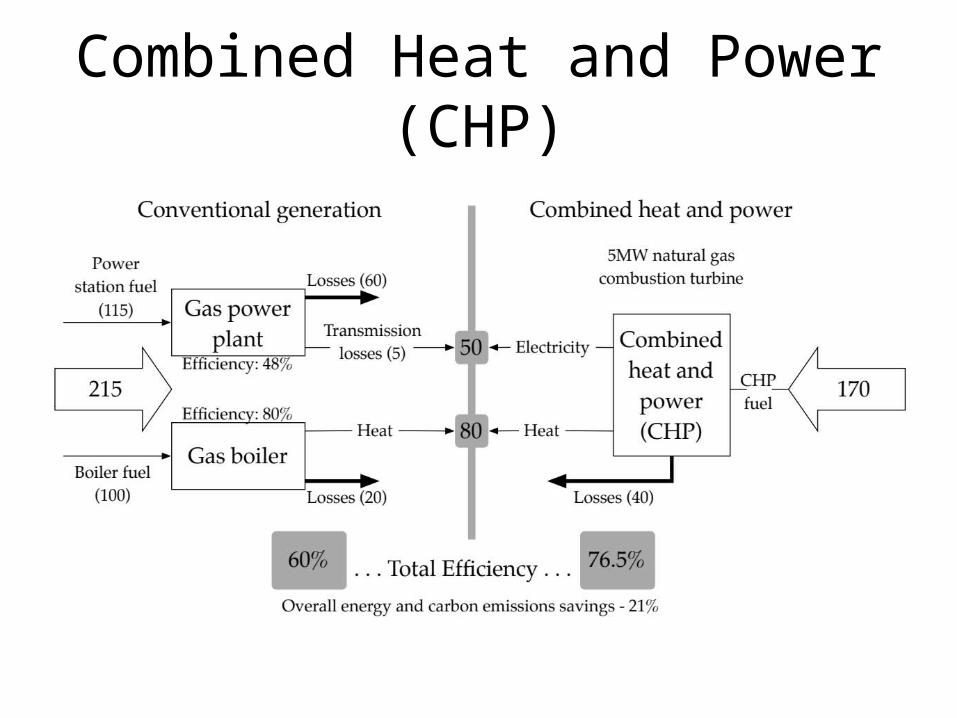

Combined Heat and Power (CHP)

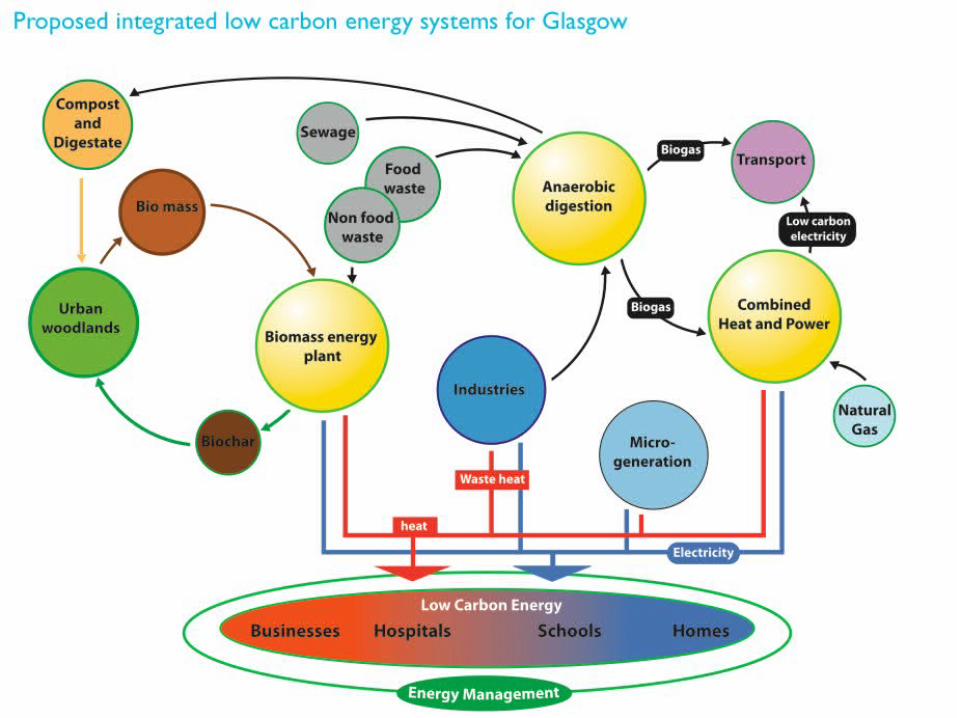

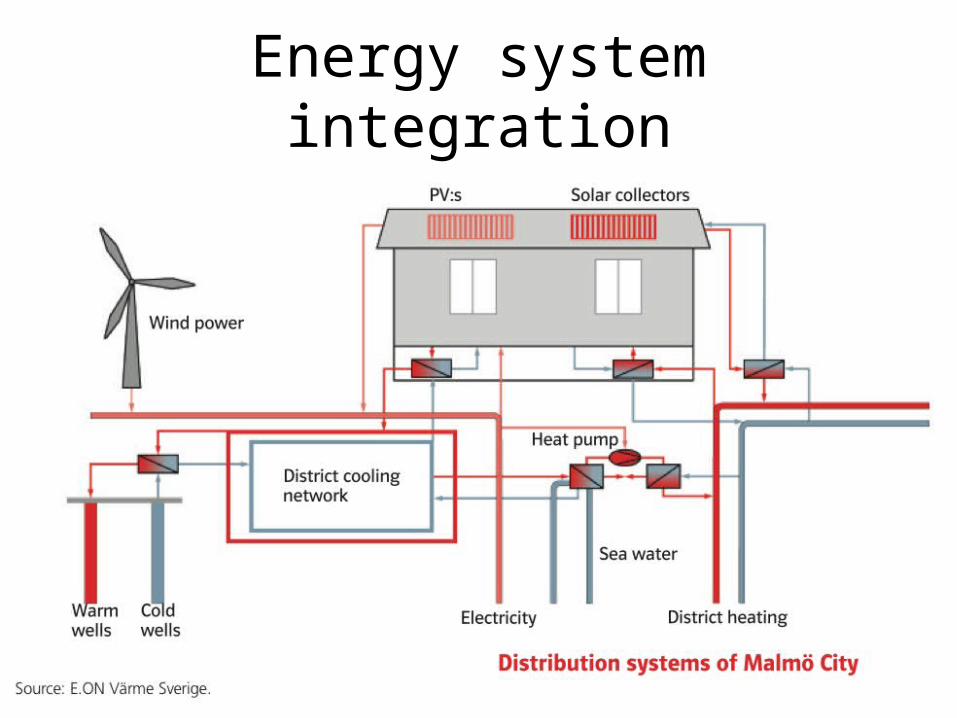

Energy system integration

• c

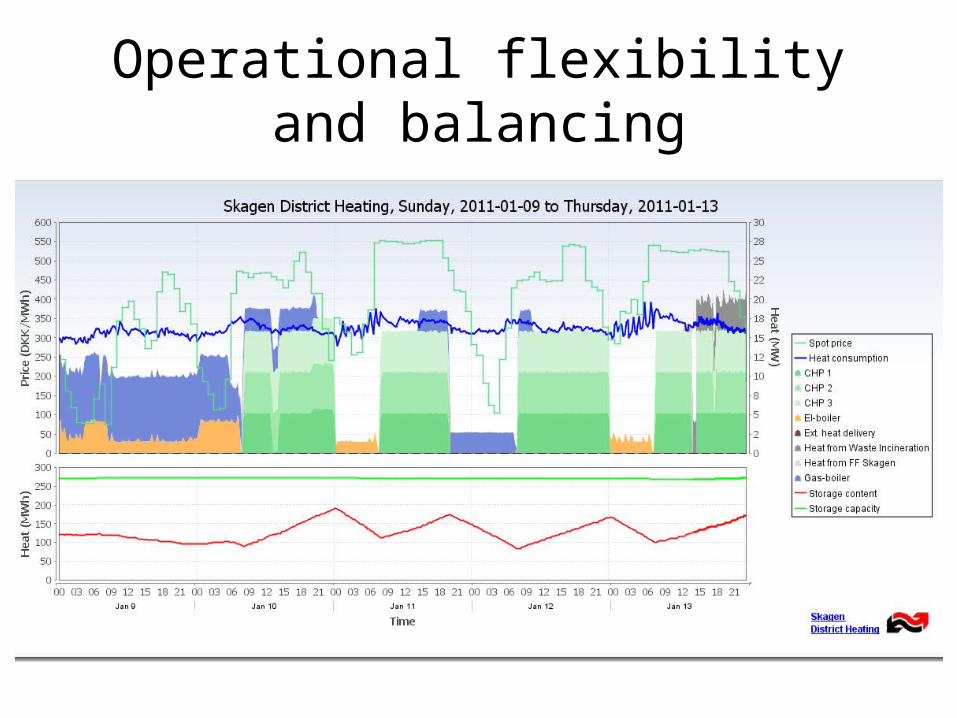

Operational flexibility and balancing

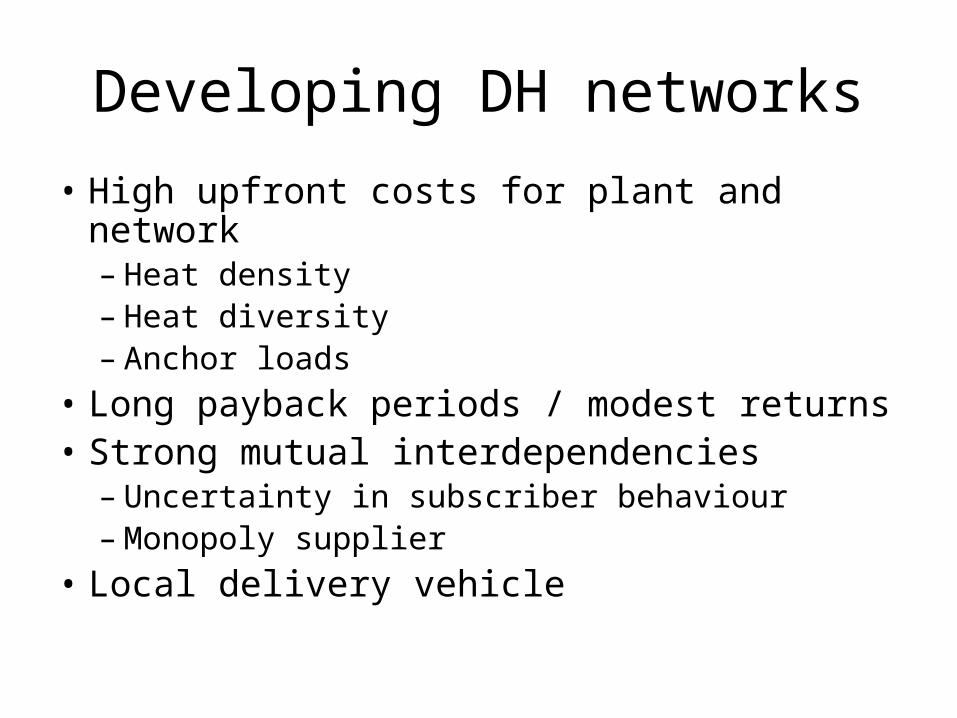

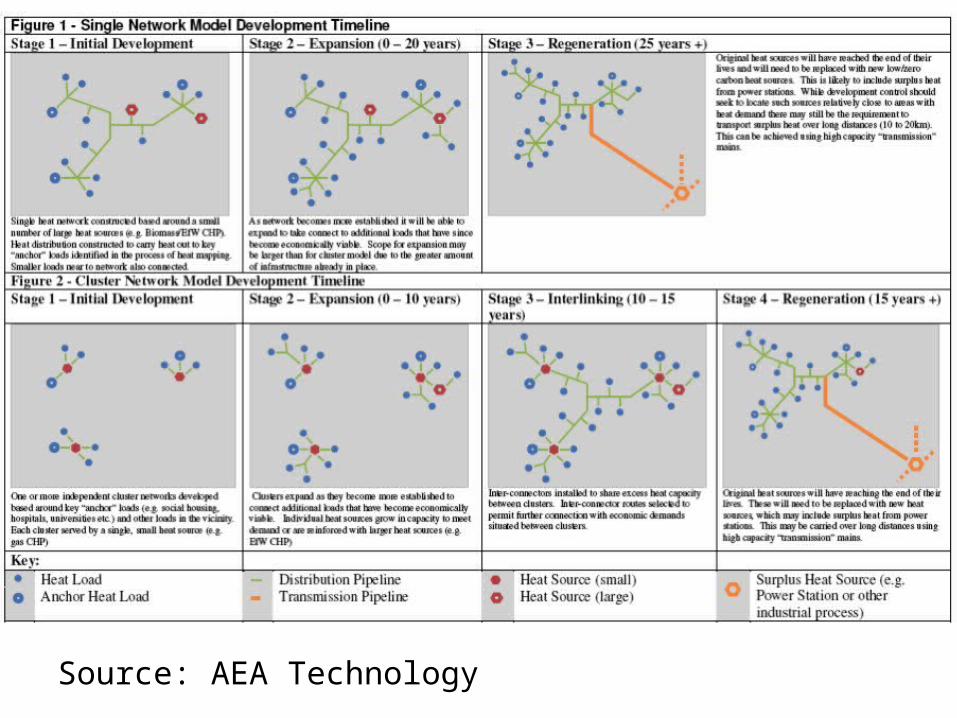

Developing DH networks

• High upfront costs for plant and network– Heat density– Heat diversity– Anchor loads

• Long payback periods / modest returns• Strong mutual interdependencies– Uncertainty in subscriber behaviour– Monopoly supplier

• Local delivery vehicle

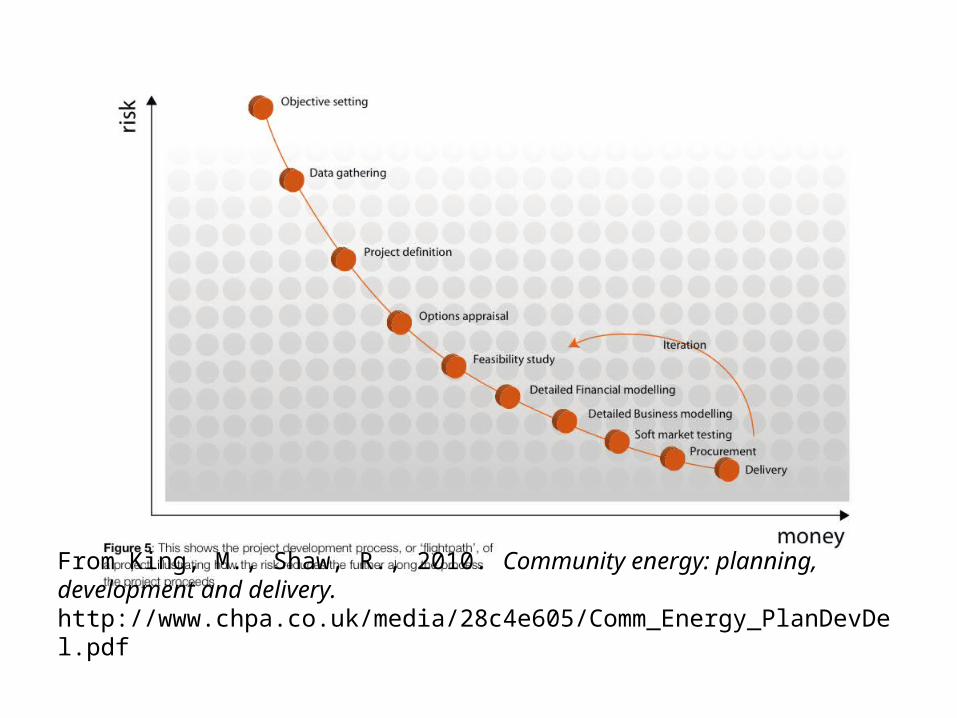

From King, M., Shaw, R., 2010. Community energy: planning, development and delivery. http://www.chpa.co.uk/media/28c4e605/Comm_Energy_PlanDevDel.pdf

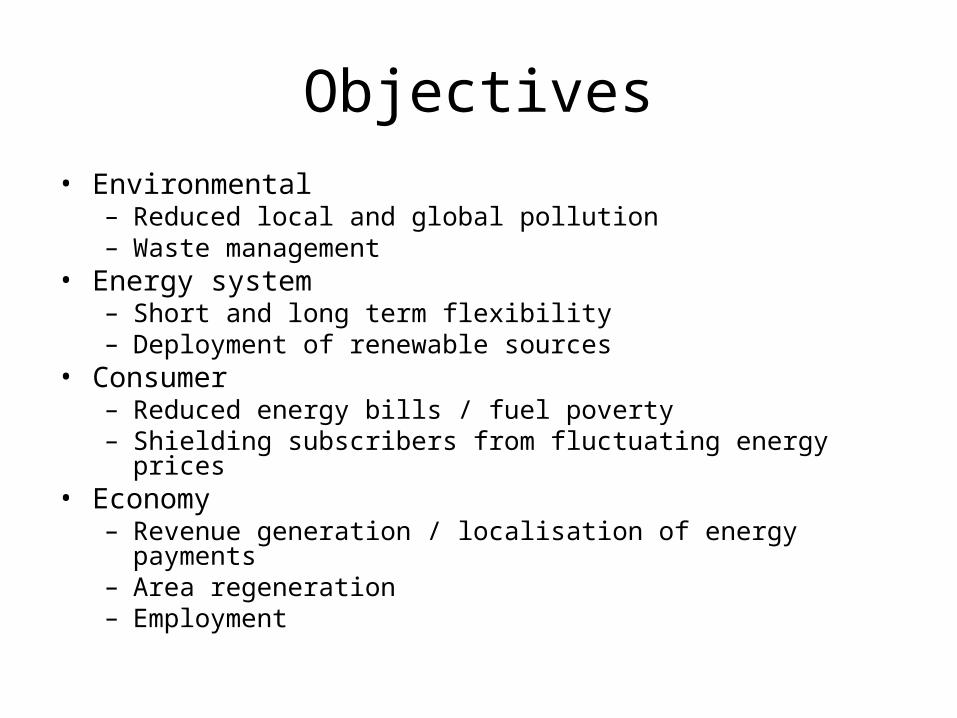

Objectives• Environmental

– Reduced local and global pollution– Waste management

• Energy system– Short and long term flexibility– Deployment of renewable sources

• Consumer– Reduced energy bills / fuel poverty– Shielding subscribers from fluctuating energy prices

• Economy– Revenue generation / localisation of energy payments– Area regeneration– Employment

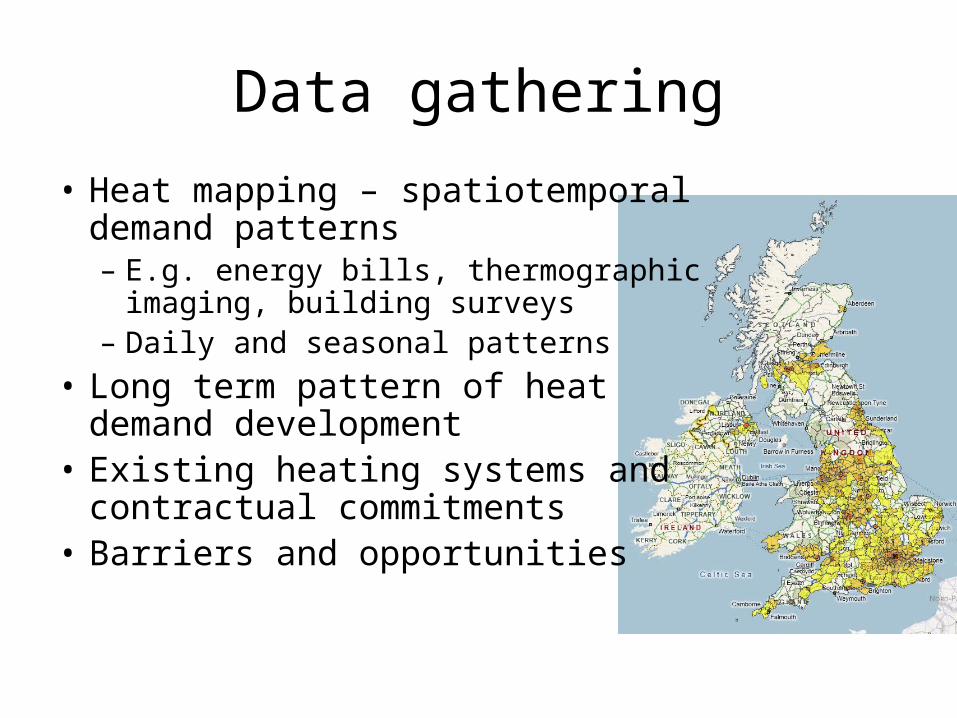

Data gathering

• Heat mapping – spatiotemporal demand patterns– E.g. energy bills, thermographic

imaging, building surveys– Daily and seasonal patterns

• Long term pattern of heat demand development

• Existing heating systems and contractual commitments

• Barriers and opportunities

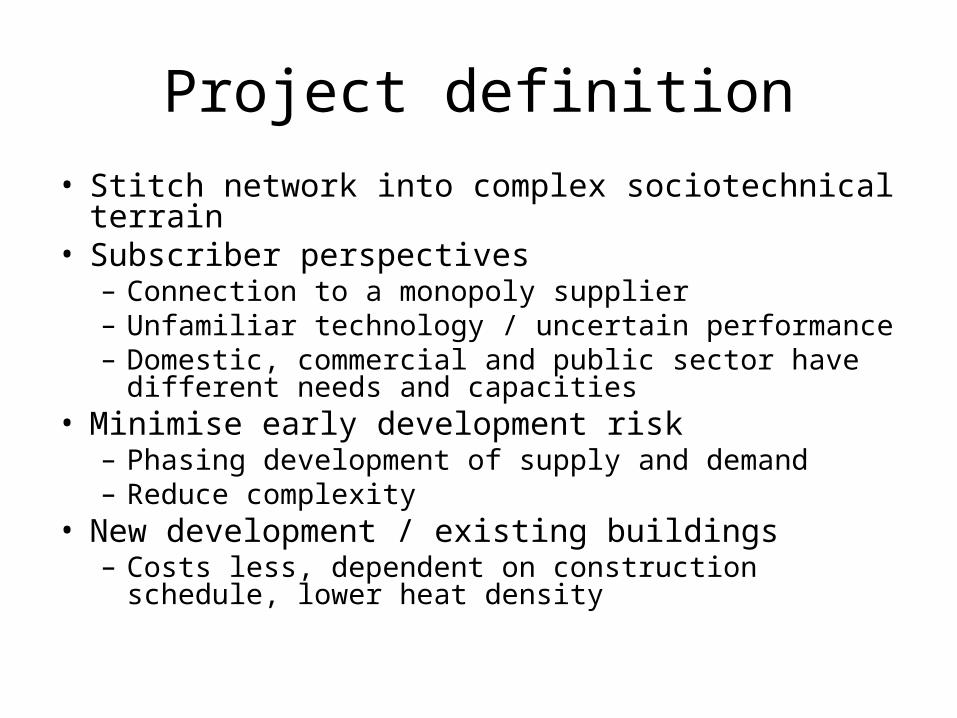

Project definition• Stitch network into complex sociotechnical terrain• Subscriber perspectives– Connection to a monopoly supplier– Unfamiliar technology / uncertain performance– Domestic, commercial and public sector have different

needs and capacities• Minimise early development risk– Phasing development of supply and demand– Reduce complexity

• New development / existing buildings– Costs less, dependent on construction schedule, lower

heat density

Source: AEA Technology

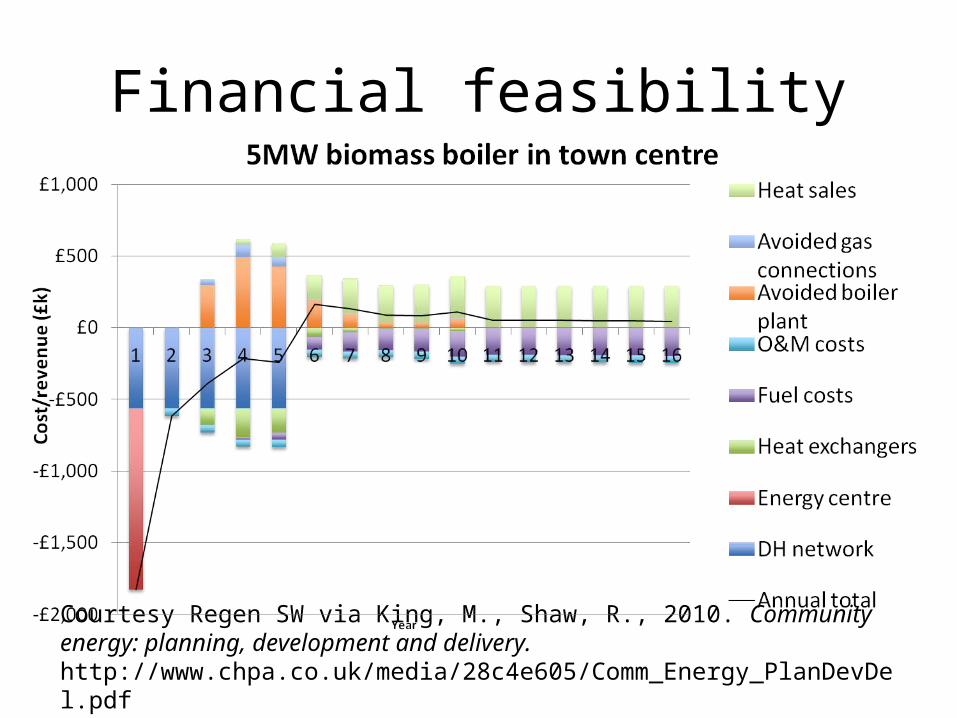

Financial feasibility

Courtesy Regen SW via King, M., Shaw, R., 2010. Community energy: planning, development and delivery. http://www.chpa.co.uk/media/28c4e605/Comm_Energy_PlanDevDel.pdf

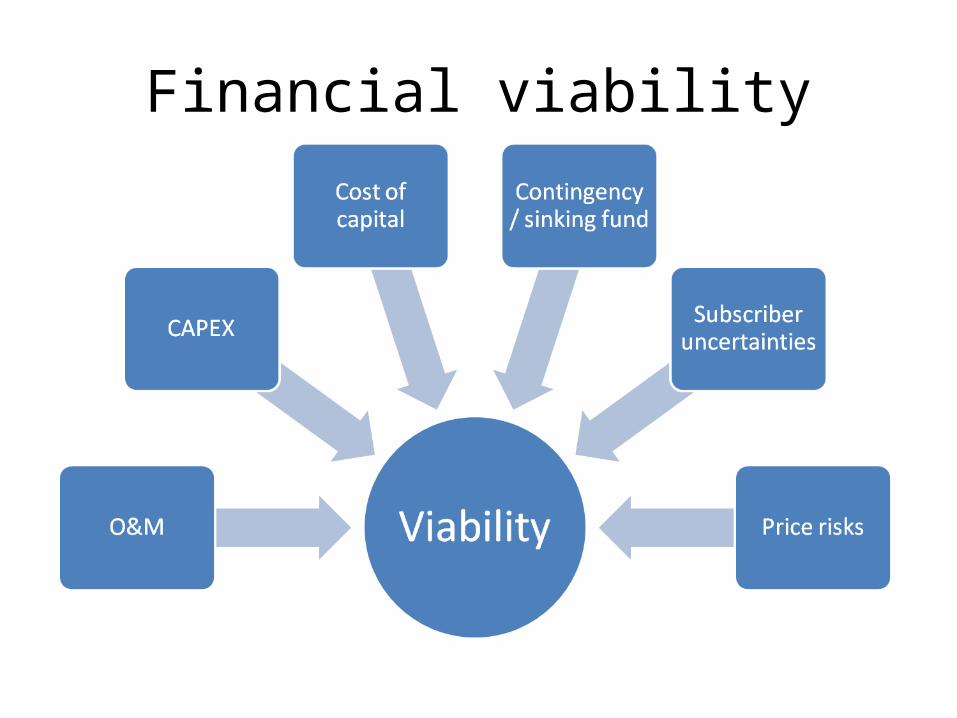

Financial viability

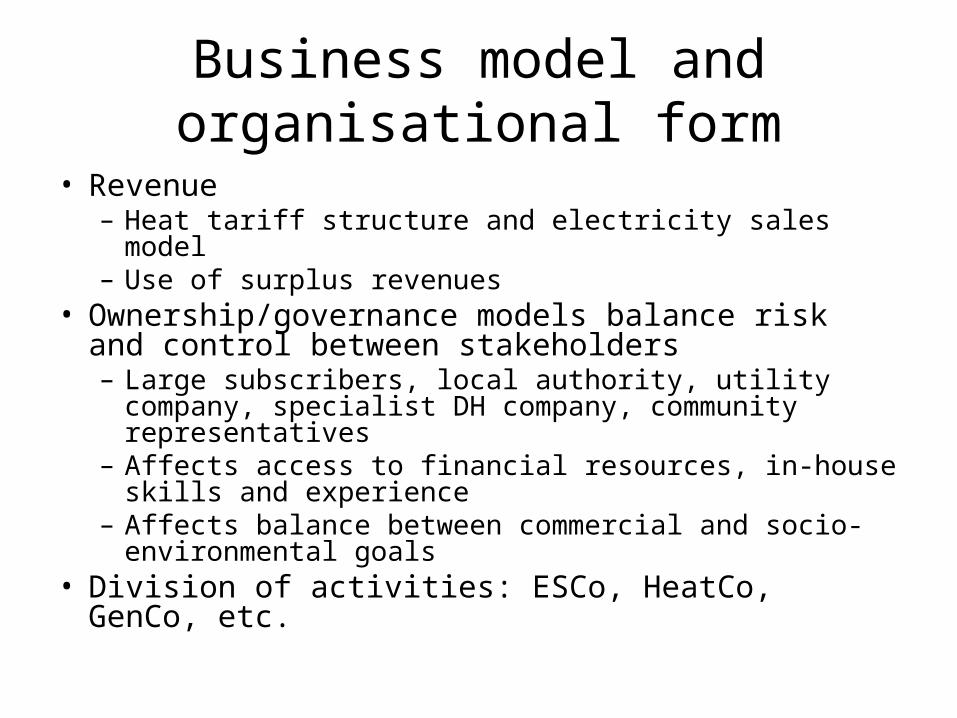

Business model and organisational form

• Revenue– Heat tariff structure and electricity sales model– Use of surplus revenues

• Ownership/governance models balance risk and control between stakeholders– Large subscribers, local authority, utility company,

specialist DH company, community representatives– Affects access to financial resources, in-house skills and

experience– Affects balance between commercial and socio-

environmental goals• Division of activities: ESCo, HeatCo, GenCo, etc.

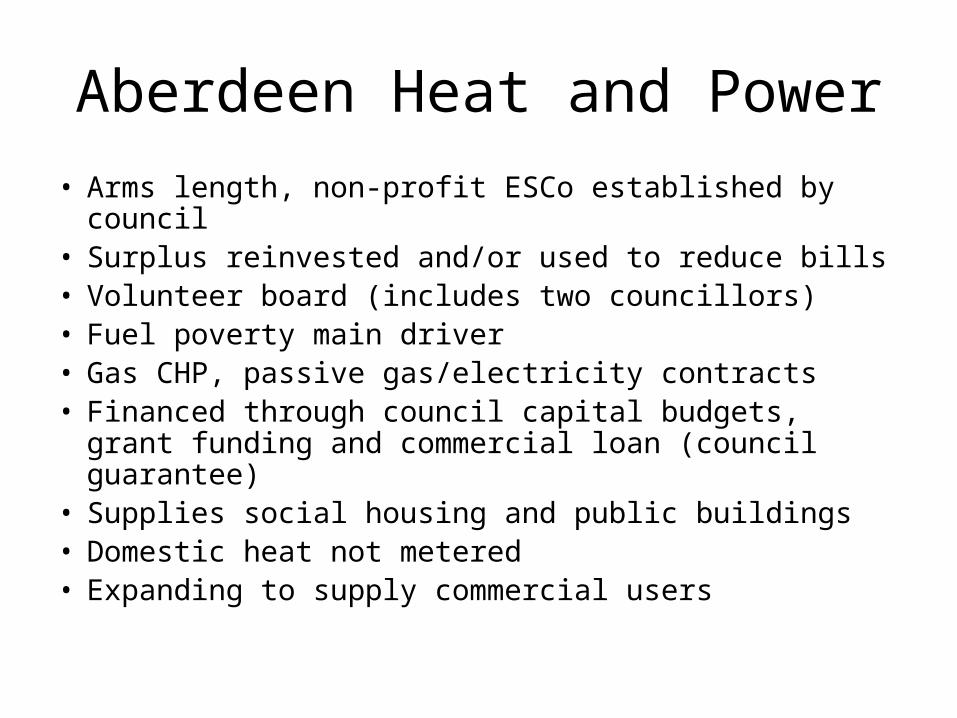

Aberdeen Heat and Power

• Arms length, non-profit ESCo established by council• Surplus reinvested and/or used to reduce bills• Volunteer board (includes two councillors)• Fuel poverty main driver• Gas CHP, passive gas/electricity contracts• Financed through council capital budgets, grant

funding and commercial loan (council guarantee)• Supplies social housing and public buildings• Domestic heat not metered• Expanding to supply commercial users

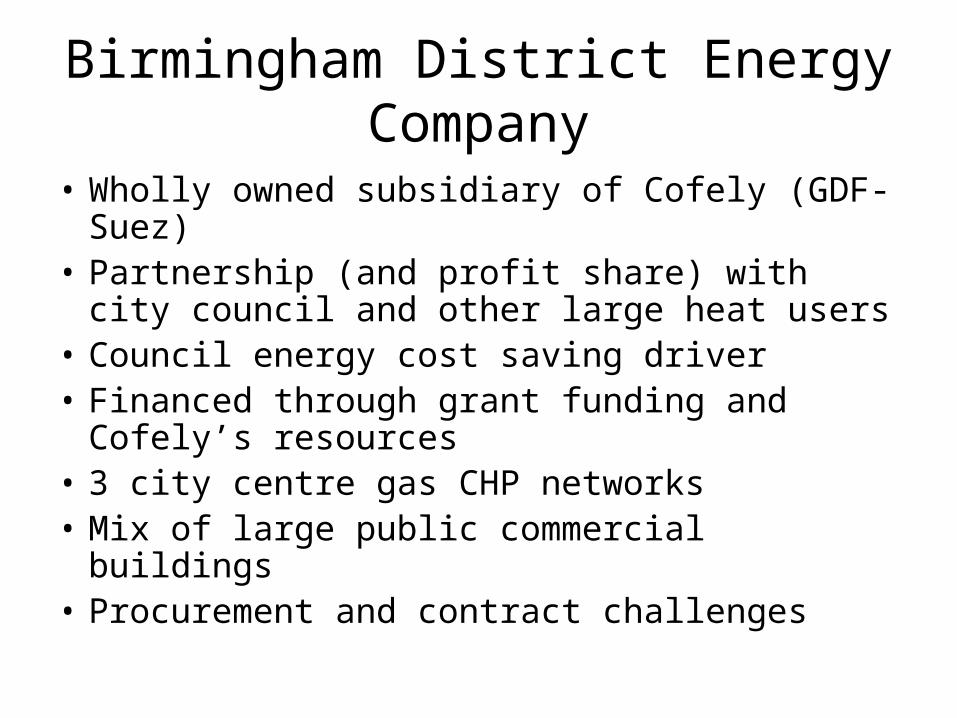

Birmingham District Energy Company

• Wholly owned subsidiary of Cofely (GDF-Suez)• Partnership (and profit share) with city council

and other large heat users• Council energy cost saving driver• Financed through grant funding and Cofely’s

resources• 3 city centre gas CHP networks• Mix of large public commercial buildings• Procurement and contract challenges

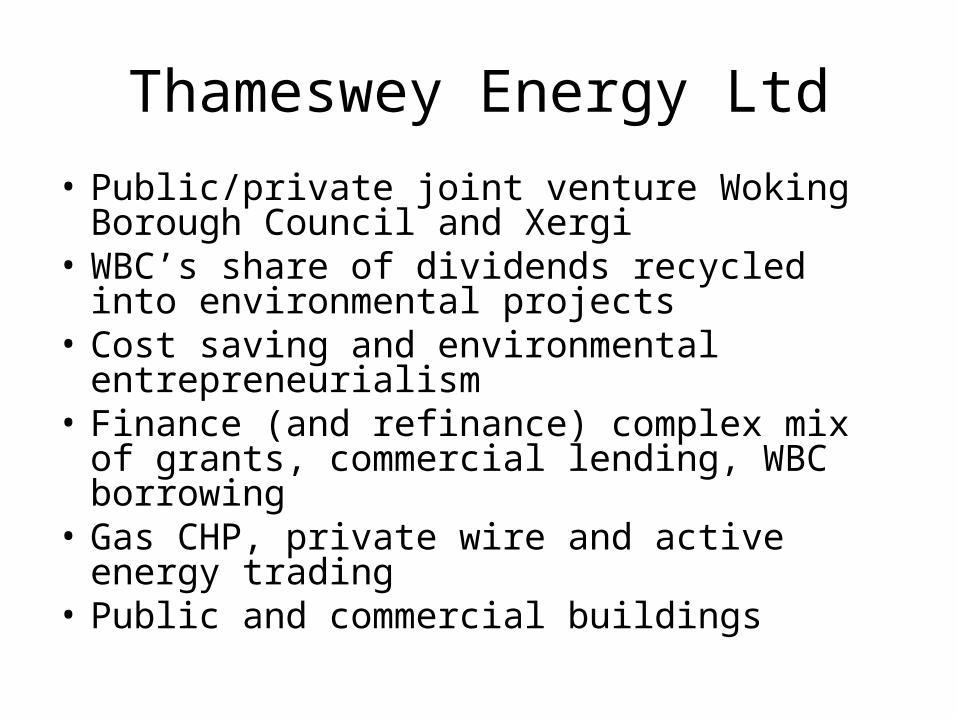

Thameswey Energy Ltd• Public/private joint venture Woking Borough

Council and Xergi• WBC’s share of dividends recycled into

environmental projects• Cost saving and environmental

entrepreneurialism• Finance (and refinance) complex mix of grants,

commercial lending, WBC borrowing• Gas CHP, private wire and active energy trading• Public and commercial buildings

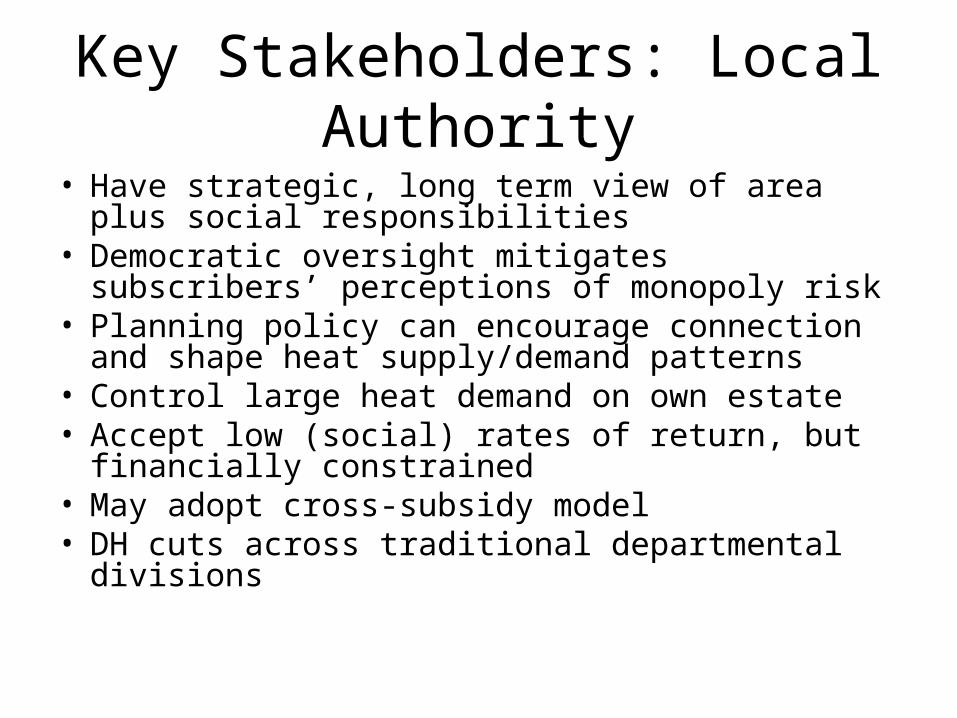

Key Stakeholders: Local Authority• Have strategic, long term view of area plus social

responsibilities• Democratic oversight mitigates subscribers’

perceptions of monopoly risk• Planning policy can encourage connection and shape

heat supply/demand patterns• Control large heat demand on own estate• Accept low (social) rates of return, but financially

constrained• May adopt cross-subsidy model• DH cuts across traditional departmental divisions

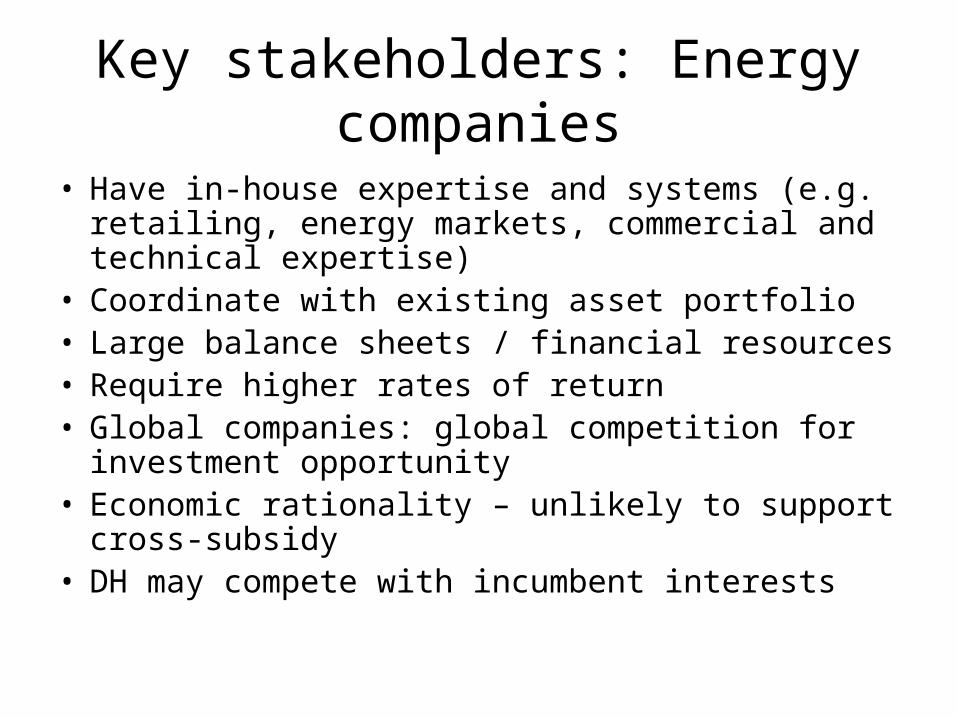

Key stakeholders: Energy companies

• Have in-house expertise and systems (e.g. retailing, energy markets, commercial and technical expertise)

• Coordinate with existing asset portfolio• Large balance sheets / financial resources• Require higher rates of return• Global companies: global competition for investment

opportunity• Economic rationality – unlikely to support cross-

subsidy• DH may compete with incumbent interests

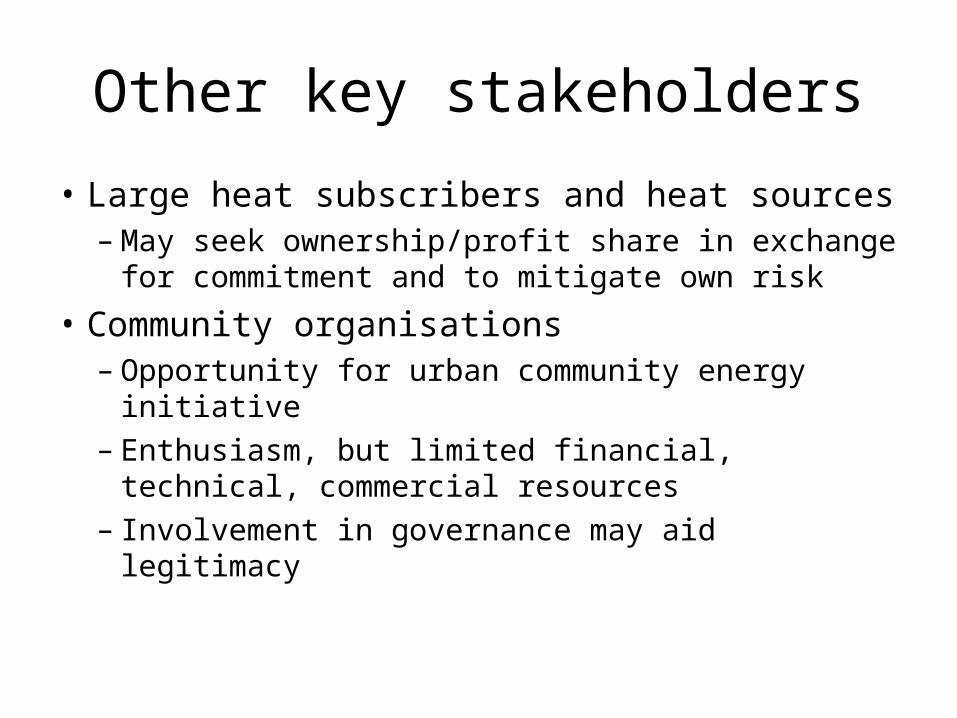

Other key stakeholders

• Large heat subscribers and heat sources– May seek ownership/profit share in exchange for

commitment and to mitigate own risk

• Community organisations– Opportunity for urban community energy

initiative– Enthusiasm, but limited financial, technical,

commercial resources– Involvement in governance may aid legitimacy

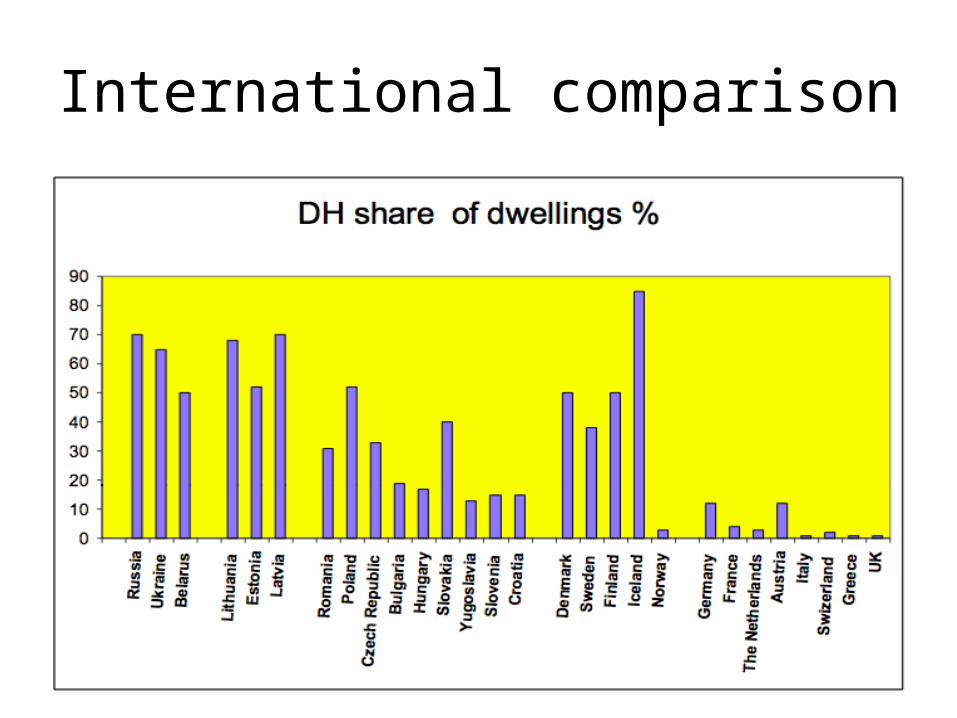

International comparison

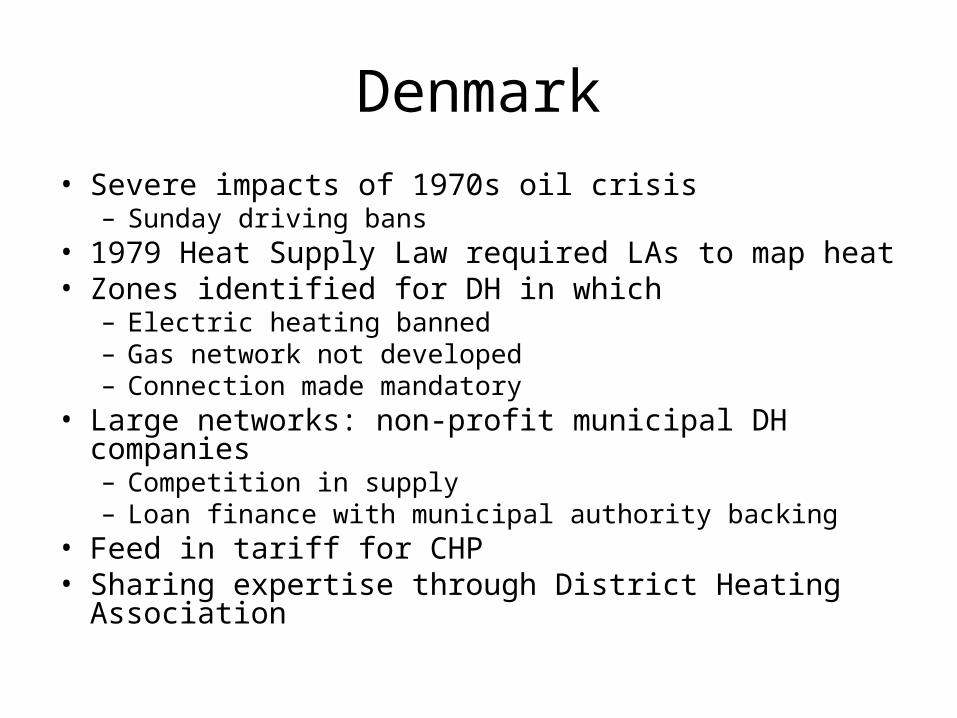

Denmark• Severe impacts of 1970s oil crisis

– Sunday driving bans• 1979 Heat Supply Law required LAs to map heat• Zones identified for DH in which

– Electric heating banned– Gas network not developed– Connection made mandatory

• Large networks: non-profit municipal DH companies– Competition in supply– Loan finance with municipal authority backing

• Feed in tariff for CHP• Sharing expertise through District Heating Association

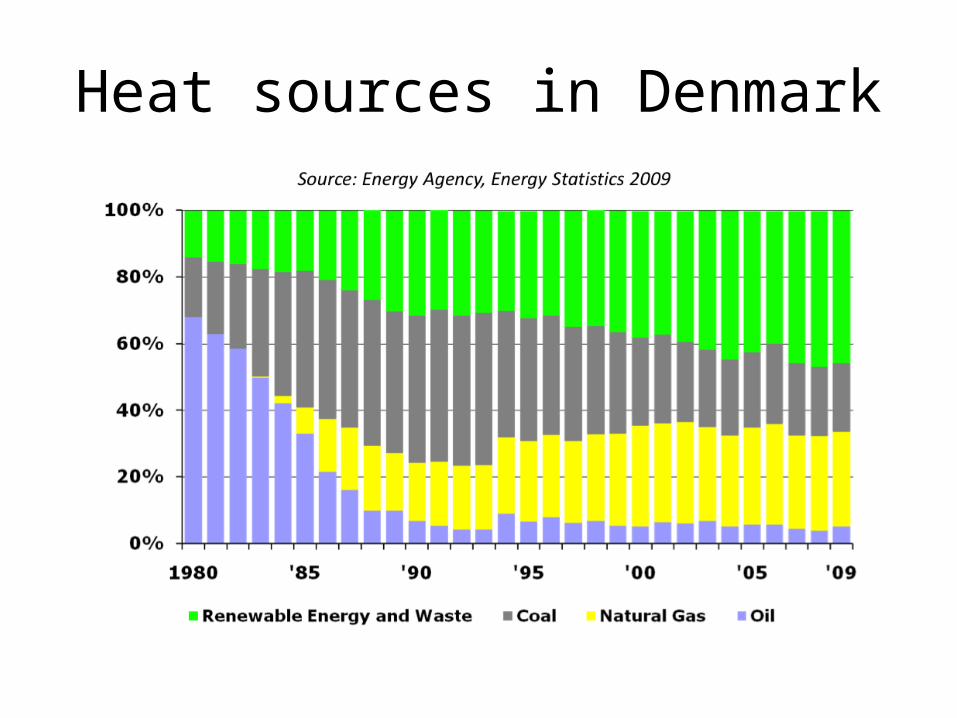

Heat sources in Denmark

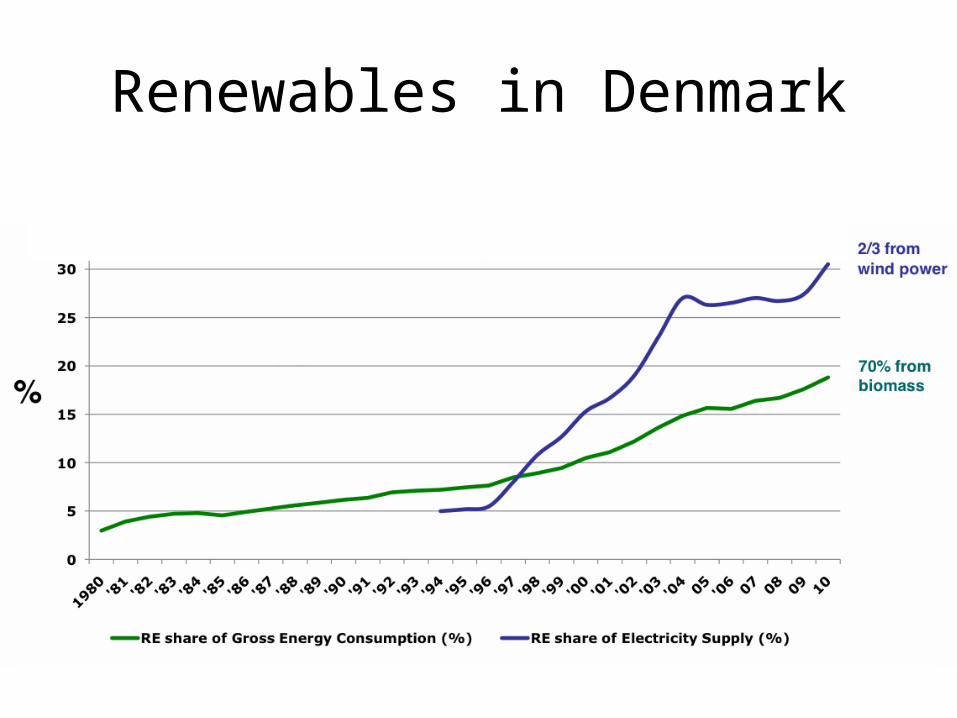

Renewables in Denmark

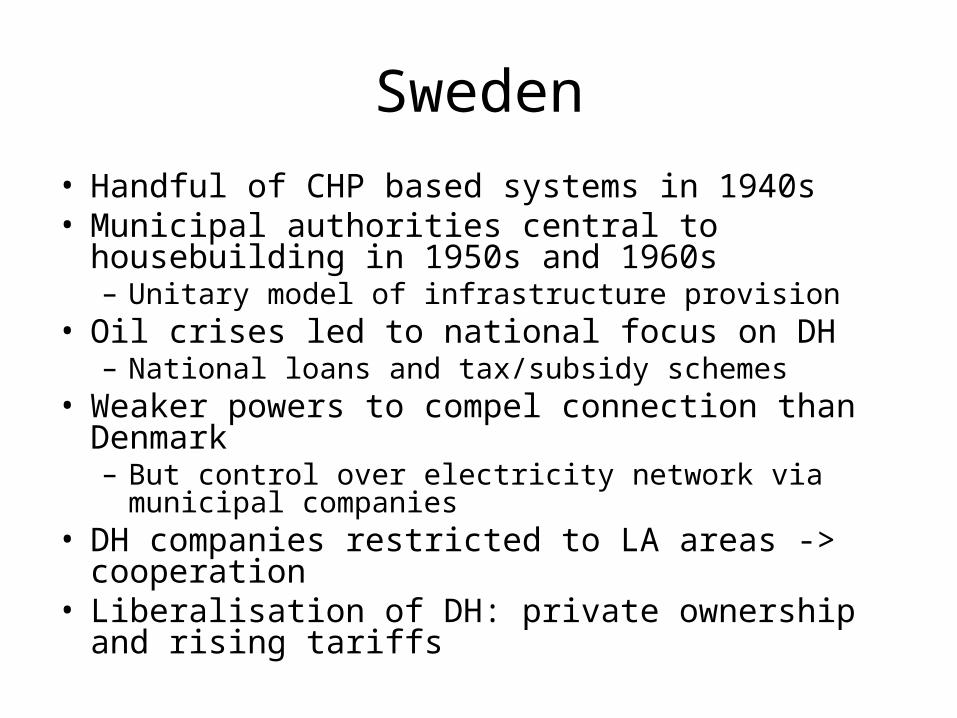

Sweden• Handful of CHP based systems in 1940s• Municipal authorities central to housebuilding in 1950s

and 1960s– Unitary model of infrastructure provision

• Oil crises led to national focus on DH– National loans and tax/subsidy schemes

• Weaker powers to compel connection than Denmark– But control over electricity network via municipal

companies• DH companies restricted to LA areas -> cooperation• Liberalisation of DH: private ownership and rising

tariffs

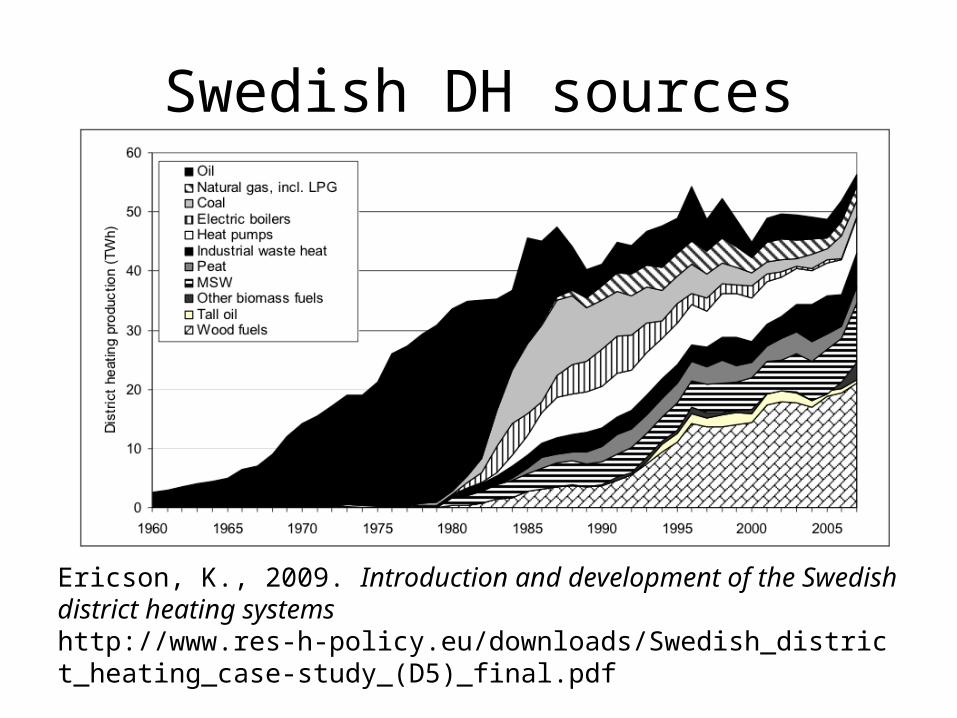

Swedish DH sources

Ericson, K., 2009. Introduction and development of the Swedish district heating systems http://www.res-h-policy.eu/downloads/Swedish_district_heating_case-study_(D5)_final.pdf

UK Historical context

• Nationalised energy industries (1940s)– No municipal involvement in energy provision– Electricity industry pursued increased electrical

efficiency (i.e. larger centralised plant)• Energy production increased in response to

resource constraints– National programme of conversion to natural gas

• Poorly installed coal-based systems in 1960s• “Lead cities” programme in 1980s found raising

private finance difficult

UK DH context

• DH not specifically regulated– Subscriber and developer risks

• Limited standardisation– Consumer charters, technical standards, appraisal

methodologies• High proportion home ownership• Limited skills and supply chains– Unpredictable bursts of grant funding

• Competing visions of low carbon heat future• Difficult to capture external benefits in business model

UK contemporary energy context• Retail dominated by six integrated utilities– Electricity generation and network operation– Subsidiaries of international companies / LSE listed

• Some DH specialist companies (UK subsidiaries)• Low gas prices– UK net importer 2004

• Access to electricity markets hard for small generators• CCGT: electricity prices follow gas• Spark spread recently grew, envisaged to grow further• Assumptions about consumer preference for switching• Large penetration of inflexible generators planned

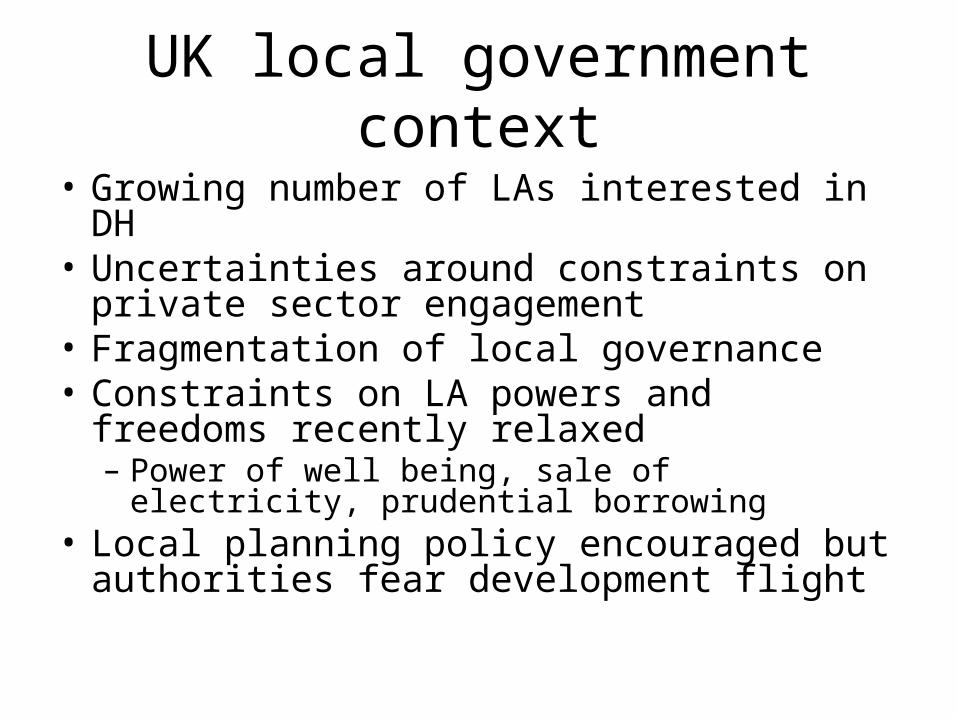

UK local government context• Growing number of LAs interested in DH• Uncertainties around constraints on private

sector engagement• Fragmentation of local governance• Constraints on LA powers and freedoms recently

relaxed– Power of well being, sale of electricity, prudential

borrowing• Local planning policy encouraged but authorities

fear development flight

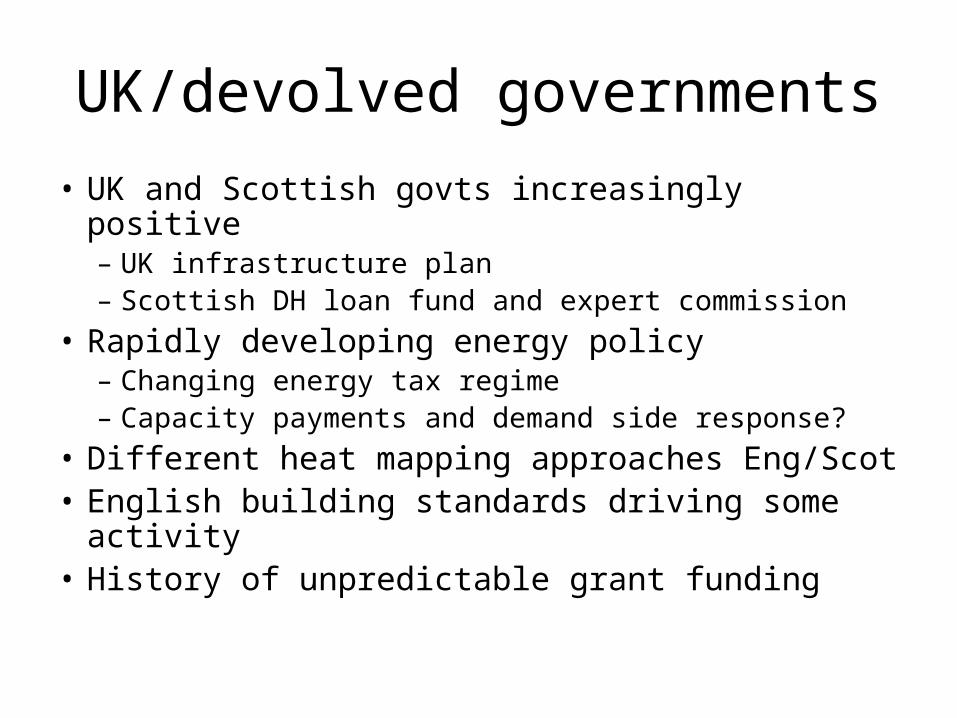

UK/devolved governments

• UK and Scottish govts increasingly positive– UK infrastructure plan– Scottish DH loan fund and expert commission

• Rapidly developing energy policy– Changing energy tax regime– Capacity payments and demand side response?

• Different heat mapping approaches Eng/Scot• English building standards driving some activity• History of unpredictable grant funding

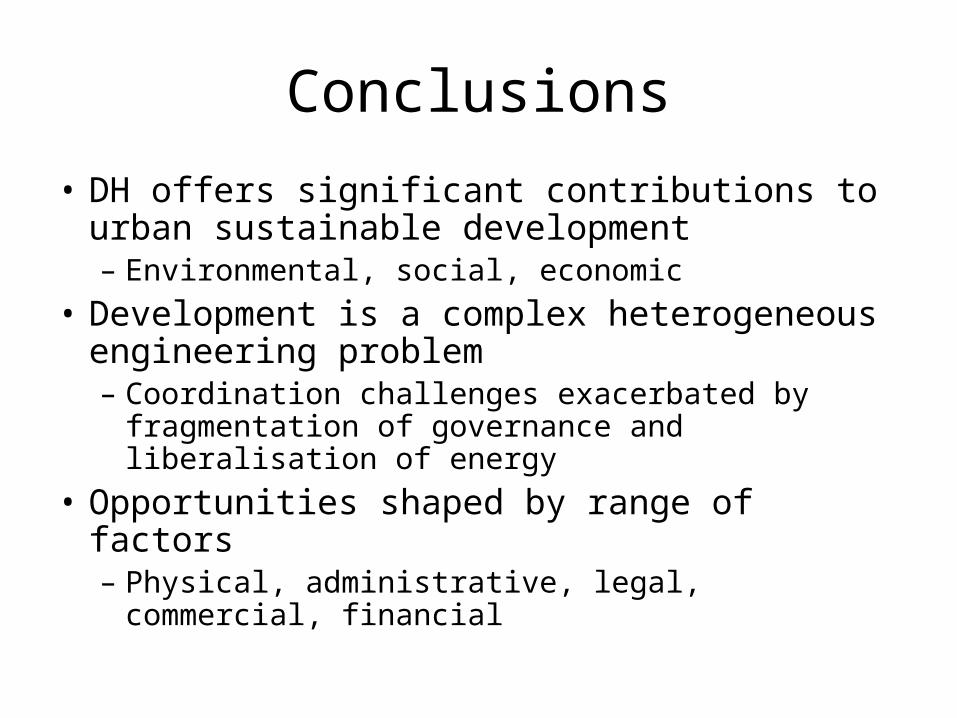

Conclusions

• DH offers significant contributions to urban sustainable development– Environmental, social, economic

• Development is a complex heterogeneous engineering problem– Coordination challenges exacerbated by

fragmentation of governance and liberalisation of energy

• Opportunities shaped by range of factors– Physical, administrative, legal, commercial, financial